UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

or

For the transition period from ___________ to ___________

Commission file number: 1-5794

(Exact name of Registrant as Specified in its Charter)

| (State of Incorporation) | (I.R.S. Employer Identification No.) | |||||||||||||

| | ||||||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||||||||

Registrant's telephone number, including area code: (313 ) 274-7400

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange On Which Registered | ||||||||||||

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

☑ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The aggregate market value of the Registrant's Common Stock held by non-affiliates of the Registrant on June 30, 2022 (based on the closing sale price of $50.60 of the Registrant's Common Stock, as reported by the New York Stock Exchange on such date) was approximately $11,359,743,400 .

Number of shares outstanding of the Registrant's Common Stock at January 31, 2023:

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant's definitive Proxy Statement to be filed for its 2023 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

Masco Corporation

2022 Annual Report on Form 10-K

TABLE OF CONTENTS

| Item | Page | |||||||||||||

1

Cautionary Statement Concerning Forward-Looking Statements

This Report contains statements that reflect our views about our future performance and constitute "forward-looking statements" under the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as "outlook," "believe," "anticipate," "appear," "may," "will," "should," "intend," "plan," "estimate," "expect," "assume," "seek," "forecast," and similar references to future periods. Our views about future performance involve risks and uncertainties that are difficult to predict and, accordingly, our actual results may differ materially from the results discussed in our forward-looking statements. We caution you against relying on any of these forward-looking statements.

Our future performance may be affected by the levels of residential repair and remodel activity, and to a lesser extent, new home construction, our ability to maintain our strong brands and to develop innovative products, our ability to maintain our public reputation, our ability to maintain our competitive position in our industries, our reliance on key customers, the cost and availability of materials, our dependence on suppliers and service providers, extreme weather events and changes in climate, risks associated with our international operations and global strategies, our ability to achieve the anticipated benefits of our strategic initiatives, our ability to successfully execute our acquisition strategy and integrate businesses that we have acquired and may in the future acquire, our ability to attract, develop and retain a talented and diverse workforce, risks associated with cybersecurity vulnerabilities, threats and attacks, risks associated with our reliance on information systems and technology and the impact of the ongoing COVID-19 pandemic on our business and operations.

These and other factors are discussed in detail in Item 1A. "Risk Factors" of this Report. Any forward-looking statement made by us speaks only as of the date on which it was made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. Unless required by law, we undertake no obligation to update publicly any forward-looking statements as a result of new information, future events or otherwise.

PART I

Item 1.Business.

Masco Corporation and its subsidiaries (the “Company”) is a global leader in the design, manufacture and distribution of branded home improvement and building products. Our portfolio of industry-leading brands includes BEHR® paint; DELTA® and HANSGROHE® faucets, bath and shower fixtures; KICHLER® decorative and outdoor lighting; LIBERTY® branded decorative and functional hardware; and HOT SPRING® spas. We leverage our powerful brands across product categories, sales channels and geographies to create value for our customers and shareholders.

We believe that our solid results of operations and financial position for 2022 resulted from our continued focus on our three strategic pillars:

•drive the full potential of our core businesses;

•leverage opportunities across our enterprise; and

•actively manage our portfolio.

In 2022, we continued to return value to our shareholders by repurchasing approximately 16.6 million shares of our common stock and increasing our quarterly dividend by approximately 19 percent compared to 2021.

Our Business Segments

We report our financial results in two segments, our Plumbing Products segment and our Decorative Architectural Products segment, which are aggregated by product similarity. Our Decorative Architectural Products segment is impacted by seasonality and normally experiences stronger sales during the second and third calendar quarters, corresponding with the peak season for repair and remodel activity.

2

Plumbing Products

The businesses in our Plumbing Products segment sell a wide variety of products that are manufactured or sourced by us.

•Our plumbing products include faucets, showerheads, handheld showers, valves, bath hardware and accessories, bathing units, shower bases and enclosures, shower drains, steam shower systems, sinks, kitchen accessories and toilets. We primarily sell these products to home center retailers, online retailers, mass merchandisers, wholesalers and distributors that, in turn, sell them to plumbers, building contractors, remodelers, smaller retailers and consumers, and homebuilders. The majority of our faucet, bathing and showering products are sold primarily in North America, Europe and China under the brand names DELTA®, BRIZO®, PEERLESS®, HANSGROHE®, AXOR®, KRAUS®, EASY DRAIN®, STEAMIST®, ELITESTEAM®, GINGER®, NEWPORT BRASS®, BRASSTECH® and WALTEC®. Our BRISTAN™ and HERITAGE™ products are sold primarily in the United Kingdom.

•We manufacture acrylic tubs, bath and shower enclosure units, and shower bases and trays. Our DELTA, PEERLESS and MIROLIN® products are sold primarily to home center retailers in North America. Our MIROLIN products are also sold to wholesalers and distributors in Canada.

•Our spas, exercise pools and aquatic fitness systems are manufactured and sold under our HOT SPRING®, CALDERA®, FREEFLOW SPAS®, FANTASY SPAS® and ENDLESS POOLS® brands, as well as under other trademarks. Our spa and exercise pools are sold worldwide to independent specialty retailers and distributors and to online mass merchant retailers. Certain exercise pools are also available on a consumer-direct basis in North America and Europe, while our aquatic fitness systems are sold through independent specialty retailers as well as on a consumer-direct basis in some areas.

•Included in our Plumbing Products segment are brass, copper and composite plumbing system components and other non-decorative plumbing products that are sold to plumbing, heating and hardware wholesalers, home center and online retailers, hardware stores, building supply outlets and other mass merchandisers. These products are marketed primarily in North America under our BRASSCRAFT®, PLUMBSHOP®, COBRA® and MASTER PLUMBER® brands and are also sold under private label.

•Within our Plumbing Products segment we develop connected water products that enhance the experience with water in homes and businesses. These systems include touchless activation, voice activation, controlled volume dispensing and provide for monitoring and controlling the temperature and flow of water and are compatible with a range of faucets, showerheads and other showering components.

•We also supply high-quality, custom thermoplastic solutions, extruded plastic profiles and specialized fabrications, as well as PEX tubing, to manufacturers, distributors and wholesalers for use in diverse applications that include faucets and plumbing supplies, appliances, oil and gas equipment and building products.

We believe that our plumbing products are among the leaders in sales in North America and Europe. Competitors of the majority of our products in this segment include Dornbracht AG & Co. KG, Zurn Elkay Water Solutions Corporation, Fortune Brands Innovations, Inc.'s Moen, Rohl and Riobel brands, Kohler Co., Lixil Group Corporation’s American Standard and Grohe brands, Spectrum Brands Holdings, Inc.'s Pfister faucets and private label brands. Competitors of our spas and exercise pools and systems include Artesian Spas, Jacuzzi and Master Spas brands, among others. Foreign manufacturers competing with us are located primarily in Europe, China and Canada. Additionally, we face significant competition from private label products and digitally native brands. The businesses in our Plumbing Products segment manufacture products primarily in North America and Europe as well as in Asia and source products from Asia and other regions. Competition for our plumbing products is based largely on brand reputation, product features and innovation, product quality, customer service, breadth of product offering and price. Many of the faucet and showering products with which our products compete are manufactured by low-cost foreign manufacturers that contribute to price competition.

3

Many of our plumbing products contain brass, the major components of which are copper and zinc. We have multiple sources, both domestic and foreign, for our raw materials used in this segment. We have encountered price volatility for brass, brass components and any components containing copper and zinc. To help reduce the impact of this volatility, from time to time we may enter into long-term agreements with certain significant suppliers. In addition, some of the products in this segment that we import have been and may in the future be subject to duties and tariffs.

Decorative Architectural Products

Our Decorative Architectural Products segment primarily includes architectural coatings, including paints, primers, specialty coatings, stains and waterproofing products, as well as paint applicators and accessories. These products are sold in North America, South America and China under the brand names BEHR®, KILZ®, WHIZZ®, Elder & Jenks® and other trademarks to “do‑it‑yourself” and professional customers through home center retailers and other retailers. Net sales of architectural coatings comprised approximately 32 percent, 30 percent and 33 percent of our consolidated net sales from our continuing operations in 2022, 2021, and 2020, respectively. Our BEHR products are sold through The Home Depot, our largest customer overall, as well as this segment’s largest customer. Our Behr business grants Behr brand exclusivity in the retail sales channel in North America to The Home Depot. The granting of exclusivity affects our ability to sell those products and brands to other customers, and the loss of this segment’s sales to The Home Depot would have a material adverse effect on this segment’s business and on our consolidated business as a whole.

Our competitors in this segment include large national and international brands such as Benjamin Moore & Co., PPG Industries, Inc.'s Glidden, Olympic, Pittsburgh Paints and PPG brands, The Sherwin‑Williams Company's Minwax, Sherwin-Williams, Thompson’s Water Seal, Valspar and Purdy brands, RPM International, Inc.'s Rust-Oleum and Zinsser brands and the Wooster Brush Company, as well as many regional and other national brands. We believe that brand reputation is an important factor in consumer selection, and that competition in this industry is also based largely on product features and innovation, product quality, customer service, breadth of product offering and price.

Acrylic resins and titanium dioxide are principal raw materials in the manufacture of architectural coatings. The price of acrylic resins fluctuates based on the price of its components, which can have a material impact on our costs and results of operations in this segment. The price for titanium dioxide can fluctuate as a result of global supply and demand dynamics and production capacity limitations, which can have a material impact on our costs and results of operations in this segment. In addition, the prices of crude oil, natural gas, propylene, methyl methacrylate (MMA) and certain petroleum by-products can impact our costs and results of operations in this segment. We have multiple sources, both domestic and foreign, for the raw materials used in this segment. We have encountered price volatility for propylene and MMA. To help reduce the impact of this price volatility, we have and may in the future enter into long-term agreements with certain significant suppliers. We import certain materials and products for this segment that have been and may in the future be subject to duties and tariffs. We also have agreements with certain significant suppliers for this segment that are intended to help assure continued supply.

Our Decorative Architectural Products segment includes branded cabinet and door hardware, functional hardware, wall plates, hook and hook rail products, closet organization systems and picture hanging accessories, which are manufactured for us and sold to home center retailers, mass retailers, online retailers, other specialty retailers, original equipment manufacturers and wholesalers. These products are sold under the LIBERTY®, BRAINERD®, FRANKLIN BRASS® and other trademarks. Our key competitors in North America include Amerock Hardware, Richelieu Hardware Ltd., Top Knobs and private label brands. Decorative bath hardware, shower accessories, mirrors and shower doors are sold under the brand names DELTA® and FRANKLIN BRASS® and other trademarks to home center retailers, mass retailers, online retailers, other specialty retailers and wholesalers. Competitors for these products include Fortune Brands Innovations, Inc.'s Moen brand, Gatco Fine Bathware, Kohler Co. and private label brands.

This segment also includes decorative indoor and outdoor lighting fixtures, ceiling fans, landscape lighting and LED lighting systems. These products are sold to home center retailers, online retailers, electrical distributors, landscape distributors and lighting showrooms under the brand names KICHLER® and ÉLAN® and under other trademarks. Competitors of these products include Acuity, FX Luminaire, Generation Brands, Hinkley Lighting, Inc., Hubbell Incorporated's Progress Lighting brand, Hunter Fan Company and private label brands.

4

Additional Information

Intellectual Property

We hold numerous U.S. and foreign patents, patent applications, licenses, trademarks, trade names, trade secrets and proprietary manufacturing processes. We view our trademarks and other intellectual property rights as important, but do not believe that there is any reasonable likelihood of a loss of such rights that would have a material adverse effect on our present business as a whole.

Laws and Regulations Affecting Our Business

We are subject to federal, state, local and foreign government laws and regulations. For a more detailed description of the various laws and regulations that impact our business, see Item 1A. Risk Factors.

We monitor applicable laws and regulations, including environmental laws and regulations, and incur ongoing expense relating to compliance, however we do not expect that compliance with federal, state, local and foreign regulations will result in material capital expenditures or have a material adverse effect on our results of operations and financial position.

Human Capital Management

The performance of our Company is impacted by our human capital management, and as a result we are focused on attracting, developing and retaining highly qualified, engaged and diverse employees. We have developed three strategic talent priorities: leadership, diversity, equity and inclusion, and future workforce. Our Chief Human Resources Officer is responsible for developing and executing our human capital strategy and provides regular updates to our Board of Directors’ Compensation and Talent Committee on our progress toward the achievement of these strategic initiatives. We believe that our human capital initiatives work together to help our employees grow and thrive, and cultivate a culture where our employees feel like they belong. We are also committed to keeping our employees healthy and safe in the workplace.

Leadership

We support and foster the growth of our employees by providing development opportunities, experiences and tools that build and strengthen leadership capabilities. Our Leadership Framework, which is how we internally describe the capabilities and behaviors that we believe make great leaders, serves as the foundation for how we select, develop and measure the performance of our leaders.

To develop a sustainable pipeline of leaders, we have robust and proactive talent management and succession planning processes to support our businesses. In addition, our Board of Directors and executive management team regularly review our Company’s critical leadership roles and succession plans.

We are focused on building a continuous learning culture by enabling frequent and candid feedback discussions about performance and development between employees and their managers, across peers, and within teams.

Diversity, Equity and Inclusion ("DE&I")

We believe a workplace that encourages different voices, perspectives and backgrounds creates better teams, better solutions and more innovation. We strive to cultivate a sense of belonging for our employees. We are focused on the following three key areas:

•Our workplace: who we are and how it feels to work at Masco

•Our marketplace: how we deliver innovative solutions that meet the needs of all our consumers and customers

•Our communities: how we can help increase access, equity, and inclusion through strong community partners and business partnerships

5

Each strategic focus area has a series of enterprise-wide initiatives, and our businesses have aligned plans that are tailored to meet their specific needs. Our enterprise DE&I Council along with business unit councils and employee resource groups serve as advisors, ambassadors and change agents in implementing our enterprise-wide initiatives and their business unit plans.

Our workforce representation statistics are one indicator of our performance in advancing a diverse workforce. Following is our workforce representation statistics as of December 31, 2022:

•In the U.S., our leadership team is comprised of 33 percent women and 26 percent racially / ethnically diverse individuals, as compared to the EEO-1 benchmark of 25 percent and 21 percent, respectively. The EEO-1 leadership benchmark includes executive-level/senior-officials and managers, and first-level officials and managers.

•In the U.S., our salaried workforce is comprised of approximately 36 percent women and 30 percent racially / ethnically diverse individuals, as compared to the EEO-1 benchmark of 28 percent and 28 percent, respectively. The EEO-1 salaried employees benchmark includes leadership, professionals and technicians.

•In the U.S., our hourly workforce, which includes hourly and exception hourly, is comprised of 37 percent women and 55 percent racially / ethnically diverse individuals, as compared to the EEO-1 benchmark of 28 percent and 38 percent, respectively. The EEO-1 hourly employees benchmark includes all other EEO categories we did not include in the EEO-1 leadership and salaried benchmark.

We have established specific aspirational representation goals for 2025 for certain groups within our U.S. workforce along with goals linked to employees’ experiences related to inclusion and belonging. These aspirational goals are ambitious and are not intended to be commitments, promises, or guarantees of future achievement. Any progress towards these goals is regularly measured and is reviewed by our Compensation and Talent Committee of our Board of Directors and executive management team. After establishing these goals, we faced and continue to face complexities and variables that are impacting our progress and may result in us not achieving our goals, such as a tightening labor market, challenging economic environment, changes to our portfolio of businesses via acquisitions or divestitures, and adjustments to our job levels and managerial headcount. We describe those goals in our Corporate Social Responsibility report, which is not incorporated by reference into this Report.

Future Workforce

There are critical capabilities that our employees and our organization need to help us achieve our businesses objectives. We leverage our Masco Operating System, our methodology to drive growth and productivity, to ensure that our businesses are focused on building these critical organizational capabilities by ensuring they have the right structure, talent, tools, and training in place.

Employee Engagement

In order to engage and retain our employees, we listen to our employees to understand their perspectives, needs and ideas by leveraging various forums, tools, and methods including surveys to measure key insights related to employee engagement, inclusion, well-being, and leadership, among others.

Employee Health and Safety

The safety of our employees is integral to our company. In support of our safety efforts, we identify, assess, and investigate incidents and injury data, and each year set a goal to improve key safety performance indicators. We communicate and train our workforce on the importance of safe work practices. We also regularly consult with our employees on safety-related improvements to our operations. Throughout 2022, we continued to implement the best practices and recommendations from the Centers for Disease Control and the Department of Labor (OSHA).

Our Workforce

At December 31, 2022, we employed approximately 19,000 people.

6

Available Information

Our website is www.masco.com. Our periodic reports and all amendments to those reports required to be filed or furnished pursuant to Section 13(a) or Section 15(d) of the Securities Exchange Act of 1934 are available free of charge through our website as soon as reasonably practicable after those reports are electronically filed with or furnished to the Securities and Exchange Commission ("SEC"). This Report is being posted on our website concurrently with its filing with the SEC. Material contained on our website is not incorporated by reference into this Report. Our reports filed with the SEC also may be found on the SEC’s website at www.sec.gov.

Item 1A. Risk Factors.

There are a number of business risks and uncertainties that could affect our business. These risks and uncertainties could cause our actual results to differ from past performance or expected results. We consider the following risks and uncertainties to be most relevant to our specific business activities. Additional risks and uncertainties not presently known to us, or that we currently believe to be immaterial, also may adversely impact our business, results of operations and financial position.

Strategic Risks

Our business strategy is focused on residential repair and remodeling activity and, to a lesser extent, on new home construction activity, both of which are impacted by a number of economic factors and other factors.

Our business relies on residential repair and remodeling activity and, to a lesser extent, on new home construction activity. A number of factors impact consumers’ spending on home improvement projects as well as new home construction activity, including:

•consumer confidence levels;

•fluctuations in home prices;

•existing home sales;

•inflationary pressures;

•unemployment and underemployment levels;

•consumer income and debt levels;

•household formation;

•the availability of skilled tradespeople for repair and remodeling work;

•the availability of home equity loans and mortgages and the interest rates for and tax deductibility of such loans;

•trends in lifestyle and housing design; and

•natural disasters, terrorist acts, pandemics, wars or conflicts or other catastrophic events.

We have been, and may in the future be, negatively impacted by adverse changes or uncertainty involving one or more of the factors listed above. In addition, the fundamentals driving our business are impacted by economic cycles. An economic contraction or recession have in the past resulted in and could in the future result in a decline in residential repair and remodeling activity or in demand for new home construction, adversely affecting our results of operations and financial position.

We may not achieve all of the anticipated benefits of our strategic initiatives.

We continue to pursue our strategy of driving the full potential of our core businesses, leveraging opportunities across our enterprise, and actively managing our portfolio. Our strategy is designed to grow revenue, improve profitability and increase shareholder value over the mid- to long-term. We execute our strategy by investing in our brands, developing innovative products, making capital investments, and focusing on continuous productivity improvement and operational excellence, among other initiatives. Our business performance and results could be adversely affected if we are unable to timely and effectively execute our strategy. We could also be adversely affected if we have not appropriately prioritized and balanced our strategic initiatives or if we are unable to effectively manage change throughout our organization.

7

We may not be able to successfully execute our acquisition strategy or integrate businesses that we acquire.

Pursuing the acquisition of businesses complementary to our portfolio is a component of our strategy for future growth. If we are not able to identify suitable acquisition candidates or consummate potential acquisitions within a desired time frame or at acceptable terms and prices, our long-term competitive positioning may be affected. Even if we are successful in acquiring businesses, the businesses we acquire may not be able to achieve the revenue, profitability or growth we anticipate, or we may experience challenges and risks in integrating these businesses into our existing business. Such risks include:

•difficulties realizing expected synergies and economies of scale;

•diversion of management attention and our resources;

•unforeseen liabilities;

•issues or conflicts with our new or existing customers or suppliers; and

•difficulties in retaining critical employees of the acquired businesses.

International acquisitions that we have made, and international acquisitions that we may make in the future, may continue to increase our exposure to foreign currency risks, risks associated with interpretation and enforcement of foreign regulations and the policies of foreign governments. Our failure to address these risks could cause us to incur additional costs and fail to realize the anticipated benefits of our acquisitions and could adversely affect our results of operations and financial position.

Business and Operational Risks

We are dependent on suppliers and service providers.

We are dependent on third parties for our raw materials, many of our components and finished products and for certain services. Our ability to offer a wide variety of products and provide high levels of service to our customers depend on our ability to obtain an adequate and timely supply of these goods and services. Failure of our suppliers to timely provide us goods and services on commercially reasonable terms or to comply with applicable legal and regulatory requirements or our supplier business practices policy could have a material adverse effect on our results of operations and financial position or could damage our reputation.

The operations of the third parties on whom we depend could be impacted by: changing laws, regulations and policies, including those related to climate change; cybersecurity breaches; labor availability; raw material shortages; energy availability; supply disruptions; and adverse weather conditions, pandemics, and other force majeure events. Any of these factors could disrupt our third parties’ operations and result in shortages of supply, assertion of force majeure and increases in the prices charged to us for the raw materials, components and finished products they produce or services they provide. Sourcing these raw materials, components, finished products and services from alternate suppliers, including suppliers from new geographic regions, or re-engineering our products as a result of supplier disruptions, is time-consuming and costly and could result in inefficiencies or delays in our business operations or could negatively impact the quality of our products. In addition, the loss of critical suppliers, or a substantial decrease in the availability of supply, has disrupted and could continue to disrupt our business and may have a material adverse effect on our results of operations and financial position.

Many of the suppliers we rely upon are located in foreign countries, primarily China. The differences in business practices, shipping and delivery requirements and costs, changes in economic conditions and trade policies and laws and regulations, together with the limited number of suppliers available to us, have increased the complexity of our supply chain logistics and the potential for interruptions in our production scheduling. We have experienced and may continue to experience constraints on and disruptions to transporting our raw materials, components and finished products from our international and domestic suppliers and have had to pay higher transportation costs. If we are unable to effectively manage our supply chain or if we continue to experience such issues, our results of operations and financial position could be adversely affected.

8

Variability in the cost and availability of our raw materials, component parts and finished products could affect our results of operations and financial position.

We purchase substantial amounts of raw materials, component parts and finished products from outside sources, including international sources, and we manufacture certain of our products outside of the United States. Increases in the cost of the materials we purchase, including as a result of diminished availability, increased tariffs and inflation or unfavorable fluctuations in foreign currency exchange rates have increased and may in the future increase the prices for our products and negatively impact our results of operations and financial position. Further, our production has been and may in the future be affected if we or our suppliers are unable to procure our requirements for various commodities, including, among others, brass, resins, titanium dioxide and zinc, or if a shortage of these commodities results in significantly increased costs. Energy prices have also increased and, this coupled with potential energy supply shortages, could continue to increase our production and transportation costs. In addition, water is a significant component of our architectural coatings products and may be subject to shortages and restrictions on supply in certain regions, due to climate-related and other influences. These factors could adversely affect our results of operations and financial position.

It can be difficult for us to pass on to customers our cost increases. Our existing arrangements with customers, competitive considerations and customer resistance to price increases may delay or make us unable to adjust selling prices. If we are not able to sufficiently increase the prices of our products or achieve cost savings to offset increased material, production, transportation and labor costs, our results of operations and financial position could be adversely affected. Increased selling prices for our products have and may in the future lead to sales declines and loss of market share, particularly if those prices are not competitive. When our material costs decline, we have experienced and may in the future receive pressure from our customers to reduce our prices. Such reductions could adversely affect our results of operations and financial position.

From time to time we enter into long-term agreements with certain significant suppliers to help ensure continued availability of the commodities we require to produce our products and to establish firm pricing, but at times these contractual commitments may result in our paying above market prices for commodities during the term of the contract. Occasionally, we may also use derivative instruments, including commodity futures and swaps. This strategy increases the possibility that we may make commitments for these commodities at prices that subsequently exceed their market prices, which has occurred and could occur in the future and may adversely affect our results of operations and financial position.

There are risks associated with our international operations and global strategies.

In 2022, 20 percent of our sales from continuing operations were made outside of North America (principally in Europe) and transacted in currencies other than the U.S. dollar. In addition to our European operations, we manufacture products in other locations, including Asia and Mexico and source products and components from third parties globally. Risks associated with our international operations include:

•differences in culture, economic and labor conditions and practices;

•the policies of the U.S. and foreign governments;

•disruptions in trade relations and economic instability;

•differences in enforcement of contract and intellectual property rights;

•timeliness of transportation and port congestion;

•social and political unrest; and

•natural disasters, terrorist attacks, pandemics, wars or conflicts or other catastrophic events.

We are also affected by domestic and international laws and regulations applicable to companies doing business outside of the U.S. or importing and exporting goods and materials. These include anti-bribery/anti-corruption laws, laws regulating competition, sanctions, tax laws, and other business practices, and trade regulations, including duties and tariffs. Compliance with these laws is costly, and future changes to these laws may require significant management attention and disrupt our operations. Additionally, while it is difficult to assess what changes may occur and the relative effect on our international tax structure, significant changes in how U.S. and foreign jurisdictions tax cross-border transactions could adversely affect our results of operations and financial position.

9

Our results of operations and financial position are also impacted by changes in currency exchange rates. Unfavorable currency exchange rates, particularly the euro, the Chinese renminbi, the Canadian dollar, the British pound sterling and the Mexican peso, have in the past adversely affected us, and could adversely affect us in the future. Fluctuations in currency exchange rates may present challenges in comparing operating performance from period to period.

The long-term performance of our businesses relies on our ability to attract, develop and retain a talented and diverse workforce.

To be successful, we must invest significant resources to attract, develop and retain highly qualified, talented and diverse employees at all levels, who have the experience, knowledge and expertise to implement our strategic and business initiatives. We compete for employees with a broad range of employers in many different industries, including large multinational firms. We may face challenges in recruiting, developing, motivating and retaining employees, particularly when the labor market is experiencing low unemployment levels, increasing compensation and increasing competition. We have been and continue to be affected by a shortage of qualified personnel primarily for our hourly workforce.

Additionally if we are unable to attract, develop and retain key employees, build strong and diverse leadership teams, successfully implement our talent strategies or develop effective succession planning, our results of operations and financial position could be adversely affected.

Extreme weather events and changes in climate could adversely impact our results of operations and financial position.

Extreme weather events, such as severe winter and other storms, hurricanes, fires, floods, tornados and droughts, as a result of climate change or other factors, have negatively impacted and may continue to negatively impact our business. These types of events can be disruptive to our operations and may impact consumer spending. In addition, we have certain suppliers located in areas that have experienced extreme weather events which have impacted and may in the future impact the availability and cost of some of our raw materials, components and finished products. If the frequency or severity of extreme weather increases, we may experience interruptions to our operations, further impact on our supply chain, increased operating costs or loss or damage to our property or inventory, which could adversely affect our results of operations and financial position.

Restrictive covenants in our credit agreement could limit our financial flexibility.

We must comply with both financial and nonfinancial covenants in our credit agreement, and in order to borrow under it, we cannot be in default with any of those provisions. Our ability to borrow under the credit agreement could be affected if our earnings significantly decline to a level where we are not in compliance with the financial covenants or if we default on any nonfinancial covenants. In the past, we have been able to amend the covenants in our credit agreement, but there can be no assurance that in the future we would be able to further amend them. If we were unable to borrow under our credit agreement, our financial flexibility could be restricted.

Competitive Risks

We could lose market share if we do not maintain our strong brands, develop innovative products or respond to changing purchasing practices and consumer preferences.

Our competitive advantage is due, in part, to our ability to maintain our strong brands and to develop and introduce innovative new and improved products. Our initiatives to invest in brand building, brand awareness and product innovation may not be successful. The uncertainties associated with developing and introducing innovative and improved products, such as gauging changing consumer demands and preferences and successfully developing, manufacturing, marketing, selling and servicing these products, may impact the success of our product introductions. If the products we introduce do not gain widespread acceptance or if our competitors improve their products more rapidly or effectively than we do, we could lose market share or be required to reduce our prices, which could adversely impact our results of operations and financial position.

10

In recent years, consumer purchasing practices and preferences have shifted and our customers’ business models and strategies have changed. As our customers execute their strategies to reach end consumers through multiple channels, they rely on us to support their efforts with our infrastructure, including maintaining robust and user-friendly websites with sufficient content for consumer research and providing comprehensive supply chain solutions and differentiated product development. If we are unable to successfully provide this support to our customers or if our customers are unable to successfully execute their strategies, our brands may lose market share.

A number of consumer preferences are changing, including a continued shift in consumer purchasing practices toward e-commerce and increased consumer demand for products with potential desired attributes, such as connected products and sustainable products. If we do not timely and effectively identify and respond to these changes our relationships with our customers and with consumers could be harmed, our ability to retain our customers and consumers may be negatively impacted, the demand for our brands and products could be reduced and our results of operations and financial position could be adversely affected.

Damage to our public reputation could adversely affect our results of operations and financial position.

Our public image and reputation are important to maintaining our strong brands. Our results of operations and financial position could be adversely affected by negative claims and comments in social media or the press, a negative perception regarding our products or company practices, positions or public statements, even if unfounded, or a data breach. Furthermore, there is increased scrutiny by stakeholders on environmental, social and governance (“ESG”) practices by companies, and we may not be able to meet such stakeholders’ expectations. Expectations regarding ESG practices are diverse and rapidly changing, and we may not be able to align our ESG practices with such evolving expectations within the timeframes expected by stakeholders or without incurring significant costs. In addition, we may not be able to achieve our aspirational goals related to our ESG initiatives, which are and may continue to be impacted by many complexities and variables, such as a tightening labor market, challenging economic environment, changes to our operations, changes to our portfolio of businesses via acquisitions or divestitures, and adjustments to our job levels and managerial headcount. A failure or perceived failure by us in this regard may damage our reputation and adversely affect our results of operations and financial position.

We face significant competition and operate in an evolving competitive landscape.

Our products face significant competition. We believe that brand reputation is an important factor affecting product selection and that we compete on the basis of product features, innovation, quality, customer service, warranty and price. We sell our products through home center retailers, online retailers, distributors and independent dealers and rely on these customers to market and promote our products to consumers. Our success with our customers is dependent on, among other things, our ability to provide quality products with desired features at the right price, timely delivery and a high level of customer service. Home center retailers, which have historically concentrated their sales efforts on retail consumers and remodelers, are increasingly selling directly to professional contractors and installers, which may adversely affect our margins on our products that contractors and installers would otherwise buy through our dealers and wholesalers. In addition, as home center retailers develop customer experience programs to attract and retain contractors and installers, they are relying on us to support their efforts. Such support has been and could continue to be time-consuming and costly and these efforts may not be successful, which may affect our growth and operating results.

Certain of our customers are selling products sourced from low-cost foreign manufacturers under their own private label brands, which directly compete with our brands. As a result of this trend, we have experienced and may in the future experience lower demand for our products or a shift in the mix of some products we sell toward more value-priced or opening price point products, which may affect our operating results.

In addition, we face competitive pricing pressure in the marketplace, including sales promotion programs, that could affect our market share or result in price reductions, which could adversely impact our results of operations and financial position.

11

Further, the growing e-commerce channel brings an increased number of competitors and greater pricing transparency for consumers, as well as conflicts between our existing distribution channels and a need for different distribution methods. These factors could affect our results of operations and financial position. In addition, our relationships with our customers, including our home center customers, may be affected if we increase the amount of business we transact in the e-commerce channel.

If we are unable to maintain our competitive position in our industries, our results of operations and financial position could be adversely affected.

Our sales are concentrated with three significant customers and this concentration may continue to increase. In 2022, our net sales from our continuing operations to The Home Depot were $3.3 billion (approximately 38 percent of our consolidated net sales), and our net sales from our continuing operations to Ferguson and Lowe’s were each less than 10 percent of our consolidated net sales. These customers can significantly affect the prices we receive for our products and the terms and conditions on which we do business with them. Additionally, these customers have reduced in the past and may in the future reduce the number of vendors from which they purchase and could make significant changes in their volume of purchases from us. Although other retailers, dealers, distributors and homebuilders represent other channels of distribution for our products and services, we might not be able to quickly replace, or replace at all, the loss of a substantial portion of our sales to The Home Depot or the loss of all of our sales to either Ferguson or Lowe’s. Any such loss would have a material adverse effect on our business, results of operations and financial position.

In addition, our Behr business grants Behr brand exclusivity in the retail sales channel in North America to The Home Depot, and from time to time, certain of our other businesses grant product and/or brand exclusivity to our customers. The granting of exclusivity affects our ability to sell those products and brands to other customers and can increase the complexity of our product offerings and our costs.

Technology and Intellectual Property Risks

We have been and may continue to be subject to cybersecurity attacks, which could adversely affect our results of operations and financial position.

Global cybersecurity vulnerabilities, threats and more frequent, sophisticated and targeted attacks pose a risk to our information technology systems and to critical third-party information technology platforms we utilize. We have implemented security policies, processes and layers of defense designed to help identify and protect against misappropriation or corruption of our systems and information and disruption of our operations. Despite these efforts, systems we utilize have been and may in the future be damaged, disrupted, ransomed or shut down due to cybersecurity attacks by unauthorized access, malware, ransomware, undetected intrusion, hardware failures, or other events, and in these circumstances our disaster recovery plans may be ineffective or inadequate. These attacks have led and could in the future lead to business interruption, production or operational downtime, product shipment delays, exposure or loss of proprietary confidential or financial information or the personal information of our employees, suppliers, customers or consumers, data corruption, an inability to report our financial results in a timely manner, damage to the reputation of our brands, damage to our relationships with our employees, suppliers, customers and consumers, exposure to litigation, and increased costs associated with the remediation and mitigation of such attacks. In addition, we could be adversely affected if any of our significant customers, suppliers or service providers experiences any similar events that disrupt their business operations or damage their reputation. Such events could adversely affect our results of operations and financial position.

12

We rely on information systems and technology, and a breakdown or interruption of these systems could adversely affect our results of operations and financial position.

We rely on many on-site and cloud-based information systems and technology to process, transmit, store and manage information to support our business activities. We may be adversely affected if these information systems breakdown, fail, or are no longer supported by third-party service providers, including cloud platform providers. In addition to the consequences that may occur from interruptions in the current systems we utilize, we continue to invest in new technology systems throughout our company, including implementations of and upgrades to critical systems at our business units. System implementations and upgrades are complex and require significant management oversight, and we have experienced, and may continue to experience, unanticipated expenses and interruptions to our operations during these implementations and upgrades. Our results of operations and financial position, as well as the effectiveness of our internal controls over financial reporting, could be adversely affected if we do not appropriately select, implement, maintain or upgrade our critical systems in a timely manner or if we experience significant unanticipated expenses or disruptions in connection with the implementation, upgrade or update of such systems.

We may not be able to adequately protect or prevent the unauthorized use of our intellectual property.

Protecting our intellectual property is important to our growth and innovation efforts. We own a number of patents, trade names, brand names and other forms of intellectual property in our products and manufacturing processes throughout the world. There can be no assurance that our efforts to protect our intellectual property rights will prevent violations. Our intellectual property has been and may again be challenged or infringed upon by third parties, particularly in countries where property rights are not highly developed or protected. In addition, the global nature of our business increases the risk that we may be unable to obtain or maintain our intellectual property rights on reasonable terms. Furthermore, others have asserted and may in the future assert intellectual property infringement claims against us. Current and former employees, contractors, customers or suppliers have or may have had access to proprietary or confidential information regarding our business operations that could harm us if used by them, or disclosed to others, including our competitors. Protecting and preventing the unauthorized use of our intellectual property could be costly, time consuming and require significant resources. If we are not able to protect our existing intellectual property rights, or prevent unauthorized use of our intellectual property, sales of our products may be affected and we may experience reputational damage to our brand names, increased litigation costs and adverse impact to our competitive position, which could adversely affect our results of operations and financial position.

Litigation and Regulatory Risks

Claims and litigation could be costly.

We are involved in various claims and litigation, including class actions, mass torts and regulatory proceedings, that arise in the ordinary course of our business and that could have a material adverse effect on us. The types of matters may include, among others: advertising, competition, contract, data privacy, employment, environmental, insurance coverage, intellectual property, personal injury, product compliance, product liability, securities and warranty. The outcome and effect of these matters are inherently unpredictable, and defending and resolving them can be costly and can divert management’s attention. We have and may continue to incur significant costs as a result of claims and litigation.

We are also subject to product safety regulations, product recalls and direct claims for product liability that can result in significant costs and, regardless of the ultimate outcome, create adverse publicity and damage the reputation of our brands and business. Also, we rely on suppliers to provide finished products and components for products that we sell. Due to the difficulty of controlling the quality of finished products and components we source from these suppliers, we are exposed to risks relating to the quality of such finished products and components and to limitations on our recourse against such suppliers.

We maintain insurance against some, but not all, of the risks of loss resulting from claims and litigation. The levels of insurance we maintain may not be adequate to fully cover our losses or liabilities. If any significant accident, judgment, claim or other event is not fully insured or indemnified against, it could adversely affect our results of operations and financial position.

13

Refer to Note U to the consolidated financial statements included in Item 8 of this Report for additional information about litigation involving our businesses.

Our failure to comply with laws, government regulations and other requirements could adversely affect our results of operations and financial position.

We are subject to a wide variety of federal, state, local and foreign laws and regulations pertaining to:

•anti-bribery/anti-corruption;

•climate change and protection of the environment;

•competition practices;

•data privacy;

•employment and labor matters;

•environment, health and safety matters;

•product safety and performance;

•protection of employees and consumers;

•securities matters;

•sanctions;

•taxation;

•trade, including duties and tariffs; and

•wage and hour matters.

In addition to complying with current requirements and known future requirements, we will be subject to new or more stringent requirements in the future.

As we sell new types of products or existing products in new geographies or channels or for new applications, we are subject to the requirements applicable to those sales. Additionally, some of our products must be certified by industry organizations. Compliance with new or changed laws, regulations and other requirements, including as a part of government or industry response to climate change, may require us to alter our product designs, our manufacturing processes, our packaging or our sourcing or may result in restrictions on our operations. These compliance activities are costly and require significant management attention and resources. If we do not effectively and timely comply with such regulations and other requirements, our results of operations and financial position could be adversely affected.

Coronavirus Disease Risks

The ongoing COVID-19 pandemic has and may continue to impact our operations, which may impact our results and our financial condition.

We operate facilities in the U.S. and around the world which have been and may in the future be adversely affected by the COVID-19 pandemic, including the closure or reduced capacity of certain of our facilities; delays or disruptions in our ability to source and increases in the cost of raw materials, components and finished products; constraints in shipping, transportation and logistics; and decreased employee availability. Future disruption of our operations or slowdown in domestic and international economic activity due to the COVID-19 pandemic could materially and adversely affect our results of operations and financial condition.

To the extent COVID-19 impacts our business and our operations, it may also have the effect of heightening certain of the other risks described in this Report, such as those relating to our international operations and global strategies and our dependence on suppliers.

Item 1B. Unresolved Staff Comments.

None.

14

Item 2.Properties.

The table below lists principal North American properties as of December 31, 2022.

| Business Segment | Manufacturing | Warehouse and Distribution | ||||||||||||

| Plumbing Products | 22 | 12 | ||||||||||||

| Decorative Architectural Products | 8 | 18 | ||||||||||||

| Totals | 30 | 30 | ||||||||||||

Most of our North American facilities range from single warehouse buildings to complex manufacturing facilities. We own most of our North American manufacturing facilities, none of which is subject to significant encumbrances. A substantial number of our warehouse and distribution facilities are leased.

The table below lists principal properties outside of North America as of December 31, 2022.

| Business Segment | Manufacturing | Warehouse and Distribution | ||||||||||||

| Plumbing Products | 8 | 16 | ||||||||||||

| Decorative Architectural Products | — | — | ||||||||||||

| Totals | 8 | 16 | ||||||||||||

Most of our international facilities are in China, Germany and the United Kingdom. We own most of our international manufacturing facilities, none of which is subject to significant encumbrances. A substantial number of our international warehouse and distribution facilities are leased.

We lease our corporate headquarters in Livonia, Michigan, and we own a building in Taylor, Michigan, that is used by our Masco Technical Services (research and development) department. We also lease an office facility in Luxembourg, which serves as a headquarters for most of our foreign operations.

Each of our operating divisions assesses the manufacturing, distribution and other facilities needed to meet its operating requirements. We regularly review our anticipated requirements for facilities and, on the basis of that review, have and may in the future, build, acquire or lease additional facilities, or expand additional facilities.

Item 3.Legal Proceedings.

Information regarding legal proceedings involving us is set forth in Note U to the consolidated financial statements included in Item 8 of this Report and is incorporated herein by reference.

Item 4.Mine Safety Disclosures.

Not applicable.

15

PART II

Item 5.Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The New York Stock Exchange is the principal market on which our common stock is traded, under the ticker symbol MAS. On January 31, 2023, there were approximately 2,600 holders of record of our common stock.

We expect that our practice of paying quarterly dividends on our common stock will continue, although the payment of future dividends is at the discretion of our Board of Directors and will depend upon our earnings, capital requirements, financial condition and other factors. The Board of Directors declared a quarterly dividend of $0.285 per share in the first quarter of 2023 with the intention to increase the annual dividend to $1.14 per share.

We repurchased and retired 16.6 million shares of our common stock for the year ended December 31, 2022 for approximately $914 million. This included 0.6 million shares to offset the dilutive impact of restricted stock units granted in 2022. Effective October 20, 2022, our Board of Directors authorized the repurchase, for retirement, of up to $2.0 billion of shares of our common stock in open-market transactions or otherwise, replacing the previous Board of Directors authorization established in 2021. At December 31, 2022, we had $2.0 billion remaining under the 2022 authorization.

16

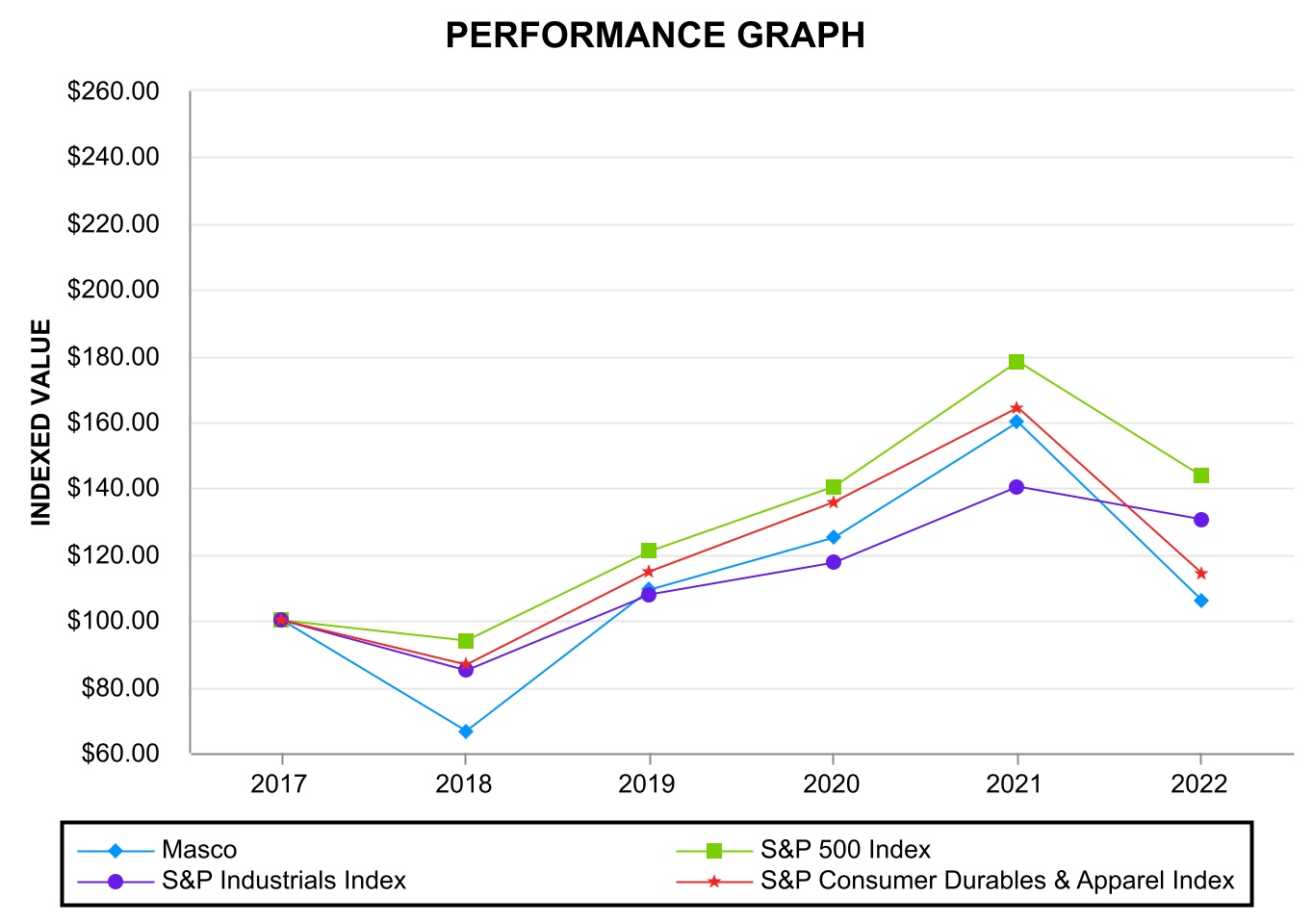

Performance Graph

The table below compares the cumulative total shareholder return on our common stock with the cumulative total return of (i) the Standard & Poor's 500 Composite Stock Index ("S&P 500 Index"), (ii) The Standard & Poor's Industrials Index ("S&P Industrials Index") and (iii) the Standard & Poor's Consumer Durables & Apparel Index ("S&P Consumer Durables & Apparel Index"), from December 31, 2017 through December 31, 2022, when the closing price of our common stock was $46.67. The graph assumes investments of $100 on December 31, 2017 in our common stock and in each of the three indices and the reinvestment of dividends.

The table below sets forth the value, as of December 31 for each of the years indicated, of a $100 investment made on December 31, 2017 in each of our common stock, the S&P 500 Index, the S&P Industrials Index and the S&P Consumer Durables & Apparel Index and includes the reinvestment of dividends.

| 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||||||||||||

| Masco | $ | 66.55 | $ | 109.22 | $ | 125.01 | $ | 159.81 | $ | 106.21 | |||||||||||||||||||

| S&P 500 Index | $ | 93.76 | $ | 120.84 | $ | 140.49 | $ | 178.27 | $ | 143.61 | |||||||||||||||||||

| S&P Industrials Index | $ | 85.00 | $ | 107.81 | $ | 117.52 | $ | 140.32 | $ | 130.35 | |||||||||||||||||||

| S&P Consumer Durables & Apparel Index | $ | 86.69 | $ | 114.67 | $ | 135.78 | $ | 164.21 | $ | 114.07 | |||||||||||||||||||

Item 6. [Reserved]

17

Item 7.Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis should be read in conjunction with, and is qualified in its entirety by, our consolidated financial statements (and notes related thereto) and other more detailed financial information appearing elsewhere in this Report. Further, you should read the following discussion and analysis of our financial condition and results of operations together with the “Risk Factors” included elsewhere in this Report for a discussion of important factors that could cause actual results to differ materially from the results described in or implied by the forward-looking statements contained in the following discussion and analysis. See also “Cautionary Statement Concerning Forward-Looking Statements” at the beginning of this Report.

Overview

We design, manufacture and distribute branded home improvement and building products. These products are sold primarily for repair and remodeling activity and, to a lesser extent, new home construction. We sell our products through home center retailers, online retailers, wholesalers and distributors, mass merchandisers, hardware stores, direct to the consumer, professional contractors and homebuilders.

We continue to pursue our strategy of driving the full potential of our core businesses, leveraging opportunities across our enterprise, and actively managing our portfolio. We remain confident in the fundamentals of our business and long-term strategy. We execute our strategy by investing in our brands, developing innovative products, making capital investments, and focusing on continuous productivity improvement and operational excellence, among other initiatives. We believe that our strong financial position and cash flow generation, together with our investments in our industry-leading branded building products, our continued focus on innovation and disciplined capital allocation, will allow us to drive long-term growth and create value for our shareholders.

We continue to leverage the Masco Operating System, our methodology to drive growth and productivity, and continuous improvement initiatives across our enterprise to identify additional opportunities to improve our business operations. From time to time, we may take actions to drive efficiency in the business focused on the strategic rationalization of our businesses, including business consolidations, plant closures, headcount reductions and other cost savings initiatives.

Recent Trends

Due to changing market conditions, we are experiencing, and may continue to experience, lower market demand for our products. We have been experiencing, and may continue to experience, elevated commodity and other input costs, elevated transportation costs and supply chain disruptions, particularly disruptions related to our ability to source products, components and raw materials. We have also been experiencing, and may continue to experience, employee-related cost inflation and constraints in hiring qualified employees. While still elevated, we have recently seen some reduction of certain costs, and we aim to offset the potential unfavorable impact of our costs and lower demand for our products with productivity improvement, pricing, and other initiatives.

Consolidated Results of Operations

We report our financial results in accordance with accounting principles generally accepted in the United States of America ("GAAP"). However, we believe that certain non-GAAP performance measures and ratios, used in managing the business, may provide users of this financial information with additional meaningful comparisons between current results and results in prior periods. These include the disclosure of net sales, operating profit and operating profit margins adjusted for certain items. Non-GAAP performance measures and ratios should be viewed in addition to, and not as an alternative for, our reported results under GAAP.

We discuss our consolidated results as well as our Business Segment and Geographic Area results of operations for the year ended December 31, 2022 versus December 31, 2021. A detailed discussion of our consolidated, Business Segment and Geographic Area results of operations for the years ended December 31, 2021 compared to the year ended December 31, 2020 can be found under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II of our Annual Report on Form 10-K for the year ended December 31, 2021, which was filed with the SEC on February 8, 2022.

18

SALES AND OPERATIONS

Net Sales

Below is a summary of our net sales, in millions, for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Net sales, as reported | $ | 8,680 | $ | 8,375 | $ | 305 | |||||||||||

| Acquisitions | (11) | — | (11) | ||||||||||||||

| Divestitures | — | (32) | 32 | ||||||||||||||

| Net sales, excluding acquisitions and divestitures | 8,669 | 8,343 | 326 | ||||||||||||||

| Currency translation | 211 | — | 211 | ||||||||||||||

| Net sales, excluding acquisitions, divestitures and the effect of currency translation | $ | 8,880 | $ | 8,343 | $ | 537 | |||||||||||

Net sales for 2022 were $8.7 billion, which increased four percent compared to 2021. Excluding acquisitions, divestitures and the effect of currency translation, net sales increased six percent.

Net sales for 2022 increased primarily due to:

•Higher net selling prices across the entire company which increased sales by nine percent.

These amounts were partially offset by:

•Lower sales volume which decreased sales by three percent.

•Unfavorable foreign currency translation which decreased sales by two percent.

Gross Profit and Gross Margin

Below is a summary of our gross profit, in millions, and gross margin for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Favorable / (Unfavorable) | |||||||||||||||

| Gross profit | $ | 2,713 | $ | 2,863 | $ | (150) | |||||||||||

| Gross margin | 31.3 | % | 34.2 | % | (290) bps | ||||||||||||

The 2022 gross profit margin was negatively impacted by:

•Increased commodity and transportation costs.

•Higher costs due to production inefficiencies and related under absorption, as well as higher excess and obsolete inventory charges resulting from business rationalization activities.

•Lower sales volume.

•Unfavorable sales mix.

These amounts were partially offset by:

•Higher net selling prices.

19

Selling, General and Administrative Expenses

Below is a summary of our selling, general and administrative expenses, in millions, and selling, general and administrative expenses as a percentage of net sales for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | (Favorable) / Unfavorable | |||||||||||||||

| Selling, general and administrative expenses | $ | 1,390 | $ | 1,413 | $ | (23) | |||||||||||

| Selling, general and administrative expenses as percentage of net sales | 16.0 | % | 16.9 | % | (90) bps | ||||||||||||

Selling, general, and administrative expenses as a percentage of net sales in 2022 was positively impacted by:

•Higher net sales resulting from favorable net selling prices.

•Lower variable compensation.

These amounts were partially offset by:

•Increased marketing costs.

Operating Profit

Below is a summary of our operating profit, in millions, and operating profit margins for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Operating profit, as reported | $ | 1,297 | $ | 1,405 | $ | (108) | |||||||||||

| Rationalization charges | 32 | 4 | 28 | ||||||||||||||

| Impairment charges for goodwill and other intangible assets | 26 | 45 | (19) | ||||||||||||||

| Operating profit, excluding rationalization charges and impairment charges | $ | 1,355 | $ | 1,454 | $ | (99) | |||||||||||

| Operating profit margin, as reported | 14.9 | % | 16.8 | % | (190) bps | ||||||||||||

| Operating profit margin, excluding rationalization charges and impairment charges | 15.6 | % | 17.4 | % | (180) bps | ||||||||||||

Operating profit in 2022 was negatively impacted by:

•Increased commodity and transportation costs.

•Higher costs due to production inefficiencies and related under absorption, as well as higher excess and obsolete inventory charges resulting from business rationalization activities.

•Lower sales volume.

•Unfavorable foreign currency translation.

•Increased marketing costs.

•Unfavorable sales mix.

These amounts were partially offset by:

•Higher net selling prices.

•Lower variable compensation.

•Lower goodwill and other intangible assets impairment charges in our lighting business.

20

OTHER INCOME (EXPENSE), NET

Interest Expense

Below is a summary of our interest expense, in millions, for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Favorable / (Unfavorable) | |||||||||||||||

| Interest expense | $ | (108) | $ | (278) | $ | 170 | |||||||||||

The decrease in interest expense is primarily due to the absence of the $168 million loss on debt extinguishment, which was recorded as additional interest expense in connection with the early retirement of debt in the first quarter of 2021.

Other, net

Below is a summary of our other, net, in millions, for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Favorable / (Unfavorable) | |||||||||||||||

| Other, net | $ | 4 | $ | (439) | $ | 443 | |||||||||||

Other, net, for 2022 included:

•$24 million of income from the revaluation of contingent consideration related to a prior acquisition.

This amount was partially offset by:

•$10 million of net periodic pension and post-retirement benefit expense.

•$6 million of losses related to equity method investments.

Other, net, for 2021 included:

•$430 million of net periodic pension and post-retirement benefit expense, which includes $399 million of net settlement loss related to the termination of our qualified domestic defined-benefit pension plans.

•$18 million loss related to the divestiture of our Hüppe GmbH ("Hüppe") business.

•$16 million expense from the revaluation of contingent consideration related to a prior acquisition.

These amounts were partially offset by:

•$14 million gain recognized on the redemption of the preferred stock of ACProducts Holding, Inc. and $6 million of related dividend income.

•$11 million of earnings related to equity method investments.

21

INCOME TAXES

Below is a summary of our income tax expense, in millions, and our effective tax rate for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | (Favorable) / Unfavorable | |||||||||||||||

| Income tax expense | $ | 288 | $ | 210 | $ | 78 | |||||||||||

| Effective tax rate | 24 | % | 31 | % | (7) | % | |||||||||||

Our 2021 income tax expense included $16 million due to the elimination of disproportionate tax effects from accumulated other comprehensive income related to our debt retirement and pension plan termination and $18 million due to losses providing no tax benefit in certain jurisdictions from our pension plan termination and a business divestiture.

Refer to Note S to the consolidated financial statements for additional information.

INCOME AND INCOME PER COMMON SHARE FROM CONTINUING OPERATIONS- ATTRIBUTABLE TO MASCO CORPORATION

Below is a summary of our income and diluted income per common share from continuing operations, in millions, except per share data, for the years ended December 31, 2022 and 2021:

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Favorable / (Unfavorable) | |||||||||||||||

| Income from continuing operations | $ | 844 | $ | 410 | $ | 434 | |||||||||||

| Diluted income per common share from continuing operations | $ | 3.63 | $ | 1.62 | $ | 2.01 | |||||||||||

22

Business Segment and Geographic Area Results

The following table sets forth our net sales and operating profit information for our continuing operations by Business Segment and Geographic Area, dollars in millions.

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2022 | 2021 | 2022 vs. 2021 | ||||||||||||||||||

| Net Sales: | ||||||||||||||||||||

| Plumbing Products | $ | 5,252 | $ | 5,135 | 2 | % | ||||||||||||||

| Decorative Architectural Products | 3,428 | 3,240 | 6 | % | ||||||||||||||||

| Total | $ | 8,680 | $ | 8,375 | 4 | % | ||||||||||||||

| North America | $ | 6,978 | $ | 6,624 | 5 | % | ||||||||||||||

| International, principally Europe | 1,702 | 1,751 | (3) | % | ||||||||||||||||

| Total | $ | 8,680 | $ | 8,375 | 4 | % | ||||||||||||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2022 | 2021 | 2022 vs. 2021 | ||||||||||||||||||

| Operating Profit (A): | ||||||||||||||||||||

| Plumbing Products | $ | 819 | $ | 929 | (12) | % | ||||||||||||||

| Decorative Architectural Products | 565 | 581 | (3) | % | ||||||||||||||||

| Total | $ | 1,384 | $ | 1,510 | (8) | % | ||||||||||||||

| North America | $ | 1,116 | $ | 1,214 | (8) | % | ||||||||||||||

| International, principally Europe | 268 | 296 | (9) | % | ||||||||||||||||

| Total | 1,384 | 1,510 | (8) | % | ||||||||||||||||

| General corporate expense, net | (87) | (105) | (17) | % | ||||||||||||||||

| Total operating profit | $ | 1,297 | $ | 1,405 | (8) | % | ||||||||||||||

(A)Before general corporate expense, net; refer to Note Q to the consolidated financial statements for additional information.

BUSINESS SEGMENT RESULTS DISCUSSION

Changes in operating profit in the following Business Segment and Geographic Area Results discussion exclude general corporate expense, net, and compares each respective period to the same period of the immediately preceding year.

23

Plumbing Products

Sales