Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 29, 2012

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 0-14706

INGLES MARKETS, INCORPORATED

(Exact name of registrant as specified in its charter)

| North Carolina | 56-0846267 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 2913 U.S. Hwy. 70 West, Black Mountain, NC | 28711 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number including area code: (828) 669-2941

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Class A Common Stock, $0.05 par value | The NASDAQ Global Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO þ.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO þ.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES þ NO ¨ NOT APPLICABLE ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer þ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO þ.

As of March 23, 2012, the aggregate market value of voting stock held by non-affiliates of the registrant, based on the closing sales price of the Class A Common Stock on The NASDAQ Global Select Market on March 23, 2012, was approximately $234.6 million. As of December 20, 2012, the registrant had 12,957,150 shares of Class A Common Stock outstanding and 11,302,626 shares of Class B Common Stock outstanding.

Certain information required in Part III hereof is incorporated by reference to the Proxy Statement for the registrant’s 2013 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A no later than 120 days after the end of the fiscal year covered by this report.

Table of Contents

Annual Report on Form 10-K

September 29, 2012

2

Table of Contents

This Annual Report of Ingles Markets, Incorporated (“Ingles” or the “Company”) contains certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical fact included in this Annual Report, including the statements under “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and elsewhere regarding the Company’s strategy, future operations, financial position, estimated revenues, projected costs, projections, prospects and plans and objectives of management, are forward-looking statements. The words “expect,” “anticipate,” “intend,” “plan,” “likely,” “goal,” “believe,” “seek” and similar expressions are intended to identify forward-looking statements. While these forward-looking statements and the related assumptions are made in good faith and reflect the Company’s current judgment regarding the direction of the Company’s business, actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Such statements are based upon a number of assumptions and estimates which are inherently subject to significant risks and uncertainties, many of which are beyond the Company’s control. Some of these assumptions inevitably will not materialize, and unanticipated events will occur which will affect the Company’s results. Some important factors (but not necessarily all factors) that affect the Company’s revenues, growth strategies, future profitability and operating results, or that otherwise could cause actual results to differ materially from those expressed in or implied by any forward-looking statement, include:

| • | business and economic conditions generally in the Company’s operating area, including inflation or deflation expectations; |

| • | the Company’s ability to successfully implement our expansion and operating strategies; |

| • | pricing pressures and other competitive factors; |

| • | sudden or significant changes in the availability of gasoline and retail gasoline prices; |

| • | the maturation of new and expanded stores; |

| • | general concerns about food safety; |

| • | the Company’s ability to reduce costs and achieve improvements in operating results, including the effect of the new distribution facility opened during fiscal 2012; |

| • | the availability and terms of financing; |

| • | increases in costs, including food, utilities and other goods and services significant to the Company’s operations; |

| • | success or failure in the ownership and development of real estate; |

| • | changes in the laws and government regulations applicable to the Company; |

| • | other risks and uncertainties, including those described under the caption “Risk Factors.” |

Consequently, actual events affecting the Company and the impact of such events on the Company’s operations may vary significantly from those described in this Annual Report or contemplated or implied by statements in this Annual Report. Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included in this Annual Report are made only as of the date hereof. The Company does not undertake and specifically declines any obligation to update any such statements or to publicly announce the results of any revisions to any of such statements to reflect future events or developments.

3

Table of Contents

| Item 1. | BUSINESS |

General

Ingles Markets, Incorporated (“Ingles” or the “Company”), a leading supermarket chain in the southeast United States, operates 203 supermarkets in Georgia (74), North Carolina (69), South Carolina (36), Tennessee (21), Virginia (2) and Alabama (1).

The Company’s strategy is to locate its supermarkets primarily in suburban areas, small towns and neighborhood shopping centers. The Company remodels, expands and relocates stores in these communities and builds stores in new locations to retain and grow its customer base with an enhanced “one stop” product offering while retaining a high level of customer service and convenience. Ingles supermarkets offer customers a wide variety of nationally advertised food products, including grocery, meat and dairy products, produce, frozen foods and other perishables, and non-food products. Non-food products include fuel centers, pharmacies, health and beauty care products and general merchandise. The Company also offers quality private label items.

The Company believes that customer service and convenience, modern stores and competitive prices on a broad selection of quality merchandise are essential to developing and retaining a loyal customer base. The Company has an ongoing renovation and expansion plan to add stores in its target market and modernize the appearance and layout of its existing stores. The Company’s new and remodeled supermarkets provide an enhanced level of customer convenience in order to accommodate the lifestyle of today’s shoppers. Design features of the Company’s modern stores focus on selling high-growth, high-margin products including perishable departments featuring organic and home meal replacement items, in-store pharmacies, on-premises fuel centers, and an expanded selection of food and non-food items to provide a “one-stop” shopping experience.

Substantially all of the Company’s stores are located within 280 miles of its warehouse and distribution facilities, near Asheville, North Carolina. During fiscal year 2012, the Company completed construction of an additional 839,000 square foot warehouse and distribution facility adjacent to its current facility. Following the expansion, the warehouse supplies the stores with approximately 56% of the goods the Company sells. The remaining 44% is purchased from third parties and is generally delivered directly to the stores. The close proximity of the Company’s purchasing and distribution operations to its stores facilitates the timely distribution of consistently high quality meat, produce and other perishable items.

To further ensure product quality, the Company also owns and operates a milk processing and packaging plant that supplies approximately 83% of the milk products sold by the Company’s supermarkets as well as a variety of organic milk, fruit juices and bottled water products. In addition, the milk processing and packaging plant sells approximately 69% of its products to other retailers, food service distributors and grocery warehouses in 17 states, which provides the Company with an additional source of revenue.

Real estate ownership is an important component of the Company’s operations. The Company owns and operates 69 shopping centers, of which 57 contain an Ingles supermarket, and owns 95 additional properties that contain a free-standing Ingles store. Shopping center ownership provides tenant income and can enhance store traffic through the presence of additional products and services that complement grocery store operations. The Company also owns 12 undeveloped sites suitable for a free-standing store. The Company’s owned real estate is generally located in the same geographic region as its supermarkets.

The Company was founded by Robert P. Ingle, who served as the Company’s Chief Executive Officer until his death in March 2011. He was succeeded as Chief Executive Officer by his son, Robert P. Ingle II. As of September 29, 2012, Mr. Ingle II owned beneficially (as defined by the Exchange Act) approximately 87% of the combined voting power and 46% of the total number of shares of the Company’s outstanding Class A and Class B Common Stock (in each case including stock held by the Company’s Investment/Profit Sharing Plan and Trust of which Mr. Ingle II serves as one of the trustees). The Company became a publicly traded company in

4

Table of Contents

September 1987. The Company’s Class A Common Stock is traded on The NASDAQ Global Select Market under the symbol “IMKTA.” The Company’s Class B Common Stock is not publicly traded.

The Company was incorporated in 1965 under the laws of the State of North Carolina. Its principal mailing address is P.O. Box 6676, Highway 70, Asheville, North Carolina 28816, and its telephone number is 828-669-2941. The Company’s website is www.ingles-markets.com. Information on the Company’s website is not a part of and is not incorporated by reference into this Annual Report on Form 10-K. The Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments and supplements to these reports are available on the Company’s website as soon as reasonably practicable after they are filed with or furnished to the Securities and Exchange Commission.

Business

The Company operates three lines of business: retail grocery sales, shopping center rentals and a fluid dairy processing plant. Information about the Company’s operations by lines of business (in millions) is as follows (for information regarding the Company’s industry segments, see Note 11, “Lines of Business” to the Consolidated Financial Statements of this Annual Report on Form 10-K):

| Fiscal Year Ended September (dollars in millions) |

||||||||||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||||||

| Revenues from unaffiliated customers: |

||||||||||||||||||||||||

| Grocery sales |

$ | 3,577.5 | 96.2 | % | $ | 3,428.7 | 96.0 | % | $ | 3,274.0 | 96.3 | % | ||||||||||||

| Shopping center rentals |

8.9 | 0.2 | % | 9.1 | 0.3 | % | 9.2 | 0.3 | % | |||||||||||||||

| Fluid dairy |

131.9 | 3.6 | % | 131.2 | 3.7 | % | 116.0 | 3.4 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| $ | 3,718.3 | 100.0 | % | $ | 3,569.0 | 100.0 | % | $ | 3,399.2 | 100.0 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income from operations: |

||||||||||||||||||||||||

| Grocery sales |

$ | 111.5 | 90.0 | % | $ | 105.6 | 89.1 | % | $ | 96.3 | 88.0 | % | ||||||||||||

| Shopping center rentals |

1.4 | 1.2 | % | 1.9 | 1.6 | % | 1.8 | 1.6 | % | |||||||||||||||

| Fluid dairy |

10.9 | 8.8 | % | 11.0 | 9.3 | % | 11.4 | 10.4 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 123.8 | 100.0 | % | 118.5 | 100.0 | % | 109.5 | 100.0 | % | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

| Other income, net |

3.5 | 4.2 | 4.2 | |||||||||||||||||||||

| Interest expense |

60.0 | 62.0 | 64.9 | |||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

| Income before income taxes |

$ | 67.3 | $ | 60.7 | $ | 48.8 | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

Sales by product category for fiscal years 2012, 2011 and 2010, respectively, are as follows:

| Fiscal Year Ended September (dollars in millions) |

||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Grocery |

$ | 1,447.5 | $ | 1,397.9 | $ | 1,366.5 | ||||||

| Non-foods |

710.0 | 690.2 | 684.5 | |||||||||

| Perishables |

866.2 | 825.1 | 787.1 | |||||||||

| Gasoline |

553.8 | 515.5 | 435.9 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total grocery segment |

$ | 3,577.5 | $ | 3,428.7 | $ | 3,274.0 | ||||||

|

|

|

|

|

|

|

|||||||

The grocery category includes grocery, dairy and frozen foods.

The non-foods category includes alcoholic beverages, tobacco, pharmacy, health and video.

The perishables category includes meat, produce, deli and bakery.

5

Table of Contents

Supermarket Operations

The Company’s strategy is to locate its supermarkets primarily in suburban areas, small towns and rural communities. At September 29, 2012, the Company operated 194 supermarkets under the name “Ingles,” and 9 supermarkets under the name “Sav-Mor” with locations in western North Carolina, western South Carolina, northern Georgia, eastern Tennessee, southwestern Virginia and northeastern Alabama. The “Sav-Mor” store concept accommodates smaller shopping areas and carries dry groceries, dairy, fresh meat and produce, all of which are displayed in a modern, readily accessible environment.

The following table sets forth certain information with respect to the Company’s supermarket operations.

| Number of Supermarkets at Fiscal Year Ended September |

Percentage of Total Net Sales for Fiscal Year Ended September |

|||||||||||||||||||||||

| 2012 | 2011 | 2010 | 2012 | 2011 | 2010 | |||||||||||||||||||

| North Carolina |

69 | 69 | 69 | 38 | % | 38 | % | 39 | % | |||||||||||||||

| South Carolina |

36 | 36 | 36 | 19 | % | 19 | % | 19 | % | |||||||||||||||

| Georgia |

74 | 74 | 73 | 34 | % | 34 | % | 33 | % | |||||||||||||||

| Tennessee |

21 | 21 | 21 | 9 | % | 9 | % | 9 | % | |||||||||||||||

| Virginia |

2 | 2 | 2 | — | — | — | ||||||||||||||||||

| Alabama |

1 | 1 | 1 | — | — | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 203 | 203 | 202 | 100 | % | 100 | % | 100 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

The Company believes that today’s supermarket customers are focused on convenience, quality and value in an attractive store environment. As a result, the Company’s “one-stop” shopping experience combines a high level of customer service, convenience-oriented quality product offerings and low overall pricing. The Company’s modern stores provide products and services such as home meal replacement items, delicatessens, bakeries, floral departments, greeting cards and broad selections of organic, beverage and health-related items. At September 29, 2012, the Company operated 81 pharmacies and 72 fuel stations. The Company plans to continue to incorporate these departments in substantially all future new and remodeled stores. The Company trains its employees to provide friendly service and to actively address the needs of customers. These employees reinforce the Company’s distinctive service-oriented image.

Selected statistics on the Company’s supermarket operations are presented below:

| Fiscal Year Ended September | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Weighted Average Sales Per Store (000’s) (1) |

$ | 17,623 | $ | 16,698 | $ | 16,241 | $ | 15,744 | $ | 15,806 | ||||||||||

| Total Square Feet at End of Year (000’s) |

11,015 | 11,013 | 10,812 | 10,686 | 10,196 | |||||||||||||||

| Average Total Square Feet per Store |

54,262 | 54,252 | 53,524 | 53,432 | 51,756 | |||||||||||||||

| Average Square Feet of Selling Space per Store (2) |

37,984 | 37,977 | 37,467 | 37,403 | 36,229 | |||||||||||||||

| Weighted Average Sales per Square Foot of Selling Space (1) (2) |

464 | 437 | 434 | 425 | 448 | |||||||||||||||

| (1) | Weighted average sales per store include the effects of increases in square footage due to the opening of replacement stores and the expansion of stores through remodeling during the periods indicated, and gasoline sales. |

| (2) | Selling space is estimated to be 70% of total interior store square footage. |

Merchandising

The Company’s merchandising strategy is designed to create a comprehensive and satisfying shopping experience that blends value and customer service with variety, quality and convenience. Management believes

6

Table of Contents

that this strategy fosters a loyal customer base by establishing a reputation for providing high quality products and a variety of specialty departments.

The Company’s stores carry broad selections of quality meats, produce and other perishables. The Company offers a wide variety of fresh and non-perishable organic products, including organic milk produced by the Company’s fluid dairy plant. Management believes that supermarkets offering a broad array of products and time-saving services are perceived by customers as part of a solution to today’s lifestyle demands. Accordingly, a principal component of the Company’s merchandising strategy is to design stores that offer a “one-stop” shopping experience.

A selection of prepared foods and home meal replacements are featured throughout Ingles’ deli, bakery and meat departments to provide customers with easy meal alternatives that they can eat at home. Many stores offer daily selections of home meal replacement items, such as rotisserie chicken and pork, Italian foods, fried chicken, meat loaf and other entrees, sandwiches, pre-packaged salads, sushi and prepared fresh vegetables. The bakery offers an expanded selection of baked goods and self-service selections. Ingles bakes most of its items on site, including bread baked daily, cakes made to order in various sizes, donuts and other pastries. The deli offers salad, chicken wing and olive bars, an expanded offering of cheeses, gourmet items and home meal replacement items. The Company also provides its customers with an expanded selection of frozen food items (including organics) to meet the increasing demands of its customers.

The Company operates fuel stations at 72 of its store locations. The Company believes fuel stations give customers a competitive fuel choice and increase store traffic by allowing customers to consolidate trips. Most new and expanded stores are designed to include a fuel station on the store property. The Company also adds fuel stations at existing stores based on its evaluation of local competition, the potential effect on overall store profitability and the availability of space on the existing property or an adjacent outparcel.

Ingles intends to continue to increase sales of its private label brands, which typically carry higher margins than comparable branded products. Ingles’ private labels cover a broad range of products throughout the store, such as milk, bread, organic products, soft drinks and canned goods. In addition to increasing margins, Ingles believes that private label sales help promote customer loyalty and provide a value-priced alternative to national brands.

The Company seeks to maintain a reputation for providing friendly service, quality merchandise and customer value and for its commitment to community involvement. The Company employs various advertising and promotional strategies to reinforce the quality and value of its products. The Company promotes these attributes using traditional advertising vehicles including radio, television, direct mail and newspapers, as well as electronic and social media. The Ingles Advantage Card is designed to foster customer loyalty by providing information to better understand the Company’s customers’ shopping patterns.

Purchasing and Distribution

The Company currently supplies approximately 56% of its supermarkets’ inventory requirements from its modern warehouse and distribution facilities. In fiscal 2012, the Company completed construction of an approximately 839,000 square foot warehouse and distribution facility adjacent to its existing facility. This addition included new energy-efficient space for meat and produce products, and allows the Company to self-distribute frozen foods, general merchandise, health, beauty and cosmetic items. The new facility includes the production of bagged ice cubes and a slicing/packaging area for cheese and other products. The Company has 1,649,000 square feet of office, warehouse and distribution facilities at its headquarters near Asheville, North Carolina. The Company believes that its warehouse and distribution facilities will contain sufficient capacity for the continued expansion of its store base for the foreseeable future.

The Company’s centrally managed purchasing and distribution operations provide several advantages, including the ability to negotiate and reduce the cost of merchandise, decrease overhead costs and better manage its inventory at both the warehouse and store level. From time to time, the Company engages in advance

7

Table of Contents

purchasing on high-turnover inventory items to take advantage of special prices offered by manufacturers for limited periods. The Company’s ability to take advantage of advance purchasing is limited by several factors including carrying costs and warehouse space.

Prior to the completion of the new warehouse and distribution facility in fiscal 2012, a significant portion of the Company’s other inventory requirements, primarily frozen food and slower moving items that the Company prefers not to stock were purchased from Merchant Distributors, Inc. (“MDI”), a wholesale grocery distributor with which the Company has had a continuing relationship since its inception. Purchases from MDI were approximately $201 million in fiscal 2012, $274 million in fiscal 2011 and $269 million in fiscal 2010. Additionally, MDI purchases product from Milkco, Inc., the Company’s fluid dairy subsidiary, and these purchases totaled approximately $39 million in fiscal 2012, $42 million in fiscal 2011 and $38 million in fiscal 2010. The Company purchases items from MDI based on cost plus a handling charge. MDI owned approximately 2% of the Company’s Class A Common Stock and approximately 1% of the Company’s Class B Common Stock at September 29, 2012, which equals 1.4% of the total voting power. The Company believes that alternative sources of supply are readily available from other third parties.

The remaining 44% of the Company’s inventory requirements, primarily beverages, gasoline, bread and snack foods, are supplied directly to the Company’s supermarkets by local distributors and manufacturers.

Goods from the warehouse and distribution facilities and the milk processing and packaging plant are distributed to the Company’s stores by a fleet of 127 tractors and 549 trailers that the Company operates and maintains, including tractors and trailers that the Company leases. The Company invests on an ongoing basis in the maintenance, upgrade and replacement of its tractor and trailer fleet. The Company also operates truck servicing and fuel storage facilities at its warehouse and distribution facilities. The Company reduces its overall distribution costs by capitalizing on back-haul opportunities (contracting to transport merchandise on trucks that would otherwise be empty).

The Company receives product recall information from various subscription, government and vendor sources. Upon receipt of recall information, the Company immediately contacts each of its stores to have the recalled product removed from the shelves, and disposes of the product as instructed. The Company has a policy of refunding and/or replacing any goods returned by customers. The details of this policy are posted inside each of the Company’s stores.

Store Development, Expansion and Remodeling

The Company believes that the appearance and design of its stores are integral components of its customers’ shopping experience and aims to develop one of the most modern supermarket chains in the industry. The ongoing modernization of the Company’s store base involves (i) the construction of new stores with continuously updated designs, and (ii) the replacement or complete remodeling and expansion of existing stores. The Company’s goal is to maintain clean, well-lit stores with attractive architectural features that enhance the image of its stores as catering to the changing lifestyle needs of quality-conscious consumers who demand increasingly diverse product offerings.

The Company is focused primarily on developing owned stores. Management believes that owning stores provides the Company with flexible, lower all-in occupancy costs. The construction of new stores by independent contractors is closely monitored and controlled by the Company.

The Company renovates and remodels stores in order to increase customer traffic and sales, respond to existing customer demand, compete effectively against new stores opened by competitors and support its quality image merchandising strategy. The Company decides to complete a major remodel of an existing store based on its evaluation of the competitive landscape of the local marketplace. A major remodel and expansion provides the quality of facilities and product offerings identical to that of a new store, capitalizing upon the existing customer

8

Table of Contents

base. The Company retains the existing customer base by keeping the store in operation during the entire remodeling process. The Company may elect to relocate, rather than remodel, certain stores where relocation provides a more convenient location for its customers and is more economical.

The following table sets forth, for the periods indicated, the Company’s new store development and store remodeling activities and the effect this program has had on the average size of its stores.

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Number of Stores: |

||||||||||||||||||||

| Opened (1) |

— | 1 | 2 | 4 | 2 | |||||||||||||||

| Closed (1) |

— | — | — | 1 | 2 | |||||||||||||||

| Major remodels and replacements |

— | 3 | 2 | 6 | 10 | |||||||||||||||

| Stores open at end of period |

203 | 203 | 202 | 200 | 197 | |||||||||||||||

| Size of Stores: |

||||||||||||||||||||

| Less than 30,000 sq. ft. |

15 | 15 | 15 | 13 | 14 | |||||||||||||||

| 30,000 up to 41,999 sq. ft. |

40 | 40 | 40 | 41 | 42 | |||||||||||||||

| 42,000 up to 51,999 sq. ft. |

26 | 26 | 27 | 27 | 28 | |||||||||||||||

| At least 52,000 sq. ft. |

122 | 122 | 120 | 119 | 113 | |||||||||||||||

| Average store size (sq. ft.) |

54,262 | 54,252 | 53,524 | 53,432 | 51,756 | |||||||||||||||

| (1) | Excludes new stores opened to replace existing stores. |

The Company has historically expanded its store base by acquiring or leasing supermarket sites and constructing stores to its specifications. From time to time, however, the Company may consider the acquisition of existing supermarkets as such opportunities become available.

The Company’s ability to open new stores is subject to many factors, including the acquisition of satisfactory sites and the successful negotiation of new leases, and may be limited by zoning and other governmental regulation. In addition, the Company’s expansion, remodeling and replacement plans are continually reviewed and are subject to change. See the “Liquidity and Capital Resources” section included in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s capital expenditures.

Competition

The supermarket industry is highly competitive and characterized by narrow profit margins. The degree of competition the Company’s stores encounter varies by location, primarily based on the size of the community in which the store is located and its proximity to other communities. The Company’s principal competitors are, in alphabetical order, Aldi, Inc., Bi-Lo, LLC., Food City (K-VA-T Food Stores, Inc.), Food Lion (Delhaize America, Inc.), The Kroger Co., Publix Super Markets, Inc., Target Corporation, and Wal-Mart Stores, Inc. Increasingly over the last few years, competition for consumers’ food dollars has intensified due to the addition of, or increase in, food sections by many types of retailers such as specialty grocers, drug and convenience stores, national general merchandisers and discount retailers, membership clubs, warehouse stores and super centers. Restaurants are another significant competitor for food dollars.

Supermarket chains generally compete on the basis of location, quality of products, service, price, convenience, product variety and store condition.

The Company believes its competitive advantages include convenient locations, the quality of service it provides its customers, competitive pricing, product variety and quality and a pleasant shopping environment, which is enhanced by its ongoing modernization program.

9

Table of Contents

By concentrating its operations within a relatively small geographic region, the Company is also positioned to more carefully monitor its markets, and the needs of its customers within those markets. The Company’s senior executives live and work in the Company’s operating region, thereby allowing management to quickly identify changes in needs and customer preference. Because of the Company’s size, store managers have direct access to corporate management and are able to receive quick decisions regarding requested changes in operations. The Company can then move quickly to make adjustments in its business in response to changes in the market and customer needs.

The Company’s large national and international competitors’ primary advantages are related to their size. These larger organizations may have an advantage through stronger buying power and more significant capital resources.

The Company’s management monitors competitive activity and regularly reviews and periodically adjusts the Company’s marketing and business strategies as management deems appropriate in light of existing conditions in the Company’s region. The Company’s ability to remain competitive in its changing markets will depend in part on its ability to pursue its expansion and renovation programs and its response to remodeling and new store openings by its competitors.

Seasonality

Sales in the grocery segment of the Company’s business are subject to a slight seasonal variance due to holiday related sales and due to sales in areas where seasonal homes are located. Sales are traditionally higher in the Company’s first fiscal quarter due to the inclusion of sales related to Thanksgiving and Christmas. The Company’s second fiscal quarter traditionally has the lowest sales of the year, unless Easter falls in that quarter. In the third and fourth quarters, sales are affected by the return of customers to seasonal homes in the Company’s market area. The fluid dairy segment of the Company’s business has slight seasonal variation to the extent of its sales into the grocery industry. The Company’s real estate segment is not subject to seasonal variations.

Employees and Labor Relations

At September 29, 2012, the Company had approximately 20,800 non-union employees, of which 90% were supermarket personnel. Approximately 61% of these employees work on a part-time basis. Management considers employee relations to be good. The Company values its employees and believes that employee loyalty and enthusiasm are key elements of its operating performance.

Trademarks and Licenses

The Company employs various trademarks and service marks in its business, the most important of which are its own “Laura Lynn” private label trademark, “The Ingles Advantage” service mark, and the “Ingles” service mark. These service marks and the trademark are federally registered in the United States pursuant to applicable intellectual property laws and are the property of Ingles. In addition, the Company uses the “Sealtest,” “Pet,” “Biltmore” and “Light N’ Lively” trademarks pursuant to agreements entered into in connection with its fluid dairy processing plant segment. The Company believes it has all material licenses and permits necessary to conduct its business.

The current expiration dates for significant trade and service marks are as follows: “Ingles” —December 9, 2015; “Laura Lynn” —March 13, 2014; and “The Ingles Advantage” —August 30, 2015. Each registration may be renewed for an additional ten-year term prior to its expiration. The Company intends to file all renewals timely. Each of the Company’s trademark license agreements has a one year term which, with respect to one license, is automatically renewed annually, unless the owner of the trademark provides notice of termination prior to the expiration date and, with respect to the other licenses, are renewed periodically by letter from the licensor. The Company currently has five pending applications for additional trademarks or service marks.

10

Table of Contents

Environmental Matters

Under applicable environmental laws, the Company may be responsible for remediation of environmental conditions and may be subject to associated liabilities relating to its stores and other buildings and the land on which such stores and other buildings are situated (including responsibility and liability related to its operation of its gas stations and the storage of gasoline in underground storage tanks), regardless of whether the Company leases or owns the stores, other buildings or land in question and regardless of whether such environmental conditions were created by the Company or by a prior owner or tenant. The Company’s liabilities may also include costs and judgments resulting from lawsuits brought by private litigants. The presence of contamination from hazardous or toxic substances, or the failure to properly remediate such contaminated property, may adversely affect the Company’s ability to sell or rent such real property or to borrow using such real property as collateral. Although the Company typically conducts an environmental review prior to acquiring or leasing new stores, other buildings or raw land, there can be no assurance that environmental conditions relating to prior, existing or future stores, other buildings or the real properties on which such stores or other buildings are situated will not have a material adverse effect on the Company’s business, financial condition and results of operations.

Federal, state and local governments could enact laws or regulations concerning environmental matters that affect the Company’s operations or facilities or increase the cost of producing or distributing the Company’s products. The Company believes that it currently conducts its operations, and in the past has conducted its operations, in substantial compliance with applicable environmental laws. The Company, however, cannot predict the environmental liabilities that may result from legislation or regulations adopted in the future, the effect of which could be retroactive. Nor can the Company predict how existing or future laws and regulations will be administered or interpreted or what environmental conditions may be found to exist at its facilities or at other properties where the Company or its predecessors have arranged for the disposal of hazardous substances. The enactment of more stringent laws or regulations or stricter interpretation of existing laws and regulations could require expenditures by the Company, some of which could have a material adverse effect on its business, financial condition and results of operations.

The Company strives to employ sound environmental operating policies, including recycling cardboard packaging, recycling wooden pallets, and re-circulating some water used in its car washes. The Company offers reusable shopping bags to its customers and will pack groceries in bags brought in by its customers. The Company’s store modernization plans include energy efficient lighting and refrigeration equipment.

Government Regulation

The Company is subject to regulation by a variety of governmental agencies, including, but not limited to, the U.S. Food and Drug Administration, the U.S. Department of Agriculture, the Occupational Health and Safety Administration and other federal, state and local agencies. The Company’s stores are also subject to local laws regarding zoning, land use and the sale of alcoholic beverages. The Company believes that its locations are in material compliance with such laws and regulations.

| Item 1A. | RISK FACTORS |

Below is a series of risk factors that may affect the Company's business, financial condition and/or results of operations. Other risk factors are contained in "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" and the Notes to the Consolidated Financial Statements of this Annual Report on Form 10-K. These and such other risk factors may not be exhaustive. The Company operates in a continually changing business environment, and new risk factors emerge from time to time. Management cannot predict such new risk factors, nor can it assess the impact, if any, of these risk factors on the Company's business, financial condition and/or results of operations or the extent to which any factor or combination of factors may impact of any of these areas.

11

Table of Contents

The Company’s expansion and renovation plans may not be successful which may adversely affect the Company’s business and financial condition due to the capital expenditures and management resources required to carry out the Company’s plans.

The Company has spent, and intends to continue to spend, significant capital and management resources on the development and implementation of the Company’s expansion and renovation plans. These plans, if implemented, may not be successful, may not improve operating results and may have an adverse effect on cash flow and management resources due to the significant amount of capital invested and management time expended.

The level of sales and profit margins in the Company’s existing stores may not be duplicated in the Company’s new stores, depending on factors such as prevailing competition, development cost, and the Company’s market position in the surrounding community. The operational benefits of the new distribution facility may not meet the Company’s expectations. These factors could have an adverse effect on the Company’s business, financial condition and/or results of operations.

The Company’s warehouse and distribution center and milk processing and packaging plant, as well as all of the Company’s stores, are concentrated in the Southeastern United States, which makes it vulnerable to economic downturns, natural disasters and other adverse conditions or other catastrophic events in this region.

The Company operates in the Southeastern United States, and its performance is therefore heavily influenced by economic developments in the Southeast region. The Company’s headquarters, warehouse and distribution center and milk processing and packaging plant are located in North Carolina and all of the Company’s stores are located in the Southeast region. As a result, the Company’s business may be more susceptible to regional factors than the operations of more geographically diversified competitors. These factors include, among others, changes in the economy, weather conditions, demographics and population.

The Company has, and expects to continue to have, a significant amount of indebtedness.

At September 29, 2012, the Company had total consolidated indebtedness for borrowed money of $835.2 million and has $126.7 million available under a $175.0 million of committed line of credit. A portion of the Company’s cash flow is used to service such indebtedness. The Company owns a significant amount of real estate, which has been and will continue to be a factor in the Company’s overall level of indebtedness. Real estate can be used as collateral for indebtedness and can be sold to reduce indebtedness. The Company’s significant indebtedness could have important consequences, including the following:

| • | It may be difficult for the Company to satisfy its obligations under its existing credit facilities and its other indebtedness and commitments; |

| • | The Company is required to use a portion of its cash flow from operations to pay interest on its current and future indebtedness, which may require the Company to reduce funds available for other purposes; |

| • | The Company may have a limited ability to obtain additional financing, if needed, to fund additional projects, working capital requirements, capital expenditures, debt service, general corporate or other obligations; and |

| • | The Company may be placed at a competitive disadvantage to its competitors that are not as highly leveraged. |

Disruptions in the capital markets could adversely affect the Company’s ability to fund its liquidity needs and its expansion and renovation plans.

Disruptions in the capital markets as a result of uncertainty, changing or increased regulation, reduced alternatives or failures of significant financial institutions could adversely affect the Company’s access to liquidity needed for its business. Any disruption could limit the Company’s access to capital and raise its cost of

12

Table of Contents

capital to the extent available and require the Company to take measures to conserve cash until the markets stabilize or until alternative credit arrangements or other funding for its business needs can be arranged. Such measures could include deferring capital expenditures, dividend payments or other discretionary uses of cash.

The Company’s principal stockholder, Robert P. Ingle II, has the ability to elect a majority of the Company’s directors, appoint new members of management and approve many actions requiring stockholder approval.

Mr. Ingle II’s beneficial ownership (as defined by the Exchange Act) represents approximately 87% of the combined voting power of all classes of the Company’s capital stock as of September 29, 2012. As a result, Mr. Ingle II has the power to elect a majority of the Company’s directors and approve any action requiring the approval of the holders of the Company’s Class A Common Stock and Class B Common Stock, including adopting certain amendments to the Company’s charter and approving mergers or sales of substantially all of the Company’s assets. Currently, two of the Company’s eight directors are members of the Ingle family.

The Company is a Controlled Company under the NASDAQ Marketplace Rules. As a result, the Company is exempt from certain of NASDAQ’s corporate governance policies, including the requirements that the majority of Directors be independent (as defined in NASDAQ rules), and that the Company have a nominating committee for Director candidates.

If the Company loses the services of its key personnel, the Company’s business could suffer.

The Company’s continued success depends upon the availability and performance of the Company’s executive officers, including Robert P. Ingle II, who possess unique and extensive industry knowledge and experience. The loss of the services of any of the Company’s executive officers or other key employees could adversely affect the Company’s business.

Various aspects of the Company’s business are subject to federal, state and local laws and regulations. The Company’s compliance with these regulations may require additional capital expenditures and could adversely affect the Company’s ability to conduct the Company’s business as planned.

The Company is subject to federal, state and local laws and regulations relating to zoning, land use, work place safety, public health, community right-to-know, beer and wine sales, country of origin labeling of food products, pharmaceutical sales and gasoline station operations. Furthermore, the Company’s business is regulated by a variety of governmental agencies, including, but not limited to, the U.S. Food and Drug Administration, the U.S. Department of Agriculture, and the Occupational Health and Safety Administration. Employers are also subject to laws governing their relationship with employees, including minimum wage requirements, overtime, working conditions, insurance coverage, disabled access and work permit requirements. Recent and proposed regulation has had or may have a future impact on the cost of insurance benefits for employees and on the cost of processing debit and credit card transactions. Compliance with, or changes in, these laws could reduce the revenue and profitability of the Company’s supermarkets and could otherwise adversely affect the Company’s business, financial condition or results of operations.

The Company is also subject to various state and federal environmental laws relating to the Company’s stores, gas stations, distribution facilities and use of hazardous or toxic substances. As a result of these laws, the Company could be responsible for remediation of environmental conditions and may be subject to associated liabilities.

The Company is affected by certain operating costs which could increase or fluctuate considerably.

The Company depends on qualified employees to operate the Company’s stores and may be affected by future labor markets. A shortage of qualified employees could require the Company to enhance the Company’s wage and benefit package in order to better compete for and retain qualified employees, and the Company may

13

Table of Contents

not be able to recover these increased labor costs through price increases charged to customers, which could significantly increase the Company’s operating costs.

The Company is self-insured for workers’ compensation and group medical and dental benefits. Risks and uncertainties are associated with self-insurance; however, the Company has limited its exposure by maintaining excess liability coverage. Self-insurance liabilities are established based on claims filed and estimates of claims incurred but not reported. The estimates are based on data provided by the respective claims administrators and analyses performed by actuaries engaged by the Company. These estimates can fluctuate if historical trends are not predictive of the future. The majority of the Company’s properties are self-insured for casualty losses and business interruption; however, liability coverage is maintained.

Energy and utility costs have been volatile in recent years, during which time the Company has expanded its store square footage. The Company attempts to increase its energy efficiency during store construction and remodeling through the use of energy-saving equipment and construction.

The Company is affected by the availability and wholesale price of gasoline and retail gasoline prices, all of which can fluctuate quickly and considerably.

The Company operates fuel stations at 72 of its store locations. While the Company obtains gasoline and diesel fuel from a number of different suppliers, long-term disruption in the availability and wholesale price of gasoline for resale could have a material adverse effect on the Company’s business, financial condition and/or results of operations.

Fluctuating fuel costs adversely affect the Company’s operating costs which depend on fuel for the Company’s fleet of tractors and trailers which distribute goods from the Company’s distribution facility and for the Company’s fluid dairy operations.

Furthermore, fluctuating fuel costs could have an adverse effect on the Company’s total gasoline sales (both in terms of dollars and gallons sold), the profitability of gasoline sales, and the Company’s plans to develop additional fuel centers. Also, retail gas price volatility could diminish customer usage of fueling centers and, thus, adversely affect customer traffic at the Company’s stores.

The Company’s industry is highly competitive. If the Company is unable to compete effectively, the Company’s financial condition and results of operations could be materially affected.

The supermarket industry is highly competitive and continues to be characterized by intense price competition, increasing fragmentation of retail formats, entry of non-traditional competitors and market consolidation. Furthermore, some of the Company’s competitors have greater financial resources and could use these financial resources to take measures, such as altering product mix or reducing prices, which could adversely affect the Company’s competitive position.

Disruptions in the efficient distribution of food products to the Company’s warehouse and stores may adversely affect the Company’s business.

The Company’s business could be adversely affected by disruptions in the efficient distribution of food products to the Company’s warehouse and to the Company’s stores. Such disruptions could be caused by, among other things, adverse weather conditions, fuel availability, food contamination recalls and civil unrest in foreign countries in which the Company’s suppliers do business.

14

Table of Contents

The Company’s operations are subject to economic conditions that impact consumer spending.

The Company’s results of operations are sensitive to changes in overall economic conditions that impact consumer spending, including discretionary spending. Future economic conditions such as employment levels, business conditions, interest rates, energy and fuel costs and tax rates could reduce consumer spending or change consumer purchasing habits. A general reduction in the level of consumer spending or the Company’s inability to respond to shifting consumer attitudes regarding products, store location and other factors could adversely affect the Company’s business, financial condition and/or results of operations.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

| Item 2. | PROPERTIES |

Owned Properties

The Company owns and operates 69 shopping centers, 57 of which contain an Ingles supermarket, and owns 95 additional properties that contain a free-standing Ingles store. The Company also owns 12 undeveloped sites which are suitable for a free-standing store or shopping center development. Ingles owns numerous outparcels and other acreage located adjacent to the shopping centers and supermarkets it owns. Real estate owned by the Company is generally located in the same geographic regions as its supermarkets.

The shopping centers owned by the Company contain an aggregate of 5.9 million square feet of leasable space, of which 3.0 million square feet is used by the Company’s supermarkets. The remainder of the leasable space in these shopping centers is leased or held for lease by the Company to third party tenants. A breakdown by size of the shopping centers owned and operated by the Company is as follows:

| Size |

Number | |||

| Less than 50,000 square feet |

18 | |||

| 50,000 – 100,000 square feet |

25 | |||

| More than 100,000 square feet |

26 | |||

|

|

|

|||

| Total |

69 | |||

|

|

|

|||

The Company owns an 1,649,000 square foot facility, which is strategically located between Interstate 40 and Highway 70 near Asheville, North Carolina, as well as the 73 acres of land on which it is situated. The facility includes the Company’s headquarters and its warehouse and distribution facility. The property also includes truck servicing and fuel storage facilities. The Company also owns a 139,000 square foot warehouse on 21 acres of land approximately one mile from its main warehouse and distribution facility that is used to store seasonal and overflow items.

The Company’s milk processing and packaging subsidiary, Milkco, Inc., owns a 140,000 square foot manufacturing and storage facility in Asheville, North Carolina. In addition to the plant, the 20-acre property includes truck cleaning and fuel storage facilities.

Certain long-term debt of the Company is secured by the owned properties. See Note 7, “Long-Term Debt” to the Consolidated Financial Statements of this Annual Report on Form 10-K for further details.

Leased Properties

The Company operates supermarkets at 51 locations leased from various unaffiliated third parties. The Company also leases two supermarket facilities in which it is not currently operating, one of which is subleased

15

Table of Contents

to third parties and one of which is held for lease by the Company. Certain of the leases give the Company the right of first refusal to purchase the entire shopping center in which the supermarkets are located. The majority of these leases require the Company to pay property taxes, utilities, insurance, repairs and certain other expenses incidental to occupation of the premises. In addition to base rent, most leases contain provisions that require the Company to pay additional percentage rent (ranging from 0.75% to 1.50%) if sales exceed a specified amount.

Rental rates generally range from $2.90 to $8.18 per square foot. During fiscal 2012, 2011 and 2010, the Company paid a total of $13.6 million, $14.2 million and $14.9 million, respectively, in supermarket rent, exclusive of property taxes, utilities, insurance, repairs and other expenses. The following table summarizes lease expiration dates as of September 29, 2012, with respect to the initial and any renewal option terms of leased supermarkets:

| Year of Expiration (Including Renewal Terms) |

Number of Leases Expiring |

|||

| 2013 – 2026 |

7 | |||

| 2027 – 2041 |

2 | |||

| 2042 or after |

42 | |||

Management believes that the long-term rent stability provided by these leases is a valuable asset of the Company.

| Item 3. | LEGAL PROCEEDINGS |

Various legal proceedings and claims arising in the ordinary course of business are pending against the Company. In the opinion of management, the ultimate liability, if any, from all pending legal proceedings and claims would not materially affect the Company’s business, financial condition and/or the results of operations.

16

Table of Contents

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

The Company has two classes of Common Stock: Class A and Class B. Class A Common Stock is traded on The NASDAQ Global Select Market under the symbol IMKTA. There is no public market for the Company’s Class B Common Stock. However, under the terms of the Company’s Articles of Incorporation, any holder of Class B Common Stock may convert any portion or all of the holder’s shares of Class B Common Stock into an equal number of shares of Class A Common Stock at any time. For additional information regarding the voting powers, preferences and relative rights of the Class A Common Stock and Class B Common Stock, please see Note 8, “Stockholders’ Equity” to the Consolidated Financial Statements of this Annual Report on Form 10-K.

As of December 20, 2012, there were approximately 571 holders of record of the Company’s Class A Common Stock and 159 holders of record of the Company’s Class B Common Stock. The following table sets forth the reported high and low closing sales price for the Class A Common Stock during the periods indicated as reported by NASDAQ. The quotations reflect actual inter-dealer prices without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

| 2012 Fiscal Year |

High | Low | ||||||

| First Quarter (ended December 24, 2011) |

$ | 15.80 | $ | 14.05 | ||||

| Second Quarter (ended March 24, 2012) |

$ | 18.11 | $ | 14.97 | ||||

| Third Quarter (ended June 23, 2012) |

$ | 18.28 | $ | 15.29 | ||||

| Fourth Quarter (ended September 29, 2012) |

$ | 16.74 | $ | 14.94 | ||||

| 2011 Fiscal Year |

High | Low | ||||||

| First Quarter (ended December 25, 2010) |

$ | 20.35 | $ | 16.46 | ||||

| Second Quarter (ended March 26, 2011) |

$ | 20.08 | $ | 18.06 | ||||

| Third Quarter (ended June 25, 2011) |

$ | 19.95 | $ | 15.78 | ||||

| Fourth Quarter (ended September 24, 2011) |

$ | 17.37 | $ | 14.06 | ||||

On December 20, 2012, the closing sales price of the Company’s Class A Common Stock on The NASDAQ Global Select Market was $17.40 per share.

Dividends

The Company has paid cash dividends on its Common Stock in each of the past thirty fiscal years, except for the 1984 fiscal year when the Company paid a 3% stock dividend. During both fiscal 2012 and fiscal 2011, the Company paid annual dividends totaling $0.66 per share of Class A Common Stock and $0.60 per share of Class B Common Stock, paid in quarterly installments of $0.165 and $0.15 per share, respectively. The Company’s last dividend payment was made on October 25, 2012 to common stockholders of record on October 11, 2012. On December 7, 2012 the Company declared a special dividend of $0.66 per share of Class A Common Stock and $0.60 per share of Class B Common Stock payable on December 31, 2012 to shareholders of record on December 21, 2012. For additional information regarding the dividend rights of the Class A Common Stock and Class B Common Stock, please see Note 8, “Stockholders’ Equity” to the Consolidated Financial Statements of this Annual Report on Form 10-K.

The Company expects to continue paying regular cash dividends on a quarterly basis. However, the Board of Directors periodically reconsiders the declaration of dividends. The Company pays these dividends at the discretion of the Board of Directors. The continuation of these payments, the amount of such dividends, and the form in which the dividends are paid (cash or stock) depends upon the results of operations, the financial condition of the Company and other factors which the Board of Directors deems relevant. The payment of cash dividends is also subject to restrictions contained in certain financing arrangements. Such restrictions are summarized in Note 7, “Long-Term Debt” to the Consolidated Financial Statements of this Annual Report on Form 10-K.

17

Table of Contents

Equity Compensation Plan Information

The Company does not have any equity compensation plans.

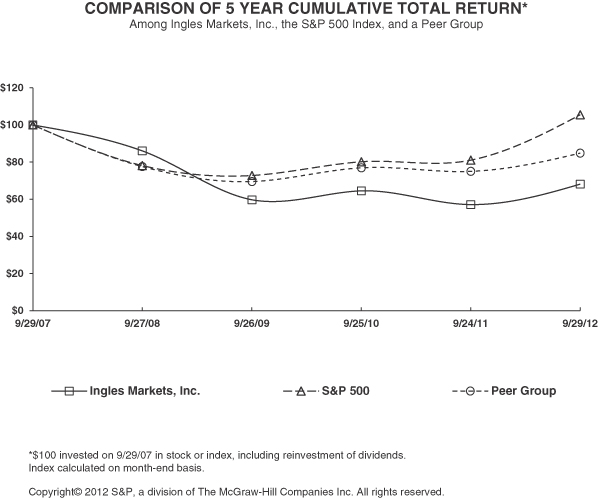

Stock Performance Graph

Set forth below are a graph and accompanying table comparing the five-year cumulative total stockholder return on the Class A Common Stock with the five-year cumulative total return of (i) the S&P 500 Comprehensive-Last Trading Day Index and (ii) a peer group of companies in the Company's line of business. The peer group consists of the following companies: Koninklijke Ahold N.V., Delhaize S.A., Harris Teeter Supermarkets, Weis Markets, Inc., The Kroger Co., Safeway Inc., Supervalu Inc., and Whole Foods Market, Inc.

The comparisons cover the five-years ended September 29, 2012 and assume that $100 was invested after the close of the market on September 29, 2007, and that dividends were reinvested quarterly. Returns of the companies included in the peer group reflected below have been weighted according to each company’s stock market capitalization at the beginning of each section for which a return is presented.

INGLES MARKETS, INCORPORATED

COMPARATIVE RETURN TO STOCKHOLDERS

18

Table of Contents

INDEXED RETURNS OF INITIAL $100 INVESTMENT*

| Company/Index |

2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||

| Ingles Markets, Incorporated Class A Common Stock |

$ | 85.89 | $ | 59.58 | $ | 64.31 | $ | 56.95 | $ | 68.05 | ||||||||||

| S&P 500 Comprehensive—Last Trading Day Index |

$ | 78.02 | $ | 72.63 | $ | 80.01 | $ | 80.93 | $ | 105.37 | ||||||||||

| Expanded Peer Group |

$ | 77.94 | $ | 69.65 | $ | 77.51 | $ | 75.81 | $ | 85.50 | ||||||||||

| * | Assumes $100 invested in the Class A Common Stock of Ingles Markets, Incorporated after the close of the market on September 29, 2007. |

The foregoing stock performance information, including the graph, shall not be deemed to be “soliciting material” or to be filed with the Securities and Exchange Commission.

| Item 6. | SELECTED FINANCIAL DATA |

The selected financial data set forth below has been derived from the Company’s Consolidated Financial Statements included elsewhere in this Annual Report on Form 10-K. This financial data should be read in conjunction with Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements and Notes thereto.

| Selected Income Statement Data for the Year Ended September (in thousands, except per share amounts) |

||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Net Sales |

$ | 3,709,434 | $ | 3,559,921 | $ | 3,390,052 | $ | 3,250,933 | $ | 3,238,046 | ||||||||||

| Net Income |

43,444 | 39,060 | 30,842 | 27,934 | 52,123 | |||||||||||||||

| Diluted Earnings per Common Share |

||||||||||||||||||||

| Class A |

$ | 1.79 | $ | 1.60 | $ | 1.26 | $ | 1.14 | $ | 2.13 | ||||||||||

| Class B |

1.70 | 1.52 | 1.20 | 1.08 | 2.02 | |||||||||||||||

| Cash Dividends per Common Share |

||||||||||||||||||||

| Class A |

$ | 0.66 | $ | 0.66 | $ | 0.66 | $ | 0.66 | $ | 0.66 | ||||||||||

| Class B |

0.60 | 0.60 | 0.60 | 0.60 | 0.60 | |||||||||||||||

| Selected Balance Sheet Data at

September (in thousands) |

||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Current Assets |

$ | 426,204 | $ | 389,364 | $ | 422,969 | $ | 423,657 | $ | 336,574 | ||||||||||

| Property and Equipment, net |

1,197,138 | 1,133,204 | 1,089,391 | 1,072,937 | 1,030,023 | |||||||||||||||

| Total Assets |

1,642,109 | 1,618,350 | 1,532,358 | 1,520,046 | 1,376,815 | |||||||||||||||

| Current Liabilities, including Current Portion of Long-Term Debt |

306,152 | 290,496 | 318,974 | 234,861 | 258,051 | |||||||||||||||

| Long-Term Liabilities, net of Current Portion (1) |

794,423 | 827,969 | 732,090 | 823,660 | 686,393 | |||||||||||||||

| Stockholders’ Equity |

457,413 | 431,946 | 409,081 | 394,302 | 381,847 | |||||||||||||||

| (1) | Excludes long-term deferred income tax liability. |

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview

Ingles, a leading supermarket chain in the Southeast United States, operates 203 supermarkets in Georgia (74), North Carolina (69), South Carolina (36), Tennessee (21), Virginia (2) and Alabama (1). The Company locates its supermarkets primarily in suburban areas, small towns and rural communities. Ingles supermarkets offer customers

19

Table of Contents

a wide variety of nationally advertised food products, including grocery, meat and dairy products, produce, frozen foods and other perishables and non-food products. Non-food products include fuel centers, pharmacies, health and beauty care products and general merchandise, as well as quality private label items. In addition, the Company focuses on selling high-growth, high-margin products to its customers through the development of certified organic products, bakery departments and prepared foods including delicatessen sections. As of September 29, 2012, the Company operated 81 in-store pharmacies and 72 fuel centers.

Ingles also operates two other lines of business, fluid dairy processing and shopping center rentals. The fluid dairy processing segment sells approximately 31% of its products to the retail grocery segment and approximately 69% of its products to third parties. Real estate ownership (including the shopping center rental segment) is an important component of the Company’s operations, providing both operational and economic benefit.

Critical Accounting Policies

Critical accounting policies are those accounting policies that management believes are important to the portrayal of Ingles’ financial condition and results of operations, and require management’s most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain. Estimates are based on historical experience and other factors believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Management estimates, by their nature, involve judgments regarding future uncertainties, and actual results may therefore differ materially from these estimates.

Self-Insurance

The Company is self-insured for workers’ compensation, general liability, and group medical and dental benefits. Risks and uncertainties are associated with self-insurance; however, the Company has limited its exposure by maintaining excess liability coverage of $750,000 per occurrence for workers’ compensation, $500,000 for general liability, and $325,000 per covered person for medical care benefits for a policy year. Self-insurance liabilities are established based on claims filed and estimates of claims incurred but not reported. The estimates are based on data provided by the respective claims administrators and analyses performed by actuaries engaged by the Company. These estimates can fluctuate if historical trends are not predictive of the future. The majority of the Company’s properties are self-insured for casualty losses and business interruption; however, liability coverage is maintained. The Company’s self insurance reserves totaled $26.7 million and $24.8 million for employee group insurance, workers’ compensation insurance and general liability insurance at September 29, 2012 and September 24, 2011, respectively.

In fiscal 2011, the Company refined its methods for calculating self-insurance liabilities which resulted in a significant increase to the previously reported estimate. The Company believes the amounts accrued under the revised method are adequate; however, future accruals may fluctuate if historical trends are not predictive of the future.

Asset Impairments

The Company accounts for the impairment of long-lived assets in accordance with Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) Topic 360. Asset groups are primarily comprised of our individual store and shopping center properties. For assets to be held and used, the Company tests for impairment using undiscounted cash flows and calculates the amount of impairment using discounted cash flows. For assets held for sale, impairment is recognized based on the excess of remaining book value over expected recovery value. The recovery value is the fair value as determined by independent quotes or expected sales prices developed by internal associates, net of costs to sell. Estimates of future cash flows and expected sales prices are judgments based upon the Company’s experience and knowledge of local operations and cash flows that are projected for several years into the future. These estimates can fluctuate significantly due to

20

Table of Contents

changes in real estate market conditions, the economic environment, capital spending decisions and inflation. The Company monitors the carrying value of long-lived assets for potential impairment each quarter based on whether any indicators of impairment have occurred.

Closed Store Accrual

For closed properties under long-term lease agreements, a liability is recognized and expensed based on the difference between the present value of any remaining liability under the lease and the present value of the estimated market rate at which the Company expects to be able to sublease the properties, in accordance with FASB ASC Topic 420. The Company’s estimates of market rates are based on its experience, knowledge and third-party advice or market data. If the real estate and leasing markets change, sublease recovery could vary significantly from the recoveries originally assumed, resulting in a material change in the Company’s recorded liability. The closed store accrual is included in the line item “Accrued expenses and current portion of other long-term liabilities” on the Consolidated Balance Sheets.

Vendor Allowances

The Company receives funds for a variety of merchandising activities from the many vendors whose products the Company buys for resale in its stores. These incentives and allowances are primarily comprised of volume or purchase based incentives, advertising allowances, slotting fees, and promotional discounts. The purpose of these incentives and allowances is generally to help defray the costs incurred by the Company for stocking, advertising, promoting and selling the vendor’s products. These allowances generally relate to short term arrangements with vendors, often relating to a period of a month or less, and are negotiated on a purchase-by-purchase or transaction-by-transaction basis. Whenever possible, vendor discounts and allowances that relate to buying and merchandising activities are recorded as a component of item cost in inventory and recognized in merchandise costs when the item is sold. Due to system constraints and the nature of certain allowances, it is sometimes not practicable to apply allowances to the item cost of inventory. In those instances, the allowances are applied as a reduction of merchandise costs using a rational and systematic methodology, which results in the recognition of these incentives when the inventory related to the vendor consideration received is sold. Vendor allowances applied as a reduction of merchandise costs totaled $114.3 million, $109.9 million and $105.2 million for the fiscal years ended September 29, 2012, September 24, 2011 and September 25, 2010, respectively. Vendor advertising allowances that represent a reimbursement of specific identifiable incremental costs of advertising the vendor’s specific products are recorded as a reduction to the related expense in the period that the related expense is incurred. Vendor advertising allowances recorded as a reduction of advertising expense totaled $13.2 million, $13.1 million, and $13.0 million for the fiscal years ended September 29, 2012, September 24, 2011 and September 25, 2010, respectively.

If vendor advertising allowances were substantially reduced or eliminated, the Company would likely consider other methods of advertising as well as the volume and frequency of the Company’s product advertising, which could increase or decrease the Company’s expenditures.

Similarly, the Company is not able to assess the impact of vendor advertising allowances on creating additional revenue, as such allowances do not directly generate revenue for the Company’s stores.

Uncertain Tax Positions

Despite the Company’s belief that its tax positions are consistent with applicable tax laws, the Company believes that certain positions are likely to be challenged by taxing authorities. Settlement of any challenge can result in no change, a complete disallowance, or some partial adjustment reached through negotiations or litigation. Significant judgment is required in evaluating the Company’s tax positions. The Company’s positions are evaluated in light of changing facts and circumstances, such as the progress of its tax audits as well as evolving case law. Income tax expense includes the impact of provisions for and changes to uncertain tax positions as the Company considers appropriate. Unfavorable settlement of any particular position would require use of cash. Favorable resolution would be recognized as a reduction to income tax expense at the time of resolution.

21

Table of Contents

Results of Operations

Ingles operates on a 52- or 53-week fiscal year ending on the last Saturday in September. The consolidated statements of income for the fiscal years ended September 29, 2012, September 24, 2011 and September 25, 2010, consisted of 53, 52 and 52 weeks of operations, respectively.

Comparable store sales are defined as sales by grocery stores in operation for five full fiscal quarters. The Company has an ongoing renovation and expansion plan to modernize the appearance and layout of its existing stores. Sales from replacement stores, major remodels and the addition of fuel stations to existing stores are included in the comparable store sales calculation from the date of completion of the replacement, remodel or addition. A replacement store is a new store that is opened to replace an existing nearby store that is closed. A major remodel entails substantial remodeling of an existing store and may include additional retail square footage. Gasoline sales from the addition of fuel stations to existing stores during the measurement period are included in comparable store sales. For the fiscal years ended September 29, 2012 and September 24, 2011 comparable store sales include 203 and 202 stores, respectively. Weighted average retail square footage added to comparable stores due to replacement and remodeled stores totaled approximately 248,000 and 218,000 for the fiscal years ended September 29, 2012 and September 24, 2011, respectively.

In fiscal years with 53 weeks, such as fiscal 2012, management analyzes annual comparable store sales for the 53 weeks of fiscal 2012 with the corresponding 53 calendar weeks of the previous year.

The following table sets forth, for the periods indicated, selected financial information as a percentage of net sales. For information regarding the various segments of the business, reference is made to Note 11 “Lines of Business” to the Consolidated Financial Statements.

| Fiscal Year Ended September | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Net sales |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Gross profit |

22.1 | 22.2 | 22.5 | |||||||||

| Operating and administrative expenses |

18.8 | 19.0 | 19.3 | |||||||||

| Rental income, net |

— | — | — | |||||||||

| Gain from sale or disposal of assets |

— | 0.1 | — | |||||||||

| Income from operations |

3.3 | 3.3 | 3.2 | |||||||||

| Other income, net |

0.1 | 0.1 | 0.1 | |||||||||

| Interest expense |

1.6 | 1.7 | 1.9 | |||||||||

| Income before income taxes |

1.8 | 1.7 | 1.4 | |||||||||

| Income taxes |

0.6 | 0.6 | 0.5 | |||||||||

| Net income |

1.2 | 1.1 | 0.9 | |||||||||

Fiscal Year Ended September 29, 2012 Compared to the Fiscal Year Ended September 24, 2011