Form 20-F

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended 31 December 2013

OR

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 1-6262

BP p.l.c.

(Exact name of Registrant as specified in its charter)

England and Wales

(Jurisdiction of incorporation or organization)

1 St James’s Square, London SW1Y 4PD

United Kingdom

(Address of

principal executive offices)

Dr Brian Gilvary

BP p.l.c.

1 St

James’s Square, London SW1Y 4PD

United Kingdom

Tel +44 (0) 20 7496 5311

Fax +44 (0) 20 7496 4573

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act

|

|

|

| Title of each class |

|

Name of each exchange on which registered |

| Ordinary Shares of 25c each |

|

New York Stock Exchange* |

| Floating Rate Guaranteed Notes due 2014 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due May 2015 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due November 2015 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due 2016 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due May 2018 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due September 2018 |

|

New York Stock Exchange |

| Floating Rate Guaranteed Notes due 2019 |

|

New York Stock Exchange |

| 3.625% Guaranteed Notes due 2014 |

|

New York Stock Exchange |

| 1.700% Guaranteed Notes due 2014 |

|

New York Stock Exchange |

| 0.700% Guaranteed Notes due 2015 |

|

New York Stock Exchange |

| 3.875% Guaranteed Notes due 2015 |

|

New York Stock Exchange |

| 3.125% Guaranteed Notes due 2015 |

|

New York Stock Exchange |

| 2.248% Guaranteed Notes due 2016 |

|

New York Stock Exchange |

| 3.200% Guaranteed Notes due 2016 |

|

New York Stock Exchange |

| 1.375% Guaranteed Notes due 2017 |

|

New York Stock Exchange |

| 1.375% Guaranteed Notes due 2018 |

|

New York Stock Exchange |

| 2.241% Guaranteed Notes due 2018 |

|

New York Stock Exchange |

| 1.846% Guaranteed Notes due 2017 |

|

New York Stock Exchange |

| 4.750% Guaranteed Notes due 2019 |

|

New York Stock Exchange |

| 2.237% Guaranteed Notes due 2019 |

|

New York Stock Exchange |

| 4.500% Guaranteed Notes due 2020 |

|

New York Stock Exchange |

| 4.742% Guaranteed Notes due 2021 |

|

New York Stock Exchange |

| 3.561% Guaranteed Notes due 2021 |

|

New York Stock Exchange |

| 2.500% Guaranteed Notes due 2022 |

|

New York Stock Exchange |

| 3.245% Guaranteed Notes due 2022 |

|

New York Stock Exchange |

| 2.750% Guaranteed Notes due 2023 |

|

New York Stock Exchange |

| 3.994% Guaranteed Notes due 2023 |

|

New York Stock Exchange |

| 3.814% Guaranteed Notes due 2024 |

|

New York Stock Exchange |

| * |

Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which

there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered

by the annual report.

|

|

|

|

|

| Ordinary Shares of 25c each |

|

|

20,426,632,529 |

|

| Cumulative First Preference Shares of £1 each |

|

|

7,232,838 |

|

| Cumulative Second Preference Shares of £1 each |

|

|

5,473,414 |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the Registrant (1) has

filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such

files).* Yes ¨ No ¨

| * |

This requirement does not apply to the registrant in respect of this filing. |

Indicate by check

mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated

filer x Accelerated

filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting

Standards as issued by the

U.S.

GAAP ¨ International Accounting Standards Board x Other ¨

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the

registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Annual Report and

Form 20-F 2013

bp.com/annualreport

Building a stronger,

safer BP

|

|

|

|

|

|

|

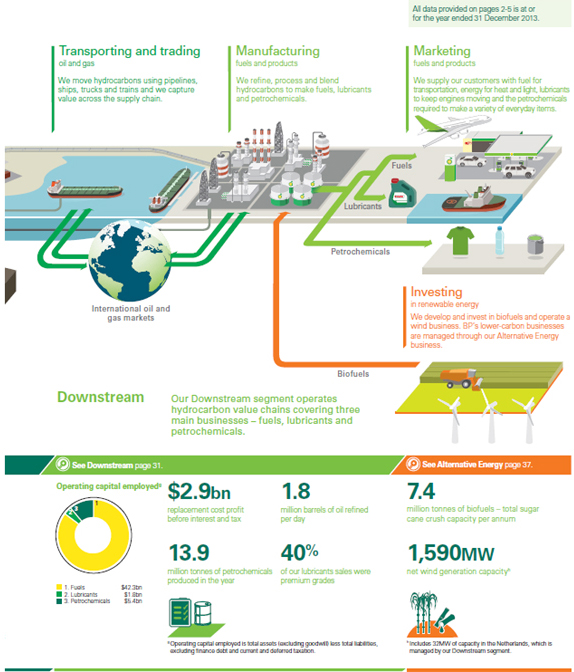

| Who we are

BP is one of the world’s leading integrated oil and

gas companies.a We aim to create

long-term value

for shareholders by helping to meet growing

demand for energy in a safe and responsible way.

We strive to be a world-class operator, a responsible corporate citizen and a good employer. |

|

|

|

|

|

|

| Through our work we provide customers with fuel for transportation, energy for heat and light, lubricants to keep engines moving and the petrochemicals products used to make everyday items as diverse as paints,

clothes and packaging. Our projects and operations help to generate employment, investment and tax revenues in countries and communities around the world. We employ more than 80,000 people, mostly in Europe and the US. |

|

As a global group, our interests and activities are held or operated through subsidiaries, branches, joint arrangements or associates established in – and subject to the laws and regulations of – many

different jurisdictions. The UK is a centre for trading, legal, finance, research and technology and other business functions. We have well-established operations in Europe, the US, Canada, Russia, South America, Australasia, Asia and parts of

Africa. |

|

|

|

|

|

|

|

|

|

|

a On the basis of market capitalization, proved reserves and

production. |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

Front cover imagery Our

second BP-operated development in Angola consists of four oil fields – Plutăo, Saturno, Vénus and Marte (PSVM).

Left image: the converted hull, floating, production, storage and offloading vessel (FPSO) has 1.6 million barrels of storage

capacity. Centre image: a PSVM mechanical technician takes part in a

site visit on board the vessel. Right image: the hawser is a 75

metre rope that we use to tie the tanker to the back of the FPSO. |

|

|

|

Your feedback

We welcome your comments and feedback on our reporting. Your views are important to us and help us shape our reporting for future years.

You can provide this at

bp.com/annualreportfeedback or by emailing or writing to the corporate reporting team. Details are on the back cover. For every survey

completed, we will make a £2 donation to the British Paralympic Association. |

BP Annual Report and Form 20-F 2013

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

i |

|

|

|

| Information about this report |

|

|

|

|

|

|

|

|

|

| Frequent abbreviations

ADR American depositary receipt.

ADS American depositary share.

Barrel (bbl) 159 litres, 42 US gallons.

bcf Billion cubic feet.

bcf/d Billion cubic feet per day.

bcfe Billion cubic feet equivalent.

bcma Billion cubic metres per annum.

b/d Barrels per day.

boe Barrels of oil equivalent.

GAAP Generally accepted accounting practice.

Gas Natural gas.

Hydrocarbons Liquids and natural gas.

IFRS International Financial Reporting Standards.

Liquids Crude oil, condensate and natural gas liquids.

LNG Liquefied natural gas.

LPG Liquefied petroleum gas.

mb/d Thousand barrels per day.

mboe/d Thousand barrels of oil equivalent per day.

mmboe Million barrels of oil equivalent.

mmBtu Million British thermal units.

mmcf Million cubic feet.

mmcf/d Million cubic feet per day.

MW Megawatt.

NGLs Natural gas liquids.

PSA Production-sharing agreement.

RC Replacement cost.

SEC The United States Securities and

Exchange Commission. Therm

100,000 British thermal units. Tonne

2,204.6 pounds.

|

|

|

|

This document constitutes the Annual Report and Accounts in accordance with UK requirements and the Annual Report on Form 20-F in accordance

with the US Securities Exchange Act of 1934, for BP p.l.c. for the year ended 31 December 2013. A cross reference to Form 20-F requirements is included on page 282.

The BP Annual Report and 20-F 2013 reflects a number of significant changes in regulations in the UK. The most significant change is the requirement to produce a

new strategic report that replaces the previous business review. The regulations require certain new disclosure to be included in the strategic report including a description of company’s strategy and business model – we have included a

more focused and graphical presentation of BP’s strategy and business model in this report, compared with the 2012 report.

This document contains the Strategic report on pages 1-58 and the inside cover (Who we are section) and the Directors’ report on pages 59-80, 109-114, 116, 200-223

and 235-280. The Strategic report and the Directors’ report together include the management report required by DTR 4.1 of the UK Financial Conduct Authority’s Disclosure and Transparency Rules. The Directors’ remuneration report is on

pages 81-108. The consolidated financial statements of the group are on pages 115-199 and the corresponding reports of the auditor are on pages 120-121.

BP Annual Report and Form 20-F 2013 and BP Strategic Report 2013 (comprising the Strategic report and supplementary information) may be downloaded from

bp.com/annualreport. No material on the BP website, other than the items identified as BP Annual Report and Form 20-F 2013 or BP Strategic Report 2013 (comprising the Strategic report and supplementary information), forms any

part of those documents. References in this document to other documents on the BP website, such as the BP Energy Outlook, are included as an aid to their location and are not incorporated by reference into this document.

BP p.l.c. is the parent company of the BP group of companies. The company was incorporated in 1909 in

England and Wales and changed its name to BP p.l.c. in 2001. Where we refer to the company, we mean BP p.l.c. Unless otherwise stated, the text does not distinguish between the activities and operations of the parent company and those of its

subsidiaries, and information in this document reflects 100% of the assets and operations of the company and its subsidiaries that were consolidated at the date or for the periods indicated, including non-controlling interests.

BP’s primary share listing is the London Stock Exchange. Ordinary shares are also traded on the

Frankfurt Stock Exchange in Germany and, in the US, the company’s securities are traded on the New York Stock Exchange (NYSE) in the form of ADSs (see page 274 for more details).

The term ‘shareholder’ in this report means, unless the context otherwise requires,

investors in the equity capital of BP p.l.c., both direct and indirect. As BP shares, in the form of ADSs, are listed on the NYSE, an Annual Report on Form 20-F is filed with the US Securities and Exchange Commission (SEC). Ordinary shares are

ordinary fully paid shares in BP p.l.c. of 25 cents each. Preference shares are cumulative first preference shares and cumulative second preference shares in BP p.l.c. of £1 each.

|

| |

|

Trade marks of the BP group

appear throughout this Annual Report and Form 20-F in italics. They include: |

| |

|

Aral

ARCO BP

Castrol Castrol

EDGE Field of the Future Fluid Strength Technology Hummingbird

|

|

LoSal Project 20K SaaBre

Veba Combi-Cracking (VCC)

Permasense is a trade mark of Permasense Limited. Pick n Pay is a registered trademark of

Pick n Pay Stores Limited. |

| |

|

|

|

|

| |

|

Registered office and our worldwide

headquarters: |

|

Our agent in the US: |

| |

|

BP p.l.c. 1 St

James’s Square London SW1Y 4PD UK Tel +44 (0)20 7496 4000 |

|

BP America Inc.

501 Westlake Park Boulevard Houston,

Texas 77079 US Tel +1 281

366 2000 |

| |

|

Registered in England and Wales No. 102498.

Stock exchange symbol ‘BP’. |

|

|

| |

|

|

|

|

|

|

|

| ii |

|

BP Annual Report and Form 20-F 2013 |

BP at a glance

|

|

|

| 2 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

3 |

BP around the world

|

|

|

| 4 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

5 |

Chairman’s letter

|

|

|

| |

|

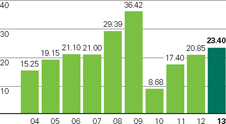

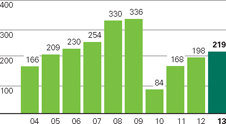

| 10-year dividend history

UK (pence per ordinary share)

US (cents per

ADS)

One ADS represents six 25 cent ordinary shares. |

|

Dear fellow shareholder,

In 2013 BP continued the programme of renewal we began following the crisis of 2010. The measures taken to secure and reshape the group are taking hold. As this report

shows, BP is stronger and safer as a result. Change within the group has taken place against the

backdrop of a rapidly evolving world. The energy landscape is developing at pace, for example, the growth of shale gas in the US. But the long-term supply challenge has not gone away. More energy is required to meet the needs and aspirations of a

rising global population. The BP Energy Outlook projects an average increase in energy demand of 1.5% per year through to 2035. That’s like adding the needs of a country twice the size of the US over the next twenty years.

We are also seeing that society has ever higher expectations of business. This is reflected in the

increasing scrutiny placed on the commercial sector, particularly by politicians and the media. Companies must work hard to maintain people’s trust and respect.

Shareholders’ expectations are shifting too, particularly in the extractive industries sector. Some investors feel that international oil companies have spent too

much for too little return. A decade of mergers and acquisitions in our industry has generated little production growth. Capital expenditure has increased but profit margins have been squeezed. Rightly, shareholders expect better returns.

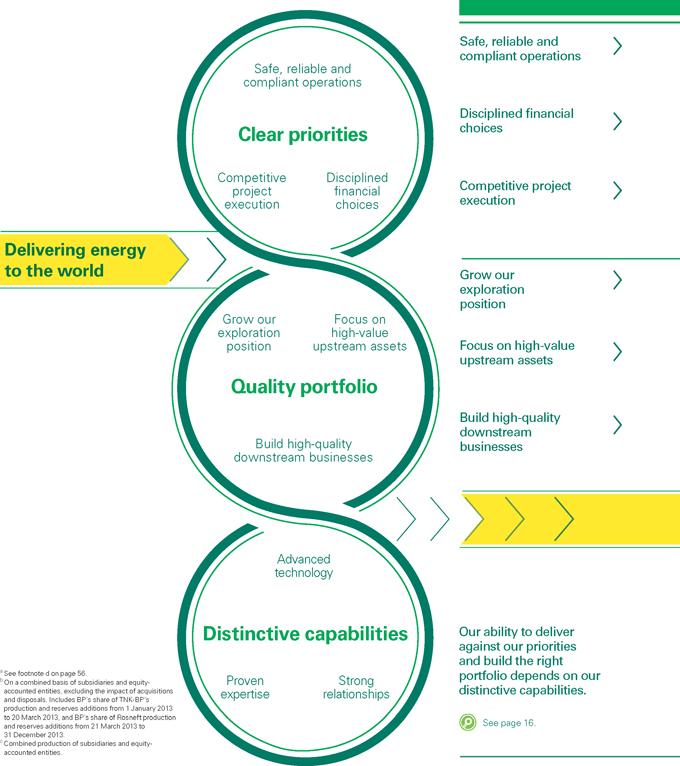

The board recognizes this changing world and the importance of our response. Throughout 2013 we gave

close attention to strategy, project appraisal and capital discipline, working with Bob Dudley and his team to ensure the group spends its money wisely. BP’s strategy is rooted in three imperatives: clear priorities, a quality portfolio and

distinctive capabilities. Our first clear priority is to run safe and reliable operations. We

must also make disciplined financial choices, selecting the smart options that can help meet demand and generate value. Furthermore, we must be competitive in how we execute our projects.

Our quality portfolio, which is at the core of our strategy, is the result of the choices we make. It

contains assets that enable us to play to our areas of greatest strength, from exploration to high-value upstream projects – particularly deepwater operations, giant fields and gas value chains – and high-quality downstream businesses.

To these assets and activities we apply our distinctive capabilities – the expertise of our

people, advanced technology and the ability to build the strong relationships required to access resources and deliver complex projects.

In all of this, we are focused on value before volume. In other words we don’t simply chase production for the sake of it, rather we choose projects where we can

generate the most value through our production. We know we must be disciplined, sticking to clear

limits on capital expenditure, and balancing rewards for shareholders today with the long-term capital investment required for tomorrow. Safety and strong governance must underpin everything we do.

2013 was a busy and successful year for BP, with progress in our underlying operations. Our growing

confidence was reflected in the dividend increase announced in October |

|

|

|

| 6 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

Board performance

Board performance

For information about the board and its

committees see page 71.

Remuneration

Remuneration For information about

our approach to executive directors’ remuneration see

page 20.

€ Top: Members of BP’s safety, ethics and environment assurance committee (SEEAC) visited Canada to see the oil sands operations at the Sunrise project site and meet local community leaders and staff.

€ Bottom: Members of SEEAC travelled to

the Gelsenkirchen refinery in Germany to speak with apprentices and control room operators about risk management and processes.

|

|

2013 – the third increase in two years. We also returned value to shareholders through the $8-billion share repurchase programme announced in March

2013. Additional distributions are planned as we make further divestments to reshape our portfolio. The milestones set for 2014 will be an important measure of progress and your board is monitoring this closely.

I am particularly pleased that in 2013 we completed our transaction with Rosneft, closing one chapter

in Russia and opening another. This is an important investment with the potential to create substantial value for BP over the years to come.

2013 also saw the shocking attack at the In Amenas facility in Algeria. Our thoughts remain with the families and friends of those who died. The response of management to

this tragedy was strong and the board acted positively and promptly. We continue to address

uncertainty in the US. In 2013, we once again met our responsibilities to the region by paying legitimate claims arising from the 2010 accident and oil spill in the Gulf of Mexico. And we met our responsibilities to shareholders by challenging and

resisting any attempt to take advantage of BP with claims that are not legitimate. We will fight through the courts until matters are resolved properly, however long that takes. In the meantime, the board is working to ensure that BP is not

distracted from growing the business and creating shareholder value. Boards set the tone and

values that shape performance and behaviour over the long term. An effective board creates an enduring framework within which management can lead. Having been through challenging times, the BP board has grown into a strong team with experienced

non-executives drawn from relevant industries. This year, more than ever, they have been out to see BP’s operations for themselves, from India to Indiana. We continue to be assisted on geopolitical matters by the international advisory

board. Our approach to governance has enabled us to focus on critical strategic issues, with our

board committees taking on the many oversight and compliance matters that require attention.

Remuneration continues to be a board matter of particular importance to shareholders, with executive pay policy now subject to a vote at the annual general meeting. BP

has a record of ensuring there are clear links between strategy, performance and remuneration. This will continue.

I believe diversity helps to strengthen the effectiveness of a board. We plan succession well ahead and are developing a pipeline of potential board candidates. We are

committed to progress and finding the right people for our board. I would like to end by thanking

you, our shareholders, for your continued support. I also want to acknowledge the people who drive your company forward every working day. From Bob Dudley and his management team to employees across the business; our people are doing a great job of

transforming BP. Their hard work has moved us forward, with the promise of more to come.

Carl-Henric Svanberg

Chairman 6 March

2014 |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

|

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

|

7 |

|

Group chief executive’s letter

|

|

|

|

|

| 95.3% 2013 refining availability. 129% Reserves

replacement ratio, excluding the impact of acquisitions and divestments. See footnote b on page 14. |

|

|

|

Dear fellow shareholder,

For BP, 2013 was a year of good progress in building a safer, stronger and better performing company.

We made new discoveries, started up new operations, strengthened our portfolio and secured a new future in Russia. We also maintained our investment in the US while standing up for what we believe to be right.

Within BP, sadly, 2013 will also be remembered for the terrorist attack in Algeria in January, when

four staff members and 36 colleagues from other companies were killed. Those who died had many friends in BP and our thoughts remain with their loved ones, and with those who survived that terrible ordeal. I was proud of the way people in BP

responded – with great compassion, but also with great fortitude. This report contains a

wealth of information on our performance. I would like to draw out a few of the year’s highlights, all of which demonstrate how we are implementing our strategy, with its emphasis on clear priorities, a quality portfolio and distinctive

capabilities. Clear priorities: safety, capital discipline, project

execution The first of our priorities is to run safe and reliable operations. In 2013 we made good progress overall, but unfortunately we also suffered two

driving-related fatalities as well as the loss of the four employees murdered at In Amenas. Our thoughts are with those who have been bereaved. We will implement the lessons learned.

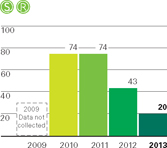

In terms of general safety performance, however, we saw some encouraging progress. The number of tier

1 process safety events – the most significant incidents – fell to 20 from 43 in 2012 and 74 in 2011. We are definitely heading in the right direction, but there is always more to do and we remain vigilant.

We also saw improvements in measures that reflect the underlying health of our business. For example,

in upstream BP-operated plant efficiencya reached 88%, and refining availability in downstream averaged 95.3% – the highest level for 10 years. These numbers reinforce my view that safety and

value have the same roots: systematic, disciplined operations, undertaken by people who respect each other and work as one team.

In terms of capital discipline, in 2013 we invested $24.6 billionb, which kept us within our $25-billion limit, and

we expect to keep capital expenditure broadly the same in 2014. We know we have to invest wisely so we maintain our shareholders’ trust.

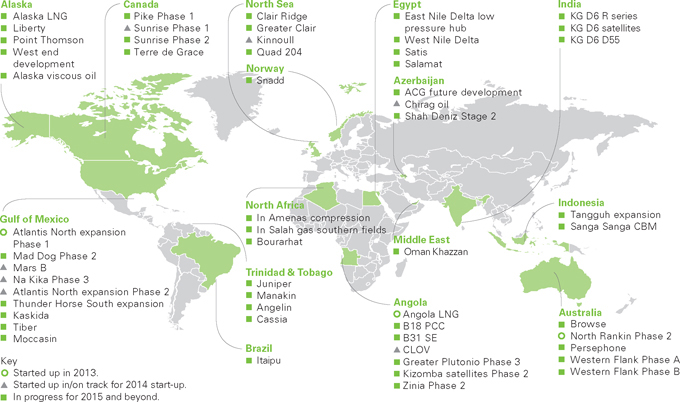

Turning to project execution, we saw three upstream major projects start up in 2013 – in the Gulf of Mexico, Angola and Australia. Three more followed closely in the

first months of 2014 – the Chirag oil project in Azerbaijan and the Mars B and Na Kika Phase 3 projects in the Gulf of Mexico.

Quality portfolio Beyond these start-ups, we

extended our portfolio as a platform for growth in several other ways. For example, we grew our

exploration position by participating in seven potentially commercial discoveries, in Angola, Brazil, Egypt, India and the Gulf of Mexico. We also drilled 17 exploration wells, more than in the previous two years put together. BP has built up great

skills in finding oil and gas and we are seeing the results of investing in our explorers. And in

the US lower 48 – which excludes Alaska and Hawaii – we intend to create a separate BP business to manage our onshore oil and gas assets, which we believe will help to unlock the significant value associated with our extensive resource

position there. |

|

|

|

| 8 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

Our strategy

For more on our strategic priorities and

longer-term objectives see page 13.

€ Top: Bob Dudley and Iraq Oil Minister

Abdul Karim Al Luaibi (right) being shown the first meter to be installed on one of the wells in Kirkuk. In October BP signed an agreement with the government of Iraq on providing technical assistance relating to the Kirkuk oil field.

€ Bottom: Investors see how BP manages

the risks of deepwater drilling at a field trip in Houston. They tested our well simulator which gives rig operators a better understanding of both prevention and response techniques.

a See footnote a on page 25. b Excludes acquisitions and Rosneft transaction. c See page 247 for further information. d See footnote c on page 56. e See footnote b on page 56. |

|

Our reserves replacement ratio was 129% of production. When we include the net growth in our Russian portfolio as a result of the change of our

holdings, the reserves replacement ratio on a combined basis was 199%.c

In the Downstream, we completed the commissioning of all major units for the Whiting refinery. This landmark modernization programme, our fourth major project start-up in

2013, is turning what began as a 19th century plant into a truly 21st century one. It is now able to compete strongly by processing a wide range of crudes, including heavy oil from Canada.

More generally, our Downstream business has transformed its shape over the last five years. In the

US, we have sold two facilities and we now have three modern refineries that are well configured and well connected to important markets. In lubricants, 40% of revenue now comes from our premium brands. In petrochemicals, we are also focusing on

high-growth regions and new technologies. Distinctive

capabilities New acetic acid and ethylene technologies announced by the petrochemical team in 2013 are among a series of innovations we have developed in

support of our exploration, production, refining and marketing activities. These include advanced seismic imaging capacity – using one of the world’s largest civilian supercomputers – enhanced oil recovery techniques and leading

lubricant processes. Our technologies are complemented by the capabilities of our people, which

we continue to deepen through training and development, and our experience in building and maintaining relationships.

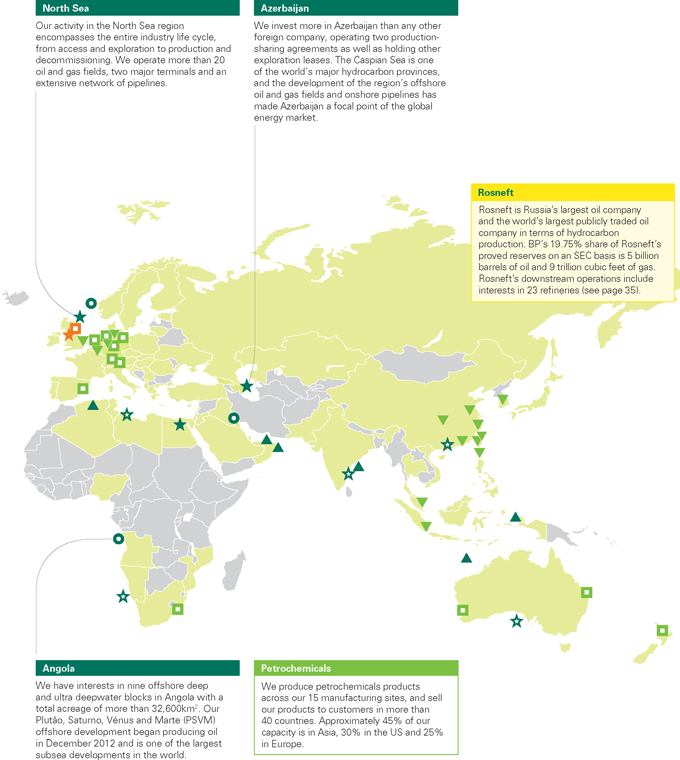

New future in Russia Relationships have been vital

in securing a new future for BP in Russia as a 19.75% shareholder in Rosneft. Rosneft is implementing its strategy for growth across a promising portfolio and paid us a dividend of $456 million in 2013. We look forward to exploring opportunities for

BP to work with Rosneft in the years ahead. Making our case in the

US BP has continued to meet its commitment to environmental and economic restoration in the Gulf of Mexico. We have also been swift to counter illegitimate

claims and to argue for a fair resolution to compensation matters. By the end of the year the total cumulative cost to the company had reached $42.7 billion, the scale of that amount underlining once again that BP is living up to its

responsibilities in the region and to the US as a whole. The US remains vitally important to today’s BP, with around 20,000 employees across the country and we estimate that our economic activity supports a further 240,000 additional jobs.

Nearly 40% of our shares are held in the US, and we invest more there than in any other country. Looking ahead We are a smaller but stronger company, having divested $38 billion of assets over three years. In October we announced

that we would divest around a further $10 billion of assets before the end of 2015 – a decision that reflects our commitment to balancing reinvestment with rewards for our shareholders. We expect to use the proceeds predominantly for

distributions to shareholders, with a bias to share buybacks. Our unrelenting focus on capital

discipline and systematic operating is increasing the free cash flowd we have available. We are on track to meet our goal of generating more than $30 billion of operating cash flow in 2014, an

increase of more than 50% on 2011.e I’m

looking forward to 2014 with great confidence. I think you will see a re-energized and refocused BP – a company that is set to become stronger and safer in every way, as we fulfil our mission of delivering energy to customers and value to

shareholders.

Bob Dudley

Group Chief Executive 6 March

2014 |

|

|

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

|

9 |

|

Our market outlook

|

|

|

|

|

| We believe that a diverse mix of fuels and technologies will

be essential to meet the growing demand for

energy

and the challenges facing our industry. |

|

|

|

|

|

| |

|

|

| Our third PTA plant in Zhuhai, China, is planned to begin production in late 2014.

It is expected to bring total capacity at the site to more than 2.7 million tonnes per year.

{

Thunder Horse in the Gulf of Mexico is one of the largest integrated offshore drilling and production platforms in the world. |

|

Population and economic growth are the main drivers of global energy demand. The world’s population is projected to increase by 1.7 billion from

2012 to 2035, with real income likely to more than double over the same period. Therefore, the

overall trend is likely to be one of increased energy demand, even with energy and climate policies and a shift towards less energy-intense activities in fast-growing economies. We expect demand for energy to increase by as much as 41% between 2012

and 2035. Challenges and opportunities

We seek energy sources that have the following attributes:

Affordability – meeting growing demand for secure and sustainable

energy presents an affordability challenge. Fossil fuels will become increasingly difficult to access and many lower-carbon resources will remain costly to produce at scale.

Security – each country knowing where its supplies will come from. More than 60% of the world’s known reserves of natural gas are

in just five countries and at least 80% of global oil reserves are located in nine countries, most of which are distant from the hubs of energy consumption. This represents a security challenge in its own right.

Sustainability – avoiding an unacceptable environmental and social

impact that ultimately negates the economic benefits. While energy is available to meet growing demand, action is needed to limit carbon dioxide (CO2) and other greenhouse gases emitted through

fossil fuel use. |

|

A diverse mix

We believe a diverse mix of fuels and technologies can enhance national and global energy security while supporting the transition to a lower-carbon economy. These are

reasons why BP’s portfolio includes oil sands, shale gas, deepwater oil and gas, and biofuels.

Oil and natural gas Oil and natural gas are likely

to play a significant part in meeting demand for several decades. We believe these energy sources

will represent about 54% of total energy consumption in 2035. Even under the International Energy Agency’s most ambitious climate policy scenario (the 450 scenario), oil and gas would still make up 47% of the energy mix in 2035.a The 450 scenario assumes governments adopt commitments to limit the long-term concentration of greenhouse gases in the atmosphere to 450 parts-per-million of CO2 equivalent. We expect oil to remain the

dominant source for transport fuels, accounting for as much as 87% of demand in 2035. Natural

gas, in particular, is likely to play an increasingly strategic role. Shale gas is expected to contribute 47% of the growth in global natural gas supplies between 2012 and 2035. The shale gas revolution has already had a significant impact on gas

prices and demand in the US and may encourage similar developments elsewhere although the scale and speed of the roll out of shale gas technology will vary between countries. When used in place of coal for power, natural gas can reduce CO2 emissions by half.

a From World Energy Outlook 2013. ©

OECD/International

Energy Agency 2013, page 573. |

| |

|

|

|

2013 pricing

2013 pricing

See Upstream on page 26 and

Downstream on page 32. |

|

|

|

|

|

|

|

| 10 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

|

|

BP Energy Outlook contains our

projections of future energy trends and factors that could affect them, based on our views of likely economic and population growth and developments in policy and technology. Available in PDF, Excel and video format.

See bp.com/energyoutlook.

See bp.com/energyoutlook.

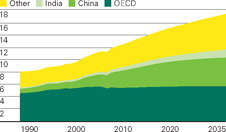

Energy consumption by region

(billion tonnes of oil equivalent)

Source: BP Energy Outlook 2035.

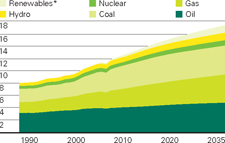

Energy consumption by fuel

(billion tonnes of oil equivalent)

* Includes biofuels.

Source: BP Energy Outlook 2035. |

|

New sources of hydrocarbons are more difficult to reach, extract and process. BP and others in our industry are working to improve techniques for

maximizing recovery from existing and currently inaccessible or undeveloped fields. In many cases, the extraction of these resources might be more energy intensive, which means operating costs and greenhouse gas emissions from operations may also

increase. Renewable energy

Renewables will play an increasingly important role in addressing the challenges of energy security and climate change over the long term. Renewables are already the

fastest-growing energy source, but they are starting from a low base. By 2035, we estimate

renewable energy, excluding large-scale hydro electricity, is likely to meet around 7% of total global energy demand.

Energy efficiency and innovation

Greater efficiency addresses several aspects of the energy challenge. It helps with affordability – because less energy is needed. It helps with security –

because it reduces dependence on imports. And it helps with sustainability – because it reduces emissions.

Innovation can play a key role in improving technology design, process and use of materials, bringing down cost and increasing efficiency. In transport, for example, we

believe that efficient technologies and combustion engines that use biofuels could offer the most cost-effective pathway to a secure, lower-carbon future.

Policy, prices and access

If the world’s growing demand for energy is to be met in a sustainable way, we believe that governments must set a stable and enduring framework for the private

sector to invest and for consumers to choose wisely. This includes secure access for exploration and development |

|

of energy resources, mutual benefits for resource owners and development partners, and an appropriate legal and regulatory environment.

We believe open and competitive markets are the most effective way to encourage companies to find,

produce and distribute diverse forms of energy sustainably. The US experience with shale gas shows how an open and competitive environment can drive technological innovation and unlock resources.

We also believe that putting a price on carbon – one that treats all carbon equally, whether it

comes out of a smokestack or a car exhaust – will make energy efficiency and conservation more attractive to businesses and individuals and lower-carbon energy sources more cost competitive. A global carbon price should be the long-term goal,

but regional and national approaches are a good first step, provided temporary financial relief is given to sectors that are exposed to international competition.

Beyond 2035

We expect that growing population and per capita incomes will continue to drive growing demand for energy. These dynamics will be shaped by future technology

developments, changes in tastes, and future policy choices – all of which are inherently uncertain. Concerns about energy security, affordability and environmental impacts are all likely to be important considerations. These factors may

accelerate the trend towards more diverse sources of energy supply, a lower average carbon footprint, increased efficiency and demand management.

Strategy

Strategy Find out how BP can help meet

energy demand for years to come on

page 13.

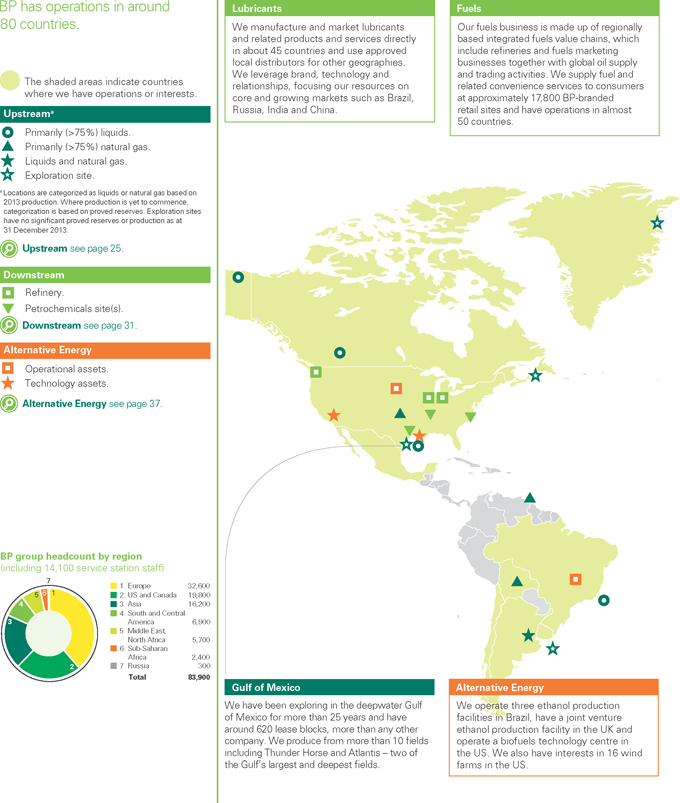

Air BP is one of the world’s largest aviation fuels suppliers, marketing aviation fuels and specialist products in more than 45 countries. It sells over seven billion gallons of fuel per year. |

|

|

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

|

11 |

|

Our business model

|

|

|

|

|

| We aim to create shareholder value across the

hydrocarbon value chain. |

|

|

|

|

|

| |

|

|

| Toledo refinery in Ohio has been in constant operation since 1919. The facility

has the capacity to process up to 160,000 barrels of crude per day. { The redevelopment

project at Valhall was one of

BP’s most complex field expansion

developments and gives the field a further

40-year design life. |

|

A rising global population and increasing levels of prosperity are set to create growing demand for energy for years to come. We can help to meet that

demand by producing oil and gas safely and reliably. We believe that the best way to achieve

sustainable success as a group is to act in the long-term interests of our shareholders, our partners and society. We aim to create value for our investors and benefits for the communities and societies in which we operate, with the responsible

supply of energy playing a vital role in economic development. Every stage of the hydrocarbon

value chain offers opportunities for us to create value – both through the successful execution of activities that are core to our industry, and through the application of our own distinctive strengths and capabilities in performing those

activities. In renewable energy our focus is on integrating biofuels into the hydrocarbon value chain, and on wind operations in the US. |

|

Our approach spans everything from exploration to marketing. Integration across the group allows us to share functional excellence more efficiently

across areas such as safety and operational risk, environmental and social practices, procurement, technology and treasury management.

A relentless focus on safety remains the top priority for everyone at BP. Rigorous management of risk helps to protect the people at the front line, the places in which

we operate and the value we create. We understand that operating in politically complex regions and technically demanding geographies requires particular sensitivity to local environments.

Our businesses

Our businesses For more information on our

upstream, downstream and alternative energy

businesses, see pages 25, 31 and 37

respectively. |

Our business model

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

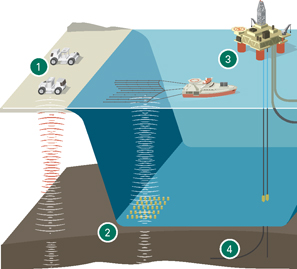

| Finding oil

and gas |

|

g |

|

|

|

Developing and extracting |

|

g |

|

|

|

Transporting and trading |

|

g |

|

|

|

Manufacturing and marketing |

|

|

|

|

|

|

|

| First, we acquire the rights to explore for oil and gas. Through our exploration activities we are able to renew

our portfolio, discover new resources and replenish our development options. |

|

|

|

When we find hydrocarbon resources, we create value by seeking to progress them into proved reserves or by divesting if they do not fit with our strategy. If we believe developing

and producing the reserves will be advantageous for BP, we produce the oil and gas, then sell it to the market or distribute it to our downstream facilities. |

|

|

|

We move oil and gas through pipelines and by ship, truck and train. Using our trading and supply skills and knowledge, we buy and sell at each stage in the value chain. Our

presence across major trading hubs gives us a good understanding of regional and international markets and allows us to create value through entrepreneurial trading. |

|

|

|

Using our technology and expertise, we manufacture fuels and products, creating value by seeking to operate a high-quality portfolio of well- located assets safely, reliably and efficiently.

We market our products to consumers and other end-users and add value through the strength of our brands. |

Our illustrated business model see page 2.

|

|

|

| 12 |

|

BP Annual Report and Form 20-F 2013 |

Our strategy

|

|

|

|

|

| Our goal is to be a focused oil and gas company that

delivers value over volume. |

|

|

|

a See footnote a on page 56. b Equivalent to net cash used in investing activities. c See footnote c on page 56. d See footnote h on page 24. e Excludes acquisitions and asset exchanges. f Unit cash margin is net cash provided by operating activities

by the relevant projects in our Upstream segment,

divided by the total number of barrels of oil

equivalent produced for the relevant projects.

g Assuming a constant oil price of $100 per barrel.

h See footnote b on page 56.

i See footnote d on page 56. |

|

We are pursuing our strategy by setting clear priorities, actively managing a quality portfolio and employing our distinctive capabilities. Our

financial objective is to create shareholder value by generating sustainable free cash flow (operating cash flow less net investment). This disciplined approach enables us to invest for the future while aiming to increase distributions to our

investors. Clear priorities

First, we aim to run safe, reliable and compliant operations – leading to better operational

efficiency and safety performance. We also aim to achieve competitive project execution, which is about delivering projects efficiently so they are on time and on budget. And we aim to make disciplined financial choices, so we can achieve continued

growth in operating cash from our underlying businesses and disciplined allocation of capital. Quality portfolio We undertake active portfolio management to concentrate

on areas where we can play to our strengths. This means we continue to grow our exploration position, reloading our upstream pipeline. We focus on high-value upstream assets in deepwater, giant fields and selected gas value chains. And, with our

downstream businesses, we plan to leverage our newly upgraded assets, customer relationships and technology to grow free cash flow. |

|

Our portfolio of projects and operations is focused where we can generate the most value, and not necessarily the most volume, through our

production. Distinctive capabilities

Our ability to deliver against our priorities and build the right portfolio depends on our

distinctive capabilities. We apply advanced technology across the hydrocarbon value chain, from finding resources to developing energy-efficient and high-performance products for customers. We rely on our strong relationships – with

governments, partners, civil society and others – to enable our operations in around 80 countries across the globe. And, the proven expertise of our employees comes to the fore in a wide range of disciplines.

Our strategy in action See page 14 for more

information on how we are going to measure our

progress. |

| |

10-point plan

2011-2014 In 2011 we laid out a 10-point plan designed to stabilize the company and

restore trust and value in response to the tragic Deepwater Horizon accident. Our priority was to make BP a safer, more risk-aware business. The plan included a series of milestones by which our progress could be tracked, from 2012 through to 2014.

Information on our progress during 2013 can be found in Group performance on page 22. |

| |

1 A

relentless focus on safety and managing risk through the systematic application of global standards.

2 We will play to our strengths in exploration, deep water, giant fields and gas value chains.

3 Stronger and more focused

with an asset base that is high graded and higher performing.

4 Simpler and more standardized with fewer assets and operations in fewer countries; more

streamlined internal reward and performance management processes.

5 Improved transparency through reporting TNK-BP as a separate segment and breaking out the numbers

for the three downstream businesses. |

|

6 Active

portfolio management to continue by completing $38 billion of disposals over the four years to the end of 2013, in order to focus on our strengths.

7 We expect to bring new upstream projects onstream with unit operating cash marginsf around double the 2011 average by 2014.g

8 We are aiming to generate an increase of around 50% in net cash provided by operating activities

by 2014 compared with 2011.h

9 We intend to use half our incremental operating cash for reinvestment, half for other

purposes. 10 Strong balance sheet with

intention to target our level of gearingi in the lower half of the 10-20% range over time. |

|

|

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

|

13 |

|

Our strategy in action

|

|

|

| 14 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| We prioritize the safety and reliability of our operations to protect the welfare of our workforce and the environment. This also helps preserve value and secure our right to operate around the

world. |

|

|

|

Recordable injury frequency, loss of primary containment, greenhouse gas emissions, tier 1 process safety events. |

|

|

|

|

|

A commitment to safe operations Toledo refinery sets a safety

record.

See page 42.

See page 42. |

|

31 fewer

reported losses of primary containment than 2012. |

|

|

|

|

|

|

|

| We rigorously screen our investments and we work to keep our annual capital expenditure within a set range. Ongoing management of our portfolio helps ensure focus on more value-driven propositions. We

balance funds between shareholder distributions and investment for the future. |

|

|

|

Operating cash flow, gearinga, total shareholder return, replacement cost

profit (loss) per ordinary share. |

|

|

|

|

|

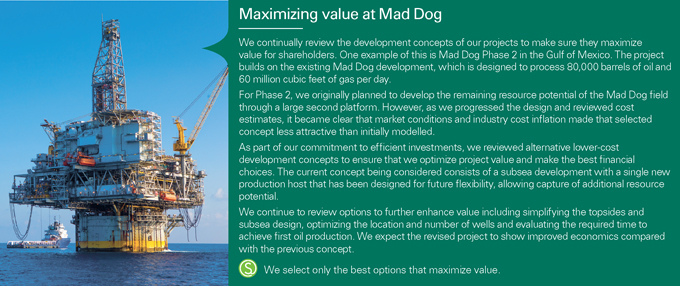

Maximizing value at Mad Dog Changing plans to make the best financial choices.

See page 29. |

|

$21.1bn

operating cash flow. |

|

|

|

|

|

|

|

| We seek efficient ways to deliver projects on time and on budget, from planning through to day-to-day operations. Our wide-ranging project experience makes us a

valued partner and enhances our ability to compete. |

|

|

|

Major project delivery. |

|

|

|

|

|

Increasing oil production

in Azerbaijan Local construction of BP’s

heaviest platform in the Caspian Sea.

See page 48. |

|

4

major project start-ups in

Upstream and Downstream. |

|

|

|

|

|

|

|

| We target basins and prospects with the greatest potential to create value, using our leading subsurface capabilities. This allows us to build a strong pipeline of future growth opportunities. |

|

|

|

Reserves replacement ratio.b |

|

|

|

|

|

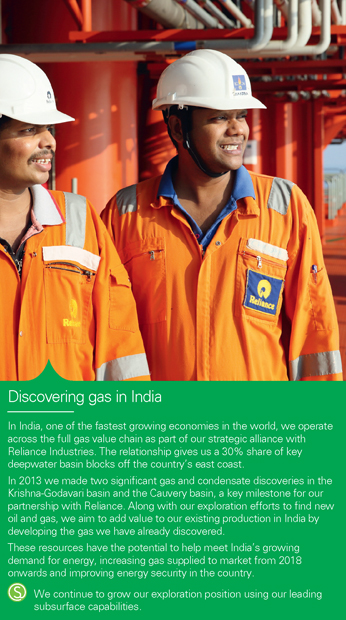

Discovering gas in India Two

significant discoveries with Reliance Industries.

See page 30. |

|

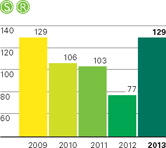

129%

reserves replacement

ratio. |

|

|

|

|

|

|

|

| We are strengthening our portfolio of high return and longer life assets – across deep water, giant fields and gas value chains – to provide BP with momentum for decades to come. |

|

|

|

Production.c |

|

|

|

|

|

Preparing for Shah Deniz Stage 2

Largest gas sales contracts in Azerbaijan’s history.

See page 27. |

|

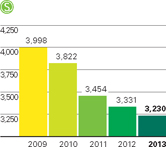

3.2

million barrels of oil equivalent

per day. |

|

|

|

|

|

|

|

| We benefit from our high-performing fuels, lubricants, petrochemicals and biofuels businesses. Through premium products, powerful brands and supply and trading, Downstream provides strong cash generation

for the group. |

|

|

|

Refining availability. |

|

|

|

|

|

Creating our North American advantaged refinery

Modernization project improves utilization and margin capture at Whiting.

See page 33. |

|

95.3%

refining availability. |

|

| Creating shareholder value by

generating sustainable free cash flow

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

| Advanced technology |

|

Strong relationships |

|

Proven expertise |

We develop and deploy technologies

we expect to make the greatest impact on

our businesses – from enhancing the safety

and reliability of our operations to

creating

competitive advantage in energy discovery,

recovery, efficiency and products. |

|

We form enduring partnerships in the

countries in which we operate, building strong

relationships with governments, customers,

partners such as Rosneft, suppliers and

communities to

create mutual advantage.

Co-operation helps unlock resources found in

challenging locations and transforms them into

products for our customers. |

|

We attract and develop the talented people

required to drive our business forward.

They apply their diverse skills and expertise

to deliver complex projects across all areas

of our business. |

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

15 |

Our distinctive capabilities

|

|

|

|

|

| We use technology to find and produce more hydrocarbons, improve our processes for converting raw materials and

develop lower-carbon products. The development of technology from

research and development through to wide-scale deployment can take several years. For example, to reach the next generation of deepwater oil reserves, where rock pressures can reach 20,000 pounds per square inch, we are developing new subsea

technologies through our Project 20K. Technology programmes

in our upstream business include advanced seismic imaging to help us find more oil and gas and enhanced oil recovery to get more from existing fields. New techniques are making recovery of unconventional oil and gas, like shale, economically

viable.

See bp.com/technology.

See bp.com/technology.

The Pangbourne

technology centre is home to chemists and liquid engineers dedicated to providing products and services for Castrol’s customers. |

|

We focus our downstream technology programmes on the safety, integrity and performance of our refineries and petrochemical plants

and on creating high quality, energy efficient, cleaner fuels, lubricants and petrochemicals.

BP employs more than 2,000 scientists and technologists.

Our long-term research programmes with universities and research institutions around the world are exploring areas from reservoir fluid flow to

energy biosciences. We have a strategic approach to university relationships across our portfolio for the purposes of research, recruitment, policy insights and education.

In 2013 we invested $707 million in research and development (2012 $674

million). See Financial statements – Note 8. |

|

|

| |

Seismic imaging

Seismic imaging We use our imaging expertise to

increase the productivity and quality of the data we capture on land and offshore. With 80% of future offshore oil and gas reserves thought to be under salt canopies up to 7 kilometres high, our new supercomputer in Houston helps to reduce the

completion times for imaging jobs from several months to a matter of days. |

|

Enhanced oil recovery (EOR)

Enhanced oil recovery (EOR) Our

LoSal EOR technology can help develop previously unexploited resources from existing oil fields. LoSal uses water with a low salt content to release more molecules of oil from the sandstone rock where they are held.

|

| |

Production optimization

Production optimization Our Field of the

Future technologies provide real-time information to help manage operational risk, improve plant equipment reliability and optimize production. We use these technologies to monitor more than 600 wells. |

|

Shipping efficiency

Shipping efficiency Our ‘virtual

arrival’ system can reduce fuel consumption and emissions by allowing vessels, ports and other parties to work together and agree an optimum arrival time for each vessel. |

|

|

|

|

|

| Our employees enable BP to deliver our strategy and meet our commitments to investors, partners and the wider world.

Our people are talented in a wide range of disciplines, from geoscience,

mechanical engineering and research technology to government affairs, trading, marketing, legal and others. And our approach to professional development programmes and training helps build individual capabilities, reducing a potential skills gap.

This is vital in a world where oil and gas companies face an increasing challenge to find and retain skilled and experienced people.

We aim to achieve a balance between building internal expertise and recruiting external professionals and graduates. We have a strong, experienced

leadership team and a pipeline of talent for the future. |

|

|

|

|

|

| 16 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

|

|

Improved conversion

Improved conversion Our Veba Combi-Cracking

technology converts a wide variety of raw materials, ranging from crude oil residue to mixtures of coal and oil, into fuels. Using this technology we can convert 95% or more of our hydrocarbon resources to marketable products. |

|

Fuels and lubricants

Fuels and lubricants We focus on providing

energy-efficient and high-performance products to customers. Castrol EDGE, which is underpinned by our proprietary Fluid Strength Technology, reduces contact between engine surfaces to improve performance and reduce wear from

friction. |

|

Biofuels

Biofuels Conversion technology allows us to produce

cellulosic ethanol using alternative raw materials such as agricultural waste and fast-growing energy grasses. At our biofuels technology centre in San Diego around 120 scientists are researching and advancing new biofuels

technologies. |

|

Corrosion prevention

Corrosion prevention Wireless Permasense® systems, developed in collaboration with Imperial College, London, are used across all our refineries to monitor the integrity of critical oil and gas assets. |

|

Petrochemicals

Petrochemicals Our SaaBre technology converts

synthesis gas (carbon monoxide and hydrogen derived from hydrocarbons) into acetic acid. The process avoids the need to purify carbon monoxide or purchase methanol, reducing manufacturing costs and environmental impacts. |

|

|

|

|

|

|

|

| Our relationships are crucial to the success of our business. We work closely with governments, national oil companies and other

resource holders. By acting responsibly and meeting our obligations we build long-lasting relationships.

From experience we know that trust can be lost, so we place enormous importance on meeting people’s expectations. We work in partnership on big

and complex projects with everyone from other oil companies through to suppliers and |

|

contractors. Our activity creates value that benefits governments, customers, local communities and other partners.

Internally we put together collaborative teams of people with the skills and

experience needed to address complex issues, work effectively with our partners and help create shared value. |

|

|

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

17 |

Our key performance indicators

|

|

|

|

|

|

|

| We assess the group’s performance according to a wide range of measures and

indicators. Our key performance indicators (KPIs) help the board and executive management measure performance against our strategic priorities and business plans. We keep these metrics under periodic review and test their relevance to our strategy

regularly. We believe non-financial measures – such as safety and an engaged and diverse workforce – have a useful role to play as leading indicators of future performance.

Changes to KPIs

This year, we introduced two new KPIs: tier 1 process safety events and major project delivery. These demonstrate two of our strategic objectives and are used as measures

for executive remuneration. We have removed the number of oil spills as a group KPI as this is

reflected within the loss of primary containment and tier 1 process safety events KPIs. We continue to report on oil spills, see Safety on page 41.

Remuneration To help align the focus of our board

and executive management with the interests of our shareholders, certain measures are reflected in the variable elements of executive remuneration.

Overall annual bonuses, deferred bonuses and performance shares are all based on performance against measures and targets linked directly to strategy and KPIs. For

details of our remuneration policy see page 96.

KPIs used to measure

KPIs used to measure progress against our

strategy.

KPIs used to determine 2013

KPIs used to determine 2013 and 2014 remuneration.

|

|

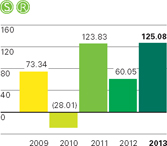

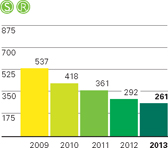

Replacement cost profit (loss) per ordinary share (cents)

Replacement cost profit (loss) is a useful measure for investors

because it is a profitability measure BP management use to assess performance and allocate resources.

It reflects the replacement cost of supplies and is calculated by removing inventory holding gains and losses and their associated tax effect from profit. This is a

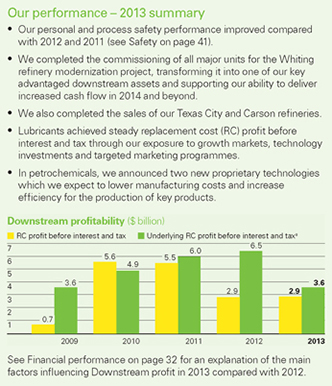

non-GAAP measure for the group. The IFRS equivalent can be found on page 236. 2013 performance The increase in replacement cost profit per ordinary share for the year compared with 2012 reflected the gain on disposal of our interest in TNK-BP. |

|

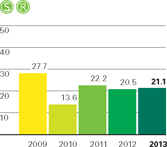

Operating cash flow ($ billion)

Operating cash flow is net cash flow provided by operating

activities, from the group cash flow statement. Operating activities are the principal revenue-generating activities of the group and other activities that are not investing or financing activities.

2013 performance Higher operating cash flow in 2013 reflected a lower

cash outflow relating to the Gulf of Mexico oil spill, partly offset by higher cash outflows as a result of working capital build. |

|

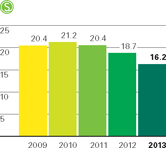

Gearing (net debt ratio) (%)

Our gearing (net debt ratio) shows investors how significant net

debt is relative to equity from shareholders in funding BP’s operations. We aim to keep our

gearing within the 10-20% range to give us the flexibility to deal with an uncertain environment.

Gearing is calculated by dividing net debt by total equity plus net debt. Net debt is equal to gross finance debt, plus associated derivative financial instruments, less

cash and cash equivalents. Net debt and net debt ratio are non-GAAP measures. See Financial statements – Note 28 for the nearest equivalent measure on an IFRS basis and for further information.

2013 performance Gearing at the end of 2013 was 16.2%, down 2.5% on 2012

and within our target band of 10-20%. |

| |

|

| |

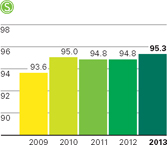

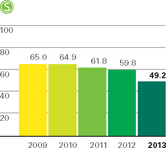

Refining availability (%)

Refining availability represents Solomon Associates’

operational availability. The measure shows the percentage of the year that a unit is available for processing after deducting the time spent on turnaround activity and all mechanical, process and regulatory maintenance downtime.

Refining availability is an important indicator of the operational performance of our Downstream

businesses. 2013 performance Refining availability increased by 0.5%

from 2012 to 95.3% reflecting strong operations around our global refining portfolio. |

|

Reported recordable injury frequencya

Reported recordable injury frequency (RIF) measures the number of

reported work-related employee and contractor incidents that result in a fatality or injury (apart from minor first aid cases) per 200,000 hours worked.

The measure gives an indication of the personal safety of our workforce.

2013 performance Our workforce RIF, which includes employees and contractors combined, was 0.31, compared with 0.35 in 2012 and 0.36 in 2011.

These successive reductions are encouraging and we continue pursuing improvement in personal safety. |

|

Loss of primary containmenta

Loss of primary containment (LOPC) is the number of unplanned or

uncontrolled releases of oil, gas or other hazardous materials from a tank, vessel, pipe, railcar or other equipment used for containment or transfer.

By tracking these losses we can monitor the safety and efficiency of our operations as well as our progress in making improvements.

2013 performance Our reported LOPC shows 31 fewer reported incidents in

2013 than in 2012, with divestments accounting for a significant part of the reduction. We remain committed to using our operating management system to further improve our operations. |

|

|

|

| 18 |

|

BP Annual Report and Form 20-F 2013 |

|

|

|

|

|

|

|

| Total shareholder return (%)

Total shareholder return (TSR) represents the change in value of a

BP shareholding over a calendar year. It assumes that dividends are re-invested to purchase additional shares at the closing price on the ex-dividend date.

We are committed to maintaining a progressive and sustainable dividend policy.

2013 performance TSR grew as a result of increases in both the BP share price and in the dividend, with the improvement for ordinary shares

slightly offset by exchange rate effects. |

|

Reserves replacement ratio (%)

Proved reserves replacement ratio is the extent to which the

year’s production has been replaced by proved reserves added to our reserve base. The ratio

is expressed in oil-equivalent terms and includes changes resulting from discoveries, improved recovery and extensions and revisions to previous estimates, but excludes changes resulting from acquisitions and disposals. The ratio reflects both

subsidiaries and equity-accounted entities. The measure helps to demonstrate our success in

accessing, exploring and extracting resources. 2013 performance The

increase in our reserves replacement ratio included the impact of final investment decisions on two significant upstream projects in Oman and Azerbaijan. |

|

Major project delivery

Major projects are defined as large-scale projects with a high

degree of complexity and a BP net investment of at least $250 million. We monitor the progress of

our major projects to gauge whether we are delivering our core pipeline of activity. Projects take many years to complete, requiring differing amounts of resource, so a smooth or increasing trend should not be anticipated.

2013 performance In total we delivered four major projects. Three

started up in Upstream – Atlantis North expansion Phase 1 in the Gulf of Mexico; Angola LNG; and North Rankin Phase 2 in Australia, and one in Downstream – the Whiting refinery modernization project. |

|

Production (mboe/d)

We report the volume of crude oil, condensate, natural gas liquids

(NGLs) and natural gas produced by subsidiaries and equity-accounted entities. These are converted to barrels of oil equivalent (boe) at 1 barrel of NGL = 1boe and 5,800 standard cubic feet of natural gas = 1boe.

2013 performance BP’s total reported production including our

Upstream segment, and our share of TNK-BP (from 1 January to 20 March) and Rosneft (from 21 March to 31 December), was 3% lower than in 2012. This was mainly due to the effect of divestments in Upstream. |

|

|

|

|

| |

|

|

|

|

|

|

| Tier 1 process safety eventsa

We report tier 1 process safety events (PSE), which are the losses

of primary containment of greatest consequence – causing harm to a member of the workforce, costly damage to equipment or exceeding defined quantities.

2013 performance Our reduction in reported tier 1 PSEs is supported by our efforts to drive improvement in process safety. Divestments also

account for part of the reduction. We are aware there is always more to do to improve.

a This represents reported incidents occurring

within BP’s operational HSSE reporting

boundary. That boundary includes BP’s

own operated facilities and certain other

locations or situations. |

|

Greenhouse gas emissions (million tonnes of CO2 equivalent)

We report greenhouse gas (GHG) emissions material to our business

on a carbon dioxide-equivalent basis. This includes CO2 and methane for direct emissions.b Our GHG reporting encompasses all BP’s

consolidated entities as well as our share of equity-accounted entities other than BP’s share of TNK-BP and Rosneft. Rosneft’s emissions data can be found on its website.

2013 performance Our total greenhouse gas emissions decreased by 18%,

primarily due to the divestment of our Texas City and Carson refineries.

b For indirect emissions data see page 45. |

|

Group priorities engagementc (%)

We track how engaged our employees are with our strategic

priorities for building long-term value. The measure is derived from answers to 12 questions about BP as a company and how it is managed in terms of leadership and standards.

2013 performance We saw continued improvement in 2013, and there was an increase in understanding of our operating management system, an area

of focus identified the previous year. While the survey showed an increase in employee confidence in BP’s leadership, work is needed to further strengthen this.

c Relates to BP employees. |

|

Diversity and inclusionc d (%)

Each year we report the percentage of women and individuals from

countries other than the UK and US among BP’s group leaders. This means we can track

progress in building a diverse and well-balanced leadership team, helping to create a sustainable pipeline of diverse talent for the future.

2013 performance We have increased the percentage of female leaders again this year and have extended our focus on diversity and inclusion

beyond the board and group leaders to include other levels of management.

d Minor amendments have been made to

2012. |

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

19 |

Our approach to executive

directors’ remuneration

Remuneration is directly linked to strategy and performance, with

particular emphasis on matching rewards to results over the long term.

|

|

|

| A simple approach |

|

|

| Total remuneration is determined by a relatively simple approach to attract and retain high calibre executives. The largest components are share based and vest over a number of years – further aligning

executives’ interests with those of our shareholders. |

|

|

Underpinned by six key principles

The remuneration policy for executive directors and the

decisions of the remuneration committee of the board

are guided by six key principles:

A substantial portion of executive remuneration is linked to success in implementing the

company’s strategy.

Strategic priorities and group key performance indicators (KPIs) provide key metrics for the performance shares and deferred bonus,

and are focused through the annual plan to provide the measures for annual bonus.

The major part of total remuneration varies with performance, with the largest elements share based,

further aligning interests with shareholders.

High pay requires high performance. Achieving the maximum pay requires sustained high performance over several

years.

|

|

|

| 20 |

|

BP Annual Report and Form 20-F 2013 |

The structure of pay is designed to reflect the long-term nature of BP’s business and the

significance of safety and environmental risks.

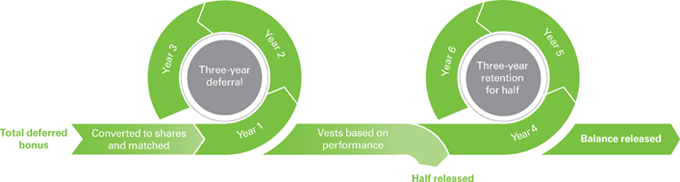

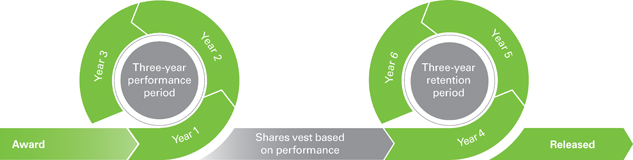

The largest components of total remuneration are share based and vest over the longest period. The deferred

bonus plan requires sustained safety and environmental performance

over three years. The matched shares that vest under the plan have an additional three-year retention period, resulting in

a six-year time frame. Similarly, performance shares have a six-year time frame – a three-year performance period followed by an additional three-year retention period for those shares that vest.

There are quantitative and qualitative assessments of performance with the remuneration committee

making informed judgements within a framework approved by shareholders.

The committee has a preference for quantifiable targets that can be factually measured

and objectively assessed according to well understood principles and definitions. It seeks the views of other relevant committees when arriving at conclusions. It is not constrained when conditions change requiring different perspectives or when

unanticipated events, both good and bad, occur.

The remuneration committee actively seeks to understand shareholder preferences and be transparent in

explaining its policy and practice.

During 2013 the remuneration committee chairman met personally with shareholders representing nearly 15% of total

outstanding shares. A number of adjustments to policy were made in response to the feedback received (see page 82).

94%

of votes cast were in favour of the 2012 Directors’ remuneration report.

Total overall pay takes account of both the external market and company conditions to achieve a

balanced, ‘fair’ outcome.

The committee attempts to balance sometimes conflicting perspectives to arrive at total pay results that not only reflect

performance relative to strategy, but also are deemed fair by external stakeholders and employees, as well as the executive team.

|

|

|

| BP Annual Report and Form 20-F 2013 |

|

21 |

Group performance

Our progress in 2013 has set us up well to deliver our

10-point plan and forms the foundations for delivering

value in the long term.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ~

In May we completed the successful commissioning of a state-of-the-art diesel hydrotreater and hydrogen plant at the Cherry Point refinery in

Washington state. { The Mad Dog field in the

Gulf of Mexico was discovered in 1998 and is one of BP’s largest discoveries in the Gulf of Mexico to date. |

|

|

|

We continued to operate within a disciplined financial framework in 2013 – with organic capital expenditurea of $24.6 billion (within

the expected $24-$25 billion range). Upstream BP-operated plant efficiencyb of 88% and strong refining availability of 95.3% in Downstream demonstrated our progress in operational efficiency. We

completed the transactions to increase our shareholding in Rosneft to 19.75%. And, we are continuing to meet our commitments in the Gulf of Mexico, while making our case in court. |

|

|

|

|

|

|

|

|

|

|

|

2013-2014 milestones set out in our 10-point plan

|

|

|

|

|

Drilling up to 25 wells per year. |

|

|

|

|

g |

|

We completed 17 exploration wells and made seven potentially commercial discoveries in 2013. It was our most

successful year for exploration drilling in almost a decade. |

|

|

|

|

A further nine major upstream project start-ups. |

|

|

|

|

g |

|

Three major projects were started up in 2013 and another three in January and February 2014. We expect a further

four major upstream projects to start up in 2014. |

|