UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) |

(Address of principal executive offices) (Zip code)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ◻

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer ☐ | |

Non-accelerated filer ☐ | Smaller reporting company |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Aggregate market value of Common Stock held by non-affiliates at June 30, 2023: $

Number of shares of Common Stock outstanding at February 16, 2024:

Documents Incorporated By Reference

The following document is incorporated by reference in Part III of the Annual Report on Form 10-K to the extent described therein: Proxy statement for the annual meeting of shareholders of Matson, Inc. to be held on April 25, 2024.

TABLE OF CONTENTS

i

MATSON, INC.

FORM 10-K

Annual Report for the Fiscal Year

Ended December 31, 2023

PART I

ITEM 1. BUSINESS

| A. | COMPANY OVERVIEW |

Matson, Inc., a holding company incorporated in the State of Hawaii, and its subsidiaries (“Matson” or the “Company”), is a leading provider of ocean transportation and logistics services. The Company consists of two segments, Ocean Transportation and Logistics.

Ocean Transportation: Matson’s Ocean Transportation business is conducted through Matson Navigation Company, Inc. (“MatNav”), a wholly-owned subsidiary of Matson, Inc. Founded in 1882, MatNav provides a vital lifeline of ocean freight transportation services to the domestic non-contiguous economies of Hawaii, Alaska and Guam, and to other island economies in Micronesia. MatNav also operates premium, expedited services from China to Long Beach, California, provides services to Okinawa, Japan and various islands in the South Pacific, and operates an international export service from Dutch Harbor, Alaska to Asia. In addition, subsidiaries of MatNav provide stevedoring, refrigerated cargo services, inland transportation and other terminal services for MatNav on the Hawaiian islands of Oahu, Hawaii, Maui and Kauai, and for MatNav and other ocean carriers in Alaska.

Matson has a 35 percent ownership interest in SSA Terminals, LLC, a joint venture between Matson Ventures, Inc., a wholly-owned subsidiary of MatNav, and SSA Ventures, Inc., a subsidiary of Carrix, Inc. (“SSAT”). SSAT currently provides terminal and stevedoring services to various carriers at eight terminal facilities on the U.S. West Coast, including three facilities dedicated for MatNav’s use. Matson records its share of income from SSAT in costs and expenses in the Consolidated Statements of Income and Comprehensive Income, and within the Ocean Transportation segment due to the nature of SSAT’s operations.

Logistics: Matson’s logistics business is conducted through Matson Logistics, Inc. (“Matson Logistics”), a wholly-owned subsidiary of MatNav. Established in 1987, Matson Logistics extends the geographic reach of Matson’s transportation network throughout North America and Asia, and is an asset-light business that provides a variety of logistics services to its customers including: (i) multimodal transportation brokerage of domestic and international rail intermodal services, long-haul and regional highway trucking services, specialized hauling, flat-bed and project services, less-than-truckload services, and expedited freight services (collectively, “Transportation Brokerage” services); (ii) less-than-container load (“LCL”) consolidation and freight forwarding services (collectively, “Freight Forwarding” services); (iii) warehousing, trans-loading, value-added packaging and distribution services (collectively, “Warehousing” services); and (iv) supply chain management, non-vessel operating common carrier (“NVOCC”) freight forwarding and other services.

Our Mission and Vision:

Our mission is to move freight better than anyone. Our vision is to create value for our shareholders by:

| ◾ | Being our customers’ first choice, |

| ◾ | Leveraging our core strengths to drive growth and increase profitability, |

| ◾ | Improving the communities in which we work and live, |

| ◾ | Being an environmental leader in our industry, and |

| ◾ | Being a great place to work. |

1

| B. | BUSINESS DESCRIPTION |

(1) | OCEAN TRANSPORTATION SEGMENT |

Ocean Transportation Services:

Matson’s Ocean Transportation segment provides the following services:

Hawaii Service: Matson’s Hawaii service provides ocean carriage (lift-on/lift-off, roll-on/roll-off and conventional services) between the ports of Long Beach and Oakland, California; Tacoma, Washington; and Honolulu, Hawaii. Matson also operates a network of inter-island barges that provide connecting services from its hub at Honolulu to other major Hawaii ports on the islands of Hawaii, Maui and Kauai. Matson is the largest carrier of ocean cargo between the U.S. West Coast and Hawaii.

Westbound cargo carried by Matson to Hawaii includes dry containers of mixed commodities, refrigerated commodities, food, beverages, retail merchandise, building materials, automobiles and household goods. Matson’s eastbound cargo from Hawaii includes automobiles, household goods, dry containers of mixed commodities and livestock. The majority of Matson’s Hawaii service revenue is derived from the westbound carriage of containerized freight.

China Service: Matson’s expedited China-Long Beach Express (“CLX”) service is part of an integrated service that carries cargo from Long Beach, California to Honolulu, Hawaii, to Guam, and then to Okinawa, Japan. The vessels continue to Ningbo and Shanghai, China, where they are loaded with cargo to be discharged primarily in Long Beach, California at a Matson-exclusive terminal operated by SSAT. These vessels also carry cargo destined for Hawaii which originated in Guam, Micronesia, Okinawa, China and other Asian countries. Matson provides container transshipment services from many locations in Asia including Southern China, Hong Kong, Vietnam and Xiamen, China to the United States via Shanghai.

Matson operates a second expedited service to the U.S. West Coast with the China-Long Beach Express Plus (“CLX+”) service. The CLX+ service primarily uses chartered vessels and operates weekly from Ningbo and Shanghai, China where they are loaded with cargo to be discharged primarily at Long Beach, California, calling at an SSAT-operated terminal. On February 18, 2024, the Company renamed the CLX+ service to Matson Asia Express (“MAX”).

Eastbound cargo from China to Long Beach, California consists mainly of garments, e-commerce related goods, consumer electronics, footwear and other merchandise.

Guam Service: Matson’s Guam service provides weekly carriage between the U.S. West Coast and Guam, as part of its CLX service. Matson also provides weekly connecting service from Guam to the Commonwealth of the Northern Mariana Islands. Cargo destined to Guam mainly includes dry containers of mixed commodities, refrigerated containers of food, beverages, retail merchandise, building materials, and household goods.

Japan Service: Matson’s Japan service provides weekly carriage between the U.S. West Coast and the port of Naha in Okinawa, Japan, as part of its CLX service. This service mainly carries general sustenance cargo in both dry and refrigerated containers and household goods supporting the U.S. military.

Micronesia Service: Matson’s Micronesia service provides carriage between the U.S. West Coast and the islands of Kwajalein, Ebeye and Majuro in the Republic of the Marshall Islands, the islands of Yap, Pohnpei, Chuuk and Kosrae in the Federated States of Micronesia, and the Republic of Palau. Cargo destined for these locations is transshipped through Guam and consists mainly of general sustenance cargo, building materials, hardware and retail merchandise.

Alaska Service: Matson’s Alaska service provides ocean carriage between the port of Tacoma, Washington, and the ports of Anchorage, Kodiak and Dutch Harbor, Alaska. Matson also provides a barge service between Dutch Harbor and Akutan in Alaska, and transportation services to other locations in Alaska including the Kenai Peninsula, Fairbanks and the North Slope.

Northbound cargo to Alaska consists mainly of dry containers of mixed commodities, refrigerated commodities, food, beverages, retail merchandise, household goods and automobiles. Southbound cargo from Alaska primarily consists of seafood, household goods and automobiles.

2

Matson’s Alaska-Asia Express (“AAX”) service provides carriage of seafood primarily from Kodiak and Dutch Harbor, Alaska to many locations in Asia via its transshipment ports of Ningbo and Shanghai, China, and Busan, South Korea. The AAX service utilizes CLX+ vessels on their westbound return voyages to China.

South Pacific Service: Matson’s New Zealand Express (“NZX”) service provides carriage of general sustenance cargo between Auckland, New Zealand and select islands in the South Pacific, including Fiji (Suva and Lautoka), Samoa (Apia), American Samoa (Pago Pago), the Cook Islands (Rarotonga and Aitutaki), Tonga (Nukualofa and Vava’u), and Niue. Additionally, Matson provides slot charter arrangements for the transportation of cargo from major ports on the east coast of Australia to ports in the South Pacific islands. The NZX service also distributes and sells domestic bulk fuel to a variety of these islands.

Terminal and Other Related Services:

Matson provides stevedoring, refrigerated cargo services, inland transportation, container equipment maintenance and other terminal services (collectively, “terminal services”) at terminals located on the Hawaiian islands of Oahu, Hawaii, Maui and Kauai; and in the Alaska terminal locations of Anchorage, Kodiak and Dutch Harbor.

SSAT currently provides terminal and stevedoring services to various carriers at eight terminal facilities on the U.S. West Coast, including three facilities dedicated for MatNav’s use, in Long Beach and Oakland, California and in Tacoma, Washington.

Matson utilizes the services of other third-party terminal operators at all of the other ports where its vessels are served.

Vessel Management Services:

Matson contracts with the U.S. Department of Transportation to provide vessel management services to manage and maintain three Ready Reserve Force vessels on behalf of the U.S. Department of Transportation Maritime Administration (“MARAD”).

3

Vessel Information:

Vessels:

Matson’s fleet includes both owned and chartered vessels. Matson’s owned vessels represent an investment of approximately $2.3 billion. The majority of Matson’s owned vessels are U.S. flagged and Jones Act qualified vessels, and operate in Matson’s Hawaii, China, Guam, Japan, Micronesia and Alaska services. Details of Matson’s active and reserve vessels as of December 31, 2023 are as follows:

Usable Cargo Capacity | Vessel | |||||||||||||||||

Containers | Vehicles | Design | Approximate | Charter | ||||||||||||||

| Year |

| Official |

|

| Reefer |

|

|

|

|

| Speed |

| Deadweight |

| Expiration | ||

Name of Vessels | Built | Number | TEUs (1) | Slots | Autos | Length | (Knots) (2) | (Long Tons) | Date (3) | |||||||||

Vessels-Owned: | ||||||||||||||||||

DANIEL K. INOUYE (4)(8) | 2018 |

| 1274136 |

| 3,160 |

| 408 | — |

| 854’ 0” |

| 23.5 |

| 51,000 |

| — | ||

KAIMANA HILA (4) | 2019 | 1274135 | 3,220 | 408 | — | 854’ 0” | 23.5 |

| 54,000 |

| — | |||||||

MANOA (4)(7) |

| 1982 |

| 651627 |

| 2,824 |

| 408 |

| — |

| 860’ 2” |

| 23.0 |

| 35,000 |

| — |

MAHIMAHI (4)(7) |

| 1982 |

| 653424 |

| 2,824 |

| 408 |

| — |

| 860’ 2” |

| 23.0 |

| 35,000 |

| — |

LURLINE (4) | 2019 | 1274143 | 2,750 | 432 | 500 | 869’ 5” | 23.0 | 51,000 | — | |||||||||

MATSONIA (4) | 2020 | 1274123 | 2,750 | 432 | 500 | 869’ 5” | 23.0 | 51,000 | — | |||||||||

MANULANI (4)(7) |

| 2005 |

| 1168529 |

| 2,378 |

| 284 |

| — |

| 712’ 0” |

| 22.5 |

| 38,000 |

| — |

MAUNAWILI (4)(7) |

| 2004 |

| 1153166 |

| 2,378 |

| 326 |

| — |

| 711’ 9” |

| 22.5 |

| 37,000 |

| — |

MANUKAI (4)(7) |

| 2003 |

| 1141163 |

| 2,378 |

| 326 |

| — |

| 711’ 9” |

| 22.5 |

| 38,000 |

| — |

R.J. PFEIFFER (4)(7) |

| 1992 |

| 979814 |

| 2,245 |

| 300 |

| — |

| 713’ 6” |

| 23.0 |

| 28,000 |

| — |

MOKIHANA (4) |

| 1983 |

| 655397 |

| 1,994 |

| 354 |

| 1,323 |

| 860’ 2” |

| 23.0 |

| 30,000 |

| — |

MAUNALEI (4)(7) |

| 2006 |

| 1181627 |

| 1,992 |

| 328 |

| — |

| 681’ 1” |

| 22.1 |

| 33,000 |

| — |

MATSON KODIAK (4)(7) |

| 1987 |

| 910308 |

| 1,668 |

| 280 |

| — |

| 710’ 0” |

| 20.0 |

| 20,000 |

| — |

MATSON ANCHORAGE (4)(7) |

| 1987 |

| 910306 |

| 1,668 |

| 280 |

| — |

| 710’ 0” |

| 20.0 |

| 20,000 |

| — |

MATSON TACOMA (4)(7) |

| 1987 |

| 910307 |

| 1,668 |

| 280 |

| — |

| 710’ 0” |

| 20.0 |

| 20,000 |

| — |

KAMOKUIKI (5) |

| 2000 |

| 9232979 |

| 707 |

| 100 |

| — |

| 433’ 9” |

| 17.5 |

| 8,000 |

| — |

OLOMANA (6) | 2004 | 9184225 | 645 | 120 | — | 388’ 7” | 14.0 | 8,000 | — | |||||||||

IMUA (6) |

| 2004 |

| 9184237 |

| 645 |

| 90 |

| — |

| 388’ 6” |

| 15.0 |

| 8,000 |

| — |

LILOA II (6) |

| 2006 |

| 9184249 |

| 630 |

| 90 |

| — |

| 388’ 6” |

| 15.0 | 8,000 | — | ||

PAPA MAU (6) |

| 1999 |

| 9141704 |

| 521 |

| 60 |

| — |

| 381’ 5” |

| 14.0 |

| 6,000 |

| — |

Vessels-Chartered: | ||||||||||||||||||

MATSON WAIKIKI (6) | 2008 | 9349801 | 4,946 | 400 | — | 902’ 0” | 22.5 | 62,000 | September 2025 | |||||||||

MATSON LANAI (6) | 2007 | 9334143 | 4,253 | 400 | — | 855’ 2” | 24.3 | 50,000 | June 2025 | |||||||||

MATSON MAUI (6) | 2007 | 9340764 | 4,253 | 400 | — | 854’ 8” | 24.5 | 50,000 | March 2026 | |||||||||

MATSON OAHU (6) | 2008 | 9352406 | 4,245 | 535 | — | 853’ 0” | 24.3 | 50,000 | October 2024 | |||||||||

MATSON KAUAI (6) | 2008 | 9353278 | 4,218 | 350 | — | 881’ 11” | 24.8 | 52,000 | January 2025 | |||||||||

MATSON MOLOKAI (6) | 2007 | 9338084 | 2,824 | 586 | — | 728’ 10” | 22.0 | 39,000 | May 2025 | |||||||||

Barges-Owned: | ||||||||||||||||||

MAUNA LOA (4) |

| 2013 |

| 1247426 |

| 500 |

| 78 |

| — |

| 362’ 6” |

| — |

| 13,000 |

| — |

HALEAKALA (4) |

| 2022 |

| 1324310 |

| 620 |

| 72 |

| — |

| 362’ 6” |

| — |

| 15,000 |

| — |

Barges-Chartered: | ||||||||||||||||||

ILIULIUK BAY (4) |

| 2013 |

| 1249384 |

| 178 |

| — |

| — |

| 250’ 0” |

| — |

| 4,000 |

| December 2024 |

| (1) | Twenty-foot Equivalent Units (“TEU”) is a standard measure of cargo volume correlated to a standard 20-foot dry cargo container. |

| (2) | Actual operating speed of the vessel may vary from the Vessel Design Speed. |

| (3) | Charter expiration date represents the approximate earliest month the vessel can be returned to its owner. Some vessel charter agreements include options for the Company to further extend the charter period. |

| (4) | U.S. flagged and Jones Act qualified vessel or barge. |

| (5) | U.S. flagged vessel. |

| (6) | Foreign-flagged vessel. |

| (7) | Vessel installed with exhaust gas cleaning systems (commonly referred to as “scrubbers”). |

| (8) | Vessel can operate on liquified natural gas (“LNG”), conventional or alternative fuels. |

4

Fleet Renewal Program:

Matson is constructing three new vessels with the following specifications and expected delivery dates:

Usable Cargo Capacity | ||||||||||||||

Containers | Maximum | Maximum | ||||||||||||

| Type of |

| Expected |

|

|

| Reefer |

| Speed |

| Deadweight | |||

Class of Vessel | Vessel | Delivery Date | TEUs | Slots | Length | (Knots) | (Long Tons) | |||||||

Aloha Class |

| Containership |

| Q4 2026 | 3,620 |

| 400 | 853’ 2” |

| 23.5 |

| 53,000 | ||

Aloha Class | Containership | Q2 2027 | 3,620 | 400 | 853’ 2” | 23.5 | 53,000 | |||||||

Aloha Class | Containership | Q4 2027 | 3,620 | 400 | 853’ 2” | 23.5 | 53,000 | |||||||

Matson expects to deploy the three new vessels in the CLX service and redeploy three existing vessels into the Alaska service. The new vessels will have dual-fuel engines and be equipped with tanks, piping and cryogenic equipment designed to operate on LNG, conventional and alternative fuels. The new vessels are also being designed with state-of-the-art green technology features and fuel-efficient hulls. Each new vessel is expected to provide approximately 500 containers of additional capacity per voyage in the CLX service.

The contract cost of the new vessel program is approximately $1.0 billion in total, and milestone payments are expected to be financed with cash currently on deposit in the Company’s Capital Construction Fund, cash and cash equivalents on the Company’s Consolidated Balance Sheets and through cash flows generated from future operations, borrowings available under the Company’s unsecured revolving credit facility or additional debt financings. Actual and future vessel construction progress milestone payments based on signed agreements and change orders, excluding vessel steel price adjustments, owners’ items and capitalized interest, are expected to be as follows:

Paid | Future Milestone Payments | |||||||||||||||||||||||

Vessel Construction Obligations (in millions) |

| As of |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| Thereafter |

| Total | ||||||||

Three Aloha Class Containerships | $ | 99.9 | $ | 71.0 | $ | 367.1 | $ | 323.0 | $ | 132.0 | $ | 6.0 | $ | — | $ | 999.0 | ||||||||

Matson is also installing tanks, piping and cryogenic equipment on existing Aloha Class vessels so that they can operate on LNG, conventional and alternative fuels. The LNG installation project on Daniel K. Inouye was completed in the third quarter of 2023 at a total cost of approximately $47 million. LNG installation work on Kaimana Hila is currently scheduled to begin during the second quarter of 2024, and the total cost is expected to be approximately $47 million. Additionally, in the third quarter of 2023, the Company commenced the reengining of Manukai to operate on LNG, conventional and alternative fuels and the total cost is expected to be approximately $72 million.

The three new Aloha Class vessels and LNG installation projects are important steps towards achieving Matson’s medium-term greenhouse gas (“GHG”) emissions goal which is to reduce Scope 1 GHG emissions from its owned fleet by 40% by 2030, using 2016 as a baseline year. Matson has also set a long-term goal to achieve net zero Scope 1 GHG emissions from its owned fleet by 2050. For more information on Matson’s environmental stewardship initiatives, including GHG reduction goals, see Matson’s Sustainability Report and other information available at https://www.matson.com/sustainability.

Vessel Emission Regulations:

Being a leader in environmental stewardship is one of Matson’s core values. Matson’s vessels transit through some of the most environmentally sensitive areas in the United States including the Hawaiian Islands and the coasts of California, Oregon, Washington and Alaska. In particular, Matson is focused on reducing transportation emissions, including carbon dioxide, methane, nitrous oxide, particulate matter and sulfur dioxide through improvements in vessel fuel consumption, choice of fuel types and the development of more fuel-efficient transportation solutions. Matson further contributes positively to the environment by testing and deploying leading technologies as the fleet is modernized.

The International Maritime Organization (“IMO”), to which the U.S. and over 100 other countries are signatories, is a specialized agency of the United Nations that sets international environmental standards applicable to vessels operating under the flag of any signatory country. Effective January 1, 2020, the IMO imposed regulations that generally require all vessels to burn fuel oil with a maximum sulfur content of ≤0.5 percent. With respect to North America, all waters,

5

with certain limited exceptions, within 200 nautical miles of U.S. and Canadian coastlines have been designated emission control areas (“ECAs”). Since January 1, 2015, U.S. Environmental Protection Agency regulations have reduced the fuel oil maximum sulfur content in designated ECAs. In addition, since August 1, 2012, the California Air Resources Board has reduced the fuel oil maximum sulfur content to ≤0.1 percent within 24 miles of the California coastline.

All of Matson’s vessels are designed to operate in compliance with current IMO and ECA regulations as applicable. Matson also maintains vessels which may operate as dry-dock relief or for emergency activation purposes under an Environmental Protection Agency (“EPA”) approved ECA permit enabling the use of fuel oil with a maximum sulfur content of ≤0.5 percent within the North America ECA or at any time on IMO compliant fuels.

In June 2021, the IMO adopted regulations requiring that, beginning with a vessel’s first annual, intermediate or renewal survey for an International Air Pollution Prevention (“IAPP”) certificate on or after January 1, 2023, all containerships with more than 10,000 dead weight tons meet specified Energy Efficiency Existing Ship Index (“EEXI”) levels. EEXI is a one-time certification measuring a ship’s theoretical carbon dioxide (“CO2”) emissions per transport work based on its design parameters. Beginning in 2023, containerships with over 5,000 gross tonnage (“GT”) are also required to meet annual Carbon Intensity Indicator (“CII”) levels that become increasingly stringent towards 2030. CII measures how efficiently a ship transports goods, and uses actual CO2 emissions to determine an annual rating. For ships that are not in compliance, a corrective action plan needs to be developed as part of the vessels’ Ship Energy Efficiency Management Plan (“SEEMP”) and approved. The Company believes that its vessels are currently in compliance with these regulations. For more information on Matson’s environmental stewardship initiatives, including GHG emission reduction goals, see Matson’s Sustainability Report and other information available at https://www.matson.com/sustainability.

Hawaii Terminal Modernization and Expansion Program:

Matson completed the first phase of its program to modernize and renovate its terminal facility at Sand Island, Honolulu, and is progressing on the second phase. As part of this program, Matson completed the installation of three new 65 long-ton capacity gantry cranes, upgraded and renovated three existing cranes, demolished four outdated cranes, and installed upgrades to the electrical infrastructure at the terminal. In addition, Matson completed the installation, energization and transition to a new redundant main switchgear. Additional projects for the second phase relate to improvements to its existing backup power generators, installation of new above ground fuel storage tanks and other upgrades at the terminal, and are expected to be completed within the next three years.

The third phase represents a broader and long-term terminal expansion program at the Sand Island terminal facility. Matson expects to expand into Pier 51A and portions of Pier 51B after Pasha Hawaii (“Pasha”) relocates to the newly constructed Kapalama container terminal (“KCT”) facility in 2025. From 2024 to 2025, Matson expects to perform surveying, planning and design work in preparation for this expansion.

Ocean Transportation Equipment:

As a complement to its fleet of vessels, Matson owns a variety of equipment including cranes, terminal equipment, containers and chassis, which represents an investment of approximately $0.8 billion as of December 31, 2023. Matson also leases containers, chassis and other equipment under various operating lease agreements.

Operating Costs:

Major components of Matson’s Ocean Transportation operating costs are as follows:

Direct Cargo Expense includes terminal handling costs including labor, purchased outside transportation and other related costs.

Vessel Operating Expense includes crew wages and related costs; fuel, pilots, tugs and line related costs; vessel charter expenses; and other vessel operating related expenses. Matson purchases fuel oil, lubricants and gasoline for its operations and pays fuel-related surcharges to other third-party transportation providers.

6

Operating Overhead includes equipment repair costs, equipment lease and repositioning expenses, vessel repair and maintenance costs, depreciation and dry-docking amortization, insurance, port engineers and other maintenance costs, and other vessel and shoreside related overhead.

Competition:

The following is a summary of major competitors in Matson’s Ocean Transportation segment:

Hawaii Service: Matson’s Hawaii service has one major U.S. flagged Jones Act competitor, Pasha, which operates container and roll-on/roll-off services between the ports of Long Beach, Oakland and San Diego, California to Hawaii. A U.S. flagged Jones Act barge operator, Aloha Marine Lines, also offers barge service between Seattle, Washington and Hawaii.

Foreign-flagged vessels carrying cargo to Hawaii from non-U.S. locations also provide alternatives for companies shipping to Hawaii. Other competitors in the Hawaii service include proprietary operators and contract carriers of bulk cargo, and air freight carriers.

Matson operates three strings of vessels to Hawaii. These strings provide customers an industry-leading five departures from ports on the U.S. West Coast – two each from Long Beach and Oakland, California and one from Tacoma, Washington, with three arrivals in Honolulu each week. Each of these strings operates on a fixed day-of-the-week schedule. One of the vessel strings continues from Honolulu to China before returning to Long Beach. Matson’s frequent sailings and punctuality permit customers to reduce inventory carrying costs. Matson also competes by offering a comprehensive service network to customers, including: the only container service to and from the three largest U.S. West Coast ports; the most efficient terminal network on the U.S. West Coast with three exclusive use terminals provided by SSAT; a dedicated inter-island barge network which is integrated with Matson’s line haul schedule; roll-on/roll-off service from Long Beach and Oakland; a world-class customer service team; and efficiency and experience in handling cargo of many types.

Alaska Service: Matson’s Alaska service has one major U.S. flagged Jones Act competitor, Totem Ocean Trailer Express, Inc., which operates a roll-on/roll-off service between Tacoma, Washington and Anchorage, Alaska. There are also two primary U.S. flagged Jones Act barge operators, Alaska Marine Lines, which mainly provides services from Seattle, Washington to the ports of Anchorage, Dutch Harbor, and other locations in Alaska, and Samson Tug & Barge, which mainly serves Western Alaska and other locations. The barge operators have historically shipped lower value commodities that can accommodate a longer transit time, as well as construction materials and other cargo that are not conducive to movement in containers. Foreign-flagged vessels provide alternatives for companies shipping cargo (mainly seafood) from the Alaska ports of Kodiak and Dutch Harbor to international destinations. Other competitors include air freight carriers and over-the-road trucking services. Matson’s AAX service has two primary competitors, CMA CGM and Maersk Lines, which provide services between Dutch Harbor, Alaska and Asia.

Matson offers customers twice weekly scheduled service from Tacoma, Washington to Anchorage and Kodiak, Alaska, and a weekly service to Dutch Harbor, Alaska. The Company also provides a barge service between Dutch Harbor and Akutan in Alaska. Matson is the only Jones Act containership operator providing service to Kodiak and Dutch Harbor in Alaska, which are the primary loading ports for southbound seafood. Matson offers dedicated terminal services at the Alaska ports of Anchorage, Kodiak and Dutch Harbor performed by Matson, and at the port of Tacoma, Washington performed by SSAT. Matson’s AAX service also offers customers a service from Kodiak and Dutch Harbor, Alaska to Ningbo and Shanghai, China, and Busan, South Korea, with transshipment services from those ports to other locations in Asia.

China Service: Major competitors to Matson’s China service include large international transpacific carriers such as CMA CGM, OOCL, ZIM, Evergreen and Cosco. Other competitors include air freight carriers.

Matson’s China service (CLX and CLX+) competes by offering fast and reliable service from the ports of Ningbo and Shanghai in China, and feeder services from other Asian ports of origin, to Long Beach, California. Matson provides fixed day-of-the-week arrivals and industry leading cargo availability. Matson’s service is further differentiated by best-in-class stevedoring services provided by SSAT, Matson dedicated terminal space, access to Shippers Transport Express off-dock container yards for faster truck turn times, Matson-dedicated equipment including chassis to speed cargo availability, one-stop intermodal connections, and world-class customer service. Matson also provides intermodal

7

services in coordination with Matson Logistics. Matson has offices located in Shanghai, Shenzhen, Xiamen, Ningbo and Hong Kong, and has contracted with terminal operators in Ningbo and Shanghai.

Guam Service: Matson’s Guam service has one major competitor, APL, a U.S. flagged subsidiary of CMA CGM, which operates a U.S. flagged container service connecting the U.S. West Coast to Guam and Saipan, via transshipments to U.S. flagged feeder vessels in Yokohama, Japan and Busan, South Korea via a two-ship feeder service. There are also other several foreign carriers that call at Guam from foreign origin ports, and air freight carriers.

Matson offers customers a weekly service to Guam as part of the CLX service from three ports on the U.S. West Coast. Matson’s ocean transit time, frequent sailing and reliable on-time performance provides an industry-leading service to its customers.

Japan Service: Matson’s Japan service has one major competitor, APL, which operates a U.S. flagged containership service from the U.S. West Coast to the port of Naha in Okinawa, Japan.

Matson offers customers a fast and reliable weekly service to the port of Naha in Okinawa, Japan as part of the CLX service from three ports on the U.S. West Coast.

Micronesia and South Pacific Services: Matson’s Micronesia and South Pacific services compete with a variety of local and international carriers that provide freight services to the area.

Customer Concentration:

Matson serves customers in numerous industries and carries a wide variety of cargo, mitigating its dependence upon any single customer or single type of cargo. The Company’s 10 largest Ocean Transportation customers account for approximately 16 percent of the Company’s Ocean Transportation revenue. For additional information on Ocean Transportation revenues for the years ended December 31, 2023, 2022 and 2021, see Note 2 to the Consolidated Financial Statements in Item 8 of Part II below.

Seasonality:

Historically, Matson’s Ocean Transportation services have typically experienced seasonality in volume, generally following a pattern of increasing volume starting in the second quarter of each year, culminating in a peak season throughout the third quarter, with subsequent decline in demand during the fourth and first quarters. This seasonality is amplified in the Alaska service primarily due to winter weather and the timing of southbound seafood trade. As a result, earnings have tended to follow a similar pattern, offset by periodic vessel dry-docking and other episodic cost factors, which can lead to earnings variability. In addition, in the China trade, volume demand is generally stronger in the second and third quarters primarily driven by U.S. consumer demand for goods ahead of key retail selling seasons. Freight rates can be impacted by these seasonality trends as well as macro supply and demand variables.

Relatively high inflation and the impact of high interest rates on household discretionary income may affect the demand for consumer goods in our markets, which could impact seasonal variability and demand for the Company’s Ocean Transportation services in 2024.

Maritime Laws and the Jones Act:

Maritime Laws: All interstate and intrastate marine commerce within the U.S. falls under the Merchant Marine Act of 1920 (commonly referred to as the Jones Act).

The Jones Act is a long-standing cornerstone of U.S. maritime policy. Under the Jones Act, all vessels transporting cargo between covered U.S. ports must, subject to limited exceptions, be built in the U.S., registered under the U.S. flag, be manned predominantly by U.S. crews, and owned and operated by U.S.-organized companies that are controlled and 75 percent owned by U.S. citizens. U.S. flagged vessels are generally required to be maintained at higher standards than foreign-flagged vessels and are subject to rigorous supervision and inspections by, or on behalf of, the U.S. Coast Guard, which requires appropriate certifications and background checks of the crew members. Under Section 27 of the Jones Act, the carriage of cargo between the U.S. West Coast, Hawaii and Alaska on foreign-built or foreign-documented vessels is prohibited.

8

During the years ended December 31, 2023, 2022 and 2021, approximately 55 percent, 39 percent and 41 percent, respectively, of Matson’s Ocean Transportation revenues came from the Hawaii and Alaska trades that were subject to the Jones Act. Matson’s Hawaii and Alaska trade routes are included within the non-contiguous Jones Act market. The commerce of both Hawaii, as an island economy, and Alaska, due to its geographical location, are dependent on ocean transportation. The Jones Act ensures frequent, reliable, roundtrip service to these locations. Matson’s vessels operating in these trade routes are Jones Act qualified and maintained in compliance with such requirements.

Matson is a member of the American Maritime Partnership (“AMP”), which supports the retention of the Jones Act and similar cabotage laws. The Jones Act has broad support from both houses of Congress and the Executive Branch. Matson believes that the geopolitical environment has further solidified political support for U.S. flagged vessels because a vital and dedicated U.S. merchant marine is a cornerstone for a strong homeland defense, as well as a critical source of trained U.S. mariners for wartime support. AMP seeks to inform elected officials and the public about the economic, national security, commercial, safety and environmental benefits of the Jones Act and similar cabotage laws. Repeal of the Jones Act would allow foreign-flagged vessel operators that do not have to abide by all U.S. laws and regulations to sail between U.S. ports in direct competition with Matson and other U.S. domestic operators that must comply with all such laws and regulations.

Other U.S. maritime laws require vessels operating between Guam, a U.S. territory, and U.S. ports to be U.S. flagged and predominantly U.S. crewed, but not U.S. built.

Cabotage laws are not unique to the United States, and similar laws exist around the world in over 90 countries, including regions in which Matson provides ocean transportation services. Any changes in such laws may have an impact on the services provided by Matson in those regions.

Rate Regulations and Fuel-Related Surcharges:

Matson is subject to the jurisdiction of the Surface Transportation Board with respect to its domestic ocean rates. A rate in the non-contiguous domestic trade is presumed reasonable and will not be subject to investigation if the aggregate of increases and decreases is not more than 7.5 percent above, or more than 10 percent below, the rate in effect one year before the effective date of the proposed rate, subject to increase or decrease by the percentage change in the U.S. Producer Price Index. Matson generally seeks to provide a 30-day notice to customers of any increases in general rates and other charges, and passes along decreases as soon as possible.

Matson’s Ocean Transportation services engaged in U.S.-foreign commerce are subject to the jurisdiction of the Federal Maritime Commission (“FMC”). The FMC is a federal independent regulatory agency that is responsible for the regulation of international ocean-borne transportation to and from the U.S.

Matson applies a fuel-related surcharge rate to its Ocean Transportation customers. Matson’s fuel-related surcharge is correlated to market rates for fuel prices and other factors, and is intended to help Matson recover fuel-related expenses.

Other Environmental Regulations:

In addition to the vessel emission regulations discussed above, Matson’s operations are required to comply with other environmental regulations and requirements including the Oil Pollution Act of 1990, the Comprehensive Environmental Response Compensation & Liability Act of 1980, the Rivers and Harbors Act of 1899, the Clean Water Act, the Invasive Species Act and the Clean Air Act. Matson is also subject to state regulations affecting terminal and vessel emissions, such as the requirement to shut down vessel generator engines while at berth at California ports and switch to shore electrical power or achieve equivalent emissions reductions. The Company actively monitors its operations for compliance with these and other regulations.

For more information on Matson’s environmental stewardship initiatives, including its environmental goals, see Matson’s Sustainability Report and other information available at https://www.matson.com/sustainability.

9

(2) | LOGISTICS SEGMENT |

Logistics Services:

Matson Logistics provides the following services:

Transportation Brokerage Services: Matson Logistics provides intermodal rail, highway, and other third-party logistics services for North American customers and international ocean carrier customers, including MatNav. Matson Logistics creates significant benefits and value for its customers through volume purchases of rail, motor carrier and ocean transportation services, augmented by services such as shipment tracking and tracing, accessibility to its private fleet of 53-foot intermodal containers and single-vendor invoicing. Matson Logistics operates customer service centers and has sales offices throughout North America.

Freight Forwarding Services: Matson Logistics provides LCL consolidation and freight forwarding services primarily to the Alaska market through its wholly-owned subsidiary, Span Intermediate, LLC (“Span Alaska”). Span Alaska’s business aggregates LCL freight at its cross-dock facility in Auburn, Washington for consolidation and shipment to its service center in Anchorage and a network of other facilities in Alaska. Span Alaska also provides trucking services to its Auburn cross-dock facility and from its Alaska based cross-dock facilities to final customer destinations in Alaska.

Warehousing and Distribution Services: Matson Logistics operates two warehouses in Georgia and two warehouses in Northern California providing warehousing, trans-loading, value-added packaging and distribution services.

Supply Chain Management and Other Services: Matson Logistics provides customers with a variety of logistics services including purchase order management, booking services, customs brokerage, LCL and full container load NVOCC freight forwarding services. Matson Logistics has supply chain operations in North America, China and other locations.

Operating Costs:

Matson Logistics’ operating costs primarily consist of the costs of purchased transportation, leases of warehouses, cross-dock and other facility operating costs, salaries and benefits, and other operating overhead.

Competition:

Matson Logistics competes with hundreds of local, regional, national and international companies that provide transportation and third-party logistics services. The industry is highly fragmented and, therefore, competition varies by geography and areas of service.

Matson Logistics’ transportation brokerage services compete most directly with C.H. Robinson Worldwide, Hub Group, RXO and other freight brokers and intermodal marketing companies, and asset-invested market leaders such as J.B. Hunt. Matson Logistics competes by relying on the depth, scale and scope of its customer relationships; vendor relationships and rates; network capacity; real-time visibility into the movement of customers’ goods; and other technology solutions. Additionally, while Matson Logistics primarily provides surface transportation brokerage, it also competes to a lesser degree with other forms of transportation for the movement of cargo such as air freight.

Matson Logistics’ freight forwarding services compete most directly with a variety of freight forwarding companies that operate within Alaska including Carlile, Lynden and American Fast Freight.

Customer Concentration:

Matson Logistics serves customers in numerous industries and geographical locations. The Company’s 10 largest logistics customers account for approximately 21 percent of the Company’s Logistics revenue. For additional information on Logistics revenues for the years ended December 31, 2023, 2022 and 2021, see Note 2 to the Consolidated Financial Statements in Item 8 of Part II below.

10

Seasonality:

In general, Matson Logistics’ services are not significantly impacted by seasonality factors, with the exception of its freight forwarding service to Alaska which may be affected by winter weather and the seasonal nature of the tourism industry.

| C. | EMPLOYEES AND LABOR RELATIONS |

Human Capital Strategy:

In support of Matson’s vision to be a great place to work for all employees, the Company focuses on a variety of human capital programs that have been developed to attract, retain and motivate its employee workforce. As a company that operates in various global locations, the Company’s human capital programs are designed to reflect the unique market practices in each geographic location. The Company’s success depends in part on employing a diverse, talented and engaged workforce that reflects its local communities, supports an environment of high standards and performance, and thrives in the Company’s collaborative and respectful culture.

During 2023, Matson had 4,315 employees worldwide, of which 158 employees were based in international locations and 3,012 employees were covered by collective bargaining agreements with unions. These numbers include seagoing personnel who rotate through billets (as described below) and temporary employees, but do not include employees of SSAT or other non-employee affiliates such as agents and contractors. The composition of Matson’s workforce by geography is as follows:

Matson’s fleet of active vessels requires 326 billets to operate. Each billet corresponds to a position on a vessel that typically is filled by two or more employees because seagoing personnel rotate between active sea-duty and time ashore. These amounts exclude billets related to Matson’s foreign-flagged chartered vessels where the vessel owner is responsible for its seagoing personnel. Matson’s vessel management services also employed personnel in 32 billets to manage three U.S. government vessels.

Diversity, Equity and Inclusion (“DE&I”):

For many years, Matson has been committed to improving diversity, providing equal pay for equal work and creating an inclusive culture. While Matson’s workforce is representative of many of the communities where it operates, the Company has taken steps intended to help improve diversity within the Company and industry and to promote inclusivity for all. In 2023, the Company continued to advance many of its diversity, equity and inclusion efforts. This included continuing its efforts to analyze pay among various employee groups to confirm pay equity across the Company.

As part of its overall DE&I strategy, Matson continues to focus on developing and promoting equal employment opportunities, particularly for leadership positions. The Company utilizes both internal and external learning and development programs to encourage and promote career opportunities and inclusivity for all within our diverse employee groups. In 2023, over half of Matson promotions in management roles were women and/or diverse individuals.

Matson is also focused on supporting a more inclusive talent pool over the long-term by encouraging historically underrepresented groups such as women and diverse individuals to pursue careers in the maritime and logistics sectors. To this end, in 2023 the Company awarded seventeen scholarships to diverse, high-achieving students at higher education institutions and maritime academies.

11

In support of the rollout of a new performance management program, Matson’s DE&I training efforts in 2023 emphasized recognizing and minimizing bias when reviewing employee performance, with over 260 managers participating in the program. Specifically, the training focused on building awareness of types of bias, using objective criteria when assessing performance and increasing the number of performance feedback opportunities.

The composition of Matson’s domestic shoreside workforce by gender and diversity status in 2023 is as follows (data for seagoing personnel is not available to the Company):

The composition of management positions within Matson’s domestic shoreside workforce by gender and diversity status in 2023 is as follows (data for seagoing personnel is not available to the Company):

“Diverse” in these graphs refers to any employee who self-identifies as a minority under the categories established by the Equal Employment Opportunity Commission.

Total Rewards Programs:

Matson provides a highly competitive and balanced total rewards program designed to attract, retain and motivate its employees. While factors such as job, location and business unit ultimately determine which plans an employee may be eligible for, the Company’s total rewards offering includes market competitive base salaries, cash and equity incentives, recognition awards, health and welfare benefits, and employee and employer funded retirement plans. The Company believes that management level positions should have a portion of pay aligned with its short- and long-term business objectives. Accordingly, the Company’s total rewards program contains several pay-for-performance components tied to individual, business unit and Company performance, as well as Matson’s stock price performance.

Succession and Career Planning:

Matson’s workforce is characterized by uniquely skilled, long-tenured employees. To create career pathways for future leaders while planning for the loss of retiring employees, the Company takes a proactive approach to succession and career planning. The Company focuses on providing the next generation of promising talent with the tools they need to build their own careers at Matson. In 2023, 41 percent of open positions were filled through internal promotions. The Company also provided approximately 2,200 hours of employee training and professional development opportunities, and tuition reimbursement programs, while giving annual performance reviews to its non-union workforce.

For more information on Matson’s human capital programs, see our Sustainability Report which is available at www.matson.com/sustainability.

12

Bargaining Agreements:

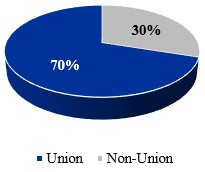

Matson’s shoreside and seagoing employees are represented by a variety of unions. Matson has collective bargaining agreements with these unions that expire at various dates in the future. As shown in the chart below, Matson’s shoreside and seagoing union employees comprise 70 percent of Matson’s global workforce.

Matson and SSAT are also members of the Pacific Maritime Association (“PMA”), which on behalf of its members negotiates collective bargaining agreements with the International Longshore and Warehouse Union (“ILWU”) on the U.S. West Coast. The PMA/ILWU collective bargaining agreements cover substantially all U.S. West Coast longshore labor. ILWU employees employed by SSAT are not included in the chart above.

Multi-employer Pension and Post-retirement Plans:

Matson contributes to several multi-employer pension and post-retirement plans. Matson has no present intention of withdrawing from and does not anticipate the termination of any of the multi-employer pension plans to which it contributes (see Notes 11 and 12 to the Consolidated Financial Statements in Item 8 of Part II below for a discussion of withdrawal liabilities under certain multi-employer pension plans).

| D. | AVAILABLE INFORMATION |

Matson makes available, free of charge on or through its Internet website, Matson’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after it electronically files such material with, or furnishes them to, the U.S. Securities and Exchange Commission (“SEC”). The address of Matson’s Internet website is www.matson.com. This website and other websites included in this document are provided for convenience only, and the contents of such websites do not constitute a part of and are not incorporated by reference into this Form 10-K.

The SEC maintains an Internet website that contains reports, proxy and information statements, and other information regarding Matson and other issuers that file electronically with the SEC. The address of the SEC’s Internet website is www.sec.gov.

ITEM 1A. RISK FACTORS

The following material risks, events and uncertainties may make an investment in the Company speculative or risky and should be reviewed carefully. The Company faces the material risks set forth below; however, the description below does not purport to include all risks the Company faces, and additional risks or uncertainties that are currently unknown or are not currently believed to be material may occur or become material. The occurrence of these or the risks and uncertainties described below may, in ways the Company may not be able to accurately predict, recognize or mitigate, adversely affect the Company’s business, competitive environment, strategy, financial condition, operating results, cash flows, liquidity, demand, revenue, growth, prospects, reputation or stock price. All forward-looking statements made in this Form 10-K are qualified by the risks and uncertainties described below.

13

Risks Related to the Jones Act

Repeal, substantial amendment, or waiver of the Jones Act or changes in its application would have an adverse effect on the Company’s business.

The Merchant Marine Act of 1920 (commonly referred to as the Jones Act) regulates all interstate and intrastate marine commerce within the U.S. If the Jones Act were to be repealed, substantially amended or waived and, as a consequence, competitors were to enter the Hawaii or Alaska markets with lower operating costs by utilizing their ability to acquire and operate foreign-flagged and foreign-built vessels and/or being exempt from other U.S. regulations, the Company’s business would be adversely affected. In addition, the Company’s position as a U.S. citizen operator of Jones Act vessels would be negatively impacted if periodic efforts and attempts by foreign interests to circumvent certain aspects of the Jones Act were successful. If maritime cabotage services were included in the General Agreement on Trade in Services, the United States-Mexico-Canada Agreement, or other international trade agreements, or if the restrictions contained in the Jones Act were otherwise altered, the shipping of cargo between covered U.S. ports could be opened to foreign-flagged or foreign-built vessels, which could have other adverse impacts to our business.

The Company’s business would be adversely affected if the Company were determined not to be a U.S. citizen under the Jones Act.

Certain provisions of the Company’s articles of incorporation protect the Company’s ability to maintain its status as a U.S. citizen under the Jones Act. If non-U.S. citizens were able to defeat such articles of incorporation restrictions and own, in the aggregate, more than 25 percent of the Company’s common stock, the Company would no longer be considered a U.S. citizen under the Jones Act. Such an event could result in the Company’s ineligibility to engage in coastwise trade and the imposition of substantial penalties against the Company, including seizure or forfeiture of its vessels.

Risks Related to the Company’s Operations

Changes in macroeconomic conditions, geopolitical developments, or governmental policies, including due to outbreaks of disease, have affected and could in the future affect the Company.

The transportation industry in which the Company operates has been and could in the future be impacted by macroeconomic fluctuations, volatility, downturns, inflation, recessions, rising interest rates and other economic shifts or market instabilities, including due to outbreaks of disease and instability in financial institutions, as well as the development of and changes in governmental policies, relations, priorities and budgeting constraints, and uncertainties resulting from the U.S. political environment, including increased political polarization and the potential for political gridlock (such as the prospect of a shutdown of the U.S. federal government), and geopolitical developments across the jurisdictions in which it operates. For example, there have been increases in geopolitical and trade tensions among a number of the world’s major economies. These tensions have resulted in the implementation of tariffs, non-tariff trade barriers and sanctions, including the use of export control restrictions and sanctions against certain countries and individual companies, which have, and may continue to have, an adverse economic impact in the markets in which the Company operates and could result in a reduced demand for the Company’s services.

These adverse economic conditions may also impact the Company’s customers’ business levels and needs. Within the U.S., a weakening of economic drivers in Hawaii, Alaska and Guam, which include tourism, military spending, construction, personal income growth and employment, the weakening of consumer confidence, market demand, the economy in the U.S. Mainland, inflation, rising interest rates, recessionary fears, increased political polarization and the potential for political gridlock (such as the prospect of a shutdown of the U.S. federal government), and the effect of a change in the strength of the U.S. dollar against other foreign currencies has reduced and could in the future reduce the demand for goods, adversely affecting inland and ocean transportation volumes or rates. In addition, overcapacity in the global or transpacific ocean transportation markets, a change in the cost of goods or currency exchange rates, pressure from U.S. or foreign governments, imposition of tariffs and uncertainties regarding tariff rates or a change in international trade policies could adversely affect freight volumes and rates in the Company’s China services. Additionally, fluctuations in the price of oil could further impact the Alaskan economy, which in turn could impact the Company’s business.

14

The shipping industry is competitive, and the Company has been and may continue to be impacted by new or increased competition.

The Company has faced and may continue to face new competition by established or start-up shipping operators that enter into the Company’s markets. The shipping industry is competitive with limited barriers to entry, especially in international tradelanes. Ocean carriers can shift vessels in and out of tradelanes or charter vessels to manage capacity and meet customer demands. The Company also competes with air freight carriers some of which are able to offer more attractive schedules and services, or to increase capacity. The entry of a new competitor or the addition of new vessels or capacity by existing competitors on any of the Company’s routes could result in a significant increase in available shipping capacity that could have an adverse effect on the Company’s volumes and rates.

The loss of or damage to key customer relationships may adversely affect the Company’s business.

The Company’s businesses are dependent on their relationships with customers and derive a significant portion of their revenues from the Company’s largest customers. The Company’s business relies on its relationships with the U.S. military, freight forwarders and non-vessel owning common carriers, large retailers and consumer goods manufacturers, as well as other larger customers. For more information regarding the Company’s significant customers, see the discussion in Part I, Item 1 of this Annual Report.

The Company could also be adversely affected by any changes in the services, or changes to the costs of services, provided by third-party vendors such as railroads, truckers, terminals, agents and shipping companies, including charter vessel owners. Service structures and relationships with these parties are important in the Company’s intermodal business, as well as in the China, Guam, Micronesia, Japan, Alaska export and South Pacific services.

The loss of or damage to any of these key relationships may adversely affect the Company’s business and revenue.

The Company is dependent upon key vendors and third parties for equipment, capacity, facilities, infrastructure and services essential to operate its business, and if the Company fails to secure sufficient third-party services, its business could be adversely affected.

The Company’s businesses are dependent upon key vendors who provide terminal, rail, truck, and ocean transportation services. If the Company cannot reliably secure sufficient transportation equipment, capacity or services from these third parties at reasonable prices or rates to meet its or its customers’ needs and schedules, customers may seek to have their transportation and logistics needs met by others on a temporary or permanent basis. If this were to occur, the Company’s business, results of operations and financial condition could be adversely affected.

An increase in fuel prices, changes in the Company’s ability to collect fuel-related surcharges, and/or the cost or limited availability of required fuels may adversely affect the Company’s profits.

Fuel, including LNG fuels and biofuels, is a significant operating expense for the Company’s Ocean Transportation business. The price and supply of fuel are unpredictable and fluctuate based on events beyond the Company’s control, including impacts from global macroeconomic conditions and geopolitical events. Increases in the price of fuel may adversely affect the Company’s results of operations. Any such increases also can lead to increases in other expenses, such as energy costs and costs to purchase outside transportation services. In the Company’s Ocean Transportation and Logistics services segments, the Company utilizes fuel-related surcharges, although increases in the fuel-related surcharges may adversely affect the Company’s competitive position and may not correspond exactly with the timing of increases in fuel expense. Changes in the Company’s ability to collect fuel-related surcharges, including recovery of all or most fuel-related expenses, also may adversely affect its results of operations.

The development of alternative fuels (such as low- or carbon-neutral fuels), including the necessary infrastructure and technology to utilize such fuels, is still in early experimental stages. There is significant uncertainty as to when, if at all, these alternative fuels will become commercially available or viable, and whether Matson will be able to utilize or have access to these alternative fuels (or any such alternative fuels developed in the future) in a timely and cost-effective manner. In addition, advances in fuel technology could require Matson to incur significant capital costs to utilize any such technologies (including, for example, efforts to accelerate building of new vessels, retrofit existing vessels, retire

15

vessels early or make reserve vessels unusable) and Matson may be unable to equip its vessels with these technologies on a timely basis, if at all.

Evolving regulations and stakeholder expectations related to sustainability matters exposes the Company to heightened scrutiny, additional costs, operational challenges and a number of risks.

The SEC and other regulators, investors, advisory firms, employees, customers, suppliers, governments and other stakeholders are increasingly focused on and have established regulations and expectations related to sustainability matters and related corporate practices, disclosures and initiatives. These evolving regulations and expectations may impact the Company’s reputation, business and attractiveness as an investment, employer or business partner to the extent the Company – including its initiatives, goals and reporting – fails to satisfy or is perceived to fail to satisfy those regulations and expectations, including as a result of any third-party rating or assessment. The adoption and expansion of related legislation and regulations have also resulted and may again result in increased capital expenditures and compliance, operational and other costs to the Company. For example, the state of California has adopted new climate change disclosure requirements. Compliance with such rules could require significant effort and resources and result in changes to the Company’s current GHG emission reduction goals.

The Company’s public disclosures on its climate, sustainability, human capital and other initiatives include its goals or expectations with respect to those matters, including GHG emission reduction targets. These disclosures are aspirational and based on standards and frameworks for presenting and measuring progress that are not harmonized and are still developing, assumptions that may change, disclosure controls and procedures that continue to evolve, and with respect to our GHG emissions targets, dependent in part on the industry’s successful and timely development of alternative fuels and technologies. The Company’s use of disclosure frameworks and standards, and the interpretation or application of those frameworks and standards, may change from time to time or differ from those of others. This may result in a lack of consistent or meaningful comparative data from period to period or between the Company and other companies in the same industry. The Company’s initiatives and goals may not be favored by certain stakeholders and could impact the attraction and retention of investors, customers and employees, as well as the Company’s willingness to do business with other companies or customers or their willingness to do business with the Company. Efforts to achieve or accurately track the Company’s initiatives and goals face numerous risks and may be untimely, be unsuccessful, result in additional costs or experience delays, and as a result may have an adverse impact on the Company, including its brand, reputation, financial performance and growth and stock price, and may expose the Company to increased scrutiny from the investment community as well as enforcement authorities.

The Company may not be timely or successful in completing its fleet upgrade initiatives, which may result in significant costs and adversely impact the Company’s ability to meet its climate goals.

The Company’s four new Aloha and Kanaloa class vessels include dual fuel capable engines that can run on low sulfur fuel oil or LNG. The Company has completed the installation of tanks, piping and cryogenic equipment on Daniel K. Inouye to operate on LNG; begun re-engining Manukai; and announced plans for LNG installations on Kaimana Hila in 2024. In addition, the Company has announced plans to construct three new LNG-ready Aloha Class vessels. The Company anticipates making significant capital expenditures in connection with these fleet initiatives. These initiatives may be hindered by substantial delays and long lead times for necessary equipment, including as a result of ongoing supply chain congestion, increased demand across the industry for LNG installations and conversions, and new ship-building. Additional operating costs may be incurred to the extent additional ships are needed to maintain schedule integrity while such updates and installations are performed. Once completed, operation of these vessels may be slowed to the extent they present new maintenance requirements or unforeseen complications.

The Company’s investments in LNG-ready vessels, whether on their own or in addition to other Company initiatives, may be insufficient to meet the Company’s previously announced GHG emission reduction goals on a timely basis or at all. There is no guarantee that the Company will be able to secure LNG via bunker barges or other methods on the U.S. West Coast or in China in sufficient amounts to fuel its vessels or at a reasonable cost, as increased demand for LNG could decrease available supply of LNG and increase prices. Governments have in the past and may again in the future impose tariffs on LNG that also may increase supply costs. As a result of these risks, the Company may not fully realize the benefits of these investments.

16

The Company’s vessel construction agreements with Philly Shipyard subject the Company to risks.

On November 1, 2022, MatNav and Philly Shipyard entered into vessel construction agreements pursuant to which Philly Shipyard will construct three new 3,600-TEU Aloha Class dual-fuel capable containerships, with expected delivery dates during the fourth quarter of 2026 and subsequent deliveries currently expected in the second and fourth quarters of 2027. Failure of any party to the vessel construction agreements to fulfill its obligations under the agreements could have an adverse effect on the Company’s financial position and results of operations. Such a failure could happen for a variety of reasons, including but not limited to (i) delivery delays, (ii) delivery of vessels that fail to meet any of the required operating specifications (for example, capacity, fuel efficiency or speed), (iii) events in South Korea that prevent one or more significant subcontractors to Philly Shipyard from performing, (iv) loss of key personnel at either Philly Shipyard or any of its subcontractors, (v) work stoppages or other labor disruptions that may occur as a result of the failure of Philly Shipyard to negotiate collective bargaining agreements with its unions, or (vi) the insolvency of, or the refusal or inability to perform for any reason, by Philly Shipyard or any of its subcontractors. Significant delays in the delivery of the new vessels could limit our ability to replace aging vessels in the Alaska service without substantial modifications and delay the Company’s ability to upsize the CLX service, which could also have an adverse impact on our business plans, financial condition and results of operations.

The Company’s operations are susceptible to weather, natural disasters, maritime accidents, spill events and other physical and operating risks, including those arising from climate change.

As a maritime transportation company, the Company’s operations are vulnerable to delay, disruptions and loss of life and property as a result of weather, natural disasters and other climate-driven events, such as rising temperatures and heat waves, rising sea levels, bad weather at sea (including increased storm severity), lightning strikes, wildfires, lava flows, hurricanes, typhoons, tsunamis, droughts, windstorms, floods and earthquakes. Climate change has increased and may continue to increase the frequency, severity and uncertainty of such events. For example, sea level rise could potentially impact coastal and other low-lying areas, cause erosion of shorelines, higher water tables and increased flooding, which could damage the Company’s vessels, terminals or facilities. In addition, the Company’s customers and the island communities it serves throughout the Pacific are particularly vulnerable to rising sea levels and severe storms, which may drive inhabitants away from these regions and reduce demand for the Company’s services in the affected areas and adversely impact our business.

The Company’s operations are also vulnerable to risks related to the operation of ocean-going vessels, including risks of potential marine accidents, or disasters, including grounding, fires, explosions, collisions, mechanical failures, human error, maintenance issues, latent defects, oil or other spill or environmental accidents, whale strikes, war, terrorism and piracy, lost or damaged cargo, delays, injury and loss of life. These risks could be exacerbated by severe weather or other climate-driven events. Changing macroeconomic and geopolitical conditions, including geopolitical conflict, may also result increased attacks on vessels, piracy or terrorism.

Such events could interfere with the Company’s ability to provide on-time scheduled service, require evacuation of personnel or stoppage of services or impact the Company’s customer’s operations, resulting in increased expenses and potential loss of business associated with such events. In addition, severe weather and natural disasters can result in interference with the Company’s terminal operations and may cause serious damage to its vessels and cranes. These impacts could be particularly acute in ports such as Dutch Harbor and Kodiak, Alaska where the Company is dependent on a single crane. The Company’s vessels and their cargoes, terminals and other facilities are also subject to operating risks such as mechanical failure, collisions and human error.

The occurrence of any of these events may result in damage to or loss of terminals, port facilities and infrastructure, vessels, containers, cargo and other equipment, increased maintenance expense, loss of life or physical injury to its employees or people, pollution, or the slow down or suspension of operations. For example, damage to the Company’s vessels could require repair at a dry-docking facility. The costs of repairs may be substantial which may adversely affect the Company’s business and financial condition. Further, the Company may be unable to find space at a suitable dry-docking facility, the vessels may be forced to wait for space or be towed to a different facility, all of which could result in additional expenses and delays, and may adversely affect the Company’s business.

These events can also expose the Company to reputational harm and liability for resulting damages, including for loss of life and property, and possible penalties that, pursuant to typical maritime industry policies, it must pay and then seek reimbursement from its insurer. Affected vessels may also be removed from service and thus would be unavailable for

17

income-generating activity. Furthermore, the Port of Alaska requires upgrades to its port facilities and infrastructure to improve operational safety and efficiency, accommodate modern shipping operations and improve resiliency, as well as to mitigate the risk of failure due to corrosion or loss of load bearing capacity. As a result, there is an increased risk that an earthquake or other natural disaster could damage or render inoperable, in whole or in part, port facilities and infrastructure at the Port of Alaska. This, in turn, could adversely affect transportation volumes or rates in Alaska and adversely impact the Company’s Ocean Transportation business and Span Alaska’s freight forwarding business, particularly given the Alaskan economy’s dependence on this port for ocean cargo.

There is no assurance that our efforts to mitigate the impact of these risks, including from severe weather or other climate-driven events on our operations, will be effective. Although we take measures that we believe are reasonable to mitigate these risks, it is not practicable to eliminate such risks altogether. The Company’s casualty and liability insurance policies are generally subject to large retentions and deductibles and may not cover all losses the Company may incur. Some types of losses, such as losses resulting from a port blockage, generally are not insured. In some cases, the Company retains the entire risk of loss because it is not economically prudent to purchase insurance coverage or because of the perceived remoteness of the risk. Other risks are uninsured because insurance coverage may not be commercially available. Finally, the Company retains all risk of loss that exceeds the limits of its insurance.

The Company may be impacted by transitional and other risks arising from climate change.

The Company may be impacted by transitional and other risks arising from climate change and the global shift toward a low carbon future. Organizational, industrial and governmental shifts in operations as well as legal and regulatory requirements to reduce or eliminate emissions and/or increase efficiency may require the Company to increase expenditures, make changes to existing infrastructure, vessels and equipment, limit the speed at which the Company’s vessels are permitted to travel, and make other changes to its business model. For example, the maritime industry is moving toward deployment of clean energy technologies and use of electricity powered by renewable energy sources to power terminal operations as a way to reduce shoreside GHG emissions. As the Company and SSAT increase their reliance on the power grid at terminals, including for cold-ironing and ground service fleets, the Company may experience increased risks related to power outages, brown outs or black outs. The likelihood of these risks is compounded by uncertainties regarding the reliability of renewable energy sources as well as any increased frequency of extreme weather events that may disrupt the generation or transmission of electricity.