UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended October 29 , 2023

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ____________________ to _________________________

Commission File Number: 1-2402

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code (507 ) 437-5611

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

1

The aggregate market value of the voting and nonvoting common stock held by non-affiliates of the registrant as of April 30, 2023, was $11,661,390,985 based on the closing price of $40.44 on the last business day of the registrant’s most recently completed second fiscal quarter.

As of December 3, 2023, the number of shares outstanding of each of the registrant’s classes of common stock was as follows:

Common Stock, $0.01465 Par Value – 546,840,056 shares

Common Stock Nonvoting, $0.01 Par Value – 0 shares

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Stockholders to be held January 30, 2024, are incorporated by reference into Part III, Items 10-14. The Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

HORMEL FOODS CORPORATION

TABLE OF CONTENTS

Unresolved Staff Comments | ||||||||

2

PART I

Item 1. BUSINESS

General Development of Business

Hormel Foods Corporation, a Delaware corporation (collectively, the "Company", "we," "us," and "our"), was founded by George A. Hormel in 1891 in Austin, Minnesota, as Geo. A. Hormel & Company. The Company started as a processor of meat and food products and continues in this line of business with emphasis on the manufacturing and distribution of branded, value-added consumer items rather than commodity fresh meat products. The Company builds on its founder's legacy of innovation, quality, and integrity with focus on its purpose statement — Inspired People. Inspired Food.™ Today, the Company is a global branded food company bringing some of the most trusted and iconic brands to tables across the globe with over $12 billion in annual revenue in more than 80 countries.

The Company has continually expanded its product portfolio through organic growth and acquisitions. In fiscal 2021, the Company acquired the Planters® snack nuts business, expanding the Company's presence in the growing snacking space. Refer to Note B - Acquisitions and Divestitures of the Notes to the Consolidated Financial Statements for additional information. During fiscal 2023, the Company purchased a 30% common stock interest in PT Garudafood Putra Putri Jaya Tbk (Garudafood), a food and beverage company in Indonesia, expanding the Company's presence in Southeast Asia and supporting global execution in the snacking and entertaining category. Refer to Note D - Investments in Affiliates of the Notes to the Consolidated Financial Statements for additional information.

Description of Business

Segments

Effective in fiscal 2023, the Company transitioned to a new strategic operating model, which aligns its businesses to be more agile, consumer and customer focused, and market driven. The Company currently operates with the following three operating and reportable segments: Retail, Foodservice, and International.

Retail

The Retail segment consists primarily of the processing, marketing, and sale of food products sold predominantly in the retail market. This segment also includes the results from the Company’s MegaMex Foods, LLC joint venture.

Foodservice

The Foodservice segment consists primarily of the processing, marketing, and sale of food and nutritional products for foodservice, convenience store, and commercial customers.

International

The International segment processes, markets, and sells Company products internationally. This segment also includes the results from the Company’s international joint ventures, equity method investments, and royalty arrangements.

Prior period results for fiscal 2022 and 2021 have been recast to reflect the new reportable segments. Net sales to unaffiliated customers, segment profit, and certain other financial information by segment are reported in Note P - Segment Reporting of the Notes to the Consolidated Financial Statements and in Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Products and Distribution

The Company develops, processes, and distributes a wide array of food products in a variety of markets and manufactures its products through various processing facilities and trusted co-manufacturers. The Company’s products primarily consist of meat, nuts, and other food products sold across multiple distribution channels, such as U.S. Retail, U.S. Foodservice, and International.

Domestically, the Company sells its products in all 50 states. The Company’s products are sold through its sales personnel, who operate in assigned territories or in dedicated teams serving major customers and who are coordinated from sales offices predominately located in major U.S. cities. The Company also utilizes independent brokers and distributors. Products are primarily distributed by common carrier.

The Company has a global presence within several major international markets, including Australia, Brazil, Canada, China, England, Indonesia, Japan, Mexico, the Philippines, Singapore, and South Korea. Distribution of export sales to customers is by common carrier, while the China and Brazil operations own and operate their own delivery systems. The Company has licensed companies to manufacture various products internationally on a royalty basis, with the primary licensees being Danish Crown UK

3

Ltd., and CJ CheilJedang Corporation. The Company also has minority positions in food companies in the Philippines (The Purefoods-Hormel Company, Inc., 40 percent holding) and Indonesia (Garudafood, 30 percent holding).

Raw Materials

The Company concentrates on the marketing and sale of branded, value-added food products. The principal raw materials used by the Company include pork, turkey, beef, chicken, and nuts. The Company takes a balanced approach to sourcing pork raw materials, including hogs purchased for the Austin, Minnesota processing facility, long-term supply agreements for pork, and spot market purchases of pork. The majority of the turkeys needed to meet raw material requirements are raised by the Company. Production costs from raising turkeys are subject to fluctuations in grain prices and fuel costs. To manage these risks, the Company uses futures, swaps, and options contracts to hedge a portion of its anticipated purchases.

The Company also purchases raw materials from various suppliers. As the Company has shifted its focus toward a more value-added portfolio, it has become increasingly dependent on these suppliers to meet its raw material needs. Certain raw materials, such as cashews, are sourced internationally, which may cause additional risks to pricing and availability. The Company utilizes supply contracts and forward buying strategies to ensure an adequate supply and mitigate price fluctuations.

Human Capital

The Company’s employees are the driving force behind innovation, improvement, and success. As of October 29, 2023, the Company had approximately 20,000 active employees, with over 90 percent located within the U.S. Approximately 20 percent of employees are covered by collective bargaining agreements.

Talent Acquisition, Development, and Retention

Hormel’s team members are the cornerstone of the Company and of the fulfillment of its purpose — Inspired People. Inspired Food.™ The Company places great importance on the growth, development, and engagement of its team members. The Company offers a competitive compensation package and a multitude of benefits, including medical, life and disability insurance, contributory and non-contributory retirement savings plans, free post-secondary tuition and tuition reimbursement programs, and two years of tuition-free community and technical college for U.S. employees’ dependent children.

The Company believes investing in the education, training, and development of employees contributes to the overall success of the business. The Company provides learning opportunities for employees through various training courses, including instructor-led internal and external programs and on-the-job training.

The Company considers the tenure of its team members to be an important indicator of overall performance and is proud of its tenure figures. As of October 29, 2023, approximately 50 percent of the Company's team members had five or more years of service, and the 34-person officer team had an average of 25 years of service.

Diversity, Equity, and Inclusion

The Company welcomes the diversity of all team members, customers, and consumers, and encourages the integration of their unique skills, thoughts, experiences, and identities. The Company’s workforce is made up of approximately 40 percent female and approximately 60 percent underrepresented minorities. The Company’s salaried employees are made up of approximately 35 percent female and over 20 percent underrepresented minorities. By fostering an inclusive culture, the Company enables every member of the workforce to leverage unique talents and high performance standards to drive innovation and success.

Executives of the Company are held accountable for creating an inclusive, diverse workplace through their annual incentive plan, which includes a component focused on overall belonging scores and the representation of female and underrepresented minorities in salaried positions.

The Company supports twelve employee resource groups (ERGs) that support the Company’s mission to create a workplace where all people feel welcomed, respected, and valued. These employee-driven groups play a critical role in diversity, equity, and inclusion efforts and provide professional development and mentorship opportunities.

Safety, Health, and Wellness

The Company’s dedicated corporate safety department develops and administers company-wide policies to ensure the safety of each employee and compliance with Occupational Safety and Health Administration standards. The corporate safety department also conducts regular audits of production facilities to ensure compliance with Company safety policies. The Company conducts safety training for all team members and completes approximately 1,000 safety assessments each month.

The Company recognizes that team members perform best when they are healthy, and that optimal performance is necessary for the Company to achieve its key results. In addition to the health care benefits package, the Company’s Inspired Health program aims to cultivate and maintain a culture of health and wellness that is focused on encouraging and empowering team members to make healthy lifestyle choices through awareness, prevention, and positive health behavior

4

changes. This program includes biometric screenings, on-site fitness centers and fitness center discounts, an online health university with robust information and resources, a tobacco cessation program, wellness challenges, and confidential health and wellness support.

Governmental Regulation and Environmental Matters

The Company’s operations are subject to regulation by various governmental agencies which oversee areas such as food safety, workforce immigration, environmental laws, animal welfare, tax regulations, and the processing, packaging, storage, distribution, advertising, and labeling of the Company’s products. The Company believes it is in compliance with current laws and regulations and does not expect continued compliance to have a material impact on capital expenditures, earnings, or competitive position. The Company continues to monitor existing and pending laws and regulations and, while the impact of regulatory changes cannot be predicted with certainty, the Company does not expect compliance to have a material adverse effect on the Company's business. In addition to compliance with environmental laws and regulations, the Company sets goals to further improve its sustainability efforts and reduce its environmental impact. These goals are outlined in the Company’s 20 by 30 Challenge and include matching energy with renewable sourcing, reducing organic waste and greenhouse gas emissions, supporting regenerative agriculture, focusing on packaging sustainability, and reducing food waste. In addition, the Company's greenhouse gas reduction targets were validated by the Science Based Targets initiative in 2023.

Significant Customers

The Company serves many customers throughout the world across various sales channels. Sales to the Company’s largest customer, Walmart Inc. (Walmart), accounted for approximately 15 percent of consolidated gross sales less returns and allowances during fiscal 2023. Walmart is a customer for the Company's Retail and International segments. The Company’s top five customers collectively represent approximately 36 percent of consolidated gross sales less returns and allowances. The loss of one or more of the top customers in any of the reportable segments could have a material adverse effect upon such segment’s financial results.

Competition

The production and sale of meat and food products in the U.S. and internationally is highly competitive. The Company competes with manufacturers of pork and turkey products as well as national and regional producers of other meat and protein sources, such as beef, chicken, fish, nuts, and plant-based proteins.

All operating segments compete on the basis of price, product quality and attributes, brand identification, breadth of product line, and customer service. Through effective marketing and strong quality assurance programs, the Company’s strategy is to provide high quality products that possess strong brand recognition, which support higher value perceptions with customers. To grow and maintain market position, the Company focuses on meeting consumer preferences, delivering product innovation, and maintaining long-term and lasting relationships with industry partners.

Patents and Trademarks

There are numerous patents and trademarks important to the Company’s business. The Company holds 23 U.S. and eight foreign patents. Most of the trademarks the Company uses are registered in the U.S. and other countries. Some of the more significant owned or licensed trademarks used by the Company or its affiliates are:

HORMEL, ALWAYS TENDER, APPLEGATE, AUSTIN BLUES, BACON 1, BLACK LABEL, BREAD READY, BURKE, CAFÉ H, CERATTI, CHI-CHI’S, COLUMBUS, COMPLEATS, CORN NUTS, CURE 81, DAN’S PRIZE, DI LUSSO, DINTY MOORE, DON MIGUEL, DOÑA MARIA, EMBASA, FAST ‘N EASY, FIRE BRAISED, FONTANINI, HAPPY LITTLE PLANTS, HERDEZ, HORMEL GATHERINGS, HORMEL SQUARE TABLE, HORMEL VITAL CUISINE, HOUSE OF TSANG, JENNIE-O, JUSTIN’S, LA VICTORIA, LAYOUT, LLOYD’S, MARY KITCHEN, MR. PEANUT, NATURAL CHOICE, NUT-RITION, OLD SMOKEHOUSE, OVEN READY, PILLOW PACK, PLANTERS, ROSA GRANDE, SADLER'S SMOKEHOUSE, SKIPPY, SPAM, SPECIAL RECIPE, THICK & EASY, VALLEY FRESH, and WHOLLY.

The Company’s patents expire after a term that is typically 20 years from the date of filing, with earlier expiration possible based on the Company’s decision whether to pay required maintenance fees. As long as the Company continues to use its trademarks, they are renewed indefinitely.

Available Information

The Company makes available its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 on its website at www.hormelfoods.com. These reports are accessible under the caption, “Investors – Filings & Reports – SEC Filings” on the Company’s website and are available as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (SEC). These filings are also available on the SEC's website at www.sec.gov. The documents are available in print, free of charge, to any stockholder who requests them.

5

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking” information within the meaning of the federal securities laws. The “forward-looking” information may include statements concerning the Company’s outlook for the future as well as other statements of beliefs, future plans, strategies, or anticipated events and similar expressions concerning matters that are not historical facts.

The Private Securities Litigation Reform Act of 1995 (the Reform Act) provides a "safe harbor" for forward-looking statements to encourage companies to provide prospective information. The Company is filing this cautionary statement in connection with the Reform Act. When used in the Company’s Annual Report to Stockholders, other filings by the Company with the SEC, the Company's press releases, and oral statements made by the Company's representatives, the words or phrases "should result," "believe," "intend," "plan," "are expected to," "targeted," "will continue," "will approximate," "is anticipated," "estimate," "project," or similar expressions are intended to identify forward-looking statements within the meaning of the Reform Act. Such statements are subject to certain risks and uncertainties that could cause actual results to differ materially from historical earnings and those anticipated or projected.

In connection with the “safe harbor” provisions of the Reform Act, the Company is identifying risk factors that could affect financial performance and cause the Company’s actual results to differ materially from opinions or statements expressed with respect to future periods. The following discussion of risk factors contains certain cautionary statements regarding the Company’s business, which should be considered by investors and others. Such risk factors should be considered in conjunction with any discussions of operations or results by the Company or its representatives, including any forward-looking discussion, as well as comments contained in press releases, presentations to securities analysts or investors, or other communications by the Company.

In making these statements, the Company is not undertaking, and specifically declines to undertake, any obligation to address or update each or any factor in future filings or communications regarding the Company’s business or results, and is not undertaking to address how any of these factors may have caused changes to discussions or information contained in previous filings or communications. Though the Company has attempted to list comprehensively these important cautionary risk factors, the Company wishes to caution investors and others that other factors may in the future prove to be important in affecting the Company’s business or results of operations.

The Company cautions readers not to place undue reliance on forward-looking statements, which represent current views as of the date made. Forward-looking statements are inherently at risk to changes in the national and worldwide economic environment, which could include, among other things, risks related to the deterioration of economic conditions; risks associated with acquisitions, joint ventures, equity investments, and divestitures; potential disruption of operations, including at co-manufacturers, suppliers, logistics providers, customers, or other third-party service providers; failure to realize anticipated cost savings or operating efficiencies associated with strategic initiatives; risk of loss of a material contract; the Company’s inability to protect information technology systems against, or effectively respond to, cyber attacks or security breaches; deterioration of labor relations, labor availability or increases to labor costs; general risks of the food industry, including food contamination; outbreaks of disease among livestock and poultry flocks; fluctuations in commodity prices and availability of raw materials and other inputs; fluctuations in market demand for the Company’s products; damage to the Company's reputation or brand image; climate change, or legal, regulatory, or market measures to address climate change; risks of litigation; potential sanctions and compliance costs arising from government regulation; compliance with stringent environmental regulations and potential environmental litigation; and risks arising from the Company’s foreign operations.

Item 1A. RISK FACTORS

Business and Operational Risks

Deterioration of economic conditions could harm the Company’s business. The Company's business may be adversely affected by changes in national or global economic conditions, including inflation, interest rates, tax rates, availability of capital, energy availability and costs (including fuel surcharges), political developments, civil unrest, and the effects of governmental initiatives to manage economic conditions. Decreases in consumer spending rates and shifts in consumer product preferences could also negatively impact the Company.

Volatility in financial markets and the deterioration of national and global economic conditions could impact the Company’s operations as follows:

▪The financial stability of the Company's customers and suppliers may be compromised, which could result in challenges in collecting accounts receivable or non-performance by suppliers.

▪Unfavorable economic conditions may lead customers and consumers to delay or reduce purchases of the Company's products.

6

▪Customer demand for products may not materialize to levels required to achieve the Company's anticipated financial results or may decline as distributors and retailers seek to reduce inventory positions if there is an economic downturn or economic uncertainty in key markets.

▪The value of the Company's investments in debt and equity securities may decline, including most significantly the trading securities held as part of a rabbi trust to fund supplemental executive retirement plans and deferred income plans and the Company’s assets held in pension plans.

▪Future volatility or disruption in the capital and credit markets could impair the Company's liquidity or increase costs of borrowing.

▪The Company may be required to redirect cash flow from operations or explore alternative strategies, such as disposing of assets, to fulfill the payment of principal and interest on its indebtedness.

The Company has no operations in Russia or Ukraine, yet it has experienced inflated fuel costs and supply chain shortages and delays due to the impact of the military conflict on the global economy. If this conflict, or others such as the Israel-Hamas war, escalates further, it could result in, among other things, additional supply chain disruptions, rising prices for oil and other commodities, volatility in capital markets and foreign exchange rates, rising interest rates, or heightened cybersecurity risks, any of which may adversely affect the Company's business. In addition, the effects of the ongoing conflict could heighten many of the other risk factors included in Item 1A.

The Company utilizes hedging programs to manage its exposure to various market risks, such as commodity prices and interest rates, which qualify for hedge accounting for financial reporting purposes. Volatile fluctuations in market conditions could cause these instruments to become ineffective, which could require any gains or losses associated with these instruments to be reported in the Company’s earnings each period. These instruments may limit the Company’s ability to benefit from market gains if commodity prices and/or interest rates become more favorable than those secured under the Company’s hedging programs.

The Company's goodwill and indefinite-lived intangible assets are initially recorded at fair value and are not amortized, but are reviewed for impairment annually or more frequently if impairment indicators arise. Impairment testing requires judgment around estimates and assumptions and is impacted by factors such as revenue growth rates, operating margins, tax rates, royalty rates, and discount rates. An unfavorable change in these factors may lead to the impairment of goodwill and/or intangible assets. During fiscal 2023, an impairment was indicated for the Justin's® trade name, resulting in an impairment charge of $28.4 million.

Additionally, if a highly pathogenic human disease outbreak developed, such as COVID-19, it may negatively impact the global economy, demand for Company products, the supply chain, the Company's co-manufacturers, and/or the Company’s workforce availability including leadership, and the Company’s financial results could suffer. The Company has developed contingency plans to address infectious disease scenarios and the potential impact on its operations, and will continue to update these plans as necessary. There can be no assurance given, however, that these plans will be effective in eliminating the negative effects of any such diseases on the Company’s operating results.

The Company’s operations are subject to the general risks associated with acquisitions, joint ventures, equity investments, and divestitures. The Company regularly reviews opportunities to support the Company’s strategic initiative of delivering long-term value to shareholders through acquisitions, joint ventures, and equity investments and to divest non-strategic assets. The Company has made several acquisitions, joint ventures, equity investments, and divestitures in recent years, including the acquisition of the Planters® snack nuts business in fiscal 2021 and purchase of a minority interest in Garudafood in fiscal 2023. Potential risks associated with these transactions include the inability to consummate a transaction timely or on favorable terms, diversion of management's attention from other business concerns, loss of key employees and customers of current or acquired companies, inability to integrate or divest operations successfully, assumption of unknown liabilities, disputes with buyers, sellers, or partners, inability to obtain favorable financing terms, impairment charges if purchase assumptions are not achieved, and the inherent risks in entering markets or lines of business in which the Company has limited or no prior experience. Due to the nature of these arrangements, joint ventures and equity investments involve further risks, including the possibility that the Company is unable to execute business strategies and manage operations given limitations of the Company's control. Additionally, partners may become bankrupt, make business decisions that are inconsistent with the Company's goals, or block or delay necessary decisions. Acquisitions, joint ventures, or equity investments outside the U.S. may also present unique challenges and increase the Company's exposure to the risks associated with foreign operations. Any or all of these risks could impact the Company’s financial results and business reputation. The Company's level of indebtedness increased significantly to fund the purchase of the Planters® snack nuts business and may continue to increase to fund future acquisitions, joint ventures, or equity investments. Higher levels of debt may, among other things, impact the Company's liquidity and increase the Company's exposure to negative fluctuations in interest rates. During fiscal 2023, an impairment was indicated for the Justin's® trade name, resulting in an impairment charge of $28.4 million and the Company recorded a $7.0 million impairment charge related to a corporate venturing investment to recognize a decline in fair value not believed to be temporary.

The Company is subject to disruption of operations at co-manufacturers, suppliers, logistics providers, customers, or other third-party service providers.

▪Disruption of operations at co‑manufacturers, suppliers, or logistics providers have and may continue to impact the Company’s product and input supplies as well as the ability to distribute products.

7

▪Disruptions related to significant customers or sales channels has and could continue to result in a reduction in sales or change in the mix of products sold.

▪Disruption in services from partners such as third-party service providers used to support various business functions such as benefit plan administration, payroll processing, information technology and cloud computing services could have an adverse effect on the Company's business.

Disruptions of third-party providers have had and may continue to have an adverse effect on the Company's financial results. Actions taken to mitigate the impact of any potential disruption, including increasing inventory in anticipation of a potential production or supply interruption, may adversely affect the Company’s financial results. Additionally, labor-related challenges have caused disruptions for many of these providers and may continue to impact the Company's ability to receive inputs or distribute products.

The Company may not realize the anticipated cost savings or operating efficiencies associated with strategic initiatives. The Company operates in the highly competitive food industry and is subject to volatile cost inputs. Strategic initiatives are implemented to achieve a profitable cost structure, operate efficiently, better serve customers, and optimize cash flow. These initiatives may focus on opportunities to improve the procurement, manufacturing, and logistics within the Company’s supply chain as well as general and administrative processes. A failure or delay in implementing the improvements associated with these strategic initiatives could adversely impact the Company’s results, ability to meet its long-term growth expectations, and ability to fund future initiatives.

The Company began an enterprise transformation and modernization initiative in the second half of fiscal 2023 to provide cost savings and operating efficiencies by fiscal 2026. If this initiative does not achieve the expected financial impact or is not completed in a timely manner, the Company’s financial results and ability to meet its long-term growth expectations could be adversely impacted.

The Company is subject to the loss of a material contract. The Company is a party to several supply, distribution, contract packaging and other material contracts. The loss of a material contract or failure to obtain new material contracts could adversely affect the Company’s financial results.

The Company may be adversely impacted if the Company is unable to protect information technology systems against, or effectively respond to, cyber attacks or security breaches. Information technology systems are an important part of the Company’s business operations. In addition, the Company increasingly relies upon third-party service providers for a variety of business functions, including cloud-based services. Cyber incidents are occurring more frequently across U.S. industries and are being made by groups and individuals with a wide range of motives and expertise. Continued high-profile data security incidents at other companies evidence an external environment that is becoming increasingly hostile. From time to time, the Company has experienced, and may experience in the future, breaches of its security measures due to human error, malfeasance, insider threats, system errors or vulnerabilities or other irregularities, none of which have been material to date. Remote work arrangements may bring additional information technology and data security risks.

Although the Company has programs in place related to business continuity, disaster recovery, and information security initiatives to maintain the confidentiality, integrity, and availability of systems, business applications, and customer information, the Company may not be able to anticipate or implement effective preventive measures against all potential cybersecurity threats, especially because the techniques used change frequently and because attacks can originate from a wide variety of sources, both domestic and foreign. Cybersecurity risk is increasingly difficult to identify and quantify and cannot be fully mitigated because of the rapidly evolving nature of the threats, targets, and consequences.

In addition, the Company is in the midst of multi-year data and technology transformation projects to achieve better analytics, customer service, and process efficiencies. The projects, including modernizing the order-to-cash process, are expected to improve the efficiency and effectiveness of certain financial and business transaction processes and the underlying systems environment. Multiple phases of these projects have already been implemented and additional phases are expected to be implemented in the upcoming years. These implementations are a major undertaking from a financial, management, and personnel perspective and may prove to be more difficult, costly, or time consuming than expected, and there can be no assurance that these projects will be beneficial to the extent anticipated.

Deterioration of labor relations, labor availability or increases in labor costs could harm the Company’s business. As of October 29, 2023, the Company employed approximately 20,000 people worldwide, of which approximately 20 percent were represented by labor unions, principally the United Food and Commercial Workers Union. Union contracts at two of the Company's manufacturing facilities, covering approximately 250 employees, will expire during fiscal 2024. A significant increase in labor costs or a deterioration of labor relations at any of the Company’s facilities or co-manufacturing facilities resulting in work slowdowns or stoppages could harm the Company’s financial results. Labor and skilled labor availability challenges could continue to have an adverse effect on the Company's business.

8

Industry Risks

The Company’s operations are subject to the general risks of the food industry. The food products manufacturing industry is subject to the risks posed by:

▪food spoilage;

▪food contamination caused by disease-producing organisms or pathogens, such as Listeria monocytogenes, Salmonella, and pathogenic E coli.;

▪food allergens;

▪nutritional and health-related concerns;

▪federal, state, and local food processing controls;

▪consumer product liability claims;

▪product tampering; and

▪the possible unavailability and/or expense of liability insurance.

The pathogens that may cause food contamination are found generally in livestock and in the environment and thus may be present in the Company's products. These pathogens can also be introduced to products as a result of improper handling by customers or consumers. The Company does not have control over handling procedures once products have been shipped for distribution. If one or more of these risks were to materialize, the Company’s brand and business reputation could be negatively impacted. In addition, revenues could decrease, costs of doing business could increase, and the Company’s operating results could be adversely affected.

Outbreaks of disease among livestock and poultry flocks could harm the Company’s revenues and operating margins. The Company is subject to risks associated with the outbreak of disease in pork and beef livestock, and poultry flocks, including African swine fever (ASF), Bovine Spongiform Encephalopathy (BSE), pneumo-virus, Porcine Circovirus 2 (PCV2), Porcine Reproduction & Respiratory Syndrome (PRRS), Foot-and-Mouth Disease (FMD), Porcine Epidemic Diarrhea Virus (PEDv), and Highly Pathogenic Avian Influenza (HPAI). The outbreak of such diseases could adversely affect the Company’s supply of raw materials, increase the cost of production, reduce utilization of the Company’s harvest facilities, and reduce operating margins. The impact of global climate change may increase these risks due to changes in weather or migratory patterns which may result in certain types of diseases occurring more frequently or with more intense effects. Additionally, the outbreak of disease may hinder the Company’s ability to market and sell products both domestically and internationally.

In recent years, the outbreak of ASF has impacted hog herds in China, Asia, Europe, and the Caribbean. If an outbreak of ASF were to occur in the U.S., the Company's supply of hogs and pork could be materially impacted.

HPAI was detected within the Company's turkey supply chain during the fourth quarter of fiscal 2023 and first quarter of fiscal 2024. The impact of HPAI has reduced and will continue to reduce production volume in the Company's turkey facilities into fiscal 2024. The Company is continuing to monitor the situation and will take the appropriate actions to protect the health of the turkeys across the supply chain.

The Company has developed business continuity plans for various disease scenarios and will continue to update these plans as necessary. There can be no assurance given, however, that these plans will be effective in eliminating the negative effects of any such diseases on the Company’s operating results.

Fluctuations in commodity prices and availability of raw materials and other inputs could harm the Company’s earnings. The Company’s results of operations and financial condition are largely dependent upon the cost and supply of pork, poultry, beef, feed grains, and nuts as well as supplies, energy and other inputs and the selling prices for many of the Company's products, which are determined by constantly changing market forces of supply and demand.

The Company takes a balanced approach to sourcing pork raw materials, including hogs purchased for the Austin, Minnesota processing facility, long-term supply agreements for pork, and spot market purchases of pork. This approach ensures a more stable supply of raw materials while minimizing extreme fluctuations in costs over the long-term. This may result, in the short-term, in higher or lower live hog costs compared to the cash spot market. Market-based pricing on certain product lines, and lead time required to implement pricing adjustments, may prevent all or part of these cost increases from being recovered, and these higher costs could adversely affect the Company's short-term financial results.

The Company raises turkeys and contracts with turkey growers to meet its raw material requirements for whole birds and processed turkey products. Results in these operations are affected by the cost and supply of feed grains, which fluctuate due to climate conditions, production forecasts, and supply and demand conditions at local, regional, national, and worldwide markets. The Company attempts to manage some of its short-term exposure to fluctuations in feed prices by forward buying, using futures contracts, and pursuing pricing advances. However, these strategies may not be adequate to overcome sustained increases in market prices due to alternate uses for feed grains or other changes in these market conditions.

9

The Company may be subject to decreased availability or less favorable pricing for nuts, tomatoes, avocados, or other produce if poor growing conditions have a negative effect on agricultural productivity. Reductions in crop size or quality due to unfavorable growing conditions may have an adverse effect on the Company’s results.

The supplies of natural and organic proteins may impact the Company’s ability to ensure a continuing supply of these products. To mitigate this risk, the Company partners with multiple long-term suppliers.

International trade barriers and other restrictions or disruptions could result in decreased foreign demand and increased domestic supply of proteins, thereby potentially lowering prices. The Company occasionally utilizes in-country production to limit this exposure.

Market demand for the Company’s products may fluctuate. The Company faces competition from producers of alternative meats and protein sources, including pork, beef, turkey, chicken, fish, nuts, nut butters, whey, and plant-based proteins. The factors on which the Company competes include:

▪price;

▪product quality and attributes;

▪brand identification;

▪breadth of product line; and

▪customer service.

Demand for the Company’s products is also affected by competitors’ promotional spending, the effectiveness of the Company’s advertising and marketing programs, and consumer perceptions. Failure to identify and react to changes in food trends such as sustainability of product sources and animal welfare could lead to, among other things, reduced demand for the Company’s brands and products. The Company may be unable to compete successfully on any or all of these factors in the future.

Damage to the Company’s reputation or brand image can adversely affect its business. Maintaining and continually enhancing the perception of the Company’s reputation and brands is critical to business success. The Company’s reputation and brands have been in the past and could in the future be adversely impacted by a number of factors, including unfavorable consumer perception related to events or rumors, adverse publicity, and negative information disseminated through social and digital media. Failure to maintain, extend, and expand the Company’s reputation or brand image could adversely impact operating results.

Climate change, or legal, regulatory or market measures to address climate change, could have an adverse impact on the Company’s business and results of operations. There is growing concern that carbon dioxide and other greenhouse gases in the atmosphere may have an adverse impact on global temperatures, weather patterns, and the frequency and severity of extreme weather and natural disasters. If such climate change has a negative impact on agricultural productivity, the Company may have decreased availability or less favorable pricing for the raw materials necessary for its operations. Climate change may also cause decreased availability or less favorable pricing for water, which could have an adverse effect on the Company’s operations and supply chain. In addition, natural disasters and extreme weather, including those caused by climate change, could cause disruptions in the Company’s operations and supply chain.

The increasing concern over climate change may also result in greater local, state, federal, and foreign legal requirements, including requirements to limit greenhouse gas emissions or conserve water usage. If such requirements are enacted, the Company could experience significant cost increases in its operations and supply chain.

The Company has developed and publicly announced goals to reduce its impact on the environment such as the 20 by 30 Challenge and the recently announced validation of its greenhouse gas reduction targets by the Science Based Targets initiative. The Company's ability to achieve these goals is subject to numerous factors and conditions, many of which are outside of its control. Examples include, among others, evolving regulatory requirements, disclosure frameworks, and methodologies for reporting data. Failure to accomplish goals set by the Company related to climate change or meet expectations of various Company stakeholders may cause decreased demand for the Company’s products and have an adverse effect on results of operations.

Legal and Regulatory Risks

The Company’s operations are subject to the general risks of litigation. The Company is involved on an ongoing basis in litigation arising in the ordinary course of business. Trends in litigation may include class actions involving employees, consumers, competitors, suppliers, shareholders, or others, and claims relating to product liability, contract disputes, antitrust regulations, intellectual property, advertising, labeling, wage and hour laws, employment practices or environmental matters. Neither litigation trends nor the outcomes of litigation can be predicted with certainty and adverse litigation trends and outcomes could negatively affect the Company’s financial results.

10

Government regulation, present and future, exposes the Company to potential sanctions and compliance costs that could adversely affect the Company’s business. The Company’s operations are subject to extensive regulation by the U.S. Department of Homeland Security, the U.S. Department of Agriculture, the U.S. Food and Drug Administration, federal and state taxing authorities and other federal, state, and local authorities which oversee workforce immigration, taxation, animal welfare, food safety, and the processing, packaging, storage, distribution, advertising, and labeling of the Company’s products. The Company’s manufacturing facilities and products are subject to ongoing inspection by federal, state and local authorities. Claims or enforcement proceedings could be brought against the Company in the future. The availability of government inspectors due to a government furlough could also cause disruption to the Company’s manufacturing facilities. Additionally, the Company is subject to new or modified laws, regulations, and accounting standards. The Company’s failure or inability to comply with such requirements could subject the Company to civil remedies, including fines, injunctions, recalls or seizures, as well as potential criminal sanctions. A federal district court ruling has had a negative impact on harvest capacity and labor costs. Harvest facilities the Company uses are negotiating to resolve the situation and expect to reach a solution, but harvest capacity and labor costs may continue to be negatively impacted until a solution is reached. There can be no assurance a solution will be reached, in which case the negative impacts of the ruling would continue.

The Company is subject to stringent environmental regulations and potentially subject to environmental litigation, proceedings, and investigations. The Company’s past and present business operations and ownership and operation of real property are subject to stringent federal, state, and local environmental laws and regulations pertaining to the discharge of materials into the environment and the handling and disposition of wastes (including solid and hazardous wastes) or otherwise relating to protection of the environment. Compliance with these laws and regulations, as well as any modifications, is material to the Company’s business. Some of the Company’s facilities have been in operation for many years and, over time, the Company and other prior operators of these facilities may have generated and disposed of wastes that now may be considered hazardous. Future discovery of contamination of property underlying or in the vicinity of the Company’s present or former properties or manufacturing facilities and/or waste disposal sites could require the Company to incur additional expenses related to additional investigation, assessment or other requirements. The occurrence of any of these events, the implementation of new laws and regulations or stricter interpretation of existing laws or regulations could adversely affect the Company’s financial results.

The Company’s foreign operations pose additional risks to the Company’s business. The Company operates its business and markets its products internationally. The Company’s foreign operations are subject to the risks described above, as well as risks related to fluctuations in currency values, foreign currency exchange controls, compliance with foreign laws, compliance with applicable U.S. laws, including the Foreign Corrupt Practices Act, and other economic or political uncertainties. International sales are subject to risks related to general economic conditions, imposition of tariffs, quotas, trade barriers and other restrictions, enforcement of remedies in foreign jurisdictions and compliance with applicable foreign laws, and other economic and political uncertainties. All of these risks could result in increased costs or decreased revenues, which could adversely affect the Company’s financial results.

Item 1B. UNRESOLVED STAFF COMMENTS

None.

11

Item 2. PROPERTIES

The Company's global headquarters are located in Austin, Minnesota. The Company has various processing plants, warehouses and operational facilities, mainly located in the U.S. The Company maintains a national sales force through strategic placement of sales offices across the U.S. Properties are also maintained internationally to support global processing and sales. A majority of the Company's property is owned. Leased property is used as needed for production, distribution, and sales.

The Company believes its operating facilities are well maintained and suitable for current production volumes. The Company regularly engages in construction and other capital improvement projects with a focus on value-added capacity projects and automation.

Many of the Company's domestic properties are utilized by more than one segment and utilization of these facilities can change over time. Therefore, it is impracticable to disclose them by segment. The facilities outside the U.S. serve the International segment.

Area (1) Square feet, in thousands | Production Facilities | Warehouse/Distribution Centers | Administration/Sales/Research Offices | Total | Leased | Owned | |||||||||||||||||

| Arizona | — | — | 2 | 2 | 2 | — | |||||||||||||||||

| Arkansas | 589 | — | 9 | 598 | 9 | 589 | |||||||||||||||||

| California | 323 | 428 | 54 | 805 | 656 | 149 | |||||||||||||||||

| Colorado | 829 | — | 10 | 839 | 10 | 829 | |||||||||||||||||

| Florida | — | — | 5 | 5 | 5 | — | |||||||||||||||||

| Georgia | 259 | — | — | 259 | — | 259 | |||||||||||||||||

| Illinois | 738 | — | 22 | 760 | 22 | 738 | |||||||||||||||||

| Iowa | 1,482 | 658 | 3 | 2,143 | 283 | 1,860 | |||||||||||||||||

| Kansas | 312 | — | 3 | 315 | 3 | 312 | |||||||||||||||||

| Massachusetts | — | — | 4 | 4 | 4 | — | |||||||||||||||||

| Michigan | — | — | 3 | 3 | 3 | — | |||||||||||||||||

| Minnesota | 3,761 | 219 | 554 | 4,534 | 89 | 4,445 | |||||||||||||||||

| Nebraska | 845 | — | — | 845 | — | 845 | |||||||||||||||||

| New Jersey | — | — | 29 | 29 | 29 | — | |||||||||||||||||

| North Carolina | — | — | 3 | 3 | 3 | — | |||||||||||||||||

| Ohio | — | 453 | 8 | 461 | 322 | 139 | |||||||||||||||||

| Pennsylvania | 13 | 348 | 9 | 370 | 357 | 13 | |||||||||||||||||

| Texas | 285 | — | 2 | 287 | 2 | 285 | |||||||||||||||||

| Utah | — | 209 | — | 209 | 209 | — | |||||||||||||||||

Virginia | 625 | — | — | 625 | — | 625 | |||||||||||||||||

| Washington | — | — | 2 | 2 | 2 | — | |||||||||||||||||

| Wisconsin | 1,227 | 102 | 3 | 1,332 | 107 | 1,225 | |||||||||||||||||

| Total Domestic | 11,288 | 2,417 | 725 | 14,430 | 2,117 | 12,313 | |||||||||||||||||

| Australia | — | — | 2 | 2 | 2 | — | |||||||||||||||||

| Brazil | 440 | — | 3 | 443 | 440 | 3 | |||||||||||||||||

| China | 842 | 33 | 26 | 901 | 2 | 899 | |||||||||||||||||

| Total International | 1,282 | 33 | 31 | 1,346 | 444 | 902 | |||||||||||||||||

| Total Square Feet | 12,570 | 2,450 | 756 | 15,776 | 2,561 | 13,215 | |||||||||||||||||

(1) Turkey growout facilities are excluded.

12

Item 3. LEGAL PROCEEDINGS

On August 15, 2023, the Company received an unexpected, unfavorable arbitration ruling involving an isolated commercial dispute with a third party. Pursuant to the ruling, the arbitrator awarded $59.6 million in damages, plus prejudgment interest of $5.3 million and attorneys’ fees, to the counterparty payable by the Company. The pre-tax impact of the adverse arbitration ruling of $68.3 million is reflected in Selling, General, and Administrative expenses in the Consolidated Statements of Operations for fiscal 2023. The arbitration award amount was paid in full by the Company in the fourth quarter of fiscal 2023. The adverse arbitration ruling is not subject to further appeal or judicial review. Standard confidentiality provisions in the arbitration rules prohibit the Company from commenting on the substance of the ruling.

Information regarding other legal proceedings is available in Note J - Commitments and Contingencies of the Notes to the Consolidated Financial Statements.

Item 4. MINE SAFETY DISCLOSURES

Not applicable.

Information About Executive Officers

| CURRENT OFFICE AND PREVIOUS | ||||||||||||||||||||

| NAME | AGE | FIVE YEARS EXPERIENCE | DATES | |||||||||||||||||

| James P. Snee | 56 | Chairman of the Board, President and Chief Executive Officer | 11/20/17 to Present | |||||||||||||||||

| Jacinth C. Smiley | 55 | Executive Vice President and Chief Financial Officer | 01/01/22 to Present | |||||||||||||||||

| Group Vice President (Corporate Strategy) | 04/05/21 to 12/31/21 | |||||||||||||||||||

| Vice President and Chief Accounting Officer, LyondellBasell | 04/01/18 to 04/04/21 | |||||||||||||||||||

| Deanna T. Brady | 58 | Executive Vice President (Retail) | 10/31/22 to Present | |||||||||||||||||

| Executive Vice President (Refrigerated Foods) | 10/28/19 to 10/30/22 | |||||||||||||||||||

| Group Vice President/President Consumer Product Sales | 10/26/15 to 10/27/19 | |||||||||||||||||||

| Mark A. Coffey | 61 | Group Vice President (Supply Chain) | 04/26/21 to Present | |||||||||||||||||

| Senior Vice President (Supply Chain and Manufacturing) | 03/28/17 to 04/25/21 | |||||||||||||||||||

| Swen Neufeldt | 50 | Group Vice President (Hormel Foods International Corporation) | 06/29/20 to Present | |||||||||||||||||

| Vice President (Meat Products) | 10/31/16 to 06/28/20 | |||||||||||||||||||

| Mark J. Ourada | 58 | Group Vice President (Foodservice) | 03/05/18 to Present | |||||||||||||||||

| Katherine M. Losness-Larson | 58 | Senior Vice President (Human Resources) | 10/31/22 to Present | |||||||||||||||||

| Director of Human Resources | 10/29/18 to 10/30/22 | |||||||||||||||||||

| Pierre M. Lilly | 52 | Senior Vice President and Chief Compliance Officer | 10/26/20 to Present | |||||||||||||||||

| Director of Internal Audit | 05/30/16 to 10/25/20 | |||||||||||||||||||

| Kevin L. Myers, Ph.D. | 58 | Senior Vice President (Research and Development, Quality Control) | 03/30/15 to Present | |||||||||||||||||

| Paul R. Kuehneman | 52 | Vice President and Controller | 02/18/22 to Present | |||||||||||||||||

| Assistant Controller | 01/04/21 to 02/17/22 | |||||||||||||||||||

| Vice President and CFO (Jennie-O Turkey Store) | 05/30/16 to 01/03/21 | |||||||||||||||||||

No family relationship exists among the executive officers.

Executive officers are designated annually by the Board of Directors at the first meeting following the Annual Meeting of Stockholders. Vacancies may be filled and additional officers elected at any time. The Company's Chief Executive Officer has the authority to appoint and remove Vice Presidents (other than Executive Vice Presidents, Group Vice Presidents, and Senior Vice Presidents).

13

PART II

Item 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Hormel Foods Corporation’s common stock is traded on the New York Stock Exchange under the symbol HRL. The CUSIP number is 440452100.

Holders

There are approximately 10,000 record stockholders and 270,000 stockholders whose shares are held in street name by brokerage firms and financial institutions.

There were no issuer purchases of equity securities in the quarter ended October 29, 2023. On January 29, 2013, the Company's Board of Directors authorized the repurchase of 10,000,000 shares of its common stock with no expiration date. On January 26, 2016, the Board of Directors approved a two-for-one split of the Company’s common stock to be effective January 27, 2016. As part of the stock split resolution, the number of shares remaining to be repurchased was adjusted proportionately. The maximum number of shares that may yet be purchased under the repurchase plans or programs as of October 29, 2023 is 3,677,494.

Dividends

The Company has paid dividends for 381 consecutive quarters. The annual dividend rate for fiscal 2024 will increase to $1.13 per share, representing the 58th consecutive annual dividend increase. The Company is dedicated to returning excess cash flow to shareholders through dividend payments.

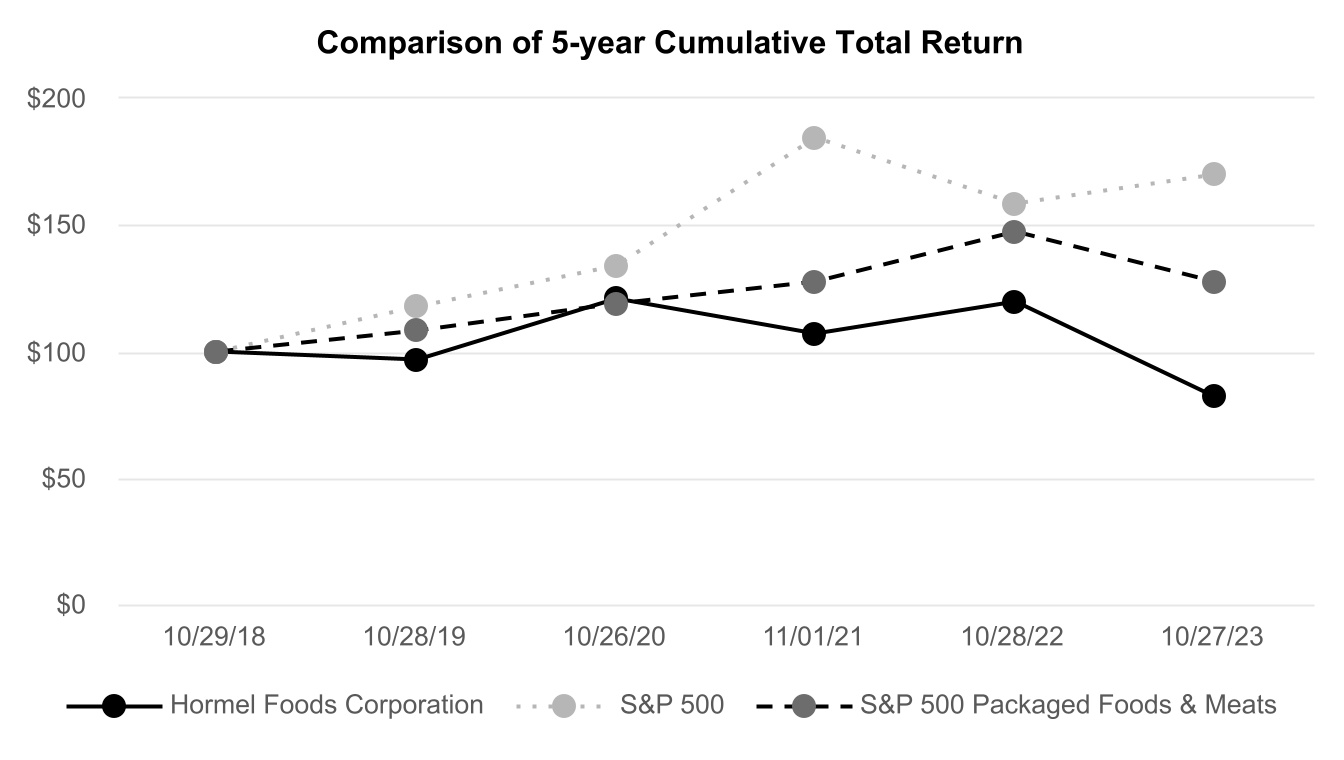

Shareholder Return Performance Graph

The following graph shows a comparison of cumulative total shareholder return, calculated on a dividend-reinvested basis, for the Company, the S&P 500 Index, and the S&P 500 Packaged Foods & Meats Index for the five years ended October 29, 2023. The graph assumes $100 was invested in each as of the market close on October 29, 2018. Note that historic stock price performance is not necessarily indicative of future stock price performance.

14

Item 6. RESERVED

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Executive Overview

Fiscal 2023: The Company achieved its second consecutive year of net sales in excess of $12 billion in fiscal 2023. Net sales were $12.1 billion, declining 3 percent compared to the prior year, as the benefit from pricing actions to mitigate inflationary pressures was more than offset by the impact of lower volumes in the Retail and International segments and lower net pricing in certain categories, such as bacon, reflecting raw material commodity deflation. Volume declined for the full year, primarily due to declines in commodity pork availability as a result of the Company's new pork supply agreement and lower turkey supply in the first half of the year due to the impacts of HPAI. Segment profit declined 11 percent, as higher results in the Foodservice segment were more than offset by significantly lower results in the Retail and International segments. Net earnings declined 21 percent due to lower segment profit and the pre-tax impact of an adverse arbitration ruling of $68.3 million. Adjusted net earnings(1) — excluding the impact of the adverse arbitration ruling, non-cash impairment charges, and costs associated with the Company's transformation and modernization initiative — declined 12 percent. Diluted net earnings per share and adjusted diluted net earnings per share(1) for fiscal 2023 were $1.45 and $1.61, respectively, compared to $1.82 last year.

Segment profit for the Foodservice segment increased due to improved mix across the portfolio. Retail segment profit declined significantly for the full year, driven primarily by lower volumes, unfavorable mix, and higher operating expenses, partially offset by the benefit from pricing actions across the portfolio and higher equity in earnings from MegaMex Foods, LLC (MegaMex Foods). International segment profit declined due to lower sales in China and lower turkey commodity sales.

The Company again reinvested into the business through capital expenditures and returned a record amount of cash to shareholders in the form of dividends. Capital expenditures in fiscal 2023 were $270 million, including investments in new production capabilities for retail and foodservice pepperoni and an expansion for the SPAM® family of products. The Company continues to prioritize investments in growth, innovation, cost savings, automation, and maintenance. The annual dividend for 2024 will be $1.13 per share, representing an increase of 3 percent and marking the 58th consecutive year of dividend increases.

During fiscal 2023, the Company purchased a 30% common stock interest in Garudafood, a food and beverage company in Indonesia. This investment expands the Company's presence in Southeast Asia and supports the global execution of the snacking and entertaining strategic priority. The Company obtained this minority interest in Garudafood for a purchase price of $426 million, including associated transaction costs. The Company funded this transaction with cash on hand.

Fiscal 2024 Outlook(2): The Company continues to navigate through a dynamic operating environment characterized by slowing consumer demand, inflationary pressures, and headwinds in its turkey business. Net sales growth of 1 percent to 3 percent is expected and assumes volume growth in key categories, higher brand support and innovation, a benefit from incremental pricing actions, and the current assumptions for raw material input costs. From a bottom-line perspective, diluted net earnings per share are expected to be $1.43 to $1.57 and adjusted diluted net earnings per share(1) are expected to be $1.51 to $1.65. Earnings are expected to decline in the first half of the year due to the impact from lower turkey markets, lower volumes in the Retail segment, expenses associated with the transformation and modernization initiative, and softness in the Company's China business. Segment profit growth from all three segments is expected in the back half of the year as these pressures abate and as benefits from the transformation and modernization initiative are realized. Major risks to the outlook include incremental inflationary pressures, significantly lower turkey markets than expected, and the impact of deteriorating macroeconomic conditions on the Company's customers, consumers, and operators.

The Company remains in a strong financial position due to its consistent cash flow, liquidity, and strong balance sheet. The Company plans to continue to support the business through increased marketing and advertising investments for its leading brands as well as investments into its production capabilities, including converting the Barron, Wisconsin, plant into a value-added facility to support growth across the portfolio. The Company is also expanding capacity for high-demand Planters® snack nuts items. Returning cash to shareholders in the form of dividends remains a top priority for the Company.

Consistent with the plan outlined at its recent investor day, the Company expects fiscal 2024 to be a year of investment and remains focused on its strategic priorities, executing on its transformation and modernization initiative, fueling its innovation pipeline, and exiting the year with momentum in its business segments. For fiscal 2024, the Company expects a modest benefit to net earnings from its transformation and modernization initiative.

15

A detailed review of the Company's fiscal 2023 performance compared to fiscal 2022 appears in the following section. A detailed review of fiscal 2022 performance compared to fiscal 2021 is also provided due to the change in reportable segments which occurred in the first quarter of fiscal 2023.

(1) See the "Non-GAAP Financial Measures" section below for a description of the Company's use of measures not defined by U.S. generally accepted accounting principles (GAAP).

(2) All forward-looking comparisons for fiscal 2024 are comparing fiscal 2023 GAAP figures to projected fiscal 2024 GAAP figures, unless otherwise noted.

Results of Operations

OVERVIEW

The Company is a processor of branded and unbranded food products for retail, foodservice, deli, and commercial customers.

The Company transitioned to a new operating model in the first quarter of fiscal 2023 and now reports its results in the following three reportable segments:

The Retail segment consists primarily of the processing, marketing, and sale of food products sold predominantly in the retail market. This segment also includes the results from the Company’s MegaMex Foods, LLC joint venture.

The Foodservice segment consists primarily of the processing, marketing, and sale of food and nutritional products for foodservice, convenience store, and commercial customers.

The International segment processes, markets, and sells Company products internationally. This segment also includes the results from the Company’s international joint ventures, equity method investments, and royalty arrangements.

Prior period segment results have been retrospectively recast to reflect the new reportable segments.

The Company’s fiscal year consisted of 52 weeks in fiscal years 2023 and 2022 and 53 weeks in fiscal year 2021. Fiscal year 2024 will consist of 52 weeks.

FISCAL YEARS 2023 AND 2022

CONSOLIDATED RESULTS

Net Earnings and Diluted Earnings Per Share

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| In thousands, except per share amounts | October 29, 2023 | October 30, 2022 | % Change | October 29, 2023 | October 30, 2022 | % Change | ||||||||||||||||||||||||||||||||

| Net Earnings | $ | 195,935 | $ | 279,883 | (30.0) | $ | 793,572 | $ | 999,987 | (20.6) | ||||||||||||||||||||||||||||

| Diluted Earnings Per Share | 0.36 | 0.51 | (29.4) | 1.45 | 1.82 | (20.3) | ||||||||||||||||||||||||||||||||

Adjusted Diluted Earnings Per Share(1) | 0.42 | 0.51 | (17.2) | 1.61 | 1.82 | (11.4) | ||||||||||||||||||||||||||||||||

(1) See the "Non-GAAP Financial Measures" section below for a description of the Company's use of measures not defined by U.S. generally accepted accounting principles (GAAP).

Volume and Net Sales

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| In thousands | October 29, 2023 | October 30, 2022 | % Change | October 29, 2023 | October 30, 2022 | % Change | ||||||||||||||||||||||||||||||||

| Volume (lbs.) | 1,155,445 | 1,160,490 | (0.4) | 4,411,738 | 4,604,169 | (4.2) | ||||||||||||||||||||||||||||||||

| Net Sales | $ | 3,198,079 | $ | 3,283,475 | (2.6) | $ | 12,110,010 | $ | 12,458,806 | (2.8) | ||||||||||||||||||||||||||||

Volume for the fourth quarter of fiscal 2023 was comparable with last year, as higher turkey volumes in each segment were offset by lower Retail volumes in the convenient meals and proteins and the snacking and entertaining verticals. Net sales declined in the fourth quarter, as higher Foodservice segment sales and the benefit from higher turkey volumes were more than offset by lower volumes in the Retail segment and continued pressure in the International segment.

Fiscal 2023 marked the second consecutive year of net sales in excess of $12 billion. Net sales declined for the full year, as the benefit from pricing actions to mitigate inflationary pressures was more than offset by the impact of lower volumes in the Retail and International segments and lower net pricing in certain categories, such as bacon, reflecting raw material commodity

16

deflation. The primary drivers of lower volume in fiscal 2023 were declines in commodity pork availability as a result of the Company's new pork supply agreement and lower turkey supply in the first half of the year from the impacts of HPAI.

In fiscal 2024, the Company expects sales growth, which assumes benefits from modestly higher volumes, growth in key categories, higher brand support and innovation, incremental pricing actions, and the current assumptions for raw material costs. Risks to this outlook include slowing consumer demand and greater-than-expected pricing headwinds in the turkey business.

Cost of Products Sold

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| October 29, | October 30, | October 29, | October 30, | |||||||||||||||||||||||||||||||||||

| In thousands | 2023 | 2022 | % Change | 2023 | 2022 | % Change | ||||||||||||||||||||||||||||||||

| Cost of Products Sold | $ | 2,683,655 | $ | 2,717,058 | (1.2) | $ | 10,110,169 | $ | 10,294,120 | (1.8) | ||||||||||||||||||||||||||||

Cost of products sold for the fourth quarter and full year of fiscal 2023 decreased due to lower sales. On a volume basis, cost of products sold increased 2 percent in fiscal 2023, driven primarily by inflationary pressures stemming from, among other inputs, packaging, logistics, and labor.

In fiscal 2024, costs are expected to moderate relative to the high levels of inflation the business has absorbed since the beginning of fiscal 2021. Raw material input costs for pork, beef, and feed are anticipated to remain volatile and above historical levels. The Company expects its transformation and modernization initiative to begin delivering modest cost savings in fiscal 2024, targeting packaging, logistics, and production costs.

Gross Profit

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| October 29, | October 30, | October 29, | October 30, | |||||||||||||||||||||||||||||||||||

| In thousands | 2023 | 2022 | % Change | 2023 | 2022 | % Change | ||||||||||||||||||||||||||||||||

| Gross Profit | $ | 514,425 | $ | 566,417 | (9.2) | $ | 1,999,841 | $ | 2,164,686 | (7.6) | ||||||||||||||||||||||||||||

Percent of Net Sales | 16.1 | % | 17.3 | % | 16.5 | % | 17.4 | % | ||||||||||||||||||||||||||||||

Consolidated gross profit as a percent of net sales for the fourth quarter and full year of fiscal 2023 decreased, driven primarily by unfavorable mix in the Retail and International segments and the persistent impact of inflationary pressures. Pricing actions helped mitigate some of the impact from inflationary pressures. Compared to fiscal 2022, gross profit as a percent of net sales for the fourth quarter and full year increased for the Foodservice segment but declined for the Retail and International segments.

In fiscal 2024, the Company expects gross profit as a percent of net sales to be comparable to fiscal 2023. Incremental cost inflation and unfavorable sales mix pose the largest risks to this outlook.

Selling, General, and Administrative (SG&A)

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| In thousands | October 29, 2023 | October 30, 2022 | % Change | October 29, 2023 | October 30, 2022 | % Change | ||||||||||||||||||||||||||||||||

| SG&A | $ | 216,546 | $ | 206,487 | 4.9 | $ | 942,167 | $ | 879,265 | 7.2 | ||||||||||||||||||||||||||||

Percent of Net Sales | 6.8 | % | 6.3 | % | 7.8 | % | 7.1 | % | ||||||||||||||||||||||||||||||

Adjusted Percent of Net Sales(1) | 6.6 | % | 6.3 | % | 7.1 | % | 7.1 | % | ||||||||||||||||||||||||||||||

(1) See the "Non-GAAP Financial Measures" section below for a description of the Company's use of measures not defined by U.S. generally accepted accounting principles (GAAP).

SG&A expenses for the fourth quarter of fiscal 2023 increased as higher professional service expense related to the Company's transformation and modernization initiative and higher advertising expense were partially offset by lower employee-related expenses. For full year fiscal 2023, the increase in SG&A expenses and SG&A expenses as a percent of net sales is attributed to an adverse arbitration ruling totaling $68.3 million. Adjusted SG&A expenses as a percent of net sales(1) for fiscal 2023 were comparable to the prior year.

Advertising investments in fiscal 2023 were $160 million, representing a 2% increase compared to fiscal 2022.

In fiscal 2024, the Company intends to continue investing in its leading brands and for full year advertising expense to increase compared to the prior year.

Research and development continues to be a vital part of the Company's strategy to grow existing brands and expand into new branded items. Research and development expenses were $33.7 million in fiscal 2023, compared to $34.7 million in fiscal 2022.

17

Equity in Earnings of Affiliates

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| October 29, | October 30, | October 29, | October 30, | |||||||||||||||||||||||||||||||||||

| In thousands | 2023 | 2022 | % Change | 2023 | 2022 | % Change | ||||||||||||||||||||||||||||||||

| Equity in Earnings of Affiliates | $ | 541 | $ | 7,234 | (92.5) | $ | 42,754 | $ | 27,185 | 57.3 | ||||||||||||||||||||||||||||

Equity in earnings of affiliates for the fourth quarter of fiscal 2023 decreased, resulting from the $7.0 million impairment of a corporate venturing investment. Equity in earnings of affiliates for the full year of fiscal 2023 increased due to significantly higher results for MegaMex Foods, reflecting a benefit from pricing actions and lower avocado input costs.

The Company accounts for its majority-owned operations under the consolidation method. Investments in which the Company owns a minority interest, and for which there are no other indicators of control, are accounted for under the equity or cost method. These investments, including balances due to or from affiliates, are included on the Consolidated Statements of Financial Position as Investments in Affiliates. The composition of this line item as of October 29, 2023, was as follows:

| In thousands | Investments in Affiliates | ||||

| U.S. | $ | 214,019 | |||

| Foreign | 511,103 | ||||

| Total | $ | 725,121 | |||

Goodwill and Intangible Impairment

An impairment charge related to the Justin's® trade name of $28.4 million was recorded in the fourth quarter of fiscal 2023.

Interest and Investment Income and Interest Expense

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||||||||||

| October 29, | October 30, | October 29, | October 30, | |||||||||||||||||||||||||||||||||||

| In thousands | 2023 | 2022 | % Change | 2023 | 2022 | % Change | ||||||||||||||||||||||||||||||||

| Interest and Investment Income | $ | (5,872) | $ | 7,933 | (174.0) | $ | 14,828 | $ | 28,012 | (47.1) | ||||||||||||||||||||||||||||

| Interest Expense | 18,360 | 17,602 | 4.3 | 73,402 | 62,515 | 17.4 | ||||||||||||||||||||||||||||||||

Interest and investment income decreased in the fourth quarter of fiscal 2023 primarily due to higher pension costs. Interest and investment income decreased for the full year of fiscal 2023 due to higher pension costs, partially offset by increased interest income and improved performance on the rabbi trust. Interest expense increased in fiscal 2023 due to the impact of an interest rate swap.

Effective Tax Rate

| Fourth Quarter Ended | Fiscal Year Ended | |||||||||||||||||||||||||

| October 29, | October 30, | October 29, | October 30, | |||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| Effective Tax Rate | 20.5 | % | 21.7 | % | 21.8 | % | 21.7 | % | ||||||||||||||||||

The effective tax rate for fiscal 2023 reflects a benefit related to the deduction for foreign-derived intangible income. The fiscal 2022 effective tax rate included a benefit for stock option exercises. For additional information, refer to Note N - Income Taxes of the Notes to the Consolidated Financial Statements.

The Company expects the effective tax rate in fiscal 2024 to be between 21.0 and 23.0 percent.

18

SEGMENT RESULTS