UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________

FORM 10-K

_________

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2022

OR

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission file number 0-362

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

(260 ) 824-2900

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Global Select Market | |||||||||||||||||

| (Title of each class) | (Trading symbol) | (Name of each exchange on which registered) | |||||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of each class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Yes | ☐ | ☒ | |||||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Yes | ☐ | ☒ | |||||||||

1

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| ☒ | No | ☐ | |||||||||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| ☒ | No | ☐ | |||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated Filer | ☐ | Non-Accelerated Filer | ☐ | Smaller Reporting Company | ||||||||||||||||||

| Emerging Growth Company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements

of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant

to §240.10D-1(b).

o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes | No | ☒ | |||||||||

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant at June 30, 2022 (the last business day of the registrant’s most recently completed second quarter) was $3,374,318,750 . The stock price used in this computation was the last sales price on that date, as reported by NASDAQ Global Select Market. For purposes of this calculation, the registrant has excluded shares held by executive officers and directors of the registrant, including restricted shares and except for shares owned by the executive officers through the registrant’s 401(k) Plan. Determination of stock ownership by non-affiliates was made solely for the purpose of responding to this requirement and the registrant is not bound by this determination for any other purpose.

Number of shares of common stock outstanding at February 6, 2023:

DOCUMENTS INCORPORATED BY REFERENCE

2

FRANKLIN ELECTRIC CO., INC.

TABLE OF CONTENTS

| Page | |||||||||||

| PART I. | Number | ||||||||||

| Item 1. | |||||||||||

| Item 1A. | |||||||||||

| Item 1B. | |||||||||||

| Item 2. | |||||||||||

| Item 3. | |||||||||||

| PART II. | |||||||||||

| Item 5. | |||||||||||

| Item 7. | |||||||||||

| Item 7A. | |||||||||||

| Item 8. | |||||||||||

| Item 9. | |||||||||||

| Item 9A. | |||||||||||

| Item 9B. | |||||||||||

| Item 9C. | |||||||||||

| PART III. | |||||||||||

| Item 10. | |||||||||||

| Item 11. | |||||||||||

| Item 12. | |||||||||||

| Item 13. | |||||||||||

| Item 14. | |||||||||||

| PART IV. | |||||||||||

| Item 15. | |||||||||||

3

PART I

ITEM 1. BUSINESS

Description of the Business

Franklin Electric Co., Inc. (“Franklin Electric” or the “Company”) is an Indiana corporation founded in 1944 and incorporated in 1946. Named after America’s pioneer electrical engineer, Benjamin Franklin, Franklin Electric manufactured the first water-lubricated submersible motor for water systems and the first submersible motor for fueling systems. With 2022 revenue of over $2.0 billion, the Company designs, manufactures and distributes water and fuel pumping systems, composed primarily of submersible motors, pumps, electronic controls, water treatment systems, and related parts and equipment.

The Company’s water pumping systems move fresh and wastewater for the residential, agricultural and other industrial end markets. The Company also sells various groundwater equipment products to well installation contractors, including water pumping systems, through its distribution branches located in the U.S. With a growing global footprint, the Company has also evolved into a top supplier of submersible fueling systems at gas stations, making pumps, pipes, electronic controls and monitoring devices.

The Company’s products are sold worldwide by its employee sales force and independent manufacturing representatives. The Company offers normal and customary trade terms to its customers, no significant part of which is of an extended nature. Special inventory requirements are not necessary, and customer merchandise return rights do not extend beyond normal warranty provisions.

Franklin Electric’s Key Factors for Success

While maintaining a culture of safety and lean principles, Franklin Electric promises to deliver quality, availability, service, innovation, and cost in every encounter the Company has with stakeholders, including direct or indirect customers, employees, shareholders, and suppliers. These key factors for success are a roadmap for the Company's growth as a global provider of water and fuel systems, through geographic expansion and product line extensions, leveraging its global platform and competency in system design, all while consistently offering the best value to its customer.

Markets and Applications

The Company’s business consists of three reportable segments based on the principal end market served: Water Systems, Fueling Systems, and Distribution. The Company includes unallocated corporate expenses in an “Intersegment Eliminations/Other” segment that, together with the Water Systems, Fueling Systems, and Distribution segments, represent the Company. Segment and geographic information appears in Note 15 - Segment and Geographic Information to the consolidated financial statements.

The market for the Company’s products is highly competitive and includes diversified accounts by size and type. The Company’s Water Systems and Fueling Systems products and related equipment are sold to specialty distributors and some original equipment manufacturers (“OEMs”), as well as industrial and petroleum equipment distributors and major oil and utility companies. The Company’s Distribution segment sells products primarily to water well contractors.

Water Systems Segment

Water Systems is a global leader in the production and marketing of water pumping systems and is a technical leader in submersible motors, pumps, drives, electronic controls, water treatment systems, and monitoring devices. The Water Systems segment designs, manufactures and sells motors, pumps, drives, electronic controls, monitoring devices, and related parts and equipment primarily for use in groundwater, water transfer and wastewater.

Water Systems motors, pumps and controls are used principally for pumping clean water and wastewater in a variety of residential, agricultural, municipal and industrial applications. Water Systems also manufactures electronic drives and controls for the motors which control functionality and provide protection from various hazards, such as electrical surges, over-heating and dry wells or dry tanks. In the last three years, the Company acquired Waterite, Inc.; Puronics, Inc.; New Aqua, LLC; and B&R Industries, Inc. expanding its portfolio to include water treatment systems and acquired Minetuff Dewatering Pumps Australia Pty Ltd expanding its industrial dewatering product line.

Water Systems products are sold in highly competitive markets. Water Systems contributed about 55 percent of the Company’s total revenue in 2022. Significant portions of segment revenue come from selling groundwater and surface pumps, motors, and controls for residential and commercial buildings, as well as agricultural sales which are more seasonal and subject to commodity price changes. The Water Systems segment generates approximately 25 to 30 percent of its revenue in developing markets, which often lack municipal water systems. As those countries install water systems, the Company views those markets

4

as an opportunity. The Company has had 6 to 9 percent compounded annual sales growth in developing regions in recent years. Water Systems competes in each of its targeted markets based on product design, quality of products and services, performance, availability and price. The Company’s principal competitors in the specialty water products industry are Grundfos Management A/S, Pentair, Inc. and Xylem, Inc.

2022 Water Systems research and development expenditures were primarily related to the following activities:

•Electronic variable frequency drives and controls for Pump and HVAC applications, including enhancements of mobile application capabilities for SubDrive Connect and Cerus X-Drive and development of standard panels to support HES (High Efficiency Systems) motors

•Development of new standard electric skid pump package designs and electronic variable frequency drive skid packages for mining and municipal dewatering markets

•Greywater pumping equipment, including the development of 60Hz electrical submersible pumps from the acquisition of Minetuff and the expansion of grinder pumps for the Brazil market

•Submersible and surface pumps for residential, commercial, municipal, and agricultural applications including the development of a standard global 4” pump family, developing a new cast stainless submersible turbine line, and upgrading the performance of line shaft turbine product offerings

•Submersible motor technology development, including the introduction of energy efficient permanent magnet motors into submersible water pumping systems, substantially reducing energy usage in residential pumping applications, 4 pole motor designs for 8” and 10” diameter products, and 4” Oil-filled motors

•Water treatment products focused on component improvements and IOT enabled sensing systems

Fueling Systems Segment

Fueling Systems is a global leader in the production and marketing of fuel pumping systems, fuel containment systems and monitoring and control systems. The Fueling Systems segment designs, manufactures and sells pumps, pipe, sumps, fittings, vapor recovery components, electronic controls, monitoring devices and related parts and equipment primarily for use in fueling system applications.

Fueling Systems offers a complete array of components between the tank and the dispenser, including submersible pumps, station hardware, piping, sumps, vapor recovery, corrosion control systems and electronic controls. The Fueling Systems segment growth has been sustained by a commitment to protecting human health and the environment while delivering the lowest total cost of ownership. Fueling Systems takes steps to ensure its products are installed and maintained properly through robust global certification tools for their third-party contractors. The segment serves other energy markets such as power reliability systems and includes intelligent electronic devices that are designed for online monitoring for the power utility, hydroelectric, and telecommunication and data center infrastructure.

Fueling Systems products are sold in highly competitive markets. Rising vehicle use is leading to more investment in fueling stations, which, in turn, leads to increased demand for the Company’s Fueling Systems products. The Company believes there is growth opportunity in developing markets. Fueling Systems competes in each of its targeted markets based on product design, quality of products and services, performance, availability and value. The Company’s principal competitors in the petroleum equipment industry are Vontier Corporation, formerly a part of Fortive Corporation, and Dover Corporation.

2022 Fueling Systems research and development expenditures were primarily related to the following activities:

•Developed and launched new distribution transformer monitor

•Developed new vapor flow meter for Chinese vapor recovery monitoring regulation

•Developed and launched UNITE, server software to collect data from battery monitoring, battery testers, NexPhase, and distribution monitoring

•Developed Press-Fit Connector for Cabletight electrical conduit

•Developed testable termination fitting for APT fueling piping system

•Developed and launched NexPhase Electric Vehicle Switchgear

•Developed car wash monitor of detergent liquids at car wash stations

•Developed new hybrid wired battery monitoring system

Distribution Segment

The Distribution segment is operated as a collection of wholly owned leading groundwater distributors known as the Headwater Companies. Headwater Companies deliver quality products and leading brands to the industry, providing contractors with the availability and service they demand to meet their application challenges. The Distribution segment operates within the U.S. professional groundwater market. Highlights of the Distribution Segment geographic growth through acquisitions in the last three years are as follows:

•2020 - Acquired Gicon Pumps & Equipment, Inc., a professional groundwater distributor operating in the south

•2021 - Acquired Blake Group Holdings, Inc., a professional groundwater distributor operating in the northeast

5

Information Regarding All Reportable Segments

Research and Development

The Company incurred research and development expenses as follows:

| (In millions) | 2022 | 2021 | 2020 | ||||||||||||||

| Research and development expenses | $ | 16.7 | $ | 17.3 | $ | 21.7 | |||||||||||

Expenses incurred were for activities related to the development of new products, improvement of existing products and manufacturing methods and other applied research and development.

The Company owns a number of patents, trademarks, and licenses. In the aggregate, these patents are of material importance to the operation of the business; however, the Company believes that its operations are not dependent on any single patent or group of patents.

Raw Materials

The principal raw materials used in the manufacture of the Company’s products are coil and bar steel, stainless steel, copper wire and aluminum ingot. Major components are electric motors, capacitors, motor protectors, forgings, gray iron castings, plastic resins and bearings. Most of these raw materials are available from multiple sources in the U.S. and world markets. Generally, the Company believes that adequate alternative sources are available for the majority of its key raw material and purchased component needs; however, the Company is dependent on a single or limited number of suppliers for certain materials or components. The Company believes that availability of fuel and energy is adequate to satisfy current and projected overall operations unless interrupted by government direction, allocation or other disruption.

Major Customers

No single customer accounted for over 10 percent of net sales in 2022, 2021, or 2020. No single customer accounted for over 10 percent of gross accounts receivable in 2022 and 2021.

Backlog

The dollar amount of backlog by segment was as follows:

| (In millions) | February 6, 2023 | February 10, 2022 | |||||||||

| Water Systems | $ | 228.2 | $ | 205.9 | |||||||

| Fueling Systems | 43.9 | 58.4 | |||||||||

| Distribution | 22.8 | 22.1 | |||||||||

| Consolidated | $ | 294.9 | $ | 286.4 | |||||||

The backlog is composed of written orders at prices adjustable on a price-at-the-time-of-shipment basis for products, primarily standard catalog items. All backlog orders are expected to be filled in 2023. The Company’s sales in the first quarter are generally less than its sales in other quarters due to less water well drilling and overall product sales during the winter months in the Northern hemisphere. Beyond that, there is no seasonal pattern to the backlog and the backlog has not proven to be a significant indicator of future sales.

Environmental Matters

The Company believes that it is in compliance with all applicable federal, state and local laws concerning the discharge of material into the environment, or otherwise relating to the protection of the environment. The Company has not experienced any material costs in connection with environmental compliance, and does not believe that such compliance will have any material effect upon the financial position, results of operations, cash flows or competitive position of the Company.

Human Capital Resources

As of December 31, 2022, the Company had approximately 6,500 employees. The Company is committed to providing safe work environments for its employees, prioritizing wellness, health and safety best practices and requiring ethical compliance with established policies. Further information regarding its human capital details and initiatives can be found in the 2022 Franklin Electric Sustainability Report available for download on the Company's website.

6

Available Information

The Company is a U.S. public reporting company under the Exchange Act and files reports, proxy statements and other information with the SEC, which can be accessed from the SEC's home page on the Internet at www.sec.gov. The Company’s website address is www.franklin-electric.com. The Company makes available free of charge on or through its website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission. Additionally, the Company’s website includes the Company’s corporate governance guidelines, its Board committee charters, Lead Independent Director charter, and the Company’s code of business conduct and ethics. Information contained on the Company’s website is not part of this annual report on Form 10-K.

ITEM 1A. RISK FACTORS

The following describes the principal risks affecting the Company and its business. Additional risks and uncertainties, not presently known to the Company, could negatively impact the Company’s results of operations or financial condition in the future.

Risks Related to the Industry

Reduced housing starts adversely affect demand for the Company’s products, thereby reducing revenues and earnings. Demand for certain Company products is affected by housing starts. Variation in housing starts due to economic volatility both within the United States and globally could adversely impact gross margins and operating results.

The Company’s results may be adversely affected by global macroeconomic supply and demand conditions related to the energy and mining industries. The energy and mining industries are users of the Company’s products, including the coal, iron ore, gold, copper, oil, and natural gas industries. Decisions to purchase the Company’s products are dependent upon the performance of the industries in which our customers operate. If demand or output in these industries increases, the demand for our products will generally increase. Likewise, if demand or output in these industries declines, the demand for our products will generally decrease. The energy and mining industries’ demand and output are impacted by the prices of commodities in these industries which are frequently volatile and change in response to general economic conditions, economic growth, commodity inventories, and any disruptions in production or distribution. Changes in these conditions could adversely impact sales, gross margin, and operating results.

Volatility in the prices and availability of raw materials, components, finished goods and other commodities could adversely affect operations. The Company purchases most of the raw materials for its products on the open market and relies on third parties for the sourcing of certain finished goods. Accordingly, the cost of its products may be affected by changes in the market price and its ability to successfully obtain raw materials, sourced components, or finished goods. The Company and its suppliers also use natural gas and electricity in manufacturing products both of which have historically been volatile. The Company does not generally engage in commodity hedging for raw materials and energy. Significant increases in the prices or disruptions in the supply chain of commodities, sourced components, finished goods, energy or other commodities could cause product prices to increase, which may reduce demand for products or make the Company more susceptible to competition. Furthermore, in the event the Company is unable to pass along increases in operating costs to its customers, margins and profitability may be adversely affected.

The growth of municipal water systems and increased government restrictions on groundwater pumping could reduce demand for private water wells and the Company’s products, thereby reducing revenues and earnings. Demand for certain Company products is affected by rural communities shifting from private and individual water well systems to city or municipal water systems. Many economic and other factors outside the Company’s control, including governmental regulations on water quality, and tax credits and incentives, could adversely impact the demand for private and individual water wells. A decline in private and individual water well systems in the United States or other economies in the international markets the Company serves could reduce demand for the Company’s products and adversely impact sales, gross margins, and operating results.

Demand for Fueling Systems products is impacted by environmental legislation which may cause significant fluctuations in costs and revenues. Environmental legislation related to air quality and fuel containment may create demand for certain Fueling Systems products which must be supplied in a relatively short time frame to meet the governmental mandate. During periods of increased demand, the Company’s revenues and profitability could increase significantly, although the Company can also be at risk of not having capacity to meet demand or cost overruns due to inefficiencies during ramp up to the higher production levels. After the Company’s customers have met the compliance requirements, the Company’s revenues and profitability may decrease significantly as the demand for certain products declines substantially. The risk of not reducing production costs in relation to the decreased demand and reduced revenues could have a material adverse impact on gross margins and the Company’s results of operations.

7

Changes in tax legislation regarding the Company’s U.S. or foreign earnings could materially affect future results. Since the Company operates in different countries and is subject to taxation in different jurisdictions, the Company’s future effective tax rates could be impacted by changes in such countries’ tax laws or their interpretations. Both domestic and international tax laws are subject to change as a result of changes in fiscal policy, legislation, evolution of regulation and court rulings. The application of these tax laws and related regulations is subject to legal and factual interpretation, judgment, and uncertainty. The Company cannot predict whether any proposed changes in tax laws will be enacted into law or what, if any, changes may be made to any such proposals prior to their being enacted into law. If the tax laws change in a manner that increases the Company’s tax obligation, it could have a material adverse impact on the Company’s results of operations and financial condition.

The Organization for Economic Co-operation and Development (the “OECD”), an international association comprised of 38 countries, including the United States, has issued proposals that change long-standing tax principles including on a global minimum tax initiative. On December 12, 2022, the European Union member states agreed to implement the OECD’s Pillar 2 global corporate minimum tax rate of 15 percent on companies with revenues of at least $790 million, which would go into effect in 2024. Other countries are also actively considering changes to their tax laws to adopt certain parts of the OECD’s proposals. If these proposals are implemented in the countries where the Company operates, it may materially impact our income tax liability, provision for income taxes and effective tax rate.

The Inflation Reduction Act signed on August 16, 2022, enacted a new excise tax under Section 4501 on certain repurchases of corporate stock. The Tax applies to repurchases of stock net of issuances after December 31, 2022. The estimated impact to the Company could be material if the Company decides to increase share repurchases.

Risks Related to the Business

The Company is exposed to political, economic and other risks that arise from operating a multinational business. The Company has significant operations outside the United States, including Europe, South Africa, Brazil, Mexico, India, China, Turkey, Canada and Argentina. Further, the Company obtains raw materials and finished goods from foreign suppliers. Accordingly, the Company’s business is subject to political, economic, and other risks that are inherent in operating a multinational business. These risks include, but are not limited to, the following:

•Difficulty in enforcing agreements and collecting receivables through foreign legal systems

•Trade protection measures and import or export licensing requirements

•Inability to obtain raw materials and finished goods in a timely manner from foreign suppliers

•Imposition of tariffs, exchange controls or other restrictions

•Difficulty in staffing and managing widespread operations and the application of foreign labor regulations

•Compliance with foreign laws and regulations

•Changes in general economic and political conditions in countries where the Company operates

Additionally, the Company’s operations outside the United States could be negatively impacted by changes in treaties, agreements, policies, and laws implemented by the United States. If the Company does not anticipate and effectively manage these risks, these factors may have a material adverse impact on its international operations or on the business as a whole.

The Company has significant investments in foreign entities and has significant sales and purchases in foreign denominated currencies creating exposure to foreign currency exchange rate fluctuations. The Company has significant investments outside the United States, including Europe, South Africa, Brazil, Mexico, India, China, Turkey, Canada and Argentina. Further, the Company has sales and makes purchases of raw materials and finished goods in foreign denominated currencies. Accordingly, the Company has exposure to fluctuations in foreign currency exchange rates relative to the U.S. dollar. Foreign currency exchange rate risk is partially mitigated through several means: maintenance of local production facilities in the markets served, invoicing of customers in the same currency as the source of the products, prompt settlement of intercompany balances, limited use of foreign currency denominated debt, and application of derivative instruments when appropriate. To the extent that these mitigating strategies are not successful, foreign currency rate fluctuations can have a material adverse impact on the Company’s international operations or on the business as a whole.

In the second quarter of 2022, the Company concluded that Turkey represents a hyperinflationary economy as its projected three-year cumulative inflation rate exceeds 100 percent. As a result, the Company started remeasuring the financial statements for the Company’s Turkish operations in accordance with the highly inflationary accounting rules in the Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") 830 "Foreign Currency Matters" as of the beginning of the second quarter of 2022. As a result, all gains and losses resulting from the remeasurement of the financial results of operations and other transactional foreign exchange gains and losses would be reflected in earnings, which could result in volatility within the Company’s earnings, rather than as a component of the Company’s comprehensive income within

8

stockholders’ equity. Turkey becoming a hyperinflationary economy may have a material adverse effect on the Company’s consolidated financial position, results of operations, or cash flows.

The Company’s acquisition strategy entails expense, integration risks, and other risks that could affect the Company’s earnings and financial condition. One of the Company’s continuing strategies is to increase revenues and expand market share through acquisitions that will provide complementary Water and Fueling Systems products, add to the Company’s global reach, or both. The Company spends significant time and effort expanding existing businesses through identifying, pursuing, completing, and integrating acquisitions, which generate expense whether or not the acquisitions are actually completed. Competition for acquisition candidates may limit the number of opportunities and may result in higher acquisition prices. There is uncertainty related to successfully acquiring, integrating and profitably managing additional businesses without substantial costs, delays or other problems. There can also be no assurance that acquired companies will achieve revenues, profitability or cash flows that justify the investment. Failure to manage or mitigate these risks could adversely affect the Company’s results of operations and financial condition.

The Company’s products are sold in highly competitive markets, by numerous competitors whose actions could negatively impact sales volume, pricing and profitability. The Company is a global leader in the production and marketing of groundwater and fuel pumping systems. End user demand, distribution relationships, industry consolidation, new product capabilities of the Company’s competitors or new competitors, and many other factors contribute to a highly competitive environment. Additionally, some of the Company’s competitors have substantially greater financial resources than the Company. The Company believes that consistency of product quality, timeliness of delivery, service, and continued product innovation, as well as price, are principal factors considered by customers in selecting suppliers. Competitive factors previously described may lead to declines in sales or in the prices of the Company’s products which could have an adverse impact on its results of operations and financial condition.

The Company’s products are sold to numerous distribution outlets based on market performance. The Company may, from time to time, change distribution outlets in certain markets based on market share and growth. These changes could adversely impact sales and operating results.

Transferring operations of the Company to lower cost regions may not result in the intended cost benefits. The Company is continuing its rationalization of manufacturing capacity between all existing manufacturing facilities and the manufacturing complexes in lower cost regions. To implement this strategy, the Company must complete the transfer of assets and intellectual property between operations. Each of these transfers involves the risk of disruption to the Company’s manufacturing capability, supply chain, and, ultimately, to the Company’s ability to service customers and generate revenues and profits and may include significant severance amounts.

Delays in introducing new products or the inability to achieve or maintain market acceptance with existing or new products may cause the Company’s revenues to decrease. The industries to which the Company belongs are characterized by intense competition, changes in end-user requirements, and evolving product offerings and introductions. The Company believes future success will depend, in part, on the ability to anticipate and adapt to these factors and offer, on a timely basis, products that meet customer demands. Failure to successfully develop new and innovative products or to enhance existing products could result in the loss of existing customers to competitors or the inability to attract new business, either of which may adversely affect the Company’s revenues.

Certain Company products are subject to regulation and government performance requirements in addition to the warranties provided by the Company. The Company’s product lines have expanded significantly and certain products are subject to government regulations and standards for manufacture, assembly, and performance in addition to the warranties provided by the Company. The Company’s failure to meet all such standards or perform in accordance with warranties could result in significant warranty or repair costs, lost sales and profits, damage to the Company’s reputation, fines or penalties from governmental organizations, and increased litigation exposure. Changes to these regulations or standards may require the Company to modify its business objectives and incur additional costs to comply. Any liabilities or penalties actually incurred could have a material adverse effect on the Company’s earnings and operating results.

The Company has significant goodwill and intangible assets and future impairment of the value of these assets may adversely affect the Company's operating results and financial condition. The Company’s total assets include substantial intangible assets, primarily goodwill. Goodwill results from the Company’s acquisitions, representing the excess of the purchase price paid over the fair value of the net assets acquired. Goodwill and indefinite-lived intangible assets are tested annually for impairment during the fourth quarter or as warranted by triggering events. If future operating performance at one or more of the Company’s operating segments were to decline significantly below current levels, the Company could incur a non-cash impairment charge to operating earnings. The recognition of an impairment of a significant portion of the Company’s

9

goodwill or intangible assets could have a material adverse impact on the Company’s results of operations and financial condition.

The Company’s business may be adversely affected by the seasonality of sales and weather conditions. The Company experiences seasonal demand in a number of markets within the Water Systems segment. End-user demand in primary markets follows warm weather trends and is at seasonal highs from April to August in the Northern Hemisphere. Demand for residential and agricultural water systems are also affected by weather-related disasters including heavy flooding and drought. Changes in these patterns could reduce demand for the Company’s products and adversely impact sales, gross margins, and operating results.

The Company depends on certain key suppliers, and any loss of those suppliers or their failure to meet commitments may adversely affect the Company's business and results of operations. The Company is dependent on a single or limited number of suppliers for some materials or components required in the manufacture of its products. If any of those suppliers fail to meet their commitments to the Company in terms of delivery or quality, the Company may experience supply shortages that could result in its inability to meet customer requirements, or could otherwise experience an interruption in operations that could negatively impact the Company’s business and results of operations.

The Company’s operations are dependent on information technology infrastructure and failures could significantly affect its business. The Company depends on information technology infrastructure in order to achieve business objectives. If the Company experiences a problem that impairs this infrastructure, such as a computer virus, a problem with the functioning of an important IT application, or an intentional disruption of IT systems by a third party, the resulting disruptions could impede the Company's ability to record or process orders, manufacture and ship products in a timely manner, or otherwise carry on business in the ordinary course. Any such events could cause the loss of customers or revenue and could cause significant expense to be incurred to eliminate these problems and address related security concerns. The Company is also subject to certain U.S. and international data protection and cybersecurity regulations. Complying with these laws may subject the Company to additional costs or require changes to the Company’s business practices. Any inability to adequately address privacy and security concerns or comply with applicable privacy and data security laws, rules and regulations could expose the Company to potentially significant liabilities.

Additional Risks to the Company. The Company is subject to various risks in the normal course of business as well as catastrophic events including severe weather events, earthquakes, fires, acts of war, terrorism, civil unrest, epidemics and pandemics and other unexpected events. Exhibit 99.1 sets forth risks and other factors that may affect future results, including those identified above, and is incorporated herein by reference.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

10

ITEM 2. PROPERTIES

Franklin Electric serves customers worldwide with over 220 manufacturing and distribution facilities located in over 20 countries. The Global Headquarters is located in Fort Wayne, Indiana, United States and houses sales, marketing and administrative offices along with a state of the art research and engineering facility. Besides the owned corporate facility, the Company considers the following to be principal properties:

| Location / Segment | Purpose | Own/Lease | ||||||

| Santa Catarina, Brazil / Water & Fueling | Manufacturing/Distribution/Sales | Own | ||||||

| Sao Paulo, Brazil / Water & Fueling | Manufacturing/Distribution/Sales | Own | ||||||

| Jiangsu Province, China / Water & Fueling | Manufacturing | Own | ||||||

| Brno, Czech Republic / Water | Manufacturing | Own | ||||||

| Vicenza, Italy / Water | Manufacturing | Own | ||||||

| Nuevo Leon, Mexico / Water & Fueling | Manufacturing | Own | ||||||

| Edenvale, South Africa / Water | Manufacturing | Own | ||||||

| Izmir, Turkey / Water | Manufacturing/Distribution/Sales/R&D | Own | ||||||

| Indiana, United States / Water | Manufacturing/Distribution/Sales | Lease | ||||||

| Montana, United States / Distribution | Distribution | Own | ||||||

| North Carolina, United States / Distribution | Distribution | Own | ||||||

| Oklahoma, United States / Water | Manufacturing | Own | ||||||

| Oregon, United States / Water | Manufacturing/Distribution/Sales/R&D | Lease | ||||||

| Wisconsin, United States / Fueling | Manufacturing/Distribution/Sales/R&D | Own | ||||||

The Company also owns and leases other smaller facilities which serve as manufacturing locations and distribution warehouses. The Company does not consider these facilities to be principal to the business or operations. In the Company’s opinion, its facilities are suitable for their intended use, adequate for the Company’s business needs, all currently utilized and in good condition.

ITEM 3. LEGAL PROCEEDINGS

The Company is defending various claims and legal actions which have arisen in the ordinary course of business. For a description of the Company's material legal proceedings, refer to Note 16 - Commitments and Contingencies, in the Notes to Consolidated Financial Statements included in Part II, Item 8, "Financial Statements and Supplementary Data," of this Annual Report on Form 10-K, which is incorporated into this Item 3 by reference. In the opinion of management, based on current knowledge of the facts and after discussion with counsel, other claims and legal actions can be defended or resolved without a material effect on the Company’s financial position, results of operations, and net cash flows.

11

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

Current executive officers of the Company, their ages, current position, and business experience during at least the past five years as of December 31, 2022, are as follows:

| Name | Age | Position Held | Period Holding Position | ||||||||

| Gregg C. Sengstack | 64 | Chairperson of the Board and Chief Executive Officer | 2015 - present | ||||||||

| Jeffery L. Taylor | 56 | Vice President, Chief Financial Officer | 2021 - present | ||||||||

| Chief Financial Officer, Blue Bird Corporation | 2020 - 2021 | ||||||||||

| Senior Vice President and Chief Financial Officer, Wabash National Corporation | 2014 - 2020 | ||||||||||

| Brent L. Spikes | 51 | Vice President, Global Manufacturing | 2022 - present | ||||||||

| Vice President, Global Water Engineering | 2020 - 2022 | ||||||||||

| Vice President, Manufacturing & Manufacturing Engineering | 2019 - 2020 | ||||||||||

| Director, Manufacturing & Manufacturing Engineering | 2018 - 2019 | ||||||||||

| Director, Advanced Manufacturing | 2014 - 2018 | ||||||||||

| DeLancey W. Davis | 57 | Vice President and President, Headwater Companies | 2017 - present | ||||||||

| Vice President and President, North America Water Systems | 2012 - 2017 | ||||||||||

| Donald P. Kenney | 62 | Vice President and President, Global Water | 2019 - present | ||||||||

| Vice President and President, North America Water Systems | 2017 - 2019 | ||||||||||

| Vice President and President, Energy Systems | 2014 - 2017 | ||||||||||

| Jay J. Walsh | 53 | Vice President and President, Fueling Systems | 2019 - present | ||||||||

| President, Fueling Systems | 2017 - 2019 | ||||||||||

| Executive Vice President, Fueling Systems | 2013 - 2017 | ||||||||||

| Jonathan M. Grandon | 47 | Vice President, Chief Administrative Officer, General Counsel and Corporate Secretary | 2016 - present | ||||||||

| Kenneth Keene | 59 | Vice President, Global Supply | 2022 - present | ||||||||

| Vice President, EMEA Manufacturing | 2021 - 2022 | ||||||||||

| Vice President, Global Sourcing | 2018 - 2021 | ||||||||||

| Vice President, Sales - US | 2014 - 2018 | ||||||||||

All executive officers are elected annually by the Board of Directors at the Board meeting held in conjunction with the annual meeting of shareholders. All executive officers hold office until their successors are duly elected or until their death, resignation or removal by the Board.

12

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

The number of shareholders of record as of February 6, 2023 was 608. The Company’s stock is traded on the NASDAQ Global Select Market under the symbol FELE. Broadridge Corporate Issuer Solutions, Inc. 1155 Long Island Avenue, Edgewood, New York, 11717 serves as the registrar, record keeper and stock transfer agent.

Dividends paid per common share as quoted by the NASDAQ Global Select Market for 2022 and 2021 were as follows:

| Dividends per Share | |||||||||||

| 2022 | 2021 | ||||||||||

| 1st Quarter | $ | .1950 | $ | .1750 | |||||||

| 2nd Quarter | .1950 | .1750 | |||||||||

| 3rd Quarter | .1950 | .1750 | |||||||||

| 4th Quarter | .1950 | .1750 | |||||||||

The Company has increased dividend payments on an annual basis for 30 consecutive years. The payment of dividends in the future will be determined by the Board of Directors and will depend on business conditions, earnings, and other factors.

Issuer Purchases of Equity Securities

In April 2007, the Company’s Board of Directors unanimously approved a plan to increase the number of shares remaining for repurchase from 628,692 to 2,300,000 shares. There is no expiration date for this plan. On August 3, 2015, the Company’s Board of Directors approved a plan to increase the number of shares remaining for repurchase by an additional 3,000,000 shares. The authorization was in addition to the 535,107 shares that remained available for repurchase as of July 31, 2015. The Company repurchased 134,835 shares for approximately $10.8 million under this plan during the fourth quarter of 2022. The maximum number of shares that may still be purchased under this plan as of December 31, 2022 is 288,107. In February 2023, the Company’s Board of Directors approved a plan to increase the number of shares remaining for repurchase by an additional 1,000,000 shares. After giving effect to the February 2023 approval and share repurchase activity in 2023, the maximum number of shares that may still be purchased under this plan as of February 22, 2023 is 1,215,872.

| Period | Total Number of Shares Repurchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plan | Maximum Number of Shares that may yet to be Repurchased | ||||||||||

| October 1 - October 31 | — | $ | — | — | 422,942 | |||||||||

| November 1 - November 30 | — | $ | — | — | 422,942 | |||||||||

| December 1 - December 31 | 134,835 | $ | 80.40 | 134,835 | 288,107 | |||||||||

| Total | 134,835 | $ | 80.40 | 134,835 | 288,107 | |||||||||

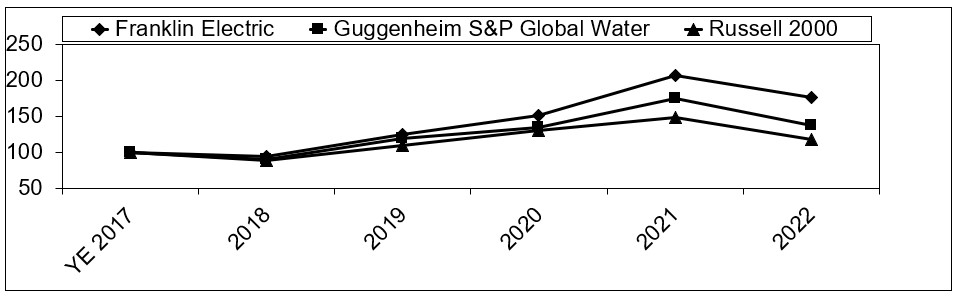

Stock Performance Graph

The following graph compares the Company’s cumulative total shareholder return (Common Stock price appreciation plus dividends, on a reinvested basis) over the last five fiscal years with the Guggenheim S&P Global Water Index and the Russell 2000 Index.

13

Hypothetical $100 invested on December 31, 2017 (fiscal year-end 2017) in Franklin Electric common stock (FELE), Guggenheim S&P Global Water Index, and Russell 2000 Index, assuming reinvestment of dividends:

| YE 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||||||||||||||||||||

| FELE | $ | 100 | $ | 94 | $ | 125 | $ | 151 | $ | 206 | $ | 176 | ||||||||||||||||||||||||||

| Guggenheim S&P Global Water | 100 | 90 | 119 | 135 | 175 | 137 | ||||||||||||||||||||||||||||||||

| Russell 2000 | 100 | 89 | 110 | 130 | 148 | 118 | ||||||||||||||||||||||||||||||||

14

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Discussion of the year-over-year comparison of changes in the Company's financial condition and results of operation as of and for the fiscal years ended December 31, 2021 and December 31, 2020 can be found in Part II, Item 7. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" of our Annual Report on Form 10-K for the fiscal year ended December 31, 2021.

2022 vs. 2021

OVERVIEW

Net sales in 2022 increased 23 percent compared to the prior year. The sales increase was primarily due to price and acquisitions. The impact of foreign currency translation decreased sales by about 5 percent. The Company's consolidated gross profit was $691.4 million for 2022, an increase of $115.3 million, or about 20 percent, from 2021. Net income attributable to the Company was $187.3 million, an increase of $33.5 million, or about 22 percent, from 2021.

RESULTS OF OPERATIONS

Net Sales

Net sales in 2022 were $2,043.7 million, an increase of $381.8 million, or about 23 percent, compared to 2021 sales of $1,661.9 million. The incremental impact to sales from acquired businesses was $131.9 million. Sales decreased by $77.1 million, or about 5 percent, in 2022 due to foreign currency translation.

| Net Sales | |||||||||||||||||

| (In millions) | 2022 | 2021 | 2022 v 2021 | ||||||||||||||

| Water Systems | $ | 1,157.5 | $ | 963.6 | $ | 193.9 | |||||||||||

| Fueling Systems | 334.1 | 289.1 | 45.0 | ||||||||||||||

| Distribution | 668.1 | 497.6 | 170.5 | ||||||||||||||

| Eliminations/Other | (116.0) | (88.4) | (27.6) | ||||||||||||||

| Consolidated | $ | 2,043.7 | $ | 1,661.9 | $ | 381.8 | |||||||||||

Net Sales-Water Systems

Water Systems sales were $1,157.5 million in 2022, an increase of $193.9 million, or about 20 percent, versus 2021. The incremental impact to sales from acquired businesses was $58.8 million. Foreign currency translation changes decreased sales $71.7 million, or about 7 percent, compared to 2021.

Water Systems sales in the U.S. and Canada increased by about 30 percent compared to 2021. The incremental impact to sales from acquired businesses was $54.1 million. Sales decreased by $3.0 million in 2022 due to foreign currency translation. In 2022, sales of groundwater pumping equipment increased by about 22 percent and sales of all surface pumping equipment increased by about 23 percent versus 2021, due to strong end market demand and pricing.

Water Systems sales in markets outside the U.S. and Canada increased by about 7 percent compared to 2021. The incremental impact to sales from acquired businesses was $4.7 million. Sales decreased by $68.7 million, or 17 percent, in 2022 due to foreign currency translation. Excluding the impact of acquisitions and foreign currency translation, sales increased in all major markets; EMEA, Latin America, and Asia Pacific.

Net Sales-Fueling Systems

Fueling Systems sales were $334.1 million in 2022, an increase of $45.0 million, or about 16 percent, from 2021. Foreign currency translation changes decreased sales $5.4 million, or about 2 percent, compared to 2021.

Fueling Systems sales in the U.S. and Canada increased by about 22 percent during 2022, primarily due to pricing actions and higher demand across all product lines. Outside the U.S. and Canada, Fueling Systems sales increased with sales growth in India more than offsetting lower sales in China. China sales were about $7 million in 2022 compared to about $12 million in 2021.

Net Sales-Distribution

Distribution sales were $668.1 million in 2022, an increase of $170.5 million, or about 34 percent, from 2021. The incremental impact to sales from acquired businesses was $73.1 million. Sales growth was driven by acquisitions, pricing and broad-based demand in all regions and product categories.

15

Cost of Sales

Cost of sales as a percent of net sales for 2022 and 2021 was 66.2 percent and 65.3 percent, respectively. Correspondingly, the gross profit margin was 33.8 percent and 34.7 percent, respectively. The gross profit margin decline was primarily a result of supply disruptions causing unfavorable absorption variances and higher inbound freight that was partially offset by realized pricing actions that more than offset inflationary cost increases. The Company's consolidated gross profit was $691.4 million for 2022, up $115.3 million from the gross profit of $576.1 million in 2021. The gross profit increase was primarily due to higher sales.

Selling, General and Administrative (“SG&A”)

SG&A expenses were $432.1 million in 2022 and increased $45.8 million compared to $386.3 million in the prior year. The increase was primarily due to incremental expenses from acquired businesses of $31 million. Additionally, higher travel and advertising expenses were partially offset by lower variable performance-based compensation expenses. SG&A costs as a percent of net sales decreased to 21.1 percent in 2022 from 23.2 percent in 2021.

Restructuring Expenses

Restructuring expenses were $2.2 million and $0.6 million in 2022 and 2021, respectively. Restructuring expenses were primarily from continued miscellaneous manufacturing realignment activities and branch closings and consolidations in the Distribution and Water Systems segments.

Operating Income

Operating income was $257.2 million in 2022, up $68.0 million, or 36 percent, from $189.2 million in 2021.

| Operating income (loss) | ||||||||||||||||||||

| (In millions) | 2022 | 2021 | 2022 v 2021 | |||||||||||||||||

| Water Systems | $ | 172.3 | $ | 139.1 | $ | 33.2 | ||||||||||||||

| Fueling Systems | 96.8 | 79.5 | 17.3 | |||||||||||||||||

| Distribution | 54.5 | 35.9 | 18.6 | |||||||||||||||||

| Eliminations/Other | (66.4) | (65.3) | (1.1) | |||||||||||||||||

| Consolidated | $ | 257.2 | $ | 189.2 | $ | 68.0 | ||||||||||||||

Operating Income-Water Systems

Water Systems operating income was $172.3 million in 2022 compared to $139.1 million in 2021, an increase of 24 percent. Operating income increased in Water Systems primarily due to higher sales volumes and SG&A cost controls. The 2022 operating income margin was 14.9 percent compared to 2021 operating income margin of 14.4 percent of net sales. Operating income margin increased in Water Systems primarily due to operating leverage on higher sales.

Operating Income-Fueling Systems

Fueling Systems operating income was $96.8 million in 2022 compared to $79.5 million in 2021, an increase of 22 percent. Operating income increased in Fueling Systems primarily due to higher sales volumes. The 2022 operating income margin was 29.0 percent compared to 27.5 percent of net sales in 2021. Operating income margin increased in Fueling Systems primarily due to operating leverage on higher sales.

Operating Income-Distribution

Distribution operating income was $54.5 million in 2022 compared to $35.9 million in 2021, an increase of 52 percent. Operating income increased in Distribution due to higher sales volumes. The 2022 operating income margin was 8.2 percent compared to 7.2 percent of net sales in 2021. The increase in operating income margin was primarily due to sales growth and operating leverage.

Operating Income-Eliminations/Other

Operating income-Eliminations/Other is composed primarily of inter-segment sales and profit eliminations and unallocated general and administrative expenses. The inter-segment profit elimination impact in 2022 decreased operating income by about $3.0 million more compared to 2021. The inter-segment elimination of operating income effectively defers the operating income on sales from Water Systems to Distribution in the consolidated financial results until the transferred product is sold from the Distribution segment to its third-party customer. Additionally, unallocated general and administrative expenses decreased $1.9 million compared to last year.

Interest Expense

Interest expense increased in 2022 to $11.5 million from $5.2 million in 2021 primarily due to higher outstanding debt levels and higher interest rates.

16

Other Income or Expense

Other income or expense was a loss of $3.2 million in 2022 compared to income of $8.0 million in 2021. Included in other income or expense in 2022 was a loss of $2.1 million related to a settlement of an indirect tax dispute. Other income or expense in 2021 included a bargain purchase gain of $6.5 million and a gain of $2.5 million related to a settlement of an indirect tax dispute.

Foreign Exchange

Foreign exchange was a loss of $7.2 million and $2.3 million in 2022 and 2021, respectively. The increase in 2022 was primarily due to transaction losses associated with the Argentine Peso and Turkish Lira. The Company reports the results of its subsidiaries in Argentina and Turkey using highly inflationary accounting, which requires that the functional currency of the entity be changed to the reporting currency of its parent.

Income Taxes

The provision for income taxes in 2022 and 2021 was $46.4 million and $34.7 million, respectively. The effective tax rate for 2022 both before and after the impact of discrete events was about 20 percent. The effective tax rate for 2021 was about 18 percent and, before the impact of discrete events, was about 21 percent. The tax rate was lower than the statutory rate of 21 percent primarily due to the recognition of the U.S. deduction for Foreign Derived Intangible Income, certain incentives, and discrete events. The increase in the effective tax rate in 2022 was primarily a result of smaller net favorable discrete events recorded in 2022 compared to 2021, primarily related to excess tax benefits from share-based compensation.

Net Income

Net income for 2022 was $188.8 million compared to 2021 net income of $155.0 million. Net income attributable to Franklin Electric Co., Inc. for 2022 was $187.3 million, or $3.97 per diluted share, compared to 2021 net income attributable to Franklin Electric Co., Inc. of $153.9 million, or $3.25 per diluted share.

CAPITAL RESOURCES AND LIQUIDITY

Sources of Liquidity

The Company's primary sources of liquidity are cash on hand, cash flows from operations, revolving credit agreements, and long-term debt funds available. The Company believes its capital resources and liquidity position at December 31, 2022 is adequate to meet projected needs for the foreseeable future. The Company expects that ongoing requirements for operations, capital expenditures, pension obligations, dividends, share repurchases, and debt service will be adequately funded from cash on hand, operations, and existing credit agreements.

As of December 31, 2022, the Company had a $350.0 million revolving credit facility. The facility is scheduled to mature on May 13, 2026. As of December 31, 2022, the Company had $223.2 million borrowing capacity under the Credit Agreement as $4.0 million in letters of commercial and standby letters of credit were outstanding and undrawn and $122.8 million in revolver borrowings were drawn and outstanding, which were primarily used for funding working capital requirements.

In addition, the Company maintains an uncommitted and unsecured private shelf agreement with NYL Investors LLC, an affiliate of New York Life, and each of the undersigned holders of Notes (the "New York Life Agreement") with a remaining borrowing capacity of $125.0 million as of December 31, 2022. The New York Life Agreement matures on July 30, 2024. The Company also has other long-term debt borrowings outstanding as of December 31, 2022. See Note 10 - Debt for additional specifics regarding these obligations and future maturities.

At December 31, 2022, the Company had $43.4 million of cash and cash equivalents held in foreign jurisdictions, which the Company intends to use to fund foreign operations. There is currently no need to repatriate these funds in order to meet domestic funding obligations or scheduled cash distributions.

Cash Flows

The following table summarizes significant sources and uses of cash and cash equivalents:

| (in thousands) | 2022 | 2021 | |||||||||

| Cash flows from operating activities | $ | 101.7 | $ | 129.8 | |||||||

| Cash flows from investing activities | $ | (43.1) | $ | (264.8) | |||||||

| Cash flows from financing activities | $ | (48.5) | $ | 50.9 | |||||||

| Impact of exchange rates on cash and cash equivalents | $ | (4.9) | $ | (6.1) | |||||||

| Change in cash and cash equivalents | $ | 5.2 | $ | (90.2) | |||||||

17

Cash Flows from Operating Activities

2022 vs 2021

Net cash provided by operating activities was $101.7 million for 2022 compared to $129.8 million for 2021. The decrease in cash provided by operating activities was primarily due to increased working capital requirements in support of higher revenues.

Cash Flows from Investing Activities

2022 vs. 2021

Net cash used in investing activities was $43.1 million in 2022 compared to $264.8 million in 2021. The decrease was primarily attributable to decreased acquisition activity in 2022.

Cash Flows from Financing Activities

2022 vs. 2021

Net cash used by financing activities was $48.5 million in 2022 compared to $50.9 million provided by financing activities in 2021. The change in financing cash flows was attributable to decreased net proceeds from debt and common stock issuances, increased stock repurchases, higher dividend payments and deferred payments related to acquisitions.

AGGREGATE CONTRACTUAL OBLIGATIONS

The majority of the Company’s contractual obligations to third parties relate to debt obligations. In addition, the Company has certain contractual obligations for future lease payments and purchase obligations. The payment schedule for these contractual obligations is as follows:

| (In millions) | More than | ||||||||||||||||||||||||||||

| Total | 2023 | 2024-2025 | 2026-2027 | 5 years | |||||||||||||||||||||||||

| Debt | $ | 216.2 | $ | 126.8 | $ | 77.8 | $ | 2.9 | $ | 8.7 | |||||||||||||||||||

| Debt interest | 19.9 | 9.4 | 8.2 | 1.3 | 1.0 | ||||||||||||||||||||||||

| Operating leases | 52.9 | 17.1 | 20.5 | 10.6 | 4.7 | ||||||||||||||||||||||||

| Purchase obligations | 12.8 | 12.8 | — | — | — | ||||||||||||||||||||||||

| Income Taxes-U.S. Tax Cuts and Jobs Act transition tax | $ | 11.6 | $ | 2.9 | $ | 8.7 | $ | — | $ | — | |||||||||||||||||||

| $ | 313.4 | $ | 169.0 | $ | 115.2 | $ | 14.8 | $ | 14.4 | ||||||||||||||||||||

Interest payments on debt obligations are calculated for future periods using interest rates in effect at the end of 2022. Certain of these projected interest payments may differ in the future based on interest rates or other factors or events. The projected interest payments only pertain to obligations and agreements outstanding at December 31, 2022.

The Company has pension and other post-retirement benefit obligations not included in the table above which will result in estimated future payments of approximately $0.8 million in 2023. In addition, due to the timing of funding in future periods being uncertain and dependent on future movements in interest rates, investment returns, changes in laws and regulations and other variables, the table above excludes the non-current liability of $24.9 million for cash outflows related to the Company's pension plans.

The Company also has unrecognized tax benefits, none of which are included in the table above. The unrecognized tax benefits of approximately $0.9 million have been recorded as liabilities and the Company is uncertain as to if or when such amounts may be settled. Related to the unrecognized tax benefits, the Company has also recorded a liability for potential penalties and interest of $0.2 million.

ACCOUNTING PRONOUNCEMENTS

For information regarding recent accounting pronouncements, refer to Note 2 - Accounting Pronouncements, in the Notes to Consolidated Financial Statements in the sections entitled ""Adoption of New Accounting Standards" and "Accounting Standards Issued But Not Yet Adopted", included in Part II, Item 8, "Financial Statements and Supplementary Data" of this Annual Report on Form 10-K.

CRITICAL ACCOUNTING ESTIMATES

Management’s discussion and analysis of its financial condition and results of operations are based upon the Company’s consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and the related disclosure of contingent assets and liabilities. Management evaluates estimates on an ongoing basis. Estimates are based on historical experience and on other

18

assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. There were no material changes to estimates or methodologies used to develop those estimates in 2022. The Company’s critical accounting estimates are identified below:

Inventory Valuation

The Company uses certain estimates and judgments to value inventory. Inventory is recorded at the lower of cost or net realizable value. The Company reviews its inventories for excess or obsolete products or components. Based on an analysis of historical usage, management’s evaluation of estimated future demand, market conditions, and alternative uses for possible excess or obsolete parts, carrying values are adjusted. The carrying value is reduced regularly to reflect the age and current anticipated product demand. If actual demand differs from the estimates, additional reductions would be necessary in the period such determination is made. Excess and obsolete inventory is periodically disposed of through sale to third parties, scrapping, or other means.

Business Combinations and Valuation of Acquired Intangible Assets

The Company follows the guidance under FASB ASC Topic 805, Business Combinations. The acquisition purchase price is allocated to the assets acquired and liabilities assumed based upon their respective fair values. The Company utilizes management estimates and an independent third-party valuation firm to assist in determining the fair values of assets acquired, including intangible assets, and liabilities assumed. The identifiable intangible assets acquired typically include customer relationships and trade names. Identifiable intangible assets are initially valued using a methodology commensurate with the intended use of the asset. The fair value of customer relationships is measured using the multi-period excess earnings method ("MPEEM"). The fair value of trade names is measured using a relief-from-royalty ("RFR") approach, which assumes the value of the trade name is the discounted amount of cash flows that would be paid to third parties had the Company not owned the trade name and instead licensed the trade name from another company. Higher royalty rates are assigned to premium brands within the marketplace based on name recognition and profitability, while other brands receive lower royalty rates. The basis for future sales projections for both the RFR and MPEEM are based on internal revenue forecasts which the Company believes represents reasonable market participant assumptions. The future cash flows are discounted using an applicable discount rate as well as any potential risk premium to reflect the inherent risk of holding a standalone intangible asset. The key uncertainties in the RFR and MPEEM calculations, as applicable, are the selection of an appropriate royalty rate, assumptions used in developing estimates of future cash flows, including revenue growth and expense forecasts, assumed customer attrition rates, as well as the perceived risk associated with those forecasts in determining the discount rate and risk premium. There is inherent uncertainty in forecasted future cash flows and therefore, actual results may differ and could result in subsequent impairment charges of acquired intangibles and/or goodwill.

Indefinite-Lived Intangible Asset and Goodwill Impairment Evaluation

According to FASB ASC Topic 350, Intangibles - Goodwill and Other, intangible assets with indefinite lives must be tested for impairment at least annually or more frequently as warranted by triggering events that indicate potential impairment. The Company uses a variety of methodologies in conducting impairment assessments including income and market approaches. For indefinite-lived assets apart from goodwill, primarily trade names for the Company, if the fair value is less than the carrying amount, an impairment charge is recognized in an amount equal to that excess. The Company has not made any material changes to the method of evaluating impairments during the last three years.

In compliance with FASB ASC Topic 350, goodwill is not amortized. Goodwill is tested at the reporting unit level for impairment annually or more frequently as warranted by triggering events that indicate potential impairment. Reporting units are operating segments or one level below, known as components, which can be aggregated for testing purposes. The Company’s goodwill is allocated to the Global Water Systems, Fueling Systems and Distribution reporting units. As the Company’s business model evolves, management will continue to evaluate its reporting units and review the aggregation criteria.

In assessing the recoverability of goodwill, the Company determines the fair value of its reporting units by utilizing a combination of both the market value and income approaches. The market value approach compares the reporting units’ current and projected financial results to entities of similar size and industry to determine the market value of the reporting unit. The income approach utilizes assumptions regarding estimated future cash flows and other factors to determine the fair value of the respective assets. These cash flows consider factors regarding expected future operating income and historical trends, as well as the effects of demand and competition. The Company is required to record an impairment if these assumptions and estimates change whereby the fair value of the reporting units is below their associated carrying values. Goodwill included on the balance sheet as of the year ended December 31, 2022 was $328.0 million.

19

During the fourth quarter of 2022, the Company completed its annual impairment test of goodwill and indefinite-lived trade names and determined the fair value of all intangibles were substantially in excess of the respective carrying values. Significant judgment is required to determine if an indication of impairment has taken place. Factors to be considered include the following: adverse changes in operating results, decline in strategic business plans, significantly lower future cash flows, and sustainable declines in market data such as market capitalization. A 10 percent decrease in the fair value estimates used in the impairment tests would not have changed this determination. The sensitivity analysis required the use of numerous subjective assumptions, which, if actual experience varies, could result in material differences in the requirements for impairment charges. Further, an extended downturn in the economy may impact certain components of the operating segments more significantly and could result in changes to the aggregation assumptions and impairment determination.

Income Taxes

Under the requirements of FASB ASC Topic 740, Income Taxes, the Company records deferred tax assets and liabilities for the future tax consequences attributable to differences between financial statement carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The Company analyzes the deferred tax assets and liabilities for their future realization based on the estimated existence of sufficient taxable income. This analysis considers the following sources of taxable income: prior year taxable income, future reversals of existing taxable temporary differences, future taxable income exclusive of reversing temporary differences and tax planning strategies that would generate taxable income in the relevant period. If sufficient taxable income is not projected then the Company will record a valuation allowance against the relevant deferred tax assets.

The Company’s operations involve dealing with uncertainties and judgments in the application of complex tax regulations in multiple jurisdictions. These jurisdictions have different tax rates, and the Company determines the allocation of income to each of these jurisdictions based upon various estimates and assumptions. In the normal course of business, the Company will undergo tax audits by various tax jurisdictions. Such audits often require an extended period of time to complete and may result in income tax adjustments if changes to the allocation are required between jurisdictions with different tax rates. The final taxes paid are dependent upon many factors, including negotiations with taxing authorities in the various jurisdictions and resolution of disputes arising from federal, state, and international tax audits. Although the Company has recorded all income tax uncertainties in accordance with FASB ASC Topic 740, these accruals represent estimates that are subject to the inherent uncertainties associated with the tax audit process. Management judgment is required in determining the Company’s provision for income taxes, deferred tax assets and liabilities, which, if actual experience varies, could result in material adjustments to tax expense and/or deferred tax assets and liabilities.

Pension and Employee Benefit Obligations

The Company consults with its actuaries to assist with the calculation of discount rates used in its pension and post retirement plans. The discount rates used to determine domestic pension and post-retirement plan liabilities are calculated using a full yield curve approach. Market conditions have caused the weighted-average discount rate to move from 2.68 percent last year to 5.15 percent this year for the domestic pension plans and from 2.57 percent last year to 5.08 percent this year for the postretirement health and life insurance plan. A change in the discount rate selected by the Company of 25 basis points would result in a change of about $0.1 million to employee benefit expense and a change of about $3.7 million of liability.

The Company consults with actuaries and investment advisors in making its determination of the expected long-term rate of return on plan assets. Using input from these consultations such as long-term investment sector expected returns, the correlations and standard deviations thereof, and the plan asset allocation, the Company will use an expected long-term rate of return on plan assets of 5.70 percent in measuring net periodic cost for 2023. Market conditions have caused the expected long-term rate or return to increase from 4.50 percent as used in measuring net periodic cost for 2022. A change in the long-term rate of return selected by the Company of 25 basis points would result in a change of about $0.3 million of employee benefit expense.

FACTORS THAT MAY AFFECT FUTURE RESULTS

This annual report on Form 10-K contains certain forward-looking information, such as statements about the Company’s financial goals, acquisition strategies, financial expectations including anticipated revenue or expense levels, business prospects, market positioning, product development, manufacturing re-alignment, capital expenditures, tax benefits and expenses, and the effect of contingencies or changes in accounting policies. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “intend,” “estimate,” “may increase,” “may fluctuate,” “plan,” “goal,” “target,” “strategy,” and similar expressions or future or conditional verbs such as “may,” “will,” “should,” “would,” and “could.” While the Company believes that the assumptions underlying such forward-looking statements are reasonable based on present conditions, forward-looking statements made by the Company involve risks and uncertainties and are not guarantees of future performance. Actual results may differ materially from those forward-looking statements as a result of

20

various factors, including general economic and currency conditions, various conditions specific to the Company’s business and industry, new housing starts, weather conditions, epidemics and pandemics, market demand, competitive factors, changes in distribution channels, supply constraints, effect of price increases, raw material costs, technology factors, integration of acquisitions, litigation, government and regulatory actions, the Company’s accounting policies, and other risks, all as described in Item 1A and Exhibit 99.1 of this Form 10-K. Any forward-looking statements included in this Form 10-K are based upon information presently available. The Company does not assume any obligation to update any forward-looking information, except as required by law.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK