UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

| FORM | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the fiscal year ended | ||||||||

| Commission File No. | |||||

| (Exact name of registrant as specified in its charter) | |||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

| Registrant's telephone number, including area code | | |||||||

Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| ☒ | No | ☐ | |||||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

| Yes | ☐ | ☒ | |||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| ☒ | No | ☐ | |||||||||

Indicate by checkmark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| ☒ | No | ☐ | |||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | |||||||||||||

| Smaller reporting company | Emerging growth company | ||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| ☐ | ||

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to

§ 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Yes | No | ☒ | |||||||||

The aggregate market value on July 1, 2022, (the last business day of the Company’s most recently completed second quarter) of the voting and non-voting common stock held by non-affiliates of the registrant, computed by reference to the closing price of the stock, was approximately

| $ | . | ||||

At January 27, 2023, there were

shares of Common Stock outstanding.

Documents Incorporated Herein By Reference

Portions of our definitive proxy statement for our 2022 Annual Meeting of Shareholders are incorporated by reference into Part III of this Report.

Kaman Corporation

Index to Form 10-K

| Part I | ||||||||

| Item 1 | ||||||||

| Item 1A | ||||||||

| Item 1B | ||||||||

| Item 2 | ||||||||

| Item 3 | ||||||||

| Item 4 | ||||||||

| Part II | ||||||||

| Item 5 | ||||||||

| Item 6 | ||||||||

| Item 7 | ||||||||

| Item 7A | ||||||||

| Item 8 | ||||||||

| Item 9 | ||||||||

| Item 9A | ||||||||

| Item 9B | ||||||||

| Item 9C | ||||||||

| Part III | ||||||||

| Item 10 | ||||||||

| Item 11 | ||||||||

| Item 12 | ||||||||

| Item 13 | ||||||||

| Item 14 | ||||||||

| Part IV | ||||||||

| Item 15 | ||||||||

| Item 16 | ||||||||

2

PART I

ITEM 1.BUSINESS

GENERAL

Kaman Corporation, headquartered in Bloomfield, Connecticut, was incorporated in 1945. As used in this annual report, "the Company", "we", "us", "our" refer to the registrant and its consolidated subsidiaries. We are a diversified company that conducts business in the aerospace and defense, medical and industrial markets. We report information in three business segments: Engineered Products, Precision Products and Structures. The Chief Operating Decision Maker ("CODM") reviews operating results for the purposes of allocating resources and assessing performance based on these three segments.

The Company's principal customers include the U.S. military, foreign allied militaries, Sikorsky Aircraft Corporation, The Boeing Company, Airbus, Lockheed Martin, Rolls-Royce, Raytheon and Bell Helicopter. The SH-2G aircraft is currently in service with the Egyptian Air Force and the New Zealand, Peruvian and Polish navies. Operations are conducted throughout the United States, as well as in manufacturing facilities located in Germany and the Czech Republic. Additionally, the Company maintains an investment in a joint venture in India. In the year ended December 31, 2022, one individual customer, The Boeing Company, accounted for more than 10% of consolidated net sales, which were primarily made by the Engineered Products and Structures segments.

Engineered Products Segment

The Engineered Products segment serves the aerospace and defense, industrial and medical markets providing sophisticated, proprietary aircraft bearings and components; super precision, miniature ball bearings; and proprietary spring energized seals, springs and contacts; and wheels, brakes and related hydraulic components for helicopters and fixed-wing and UAV aircraft.

Precision Products Segment

The Precision Products segment serves the aerospace and defense markets providing precision safe and arming solutions for missile and bomb systems for the U.S. and allied militaries; subcontract helicopter work; restoration, modification and support of our SH-2G Super Seasprite maritime helicopters; support of our heavy lift K-MAX® manned helicopter; and development of the KARGO UAV unmanned aerial system, a purpose built autonomous medium lift logistics vehicle.

Structures Segment

The Structures segment serves the aerospace and defense and medical end markets providing sophisticated complex metallic and composite aerostructures for commercial, military and general aviation fixed and rotary wing aircraft, and medical imaging solutions.

A discussion of 2022 developments is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Form 10-K.

WORKING CAPITAL

A discussion of our working capital is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources, in this Form 10-K.

Our working capital requirements are dependent on the nature and life cycles of the programs for which work is performed. New programs may initially require higher working capital to complete nonrecurring start-up activities and fund the purchase of inventory and equipment necessary to perform the work. Nonrecurring start-up costs on large and complex programs often take longer to recover, negatively impacting working capital in the short-term and producing a corresponding benefit in future periods. As these programs mature and efficiencies are gained in the production process, working capital requirements generally decrease.

Our credit agreement is a revolving credit facility which is available for additional working capital requirements and investment opportunities. See Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Note 14, Debt, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K.

3

PRINCIPAL PRODUCTS AND SERVICES

The following table sets forth the percentage contribution of each major product line to consolidated net sales for each of the three most recently completed years:

| For the year ended December 31, | ||||||||||||||||||||

| 2022 | 2021 | 2020 | ||||||||||||||||||

| Sales | ||||||||||||||||||||

| Defense | 21.2 | % | 23.8 | % | 23.0 | % | ||||||||||||||

| Safe and Arm Devices | 18.3 | % | 27.0 | % | 31.7 | % | ||||||||||||||

| Commercial, Business, & General Aviation | 35.3 | % | 26.1 | % | 28.1 | % | ||||||||||||||

| Medical | 13.7 | % | 12.2 | % | 8.9 | % | ||||||||||||||

| Industrial & Other | 11.5 | % | 10.9 | % | 8.3 | % | ||||||||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||||

AVAILABILITY OF RAW MATERIALS

While we believe we have sufficient sources for the materials, components, services and supplies used in our manufacturing activities, we are highly dependent on the availability of essential materials, parts and subassemblies from our suppliers and subcontractors. The most important raw materials required for our products are aluminum (sheet, plate, forgings and extrusions), titanium, nickel, steel, copper, composites and adhesives. Many major components and product equipment items are procured from or subcontracted on a sole-source basis with a number of domestic and non-U.S. companies. Although alternative sources generally exist for these raw materials, qualification of the sources could take a year or more. We are dependent upon the ability of a large number of suppliers and subcontractors to meet performance specifications, quality standards and delivery schedules at anticipated costs. While we maintain an extensive qualification system to control risk associated with such reliance on third parties, failure of suppliers or subcontractors to meet commitments could adversely affect production schedules and contract profitability, while jeopardizing our ability to fulfill commitments to our customers. The current economy has put pressure on the supply chain and we have experienced some shortages in raw materials which have impacted our near term results; however, we do not foresee any near term unavailability of materials, components or supplies that would have a material adverse effect on our business. For further discussion of the possible effects of changes in the cost or availability of raw materials on our business, see Item 1A, Risk Factors, in this Form 10-K.

INTELLECTUAL PROPERTY

We use patented and unpatented proprietary information, know-how and trade secrets to develop, maintain and enhance our competitive position, but we believe our continued success depends more on the knowledge, ability, experience and technological expertise of our employees than the legal protection that our patents and other proprietary rights may afford. Moreover, while we rely on a combination of patents, trademarks, copyrights, trade secrets, nondisclosure agreements, physical and information technology security systems, internal controls and compliance systems and other measures to protect our intellectual property, data and technology rights and that of third parties with which we are entrusted, our ability to protect and enforce our intellectual property, data and technology rights may be limited by a variety of factors and may be even more limited in certain countries outside the U.S., as may be our ability to prevent theft or compromise of our intellectual property, data and technology by competitors or third parties.

As of December 31, 2022, we held a total of 409 patents, 116 of which were U.S. patents and 293 of which were foreign patents. In addition, we have numerous U.S. and foreign patents pending. The Company believes the duration of its patents is adequate relative to the expected lives of its products.

Trademarks are also an important aspect of our business. The availability and duration of trademark registrations vary by country; however, trademarks are generally valid and may be renewed indefinitely as long as they are in use and registrations are maintained. We sell products under a number of registered trademarks that we own. Registered trademarks of the Company include KAflex®, KAron®, and K-MAX®. In all, we maintain 102 U.S. and foreign trademarks as of December 31, 2022.

BACKLOG

We anticipate that approximately 70% of our backlog at the end of 2022 will be performed in 2023. Approximately 41% of our backlog at the end of 2022 is related to U.S. Government ("USG") contracts or subcontracts.

4

Total backlog at December 31, 2022, 2021 and 2020, and the portion of the backlog we expect to complete in 2023, is as follows:

Total Backlog at December 31, 2022 | 2022 Backlog to be completed in 2023 | Total Backlog at December 31, 2021 | Total Backlog at December 31, 2020 | |||||||||||||||||||||||

| In thousands | ||||||||||||||||||||||||||

| Engineered Products | $ | 322,452 | $ | 290,618 | $ | 169,144 | $ | 134,257 | ||||||||||||||||||

| Precision Products | 134,903 | 84,118 | 180,082 | 293,261 | ||||||||||||||||||||||

| Structures | 263,581 | 127,872 | 351,697 | 203,718 | ||||||||||||||||||||||

| Total | $ | 720,936 | $ | 502,608 | $ | 700,923 | $ | 631,236 | ||||||||||||||||||

Backlog related to uncompleted contracts for which we have recorded a provision for estimated losses was $0.2 million as of December 31, 2022. At December 31, 2022, there was no backlog related to firm but not yet funded orders. See Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Note 1, Summary of Significant Accounting Policies, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K, for further discussion.

REGULATORY MATTERS

Government Contracts

The USG, and other governments, may terminate any of our government contracts at their convenience or for default if we fail to meet specified performance measurements. If any of our government contracts were to be terminated for convenience, we generally would be entitled to receive payment for work completed and allowable termination or cancellation costs. If any of our government contracts were to be terminated for default, generally the USG would pay only for the work that has been accepted and can require us to pay the difference between the original contract price and the cost to re-procure the contract items, net of the work accepted from the original contract. The USG can also hold us liable for damages resulting from the default.

During 2022, approximately 87% of the work performed by the Company directly or indirectly for the USG was performed on a fixed-price basis and the balance was performed on a cost-reimbursement basis. Under a fixed-price contract, the price paid to the contractor is negotiated at the outset of the contract and is not generally subject to adjustment to reflect the actual costs incurred by the contractor in the performance of the contract. Cost reimbursement contracts provide for the reimbursement of allowable costs and an additional negotiated fee.

Compliance with Environmental Protection Laws

Our operations are subject to and affected by a variety of federal, state, local and non-U.S. environmental laws and regulations relating to the discharge, treatment, storage, disposal, investigation and remediation of certain materials, substances and wastes. We are committed to monitoring the Company's environmental performance. As such, we continually assess our compliance status and management of environmental matters in an effort to ensure our operations are in substantial compliance with all applicable environmental laws and regulations.

Operating and maintenance costs associated with environmental compliance and management of sites are a normal, recurring part of our operations. These costs often are generally allowable costs under our contracts with the USG. It is reasonably possible that continued environmental compliance could have a material impact on our results of operations, financial condition or cash flows if more stringent clean-up standards are imposed, additional contamination is discovered and/or clean-up costs are higher than estimated.

See Environmental Matters in Item 3, Legal Proceedings and Note 19, Commitments and Contingencies, in the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K, for further discussion of our environmental matters.

International Operations

Our international sales are subject to U.S. and non-U.S. governmental regulations and procurement policies and practices, including regulations relating to import-export control, investment, exchange controls and repatriation of earnings. International sales are also subject to varying currency, political and economic risks.

5

COMPETITION

The Company operates in a highly competitive environment with many other organizations, some of which are substantially larger than us and have greater financial strength and more extensive resources. We compete for composite and metallic aerostructures subcontracts, and helicopter sales and structures, bearings, springs, seals and contacts, wheel and brake and components business on the basis of price and/or quality; product endurance and special performance characteristics; proprietary knowledge; the quality of our products and services; the availability of facilities, equipment and personnel to perform contracts; and the reputation of our business. Competitors for our business include small machine shops and offshore manufacturing facilities. We compete for advanced technology fuzing business primarily on the basis of technical competence, product quality and price, and also on the basis of our experience as a developer and manufacturer of fuzes for particular weapon types and the availability of our facilities, equipment and personnel. We are also affected by the political and economic circumstances of our potential foreign customers and, in certain situations, the relationships of those foreign customers with the USG, the USG's perceptions of those foreign customers, such as our Middle Eastern customers, and the ability to obtain necessary export approvals, licenses or authorizations from the USG.

ENVIRONMENTAL, SOCIAL AND GOVERNANCE

Climate Change

There have been no, and we do not expect there to be in the near term, material impacts on our business, financial condition or results of operations as a result of compliance with legislation or regulatory rules regarding climate change, from the known physical effects of climate change or as a result of supporting our Environmental, Social and Governance ("ESG") initiatives. Increased regulation and other climate change concerns, however, could subject us to additional costs and restrictions, and we are not able to predict how such regulations or concerns would affect our business, operations or financial results.

Human Capital

The Company employs a global workforce focused on serving its customers and creating solutions to meet their needs. We consider our employees to be the most valuable resource for current and future organizational success and we seek to provide a work environment that fosters growth, encourages self-development, and provides meaningful work. How we manage our human capital is critical to how we deliver on our strategy and create sustained growth and value for our shareholders. Kaman Corporation is a place where people who want to make a difference come to work.

Employee Demographics

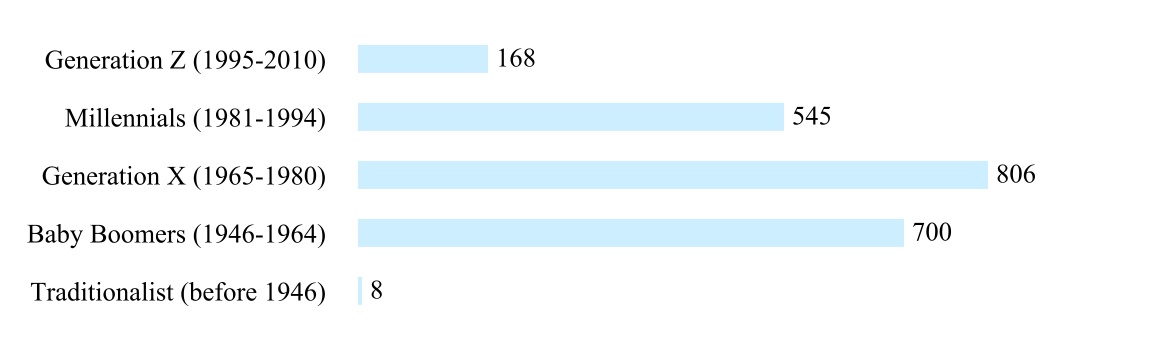

As of December 31, 2022, we employed 3,063 individuals. Of these employees, approximately 73% are employed in the United States and 27% are employed internationally. Within the United States, 63% of the employees are non-exempt and 37% are exempt.

The Company's average age of U.S. employees is 49. U.S. headcount by generation at December 31, 2022 is as follows:

Values

The Company’s core values are Respect, Excellence, Accountability, Creativity and Honor ("REACH"):

•Respect - Employees value each other as people and appreciate their skills and perspectives.

•Excellence - Employees do their best, giving full attention to the quality of every job, outcome and relationship. The highest level of customer service is provided to customers, both externally and internally.

6

•Accountability - Employees accept responsibility for their actions and work to achieve desired results.

•Creativity - Employees take on every challenge with a spirit of discovery and ingenuity, offering best ideas and resources.

•Honor - Employees behave with integrity.

Our employees are committed to these values, which define how employees behave, treat others, and fulfill job requirements.

Talent Acquisition

An important component of the Company’s Human Capital strategy is acquiring new talent. The Company strives to attract top talent with diverse backgrounds and experiences who align with the commitment of driving a culture of innovation.

The foundation of the talent acquisition strategy is the commitment to being an Equal Opportunity Employer. Qualified applicants receive consideration for employment without regard for race, color, religion, sex, sexual orientation, gender identity, national origin, disability, protected veteran status or any other protected class. The Company provides reasonable accommodations for qualified individuals with disabilities and disabled veterans in job application procedures and processes. The Company is committed to providing equal opportunity for all.

The Company uses a number of programs to ensure it attracts and hires top talent to develop as future leaders of the organization. The Kaman Internship Program is designed to provide meaningful work experiences and professional development for students. The goal of this program is to ensure a mutual benefit to both the students engaging in the internship and the Company with a pipeline of future employees. The Kaman Early Career Rotational Program is designed to provide prospective Leadership Development Candidates, who, if selected, have the opportunity to develop leadership skills and learn key organizational processes across multiple business functions. The Early Career Rotational Program is 18 to 24 months in duration and consists of rotations through Operations, Program Management, Engineering, Quality and Supply Chain Management. The Campus Champions Program is designed to engage universities and military organizations through hands-on involvement in a variety of interactive activities including participation in recruitment drives, meeting with faculty, alumni, students, student organizations and veterans’ organizations. This program allows the Company to explore opportunities to strengthen its relationships and develop mutually beneficial partnerships with these institutions.

Talent Development

In addition to acquiring new talent, the Company focuses on growing and developing its existing talent. The Company makes significant investments in enhancing its employees’ skill levels and providing professional opportunities for career development and advancement. The Company’s leadership team utilizes a robust succession planning program for identifying the next generation of leaders to ensure that the organization is well positioned to fill critical roles with employees who are prepared to support the strategy of the business and respond to the needs of key stakeholders.

Training and employee learning opportunities are offered to employees, which allows the Company to efficiently develop its staff and meet legal and compliance training requirements. Over ten thousand webinar courses were completed in 2022 in comparison to seven thousand courses in 2021, which included compliance, wellness and leadership topics delivered to the employee population.

The Company uses several mechanisms to support the development of current employees for future leadership roles. First, the Company has evolved its coaching strategy to adjust to the work environment post pandemic. Created initially in 2021, a model that embraces virtual employee coaching has expanded across all business units. Second, the Women in Leadership Program develops capabilities of female leaders through a process of learning and personal discovery to empower them to make stronger contributions within their careers and the organizations in which they work. With the use of a leadership assessment tool, management discovers the strengths and opportunities of the program participants and creates actions plans to help improve their performance. The professional networking and mentoring, which are components of the program, help prepare future leaders for larger roles in the organization. Third, in 2022, the Human Resources Team launched the Learning, Growing and Leading Series, a monthly training session in support of individuals' learning and professional development. The target audience for the 30-minute micro learning sessions includes people managers, aspiring leaders who want to continue to learn and grow in preparation for the next career opportunity, and all lifelong learners in pursuit of knowledge for personal and/or professional reasons. As of December 31, 2022, 73% and 27% of the Company's management positions were held by men and women, respectively. This compares to the Company's overall U.S. population comprised of 68% males and 32% females.

The Company executed an All-Employee Engagement Survey in 2021. The survey was an opportunity for employees to offer open, honest and confidential feedback as it was administered by a third-party organization. It was launched in the spirit of

7

continuous improvement to shape and strengthen the Company’s culture, teamwork and overall work environment. The survey is used as a tool to measure and improve engagement and satisfaction while helping us discover areas and topics where we may need more dialogue and conversation. In 2022, the Company continued to drive and embrace action plans to address the focus areas of Training and Development, Inclusive Culture and Belonging and Communication.

The Company conducts annual performance appraisals with all employees. Feedback is used to support continuous improvement. Employee annual goal setting activities align to the overall Company and business unit strategies and objectives.

Total Rewards

The Company focuses on paying its employees fairly and competitively. The Company strives to provide competitive pay opportunities which reward its employees for achieving and exceeding objectives that create long-term value for shareholders. Management aims to have all compensation programs, processes and decisions be transparent and easy to understand. Providing equitable and competitive pay enhances the Company's ability to attract and retain strong, innovative talent.

Providing comprehensive, competitive and affordable benefits is important to the Company's attraction and retention strategy. The Company offers the following:

Health Benefits

The Company offers various medical and prescription plan options and provides employees with an online cost comparison tool to assist employees with their enrollment decision. The options for dental and vision care coverage are also provided for employees. In addition to insurance benefits, Kaman’s Chronic Condition Management programs provide valuable resources to support employees and their family members dealing with a chronic condition, such as diabetes or cancer.

Wealth Benefits

The Kaman Corporation 401(k) Plan and the Bal Seal Engineering Savings and Investment Plan provides employees with a tax advantageous way to save for retirement. Both Plans provide employees with the ability to make contributions with a Company Match component. Additionally, the Company offers an Employee Stock Purchase Plan, Health Savings Accounts for those in a high deductible health plan, Health Reimbursement Accounts for Cigna health plan participants that elect to receive care from the highest-quality doctors in-network, Flexible Spending Accounts for both health care and dependent care, life and accidental death and dismemberment insurance, disability benefits and voluntary accident, hospital indemnity and critical illness insurance.

Wellness Benefits

The Fit for Life Wellness program provides all employees with opportunities to participate in Company-wide events, webinars and local wellness challenges focused on living a healthy lifestyle. Kaman’s Employee Assistance Program through LifeWorks is available to all employees and their household members who need help dealing with issues affecting their personal or professional lives. This resource connects employees with individuals who can help them with an array of issues such as locating child care programs and individual counseling.

The Company recognizes the need to support its employees’ work-life balance. In addition to FMLA benefits, the Company provides a Paid Parental Leave of Absence to better enable employees to care for and bond with a newborn, newly adopted, or newly placed foster child during the six-month period immediately following the event. Eligible employees receive three weeks of parental leave at 100% of base pay, inclusive of shift premiums, if applicable. This benefit is in addition to short-term disability benefits provided to female employees for pregnancy and childbirth.

The Company’s approach to remote work aligns with its wellness and retention strategies. The Company offers work from home opportunities, recognizing it as a strategic imperative to attract and retain employees as well as address how both current and potential employees view work, post pandemic, and value flexibility.

Health & Safety

The Company is committed to protecting and preserving the health and safety of our employees, minimizing risks, assuring compliance, and reducing business uncertainty. The Company strives for a sustainable health and safety culture based on

8

management leadership and an engaged workforce, and is committed to continuous improvement to eliminate workplace injuries, illnesses and negative environmental impacts.

The Company continues to diligently monitor and respond to the challenges faced by the organization and its employees navigating the post COVID-19 pandemic, with an emphasis on well-being. The Company's employees have worked to keep the business operational and meet customer requirements throughout the pandemic, while respecting the recommendations of local governments and regulatory agencies.

The Company's first priority continues to be the health and safety of employees and their families. As the COVID-19 pandemic evolved, a number of initiatives were implemented across the Company to ensure employees’ safety, including an increase in communications and workforce outreach. Additionally, best practices for hygiene and preventing the spread of germs continue. The increased frequency of cleaning and disinfecting common areas has been maintained and our leadership teams have responded to local business needs and priorities to ensure safe operations and minimal business disruptions.

At the onset of the pandemic, a remote work strategy was implemented where appropriate, which the Company has evolved into a formal Work from Home policy. For those employees returning to work in the Company’s offices, a formal Return to Office process was implemented to ensure those returning were trained on the Company’s enhanced health and safety protocols. In addition, the process focuses on employee re-acclimation. As we work and live in the post-pandemic world, the Company has shifted the conversation to well-being. Enhanced resources have been provided to help all employees to manage stress and anxiety.

Corporate Responsibility

The Company is a strong supporter of education, including employees’ children, employees pursuing undergraduate and graduate degrees, engineering students, museums with educational programs and various local educational programs across the country. The Company also financially supports charitable and civic organizations such as art councils, boy and girl scouts, food pantries, health organizations and veterans' organizations. Additionally, employees volunteer their time to give back to the communities in which they live and work.

Business Ethics

The Company's Code of Conduct ("Code") is a statement of the principles and standards that the Company expects the Kaman community to follow. Each officer, director and employee is required to use good ethical judgement when conducting business and comply with applicable laws, rules and regulations. The Code, which was updated effective January 1, 2022, describes what is appropriate behavior and guides ethical business decisions that support our commitment to integrity. Failure to comply with the Code and applicable laws can have severe consequences for both the Company and the individuals involved, including disciplinary action, civil penalties, or criminal prosecution under certain circumstances. In conjunction with the Code, the Company requires annual compliance training for officers, directors and employees with a goal of 100% participation.

The Company has designated Compliance Advocates who are responsible for the following:

•Distributing of the Code to the Kaman community;

•Educating and training personnel on the Code annually;

•Obtaining written acknowledgments annually from employees, officers, directors, agents, contractors, suppliers and customers that they have read, understand and will comply with the Code as a condition of their association with the Company;

•Investigating reported Code violations and implementing remedial actions when a violation has been confirmed; and

•Reporting Code submissions to the Company’s Chief Compliance Officer.

In addition to the Code, the Company has policies for anti-bribery, export and trade, antitrust, human trafficking, environmental and safety. To further facilitate these policies, annual training is provided for relevant employees on anti-bribery and anti-corruption, export compliance and data privacy. The Code and other policies discussed above are available on the Company website via www.kaman.com/investors/corporate-governance.

Diversity, Equity and Inclusion

The Company views diversity as a competitive advantage and integral to future success. Diversity helps create an innovative workforce, while inclusion ensures the Company has the right culture, processes, policies, and practices to ensure employees feel valued and included.

9

Women Advocating Leadership at Kaman ("WALK") is a program that is designed to support the advancement of Kaman’s strategic diversity goals by implementing specific business initiatives that increase the global representation of women in leadership roles. WALK’s long-term objectives include hiring; retaining and promoting more women; supporting the change in Kaman’s culture of being more accepting of women in leadership roles; providing women with equal access to development opportunities; and creating a life balance and family-friendly culture.

The Company also seeks opportunities to recruit and hire skilled veterans as well as engage in partnerships and support programs that allow the Company to give back to the veteran community. The Company has a multitude of recognition programs to show its appreciation for veterans’ service to the United States. An employee resource group is dedicated to veteran employees, which supports community engagement as well as professional development activities.

Lastly, the Company believes leadership starts from the very top. During the last two years the composition of our Board of Directors has shifted to eight members, of which 50% are women and 29% are racially or ethnically diverse. In 2020, our Board consisted of nine members, of which 22% were women and no members were racially or ethnically diverse.

Data Security

The Company maintains a commitment to cybersecurity using a combination of policy, technology, and training across the corporation. Emerging threats and regulatory compliance require constant monitoring and maintenance of the information technology environment, which the Company accomplishes by exercising internal resources, contracted partners, and industry-standard practices to meet security goals. These include implementation of technical controls such as NIST SP 800-53 and NIST SP 800-171, and adherence to guidelines including Sarbanes-Oxley and the U.S. Department of Defense Federal Acquisition Regulation Supplement ("DFARS").

The Company's cybersecurity protection is based on layered technology supporting trained employees. Periodic testing of networks, systems, and personnel is performed to validate implementation and effectiveness of controls. Penetration testing, internal and external audit and annual review of policies and response plans provide governance and independent verification that the Company maintains effective cybersecurity controls.

For further information on our ESG initiatives, refer to Information about the Board of Directors and Corporate Governance section of the Proxy Statement.

AVAILABLE INFORMATION

We are subject to the reporting requirements of the Exchange Act and its rules and regulations. The Exchange Act requires us to file reports, proxy statements and other information with the SEC.

We make available, free of charge on our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, proxy statements, and current reports on Form 8-K as well as amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Exchange Act, together with Section 16 insider beneficial stock ownership reports, as soon as reasonably practicable after we electronically file these documents with, or furnish them to, the SEC. These documents are posted on our website at www.kaman.com — select the “Investors” link, then the "Financial Information" link and then view under “SEC Filings”.

We also make available, free of charge on our website, our Certificate of Incorporation, By–Laws, Governance Principles and all Board of Directors' standing Committee Charters (Audit, Corporate Governance, Compensation and Finance). These documents are posted on our website at www.kaman.com — select the “Investors” link, then the "Corporate Governance" link and then view under "Documents and Downloads".

The information contained on our website is not intended to be, and shall not be deemed to be, incorporated into this Form 10-K or any other filing under the Exchange Act or the Securities Act of 1933, as amended.

10

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The Company’s executive officers as of the date of this report are as follows:

| Name | Age | Position | Prior Experience | ||||||||

| Ian K. Walsh | 56 | Chairman, President, Chief Executive Officer and Director | Mr. Walsh was appointed President and Chief Executive Officer as well as elected as a Director of the Company effective September 8, 2020. Effective April 14, 2021, Mr. Walsh was appointed Chairman of the Board. Prior to joining the Company, Mr. Walsh was Chief Operating Officer at REV Group, Inc., a leading designer, manufacturer, and distributor of specialty vehicles and related aftermarket parts and services, since 2018. Prior to that, he progressed through leadership roles of increasing responsibility at Textron Inc., where he most recently served as President and Chief Executive Officer of TRU Simulation and Training from 2015 to 2018. Prior to joining Textron, he served as an officer and naval aviator in the U.S. Marine Corps. Mr. Walsh is a certified Six Sigma Black Belt. | ||||||||

| James G. Coogan | 42 | Senior Vice President, Chief Financial Officer and Treasurer | Mr. Coogan was appointed Senior Vice President and Chief Financial Officer, effective July 8, 2021, and he was appointed Treasurer, effective January 18, 2023. Mr. Coogan has served in various roles since joining the Company in 2008, most recently as Vice President, Investor Relations & Business Development from January 2020 through July 2021 and prior to that, Vice President, Investor Relations from April 2017 through December 2019. Previous Kaman positions include: Assistant Vice President, SEC Compliance and External Reporting, Director, External Reporting and SEC Compliance, and Manager, External Reporting and SEC Compliance. Prior to joining the Company, Mr. Coogan held positions at Ann Taylor Stores Corporation, Mohegan Tribal Gaming Authority and PricewaterhouseCoopers. | ||||||||

| Carroll K. Lane | 47 | Senior Vice President and Segment Lead, Engineered Products and Precision Products | Mr. Lane joined the Company in July 2022 and was appointed segment lead of Precision Products as well as Senior Vice President and President, Kaman Air Vehicles and Kaman Precision Products. In January 2023, he was appointed segment lead of Engineered Products in addition to his previous responsibilities. Prior to joining the Company, Mr. Lane held positions of increasing responsibility at United Technologies Corporation ("UTC"), now Raytheon Technologies Corporation, including President of Commercial Engines, Pratt & Whitney from 2020 to 2022; Vice President of Investor Relations from 2016 to 2020; and Vice President of Commercial Engines Aftermarket, Pratt & Whitney. Prior to joining UTC, Mr. Lane was a Director with CSP Associates, an aerospace and defense advisory firm. | ||||||||

| Richard S. Smith, Jr. | 63 | Senior Vice President, General Counsel and Secretary | Mr. Smith was appointed Senior Vice President and General Counsel, effective January 27, 2023, after having previously served as Vice President, Deputy General Counsel and Secretary since joining the Company in the fall of 2012. Before joining the Company, Mr. Smith had been a partner with the Hartford, Connecticut law firm Murtha Cullina LLP, for approximately 21 years and, before that, an associate since graduating from the Duke University School of Law in the spring of 1984. | ||||||||

11

| Name | Age | Position | Prior Experience | ||||||||

| Roy Dilig | 57 | Vice President, Information Technology | Mr. Dilig was appointed Vice President, Information Technology, effective January 27, 2023. Prior to this role, Mr. Dilig served as Director of Information Technology for the Company's Bal Seal Engineering division, since 2011. He held positions of increasing responsibility at Bal Seal Engineering, including Systems Development Manager and Programmer Analyst. Prior to this, Mr. Dilig was a Programmer Analyst for The Walt Disney Company. | ||||||||

| Megan A. Morgan | 46 | Vice President, Human Resources and Chief Human Resources Officer | Ms. Morgan was appointed Vice President, Human Resources and Chief Human Resources Officer, effective February 1, 2021. Ms. Morgan has served in various roles since joining the Company in 2018, most recently as Vice President of Human Resources, Kaman Aerospace Group. Prior to joining the company, Ms. Morgan held positions at Legrand Electrical Wiring Systems, Barnes Group Inc., and PricewaterhouseCoopers. | ||||||||

| Kristen M. Samson | 49 | Vice President and Chief Marketing and Communications Officer | Ms. Samson joined Kaman as Vice President and Chief Marketing and Communications Officer effective January 18, 2021. Prior to joining Kaman, Ms. Samson served in various leadership roles, including Vice President, Marketing and Communications for Textron Systems from 2019 to 2021; Vice President, Marketing and Communications for TRU Simulation + Training from 2016 to 2019; and Vice President of Marketing, Communications and Product Management at Lycoming Engines. Prior to this, Ms. Samson held positions at Comcast Sportsnet and Time Warner Cable. She is a certified Six Sigma Green Belt. | ||||||||

Each executive officer holds office for a term of one year and until his or her successor is duly appointed and qualified, in accordance with the Company’s By-Laws.

12

ITEM 1A. RISK FACTORS

Our business, financial condition, operating results and cash flows can be impacted by the factors set forth below, any one of which could cause our actual results to vary materially from recent results or from our anticipated future results.

RISKS RELATED TO OUR BUSINESS, THE INDUSTRIES IN WHICH WE OPERATE, OUR PROGRAMS AND OUR CONTRACTS

Our failure to comply with the covenants contained in our credit facility could trigger an event of default, which could materially and adversely affect our operating results and our financial condition.

Our credit facility requires us to maintain certain financial ratios and comply with various operational and other covenants. As of December 31, 2022, our Consolidated Total Net Leverage Ratio was 3.65, as calculated in accordance with the Credit Agreement, compared to the maximum permitted ratio of 5.00 to 1.00. If we were unable to maintain these ratios and comply with such covenants, we would need to seek relief from our lenders in order to avoid, cure or have waived an event of default under the facility. There can be no assurance that we would be able to obtain such relief on commercially reasonable terms or otherwise. If an event of default occurs and is not cured or waived, we may not be able to make further borrowings under the credit facility and our lenders could, among other things, cause all outstanding indebtedness under the credit facility to be due and payable immediately. There can be no assurance that our assets or cash flows would be sufficient to provide us with the liquidity to fund outstanding commitments or meet other business requirements or to enable us to fully repay those amounts or that we would be able to refinance or restructure the indebtedness. If, as or when required, we are unable to repay, refinance or restructure the indebtedness outstanding under our credit facility, or amend the financial ratios and covenants contained therein, the lenders under our credit facility could elect to terminate their commitments thereunder, cease making further loans and institute foreclosure proceedings against our assets. This, in turn, could result in an event of default under one or more of our other financing agreements, including our convertible notes.

In addition, in the ordinary course of business, certain of our customers require us to deliver standby letters of credit to guarantee our performance under our contractual obligations with them, which are currently issued by certain of our lenders pursuant to our credit facility. If we are unable to obtain letters of credit as needed to operate our business as a result of any of the circumstances described above or otherwise, our ability to enter into certain contracts may be adversely affected. Moreover, by their nature, standby letters of credit may be drawn upon by the beneficiaries thereof, which could affect our financial ratios and ability to make additional borrowings. The occurrence of any of these events could have a material adverse effect on our liquidity, financial position or results of operations.

We have increased debt and high leverage, which could have a negative impact on our financing options and liquidity position and which could adversely affect our business.

As of December 31, 2022, we had $562.5 million in long-term debt outstanding excluding debt issuance costs. Additionally, our secured revolving credit facility has a remaining borrowing capacity of $211.1 million, subject to EBITDA, as of December 31, 2022 (all of which would be secured when drawn).

Our overall leverage and the terms of our financing arrangements could:

•limit our ability to obtain additional financing in the future for working capital, capital expenditures or acquisitions, to fund growth or for general corporate purposes, even when necessary to maintain adequate liquidity, particularly if any ratings assigned to our debt securities by ratings organizations were revised downward;

•make it more difficult for us to satisfy the terms of our obligations under the terms of our financing arrangements;

•limit our ability to refinance our indebtedness on terms acceptable to us, or at all;

•limit our flexibility to plan for and to adjust to changing business and market conditions in the industries in which we operate and increase our vulnerability to general adverse economic and industry conditions;

•require us to dedicate a substantial portion of our cash flow from operations to make interest and principal payments on our debt, thereby limiting the availability of our cash flow to fund future investments, capital expenditures, working capital, business activities and other general corporate requirements;

•increase our vulnerability to adverse economic or industry conditions; and

•subject us to higher levels of indebtedness than our competitors, which may cause a competitive disadvantage and may reduce our flexibility in responding to increased competition.

Our ability to meet expenses and debt service obligations will depend on our future performance, which will be affected by financial, business, economic and other factors, including the impact of the COVID-19 pandemic, the inflationary environment,

13

rising interest rates, potential changes in consumer and customer preferences and behaviors, the success of product and marketing innovation and pressure from competitors. If we do not generate enough cash to pay our debt service obligations, we may be required to refinance all or part of our existing debt, sell assets, borrow more money or issue additional equity.

We will complete JPF production under our USG contract in early 2023, so the future viability of our JPF program will depend on our ability to market and sell the FMU 152 A/B to foreign militaries in direct commercial sales transactions.

Our JPF program continues to wind down as it moves to the end of its lifecycle, reflecting the previously announced decision of the United States Air Force ("USAF") to move from the FMU 152 A/B (the "JPF") (which we manufacture and produce) to the FMU-139 D/B (which we do not manufacture or produce) as its primary fuze system. We expect to complete Option 16 of our JPF contract with the USG in the first half of 2023. Like the option before it, Option 16 related solely to the procurement of fuzes by or in support of foreign militaries and did not include any sales to the USAF. The USG has indicated that they will not award us any future options, either as direct sales to the USG or indirect sales to foreign militaries through the USG. Therefore, the future viability of our JPF program will depend entirely on our ability to market and sell the JPF to foreign militaries in direct commercial sales (“DCS”) transactions. As of December 31, 2022, our total JPF backlog was $20.0 million, and we expect to recognize substantially all of the backlog within the first half of 2023. We are currently in discussions with two Middle Eastern customers for one or more follow-on orders aggregating a minimum of $45.0 million that would further extend the life of the program, but there can be no assurance as to the receipt, magnitude and timing of these orders. Moreover, any such orders, if received, would be subject to the receipt of all necessary export approvals, licenses and other authorizations, including the receipt of manufacturing authorization from the USG, needed to effectuate the sales, which are subject to political and geopolitical conditions beyond our control.

As a result of the inability to successfully market and sell the JPF to foreign militaries in DCS transactions in a timely manner at prices and in quantities that would continue to support production at current levels, in the fourth quarter, we announced a restructuring plan that will lead to the permanent closure of our Orlando, Florida manufacturing facility by the end of 2024. We expect to consolidate JPF production in our Middletown, Connecticut, facility during the first half of 2023 as the facility has the potential capacity to deliver against future DCS orders.

Our business, results of operations, financial condition and cash flows have been and are expected to continue to be adversely impacted by the ongoing COVID-19 pandemic.

The COVID-19 pandemic has created significant disruption and uncertainty in the global economy. Its impact has resulted in business and manufacturing disruptions, plant closures, inventory shortages, delivery delays, supply chain disruptions, and order reductions, cancellations and deferrals, all of which have adversely affected our business, results of operations, financial condition and cash flows. Although we continue to meet the demands of our customers, we have seen some disruptions in our supply chain, such as delays in materials and components used in our manufacturing process, and we continue to operate below pre-pandemic levels for certain commercial aerospace products. We are encouraged by the recoveries for these products and the strong order intake we saw throughout 2022; however, the extent to which COVID-19 may continue to adversely impact our business depends on future developments, which are highly uncertain and unpredictable, the severity and duration of the pandemic and the effectiveness of actions taken globally to contain or mitigate its effects. To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this report, such as those relating to our products and financial performance.

Our financial performance is significantly influenced by conditions within the aerospace and defense industries.

The financial performance of our business is directly tied to economic conditions in the commercial aviation and defense industries. The commercial aviation industry tends to be cyclical, and capital spending by airlines and aircraft manufacturers may be influenced by a variety of global factors including current and future traffic levels, aircraft fuel pricing, labor issues, competition, the retirement of older aircraft, regulatory changes, terrorism and related safety concerns, general economic conditions, worldwide airline profits and backlog levels. The defense industry may be influenced by a changing global political environment, changes in U.S. and global defense spending, U.S. foreign policy and the activity level of military flight operations. Changes to the aerospace and defense industries and any reductions in U.S. defense spending could have a material impact on our current and proposed aerospace programs, which could adversely affect our operating results and future prospects. In addition, changes in economic conditions may cause customers to request that firm orders be rescheduled or canceled, which could put a portion of our backlog at risk.

Furthermore, because of the lengthy research and development cycle involved in bringing new products to market, we cannot predict the economic conditions that will exist when a new product is introduced. A reduction in capital spending in the aviation

14

or defense industries could have a significant effect on the demand for our products, which could have an adverse effect on our financial performance or results of operations.

We are subject to a number of risks and uncertainties related to the timing and conditions surrounding the production of the 737 MAX.

On March 13, 2019, the Federal Aviation Administration ("FAA") issued an order to suspend operations of all 737 MAX aircraft in the U.S. and by U.S. aircraft operators following two fatal 737 MAX accidents. Non-U.S. civil aviation authorities issued directives to the same effect. Boeing suspended deliveries until the FAA and other civil aviation authorities worldwide granted the clearance to return the aircraft to service and suspended production of the 737 MAX in January 2020 as a result of the ongoing evaluation. In November 2020, the FAA lifted the orders to suspend operations of the Boeing 737 MAX and in early 2021, airlines around the globe began to clear the Boeing 737 MAX for flight. Although production rates increased in 2022 and higher output rates are expected in 2023, there can be no assurance that the production rate will return to the production rate prior to the grounding of the 737 MAX fleet. We have recognized $11.7 million, $4.0 million and $5.6 million in revenue associated with the sale of our products that are utilized on the 737 MAX aircraft fleet in the years ended December 31, 2022, 2021 and 2020, respectively. Any future reductions to the production rate or lower than anticipated production levels could have an adverse effect on our financial position, results of operations, and/or cash flows.

Our USG programs are subject to unique risks.

We have several significant long-term contracts either directly with the USG or where the USG is the ultimate customer, including the Sikorsky BLACK HAWK cockpit program, the A-10 program and the JPF program. These contracts are subject to unique risks, some of which are beyond our control. Examples of such risks include:

•The USG may modify, curtail or terminate its contracts and subcontracts at its convenience without prior notice, upon payment for work done and commitments made at the time of termination. As discussed above, the Company has been advised by our customer that Option 16, received in 2021, will be the last order under our JPF contract with the USG. Modification, curtailment or termination of our major programs or contracts could have a material adverse effect on our business, financial condition, results of operations and cash flows.

•Our USG business is subject to specific procurement regulations and other requirements. These requirements, although customary in USG contracts, increase our performance and compliance costs. These costs might increase in the future, reducing our margins, which could have a negative effect on our financial condition. Although we have procedures designed to assure compliance with these regulations and requirements, failure to do so under certain circumstances could lead to suspension or debarment, for cause, from USG contracting or subcontracting for a period of time and could have a material adverse effect on our business, financial condition, results of operations and cash flows and could adversely impact our reputation and our ability to receive other USG contract awards in the future.

•The costs we incur on our USG contracts, including allocated indirect costs, may be audited by USG representatives. Any costs found to be improperly allocated to a specific contract would not be reimbursed, and such costs already reimbursed would have to be refunded, which could have a material adverse effect on our business, financial condition, results of operations and cash flows. Moreover, if any audit were to reveal the existence of improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with the USG.

•We are from time to time subject to governmental inquiries and investigations of our business practices due to our participation in domestic and foreign government contracts and programs and our transaction of business domestically and internationally. Adverse findings associated with any such inquiry or investigation could also result in civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with domestic and foreign governments.

•The costs to implement and comply with the Cybersecurity Maturity Model Certification ("CMMC") as initiated by the U.S. Department of Defense in order to measure their defense contractors' capabilities, readiness, and sophistication in the area of cybersecurity.

Our business may be adversely affected by changes in budgetary priorities of the USG.

Because a significant percentage of our revenue is derived either directly or indirectly from contracts with the USG, changes in federal government budgetary priorities could directly affect our financial performance. A significant decline in government expenditures, a shift of expenditures away from programs that we support or a change in federal government contracting policies could cause federal government agencies to reduce their purchases under contracts, to exercise their right to terminate contracts at any time without penalty or not to exercise options to renew contracts.

15

Estimates of future costs for long-term contracts impact our current and future operating results and profits.

We generally recognize sales and gross margin on long-term contracts based on the over time method of accounting. This method allows for revenue recognition as our work progresses on a contract and requires that we estimate future revenues and costs over the life of a contract. Revenues are estimated based upon the negotiated contract price, with consideration being given to exercised contract options, change orders and, in some cases, projected customer requirements. Contract costs may be incurred over a period of several years, and the estimation of these costs requires significant judgment based upon the acquired knowledge and experience of program managers, engineers and financial professionals.

Estimated costs are based primarily on anticipated purchase contract terms, historical performance trends, business base and other economic projections. The complexity of certain programs as well as technical risks and the availability of materials and labor resources could affect our ability to accurately estimate future contract costs. Additional factors that could affect recognition of revenue and gross margin under this method include:

•Accounting for initial program costs;

•The effect of nonrecurring work;

•Delayed contract start-up or changes to production schedules;

•Transition of work to or from the customer or other vendors;

•Claims or unapproved change orders;

•Product warranty issues;

•Delayed completion of certain programs for which inventory has been built up;

•Our ability to estimate or control scrap level;

•Accrual of contract losses; and

•Changes in our overhead rates.

Because of the significance of the judgments and estimation processes, it is likely that materially different sales and profit amounts could be recorded if we used different assumptions or if the underlying circumstances were to change. Changes in underlying assumptions, circumstances or estimates may adversely affect current and future financial performance. While we perform quarterly reviews of our long-term contracts to address and lessen the effects of these risks, there can be no assurance that we will not make material adjustments to underlying assumptions or estimates relating to one or more long-term contracts that have a material adverse effect on our business, financial condition, results of operations and cash flows.

We may lose money or generate lower than expected profits on our fixed-price contracts.

Our customers set demanding specifications for product performance, reliability and cost. Most of our government contracts and subcontracts provide for a predetermined, fixed price for the products we make regardless of the costs we incur. Therefore, we must absorb cost overruns, notwithstanding the difficulty of estimating all of the costs we will incur in performing these contracts and in projecting the ultimate level of sales that we may achieve. Our failure to anticipate technical problems, estimate costs accurately, integrate technical processes effectively or control costs during performance of a fixed-price contract may reduce the profitability of a fixed-price contract or cause a loss. Given the current inflationary environment, we have and may continue to experience material and labor cost increases at a higher rate than what we have historically experienced. While we believe that we have recorded adequate provisions in our financial statements for losses on our fixed-price contracts as required under GAAP, there can be no assurance that our contract loss provisions will be adequate to cover all actual future losses.

Inflation may have an adverse effect on our business, our suppliers and our customers.

Although inflation in the United States had been relatively low for several years, there has been a significant increase in inflation in 2022. The Federal Reserve has raised certain benchmark interest rates in an effort to combat inflation. Inflation increases the cost of goods and services we utilize in our operations, such as electricity, heating and other utilities, which increases our expenses. Inflation may also cause us to increase wages by a larger amount than we have budgeted to retain our employees. Our suppliers may also be affected by inflation and the rising costs of goods and services used in their businesses, and they may attempt to pass these costs down to us. Inflation may also have a negative impact on our customers' ability to afford our products. If we are unable to recover inflationary cost increases with increased prices on our products, this could impact margin profitability.

We face significant pressure to lower our pricing notwithstanding our own internal costs.

There is substantial and continuing pressure from original equipment manufacturers ("OEMs") in the commercial aerospace industry to reduce the prices they pay to suppliers, such as Kaman. We attempt to manage such downward pricing pressure,

16

while trying to preserve our business relationships with our customers, by seeking to reduce our production and procurement costs through various measures, including implementing cost-effective process improvements and partnering with our own suppliers to reduce our cost of raw materials and components. Our suppliers have periodically resisted, and in the future may resist, pressure to lower their prices and have begun to impose price increases. If we are unable to offset price reductions from our OEM customers, this could have a material adverse effect on our business, financial condition, results of operations and cash flows.

The ability to obtain and retain product approvals issued by the FAA and any intellectual property claims could adversely affect our operating results and profits.

Our business may be impacted by regulations set forth by the FAA to obtain Parts Manufacturer Approvals ("PMAs") to design or produce a modification or replacement aircraft part. The loss or suspension of the Company's product and design approvals could negatively impact our operating results and profits. We believe our current design and production processes that are subject to such regulations by the FAA are in compliance; however, there can be no assurance that we will not lose approvals for our products in the future. Additionally, we have been subject to claims of intellectual property infringement by third parties, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Competition from domestic and foreign manufacturers may result in the loss of potential contracts and opportunities.

The markets in which we participate are highly competitive, and we often compete for work not only with large OEMs but also sometimes with our own customers and suppliers. Many of our large customers may choose not to outsource production due to, among other things, their own direct labor and overhead considerations and capacity utilization objectives. This could result in these customers supplying their own products or services and competing directly with us for sales of these products or services, all of which could significantly reduce our revenues.

Our competitors may have more extensive or more specialized engineering, manufacturing and marketing capabilities than we do in some areas, and we may not have the technology, cost structure, or available resources to effectively compete with them. We believe that developing and maintaining a competitive advantage requires continued investment in product development; engineering; supply chain management; production capabilities, including technology, equipment and facilities; and sales and marketing, and we may not have enough resources to make the necessary investments to do so. Further, our significant customers may attempt to use their position to negotiate price or other concessions for a particular product or service without regard to the terms of an existing contract or the underlying cost of production.

We believe our strategies for our business will allow us to continue to effectively compete for key contracts and customers, but there can be no assurance that we will be able to compete successfully in this market or against such competitors.

RISKS RELATED TO INFORMATION TECHNOLOGY AND CYBERSECURITY

Cybersecurity requirements, vulnerabilities, threats and more sophisticated and targeted computer crime could pose a risk to our systems, networks, products and data.

Our information technology systems provide critical data connectivity, information and services for internal and external users. These interactions include, but are not limited to, ordering and managing materials from suppliers, inventory management, shipping products to customers, processing transactions, summarizing and reporting results of operations, complying with regulatory, legal or tax requirements and other processes necessary to manage our business. Our computer systems face the threat of unauthorized access, computer hackers, computer viruses, malicious code, organized cyber-attacks and other security problems and system disruptions. These threats may be heightened due to the ongoing military conflict between Ukraine and Russia. We rely heavily on our information technology systems, networks and services, some of which are managed, hosted and provided by third-parties to conduct our business.

Cyber-attacks are evolving and include, but are not limited to, malicious software, destructive malware, attempts to gain unauthorized access to data, manipulation of data, disruption or denial of service attacks and other electronic security breaches that could lead to disruptions in critical systems, unauthorized release of confidential, personal or otherwise protected information, including trade secrets, and corruption of data, networks or systems. We provide products and services to customers who also face cyber threats. Our products and services may be subject to cyber threats and we may not be able to detect or deter such threats, which could result in losses that could adversely affect our customers and our company. For example, in December 2020, Bal Seal identified file encryption activity and ransom notes on systems within its environment indicative of a Doppelpaymer ransomware attack, which disrupted Bal Seal's information technology systems. Although no payments were made to the threat actor, the interruption resulted in a temporary delay of revenue and in the incurrence of

17

incremental costs for the year ended December 31, 2020; however, the incident was not material to the Company's fiscal year 2020 financial results.

We could also be impacted by cyber threats in our suppliers', partners' and customers' systems that are used in connection with our business, including threats directed towards our third-party and cloud service providers. Any such breach could compromise our networks and the information there could be accessed, publicly disclosed, lost or stolen. These events, if not prevented or mitigated, could damage our reputation, require remedial action and lead to loss of business, regulatory actions, potential liability and other financial losses. To address the risks to our information technology systems and data, we manage an information security program, maintain strong incident report capabilities and perform daily off-site backups. Additionally, we have put in place business continuity plans and security precautions for our critical systems, including a back-up data center. Updates on cyber security are provided to the Board of Directors at least twice a year.

Our information technology systems, processes and sites may suffer interruptions or failures which may affect our ability to conduct our business.

In the event our information technology systems are damaged or cease to function properly due to any number of causes, such as catastrophic events, power outages and security breaches resulting in unauthorized access or cyber-attacks, and our information security program, incident report capabilities, business continuity plans and security precautions do not function effectively on a timely basis, we may suffer interruptions in our operations or the misappropriation of proprietary information, which may adversely impact our business, financial condition, results of operations and cash flows. In December 2020, an unauthorized party disrupted access to Bal Seal's information technology systems. The interruption resulted in a temporary delay of revenue and in the incurrence of incremental costs for the year ended December 31, 2020; however, the incident was not material to the Company's fiscal year 2020 financial results. Bal Seal was able to restore its affected systems and resume business operations in a relatively short period of time.

We have outsourced our information technology functions and transitioned to cloud-based technologies. Disruptions or delays at our third-party service providers could impact our operations.

As part of the comprehensive review of our general and administrative functions in order to improve operational efficiency and to align the Company's costs with its revenues, we outsourced certain information technology functions. While we believe we conducted appropriate diligence before entering into agreements with our third-party service providers and have the proper controls and oversight over the IT functions performed by our third parties, the failure of one or more of such entities to meet our performance standards and expectations, with respect to data security, compliance with data protection and privacy laws, providing services on a timely basis or providing services at the prices we expect, may have an adverse effect on our results of operations or financial condition. Additionally, we have transitioned certain technology to cloud-based infrastructure. Our utilization of cloud services is critical to developing and providing products and services to our customers, scaling our business for future growth, accurately maintaining data and otherwise operating our business. Failure of cloud infrastructure providers to maintain adequate physical, technical and administrative safeguards to protect the security of our confidential information and data could result in unauthorized access to our systems or a system or network disruption that could lead to improper disclosure of confidential information or data, regulatory penalties and remedial costs. There may also be a discrepancy between the contractual liability profile that the cloud service provider has agreed to and our contractual liability profile with our customers. Any disruption to either the outsourced systems or the communication links between us and the outsourced suppliers could negatively affect our ability to operate our data systems, and could impair our ability to provide services to our customers. As we increase our reliance on these third-party systems, our exposure to damage from service disruptions may increase and we may incur additional costs to remedy the damages caused by these disruptions.

RISKS RELATED TO COMPLIANCE

Exports of certain of our products are subject to various export control regulations and authorizations, and we may not be successful in obtaining the necessary U.S. Government approvals and resultant export licenses for proposed sales to certain foreign customers.

We must comply with numerous laws and regulations relating to the export of our products and technologies, including, among others, the FMU-152A/B JPF, before we are permitted to sell those products and technologies outside of the United States. Compliance often entails the submission and timely receipt of necessary export approvals, licenses or authorizations from the USG and, depending on the size and nature of the proposed transaction, may even require the submission of formal notification to the United States Congress, which then has the ability to pass a joint resolution of disapproval blocking or amending the sale. Over the last several years, the U.S. export licensing environment for munitions, such as the JPF, has been adversely affected by a number of factors, including, but not limited to, the changing geopolitical environment and heightened tensions with other

18