UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-1193

Fidelity Magellan Fund

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Marc Bryant, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

Date of fiscal year end: | March 31 |

Date of reporting period: | September 30, 2017 |

Item 1.

Reports to Stockholders

|

Fidelity® Magellan® Fund Semi-Annual Report September 30, 2017 |

|

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-835-5092 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2017 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Investment Summary (Unaudited)

Top Ten Stocks as of September 30, 2017

| % of fund's net assets | % of fund's net assets 6 months ago | |

| Apple, Inc. | 6.1 | 7.7 |

| Amgen, Inc. | 3.1 | 3.1 |

| Caterpillar, Inc. | 2.8 | 1.8 |

| JPMorgan Chase & Co. | 2.6 | 2.8 |

| Alphabet, Inc. Class A | 2.6 | 1.7 |

| Alphabet, Inc. Class C | 2.6 | 1.7 |

| Facebook, Inc. Class A | 2.5 | 2.2 |

| Amazon.com, Inc. | 2.4 | 2.4 |

| UnitedHealth Group, Inc. | 2.3 | 1.9 |

| Bank of America Corp. | 2.2 | 3.6 |

| 29.2 |

Top Five Market Sectors as of September 30, 2017

| % of fund's net assets | % of fund's net assets 6 months ago | |

| Information Technology | 28.1 | 24.5 |

| Financials | 16.5 | 20.8 |

| Health Care | 14.0 | 12.4 |

| Industrials | 12.7 | 10.6 |

| Consumer Discretionary | 10.9 | 11.7 |

Asset Allocation (% of fund's net assets)

| As of September 30, 2017 * | ||

| Stocks and Equity Futures | 98.4% | |

| Convertible Securities | 1.0% | |

| Short-Term Investments and Net Other Assets (Liabilities) | 0.6% | |

* Foreign investments - 8.1%

| As of March 31, 2017 * | ||

| Stocks and Equity Futures | 98.2% | |

| Convertible Securities | 1.2% | |

| Short-Term Investments and Net Other Assets (Liabilities) | 0.6% | |

* Foreign investments - 7.7%

Investments September 30, 2017

Showing Percentage of Net Assets

| Common Stocks - 97.9% | |||

| Shares | Value (000s) | ||

| CONSUMER DISCRETIONARY - 10.8% | |||

| Automobiles - 0.5% | |||

| Tesla, Inc. (a) | 225,900 | $77,054 | |

| Diversified Consumer Services - 1.0% | |||

| New Oriental Education & Technology Group, Inc. sponsored ADR | 959,400 | 84,677 | |

| Service Corp. International | 2,386,132 | 82,322 | |

| 166,999 | |||

| Hotels, Restaurants & Leisure - 0.8% | |||

| Darden Restaurants, Inc. | 1,111,800 | 87,588 | |

| Papa John's International, Inc. | 569,400 | 41,606 | |

| 129,194 | |||

| Household Durables - 0.4% | |||

| Roku, Inc. Class A | 2,665,553 | 63,669 | |

| Internet & Direct Marketing Retail - 5.3% | |||

| Amazon.com, Inc. (a) | 407,400 | 391,654 | |

| JD.com, Inc. sponsored ADR (a) | 395,700 | 15,116 | |

| Netflix, Inc. (a) | 1,003,700 | 182,021 | |

| Priceline Group, Inc. (a) | 150,300 | 275,172 | |

| 863,963 | |||

| Media - 0.4% | |||

| Sirius XM Holdings, Inc. (b) | 7,532,900 | 41,582 | |

| WME Entertainment Parent, LLC Class A (a)(c)(d)(e) | 7,417,027 | 18,543 | |

| 60,125 | |||

| Multiline Retail - 0.3% | |||

| Dollar Tree, Inc. (a) | 394,400 | 34,242 | |

| JC Penney Corp., Inc. (a) | 436,800 | 1,664 | |

| Macy's, Inc. | 294,500 | 6,426 | |

| 42,332 | |||

| Specialty Retail - 1.5% | |||

| Home Depot, Inc. | 1,374,900 | 224,879 | |

| Ross Stores, Inc. | 437,300 | 28,236 | |

| 253,115 | |||

| Textiles, Apparel & Luxury Goods - 0.6% | |||

| PVH Corp. | 815,900 | 102,852 | |

| TOTAL CONSUMER DISCRETIONARY | 1,759,303 | ||

| CONSUMER STAPLES - 7.2% | |||

| Beverages - 3.5% | |||

| Anheuser-Busch InBev SA NV | 351,260 | 41,989 | |

| Constellation Brands, Inc. Class A (sub. vtg.) | 452,900 | 90,331 | |

| Molson Coors Brewing Co. Class B | 615,700 | 50,266 | |

| Monster Beverage Corp. (a) | 4,000,700 | 221,039 | |

| The Coca-Cola Co. | 3,622,300 | 163,040 | |

| 566,665 | |||

| Food & Staples Retailing - 1.4% | |||

| CVS Health Corp. | 1,258,100 | 102,309 | |

| Wal-Mart Stores, Inc. | 1,545,100 | 120,734 | |

| 223,043 | |||

| Food Products - 1.0% | |||

| Mondelez International, Inc. | 1,347,400 | 54,785 | |

| Post Holdings, Inc. (a) | 959,400 | 84,686 | |

| The J.M. Smucker Co. | 282,000 | 29,590 | |

| 169,061 | |||

| Personal Products - 1.3% | |||

| elf Beauty, Inc. (b) | 1,943,200 | 43,819 | |

| Estee Lauder Companies, Inc. Class A | 584,000 | 62,979 | |

| Unilever NV (Certificaten Van Aandelen) (Bearer) | 1,825,500 | 107,907 | |

| 214,705 | |||

| TOTAL CONSUMER STAPLES | 1,173,474 | ||

| ENERGY - 6.5% | |||

| Energy Equipment & Services - 1.8% | |||

| Baker Hughes, a GE Co. Class A | 2,121,400 | 77,686 | |

| National Oilwell Varco, Inc. | 2,684,900 | 95,931 | |

| Schlumberger Ltd. | 1,834,200 | 127,954 | |

| 301,571 | |||

| Oil, Gas & Consumable Fuels - 4.7% | |||

| Anadarko Petroleum Corp. | 2,982,000 | 145,671 | |

| Apache Corp. | 2,104,000 | 96,363 | |

| Cimarex Energy Co. | 474,600 | 53,948 | |

| ConocoPhillips Co. | 3,820,800 | 191,231 | |

| EOG Resources, Inc. | 936,400 | 90,587 | |

| Newfield Exploration Co. (a) | 1,245,600 | 36,957 | |

| Pioneer Natural Resources Co. | 309,300 | 45,634 | |

| The Williams Companies, Inc. | 3,316,800 | 99,537 | |

| 759,928 | |||

| TOTAL ENERGY | 1,061,499 | ||

| FINANCIALS - 16.5% | |||

| Banks - 9.7% | |||

| Bank of America Corp. | 14,232,200 | 360,644 | |

| Citigroup, Inc. | 4,456,216 | 324,145 | |

| JPMorgan Chase & Co. | 4,449,598 | 424,981 | |

| Regions Financial Corp. | 3,753,100 | 57,160 | |

| U.S. Bancorp | 2,668,259 | 142,992 | |

| Wells Fargo & Co. | 4,908,855 | 270,723 | |

| 1,580,645 | |||

| Capital Markets - 4.1% | |||

| BlackRock, Inc. Class A | 293,300 | 131,131 | |

| Goldman Sachs Group, Inc. | 644,500 | 152,869 | |

| Morgan Stanley | 1,972,700 | 95,025 | |

| MSCI, Inc. | 832,300 | 97,296 | |

| Northern Trust Corp. | 1,095,000 | 100,663 | |

| PJT Partners, Inc. | 161,145 | 6,173 | |

| The Blackstone Group LP | 2,505,400 | 83,605 | |

| 666,762 | |||

| Diversified Financial Services - 2.2% | |||

| Berkshire Hathaway, Inc. Class B (a) | 1,931,466 | 354,076 | |

| Insurance - 0.5% | |||

| Chubb Ltd. | 650,596 | 92,742 | |

| TOTAL FINANCIALS | 2,694,225 | ||

| HEALTH CARE - 14.0% | |||

| Biotechnology - 5.0% | |||

| Alexion Pharmaceuticals, Inc. (a) | 671,300 | 94,177 | |

| Amgen, Inc. | 2,724,987 | 508,074 | |

| Amicus Therapeutics, Inc. (a) | 5,739,034 | 86,545 | |

| Clinical Data, Inc. rights 4/4/18 (a)(e) | 988,714 | 0 | |

| Regeneron Pharmaceuticals, Inc. (a) | 163,300 | 73,015 | |

| Vertex Pharmaceuticals, Inc. (a) | 345,200 | 52,484 | |

| 814,295 | |||

| Health Care Equipment & Supplies - 2.4% | |||

| Boston Scientific Corp. (a) | 6,984,000 | 203,723 | |

| Danaher Corp. | 2,246,800 | 192,731 | |

| 396,454 | |||

| Health Care Providers & Services - 3.0% | |||

| Cigna Corp. | 482,700 | 90,236 | |

| Humana, Inc. | 101,700 | 24,777 | |

| UnitedHealth Group, Inc. | 1,960,100 | 383,886 | |

| 498,899 | |||

| Life Sciences Tools & Services - 1.8% | |||

| Agilent Technologies, Inc. | 2,113,800 | 135,706 | |

| Bruker Corp. | 2,807,662 | 83,528 | |

| Thermo Fisher Scientific, Inc. | 396,100 | 74,942 | |

| 294,176 | |||

| Pharmaceuticals - 1.8% | |||

| Allergan PLC | 605,561 | 124,110 | |

| Bristol-Myers Squibb Co. | 1,943,200 | 123,860 | |

| Jazz Pharmaceuticals PLC (a) | 274,140 | 40,093 | |

| 288,063 | |||

| TOTAL HEALTH CARE | 2,291,887 | ||

| INDUSTRIALS - 12.7% | |||

| Aerospace & Defense - 6.7% | |||

| General Dynamics Corp. | 834,200 | 171,495 | |

| Huntington Ingalls Industries, Inc. | 812,433 | 183,967 | |

| Lockheed Martin Corp. | 288,900 | 89,643 | |

| Northrop Grumman Corp. | 1,163,200 | 334,676 | |

| Raytheon Co. | 1,124,800 | 209,865 | |

| United Technologies Corp. | 896,300 | 104,043 | |

| 1,093,689 | |||

| Airlines - 0.4% | |||

| Southwest Airlines Co. | 1,160,500 | 64,965 | |

| Building Products - 0.3% | |||

| A.O. Smith Corp. | 768,600 | 45,678 | |

| Construction & Engineering - 0.3% | |||

| Jacobs Engineering Group, Inc. | 799,500 | 46,587 | |

| Electrical Equipment - 0.1% | |||

| Fortive Corp. | 407,750 | 28,865 | |

| Machinery - 3.5% | |||

| Allison Transmission Holdings, Inc. | 2,040,200 | 76,569 | |

| Caterpillar, Inc. | 3,721,200 | 464,071 | |

| WABCO Holdings, Inc. (a) | 198,100 | 29,319 | |

| 569,959 | |||

| Professional Services - 1.1% | |||

| IHS Markit Ltd. (a) | 4,125,400 | 181,848 | |

| Trading Companies & Distributors - 0.3% | |||

| HD Supply Holdings, Inc. (a) | 1,265,200 | 45,636 | |

| TOTAL INDUSTRIALS | 2,077,227 | ||

| INFORMATION TECHNOLOGY - 27.2% | |||

| Electronic Equipment & Components - 0.2% | |||

| CDW Corp. | 529,600 | 34,954 | |

| Internet Software & Services - 8.1% | |||

| Alibaba Group Holding Ltd. sponsored ADR (a) | 110,200 | 19,033 | |

| Alphabet, Inc.: | |||

| Class A (a) | 432,416 | 421,052 | |

| Class C (a) | 436,154 | 418,320 | |

| Facebook, Inc. Class A (a) | 2,367,600 | 404,552 | |

| GoDaddy, Inc. (a) | 474,400 | 20,641 | |

| MuleSoft, Inc. Class A | 300 | 6 | |

| Nutanix, Inc. Class B (f) | 462,283 | 10,351 | |

| Tencent Holdings Ltd. | 447,300 | 19,556 | |

| 1,313,511 | |||

| IT Services - 5.2% | |||

| Accenture PLC Class A | 789,200 | 106,597 | |

| Cognizant Technology Solutions Corp. Class A | 1,727,700 | 125,327 | |

| Global Payments, Inc. | 969,100 | 92,094 | |

| MasterCard, Inc. Class A | 1,076,500 | 152,002 | |

| PayPal Holdings, Inc. (a) | 2,864,000 | 183,382 | |

| Visa, Inc. Class A | 1,864,200 | 196,188 | |

| 855,590 | |||

| Semiconductors & Semiconductor Equipment - 2.4% | |||

| Broadcom Ltd. | 477,200 | 115,740 | |

| NVIDIA Corp. | 938,300 | 167,740 | |

| Qualcomm, Inc. | 1,946,000 | 100,881 | |

| 384,361 | |||

| Software - 5.2% | |||

| Adobe Systems, Inc. (a) | 1,047,500 | 156,266 | |

| Autodesk, Inc. (a) | 1,273,900 | 143,008 | |

| DocuSign, Inc. (a)(d)(e) | 16,185 | 393 | |

| Electronic Arts, Inc. (a) | 604,300 | 71,344 | |

| Oracle Corp. | 4,005,300 | 193,656 | |

| Salesforce.com, Inc. (a) | 1,349,875 | 126,105 | |

| SAP SE sponsored ADR (b) | 748,700 | 82,095 | |

| Tanium, Inc. Class B (d)(e) | 415,800 | 2,064 | |

| Workday, Inc. Class A (a) | 760,800 | 80,181 | |

| Xero Ltd. (a) | 4 | 0 | |

| 855,112 | |||

| Technology Hardware, Storage & Peripherals - 6.1% | |||

| Apple, Inc. | 6,461,713 | 995,875 | |

| TOTAL INFORMATION TECHNOLOGY | 4,439,403 | ||

| MATERIALS - 1.8% | |||

| Chemicals - 1.8% | |||

| CF Industries Holdings, Inc. | 1,815,700 | 63,840 | |

| FMC Corp. | 521,000 | 46,531 | |

| LyondellBasell Industries NV Class A | 1,856,419 | 183,878 | |

| 294,249 | |||

| REAL ESTATE - 1.2% | |||

| Equity Real Estate Investment Trusts (REITs) - 1.0% | |||

| American Tower Corp. | 1,239,061 | 169,355 | |

| Real Estate Management & Development - 0.2% | |||

| Rialto Real Estate Fund LP (c)(d)(e)(g) | 500,000 | 2,919 | |

| RREF CMBS AIV, LP (c)(d)(e)(g)(h) | 500,000 | 21,036 | |

| RREF Midtown Colony REIT, Inc. (c)(d)(e)(g)(i) | 500,000 | 0 | |

| 23,955 | |||

| TOTAL REAL ESTATE | 193,310 | ||

| TOTAL COMMON STOCKS | |||

| (Cost $10,739,169) | 15,984,577 | ||

| Convertible Preferred Stocks - 1.0% | |||

| CONSUMER DISCRETIONARY - 0.1% | |||

| Internet & Direct Marketing Retail - 0.1% | |||

| China Internet Plus Holdings Ltd. Series A-11 (a)(d)(e) | 3,163,704 | 17,682 | |

| INFORMATION TECHNOLOGY - 0.9% | |||

| Internet Software & Services - 0.3% | |||

| Uber Technologies, Inc. Series D, 8.00% (a)(d)(e) | 966,928 | 47,159 | |

| Software - 0.6% | |||

| Cloudflare, Inc. Series D 8.00% (a)(d)(e) | 571,642 | 3,721 | |

| DocuSign, Inc.: | |||

| Series B (a)(d)(e) | 7,510 | 182 | |

| Series B-1 (a)(d)(e) | 2,249 | 55 | |

| Series D (a)(d)(e) | 2,376,438 | 57,731 | |

| Series E (a)(d)(e) | 139,427 | 3,387 | |

| Malwarebytes Corp. Series B (a)(d)(e) | 3,373,494 | 37,965 | |

| 103,041 | |||

| TOTAL INFORMATION TECHNOLOGY | 150,200 | ||

| TOTAL CONVERTIBLE PREFERRED STOCKS | |||

| (Cost $76,533) | 167,882 | ||

| Principal Amount (000s) | Value (000s) | ||

| U.S. Treasury Obligations - 0.0% | |||

| U.S. Treasury Bills, yield at date of purchase 1.01% to 1.02% 12/14/17 to 12/21/17 (j) | |||

| (Cost $3,173) | 3,180 | 3,173 | |

| Shares | Value (000s) | ||

| Money Market Funds - 1.1% | |||

| Fidelity Cash Central Fund, 1.09%(k) | 113,231,209 | $113,254 | |

| Fidelity Securities Lending Cash Central Fund 1.10%(k)(l) | 64,310,421 | 64,323 | |

| TOTAL MONEY MARKET FUNDS | |||

| (Cost $177,562) | 177,577 | ||

| TOTAL INVESTMENT IN SECURITIES - 100.0% | |||

| (Cost $10,996,437) | 16,333,209 | ||

| NET OTHER ASSETS (LIABILITIES) - 0.0% | (2,937) | ||

| NET ASSETS - 100% | $16,330,272 |

| Futures Contracts | |||||

| Number of contracts | Expiration Date | Notional amount (000s) | Value (000s) | Unrealized Appreciation/(Depreciation) (000s) | |

| Purchased | |||||

| Equity Index Contracts | |||||

| CME E-mini S&P 500 Index Contracts (United States) | 664 | Dec. 2017 | $83,535 | $1,737 | $1,737 |

The notional amount of futures purchased as a percentage of Net Assets is 0.5%

Values shown as $0 may reflect amounts less than $500.

Legend

(a) Non-income producing

(b) Security or a portion of the security is on loan at period end.

(c) Investment is owned by a wholly-owned subsidiary (Subsidiary) that is treated as a corporation for U.S. tax purposes.

(d) Restricted securities - Investment in securities not registered under the Securities Act of 1933 (excluding 144A issues). At the end of the period, the value of restricted securities (excluding 144A issues) amounted to $212,837,000 or 1.3% of net assets.

(e) Level 3 instrument

(f) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $10,351,000 or 0.1% of net assets.

(g) Affiliated company

(h) Investment represents the Fund's ownership interest in a limited partnership, which is under common ownership and management with Rialto Real Estate Fund, LP.

(i) Investment represents the Fund's ownership interest in a real estate investment trust, which is under common ownership and management with Rialto Real Estate Fund, LP.

(j) Security or a portion of the security was pledged to cover margin requirements for futures contracts. At period end, the value of securities pledged amounted to $3,173,000.

(k) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC's website or upon request.

(l) Investment made with cash collateral received from securities on loan.

Additional information on each restricted holding is as follows:

| Security | Acquisition Date | Acquisition Cost (000s) |

| China Internet Plus Holdings Ltd. Series A-11 | 1/26/15 | $10,000 |

| Cloudflare, Inc. Series D 8.00% | 11/5/14 | $3,502 |

| DocuSign, Inc. | 10/21/13 | $90 |

| DocuSign, Inc. Series B | 3/3/14 | $99 |

| DocuSign, Inc. Series B-1 | 3/3/14 | $30 |

| DocuSign, Inc. Series D | 6/29/12 - 3/3/14 | $11,071 |

| DocuSign, Inc. Series E | 3/3/14 | $1,831 |

| Malwarebytes Corp. Series B | 12/21/15 | $35,000 |

| Rialto Real Estate Fund LP | 2/24/11 - 8/17/12 | $33,049 |

| RREF CMBS AIV, LP | 8/10/11 - 8/17/12 | $15,528 |

| RREF Midtown Colony REIT, Inc. | 12/31/12 | $1,423 |

| Tanium, Inc. Class B | 4/21/17 | $2,064 |

| Uber Technologies, Inc. Series D, 8.00% | 6/6/14 | $15,000 |

| WME Entertainment Parent, LLC Class A | 4/13/16 | $15,000 |

Affiliated Central Funds

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows:

| Fund | Income earned |

| (Amounts in thousands) | |

| Fidelity Cash Central Fund | $965 |

| Fidelity Securities Lending Cash Central Fund | 134 |

| Total | $1,099 |

Other Affiliated Issuers

An affiliated company is a company in which the Fund has ownership of at least 5% of the voting securities. Fiscal year to date transactions with companies which are or were affiliates are as follows:

| Affiliate (Amounts in thousands) | Value, beginning of period | Purchases | Sales Proceeds | Dividend Income | Realized Gain (loss) | Change in Unrealized appreciation (depreciation) | Value, end of period |

| Rialto Real Estate Fund LP | $3,249 | $-- | $-- | $1,077 | $-- | $(330) | $2,919 |

| RREF CMBS AIV, LP | 21,461 | -- | -- | 555 | -- | (425) | 21,036 |

| RREF Midtown Colony REIT, Inc. | -- | -- | -- | -- | -- | -- | -- |

| Total | $24,710 | $-- | $-- | $1,632 | $-- | $(755) | $23,955 |

Investment Valuation

The following is a summary of the inputs used, as of September 30, 2017, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used below, please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: | ||||

| Description | Total | Level 1 | Level 2 | Level 3 |

| (Amounts in thousands) | ||||

| Investments in Securities: | ||||

| Equities: | ||||

| Consumer Discretionary | $1,776,985 | $1,677,091 | $63,669 | $36,225 |

| Consumer Staples | 1,173,474 | 1,023,578 | 149,896 | -- |

| Energy | 1,061,499 | 1,061,499 | -- | -- |

| Financials | 2,694,225 | 2,694,225 | -- | -- |

| Health Care | 2,291,887 | 2,291,887 | -- | -- |

| Industrials | 2,077,227 | 2,077,227 | -- | -- |

| Information Technology | 4,589,603 | 4,417,390 | 19,556 | 152,657 |

| Materials | 294,249 | 294,249 | -- | -- |

| Real Estate | 193,310 | 169,355 | -- | 23,955 |

| U.S. Government and Government Agency Obligations | 3,173 | -- | 3,173 | -- |

| Money Market Funds | 177,577 | 177,577 | -- | -- |

| Total Investments in Securities: | $16,333,209 | $15,884,078 | $236,294 | $212,837 |

| Derivative Instruments: | ||||

| Assets | ||||

| Futures Contracts | $1,737 | $1,737 | $-- | $-- |

| Total Assets | $1,737 | $1,737 | $-- | $-- |

| Total Derivative Instruments: | $1,737 | $1,737 | $-- | $-- |

The following is a reconciliation of Investments in Securities and Derivative Instruments for which Level 3 inputs were used in determining value:

| (Amounts in thousands) | ||||

| Investments in Securities: | ||||

| Beginning Balance | $219,988 | |||

| Net Realized Gain (Loss) on Investment Securities | -- | |||

| Net Unrealized Gain (Loss) on Investment Securities | 6,878 | |||

| Cost of Purchases | 2,064 | |||

| Proceeds of Sales | (16,093) | |||

| Amortization/Accretion | -- | |||

| Transfers into Level 3 | -- | |||

| Transfers out of Level 3 | -- | |||

| Ending Balance | $212,837 | |||

| The change in unrealized gain (loss) for the period attributable to Level 3 securities held at September 30, 2017 | $41,127 |

The information used in the above reconciliation represents fiscal year to date activity for any Investments in Securities identified as using Level 3 inputs at either the beginning or the end of the current fiscal period. Transfers in or out of Level 3 represent the beginning value of any Security or Instrument where a change in the pricing level occurred from the beginning to the end of the period. The cost of purchases and the proceeds of sales may include securities received or delivered through corporate actions or exchanges. Realized and unrealized gains (losses) disclosed in the reconciliation are included in Net Gain (Loss) on the Fund’s Statement of Operations.

Value of Derivative Instruments

The following table is a summary of the Fund's value of derivative instruments by primary risk exposure as of September 30, 2017. For additional information on derivative instruments, please refer to the Derivative Instruments section in the accompanying Notes to Financial Statements.

| Primary Risk Exposure / Derivative Type | Value | |

| Asset | Liability | |

| (Amounts in thousands) | ||

| Equity Risk | ||

| Futures Contracts(a) | $1,737 | $0 |

| Total Equity Risk | 1,737 | 0 |

| Total Value of Derivatives | $1,737 | $0 |

(a) Reflects gross cumulative appreciation (depreciation) on futures contracts as presented in the Schedule of Investments. In the Statement of Assets and Liabilities, the period end daily variation margin is included in receivable or payable for daily variation margin on futures contracts, and the net cumulative appreciation (depreciation) is included in net unrealized appreciation (depreciation).

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| Amounts in thousands (except per-share amounts) | September 30, 2017 | |

| Assets | ||

| Investment in securities, at value (including securities loaned of $62,885) — See accompanying schedule: Unaffiliated issuers (cost $10,786,630) | $16,131,677 | |

| Fidelity Central Funds (cost $177,562) | 177,577 | |

| Other affiliated issuers (cost $32,245) | 23,955 | |

| Total Investment in Securities (cost $10,996,437) | $16,333,209 | |

| Restricted cash | 60 | |

| Receivable for investments sold | 105,217 | |

| Receivable for fund shares sold | 1,199 | |

| Dividends receivable | 6,307 | |

| Distributions receivable from Fidelity Central Funds | 204 | |

| Receivable for daily variation margin on futures contracts | 279 | |

| Prepaid expenses | 41 | |

| Other receivables | 2,084 | |

| Total assets | 16,448,600 | |

| Liabilities | ||

| Payable for investments purchased | $34,242 | |

| Payable for fund shares redeemed | 8,479 | |

| Accrued management fee | 7,313 | |

| Other affiliated payables | 1,845 | |

| Other payables and accrued expenses | 2,130 | |

| Collateral on securities loaned | 64,319 | |

| Total liabilities | 118,328 | |

| Net Assets | $16,330,272 | |

| Net Assets consist of: | ||

| Paid in capital | $10,466,463 | |

| Undistributed net investment income | 82,531 | |

| Accumulated undistributed net realized gain (loss) on investments and foreign currency transactions | 442,760 | |

| Net unrealized appreciation (depreciation) on investments and assets and liabilities in foreign currencies | 5,338,518 | |

| Net Assets | $16,330,272 | |

| Magellan: | ||

| Net Asset Value, offering price and redemption price per share ($14,375,188 ÷ 140,753 shares) | $102.13 | |

| Class K: | ||

| Net Asset Value, offering price and redemption price per share ($1,955,084 ÷ 19,163 shares) | $102.02 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Amounts in thousands | Six months ended September 30, 2017 | |

| Investment Income | ||

| Dividends (including $1,632 earned from other affiliated issuers) | $98,603 | |

| Special dividends | 37,125 | |

| Interest | 20 | |

| Income from Fidelity Central Funds | 1,099 | |

| Total income | 136,847 | |

| Expenses | ||

| Management fee | ||

| Basic fee | $42,891 | |

| Performance adjustment | (1,409) | |

| Transfer agent fees | 9,859 | |

| Accounting and security lending fees | 763 | |

| Custodian fees and expenses | 97 | |

| Independent trustees' fees and expenses | 31 | |

| Appreciation in deferred trustee compensation account | 5 | |

| Registration fees | 56 | |

| Audit | 97 | |

| Legal | 9 | |

| Miscellaneous | 63 | |

| Total expenses before reductions | 52,462 | |

| Expense reductions | (217) | 52,245 |

| Net investment income (loss) | 84,602 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 461,051 | |

| Fidelity Central Funds | (1) | |

| Foreign currency transactions | 39 | |

| Futures contracts | 2,780 | |

| Total net realized gain (loss) | 463,869 | |

| Change in net unrealized appreciation (depreciation) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 1,129,292 | |

| Fidelity Central Funds | 6 | |

| Other affiliated issuers | (755) | |

| Assets and liabilities in foreign currencies | 9 | |

| Futures contracts | 2,363 | |

| Total change in net unrealized appreciation (depreciation) | 1,130,915 | |

| Net gain (loss) | 1,594,784 | |

| Net increase (decrease) in net assets resulting from operations | $1,679,386 |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Amounts in thousands | Six months ended September 30, 2017 | Year ended March 31, 2017 |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $84,602 | $104,875 |

| Net realized gain (loss) | 463,869 | 1,175,058 |

| Change in net unrealized appreciation (depreciation) | 1,130,915 | 759,441 |

| Net increase (decrease) in net assets resulting from operations | 1,679,386 | 2,039,374 |

| Distributions to shareholders from net investment income | (26,573) | (90,353) |

| Distributions to shareholders from net realized gain | (841,889) | (346,796) |

| Total distributions | (868,462) | (437,149) |

| Share transactions - net increase (decrease) | 159,186 | (1,444,067) |

| Total increase (decrease) in net assets | 970,110 | 158,158 |

| Net Assets | ||

| Beginning of period | 15,360,162 | 15,202,004 |

| End of period | $16,330,272 | $15,360,162 |

| Other Information | ||

| Undistributed net investment income end of period | $82,531 | $24,502 |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Magellan Fund

| Six months ended September 30, | Years ended March 31, | |||||

| 2017 | 2017 | 2016 | 2015 | 2014 | 2013 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $97.23 | $87.51 | $95.15 | $94.25 | $79.96 | $73.30 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .52B | .62 | .56 | .77 | .81 | .93 |

| Net realized and unrealized gain (loss) | 9.93 | 11.77 | (1.22)C | 12.27 | 20.00 | 6.75 |

| Total from investment operations | 10.45 | 12.39 | (.66) | 13.04 | 20.81 | 7.68 |

| Distributions from net investment income | (.17) | (.55) | (.54) | (.71) | (.67) | (1.00) |

| Distributions from net realized gain | (5.38) | (2.12) | (6.44) | (11.43) | (5.85) | (.02) |

| Total distributions | (5.55) | (2.67) | (6.98) | (12.14) | (6.52) | (1.02) |

| Net asset value, end of period | $102.13 | $97.23 | $87.51 | $95.15 | $94.25 | $79.96 |

| Total ReturnD,E | 11.21% | 14.46% | (.99)%C | 14.98% | 26.50% | 10.63% |

| Ratios to Average Net AssetsF,G | ||||||

| Expenses before reductions | .68%H | .68% | .84% | .68% | .50% | .47% |

| Expenses net of fee waivers, if any | .68%H | .67% | .84% | .68% | .50% | .47% |

| Expenses net of all reductions | .67%H | .67% | .83% | .68% | .50% | .46% |

| Net investment income (loss) | .83%B,H | .68% | .62% | .83% | .92% | 1.27% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $14,375 | $13,467 | $12,950 | $14,224 | $13,521 | $12,341 |

| Portfolio turnover rateI | 43%H | 51%J | 78% | 71% | 77% | 88% |

A Calculated based on average shares outstanding during the period.

B Net Investment income per share reflects a large, non-recurring dividend which amounted to $.23 per share. This dividend is not annualized in the ratio of net investment income (loss) to average net assets. Excluding this dividend the ratio would have been .59%.

C Net realized and unrealized gain (loss) per share reflects proceeds received from litigation which amounted to $.05 per share. Excluding these litigation proceeds, the total return would have been (1.05)%.

D Total returns for periods of less than one year are not annualized.

E Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

F Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

G Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from brokerage service arrangements or reductions from other expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

H Annualized

I Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

J Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Magellan Fund Class K

| Six months ended September 30, | Years ended March 31, | |||||

| 2017 | 2017 | 2016 | 2015 | 2014 | 2013 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $97.12 | $87.41 | $95.04 | $94.16 | $79.89 | $73.24 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .56B | .71 | .65 | .86 | .90 | 1.02 |

| Net realized and unrealized gain (loss) | 9.91 | 11.75 | (1.21)C | 12.25 | 19.99 | 6.75 |

| Total from investment operations | 10.47 | 12.46 | (.56) | 13.11 | 20.89 | 7.77 |

| Distributions from net investment income | (.19) | (.63) | (.63) | (.80) | (.77) | (1.10) |

| Distributions from net realized gain | (5.38) | (2.12) | (6.44) | (11.43) | (5.85) | (.02) |

| Total distributions | (5.57) | (2.75) | (7.07) | (12.23) | (6.62) | (1.12) |

| Net asset value, end of period | $102.02 | $97.12 | $87.41 | $95.04 | $94.16 | $79.89 |

| Total ReturnD,E | 11.25% | 14.57% | (.89)%C | 15.08% | 26.63% | 10.77% |

| Ratios to Average Net AssetsF,G | ||||||

| Expenses before reductions | .59%H | .58% | .74% | .58% | .39% | .35% |

| Expenses net of fee waivers, if any | .59%H | .58% | .74% | .58% | .39% | .35% |

| Expenses net of all reductions | .58%H | .58% | .74% | .58% | .39% | .34% |

| Net investment income (loss) | .92%B,H | .78% | .71% | .93% | 1.02% | 1.40% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $1,955 | $1,893 | $2,252 | $2,528 | $2,585 | $2,424 |

| Portfolio turnover rateI | 43%H | 51%J | 78% | 71% | 77% | 88% |

A Calculated based on average shares outstanding during the period.

B Net Investment income per share reflects a large, non-recurring dividend which amounted to $.23 per share. This dividend is not annualized in the ratio of net investment income (loss) to average net assets. Excluding this dividend the ratio would have been .68%.

C Net realized and unrealized gain (loss) per share reflects proceeds received from litigation which amounted to $.05 per share. Excluding these litigation proceeds, the total return would have been (.95)%.

D Total returns for periods of less than one year are not annualized.

E Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

F Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

G Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from brokerage service arrangements or reductions from other expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

H Annualized

I Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

J Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements

For the period ended September 30, 2017

(Amounts in thousands except percentages)

1. Organization.

Fidelity Magellan Fund (the Fund) is a fund of Fidelity Magellan Fund (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. The Fund offers Magellan and Class K shares, each of which has equal rights as to assets and voting privileges. Each class has exclusive voting rights with respect to matters that affect that class.

2. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies generally available only to other investment companies and accounts managed by the investment adviser and its affiliates. The Fund's Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of the investment adviser. Annualized expenses of the Money Market Central Funds as of their most recent shareholder report date are less than .005%.

A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) website at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC website or upon request.

3. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investments Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Board of Trustees (the Board) has delegated the day to day responsibility for the valuation of the Fund's investments to the Fair Value Committee (the Committee) established by the Fund's investment adviser. In accordance with valuation policies and procedures approved by the Board, the Fund attempts to obtain prices from one or more third party pricing vendors or brokers to value its investments. When current market prices, quotations or currency exchange rates are not readily available or reliable, investments will be fair valued in good faith by the Committee, in accordance with procedures adopted by the Board. Factors used in determining fair value vary by investment type and may include market or investment specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The Committee oversees the Fund's valuation policies and procedures and reports to the Board on the Committee's activities and fair value determinations. The Board monitors the appropriateness of the procedures used in valuing the Fund's investments and ratifies the fair value determinations of the Committee.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

Valuation techniques used to value the Fund's investments by major category are as follows:

Equity securities, including restricted securities, for which market quotations are readily available, are valued at the last reported sale price or official closing price as reported by a third party pricing vendor on the primary market or exchange on which they are traded and are categorized as Level 1 in the hierarchy. In the event there were no sales during the day or closing prices are not available, securities are valued at the last quoted bid price or may be valued using the last available price and are generally categorized as Level 2 in the hierarchy. For foreign equity securities, when market or security specific events arise, comparisons to the valuation of American Depositary Receipts (ADRs), futures contracts, Exchange-Traded Funds (ETFs) and certain indexes as well as quoted prices for similar securities may be used and would be categorized as Level 2 in the hierarchy. Utilizing these techniques may result in transfers between Level 1 and Level 2. For equity securities, including restricted securities, where observable inputs are limited, assumptions about market activity and risk are used and these securities may be categorized as Level 3 in the hierarchy. Equity securities, including restricted securities, for which observable inputs are not available are valued using alternate valuation approaches, including the market approach and the income approach and are categorized as Level 3 in the hierarchy. The market approach generally consists of using comparable market transactions while the income approach generally consists of using the net present value of estimated future cash flows, adjusted as appropriate for liquidity, credit, market and/or other risk factors.

Debt securities, including restricted securities, are valued based on evaluated prices received from third party pricing vendors or from brokers who make markets in such securities. U.S. government and government agency obligations are valued by pricing vendors who utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type or by broker-supplied prices. When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing methodologies which consider similar factors that would be used by third party pricing vendors. Debt securities are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

Futures contracts are valued at the settlement price established each day by the board of trade or exchange on which they are traded and are categorized as Level 1 in the hierarchy. Investments in open-end mutual funds, including the Fidelity Central Funds, are valued at their closing net asset value (NAV) each business day and are categorized as Level 1 in the hierarchy.

The following provides information on Level 3 securities held by the Fund that were valued at period end based on unobservable inputs. These amounts exclude valuations provided by a broker.

| Asset Type | Fair Value | Valuation Technique(s) | Unobservable Input | Amount or Range/Weighted Average | Impact to Valuation from an Increase in Input(a) |

| Equities | $212,837 | Recovery value | Recovery value | 0.0% | Increase |

| Market approach | Transaction price | $2.50 - $48.77 / $28.74 | Increase | ||

| Market comparable | Enterprise value/Sales multiple (EV/S) | 4.5 - 7.9 / 5.8 | Increase | ||

| Discount rate | 7.5% | Decrease | |||

| Discount for lack of marketability | 10.0% - 20.0% / 13.3% | Decrease | |||

| Premium rate | 6.1% | Increase | |||

| Book value | Book value multiple | 1.0 | Increase |

(a) Represents the expected directional change in the fair value of the Level 3 investments that would result from an increase in the corresponding input. A decrease to the unobservable input would have the opposite effect. Significant changes in these inputs could result in significantly higher or lower fair value measurements.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The aggregate value of investments by input level as of September 30, 2017, as well as a roll forward of Level 3 investments, is included at the end of the Fund's Schedule of Investments.

Foreign Currency. The Fund may use foreign currency contracts to facilitate transactions in foreign-denominated securities. Gains and losses from these transactions may arise from changes in the value of the foreign currency or if the counterparties do not perform under the contracts' terms.

Foreign-denominated assets, including investment securities, and liabilities are translated into U.S. dollars at the exchange rates at period end. Purchases and sales of investment securities, income and dividends received and expenses denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date.

The effects of exchange rate fluctuations on investments are included with the net realized and unrealized gain (loss) on investment securities. Other foreign currency transactions resulting in realized and unrealized gain (loss) are disclosed separately.

Investment Transactions and Income. For financial reporting purposes, the Fund's investment holdings and NAV include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day. Gains and losses on securities sold are determined on the basis of identified cost and may include proceeds received from litigation. Dividend income is recorded on the ex-dividend date, except for certain dividends from foreign securities where the ex-dividend date may have passed, which are recorded as soon as the Fund is informed of the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Income and capital gain distributions from Fidelity Central Funds, if any, are recorded on the ex-dividend date. Certain distributions received by the Fund represent a return of capital or capital gain. The Fund determines the components of these distributions subsequent to the ex-dividend date, based upon receipt of tax filings or other correspondence relating to the underlying investment. These distributions are recorded as a reduction of cost of investments and/or as a realized gain. Large, non-recurring dividends recognized by the Fund are presented separately on the Statement of Operations as "Special Dividends" and the impact of these dividends is presented in the Financial Highlights. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable. Investment income is recorded net of foreign taxes withheld where recovery of such taxes is uncertain.

Class Allocations and Expenses. Investment income, realized and unrealized capital gains and losses, common expenses of the Fund, and certain fund-level expense reductions, if any, are allocated daily on a pro-rata basis to each class based on the relative net assets of each class to the total net assets of the Fund. Each class differs with respect to transfer agent fees incurred. Certain expense reductions may also differ by class. For the reporting period, the allocated portion of income and expenses to each class as a percent of its average net assets may vary due to the timing of recording these transactions in relation to fluctuating net assets of the classes. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Deferred Trustee Compensation. Under a Deferred Compensation Plan (the Plan), independent Trustees may elect to defer receipt of a portion of their annual compensation. Deferred amounts are invested in a cross-section of Fidelity funds, are marked-to-market and remain in the Fund until distributed in accordance with the Plan. The investment of deferred amounts and the offsetting payable to the Trustees are included in the accompanying Statement of Assets and Liabilities.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction. Foreign taxes are provided for based on the Fund's understanding of the tax rules and rates that exist in the foreign markets in which it invests.

Distributions are declared and recorded on the ex-dividend date. Income dividends and capital gain distributions are declared separately for each class. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to futures contracts, foreign currency transactions, market discount, redemptions in kind, partnerships, deferred trustees compensation, and losses deferred due to wash sales.

As of period end, the cost and unrealized appreciation (depreciation) in securities, and derivatives if applicable, for federal income tax purposes were as follows:

| Gross unrealized appreciation | $5,493,332 |

| Gross unrealized depreciation | (165,736) |

| Net unrealized appreciation (depreciation) | $5,327,596 |

| Tax cost | $11,007,350 |

Restricted Securities. The Fund may invest in securities that are subject to legal or contractual restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are registered. Disposal of these securities may involve time-consuming negotiations and expense, and prompt sale at an acceptable price may be difficult. Information regarding restricted securities is included at the end of the Fund's Schedule of Investments.

Consolidated Subsidiary. The Fund invests in certain investments through a wholly-owned subsidiary ("Subsidiary"), which may be subject to federal and state taxes upon disposition.

As of period end, the Fund held an investment of $42,558 in these Subsidiaries, representing .26% of the Fund's net assets. The financial statements have been consolidated and include accounts of the Fund and each Subsidiary. Accordingly, all inter-company transactions and balances have been eliminated.

Any cash held by the Subsidiaries is restricted as to its use and is presented as Restricted cash in the Statement of Assets and Liabilities.

4. Derivative Instruments.

Risk Exposures and the Use of Derivative Instruments. The Fund's investment objective allows the Fund to enter into various types of derivative contracts, including futures contracts. Derivatives are investments whose value is primarily derived from underlying assets, indices or reference rates and may be transacted on an exchange or over-the-counter (OTC). Derivatives may involve a future commitment to buy or sell a specified asset based on specified terms, to exchange future cash flows at periodic intervals based on a notional principal amount, or for one party to make one or more payments upon the occurrence of specified events in exchange for periodic payments from the other party.

The Fund used derivatives to increase returns and to manage exposure to certain risks as defined below. The success of any strategy involving derivatives depends on analysis of numerous economic factors, and if the strategies for investment do not work as intended, the Fund may not achieve its objectives.

The Fund's use of derivatives increased or decreased its exposure to the following risk:

| Equity Risk | Equity risk relates to the fluctuations in the value of financial instruments as a result of changes in market prices (other than those arising from interest rate risk or foreign exchange risk), whether caused by factors specific to an individual investment, its issuer, or all factors affecting all instruments traded in a market or market segment. |

The Fund is also exposed to additional risks from investing in derivatives, such as liquidity risk and counterparty credit risk. Liquidity risk is the risk that the Fund will be unable to close out the derivative in the open market in a timely manner. Counterparty credit risk is the risk that the counterparty will not be able to fulfill its obligation to the Fund. Counterparty credit risk related to exchange-traded futures contracts may be mitigated by the protection provided by the exchange on which they trade.

Investing in derivatives may involve greater risks than investing in the underlying assets directly and, to varying degrees, may involve risk of loss in excess of any initial investment and collateral received and amounts recognized in the Statement of Assets and Liabilities. In addition, there may be the risk that the change in value of the derivative contract does not correspond to the change in value of the underlying instrument.

Futures Contracts. A futures contract is an agreement between two parties to buy or sell a specified underlying instrument for a fixed price at a specified future date. The Fund used futures contracts to manage its exposure to the stock market.

Upon entering into a futures contract, a fund is required to deposit either cash or securities (initial margin) with a clearing broker in an amount equal to a certain percentage of the face value of the contract. Futures contracts are marked-to-market daily and subsequent daily payments (variation margin) are made or received by a fund depending on the daily fluctuations in the value of the futures contracts and are recorded as unrealized appreciation or (depreciation). This receivable and/or payable, if any, is included in daily variation margin on futures contracts in the Statement of Assets and Liabilities. Realized gain or (loss) is recorded upon the expiration or closing of a futures contract.

Any open futures contracts at period end are presented in the Schedule of Investments under the caption "Futures Contracts". The underlying face amount at value reflects each contract's exposure to the underlying instrument or index at period end and is representative of volume of activity during the period. Securities deposited to meet initial margin requirements are identified in the Schedule of Investments.

During the period the Fund recognized net realized gain (loss) of $2,780 and a change in net unrealized appreciation (depreciation) of $2,363 related to its investment in futures contracts. These amounts are included in the Statement of Operations.

5. Purchases and Sales of Investments.

Purchases and sales of securities, other than short-term securities, aggregated $3,351,225 and $3,847,702, respectively.

Prior Fiscal Year Redemptions In-Kind. During the prior period, 2,125 shares of the Fund held by unaffiliated entities were redeemed in-kind for investments and cash with a value of $193,652. The Fund had a net realized gain of $71,761 on investments delivered through the in-kind redemptions. The amount of in-kind redemptions is included in share transactions activity shown in the accompanying Statement of Changes in Net Assets as well as the Notes to Financial Statements. The Fund recognized no gain or loss for federal income tax purposes.

6. Fees and Other Transactions with Affiliates.

Management Fee. Fidelity Management & Research Company (the investment adviser) and its affiliates provide the Fund with investment management related services for which the Fund pays a monthly management fee. The management fee is the sum of an individual fund fee rate that is based on an annual rate of .30% of the Fund's average net assets and an annualized group fee rate that averaged .24% during the period. The group fee rate is based upon the average net assets of all the mutual funds advised by the investment adviser, including any mutual funds previously advised by the investment adviser that are currently advised by Fidelity SelectCo, LLC, an affiliate of the investment adviser. The group fee rate decreases as assets under management increase and increases as assets under management decrease. In addition, the management fee is subject to a performance adjustment (up to a maximum of +/- .20% of the Fund's average net assets over a 36 month performance period). The upward or downward adjustment to the management fee is based on the relative investment performance of Magellan as compared to its benchmark index, the S&P 500 Index, over the same 36 month performance period. For the reporting period, the total annualized management fee rate, including the performance adjustment, was .53% of the Fund's average net assets. The performance adjustment included in the management fee rate may be higher or lower than the maximum performance adjustment rate due to the difference between the average net assets for the reporting and performance periods.

Transfer Agent Fees. Fidelity Investments Institutional Operations Company, Inc., (FIIOC), an affiliate of the investment adviser, is the transfer, dividend disbursing and shareholder servicing agent for each class of the Fund. FIIOC receives account fees and asset-based fees that vary according to the account size and type of account of the shareholders of Magellan. FIIOC receives an asset-based fee of Class K's average net assets. FIIOC pays for typesetting, printing and mailing of shareholder reports, except proxy statements.

For the period, transfer agent fees for each class were as follows:

| Amount | % of Class-Level Average Net Assets(a) |

|

| Magellan | $9,410 | .14 |

| Class K | 449 | .05 |

| $9,859 |

(a) Annualized

Accounting and Security Lending Fees. Fidelity Service Company, Inc. (FSC), an affiliate of the investment adviser, maintains the Fund's accounting records. The accounting fee is based on the level of average net assets for each month. Under a separate contract, FSC administers the security lending program. The security lending fee is based on the number and duration of lending transactions.

Brokerage Commissions. The Fund placed a portion of its portfolio transactions with brokerage firms which are affiliates of the investment adviser. Brokerage commissions are included in net realized gain (loss) and change in net unrealized appreciation (depreciation) in the Statement of Operations. The commissions paid to these affiliated firms were $107 for the period.

Interfund Trades. The Fund may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act. Interfund trades are included within the respective purchases and sales amounts shown in the Purchases and Sales of Investments note.

7. Committed Line of Credit.

The Fund participates with other funds managed by the investment adviser or an affiliate in a $4.25 billion credit facility (the "line of credit") to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The Fund has agreed to pay commitment fees on its pro-rata portion of the line of credit, which amounted to $13 and is reflected in Miscellaneous expenses on the Statement of Operations. During the period, the Fund did not borrow on this line of credit.

8. Security Lending.

The Fund lends portfolio securities through a lending agent from time to time in order to earn additional income. For equity securities, a lending agent is used and may loan securities to certain qualified borrowers, including Fidelity Capital Markets (FCM), a broker-dealer affiliated with the Fund. On the settlement date of the loan, the Fund receives collateral (in the form of U.S. Treasury obligations, letters of credit and/or cash) against the loaned securities and maintains collateral in an amount not less than 100% of the market value of the loaned securities during the period of the loan. The market value of the loaned securities is determined at the close of business of the Fund and any additional required collateral is delivered to the Fund on the next business day. The Fund or borrower may terminate the loan at any time, and if the borrower defaults on its obligation to return the securities loaned because of insolvency or other reasons, the Fund may apply collateral received from the borrower against the obligation. The Fund may experience delays and costs in recovering the securities loaned. Any cash collateral received is invested in the Fidelity Securities Lending Cash Central Fund. The value of loaned securities and cash collateral at period end are disclosed on the Fund's Statement of Assets and Liabilities. At period end, there were no security loans outstanding with FCM. Security lending income represents the income earned on investing cash collateral, less rebates paid to borrowers and any lending agent fees associated with the loan, plus any premium payments received for lending certain types of securities. Security lending income is presented in the Statement of Operations as a component of income from Fidelity Central Funds. Total security lending income during the period amounted to $134, including $4 from securities loaned to FCM.

9. Expense Reductions.

Commissions paid to certain brokers with whom the investment adviser, or its affiliates, places trades on behalf of the Fund include an amount in addition to trade execution, which may be rebated back to the Fund to offset certain expenses. This amount totaled $150 for the period.

In addition, during the period the investment adviser reimbursed and/or waived a portion of fund-level operating expenses in the amount of $67.

10. Distributions to Shareholders.

Distributions to shareholders of each class were as follows:

| Six months ended September 30, 2017 | Year ended March 31, 2017 | |

| From net investment income | ||

| Magellan | $22,940 | $77,138 |

| Class K | 3,633 | 13,215 |

| Total | $26,573 | $90,353 |

| From net realized gain | ||

| Magellan | $739,014 | $301,130 |

| Class K | 102,875 | 45,666 |

| Total | $841,889 | $346,796 |

11. Share Transactions.

Share transactions for each class were as follows and may contain automatic conversions between classes or exchanges between affiliated funds:

| Shares | Shares | Dollars | Dollars | |

| Six months ended September 30, 2017 | Year ended March 31, 2017 | Six months ended September 30, 2017 | Year ended March 31, 2017 | |

| Magellan | ||||

| Shares sold | 1,036 | 2,318 | $101,244 | $212,737 |

| Reinvestment of distributions | 7,676 | 4,052 | 724,899 | 360,034 |

| Shares redeemed | (6,461) | (15,845) | (631,240) | (1,446,824) |

| Net increase (decrease) | 2,251 | (9,475) | $194,903 | $(874,053) |

| Class K | ||||

| Shares sold | 630 | 1,626 | $61,484 | $148,358 |

| Reinvestment of distributions | 1,130 | 664 | 106,508 | 58,881 |

| Shares redeemed | (2,090) | (8,559)(a) | (203,709) | (777,254)(a) |

| Net increase (decrease) | (330) | (6,269) | $(35,717) | $(570,015) |

(a) Amount includes in-kind redemptions (see the Prior Fiscal Year Redemptions In-Kind note for additional details).

12. Other.

The Fund's organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

Report of Independent Registered Public Accounting Firm

To the Trustees of Fidelity Magellan Fund and Shareholders of Fidelity Magellan Fund:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Fidelity Magellan Fund as of September 30, 2017 the results of its operations for the periods indicated, the changes in its net assets for each of the periods indicated and the financial highlights for each of the periods indicated, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fidelity Magellan Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of September 30, 2017 by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Boston, Massachusetts

November 16, 2017

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2017 to September 30, 2017).

Actual Expenses

The first line of the accompanying table for each class of the Fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class of the Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table for each class of the Fund provides information about hypothetical account values and hypothetical expenses based on a Class' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class' actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Annualized Expense Ratio-A | Beginning Account Value April 1, 2017 | Ending Account Value September 30, 2017 | Expenses Paid During Period-B April 1, 2017 to September 30, 2017 |

|

| Magellan | .68% | |||

| Actual | $1,000.00 | $1,112.10 | $3.60 | |

| Hypothetical-C | $1,000.00 | $1,021.66 | $3.45 | |

| Class K | .59% | |||

| Actual | $1,000.00 | $1,112.50 | $3.12 | |

| Hypothetical-C | $1,000.00 | $1,022.11 | $2.99 |

A Annualized expense ratio reflects expenses net of applicable fee waivers.

B Expenses are equal to each Class' annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

C 5% return per year before expenses

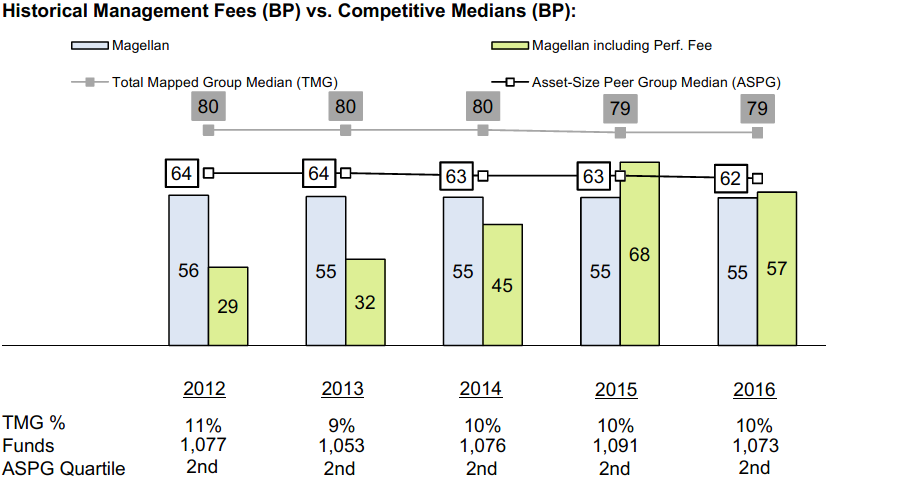

Board Approval of Investment Advisory Contracts and Management Fees

Fidelity Magellan Fund

Each year, the Board of Trustees, including the Independent Trustees (together, the Board), votes on the renewal of the management contract with Fidelity Management & Research Company (FMR) and the sub-advisory agreements (together, the Advisory Contracts) for the fund. FMR and the sub-advisers are referred to herein as the Investment Advisers. The Board, assisted by the advice of fund counsel and Independent Trustees' counsel, requests and considers a broad range of information relevant to the renewal of the Advisory Contracts throughout the year.

The Board meets regularly and, at each of its meetings, covers an extensive agenda of topics and materials and considers factors that are relevant to its annual consideration of the renewal of the fund's Advisory Contracts, including the services and support provided to the fund and its shareholders. The Board has established various standing committees (Committees), each composed of and chaired by Independent Trustees with varying backgrounds, to which the Board has assigned specific subject matter responsibilities in order to enhance effective decision-making by the Board. The Board, acting directly and through its Committees, requests and receives information concerning the annual consideration of the renewal of the fund's Advisory Contracts. The Board also meets as needed to review matters specifically related to the Board's annual consideration of the renewal of the Advisory Contracts. Members of the Board may also meet with trustees of other Fidelity funds through ad hoc joint committees to discuss certain matters relevant to all of the Fidelity funds.

At its July 2017 meeting, the Board unanimously determined to renew the fund's Advisory Contracts. In reaching its determination, the Board considered all factors it believed relevant, including (i) the nature, extent, and quality of the services to be provided to the fund and its shareholders (including the investment performance of the fund); (ii) the competitiveness of the fund's management fee and total expense ratio relative to peer funds; (iii) the total costs of the services to be provided by and the profits to be realized by Fidelity from its relationships with the fund; and (iv) the extent to which, if any, economies of scale exist and would be realized as the fund grows, and whether any economies of scale are appropriately shared with fund shareholders.

In considering whether to renew the Advisory Contracts for the fund, the Board reached a determination, with the assistance of fund counsel and Independent Trustees' counsel and through the exercise of its business judgment, that the renewal of the Advisory Contracts was in the best interests of the fund and its shareholders and that the compensation payable under the Advisory Contracts was fair and reasonable. The Board's decision to renew the Advisory Contracts was not based on any single factor, but rather was based on a comprehensive consideration of all the information provided to the Board at its meetings throughout the year. The Board, in reaching its determination to renew the Advisory Contracts, was aware that shareholders of the fund have a broad range of investment choices available to them, including a wide choice among funds offered by Fidelity's competitors, and that the fund's shareholders, who have the opportunity to review and weigh the disclosure provided by the fund in its prospectus and other public disclosures, have chosen to invest in this fund, which is part of the Fidelity family of funds.

Amendment to Group Fee Rate. The Board also approved an amendment to the management contract for the fund to add an additional breakpoint to the group fee schedule, effective October 1, 2017. The Board noted that the additional breakpoint would result in lower management fee rates as Fidelity's assets under management increase.