UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the fiscal year ended December 31 , 2023

or

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the transition period from to

(Address of principal executive offices)

(704 ) 885-2555

(Registrant's telephone number, including area code)

| Commission file number | Exact name of registrant as specified in its charter | IRS Employer Identification No. | State or other jurisdiction of incorporation or organization | ||||||||

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on which registered | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. ☐ Large accelerated filer ☑ Accelerated filer ☐ Non-accelerated filer ☐ Small reporting company ☐ Emerging Growth Company

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑ .

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Based on the closing price as of June 30, 2023, the aggregate market value of the Common Stock of the Registrant held by non‑affiliates was $112.7 million.

Common Stock outstanding on February 26, 2024 totaled 45,147,547 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement to be delivered to shareholders in connection with the Annual Meeting of Shareholders to be held on May 10, 2024 are incorporated by reference into Part III.

GLATFELTER CORPORATION

ANNUAL REPORT ON FORM 10-K

For the Year Ended

December 31, 2023

Table of Contents

| Page | ||||||||

| Item 6 | ||||||||

Report of Independent Registered Public Accounting Firm (PCAOB ID # | ||||||||

| Item 9B | ||||||||

| Item 9C | ||||||||

PART I

Glatfelter Corporation makes regular filings with the Securities and Exchange Commission (“SEC”), including this Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. These filings are available, free of charge, on our website, www.glatfelter.com, and the SEC’s website at www.sec.gov. We also provide copies of our SEC filings at no charge upon request to Investor Relations at (717) 225-2746, ir@glatfelter.com, or by mail to Investor Relations, 4350 Congress Street, Suite 600, Charlotte, NC 28209. In this filing, unless the context indicates otherwise, the terms “we,” “our,” “us,” “the Company,” or “Glatfelter” refer to Glatfelter Corporation and subsidiaries.

The following discussion of our Business sets forth an update of the material developments since our most recent full discussion included in Item 1 – “Business” of our 2022 Annual Report on Form 10-K filed with the SEC on February 27, 2023.

ITEM 1 BUSINESS

Overview Glatfelter is a leading global supplier of engineered materials. Our high-quality, innovative, and customizable solutions are found in tea and single-serve coffee filtration, personal hygiene, as well as in many diverse packaging, home improvement and industrial applications. Our 2023 net sales were approximately $1.4 billion with customers in over 100 countries. Our operations utilize a variety of manufacturing technologies including airlaid, wetlaid, and spunlace with fifteen manufacturing sites located in the United States, Canada, Germany, the United Kingdom, France, Spain, and the Philippines. We have sales offices in all major geographies serving customers under the Glatfelter and Sontara brands.

In 2022, Glatfelter began its turnaround strategy in conjunction with the appointment of Thomas Fahnemann as the new Chief Executive Officer of the Company. In making the transition, the Board of Directors reaffirmed its view that Glatfelter has the right combination of business segments serving attractive, growth-oriented markets and customers with sustainable product offerings, but had brought in a new CEO to address the challenges impacting Glatfelter’s financial performance while charting a new direction to unlock the full value of Glatfelter. In 2023, Glatfelter continued to deliver benefits from the turnaround strategy under new CEO leadership and the benefits from the program helped offset most of the the adverse impacts from volume declines and related machine downtimes. The turnaround strategy focuses on six key initiatives to drive profitability improvements:

•Portfolio optimization - Includes reviewing our entire asset portfolio and considering the strategic, financial, and operational value of each asset in the near- and long-term. We are focusing on areas of our portfolio that have scale, or the potential for scale, a strong market leading position and core competencies in manufacturing technology. During 2023, we divested our Ober-Schmitten, Germany and Costa Rica operations both part of the Composite Fibers segment.

•Margin improvement - This is a fundamental part of the turnaround strategy which includes placing greater focus on profitability rather than simple top-line growth. Price increases and energy surcharges implemented during 2022 to combat the significant impact of inflation and higher energy prices were largely maintained through the first quarter of 2023 and to the extent possible much of the year. In 2023, raw material and energy prices started to declined compared to high levels in 2022 and prices for customers with pass-through arrangements started to decline. For customers not on a contractual pass-through agreement, we selectively began to lower prices to maintain volume yet also focused on returning margins closer to pre-pandemic levels.

•Fixed cost reduction - Includes evaluating our fixed costs and taking actions to make significant reductions. We implemented select headcount reductions, partial capacity rationalizations, and created greater emphasis on reduction of indirect spend to deliver significant savings for 2023 and beyond.

•Cash liberation - This initiative is supported by the work on the first three initiatives in our plan. We will focus on paying down debt, decreasing our leverage, and increasing EBITDA. We will continue to make prudent decisions with respect to capital allocation and maintain a disciplined approach to managing our accounts receivables, finished goods inventory and raw material pricing.

•Operational effectiveness - We are driving continuous improvements across our operations, identifying areas for process enhancements and waste reduction, and expanding operational best practices across the organization. In addition, the team has made significant progress on reducing the cost of our supply chain by improving our warehousing, freight, and distribution processes.

GLATFELTER 2023 FORM 10-K | 1 | ||||

•Return Spunlace to profitability - We are executing all the initiatives in our turnaround plan with a heightened sense of urgency of returning our Spunlace segment to profitability. In 2023, the profitability for this segment improved by approximately $9 million compared to 2022 as a result of the actions taken.

We manage our business and make investment decisions under a functional operating model with three distinct reporting segments: Airlaid Materials, Composite Fibers and Spunlace. These segments serve growing global customers and markets providing innovative and customizable solutions, ultimately delivering high-quality engineered materials. As a leading global supplier of engineered materials for consumer and industrial applications, we partner with leading consumer product companies and other market leaders to provide innovative solutions delivering outstanding performance to meet market requirements. Over the past several years, we have divested non-strategic assets and made investments to increase production capacity and improve our technical capabilities to ensure we are best positioned to serve the market demands and grow our sales. We are committed to growing with our key markets and will make appropriate investments to support our customers and satisfy market demands.

In 2021, we completed two significant acquisitions to further our business transformation and in alignment with our stated strategy. On May 13, 2021, we completed the acquisition of all the outstanding equity interests of Georgia-Pacific Mt. Holly LLC, Georgia-Pacific’s U.S. nonwovens business (“Mount Holly”), for $170.9 million. This business includes the Mount Holly, NC manufacturing facility and an R&D center and pilot line for nonwovens product development in Memphis, TN. The Mount Holly facility produces high-quality airlaid products for the wipes, hygiene, and other nonwoven materials markets, competing in the marketplace with nonwoven technologies and substrates, as well as other materials focused primarily on consumer based end-use applications. The Mount Holly acquisition expanded our footprint and income generation in the U.S. and balanced our sales mix between the Airlaid Materials and Composite Fibers segments.

On October 29, 2021, we completed the acquisition of PMM Holding (Luxembourg) AG, and its wholly-owned subsidiaries (“Jacob Holm”), a global leading manufacturer of premium quality spunlace nonwoven fabrics for critical cleaning, high-performance materials, personal care, hygiene and medical applications, for an enterprise value of approximately $304.0 million, including the extinguishment of debt. The combination created an expanded portfolio of engineered specialty applications manufactured on spunlace-based production assets with opportunities for long-term growth aligned with post-COVID lifestyle changes. Jacob Holm's results are reported prospectively from the date of acquisition as Spunlace, a newly established reporting segment.

Additional information related to these acquisitions is set forth in Item 8 – Financial Statements and Supplementary Data - Note 3 – “Acquisitions.”

On February 7, 2024, we announced our entrance into definitive agreements with Berry Global Group, Inc. (NYSE:BERY) for Berry to spin-off and merge the majority of its Health, Hygiene and Specialties segment to include its Global Nonwovens and Films business (“HHNF”) with Glatfelter, to create a leading, publicly-traded company in the specialty materials industry. The new combined company (“NewCo”) will become a global leader in the growing specialty materials industry, serving the world’s largest brand owners across global end markets with favorable long-term growth dynamics.

The proposed transaction represents the next significant milestone in the Company’s time-tested strategy as a leading global supplier of specialty materials. The combination of Berry’s HHNF business and Glatfelter provides meaningful scale given the complementary technology and product portfolios, along with a platform for considerable growth in future periods. The transaction provides NewCo the opportunity to deliver significant value creation for Glatfelter shareholders by immediately deleveraging Glatfelter’s balance sheet and increasing the equity value of the overall enterprise, while also enhancing our credit profile with customers and suppliers. Glatfelter’s recent focus on optimizing its portfolio, managing the price/cost spread dynamic, and driving commercial and operational excellence, along with G&A cost discipline, provides the foundation to meaningfully contribute towards the overall success of NewCo.

Segments Consolidated net sales and the relative net sales contribution of each of our segments for the past three years are summarized below (the data includes the results of the recently completed acquisitions prospectively from the closing date):

Dollars in thousands | 2023 | 2022 | 2021 | ||||||||||||||

| Net sales | $ | 1,385,516 | $ | 1,491,326 | $ | 1,084,694 | |||||||||||

| Operating segment contribution | |||||||||||||||||

| Airlaid Materials | 42.3 | % | 40.4 | % | 43.4 | % | |||||||||||

| Composite Fibers | 34.8 | % | 35.1 | % | 51.3 | % | |||||||||||

| Spunlace | 22.9 | % | 24.5 | % | 5.3 | % | |||||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||

Net tons sold by each segment for the past three years were as follows:

| Metric tons | 2023 | 2022 | 2021 | ||||||||||||||

| Airlaid Materials | 156,442 | 164,844 | 148,134 | ||||||||||||||

| Composite Fibers | 94,742 | 103,092 | 132,196 | ||||||||||||||

| Spunlace | 61,618 | 72,725 | 12,514 | ||||||||||||||

| Inter-segment sales elimination | (1,258) | — | — | ||||||||||||||

| Total | 311,544 | 340,661 | 292,844 | ||||||||||||||

AIRLAID MATERIALS Airlaid Materials, with 2023 net sales of approximately $586.5 million, is a leading global supplier of highly absorbent and engineered cellulose-based airlaid nonwoven materials, primarily used to manufacture consumer products for growing global end-user markets. Our products are composed of all-natural fluff pulp, which is sustainable by design. The categories served by Airlaid Materials include:

•feminine hygiene and other hygiene products;

•specialty wipes;

•tabletop;

•adult incontinence;

•home care;

•food pads; and

•other consumer and industrial products.

Airlaid Materials’ customers are industry leading consumer product companies, as well as private label converters. We believe this business holds a leading position in the majority of the markets it serves. Airlaid Materials has developed long-term customer relationships through superior quality, customer service, and a reputation for quickly bringing product and process innovations to market.

This segment’s net sales composition by categories is set forth in Item 8 – Financial Statements and Supplementary Data - Note 8 – “Revenue. “

The feminine hygiene category accounted for 37.0% and 39.6% of Airlaid Material’s net sales in 2023 and 2022, respectively. Most feminine hygiene sales are to a group of large, leading global consumer products companies. We believe these markets are growth oriented due to population growth in certain geographic regions and changing consumer preferences. In developing regions, demand is also influenced by increases in disposable income and cultural preferences.

Airlaid Materials operates state-of-the-art facilities in Falkenhagen and Steinfurt, Germany, Gatineau, Canada, Fort Smith, Arkansas, and Mount Holly, North Carolina. The segment's five facilities operate with the following combined attributes (in metric tons):

Airlaid Materials Production Capacity | Principal Raw Material (“PRM”) | Estimated Annual Quantity of PRM | ||||||||||||

| 190,000 | Fluff pulp | 130,000 | ||||||||||||

Key raw materials used in the airlaid production process other than fluff pulp include synthetic fibers, super absorbent polymers, and latex. The cost to produce is influenced by the cost of critical raw materials and energy prices. Airlaid Materials purchases substantially all the electricity and natural gas used in its operations. Approximately 77% of this segment’s net sales in 2023 was earned under contracts whose selling price is influenced by pass-through provisions directly related to the cost of certain key raw materials.

GLATFELTER 2023 FORM 10-K | 3 | ||||

Airlaid Materials continues to be a technology and product innovation leader in technically demanding segments of the markets it serves. Its airlaid material production employs multi-bonded, thermal-bonded and hydrogen-bonded airlaid technologies. We believe that its facilities are among the most modern and flexible airlaid facilities in the world, allowing it to produce at industry leading operating rates. Its proprietary single-lane festooning technology provides converting and product packaging capabilities which supports efficiency in the customers converting processes. Airlaid Materials’ in-house technical expertise combined with significant capital investment requirements and rigorous customer expectations creates large barriers to entry for new competitors.

The following summarizes Airlaid Materials’ key competitors:

| Market segment | Competitor | |||||||

| Hygiene and other absorbent products | Fitesa, McAirlaid’s, Domtar, Suominen, Karweb Nonwovens, and Gelok International | |||||||

| Wipes | Suominen, Berry Global, Kimberly-Clark, Spuntech Industries, Domtar, and AS Nonwovens | |||||||

| Tabletop | SharpCell, Duni/Rexcell, Ascutec, Karweb Nonwovens, Domtar, and Main | |||||||

Our strategy in Airlaid Materials is focused on:

•maintaining and expanding relationships with customers that are market-leading consumer product companies, as well as companies converting and distributing through private label arrangements;

•emphasizing our product development and process innovation capabilities, broadening of our product portfolio mix, and developing plastic-free technologies;

•expanding geographic reach of markets served;

•optimizing the use of existing production capacity; and

•employing continuous improvement methodologies and initiatives to reduce costs, improve efficiencies and create additional capacity.

COMPOSITE FIBERS Our Composite Fibers segment, with 2023 net sales of approximately $483.5 million, processes specialty long fibers, primarily from natural sources such as abaca, and other materials to create premium value-added products in the following categories:

•Food & beverage filtration material primarily used for single-serve coffee and tea products;

•Technical specialties consists of a diverse line of specialty engineered products used in commercial and industrial applications such as electrical energy storage, home, hygiene, and other highly-engineered fiber-based applications;

•Wallcover base materials used by wallpaper manufacturers;

•Composite laminates decorative laminate solutions used in furniture, and household and commercial flooring, and other applications; and

•Metallized products used in labels, packaging liners, gift wrap, and other consumer product applications.

We believe Composite Fibers maintains a market leadership position in the single-serve coffee and tea filtration markets, wallcover base material and many other products it produces. We believe many of the markets served by Composite Fibers present attractive growth opportunities due to evolving consumer preferences, new or emerging geographic markets, new product innovation and increased market share through superior products and quality.

This segment’s net sales composition by categories is set forth in Item 8 – Financial Statements and Supplementary Data - Note 8 – “Revenue.”

Composite Fibers is comprised of four production facilities (Germany (2), France, and England), a metallizing operation (Wales) and a pulp mill (the Philippines). The combined attributes of the facilities are summarized as follows (in metric tons):

Composite Fibers Production Capacity | Principal Raw Material (“PRM”) | Estimated Annual Quantity of PRM | ||||||||||||

142,500 lightweight and other paper | Abaca pulp | 14,400 | ||||||||||||

| Wood pulp | 81,000 | |||||||||||||

| Synthetic fiber | 21,500 | |||||||||||||

| 11,200 metallized | Base stock | 7,500 | ||||||||||||

| 12,000 abaca pulp | Abaca fiber | 20,000 | ||||||||||||

The primary raw materials used in the production of our lightweight materials are softwood pulps, abaca pulp, and other specialty fibers. Securing adequate quantities of abaca pulp and its source material, abaca fiber, are important to support growth in this segment. Abaca pulp, a specialized pulp with limited sources of availability globally, is produced by our Philippine pulp mill, providing a unique advantage to our Composite Fibers segment. At certain times, when the supply of abaca fiber becomes constrained or when production demands exceed the capacity of the Philippines mill, alternative sources and/or substitute fibers are used to meet customer demands. Glatfelter has also partnered with an external firm to sell any of the excess high quality, specialty abaca produced as part of the cash liberation turnaround initiative.

In addition to critical raw materials, Composite Fibers’ production cost is influenced by the price of electricity and natural gas. In 2023, Composite Fibers purchased approximately 45% of its electricity needs, the cost of which is influenced by the natural gas markets. In addition, the segment generates all the steam used in production by burning natural gas. Approximately 50% of this segment’s net sales in 2023 was earned under contracts whose selling price is influenced by pass-through provisions directly related to the cost of certain key raw materials.

In Composite Fibers’ markets, competition is product line specific as the necessity for technical expertise and specialized manufacturing equipment limits the number of companies offering multiple product lines. In addition, Composite Fibers’ lightweight products are produced using highly specialized inclined wire paper machine technology. The following chart summarizes key competitors by market segment:

| Market segment | Competitor | |||||||

| Single serve coffee & tea | Ahlstrom, Delfort, Purico, Miquel y Costas, and Zhejiang Kan | |||||||

| Technical specialties | Nippon Kodoshi (NKK), Zhejiang Kan, Twin Rivers, Suominen, and Miquel y Costas | |||||||

| Wallcovering | Technocell, Neu Kaliss, Kaemmerer, and Ahlstrom | |||||||

| Composite laminates | Mativ, Purico, Miquel y Costas, and Qi Feng | |||||||

| Metallized | AR Metallizing, Torras Papel Novelis, Vaassen, Galileo Nanotech, and Wenzhou Protec Vacuum Metallizing Co. | |||||||

Our strategy in Composite Fibers is focused on:

•leveraging innovation resources to drive plastic free applications, and new product and new business development;

•optimizing our asset utilization and product portfolio while capitalizing on growing global markets in beverage filtration, electrical storage, and consumer products trends;

•maximize continuous improvement methodologies to increase productivity, reduce costs, and expand capacity; and

•ensuring readily available access to specialized raw material requirements or suitable alternatives to support projected growth.

SPUNLACE Our Spunlace segment, with 2023 net sales of approximately $317.9 million, is a global leading specialty manufacturer of premium quality spunlace nonwovens for critical cleaning, high-performance materials, personal care, surface disinfecting wipes, hygiene, beauty care and medical applications. Spunlace, formed as a result of our Jacob Holm acquisition, is a global manufacturer with state of the art proprietary production technology, conversion capabilities and branded products. Spunlace serves the world's largest consumer brands and focuses on quality, sustainability, and innovation. The categories served by Spunlace include:

•consumer wipes;

•critical cleaning;

•health care;

•feminine hygiene;

•high performance materials; and

•beauty care.

Spunlace's products are used by a wide range of end users. The critical cleaning and high performance product categories are used in applications such as automotive refinishing, aerospace, cleanroom, automotive acoustics, fire blocking and filtration. It has long-standing relationships with its customers who are niche players with highly specialized requirements. Health and beauty care includes medical gowns and drapes, wound care, surgical towels, facial masks and face and body wipes. Customers in the wipes and feminine hygiene category consist of some of the world's largest consumer brands, retailers, and converters.

GLATFELTER 2023 FORM 10-K | 5 | ||||

Spunlace operates four manufacturing facilities, two of which are located in the United States, and one each in France and Spain. In addition, Spunlace provides converting capabilities transforming semi-finished roll goods into finished products using various converting technologies. Spunlace production facilities have the following combined attributes (in metric tons):

Spunlace Production Capacity | Principal Raw Material (“PRM”) | Estimated Annual Quantity of PRM | ||||||||||||

91,000 | Synthetic fibers | 21,400 | ||||||||||||

| Pulp-based fibers | 24,200 | |||||||||||||

| Fluff pulp | 12,800 | |||||||||||||

Non-wood fibers | 1,500 | |||||||||||||

| Base paper | 12,100 | |||||||||||||

Key raw materials used in the spunlace production process include natural and synthetic fibers, pulps, and paper stock. The spunlace production process utilized by Spunlace's facilities consumes a significant amount of water to facilitate the formation of fibers into salable product. The cost to produce is influenced by the cost of critical raw materials and energy prices, including electricity and natural gas used in its operations. Approximately 48% of this segment’s net sales in 2023 was earned under contracts whose selling price is influenced by pass-through provisions directly related to the price indices of certain key raw materials.

The following summarizes Spunlace's key competitors:

| Market segment | Competitor | |||||||

| Critical cleaning and high performance | Kimberly-Clark, Berry Global, Sellars, Suominen, and Norafin | |||||||

| Feminine hygiene, personal care, health and beauty | Sandler, Suominen, BC Nonwovens, Spuntech, Mogul, Dalian Ruiguang Nonwoven Group, and Asahi Kasei | |||||||

Our strategy in Spunlace is focused on:

•integrating its operations to maximize planned synergies;

•leading the industry transition in sustainability by leveraging our technological advantage;

•being the preferred co-innovator;

•optimizing the use of existing production capacity; and

•delivering operational excellence.

Concentration of Customers In 2023, 2022 and 2021, approximately 16%, 15% and 16%, respectively, of our consolidated net sales were from sales to Procter & Gamble Company, a customer in the Airlaid Materials and Spunlace segments.

The top three customers, in the aggregate, accounted for approximately 57% of Airlaid Materials’ and approximately 42% of Spunlace’s net sales in 2023.

Capital Expenditures Our business requires expenditures for equipment enhancements to support growth strategies, research and development initiatives, and for normal upgrades or replacements. Capital expenditures totaled $33.8 million, $37.7 million and $30.0 million in 2023, 2022 and 2021, respectively. Capital expenditures in 2024 are estimated to total between approximately $35 million and $40 million.

Government Regulations We are subject to various federal, state and local laws and regulations intended to protect the environment, as well as human health and safety. These regulations include, among others, limits on air emissions and water use and discharges by our facilities and protection of our employees throughout the world. Glatfelter is committed to operating responsibly and addressing the concerns and needs of our stakeholders. At various times, we have incurred costs to comply with these regulations and we could incur additional costs as new regulations are developed or regulatory priorities change.

Human Capital Our business is guided by our Board of Directors and a diverse management team comprised of leaders with extensive business and industry experience. Additional information on our leadership team is set forth within this Form 10-K under the caption “Executive Officers.” As of December 31, 2023, we employed approximately 2,920 people worldwide, the substantial majority of whom are skilled personnel responsible for the production and commercialization of our Airlaid Materials, Composite Fibers, and Spunlace products. Our facilities are a continuous flow manufacturing operation with approximately 68.3% of our employees represented by local works councils or trade unions in Europe, the United Kingdom, Canada, and the Philippines.

The daily work of Glatfelter employees is rooted in the Company’s longstanding Code of Business Conduct and Core Values of Integrity, Financial Discipline, Mutual Respect, Customer Focus, Environmental Responsibility, and Social Responsibility.

Employee Health and Safety We have a well-established safety management system and ongoing employee well-being programs. The health and safety of our employees have remained a top priority, and we have been diligently taking the necessary measures to protect employees throughout our various facilities. This includes expanded safety, hygiene, and communication protocols as we operate in a post-pandemic environment.

We view health and safety as everyone’s responsibility and involve all employees at every level of the organization in our programs. Glatfelter facilities are striving to be “injury free every day” through implementation of our Global Health & Safety Program, regulatory compliance, site-specific safety plans, safety resources and training, ongoing risk assessment and a safety auditing program. We track multiple safety metrics, including total case incident rate (“TCIR”), to encourage and ensure continuous improvement and mitigation of potential safety risks. In recent years, our TCIR has consistently ranked in the top quartile of safety performance in our industry.

Talent Attraction, Retention, and Development Our employees make essential contributions to our success and ability to drive growth and innovation. Even as the organization has undertaken substantial change in recent years, our vision and Core Values remain the center of our steadfast compliant culture. We are always working to enhance our human resources programs by implementing and integrating enterprise-level processes for talent attraction, career development, and training.

Glatfelter supports its team by providing competitive wages, comprehensive benefits, diverse well-being programs, and other benefits to help enhance the lives of our employees. We provide various work arrangements for employees whose jobs are conducive to remote or hybrid structures. We regularly review our employee offerings to ensure we are positioned competitively to attract and retain top-tier talent.

Employee Training Training and professional growth are central to developing our workforce and driving long-term success for our organization. Global training encompasses a variety of programs, from apprenticeships and machine-specific skill development, grant-funded partnerships, Lean Six Sigma principles training, leadership development and compliance training. To ensure we continue to have the necessary resources with skills necessary to support the production of increasingly sophisticated engineered materials, we invest in the development of skills necessary to operate our machinery, including operational apprenticeship programs in many of our global locations.

Diversity, Equity and Inclusion We are a global company that encourages and embraces different cultures and backgrounds. Our employees, including our management team, are diverse – as our facilities hire locally for leadership positions, as well as salaried and production positions at all levels. We strive to create an inclusive culture and provide opportunities for people of all backgrounds to share their unique viewpoints and contribute to our success. The global nature of our business helps drive our inclusive corporate environment, as we regularly collaborate with colleagues who have different backgrounds, ethnicities, and world views.

We are committed to ensuring our Company is a diverse and inclusive place to work, while also strengthening the communities in which we live.

Other Available Information The Corporate Governance page of our website includes our Articles of Incorporation, Bylaws, Corporate Governance Principles, Code of Business Conduct, and biographies of our Board of Directors and identifies our Executive Officers. In addition, the website includes charters of the Audit, Compensation, and Nominating and Corporate Governance Committees of the Board of Directors. The Corporate Governance page also includes the Code of Business Ethics for the CEO and Senior Financial Officers of Glatfelter, our “whistle-blower” hotline information and other related material. We satisfy the disclosure requirement for any future amendments to, or waivers from, our Code of Business Conduct or Code of Business Ethics for the CEO and Senior Financial Officers by posting such information on our website. We will provide a copy of these documents, without charge, to any person who requests one by contacting Investor Relations at (717) 225-2746, ir@glatfelter.com or by mail to 4350 Congress Street, Suite 600, Charlotte, NC 28209.

GLATFELTER 2023 FORM 10-K | 7 | ||||

ITEM 1A RISK FACTORS

Our business and financial performance may be adversely affected by a weak global economic environment or downturns in the target markets that we serve.

Adverse global economic conditions could impact our target markets resulting in decreased demand for our products. Our results could be adversely affected if economic conditions weaken. Also, there may be periods during which demand for our products could be insufficient to enable us to operate our production facilities at full capacity and in an economical manner which may force us to curtail production by taking machine downtime.

Approximately 46% of our net sales in 2023 was from shipments to customers in Europe, the demand for which is dependent on economic conditions in this region, or to the extent such customers do business outside of Europe, in other regions of the world. Uncertain economic conditions in this region may cause weakness in demand for our products, as well as volatility in our customers buying patterns.

The cost of raw materials and energy used to manufacture our products could increase or the availability of certain raw materials could become constrained.

Our business requires access to sufficient, and reasonably priced, quantities of wood pulps, different pulps, pulp substitutes, abaca fiber, polyester and various synthetic fibers, and certain other raw materials, as well as access to reliable and abundant supplies of water to support many of our production facilities. Therefore, volatility in the price of key raw materials can have a significant impact on our results of operations.

Our Philippine production site purchases raw abaca fiber to produce abaca pulp, a key material used to manufacture material for single-serve coffee, tea, and technical specialty products at Composite Fibers’ facilities. At certain times, the supply of abaca fiber has been constrained or the quality diminished due to factors such as weather-related damage to the source crop, as well as decisions by landowners to produce alternative crops in lieu of those used to produce abaca fiber. These factors have contributed to volatility in fiber prices or limited available supply.

Airlaid Materials requires access to sufficient quantities of fluff pulp, the supply of which is subject to availability of certain softwoods.

The cost of many of our production materials, including petroleum-based chemicals and freight charges, are influenced by the cost of oil. Natural gas is the principal source of fuel for each of our facilities worldwide and prices have historically been more volatile than other fuels. Our manufacturing operations are energy-intensive and prices can fluctuate significantly based on demand.

Government rules, regulations and policies have an impact on the cost of certain energy sources, particularly for our European operations. In Europe, we currently benefit from a number of government-sponsored programs related to, among others, green energy or renewable energy initiatives designed to mitigate the cost of electricity to larger industrial consumers of power. Any reduction in the extent of government sponsored incentives may adversely affect the cost ultimately borne by our operations.

Although we have contractual arrangements with certain customers pursuant to which our product’s selling price is adjusted for changes in the cost of certain raw materials and energy, we may not be able to fully pass increased raw materials or energy costs on to all customers if the market will not bear the higher price or if existing supply agreements limit price increases. If price adjustments significantly trail increases in raw materials costs, our operating results could be adversely affected.

Our turnaround strategy is time-consuming and expensive and could significantly disrupt our business.

We initiated a significant turnaround strategy in late 2022 in an effort to optimize our portfolio, improve margins, reduce fixed costs, liberate cash, improve operational effectiveness and return Spunlace to profitability. These turnaround actions were, and will continue to be, initiated to deliver significantly improved financial performance. The nature of these activities involves topics that are complex and time-consuming in nature, and could significantly disrupt our business if we fail to execute them properly, which could ultimately result in financial impacts to the Company.

The conflict between Russia and Ukraine has adversely affected, and may continue to adversely affect, our business, financial condition, and results of operations.

Approximately $36 million and $40 million, or 2.6% and 2.7% of our net sales in 2023 and 2022, respectively, were earned from customers located in Russia and Ukraine. The geopolitical conditions resulting from the Russia/Ukraine military conflict, including government-imposed sanctions and the current macroeconomic climate in Russia and Ukraine,

have adversely impacted both demand for our products and our ability to deliver products to this region, as well as, limited customers' access to financial resources and their ability to satisfy obligations to us. For example, as a direct result of the military conflict, economic sanctions, and the disruptions in the region’s financial systems, we have had a significant reduction in wallcover revenues and cash flows. We expect this reduction to continue for the foreseeable future and most directly impact our facility located in Dresden, Germany that produces wallcover base paper, a significant portion of which historically was sold into the Ukraine and Russian markets. As a result, during the first quarter of 2022, we recorded a $117.3 million non-cash asset impairment charge related to assets of our Dresden facility and an impairment of our Composite Fibers business' goodwill. In addition, we operate manufacturing sites elsewhere in Europe that have been adversely impacted as a result of the military conflict in Ukraine and related geopolitical events and sanctions.

In the event that current geopolitical tensions fail to abate, or deteriorate further, or additional governmental sanctions are enacted against the Russian economy or its banking and monetary systems, we may face additional adverse consequences to our business and results of operations. Even if the conflict moderates or a resolution between Ukraine and Russia is reached, we expect that we will continue to experience ongoing adverse consequences to our business, financial condition, and results of operation resulting from the conflict for the foreseeable future, including and because certain of the economic and other sanctions imposed, or that may be imposed, against Russia may continue for a period of time after any resolution has been reached.

Disruption of our global supply chain could adversely affect our business.

Our ability to manufacture, sell and distribute products is critical to our operations. Our products contain raw materials that we source globally from suppliers. If there is a shortage of a key raw material in our supply chain, and a replacement cannot be readily sourced from an alternative supplier, the shortage may disrupt our production. Likewise, disruptions in the transportation and delivery of products - both from suppliers to our production facilities, and from our production facilities to our customers - may impact our ability to sell product and deliver goods to our customers on time and in full. In addition, the costs of transporting materials and products through our chain of sourcing and production may increase, and such increases could be significant. The failure of third parties on which we rely, including those third parties who supply our raw materials, packaging, capital equipment and other necessary operating materials, contract manufacturers, commercial transport, distributors, contractors, and external business partners, to meet their obligations to us, or significant disruptions in their ability to do so, may negatively impact our operations. Failure to take adequate steps to mitigate the likelihood or potential impact of such disruptions, or to effectively manage such disruptions if they occur, could adversely affect our business and results of operations, as well as require additional resources to restore our global supply chain. Any of these factors could have a material adverse impact on our results of operations and financial condition.

Foreign currency exchange rate fluctuations could adversely affect our results of operations.

A significant proportion of our net sales and earnings is generated from operations outside of the United States. In addition, we own and operate manufacturing facilities in Canada, Germany, France, Spain, the United Kingdom, and the Philippines. A significant portion of our business is transacted in currencies other than the U.S. dollar, including the euro, British pound, Canadian dollar, and Philippine peso, among others. Our euro denominated net sales exceed euro expenses by an estimated €170 million. With respect to the British pound, Canadian dollar, and Philippine peso, we have greater outflows than inflows of these currencies, although to a lesser degree than the euro. As a result, we are exposed to changes in currency exchange rates and such changes could be significant.

Our ability to maintain our products' price competitiveness is reliant, in part, on the relative strength of the currency in which the product is denominated compared to the currency of the market into which it is sold and the functional currency of our competitors. Changes in the rate of exchange of foreign currencies in relation to the U.S. dollar, and other currencies, may adversely impact our results of operations and our ability to offer products in certain markets at acceptable prices.

In the event of significant currency weakening in the countries into which our products are sold, demand for our products, pricing of our products, or a customer’s ability to satisfy obligations to us, could be adversely impacted.

GLATFELTER 2023 FORM 10-K | 9 | ||||

Our industry is highly competitive and increased competition could reduce our sales and profitability.

The global markets in which we compete are served by a variety of competitors and a variety of substrates. As a result, our ability to compete is sensitive to, and may be adversely impacted by:

•the entry of new competitors into the segments we serve;

•the aggressiveness of our competitors’ pricing strategies, which could force us to decrease prices in order to maintain market share;

•our failure to anticipate and respond to changing customer preferences; and

•technological advances or changes that impact production or cost competitiveness of our products.

The impact of any significant changes may result in our inability to effectively compete in the segments in which we operate, and as a result our sales and operating results would be adversely affected.

We may not be able to develop new products acceptable to our existing or potential customers.

Our business strategy is market focused and includes investments in developing new products to meet the changing needs of our customers, serve new customers and to maintain our market share. Our success will depend, in part, on our ability to develop and introduce new and enhanced products that keep pace with introductions by our competitors and changing customer preferences. If we fail to anticipate or respond adequately to these factors, we may lose opportunities for business with both current and potential customers. The success of our new product offerings will depend on several factors, including our ability to:

•anticipate and properly identify our customers' needs and industry trends;

•develop and commercialize new products and applications in a timely manner;

•price our products competitively;

•differentiate our products from our competitors' products; and

•invest efficiently in research and development activities.

Our inability to develop new products or new business opportunities could adversely impact our business and ultimately harm our profitability.

We are subject to substantial costs and potential liability for environmental matters.

We are subject to various environmental laws and regulations that govern our operations, including discharges into the environment, and the handling and disposal of hazardous substances and wastes. We are also subject to laws and regulations that impose liability and clean-up responsibility for releases of hazardous substances. To comply with environmental laws and regulations, we have incurred, and will continue to incur, substantial expenditures.

We may incur obligations to remove or mitigate any adverse effects on the environment, such as air and water quality, resulting from production sites we operate or have operated. Potential obligations include costs for government oversight of the remediation activities, the restoration of natural resources, and/or personal injury and property damages.

We generate a substantial portion of Airlaid Materials' and Spunlace's net sales from a few large customers and the loss of any one could have a material adverse effect on our results of operations.

The top three customers in each of these segments, in the aggregate, accounted for approximately 57% of Airlaid Materials’ and approximately 42% of Spunlace’s net sales in 2023. Furthermore, Airlaid Materials and Spunlace derive approximately 37% and 7%, respectively, of their annual net sales from sales to the feminine hygiene market. The loss of any one of these large customers or a decline in sales of hygiene products could have a material adverse effect on these segments’ operating results. Our ability to effectively compete could be affected by technological production alternatives, which could provide substitute products into this segment. Customers in the airlaid and spunlace nonwoven fabric material segments including hygiene, may also switch to less expensive products, change preferences or otherwise reduce demand for our products, thus reducing the size of the segments in which we currently sell our products. Any of the foregoing could have a material adverse effect on our financial performance and business prospects.

Our operations may be impaired, and we may be exposed to potential losses and liability as a result of natural disasters, acts of terrorism or sabotage or similar events.

If we have a catastrophic loss or unforeseen operational disruption at any of our facilities, we could suffer significant lost production which could impair our ability to satisfy customer demands.

Natural disasters, such as earthquakes, hurricanes, tornadoes, typhoons, flooding or fire, and acts of terrorism or sabotage affecting our operating activities and major facilities could materially and adversely affect our operations, operating results and financial condition.

In addition, many of our operations require a reliable and abundant supply of water. Such sites rely on local bodies of water or water sources for their production needs and, therefore, are particularly sensitive to drought conditions or other natural or man-made interruptions to water supplies. Any interruption or curtailment of operations at any of our production facilities due to flooding, drought or low flow conditions at the principal water source or another cause could materially and adversely affect our operating results and financial condition.

Our pulp facility in Lanao del Norte on the Island of Mindanao in the Republic of the Philippines is located along the Pacific Rim, one of the world’s hazard belts. By virtue of its geographic location, this site is subject to similar types of natural disasters discussed above, cyclones, typhoons, and volcanic activity. Moreover, the area of Lanao del Norte has been a target of suspected terrorist activities. Our pulp mill in Mindanao is located in a rural portion of the island and is susceptible to attacks and/or power interruptions. The Mindanao site supplies the abaca pulp used by Composite Fibers to manufacture paper for single serve coffee and tea products and certain technical specialties products. Any interruption, loss, or extended curtailment of operations at our Mindanao site could affect our ability to meet customer demands for our products and materially affect our operating results and financial condition.

We have operations in a potentially politically and economically unstable location.

Our pulp facility in the Philippines is located in a region that is unstable and subject to political unrest. As discussed above, our Philippine pulp facility produces abaca pulp, a significant raw material used by Composite Fibers and is currently our main source of abaca pulp. There are limited suitable alternative sources of readily available abaca pulp in the world. In the event of a disruption in supply from our Philippine site, there is no guarantee that we could obtain adequate amounts of abaca pulp, if at all, from alternative sources at a reasonable price. Further, there is no assurance the performance of such alternative materials will satisfy customer performance requirements. As a consequence, any civil disturbance, unrest, political instability, or other event that causes a disruption in supply could limit the availability of abaca pulp and would increase our cost of obtaining abaca pulp. Such occurrences could adversely impact our sales volumes, net sales, and operating results.

Our international operations pose certain risks that may adversely impact sales and earnings.

We have significant operations and assets located in Canada, Germany, France, Spain, the United Kingdom, and the Philippines. Our international sales and operations are subject to a number of unique risks, in addition to the risks in our domestic sales and operations, including, but not limited to, economic and trade disruptions resulting from geopolitical developments, wars or other military conflicts (such as the ongoing conflicts in Ukraine and the Middle East), differing protections of intellectual property, trade barriers, labor unrest, exchange controls, regional economic uncertainty, differing (and possibly more stringent) labor regulation, risk of governmental expropriation, domestic and foreign customs and tariffs, differing regulatory environments, difficulty in managing widespread operations and political instability. These factors may adversely affect our future profits. Also, in some foreign jurisdictions, we may be subject to laws limiting the right and ability of entities organized or operating therein to pay dividends or remit earnings to affiliated companies unless specified conditions are met. Any such limitations would restrict our flexibility in using funds generated in those jurisdictions.

Our business depends on good relations with our employees and attracting and retaining key employees.

As of December 31, 2023, we employed approximately 2,920 people worldwide, the substantial majority of whom are skilled personnel responsible for the production and commercialization of our Airlaid Materials, Composite Fibers, and Spunlace products. Our facilities are a continuous flow manufacturing operation with approximately 68.3% of our employees represented by local works councils or trade unions in Europe, the United Kingdom, Canada, and the Philippines. The risk of labor disputes, work stoppages or other disruptions in production could adversely affect us, especially in conjunction with potential restructuring activities. Any work stoppage or failure to reach agreements with local works councils or trade unions could have a material adverse effect on our customer relations, our productivity, the profitability of a manufacturing facility, our ability to develop new products and our operations as a whole. Furthermore, the loss of any of our key employees, including our CEO and their direct reports, could adversely affect our business and thus our financial condition, results of operations and cash flows.

GLATFELTER 2023 FORM 10-K | 11 | ||||

We are subject to cyber-security risks related to unauthorized or malicious access to sensitive customer, vendor, company, or employee information, as well as to the technology that supports our operations and other business processes.

Our business operations rely upon secure systems for site operations, and data capture, processing, storage, and reporting. Although we maintain appropriate data security and controls, our information technology systems, and those of our third-party providers, could become subject to cyberattacks. The result of such attacks could result in a breach of data security and controls. Such a breach of our network, systems, applications or data could result in operational disruptions or damage or information misappropriation including, but not limited to, interruption to systems availability; denial of access to and misuse of applications required by our customers to conduct business with us; denial of access to the applications we use to plan our operations, procure materials, manufacture and ship products and account for orders; theft of intellectual know-how and trade secrets; and inappropriate disclosure of confidential company, employee, customer or vendor information, could stem from such incidents. In addition, the rapid evolution and increased adoption of artificial intelligence technologies increases our cybersecurity risks, including generative artificial intelligence augmenting threat actors’ technological sophistication to enhance existing or create new malware.

Any of these operational disruptions and/or misappropriation of information could adversely affect our results of operations, create negative publicity, and could have a material effect on our business. While we believe we devote significant resources to network security, disaster recovery, employee training and other measures to secure our information technology systems and prevent unauthorized access to or loss of data, there are no guarantees that they will be adequate to safeguard against all cyber incidents, systems disruptions, system compromises or misuses of data. In addition, while we currently maintain insurance coverage that, subject to its terms and conditions, is intended to address costs associated with certain aspects of cyber incidents and information systems failures, this insurance coverage may not, depending on the specific facts and circumstances surrounding an incident, cover all losses or all types of claims that arise from an incident, or the damage to our reputation or brands that may result from an incident.

We operate in and are subject to taxation from numerous U.S. and foreign jurisdictions.

The multinational nature of our business subjects us to taxation in the U.S. and numerous foreign jurisdictions. Due to economic and political conditions, tax rates in various jurisdictions are subject to significant change. Our effective tax rates could be affected by changes in tax laws or their interpretation, changes in the mix of earnings in jurisdictions with differing statutory tax rates, and changes in the valuation of deferred tax assets and liabilities. The Organization for Economic Cooperation and Development (“OECD”) reached agreement among various countries to implement a minimum 15% tax rate on certain multinational enterprises, commonly referred to as Pillar Two. The minimum tax directive has been adopted by the EU for implementation by its Member States into national legislation effective for fiscal years beginning after 2023 and may be adopted by other jurisdictions including the U.S. Many countries where we have operations continue to announce changes in their tax laws and regulations based on the Pillar Two principles. These and other developments could significantly negatively impact the Company’s overall tax expense, results of operations, and future cash flows.

In the event any of the above risk factors impact our business in a material way or in combination during the same period, we may be unable to generate enough cash flow to simultaneously fund our operations, finance capital expenditures, and satisfy obligations.

In addition to debt service obligations, our business requires expenditures to support growth strategies, research and development initiatives, and for normal upgrades or replacements. We expect to meet all our near and long-term cash needs from a combination of operating cash flow, cash and cash equivalents, availability under our credit facility or other long-term debt. If we are unable to generate enough cash flow from these sources, we could be unable to fund our operations, finance capital expenditures, or satisfy our near and long-term cash needs.

We have substantial indebtedness and may incur substantial additional indebtedness, which could adversely affect our financial health and our ability to obtain financing in the future, react to changes in our business and make payments on the notes.

As of December 31, 2023, we had approximately $370.7 million of secured debt and $501.0 million of unsecured debt. We are able to, and may, incur additional indebtedness in the future, subject to the limitations contained in the agreements governing our indebtedness. Our substantial indebtedness could have important consequences to holders of our indebtedness, including:

•making it more difficult for us to satisfy our obligations with respect to our long-term debt;

•limiting our ability to obtain additional financing to fund future working capital, capital expenditures, acquisitions or other general corporate requirements, and our ability to satisfy our obligations with respect to the notes in the future;

•requiring a substantial portion of our cash flows to be dedicated to debt service payments instead of other purposes, thereby reducing the amount of cash flows available for working capital, capital expenditures, acquisitions, and other general corporate purposes;

•increasing our vulnerability to general adverse economic and industry conditions;

•exposing us to the risk of increased interest rates as certain of our borrowings are at variable rates of interest;

•limiting our flexibility in planning for and reacting to changes in the industry in which we compete;

•placing us at a disadvantage compared to other, less leveraged competitors or competitors with comparable debt and more favorable terms and thereby affecting our ability to compete;

•increasing our cost of borrowing; and

•failing to comply with the covenants and other requirements contained in our credit agreements or our other debt instruments could cause an event of default under the relevant debt instrument.

Although our borrowing arrangements contain restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of qualifications and exceptions, and the additional indebtedness incurred in compliance with these restrictions could be substantial. These restrictions also will not prevent us from incurring obligations that do not constitute indebtedness. If new debt is added to our current debt levels, the related risks that we face would increase, and we may not be able to meet all our debt obligations, including the repayment of the notes. On March 30, 2023, we entered into an amendment to the Credit Agreement which obligates us to maintain a leverage ratio under 4.25 to 1.0 through the quarter ended December 31, 2024, stepping down to 4.0 to 1.0 at March 31, 2025, and 3.50 to 1.0 at March 31, 2026 and a debt service coverage ratio less than 1.25 to 1.0 through the quarter ended December 31, 2024, stepping up to 1.50 to 1.0 at March 31, 2025, and 2.00 to 1.0 at March 31, 2026.

ESG issues may have an adverse effect on our business, financial condition and results of operations, the desirability of our stock, and may damage our reputation.

If we are unable to meet our ESG goals or evolving investor, industry, or stakeholder expectations and standards, our customers may choose alternative suppliers and/or our reputation, the desirability of our stock to investors, and our business and/or financial condition may be adversely affected. Any failure to achieve our ESG goals, challenges to our ESG reporting or our failure to effectively respond to new, or changes in, legal or regulatory requirements concerning environmental or other ESG matters could adversely affect our business and thus our financial condition, results of operations and cash flows.

The pending Reverse Morris Trust transaction with Berry’s HHNF Business may not be completed on the terms or timeline currently contemplated, or at all, and the failure to complete the transaction could adversely impact the market price of Glatfelter common stock, as well as its business and operating results.

On February 6, 2024, we entered into certain definitive agreements with Berry, for Berry to spin-off and merge the majority of its Health, Hygiene and Specialties segment including its Global Nonwovens and Films business (“HHNF”) with Glatfelter (the “Merger”). Immediately following the transaction, pre-merger holders of the shares of common stock of Glatfelter will own, in the aggregate, approximately 10% of the outstanding capital stock of Glatfelter and Berry stockholders will own, in the aggregate, approximately 90% of the outstanding capital stock of Glatfelter.

The consummation of the transaction is subject to certain conditions, including: (i) approval of the required transactions by Glatfelter’s shareholders; (ii) the effectiveness of the registration statements with the SEC registering the issuance of Glatfelter common stock (iii) the listing of Glatfelter common stock issuable to shareholders on the NYSE; (iv) receipt of applicable regulatory approvals, including the expiration or early termination of the statutory waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, and other required regulatory approvals, and (v) the receipt of a private letter ruling from the IRS to the effect that the transactions will qualify for tax-free treatment under the Code, among other customary conditions to closing. There is no assurance that these conditions will be met or waived or that the transaction will be completed on the terms or timeline currently contemplated, or at all.

If the transaction is not completed for any reason, the price of Glatfelter common stock could decline. Glatfelter also could experience negative reactions from employees, customers, suppliers or other third parties if the transaction is not completed.

GLATFELTER 2023 FORM 10-K | 13 | ||||

Glatfelter and Berry have expended and will continue to expend significant management time and resources and have incurred and will continue to incur significant expenses related to the transaction, including legal, advisory, and financial services fees. Even if the transaction is completed, any delay in the completion of the transaction could diminish the anticipated benefits of the transaction or result in additional transaction expenses, loss of revenue or other effects associated with uncertainty about the transaction. If the transaction is not consummated because the merger agreement is terminated, Glatfelter may be required under certain circumstances to pay Berry a termination fee of $10 million.

ITEM 1B UNRESOLVED STAFF COMMENTS

None.

ITEM 1C CYBERSECURITY

Cybersecurity Risk Management and Strategy

We operate in the engineered materials manufacturing sector, which is subject to various cybersecurity risks that could adversely affect our business, financial condition, and results of operations, including: intellectual property theft; fraud; extortion; harm to employees or customers; violation of privacy laws; and other litigation, legal and reputational risks. We have implemented a risk-based approach to identify and assess the cybersecurity threats that could affect our business and information systems. Our cybersecurity program is aligned with industry standards and best practices, such as the National Institute of Standards and Technology (NIST) Cybersecurity Framework. We conduct periodic risk assessments to identify the potential impact and likelihood of various cyber scenarios, including those involving third-party service providers, and to determine the appropriate mitigation strategies and controls. We use various tools and methodologies to manage cybersecurity risk, including implementation of a business continuity process that includes a comprehensive incident response plan and procedure that is tested on a regular cadence. We also monitor and evaluate our cybersecurity performance on an ongoing basis through regular vulnerability scans, threat intelligence feeds, and penetration tests by an independent third party. We require third-party service providers with access to personal, confidential or proprietary information to implement and maintain comprehensive cybersecurity practices consistent with applicable legal standards and industry best practices. The incident response team, which includes senior IT subject matter experts and security analysts, determines the apparent severity of reported potential incidents, and operationalizes the appropriate incident response plan. In addition, we continue to provide training and awareness practices to mitigate human risk, including mandatory computer-based training, internal communications, and regular phishing awareness campaigns that are designed to emulate real-world contemporary threats and provide feedback (and, if necessary, additional training or remedial action) to employees. We also maintain insurance coverage that, subject to its terms and conditions, is intended to address costs associated with certain aspects of cyber incidents and information systems failures should they occur.

Our business depends on the availability, reliability, and security of our information systems, networks, data, and intellectual property. Any disruption, compromise, or breach of our systems or data due to a cybersecurity threat or incident could adversely affect our operations, administrative functions, customer service, product development, and competitive position. They might also result in a breach of our contractual obligations or legal duties to protect the privacy and confidentiality of our stakeholders. Such a breach could expose us to business interruption, lost revenue, ransom payments, remediation costs, liabilities to affected parties, cybersecurity protection costs, lost assets, litigation, regulatory scrutiny and actions, reputational harm, customer dissatisfaction, harm to our vendor relationships, or loss of market share.

Cybersecurity Governance

The Company has increased its investment into combating cybersecurity risks which include increased Board Audit Committee oversight of IT’s security risk reporting, formation of the Cybersecurity Steering Committee to directly govern IT cybersecurity strategies and strengthening the IT security management team which deploys resources to address cybersecurity risks on a day-to-day basis. Our internal cross-functional Cybersecurity Committee meets quarterly to discuss any issues and regulatory updates. The Board’s Audit Committee exercises its oversight role and provides the Board with reports and findings from its annual cybersecurity meeting with management, including the Vice President of Global Information Technology and the Senior IT Director over Cybersecurity. Our Senior IT Director over Cybersecurity holds a Certified Information Systems Security Professional (CISSP) certification and has more than 25 years of experience in cybersecurity. Our Board also reviews our cybersecurity budget on an annual basis.

ITEM 2 PROPERTIES

We own substantially all the land and buildings comprising our manufacturing facilities located in the United States; Canada; the United Kingdom; Germany; France; Spain and the Philippines; as well as substantially all of the equipment used in our manufacturing and related operations. Certain of our operations are under lease arrangements, including our metallized paper production facility located in Caerphilly, Wales, land at our Mount Holly, North Carolina site, a converting and warehousing facility in Madison, Tennessee, office and various warehouse space in the United States, Canada, Europe, China and our corporate offices in Charlotte, North Carolina. All our properties, other than those that are leased, are free from any material liens or encumbrances. We consider all our buildings to be in good structural condition and well maintained and our properties to be suitable and adequate for present operations.

ITEM 3 LEGAL PROCEEDINGS

We are involved in various lawsuits that we consider to be ordinary and incidental to our business. The ultimate outcome of these lawsuits cannot be predicted with certainty; however, we do not expect such lawsuits, individually or in the aggregate, will have a material adverse effect on our consolidated financial position, liquidity, or results of operations.

EXECUTIVE OFFICERS

The following table sets forth certain information with respect to our executive officers and other senior management members of February 28, 2024.

| Name | Age | Office with the Company | ||||||

| Thomas M. Fahnemann | 62 | President & Chief Executive Officer | ||||||

Boris Illetschko | 51 | Senior Vice President, Chief Operating Officer | ||||||

| Eileen L. Beck | 61 | Senior Vice President, Global Human Resources & Administration | ||||||

| Ramesh Shettigar | 48 | Senior Vice President, Chief Financial Officer & Treasurer | ||||||

| David C. Elder | 55 | Vice President, Strategic Initiatives, Business Optimization & Chief Accounting Officer | ||||||

| Jill L. Urey | 57 | Vice President, General Counsel & Compliance | ||||||

Thomas M. Fahnemann became President and Chief Executive Officer effective August 25, 2022. Since October 2017, he has served as Non-Executive Director, Member of the Board and Chairman of the Audit Committee for AustroCel Hallein, GmbH, in Amsterdam, the Netherlands. From 2010 to 2017, Mr. Fahnemann served as CEO and Chairman of the Management Board of Semperit Holding AG in Vienna, Austria.

Boris Illetschko became Senior Vice President, Chief Operating Officer effective August 1, 2023. From October 2019 until joining Glatfelter, Mr. Illetschko served as the global Group Chief Commercial Officer & Group Managing Director for voestalpine Rotec GmbH, Krieglach, Austria. Prior to this role, Boris worked as an independent industry consultant from 2017 to 2019 and from 2011 to 2017, he held various positions for Semperit AG Holding, Austria.

Eileen L. Beck was promoted to Senior Vice President, Global Human Resources & Administration in February 2023. She joined us in 2012 as Director, Global Compensation and Benefits, was promoted to Vice President in September 2015, and promoted to Vice President Human Resources & Administration in April 2017. Ms. Beck previously held various Human Resources roles at Armstrong World Industries.

Ramesh Shettigar was promoted to Senior Vice President, Chief Financial Officer and Treasurer in May 2022. He joined us in July 2014 as Vice President and Treasurer and was promoted to Vice President, ESG, Investor Relations and Corporate Treasurer in September 2021. Prior to joining Glatfelter, Mr. Shettigar was Director of Treasury at Quest Diagnostics with responsibility for a broad range of corporate finance activities including cash management, global liquidity, FX, debt/equity financing and capital planning. Mr. Shettigar has also held treasury and related positions with Praxair Inc, Delphi Corporation and McDermott International.

David C. Elder was named Vice President, Strategic Initiatives, Business Optimization and Chief Accounting Officer in April 2023. Prior to his promotion, he was Vice President, Finance and Chief Accounting Officer. Mr. Elder joined Glatfelter in January 2006 as our Vice President, Corporate Controller. Mr. Elder was previously Corporate Controller for YORK International Corporation.

Jill L. Urey was named Vice President, General Counsel & Compliance in December 2023. Prior to her promotion, she was Vice President, Chief Legal & Compliance Officer and Corporate Secretary since July 2019 and has led our legal function since December 2018. She joined Glatfelter in January 2013 as Assistant General Counsel and assumed the additional role of Chief Compliance Officer in the beginning of 2016. Prior to joining us, Ms. Urey was Corporate Counsel and later Interim General Counsel for Graham Packaging Company from 2007 to 2012.

GLATFELTER 2023 FORM 10-K | 15 | ||||

ITEM 4 MINE SAFETY DISCLOSURES

Not Applicable

PART II

ITEM 5 MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is traded on the New York Stock Exchange under the symbol “GLT”.

Our Board of Directors declared quarterly cash dividends of $0.14 per common share for the first two quarters of 2022. In the third quarter of 2022, the Board of Directors suspended the quarterly cash dividend as part of our focused efforts to optimize the operational and financial results of the business. There were no cash dividends declared in 2023.

As of February 26, 2024, we had 850 shareholders of record.

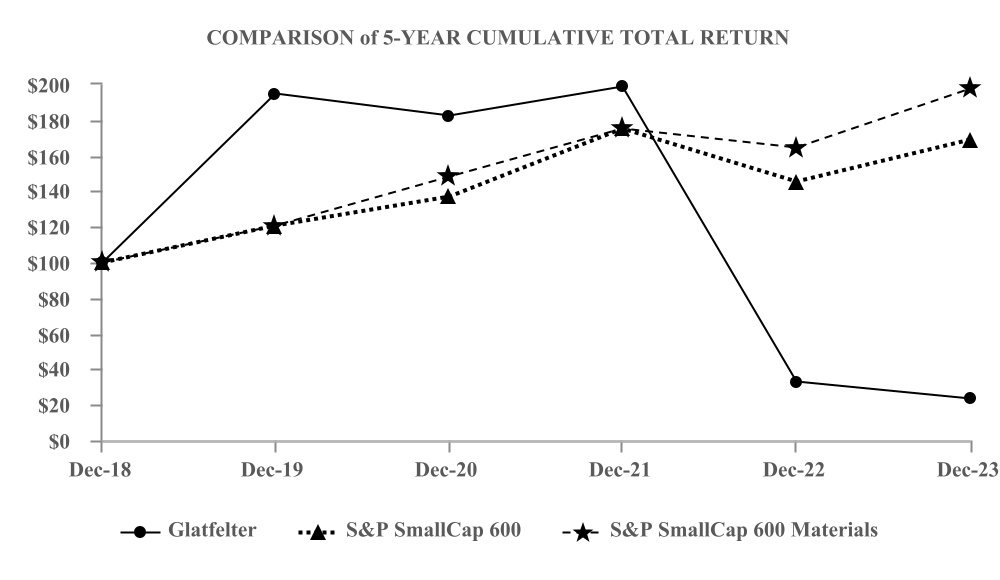

STOCK PERFORMANCE GRAPH

The following stock performance graph compares the cumulative 5-year total return of our common stock with the cumulative total returns of both a broad market index and a peer group. We compare our stock performance to the S&P Small Cap 600 index and to the S&P Small Cap 600 Materials index.

The following graph assumes $100 was invested in our common stock and in each index (including reinvestment of dividends) on December 31, 2018 and charts the performance through December 31, 2023.

ITEM 6 [RESERVED]

ITEM 7 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion of our financial condition and results of operations in conjunction with the financial statements and the notes thereto included elsewhere in this annual report. Our discussion and analysis of 2023 compared to 2022 is included herein. For discussion and analysis of 2022 compared to 2021, please refer to Item 7 of Part II, "Management's Discussion and Analysis of Financial Condition and Results of Operations" in our Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the United States Securities and Exchange Commission on February 27, 2023 and is incorporated herein by reference.