CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities Offered |

|

Maximum Aggregate Offering Price |

|

Amount of Registration Fee(1) |

|

|

|

|

|

|

|

Global Medium-Term Notes, Series A |

|

$27,000,000 |

|

$3,361.50 |

(1) Calculated in accordance with Rule 457(r) of the Securities Act of 1933.

|

Pricing Supplement dated February 21, 2018 |

Filed Pursuant to Rule 424(b)(2) |

![]()

US$27,000,000

CAPPED CALLABLE CMS STEEPENER NOTES DUE FEBRUARY 26, 2038

|

Principal Amount: |

US$27,000,000 |

Issuer: |

Barclays Bank PLC | |||

|

Issue Price: |

Variable Price Re-Offer |

Series: |

Global Medium-Term Notes, Series A | |||

|

Payment at Maturity: |

If you hold the Notes to maturity, you will receive 100% of your principal, subject to the creditworthiness of Barclays Bank PLC and the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. Any payment on the Notes is not guaranteed by any third party and is subject to both the creditworthiness of the Issuer and to the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. If Barclays Bank PLC were to default on its payment obligations or become subject to the exercise of any U.K. Bail-in Power (or any other resolution measure) by the relevant U.K. resolution authority, you might not receive any amounts owed to you under the Notes. See “Consent to U.K. Bail-in Power” and “Selected Risk Factors” in this pricing supplement and “Risk Factors” in the accompanying prospectus supplement for more information. | |||||

|

Original Trade Date: |

February 21, 2018 |

Maturity Date: |

February 26, 2038, subject to Redemption at the Option of the Company (as set forth below). | |||

|

Original Issue Date: |

February 28, 2018 |

Denominations: |

Minimum denominations of US$1,000 and integral multiples of US$1,000 thereafter. | |||

|

CUSIP/ISIN: |

06744CUW9/US06744CUW99 |

| ||||

|

Reference Asset/Reference Rate: The CMS spread minus the Fixed Percentage Amount | ||||||

|

CMS Spread: The CMS spread for any swap business day is 30-Year swap rate minus 2-Year swap rate, each as determined on that swap business day.

30-Year Swap Rate: 30-Year swap rate is, on any swap business day, the fixed rate of interest payable on a U.S. dollar interest rate swap with a 30-year maturity as reported on Reuters page ICESWAP1 (or such other page as may replace that page on such service) as of 11:00 a.m. New York City time on that swap business day.

2-Year Swap Rate: 2-Year swap rate is, on any swap business day, the fixed rate of interest payable on a U.S. dollar interest rate swap with a 2-year maturity as reported on Reuters page ICESWAP1 (or such other page as may replace that page on such service) as of 11:00 a.m. New York City time on that swap business day.

Swap Rate Fall Back Provisions: If either 30-Year swap rate or the 2-Year swap rate (together, the “CMS rates”) is not displayed by approximately 11:00 a.m., New York City time, on Reuters page ICESWAP1 on any day on which the CMS spread must be determined, that CMS rate on that day will be determined on the basis of the mid-market, semi-annual CMS rate quotations provided to the calculation agent by five leading swap dealers in the New York City interbank market (the “reference banks”) at approximately 11:00 a.m., New York City time, on that day. For this purpose, the semi-market annual CMS rate means the mean of the bid and offered rates for the semi-annual fixed leg, calculated on a 30/360 day count basis, of a fixed-for-floating U.S. dollar interest rate swap transaction with a 30-year term or 2-year term, as applicable, commencing on that day with an acknowledged dealer of good credit in the swap market, where the floating leg, calculated on an actual/360 day count basis, is equivalent to three-month U.S. Dollar London Interbank Offered Rate (ICE Benchmark Administration). The calculation agent will request the principal New York City offices of each of the reference banks to provide a quotation of its rate. If at least three quotations are provided, the affected CMS rate for that day will be the arithmetic mean of the quotations, eliminating the highest quotation (or, in the event of equality, one of the highest) and the lowest quotation (or, in the event of equality, one of the lowest). If fewer than three quotations are provided as requested, the affected CMS rate will be determined by the calculation agent in good faith and in a commercially reasonable manner.

Swap business day: A swap business day means any day except for a Saturday, Sunday or a day on which the Securities Industry and Financial Markets Association recommends that the fixed income department of its members be closed for the entire day for purposes of trading in U.S. government securities. | ||||||

|

Maximum Interest Rate: |

9.00% per annum. |

Minimum Interest Rate: |

0.00% per annum. | |||

[Terms of Notes continue on next page]

|

|

|

Price to Public(1) |

|

Agent’s Commission(1)(2) |

|

Proceeds to Barclays Bank |

|

Per Note |

|

At Variable Prices |

|

5.00% |

|

95.00% |

|

Total |

|

At Variable Prices |

|

$1,350,000 |

|

$25,650,000 |

(1)Barclays Capital Inc. has agreed to purchase the Notes from us at 100% of the principal amount minus a maximum commission equal to $50.00 per $1,000 principal amount, or 5.00%, resulting in a minimum aggregate proceeds to Barclays Bank PLC of $950.00 per $1,000 principal amount. Barclays Capital Inc. proposes to offer the Notes from time to time for sale in negotiated transactions, or otherwise, at varying prices to be determined at the time of each sale; provided that, such prices are not less than $950.00 or greater than $1,000 per $1,000 principal amount. Barclays Capital Inc. may also use all or a portion of its commissions on the Notes to pay selling concessions or fees to other dealers. See “Selected Risk Factors—The Price You Paid for the Notes May Be Higher than the Prices Paid by Other Investors” below for additional detail.

(2) The total Agent’s Commission and Proceeds to Barclays Bank PLC, will be based on the aggregate dollar amount of notes sold by Barclays Bank PLC to Barclays Capital Inc. as determined on the Original Trade Date.

Our estimated value of the Notes on the Original Trade Date, based on our internal pricing models, is $909.74 per Note. The estimated value is less than the initial issue price of the Notes. See “Additional Information Regarding Our Estimated Value of the Notes” below. We may decide to sell additional Notes after the date of this pricing supplement, at issue prices and with commissions and aggregate proceeds that differ from the amounts set forth above. In addition, the estimated value of the Notes on the date any additional Notes are priced for sale to be traded will take into account a number of variables, including prevailing market conditions and our subjective assumptions, which may or may not materialize, on the date that such additional Notes are traded. As a result of changes in these variables, our estimated value of the Notes on any subsequent trade date may be lower or higher than our estimated value of the Notes on the Original Trade Date, but in no case will be less than $909.74 per Note.

Investing in the Notes involves a number of risks. See “Risk Factors” beginning on page S-7 of the prospectus supplement and “Selected Risk Factors” beginning on page PS–4 of this pricing supplement.

We may use this pricing supplement in the initial sale of Notes. In addition, Barclays Capital Inc. or another of our affiliates may use this pricing supplement in market resale transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, this pricing supplement is being used in a market resale transaction.

The Notes will not be listed on any U.S. securities exchange or quotation system. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Notes or determined that this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes constitute our direct, unconditional, unsecured and unsubordinated obligations and are not deposit liabilities of Barclays Bank PLC and are not insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency of the United States, the United Kingdom or any other jurisdiction.

|

Fixed Percentage Amount: |

0.00% |

Initial Interest Rate: |

9.00% per annum. |

|

Interest Rate Formula: |

For each Interest Period commencing on or after the Original Issue Date to but excluding February 28, 2020 (the “Initial Interest Payment Period”): the Initial Interest Rate For each Interest Period commencing on or after February 28, 2020 (the “Floating Interest Payment Period”), the interest rate per annum will be equal to the product of (1) the Multiplier times (2) the Reference Rate, subject to the Minimum Interest Rate and the Maximum Interest Rate. | ||

|

Multiplier: |

8.00 | ||

|

Business Day: |

A Monday, Tuesday, Wednesday, Thursday or Friday that is neither a day on which banking institutions in London or New York City generally are authorized or obligated by law, regulation, or executive order to close. | ||

|

Business Day Convention/Day Count Fraction: |

Following, unadjusted; 30/360 | ||

|

Interest Period: |

The initial Interest Period will begin on, and include, the Original Issue Date and end on, but exclude, the first Interest Payment Date. Each subsequent Interest Period will begin on, and include, the Interest Payment Date for the preceding Interest Period and end on, but exclude, the next following Interest Payment Date. The final Interest Period will end on, but exclude, the Maturity Date (or the Early Redemption Date, if applicable). | ||

|

Reference Rate Reset Dates: |

For each Interest Period commencing on or after February 28, 2018, the first day of such Interest Period | ||

|

Interest Payment Dates: |

Payable quarterly in arrears on the 28th day of each February, May, August and November, commencing on May 28, 2018 and ending on the Maturity Date or the Early Redemption Date, if applicable. | ||

|

Reference Rate Determination Dates: |

Two swap business days prior to the relevant Reference Rate Reset Date. A reference rate determination date will be postponed if that day is not a swap business day, in which case the reference rate determination date will be the first following day that is a swap business day. In no event, however, will the reference rate determination date be postponed by more than five business days. If the last possible reference rate determination date is not a swap business day, that day will nevertheless be the reference rate determination date, in which case 30-Year swap rate and 2-Year swap rate will be determined as described under “—Swap Rate Fall Back Provisions” above. | ||

|

Redemption at the Option of the Company: |

We may redeem your Notes, in whole or in part, at the Redemption Price set forth below, on any Interest Payment Date commencing on February 28, 2020, provided we give at least five business days’ prior written notice to the trustee. If we exercise our redemption option, the Interest Payment Date on which we so exercise will be referred to as the “Early Redemption Date”. | ||

|

Redemption Price: |

If we exercise our redemption option, you will receive on the Early Redemption Date 100% of the principal amount, together with any accrued and unpaid interest to but excluding the Early Redemption Date. | ||

|

Settlement: |

DTC; Book-entry; Transferable. | ||

|

Listing: |

The Notes will not be listed on any U.S. securities exchange or quotation system. | ||

|

Calculation Agent: |

Barclays Bank PLC | ||

![]()

You should read this pricing supplement together with the prospectus dated July 18, 2016, as supplemented by the prospectus supplement dated July 18, 2016 relating to our Global Medium-Term Notes, Series A, of which these Notes are a part. This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the prospectus supplement and the prospectus addendum, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes.

· You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

· Prospectus dated July 18, 2016:

https://www.sec.gov/Archives/edgar/data/312070/000119312516650074/d219304df3asr.htm

· Prospectus Supplement dated July 18, 2016:

https://www.sec.gov/Archives/edgar/data/312070/000110465916132999/a16-14463_21424b3.htm

Our SEC file number is 1-10257 and our Central Index Key, or CIK, on the SEC website is 0000312070. As used in this term sheet, the “Company,” “we,” “us,” or “our” refers to Barclays Bank PLC.

Notwithstanding any other agreements, arrangements or understandings between us and any holder of the Notes, by acquiring the Notes, each holder of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority.

Under the U.K. Banking Act 2009, as amended, the relevant U.K. resolution authority may exercise a U.K. Bail-in Power in circumstances in which the relevant U.K. resolution authority is satisfied that the resolution conditions are met. These conditions include that a U.K. bank or investment firm is failing or is likely to fail to satisfy the Financial Services and Markets Act 2000 (the “FSMA”) threshold conditions for authorization to carry on certain regulated activities (within the meaning of section 55B FSMA) or, in the case of a U.K. banking group company that is a European Economic Area (“EEA”) or third country institution or investment firm, that the relevant EEA or third country relevant authority is satisfied that the resolution conditions are met in the respect of that entity.

The U.K. Bail-in Power includes any write-down, conversion, transfer, modification and/or suspension power, which allows for (i) the reduction or cancellation of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes; (ii) the conversion of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes into shares or other securities or other obligations of Barclays Bank PLC or another person (and the issue to, or conferral on, the holder of the Notes such shares, securities or obligations); and/or (iii) the amendment or alteration of the maturity of the Notes, or amendment of the amount of interest or any other amounts due on the Notes, or the dates on which interest or any other amounts become payable, including by suspending payment for a temporary period; which U.K. Bail-in Power may be exercised by means of a variation of the terms of the Notes solely to give effect to the exercise by the relevant U.K. resolution authority of such U.K. Bail-in Power. Each holder of the Notes further acknowledges and agrees that the rights of the holders of the Notes are subject to, and will be varied, if necessary, solely to give effect to, the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. For the avoidance of doubt, this consent and acknowledgment is not a waiver of any rights holders of the securities may have at law if and to the extent that any U.K. Bail-in Power is exercised by the relevant U.K. resolution authority in breach of laws applicable in England.

For more information, please see “Selected Risk Factors—You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

ADDITIONAL INFORMATION REGARDING OUR ESTIMATED VALUE OF THE NOTES

Our internal pricing models take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize, typically including volatility, interest rates, and our internal funding rates. Our internal funding rates (which are our internally published borrowing rates based on variables such as market benchmarks, our appetite for borrowing, and our existing obligations coming to maturity) may vary from the levels at which our benchmark debt securities trade in the secondary market. Our estimated value on the pricing date is based on our internal funding rates. Our estimated value of the Notes may be lower if such valuation were based on the levels at which our benchmark debt securities trade in the secondary market.

Our estimated value of the Notes on the pricing date is less than the initial issue price of the Notes. The difference between the initial issue price of the Notes and our estimated value of the Notes results from several factors, including any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

Our estimated value on the pricing date is not a prediction of the price at which the Notes may trade in the secondary market, nor will it be the price at which Barclays Capital Inc. may buy or sell the Notes in the secondary market. Subject to normal market and funding conditions, Barclays Capital Inc. or another affiliate of ours intends to offer to purchase the Notes in the secondary market but it is not obligated to do so.

Assuming that all relevant factors remain constant after the pricing date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market, if any, and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value on the pricing date for a temporary period expected to be approximately twelve months after the initial issue date of the Notes because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the Notes and other costs in connection with the Notes which we will no longer expect to incur over the term of the Notes. We made such discretionary election and determined this temporary reimbursement period on the basis of a number of factors, including the tenor of the Notes and any agreement we may have with the distributors of the Notes. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the initial issue date of the Notes based on changes in market conditions and other factors that cannot be predicted.

Barclays Capital Inc., or another affiliate of ours, or a third party distributor may purchase and hold some of the Notes for subsequent resale at variable prices after the initial issue date of the Notes. There may be circumstances where investors may be offered to purchase those Notes from one distributor (including Barclays Capital Inc. or an affiliate) at a more favorable price than from other distributors. Furthermore, from time to time, Barclays Capital Inc. or an affiliate may offer and sell the Notes to purchasers of a large number of the Notes at a more favorable price than a purchaser acquiring a lesser number of the Notes.

At our sole option, we may decide to offer additional Notes after the Original Trade Date. Our estimated value of the Notes on any subsequent trade date may reflect issue prices, commissions and aggregate proceeds that differ from the amounts set forth in this pricing supplement and will take into account a number of variables, including prevailing market conditions and our subjective assumptions, which may or may not materialize, on the date that such additional Notes are traded. As a result of changes in these variables, our estimated value of the Notes on any subsequent trade date may differ significantly from our estimated value of the Notes on the original trade date, but in no case will be less than $892.50.

We urge you to read the “Selected Risk Factors” beginning on page PS-4 of this pricing supplement.

An investment in the Notes involves significant risks not associated with an investment in conventional floating rate or fixed rate medium term notes. You should read the risks summarized below in connection with, and the risks summarized below are qualified by reference to, the risks described in more detail in the “Risk Factors” section beginning on page S-7 of the prospectus supplement. We urge you to consult your investment, legal, tax, accounting and other advisers and to invest in the Notes only after you and your advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances.

· Issuer Credit Risk— The Notes are our unsecured debt obligations, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Notes, including any repayment of principal provided at maturity, depends on our ability to satisfy our obligations as they come due. As a result, the actual and perceived creditworthiness of Barclays Bank PLC may affect the market value of the Notes and, in the event we were to default on our obligations, you may not receive any repayment of principal or any other amounts owed to you under the terms of the Notes.

· You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority—Notwithstanding any other agreements, arrangements or understandings between Barclays Bank PLC and any holder of the Notes, by acquiring the Notes, each holder of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority as set forth under “Consent to U.K. Bail-in Power” in this pricing supplement. Accordingly, any U.K. Bail-in Power may be exercised in such a manner as to result in you and other holders of the Notes losing all or a part of the value of your investment in the Notes or receiving a different security from the Notes, which may be worth significantly less than the Notes and which may have significantly fewer protections than those typically afforded to debt securities. Moreover, the relevant U.K. resolution authority may exercise the U.K. Bail-in Power without providing any advance notice to, or requiring the consent of, the holders of the Notes. The exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes will not be a default or an Event of Default (as each term is defined in the indenture) and the trustee will not be liable for any action that the trustee takes, or abstains from taking, in either case, in accordance with the exercise of the U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes. See “Consent to U.K. Bail-in Power” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

· Reference Rate / Interest Payment Risk— Investing in the Notes is not equivalent to investing in securities directly linked to the CMS rates. Instead, after the initial Interest Periods for which the Initial Interest Rate applies, the amount of interest payable on the Notes is determined by multiplying the (a) Multiplier by (b) the difference between the CMS rates of the two maturities identified on the cover page hereof (the “CMS Spread”) minus the Fixed Percentage Amount (the “Reference Rate”), as determined on the Reference Rate Determination Date applicable to the relevant Interest Period, subject to the Minimum Interest Rate and the Maximum Interest Rate. Accordingly, the amount of interest payable on the Notes is dependent on whether, and the extent to which, the CMS Spread is greater than the Fixed Percentage Amount on each Reference Rate Determination Date. If the CMS Spread on any Reference Rate Determination Date is equal to or less than the Fixed Percentage Amount (i.e., the difference between the CMS rates of the two maturities identified on the cover page hereof is equal to or less than the Fixed Percentage Amount), you would receive no interest payment on the related Interest Payment Date (i.e., the interest rate for that Interest Payment Date would be equal to the Minimum Interest Rate of 0.00%). If the CMS Spread is equal to or less than the Fixed Percentage Amount on every Reference Rate Determination Date throughout the term of the Notes, you would receive no interest payments on your Notes throughout their term after the initial Interest Periods for which the Initial Interest Rate applies. Given these various scenarios, it is possible that the interest payment related to each Interest Period, after the initial Interest Periods for which the Initial Interest Rate applies, during the term of the Notes will be less than the amount that would be paid on an ordinary debt security of comparable maturity and may be zero in many instances.

· The Amount of Interest Payable on the Notes Related to Any Interest Period is Capped — The interest rate on the Notes for each quarterly Interest Period, after the Initial Interest Payment Period when the Initial Interest Rate applies, is capped for that quarter at the maximum interest rate of 9.00% per annum. Furthermore, due to the leverage factor or multiplier, you will not get the benefit of any increase in the Reference Rate (as determined on the relevant Reference Rate Determination Date) above a level of approximately 1.125%.

· The Price You Paid for the Notes May Be Higher than the Prices Paid by Other Investors— Barclays Capital Inc. proposes to offer the Notes from time to time for sale to investors in one or more negotiated transactions, or otherwise, at prevailing market prices at the time of sale, at prices related to then-prevailing prices, at negotiated prices, or otherwise. Accordingly, there is a risk that the price you paid for your Notes will be higher than the prices paid by other investors based on the date and time you made your purchase, from whom you purchased the Notes, any related transaction costs, whether you hold your Notes in a brokerage account, a fiduciary or fee-based account or another type of account and other market factors.

· Early Redemption—We may redeem the Notes prior to the Maturity Date on any Interest Payment Date, beginning on the date specified on the cover page hereof. If you intend to purchase the Notes, you must be willing to have your Notes redeemed early. We are generally more likely to redeem the Notes during periods when we expect that interest will accrue on the Notes at a rate that is greater than that which we would pay on our traditional interest-bearing deposits or debt securities having a maturity equal to the remaining term of the Notes. In contrast, we are generally less likely to redeem the Notes during periods when we expect interest to accrue on the Notes at a rate that is less than that which we would pay on those instruments. If we redeem the Notes prior to the Maturity Date, accrued interest will be paid on the Notes until such early redemption, but you will not receive any future interest payments from the Notes redeemed and you may be unable to reinvest your proceeds from the redemption in an investment with a return that is as high as the return on the Notes would have been if they had not been redeemed.

· Lack of Liquidity—The Notes will not be listed on any securities exchange. Barclays Capital Inc. and other affiliates of Barclays Bank PLC intend to make a secondary market for the Notes but are not required to do so, and may discontinue any such secondary market making at any time, without notice. Barclays Capital Inc. may at any time hold unsold inventory, which may inhibit the development of a secondary market for the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which Barclays Capital Inc. and other affiliates of Barclays Bank PLC are willing to buy the Notes. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity.

· The Historical Performance of the Reference Rate is Not an Indication of Its Future Performance—The historical performance of the CMS rates should not be taken as an indication of their future performance during the term of the Notes. Changes in the levels of the CMS rates will affect the value of the Notes, but it is impossible to predict whether such levels will rise or fall. During the Floating Interest Payment Period, there can be no assurance that the CMS Spread will be greater than the Fixed Percentage Amount during the relevant Interest Periods. Furthermore, the historical performance of the CMS Spread does not reflect the return the Notes would have had because it does not take into account the Multiplier, the Fixed Percentage Amount or the Maximum Interest Rate.

· Exposure to the CMS rates—Payments on the Notes are determined with reference to the CMS rates. The CMS rates or the 30 Year swap rate and the 2 Year swap rate are the “constant maturity swap rates” that measure the fixed rate of interest payable on a hypothetical fixed-for-floating U.S. dollar interest rate swap transaction with a maturity of thirty years and two years, respectively. In such a hypothetical swap transaction, the fixed rate of interest, payable semi-annually on the basis of a 360-day year consisting of twelve 30-day months, is exchangeable for a floating 3-month LIBOR-based payment stream that is payable quarterly on the basis of the actual number of days elapsed during a quarterly period in a 360-day year. “LIBOR” is the London Interbank Offered Rate, and is the rate of interest at which banks borrow funds from each other in the London interbank market. 3-Month LIBOR is the rate of interest which banks in London charge each other for loans for a period of three months.

For additional information about CMS rates, and more specifically, how the CMS Spread is calculated, see “The CMS rates” below.

· The CMS rates may be calculated based on dealer quotations or by the calculation agent in good faith and in a commercially reasonable manner—If, on any reference rate determination date, either CMS rate cannot be determined by reference to Reuters page ICESWAP1 (or any successor page), then that CMS rate on that day will be determined on the basis of the mid-market, semi-annual CMS rate quotations provided to the calculation agent by five leading swap dealers in the New York City interbank market at approximately 11:00 a.m., New York City time, on that day. If fewer than three quotations are provided as requested, the affected CMS rate will be determined by the calculation agent in good faith and in a commercially reasonable manner. The CMS rate determined in this manner and used in the determination of the final spread and the payment at maturity on the securities may be different from the CMS rate that would have been published on the applicable Reuters page and may be different from other published rates, or other estimated rates, of the affected CMS rate.

· Changes in the Method Pursuant to Which the Reference Rate is Determined May Adversely Affect the Value of the Notes—The method by which the Reference Rate is calculated may change in the future, as a result of governmental actions, actions by the publisher of the Reference Rate or otherwise. We cannot predict whether the method by which the Reference Rate is calculated will change or what the impact of any change might be. Any of these changes could adversely affect the Reference Rate, the market value of the Notes and any amounts payable on the Notes.

In particular, LIBOR and other rates that are deemed “benchmarks” are the subject of recent national, international and other regulatory guidance and proposals for reform. Some of these reforms are already effective while others are still to be implemented. These reforms may cause these “benchmarks” to perform differently than in the past, or to disappear entirely, or have other consequences which cannot be predicted. Any of these consequences could adversely affect any securities based on, or linked to, these “benchmarks” such as the Notes. Any of these international, national or other proposals for reform or the general increased regulatory scrutiny of “benchmarks” could increase the costs and risks of administering or otherwise participating in the setting of a “benchmark” and complying with any of these regulations or requirements. These factors may have the effect of discouraging market participants from continuing to administer or participate in certain “benchmarks,” trigger changes in the rules or methodologies used in certain “benchmarks” or lead to the disappearance of certain “benchmarks.” The disappearance of a “benchmark” or changes in the manner of administration of a “benchmark” could result in adjustment to the terms and conditions, discretionary valuation by the calculation agent, or other consequences in relation to securities linked to that “benchmark.” Any of these consequences could adversely affect the market value of the Notes and any amounts payable on the Notes.

· The Estimated Value of Your Notes is Lower Than the Initial Issue Price of Your Notes—The estimated value of your Notes on the pricing date is lower than the initial issue price of your Notes. The difference between the initial issue price of your Notes and the estimated value of the Notes is a result of certain factors, such as any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

· The Estimated Value of Your Notes Might be Lower if Such Estimated Value Were Based on the Levels at Which Our Debt Securities Trade in the Secondary Market—The estimated value of your Notes on the pricing date is based on a number of variables, including our internal funding rates. Our internal funding rates may vary from the levels at which our benchmark debt securities trade in the secondary market. As a result of this difference, the estimated value referenced above may be lower if such estimated value were based on the levels at which our benchmark debt securities trade in the secondary market.

· The Estimated Value of the Notes is Based on Our Internal Pricing Models, Which May Prove to be Inaccurate and May be Different from the Pricing Models of Other Financial Institutions—The estimated value of your Notes on the pricing date is based on our internal pricing models, which take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize. These variables and assumptions are not evaluated or verified on an independent basis. Further, our pricing models may be different from other financial institutions’ pricing models and the methodologies used by us to estimate the value of the Notes may not be consistent with those of other financial institutions which may be purchasers or sellers of Notes in the secondary market. As a result, the secondary market price of your Notes may be materially different from the estimated value of the Notes determined by reference to our internal pricing models. Moreover, at our sole option, we may decide to sell additional Notes after the Original Trade Date. Our estimated value of the Notes on any subsequent trade date may reflect issue prices, commissions and aggregate proceeds that differ from the amounts set forth in this pricing supplement and will take into account a number of variables, including prevailing market conditions and our subjective assumptions, which may or may not materialize, on the date that such additional Notes are traded. As a result of changes in these variables, our estimated value of the Notes on any subsequent trade may differ significantly from our estimated value of the Notes on the Original Trade Date.

· The Estimated Value of Your Notes Is Not a Prediction of the Prices at Which You May Sell Your Notes in the Secondary Market, if any, and Such Secondary Market Prices, If Any, Will Likely be Lower Than the Initial Issue Price of Your Notes and Maybe Lower Than the Estimated Value of Your Notes—The estimated

value of the Notes will not be a prediction of the prices at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions (if they are willing to purchase, which they are not obligated to do). The price at which you may be able to sell your Notes in the secondary market at any time will be influenced by many factors that cannot be predicted, such as market conditions, and any bid and ask spread for similar sized trades, and may be substantially less than our estimated value of the Notes. Further, as secondary market prices of your Notes take into account the levels at which our debt securities trade in the secondary market, and do not take into account our various costs related to the Notes such as fees, commissions, discounts, and the costs of hedging our obligations under the Notes, secondary market prices of your Notes will likely be lower than the initial issue price of your Notes. As a result, the price, at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions, if any, will likely be lower than the price you paid for your Notes, and any sale prior to the maturity date could result in a substantial loss to you.

· The Temporary Price at Which We May Initially Buy The Notes in the Secondary Market And the Value We May Initially Use for Customer Account Statements, If We Provide Any Customer Account Statements At All, May Not Be Indicative of Future Prices of Your Notes—Assuming that all relevant factors remain constant after the pricing date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market (if Barclays Capital Inc. makes a market in the Notes, which it is not obligated to do) and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value of the Notes on the Original Trade Date, as well as the secondary market value of the Notes, for a temporary period after the initial issue date of the Notes. The price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market and the value that we may initially use for customer account statements may not be indicative of future prices of your Notes.

· We and Our Affiliates May Engage in Various Activities or Make Determinations That Could Materially Affect Your Notes in Various Ways and Create Conflicts of Interest— We and our affiliates play a variety of roles in connection with the issuance of the Notes, as described below. In performing these roles, our and our affiliates’ economic interests are potentially adverse to your interests as an investor in the Notes.

In connection with our normal business activities and in connection with hedging our obligations under the Notes, we and our affiliates make markets in and trade various financial instruments or products for our accounts and for the account of our clients and otherwise provide investment banking and other financial services with respect to these financial instruments and products. These financial instruments and products may include securities, derivative instruments or assets that may relate to interest rates. In any such market making, trading and hedging activity, and other services, we or our affiliates may take positions or take actions that are inconsistent with, or adverse to, the investment objectives of holders of the Notes. We and our affiliates have no obligation to take the needs of any buyer, seller or holder of the Notes into account in conducting these activities. Such market making, trading and hedging activity, investment banking and other financial services may negatively impact the value of the Notes.

In addition, the role played by Barclays Capital Inc., as the agent for the Notes, could present significant conflicts of interest with the role of Barclays Bank PLC, as issuer of the Notes. For example, Barclays Capital Inc. or its representatives may derive compensation or financial benefit from the distribution of the Notes. Furthermore, we and our affiliates establish the offering price of the Notes for initial sale to the public, and the offering price is not based upon any independent verification or valuation.

In addition to the activities described above, we will also act as the Calculation Agent for the Notes. As Calculation Agent, we will make any determinations necessary to calculate any payments on the Notes. In making these determinations, we may be required to make certain discretionary judgments. In making these discretionary judgments, our economic interests are potentially adverse to your interests as an investor in the Notes, and any of these determinations may adversely affect any payments on the Notes.

· Many Economic and Market Factors Will Impact the Value of the Notes—In addition to the Reference Rate on any day, the value of the Notes will be affected by a number of economic and market factors that may either offset or magnify each other, including:

o the expected volatility of the Reference Rate;

o the time to maturity of the Notes;

o interest and yield rates in the market generally;

o a variety of economic, financial, political, regulatory or judicial events; and

o our creditworthiness, whether actual or perceived, including actual or anticipated downgrades in our credit ratings.

HYPOTHETICAL INTEREST RATE AND INTEREST PAYMENT CALCULATIONS

The examples below illustrate the various payments you may receive on the Notes in a number of different hypothetical scenarios. These examples are only hypothetical and do not indicate the actual payments or return you will receive on the Notes. The examples below assume that the Notes are held until maturity and do not take into account the tax consequences of an investment in the Notes.

As described above, after the initial Interest Periods for which the Initial Interest Rate is payable, the Notes will pay interest on each Interest Payment Date at an effective per annum interest rate calculated in accordance with the Interest Rate Formula. The following illustrates the process by which the interest rate and interest payment amount are determined for each Interest Period during the term of the Notes.

For purposes of these examples, we assume that the Notes are not being redeemed on the applicable Interest Payment Date pursuant to the Redemption at the Option of the Company provisions above. If we exercise our redemption option, you will receive on the Early Redemption Date the Redemption Price applicable to that Early Redemption Date, calculated as described above. The examples below are based on the Fixed Percentage Amount of 0.00% per annum, the Minimum Interest Rate of 0.00% per annum and the Maximum Interest Rate of 9.00% per annum.

Interest Rate Calculation

Step 1: Calculate the Reference Rate.

For each Interest Period commencing on or after February 28, 2020, a value for the Reference Rate is determined by calculating the CMS Spread (the 30 Year swap rate minus the 2 Year swap rate) minus the Fixed Percentage Amount. If the value of the first CMS rate is not sufficiently greater than the second CMS rate, the subtraction of the second CMS rate from the first CMS rate will be less than or equal to the Fixed Percentage Amount which will result in a negative Reference Rate or a Reference Rate of zero.

Step 2: Calculate the per annum interest rate for each Interest Payment Date.

For each Interest Period commencing on or after February 28, 2020 (“Floating Interest Payment Period”), the interest rate per annum will be equal to the product of (i) the Multiplier and (2) the Reference Rate, subject to the Minimum Interest Rate and the Maximum Interest Rate.

For each Interest Period commencing on or after the Original Issue Date to but excluding February 28, 2020, the interest rate per annum will be equal to the Initial Interest Rate.

As the Maximum Interest Rate is set at 9.00%, the maximum possible per annum interest rate for any Interest Period is 9.00%. The Minimum Interest Rate applicable to any Interest Period during the Floating Interest Payment Period is 0.00%. As such, the per annum interest rate for any Interest Period during the Floating Interest Payment Period could potentially be between 0.00% per annum and 9.00%. See “Selected Risk Factors—Reference Rate/Interest Payment Risk”.

Example Interest Rate and Interest Payment Calculations

The table below presents examples of hypothetical interest that would accrue on the Notes during various Interest Periods during the term of the Notes. For the Initial Interest Payment Period, interest will accrue at a rate equal to the Initial Interest Rate. For the Floating Interest Payment Period, interest will accrue on the Notes at an effective per annum interest rate calculated in accordance with the Interest Rate Formula.

The examples below assume the Notes are held until the Maturity Date. These examples do not take into account any tax consequences from investing in the Notes.

Also, as stated above, the below is merely a sampling of Interest Periods during the Floating Interest Payment Period and does not reflect the total number of Interest Periods that occur during the term of the Notes.

|

Reference |

Multiplier times |

Interest |

Interest Payment |

|

-4.000% |

-32.00% |

0.00% |

$0.00 |

|

-2.500% |

-20.00% |

0.00% |

$0.00 |

|

-1.000% |

-8.00% |

0.00% |

$0.00 |

|

0.000% |

0.00% |

0.00% |

$0.00 |

|

0.500% |

4.00% |

4.00% |

$10.00 |

|

1.000% |

8.00% |

8.00% |

$20.00 |

|

1.500% |

12.00% |

9.00% |

$22.50 |

|

2.000% |

16.00% |

9.00% |

$22.50 |

|

2.500% |

20.00% |

9.00% |

$22.50 |

|

3.000% |

24.00% |

9.00% |

$22.50 |

|

3.500% |

28.00% |

9.00% |

$22.50 |

|

4.000% |

32.00% |

9.00% |

$22.50 |

1. For each Interest Period occurring within the Initial Interest Payment Period, the interest rate is equal to the Initial Interest Rate.

2. For each Interest Period occurring during the Floating Interest Payment Period, the interest rate per annum is equal to the product of (1) the Multiplier of 8.00 and (2) the Reference Rate, subject to the Minimum Interest Rate of 0.00% and the Maximum Interest Rate of 9.00%, if applicable.

3. The interest payment amount for an Interest Payment Date equals the principal amount times the effective interest rate for the related Interest Period.

4. For each Interest Period, the value of the Reference Rate is equal to the CMS Spread (the 30 Year swap rate minus the 2 Year swap rate) minus the Fixed Percentage Amount, as determined on the related Reference Rate Determination Date.

Example 1: If on the Reference Rate Determination Date for the relevant Interest Period the value of the 30 Year swap rate is 6.00% and the 2 Year swap rate is 5.00%, the Reference Rate for the Interest Period would be 1.00% (equal to the 30 Year swap rate minus the 2 Year swap rate minus the Fixed Percentage Amount of 0.00%). In this case, the per annum interest rate for that Interest Period would be 8.00% (equal to the Reference Rate times the Multiplier of 8.00), and you would receive an interest payment of $20.00 per $1,000 principal amount of Notes on the related quarterly Interest Payment Date, calculated as follows:

Effective Interest Rate = 8.00% x (90/360) = 2.00%

Interest Payment = $1,000 x 2.00% = $20.00

Example 2: If on the Reference Rate Determination Date for the relevant Interest Period the value of the 30 Year swap rate is 4.00% and the 2 Year swap rate is 4.60%, the Reference Rate for the Interest Period would be –0.60% (equal to the 30 Year swap rate minus the 2 Year swap rate minus the Fixed Percentage Amount of 0.00%). Because the value of the Reference Rate times the Multiplier of 8.00 results in a per annum interest rate of –4.80%, which is less than the Minimum Interest Rate of 0.00%, the per annum interest rate for that Interest Period would be 0.00% (the Minimum Interest Rate), and you would receive no interest payment on the related quarterly Interest Payment Date (the interest payment would be $0).

Example 3: If on the Reference Rate Determination Date for the relevant Interest Period the value of the 30 Year swap rate is 9.25% and the 2 Year swap rate is 5.95%, the Reference Rate for the Interest Period would be 3.30% (equal to the 30 Year swap rate minus the 2 Year swap rate minus the Fixed Percentage Amount of 0.00%). Because the value of the Reference Rate times the Multiplier of 8.00 results in a per annum interest rate of 26.40%, which is greater than the Maximum Interest Rate of 9.00%, the per annum interest rate for that Interest Period would be equal to the Maximum Interest Rate of 9.00%, and you would receive an interest payment of $22.50 per $1,000 principal amount of Notes on the related quarterly Interest Payment Date, calculated as follows:

Effective Interest Rate = 9.00% x (90/360) = 2.25%

Interest Payment = $1,000 x 2.25% = $22.50

THE CMS RATES

The 30-Year swap rate is, on any swap business day, the fixed rate of interest payable on a U.S. dollar interest rate swap with a 30-year maturity as reported on Reuters page ICESWAP1 (or such other page as may replace that page on such service) as of 11:00 a.m. New York City time on that swap business day.

The 2-Year swap rate is, on any swap business day, the fixed rate of interest payable on a U.S. dollar interest rate swap with a 2-year maturity as reported on Reuters page ICESWAP1 (or such other page as may replace that page on such service) as of 11:00 a.m. New York City time on that swap business day.

A U.S. dollar interest rate swap rate, at any given time, generally indicates the fixed rate of interest (paid annually) that a counterparty in the swaps market would have to pay for a given maturity in order to receive a floating rate (paid quarterly) equal to three-month USD London Interbank Offered Rate (“three month USD LIBOR”) for that same maturity. Three-month USD LIBOR reflects the rate at which banks lend U.S. dollars to each other for a term of three months in the London interbank market. The 30-Year U.S. Dollar ICE Swap Rate is one of the market-accepted indicators of longer term interest rates.

Please see “—Swap Rate Fall Back Provisions” on the cover of this pricing supplement for information regarding the procedures that will be applied by the calculation agent if either CMS rate cannot be determined in the manner described above on the valuation date.

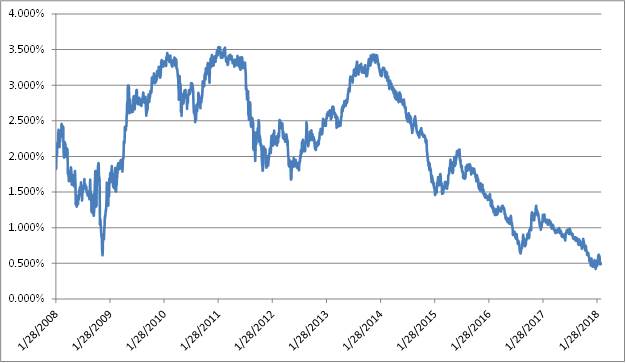

Historical Information for the Reference Rate

The following graph sets forth the Reference Rate, which is calculated as the CMS Spread minus the Fixed Percentage Amount, for the period from January 28, 2008 to February 21, 2018. The Reference Rate on February 21, 2018 was 0.485%. The historical performance of the Reference Rate should not be taken as an indication of its future performance. We obtained the information in the graph below from Bloomberg Financial Markets (“Bloomberg”), without independent verification. Historical Performance is not indicative of future performance.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

TAX CONSIDERATIONS

You should review carefully the sections entitled “Material U.S. Federal Income Tax Consequences—Tax Consequences to U.S. Holders—Notes Treated as Indebtedness for U.S. Federal Income Tax Purposes” and, if you are a non-U.S. holder, “—Tax Consequences to Non-U.S. Holders,” in the accompanying prospectus supplement. The discussion below applies to you only if you are an initial purchaser of the Notes; if you are a secondary purchaser of the Notes, the tax consequences to you may be different. In the opinion of our special tax counsel, Davis Polk & Wardwell LLP, the Notes should be treated as debt instruments for U.S. federal income tax purposes. The remainder of this discussion assumes that this treatment is correct.

Assuming the treatment described above is correct, in the opinion of our special tax counsel, the Notes should be treated as “contingent payment debt instruments” for U.S. federal income tax purposes, as described under “—Contingent Payment Debt Instruments” in the accompanying prospectus supplement. Because the Notes will be offered to initial purchasers at varying prices, it is expected that the “issue price” of the Notes for U.S. federal income tax purposes will be uncertain. We currently intend to treat the issue price as $1,000 for each $1,000 principal amount Note, and the remainder of this discussion so assumes, unless otherwise indicated. Our intended treatment will affect the amounts you will be required to include in income for U.S. federal income tax purposes. You should consult your tax advisor regarding the uncertainty with respect to the Notes’ issue price, including the tax consequences to you if the actual issue price of the Notes for U.S. federal income tax purposes is not $1,000 per Note.

Assuming that our treatment of the Notes as contingent payment debt instruments is correct, regardless of your method of accounting for U.S. federal income tax purposes, you generally will be required to accrue taxable interest income in each year on a constant yield to maturity basis at the “comparable yield,” as determined by us, with certain adjustments in each year to reflect the difference, if any, between the actual and the projected amounts of the interest payments on the Notes in that year according to the “projected payment schedule” determined by us. Any income recognized upon a sale or exchange of a Note (including early redemption or redemption at maturity) will be treated as interest income for U.S. federal income tax purposes.

The discussions herein and in the accompanying prospectus supplement do not address the consequences to taxpayers subject to special tax accounting rules under Section 451(b).

After the original issue date, you may obtain the comparable yield and the projected payment schedule by requesting them from Barclays Cross Asset Sales Americas, at (212) 528-7198. Neither the comparable yield nor the projected payment schedule constitutes a representation by us regarding the actual contingent interest payments, if any, that we will make on the Notes.

If you purchase Notes at their original issuance for an amount that is different from their issue price, you will be required to account for this difference, generally by allocating it reasonably among projected payments on the Notes and treating these allocations as adjustments to your income when the payment is made. You should consult your tax advisor regarding the treatment of the difference between your basis in your Notes and their issue price.

You should consult your tax advisor regarding the U.S. federal tax consequences of an investment in the Notes, as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

Non-U.S. Holders. We do not believe that non-U.S. holders should be required to provide a Form W-8 in order to avoid 30% U.S. withholding tax with respect to interest on the Notes, although the IRS could challenge this position. However, non-U.S. holders should in any event expect to be required to provide appropriate Forms W-8 or other documentation in order to establish an exemption from backup withholding, as described under the heading “—Information Reporting and Backup Withholding” in the accompanying prospectus supplement. If any withholding is required, we will not be required to pay any additional amounts with respect to amounts withheld.

CERTAIN EMPLOYEE RETIREMENT INCOME SECURITY ACT CONSIDERATIONS

Your purchase of a Note in an Individual Retirement Account (an “IRA”), will be deemed to be a representation and warranty by you, as a fiduciary of the IRA and also on behalf of the IRA, that (i) neither the issuer, the placement agent nor any of their respective affiliates has or exercises any discretionary authority or control or acts in a fiduciary capacity with respect to the IRA assets used to purchase the Note or renders investment advice (within the meaning of Section 3(21)(A)(ii) of the Employee Retirement Income Security Act (“ERISA”)) with respect to any such IRA assets and (ii) in connection with the purchase of the Note, the IRA will pay no more than “adequate consideration” (within the meaning of Section 408(b)(17) of ERISA) and in connection with any redemption of the Note pursuant to its terms will receive at least adequate consideration, and, in making the foregoing representations and warranties, you have (x) applied sound business principles in determining whether fair market value will be paid, and (y) made such determination acting in good faith.

For additional ERISA considerations, see “Benefit Plan Investor Considerations” in the prospectus supplement.

SUPPLEMENTAL PLAN OF DISTRIBUTION

We have agreed to sell to Barclays Capital Inc. (the “Agent”), and the Agent has agreed to purchase from us, the principal amount of the Notes, and at the price, specified on the cover of this pricing supplement. The Agent commits to take and pay for all of the Notes, if any are taken.

Delivery of the Notes of a particular series may be made against payment for the Notes more than three business days following the pricing date for those Notes (that is, a particular series of Notes may have a settlement cycle that is longer than “T+3”). For considerations relating to an offering of Notes with a settlement cycle longer than T+3, see “Plan of Distribution” in the prospectus supplement.

The Notes are not intended to be offered, sold or otherwise made available to and may not be offered, sold or otherwise made available to any retail investor in the European Economic Area (“EEA Retail Investor”). For these purposes, an EEA Retail Investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (“MiFID II”); (ii) a customer within the meaning of Directive 2002/92/EC, where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in Directive 2003/71/EC. Consequently no key information document required by Regulation (EU) No 1286/2014 (as amended from time to time, the “PRIIPs Regulation”) for offering or selling the Notes or otherwise making them available to EEA Retail Investors has been prepared and therefore offering or selling such Notes or otherwise making them available to any EEA Retail Investor may be unlawful under the PRIIPs Regulation.

VALIDITY OF THE NOTES

In the opinion of Davis Polk & Wardwell LLP, as special United States products counsel to Barclays Bank PLC, when the Notes offered by this pricing supplement have been executed and issued by Barclays Bank PLC and authenticated by the trustee pursuant to the indenture, and delivered against payment as contemplated herein, such Notes will be valid and binding obligations of Barclays Bank PLC, enforceable in accordance with their terms, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith) and possible judicial or regulatory actions giving effect to governmental actions or foreign laws affecting creditors’ rights, provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date hereof and is limited to the laws of the State of New York. Insofar as this opinion involves matters governed by English law, Davis Polk & Wardwell LLP has relied, with Barclays Bank PLC’s permission, on the opinion of Davis Polk & Wardwell London LLP, dated as of June 28, 2017, filed as an exhibit to a report on Form 6-K by Barclays Bank PLC on June 28, 2017, and this opinion is subject to the same assumptions, qualifications and limitations as set forth in such opinion of Davis Polk & Wardwell London LLP. In addition, this opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the indenture and its authentication of the Notes and the validity, binding nature and enforceability of the indenture with respect to the trustee, all as stated in the letter of Davis Polk & Wardwell LLP, dated June 28, 2017, which has been filed as an exhibit to the report on Form 6-K referred to above.

![]()

US$27,000,000

BARCLAYS BANK PLC

CAPPED CALLABLE CMS STEEPENER NOTES DUE FEBRUARY 28, 2038

GLOBAL MEDIUM-TERM NOTES, SERIES A

(TO PROSPECTUS DATED JULY 18, 2016, AND THE

PROSPECTUS SUPPLEMENT DATED JULY 18, 2016)

______________

![]()