UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31, 2024

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission File Number:1-13107

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| , | ||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| | ||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| þ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

As of June 28, 2024, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the common stock of the registrant held by non-affiliates was approximately $4.1 billion based on the closing price of the common stock on the New York Stock Exchange on such date (for the purpose of this calculation, the registrant assumed that each of its directors, executive officers, and greater than 10% stockholders was an affiliate of the registrant as of June 28, 2024).

As of February 12, 2025, the registrant had 39,056,586 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement relating to its 2025 Annual Meeting of Stockholders to be filed with the SEC within 120 days after the end of the fiscal year ended December 31, 2024, are incorporated herein by reference in Part III.

AUTONATION, INC.

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2024

INDEX

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

PART I

ITEM 1. BUSINESS

General

AutoNation, Inc., through its subsidiaries, is one of the largest automotive retailers in the United States. As of December 31, 2024, we owned and operated 325 new vehicle franchises from 243 stores located in the United States, predominantly in major metropolitan markets in the Sunbelt region. Our stores, which we believe include some of the most recognizable and well-known in our key markets, sell 31 different new vehicle brands. The core brands of new vehicles that we sell, representing approximately 88% of the new vehicles that we sold in 2024, are manufactured by Toyota (including Lexus), Honda, Ford, General Motors, BMW, Mercedes-Benz, Stellantis, and Volkswagen (including Audi and Porsche). As of December 31, 2024, we also owned and operated 52 AutoNation-branded collision centers, 24 AutoNation USA used vehicle stores, 4 AutoNation-branded automotive auction operations, 3 parts distribution centers, a mobile automotive repair and maintenance business, and an auto finance company.

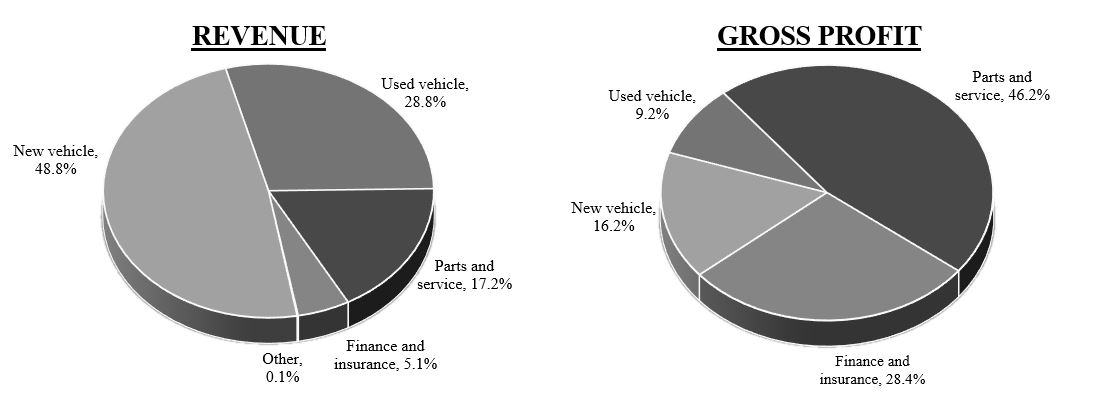

We offer a diversified range of automotive products and services, including new vehicles, used vehicles, “parts and service” (also referred to as “After-Sales”), which includes automotive repair and maintenance services as well as wholesale parts and collision businesses, and automotive “finance and insurance” products (also referred to as “Customer Financial Services”), which include vehicle service and other protection products, as well as the arranging of financing for vehicle purchases through third-party finance sources. We also offer indirect financing through our captive auto finance company on vehicles we sell. The following charts present the contribution to total revenue and gross profit by each of new vehicle, used vehicle, parts and service, and finance and insurance sales in 2024.

For convenience, the terms “AutoNation,” “Company,” “we,” “us,” and “our” are used to refer collectively to AutoNation, Inc. and its subsidiaries, unless otherwise required by the context. Our store and other operations are conducted by our subsidiaries.

Reportable Segments

As of December 31, 2024, we had four reportable segments: Domestic, Import, Premium Luxury, and AutoNation Finance. Our Domestic, Import, and Premium Luxury segments are comprised of retail automotive franchises that sell the following new vehicle brands:

| Domestic | Import | Premium Luxury | |||||||||||||||||||||

| Buick | Ford | Acura | Mazda | Aston Martin | Land Rover | ||||||||||||||||||

| Cadillac | GMC | Genesis | Nissan | Audi | Lexus | ||||||||||||||||||

| Chevrolet | Jeep | Honda | Subaru | Bentley | Mercedes-Benz | ||||||||||||||||||

| Chrysler | Lincoln | Hyundai | Toyota | BMW | MINI | ||||||||||||||||||

| Dodge | Ram | Infiniti | Volkswagen | Jaguar | Porsche | ||||||||||||||||||

| Volvo | |||||||||||||||||||||||

1

The following table sets forth information regarding our new vehicle revenues and retail new vehicle unit sales for the year ended, and the number of franchises owned as of, December 31, 2024:

| New Vehicle Revenues (in millions) | Retail New Vehicle Unit Sales | % of Total Retail New Vehicle Units Sold | Franchises Owned | |||||||||||||||||||||||

| Domestic: | ||||||||||||||||||||||||||

| Ford, Lincoln | $ | 1,453.8 | 28,154 | 11.1 | 30 | |||||||||||||||||||||

| Chevrolet, Buick, Cadillac, GMC | 1,305.5 | 27,504 | 10.8 | 39 | ||||||||||||||||||||||

| Chrysler, Dodge, Jeep, Ram | 767.8 | 13,610 | 5.3 | 76 | ||||||||||||||||||||||

| Domestic Total | 3,527.1 | 69,268 | 27.2 | 145 | ||||||||||||||||||||||

| Import: | ||||||||||||||||||||||||||

| Toyota | 2,030.4 | 52,427 | 20.6 | 19 | ||||||||||||||||||||||

| Honda | 1,153.0 | 33,048 | 13.0 | 24 | ||||||||||||||||||||||

| Nissan | 136.9 | 4,421 | 1.7 | 6 | ||||||||||||||||||||||

| Hyundai | 343.2 | 9,227 | 3.6 | 11 | ||||||||||||||||||||||

| Subaru | 333.6 | 9,763 | 3.8 | 8 | ||||||||||||||||||||||

| Other Import | 322.9 | 7,356 | 2.9 | 18 | ||||||||||||||||||||||

| Import Total | 4,320.0 | 116,242 | 45.6 | 86 | ||||||||||||||||||||||

| Premium Luxury: | ||||||||||||||||||||||||||

| Mercedes-Benz | 1,798.2 | 23,130 | 9.1 | 38 | ||||||||||||||||||||||

| BMW | 1,651.9 | 22,939 | 9.0 | 16 | ||||||||||||||||||||||

| Lexus | 480.0 | 8,830 | 3.5 | 3 | ||||||||||||||||||||||

| Audi | 327.1 | 5,191 | 2.0 | 9 | ||||||||||||||||||||||

| Jaguar Land Rover | 512.1 | 5,176 | 2.0 | 14 | ||||||||||||||||||||||

| Other Premium Luxury | 431.8 | 3,939 | 1.6 | 14 | ||||||||||||||||||||||

| Premium Luxury Total | 5,201.1 | 69,205 | 27.2 | 94 | ||||||||||||||||||||||

| $ | 13,048.2 | 254,715 | 100.0 | 325 | ||||||||||||||||||||||

The franchises in each of our Domestic, Import, and Premium Luxury segments also sell used vehicles, parts and automotive repair and maintenance services, and automotive finance and insurance products.

Our AutoNation Finance segment is comprised of our captive auto finance company, which provides indirect financing to qualified retail customers on vehicles we sell.

Except to the extent that differences among reportable segments are material to an understanding of our business taken as a whole, the description of our business in this report is presented on a consolidated basis. For additional financial information regarding our four reportable segments, refer to Note 22 of the Notes to Consolidated Financial Statements set forth in Part II, Item 8 of this Form 10-K.

Business Strategy

We seek to create long-term value for our stockholders and to be the best-run, most profitable automotive retailer and provider of personalized transportation services in the United States. We believe that the significant scale of our operations, our digital customer experience, and the quality of our managerial talent allow us to achieve efficiencies in our key markets. To achieve and sustain operational excellence, we are pursuing the following strategies:

•We strive to be the nation’s most comprehensive provider of transportation solutions to meet the mobility needs of our current and future customers through a comprehensive, unique suite of transportation solutions.

We seek to maximize the performance and utilization of our assets through operational excellence and expand through the development and/or acquisition of key capabilities, products, and resources. We achieve this by both

2

optimizing our existing business and capturing new and developing opportunities. We continue to invest in strategic partnerships and broaden our offerings to evolve with the changing automotive retail industry and to widen our access to new and expanding sales channels for vehicles, parts and service, financing, and personal transportation services.

AutoNation Finance, our captive auto finance company, provides financing to qualified retail customers on certain new and used vehicles we sell. Through AutoNation Finance, we have further extended our relationship with our customers beyond the car-buying experience and participate in the customer’s entire vehicle ownership cycle. As a result, we are able to diversify our sources of income, generate additional profits, cash flows, and sales, and increase customer retention.

We also pursue opportunities to penetrate the extensive After-Sales service market and respond to our customers’ needs by broadening the reach of our existing After-Sales network. AutoNation Mobile Service, our mobile solution for automotive repair and maintenance services, offers customers the convenience of services and repairs at their home, workplace, or on-site for fleet vehicles. AutoNationParts.com, our e-commerce website, enables customers to purchase high-quality automotive parts and accessories at competitive prices, shipped directly to their homes.

Additionally, we have minority ownership stakes in and productive collaborations with Waymo, the self-driving technology company of Alphabet Inc., and TrueCar, Inc., a leading automotive digital marketplace that lets auto buyers and sellers connect to its nationwide network of certified dealers. These investments and collaborations reflect our continued commitment to emerging technologies that impact the automotive industry.

We also continue to actively pursue acquisitions and new store opportunities, as well as other strategic initiatives, that meet our strategic and financial objectives. We expect that these offerings, initiatives, partnerships, and acquisitions will continue to expand and strengthen the AutoNation retail brand, improve the customer experience, provide new growth opportunities, and enable us to expand our footprint in our core and other markets.

•Hire, train, and retain the best talent available to build dynamic teams to serve our customers.

At AutoNation, nothing drives our success more than how we hire, train, and retain great people. We value the dignity of all employees and are committed to maintaining a work environment where all associates are valued and treated with respect. Our associates are at the core of our performance, by driving innovation and meeting the needs of our more than 11 million customers while protecting and enhancing AutoNation’s brand and reputation. See “Human Capital Resources” below for more information about how we invest in our associates to help us prepare leaders with the vision, integrity, and expertise that enhance our operational excellence every day, drive store profitability, and create both positive employee and customer experiences.

•Continue to provide an industry-leading automotive retail customer experience in our stores and through our digital channels.

We seek to deliver a consistently superior customer experience by offering a broad selection of inventory, customer-friendly, transparent sales and service processes, vehicle financing, and competitive pricing. We believe that this will benefit us by increasing customer loyalty and will encourage our customers to bring their vehicles to our stores for all of their vehicle service, maintenance, and collision repair needs and also by driving repeat and referral vehicle sales business.

We continue to focus on providing a seamless, end-to-end customer experience in our stores and through our digital channels, and improving our ability to generate business through those channels. We offer an integrated retailing solution that provides customers with a seamless and intuitive omnichannel vehicle shopping and purchase experience. We continue to build omnichannel digital capabilities that provide a personalized digital customer experience online and in-store. Our customers are able to complete key automotive retail- and service-related transactions online through our digital channels such as selecting a vehicle with a guaranteed price, scheduling a test drive, calculating payment options, receiving a certified trade-in or purchase offer for a vehicle that a customer wants to sell, applying for financing, selecting vehicle protection products, scheduling in-store pick-up or home delivery, arranging service appointments, receiving service updates, paying for maintenance and

3

repair services, and signing paperwork electronically. We also utilize proprietary tools that leverage real-time customer data to guide and personalize the customer experience.

•Continue to invest in the AutoNation retail brand to enhance our strong customer satisfaction and expand our market share.

AutoNation is a brand that connects people and places. We continue to invest in the AutoNation retail brand, promoting personal transportation for America’s drivers, leading the charge to make transformational change in the automotive industry, and driving out cancer coast to coast. We are committed to delivering easy, transparent, and customer-centric services for our customers’ personal transportation needs.

The AutoNation retail brand includes our AutoNation USA used vehicle stores, as well as AutoNation Finance, our captive auto finance company. We expect to continue to expand the AutoNation Finance loan portfolio as we increase finance penetration rates at our stores. In addition, we offer AutoNation-branded Customer Financial Services products (including extended service and maintenance contracts and other vehicle protection products) and parts and accessories, as well as collision repair services at AutoNation-branded collision centers, mobile automotive repair and maintenance services through AutoNation Mobile Services, and auction services at AutoNation-branded automotive auctions. We also offer our One Price used vehicle centralized pricing and appraisal strategy, and our “We’ll Buy Your Car” program under which customers receive a guaranteed trade-in offer honored for 7 days or 500 miles at any of our locations.

•Leverage our significant scale and cost structure to improve our operating efficiency.

As one of the largest automotive retailers in the United States, we are uniquely positioned to leverage our significant scale so that we are able to achieve competitive operating margins by centralizing and streamlining various business processes. We strive to manage our new and used vehicle inventories so that our stores’ supply and mix of vehicles are in line with seasonal sales trends and also minimize our carrying costs. We are able to self-source a significant portion of our used vehicle inventory through our “We’ll Buy Your Car” program, and quickly make available such used vehicles through optimization of our reconditioning capabilities at our parts and service departments. Additionally, we are able to improve financial controls and lower servicing costs by maintaining many key store-level accounting and administrative activities in our shared service center located in Irving, Texas. We also leverage our digital capabilities to drive cost reductions and increased efficiency for the long-term success of our business. Finally, we leverage our scale to reduce costs related to purchasing certain equipment, supplies, and services through national vendor relationships.

Our business benefits from a well-diversified portfolio of automotive retail franchises. In 2024, approximately 38% of total revenue was generated by Premium Luxury franchises, approximately 30% by Import franchises, and approximately 27% by Domestic franchises. We believe that our business also benefits from diverse revenue streams generated by our new and used vehicle sales, parts and service business, and finance and insurance sales. Our higher-margin parts and service business has historically been less sensitive to macroeconomic conditions as compared to new and used vehicle sales. In addition, we have been able to attain industry-leading finance and insurance gross profit per vehicle retailed as we have maintained a strong product penetration of products sold per vehicle.

Our capital allocation strategy is focused on growing long-term value per share. We invest capital in our business to maintain and upgrade our existing facilities and to build new facilities for existing franchises and new AutoNation USA used vehicle stores, as well as for other strategic and technology initiatives. We also deploy capital opportunistically to complete acquisitions or investments, build facilities for newly awarded franchises, and/or repurchase our common stock and/or debt. Our capital allocation decisions are based on factors such as the expected rate of return on our investment, the market price of our common stock versus our view of its intrinsic value, the market price of our debt, the potential impact on our capital structure, our ability to complete acquisitions that meet our strategic objectives, market and vehicle brand criteria, and/or return on investment threshold, and limitations set forth in our debt agreements. For additional information regarding our capital allocation, refer to “Liquidity and Capital Resources – Capital Allocation” in Part II, Item 7 of this Form 10-K.

4

Operations

Each of our franchised dealerships acquires new vehicles for retail sale either directly from the applicable automotive manufacturer or distributor or through dealer trades with other stores of the same brand franchise. We generally acquire used vehicles from customers, primarily through trade-ins and our “We’ll Buy Your Car” program, as well as through auctions, lease terminations, and other sources, and we generally recondition used vehicles acquired for retail sale in our parts and service departments. Used vehicles that we do not sell at our stores generally are sold at wholesale prices through auctions. See also “Inventory Management” in Part II, Item 7 of this Form 10-K.

Our stores provide a wide range of vehicle maintenance, repair, and collision repair services, including manufacturer recall repairs and other warranty work that can be performed only at franchised dealerships and customer-pay service work. Our parts and service departments also recondition used vehicles acquired by our used vehicle departments and perform preparatory work and accessory installation on new vehicles acquired by our new vehicle departments. We also offer product and accessory lines that are integrated into our parts and service operations. AutoNationParts.com, our e-commerce website, enables customers to purchase high-quality automotive parts and accessories at competitive prices, shipped directly to their homes. In addition to our retail business, we also have wholesale parts operations, which sell automotive parts to both collision repair shops and independent vehicle repair providers.

We offer a wide variety of automotive finance and insurance products to our customers. We primarily arrange for our customers to finance vehicles through installment loans or leases with third-party lenders, including the vehicle manufacturers’ and distributors’ captive finance subsidiaries, and receive a commission payable to us from the lender. Our exposure to loss in connection with financing arrangements with third-party lenders generally is limited to the commissions that we receive. We also originate and service consumer auto finance loans through our captive auto finance company. See the risk factor “We are subject to various risks associated with originating and servicing auto finance loans through indirect lending to customers, any of which could have an adverse effect on our business” in Part I, Item 1A of this Form 10-K for additional information.

We also offer our customers various vehicle protection products, including extended service contracts, maintenance programs, guaranteed auto protection (known as “GAP,” this protection covers the shortfall between a customer’s loan balance and insurance payoff in the event of a casualty), “tire and wheel” protection, and theft protection products, some of which are AutoNation-branded. These products are underwritten and administered by independent third parties, including the vehicle manufacturers’ and distributors’ captive finance subsidiaries. We sell the products on a commission basis, and we also participate in future underwriting profit for certain products pursuant to retrospective commission arrangements with the issuers of those products.

5

As of December 31, 2024, we operated stores in the following states:

| State | Number of Retail Stores (1) | Number of Franchises | Number of Other Locations (2) | % of Total Revenue | ||||||||||||||||||||||

| Florida | 51 | 57 | 18 | 26 | ||||||||||||||||||||||

| California | 41 | 55 | 2 | 19 | ||||||||||||||||||||||

| Texas | 46 | 61 | 17 | 19 | ||||||||||||||||||||||

| Colorado | 20 | 31 | 1 | 6 | ||||||||||||||||||||||

| Arizona | 17 | 17 | 4 | 6 | ||||||||||||||||||||||

| Washington | 14 | 18 | 3 | 5 | ||||||||||||||||||||||

| Georgia | 14 | 20 | 4 | 4 | ||||||||||||||||||||||

| Nevada | 12 | 13 | 1 | 4 | ||||||||||||||||||||||

| Maryland | 14 | 14 | 3 | 3 | ||||||||||||||||||||||

| Illinois | 7 | 8 | 1 | 2 | ||||||||||||||||||||||

| Tennessee | 7 | 7 | 1 | 1 | ||||||||||||||||||||||

| South Carolina | 10 | 12 | 1 | 1 | ||||||||||||||||||||||

| North Carolina | 1 | — | — | 1 | ||||||||||||||||||||||

| Ohio | 3 | 3 | 3 | 1 | ||||||||||||||||||||||

| Virginia | 2 | 2 | — | 1 | ||||||||||||||||||||||

| Alabama | 2 | 2 | — | 1 | ||||||||||||||||||||||

New Mexico (3) | 1 | — | — | — | ||||||||||||||||||||||

New York (3) | 3 | 4 | — | — | ||||||||||||||||||||||

Missouri (3) | 1 | — | — | — | ||||||||||||||||||||||

New Jersey (3) | 1 | 1 | — | — | ||||||||||||||||||||||

| Total | 267 | 325 | 59 | 100 | ||||||||||||||||||||||

(1)Includes franchised dealerships and AutoNation USA used vehicle stores.

(2)Includes collision centers, automotive auction operations, and parts distribution centers.

(3)Revenue represented less than 1% of total revenue.

Agreements with Vehicle Manufacturers

Framework Agreements

We have entered into framework and related agreements with most major vehicle manufacturers and distributors. These agreements, which are in addition to the franchise agreements described below, contain provisions relating to our management, operation, advertising and marketing, and acquisition and ownership structure of automotive stores franchised by such manufacturers. These agreements contain certain requirements pertaining to our operating performance (with respect to matters such as sales volume, sales effectiveness, and customer satisfaction or loyalty), which, if we do not satisfy, adversely impact our ability to make further acquisitions of such manufacturers’ stores or could result in us being compelled to take certain actions, such as divesting a significantly underperforming store, subject to applicable state franchise laws. Additionally, these agreements set limits (nationally, regionally, and in local markets) on the number of stores that we may acquire of the particular manufacturer and contain certain restrictions on our ability to name and brand our stores. Some of these framework agreements give the manufacturer or distributor the right to acquire at fair market value, or the right to compel us to sell, the automotive stores franchised by that manufacturer or distributor under specified circumstances in the event of a change in control of our Company (generally including certain material changes in the composition of our Board of Directors during a specified time period, the acquisition of 20% or more of the voting stock of our Company by another vehicle manufacturer or distributor, or the acquisition of 50% or more of our voting stock by a person, entity, or group not affiliated with a vehicle manufacturer or distributor) or other extraordinary corporate transactions such as a merger or sale of all or substantially all of our assets. In addition, we have granted certain manufacturers the right to acquire, at fair market value, our automotive dealerships franchised by such manufacturers in specified circumstances in the event of our default under certain of our debt agreements.

6

Franchise Agreements

We operate each of our new vehicle stores under a franchise agreement with a vehicle manufacturer or distributor. The franchise agreements grant the franchised automotive store a non-exclusive right to sell the manufacturer’s or distributor’s brand of vehicles and offer related parts and service within a specified market area. These franchise agreements grant our stores the right to use the relevant manufacturer’s or distributor’s trademarks in connection with their operations, and they also impose numerous operational requirements and restrictions relating to inventory levels, working capital levels, the sales process, marketing and branding, showroom and service facilities, signage, personnel, changes in management, and monthly financial reporting, among other things. The contractual terms of our stores’ franchise agreements provide for various durations, ranging from one year to no expiration date, and in certain cases manufacturers have undertaken to renew such franchises upon expiration so long as the store is in compliance with the terms of the agreement. We generally expect our franchise agreements to survive for the foreseeable future and, when the agreements do not have indefinite terms, anticipate routine renewals of the agreements without substantial cost or modification. Our stores’ franchise agreements provide for termination of the agreement by the manufacturer or non-renewal for a variety of causes (including performance deficiencies in such areas as sales volume, sales effectiveness, and customer satisfaction or loyalty). However, in general, the states in which we operate have automotive dealership franchise laws that provide that, notwithstanding the terms of any franchise agreement, it is unlawful for a manufacturer to terminate or not renew a franchise unless “good cause” exists. It generally is difficult, outside of bankruptcy, for a manufacturer to terminate, or not renew, a franchise under these laws, which were designed to protect dealers. In addition, in our experience and historically in the automotive retail industry, dealership franchise agreements are rarely involuntarily terminated or not renewed by the manufacturer outside of bankruptcy. From time to time, certain manufacturers assert sales and customer satisfaction performance deficiencies under the terms of our framework and franchise agreements. We generally work with these manufacturers to address the asserted performance issues. For additional information, please refer to the risk factor captioned “We are subject to restrictions imposed by, and significant influence from, vehicle manufacturers that may adversely impact our business, financial condition, results of operations, cash flows, and prospects, including our ability to acquire additional stores” in Part I, Item 1A of this Form 10-K.

Regulations

We operate in a highly regulated industry. A number of state and federal laws and regulations affect our business. In every state in which we operate, we must obtain various licenses in order to operate our businesses, including dealer, sales and finance, and insurance licenses issued by state regulatory authorities. Numerous laws and regulations govern how we conduct our business, including those relating to our sales, operations, finance and insurance, advertising, indirect auto financing, origination and servicing of consumer auto finance loans, and employment practices. These laws and regulations include state franchise laws and regulations, federal and state consumer protection laws and regulations, privacy laws, escheatment laws, anti-money laundering laws, and other extensive laws and regulations applicable to new and used motor vehicle dealers and auto finance companies, as well as a variety of other laws and regulations. These laws also include federal and state wage and hour, anti-discrimination, and other employment practices laws. See the risk factor “Our operations are subject to extensive governmental laws and regulations. If we are found to be in purported violation of or subject to liabilities under any of these laws or regulations, or if new laws or regulations are enacted that adversely affect our operations, our business, operating results, and prospects could suffer” in Part I, Item 1A of this Form 10-K.

Automotive and Other Laws and Regulations

Our operations are subject to the National Traffic and Motor Vehicle Safety Act, Federal Motor Vehicle Safety Standards promulgated by the United States Department of Transportation, and the rules and regulations of various state motor vehicle regulatory agencies. In addition, automotive dealers are subject to regulation by the Federal Trade Commission (the “FTC”). The imported automobiles, parts, and accessories we purchase are subject to United States customs duties and, in the ordinary course of our business we may, from time to time, be subject to claims for duties, penalties, liquidated damages, or other charges. Further, our captive auto finance company operations are subject to regulations and supervision by the Consumer Financial Protection Bureau (the “CFPB”). Among other things, the CFPB is authorized to take action to prevent auto finance companies from engaging in unfair, deceptive, or abusive acts and practices and to issue rules requiring enhanced disclosures concerning consumer financial products and services. In addition, state attorneys general have authority under their respective laws and regulations, and under the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), enacted in 2010, to investigate and/or regulate certain aspects of our operations.

7

Our financing activities with customers, including our origination and servicing activities through our captive auto finance company, are subject to the federal Truth-in-Lending Act, Consumer Leasing Act, Equal Credit Opportunity Act, Fair Credit Reporting Act, federal and state prohibitions against unfair, deceptive, and abusive acts and practices, and various other federal laws and regulations, as well as state and local motor vehicle finance laws, leasing laws, collection, repossession, and installment finance laws, usury laws, and other installment sales and leasing laws and regulations. Among other things, these laws and regulations regulate finance and other fees and charges that may be imposed or received in connection with motor vehicle retail installment sales and leasing, require specific disclosures to consumers, define the rights to collect payments and repossess and sell collateral, and govern the sale and terms of ancillary products. Claims arising out of actual or alleged violations of law or regulation may be asserted against us by individuals, a class of individuals, or governmental entities and may expose us to significant damages or other penalties, including fines and revocation or suspension of our licenses to conduct our operations. See the risk factor “Our operations are subject to extensive governmental laws and regulations. If we are found to be in purported violation of or subject to liabilities under any of these laws or regulations, or if new laws or regulations are enacted that adversely affect our operations, our business, operating results, and prospects could suffer” in Part I, Item 1A of this Form 10-K for additional information.

Environmental, Health, and Safety Laws and Regulations

Our operations involve the use, handling, storage, and contracting for recycling and/or disposal of materials such as motor oil and filters, transmission fluids, antifreeze, refrigerants, paints, thinners, batteries, cleaning products, lubricants, degreasing agents, tires, and fuel. Consequently, our business is subject to a complex variety of federal, state, and local requirements that regulate the environment and public health and safety.

Most of our stores utilize aboveground storage tanks and, to a lesser extent, underground storage tanks, primarily for petroleum-based products. Storage tanks are subject to periodic testing, containment, upgrading, and removal under the Resource Conservation and Recovery Act and its state law counterparts. Clean-up or other remedial action may be necessary in the event of leaks or other discharges from storage tanks or other sources. In addition, water quality protection programs under the federal Water Pollution Control Act (commonly known as the Clean Water Act), the Safe Drinking Water Act, and comparable state and local programs govern certain discharges from some of our operations. Similarly, certain air emissions from operations, such as auto body painting, may be subject to the federal Clean Air Act and related state and local laws. Certain health and safety standards promulgated by the Occupational Safety and Health Administration of the United States Department of Labor and related state agencies also apply.

Some of our stores are parties to proceedings under the Comprehensive Environmental Response, Compensation, and Liability Act, or CERCLA, typically in connection with materials that were sent to former recycling, treatment, and/or disposal facilities owned and operated by independent businesses. The remediation or clean-up of facilities where the release of a regulated hazardous substance occurred is required under CERCLA and other laws.

We have a proactive strategy related to environmental, health, and safety laws and regulations, which includes contracting with third-party vendors to inspect our facilities routinely in an effort to ensure compliance. We incur significant costs to comply with applicable environmental, health, and safety laws and regulations in the ordinary course of our business. We do not anticipate, however, that the costs of such compliance will have a material adverse effect on our business, results of operations, cash flows, or financial condition, although such outcome is possible given the nature of our operations and the extensive environmental, health, and safety regulatory framework. We do not have any material known environmental commitments or contingencies.

Markets and Competition

We operate in a highly competitive industry. We believe that the principal competitive factors in the automotive retail business are location, service, price, selection, and online and mobile offerings. Each of our markets includes a large number of well-capitalized competitors that have extensive automotive retail managerial experience and strong retail locations and facilities.

New vehicle unit volume in 2024 benefited from increases in new vehicle inventory levels due to higher levels of manufacturer vehicle production. The increasing supply and availability of new vehicle inventory has resulted in a shift in mix from used vehicles to new vehicles. Lower new vehicle sales in recent years has also resulted in lower availability of used vehicle inventory, particularly for late model used vehicles. According to industry sources, as of December 31, 2024,

8

there were approximately 17,000 franchised automotive dealerships, which sell both new and used vehicles, in the United States. In addition, we estimate that there were approximately twice as many independent used vehicle dealers in the United States. We continue to expand our footprint and increase scope and scale through both the acquisition of new dealerships and franchises and through the expansion of our AutoNation USA used vehicle stores. We face competition from (i) several public companies that operate numerous automotive retail stores or collision centers on a regional or national basis, including franchised dealers that sell new and used vehicles, non-franchised dealers that sell only used vehicles, and manufacturers that sell directly to customers, (ii) private companies that operate automotive retail stores or collision centers in our markets, (iii) electric vehicle manufacturers who sell directly to consumers, and (iv) online and mobile sales and service platforms. We compete with dealers that sell the same vehicle brands that we sell, as well as dealers and certain manufacturers that sell other vehicle brands that we do not represent in a particular market. Our new vehicle store competitors have franchise agreements with the various vehicle manufacturers and, as such, generally have access to new vehicles on the same terms as we have. We also compete with other dealers for qualified employees, including general managers and sales and service personnel.

In general, the vehicle manufacturers have designated marketing and sales areas within which only one franchised dealer of a given vehicle brand may operate. Under most framework agreements with vehicle manufacturers, the ability to acquire multiple dealers of a given vehicle brand within a particular market is limited. Dealers are also restricted by various state franchise laws from relocating stores or establishing new stores of a particular vehicle brand within any area that is served by another dealer of the same vehicle brand, and generally need the manufacturer to approve any relocation or the grant of a new franchise. However, to the extent that a market has multiple dealers of a particular vehicle brand, as most of our key markets do with respect to most vehicle brands we sell, we face significant intra-brand competition.

We also compete with independent automobile service shops, service center chains, collision service operations, and wholesale parts outlets. We believe that the principal competitive factors in the parts and service business are price, location, expertise with the particular vehicle lines, and customer service. We also compete with a broad range of financial institutions in our finance and insurance business. We believe that the principal competitive factors in the finance and insurance business are product selection, convenience, price, contract terms, and the ability to finance vehicle protection and aftermarket products.

We also operate in the auto finance sector of the consumer finance market. This sector is primarily comprised of banks, captive finance divisions of new car manufacturers, credit unions, and independent finance companies. According to industry sources, this sector represented more than $1 trillion in outstanding receivables as of December 31, 2024. Our primary competitors in this sector are banks and credit unions that offer direct and indirect financing to customers purchasing vehicles.

Insurance and Bonding

Our business exposes us to the risk of liabilities arising out of our operations. For example, liabilities may arise out of claims of employees, customers, or other third parties for personal injury or property damage occurring in the course of our operations. We could also be subject to fines and civil and criminal penalties in connection with alleged violations of federal and state laws or regulatory requirements.

The automotive retail business is also subject to substantial risk of property loss due to the significant concentration of property values at store locations. In our case in particular, our operations are concentrated in states and regions in which natural disasters and severe weather events (such as hailstorms, hurricanes, earthquakes, fires, tornadoes, snowstorms, and landslides) may subject us to substantial risk of property loss and operational disruption. Under self-insurance programs, we retain various levels of aggregate loss limits, per claim deductibles, and claims-handling expenses as part of our various insurance programs, including property and casualty, automobile, workers’ compensation, and employee medical benefits. Costs in excess of this retained risk per claim may be insured under various contracts with third-party insurance carriers. We estimate the ultimate costs of these retained insurance risks based on actuarial evaluations and historical claims experience, adjusted for current trends and changes in claims-handling procedures. The level of risk we retain may change in the future as insurance market conditions or other factors affecting the economics of our insurance purchasing change. Although we have, subject to certain limitations and exclusions, substantial insurance, we cannot assure you that we will not be exposed to uninsured or underinsured losses that could have a material adverse effect on our business, financial condition, results of operations, or cash flows. During 2024, we recognized self-insured losses of $11.7 million primarily due to weather-related events.

9

Provisions for retained losses and deductibles are made by charges to expense based upon periodic evaluations of the estimated ultimate liabilities on reported and unreported claims. The insurance companies that underwrite our insurance require that we secure certain of our obligations for deductible reimbursements with collateral. Our collateral requirements are set by the insurance companies and, to date, have been satisfied by posting surety bonds, letters of credit, and/or cash deposits. Our collateral requirements may change from time to time based on, among other things, our claims experience.

Seasonality

In a stable environment, our operations generally experience higher volumes of vehicle unit sales in the second and third quarters of each year due in part to consumer buying trends and the introduction of new vehicle models. Also, demand for vehicles and light trucks is generally lower during the winter months than in other seasons, particularly in regions of the United States where stores may be subject to adverse winter conditions. However, we typically experience higher sales of Premium Luxury vehicles, which have higher average selling prices and gross profit per vehicle retailed, in the fourth quarter. Revenue and operating results may be impacted significantly from quarter to quarter by changing economic conditions, vehicle manufacturer incentive programs, and actual or threatened severe weather events.

Trademarks

We own a number of registered service marks and trademarks, including, among other marks, AutoNation® and AutoNation USA®. Pursuant to agreements with vehicle manufacturers, we have the right to use and display manufacturers’ trademarks, logos, and designs at our stores and in our advertising and promotional materials, subject to certain restrictions. We also have licenses pursuant to various agreements with third parties authorizing the use and display of the marks and/or logos of such third parties, subject to certain restrictions. The current registrations of our service marks and trademarks are effective for varying periods of time, which we may renew periodically, provided that we comply with all applicable laws.

Human Capital Resources

At AutoNation, our associates are our greatest asset. As of December 31, 2024, we employed approximately 25,100 full-time and part-time employees, whom we refer to as “associates,” approximately 170 of whom were covered by collective bargaining agreements. The development, attraction, and retention of people is central to the culture at AutoNation. We are committed to ensuring we create an environment where all associates feel valued, respected, and empowered to achieve their highest potential. Our Board of Directors and its Committees provide oversight on a broad range of human capital management topics, including corporate culture, talent, compensation, and benefits.

Recruitment and Development

Our recruitment efforts include branded advertising nationwide on well-known online job websites, as well as recruitment efforts through technical schools, veteran partnerships, colleges, and universities. In addition, AutoNation provides extensive on-the-job training and opportunities for career growth. We provide a range of formal and informal learning programs, which are designed to help our associates continuously grow and strengthen their skills throughout their careers. Creating opportunities for employee recognition, development, and advancement is a key initiative in our talent efforts.

Compensation and Benefits

AutoNation offers a comprehensive total rewards program, including competitive salaries and compensation plans, incentive compensation potential, and health and welfare benefits. We offer many benefits at no additional cost to our associates, including our Employee Assistance Program, Company-paid maternity leave, and our innovative “Drive Pink”-inspired Company-paid cancer insurance plan that provides financial assistance to associates and their eligible dependents who are diagnosed with cancer.

Engagement

AutoNation believes that fostering an open-door culture based on trust, respect, and open communication among team members is vital for driving long-term sustainable growth. AutoNation conducts associate engagement surveys, which allows the Company to gain comprehensive insights and establish organization priorities. More than simply listening to associates, AutoNation also provides managers with tools they need to be able to address associate feedback constructively

10

with actionable next steps. The combined effort of these engagement activities drives AutoNation to continuously improve the culture of the organization.

Information about our Executive Officers

The following sets forth certain information regarding our executive officers as of February 14, 2025.

| Name | Age | Position | Years with AutoNation | Years in Automotive Industry | ||||||||||||||||||||||

| Michael Manley | 60 | Chief Executive Officer and Director | 4 | 37 | ||||||||||||||||||||||

Thomas A. Szlosek | 61 | Executive Vice President and Chief Financial Officer | 2 | 2 | ||||||||||||||||||||||

| Gianluca Camplone | 55 | Chief Operating Officer, AutoNation Parts, and Executive Vice President, Business Development | 3 | 27 | ||||||||||||||||||||||

| C. Coleman Edmunds | 60 | Executive Vice President, General Counsel and Corporate Secretary | 29 | 29 | ||||||||||||||||||||||

| Lisa Esparza | 55 | Executive Vice President and Chief Human Resource Officer | 3 | 3 | ||||||||||||||||||||||

| Dave Koehler | 56 | Chief Operating Officer, Non-Franchised Business | 13 | 32 | ||||||||||||||||||||||

Jeff Parent | 60 | Chief Operating Officer | 2 | 27 | ||||||||||||||||||||||

Michael Manley has served as our Chief Executive Officer and as a member of our Board since November 2021. Prior to joining AutoNation, Mr. Manley served as Head of Americas and as a member of the Group Executive Council for Stellantis N.V., one of the largest automotive original equipment manufacturers in the world, from January 2021 until October 2021. From July 2018 until January 2021, he served as Chief Executive Officer of Fiat Chrysler Automobiles N.V. (“FCA”), a predecessor to Stellantis N.V. Mr. Manley joined DaimlerChrysler (a predecessor to FCA) in 2000 and, prior to becoming FCA’s Chief Executive Officer, served in a number of management-level roles with increasing responsibility overseeing various aspects of FCA’s operations, including as Executive Vice President - International Sales & Marketing, Business Development and Global Product Planning Operations, Chief Executive Officer of Jeep, Chief Executive Officer of Ram, Chief Operating Officer for the Asia Pacific region, and FCA Global Executive Council member. Mr. Manley currently serves on the Board of Directors of Dover Corporation (NYSE: DOV), a diversified global manufacturer and solutions provider delivering innovative equipment and components, consumable supplies, aftermarket parts, software and digital solutions, and support services.

Thomas A. Szlosek has served as our Executive Vice President and Chief Financial Officer since August 2023. Mr. Szlosek is responsible for overseeing the finance department and for all financial controls and external reporting, financial planning and analysis, and accounting, as well as the tax, internal audit, treasury, investor relations, and corporate real estate functions. He is also responsible for our shared service center in Irving, Texas. Prior to joining AutoNation, Mr. Szlosek served as Executive Vice President and Chief Financial Officer at Avantor, Inc., a leading global provider of mission-critical products and services to customers in the life sciences, education and government, advanced technologies, and applied materials industries, from December 2018 until August 2023. Prior to joining Avantor, Mr. Szlosek served as the Senior Vice President and Chief Financial Officer of Honeywell International, a diversified technology and manufacturing company, from April 2014 to August 2018.

Gianluca Camplone has served as our Chief Operating Officer, AutoNation Parts, and Executive Vice President, Business Development since March 2022. Mr. Camplone is responsible for overseeing the Company’s business strategy, corporate development, and Parts teams. Prior to joining AutoNation, Mr. Camplone was a Senior Partner at McKinsey & Company, a global management consulting firm, from December 1996 to February 2022, where he was the leader in their Advanced Industries global practice and Private Equity Industrial practice in North America.

C. Coleman Edmunds has served as our Executive Vice President, General Counsel and Corporate Secretary since April 2017. From October 2007 through March 2017, Mr. Edmunds served as our Senior Vice President, Deputy General Counsel and Assistant Secretary. He joined AutoNation in November 1996. Prior to joining AutoNation, Mr. Edmunds was in private practice with the international law firm of Baker & McKenzie.

Lisa Esparza has served as our Executive Vice President and Chief Human Resource Officer since September 2022. Prior to joining AutoNation, Ms. Esparza served as Chief Human Resource Officer of Essilor North America, part of

11

EssilorLuxottica, the global leader in the design, manufacture, and distribution of ophthalmic lenses, frames, and sunglasses, from July 2019 to June 2022. From 2017 to 2019, Ms. Esparza served as Chief Human Resources Officer at Par Pacific Holdings, Inc. (NYSE: PARR), which owns and operates market-leading energy and infrastructure businesses. In addition, Ms. Esparza has held various human resources leadership roles at Celanese, Flowserve, Ingersoll-Rand, and Eaton with global responsibilities.

Dave Koehler has served as our Chief Operating Officer, Non-Franchised Business since March 2022. Mr. Koehler is responsible for overseeing AutoNation USA, AutoNation Mobile Service, and AutoNation Auto Auctions. Previously, Mr. Koehler was the Eastern Region President for our stores located in Alabama, Florida, Georgia, Illinois, Maryland, Minnesota, New York, Ohio, Tennessee, and Virginia from May 2019 to February 2022. Prior to being promoted to Eastern Region President in May 2019, Mr. Koehler held several key positions within AutoNation, including General Manager, Market President, and Senior Vice President of Sales between 2011 to 2019.

Jeff Parent has served as our Chief Operating Officer since October 2023. Mr. Parent oversees AutoNation’s day-to-day operations and works as part of the leadership team to execute the company’s strategic vision and drive operational excellence. Prior to joining AutoNation, Mr. Parent served as President and General Manager of Gulf States Toyota, Inc., one of the world’s largest independent distributors of Toyota vehicles and parts, from February 2017 until October 2023. Prior to joining Gulf States Toyota as a Senior Vice President in 2010, Mr. Parent held various senior executive positions at Nissan Canada Inc., Volkswagen of America, Inc., and VW Credit, Inc.

Available Information

Our website is located at www.autonation.com, and our Investor Relations website is located at investors.autonation.com. The information on or accessible through our websites and social media channels is not incorporated by reference in this Annual Report on Form 10-K. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, on our Investor Relations website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (the “SEC”).

12

ITEM 1A. RISK FACTORS

Our business, financial condition, results of operations, cash flows, and prospects, and the prevailing market price and performance of our common stock may be adversely affected by a number of factors, including the matters discussed below. Certain statements and information set forth in this Annual Report on Form 10-K, including, without limitation, statements regarding our strategic initiatives, partnerships, or investments, including AutoNation Finance, statements regarding our expectations for the future performance of our business and the automotive retail industry, including during 2025, statements regarding the impact of the CDK Global (“CDK”) outage on our business and the availability of insurance or other sources of recovery, as well as other written or oral statements made from time to time by us or by our authorized executive officers on our behalf that describe our objectives, goals, or plans constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact, including statements that describe our objectives, plans or goals are, or may be deemed to be, forward-looking statements. Words such as “anticipate,” “expect,” “estimate,” “intend,” “goal,” “target,” “project,” “plan,” “believe,” “continue,” “may,” “will,” “could,” and variations of such words and similar expressions are intended to identify such forward-looking statements. Our forward-looking statements reflect our current expectations concerning future results and events, and they involve known and unknown risks, uncertainties and other factors that are difficult to predict and may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by these statements. These forward-looking statements speak only as of the date of this report, and we undertake no obligation to revise or update these statements to reflect subsequent events or circumstances. The risks, uncertainties, and other factors that our stockholders and prospective investors should consider include, but are not limited to, the following:

Risks Related to Economic Conditions

The automotive retail industry is sensitive to changing economic conditions and various other factors, including, but not limited to, unemployment levels, consumer confidence, fuel prices, interest rates, and tariffs. Our business and results of operations are substantially dependent on new and used vehicle sales levels in the United States and in our particular geographic markets, as well as the gross profit margins that we can achieve on our sales of vehicles, all of which are very difficult to predict.

We believe that many factors affect sales of new and used vehicles and automotive retailers’ gross profit margins in the United States and in our particular geographic markets, including the economy, fuel prices, credit availability, interest rates, consumer confidence, consumer shopping preferences and the success of third-party online and mobile sales platforms, the level of personal discretionary spending, labor force participation and unemployment rates, the state of housing markets, vehicle production levels and capacity, auto emission and fuel economy standards, the rate of inflation, currency exchange rates, tariffs, manufacturer incentives (and consumers’ reaction to such offers), intense industry competition, the prospects of war, other international conflicts or terrorist attacks, global pandemics, severe weather events, product quality, affordability and innovation, the number of consumers whose vehicle leases are expiring, the length of consumer loans on existing vehicles, and the rise of ride-sharing applications. Changes in interest rates can significantly impact new and used vehicle sales and vehicle affordability due to the direct relationship between interest rates and monthly loan payments, a critical factor for many vehicle buyers, and the impact interest rates have on customers’ borrowing capacity and disposable income. Sales of certain vehicles, particularly trucks and sport utility vehicles that historically have provided us with higher gross profit per vehicle retailed, are sensitive to fuel prices and the level of construction activity. In addition, rapid changes in fuel prices can cause shifts in consumer preferences which are difficult to accommodate given the long lead-time of inventory acquisition. The imposition of new tariffs, quotas, duties, or other restrictions or limitations could increase prices for vehicles and/or parts imported into the United States and adversely impact demand for such vehicles and/or parts. Our vehicle sales, service, and collision businesses could also be adversely affected by changes in the automotive industry driven by new technologies, distribution channels, or products, including ride-sharing applications, subscription services, autonomous and electric vehicles, and accident avoidance technology.

Approximately 16.0 million, 15.6 million, and 13.9 million new vehicles, including retail and fleet vehicles, were sold in the United States in 2024, 2023, and 2022, respectively. Our performance may differ from the performance of the automotive retail industry due to particular economic conditions and other factors in the geographic markets in which we operate. Economic conditions and the other factors described above may also materially adversely impact our sales of parts and

13

automotive repair and maintenance services and automotive finance and insurance products and our ability to approve/provide financing to customers.

Risks Related to Vehicle Manufacturers and Other Third-Party Suppliers

Our new vehicle sales are impacted by the incentive, marketing, and other programs of vehicle manufacturers.

Most vehicle manufacturers from time to time establish various marketing and sales incentive programs designed to spur consumer demand for their vehicles, particularly during periods of excess supply and/or in a flat or declining new vehicle sales market. These programs impact our operations, particularly our sales of new vehicles. Since these programs are often not announced in advance, they can be difficult to plan for when ordering inventory. Furthermore, manufacturers may modify and discontinue these marketing and incentive programs from time to time, which could have a material adverse effect on our results of operations and cash flows.

In prior years, our new vehicle unit volume and new vehicle gross profit on a per vehicle retailed basis were adversely impacted by certain manufacturers’ disruptive marketing and sales incentive programs based upon store-level growth targets established by those manufacturers (commonly referred to as “stair-step” incentive programs), which result in multi-tier pricing and adversely impact our ability to compete with other dealers. If those manufacturers continue to use such incentive programs or if other manufacturers adopt similar incentive programs, our operating results could be adversely impacted.

We are dependent upon the success and continued financial viability of the vehicle manufacturers and distributors with which we hold franchises. In addition, we rely on various third-party suppliers for key products and services.

The success of our stores is dependent on vehicle manufacturers in several key respects. First, we rely exclusively on the various vehicle manufacturers for our new vehicle inventory. Our ability to sell new vehicles is dependent on a vehicle manufacturer’s ability to design, manufacture, and allocate to our stores an attractive, high-quality, and desirable product mix at the right time and at the right price in order to satisfy customer demand. Second, manufacturers generally support their franchisees by providing direct financial assistance in various areas, including, among others, floorplan assistance and advertising assistance. Third, manufacturers provide product warranties and, in some cases, service contracts to customers.

Our stores perform warranty and service contract work for vehicles under manufacturer product warranties and service contracts, and direct bill the manufacturer as opposed to invoicing the store customer. At any particular time, we have significant receivables from manufacturers for warranty and service work performed for customers. In addition, we rely on manufacturers to varying extents for original equipment manufactured replacement parts, training, product brochures and point of sale materials, and other items for our stores. Our business, results of operations, and financial condition could be materially adversely affected as a result of any event that has a material adverse effect on the vehicle manufacturers or distributors that are our primary franchisors.

The core brands of vehicles that we sell, representing approximately 88% of the new vehicles that we sold in 2024, are manufactured by Toyota (including Lexus), Honda, Ford, General Motors, BMW, Mercedes-Benz, Stellantis, and Volkswagen (including Audi and Porsche). As a result, we are subject to a concentration of risk, and our business could be materially adversely impacted by the financial distress, including bankruptcy, of or other adverse event related to a major vehicle manufacturer or related lender or supplier.

Vehicle manufacturers may be adversely impacted by economic downturns or recessions, significant declines in the sales of their new vehicles, natural disasters, increases in interest rates, adverse fluctuations in currency exchange rates, declines in their credit ratings, liquidity concerns, labor strikes or similar disruptions (including within their major suppliers), supply shortages or rising raw material costs, rising employee benefit costs, vehicle recall campaigns, adverse publicity that may reduce consumer demand for their products (including due to bankruptcy), product defects, litigation, poor product mix or unappealing vehicle design, governmental laws and regulations (including fuel economy requirements), tariffs and other import product restrictions, the rise of ride-sharing applications, or other adverse events. These and other risks could materially adversely affect any manufacturer and impact its ability to profitably design, market, produce, or distribute new vehicles, which in turn could materially adversely affect our ability to obtain or finance our desired new vehicle inventories, our ability to take advantage of manufacturer financial assistance programs, our ability to collect in full or on a timely basis our manufacturer warranty and other receivables, and/or our ability to obtain other goods and services provided by the

14

impacted manufacturer. In addition, vehicle recall campaigns could materially adversely affect our business, results of operations, and financial condition.

Our business could be materially adversely impacted by the bankruptcy of a major vehicle manufacturer or related lender. For example, (i) a manufacturer in bankruptcy could attempt to terminate all or certain of our franchises, in which case we may not receive adequate compensation for our franchises, (ii) consumer demand for such manufacturer’s products could be materially adversely affected, (iii) a lender in bankruptcy could attempt to terminate our floorplan financing and demand repayment of any amounts outstanding, (iv) we may be unable to arrange financing for our customers for their vehicle purchases and leases through such lender, in which case we would be required to seek financing with alternate financing sources, which may be difficult to obtain on similar terms, if at all, (v) we may be unable to collect some or all of our significant receivables that are due from such manufacturer or lender, and we may be subject to preference claims relating to payments made by such manufacturer or lender prior to bankruptcy, and (vi) such manufacturer may be relieved of its indemnification obligations with respect to product liability claims. Additionally, any such bankruptcy may result in us being required to incur impairment charges with respect to the inventory, fixed assets, right-of-use assets, and intangible assets related to certain franchises, which could adversely impact our results of operations and financial condition.

Further, we rely on various third-party suppliers for key products and services to support our business, including CDK, the provider of our dealer management system (“DMS”), which supports our dealership operations, including our sales, service, inventory, customer relationship management, and accounting functions. Outsourcing to third-party suppliers reduces our direct control over the services rendered, as we do not have control over their business operations, governance, or compliance systems, practices, and procedures. If our suppliers fail to deliver products or services on a timely basis and at reasonable prices for any reason, or if the third-parties’ services are interrupted, disabled, sub-standard, or otherwise deficient, as they have been or may be in the future, our business continuity or recovery programs may not be sufficient to mitigate the harm that may result, and we could face difficulties operating our business and suffer reputational harm, and our results of operations and financial condition could be adversely impacted. See the risk factor, “We depend on information technology for our business and are subject to risks related to cybersecurity threats and incidents, including those affecting our third-party suppliers and other service providers. A failure of our information systems or any cybersecurity breaches or unauthorized disclosure of confidential information could have a material adverse effect on our business, disrupt our business, and adversely impact our reputation and results of operations” below for additional information on the CDK cyber incident in June 2024.

We are subject to restrictions imposed by, and significant influence from, vehicle manufacturers that may adversely impact our business, financial condition, results of operations, cash flows, and prospects, including our ability to acquire additional stores.

Vehicle manufacturers and distributors with whom we hold franchises have significant influence over the operations of our stores. The terms and conditions of our framework, franchise, and related agreements and the manufacturers’ interests and objectives may, in certain circumstances, conflict with our interests and objectives. For example, manufacturers can set performance standards with respect to sales volume, sales effectiveness, and customer satisfaction or loyalty, and can influence our ability to acquire additional stores, the naming and marketing of our stores, our digital channels, our selection of store management, product stocking and advertising spending levels, and the level at which we capitalize our stores. Manufacturers also impose minimum facility requirements that can require significant capital expenditures. Manufacturers may also have certain rights to restrict our ability to provide guaranties of our operating companies, pledges of the capital stock of our subsidiaries, and liens on our assets, which could adversely impact our ability to obtain financing for our business and operations on favorable terms or at desired levels. From time to time, we are precluded under agreements with certain manufacturers from acquiring additional franchises, or subject to other adverse actions, to the extent we are not meeting certain performance criteria at our existing stores (with respect to matters such as sales volume, sales effectiveness, and customer satisfaction or loyalty) until our performance improves in accordance with the agreements, subject to applicable state franchise laws.

Manufacturers also have the right to establish new franchises or relocate existing franchises, subject to applicable state franchise laws. The establishment or relocation of franchises in our markets could have a material adverse effect on the financial condition, results of operations, cash flows, and prospects of our stores in the market in which the franchise action is taken.

15

Our framework, franchise, and related agreements also grant the manufacturer the right to terminate or compel us to sell our franchise for a variety of reasons (including uncured performance deficiencies, any unapproved change of ownership or management, or any unapproved transfer of franchise rights or impairment of financial standing or failure to meet capital requirements), subject to applicable state franchise laws. From time to time, certain major manufacturers assert sales and customer satisfaction performance deficiencies under the terms of our framework and franchise agreements. Additionally, our framework agreements contain restrictions regarding a change in control, which may be outside of our control. See “Agreements with Vehicle Manufacturers” in Part I, Item 1 of this Form 10-K. While we believe that we will be able to renew all of our franchise agreements, we cannot guarantee that all of our franchise agreements will be renewed or that the terms of the renewals will be favorable to us. We cannot assure you that our stores will be able to comply with manufacturers’ sales, customer satisfaction, loyalty, performance, facility, and other requirements in the future, which may affect our ability to acquire new stores or renew our franchise agreements, or subject us to other adverse actions, including termination or compelled sale of a franchise, any of which could have a material adverse effect on our financial condition, results of operations, cash flows, and prospects. Furthermore, we rely on the protection of state franchise laws in the states in which we operate and if those laws are repealed or weakened, our framework, franchise, and related agreements may become more susceptible to termination, non-renewal, or renegotiation.

In addition, we have granted certain manufacturers the right to acquire, at fair market value, our automotive dealerships franchised by that manufacturer in specified circumstances in the event of our default under certain of our debt agreements.

Risks Related to Strategic Initiatives

We are investing significantly in various strategic initiatives, including the planned expansion of our AutoNation Finance business, our AutoNation USA used vehicle stores, and our AutoNation Mobile Service business, and if they are not successful, we will have incurred significant expenses without the benefit of improved financial results.

We have invested and will continue to invest substantial resources in marketing activities with the goals of, among other things, extending and enhancing the AutoNation retail brand and attracting consumers to our own digital channels. We are also investing significantly in various strategic initiatives, including the planned expansion of our AutoNation Finance business, our AutoNation USA used vehicle stores, and our AutoNation Mobile Service business. These strategic initiatives may be impacted by a number of variables, including customer adoption, availability of used vehicle inventory, demand for our branded products, market conditions, and our ability to identify, acquire, and build out suitable locations in a timely manner. There can be no assurance that these initiatives will be successful or that the amount we invest in these initiatives will result in improved financial results. If our initiatives are not successful, we will have incurred significant expenses without the benefit of improved financial results, and we may be required to incur impairment charges.

If we are not able to maintain and enhance our retail brands and reputation or to attract consumers to our own digital channels, or if events occur that damage our retail brands, reputation, or sales channels, our business and financial results may be harmed.

We have made significant investments to build an excellent reputation as an automotive retailer in the United States in a highly competitive industry. All of our Domestic and Import stores are unified under the AutoNation retail brand. We believe that our continued success will depend on our ability to maintain and enhance the value of our retail brands across all of our sales channels, including in the communities in which we operate, and to attract consumers to our own digital channels.

Consumers are increasingly shopping for new and used vehicles, automotive repair and maintenance services, and other automotive products and services online and through mobile applications, including through third-party online and mobile sales platforms, with which we compete. We have invested and will continue to invest substantial resources on offering our vehicles and services through digital channels. There can be no assurance that our initiatives and investments in digital channels will be successful or result in improved financial performance. We face increased competition for market share from other automotive retailers and sales platforms, including electric vehicle manufacturers who sell directly to consumers, that have also invested substantial resources on offering their vehicles and services through digital channels. If we fail to preserve the value of our retail brands, maintain our reputation, or attract consumers to our own digital channels, our business could be adversely impacted.

In addition, an isolated business incident at a single store could materially adversely affect our other stores, retail brands, reputation, and sales channels, particularly if such incident results in adverse publicity, governmental investigations, or

16