UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||||||

| For the quarterly period ended | |||||||||||

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the transition period from to | ||||||||

Commission File Number: 000-06217

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Accelerated filer | Non-accelerated filer | Smaller reporting company | Emerging growth company | |||||||||||

| ☑ | ¨ | ¨ | ||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of April 19, 2024, the registrant had outstanding 4,257 million shares of common stock.

Table of Contents

Organization of Our Form 10-Q

The order and presentation of content in our Form 10-Q differs from the traditional SEC Form 10-Q format. Our format is designed to improve readability and better present how we organize and manage our business. See "Form 10-Q Cross-Reference Index" within Risk Factors and Other Key Information for a cross-reference index to the traditional SEC Form 10-Q format.

We have defined certain terms and abbreviations used throughout our Form 10-Q in "Key Terms" within the Consolidated Condensed Financial Statements and Supplemental Details.

The preparation of our Consolidated Condensed Financial Statements is in conformity with US GAAP. Our Form 10-Q includes key metrics that we use to measure our business, some of which are non-GAAP measures. See "Non-GAAP Financial Measures" within MD&A for an explanation of these measures and why management uses them and believes they provide investors with useful supplemental information.

| Page | |||||||||||

Forward-Looking Statements | |||||||||||

Availability of Company Information | |||||||||||

A Quarter in Review | |||||||||||

Consolidated Condensed Financial Statements and Supplemental Details | |||||||||||

| Consolidated Condensed Statements of Income | |||||||||||

| Consolidated Condensed Statements of Comprehensive Income | |||||||||||

| Consolidated Condensed Balance Sheets | |||||||||||

| Consolidated Condensed Statements of Cash Flows | |||||||||||

| Consolidated Condensed Statements of Stockholders' Equity | |||||||||||

| Notes to Consolidated Condensed Financial Statements | |||||||||||

| Key Terms | |||||||||||

Management's Discussion and Analysis (MD&A) | |||||||||||

| Segment Trends and Results | |||||||||||

| Consolidated Condensed Results of Operations | |||||||||||

| Liquidity and Capital Resources | |||||||||||

| Non-GAAP Financial Measures | |||||||||||

Risk Factors and Other Key Information | |||||||||||

| Risk Factors | |||||||||||

| Quantitative and Qualitative Disclosures About Market Risk | |||||||||||

| Controls and Procedures | |||||||||||

| Issuer Purchases of Equity Securities | |||||||||||

| Rule 10b5-1 Trading Arrangements | |||||||||||

| Disclosure Pursuant to Section 13(r) of the Securities Exchange Act of 1934 | |||||||||||

| Exhibits | |||||||||||

| Form 10-Q Cross-Reference Index | |||||||||||

Forward-Looking Statements

This Form 10-Q contains forward-looking statements that involve a number of risks and uncertainties. Words such as "accelerate", "achieve", "aim", "ambitions", "anticipate", "believe", "committed", "continue", "could", "designed", "estimate", "expect", "forecast", "future", "goals", "grow", "guidance", "intend", "likely", "may", "might", "milestones", "next generation", "objective", "on track", "opportunity", "outlook", "pending", "plan", "position", "possible", "potential", "predict", "progress", "ramp", "roadmap", "seek", "should", "strive", "targets", "to be", "upcoming", "will", "would", and variations of such words and similar expressions are intended to identify such forward-looking statements, which may include statements regarding:

•our business plans and strategy and anticipated benefits therefrom, including with respect to our IDM 2.0 strategy, Smart Capital strategy, partnership with Brookfield, internal foundry model, updated reporting structure, and AI strategy;

•projections of our future financial performance, including future revenue, gross margins, capital expenditures, and cash flows;

•projected costs and yield trends;

•future cash requirements, the availability, uses, sufficiency, and cost of capital resources, and sources of funding, including for future capital and R&D investments and for returns to stockholders, such as stock repurchases and dividends, and credit ratings expectations;

•future products, services, and technologies, and the expected goals, timeline, ramps, progress, availability, production, regulation, and benefits of such products, services, and technologies, including future process nodes and packaging technology, product roadmaps, schedules, future product architectures, expectations regarding process performance, per-watt parity, and metrics, and expectations regarding product and process leadership;

•investment plans and impacts of investment plans, including in the US and abroad;

•internal and external manufacturing plans, including future internal manufacturing volumes, manufacturing expansion plans and the financing therefor, and external foundry usage;

•future production capacity and product supply;

•supply expectations, including regarding constraints, limitations, pricing, and industry shortages;

•plans and goals related to Intel's foundry business, including with respect to anticipated customers, future manufacturing capacity and service, technology, and IP offerings;

•expected timing and impact of acquisitions, divestitures, and other significant transactions, including the sale of our NAND memory business;

•expected completion and impacts of restructuring activities and cost-saving or efficiency initiatives;

•future social and environmental performance goals, measures, strategies, and results;

•our anticipated growth, future market share, and trends in our businesses and operations;

•projected growth and trends in markets relevant to our businesses;

•anticipated trends and impacts related to industry component, substrate, and foundry capacity utilization, shortages, and constraints;

•expectations regarding government incentives;

•future technology trends and developments, such as AI;

•future macro environmental and economic conditions;

•geopolitical tensions and conflicts and their potential impact on our business;

•tax- and accounting-related expectations;

•expectations regarding our relationships with certain sanctioned parties; and

•other characterizations of future events or circumstances.

Such statements involve many risks and uncertainties that could cause our actual results to differ materially from those expressed or implied, including those associated with:

•the high level of competition and rapid technological change in our industry;

•the significant long-term and inherently risky investments we are making in R&D and manufacturing facilities that may not realize a favorable return;

•the complexities and uncertainties in developing and implementing new semiconductor products and manufacturing process technologies;

•our ability to time and scale our capital investments appropriately and successfully secure favorable alternative financing arrangements and government grants;

•implementing new business strategies and investing in new businesses and technologies;

•changes in demand for our products;

•macroeconomic conditions and geopolitical tensions and conflicts, including geopolitical and trade tensions between the US and China, the impacts of Russia's war on Ukraine, tensions and conflict affecting Israel and the Middle East, and rising tensions between mainland China and Taiwan;

•the evolving market for products with AI capabilities;

| 1 | |||||||

•our complex global supply chain, including from disruptions, delays, trade tensions and conflicts, or shortages;

•product defects, errata and other product issues, particularly as we develop next-generation products and implement next-generation manufacturing process technologies;

•potential security vulnerabilities in our products;

•increasing and evolving cybersecurity threats and privacy risks;

•IP risks including related litigation and regulatory proceedings;

•the need to attract, retain, and motivate key talent;

•strategic transactions and investments;

•sales-related risks, including customer concentration and the use of distributors and other third parties;

•our significantly reduced return of capital in recent years;

•our debt obligations and our ability to access sources of capital;

•complex and evolving laws and regulations across many jurisdictions;

•fluctuations in currency exchange rates;

•changes in our effective tax rate;

•catastrophic events;

•environmental, health, safety, and product regulations;

•our initiatives and new legal requirements with respect to corporate responsibility matters; and

•other risks and uncertainties described in this report, our 2023 Form 10-K and our other filings with the SEC.

Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Readers are urged to carefully review and consider the various disclosures made in this Form 10-Q and in other documents we file from time to time with the SEC that disclose risks and uncertainties that may affect our business.

Unless specifically indicated otherwise, the forward-looking statements in this Form 10-Q do not reflect the potential impact of any divestitures, mergers, acquisitions, or other business combinations that have not been completed as of the date of this filing. In addition, the forward-looking statements in this Form 10-Q are based on management's expectations as of the date of this filing, unless an earlier date is specified, including expectations based on third-party information and projections that management believes to be reputable. We do not undertake, and expressly disclaim any duty, to update such statements, whether as a result of new information, new developments, or otherwise, except to the extent that disclosure may be required by law.

Availability of Company Information

We use our Investor Relations website, www.intc.com, as a routine channel for distribution of important, and often material, information about us, including our quarterly and annual earnings results and presentations, press releases, announcements, information about upcoming webcasts, analyst presentations, and investor days, archives of these events, financial information, corporate governance practices, and corporate responsibility information. We also post our filings on this website the same day they are electronically filed with, or furnished to, the SEC, including our annual and quarterly reports on Forms 10-K and 10-Q and current reports on Form 8-K, our proxy statements, and any amendments to those reports. All such information is available free of charge. Our Investor Relations website allows interested persons to sign up to automatically receive e-mail alerts when we post financial information and issue press releases, and to receive information about upcoming events. We encourage interested persons to follow our Investor Relations website in addition to our filings with the SEC to timely receive information about the company.

Intel, the Intel logo, Intel Core, and Altera are trademarks of Intel Corporation or its subsidiaries in the US and/or other countries.

* Other names and brands may be claimed as the property of others.

| 2 | |||||||

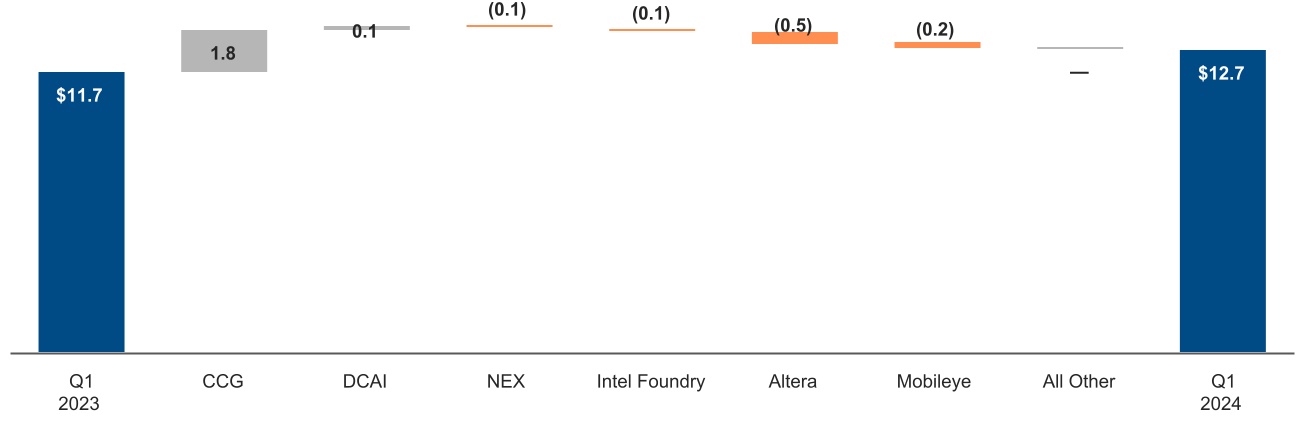

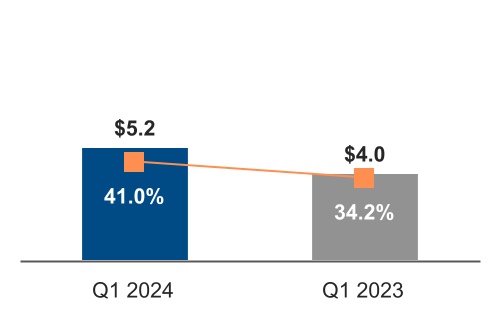

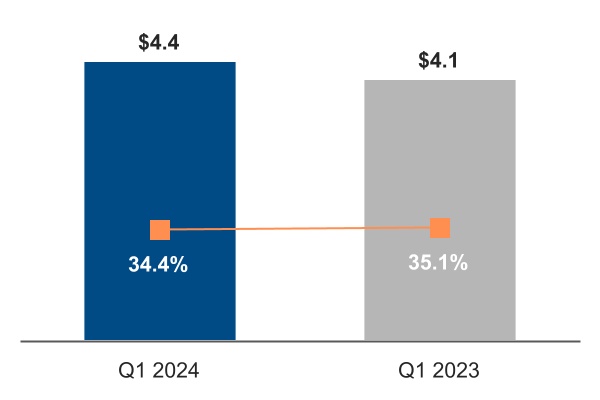

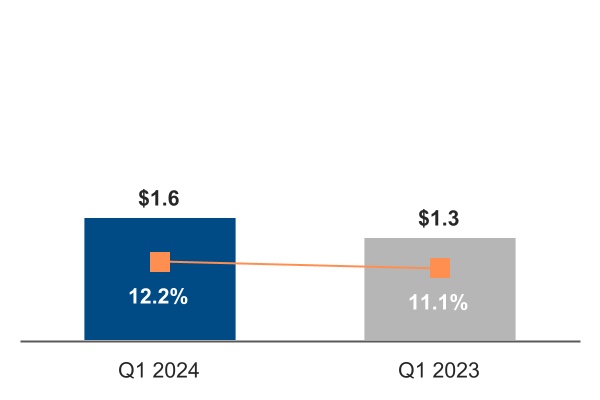

A Quarter in Review | |||||

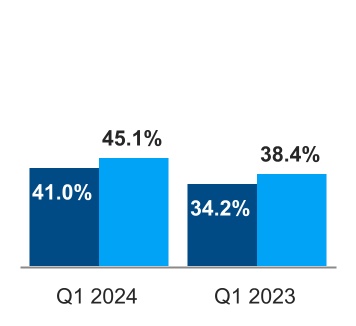

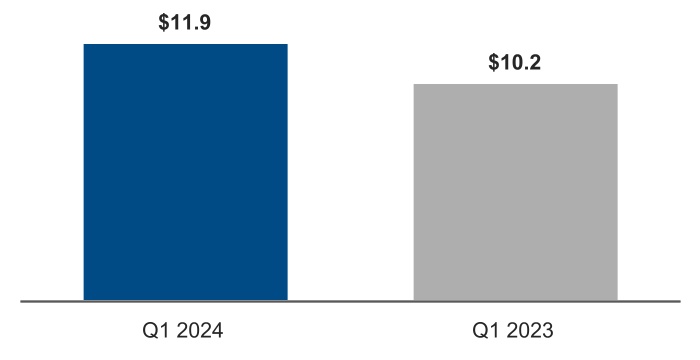

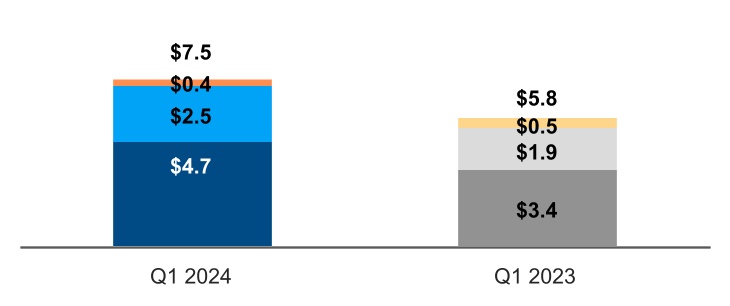

Total revenue of $12.7 billion was up $1.0 billion or 9% from Q1 2023, as CCG revenue increased 31%, DCAI revenue increased 5%, and NEX revenue decreased 8%. CCG revenue increased primarily due to higher notebook and desktop volumes as customer inventory levels normalized compared to higher levels in Q1 2023. DCAI revenue increased due to higher server ASPs primarily due to a lower mix of hyperscale customer-related revenue and a higher mix of high core count products, partially offset by lower server volume due to lower demand in a competitive environment and a higher mix of high core count products. NEX revenue decreased primarily due to 5G customers tempering purchases to reduce existing inventories, partially offset by higher Edge and Network revenue. Altera, an Intel Company (previously Intel's Programmable Solutions Group) and Mobileye revenue decreased as customers tempered purchases to reduce existing inventories.

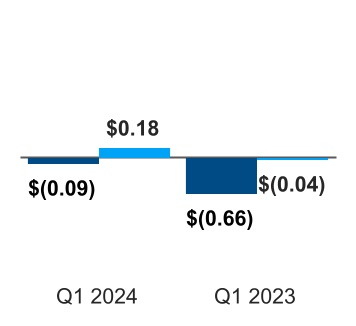

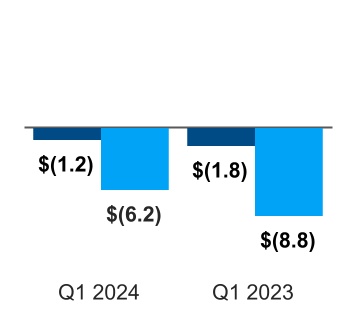

| Revenue | Gross Margin | Diluted EPS attributable to Intel | Cash Flows | |||||||||||||||||

■ GAAP $B | ■ GAAP ■ Non-GAAP | ■ GAAP ■ Non-GAAP | ■ Operating Cash Flow $B ■ Adjusted Free Cash Flow $B | |||||||||||||||||

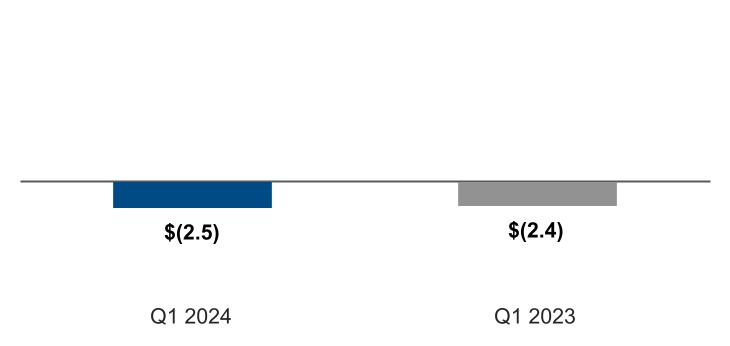

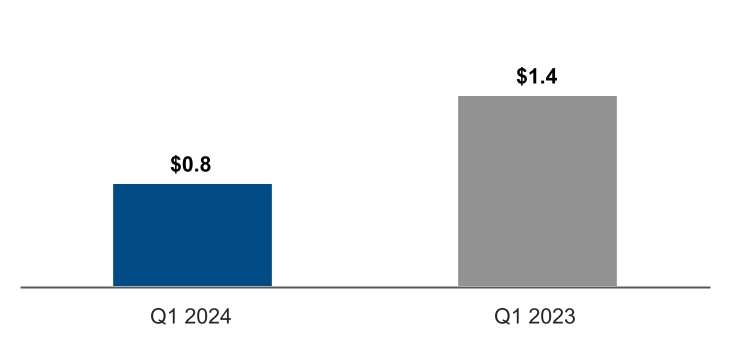

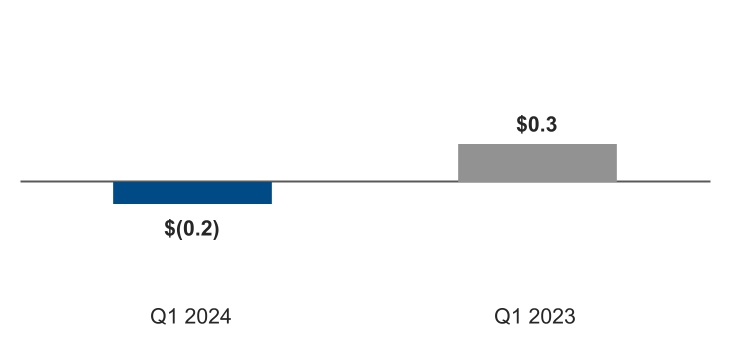

| $12.7B | 41.0% | 45.1% | $(0.09) | $0.18 | $(1.2)B | $(6.2)B | ||||||||||||||||||||||||||||||||||||||

| GAAP | GAAP | non-GAAP1 | GAAP | non-GAAP1 | GAAP | non-GAAP1 | ||||||||||||||||||||||||||||||||||||||

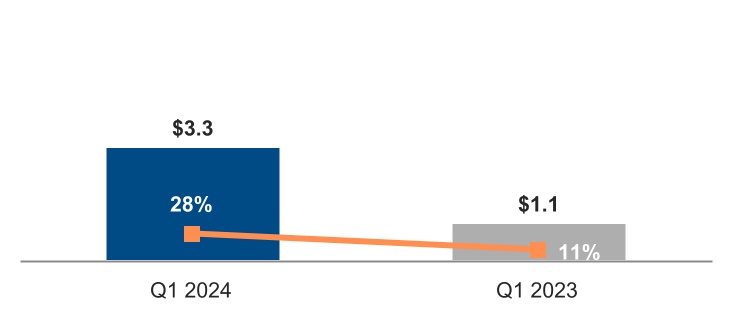

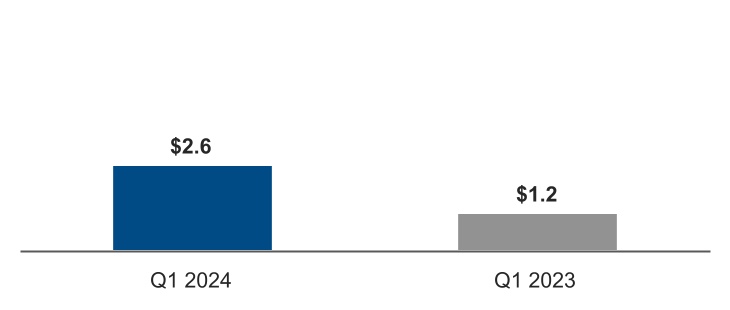

| Revenue up $1.0B or 9% from Q1 2023 | Gross margin up 6.8 ppts from Q1 2023 | Gross margin up 6.7 ppts from Q1 2023 | Diluted EPS attributable to Intel up $0.57 or 86% from Q1 2023 | Diluted EPS attributable to Intel up $0.22 from Q1 2023 | Operating cash flow up $0.6B or 31% from Q1 2023 | Adjusted free cash flow up $2.6B or 30% from Q1 2023 | ||||||||||||||||||||||||||||||||||||||

Higher CCG revenue. | Higher GAAP gross margin from higher revenue and lower period charges, partially offset by higher unit cost. | Higher GAAP EPS attributable to Intel from higher gross margin and a tax benefit compared to a tax expense in Q1 2023, partially offset by higher operating expenses. | Lower cash used for operating activities driven primarily by a reduced net operating loss, partially offset by certain cash unfavorable changes in working capital. | |||||||||||||||||||||||||||||||||||||||||

Key Developments

▪We launched Intel Foundry as a more sustainable systems foundry business designed for the AI era and announced an expanded process roadmap, which includes evolutions for Intel 3, Intel 18A, and Intel 14A process technologies.

▪The U.S. Department of Commerce has proposed up to $8.5 billion in direct funding and to make up to $11.0 billion in loans available under the CHIPS and Science Act to help advance our manufacturing and research and development projects at sites in Arizona, New Mexico, Ohio, and Oregon.

▪We launched Altera® as a new standalone FPGA company, in order to deliver programmable solutions and accessible AI across a broad range of applications in the cloud, network, and edge markets.

▪We opened Fab 9 in New Mexico, producing the world's most advanced packaging solutions at scale.

1 See "Non-GAAP Financial Measures" within MD&A.

| A Quarter in Review | 3 | ||||||

Consolidated Condensed Statements of Income | |||||

| Three Months Ended | ||||||||||||||

(In Millions, Except Per Share Amounts; Unaudited) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Net revenue | $ | $ | ||||||||||||

| Cost of sales | ||||||||||||||

| Gross margin | ||||||||||||||

| Research and development | ||||||||||||||

| Marketing, general, and administrative | ||||||||||||||

| Restructuring and other charges | ||||||||||||||

| Operating expenses | ||||||||||||||

| Operating income (loss) | ( | ( | ||||||||||||

| Gains (losses) on equity investments, net | ||||||||||||||

| Interest and other, net | ||||||||||||||

| Income (loss) before taxes | ( | ( | ||||||||||||

| Provision for (benefit from) taxes | ( | |||||||||||||

| Net income (loss) | ( | ( | ||||||||||||

| Less: Net income (loss) attributable to non-controlling interests | ( | ( | ||||||||||||

| Net income (loss) attributable to Intel | $ | ( | $ | ( | ||||||||||

| Earnings (loss) per share attributable to Intel—basic | $ | ( | $ | ( | ||||||||||

| Earnings (loss) per share attributable to Intel—diluted | $ | ( | $ | ( | ||||||||||

| Weighted average shares of common stock outstanding: | ||||||||||||||

| Basic | ||||||||||||||

| Diluted | ||||||||||||||

See accompanying notes.

| Financial Statements | Consolidated Condensed Statements of Income | 4 | ||||||||

Consolidated Condensed Statements of Comprehensive Income | |||||

| Three Months Ended | ||||||||||||||

(In Millions; Unaudited) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Net income (loss) | $ | ( | $ | ( | ||||||||||

| Changes in other comprehensive income (loss), net of tax: | ||||||||||||||

| Net unrealized holding gains (losses) on derivatives | ( | |||||||||||||

| Actuarial valuation and other pension benefits (expenses), net | ||||||||||||||

| Translation adjustments and other | ||||||||||||||

| Other comprehensive income (loss) | ( | |||||||||||||

| Total comprehensive income (loss) | ( | ( | ||||||||||||

| Less: comprehensive income (loss) attributable to non-controlling interests | ( | ( | ||||||||||||

| Total comprehensive income (loss) attributable to Intel | $ | ( | $ | ( | ||||||||||

See accompanying notes.

| Financial Statements | Consolidated Condensed Statements of Comprehensive Income | 5 | ||||||||

Consolidated Condensed Balance Sheets | |||||

(In Millions; Unaudited) | Mar 30, 2024 | Dec 30, 2023 | ||||||||||||

| Assets | ||||||||||||||

| Current assets: | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Short-term investments | ||||||||||||||

| Accounts receivable, net | ||||||||||||||

| Inventories | ||||||||||||||

| Other current assets | ||||||||||||||

| Total current assets | ||||||||||||||

| Property, plant, and equipment, net of accumulated depreciation of $99,315 ($98,010 as of December 30, 2023) | ||||||||||||||

| Equity investments | ||||||||||||||

| Goodwill | ||||||||||||||

| Identified intangible assets, net | ||||||||||||||

| Other long-term assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

| Liabilities and stockholders’ equity | ||||||||||||||

| Current liabilities: | ||||||||||||||

| Short-term debt | $ | $ | ||||||||||||

| Accounts payable | ||||||||||||||

| Accrued compensation and benefits | ||||||||||||||

| Income taxes payable | ||||||||||||||

| Other accrued liabilities | ||||||||||||||

| Total current liabilities | ||||||||||||||

| Debt | ||||||||||||||

| Other long-term liabilities | ||||||||||||||

| Contingencies (Note 13) | ||||||||||||||

| Stockholders’ equity: | ||||||||||||||

| Common stock and capital in excess of par value, 4,257 issued and outstanding (4,228 issued and outstanding as of December 30, 2023) | ||||||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | ||||||||||||

| Retained earnings | ||||||||||||||

| Total Intel stockholders' equity | ||||||||||||||

| Non-controlling interests | ||||||||||||||

| Total stockholders' equity | ||||||||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||||||||

See accompanying notes.

| Financial Statements | Consolidated Condensed Balance Sheets | 6 | ||||||||

Consolidated Condensed Statements of Cash Flows | |||||

| Three Months Ended | ||||||||||||||

(In Millions; Unaudited) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Cash and cash equivalents, beginning of period | $ | $ | ||||||||||||

| Cash flows provided by (used for) operating activities: | ||||||||||||||

| Net income (loss) | ( | ( | ||||||||||||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||||||||

| Depreciation | ||||||||||||||

| Share-based compensation | ||||||||||||||

| Restructuring and other charges | ||||||||||||||

| Amortization of intangibles | ||||||||||||||

| (Gains) losses on equity investments, net | ( | ( | ||||||||||||

| Changes in assets and liabilities: | ||||||||||||||

| Accounts receivable | ||||||||||||||

| Inventories | ( | |||||||||||||

| Accounts payable | ( | ( | ||||||||||||

| Accrued compensation and benefits | ( | ( | ||||||||||||

| Income taxes | ( | |||||||||||||

| Other assets and liabilities | ( | ( | ||||||||||||

| Total adjustments | ( | |||||||||||||

| Net cash provided by (used for) operating activities | ( | ( | ||||||||||||

| Cash flows provided by (used for) investing activities: | ||||||||||||||

| Additions to property, plant, and equipment | ( | ( | ||||||||||||

| Proceeds from capital-related government incentives | ||||||||||||||

| Purchases of short-term investments | ( | ( | ||||||||||||

| Maturities and sales of short-term investments | ||||||||||||||

| Other investing | ( | |||||||||||||

| Net cash provided by (used for) investing activities | ( | ( | ||||||||||||

| Cash flows provided by (used for) financing activities: | ||||||||||||||

| Issuance of commercial paper, net of issuance costs | ||||||||||||||

| Repayment of commercial paper | ( | |||||||||||||

| Payments on finance leases | ( | |||||||||||||

| Partner contributions | ||||||||||||||

| Issuance of long-term debt, net of issuance costs | ||||||||||||||

| Proceeds from sales of common stock through employee equity incentive plans | ||||||||||||||

| Payment of dividends to stockholders | ( | ( | ||||||||||||

| Other financing | ( | ( | ||||||||||||

| Net cash provided by (used for) financing activities | ||||||||||||||

| Net increase (decrease) in cash and cash equivalents | ( | ( | ||||||||||||

| Cash and cash equivalents, end of period | $ | $ | ||||||||||||

| Supplemental disclosures: | ||||||||||||||

| Acquisition of property, plant, and equipment included in accounts payable and accrued liabilities | $ | $ | ||||||||||||

| Cash paid during the period for: | ||||||||||||||

| Interest, net of capitalized interest | $ | $ | ||||||||||||

| Income taxes, net of refunds | $ | $ | ||||||||||||

See accompanying notes.

| Financial Statements | Consolidated Condensed Statements of Cash Flows | 7 | ||||||||

Consolidated Condensed Statements of Stockholders' Equity | |||||

| (In Millions, Except Per Share Amounts; Unaudited) | Common Stock and Capital in Excess of Par Value | Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Non-Controlling Interests | Total | |||||||||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||||||||

| Three Months Ended | ||||||||||||||||||||||||||||||||||||||

| Balance as of December 30, 2023 | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||

| Net proceeds from partner contributions | — | — | — | |||||||||||||||||||||||||||||||||||

| Employee equity incentive plans and other | — | — | — | |||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | |||||||||||||||||||||||||||||||||||

| Restricted stock unit withholdings | ( | ( | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Cash dividends declared ($0.13 per share of common stock) | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Balance as of March 30, 2024 | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Balance as of December 31, 2022 | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Net proceeds from partner contributions | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Employee equity incentive plans and other | — | — | — | |||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | |||||||||||||||||||||||||||||||||||

| Restricted stock unit withholdings | ( | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Cash dividends declared ($0.49 per share of common stock) | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Balance as of April 1, 2023 | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||

See accompanying notes.

| Financial Statements | Consolidated Condensed Statements of Stockholders' Equity | 8 | ||||||||

Notes to Consolidated Condensed Financial Statements | |||||

| Note 1 : | Basis of Presentation | ||||

We prepared our interim Consolidated Condensed Financial Statements that accompany these notes in conformity with US GAAP, consistent in all material respects with those applied in our 2023 Form 10-K.

We have made estimates and judgments affecting the amounts reported in our Consolidated Condensed Financial Statements and the accompanying notes. The actual results that we experience may differ materially from our estimates. The interim financial information is unaudited, and reflects all normal adjustments that are, in our opinion, necessary to provide a fair statement of results for the interim periods presented. This report should be read in conjunction with our 2023 Form 10-K where we include additional information on our critical accounting estimates, policies, and the methods and assumptions used in our estimates.

| Note 2 : | Operating Segments | ||||

We previously announced the implementation of our internal foundry operating model, which took effect in the first quarter of 2024, and creates a foundry relationship between our Intel Products business (collectively CCG, DCAI, and NEX) and our Intel Foundry business. Intel Products consists substantially of design and development of CPUs and related solutions for third party customers. Intel Foundry consists substantially of process engineering, manufacturing, and foundry services groups that provide manufacturing, test, and assembly services to our Intel Products business and to third party customers. Both businesses utilize marketing, sales, and other support functions.

Our internal foundry model is a key component of our strategy and is designed to reshape our operational dynamics and drive greater transparency, accountability, and focus on costs and efficiency. We also previously announced our intent to operate Altera, an Intel Company (previously Intel's Programmable Solutions Group), as a standalone business, with segment reporting beginning in the first quarter of 2024. Altera was previously included in our DCAI segment results. As a result of these changes, we modified our segment reporting in the first quarter of 2024 to align to this new operating model. All prior period segment data has been retrospectively adjusted to reflect the way our Chief Operating Decision Maker (CODM) internally receives information and manages and monitors our operating segment performance starting in fiscal year 2024. There are no changes to our consolidated financial statements for any prior periods.

We organize our business as follows:

▪Intel Products:

▪Client Computing Group (CCG)

▪Data Center and AI (DCAI)

▪Network and Edge (NEX)

▪Intel Foundry

▪All other

▪Altera

▪Mobileye

▪Other

CCG, DCAI, and Intel Foundry qualify as reportable operating segments. NEX, Altera, and Mobileye do not qualify as reportable operating segments; however, we have elected to disclose their results. When we enter into federal contracts, they are aligned to the sponsoring operating segment.

The accounting policies for our segment reporting are the same for Intel as a whole. A summary of the basis for which we report our operating segment revenues and operating margin is as follows:

Intel Products: CCG, DCAI, and NEX

▪Segment revenue: consists of revenues from third party customers. The Intel Products operating segments represent a substantial majority of Intel consolidated revenue and are derived from our principal products that incorporate various components and technologies, including a microprocessor and chipset, a stand-alone SoC, or a multichip package, which are based on Intel architecture.

▪Segment expenses: consists of intersegment charges for product manufacturing and related services from Intel Foundry, external foundry and other manufacturing, product development costs, allocated expenses as described below, and direct operating expenses.

| Financial Statements | Notes to Financial Statements | 9 | ||||||||

Intel Foundry

▪Segment revenue: consists substantially of intersegment product and services revenue for wafer fabrication and related products and services sold to Intel Products, Altera, and certain other Intel internal businesses. We recognize intersegment revenue when we satisfy performance obligations as evidenced by the transfer of control of Intel Foundry products and services to the Intel Products businesses, which is generally at the completion of wafer sorting and at the completion of assembly and test services. Intersegment sales are recorded at prices that are intended to approximate market pricing. Intel Foundry also includes certain third party foundry and assembly and test revenues from external customers that were $27 million in first three months of 2024 and $118 million in the first three months of 2023.

▪Segment expenses: consists of direct expenses for technology development, product manufacturing and services provided by Intel Foundry to internal and external customers, allocated expenses as described below, and direct operating expenses. Direct expenses for product manufacturing includes excess capacity charges that were previously allocated primarily to CCG, DCAI, and NEX.

All other: Altera & Mobileye

▪Segment revenue: consists of product revenues from third party customers. Altera revenue is derived from programmable semiconductors, primarily FPGAs, CPLDs, acceleration platforms, software, IP, and related products. Mobileye revenue is derived from advanced driver-assistance systems (ADAS) and autonomous driving technologies and solutions.

▪Segment expenses: Altera expenses consist of intersegment charges for product manufacturing and related services from Intel Foundry, third party manufacturing, allocated expenses as described below, and direct operating expenses. Mobileye expenses consists of third party direct expenses for product manufacturing and related services for the manufacturing of Mobileye products and direct operating expenses.

Our "all other" category also consists of "other", which includes:

▪results of operations from non-reportable segments not otherwise presented, and from start-up businesses that support our initiatives; and

▪historical results of operations from divested businesses.

We allocate operating expenses from our sales and marketing group to the Intel Products operating segments, and allocate operating expenses from our finance and administration groups to all of our operating segments, except Mobileye. Previously, operating expense from all of these groups as well as manufacturing and engineering, were generally allocated to all the operating segments, except Mobileye.

We estimate that the substantial majority of our consolidated depreciation expense was incurred by Intel Foundry in the first three months of 2024 and in the first three months of 2023. Intel Foundry depreciation expense is substantially included in overhead cost pools and then combined with other costs, and subsequently absorbed into inventory as each product passes through the manufacturing process and is sold to Intel Products and other customers. As a result, it is impractical to determine the total depreciation expense included as a component of each Intel Products operating segment's operating income (loss) results.

We do not allocate to our operating segments corporate operating expenses that primarily consist of:

▪restructuring and other charges;

▪share-based compensation;

▪certain impairment charges; and

▪certain acquisition-related costs, including amortization and any impairment of acquisition-related intangibles and goodwill.

We do not allocate to our operating segments non-operating items such as:

▪gains and losses from equity investments;

▪interest and other income; and

▪income taxes.

The CODM, who is our CEO, allocates resources to and assesses the performance of each operating segment using information about the operating segment's revenue and operating income (loss). Although the CODM uses operating income (loss) to evaluate the segments, operating costs included in one segment may benefit other segments. The measures regularly provided to and used by our CODM under our new operating model continue to evolve; currently, our CODM does not regularly review or receive discrete asset information by segment.

Intersegment eliminations: Intersegment sales and related gross margin on inventory recorded at the end of the period or sold through to third party customers is eliminated for consolidation purposes. The Intel Products operating segments and Intel Foundry are meant to reflect separate fabless semiconductor and foundry companies. Thus certain intersegment activity is captured within the intersegment eliminations upon consolidation and presented at the Intel consolidated level. This activity primarily relates to inventory reserves which are determined and recorded based on our accounting policies for Intel as a whole, but are only recorded by the Intel Products operating segments upon transfer of inventory from Intel Foundry. If a reserve is identified prior to the related inventory transferring to Intel Products, that reserve is presented as activity within the intersegment eliminations.

| Financial Statements | Notes to Financial Statements | 10 | ||||||||

Reporting units and goodwill reallocation: As a result of modifying our segment reporting in the first quarter of 2024, we reallocated goodwill among our affected reporting units on a relative fair value basis. We performed a quantitative goodwill impairment assessment for each of our reporting units immediately before and after our business reorganization. We concluded based on our pre-reorganization impairment test that goodwill was not impaired. As a result of our post-reorganization impairment test, we recognized a non-cash goodwill impairment loss of $222 million in the first three months of 2024 related to our new Intel Foundry reporting unit as the estimated fair value of the new reporting unit was lower than the assigned carrying value, which now includes substantially all of our allocated property, plant, and equipment. The Intel Foundry reporting unit has no remaining goodwill. The fair value substantially exceeded the carrying value for all remaining reporting units tested as part of our post-reorganization impairment test.

Operating segment and consolidated net revenue and operating income (loss) for each period were as follows:

| Three Months Ended | ||||||||||||||

| (In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Operating segment revenue: | ||||||||||||||

Intel Products: | ||||||||||||||

Client Computing Group | ||||||||||||||

Desktop | $ | $ | ||||||||||||

Notebook | ||||||||||||||

Other | ||||||||||||||

Data Center and AI | ||||||||||||||

Network and Edge | ||||||||||||||

| Total Intel Products revenue | $ | $ | ||||||||||||

| Intel Foundry | $ | $ | ||||||||||||

All other | ||||||||||||||

Altera | ||||||||||||||

Mobileye | ||||||||||||||

Other | ||||||||||||||

Total all other revenue | ||||||||||||||

Total operating segment revenue | $ | $ | ||||||||||||

Intersegment eliminations | ( | ( | ||||||||||||

| Total net revenue | $ | $ | ||||||||||||

Segment operating income (loss): | ||||||||||||||

Intel Products: | ||||||||||||||

Client Computing Group | $ | $ | ||||||||||||

Data Center and AI | ||||||||||||||

Network and Edge | ( | |||||||||||||

Total Intel Products operating income (loss) | $ | $ | ||||||||||||

| Intel Foundry | $ | ( | $ | ( | ||||||||||

All Other | ||||||||||||||

Altera | ( | |||||||||||||

Mobileye | ( | |||||||||||||

Other | ( | ( | ||||||||||||

Total all other operating income (loss) | ( | |||||||||||||

| Total segment operating income (loss) | $ | $ | ( | |||||||||||

Intersegment eliminations | ||||||||||||||

Corporate unallocated expenses | ( | ( | ||||||||||||

| Total operating income (loss) | $ | ( | $ | ( | ||||||||||

| Financial Statements | Notes to Financial Statements | 11 | ||||||||

Corporate Unallocated Expenses

Corporate unallocated expenses represent costs incurred that are not directly attributed to an operating segment. The nature of these expenses may vary, but primarily consist of restructuring and other charges, share-based compensation, certain impairment charges, and certain acquisition-related costs.

| Three Months Ended | ||||||||||||||

(In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Acquisition-related adjustments | $ | ( | $ | ( | ||||||||||

| Share-based compensation | ( | ( | ||||||||||||

| Restructuring and other charges | ( | ( | ||||||||||||

| Other | ( | |||||||||||||

Total corporate unallocated expenses | $ | ( | $ | ( | ||||||||||

| Note 3 : | Non-Controlling Interests | ||||

| Mar 30, 2024 | Dec 30, 2023 | |||||||||||||||||||||||||

(In Millions) | Non-Controlling Interests | Non-Controlling Ownership % | Non-Controlling Interests | Non-Controlling Ownership % | ||||||||||||||||||||||

Arizona Fab LLC | $ | % | $ | % | ||||||||||||||||||||||

Mobileye | % | % | ||||||||||||||||||||||||

IMS Nanofabrication | % | % | ||||||||||||||||||||||||

Non-controlling interests | $ | $ | ||||||||||||||||||||||||

Semiconductor Co-Investment Program

In 2022, we closed a transaction with Brookfield Asset Management (Brookfield) resulting in the formation of Arizona Fab LLC (Arizona Fab). We consolidate the results of Arizona Fab, a VIE, into our consolidated financial statements because we are the primary beneficiary. Generally, contributions will be made to, and distributions will be received from Arizona Fab based on both parties' proportional ownership. We will be the sole operator and main beneficiary of two new chip factories that will be constructed by Arizona Fab, and we will have the right to purchase 100 % of the related factory output. Once production commences, we will be required to operate Arizona Fab at minimum production levels measured in wafer starts per week and will be required to limit excess inventory held on site or we will be subject to certain penalties.

We have an unrecognized commitment to fund our respective share of the total construction costs of Arizona Fab of $29.0 billion.

As of March 30, 2024, substantially all of the assets of Arizona Fab consisted of property, plant, and equipment. The assets held by Arizona Fab, which can be used only to settle obligations of the VIE and are not available to us, were $5.6 billion as of March 30, 2024 ($4.8 billion as of December 30, 2023).

Mobileye

In 2022, Mobileye completed its IPO and certain other equity financing transactions. During 2023, we converted 38.5 million of our Mobileye Class B shares into Class A shares, representing 5 % of Mobileye's outstanding capital stock, and subsequently sold the Class A shares for $42 per share as part of a secondary offering, receiving net proceeds of $1.6 billion and increasing our capital in excess of par value by $663 million, net of tax. We continue to consolidate the results of Mobileye into our consolidated financial statements.

IMS Nanofabrication

| Financial Statements | Notes to Financial Statements | 12 | ||||||||

| Note 4 : | Earnings (Loss) Per Share | ||||

We computed basic earnings (loss) per share of common stock based on the weighted average number of shares of common stock outstanding during the period. We computed diluted earnings (loss) per share of common stock based on the weighted average number of shares of common stock outstanding plus potentially dilutive shares of common stock outstanding during the period.

| Three Months Ended | ||||||||||||||

| (In Millions, Except Per Share Amounts) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Net income (loss) | $ | ( | $ | ( | ||||||||||

| Less: Net income (loss) attributable to non-controlling interests | ( | ( | ||||||||||||

| Net income (loss) attributable to Intel | ( | ( | ||||||||||||

| Weighted average shares of common stock outstanding—basic | ||||||||||||||

| Weighted average shares of common stock outstanding—diluted | ||||||||||||||

| Earnings (loss) per share attributable to Intel—basic | $ | ( | $ | ( | ||||||||||

| Earnings (loss) per share attributable to Intel—diluted | $ | ( | $ | ( | ||||||||||

Potentially dilutive shares of common stock from employee equity incentive plans are determined by applying the treasury stock method to the assumed exercise of outstanding stock options, the assumed vesting of outstanding RSUs, and the assumed issuance of common stock under the stock purchase plan.

Due to our net losses in the three months ended March 30, 2024 and April 1, 2023, the assumed exercise of outstanding stock options, the assumed vesting of outstanding RSUs, and the assumed issuance of common stock under the stock purchase plan had an anti-dilutive effect on diluted loss per share for the period and were excluded from the computation of diluted loss per share.

| Note 5 : | Other Financial Statement Details | ||||

Accounts Receivable

We sell certain of our accounts receivable on a non-recourse basis to third-party financial institutions. We record these transactions as sales of receivables and present cash proceeds as cash provided by operating activities in the Consolidated Condensed Statements of Cash Flows. Accounts receivable sold under non-recourse factoring arrangements were $500 million during the first three months of 2024 ($500 million in the first three months of 2023). After the sale of our accounts receivable, we expect to collect payment from the customers and remit it to the third-party financial institution.

Inventories

(In Millions) | Mar 30, 2024 | Dec 30, 2023 | ||||||||||||

Raw materials | $ | $ | ||||||||||||

Work in process | ||||||||||||||

Finished goods | ||||||||||||||

| Total inventories | $ | $ | ||||||||||||

Other Accrued Liabilities

Other accrued liabilities include deferred compensation of $2.9 billion as of March 30, 2024 ($2.9 billion as of December 30, 2023).

Interest and Other, Net

| Three Months Ended | ||||||||||||||

(In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

Interest income | $ | $ | ||||||||||||

Interest expense | ( | ( | ||||||||||||

Other, net | ||||||||||||||

| Total interest and other, net | $ | $ | ||||||||||||

Interest expense is net of $363 million of interest capitalized in the first three months of 2024 ($363 million in the first three months of 2023).

| Financial Statements | Notes to Financial Statements | 13 | ||||||||

| Note 6 : | Restructuring and Other Charges | ||||

| Three Months Ended | ||||||||||||||

| (In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Employee severance and benefit arrangements | $ | $ | ( | |||||||||||

| Litigation charges and other | ||||||||||||||

| Asset impairment charges | ||||||||||||||

| Total restructuring and other charges | $ | $ | ||||||||||||

Employee severance and benefit arrangements includes a charge of $129 million in the first quarter of 2024 relating to actions taken to streamline operations and to reduce costs. We expect these actions to be substantially completed by the third quarter of 2024, but this is subject to change. Any changes to the estimates or timing will be reflected in our results of operations.

Asset impairment charges includes a goodwill impairment loss of $222 million in the first quarter of 2024 related to our new Intel Foundry reporting unit. Refer to "Note 2: Operating Segments" within Notes to Consolidated Condensed Financial Statements for further information on our business reorganization and goodwill impairment.

| Note 7 : | Income Taxes | ||||

| Three Months Ended | ||||||||||||||

(In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

| Income (loss) before taxes | $ | ( | $ | ( | ||||||||||

| Provision for (benefit from) taxes | $ | ( | $ | |||||||||||

Effective tax rate | % | ( | % | |||||||||||

Our provision for, or benefit from, income taxes for an interim period has historically been determined using an estimated annual effective tax rate, adjusted for discrete items, if any. Under certain circumstances where we are unable to make a reliable estimate of the annual effective tax rate, we use the actual effective tax rate for the year-to-date period. During the first quarter of 2024, we used the actual effective tax rate approach due to the variability of the rate as a result of fluctuations in forecasted income and the effects of being taxed in multiple tax jurisdictions.

| Note 8 : | Investments | ||||

Short-term Investments

Short-term investments include marketable debt investments in corporate debt, government debt, and financial institution instruments, and are recorded within cash and cash equivalents and short-term investments on the Consolidated Condensed Balance Sheets. Government debt includes instruments such as non-US government bills and bonds and US agency securities. Financial institution instruments include instruments issued or managed by financial institutions in various forms, such as commercial paper, fixed- and floating-rate bonds, money market fund deposits, and time deposits. As of March 30, 2024, and December 30, 2023, substantially all time deposits were issued by institutions outside the US.

For certain of our marketable debt investments, we economically hedge market risks at inception with a related derivative instrument or the marketable debt investment itself is used to economically hedge currency exchange rate risk from remeasurement. These hedged investments are reported at fair value with gains or losses from the investments and the related derivative instruments recorded in interest and other, net. The fair value of our hedged investments was $13.8 billion as of March 30, 2024 ($17.1 billion as of December 30, 2023). For hedged investments still held at the reporting date, we recorded net losses of $307 million in the first three months of 2024 ($90 million of net gains in the first three months of 2023). We recorded net gains on the related derivatives of $345 million in the first three months of 2024 ($102 million of net losses in the first three months of 2023).

Our remaining unhedged marketable debt investments are reported at fair value, with unrealized gains or losses, net of tax, recorded in accumulated other comprehensive income (loss) and realized gains or losses recorded in interest and other, net. The adjusted cost of our unhedged investments was $4.0 billion as of March 30, 2024 ($4.7 billion as of December 30, 2023), which approximated the fair value for these periods.

| Financial Statements | Notes to Financial Statements | 14 | ||||||||

The fair value of marketable debt investments, by contractual maturity, as of March 30, 2024, was as follows:

| (In Millions) | Fair Value | |||||||

Due in 1 year or less | $ | |||||||

Due in 1–2 years | ||||||||

Due in 2–5 years | ||||||||

Due after 5 years | ||||||||

Instruments not due at a single maturity date1 | ||||||||

| Total | $ | |||||||

Equity Investments

| (In Millions) | Mar 30, 2024 | Dec 30, 2023 | ||||||||||||

Marketable equity securities1 | $ | $ | ||||||||||||

Non-marketable equity securities | ||||||||||||||

Equity method investments | ||||||||||||||

| Total | $ | $ | ||||||||||||

1 Approximately 90 % of our marketable equity securities are subject to trading-volume or market-based restrictions, which limit the number of shares we may sell in a specified period of time, impacting our ability to liquidate these investments. Certain of the trading volume restrictions generally apply for as long as we own more than 1 % of the outstanding shares. Market-based restrictions result from the rules of the respective exchange.

The components of gains (losses) on equity investments, net for each period were as follows:

| Three Months Ended | ||||||||||||||

(In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

Ongoing mark-to-market adjustments on marketable equity securities | $ | ( | $ | |||||||||||

Observable price adjustments on non-marketable equity securities | ||||||||||||||

Impairment charges | ( | ( | ||||||||||||

Sale of equity investments and other1 | ||||||||||||||

| Total gains (losses) on equity investments, net | $ | $ | ||||||||||||

1 Sale of equity investments and other includes initial fair value adjustments recorded upon a security becoming marketable, realized gains (losses) on sales of non-marketable equity investments and equity method investments, and our share of equity method investee gains (losses) and distributions.

| Note 9 : | Divestitures | ||||

NAND Memory Business

The NAND memory business included our NAND memory technology and manufacturing business (the NAND OpCo Business), which we deconsolidated upon closing the first phase of our sale agreement with SK hynix Inc (SK hynix) on December 29, 2021. We have a receivable within other current assets for the remaining proceeds of $2.0 billion, which remains outstanding as of March 30, 2024 and will be received upon the second closing of the transaction, expected to be in March 2025.

The wafer manufacturing and sale agreement includes incentives and penalties that are contingent on the cost of operation and output of the NAND OpCo Business. These incentives and penalties present a maximum exposure of up to $500 million annually, and $1.5 billion in the aggregate. We are currently in negotiations with SK hynix to update the operating plan of the NAND OpCo Business, which may impact the metrics associated with the incentives and penalties and our expectations of the performance of the NAND OpCo Business against those metrics.

We were reimbursed for costs that we incurred on behalf of the NAND OpCo Business for corporate function services, which include human resources, information technology, finance, supply chain, and other compliance requirements. We recorded a receivable related to these reimbursable costs due from the NAND OpCo Business, a deconsolidated entity, of $150 million within other current assets as of March 30, 2024 ($145 million recorded as of December 30, 2023).

| Financial Statements | Notes to Financial Statements | 15 | ||||||||

| Note 10 : | Borrowings | ||||

In the first quarter of 2024, we issued a total of $2.6 billion aggregate principal amount of senior notes. We also expanded both our 5-year $5.0 billion revolving credit facility agreement and our 364-day $5.0 billion credit facility agreement, to $7.0 billion and $8.0 billion, respectively, and the maturity dates were extended by one year to February 2029 and January 2025, respectively. The revolving credit facilities had no

We have an ongoing authorization from our Board of Directors to borrow up to $10.0 billion under our commercial paper program. We had $793 million of commercial paper outstanding as of March 30, 2024 (no commercial paper outstanding as of December 30, 2023).

Our senior fixed rate notes pay interest semiannually. We may redeem the fixed rate notes prior to their maturity at our option at specified redemption prices and subject to certain restrictions. The obligations under our senior fixed rate notes rank equally in the right of payment with all of our other existing and future senior unsecured indebtedness and effectively rank junior to all liabilities of our subsidiaries.

| Note 11 : | Fair Value | ||||

Assets and Liabilities Measured and Recorded at Fair Value on a Recurring Basis

| Mar 30, 2024 | Dec 30, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Fair Value Measured and Recorded at Reporting Date Using | Fair Value Measured and Recorded at Reporting Date Using | |||||||||||||||||||||||||||||||||||||||||||||||||

(In Millions) | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash equivalents: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate debt | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Financial institution instruments¹ | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Reverse repurchase agreements | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Short-term investments: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate debt | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Financial institution instruments¹ | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Government debt² | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Other current assets: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivative assets | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Other long-term assets: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivative assets | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total assets measured and recorded at fair value | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Liabilities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Other accrued liabilities: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivative liabilities | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Other long-term liabilities: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivative liabilities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total liabilities measured and recorded at fair value | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

1Level 1 investments consist of money market funds. Level 2 investments consist primarily of certificates of deposit, time deposits, commercial paper, notes and bonds issued by financial institutions.

2Level 2 investments consist primarily of non-US government debt.

Assets Measured and Recorded at Fair Value on a Non-Recurring Basis

Our non-marketable equity securities, equity method investments, and certain non-financial assets—such as intangible assets, goodwill, and property, plant, and equipment—are recorded at fair value only if an impairment or observable price adjustment is recognized in the current period. If an observable price adjustment or impairment is recognized on our non-marketable equity securities during the period, we classify these assets as Level 3.

| Financial Statements | Notes to Financial Statements | 16 | ||||||||

Financial Instruments Not Recorded at Fair Value on a Recurring Basis

Financial instruments not recorded at fair value on a recurring basis include non-marketable equity securities and equity method investments that have not been remeasured or impaired in the current period, grants receivable, certain other receivables, and issued debt. We classify the fair value of grants receivable as Level 2. The estimated fair value of these financial instruments approximates their carrying value. The aggregate carrying value of grants receivable as of March 30, 2024 was $666 million (the aggregate carrying value as of December 30, 2023 was $559 million).

| Note 12 : | Derivative Financial Instruments | ||||

Volume of Derivative Activity

Total gross notional amounts for outstanding derivatives (recorded at fair value) at the end of each period were as follows:

(In Millions) | Mar 30, 2024 | Dec 30, 2023 | ||||||||||||

Foreign currency contracts | $ | $ | ||||||||||||

Interest rate contracts | ||||||||||||||

Other | ||||||||||||||

| Total | $ | $ | ||||||||||||

The total notional amount of outstanding pay-variable, receive-fixed interest rate swaps was $12.0 billion as of March 30, 2024 and December 30, 2023.

Fair Value of Derivative Instruments in the Consolidated Condensed Balance Sheets

| Mar 30, 2024 | Dec 30, 2023 | |||||||||||||||||||||||||

(In Millions) | Assets1 | Liabilities2 | Assets1 | Liabilities2 | ||||||||||||||||||||||

Derivatives designated as hedging instruments: | ||||||||||||||||||||||||||

Foreign currency contracts3 | $ | $ | $ | $ | ||||||||||||||||||||||

Interest rate contracts | ||||||||||||||||||||||||||

Total derivatives designated as hedging instruments | $ | $ | $ | $ | ||||||||||||||||||||||

Derivatives not designated as hedging instruments: | ||||||||||||||||||||||||||

Foreign currency contracts3 | $ | $ | $ | $ | ||||||||||||||||||||||

Interest rate contracts | ||||||||||||||||||||||||||

Equity contracts | ||||||||||||||||||||||||||

| Total derivatives not designated as hedging instruments | $ | $ | $ | $ | ||||||||||||||||||||||

| Total derivatives | $ | $ | $ | $ | ||||||||||||||||||||||

1Derivative assets are recorded as other assets, current and long-term.

2Derivative liabilities are recorded as other liabilities, current and long-term.

3A substantial majority of these instruments mature within 12 months.

| Financial Statements | Notes to Financial Statements | 17 | ||||||||

Amounts Offset in the Consolidated Condensed Balance Sheets

Agreements subject to master netting arrangements with various counterparties, and cash and non-cash collateral posted under such agreements at the end of each period were as follows:

| Mar 30, 2024 | ||||||||||||||||||||||||||||||||||||||

| Gross Amounts Not Offset in the Balance Sheet | ||||||||||||||||||||||||||||||||||||||

(In Millions) | Gross Amounts Recognized | Gross Amounts Offset in the Balance Sheet | Net Amounts Presented in the Balance Sheet | Financial Instruments | Cash and Non-Cash Collateral Received or Pledged | Net Amount | ||||||||||||||||||||||||||||||||

Assets: | ||||||||||||||||||||||||||||||||||||||

| Derivative assets subject to master netting arrangements | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

Reverse repurchase agreements | ( | |||||||||||||||||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||||||||||||||

| Derivative liabilities subject to master netting arrangements | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Total liabilities | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Dec 30, 2023 | ||||||||||||||||||||||||||||||||||||||

| Gross Amounts Not Offset in the Balance Sheet | ||||||||||||||||||||||||||||||||||||||

| (In Millions) | Gross Amounts Recognized | Gross Amounts Offset in the Balance Sheet | Net Amounts Presented in the Balance Sheet | Financial Instruments | Cash and Non-Cash Collateral Received or Pledged | Net Amount | ||||||||||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||||||||

| Derivative assets subject to master netting arrangements | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Reverse repurchase agreements | ( | |||||||||||||||||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||||||||||||||

| Derivative liabilities subject to master netting arrangements | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

| Total liabilities | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||

We obtain and secure available collateral from counterparties against obligations, including securities lending transactions and reverse repurchase agreements, when we deem it appropriate.

Derivatives in Cash Flow Hedging Relationships

The before-tax net gains or losses attributed to cash flow hedges recognized in other comprehensive income (loss) were $431 million net loss in the first three months of 2024 ($53 million net gains in the first three months of 2023). Substantially all of our cash flow hedges were foreign currency contracts for all periods presented.

During the first three months of 2024 and 2023, the amounts excluded from effectiveness testing were insignificant.

| Financial Statements | Notes to Financial Statements | 18 | ||||||||

Derivatives in Fair Value Hedging Relationships

The effects of derivative instruments designated as fair value hedges, recognized in interest and other, net for each period were as follows:

| Gains (Losses) on Derivatives Recognized in Consolidated Condensed Statements of Income | ||||||||||||||

| Three Months Ended | ||||||||||||||

(In Millions) | Mar 30, 2024 | Apr 1, 2023 | ||||||||||||

Interest rate contracts | $ | ( | $ | |||||||||||

Hedged items | ( | |||||||||||||

| Total | $ | $ | ||||||||||||

The amounts recorded on the Consolidated Condensed Balance Sheets related to cumulative basis adjustments for fair value hedges for each period were as follows:

| Line Item in the Consolidated Condensed Balance Sheets in Which the Hedged Item is Included | Carrying Amount of the Hedged Item Assets/(Liabilities) | Cumulative Amount of Fair Value Hedging Adjustment Included in the Carrying Amount Assets/(Liabilities) | ||||||||||||||||||||||||

(In Millions) | Mar 30, 2024 | Dec 30, 2023 | Mar 30, 2024 | Dec 30, 2023 | ||||||||||||||||||||||

| Long-term debt | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||

Derivatives Not Designated as Hedging Instruments

The effects of derivative instruments not designated as hedging instruments on the Consolidated Condensed Statements of Income for each period were as follows:

| Three Months Ended | ||||||||||||||||||||

(In Millions) | Location of Gains (Losses) Recognized in Income on Derivatives | Mar 30, 2024 | Apr 1, 2023 | |||||||||||||||||

Foreign currency contracts | Interest and other, net | $ | $ | |||||||||||||||||

Interest rate contracts | Interest and other, net | ( | ||||||||||||||||||

Other | Various | |||||||||||||||||||

| Total | $ | $ | ||||||||||||||||||

| Note 13 : | Contingencies | ||||

Legal Proceedings

We are regularly party to various ongoing claims, litigation, and other proceedings, including those noted in this section. We have accrued a charge of $1.0 billion related to litigation involving VLSI and a charge of $401 million related to an EC-imposed fine, both as described below. Excluding the VLSI claims, management at present believes that the ultimate outcome of these proceedings, individually and in the aggregate, will not materially harm our financial position, results of operations, cash flows, or overall trends; however, legal proceedings and related government investigations are subject to inherent uncertainties, and unfavorable rulings, excessive verdicts, or other events could occur. Unfavorable resolutions could include substantial monetary damages, fines, or penalties. Certain of these outstanding matters include speculative, substantial, or indeterminate monetary awards. In addition, in matters for which injunctive relief or other conduct remedies are sought, unfavorable resolutions could include an injunction or other order prohibiting us from selling one or more products at all or in particular ways, precluding particular business practices, or requiring other remedies. An unfavorable outcome may result in a material adverse impact on our business, results of operations, financial position, and overall trends. We might also conclude that settling one or more such matters is in the best interests of our stockholders, employees, and customers, and any such settlement could include substantial payments. Unless specifically described below, we have not concluded that settlement of any of the legal proceedings noted in this section is appropriate at this time.

| Financial Statements | Notes to Financial Statements | 19 | ||||||||

European Commission Competition Matter

In 2009, the EC found that we had used unfair business practices to persuade customers to buy microprocessors in violation of Article 82 of the EC Treaty (later renumbered Article 102) and Article 54 of the European Economic Area Agreement. In general, the EC found that we violated Article 82 by offering alleged “conditional rebates and payments” that required customers to purchase all or most of their x86 microprocessors from us and by making alleged “payments to prevent sales of specific rival products.” The EC ordered us to end the alleged infringement referred to in its decision and imposed a €1.1 billion fine, which we paid in the third quarter of 2009.

We appealed the EC decision to the European Court of Justice in 2014, after the General Court (then called the Court of First Instance) rejected our appeal of the EC decision in its entirety. In September 2017, the Court of Justice sent the case back to the General Court to examine whether the rebates at issue were capable of restricting competition. In January 2022, the General Court annulled the EC’s 2009 findings against us regarding rebates, as well as the €1.1 billion fine imposed on Intel, which was returned to us in February 2022. The General Court’s January 2022 decision did not annul the EC’s 2009 finding that we made payments to prevent sales of specific rival products.

In April 2022 the EC appealed the General Court’s decision to the Court of Justice. In addition, in September 2023 the EC imposed a €376 million ($401 million) fine against us based on its finding that we made payments to prevent sales of specific rival products. We have appealed the EC’s decision. We have accrued a charge for the fine and are unable to make a reasonable estimate of the potential loss or range of losses in excess of this amount given the procedural posture and the nature of these proceedings.

In a related matter, in April 2022 we filed applications with the General Court seeking an order requiring the EC to pay us approximately €593 million in default interest on the original €1.1 billion fine that was held by the EC for 12 years, which applications have been stayed pending the EC’s appeal of the General Court’s January 2022 decision.

Litigation Related to Security Vulnerabilities

In June 2017, a Google research team notified Intel and other companies that it had identified security vulnerabilities, the first variants of which are now commonly referred to as “Spectre” and “Meltdown,” that affect many types of microprocessors, including our products. As is standard when findings like these are presented, we worked together with other companies in the industry to verify the research and develop and validate software and firmware updates for impacted technologies. In January 2018, information on the security vulnerabilities was publicly reported, before software and firmware updates to address the vulnerabilities were made widely available.

As of April 24, 2024, consumer class action lawsuits against us were pending in the US and Canada. The plaintiffs, who purport to represent various classes of purchasers of our products, generally claim to have been harmed by our actions and/or omissions in connection with Spectre, Meltdown, and other variants of this class of security vulnerabilities that have been identified since 2018, and assert a variety of common law and statutory claims seeking monetary damages and equitable relief. In the US, class action suits filed in various jurisdictions between 2018 and 2021 were consolidated for all pretrial proceedings in the US District Court for the District of Oregon, which entered final judgment in favor of Intel in July 2022 based on plaintiffs’ failure to plead a viable claim. The Ninth Circuit Court of Appeals affirmed the district court’s judgment in November 2023, ending the litigation. In November 2023, new plaintiffs filed a consumer class action complaint in the US District Court for the Northern District of California with respect to a further vulnerability variant disclosed in August 2023 and commonly referred to as “Downfall.” We moved to dismiss that complaint in January 2024. In Canada, an initial status conference has not yet been scheduled in one case relating to Spectre and Meltdown pending in the Superior Court of Justice of Ontario, and a stay of a second case pending in the Superior Court of Justice of Quebec is in effect. In a class action relating to Spectre and Meltdown previously pending in Argentina, plaintiffs’ appeal of a May 2023 order dismissing their complaint for lack of standing was denied in February 2024, ending the lawsuit. Additional lawsuits and claims may be asserted seeking monetary damages or other related relief. Given the procedural posture and the nature of these cases, including that the pending proceedings are in the early stages, that alleged damages have not been specified, that uncertainty exists as to the likelihood of a class or classes being certified or the ultimate size of any class or classes if certified, and that there are significant factual and legal issues to be resolved, we are unable to make a reasonable estimate of the potential loss or range of losses, if any, that might arise from these matters.

Litigation Related to 7nm Product Delay Announcement

Multiple securities class action lawsuits were filed in the US District Court for the Northern District of California against us and certain officers following our July 2020 announcement of 7nm product delays. The court consolidated the lawsuits and appointed lead plaintiffs in October 2020, and in January 2021 plaintiffs filed a consolidated complaint. Plaintiffs purport to represent all persons who purchased or otherwise acquired our common stock from October 25, 2019 through October 23, 2020, and they generally allege that defendants violated the federal securities laws by making false or misleading statements about the timeline for 7nm products. In March 2023, the district court granted the defendants’ motion to dismiss the consolidated complaint, and in April 2023 entered judgment. Plaintiffs appealed, and on April 19, 2024 the Ninth Circuit affirmed the judgment; the Ninth Circuit’s ruling is subject to appeal. Given the procedural posture and the nature of the case, including that it is in the early stages, that alleged damages have not been specified, that uncertainty exists as to the likelihood of a class being certified or the ultimate size of any class if certified, and that there are significant factual and legal issues to be resolved, we are unable to make a reasonable estimate of the potential loss or range of losses, if any, that might arise from the matter. In July 2021, we introduced a new process node naming structure, and the 7nm process is now called Intel 4.

| Financial Statements | Notes to Financial Statements | 20 | ||||||||

Litigation Related to Patent and IP Claims

We have had IP infringement lawsuits filed against us, including but not limited to those discussed below. Most involve claims that certain of our products, services, and technologies infringe others' IP rights. Adverse results in these lawsuits may include awards of substantial fines and penalties, costly royalty or licensing agreements, or orders preventing us from offering certain features, functionalities, products, or services. As a result, we may have to change our business practices, and develop non-infringing products or technologies, which could result in a loss of revenue for us and otherwise harm our business. In addition, certain agreements with our customers require us to indemnify them against certain IP infringement claims, which can increase our costs as a result of defending such claims, and may require that we pay significant damages, accept product returns, or supply our customers with non-infringing products if there were an adverse ruling in any such claims. In addition, our customers and partners may discontinue the use of our products, services, and technologies, as a result of injunctions or otherwise, which could result in loss of revenue and adversely affect our business.

VLSI Technology LLC v. Intel

In October 2017, VLSI Technology LLC (VLSI) filed a complaint against us in the US District Court for the Northern District of California alleging that various Intel FPGA and processor products infringe eight patents VLSI acquired from NXP Semiconductors, N.V. (NXP). Intel prevailed on all eight patents and the court entered final judgment in April 2024. Further appeals are possible. In April 2019, VLSI filed three infringement suits against us in the US District Court for the Western District of Texas accusing various of our processors of infringement of eight additional patents it had acquired from NXP:

▪The first Texas case went to trial in February 2021, and the jury awarded VLSI $1.5 billion for literal infringement of one patent and $675 million for infringement of another patent under the doctrine of equivalents. In April 2022, the court entered final judgment, awarding VLSI $2.1 billion in damages and approximately $162.3 million in pre-judgment and post-judgment interest. We appealed the judgment to the Federal Circuit Court of Appeals, including the court’s rejection of Intel’s claim to have a license from Fortress Investment Group’s acquisition of Finjan. The Federal Circuit Court heard oral argument in October 2023. In December 2023, the Federal Circuit reversed the finding of infringement as to the patent for which VLSI was awarded $675 million. The Federal Circuit affirmed the finding of infringement as to the patent for which VLSI had been awarded $1.5 billion, but vacated the damages award and sent the case back to the trial court for further damages proceedings on that patent. The Federal Circuit also ruled that Intel can advance the defense that it is licensed to VLSI’s patents. In December 2021 and January 2022 the Patent Trial and Appeal Board (PTAB) instituted Inter Partes Reviews (IPR) on the claims found to have been infringed in the first Texas case, and in May and June 2023 found all of those claims unpatentable; VLSI has appealed the PTAB’s decision. In March 2024, Intel filed a motion to stay the case pending appeals of the IPRs. In April 2024, Intel moved to add the defense that it is licensed to VLSI’s patents.

▪The second Texas case went to trial in April 2021, and the jury found that we do not infringe the asserted patents. VLSI had sought approximately $3.0 billion for alleged infringement, plus enhanced damages for willful infringement. The court has not yet entered final judgment.

▪The third Texas case went to trial in November 2022, with VLSI asserting one remaining patent. The jury found the patent valid and infringed, and awarded VLSI approximately $949 million in damages, plus interest and a running royalty. The court has not yet entered final judgment. In February 2023, we filed motions for a new trial and for judgment as a matter of law notwithstanding the verdict on various grounds. Further appeals are possible. In April 2024, Intel moved to add the defense that it is licensed to VLSI’s patents.