Document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-Q

(Mark One)

|

| |

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended February 3, 2018

OR

|

| |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 1-7819

Analog Devices, Inc.

(Exact name of registrant as specified in its charter)

|

| | |

Massachusetts | | 04-2348234 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

One Technology Way, Norwood, MA | | 02062-9106 |

(Address of principal executive offices) | | (Zip Code) |

(781) 329-4700

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES þ NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

Large accelerated filer | | þ | | Accelerated filer | | ¨ |

| | | | | | |

Non-accelerated filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

| | | | | | |

| | | | Emerging growth company | | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO þ

As of February 3, 2018 there were 369,803,589 shares of common stock of the registrant, $0.16 2/3 par value per share, outstanding.

PART I - FINANCIAL INFORMATION

|

| |

ITEM 1. | Financial Statements |

ANALOG DEVICES, INC. CONDENSED CONSOLIDATED STATEMENTS OF INCOME (Unaudited) (thousands, except per share amounts)

|

| | | | | | | |

| Three Months Ended |

| February 3, 2018 | | January 28, 2017 |

Revenue | $ | 1,518,624 |

| | $ | 984,449 |

|

Cost of sales (1) | 483,434 |

| | 335,945 |

|

Gross margin | 1,035,190 |

| | 648,504 |

|

Operating expenses: | | | |

Research and development (1) | 288,597 |

| | 183,954 |

|

Selling, marketing, general and administrative (1) | 176,908 |

| | 130,659 |

|

Amortization of intangibles | 107,019 |

| | 18,160 |

|

Special charges | 57,318 |

| | 49,463 |

|

| 629,842 |

| | 382,236 |

|

Operating income | 405,348 |

| | 266,268 |

|

Nonoperating expense (income): | | | |

Interest expense | 68,030 |

| | 42,614 |

|

Interest income | (2,092 | ) | | (10,000 | ) |

Other, net | 556 |

| | 345 |

|

| 66,494 |

| | 32,959 |

|

Income before income taxes | 338,854 |

| | 233,309 |

|

Provision for income taxes | 70,682 |

| | 16,180 |

|

Net income | $ | 268,172 |

| | $ | 217,129 |

|

Shares used to compute earnings per common share – basic | 369,093 |

| | 308,786 |

|

Shares used to compute earnings per common share – diluted | 374,189 |

| | 313,076 |

|

Basic earnings per common share | $ | 0.72 |

| | $ | 0.70 |

|

Diluted earnings per common share | $ | 0.71 |

| | $ | 0.69 |

|

Dividends declared and paid per share | $ | 0.45 |

| | $ | 0.42 |

|

(1) Includes stock-based compensation expense as follows: | | | |

Cost of sales | $ | 4,221 |

| | $ | 1,944 |

|

Research and development | $ | 19,728 |

| | $ | 7,021 |

|

Selling, marketing, general and administrative | $ | 13,953 |

| | $ | 7,564 |

|

See accompanying notes.

ANALOG DEVICES, INC. CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Unaudited) (thousands)

|

| | | | | | | |

| Three Months Ended |

| February 3, 2018 | | January 28, 2017 |

Net income | $ | 268,172 |

| | $ | 217,129 |

|

Foreign currency translation adjustments | 10,171 |

| | (4,962 | ) |

Change in fair value of available-for-sale securities (net of taxes of $0 and $4, respectively) | (2 | ) | | 219 |

|

Change in fair value of derivative instruments designated as cash flow hedges (net of taxes of $2,094 and $1,395, respectively) | 8,350 |

| | 2,085 |

|

Changes in pension plans including prior service cost, transition obligation, net actuarial loss and foreign currency translation adjustments (net of taxes of $103 and $101 respectively) | (1,517 | ) | | 179 |

|

Other comprehensive income | 17,002 |

| | (2,479 | ) |

Comprehensive income | $ | 285,174 |

| | $ | 214,650 |

|

See accompanying notes.

ANALOG DEVICES, INC. CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited) (thousands, except share and per share amounts) |

| | | | | | | |

| February 3, 2018 | | October 28, 2017 |

ASSETS | |

| | |

|

Current Assets | | | |

Cash and cash equivalents | $ | 827,550 |

| | $ | 1,047,838 |

|

Accounts receivable | 709,761 |

| | 688,953 |

|

Inventories (1) | 559,720 |

| | 550,816 |

|

Prepaid income tax | 4,940 |

| | 3,522 |

|

Prepaid expenses and other current assets | 75,775 |

| | 60,209 |

|

Total current assets | 2,177,746 |

| | 2,351,338 |

|

Property, Plant and Equipment, at Cost | | | |

Land and buildings | 801,191 |

| | 794,456 |

|

Machinery and equipment | 2,412,970 |

| | 2,368,215 |

|

Office equipment | 68,144 |

| | 66,493 |

|

Leasehold improvements | 84,698 |

| | 75,263 |

|

| 3,367,003 |

| | 3,304,427 |

|

Less accumulated depreciation and amortization | 2,251,586 |

| | 2,197,123 |

|

Net property, plant and equipment | 1,115,417 |

| | 1,107,304 |

|

Other Assets | | | |

Deferred compensation plan investments | 38,847 |

| | 32,572 |

|

Other investments | 26,246 |

| | 24,838 |

|

Goodwill | 12,224,141 |

| | 12,217,455 |

|

Intangible assets, net | 5,182,355 |

| | 5,319,425 |

|

Deferred tax assets | 31,000 |

| | 32,322 |

|

Other assets | 57,563 |

| | 56,040 |

|

Total other assets | 17,560,152 |

| | 17,682,652 |

|

| $ | 20,853,315 |

| | $ | 21,141,294 |

|

LIABILITIES AND SHAREHOLDERS’ EQUITY | | | |

Current Liabilities | | | |

Accounts payable | $ | 223,107 |

| | $ | 236,629 |

|

Deferred income on shipments to distributors, net | 529,532 |

| | 473,972 |

|

Income taxes payable | 48,599 |

| | 86,905 |

|

Debt, current | 50,000 |

| | 300,000 |

|

Accrued liabilities | 385,310 |

| | 498,826 |

|

Total current liabilities | 1,236,548 |

| | 1,596,332 |

|

Non-current liabilities | | | |

Long-term debt | 7,384,856 |

| | 7,551,084 |

|

Deferred income taxes | 981,866 |

| | 1,674,683 |

|

Deferred compensation plan liability | 38,847 |

| | 32,572 |

|

Income taxes payable | 742,390 |

| | 49,583 |

|

Other non-current liabilities | 121,029 |

| | 75,500 |

|

Total non-current liabilities | 9,268,988 |

| | 9,383,422 |

|

Commitments and contingencies |

|

| |

|

|

Shareholders’ Equity | | | |

Preferred stock, $1.00 par value, 471,934 shares authorized, none outstanding | — |

| | — |

|

Common stock, $0.16 2/3 par value, 1,200,000,000 shares authorized, 369,803,589 shares outstanding (368,635,788 on October 28, 2017) | 61,635 |

| | 61,441 |

|

Capital in excess of par value | 5,318,109 |

| | 5,250,519 |

|

Retained earnings | 5,012,392 |

| | 4,910,939 |

|

Accumulated other comprehensive loss | (44,357 | ) | | (61,359 | ) |

Total shareholders’ equity | 10,347,779 |

| | 10,161,540 |

|

| $ | 20,853,315 |

| | $ | 21,141,294 |

|

| |

(1) | Includes $5,270 and $5,373 related to stock-based compensation at February 3, 2018 and October 28, 2017, respectively. |

See accompanying notes.

ANALOG DEVICES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(thousands)

|

| | | | | | | |

| Three Months Ended |

| February 3, 2018 | | January 28, 2017 (as adjusted, See Note 1) |

Cash flows from operating activities: | | | |

Net income | $ | 268,172 |

| | $ | 217,129 |

|

Adjustments to reconcile net income to net cash provided by operations: | | | |

Depreciation | 56,415 |

| | 34,379 |

|

Amortization of intangibles | 142,050 |

| | 19,947 |

|

Stock-based compensation expense | 37,902 |

| | 16,529 |

|

Deferred income taxes | (691,496 | ) | | (7,055 | ) |

Other non-cash activity | 6,762 |

| | 13,071 |

|

Changes in operating assets and liabilities | 568,883 |

| | 28,594 |

|

Total adjustments | 120,516 |

| | 105,465 |

|

Net cash provided by operating activities | 388,688 |

| | 322,594 |

|

Cash flows from investing activities: | | | |

Purchases of short-term available-for-sale investments | — |

| | (326,908 | ) |

Maturities of short-term available-for-sale investments | — |

| | 1,844,380 |

|

Sales of short-term available-for-sale investments | — |

| | 287,601 |

|

Additions to property, plant and equipment | (63,222 | ) | | (28,337 | ) |

Payments for acquisitions, net of cash acquired | — |

| | (1,036 | ) |

Changes in other assets | (1,278 | ) | | (5,946 | ) |

Net cash (used for) provided by investing activities | (64,500 | ) | | 1,769,754 |

|

Cash flows from financing activities: | | | |

Proceeds from debt | — |

| | 2,072,306 |

|

Payments of deferred financing fees | — |

| | (5,625 | ) |

Proceeds from derivative instruments | — |

| | 3,904 |

|

Debt repayments | (420,000 | ) | | — |

|

Dividend payments to shareholders | (166,719 | ) | | (129,683 | ) |

Repurchase of common stock | (7,930 | ) | | (3,106 | ) |

Proceeds from employee stock plans | 37,812 |

| | 34,432 |

|

Changes in other financing activities | 8,811 |

| | 2,221 |

|

Net cash (used for) provided by financing activities | (548,026 | ) | | 1,974,449 |

|

Effect of exchange rate changes on cash | 3,550 |

| | (666 | ) |

Net (decrease) increase in cash and cash equivalents | (220,288 | ) | | 4,066,131 |

|

Cash and cash equivalents at beginning of period | 1,047,838 |

| | 921,132 |

|

Cash and cash equivalents at end of period | $ | 827,550 |

| | $ | 4,987,263 |

|

See accompanying notes.

ANALOG DEVICES, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE MONTHS ENDED FEBRUARY 3, 2018

(all tabular amounts in thousands except per share amounts and percentages)

Note 1 – Basis of Presentation

In the opinion of management, the information furnished in the accompanying condensed consolidated financial statements reflects all normal recurring adjustments that are necessary to fairly state the results for these interim periods and should be read in conjunction with Analog Devices, Inc.’s (the Company) Annual Report on Form 10-K for the fiscal year ended October 28, 2017 (fiscal 2017) and related notes. The results of operations for the interim periods shown in this report are not necessarily indicative of the results that may be expected for the fiscal year ending November 3, 2018 (fiscal 2018) or any future period.

On March 10, 2017 (Acquisition Date), the Company completed the acquisition of Linear Technology Corporation (Linear), a designer, manufacturer and marketer of high performance analog integrated circuits. The acquisition of Linear is referred to as the Acquisition. The condensed consolidated financial statements included in this Quarterly Report on Form 10-Q include the financial results of Linear prospectively from the Acquisition Date. See Note 13, Acquisitions, of these Notes to Condensed Consolidated Financial Statements for further information.

Certain amounts reported in previous periods have been reclassified to conform to the fiscal 2018 presentation. In March 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update 2016-09, Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting (ASU 2016-09). As a result of the adoption of ASU 2016-09 in the first quarter of fiscal 2018, excess tax benefits from share-based payments are presented within operating activities in the Consolidated Statements of Cash Flows. We applied this change in presentation retrospectively and have adjusted the prior year presentation by removing the reclass of $8.1 million of excess tax benefit-stock options from net cash provided by operating activities to net cash provided by financing activities. All other reclassified amounts are immaterial.

The Company has a 52-53 week fiscal year that ends on the Saturday closest to the last day in October. Fiscal 2018 is a 53-week fiscal year and fiscal 2017 was a 52-week fiscal year. The additional week in fiscal 2018 is included in the first quarter ended February 3, 2018. Therefore, the first quarter of fiscal 2018 included 14 weeks of operations and the first quarter of fiscal 2017 included 13 weeks of operations.

Note 2 – Revenue Recognition

Revenue from product sales to customers is generally recognized when title passes, which is upon shipment in the U.S. and in certain foreign countries. Revenue from product sales to customers in other foreign countries is recognized subsequent to product shipment. Title for shipments to these other foreign countries ordinarily passes within a week of shipment. Accordingly, the Company defers the revenue recognized relating to these other foreign countries until title has passed. For multiple element arrangements, the Company allocates arrangement consideration among the elements based on the relative fair values of those elements as determined using vendor-specific objective evidence or third-party evidence. The Company uses its best estimate of selling price to allocate arrangement consideration between the deliverables in cases where neither vendor-specific objective evidence nor third-party evidence is available. A reserve for sales returns and allowances for customers is recorded based on historical experience or specific identification of an event necessitating a reserve.

Revenue from contracts with the United States government, government prime contractors and some commercial customers is generally recorded on a percentage of completion basis using either units delivered or costs incurred as the measurement basis for progress towards completion. The output measure is used to measure results directly and is generally the best measure of progress toward completion in circumstances in which a reliable measure of output can be established. Estimated revenue in excess of amounts billed is reported as unbilled receivables. Contract accounting requires judgment in estimating costs and assumptions related to technical issues and delivery schedule. Contract costs include material, subcontractor costs, labor and an allocation of indirect costs. The estimation of costs at completion of a contract is subject to numerous variables involving contract costs and estimates as to the length of time to complete the contract. Changes in contract performance, estimated gross margin, including the impact of final contract settlements, and estimated losses are recognized in the period in which the changes or losses are determined.

Product sales to certain international distributors are made under agreements that permit limited stock return privileges but not sales price rebates. Revenue on these sales is recognized upon shipment at which time title passes.

The Company defers revenue and the related cost of sales on shipments to U.S. distributors and certain international distributors until the distributors resell the products to their customers. As a result, the Company’s revenue fully reflects end

customer purchases and is not impacted by distributor inventory levels. Sales to certain of these distributors are made under agreements that allow such distributors to receive price-adjustment credits, as discussed below, and to return qualifying products for credit, as determined by the Company, in order to reduce the amounts of slow-moving, discontinued or obsolete product from their inventory. These agreements limit such returns to a certain percentage of the value of the Company’s shipments to that distributor during the prior quarter. In addition, such distributors are allowed to return unsold products if the Company terminates the relationship with the distributor.

Certain distributors are granted price-adjustment credits for sales to their customers when the distributor’s standard cost (i.e., the Company’s sales price to the distributor) does not provide the distributor with an appropriate margin on its sales to its customers. As distributors negotiate selling prices with their customers, the final sales price agreed upon with the customer will be influenced by many factors, including the particular product being sold, the quantity ordered, the particular customer, the geographic location of the distributor and the competitive landscape. As a result, the distributor may request and receive a price-adjustment credit from the Company to allow the distributor to earn an appropriate margin on the transaction.

Certain distributors are also granted price-adjustment credits in the event of a price decrease subsequent to the date the product was shipped and billed to the distributor. Generally, the Company will provide a credit equal to the difference between the price paid by the distributor (less any prior credits on such products) and the new price for the product multiplied by the quantity of the specific product in the distributor’s inventory at the time of the price decrease.

Given the uncertainties associated with the levels of price-adjustment credits to be granted to certain distributors, the sales price to the distributor is not fixed or determinable until the distributor resells the products to their customers. Therefore, the Company defers revenue recognition from sales to certain distributors until the distributors have sold the products to their customers.

Generally, title to the inventory transfers to the distributor at the time of shipment or delivery to the distributor, and payment from the distributor is due in accordance with the Company’s standard payment terms. These payment terms are not contingent upon the distributors’ sale of the products to their customers. Upon title transfer to distributors, inventory is reduced for the cost of goods shipped, the margin (sales less cost of sales) is recorded as “deferred income on shipments to distributors, net” and an account receivable is recorded. Shipping costs are charged to cost of sales as incurred.

The deferred costs of sales to distributors have historically had very little risk of impairment due to the margins the Company earns on sales of its products and the relatively long life-cycle of the Company’s products. Product returns from distributors that are ultimately scrapped have historically been immaterial. In addition, price protection and price-adjustment credits granted to distributors historically have not exceeded the margins the Company earns on sales of its products. The Company continuously monitors the level and nature of product returns and is in frequent contact with the distributors to ensure reserves are established for all known material issues.

As of February 3, 2018 and October 28, 2017, the Company had gross deferred revenue of $656.3 million and $589.5 million, respectively, and gross deferred cost of sales of $126.8 million and $115.5 million, respectively.

The Company generally offers a twelve-month warranty for its products. The Company’s warranty policy provides for replacement of defective products. Specific accruals are recorded for known product warranty issues. Product warranty expenses during each of the three-month periods ended February 3, 2018 and January 28, 2017 were not material.

Note 3 – Stock-Based Compensation

A summary of the Company’s stock option activity as of February 3, 2018 and changes during the three-month period then ended is presented below:

|

| | | | | | | | | | | | |

Activity during the Three Months Ended February 3, 2018 | Options Outstanding (in thousands) | | Weighted- Average Exercise Price Per Share | | Weighted- Average Remaining Contractual Term in Years | | Aggregate

Intrinsic

Value |

Options outstanding at October 28, 2017 | 9,347 |

| |

| $52.27 |

| | | | |

Options granted | 21 |

| |

| $91.63 |

| | | | |

Options exercised | (1,005 | ) | |

| $37.66 |

| | | | |

Options forfeited | (113 | ) | |

| $62.38 |

| | | | |

Options expired | (7 | ) | |

| $29.91 |

| | | | |

Options outstanding at February 3, 2018 | 8,243 |

| |

| $54.04 |

| | 6.3 | |

| $289,183 |

|

Options exercisable at February 3, 2018 | 3,934 |

| |

| $43.51 |

| | 4.7 | |

| $179,426 |

|

Options vested or expected to vest at February 3, 2018 (1) | 7,968 |

| |

| $53.52 |

| | 6.2 | |

| $283,587 |

|

| |

(1) | In addition to the vested options, the Company expects a portion of the unvested options to vest at some point in the future. The number of options expected to vest is calculated by applying an estimated forfeiture rate to the unvested options. |

During the three-month period ended February 3, 2018, the total intrinsic value of options exercised (i.e., the difference between the market price at exercise and the price paid by the employee to exercise the options) was $53.9 million, and the total amount of proceeds received by the Company from the exercise of these options was $37.8 million.

During the three-month period ended January 28, 2017, the total intrinsic value of options exercised (i.e., the difference between the market price at exercise and the price paid by the employee to exercise the options) was $35.6 million, and the total amount of proceeds received by the Company from the exercise of these options was $34.4 million.

A summary of the Company’s restricted stock unit/award activity as of February 3, 2018 and changes during the three-month period then ended is presented below:

|

| | | | | | |

Activity during the Three Months Ended February 3, 2018 | Restricted Stock Units/Awards Outstanding (in thousands) | | Weighted- Average Grant- Date Fair Value Per Share |

Restricted stock units/awards outstanding at October 28, 2017 | 5,680 |

| |

| $71.88 |

|

Units/Awards granted | 281 |

| |

| $87.15 |

|

Restrictions lapsed | (241 | ) | |

| $75.11 |

|

Forfeited | (173 | ) | |

| $70.98 |

|

Restricted stock units/awards outstanding at February 3, 2018 | 5,547 |

| |

| $72.66 |

|

As of February 3, 2018, there was $349.2 million of total unrecognized compensation cost related to unvested stock-based awards comprised of stock options and restricted stock units/awards. That cost is expected to be recognized over a weighted-average period of 1.8 years. The total grant-date fair value of shares that vested during the three-month period ended February 3, 2018 was approximately $20.4 million. The total grant-date fair value of shares that vested during the three-month period ended January 28, 2017 was approximately $5.1 million.

Note 4 – Accumulated Other Comprehensive Income (Loss)

The following table provides the changes in accumulated other comprehensive income (loss) (OCI) by component and the related tax effects during the first three months of fiscal 2018.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Foreign currency translation adjustment | | Unrealized holding gains on available for sale securities | | Unrealized holding (losses) on available for sale securities | | Unrealized holding gains (losses) on derivatives | | Pension plans | | Total |

October 28, 2017 | $ | (22,489 | ) | | $ | 1 |

| | $ | (1 | ) | | $ | (10,879 | ) | | $ | (27,991 | ) | | $ | (61,359 | ) |

Other comprehensive income (loss) before reclassifications | 10,171 |

| | 1 |

| | (3 | ) | | 13,127 |

| | (1,841 | ) | | 21,455 |

|

Amounts reclassified out of other comprehensive income (loss) | — |

| | — |

| | — |

| | (2,683 | ) | | 427 |

| | (2,256 | ) |

Tax effects | — |

| | 1 |

| | (1 | ) | | (2,094 | ) | | (103 | ) | | (2,197 | ) |

Other comprehensive income (loss) | 10,171 |

| | 2 |

| | (4 | ) | | 8,350 |

| | (1,517 | ) | | 17,002 |

|

February 3, 2018 | $ | (12,318 | ) | | $ | 3 |

| | $ | (5 | ) | | $ | (2,529 | ) | | $ | (29,508 | ) | | $ | (44,357 | ) |

The amounts reclassified out of accumulated OCI with presentation location during each period were as follows:

|

| | | | | | | | | | |

| | Three Months Ended | | |

Comprehensive Income Component | | February 3, 2018 | | January 28, 2017 | | Location |

Unrealized holding losses (gains) on derivatives | | | | | | |

Currency forwards | | $ | (1,275 | ) | | $ | 1,700 |

| | Cost of sales |

| | (1,069 | ) | | 1,014 |

| | Research and development |

| | (969 | ) | | 1,093 |

| | Selling, marketing, general and administrative |

Interest rate derivatives | | 630 |

| | 529 |

| | Interest expense |

| | (2,683 | ) | | 4,336 |

| | Total before tax |

| | 344 |

| | (855 | ) | | Tax |

| | $ | (2,339 | ) | | $ | 3,481 |

| | Net of tax |

| |

| | | | |

Amortization of pension components | | | | | | |

Transition obligation | | $ | 2 |

| | $ | 3 |

| | (a) |

Prior service credit | | — |

| | (2 | ) | | (a) |

Actuarial losses | | 425 |

| | 455 |

| | (a) |

| | 427 |

| | 456 |

| | Total before tax |

| | (103 | ) | | (101 | ) | | Tax |

| | $ | 324 |

| | $ | 355 |

| | Net of tax |

| | | | | | |

Total amounts reclassified out of accumulated other comprehensive income (loss), net of tax | | $ | (2,015 | ) | | $ | 3,836 |

| | |

______________

a) The amortization of pension components is included in the computation of net periodic pension cost. For further information see Note 13, Retirement Plans, contained in Item 8 of the Annual Report on Form 10-K for the fiscal year ended October 28, 2017.

The Company estimates $5.9 million, net of tax, of forward foreign currency derivative instruments included in OCI will be reclassified into earnings within the next 12 months. There was no material ineffectiveness related to designated forward foreign currency derivative instruments in the three-month periods ended February 3, 2018 and January 28, 2017.

As of February 3, 2018, the Company held 11 investment securities, 5 of which were in an unrealized loss position with immaterial gross unrealized losses and an aggregate fair value of $99.9 million. As of October 28, 2017, the Company held 18 investment securities, 8 of which were in an unrealized loss position with immaterial gross unrealized losses and an aggregate fair value of $143.9 million. These unrealized losses were primarily related to corporate obligations that earn lower interest rates than current market rates. None of these investments have been in a loss position for more than twelve months. As the Company does not intend to sell these investments and it is unlikely that the Company will be required to sell the investments

before recovery of their amortized basis, which will be at maturity, the Company does not consider those investments to be other-than-temporarily impaired at February 3, 2018 and October 28, 2017.

Realized gains or losses on investments are determined based on the specific identification basis and are recognized in nonoperating expense (income). There were no material net realized gains or losses from the sales of available-for-sale investments during any of the fiscal periods presented.

Note 5 – Earnings Per Share

Basic earnings per share is computed based only on the weighted average number of common shares outstanding during the period. Diluted earnings per share is computed using the weighted average number of common shares outstanding during the period, plus the dilutive effect of potential future issuances of common stock relating to stock option programs and other potentially dilutive securities using the treasury stock method. In calculating diluted earnings per share, the dilutive effect of stock options and restricted stock units is computed using the average market price for the respective period. In addition, the assumed proceeds under the treasury stock method include the average unrecognized compensation expense of stock options that are in-the-money and restricted stock units. This results in the “assumed” buyback of additional shares, thereby reducing the dilutive impact of in-the-money stock options. Potential shares related to certain of the Company’s outstanding stock options and restricted stock units were excluded because they were anti-dilutive. Those potential shares, determined based on the weighted average exercise prices during the respective periods, could be dilutive in the future.

In connection with the Acquisition, the Company granted restricted stock awards to replace outstanding restricted stock awards of Linear employees. These restricted stock awards entitle recipients to voting and nonforfeitable dividend rights from the date of grant. These unvested stock-based compensation awards are considered participating securities and the two-class method is used for purposes of calculating earnings per share. Under the two-class method, a portion of net income is allocated to these participating securities and therefore is excluded from the calculation of earnings per share allocated to common stock, as shown in the table below. The difference between the income allocated to participating securities under the basic and diluted two-class methods is not material.

The following table sets forth the computation of basic and diluted earnings per share:

|

| | | | | | | |

| Three Months Ended |

| February 3, 2018 | | January 28, 2017 |

Net Income | $ | 268,172 |

| | $ | 217,129 |

|

Less: income allocated to participating securities | 1,243 |

| | — |

|

Net income allocated to common stockholders | $ | 266,929 |

| | $ | 217,129 |

|

| | | |

Basic shares: | | | |

Weighted-average shares outstanding | 369,093 |

| | 308,786 |

|

Earnings per common share basic: | $ | 0.72 |

| | $ | 0.70 |

|

Diluted shares: | | | |

Weighted-average shares outstanding | 369,093 |

| | 308,786 |

|

Assumed exercise of common stock equivalents | 5,096 |

| | 4,290 |

|

Weighted-average common and common equivalent shares | 374,189 |

| | 313,076 |

|

Earnings per common share diluted: | $ | 0.71 |

| | $ | 0.69 |

|

Anti-dilutive shares related to: | | | |

Outstanding share-based awards | 1,472 |

| | 66 |

|

Note 6 – Special Charges

The Company monitors global macroeconomic conditions on an ongoing basis and continues to assess opportunities for improved operational effectiveness and efficiency, as well as a better alignment of expenses with revenues. As a result of these assessments, the Company has undertaken various restructuring actions over the past several years. These actions are described below.

The following tables display the special charges taken for ongoing actions and a roll-forward from October 28, 2017 to February 3, 2018 of the employee separation and exit cost accruals established related to these actions.

|

| | | | | | | | | | | | | | | |

| Closure of Manufacturing Facilities | | Reduction of Operating Costs Action | | Early Retirement Action | | Total Special Charges |

Statements of Income | | | | | | | |

Fiscal 2016 - Workforce reductions | $ | — |

| | $ | 13,684 |

| | $ | — |

| | 13,684 |

|

Fiscal 2017 - Workforce reductions | $ | — |

| | $ | 8,126 |

| | $ | 41,337 |

| | $ | 49,463 |

|

Fiscal 2018 - Workforce reductions | $ | 41,201 |

| | $ | 16,117 |

| | $ | — |

| | $ | 57,318 |

|

|

| | | | | | | | | | | |

Accrued Restructuring | Closure of Manufacturing Facilities | | Reduction of Operating Costs Action | | Early Retirement Action |

Balance at October 28, 2017 | $ | — |

| | $ | 5,137 |

| | $ | 32,211 |

|

Fiscal 2018 special charges | 41,201 |

| | 16,117 |

| | — |

|

Severance and other payments | — |

| | (2,798 | ) | | (6,461 | ) |

Effect of foreign currency on accrual | — |

| | 66 |

| | — |

|

Balance at February 3, 2018 | $ | 41,201 |

| | $ | 18,522 |

| | $ | 25,750 |

|

Closure of Manufacturing Facilities

During the first quarter of fiscal 2018, the Company recorded a special charge of $41.2 million as a result of its decision to consolidate certain wafer and test facility operations acquired as part of the Acquisition. Over the next three to five years, the Company plans to close its Hillview wafer fabrication facility located in Milpitas, California and its Singapore test facility. The Company intends to transfer Hillview wafer fabrication production to its other internal facilities and to external foundries. In addition, the Company is planning to transition testing operations currently handled in its Singapore facility to its facilities in Penang, Malaysia and the Philippines, in addition to its outsourced assembly and test partners. The special charge was for severance and fringe benefit costs in accordance with the Company's ongoing benefit plan or statutory requirements at foreign locations for 1,249 manufacturing, engineering and SMG&A employees. As of February 3, 2018, the Company still employed all employees included in this cost reduction action. These employees must continue to be employed by the Company until their employment is terminated in order to receive the severance benefits. The accrual related to this action is included in other non-current liabilities in the condensed consolidated balance sheet as of February 3, 2018.

Reduction of Operating Costs Action

During the second quarter of fiscal 2016, the Company recorded special charges of approximately $13.7 million for severance and fringe benefit costs in accordance with the Company's ongoing benefit plan for 123 manufacturing, engineering and SMG&A employees. As of February 3, 2018, the Company still employed 6 of the 123 employees included in this cost reduction action. These employees must continue to be employed by the Company until their employment is involuntarily terminated in order to receive the severance benefits.

During the first quarter of fiscal 2017, the Company recorded special charges of approximately $8.1 million for severance and fringe benefit costs in accordance with the Company's ongoing benefit plan or statutory requirements at foreign locations for 177 manufacturing, engineering and SMG&A employees. As of February 3, 2018, the Company still employed 7 of the 177 employees included in this cost reduction action. These employees must continue to be employed by the Company until their employment is terminated in order to receive the severance benefits.

During the first quarter of fiscal 2018, the Company recorded special charges of approximately $16.1 million for severance and fringe benefit costs in accordance with the Company's ongoing benefit plan or statutory requirements at foreign locations for 126 manufacturing, engineering and SMG&A employees. As of February 3, 2018, the Company still employed 61 of the 126 employees included in this cost reduction action. These employees must continue to be employed by the Company until their employment is terminated in order to receive the severance benefits.

The accrual related to these actions is include in accrued liabilities in the condensed consolidated balance sheet as of February 3, 2018.

Early Retirement Offer Action

During the first quarter of fiscal 2017, the Company initiated an early retirement offer. This resulted in a special charge of approximately $41.3 million for severance, related benefits and other costs in accordance with this program for 225 manufacturing, engineering and selling, marketing, general and administrative (SMG&A) employees. As of February 3,

2018, the Company still employed 5 of the 225 employees included in these cost reduction actions. These employees must continue to be employed by the Company until their employment is terminated in order to receive the severance benefits.

The accrual related to this action is include in accrued liabilities in the condensed consolidated balance sheet as of February 3, 2018.

Note 7 – Segment Information

In the first quarter of fiscal 2018, the Company completed organizational changes designed to integrate the operations of Linear into the Company’s organizational structure and to reflect the evolution of the Company's markets. As a result of these organizational changes, the Company re-evaluated its reporting structure under the new organization and concluded that the Company continues to operate in one reportable segment based on the aggregation of eight operating segments. The Company designs, develops, manufactures and markets a broad range of integrated circuits (ICs). The Chief Executive Officer has been identified as the Company's Chief Operating Decision Maker. The Company has determined that all of the Company's operating segments share the following similar economic characteristics, and therefore meet the criteria established for operating segments to be aggregated into one reportable segment, namely:

•The primary source of revenue for each operating segment is the sale of ICs.

•The ICs sold by each of the Company's operating segments are manufactured using similar semiconductor manufacturing processes and raw materials in either the Company’s own production facilities or by third-party wafer fabricators using proprietary processes.

•The Company sells its products to tens of thousands of customers worldwide. Many of these customers use products spanning all operating segments in a wide range of applications.

•The ICs marketed by each of the Company's operating segments are sold globally through a direct sales force, third-party distributors, independent sales representatives and via the Company's website to the same types of customers.

All of the Company's operating segments share similar economic characteristics, including long-term gross margins. The causes for variation in operating and financial performance are the same among the Company's operating segments and include factors such as (i) life cycle and price and cost fluctuations, (ii) number of competitors, (iii) product differentiation and (iv) size of market opportunity. Additionally, each operating segment is subject to the overall cyclical nature of the semiconductor industry. Lastly, the number and composition of employees and the amounts and types of tools and materials required for production of products are proportionately similar for each operating segment.

Revenue Trends by End Market

The following table summarizes revenue by end market for the three-month periods ended February 3, 2018 and January 28, 2017. The categorization of revenue by end market is determined using a variety of data points including the technical characteristics of the product, the “sold to” customer information, the “ship to” customer information and the end customer product or application into which the Company’s product will be incorporated. As data systems for capturing and tracking this data evolve and improve, the categorization of products by end market can vary over time. When this occurs, the Company reclassifies revenue by end market for prior periods. Such reclassifications typically do not materially change the sizing of, or the underlying trends of results within, each end market.

|

| | | | | | | | | | | | | | | | |

| Three Months Ended |

| February 3, 2018 | | January 28, 2017 |

| Revenue | | % of Revenue* | | Y/Y% | | Revenue | | % of Revenue |

Industrial | $ | 743,623 |

| | 49 | % | | 87 | % | | $ | 396,784 |

| | 40 | % |

Automotive | 252,170 |

| | 17 | % | | 76 | % | | 142,962 |

| | 15 | % |

Consumer | 238,506 |

| | 16 | % | | (12 | )% | | 270,293 |

| | 27 | % |

Communications | 284,325 |

| | 19 | % | | 63 | % | | 174,410 |

| | 18 | % |

Total revenue | $ | 1,518,624 |

| | 100 | % | | 54 | % | | $ | 984,449 |

| | 100 | % |

* The sum of the individual percentages may not equal the total due to rounding.

Revenue Trends by Geographic Region

Revenue by geographic region, based on the primary end customer location, for the three-month periods ended February 3, 2018 and January 28, 2017 were as follows:

|

| | | | | | | |

| Three Months Ended |

Region | February 3, 2018 | | January 28, 2017 |

United States | $ | 539,775 |

| | $ | 430,998 |

|

Rest of North and South America | 24,486 |

| | 22,957 |

|

Europe | 358,236 |

| | 226,335 |

|

Japan | 181,225 |

| | 88,891 |

|

China | 268,124 |

| | 152,983 |

|

Rest of Asia | 146,778 |

| | 62,285 |

|

Total revenue | $ | 1,518,624 |

| | $ | 984,449 |

|

In the three-month periods ended February 3, 2018 and January 28, 2017, the predominant country comprising “Rest of North and South America” is Canada; the predominant countries comprising “Europe” are Germany, the Netherlands and Sweden; and the predominant countries comprising “Rest of Asia” are South Korea and Taiwan.

Note 8 – Fair Value

The Company defines fair value as the price that would be received to sell an asset or be paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Company applies the following fair value hierarchy, which prioritizes the inputs used to measure fair value into three levels and bases the categorization within the hierarchy upon the lowest level of input that is available and significant to the fair value measurement. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Level 1 — Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date.

Level 2 — Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly. If the asset or liability has a specified (contractual) term, a Level 2 input must be observable for substantially the full term of the asset or liability.

Level 3 — Level 3 inputs are unobservable inputs for the asset or liability in which there is little, if any, market activity for the asset or liability at the measurement date.

The tables below, set forth by level, presents the Company’s financial assets and liabilities, excluding accrued interest components that are accounted for at fair value on a recurring basis as of February 3, 2018 and October 28, 2017. The tables exclude cash on hand and assets and liabilities that are measured at historical cost or any basis other than fair value. As of February 3, 2018 and October 28, 2017, the Company held $306.0 million and $296.2 million, respectively, of cash and held-to-maturity investments that were excluded from the tables below.

|

| | | | | | | | | | | |

| February 3, 2018 |

| Fair Value measurement at Reporting Date using: | | |

| Quoted Prices in Active Markets for Identical Assets (Level 1) | | Significant Other Observable Inputs (Level 2) | | Total |

Assets | | | | | |

Cash equivalents: | | | | | |

Available-for-sale: | | | | | |

Government and institutional money market funds | $ | 391,726 |

| | $ | — |

| | $ | 391,726 |

|

Corporate obligations (1) | — |

| | 129,784 |

| | 129,784 |

|

Other assets: | | | | | |

Deferred compensation investments | 39,841 |

| | — |

| | 39,841 |

|

Interest rate derivatives | — |

| | 5,572 |

| | 5,572 |

|

Forward foreign currency exchange contracts (2) | — |

| | 10,522 |

| | 10,522 |

|

Total assets measured at fair value | $ | 431,567 |

| | $ | 145,878 |

| | $ | 577,445 |

|

| |

(1) | The amortized cost of the Company’s investments classified as available-for-sale as of February 3, 2018 was $129.8 million. |

| |

(2) | The Company has master netting arrangements by counterparty with respect to derivative contracts. See Note 9, Derivatives, of these Notes to Condensed Consolidated Financial Statements for more information related to the Company's master netting arrangements. |

|

| | | | | | | | | | | |

| October 28, 2017 |

| Fair Value measurement at Reporting Date using: | | |

| Quoted Prices in Active Markets for Identical Assets

(Level 1) | | Significant Other Observable Inputs

(Level 2) | | Total |

Assets | | | | | |

Cash equivalents: | | | | | |

Available-for-sale: | | | | | |

Government and institutional money market funds | $ | 512,882 |

| | $ | — |

| | $ | 512,882 |

|

Corporate obligations (1) | — |

| | 238,796 |

| | 238,796 |

|

Other assets: | | | | | |

Deferred compensation investments | 33,510 |

| | — |

| | 33,510 |

|

Interest rate derivatives | — |

| | 2,966 |

| | 2,966 |

|

Total assets measured at fair value | $ | 546,392 |

| | $ | 241,762 |

| | $ | 788,154 |

|

Liabilities | | | | | |

Forward foreign currency exchange contracts (2) | — |

| | 1,527 |

| | 1,527 |

|

Total liabilities measured at fair value | $ | — |

| | $ | 1,527 |

| | $ | 1,527 |

|

| |

(1) | The amortized cost of the Company’s investments classified as available-for-sale as of October 28, 2017 was $238.9 million. |

| |

(2) | The Company has master netting arrangements by counterparty with respect to derivative contracts. See Note 9, Derivatives, of these Notes to Condensed Consolidated Financial Statements for more information related to the Company's master netting arrangements. |

In addition to the above, the Company has recognized contingent consideration payable at fair value (Level 3 measure) of $7.7 million and $7.8 million as of February 3, 2018 and October 28, 2017, respectively. The changes in fair value in those periods ended were not material.

The following methods and assumptions were used by the Company in estimating its fair value disclosures for financial instruments:

Cash equivalents and short-term investments — These investments are adjusted to fair value based on quoted market prices or are determined using a yield curve model based on current market rates.

Deferred compensation plan investments — The fair value of these mutual fund, money market fund and equity investments are based on quoted market prices.

Forward foreign currency exchange contracts — The estimated fair value of forward foreign currency exchange contracts, which includes derivatives that are accounted for as cash flow hedges and those that are not designated as cash flow hedges, is based on the estimated amount the Company would receive if it sold these agreements at the reporting date taking into consideration current interest rates as well as the creditworthiness of the counterparty for assets and the Company’s creditworthiness for liabilities. The fair value of these instruments is based upon valuation models using current market information such as strike price, spot rate, maturity date and volatility.

Interest rate derivatives — The fair value of the interest rate derivatives is estimated using a discounted cash flow analysis based on the contractual terms of the derivative.

Contingent consideration — The fair value of the contingent consideration was estimated utilizing the income approach and is based upon significant inputs not observable in the market. The income approach is based on two steps. The first step

involves a projection of the cash flows that is based on the Company’s estimates of the timing and probability of achieving the defined milestones. The second step involves converting the cash flows into a present value equivalent through discounting. The discount rate reflects the Baa costs of debt plus the relevant risk associated with the asset and the time value of money.

Financial Instruments Not Recorded at Fair Value on a Recurring Basis

The table below presents the estimated fair value of certain financial instruments not recorded at fair value on a recurring basis. The carrying amounts of the term loans approximate fair value. The term loans are classified as Level 2 measurements according to the fair value hierarchy. The fair values of the senior unsecured notes are obtained from broker prices and are classified as Level 1 measurements according to the fair value hierarchy.

|

| | | | | | | | | | | | | | | |

| February 3, 2018 | | October 28, 2017 |

| Principal Amount Outstanding | | Fair Value | | Principal Amount Outstanding | | Fair Value |

3-Year term loan | $ | 1,530,000 |

| | 1,530,000 |

| | 1,950,000 |

| | 1,950,000 |

|

5-Year term loan | 2,100,000 |

| | 2,100,000 |

| | 2,100,000 |

| | 2,100,000 |

|

2021 Notes, due December 2021 | 400,000 |

| | 393,128 |

| | 400,000 |

| | 399,530 |

|

2023 Notes, due June 2023 | 500,000 |

| | 489,917 |

| | 500,000 |

| | 498,582 |

|

2023 Notes, due December 2023 | 550,000 |

| | 543,756 |

| | 550,000 |

| | 554,411 |

|

2025 Notes, due December 2025 | 850,000 |

| | 866,552 |

| | 850,000 |

| | 884,861 |

|

2026 Notes, due December 2026 | 900,000 |

| | 884,966 |

| | 900,000 |

| | 902,769 |

|

2036 Notes, due December 2036 | 250,000 |

| | 258,660 |

| | 250,000 |

| | 259,442 |

|

2045 Notes, due December 2045 | 400,000 |

| | 463,074 |

| | 400,000 |

| | 460,588 |

|

Total Debt | $ | 7,480,000 |

| | $ | 7,530,053 |

| | $ | 7,900,000 |

| | $ | 8,010,183 |

|

Note 9 – Derivatives

Foreign Exchange Exposure Management — The Company enters into forward foreign currency exchange contracts to offset certain operational and balance sheet exposures from the impact of changes in foreign currency exchange rates. Such exposures result from the portion of the Company’s operations, assets and liabilities that are denominated in currencies other than the U.S. dollar, primarily the Euro; other significant exposures include the Philippine Peso, the Japanese Yen and the British Pound. These foreign currency exchange contracts are entered into to support transactions made in the normal course of business, and accordingly, are not speculative in nature. The contracts are for periods consistent with the terms of the underlying transactions, generally one year or less. Hedges related to anticipated transactions are designated and documented at the inception of the respective hedges as cash flow hedges and are evaluated for effectiveness monthly. Derivative instruments are employed to eliminate or minimize certain foreign currency exposures that can be confidently identified and quantified. As the terms of the contract and the underlying transaction are matched at inception, forward contract effectiveness is calculated by comparing the change in fair value of the contract to the change in the forward value of the anticipated transaction, with the effective portion of the gain or loss on the derivative reported as a component of accumulated OCI in shareholders’ equity and reclassified into earnings in the same period during which the hedged transaction affects earnings. Any residual change in fair value of the instruments, or ineffectiveness, is recognized immediately in other (income) expense.

The total notional amount of forward foreign currency derivative instruments designated as hedging instruments of cash flow hedges denominated in Euros, British Pounds, Philippine Pesos and Japanese Yen as of February 3, 2018 and October 28, 2017 was $205.9 million and $194.3 million, respectively. The fair value of forward foreign currency derivative instruments designated as hedging instruments in the Company’s condensed consolidated balance sheets as of February 3, 2018 and October 28, 2017 was as follows:

|

| | | | | | | | | |

| | | Fair Value At |

| Balance Sheet Location | | February 3, 2018 | | October 28, 2017 |

Forward foreign currency exchange contracts | Prepaid expenses and other current assets | | $ | 8,593 |

| | $ | 257 |

|

Additionally, the Company enters into forward foreign currency contracts that economically hedge the gains and losses generated by the re-measurement of certain recorded assets and liabilities in a non-functional currency. Changes in the fair value of these undesignated hedges are recognized in other (income) expense immediately as an offset to the changes in the fair value of the asset or liability being hedged. As of February 3, 2018 and October 28, 2017, the total notional amount of these undesignated hedges was $94.8 million and $100.4 million, respectively. The fair value of these hedging instruments in the

Company’s condensed consolidated balance sheets was an asset of $1.9 million as of February 3, 2018 and a liability of $1.8 million as of October 28, 2017.

All of the Company’s derivative financial instruments are eligible for netting arrangements that allow the Company and its counterparties to net settle amounts owed to each other. Derivative assets and liabilities that can be net settled under these arrangements have been presented in the Company's condensed consolidated balance sheet on a net basis. As of February 3, 2018 and October 28, 2017, none of the master netting arrangements involved collateral. The following table presents the gross amounts of the Company's derivative assets and liabilities and the net amounts recorded in the Company's condensed consolidated balance sheet:

|

| | | | | | | |

| February 3, 2018 | | October 28, 2017 |

Gross amount of recognized assets (liabilities) | $ | 11,645 |

| | $ | (5,039 | ) |

Gross amounts of recognized (liabilities) assets offset in the condensed consolidated balance sheet | (1,123 | ) | | 3,512 |

|

Net assets (liabilities) presented in the condensed consolidated balance sheet | $ | 10,522 |

| | $ | (1,527 | ) |

Interest Rate Exposure Management — The Company's current and future debt may be subject to interest rate risk. The Company utilizes interest rate derivatives to alter interest rate exposure in an attempt to reduce the effects of these changes.

The market risk associated with the Company’s derivative instruments results from currency exchange rate or interest rate movements that are expected to offset the market risk of the underlying transactions, assets and liabilities being hedged. The counterparties to the agreements relating to the Company’s derivative instruments consist of a number of major international financial institutions with high credit ratings. Based on the credit ratings of the Company’s counterparties as of February 3, 2018 and October 28, 2017, nonperformance is not perceived to be a significant risk. Furthermore, none of the Company’s derivatives are subject to collateral or other security arrangements and none contain provisions that are dependent on the Company’s credit ratings from any credit rating agency. While the contract or notional amounts of derivative financial instruments provide one measure of the volume of these transactions, they do not represent the amount of the Company’s exposure to credit risk. The amounts potentially subject to credit risk (arising from the possible inability of counterparties to meet the terms of their contracts) are generally limited to the amounts, if any, by which the counterparties’ obligations under the contracts exceed the obligations of the Company to the counterparties. As a result of the above considerations, the Company does not consider the risk of counterparty default to be significant.

The Company records the fair value of its derivative financial instruments in its condensed consolidated financial statements in other current assets, other assets or accrued liabilities, depending on their net position, regardless of the purpose or intent for holding the derivative contract. Changes in the fair value of the derivative financial instruments are either recognized periodically in earnings or in shareholders’ equity as a component of OCI. Changes in the fair value of cash flow hedges are recorded in OCI and reclassified into earnings when the underlying contract matures and, for interest rate exposure derivatives, over the term of the corresponding debt instrument. Changes in the fair values of derivatives not qualifying for hedge accounting or the ineffective portion of designated hedges are reported in earnings as they occur.

For information on the unrealized holding gains (losses) on derivatives included in and reclassified out of accumulated other comprehensive income into the condensed consolidated statement of income related to forward foreign currency exchange contracts, see Note 4, Accumulated Other Comprehensive Income (Loss) of these Notes to Condensed Consolidated Financial Statements for further information.

Note 10 – Goodwill and Intangible Assets

Goodwill

The Company evaluates goodwill for impairment annually, as well as whenever events or changes in circumstances suggest that the carrying value of goodwill may not be recoverable. The Company tests goodwill for impairment at the reporting unit level, which we have determined is consistent with our operating segments, on an annual basis on the first day of the fourth quarter (on or about August 1) or more frequently if indicators of impairment exist or the Company reorganizes its reporting units. In the first quarter of fiscal 2018, the Company completed organizational changes designed to integrate the operations of Linear into the Company’s organizational structure and to reflect the evolution of the Company's markets. The Company performed an impairment analysis immediately prior to and subsequent to the reorganization and evaluated goodwill for impairment as of the date of reorganization. The goodwill impairment test requires an entity to compare the fair value of a reporting unit with its carrying amount. The Company determines the fair value of its reporting units using a weighting of the income and market approaches. Under the income approach, the Company uses a discounted cash flow methodology which requires management to make significant estimates and assumptions related to forecasted revenues, gross profit margins,

operating income margins, working capital cash flow, perpetual growth rates, and long-term discount rates, among others. For the market approach, the Company uses the guideline public company method. Under this method, the Company utilizes information from comparable publicly traded companies with similar operating and investment characteristics as the reporting units, to create valuation multiples that are applied to the operating performance of the reporting unit being tested, in order to estimate their respective fair values. In order to assess the reasonableness of the calculated reporting unit fair values, the Company reconciles the aggregate estimated fair values of its reporting units determined to its current market capitalization, allowing for a reasonable control premium. If the carrying amount of a reporting unit, calculated using the above approaches, exceeds the reporting unit’s fair value, an impairment loss is recognized for the amount of the carrying value that exceeds the amount of the reporting unit's fair value, not to exceed the total amount of goodwill allocated to the reporting unit. Additionally, the Company considers income tax effects from any tax deductible goodwill on the carrying amount of the reporting unit when measuring the goodwill impairment loss, if applicable. There was no impairment of goodwill in any period presented. The Company's next annual impairment assessment will be performed as of the first day of the fourth quarter of fiscal 2018 unless indicators arise that would require the Company to re-evaluate at an earlier date. The following table presents the changes in goodwill during the first three months of fiscal 2018:

|

| | | |

| Three Months Ended |

| February 3, 2018 |

Balance as of October 28, 2017 | $ | 12,217,455 |

|

Goodwill related to acquisition of Linear (Note 13) | 1,647 |

|

Foreign currency translation adjustment | 5,039 |

|

Balance as of February 3, 2018 | $ | 12,224,141 |

|

Intangible Assets

The Company reviews finite-lived intangible assets for impairment whenever events or changes in circumstances indicate that the carrying value of assets may not be recoverable. Recoverability of these assets is determined by comparison of their carrying value to the estimated future undiscounted cash flows the assets are expected to generate over their remaining estimated useful lives. If such assets are considered to be impaired, the impairment to be recognized in earnings equals the amount by which the carrying value of the assets exceeds their estimated fair value determined by either a quoted market price, if any, or a value determined by utilizing a discounted cash flow technique.

Indefinite-lived intangible assets are tested for impairment on an annual basis on the first day of the fourth quarter (on or about August 1) or more frequently if indicators of impairment exist. The impairment test involves a qualitative assessment on the indefinite-lived intangible assets to determine whether it is more likely-than not that the indefinite-lived intangible asset is impaired. If it is determined that the fair value of the indefinite-lived intangible asset is less than the carrying value, the Company would recognize into earnings the amount by which the carrying value of the assets exceeds the estimated fair value. No impairment of intangible assets resulted from the impairment tests in any of the fiscal years presented.

Definite-lived intangible assets are amortized on a straight-line basis over their estimated useful lives or on an accelerated method of amortization that is expected to reflect the estimated pattern of economic use. In-process research and development (IPR&D) assets are considered indefinite-lived intangible assets until completion or abandonment of the associated research and development (R&D) efforts. Upon completion of the projects, the IPR&D assets are reclassified to technology-based intangible assets and amortized over their estimated useful lives.

As of February 3, 2018 and October 28, 2017, the Company’s intangible assets consisted of the following:

|

| | | | | | | | | | | | | | | |

| February 3, 2018 | | October 28, 2017 |

| Gross Carrying Amount | | Accumulated Amortization | | Gross Carrying Amount | | Accumulated Amortization |

Customer relationships | $ | 4,688,167 |

| | $ | 553,710 |

| | $ | 4,683,461 |

| | $ | 449,369 |

|

Technology-based | 1,097,078 |

| | 137,034 |

| | 1,097,025 |

| | 101,920 |

|

Trade-name | 72,800 |

| | 9,559 |

| | 72,800 |

| | 6,906 |

|

IPR&D | 24,613 |

| | — |

| | 24,334 |

| | — |

|

Total (1)(2) | $ | 5,882,658 |

| | $ | 700,303 |

| | $ | 5,877,620 |

| | $ | 558,195 |

|

___________

(1) Foreign intangible asset carrying amounts are affected by foreign currency translation.

(2) Increases in intangible assets primarily relate to the Acquisition and other acquisitions. See Note 13, Acquisitions, of these Notes to Condensed Consolidated Financial Statements for further information.

Intangible assets, along with the related accumulated amortization, are removed from the table above at the end of the fiscal year they become fully amortized.

For the three-month periods ended February 3, 2018 and January 28, 2017, amortization expense related to finite-lived intangible assets was $142.1 million and $19.9 million, respectively. The remaining amortization expense will be recognized over an estimated weighted average life of approximately 5.0 years.

The Company expects annual amortization expense for intangible assets to be:

|

| | | |

Fiscal Year | Amortization Expense |

Remainder of fiscal 2018 |

| $424,435 |

|

2019 |

| $563,097 |

|

2020 |

| $562,859 |

|

2021 |

| $562,438 |

|

2022 |

| $559,508 |

|

Note 11 – Debt

On November 10, 2017, the Company paid $300.0 million of principal on its 3-year unsecured term loan using cash on hand as of October 28, 2017. This amount was not contractually due under the terms of the loan. As such, this amount was classified as current in the condensed consolidated balance sheet as of October 28, 2017. On January 10, 2018, the Company paid $120.0 million of principal on its 3-year unsecured term loan. This amount was not contractually due under the terms of the loan. Subsequent to the close of the first quarter of fiscal 2018, on February 12, 2018, the Company paid $50.0 million of principal on its 3-year unsecured term loan. This amount was not contractually due under the terms of the loan. As such this amount was classified as current in the condensed consolidated balance sheet as of February 3, 2018.

Note 12 – Inventories

Inventories are valued at the lower of cost (first-in, first-out method) or market. The valuation of inventory requires the Company to estimate obsolete or excess inventory as well as inventory that is not of saleable quality. The Company employs a variety of methodologies to determine the net realizable value of its inventory. While a portion of the calculation to record inventory at its net realizable value is based on the age of the inventory and lower of cost or market calculations, a key factor in estimating obsolete or excess inventory requires the Company to estimate the future demand for its products. If actual demand is less than the Company’s estimates, impairment charges, which are recorded to cost of sales, may need to be recorded in future periods. Inventory in excess of saleable amounts is not valued, and the remaining inventory is valued at the lower of cost or market.

Inventories at February 3, 2018 and October 28, 2017 were as follows:

|

| | | | | | | |

| February 3, 2018 | | October 28, 2017 |

Raw materials | $ | 37,753 |

| | $ | 35,436 |

|

Work in process | 359,809 |

| | 376,476 |

|

Finished goods | 162,158 |

| | 138,904 |

|

Total inventories | $ | 559,720 |

| | $ | 550,816 |

|

Note 13 – Acquisitions

Linear Technology Corporation

On March 10, 2017 (Acquisition Date), the Company completed its acquisition of all of the voting interests of Linear, an independent manufacturer of high performance analog integrated circuits. The total consideration paid, which consisted of cash, common stock of the Company and share-based compensation awards, to acquire Linear was approximately $15.8 billion. The Company believes that the combination creates the premier analog technology company with the industry’s most comprehensive suite of high-performance analog offerings. The results of operations of Linear from the Acquisition Date are

included in the Company’s condensed consolidated statements of income, condensed consolidated balance sheet, and condensed consolidated statement of cash flows for the three-month period ended February 3, 2018.

During the first quarter of fiscal 2018, the Company recorded acquisition accounting adjustments of $1.6 million to goodwill comprised of $4.7 million to intangible assets, $2.7 million to accounts receivable, $2.4 million to assumed liabilities and $1.1 million to deferred tax liabilities. The Acquisition accounting is not complete and additional information that existed at the Acquisition Date may become known to the Company during the remainder of the measurement period. As of the filing date of this Quarterly Report on Form 10-Q, the Company is still in the process of valuing the assets acquired with Linear’s business, including deferred income taxes.

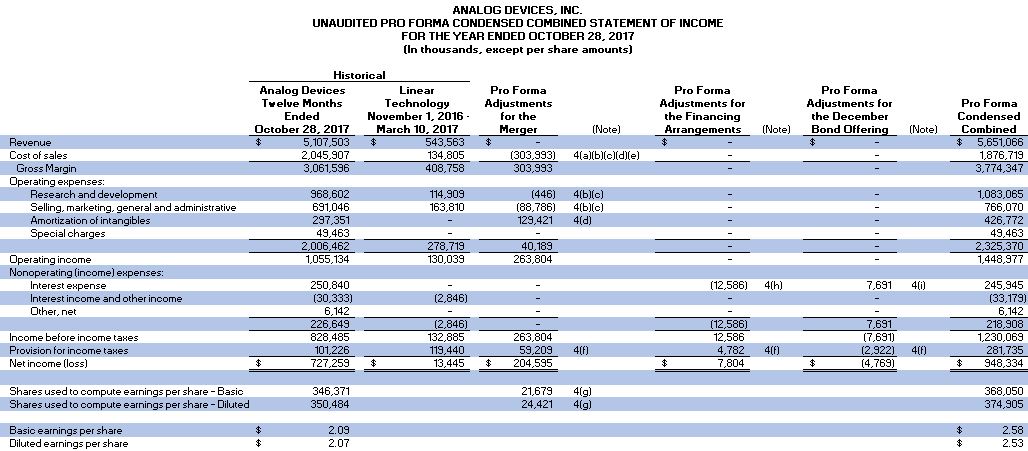

The following unaudited pro forma consolidated financial information combines the unaudited results of the Company for the three-month period ended January 28, 2017 and the unaudited results of Linear for the three-month period ended January 28, 2017 and assumes that the Acquisition, which closed on March 10, 2017, was completed on November 1, 2015 (the first day of fiscal 2016). The pro forma consolidated financial information has been calculated after applying the Company’s accounting policies and includes adjustments for amortization expense of acquired intangible assets, transaction-related costs, a step-up in the value of acquired inventory and property, plant and equipment, compensation expense for ongoing share-based compensation arrangements replaced and interest expense for the debt incurred to fund the Acquisition, together with the consequential tax effects. These pro forma results have been prepared for comparative purposes only and do not purport to be indicative of the operating results of the Company that would have been achieved had the Acquisition actually taken place on November 1, 2015. In addition, these results are not intended to be a projection of future results and do not reflect events that may occur after the Acquisition, including but not limited to revenue enhancements, cost savings or operating synergies that the combined Company may achieve as a result of the Acquisition.

|

| | | | |

(thousands, except per share data) | | Pro Forma Three Months Ended |

| | January 28, 2017 |

Revenue | | $ | 1,362,447 |

|

Net income | | $ | 233,398 |

|

Basic net income per common share | | $ | 0.64 |

|

Diluted net income per common share | | $ | 0.63 |

|

Other Acquisitions

The Company has not provided pro forma results of operations for any other acquisitions completed in the three-month periods ended February 3, 2018 or January 28, 2017 herein as they were not material to the Company on either an individual or an aggregate basis. The Company included the results of operations of each acquisition in its consolidated statement of income from the date of each acquisition.

Note 14 – Income Taxes

The Company has provided for potential tax liabilities due in the various jurisdictions in which the Company operates. Judgment is required in determining the worldwide income tax provision. In the ordinary course of global business, there are many transactions and calculations where the ultimate tax outcome is uncertain. Some of these uncertainties arise as a consequence of cost reimbursement arrangements among related entities. Although the Company believes its estimates are reasonable, no assurance can be given that the final tax outcome of these matters will not be different from that which is reflected in the historical income tax provisions and accruals. Such differences could have a material impact on the Company’s income tax provision and operating results in the period in which such determination is made.

The Company’s effective tax rate reflects the applicable tax rate in effect in the various tax jurisdictions around the world where the Company's income is earned. The Company's effective tax rate is generally lower than the U.S. federal statutory rate, primarily due to lower statutory tax rates applicable to the Company's operations in jurisdictions in which the Company earns a portion of its income.

The Tax Cuts and Jobs Act of 2017 (Tax Legislation), enacted on December 22, 2017, contains significant changes to U.S. tax law, including lowering the U.S. corporate income tax rate to 21.0%, implementing a territorial tax system, and imposing a one-time tax on deemed repatriated earnings of foreign subsidiaries. As of February 3, 2018, the Company has not completed its accounting for the tax effects of the enactment of the Tax Legislation. However, as described below the Company has made reasonable estimates of the effects on its existing deferred tax balances and the one-time transition tax.

The Tax Legislation reduces the U.S. statutory tax rate from 35.0% to 21.0%, effective January 1, 2018, which results in a blended statutory income tax rate for the Company of 23.4% for fiscal 2018. For the fiscal year ending November 2, 2019 (fiscal 2019), the Company’s statutory income tax rate will be 21.0%.

During the three months ended February 3, 2018, the Company recorded a $639.7 million discrete tax benefit for the remeasurement of deferred tax assets and liabilities based on the rates at which they are expected to reverse in the future, which is generally 21.0%. This provisional benefit is subject to revision based on further analysis and interpretation of the Tax Legislation and to the extent that future results differ from currently available projections.

The Tax Legislation also implements a territorial tax system. As part of transitioning to the territorial tax system, the Tax Legislation includes a one-time transition tax based on our total post-1986 undistributed foreign earnings and profits that were previously deferred from U.S. income tax. During the three-month period ended February 3, 2018, the Company recorded a provisional tax expense amount for the one-time transition tax of $687.1 million, which is comprised of the $751.1 million transition tax liability less a deferred tax liability of $64.0 million recorded in prior years. This provisional estimate may be impacted by a number of additional considerations, including, but not limited to, the issuance of final tax regulations, the Company's ongoing analysis of the Tax Legislation, the Company's earnings and profits subject to the one-time transition tax, and estimated earnings and profits and foreign tax credit pools for fiscal 2018 as well as the amount of earnings and profits held in cash or other specified assets. The Company intends to elect to pay this transition tax starting in fiscal 2019 without incurring interest over a period of eight years. As a result, $60.1 million of the transition tax is classified as current taxes payable and $691.0 million is classified as non-current taxes payable.

The Company recorded a $10.0 million discrete benefit for excess tax benefits from share-based payments, pursuant to ASU 2016-09, which became effective for fiscal 2018.