UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2021

OR

For the transition period from to

Commission file number 0-6233

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

Registrant’s telephone number, including area code: (574 ) 235-2000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of the voting common stock held by non-affiliates of the registrant as of June 30, 2021 was $906,733,159

The number of shares outstanding of each of the registrant’s classes of stock as of February 11, 2022: Common Stock, without par value — 24,750,203 shares

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| Certifications | |||||||||||

2

Part I

Item 1. Business.

1ST SOURCE CORPORATION

1st Source Corporation, an Indiana corporation incorporated in 1971, is a bank holding company headquartered in South Bend, Indiana that provides, through its subsidiaries (collectively referred to as “1st Source”, “we”, and “our”), a broad array of financial products and services. 1st Source Bank (“Bank”), its banking subsidiary, offers commercial and consumer banking services, trust and wealth advisory services, and insurance to individual and business clients through most of our 79 banking center locations in 18 counties in Indiana and Michigan and Sarasota County in Florida. 1st Source Bank’s Specialty Finance Group, with 18 locations nationwide, offers specialized financing services for construction equipment, new and pre-owned private and cargo aircraft, and various vehicle types (cars, trucks, vans) for fleet purposes. While our lending portfolio is concentrated in certain equipment types, we serve a diverse client base. We are not dependent upon any single industry or client. At December 31, 2021, we had consolidated total assets of $8.10 billion, total loans and leases of $5.35 billion, total deposits of $6.68 billion, and total shareholders’ equity of $916.26 million.

Our principal executive office is located at 100 North Michigan Street, South Bend, Indiana 46601 and our telephone number is (574) 235-2000. Access to our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports is available, free of charge, at www.1stsource.com soon after the material is electronically filed with or furnished to the Securities and Exchange Commission (SEC). The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

1ST SOURCE BANK

1st Source Bank is a wholly owned subsidiary of 1st Source Corporation that offers a broad range of consumer and commercial banking services through its lending operations, retail branches, and fee based businesses.

Commercial, Agricultural, and Real Estate Loans — 1st Source Bank provides commercial, small business, agricultural, and real estate loans to primarily privately owned business clients mainly located within our regional market area. Loans are made for a wide variety of general corporate purposes, including financing for industrial and commercial properties, financing for equipment, inventories and accounts receivable, renewable energy financing, and acquisition financing. Other services include commercial leasing, treasury management services and retirement planning services.

Renewable Energy Financing — 1st Source Bank provides financing for commercial solar projects across the contiguous United States, with a focus in the Northeast and Midwest states. 1st Source Bank’s approach provides solar developers with one-stop shop financing including construction loans, permanent loans, and tax equity investments for community solar, commercial and industrial, small utility scale, university, and municipal projects. Project sizes generally range from five megawatts to 20 megawatts.

Consumer Services — 1st Source Bank provides a full range of consumer banking products and services through our banking centers and at 1stsource.com. The traditional banking services include checking and savings accounts, certificates of deposits and Individual Retirement Accounts. 1st Source offers a full line of on-line and mobile banking products which includes person-to-person payments, mobile deposit, outside account aggregation, money management budgeting solution and bill payment. As an added convenience, a strategically located Automated Teller Machine network serves our customers and supports the debit and credit card programs of the bank. Consumers also have the ability to obtain consumer loans, credit cards, real estate mortgage loans and home equity lines of credit in any of our banking centers or on-line. In a number of our markets, 1st Source also offers insurance products through 1st Source Insurance offices or in our banking centers. Finally, 1st Source offers a variety of financial planning, financial literacy and other consultative services to our customers.

Trust and Wealth Advisory Services — 1st Source Bank provides a wide range of trust, investment, agency, and custodial services for individual, corporate, and not-for-profit clients. These services include the administration of estates and personal trusts, as well as the management of investment accounts for individuals, employee benefit plans, and charitable foundations.

Specialty Finance Group Services — 1st Source Bank, through its Specialty Finance Group, provides a broad range of comprehensive equipment loan and lease products addressing the financing needs of a broad array of companies. This group can be broken down into four areas: construction equipment; new and pre-owned aircraft; auto and light trucks; and medium and heavy duty trucks.

Construction equipment financing includes financing of equipment (i.e., asphalt and concrete plants, bulldozers, excavators, cranes and loaders, etc.) to the construction industry. Construction equipment finance receivables generally range from $50,000 to $25 million with fixed or variable interest rates and terms of one to ten years.

3

Aircraft financing consists of financings for new and pre-owned general aviation aircraft (including helicopters) for private and corporate aircraft users, aircraft distributors and dealers, air charter operators, air cargo carriers, and other aircraft operators. For many years, on a limited and selective basis, 1st Source Bank has provided international aircraft financing, primarily in Mexico and Brazil. Aircraft finance receivables generally range from $500,000 to $20 million with fixed or variable interest rates and terms of one to ten years.

The auto and light truck division (including specialty vehicles such as step vans, vocational work trucks, motor coaches, shuttle buses and funeral cars) consists of fleet financings to automobile and light truck rental companies, commercial leasing companies, and single unit to fleet financing for users of specialty vehicles. The auto and light truck finance receivables generally range from $50,000 to $35 million with fixed or variable interest rates and terms of one to eight years.

The medium and heavy duty truck division provides fleet financing for highway tractors, medium duty trucks and trailers to the commercial trucking industry. Medium and heavy duty truck finance receivables generally range from $50,000 to $25 million with fixed or variable interest rates and terms of three to seven years.

In addition to loan and lease financings during 2021, the group had average total deposit account balances of approximately $231 million.

SPECIALTY FINANCE GROUP SUBSIDIARIES

The Specialty Finance Group also consists of separate wholly owned subsidiaries of 1st Source Bank which include: Michigan Transportation Finance Corporation, 1st Source Specialty Finance, Inc., SFG Aircraft, Inc., 1st Source Intermediate Holding, LLC, SFG Commercial Aircraft Leasing, Inc., and SFG Equipment Leasing Corporation I.

1ST SOURCE INSURANCE, INC.

1st Source Insurance, Inc. is a wholly owned subsidiary of 1st Source Bank that provides insurance products and services to individuals and businesses covering corporate and personal property, casualty insurance, individual and group health insurance and life insurance. 1st Source Insurance, Inc. has ten offices.

CONSOLIDATED VARIABLE INTEREST SUBSIDIARIES

1st Source Bank is the managing general partner in the following subsidiaries that have interests in tax-advantaged investments with third parties: 1st Source Solar 2, LLC, 1st Source Solar 3, LLC, 1st Source Solar 4, LLC, 1st Source Solar 5, LLC, 1st Source Solar 6, LLC and 1st Source Solar 7, LLC.

OTHER CONSOLIDATED SUBSIDIARIES

We have other subsidiaries that are not significant to the consolidated entity.

1ST SOURCE MASTER TRUST

Our unconsolidated subsidiary includes 1st Source Master Trust. This subsidiary was created for the purpose of issuing $57.00 million of trust preferred securities and lending the proceeds to 1st Source. We guarantee, on a limited basis, payments of distributions on the trust preferred securities and payments on redemption of the trust preferred securities.

COMPETITION

The activities in which we and the Bank engage are highly competitive. Our businesses and the geographic markets we serve require us to compete with other banks, some of which are affiliated with large bank holding companies headquartered outside of our principal market. We generally compete on the basis of client service and responsiveness to client needs, available loan and deposit products, the rates of interest charged on loans and leases, the rates of interest paid for funds, other credit and service charges, the quality of services rendered, the convenience of banking facilities, and in the case of loans and leases to large commercial borrowers, relative lending limits.

In addition to competing with other banks within our primary service areas, the Bank also competes with other financial service companies, such as credit unions, industrial loan associations, securities firms, insurance companies, small loan companies, finance companies, mortgage companies, real estate investment trusts, certain governmental agencies, credit organizations, and other enterprises.

Additional competition for depositors’ funds comes from United States Government securities, private issuers of debt obligations, and suppliers of other investment alternatives for depositors. Many of our non-bank competitors are not subject to the same extensive Federal and State regulations that govern bank holding companies and banks. Such non-bank competitors may, as a result, have certain advantages over us in providing some services.

4

We compete against these financial institutions by being convenient to do business with, and by taking the time to listen and understand our clients’ needs. We deliver personalized, one-on-one banking through knowledgeable local members of the community always keeping the clients’ best interest in mind while offering a full array of products and highly personalized services. We rely on our history and our reputation in northern Indiana dating back to 1863.

HUMAN CAPITAL

At December 31, 2021, we had approximately 1,130 colleagues on a full-time equivalent basis. As a service-driven business, our long-term success depends on our people. And as the Company grows, the importance of our talent strategy has only intensified. For these reasons, we are committed to taking a multi-dimensional approach to talent and culture.

We are concerned with the health and safety of our colleagues, clients and the communities we serve. The COVID-19 pandemic has created challenges that required an immediate and evolving response to ensure the safety of our team members and our clients. See Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations under the heading “Coronavirus (COVID-19) Impact” for more information regarding the actions we have taken in response to the ongoing pandemic.

Diversity, Equity and Inclusion — At 1st Source, we cultivate and advance diversity in all forms as part of building a strong culture, a culture in which inclusion and belonging are paramount, and where all of our colleagues strive to be open and inclusive leaders and teammates. Our culture is what unifies our colleagues across our diverse business model, ensures we are best positioned to serve our diverse clients and propels our continuous evolution. In 2021, Forbes Magazine recognized the Company again as one of America’s best employers for veterans which included our approach to diversity and inclusion. While we appreciate such recognition, we are committed to continuous improvement in this area.

Oversight of Our Progress — Senior-level oversight and ongoing monitoring are critical to informing and improving our recruiting and development practices as we seek to continually create a more inclusive and diverse organization. We are proud of a 50+ year tradition since 1st Source became independent again in 1971 supported by consistent leadership of a Board representative of racial, ethnic, gender, and experiential diversity. This was highlighted in 2021 as two of our board members, Melody Birmingham and Tracy Graham, were recognized by Savoy Magazine on their list of Most Influential Black Corporate Directors.

Transparency and Accountability — We reinforce oversight and monitoring by, among other things, setting annual goals for diversity, equity and inclusion in our primary performance incentive plans. In 2021, all employees completed a required series of facilitated training sessions on unconscious bias. In addition, with our workforce, we track and monitor voluntarily disclosed diversity data to review hiring, promotion and attrition at the Company, regional and functional levels. We also review performance data and promotion and compensation information to ensure fair and objective decision-making. During our regular reviews of each business unit, senior management engages in focused conversations with each business about their plans and progress in professional development of their teams and with respect to diversity and inclusion.

Talent Vision and Strategy — Our people and culture are critical to the Company’s long-term success. As such, our talent vision and strategy focus on:

•Ensuring every candidate selected has a desire to serve others and demonstrates our unique service delivery model in their personal reoccurring patterns of behavior.

•Enabling change management and performance teams that generate career opportunities for our people and create future leaders of the firm.

•Creating an environment of inclusion, belonging and diversity, where we work with purpose and everyone feels seen, heard, and engaged.

•Promoting emotional ownership and partnership throughout the Company.

Our talent vision and strategy must be implemented in the context of an evolving business with accelerating velocity of change. To reflect the ongoing transformation in our industry, we are focused on:

•Reinforcing our culture and diversity as a source of competitive advantage.

•Delivering a consistent, fair, and high-quality experience for our people.

•Designing an organizational model that supports our diversified lines of business and growing technology capabilities.

•Developing a scalable technology platform to effectively deploy and manage our people. processes, and technologies.

5

Talent Development — We believe a critical driver of our firm’s future growth is our ability to grow leaders. We are committed to identifying and developing talent to help our colleagues accelerate their growth and achieve their career goals. We provide developmental opportunities for our colleagues through a robust set of formal and informal programs.

•1st Source University focuses on enabling colleagues to build skills and knowledge in specific facets of our business. These educational experiences and resources include topics such as client relationships, technology, investments, compliance, leadership and management, and professional development.

•The 1st Source L.E.A.D. program is a set of immersive experiences and collaborative interactions, developing leadership capability over a fourteen-month period. The program is built around a series of best-in-class leadership principles and their application by participants as they lead their current teams.

•The Business of Banking is a year-long set of presentations for new colleagues and early career program participants to share resources and experiences designed to help colleagues explore our history and engage in shaping our future.

•1st Source Mastery Programs provide a deep dive into skill development and mastery of specific roles to enhance role competencies and increase levels of overall performance. These mastery programs are designed to deliver increased levels of outstanding client service by our colleagues, continually differentiating our service above our competitors over time. They also increase talent/diversity attraction, engagement, and retention for the long term.

•The Commercial Banker Development Program is a two-year rotational program for recent college graduates designed to expose participants to fundamentals of commercial banking, including the funding and pricing of commercial loans, credit analysis and relationship sales.

•The Customer Service Representative Career Development Program is a structured approach to developing and improving one’s career serving clients in our Banking Centers.

•The Tuition Reimbursement Program reflects our philosophy of continuous learning and provides for reimbursement of tuition related expenses incurred through approved and accredited public and private not-for-profit institutions of higher education.

•The IVY Tech Bank Cohort Education Program was developed and made available through a partnership between the Company and IVY Tech Community College to provide opportunities for obtaining a college degree among colleagues in the hourly and lower-level salaried workforce. This newly developed program has been an important investment in education and has an undeniable jumpstart effect. We have moved from a low of 16 colleagues attending eight colleges and universities in the year prior to the program creation, to now almost 50 colleagues who are attending 22 different schools. Many in our first cohort of students have gone on to obtain their bachelor’s degree and found success in new growth opportunities at 1st Source.

•The Banking Apprentice Program attracts locally embedded diverse high school graduates and rising seniors to work for the Company and experience the pride and fulfillment to be found in serving others and introduce them to the business of banking.

•New Employee Orientation introduces new colleagues to our history, vision, mission, and values.

•We engage in talent review and succession planning continuously but engage in a formal review annually to reaffirm existing and identify new high potential, talented and diverse colleagues as we strive to deepen, enhance, and diversify our leadership bench. We then implement multi-year individual development plans for these colleagues which include special assignments, structured learning, assessments, external coaching, sponsorship and hands-on work, and a blend of full cohort, small group, and individually tailored development opportunities.

•As noted above, all employees in 2021 completed a multi-module unconscious bias training program which gave us an opportunity to collectively work together to identify and address our biases that will improve our interactions and make us a stronger organization.

REGULATION AND SUPERVISION

General — 1st Source and the Bank are extensively regulated under federal and state law. To the extent the following information describes statutory or regulatory provisions, it is qualified in its entirety by reference to the particular statutory and regulatory provisions. Any change in applicable laws or regulations may have a material effect on our existing and prospective business and operations. We are unable to predict the nature or the extent of the effects on our business, operations and earnings that fiscal or monetary policies, economic controls, or new federal or state legislation or regulation may have in the future.

We are a registered bank holding company under the Bank Holding Company Act of 1956, as amended (BHCA), and, as such, we are subject to regulation, supervision, and examination by the Board of Governors of the Federal Reserve System (Federal Reserve). We are required to file annual reports with the Federal Reserve and to provide the Federal Reserve such additional information as it may require.

6

The Bank, as an Indiana state bank and member of the Federal Reserve System, is subject to prudential supervision by the Indiana Department of Financial Institutions (DFI) and the Federal Reserve Bank of Chicago (FRB Chicago). As such, 1st Source Bank is regularly examined by and subject to regulations promulgated by the DFI and the Federal Reserve. Because the Federal Deposit Insurance Corporation (FDIC) provides deposit insurance to the Bank, we are also subject to supervision and regulation by the FDIC (even though the FDIC is not our primary Federal regulator). The Bank is also subject to regulations promulgated by the Consumer Financial Protection Bureau (CFPB) and to supervision for compliance with such regulations by the DFI and the FRB Chicago.

Bank Holding Company Act — Under the BHCA our activities are limited to (i) business so closely related to banking, managing, or controlling banks as to be a proper incident thereto and (ii) non-bank activities, determined by law or regulation, to be closely related to the business of banking or of managing or controlling banks. We are also subject to capital requirements applied on a consolidated basis in a form substantially similar to those required of the Bank. The BHCA also requires a bank holding company to obtain approval from the Federal Reserve before (i) acquiring, or holding more than 5% voting interest in any bank or bank holding company, (ii) acquiring all or substantially all of the assets of another bank or bank holding company, or (iii) merging or consolidating with another bank holding company.

Capital Standards — The federal bank regulatory agencies use capital adequacy guidelines in their examination and regulation of bank holding companies and banks. If capital falls below the minimum levels established by these guidelines, a bank holding company or bank must submit an acceptable plan for achieving compliance with the capital guidelines and, until its capital sufficiently improves, will be subject to denial of applications and appropriate supervisory enforcement actions. For banks, the FDIC’s prompt corrective action regulations establish five capital levels for financial institutions (“well capitalized,” “adequately capitalized,” “undercapitalized,” “significantly undercapitalized,” and “critically undercapitalized”), and impose mandatory regulatory scrutiny and limitations on institutions that are less than adequately capitalized. At December 31, 2021, the Bank was categorized as “well capitalized,” meaning that our total risk-based capital ratio exceeded 10.00%, our Tier 1 risk-based capital ratio exceeded 8.00%, our common equity Tier 1 risk-based capital ratio exceeded 6.50%, our leverage ratio exceeded 5.00%, and we are not subject to a regulatory order, agreement, or directive to meet and maintain a specific capital level for any capital measure. The various regulatory capital requirements that we are subject to are disclosed in Part II, Item 8, Financial Statements and Supplementary Data — Note 20 of the Notes to Consolidated Financial Statements.

As of December 31, 2021, we were in compliance with all applicable regulatory capital requirements and guidelines.

In September 2019, the Federal Reserve and other federal banking agencies adopted a final rule, effective January 1, 2020, creating a community bank leverage ratio (“CBLR”) for institutions with total consolidated assets of less than $10 billion and that meet other qualifying criteria. The CBLR provides for a simple measure of capital adequacy for qualifying institutions. Qualifying institutions that elect to use the CBLR framework and that maintain a leverage ratio of greater than 9% will be considered to have satisfied the generally applicable risk-based and leverage capital requirements in the regulatory agencies’ capital rules and to have met the well-capitalized ratio requirements. Management reviewed the CBLR framework and has determined that 1st Source and the Bank will not elect to use the CBLR framework.

Securities and Exchange Commission (SEC) and The NASDAQ Stock Market (NASDAQ) — We are also subject to regulations promulgated by the SEC and certain state securities commissions for matters relating to the offering and sale of our securities. We are subject to the disclosure and regulatory requirements of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended, as administered by the SEC. We are listed on the NASDAQ Global Select Market under the trading symbol “SRCE,” and we are subject to the rules of NASDAQ for listed companies.

Gramm-Leach-Bliley Act of 1999 — The GLBA expanded the types of financial activities a bank may conduct through a financial subsidiary and established a distinct type of bank holding company, known as a financial holding company, which may engage in an expanded list of activities that are “financial in nature.” These activities include securities and insurance brokerage, securities underwriting, insurance underwriting, and merchant banking. We do not currently intend to file notice with the Federal Reserve to become a financial holding company or to engage in expanded financial activities through a financial subsidiary of the Bank.

Financial Privacy — The GLBA also includes privacy protections for nonpublic personal information held by financial institutions regarding their customers. In accordance with the GLBA, Federal banking regulators adopted rules that limit the ability of banks and other financial institutions to disclose non-public information about customers to nonaffiliated third parties. These limitations require disclosure of privacy policies to consumers and, in some circumstances, allow consumers to prevent disclosure of certain personal information to a nonaffiliated third party. The privacy provisions of the GLBA affect how consumer information is transmitted through diversified financial companies and conveyed to outside vendors. We are also subject to various state laws, including the recently enacted California Consumer Privacy Act, that generally require us (directly or indirectly through our vendors) to protect the personal information of individual customers and notify them if confidentiality of their personal information is or may have been compromised as the result of a data security breach or failure.

7

USA Patriot Act of 2001 — The USA Patriot Act of 2001 (USA Patriot Act) substantially broadened the scope of anti-money laundering laws and regulations by imposing significant new compliance and due diligence obligations on financial institutions. The regulations adopted by the Treasury under the USA Patriot Act require financial institutions to maintain appropriate controls to combat money laundering activities, perform due diligence of private banking and correspondent accounts, establish standards for verifying customer identity, and provide records related to suspected anti-money laundering activities upon request from federal authorities. A financial institution’s failure to comply with these regulations could result in fines or sanctions, including restrictions on conducting acquisitions or establishing new branches, and could also have other serious legal and reputational consequences for the institution. We have established policies, procedures and systems designed to comply with these regulations.

Community Reinvestment Act — The Community Reinvestment Act of 1977 requires that, in connection with examinations of financial institutions within their jurisdiction, the federal banking regulators must evaluate the record of the financial institutions in meeting the credit needs of their local communities, including low and moderate income neighborhoods, consistent with the safe and sound operation of those banks. Federal banking regulators are required to consider a financial institution’s performance in these areas as they review applications filed by the institution to engage in mergers or acquisitions or to open a branch or facility.

Laws and Regulations Governing Extensions of Credit — The Bank is subject to certain restrictions imposed by the Federal Reserve Act on extensions of credit to 1st Source or our subsidiaries, and on investments in our securities and the use of our securities as collateral for loans to any borrowers. These restrictions may limit our ability to obtain funds from the Bank for our cash needs, including funds for acquisitions and for payment of dividends, interest and operating expenses. Further, the BHCA, certain regulations issued by the Federal Reserve, state laws and many other federal laws govern extensions of credit and generally prohibit a bank from extending credit, engaging in a lease or sale of property, or furnishing services to a customer on condition that the customer request and obtain additional services from the bank’s holding company or from one of its subsidiaries.

The Bank is also subject to numerous restrictions imposed by the Federal Reserve Act on extensions of credit to insiders of 1st Source and/or the Bank – executive officers, directors, principal shareholders, or any related interest of such persons.

Reserve Requirements — The Federal Reserve requires all depository institutions to maintain reserves against their transaction account deposits. For all net transaction accounts in 2021, the reserve requirement ratio was set to zero percent in March 2020; therefore, all net transaction accounts are exempt from reserve requirements.

Dividends — The ability of the Bank to pay dividends is limited by state and federal laws and regulations that require the Bank to obtain the prior approval of the DFI and the FRB Chicago before paying a dividend that, together with other dividends it has paid during a calendar year, would exceed the sum of its net income for the year to date combined with its retained net income for the previous two years. The amount of dividends the Bank may pay may also be limited by certain covenant agreements and by the principles of prudent bank management. See Part II, Item 5, Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities for further discussion of dividend limitations.

Monetary Policy and Economic Control — The commercial banking business in which we engage is affected not only by general economic conditions, but also by the monetary policies of the Federal Reserve. Changes in the discount rate on member bank borrowing, availability of borrowing at the “discount window,” open market operations, the imposition of changes in reserve requirements against member banks’ deposits and assets of foreign branches, and the imposition of, and changes in, reserve requirements against certain borrowings by banks and their affiliates, are some of the tools of monetary policy available to the Federal Reserve. These monetary policies are used in varying combinations to influence overall growth and distributions of bank loans, investments, and deposits, and such use may affect interest rates charged on loans and leases or paid on deposits. The monetary policies of the Federal Reserve have had a significant effect on the operating results of commercial banks and are expected to do so in the future. The monetary policies of the Federal Reserve are influenced by various factors, including economic growth, inflation, unemployment, short-term and long-term changes in the international trade balance, and in the fiscal policies of the U.S. Government. Future monetary policies and the effect of such policies on our future business and earnings, and the effect on the future business and earnings of the Bank cannot be predicted.

Sarbanes-Oxley Act of 2002 — The Sarbanes-Oxley Act of 2002 (SOA) includes provisions intended to enhance corporate responsibility and protect investors by improving the accuracy and reliability of corporate disclosures pursuant to the securities laws, and which increase penalties for accounting and auditing improprieties at public traded companies. The SOA generally applies to all companies, including 1st Source, that file or are required to file periodic reports with the SEC under the Exchange Act.

8

Among other things, the SOA also addresses functions and responsibilities of audit committees of public companies. The statute, by mandating certain stock exchange listing rules, makes the audit committee directly responsible for the appointment, compensation, and oversight of the work of the company’s outside auditor, and requires the auditor to report directly to the audit committee. The SOA authorizes each audit committee to engage independent counsel and other advisors, and requires a public company to provide the appropriate funding, as determined by its audit committee, to pay the company’s auditors and any advisors that its audit committee retains.

Consumer Financial Protection Laws — The Bank is subject to numerous federal and state consumer financial protection laws and regulations that extensively govern its transactions with consumers. These laws include, but are not limited to, the Equal Credit Opportunity Act, the Fair Credit Reporting Act, the Truth in Lending Act, the Truth in Savings Act, the Electronic Funds Transfer Act, the Expedited Funds Availability Act, the Home Mortgage Disclosure Act, the Fair Housing Act, the Real Estate Settlement Procedures Act, the Fair Debt Collection Practices Act, and the Service Members Civil Relief Act. The Bank must also comply with applicable state usury and other credit and deposit related laws and regulations and other laws and regulations prohibiting unfair, deceptive and abusive acts and practices. These laws and regulations, among other things, require disclosures of the cost of credit and the terms of deposit accounts, prohibit discrimination in credit transactions, regulate the use of credit report information, restrict the Bank’s ability to raise interest rates and subject the Bank to substantial regulatory oversight. Violations of these laws may expose us to liability from potential lawsuits brought by affected customers. Federal bank regulators, state attorneys general and state and local consumer protection agencies may also seek to enforce these consumer financial protection laws, in which case we may be subject to regulatory sanctions, civil money penalties, and customer rescission rights. Failure to comply with these laws may also cause the Federal Reserve or DFI to deny approval of any applications we may file to engage in merger and acquisition transactions with other financial institutions or open a new banking center.

Dodd-Frank Wall Street Reform and Consumer Protection Act — The Dodd-Frank Act, which was signed into law in 2010, significantly changed the regulation of financial institutions and the financial services industry. The Dodd-Frank Act includes provisions affecting large and small financial institutions alike, including several provisions that profoundly affected the regulation of community banks, thrifts, and small bank and thrift holding companies. Among other things, these provisions relax rules on interstate branching, allow financial institutions to pay interest on business checking accounts, and impose heightened capital requirements on bank and thrift holding companies. The Dodd-Frank Act also includes several corporate governance provisions that apply to all public companies, not just financial institutions. These include provisions mandating certain disclosures regarding executive compensation and provisions addressing proxy access by shareholders.

The Dodd-Frank Act also establishes the CFPB as an independent entity within the Federal Reserve, and the Act transferred to the CFPB primary responsibility for administering substantially all of the consumer compliance protection laws formerly administered by other federal agencies. The Dodd-Frank Act also authorizes the CFPB to promulgate consumer protection regulations that will apply to all entities, including banks, that offer consumer financial services or products. It also includes a series of provisions covering mortgage loan origination standards affecting, among other things, originator compensation, minimum repayment standards, and pre-payment penalties.

The Dodd-Frank Act contains numerous other provisions affecting financial institutions of all types, including some that may affect our business in substantial and unpredictable ways. We have incurred higher operating costs in complying with the Dodd -Frank Act, and we expect that these higher costs will continue for the foreseeable future. Our management continues to monitor the ongoing implementation of the Dodd-Frank Act and as new regulations are issued, will assess their effect on our business, financial condition, and results of operations.

The Volcker Rule — The Dodd-Frank Act prohibits banks and their affiliates from engaging in proprietary trading and from investing and sponsoring hedge funds and private equity funds. The provision of the statute imposing these restrictions is commonly called the “Volcker Rule.” The regulations implementing the Volcker Rule exempt the Bank, as a bank with less than $10 billion in total consolidated assets that does not engage in any covered activities other than trading in certain government, agency, state or municipal obligations, from any significant compliance obligations under the Volcker Rule.

Pending Legislation — Because of concerns relating to competitiveness and the safety and soundness of the banking industry, Congress often considers a number of wide-ranging proposals for altering the structure, regulation, and competitive relationships of the nation’s financial institutions. We cannot predict whether or in what form any proposals will be adopted or the extent to which our business may be affected.

Item 1A. Risk Factors.

An investment in our common stock is subject to risks inherent to our business. The material risks and uncertainties that we believe affect us are described below. See “Forward Looking Statements” under Item 7 of this report for a discussion of other important factors that can affect our business.

9

Credit Risks

We are subject to credit risks relating to our loan and lease portfolios — We have certain lending policies and procedures in place that are designed to optimize loan and lease income within an acceptable level of risk. Our management reviews and approves these policies and procedures on a regular basis. A reporting system supplements the review process by providing our management with frequent reports related to loan and lease production, loan quality, concentrations of credit, loan and lease delinquencies, and nonperforming and potential problem loans and leases. Diversification in the loan and lease portfolios is a means of managing risk associated with fluctuations in economic conditions.

We maintain an independent loan review department that reviews and validates the credit risk program on a periodic basis. Results of these reviews are presented to our management. The loan and lease review process complements and reinforces the risk identification and assessment decisions made by lenders and credit personnel, as well as our policies and procedures.

Commercial and commercial real estate loans generally involve higher credit risks than residential real estate and consumer loans. Because payments on loans secured by commercial real estate or equipment are often dependent upon the successful operation and management of the underlying assets, repayment of such loans may be influenced to a great extent by conditions in the market or the economy. We seek to minimize these risks through our underwriting standards. We obtain financial information and perform credit risk analysis on our customers. Credit criteria may include, but are not limited to, assessments of income, cash flows, collateral, and net worth; asset ownership; bank and trade credit references; credit bureau reports; and operational history.

Commercial real estate or equipment loans are underwritten after evaluating and understanding the borrower’s ability to operate profitably and generate positive cash flows. Our management examines current and projected cash flows of the borrower to determine the ability of the borrower to repay their obligations as agreed. Underwriting standards are designed to promote relationship banking rather than transactional banking. Most commercial and industrial loans are secured by the assets being financed or other business assets; however, some loans may be made on an unsecured basis. Our credit policy sets different maximum exposure limits both by business sector and our current and historical relationship and previous experience with each customer.

We offer both fixed-rate and adjustable-rate consumer mortgage loans secured by properties, substantially all of which are located in our primary market area. Adjustable-rate mortgage loans help reduce our exposure to changes in interest rates; however, during periods of rising interest rates, the risk of default on adjustable-rate mortgage loans may increase as a result of repricing and the increased payments required from the borrower. Additionally, some residential mortgages are sold into the secondary market and serviced by our principal banking subsidiary, 1st Source Bank.

Consumer loans are primarily all other non-real estate loans to individuals in our regional market area. Consumer loans can entail risk, particularly in the case of loans that are unsecured or secured by rapidly depreciating assets. In these cases, any repossessed collateral may not provide an adequate source of repayment of the outstanding loan balance. The remaining deficiency often does not warrant further substantial collection efforts against the borrower beyond obtaining a deficiency judgment. In addition, consumer loan collections are dependent on the borrower’s continuing financial stability, and thus are more likely to be adversely affected by job loss, divorce, illness, or personal bankruptcy.

The 1st Source Specialty Finance Group loan and lease portfolio consists of commercial loans and leases secured by construction and transportation equipment, including aircraft, autos, trucks, and vans. Finance receivables for this Group generally provide for monthly payments and may include prepayment penalty provisions.

Our construction and transportation related businesses could be adversely affected by slowdowns in the economy. Clients who rely on the use of assets financed through the Specialty Finance Group to produce income could be negatively affected, and we could experience substantial loan and lease losses. By the nature of the businesses these clients operate in, we could be adversely affected by rapid increases or decreases in fuel costs, terrorist and other potential attacks, and other destabilizing events. These factors could contribute to the deterioration of the quality of our loan and lease portfolio, as they could have a negative impact on the travel and transportation sensitive businesses for which our specialty finance businesses provide financing.

Our aircraft portfolio has foreign exposure, particularly in Mexico and Brazil. We establish exposure limits for each country through a centralized oversight process, and in consideration of relevant economic, political, social and legal risks. We monitor exposures closely and adjust our country limits in response to changing conditions. Currency fluctuations could have a negative impact on our client’s cost of paying dollar denominated debts and, as a result, we could experience higher delinquency in this portfolio. Also, since some of the relationships in this portfolio are large, a slowdown in these markets could have a significant adverse impact on our performance.

10

In addition, our leasing and equipment financing activity is subject to the risk of cyclical downturns, industry concentration and clumping, and other adverse economic developments affecting these industries and markets. This area of lending, with transportation in particular, is dependent upon general economic conditions and the strength of the travel, construction, and transportation industries.

Our allowance for credit losses may prove to be insufficient to absorb losses in our loan and lease portfolio — In the financial services industry, there is always a risk that certain borrowers may not repay borrowings. The determination of the appropriate level of the allowance for credit losses inherently involves a high degree of subjectivity and requires us to make significant estimates of current credit risks and future trends, all of which may undergo material changes. Our allowance for credit losses may not be sufficient to cover the loan and lease losses that we may actually incur. If we experience defaults by borrowers in any of our businesses, our earnings could be negatively affected. Changes in local economic conditions could adversely affect credit quality, particularly in our local business loan and lease portfolio. Changes in national or international economic conditions could also adversely affect the quality of our loan and lease portfolio and negate, to some extent, the benefits of national or international diversification through our Specialty Finance Group’s portfolio. In addition, bank regulatory agencies periodically review our allowance for credit losses and may require an increase in the provision for credit losses or the recognition of further loan or lease charge-offs based upon their judgments, which may be different from ours.

The soundness of other financial institutions could adversely affect us — Financial services institutions are interrelated as a result of trading, clearing, counterparty, or other relationships. We have exposure to many different industries and counterparties, and we routinely execute transactions with counterparties in the financial services industry, including commercial banks, brokers and dealers, investment banks, and other institutional clients. Many of these transactions expose us to credit risk in the event of a default by our counterparty or client. In addition, our credit risk may be exacerbated when the collateral held by us cannot be realized or is liquidated at prices not sufficient to recover the full amount of the credit or derivative exposure due us. Any such losses could have a material adverse effect on our financial condition and results of operations.

We may be adversely affected by climate change and related legislative and regulatory initiatives — Political and social attention to the issue of climate change has increased. Federal and state legislatures and regulatory agencies continue to propose and advance numerous legislative and regulatory initiatives seeking to mitigate the effects of climate change. As a financial institution, it is unclear how future governmental regulations and shifts in business trends resulting from increased concern about climate change will affect our operations; however, natural or man-made disasters and severe weather events may cause operational disruptions and damage to both our properties and properties securing our loans. Losses resulting from these disasters and severe weather events may make it more difficult for borrowers to timely repay their loans. Additionally, our customers who finance vehicles and equipment reliant on fossil fuels could face cost increases, asset value reductions, operating process changes, and the like. If these events occur, we may experience a decrease in the value of our loan and lease portfolio and our revenue, and may incur additional operational expenses, each of which could have a material adverse effect on our financial condition and results of operations.

Market Risks

We may be adversely affected by the world-wide coronavirus (COVID-19) pandemic — The coronavirus (COVID-19) outbreak that began during 2020 has continued to have an adverse impact on certain of our customers directly or indirectly. Entire industries within our loan and lease portfolio such as buses, auto rental and hotels were immediately impacted due to reduced demand related to quarantines and travel re strictions. Other industries within our loan and lease portfolio or the communities we serve are likely to experience similar prolonged disruptions and economic hardships as the current coronavirus pandemic persists. In addition, such events affect the stability of our deposit base, lead to mass layoffs and furloughs which could impair the ability of borrowers to repay outstanding loans, impair the value of collateral securing loans, result in lost revenue or cause us to incur additional expenses.

Additionally, the Federal Reserve reduced interest rates substantially during 2020 in an attempt to boost consumer spending due to the coronavirus pandemic which could have a sustained negative impact on our results of operations. Pandemic related disruptions in labor markets and upended global supply chains have led to the emergence of high inflation which may not subside until societies feel assured future outbreaks can be reasonably contained.

Even with operational precautions we have implemented such as mask utilization, social distancing and disinfection of surfaces, the continued spread or prolonged impact of the coronavirus could negatively impact the availability of key personnel or significant numbers of our staff, who are necessary to conduct our business. Such a continued spread or outbreak could also impact the business and operations of third party service providers who perform critical services for our business. Similarly, the adverse impacts already seen by our commercial and retail customers from the pandemic, may be exacerbated or more prolonged than we currently anticipate. If new coronavirus variants continue to form and spread and containment and mitigation responses are unable to curtail the global impact of the coronavirus pandemic for a prolonged period of time, we could experience a material adverse effect on our business, financial condition, and results of operations.

11

Fluctuations in interest rates could reduce our profitability and affect the value of our assets — Like other financial institutions, we are subject to interest rate risk. Our primary source of income is net interest income, which is the difference between interest earned on loans and leases and investments, and interest paid on deposits and borrowings. We expect that we will periodically experience imbalances in the interest rate sensitivities of our assets and liabilities and the relationships of various interest rates to each other. Over any defined period of time, our interest-earning assets may be more sensitive to changes in market interest rates than our interest-bearing liabilities, or vice-versa. In addition, the individual market interest rates underlying our loan and lease and deposit products may not change to the same degree over a given time period. If market interest rates should move contrary to our position, earnings may be negatively affected. In addition, loan and lease volume and quality and deposit volume and mix can be affected by market interest rates as can the businesses of our clients. Changes in levels of market interest rates could have a material adverse effect on our net interest spread, asset quality, origination volume, and overall profitability. Additionally, changes in levels of market interest rates could cause our debt securities available-for-sale to move into unrealized loss positions which is a negative component of total shareholders’ equity.

Market interest rates are beyond our control, and they fluctuate in response to general economic conditions and the policies of various governmental and regulatory agencies, in particular, the Federal Reserve Board. Changes in monetary policy, including changes in interest rates, may negatively affect our ability to originate loans and leases, the value of our assets and our ability to realize gains from the sale of our assets, all of which ultimately could affect our earnings.

Adverse changes in economic conditions could impair our financial condition and results of operations — We are impacted by general business and economic conditions in the United States and abroad. These conditions include short-term and long-term interest rates, inflation, money supply, political issues, legislative and regulatory changes, fluctuations in both debt and equity capital markets, broad trends in industry and finance, unemployment, infectious disease epidemics or outbreaks and the strength of the U.S. economy and the local economies in which we operate, all of which are beyond our control. A deterioration in economic conditions could result in an increase in loan delinquencies and non-performing assets, decreases in loan collateral values and a decrease in demand for our products and services.

Changes in economic conditions may negatively impact the fees generated by our trust and wealth advisory business — Trust and wealth advisory fees are largely based on the size of client relationships and the market value of assets held under management. Changes in general economic conditions and in the financial and securities markets may negatively impact the value of our clients’ wealth management accounts and the market value of assets held under management. Market declines, reductions in the value of our clients’ accounts, and the loss of wealth management clients may negatively impact the fees generated by our trust and wealth management business and could have an adverse effect on our business, financial condition and results of operations.

We may be adversely impacted by the transition away from LIBOR as a reference interest rate — The London Interbank Offered Rate (“LIBOR”) is a short-term interest rate used as a pricing reference for loans, derivatives and other financial instruments. In July 2017, the United Kingdom Financial Conduct Authority, which regulates the process for establishing LIBOR, announced that it intends to stop persuading or compelling banks to submit rates for the calculation of LIBOR after 2021. In November 2020, the Federal Reserve, FDIC and OCC issued a joint statement confirming that the lesser used one-week and two-month USD LIBOR settings would cease publication at the end of 2021, but the remaining USD LIBOR settings would continue publication until June 30, 2023 to better facilitate an orderly transition. The agencies also stated that the act of entering into new contracts that use USD LIBOR as a reference rate after December 31, 2021 would create safety and soundness risks. The exact impact this ongoing transition will have on financial markets and their individual participants is not currently known. Various substitute benchmarks are developing in the marketplace but at this time it is not feasible to predict exactly which of these will emerge as enduring substitutes for LIBOR.

We convened a transition committee in 2019 to monitor market developments and implement a transition plan. Existing loans impacted by the transition are actively tracked, appropriate legal fallback language has been created and incorporated into documentation where appropriate and we are an adhering party to the ISDA IBOR Fallbacks Protocol. In 2021, we began to utilize other interest rate benchmarks to remain in alignment with the regulatory prohibitions of originating LIBOR-denominated loans in 2022, and are continuing our transition efforts.

As of December 31, 2021, we have approximately $1.1 billion of loans and other financial instruments with attributes that are either directly or indirectly influenced by LIBOR. The impact of the transition away from LIBOR may adversely affect revenues, expenses and the value of those financial instruments. Such transition could result in litigation with counterparties impacted by the transition as well as increased regulatory scrutiny and other adverse consequences. Any replacement benchmark ultimately adopted as a substitute for LIBOR may behave differently than LIBOR in a manner detrimental to our financial performance. Although we are currently unable to assess what the ultimate impact of the transition from LIBOR will be, failure to adequately manage the transition could have a material adverse effect on our business, financial condition and results of operation.

12

Liquidity Risks

We could experience an unexpected inability to obtain needed liquidity — Liquidity measures the ability to meet current and future cash flow needs as they become due. The liquidity of a financial institution reflects its ability to meet loan requests, to accommodate possible outflows in deposits, and to take advantage of interest rate market opportunities and is essential to a financial institution’s business. The ability of a financial institution to meet its current financial obligations is a function of its balance sheet structure, its ability to liquidate assets, and its access to alternative sources of funds. We seek to ensure our funding needs are met by maintaining a level of liquidity through asset and liability management. If we become unable to obtain funds when needed, it could have a material adverse effect on our business, financial condition, and results of operations. Additionally, under Indiana law governing the collateralization of public fund deposits, the Indiana Board for Depositories determines which financial institutions are required to pledge collateral based on the strength of their financial ratings. We have been informed that no collateral is required for our public fund deposits. However, the Board of Depositories could alter this requirement in the future, which could adversely affect our liquidity depending on the amount of collateral we may be required to pledge.

We rely on dividends from our subsidiaries — We receive substantially all of our revenue from dividends from our subsidiaries, including, primarily, the Bank. These dividends are the principal source of funds we use to pay dividends on our common stock and interest and principal on our debt. Various federal and state laws and regulations limit the amount of dividends our subsidiaries may pay to us. In the event our subsidiaries are unable to pay dividends to us, we may not be able to service debt, pay other obligations, or pay dividends on our common stock. Our inability to receive dividends from our subsidiaries could have a material adverse effect on our business, financial condition and results of operations.

Operational Risks

Our risk management framework could prove ineffective which could have a material adverse effect on our ability to mitigate risks and/or losses — We have established a risk management framework to identify and manage our risk exposure. This framework is comprised of various processes, systems and strategies, and is designed to manage the types of risk to which we are subject, including, credit, market, liquidity, operational, legal/compliance, and reputational risks. Our framework also includes financial, analytical and forecasting modeling methodologies which involve significant management assumptions and judgment that may not be accurate, particularly in times of market stress or other unforeseen circumstances. Additionally, our Board of Directors has adopted a risk appetite statement in consultation with management which sets forth certain thresholds and limits to govern our overall risk profile. There can be no assurance that our risk management framework will be effective under all circumstances or that it will adequately identify, manage or limit any risk of loss to us. Any such failure in our risk management framework could have a material adverse effect on our business, financial condition, and results of operations.

We are dependent upon the services of our management team — Our future success and profitability is substantially dependent upon our management and the banking acumen of our senior executives. We believe that our future results will also depend in part upon our ability to attract and retain highly skilled and qualified management. We are especially dependent on a limited number of key management personnel, many of whom do not have employment agreements with us. The loss of the chief executive officer and other senior management and key personnel could have a material adverse impact on our operations because other officers may not have the experience and expertise to readily replace these individuals. Many of these senior officers have primary contact with our clients and are important in maintaining personalized relationships with our client base. The unexpected loss of services of one or more of these key employees could have a material adverse effect on our operations and possibly result in reduced revenues if we were unable to find suitable replacements promptly. Competition for senior personnel is intense, and we may not be successful in attracting and retaining such personnel. Changes in key personnel and their responsibilities may be disruptive to our businesses and could have a material adverse effect on our businesses, financial condition, and results of operations.

Technology security breaches — Information security risks have increased due to the sophistication and activities of organized crime, hackers, terrorists and other external parties and the use of online, telephone, and mobile banking channels by clients. Any compromise of our security could deter our clients from using our banking services. We rely on security systems to provide the protection and authentication necessary to secure transmission of data against damage by theft, fire, power loss, telecommunications failure or similar catastrophic event, as well as from security breaches, ransomware, denial of service attacks, viruses, worms, and other disruptive problems caused by hackers. Computer break-ins, phishing and other disruptions of customer or vendor systems could also jeopardize the security of information stored in and transmitted through our computer systems and network infrastructure. We maintain a cyber insurance policy that is designed to cover a majority of loss resulting from cyber security breaches, but there is no assurance such coverage will be adequate to address all potential material adverse impacts.

13

We also confront the risk of being compromised by emails sent by perpetrators posing as company executives or vendors in order to dupe company personnel into sending large sums of money to accounts controlled by the perpetrators. We require all our employees to complete annual information security awareness training to increase their awareness of these risks and to engage them in our mitigation efforts. If these precautions are not sufficient to protect our systems from data breaches or compromises, our reputation and business could be adversely affected.

We depend on the services of a variety of third-party vendors to meet data processing and communication needs and we have contracted with third parties to run their proprietary software on our behalf. While we perform reviews of security controls instituted by the vendor in accordance with industry standards and institute our own internal security controls, we rely on continued maintenance of the controls by the outside party to safeguard our customer data.

Additionally, we issue debit cards which are susceptible to compromise at the point of sale via the physical terminal through which transactions are processed and by other means of hacking. The security and integrity of these transactions are dependent upon the retailers’ vigilance and willingness to invest in technology and upgrades. Issuing debit cards to our clients exposes us to potential losses which, in the event of a data breach at one or more major retailers may adversely affect our business, financial condition, and results of operations.

We continually encounter technological change — The financial services industry is constantly undergoing rapid technological change with frequent introductions of new technology-driven products and services. The effective use of technology increases efficiency and enables financial institutions to better service clients and reduce costs. Our future success depends, in part, upon our ability to address the needs of our clients by using technology to provide products and services that will satisfy client demands, as well as create additional efficiencies within our operations. Many of our large competitors have substantially greater resources to invest in technological improvements. We may not be able to effectively implement new technology-driven products and services quickly or be successful in marketing these products and services to our clients. Failure to successfully keep pace with technological change affecting the financial services industry could have a material adverse impact on our business and, in turn, our financial condition and results of operations.

Our accounting estimates rely on analytical and forecasting models — The processes we use to estimate our allowance for credit losses and to measure the fair value of financial instruments, as well as the processes used to estimate the effects of changing interest rates and other market measures on our financial condition and results of operations, depend upon the use of analytical and forecasting models. These models reflect assumptions that may not be accurate, particularly in times of market stress or other unforeseen circumstances. Even if these assumptions are adequate, the models may prove to be inadequate or inaccurate because of other flaws in their design or their implementation. Any such failure in our analytical or forecasting models could have a material adverse effect on our business, financial condition and results of operations.

Legal/Compliance Risks

We are subject to extensive government regulation and supervision — Our operations are subject to extensive federal and state regulation and supervision. Banking regulations are primarily intended to protect depositors’ funds, federal deposit insurance funds and the banking system as a whole, not security holders. These regulations affect our lending practices, capital structure, investment practices, dividend policy and growth, among other things. Congress and federal regulatory agencies continually review banking laws, regulations and policies for possible change. Changes to statutes, regulations or regulatory policies, including changes in interpretation or implementation of statutes, regulation or policies, could affect us in substantial and unpredictable ways. Such changes could subject us to additional costs and limit the types of financial services and products we may offer. Failure to comply with laws, regulations or policies could result in sanctions by regulatory agencies, civil money penalties and/or reputation damage, which could have a material adverse effect on our business, financial condition and results of operations. While we have policies and procedures designed to prevent any such violations, there can be no assurance that such violations will not occur.

Our investments and/or financings in certain tax-advantaged projects may not generate returns as anticipated and may have an adverse impact on our financial results — We invest and/or finance certain tax-advantaged projects promoting affordable housing, community redevelopment and renewable energy sources. Our investments in these projects are designed to generate a return primarily through the realization of federal and state income tax credits, and other tax benefits, over specified time periods. We are subject to the risk that previously recorded tax credits will not be able to be fully realized. Such credits are subject to recapture by taxing authorities based on compliance features required to be met at the project level which may not be met. The possible inability to realize these tax credits and other tax benefits can have a negative impact on our financial results. The risk of not being able to realize the tax credits and other tax benefits depends on many factors outside of our control, including changes in the applicable tax code and the ability of the projects to be completed and properly managed.

Substantial ownership concentration — Our directors, executive officers and 1st Source Bank, as trustee, collectively hold a significant ownership concentration of our common shares. Due to this significant level of ownership among our affiliates, our directors, executive officers, and 1st Source Bank, as trustee, may be able to influence the outcome of director elections or impact significant transactions, such as mergers or acquisitions, or any other matter that might otherwise be favored by other shareholders.

14

Reputational Risks

Competition from other financial services providers could adversely impact our results of operations — The banking and financial services business is highly competitive. We face competition in making loans and leases, attracting deposits and providing insurance, investment, trust and wealth advisory, and other financial services. Increased competition in the banking and financial services businesses may reduce our market share, impair our growth or cause the prices we charge for our services to decline. Our results of operations may be adversely impacted in future periods depending upon the level and nature of competition we encounter in our various market areas.

Managing reputational risk is important to attracting and maintaining customers, investors, and employees — Threats to our reputation can come from many sources, including adverse sentiment about financial institutions generally, unethical practices, employee misconduct, failure to deliver minimum standards of service or quality, compliance deficiencies, and questionable or fraudulent activities of our customers. We have policies and procedures in place that seek to protect our reputation and promote ethical conduct. Nonetheless, negative publicity may arise regarding our business, employees, or customers, with or without merit, and could result in the loss of customers, investors, or employees, costly litigation, a decline in revenues, and increased government regulation.

In addition, increased focus on environmental, social and governance (“ESG”) issues could damage our reputation or prospects. Customers, prospective customers, investors or third parties assigning ESG ratings may believe that our practices, including our lending practices, are not sufficiently robust from an ESG perspective.

Item 1B. Unresolved Staff Comments.

None

Item 2. Properties.

Our headquarters building is located in downtown South Bend, Indiana. The building is part of a larger complex, including a 300-room hotel and a 500-car parking garage. In September 2019, we extended the lease on this property through September 2027. As of December 31, 2021, 1st Source leases approximately 71% of the office space in this complex.

At December 31, 2021, we owned or leased property and/or buildings where 1st Source Bank’s 79 banking centers were located. Our facilities are located in Allen, DeKalb, Elkhart, Fulton, Huntington, Kosciusko, LaPorte, Marshall, Porter, Pulaski, St. Joseph, Starke, Tippecanoe, Wells, and Whitley Counties in the State of Indiana, Berrien, Cass, and Kalamazoo Counties in the State of Michigan, and Sarasota County in the state of Florida. 1st Source Bank also owns approximately 35 acres in St. Joseph County of which approximately 29 acres have been approved by the Board for development and construction of an operations and training facility. We are marketing the remaining six acres for sale. We anticipate moving forward with construction in 2022 subject to receiving appropriate agreements, approvals and authorizations from local city and county building and economic development authorities. Additionally, we utilize an operations center for business operations. The Bank leases additional property and/or buildings to and from third parties under lease agreements negotiated at arms-length.

Item 3. Legal Proceedings.

1st Source and our subsidiaries are involved in various legal proceedings that are inherent risks of, or incidental to, the conduct of our businesses. Management does not expect the outcome of any such proceedings will have a material adverse effect on our consolidated financial position or results of operations. One such proceeding involves the consolidated bankruptcy cases of IOI Integrated Systems, Inc., its affiliates (collectively, “IOI”) and the owner of IOI, Najeeb Khan. The consolidated cases commenced in August 2019 and are pending in the United States Bankruptcy Court, Western District of Michigan, Southern Division. IOI and Mr. Khan were customers of 1st Source Bank. Mr. Khan was also a director of 1st Source and 1st Source Bank until his resignation on July 9, 2019. The liquidating trustee of the consolidated bankruptcy estates has alleged Mr. Khan misappropriated funds of IOI over many years for his own benefit and to the detriment of IOI creditors. The trustee is investigating whether various banks and other third parties, including 1st Source Bank, may have liability because of prior business relationships with IOI and/or Mr. Khan. The trustee’s focus regarding the Bank is on transaction activity in respective deposit accounts of Mr. Khan and entities controlled by Mr. Khan at the Bank. The Bank has fully cooperated with the trustee’s information requests. The trustee has variously asserted that the Bank received avoidable transfers under applicable federal bankruptcy and state law by virtue of transactions involving deposit accounts of Mr. Khan and IOI, and that the Bank had actual knowledge of and aided and abetted Mr. Khan’s fraudulent activity. No claims have previously been formally served on the Bank. The trustee had filed a complaint but withheld service of process and agreed to stay prosecution through February 28, 2022. Management expects the trustee may formally commence litigation against various parties including the Bank during the first or second quarters of 2022. The Bank will vigorously defend any claim that it was involved with and/or benefited from the alleged misconduct of Mr. Khan and/or IOI.

Item 4. Mine Safety Disclosures.

None

15

Part II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the NASDAQ Global Select Market under the symbol “SRCE.” As of February 11, 2022, there were 1,767 holders of record of 1st Source common stock.

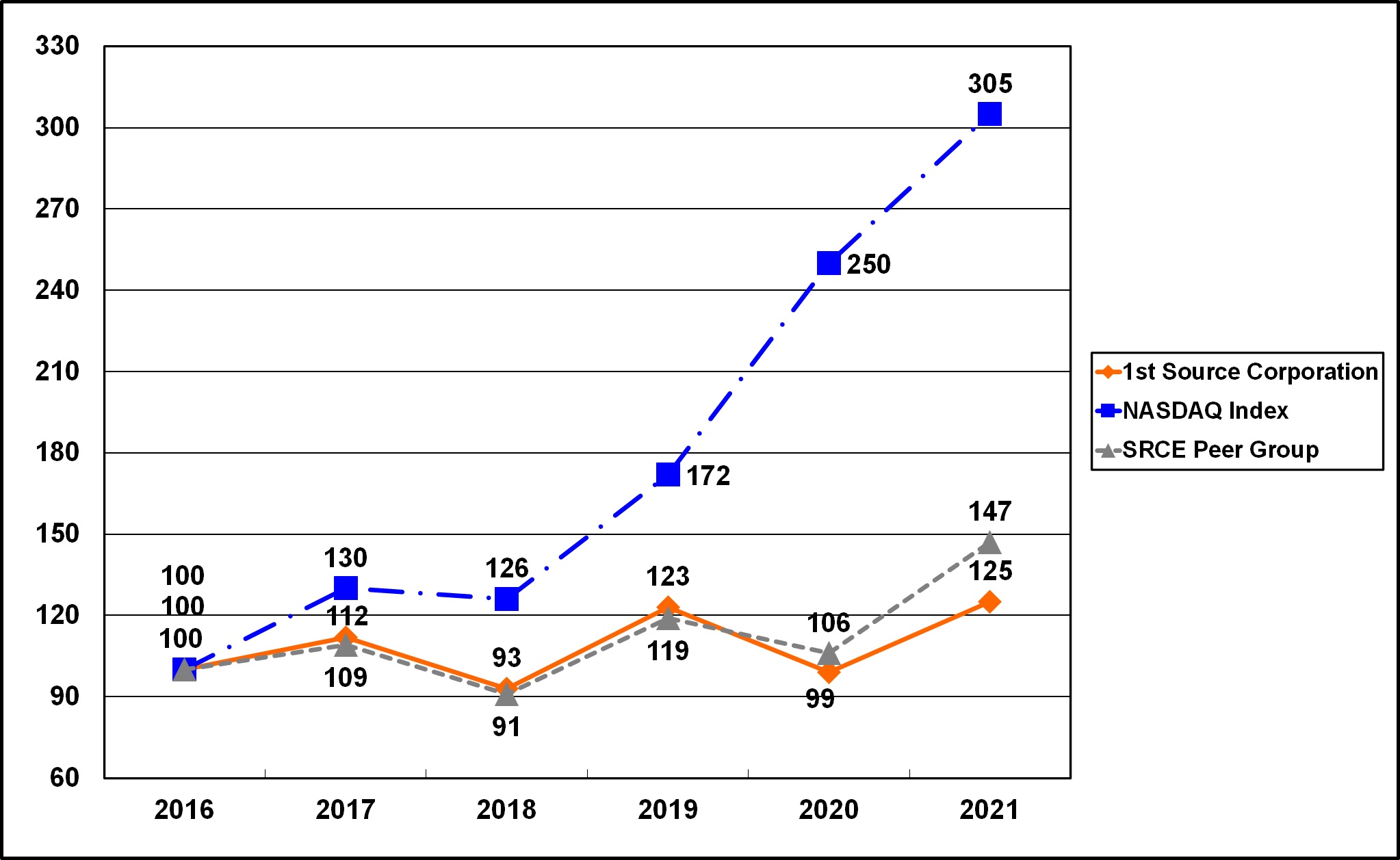

Comparison of Five Year Cumulative Total Return*

Among 1st Source, Morningstar Market Weighted NASDAQ Index** and Peer Group Index***

* Assumes $100 invested on December 31, 2016, in 1st Source Corporation common stock, NASDAQ market index, and peer group index.

** The Morningstar Weighted NASDAQ Index Return is calculated using all companies which trade as NASD Capital Markets, NASD Global Markets or NASD Global Select. It includes both domestic and foreign companies. The index is weighted by the then current shares outstanding and assumes dividends reinvested. The return is calculated on a monthly basis.

*** The peer group is a market-capitalization-weighted stock index of 35 banking companies in Illinois, Indiana, Michigan, Ohio, and Wisconsin.

NOTE: Total return assumes reinvestment of dividends.