UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended September 30 , 2024

OR

For the transition period from to

Commission file number 001-08359

| (Exact name of registrant as specified in its charter) | ||||||||||||||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||||||||||||||

| (Address of principal executive offices) | (Registrant’s telephone number, including area code) | |||||||||||||||||||

| Securities registered pursuant to Section 12 (b) of the Act: | ||||||||

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12 (g) of the Act: None | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by checkmark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

The aggregate market value of the registrant’s common stock held by non-affiliates was $4,220,553,504 based on the closing price of $42.91 per share on March 31, 2024, as reported on the New York Stock Exchange.

The number of shares outstanding of $2.50 par value common stock as of November 22, 2024 was 99,769,083 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the Annual Meeting of Shareowners (Proxy Statement) to be held on January 21, 2025, are incorporated by reference into Part I and Part III of this report.

New Jersey Resources Corporation

TABLE OF CONTENTS

| Page | |||||||||||

| PART I | |||||||||||

| ITEM 1. | |||||||||||

| ITEM 1A. | |||||||||||

| ITEM 1B. | |||||||||||

| ITEM 1C. | Cybersecurity | ||||||||||

| ITEM 2. | |||||||||||

| ITEM 3. | |||||||||||

| ITEM 4. | |||||||||||

| PART II | |||||||||||

| ITEM 5. | |||||||||||

| ITEM 6. | |||||||||||

| ITEM 7. | |||||||||||

| ITEM 7A. | |||||||||||

| ITEM 8. | |||||||||||

Report of Independent Registered Public Accounting Firm (PCAOB ID No. | |||||||||||

| ITEM 9. | |||||||||||

| ITEM 9A. | |||||||||||

| ITEM 9B. | |||||||||||

| PART III* | |||||||||||

| ITEM 10. | |||||||||||

| ITEM 11. | |||||||||||

| ITEM 12. | |||||||||||

| ITEM 13. | |||||||||||

| ITEM 14. | |||||||||||

| PART IV | |||||||||||

| ITEM 15. | |||||||||||

| * Portions of Item 10 and Items 11-14 are Incorporated by Reference from the Proxy Statement. | |||||||||||

i

New Jersey Resources Corporation

GLOSSARY OF KEY TERMS

| Adelphia | Adelphia Gateway, LLC | ||||

| ADI | Administratively Determined Incentive | ||||

| AFUDC | Allowance for Funds Used During Construction | ||||

| AMA | Asset Management Agreement | ||||

| ARO | Asset Retirement Obligation | ||||

| ASC | Accounting Standards Codification | ||||

| ASU | Accounting Standards Update | ||||

| B | Billion | ||||

| Bcf | Billion Cubic Feet | ||||

| BGSS | Basic Gas Supply Service | ||||

| BPU | New Jersey Board of Public Utilities | ||||

| CEO | Chief Executive Officer | ||||

| CIO | Chief Information Officer | ||||

| CIP | Conservation Incentive Program | ||||

| Clean Energy Ventures or CEV | Clean Energy Ventures segment | ||||

| CME | Chicago Mercantile Exchange | ||||

| CR&R | Commercial Realty & Resources Corp. | ||||

| CSI | Competitive Solar Incentive | ||||

| Degree-day | The measure of the variation in the weather based on the extent to which the average daily temperature falls below 65 degrees Fahrenheit | ||||

| DEI | Diversity, equity and inclusion | ||||

| DRP | NJR Direct Stock Purchase and Dividend Reinvestment Plan | ||||

| Dths | Dekatherms | ||||

| EDECA | Electric Discount and Energy Competition Act | ||||

| EE | Energy Efficiency | ||||

| EMP | New Jersey Energy Master Plan | ||||

| Energy Services or ES | Energy Services segment | ||||

| Exchange Act | Securities Exchange Act of 1934, as amended | ||||

| FASB | Financial Accounting Standards Board | ||||

| FCM | Futures Commission Merchant | ||||

| FERC | Federal Energy Regulatory Commission | ||||

| Financial Margin | A non-GAAP financial measure, which represents revenues earned from the sale of natural gas less costs of natural gas sold including any transportation and storage costs, and excludes certain operations and maintenance expense and depreciation and amortization, as well as any accounting impact from the change in the fair value of certain derivative instruments | ||||

| Fitch | Fitch Ratings Company | ||||

| FMB | First Mortgage Bond | ||||

| GAAP | Generally Accepted Accounting Principles of the United States | ||||

| GWRA | Global Warming Response Act of 2007 | ||||

| HCCTR | Health Care Cost Trend Rate | ||||

| Home Services and Other or HSO | Home Services and Other Operations | ||||

| ICE | Intercontinental Exchange | ||||

| IIP | Infrastructure Investment Program | ||||

| Inflation Reduction Act | Inflation Reduction Act of 2022 | ||||

| IRS | Internal Revenue Service | ||||

| ISDA | The International Swaps and Derivatives Association | ||||

| ITC | Federal Investment Tax Credit | ||||

| LDCC | Leadership Development and Compensation Committee | ||||

| Leaf River | Leaf River Energy Center LLC | ||||

| LNG | Liquefied Natural Gas | ||||

| M | Million | ||||

| MGP | Manufactured Gas Plant | ||||

| MMBtu | Million British Thermal Units | ||||

| Moody’s | Moody’s Investors Service, Inc. | ||||

| Mortgage Indenture | The Amended and Restated Indenture of Mortgage, Deed of Trust and Security Agreement between NJNG and U.S. Bank National Association dated as of September 1, 2014, as amended | ||||

Page 1

New Jersey Resources Corporation

| GLOSSARY OF KEY TERMS (cont.) | |||||

| MW | Megawatts | ||||

| MWh | Megawatt Hour | ||||

| NAESB | The North American Energy Standards Board | ||||

| NAV | Net Asset Value | ||||

| NFE | Net Financial Earnings | ||||

| NJCEP | New Jersey’s Clean Energy Program | ||||

| NJDEP | New Jersey Department of Environmental Protection | ||||

| NJNG | New Jersey Natural Gas Company or our Natural Gas Distribution segment | ||||

| NJNG Credit Facility | The $250M unsecured committed credit facility expiring in August 2029 | ||||

| NJR Credit Facility | The $575M unsecured committed credit facility expiring in August 2029 | ||||

| NJR or The Company | New Jersey Resources Company | ||||

| NJR Retail | NJR Retail Company | ||||

| NJRCEV | NJR Clean Energy Ventures Corporation | ||||

| NJRES | NJR Energy Services Company, LLC | ||||

| NJRHS | NJR Home Services Company | ||||

| Non-GAAP | Not in accordance with GAAP | ||||

| NPNS | Normal Purchase/Normal Sale | ||||

| NYMEX | New York Mercantile Exchange | ||||

| OCI | Other Comprehensive Income | ||||

| O&M | Operations and Maintenance Expense | ||||

| OPEB | Other Postemployment Benefit Plans | ||||

| PBO | Projected Benefit Obligation | ||||

| PennEast | PennEast Pipeline Company, LLC | ||||

| PEP | Pension Equalization Plan | ||||

| PIM | Pipeline Integrity Management | ||||

| PPA | Power Purchase Agreement | ||||

| RAC | Remediation Adjustment Clause | ||||

| REC | Renewable Energy Certificate | ||||

| Sarbanes-Oxley | Sarbanes-Oxley Act of 2002 | ||||

| SAVEGREEN | The SAVEGREEN Project® | ||||

| Savings Plan | Employees’ Retirement Savings Plan | ||||

| SBC | Societal Benefits Charge | ||||

| SEC | Securities and Exchange Commission | ||||

| Securities Act | Securities Act of 1933, as amended | ||||

| SG&A | Selling, General and Administrative expenses | ||||

| SREC | Solar Renewable Energy Certificate | ||||

| S&P | Standard & Poor’s Financial Services, LLC | ||||

| Steckman Ridge | Collectively, Steckman Ridge GP, LLC and Steckman Ridge, LP | ||||

| Storage and Transportation or S&T | Storage and Transportation segment | ||||

| TETCO | Texas Eastern Transmission | ||||

| TREC | Transition Renewable Energy Certificate | ||||

| Trustee | U.S. Bank National Association | ||||

| TSR | Total Shareholder Return | ||||

| U.S. | The United States of America | ||||

| Union | International Brotherhood of Electrical Workers Local 1820 | ||||

| USF | Universal Service Fund | ||||

| Utility Gross Margin | A non-GAAP financial measure, which represents operating revenues less natural gas purchases, sales tax, and regulatory rider expense, and excludes certain operations and maintenance expense and depreciation and amortization | ||||

Page 2

New Jersey Resources Corporation

INFORMATION CONCERNING FORWARD-LOOKING STATEMENTS

Certain statements contained in this report, including, without limitation, statements as to management expectations, assumptions and beliefs presented in Part I, Item 1. Business and Item 3. Legal Proceedings, and in Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 7A. Quantitative and Qualitative Disclosures About Market Risk, and in the notes to the financial statements, are forward-looking statements within the meaning of Section 27A of the Securities Act, Section 21E of the Exchange Act and the Private Securities Litigation Reform Act of 1995. Forward-looking statements can also be identified by the use of forward-looking terminology such as “anticipate,” “estimate,” “may,” “could,” “might,” “intend,” “expect,” “believe,” “will,” “plan,” “should” or comparable terminology and are made based upon management’s current expectations, assumptions and beliefs as of this date concerning future developments and their potential effect on us. There can be no assurance that future developments will be in accordance with management’s expectations, assumptions or beliefs, or that the effect of future developments on us will be those anticipated by management.

We caution readers that the expectations, assumptions and beliefs that form the basis for forward-looking statements regarding customer growth, customer usage, qualifications for ITCs, RECs, future rate case proceedings, financial condition, results of operations, cash flows, capital requirements, future capital expenditures, market risk, effective tax rate, the gain on the sale of the CEV residential solar asset portfolio and other matters for fiscal 2025 and thereafter include many factors that are beyond our ability to control or estimate precisely, such as estimates of future market conditions, the behavior of other market participants and changes in the debt and equity capital markets. The factors that could cause actual results to differ materially from our expectations, assumptions and beliefs include, but are not limited to, those discussed in Part I, Item 1A. Risk Factors, as well as the following, which are neither presented in order of importance nor weighted:

•our ability to obtain governmental and regulatory approvals, permits, certificates, land-use rights, electric grid connection (in the case of clean energy projects) and/or financing for the construction, development and operation of our unregulated energy investments, pipeline transportation systems and NJNG and S&T infrastructure projects in a timely manner;

•our ability to address concerns over climate change and its impacts on business operations;

•risks associated with our investments in clean energy projects, including the availability of regulatory incentives and federal tax credits, the availability of viable projects, our eligibility for ITCs, the future market for RECs and electricity prices, our ability to complete construction of the projects and operational risks related to projects in service;

•risks associated with acquisitions and the related integration of acquired assets with our current operations;

•our ability to comply with current and future regulatory requirements;

•risks associated with our pipeline of projects and timely completion of such projects;

•commercial and wholesale credit risks, including the availability of creditworthy customers and counterparties, and liquidity in the wholesale energy trading market;

•volatility of natural gas and other commodity prices and their impact on NJNG customer usage, NJNG’s BGSS incentive programs, ES operations and our risk management efforts;

•the performance of our subsidiaries;

•access to adequate supplies of natural gas and dependence on third-party S&T facilities for natural gas supply;

•the level and rate at which NJNG’s costs are incurred and the extent to which they are approved for recovery from customers through the regulatory process, including through future base rate case filings;

•impacts of inflation, including the current inflationary environment, and increased natural gas costs;

•the impact of a disallowance of recovery of environmental-related expenditures and other regulatory changes;

•operating risks incidental to handling, storing, transporting and providing customers with natural gas;

•demographic changes in our service territory and their effect on our customer growth;

•changes in rating agency requirements and/or credit ratings and their effect on availability and cost of capital to the Company;

•the impact of events causing volatility in the equity and credit markets on our access to capital, including natural disasters, pandemic illness and other extreme events and risks, political and economic disruption and uncertainty related to Russia’s military invasion of Ukraine, the conflict in the Middle East, and the international community’s responses;

•risks of prolonged constriction of credit availability in the markets and our ability to secure short-term financing;

•our ability to comply with debt covenants;

•the results of legal or administrative proceedings with respect to claims, rates, environmental issues, natural gas cost prudence reviews and other matters;

•risks related to cyberattacks, including ransomware, terrorism and other malicious acts against, or failure of, information technology systems;

•the impact to the asset values and resulting higher costs and funding obligations of our pension and postemployment benefit plans as a result of potential downturns in the financial markets, including, but not limited to, inflationary pressures, recessionary pressures, or rising interest rates, and/or reductions in bond yields;

•accounting effects and other risks associated with hedging activities and use of derivatives contracts;

•our ability to optimize our physical assets;

•weather and economic conditions, including those changes in weather and weather patterns that could be attributable to climate change;

•the costs of compliance with present and future environmental laws, potential climate change-related legislation or any legislation resulting from the 2019 New Jersey EMP, as well as future executive orders and the outcomes of regulatory proceedings concerning natural gas;

•uncertainties related to litigation, regulatory, administrative or environmental proceedings;

•changes to tax laws and regulations, including our ability to optimize those changes brought about by the passage of the Inflation Reduction Act;

•any potential need to record a valuation allowance for our deferred tax assets;

•the delay or prevention of a favorable transaction due to changes in control provisions or laws;

•risks related to our employee workforce and succession planning;

•risks associated with the management of our joint ventures and partnerships; and

•risks associated with keeping pace with technological change.

Forward-looking statements made in this report apply only as of the date of this report. While we periodically reassess material trends and uncertainties affecting our results of operations and financial condition in connection with the preparation of management’s discussion and analysis of results of operations and financial condition contained in our Quarterly and Annual Reports on Form 10-Q and Form 10-K, respectively, we do not, by including this statement, assume any obligation to review or revise any particular forward-looking statement referenced herein in light of future events.

Page 3

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS

| ORGANIZATIONAL STRUCTURE | ||

New Jersey Resources Corporation is a New Jersey corporation and a diversified energy services holding company whose principal business is the distribution of natural gas through a regulated utility, investing in and operating clean energy projects and natural gas storage and transportation assets, and providing other retail and wholesale energy services to customers. We are an exempt holding company under Section 1263 of the Energy Policy Act of 2005.

Our primary subsidiaries include the following:

New Jersey Natural Gas Company provides regulated natural gas utility service to residential and commercial customers throughout Burlington, Middlesex, Monmouth, Morris, Ocean and Sussex counties in New Jersey and participates in the off-system sales and capacity release markets. NJNG, a local natural gas distribution company, is regulated by the BPU and comprises the Company’s Natural Gas Distribution segment.

NJR Clean Energy Ventures Corporation includes the results of operations and assets related to the Company’s unregulated capital investments in clean energy projects, including commercial and residential solar projects. NJRCEV comprises the Company’s Clean Energy Ventures segment.

NJR Energy Services Company, LLC maintains and transacts around a portfolio of physical assets consisting of natural gas transportation and storage contracts in the U.S. NJRES also provides unregulated wholesale energy management services to other energy companies and natural gas producers. NJRES comprises our Energy Services segment.

NJR Midstream Holdings Corporation, which comprises the Storage and Transportation segment, invests in energy-related ventures through its subsidiaries: NJR Midstream Company, which includes our wholly-owned subsidiaries of Leaf River, located in southeastern Mississippi, and Adelphia, located in eastern Pennsylvania, which are subject to FERC regulation; and NJR Steckman Ridge Storage Company, which holds our 50% combined ownership interest in Steckman Ridge, located in Pennsylvania.

NJR Home Services Company provides heating, ventilation and cooling service, sales and installation of appliances, as well as solar installation projects, and is the primary contributor to Home Services and Other operations.

Page 4

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

| REPORTING SEGMENTS | ||

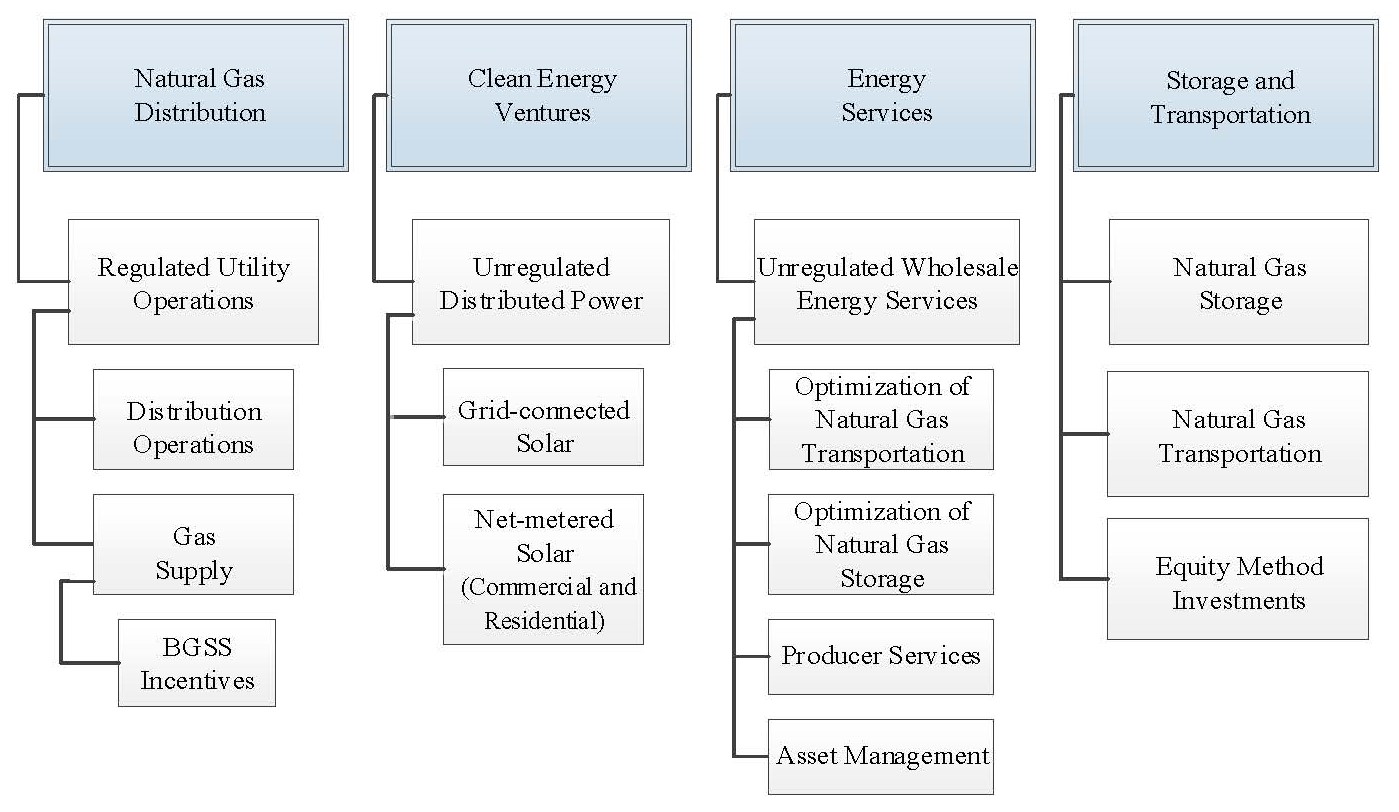

We operate within four reporting segments: Natural Gas Distribution, Clean Energy Ventures, Energy Services and Storage and Transportation.

NJNG consists of regulated natural gas services, off-system sales, capacity and storage management operations. ES consists of unregulated wholesale and retail energy operations, as well as energy management services. CEV consists of capital investments in clean energy projects. S&T consists of operations and investments in the natural gas storage and transportation market, such as natural gas storage and transportation facilities.

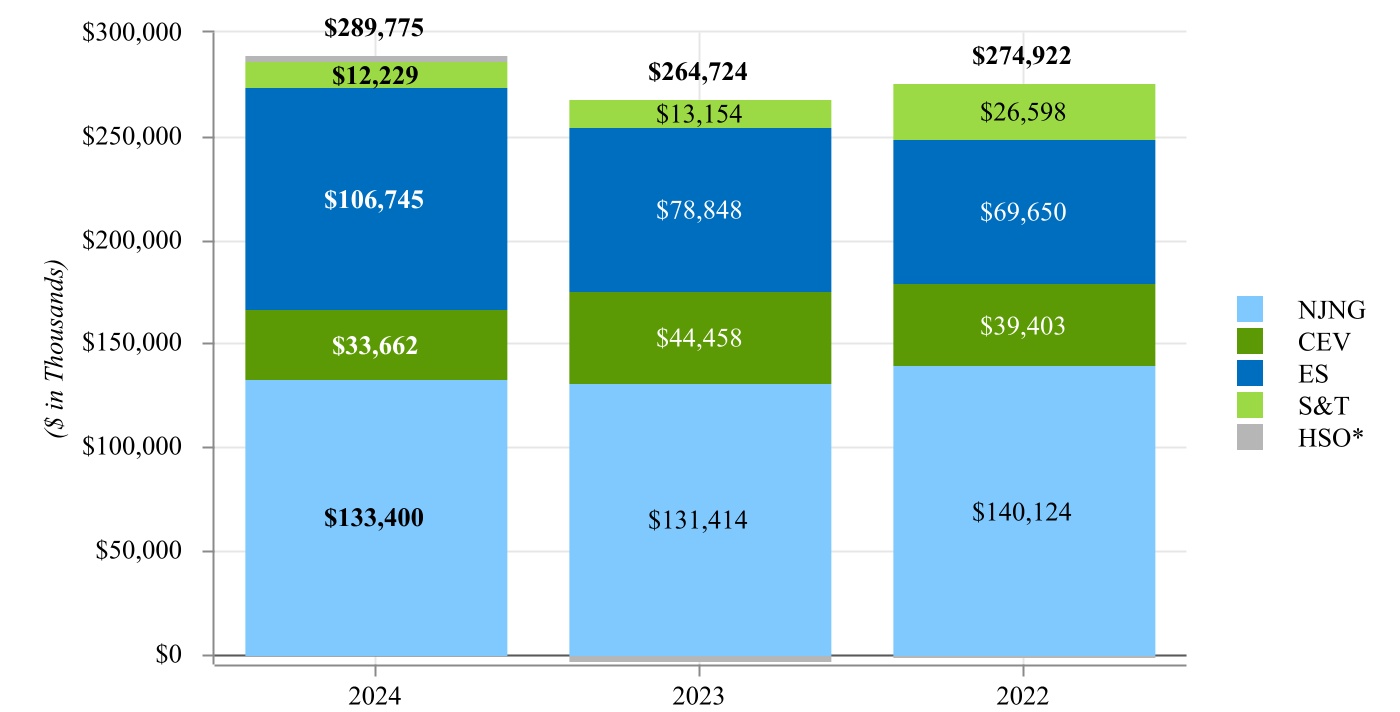

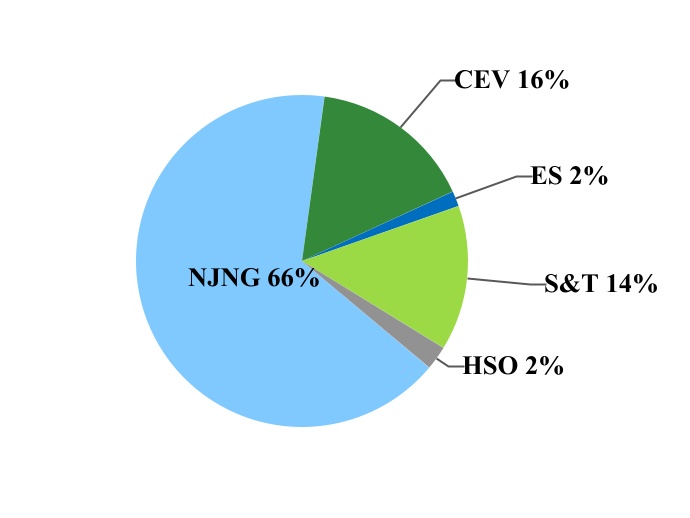

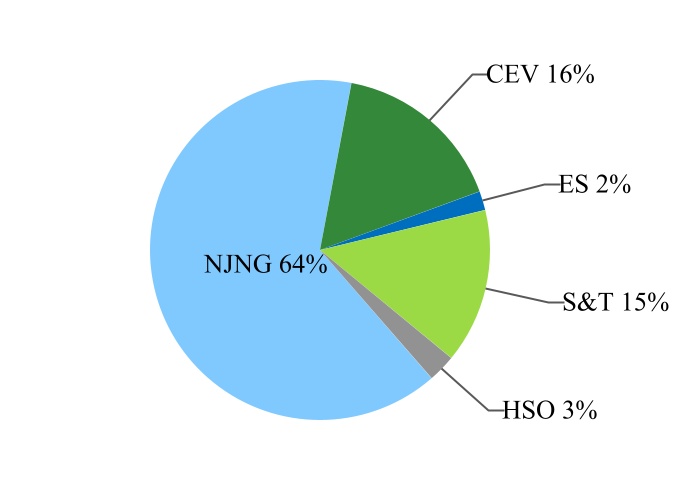

Net income by reporting segment and other business operations for the fiscal years ended September 30, are as follows:

* HSO includes intercompany eliminations.

Asset composition by reporting segment and other business operations at September 30, are as follows:

| 2024 | 2023 | ||||

Page 5

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

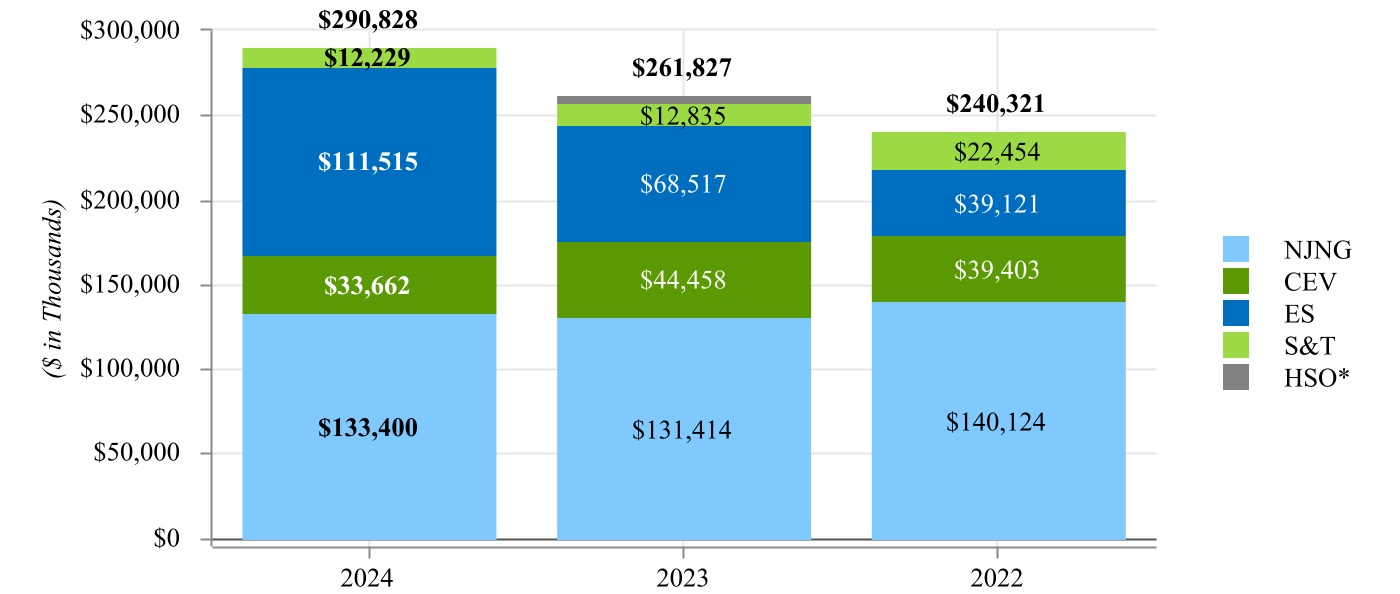

Management uses NFE, a non-GAAP financial measure, when evaluating its operating results. NFE is a measure of the earnings based on eliminating timing differences surrounding the recognition of certain gains or losses to effectively match the earnings effects of the economic hedges with the physical sale of natural gas and, therefore, eliminates the impact of volatility to GAAP earnings associated with the derivative instruments. To the extent we utilize forwards, futures or other derivatives to hedge natural gas transactions and forecasted SREC production, the resulting unrealized gains and losses are also eliminated from NFE. ES economically hedges its natural gas inventory with financial derivative instruments and calculates the related tax effect based on the statutory rate. NFE also excludes certain transactions associated with equity method investments, including impairment charges, which are non-cash charges, and return of capital in excess of the carrying value of our investment. These are considered unusual in nature and occur infrequently and are not indicative of the Company’s performance for its ongoing operations. Included in the tax effects are current and deferred income tax expense corresponding with the components of NFE.

Non-GAAP financial measures are not in accordance with, or an alternative to, GAAP, and should be considered in addition to, and not as a substitute for, the comparable GAAP measure. The following is a reconciliation of consolidated net income, the most directly comparable GAAP measure, to NFE for the fiscal years ended September 30:

| (Thousands) | 2024 | 2023 | 2022 | ||||||||

| Net income | $ | 289,775 | $ | 264,724 | $ | 274,922 | |||||

| Add: | |||||||||||

| Unrealized loss (gain) on derivative instruments and related transactions | 19,574 | (38,081) | (59,906) | ||||||||

| Tax effect | (4,652) | 9,050 | 14,248 | ||||||||

Effects of economic hedging related to natural gas inventory (1) | (18,192) | 34,699 | 19,939 | ||||||||

| Tax effect | 4,323 | (8,246) | (4,738) | ||||||||

| Gain on equity method investment | — | (300) | (5,521) | ||||||||

| Tax effect | — | (19) | 1,377 | ||||||||

| NFE | $ | 290,828 | $ | 261,827 | $ | 240,321 | |||||

| Basic earnings per share | $ | 2.94 | $ | 2.73 | $ | 2.86 | |||||

| Add: | |||||||||||

| Unrealized loss (gain) on derivative instruments and related transactions | 0.20 | (0.39) | (0.62) | ||||||||

| Tax effect | (0.05) | 0.09 | 0.15 | ||||||||

Effects of economic hedging related to natural gas inventory (1) | (0.18) | 0.36 | 0.21 | ||||||||

| Tax effect | 0.04 | (0.09) | (0.05) | ||||||||

| Gain on equity method investment | — | — | (0.06) | ||||||||

| Tax effect | — | — | 0.01 | ||||||||

| Basic NFE per share | $ | 2.95 | $ | 2.70 | $ | 2.50 | |||||

(1)Effects of hedging natural gas inventory transactions where the economic impact is realized in a future period.

NFE by reporting segment and other business operations for the fiscal years ended September 30, are as follows:

* HSO includes intercompany eliminations.

Page 6

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

Natural Gas Distribution

General

NJNG consists of regulated utility operations that provide natural gas service to residential and commercial customers. NJNG’s service territory includes Burlington, Middlesex, Monmouth, Morris, Ocean and Sussex counties in New Jersey. It encompasses 1,538 square miles, covering 109 municipalities with an estimated population of 1.7M people. It is primarily suburban, highlighted by approximately 100 miles of New Jersey coastline. It is in close proximity to New York City, Philadelphia and the metropolitan areas of northern New Jersey, and is accessible through a network of major roadways and mass transportation.

NJNG’s business is subject to various risks, such as those associated with adverse economic conditions, which can negatively impact customer growth and operating and financing costs; fluctuations in commodity prices, which can impact customer usage; certain regulatory actions; and environmental remediation. It is often difficult to predict the impact of trends associated with these risks. NJNG employs strategies to pursue customer conversions from other fuel sources and monitor new construction markets through contact with developers, utilize incentive programs through BPU-approved mechanisms to reduce natural gas costs, pursue rate and other regulatory strategies designed to stabilize and decouple gross margin, and work actively with consultants and the NJDEP to manage expectations related to its obligations associated with its former MGP sites.

Operating Revenues/Throughput

For the fiscal years ended September 30, operating revenues and throughput by customer class for NJNG are as follows:

| 2024 | 2023 | 2022 | ||||||||||||||||||||||||

| ($ in thousands) | Operating Revenue | Bcf | Operating Revenue | Bcf | Operating Revenue | Bcf | ||||||||||||||||||||

| Residential | $ | 642,352 | 44.5 | $ | 643,756 | 43.4 | $ | 598,433 | 45.5 | |||||||||||||||||

| Commercial and other | 124,127 | 8.5 | 137,343 | 8.4 | 140,727 | 8.7 | ||||||||||||||||||||

| Firm transportation | 86,138 | 11.7 | 79,537 | 12.1 | 80,915 | 13.0 | ||||||||||||||||||||

| Total residential and commercial | 852,617 | 64.7 | 860,636 | 63.9 | 820,075 | 67.2 | ||||||||||||||||||||

| Interruptible/off-tariff agreements/other | 9,950 | 25.8 | 9,996 | 29.5 | 9,740 | 32.4 | ||||||||||||||||||||

| Total system | 862,567 | 90.5 | 870,632 | 93.4 | 829,815 | 99.6 | ||||||||||||||||||||

BGSS incentive programs (1) | 157,265 | 67.7 | 142,001 | 34.9 | 298,952 | 44.5 | ||||||||||||||||||||

| Total | $ | 1,019,832 | 158.2 | $ | 1,012,633 | 128.3 | $ | 1,128,767 | 144.1 | |||||||||||||||||

(1)Does not include 17.3, 37.7 and 50.7 Bcf for the capacity release program and related amounts of approximately $0.8M, $0.9M and $0.7M, which are recorded as a reduction of natural gas purchases on the Consolidated Statements of Operations during fiscal 2024, 2023 and 2022, respectively.

In fiscal 2024, no single customer represented more than 10% of consolidated operating revenues.

Seasonality of Natural Gas Revenues

Therm sales are significantly affected by weather conditions, with customer demand being greatest during the winter months when natural gas is used for heating purposes. The relative measurement of the impact of weather is in Degree-days. Degree-day data is used to estimate amounts of energy required to maintain comfortable indoor temperature levels based on each day’s average temperature. Each degree of temperature below 65 degrees Fahrenheit is counted as one heating Degree-day. Normal heating Degree-days are based on a 20-year average, calculated based on three reference areas representative of NJNG’s service territory.

CIP, a mechanism authorized by the BPU, stabilizes NJNG’s Utility Gross Margin, regardless of variations in weather. In addition, CIP decouples the link between Utility Gross Margin and customer usage, allowing NJNG to promote energy conservation measures. Recovery of Utility Gross Margin is subject to additional conditions, including an earnings test, a revenue test and an evaluation of BGSS-related savings achieved over a 12-month period. The BPU approved the continuation of the CIP program with no expiration date.

Concurrent with its annual BGSS filing, NJNG files for an annual review of its CIP, at which time it can request rate changes, as appropriate. For additional information regarding CIP, including rate actions and impact to margin, see Note 4. Regulation in the accompanying Consolidated Financial Statements and Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations-Natural Gas Distribution.

Page 7

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

Natural Gas Supply

Firm Natural Gas Supplies

In fiscal 2024, NJNG purchased natural gas from approximately 56 suppliers under contracts ranging from one day to five months and purchased over 10% of its natural gas from two suppliers. NJNG believes the loss of either of these suppliers would not have a material adverse impact on its results of operations, financial position or cash flows, as an adequate number of alternative suppliers exist. NJNG believes that its supply strategy should adequately meet its expected firm load for the upcoming winter season.

Firm Transportation and Storage Capacity

NJNG maintains agreements for firm transportation and storage capacity with several interstate pipeline companies to take delivery of firm natural gas supplies, which ensures the ability to reliably service its customers. NJNG receives natural gas at 11 citygate stations located in Burlington, Middlesex, Morris and Passaic counties in New Jersey.

The pipeline companies that provide firm transportation service to NJNG’s citygate stations, the maximum daily deliverability of that capacity and the contract expiration dates are as follows:

| Pipeline | Dths (1) | Expiration | |||||||||

| Texas Eastern Transmission, LP | 390,738 | 2025 to 2026 | |||||||||

| Algonquin Gas Transmission, LLC | 12,000 | 2026 | |||||||||

| Columbia Gas Transmission, LLC | 50,000 | 2027 to 2030 | |||||||||

| Tennessee Gas Pipeline Company, LLC | 35,894 | 2028 to 2029 | |||||||||

| Transcontinental Gas Pipe Line Company, LLC | 425,531 | 2025 to 2039 | |||||||||

| Total | 914,163 | ||||||||||

(1) Numbers are shown net of any capacity release contracted amounts.

Eastern Gas Transmission and Storage, Inc., Tennessee Gas Pipeline Company, LLC, Transcontinental Gas Pipe Line Company, LLC and Adelphia provide NJNG upstream firm contract transportation service and supply pipelines included in the table above.

In addition, NJNG has storage contracts that provide an additional 102,941 Dths of maximum daily deliverability to NJNG’s citygate stations from storage fields in its Northeast market area. The storage suppliers, the maximum daily deliverability of that storage capacity and the contract expiration dates are as follows:

| Pipeline | Dths | Expiration | |||||||||

| Texas Eastern Transmission, LP | 94,557 | 2026 | |||||||||

| Transcontinental Gas Pipe Line Company, LLC | 8,384 | 2028 | |||||||||

| Total | 102,941 | ||||||||||

NJNG also has upstream storage contracts. The maximum daily deliverability and contract expiration dates are as follows:

| Company | Dths | Expiration | |||||||||

| Eastern Gas Transmission and Storage, Inc. | 286,829 | various dates from 2025 to 2027 | |||||||||

| Steckman Ridge | 38,000 | 2025 | |||||||||

| Stagecoach Pipeline and Storage Company, LLC | 47,065 | 2028 | |||||||||

| Total | 371,894 | ||||||||||

NJNG utilizes its transportation contracts to transport natural gas to NJNG’s citygates from the Eastern Gas Transmission and Storage, Inc., Steckman Ridge and Stagecoach Pipeline & Storage Company LLC storage fields. NJNG has sufficient firm transportation, storage and supply capacity to fully meet its customer demand for natural gas within its service territory.

Citygate Supplies from ES

NJNG and ES had one AMA where NJNG released certain transportation and storage capacity to ES, which NJNG could have called upon if needed. This agreement expired on March 31, 2024 and was not renewed.

Page 8

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

Peaking Supply

To manage its winter peak day demand, NJNG maintains two LNG facilities with a combined deliverability of approximately 170,000 Dths/day, which represents approximately 17% of its estimated peak day sendout. NJNG’s liquefaction facility allows NJNG to convert natural gas into LNG to fill NJNG’s existing LNG storage tanks. See Item 2. Properties-Natural Gas Distribution for additional information regarding the LNG storage facilities.

Basic Gas Supply Service

BGSS is a BPU-approved clause designed to allow for the recovery of natural gas commodity costs on an annual basis. The clause requires all New Jersey natural gas utilities to make an annual filing by each June 1 for review of BGSS rates and to request a potential rate change effective the following October 1. The BGSS also allows each natural gas utility to provisionally increase residential and small commercial customer BGSS rates on December 1 and February 1 for up to a 5% increase to the average residential heat customer’s bill on a self-implementing basis with proper notice. Such increases are subject to subsequent BPU review and final approval.

In addition to making periodic rate adjustments to reflect changes in commodity prices, NJNG is also permitted to refund or credit back a portion of the commodity costs to customers when the natural gas commodity costs decrease in comparison to amounts projected or to amounts previously collected from customers. Decreases in the BGSS rate and BGSS refunds can be implemented with five days’ notice to the BPU. Rate changes, as well as other regulatory actions related to BGSS, are discussed further in Note 4. Regulation in the accompanying Consolidated Financial Statements.

Wholesale natural gas prices are, by their nature, volatile. NJNG mitigates the impact of volatile price changes on customers through the use of financial derivative instruments, which are part of its storage incentive program and its BGSS clause.

Future Natural Gas Supplies

NJNG expects to meet the natural gas requirements for existing and projected firm customers. If NJNG’s long-term natural gas requirements change, NJNG expects to renegotiate and restructure its contract portfolio to better match the changing needs of its customers and changing natural gas supply landscape.

Regulation and Rates

State

NJNG is subject to the jurisdiction of the BPU with respect to a wide range of matters such as base rates and regulatory rider rates, the issuance of securities, the safety and adequacy of service, the manner of keeping its accounts and records, the sufficiency of natural gas supply, pipeline safety, environmental issues, compliance with affiliate standards and the sale or encumbrance of its properties. See Note 4. Regulation in the accompanying Consolidated Financial Statements for additional information regarding NJNG’s rate proceedings.

Federal

FERC regulates rates charged by interstate pipeline companies for the transportation and storage of natural gas. This may affect NJNG’s agreements with several interstate pipeline companies for the purchase of such services. Costs associated with these services are currently recoverable through the BGSS.

Competition

Although its franchises are nonexclusive, NJNG is not currently subject to competition from other natural gas distribution utilities with regard to the transportation of natural gas in its service territory. Due to significant distances between NJNG’s current large industrial customers and the nearest interstate natural gas pipelines, as well as the availability of its transportation tariff, NJNG currently does not believe it has significant exposure to the risk that its distribution system will be bypassed. Competition does exist from suppliers of oil, electricity and propane. Natural gas prices are a function of market supply and demand. Although NJNG believes natural gas will remain competitive with alternative fuels, no assurance can be given in this regard.

The BPU, within the framework of the EDECA, fully opened NJNG’s residential markets to competition, including third-party suppliers, and restructured rates to segregate its BGSS and delivery (i.e., transportation) prices. New Jersey’s natural gas utilities must provide BGSS in the absence of a third-party supplier. On September 30, 2024, NJNG had 14,470 residential and 7,972 commercial and industrial customers utilizing the transportation service.

Page 9

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

Clean Energy Ventures

CEV owns and operates clean energy projects, including commercial and residential solar installations located in six states, including New Jersey, Rhode Island, New York, Connecticut, Michigan and Indiana.

As of September 30, 2024, CEV has approximately 477 MW of solar capacity in service, including a combination of commercial and residential net-metered and commercial grid-connected commercial solar systems.

As part of its solar investment portfolio, CEV operates a residential and small commercial solar program, The Sunlight Advantage®, which provides qualifying homeowners and small business owners with the opportunity to have a solar system installed at their home or place of business with no installation or maintenance expenses. CEV owns, operates and maintains the system over the life of the lease in exchange for monthly lease payments. The program is operated by CEV using qualified contracting partners in addition to strategic suppliers for material standardization and sourcing.

On November 25, 2024, CEV completed the sale of its 91 MW residential solar asset portfolio. See Note 17. Subsequent Events for more information regarding the transaction.

CEV’s commercial solar projects are sourced through various channels and include both net-metered and grid-connected systems. Net-metered projects involve the sale of energy to a host and grid-connected systems into the wholesale energy markets. Project construction is competitively sourced through third parties. New Jersey has the tenth largest solar market in the U.S., according to the Solar Energy Industries Association®, with a large number of firms competing in all facets of the market including development, financing and construction.

Our solar systems located in New Jersey are registered and certified with the BPU’s Office of Clean Energy and qualified to produce RECs. One REC is created for every MWh of electricity produced by a solar generator. CEV sells SRECs generated to a variety of counterparties, including electric load-serving entities that serve electric customers in New Jersey and are required to comply with the solar carve-out of the Renewable Portfolio Standard, a regulation that requires the increased production of energy from renewable energy sources. Solar projects are also currently eligible for federal ITCs in the year that they are placed into service. In December 2019, the BPU established the TREC as the interim program successor to the SREC program. TRECs provide a fixed compensation base multiplied by an assigned project factor in order to determine their value. The project factor is determined by the type and location of the project, as defined. All TRECs generated are required to be purchased monthly by a TREC program administrator as appointed by the BPU.

In July 2021, the BPU approved the first portion of the solar successor program for net-metered projects under 5 MWs. The new program opened to new applications in August 2021. Incentives are structured as a 15-year fixed incentive ranging from $85 to $130/MWh depending on market segment, project siting and size. The second phase of the successor program, the CSI program, was established in December 2022. The CSI program was designed to encourage grid scale solar generation with a goal of incentivizing development of at least 300 MW of solar annually until 2026. Solicitations take place annually, and all projects that meet pre-qualification requirements will compete on price only. Dates for the next solicitation have yet to be announced.

CEV is subject to various risks including those associated with adverse federal and state legislation and regulatory policies, electric grid connection, supply chain and/or construction delays that can impact the timing or eligibility of tax incentives, technological changes and the future market of RECs. See Item 1A. Risk Factors for additional information regarding these risks.

Energy Services

ES consists of unregulated wholesale and retail natural gas operations and provides producer and asset management services to a diverse customer base across North America. ES has acquired contractual rights to natural gas transportation and storage assets it utilizes to implement its strategic and opportunistic market strategies. The rights to these assets were acquired in anticipation of delivering natural gas, performing asset management services for customers or identifying strategic opportunities that exist in or between the market areas that it serves. These opportunities are driven by price differentials between market locations and/or time periods. ES differentiates itself in the marketplace based on price, reliability and quality of service. Its competitors include wholesale marketing and trading companies, utilities, natural gas producers and financial institutions. ES’s portfolio of customers includes regulated natural gas distribution companies, industrial companies, electric generators, natural gas/liquids processors, retail aggregators, wholesale marketers and natural gas producers.

Page 10

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

While focusing on maintaining a low-risk operating and counterparty credit profile, ES’s activities specifically consist of the following elements:

•Providing natural gas portfolio management services to nonaffiliated and our affiliated natural gas utility, electric generation facilities and natural gas producers;

•Managing strategies for new and existing natural gas transportation and storage assets to capture value from changes in price due to location or timing differences;

•Managing transactional logistics to minimize the cost of natural gas delivery to customers while maintaining security of supply. Transactions utilize the most optimal and advantageous natural gas supply transportation routing available within its contractual asset portfolio and various market areas; and

•Managing economic hedging programs that are designed to mitigate the impact of changes in market prices on Financial Margin generated on its natural gas transportation and storage commitments.

In an effort to deliver more predictable earnings contributions, reduce earnings volatility and monetize the value of its natural gas transportation portfolio, ES entered into a series of AMAs in December 2020 with an investment grade public utility to release pipeline capacity associated with certain natural gas transportation contracts. The AMAs include a series of initial and permanent releases, which commenced in November 2021. NJR received a total of approximately $260M in cash from fiscal 2022 through fiscal 2024 and will receive approximately $34M per year from fiscal 2025 through fiscal 2031 under the agreements.

During fiscal 2024, ES purchased more than 10% of its natural gas from one supplier. ES believes the loss of this supplier would not have a material adverse impact on its results of operations, financial position or cash flows, as an adequate number of alternative suppliers exist.

Transportation and Natural Gas Storage Transactions

ES focuses on creating value from the use of its physical assets, which are typically amassed through contractual rights to natural gas transportation and storage capacity. These assets become more valuable when favorable price changes occur that impact the value between or within market areas and across time periods. On a forward basis, ES may hedge these price differentials through the use of financial instruments. In addition, ES may seek to optimize these assets on a daily basis, as market conditions warrant, by evaluating natural gas supply and transportation availability within its portfolio. This enables ES to capture geographic pricing differences across various regions, as delivered natural gas prices may change favorably as a result of market conditions. ES may, for example, initiate positions when intrinsic Financial Margin is present, and then enhance that Financial Margin as prices change across regions or time periods.

ES also engages in park and loan transactions with storage and pipeline operators, where ES will either borrow (receive a loan of) natural gas with an obligation to repay the storage or pipeline operator at a later date or “park” natural gas with an obligation to withdraw at a later date. In these cases, ES evaluates the economics of the transaction to determine if it can capture pricing differentials in the marketplace and generate Financial Margin. ES evaluates deal attributes such as fixed fees and calendar-spread value from deal inception until volumes are scheduled to be returned and/or repaid, as well as the time value of money. If this evaluation demonstrates that Financial Margin exists, ES may enter into the transaction and hedge with natural gas futures contracts, thereby locking in Financial Margin.

ES maintains inventory balances to satisfy existing or anticipated sales of natural gas to its counterparties and/or to create additional value, as described above. During fiscal 2024 and 2023, ES managed and sold 125.3 Bcf and 150.4 Bcf of natural gas, respectively. In addition, as of September 30, 2024 and 2023, ES had 13.1 Bcf of natural gas in storage and 14.6 Bcf of natural gas in storage, respectively.

Weather/Seasonality

ES activities are typically seasonal in nature as a result of changes in the supply and demand for natural gas. Demand for natural gas is generally higher during the winter months when there may also be supply constraints; however, during periods of milder temperatures, demand can decrease. In addition, demand for natural gas can also be high during periods of extreme heat in the summer months, resulting from the need for additional natural gas supply for natural gas-fired electric generation facilities. Accordingly, ES can be subject to variations in earnings and working capital throughout the year as a result of changes in weather.

Page 11

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

Volatility

ES’s activities are also subject to price volatility or supply/demand dynamics within its North American wholesale markets, including in the Northeastern, Appalachian, Mid-Continent and Southeast regions. Changes in natural gas supply can affect capacity values and ES’s Financial Margin, which, as described below, is generated from the optimization of transportation and storage assets. With its focus on risk management, ES continues to diversify its revenue stream by identifying new growth opportunities in producer and asset management services. ES monitors changing market dynamics and strategically adjusts its portfolio of transportation and storage assets, which currently includes an average of approximately 16.5 Bcf of firm storage and 0.6 Bcf of firm transportation capacity.

Financial Margin

To economically hedge the commodity price risk associated with its existing and anticipated commitments for the purchase and sale of natural gas, ES enters into a variety of derivative instruments including, but not limited to, futures contracts, physical forward contracts, financial swaps and options. These derivative instruments are accounted for at fair value with changes in fair value recognized in earnings as they occur. ES views Financial Margin, a non-GAAP financial measure, as a key internal financial metric. For additional information regarding Financial Margin, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations-Energy Services.

Risk Management

In conducting its business, ES mitigates risk by following formal risk management guidelines, including transaction limits, segregation of duties and formal contract and credit review approval processes. ES continuously monitors and seeks to reduce the risk associated with its counterparty credit exposures. Our Risk Management Committee oversees compliance with these established guidelines.

Storage and Transportation

S&T includes investments in FERC-regulated interstate natural gas storage and transportation assets and comprises NJR Midstream Company, which owns and operates Leaf River, FERC-regulated Adelphia, and NJR Steckman Ridge Storage Company, which holds our 50% equity method investment in Steckman Ridge.

Leaf River

Leaf River is a salt dome cavern natural gas storage facility located in southeastern Mississippi. The facility consists of three salt caverns with a combined natural gas storage capacity of 32.2M Dth. A 40-mile, dual 24 inch pipeline header system provides interconnections with seven different pipelines: Tennessee Gas Pipeline, Destin Pipeline, Transcontinental Pipeline, Southern Natural Gas Pipeline, Midcontinent Express Pipeline, Gulf South Pipeline, and Venture Oil & Gas Pipeline, and serves as a bridge between the Northeast, Mid-Atlantic and Southeast markets. Leaf River provides reliable storage and balancing services to utilities, pipelines, marketers, and power markets in the Gulf and Southeast region.

Adelphia

Adelphia operates a FERC-regulated interstate natural gas transmission pipeline system in eastern Pennsylvania, providing firm and interruptible natural gas transportation service. The Adelphia pipeline system extends from Lower Mount Bethel Township in North Hampton County to Marcus Hook in Delaware County. Adelphia provides up to 850,000 Dths of natural gas to constrained energy markets in the greater Philadelphia region and serves customers from local distributors and producers to electric generators and wholesale marketers through its pipeline and storage assets.

Steckman Ridge

Steckman Ridge is a Delaware limited partnership, jointly owned and controlled by our subsidiaries and subsidiaries of Enbridge Inc., which built, owns and operates a natural gas storage facility with up to 12 Bcf of working natural gas capacity in Bedford County, Pennsylvania. The facility has direct access to the TETCO and Eastern Gas Transmission and Storage, Inc. pipelines and has access to the Northeast and Mid-Atlantic markets.

Page 12

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

OTHER BUSINESS OPERATIONS

Home Services and Other

HSO operations consist primarily of the following unregulated affiliates:

•NJR Home Services, Inc., which provides heating, ventilation and cooling service, electrical and generator service and installations, sales and installation of appliances, as well as installation of solar equipment;

•NJR Plumbing Services, Inc., which provides plumbing repair and installation services;

•New Jersey Resources Corporation, a diversified energy services holding company;

•CR&R, which holds commercial real estate; and

•NJR Service Corporation, which provides shared administrative and financial services to the Company and all of its subsidiaries and affiliates.

ENVIRONMENT

We, along with our subsidiaries, are subject to legislation and regulation by federal, state and local authorities with respect to environmental matters. We believe that we are, in all material respects, in compliance with all applicable environmental laws and regulations.

NJNG is responsible for the environmental remediation of identified former MGP sites, which contain contaminated residues from former gas manufacturing operations that ceased at these sites by the mid-1950s and, in some cases, had been discontinued many years earlier. NJNG periodically, and at least annually, performs an environmental review of the former MGP sites, including a review of potential estimated liabilities related to the investigation and remedial action on these sites. Based on this review, NJNG has estimated that the total future expenditures to remediate and monitor the former MGP sites for which it is responsible will range from approximately $130.9M to $194.6M.

NJNG’s estimate of these liabilities is based upon known and measurable facts, existing technology and enacted laws and regulations in place when the review was completed in fiscal 2024. Where it is probable that costs will be incurred, and the information is sufficient to establish a range of possible liability, NJNG accrues the most likely amount in the range. If no point within the range is more likely than the other, it is NJNG’s policy to accrue the lower end of the range. As of September 30, 2024, NJNG recorded an MGP remediation liability and a corresponding regulatory asset of $161.7M on the Consolidated Balance Sheets, based on the most likely amount; however, actual costs may differ from these estimates.

HUMAN CAPITAL RESOURCES

Employee Overview

NJR fundamentally believes that its employees make the Company a unique, successful organization – in commitment, ingenuity, hard work and innovation. NJR employees fulfill the responsibilities that enable the Company to deliver natural gas service to its customers; to be a leader in clean energy investments; to grow its storage and transportation energy business; and to earn the loyalty of its retail home services customers. NJR also is committed to provide every appropriate resource to ensure its employees’ safety. Through initiatives that start at the top, NJR has invested time, energy and manpower to foster a culture in which safety is top-of-mind at all times and achieving safety goals is a shared priority for every NJR employee.

As of September 30, 2024, the Company and our subsidiaries employed 1,372 employees compared with 1,350 employees as of September 30, 2023. Of the total number of employees, NJNG had 510 and 509 and NJRHS had 118 and 117 Union or Represented employees as of September 30, 2024 and 2023, respectively. NJNG and NJRHS have collective bargaining agreements with the Union, which is affiliated with the American Federation of Labor and Congress of Industrial Organizations. NJNG and the Union agreed and ratified a contract on December 7, 2023, expiring in December 2026. The collective bargaining agreement between NJRHS and the Union was agreed and ratified on September 27, 2024, expiring in April 2029. The labor agreements cover wage increases and other benefits, including the defined benefit pension (which was closed to all employees hired on or after January 1, 2012, with the exception of certain rehires who are eligible to resume active participation), the postemployment benefit plan (which was closed to all employees hired on or after January 1, 2012) and the enhanced 401(k) retirement savings plan. We consider our relationship with employees, including those covered by collective bargaining agreements, to be in good standing.

Page 13

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

The Company depends on its key personnel to successfully operate its businesses, including its executive officers, senior corporate management and management at its operating units. NJR seeks to attract and retain its employees by offering competitive compensation packages including base and incentive compensation (and in certain instances share-based compensation and retention incentives), attractive benefits and opportunities for advancement and rewarding careers. NJR periodically reviews and adjusts, if needed, its employees’ total compensation (including salaries, annual cash incentive compensation, other cash and equity incentives and benefits) to ensure that it is competitive within the industry and is consistent with our level of performance. NJR has also implemented enterprise-wide talent development and succession planning programs designed to identify future talent for key positions. To promote a collaborative and rewarding work environment and support the communities we serve, NJR sponsors numerous charitable, philanthropic and social awareness programs.

Further, in order to take advantage of available opportunities and successfully implement our long-term strategy, NJR must be able to employ, train and retain the necessary skilled employees. As a result, NJR supports and utilizes various training and educational programs and has developed additional company-wide and project-specific employee training and educational programs. NJR continues key programs focused on employee safety, leadership development, work-life balance, talent management, health and wellness, DEI and employee engagement. Moreover, DEI and employee engagement are integral to NJR’s vision, strategy and business success. Fostering an environment that values DEI and ethics helps create an organization that is able to embrace, leverage and respect the differences of employees, customers and the communities where we live, work and serve. We are proud of the strides we have made in furthering our DEI strategy and increasing employee engagement. NJR is committed to this journey and knows our success makes us stronger as a company and community. Complementing our efforts are a DEI Council and our employee-led Business Resource Groups, cross-functional teams of employees whose core mission is to advance their own professional development and cultivate deeper connections with co-workers and communities.

NJR periodically evaluates employees and their productivity against future demand expectations and historical trends. NJR employees continue to maintain high levels of engagement, satisfaction and retention according to NJR’s most recent employee survey conducted in October 2023.

NJR Board of Directors’ Role in Human Capital Resource Management

NJR’s Board of Directors believes that human capital management is an important component of the Company’s continued growth and success, and is essential for our ability to attract, retain and develop talented and skilled employees. We pride ourselves on a culture that is innovative, talent- and team-focused and inclusive.

Management regularly reports to the LDCC of the Board of Directors on human capital management topics, including corporate culture, DEI, employee development, compensation and benefits. The LDCC maintains oversight of matters related to human capital management, including talent retention, development and succession planning, and the Board of Directors provides input on important decisions in each of these areas.

NJR conducts an annual employee survey, which is reviewed by the LDCC, designed to help the Company measure overall employee engagement. The feedback employees provide through the survey helps NJR evaluate the Company’s culture and the employee experience and monitor its current practices for potential areas of improvement.

Employee Benefits

The LDCC believes employee benefits are an essential component of the Company’s competitive total rewards package. These benefits are designed to attract and retain our employees and include medical, vision and dental insurance, short- and long-term disability insurance, accidental death and disability insurance, travel and accident insurance and our 401(k) Plan. As part of the 401(k) Plan, NJR has matched 85% of the first 6% of base compensation contributed by the employee into the 401(k) Plan, subject to the Internal Revenue Code and NJR’s 401(k) Plan limits. Beginning on March 6, 2024, NJR’s contribution changed to 100% of the first 3% and 80% of the next 3% of base compensation. Additionally, for employees who are not eligible to participate in the defined benefit plans, NJR annually contributes between 4% and 5% of base compensation, depending upon years of service, into the 401(k) Plan on their behalf.

AVAILABLE INFORMATION AND CORPORATE GOVERNANCE DOCUMENTS

The following reports and any amendments to those reports are available on our website at https://investor.njresources.com/financials/sec-filings as soon as reasonably possible after filing or furnishing them with the SEC:

•Annual reports on Form 10-K;

•Quarterly reports on Form 10-Q; and

•Current reports on Form 8-K.

Page 14

New Jersey Resources Corporation

Part I

ITEM 1. BUSINESS (Continued)

The following documents are available on our website at https://investor.njresources.com/governance/governance-documents:

•NJR Code of Conduct;

•Amended and Restated Bylaws;

•Corporate Governance Guidelines;

•Wholesale Trading Code of Conduct;

•Dodd-Frank Compensation Recoupment Policy;

•Supplemental Clawback Policy;

•Insider Trading Policy;

•Charters of the following Board of Directors Committees: Audit, Nominating/Corporate Governance and Leadership Development and Compensation;

•Audit Complaint Procedure;

•Communicating with Non-Management Directors Procedure;

•Statement of Policy with Respect to Related Person Transactions; and

•Legal Procedure.

In Part III of this Form 10-K, we incorporate certain information by reference from our Proxy Statement for our 2024 Annual Meeting of Shareowners. We expect to file the Proxy Statement with the SEC on or about December 11, 2024. We will make it available on our website as soon as reasonably possible following the filing date. Please refer to the Proxy Statement when it is available.

A printed copy of each document is available free of charge to any shareowner who requests it by contacting the Corporate Secretary at New Jersey Resources Corporation, 1415 Wyckoff Road, Wall, New Jersey 07719.

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The Company’s Executive Officers and their age, position and business experience during the past five years are below.

| Name | Age | Officer since | Business experience during last five years | ||||||||

| Stephen D. Westhoven | 56 | 2004 | President and CEO (October 2019 - present) President and Chief Operating Office (October 2018 - September 2019) | ||||||||

| Roberto Bel | 51 | 2019 | Senior Vice President and Chief Financial Officer (January 2022 - present) Vice President, Treasury and Investor Relations (April 2019 - December 2021) | ||||||||

| Patrick J. Migliaccio | 50 | 2013 | Senior Vice President and Chief Operating Officer (January 2022 - present) Senior Vice President and Chief Financial Officer (January 2016 - December 2021) | ||||||||

| Amy Cradic | 53 | 2018 | Senior Vice President and Chief Operating Officer of Nonutility Businesses, Strategy and External Affairs (March 2020 - present) Vice President, Corporate Strategy and External Affairs (January 2020 – February 2020) Vice President, Government Affairs and Policy (January 2018 – December 2019) | ||||||||

| Richard Reich | 49 | 2016 | Senior Vice President and General Counsel (June 2022 - present) Senior Vice President, General Counsel and Corporate Secretary (September 2021 - June 2022) Corporate Secretary and Assistant General Counsel (January 2016 - September 2021) | ||||||||

| Lori DelGiudice | 49 | 2023 | Senior Vice President, Human Resources (November 2022 - present) Vice President of Human Resources for Honeywell Advanced Materials (September 2017 - October 2022) | ||||||||

| Jacqueline K. Shea | 60 | 2016 | Senior Vice President and CIO (January 2023 - present) Vice President and CIO (June 2016 - December 2022) | ||||||||

| Stephen M. Skrocki | 48 | 2023 | Corporate Controller (Principal Accounting Officer) (January 2023 - present) Corporate Controller (January 2021 - December 2022) Assistant Corporate Controller (March 2017 - January 2021) | ||||||||

ITEM 1A. RISK FACTORS

When considering any investment in our securities, investors should consider the following risk factors, as well as the information contained under the caption “Information Concerning Forward-Looking Statements,” in analyzing our present and future business performance. While this list is not exhaustive, management also places no priority or likelihood based on their descriptions or order of presentation. Listed below, not necessarily in order of importance or probability of occurrence, are the most significant risk factors applicable to us. Unless indicated otherwise or the content requires otherwise, references below to “we,” “us,” and “our” should be read to refer to the Company and its subsidiaries and affiliates.

Page 15

New Jersey Resources Corporation

Part I

ITEM 1A. RISK FACTORS (Continued)

| Risks Related to Our Business Operations | ||

Our investments in solar energy projects are subject to substantial risks and uncertainties. There are risks associated with our ability to execute on our investment strategy of clean energy projects, which includes our ability to develop and manage such projects profitably. These include logistical risks and potential delays related to construction, permitting and regulatory approvals (including any approvals by the BPU required pursuant to solar energy legislation in the State of New Jersey, and similar approvals required by the other states where our solar projects are located); electric grid interconnection delays associated with the PJM Interconnection, LLC queue reform process; and the operational risk that the projects in service will not perform according to expectations due to equipment failure, suboptimal weather conditions or other economic factors beyond our control. All of the aforementioned risks could reduce the availability of viable solar energy projects for development. Furthermore, at the development or acquisition stage, our ability to predict actual performance results may be hindered or inaccurate and the projects may not perform as predicted. In addition, our investments in solar energy projects are dependent, in part, upon current state regulatory incentives and federal tax credits in order for the projects to be economically viable. Our return on investment for these solar projects is based substantially on our eligibility for ITCs and the future market value of RECs that are traded in a competitive marketplace in the State of New Jersey. These projects face the risk that the current state regulatory programs and tax laws may expire or be adversely modified. A sustained decrease in the value of RECs could negatively impact the return on our investments and could impair our portfolio of solar assets. | ||

Actions or limitations to address concerns over climate change, both globally and within our utilities' service areas, may affect our operations and financial performance. Legislative, regulatory and advocacy efforts at the local, state and national levels concerning climate change and other environmental issues could have significant impacts on our operations. The natural gas utility industry may be affected by proposals to curb greenhouse gas and other air emissions. Various regulatory and legislative proposals have been made to limit or further restrict byproducts of combustion, including byproducts resulting from the use of natural gas by our customers. In addition, regionally, a number of regulatory and legislative initiatives have been passed that are designed to limit greenhouse gas emissions and increase the use of renewable sources of energy, such as the ban of natural gas equipment in new construction in New York and elsewhere in the U.S. In addition, regulatory and legislative initiatives may restrict customers’ access to natural gas and/or require or limit natural gas infrastructure in buildings. Other initiatives may seek to promote social interests expressed as energy equity, environmental justice or similar frameworks. Any such legislation could direct and/or restrict the operation and raise the costs of our energy delivery infrastructure as well as the distribution of natural gas to our customers. | ||

Uncertainties associated with our pipeline of projects could adversely affect our business, results of operations, financial condition and cash flows. Business development projects involve many risks. We are currently engaged in business development projects, including projects in various stages of development tied to decarbonization efforts. Timely completion of our projects is subject to certain risks, including those related to regulatory proceedings regarding permitting and adverse outcomes from legal challenges related to the projects’ authorizations from federal and state regulatory agencies. We could also experience issues such as: technological challenges; ineffective scalability; failure to achieve expected outcomes; unsuccessful business models; startup and construction delays; construction cost overruns; disputes with contractors; the inability to negotiate acceptable agreements such as rights-of-way, easements, construction, gas supply or other material contracts; changes in customer demand, perception or commitment; public opposition to projects; marketing risk and changes in market regulation, behavior or prices; market volatility or unavailability, including markets for RNG and its associated attributes or other environmental attributes; the inability to receive expected tax or regulatory treatment; and operating cost increases. Additionally, we may be unable to finance our business development projects at acceptable costs or within a scheduled time frame necessary for completing the project. Any of the foregoing risks, if realized, could result in business development efforts failing to produce expected financial results and the project investment becoming impaired, and such failure or impairment could have an adverse effect on our business, results of operations, financial condition and cash flows. | ||

Page 16

New Jersey Resources Corporation

Part I

ITEM 1A. RISK FACTORS (Continued)

ES’s earnings and cash flows are dependent upon optimization of its contractual assets. ES’s earnings and cash flows are based, in part, on its ability to optimize its portfolio of contractually based natural gas storage and pipeline assets. The optimization strategy involves utilizing its physical assets to take advantage of differences in natural gas prices between geographic locations and/or time periods. Any change among various pricing points could affect these differentials. In addition, significant increases in the supply of natural gas in ES’s market areas, including as a result of increased production along the Marcellus Shale, can reduce ES’s ability to take advantage of pricing fluctuations in the future. Changes in pricing dynamics and supply could have an adverse impact on ES’s optimization activities, earnings and cash flows. ES incurs fixed demand fees to acquire its contractual rights to transportation and storage assets. Should commodity prices at various locations or time periods change in such a way that ES is not able to recoup these costs from its customers, the cash flows and earnings at ES, and ultimately the Company, could be adversely impacted. | ||

NJNG and ES rely on storage, transportation assets and suppliers, which they do not own or control, to deliver natural gas, which may affect their ability to deliver their products and services. NJNG and ES depend on natural gas pipelines and other transportation and storage facilities owned and operated by third parties to deliver natural gas to wholesale and retail markets and to provide retail energy services to customers. Their ability to provide natural gas for their present and projected sales will depend upon their suppliers’ ability to obtain and deliver additional supplies of natural gas, as well as NJNG’s ability to acquire supplies directly from new sources. Factors beyond the control of NJNG, its suppliers and the independent suppliers that have obligations to provide natural gas to certain NJNG customers may affect NJNG’s ability to deliver such supplies. These factors include other parties’ control over the drilling of new wells and the facilities to transport natural gas to NJNG’s citygate stations; development of additional interstate pipeline infrastructure; availability of supply sources; third-party pipelines or other midstream facilities interconnected to our gathering or transportation system, such as the TETCO or Transcontinental Pipeline, becoming partially or fully unavailable; competition for the acquisition of natural gas; priority allocations; impact of severe weather disruptions to natural gas supplies; and the regulatory and pricing policies of federal and state regulatory agencies. Energy deregulation legislation may increase competition among natural gas utilities and impact the quantities of natural gas requirements needed for sales service. ES also relies on a firm supply source to meet its energy management obligations to its customers. If supply, transportation or storage is disrupted, including for reasons of force majeure, the ability of NJNG and ES to sell and deliver their products and services may be hindered. As a result, they may be responsible for damages incurred by their customers, such as the additional cost of acquiring alternative supply at then-current market rates. Particularly for ES, these conditions could have a material impact on our financial condition, results of operations and cash flows. | ||

Failure to attract and retain an appropriately qualified employee workforce could adversely affect operations. Our ability to implement our business strategy and serve our customers is dependent upon our continuing ability to attract and retain talented professionals and a technically skilled workforce, and being able to transfer the knowledge and expertise of our workforce to new employees as our aging employees retire. Failure to hire and adequately train replacement employees, including the transfer of significant internal historical knowledge and expertise to the new employees, or the future availability and cost of contract labor could adversely affect the ability to manage and operate our business. Disputes with the Union over terms and conditions of the collective bargaining agreements could result in instability in our labor relationship and work stoppages that could impair the timely delivery of natural gas and other services from our utility and Home Services business, which could strain relationships with customers and state regulators and cause a loss of revenues that could adversely affect our results of operations. Our collective bargaining agreements may also increase the cost of employing NJNG and Home Services workforce, affect our ability to continue offering market-based salaries and employee benefits, limit our flexibility in dealing with our workforce and limit our ability to change work rules and practices and implement other efficiency-related improvements to successfully compete in today’s challenging marketplace. Our success depends upon our ability to attract, effectively transition, motivate and retain key employees and identify and develop talent to succeed senior management. We depend on senior executive officers and other key personnel to develop, implement and execute on our overall business strategy. The inability to recruit and retain or effectively transition key personnel or the unexpected loss of key personnel may adversely affect our operations. | ||

Page 17

New Jersey Resources Corporation

Part I

ITEM 1A. RISK FACTORS (Continued)