| Preliminary Pricing Supplement (To the Prospectus dated August 31, 2010, the Prospectus Supplement dated May 27, 2011 and Index Supplement dated May 31, 2011) |

Filed Pursuant to Rule 424(b)(2) Registration No. 333-169119 |

The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement and the accompanying prospectus and prospectus supplement do not constitute an offer to sell these securities, and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Pricing Supplement dated October 5, 2011

|

Buffered iSuperTrackSM Notes due October 20, 2016 Linked to the S&P 500® Index

Global Medium-Term Notes, Series A, No. E-6925 |

Terms used in this preliminary pricing supplement are described or defined in the prospectus supplement. The Buffered iSuperTrackSM Notes (the “Notes”) offered will have the terms described in the prospectus supplement and the prospectus, as supplemented by this preliminary pricing supplement.

THE NOTES DO NOT GUARANTEE ANY RETURN OF PRINCIPAL AT MATURITY.

| Note |

Reference Asset |

Initial |

Principal |

Annual Periodic Amount per

$1,000 |

Buffer Percentage |

CUSIP/ISIN | ||||||||||||

| E-6925 |

S&P 500® Index (the “Index”) (Bloomberg ticker symbol “SPX <Index>”) | [—] | $ | [ | —] | [$ | 10.00 - $15.00 | ]*** | 20.00 | % | 06738KWK3/ US06738KWK32 | |||||||

| * | Subject to postponement in the event of a market disruption event and as described under “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities” in the prospectus supplement. |

| ** | Subject to postponement in the event of a market disruption event and as described under “Terms of the Notes—Maturity Date” and “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities” in the prospectus supplement. |

| *** | The actual Annual Periodic Amount will be set on the Initial Valuation Date and will not be less than $10.00 per $1,000 principal amount Note. |

Investing in the Notes involves a number of risks. See “Risk Factors” beginning on page S-6 of the prospectus supplement, “Risk Factors” beginning on page IS-2 of the index supplement and “Selected Risk Considerations” beginning on page PPS-4 of this preliminary pricing supplement.

The Notes will not be listed on any U.S. securities exchange or quotation system. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined that this preliminary pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes constitute our direct, unconditional, unsecured and unsubordinated obligations and are not deposit liabilities of Barclays Bank PLC and are not insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency of the United States, the United Kingdom or any other jurisdiction.

| Price to Public |

Agent’s Commission‡ |

Proceeds to Barclays Bank PLC | ||||

| Per Note |

100% | % | % | |||

| Total |

$ | $ | $ |

| ‡ | Barclays Capital Inc. will receive commissions from the Issuer equal to [TBD]% of the principal amount of the Notes, or [$TBD] per $[1,000] principal amount, and may retain all or a portion of these commissions or use all or a portion of these commissions to pay selling concessions or fees to other dealers. Accordingly, the percentage and total proceeds to Issuer listed herein is the minimum amount of proceeds that Issuer receives. |

You may revoke your offer to purchase the Notes at any time prior to the Initial Valuation Date as described on the cover of this preliminary pricing supplement. We reserve the right to change the terms of, or reject any offer to purchase the Notes prior to their issuance. In the event of any changes to the terms of the Notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

ADDITIONAL TERMS SPECIFIC TO THE NOTES

You should read this preliminary pricing supplement together with the prospectus dated August 31, 2010, as supplemented by the prospectus supplement dated May 27, 2011 and the index supplement dated May 31, 2011 relating to our Global Medium-Term Notes, Series A, of which these Notes are a part. This preliminary pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the prospectus supplement and the index supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Prospectus dated August 31, 2010: |

http://www.sec.gov/Archives/edgar/data/312070/000119312510201448/df3asr.htm

| • | Prospectus Supplement dated May 27, 2011: |

http://www.sec.gov/Archives/edgar/data/312070/000119312511152766/d424b3.htm

| • | Index Supplement dated May 31, 2011: |

http://www.sec.gov/Archives/edgar/data/312070/000119312511154632/d424b3.htm

Our SEC file number is 1-10257. As used in this preliminary pricing supplement, the “Company,” “we,” “us,” or “our” refers to Barclays Bank PLC.

What is the Total Return on the Notes at Maturity Assuming a Range of Performance of the Index?

The following table below illustrates the hypothetical total return on the Notes at maturity. The “total return” as used in this preliminary pricing supplement is the number, expressed as a percentage, which results from comparing (a) the Payment at Maturity per $1,000 principal amount plus the aggregate Periodic Amounts paid up to and on the Maturity Date (without taking into account any reinvestment of any such Periodic Amounts), to (b) $1,000. The examples below do not take into account any tax consequences of investing in the Notes.

All hypothetical total returns are for illustrative purposes only and may not be the actual total returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

The hypothetical Initial Level and the hypothetical Final Level of the Index have been chosen arbitrarily for the purpose of these examples and should not be taken as indicative of the future performance of the Index.

Assumptions

| • | Investor purchases $1,000 principal amount of Notes on the Issue Date at the Price to the Public indicated on the cover of this preliminary pricing supplement, holds the Notes to maturity and receives all Periodic Amounts during the term of the Notes in the total amount of $50 per $1,000 principal amount Note, including the final Periodic Amount payable on the Maturity Date. |

PPS–2

| • | No market disruption events, reorganization events or events of default occur during the term of the Notes. |

| • | Initial Level: 1,131.42 |

| • | Buffer Percentage: 20.00% |

| • | Periodic Amounts: $10.00 per $1,000 principal amount Note, paid annually, resulting in aggregate Periodic Amount payments of $50.00 per $1,000 principal amount Note, or 5.00% per Note, over the term of the Notes. |

| Final Level |

Index Return |

Payment at Maturity* (Not Including any Periodic Amount) |

Total Return | |||

| 1,979.99 |

75.00% | $1,750.00 | 80.00% | |||

| 1,923.41 |

70.00% | $1,700.00 | 75.00% | |||

| 1,810.27 |

60.00% | $1,600.00 | 65.00% | |||

| 1,697.13 |

50.00% | $1,500.00 | 55.00% | |||

| 1,583.99 |

40.00% | $1,400.00 | 45.00% | |||

| 1,470.85 |

30.00% | $1,300.00 | 35.00% | |||

| 1,357.70 |

20.00% | $1,200.00 | 25.00% | |||

| 1,244.56 |

10.00% | $1,100.00 | 15.00% | |||

| 1,216.28 |

7.50% | $1,075.00 | 12.50% | |||

| 1,187.99 |

5.00% | $1,050.00 | 10.00% | |||

| 1,159.71 |

2.50% | $1,025.00 | 7.50% | |||

| 1,131.42 |

0.00% | $1,000.00 | 5.00% | |||

| 1,074.85 |

-5.00% | $1,000.00 | 5.00% | |||

| 1,018.28 |

-10.00% | $1,000.00 | 5.00% | |||

| 961.71 |

-15.00% | $1,000.00 | 5.00% | |||

| 905.14 |

-20.00% | $1,000.00 | 5.00% | |||

| 791.99 |

-30.00% | $900.00 | -5.00% | |||

| 678.85 |

-40.00% | $800.00 | -15.00% | |||

| 565.71 |

-50.00% | $700.00 | -25.00% | |||

| 452.57 |

-60.00% | $600.00 | -35.00% | |||

| 339.43 |

-70.00% | $500.00 | -45.00% | |||

| 282.86 |

-75.00% | $450.00 | -50.00% |

| * | per $1,000 principal amount Note |

Hypothetical Examples of Amounts Payable at Maturity

The following examples illustrate how the total returns set forth in the tables above are calculated. In each of the following examples.

Example 1: The Index Return is greater than 0%.

On the Final Valuation Date, the Final Level of 1,187.99 is greater than the Initial Level of 1,131.42, resulting in a positive Index Return of 5.00%. Because the Index Return of 5.00% is greater than 0%, the investor receives, in addition to the final Periodic Amount, a payment at maturity of $1,050 per $1,000 principal amount Note, calculated as follows:

$1,000 + [$1,000 × Index Return]

$1,000 + [$1,000 × (5.00%)] = $1,050.00

The total return on the Notes (including all Periodic Amounts paid during the term of the Notes) will be 10.00% (5.00% + 5.00%).

Example 2: The Final Level is less than the Initial Level by a percentage not greater than the Buffer Percentage.

On the Final Valuation Date, the Final Level of 1,018.28 is less than the Initial Level of 1,131.42, resulting in a negative Index Return of –10.00%. Because the Index Return of –10.00% is greater than –20.00%, on the Maturity Date, the investor receives, in addition to the final Periodic Amount, a payment at maturity of $1,000 per $1,000 principal amount Note.

PPS–3

The total return on the Notes (including all Periodic Amounts paid during the term of the Notes) will be 5.00% (0.00% + 5.00%).

Example 3: The Final Level is less than the Initial Level by a percentage greater than the Buffer Percentage.

On the Final Valuation Date, the Final Level of 791.99 is less than the Initial Level of 1,131.42, resulting in a negative Index Return of –30.00%. Because the Index Return of –30.00% is less than –20.00%, on the Maturity Date, the investor receives, in addition to the final Periodic Amount, a payment at maturity of $900.00 per $1,000 principal amount Note, calculated as follows:

$1,000 + [$1,000 × (Index Return + Buffer Percentage)]

$1,000 + [$1,000 × (–30.00% + 20.00%)] = $900.00

In this case, the investor will lose 10.00% of the principal amount of their Notes. The total return on the Notes (including all Periodic Amounts paid during the term of the Notes) will be -5.00% (-10.00% + 5.00%).

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Index. These risks are explained in more detail in the “Risk Factors” section of the prospectus supplement, including the risk factors discussed under the following headings:

| • | “Risk Factors—Risks Relating to All Securities”; |

| • | “Risk Factors—Additional Risks Relating to Notes Which Are Not Characterized as Being Fully Principal Protected or Are Characterized as Being Partially Protected or Contingently Protected”; |

| • | “Risk Factors—Additional Risks Relating to Securities with a Barrier Percentage or a Barrier Level; and |

| • | “Risk Factors—Additional Risks Relating to Securities with Reference Assets That Are Equity Securities or Shares or Other Interests in Exchange-Traded Funds, That Contain Equity Securities or Shares or Other Interests in Exchange-Traded Funds or That Are Based in Part on Equity Securities or Shares or Other Interests in Exchange-Traded Funds.” |

In addition to the risks discussed under the headings above, you should consider the following:

| • | Your Investment in the Notes May Result in Significant Loss—The Notes do not guarantee any return of principal, even if the Notes are held to maturity. Periodic Amounts will be payable on the dates set forth on the cover page of this preliminary pricing supplement, including the Maturity Date. However, the payment at maturity (excluding the final Periodic Amount payable on the Maturity Date) is linked to the performance of the Index and will depend on whether, and the extent to which, the Index Return is positive or negative. If the Final Level declines from the Initial Level by more than 20%, you will lose 1% of the principal amount of your Notes for every 1% that the Index Return falls below -20%. You may lose up to 80% of the principal amount of your Notes at maturity, without considering the Periodic Amounts. |

| • | Credit of Issuer—The Notes are senior unsecured debt obligations of the issuer, Barclays Bank PLC and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Notes, including payment of any Periodic Amounts and any payment due at maturity, depends on the ability of Barclays Bank PLC to satisfy its obligations as they come due and is not guaranteed by any third party. In the event Barclays Bank PLC were to default on its obligations, you may not receive any amounts owed to you under the terms of the Notes. |

| • | Exposure to U.S. Equities of the S&P 500® Index—The return on the Notes is linked to the Index. The Index consists of 500 component stocks selected to provide a performance benchmark for the U.S. equity markets. For additional information about the Index, see the information set forth under “Non Proprietary Indices—Equity Indices—S&P 500® Index” in the Index Supplement. |

| • | No Dividend Payments or Voting Rights—As a holder of the Notes, you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of the stocks comprising the Index would have. |

PPS–4

| • | The Payment at Maturity of Your Notes (Excluding the Final Periodic Amount) is Not Based on the Level of the Index at Any Time Other than the Final Level on the Final Valuation Date—The Final Level of the Index will be based solely on the Index Closing Level on the Final Valuation Date (subject to adjustments as described in the prospectus supplement). Therefore, if the level of the Index drops precipitously on the Final Valuation Date, the payment at maturity, if any, that you will receive for your Notes (in addition to the final Periodic Amount) may be significantly less than it would otherwise have been had such payment been linked to the level of the Index prior to such drop. Although the level of the Index on the Maturity Date or at other times during the life of your Notes may be higher than the Final Level of the Index on the Final Valuation Date, you will not benefit from any increases in the level of the Index other than the increase, if any, in the level of the Index from the Initial Level on the Initial Valuation Date to the Final Level on the Final Valuation Date. |

| • | Certain Built-In Costs Are Likely to Adversely Affect the Value of the Notes Prior to Maturity—While the Payment at Maturity described in this preliminary pricing supplement is based on the full principal amount of your Notes, the original issue price of the Notes includes the agent’s commission and the cost of hedging our obligations under the Notes through one or more of our affiliates. As a result, the price, if any, at which Barclays Capital Inc. and other affiliates of Barclays Bank PLC will be willing to purchase Notes from you in secondary market transactions will likely be lower than the original issue price, and any sale prior to the maturity date could result in a substantial loss to you. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity. |

| • | Lack of Liquidity—The Notes will not be listed on any securities exchange. Barclays Capital Inc. and other affiliates of Barclays Bank PLC intend to offer to purchase the Notes in the secondary market but are not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which Barclays Capital Inc. and other affiliates of Barclays Bank PLC are willing to buy the Notes. |

| • | Potential Conflicts—We and our affiliates play a variety of roles in connection with the issuance of the Notes, including acting as calculation agent and hedging our obligations under the Notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the Notes. |

| • | Many Economic and Market Factors Will Impact the Value of the Notes—In addition to the level of the Index on any day, the value of the Notes will be affected by a number of economic and market factors that may either offset or magnify each other, including: |

| • | the expected volatility of the Index; |

| • | the time to maturity of the Notes; |

| • | the dividend rate on the common stocks underlying the Index; |

| • | interest and yield rates in the market generally; |

| • | the supply and demand for the Notes; |

| • | a variety of economic, financial, political, regulatory or judicial events; and |

| • | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

| • | Taxes—The U.S. federal income tax treatment of the Notes is uncertain and the Internal Revenue Service could assert that the Notes should be taxed in a manner that is different than described herein. As discussed further in the accompanying prospectus supplement, on December 7, 2007, the Internal Revenue Service issued a notice indicating that it and the Treasury Department are actively considering whether, among other issues, you should be required to accrue interest over the term of an instrument such as the Notes at a rate that may exceed the Periodic Amounts you receive during the term of the Notes and whether all or part of the gain you may recognize upon the sale or maturity of an instrument such as the Notes could be treated as ordinary income. The outcome of this process is uncertain and could apply on a retroactive basis. In addition, any character mismatch arising from your inclusion of ordinary income and capital loss (if any) upon the sale or maturity of your Notes may result in adverse tax consequences to you because an investor's ability to deduct capital losses is subject to significant limitations. You should consult your tax advisor as to the possible alternative treatments in respect of the Notes. |

Selected Purchase Considerations

| • | Market Disruption Events and Adjustments—The Final Valuation Date, the Maturity Date and the payment at maturity are subject to adjustment as described in the following sections of the prospectus supplement: |

| • | For a description of what constitutes a market disruption event with respect to the Index as well as the consequences of that market disruption event, see “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities”; and |

PPS–5

| • | For a description of further adjustments that may affect the Index, see “Reference Assets—Indices—Adjustments Relating to Securities with the Reference Asset Comprised of an Index”. |

| • | Limited Protection (Subject to Our Credit Risk) Only at Maturity and Only to the Extent Afforded By The Buffer Percentage—If the Index Return is negative, payment at maturity of the Notes will depend on the extent to which the Final Level declines from the Initial Level. If the Final Level declines from the Initial Level by more than 20%, you will lose 1% of the principal amount of your Notes for every 1% that the Reference Asset Return falls below -20%. You may lose up to 80% of your initial investment, without considering the Periodic Amounts. Any payment on the Notes, including the payment of any Periodic Amounts and any payment at maturity, is subject to the creditworthiness of the Issuer and is not guaranteed by any third party. For a description of risks with respect to the ability of Barclays Bank PLC to satisfy its obligations as they come due, see “Credit of Issuer” in this preliminary pricing supplement. |

| • | Certain U.S. Federal Income Tax Considerations—Some of the tax consequences of your investment in the Notes are summarized below. The discussion below supplements the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement. Except as noted under “Non-U.S. Holders” below, this section applies to you only if you are a U.S. holder (as defined in the accompanying prospectus supplement) and you hold your Notes as capital assets for tax purposes and does not apply to you if you are a member of a class of holders subject to special rules or are otherwise excluded from the discussion in the prospectus supplement (for example, if you did not purchase your Notes in the initial issuance of the Notes). |

The United States federal income tax consequences of your investment in the Notes are uncertain and the Internal Revenue Service could assert that the Notes should be taxed in a manner that is different than described below. Pursuant to the terms of the Notes, Barclays Bank PLC and you agree, in the absence of a change in law or an administrative or judicial ruling to the contrary, to characterize your Notes as a pre-paid income-bearing executory contract with respect to the Index. If your Notes are so treated, you will likely be taxed on the interest paid on the Notes as ordinary income in accordance with your regular method of accounting for United States federal income tax purposes, and you should generally recognize capital gain or loss upon the sale or maturity of your Notes in an amount equal to the difference between the amount you receive at such time (excluding amounts attributable to interest) and the amount you paid for your Notes. Such gain or loss should generally be long-term capital gain or loss if you have held your Notes for more than one year. Any character mismatch arising from your inclusion of ordinary income and capital loss (if any) upon the sale or maturity of your Notes may result in adverse tax consequences to you because an investor's ability to deduct capital losses is subject to significant limitations.

In the opinion of our special tax counsel, Sullivan & Cromwell LLP, it would be reasonable to treat your Notes in the manner described above. This opinion assumes that the description of the terms of the Notes in this preliminary pricing supplement is materially correct.

As discussed further in the accompanying prospectus supplement, the Treasury Department and the Internal Revenue Service are actively considering various alternative treatments that may apply to instruments such as the Notes, possibly with retroactive effect.

For a further discussion of the tax treatment of your Notes as well as possible alternative characterizations, please see the discussion under the heading “Certain U.S. Federal Income Tax Considerations—Certain Notes Treated as Forward Contracts or Executory Contracts” in the accompanying prospectus supplement. You should consult your tax advisor as to the possible alternative treatments in respect of the Notes. For additional, important considerations related to tax risks associated with investing in the Notes, you should also examine the discussion in “Selected Risk Considerations—Taxes”, in this preliminary pricing supplement.

“Specified Foreign Financial Asset” Reporting. Under legislation enacted in 2010, individuals that own “specified foreign financial assets” with an aggregate value in excess of $50,000 are generally required to file an information report with respect to such assets with their tax returns. “Specified foreign financial assets” include any financial accounts maintained by foreign financial institutions, as well as any of the following (which may include your Notes), but only if they are not held in accounts maintained by financial institutions: (i) stocks and securities issued by non-U.S. persons, (ii) financial instruments and contracts held for investment that have non-U.S. issuers or counterparties and (iii) interests in foreign entities. The Internal Revenue Service has suspended this

PPS–6

filing requirement for tax returns that are filed before it issues the form on which to report the relevant information. However, once the Internal Revenue Service issues the form, taxpayers that were not required to report in prior years because of the suspension will nevertheless be required to report the relevant information for such prior years on such form. Individuals are urged to consult their tax advisors regarding the application of this legislation to their ownership of the Notes.

Non-U.S. Holders. Barclays currently does not withhold on payments to non-U.S. holders in respect of instruments such as the Notes. However, if Barclays determines that there is a material risk that it will be required to withhold on any such payments, Barclays may withhold on any Periodic Amounts at a 30% rate, unless you have provided to Barclays (i) a valid Internal Revenue Service Form W-8ECI or (ii) a valid Internal Revenue Service W-8BEN claiming tax treaty benefits that reduce or eliminate withholding. If Barclays elects to withhold and you have provided Barclays with a valid Internal Revenue Service W-8BEN claiming tax treaty benefits that reduce or eliminate withholding, Barclays may nevertheless withhold up to 30% on the Periodic Amounts if there is any possible characterization of the payments that would not be exempt from withholding under the treaty. In addition, non-U.S. holders will be subject to the general rules regarding information reporting and backup withholding as described under the heading “Certain U.S. Federal Income Tax Considerations—Information Reporting and Backup Withholding ” in the accompanying prospectus supplement.

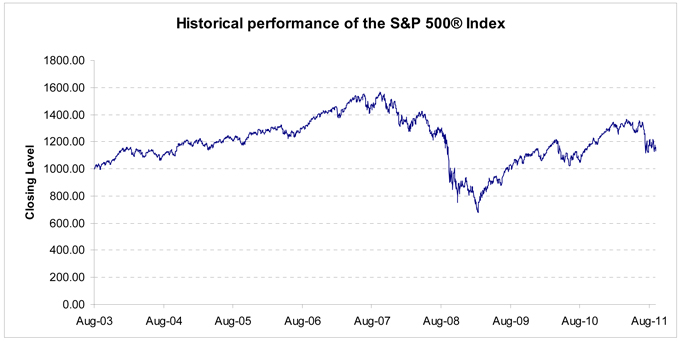

Historical Information

The following graph sets forth the historical performance of the Index based on the daily Index Closing Level from August 27, 2003 through September 30, 2011. The Index Closing Level on September 30, 2011 was 1,131.42.

We obtained the Index Closing Levels below from Bloomberg, L.P. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg, L.P. The historical levels of the Index should not be taken as an indication of future performance, and no assurance can be given as to the Index Closing Level on the Final Valuation Date. We cannot give you assurance that the performance of the Index will result in the return of any of your initial investment.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

SUPPLEMENTAL PLAN OF DISTRIBUTION

We will agree to sell to Barclays Capital Inc. (the “Agent”), and the Agent will agree to purchase from us, the principal amount of the Notes, and at the price, specified on the cover of the related pricing supplement, the document that will be filed pursuant to Rule 424(b) containing the final pricing terms of the Notes. The Agent will commit to take and pay for all of the Notes, if any are taken.

PPS–7