2021

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | ||||||||

| ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the fiscal year ended December 31, 2021

| OR | ||||||||

| TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

____________________________________________________________________________

Commission File Number 001-38710

(Exact Name of Registrant as Specified in Its Charter)

| (State or other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||||||||

| (Address of Principal Executive Offices) (Zip Code) | (Registrant’s Telephone Number, including area code) | ||||||||||||||||||||||

Commission File Number 1-815

(Exact Name of Registrant as Specified in Its Charter)

| (State or other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||||||||

| (Address of Principal Executive Offices) (Zip Code) | (Registrant’s Telephone Number, including area code) | ||||||||||||||||||||||

Securities registered pursuant to Section 12(b) of the Act for Corteva, Inc.:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(b) of the Act for E. I. du Pont de Nemours and Company:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

No securities are registered pursuant to Section 12(g) of the Act.

_____________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act).

Corteva, Inc. Yes x No o

E. I. du Pont de Nemours and Company Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Corteva, Inc. Yes o No x

E. I. du Pont de Nemours and Company Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Corteva, Inc. Yes x No o

E. I. du Pont de Nemours and Company Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit files).

Corteva, Inc. Yes ý No o

E. I. du Pont de Nemours and Company Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Corteva, Inc. | x | Accelerated Filer o | Non-Accelerated Filer | o | Smaller reporting company o | Emerging growth company o | |||||||||||||||||

| E. I. du Pont de Nemours and Company | Large Accelerated Filer | o | Accelerated Filer o | x | Smaller reporting company o | Emerging growth company o | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Corteva, Inc. o

E. I. du Pont de Nemours and Company o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Corteva, Inc. Yes ý No o

E. I. du Pont de Nemours and Company Yes ý No o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Corteva, Inc. Yes o No ý

E. I. du Pont de Nemours and Company Yes o No ý

The aggregate market value of voting stock of Corteva, Inc. held by non-affiliates of the registrant (excludes outstanding shares beneficially owned by directors and officers and treasury shares) as of June 30, 2021 was $32.5 billion.

As of February 3, 2022, 727,021,000 shares of Corteva, Inc's common stock, $0.01 par value, were outstanding.

As of February 3, 2022, all of E. I. du Pont de Nemours and Company’s issued and outstanding common stock, comprised of 200 shares, $0.30 par value per share, is held by Corteva, Inc.

E.I. du Pont de Nemours and Company meets the conditions set forth in General Instruction I(1)(a), (b) and (d) of Form 10-K (as modified by a grant of no-action relief dated February 12, 2018) and is therefore filing this form with reduced disclosure format.

Documents Incorporated by Reference

CORTEVA, INC.

Form 10-K

Table of Contents

1

Explanatory Note

This Annual Report on Form 10-K is a combined report being filed separately by Corteva, Inc. and EID. Corteva, Inc. owns all of the common equity interests in EID, and EID meets the conditions set forth in General Instruction I(1)(a), (b) and (d) of Form 10-K and is therefore filing its information within this Form 10-K with the reduced disclosure format. Each of Corteva, Inc. and EID is filing on its own behalf the information contained in this report that relates to itself, and neither company makes any representation as to information relating to the other company. Where information or an explanation is provided that is substantially the same for each company, such information or explanation has been combined in this report. Where information or an explanation is not substantially the same for each company, separate information and explanation has been provided. In addition, separate consolidated financial statements for each company, along with notes to the consolidated financial statements, are included in this report.

The primary differences between Corteva and EID's financial statements relate to EID's Preferred Stock - $4.50 Series and EID's Preferred Stock - $3.50 Series, a related party loan between EID and Corteva, Inc. and the associated tax deductible interest expense for EID, and the capital structure of Corteva. Inc. (See EID's Note 1 - Basis of Presentation to EID's Consolidated Financial Statements, for additional information for above items). The separate EID financial statements and footnotes for areas that differ from Corteva, are included within this Annual Report on Form 10-K and begin on page F-83. Footnotes of EID that are identical to that of Corteva are cross-referenced accordingly.

2

Part I

ITEM 1. BUSINESS

Unless otherwise indicated or the context otherwise requires, references in this Annual Report on Form 10-K to:

•"Corteva" or "the company" refers to Corteva, Inc. and its consolidated subsidiaries (including EID);

•"EID" refers to E. I. du Pont de Nemours and Company and its consolidated subsidiaries or E. I. du Pont de Nemours and Company excluding its consolidated subsidiaries, as the context may indicate;

•"DowDuPont" refers to DowDuPont Inc. and its subsidiaries prior to the Separation (as defined below) of Corteva;

•"Historical Dow" refers to The Dow Chemical Company and its consolidated subsidiaries prior to the Internal Reorganization as defined on page 4;

•"Historical DuPont" and "Historical EID" refers to EID prior to the Internal Reorganization (as defined on page 4);

•"Dow" refers to Dow Inc. after The Dow Distribution (as defined below);

•"DuPont" refers to DuPont de Nemours, Inc. after the Separation of Corteva;

•"DAS" refers to the agriculture business of Historical Dow, Dow AgroSciences; and

•"Merger" refers to the all-stock merger of equals strategic combination between Historical Dow and Historical DuPont.

Background

Corteva is a leading global provider of seed and crop protection solutions focused on the agriculture industry and contributing to a healthier, more secure and sustainable food supply. Corteva was incorporated in Delaware in March 2018 and maintains its business headquarters in Indianapolis, Indiana. The company is focused on advancing its science-based innovation, which aims to deliver a wide range of improved products and services to its customers. Corteva has one of the broadest and most productive new product pipelines in the agriculture industry. The company intends to leverage its rich heritage of scientific achievement to advance its robust innovation pipeline and continue to shape the future of responsible agriculture. New products are crucial to solving farmers’ productivity challenges amid a growing global population while addressing natural resistance, regulatory changes, safety requirements and competitive dynamics. The company’s investment in technology-based and solution-based product offerings allows it to meet farmers’ evolving needs while ensuring that its investments generate sufficient returns. Meanwhile, through Corteva’s unique routes to market, the company continues to work face-to-face with farmers around the world to understand their needs.

The company's broad portfolio of agriculture solutions fuels farmer productivity in approximately 140 countries. See Note 24 - Geographic Information, to the Consolidated Financial Statements for details on the location of the company's sales and property.

On June 1, 2019, Corteva, Inc. became an independent, publicly traded company through the completed separation (the “Separation”) of the agriculture business of DuPont de Nemours, Inc. (formerly known as DowDuPont Inc.) (“DuPont” or "DowDuPont"). The separation was effectuated through a pro rata distribution (the “Corteva Distribution”) of all of the then- issued and outstanding shares of common stock of Corteva, Inc.

As a result of the Internal Reorganization (defined below), on May 31, 2019, EID was contributed to Corteva, Inc. and, as a result, Corteva, Inc. owns 100% of the outstanding common stock of EID. Prior to March 31, 2019, Corteva, Inc. had engaged in no business operations and had no assets or liabilities of any kind, other than those incident to its formation.

EID continues to be a reporting company and is deemed to be the predecessor to Corteva, Inc., with the historical results of EID to be deemed the historical results of Corteva for periods prior to and including May 31, 2019. Shares of EID preferred stock, $3.50 Series and $4.50 Series, issued and outstanding immediately prior to the Separation remain issued and outstanding and were unaffected by the Separation.

Internal Reorganizations and Business Separations

Subsequent to the Merger, Historical Dow and EID engaged in a series of internal reorganization and realignment steps to realign their businesses into three subgroups: agriculture, materials science and specialty products (collectively, the "Business Separations”). On April 1, 2019, DowDuPont completed the separation of its materials science business into a separate and independent public company by way of a distribution of Dow through a pro rata dividend in-kind of all of the then-issued and outstanding shares of Dow’s common stock, to holders of DowDuPont's common stock, as of the close of business on March 21, 2019 (the “Dow Distribution” and together with the Corteva Distribution, the “Distributions”).

3

Part I

ITEM 1. BUSINESS, continued

Prior to the Dow Distribution, Historical Dow conveyed or transferred the assets and liabilities aligned with Historical Dow’s agriculture business to separate legal entities (“Dow Ag Entities”) and the assets and liabilities associated with its specialty products business to separate legal entities (the “Dow SP Entities”). On April 1, 2019, Dow Ag Entities and the Dow SP Entities were transferred and conveyed to DowDuPont.

In furtherance of the Business Separations, EID engaged in a series of internal reorganization and realignment steps (the “Internal Reorganization” and the "Business Realignment," respectively) to realign its businesses into three subgroups: agriculture, materials science and specialty products. As part of the Internal Reorganization:

•the assets and liabilities aligned with EID’s materials science business ("EID ECP"), were transferred or conveyed to separate legal entities that were ultimately conveyed by DowDuPont to Dow on April 1, 2019;

•the assets and liabilities aligned with EID’s specialty products business were transferred or conveyed to separate legal entities that were ultimately distributed to DowDuPont ("EID Specialty Products Entities") on May 1, 2019;

•on May 2, 2019, DowDuPont conveyed Dow Ag Entities to EID and in connection with the foregoing, EID issued additional shares of its common stock to DowDuPont; and

•on May 31, 2019, DowDuPont contributed EID to Corteva, Inc.

On May 6, 2019, the Board of Directors of DowDuPont approved the distribution of all the then issued and outstanding shares of common stock of Corteva, Inc., then a wholly-owned subsidiary of DowDuPont, to DowDuPont stockholders. On June 1, 2019, DowDuPont completed the Separation. Corteva, Inc.'s common stock began trading on the New York Stock Exchange under the ticker symbol "CTVA" on June 3, 2019.

As a result of the Business Realignment and the Internal Reorganization discussed above, Corteva owns 100% of the outstanding common stock of EID. EID is a subsidiary of Corteva, Inc. and continues to be a reporting company, subject to the requirements of the Securities Exchange Act of 1934, as amended.

Separation Agreements

In connection with the Distributions, DuPont, Corteva, and Dow (together, the “Parties” and each a “Party”) have entered into certain agreements to effect the separation, provide for the allocation of DowDuPont’s assets, employees, liabilities and obligations (including its investments, property and employee benefits and tax-related assets and liabilities) among the Parties, and provide a framework for Corteva's relationship with Dow and DuPont following the separations and Distributions. Effective April 1, 2019, the Parties entered into the following agreements:

•Separation and Distribution Agreement - Effective April 1, 2019, the Parties entered into an agreement that sets forth, among other things, the agreements among the Parties regarding the principal transactions necessary to effect the Distributions. It also sets forth other agreements that govern certain aspects of the Parties’ ongoing relationships after the completion of the Distributions (the "Corteva Separation Agreement").

•Tax Matters Agreement - The Parties entered into an agreement effective as of April 1, 2019, as amended on June 1, 2019, that governs their respective rights, responsibilities and obligations with respect to tax liabilities and benefits, tax attributes, the preparation and filing of tax returns, the control of audits and other tax proceedings and other matters regarding taxes.

•Employee Matters Agreement - The Parties entered into an agreement that identifies employees and employee-related liabilities (and attributable assets) to be allocated (either retained, transferred and accepted, or assigned and assumed, as applicable) to the Parties as part of the Distributions and describes when and how the relevant transfers and assignments would occur.

•Intellectual Property Cross-License Agreement - Effective as of April 1, 2019 Corteva and Dow, and effective June 1, 2019, Corteva and DuPont, entered into Intellectual Property Cross-License Agreements. The Intellectual Property Cross-License Agreements set forth the terms and conditions under which the applicable Parties may use in their respective businesses, following each of the Distributions, certain know-how (including trade secrets), copyrights, and software, and certain patents and standards, allocated to another Party pursuant to the Corteva Separation Agreement.

4

Part I

ITEM 1. BUSINESS, continued

•Letter Agreement - Effective as of June 1, 2019 DuPont and Corteva entered into a Letter Agreement. The Letter Agreement sets forth certain additional terms and conditions related to the Separation, including certain limitations on each party’s ability to transfer certain businesses and assets to third parties without assigning certain of such party’s indemnification obligations under the Corteva Separation Agreement to the other party to the transferee of such businesses and assets or meeting certain other alternative conditions.

Business Segments

The company’s operations are managed through two reportable segments: seed and crop protection. The seed segment develops and supplies commercial seed combining superior germplasm with advanced traits to produce high yield potential for farmers around the world. The crop protection segment supplies products to protect crop yields against weeds, insects and disease, enabling farmers to achieve optimal results. The combination of these leading platforms creates one of the broadest portfolios of agriculture solutions in the industry. Additional information with respect to business segment results is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, on page 47 of this report and Note 25 - Segment Information, to the Consolidated Financial Statements.

Seed

The seed segment is a global leader in developing and supplying commercial seed combining advanced germplasm and traits that produce optimum yield for farms around the world. The company’s seed segment is a leader in many key seed markets, including North America corn and soybeans, Europe corn and sunflower, as well as Brazil, India, South Africa and Argentina corn. The company offers trait technologies that improve resistance to weather, disease, insects and herbicides used to control weeds, and trait technologies that enhance food and nutritional characteristics. In addition, the company provides digital solutions that assist farmer decision-making with a view to optimize product selection and, ultimately, help maximize yield and profitability.

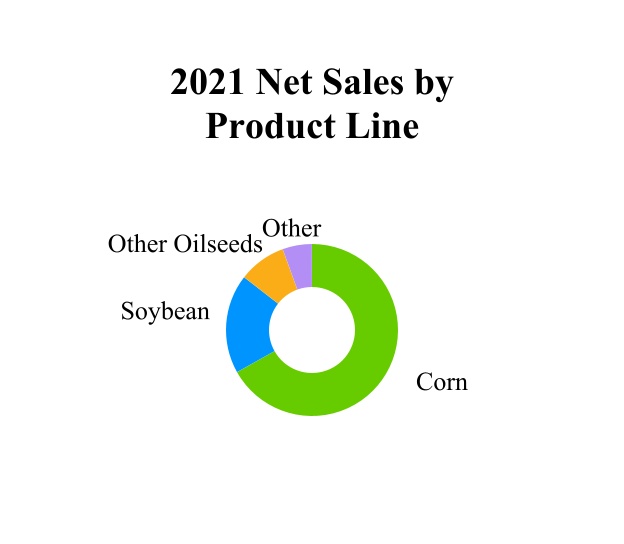

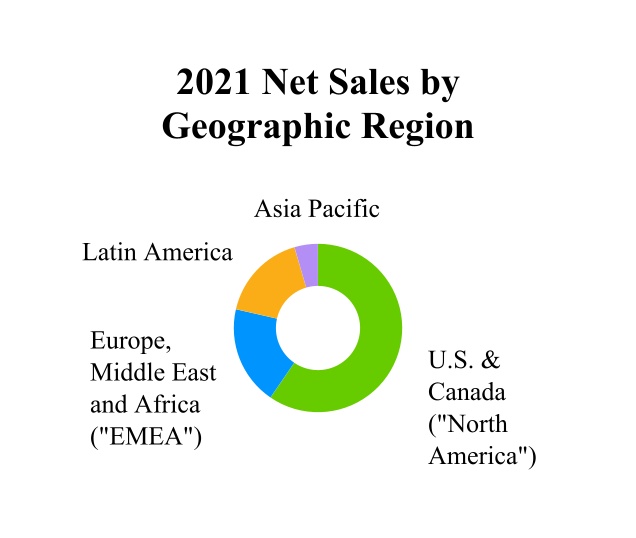

Details on the seed segment’s net sales by major product line and geographic region (based on customer location) are as follows:

5

Part I

ITEM 1. BUSINESS, continued

Products and Brands

The seed segment’s major brands and technologies, by key product line, are listed below:

| Seed Solutions Brands | Pioneer®; Brevant® seeds; Dairyland Seed®; Hoegemeyer®; Nutech®; Seed Consultants®; AgVenture®; Alforex®; PhytoGen®; Pannar®; VP Maxx®; HPT®; G2®; Supreme EX®; XL®; Power Plus® | ||||

| Seed Solutions Traits and Technologies | ENLIST E3® soybeans; ENLIST® cotton; EXZACT™ Precision Technology; HERCULEX® Insect Protection; Pioneer® brand hybrids with Leptra® insect protection technology offering protection against above ground pests; POWERCORE® trait technology family of products; Pioneer® brand Optimum® AcreMax® family of products offering above and below ground insect protection; REFUGE ADVANCED® trait technology; SMARTSTAX® trait technology; NEXERA® canola trait; Omega-9 Oils; Pioneer® brand Optimum® AQUAmax® hybrids; Pioneer® brand A-Series soybeans; Pioneer® brand Plenish® high oleic soybeans; ExpressSun® herbicide tolerant trait; Pioneer Protector® products for canola, sunflower and sorghum; Pioneer MAXIMUS® rapeseed hybrids; Qrome® products for corn; Pioneer® brand canola hybrids with Clearfield® trait; PROPOUND™ advanced canola meal; Conkesta E3® soybeans; WideStrike® insect protection trait; WideStrike® 3 insect protection trait. | ||||

| Other | LumiGEN® seed treatments, LUMIDERM®, LUMIVIA® and LUMIALZA™; GRANULAR®; Granular® Insights™ (e.g. LANDVisor™) | ||||

U.S. federal regulatory authorizations have been obtained for the commercialization of ENLIST™ corn, ENLIST E3® soybeans and ENLIST® cotton, including the U.S. Environmental Protection Agency's registration of ENLIST DUO® and ENLIST ONE® for use with ENLIST™ corn, soybeans and cotton in 34 states. The company has also secured cultivation authorizations of ENLIST E3® soybeans and ENLIST™ corn in Argentina, Brazil, and North America

In 2020, Corteva signed an agreement with J.G. Boswell Company to purchase the remaining 46.5 percent interest in PhytoGen® Seed Company, LLC – a joint venture between the two companies. With a 100% ownership position in PhytoGen® Seed Company, LLC, Corteva became the sole owner of the intellectual property, including patents, trademarks, proprietary germplasm and information, as well as know-how.

In 2020, Corteva announced the launch of Brevant™ seeds in the U.S. for sale exclusively through retail locations in the Midwest and Eastern Corn Belt starting with 2021 planting. As a global brand, Brevant™ seeds, which was originally launched in Latin America, Canada, and select European countries in 2018, provides farmers a greater choice with a high-performance retail solution. Brevant™ provides multiple seed offerings including corn, soybeans, sunflowers and canola.

In connection with the validation of breeding plans and large-scale product development timelines focused on rapidly ramping up differentiated technology solutions, during the fourth quarter of 2019, the company began accelerating the ramp up of the Enlist E3TM trait platform in the company’s soybean portfolio mix across all brands, including Pioneer® brands, over the subsequent five years. During the ramp-up period, the company is expected to significantly reduce the volume of products with the Roundup Ready 2 Yield® and Roundup Ready 2 Xtend® herbicide tolerance traits beginning in 2021, with expected minimal use of the Roundup Ready 2 Yield® and Roundup Ready 2 Xtend® traits thereafter for the remaining term of the non-exclusive license with the Monsanto Company. Refer to Prepaid Royalties within the Critical Accounting Estimates section on page 63 for additional information.

In 2019, Corteva received import authorization from China for the Conkesta® soybean insect control trait, which was a necessary step for commercialization of Conkesta E3® soybeans in Latin America. Conkesta E3® soybeans received regulatory approvals and was commercialized in the second half of 2021.

In 2019, the company launched Qrome® corn products in U.S. Pioneer® brands. Qrome® products offer growers high yield potential insect control options to help drive productivity for their operations by combining top-tier genetics and strong defensive traits. In 2020, Qrome® products were expanded to the U.S. multi-channel and Canada Pioneer® brands.

6

Part I

ITEM 1. BUSINESS, continued

The company acquired exclusive rights to the Clearfield® canola production system in North America from BASF in 2019. The Clearfield® canola trait provides non-genetically modified tolerance to imidazolinone herbicides. Clearfield® canola in the Pioneer® and Nexera® brands were already highly established in the market and integrated into the company’s breeding, production and commercial processes.

In addition, the company creates digital tools that provide both farmers and internal sales resources with platforms to support agronomic and operational decision-making, particularly in the areas of product selection, targeted crop protection application, and financial analysis, designed to help maximize yield and profitability.

Distribution

The seed segment has a diverse worldwide network which markets and distributes the company’s brands to customers, primarily through the company’s multi-channel, multi-brand strategy, which includes four differentiated channels: Pioneer agency model, regional brands, retail brands, as well as third parties through licensing and distribution channels.

The Pioneer agency model is unique to Corteva and represents sales made directly to farmers via independent sales representatives. Through this agency model, the company interacts directly with farmers at multiple points in the growing season, from prior to planting all the way through harvest. These regular interactions enable the company to provide the advice and service farmers need while giving the company real-time insights into the customers’ future ordering decisions. The company’s regional brands connect to customers through regional brand employees and farmer-dealer networks. Retail brands provide a one-stop shop for seed and chemistry solutions and may include sales to distributors, agricultural cooperatives, and dealers. Finally, Corteva out-licenses traits and germplasm to third parties.

Key Raw Materials

The key raw materials for seed include corn and soybean seeds. To produce high-quality seeds, the company contracts with third-party growers globally. Corteva focuses on production close to the customer to provide the seed product, which is suitable for that region and its weed, insect and disease challenges, weather, soil and other conditions. The company conditions and packages the seeds using its own plants and third-party contract manufacturers. By striking a balance between owning production facility assets directly and contracting with third-party growers, the company believes it is best able to maintain flexibility to react to demand changes unique to each geography while minimizing costs. The company seeks to collaborate with strategic seed growers and share its digital agronomy and product management knowledge with them. The company’s third-party growers are an important part of its supply chain. Corteva provides them with rigorous training, planning tools and access to a system that tests and advances products matched to specific geographic needs.

The seed segment's R&D and supply chain groups work seamlessly to select and maintain product characteristics that enhance the quality of its seed products and solutions. Corteva focuses on customer-driven innovation to deliver superior germplasm and trait technologies. With its large sets of digitized data and its seed field management solution, the company can manage its field operations efficiently and draw insights from data quickly and effectively. This allows the company’s supply chain to react quickly to changing customer needs and provides R&D with tremendous amounts of data to analyze and incorporate into resource allocation decisions. The company continues to invest in and build capabilities that drive value via data digitization and analytics that enable it to create an even more responsive and efficient answer to customer needs.

Crop Protection

The crop protection segment serves the global agricultural input industry with products that protect against weeds, insects and other pests, and disease, and that improve overall crop health both above and below ground via nitrogen management and seed-applied technologies. The company offers crop protection solutions that provide farmers the tools they need to improve productivity and profitability, and help keep fields free of weeds, insects and diseases. The company is a leader in global herbicides, insecticides, nitrogen stabilizers and pasture and range management herbicides.

7

Part I

ITEM 1. BUSINESS, continued

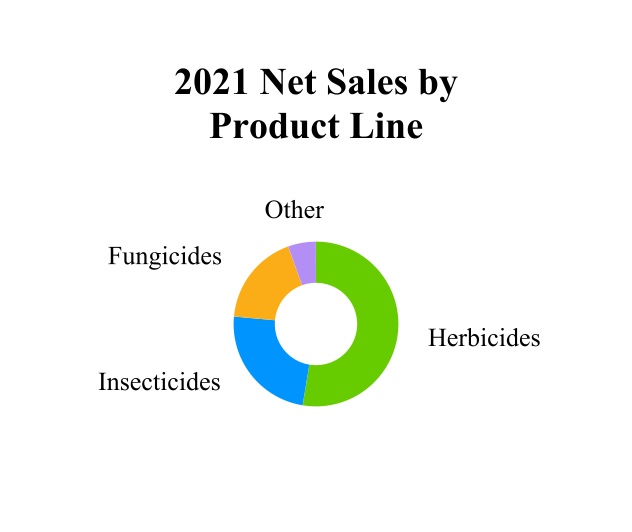

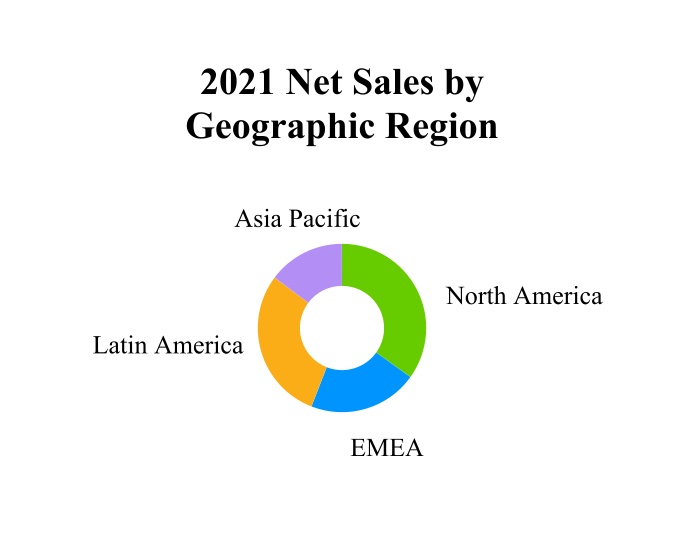

Details on the crop protection segment’s net sales by major product line and geographic region (based on customer location) are as follows:

Products and Brands

The crop protection segment’s major brands and technologies, by key product line, are listed below:

| Insect and Nematode Management | CLOSER™; DELEGATE™; INTREPID®; ISOCLAST™; LANNATE®; EXALT™; PEXALON™; TRANSFORM™; VYDATE®; OPTIMUM®; RADIANT™; SENTRICON™; ENTRUST® SC; GF-120™; and TRACER™ | ||||

| Disease Management | APROACH PRIMA®; VESSARYA®; APROACH™, APROACH POWER®; TALENDO™; TALIUS®; EQUATION PRO®; EQUATION CONTACT®; ZORVEC™; INATREQ™; CURZATE™; TANOS®, FONTELIS™; ACANTO™; and GALILEO® | ||||

| Weed Control | ARIGO®; ARYLEX®; ENLIST™ weed control system; ENLIST ONE™; BROADWAY™; RINSKOR™; ZYPAR™; MUSTANG™; GALLANT™; VERDICT®; LANCET®; KERB™; PIXXARO®; QUELEX™; GALLERY®; CENT-7®; SNAPSHOT®; TRELLIS®; CITADEL™; CLIPPER™; GRANITE®; RAINBOW™; PINDAR® GT; VIPER®; WIDEATTACK®; BELKAR®; WIDEMATCH®; PERFECTMATCH®; CLINCHER™; DURANGO™; FENCER®; GARLON™; SONIC®; TEXARO®; KEYSTONE®; PACTO®; LIGATE®; DIMENSION®; TOPSHOT™; RICER™; LOYANT™; CLASSIC®; REALM® Q; TRIVENCE®; LONTREL®; GRAZON®; PANZER®; PRIMUS®; RESICORE™; SPIDER®; STARANE®; SURESTART®; and TORDON® | ||||

| Nitrogen Management | INSTINCT™; N-LOCK™; N-SERVE® Nitrogen Stabilizer | ||||

Key Raw Materials

The key raw materials and supplies for crop protection include chlorinated pyridines derivatives, specialty intermediates and technical grade active ingredients, chlorine, and seed treatments. Typically, the company purchases major raw materials through long-term contracts with multiple suppliers, which sometimes require minimum purchase commitments. Certain important raw materials are supplied by a few major suppliers. The company expects the markets for its raw materials to remain balanced, though pricing may be volatile given the current state of the global economy. The company relies on contract manufacturers, both domestically and internationally, to produce certain inputs or key components for its product formulations. These inputs are typically sourced close to where the company ultimately formulates and sells its products. Shifts in customer demand, reduced local availability of raw materials, and/or production capacity constraints may, at times, necessitate sourcing from an alternative geography. The company strives to maintain multiple high-quality supply sources for each input.

Corteva’s supply chain strategy will involve managing global supplies of active and intermediate ingredients sourced regionally with global best practices and oversight. Corteva’s supply strategy includes a robust and flexible global footprint to meet future

8

Part I

ITEM 1. BUSINESS, continued

portfolio growth. The company’s supply chain also provides competitive advantages including reducing time to meet customer requirements in regions while minimizing costs through the value chain.

Seasonality

Corteva’s sales are generally strongest in the first half of the calendar year, which aligns with the planting and growing season in the northern hemisphere. The company typically generates about 65 percent of its sales in the first half of the calendar year, driven by northern hemisphere seed and crop protection sales. The company generates about 35 percent of its sales in the second half of the calendar year, led by seed sales in the southern hemisphere. The seasonality in sales impacts both the seed and crop protection segments. The company’s direct distribution channel, where products are shipped to farmers, is more affected by planting delays than its competitors. Generally speaking, unfavorable weather slows the planting season and can affect the company’s quarterly results and sales mix. Severe unfavorable weather, however, can impact overall sales. Accounts receivable tends to be higher during the first half of the year, consistent with the peak sales period in the northern hemisphere, with cash collection focused in the fourth quarter.

Human Capital Management

Corteva aims to attract the best employees, to retain those employees through offering career development and training opportunities while also prioritizing their safety and wellness in an inclusive and productive work environment. The company’s strong employee base of approximately 21,000 employees, along with its commitment to Corteva’s core values, is a key element to the success of its business.

Workforce Composition. As of December 31, 2021, the company globally employs approximately 21,000 employees. In order to address regional specific customer needs within its global business, the company has a geographically diverse employee base with 48%, 18%, 17%, 13% and 4% located in North America, Latin America, Europe, Asia-Pacific and Africa regions, respectively.

Approximately 1% of the workforce is unionized in the United States and another 11% participate in work councils and collective bargaining arrangements outside the United States. In 2021, the company did not experience any work stoppages due to strike or lockouts.

Safety. Living safely is one of the company’s core values by which the company manages its business. The company has implemented safety programs and management practices to promote a culture of safety to protect its employees, as well as the environment. This includes required trainings for employees, as well as specific qualifications and certifications for certain operational employees.

Diversity. The company has a robust inclusion, diversity, and equity (“ID&E”) vision and strategy, based upon the belief that embracing diversity and inclusion benefits the company by creating a workforce with a greater variety of skills and perspectives as a result of their differentiated backgrounds and experiences. Specific ID&E initiatives are identified and tracked to create a culture of belonging where a diverse population of employees are attracted, retained, and engaged. Management is expected to support specific diversity initiatives for their respective geographies and business, as applicable, in order to build a more representative workforce. Critical to creating this environment are company-sponsored employee business resource groups (“BRGs”) that support and promote certain mutual objectives of both the employee and the company, including community engagement and the professional development of employees. The BRGs provide a space where employees can foster connections within a supportive environment. As of the 2021 year end, the company had eight global BRGs, each led by a member of the company’s senior leadership: Disability Awareness Network; Global African Heritage Alliance; Growing Asian Impact Network; Latin Network; Pride (LGBTQ+); Professional Learning Acceleration Network; Veteran’s Network; and Women’s Inclusion Network.

The company is focused on recruitment of diverse candidates and on internal talent development of its diverse leaders so that they can advance their careers and move into leadership positions within the company. The company monitors its diversity and inclusion efforts through periodic engagement surveys and other measures. The results of the company’s efforts, along with its ID&E strategy, are reviewed periodically with the company’s management, and through regular reviews of the company’s leadership pipelines with the People and Compensation Committee of the Board of Directors.

Experienced Management. The company believes its management team has the experience necessary to effectively execute its strategy and advance its product pipelines and technology. The company's chief executive officer and executive vice presidents have an average of approximately 26 years of agriculture experience and are supported by an experienced and talented management team who is dedicated to maintaining and expanding its position as a global force in the agriculture industry.

9

Part I

ITEM 1. BUSINESS, continued

Intellectual Property

Corteva considers its intellectual property estate, which includes patents, trade secrets, trademarks and copyrights, in the aggregate, to constitute a valuable asset of Corteva and actively seeks to secure intellectual property rights as part of an overall strategy to protect its investment in innovations and maximize the results of its research and development program. While the company believes that its intellectual property estate, taken as a whole, provides a competitive advantage in many of its businesses, no single patent, trademark, license or group of related patents or licenses is in itself essential to the company as a whole or to any of the company’s segments.

Trade secrets are an important element of the company's intellectual property. Many of the processes used to make Corteva products are kept as trade secrets which, from time to time, may be licensed to third parties. Corteva vigilantly protects all of its intellectual property including its trade secrets. When the company discovers that its trade secrets have been unlawfully taken, it reports the matter to governmental authorities for investigation and potential criminal action, as appropriate. In addition, the company takes measures to mitigate any potential impact, which may include civil actions seeking redress, restitution and/or damages based on loss to the company and/or unjust enrichment.

Patents & Trademarks: Corteva continually applies for and obtains U.S. and foreign patents and has access to a large patent portfolio, both owned and licensed. Corteva’s rights under these patents and licenses, as well as the products made and sold under them, are important to the company in the aggregate. The protection afforded by these patents varies based on country, scope of individual patent coverage, as well as the availability of legal remedies in each country. This significant patent estate may be leveraged to align with the company’s strategic priorities within and across product lines. At December 31, 2021, the company owned about 5,600 U.S. patents and about 11,100 active patents outside of the U.S.

Remaining life of granted patents owned as of December 31, 2021:

| Approximate U.S. | Approximate Other Countries | |||||||

| Within 5 years | 700 | 1,300 | ||||||

| 6 to 10 years | 1,700 | 4,300 | ||||||

| 11 to 16 years | 2,100 | 5,100 | ||||||

| 16 to 20 years | 1,100 | 400 | ||||||

| Total | 5,600 | 11,100 | ||||||

In addition to its owned patents, the company owns over 5,500 patent applications.

The company also owns or has licensed a substantial number of trade names, trademarks and trademark registrations in the United States and other countries, including approximately 14,500 registrations and pending trademark applications in a number of jurisdictions.

In addition, the company holds multiple long-term biotechnology trait licenses from third parties in the normal course of business. Most corn hybrids and soybean varieties sold to customers contain biotechnology traits licensed from third parties under these long-term licenses.

Competition

The company competes with producers of seed germplasm, trait developers, and crop protection products on a global basis. The global market for products within the industry is highly competitive and the company believes competition has and will continue to intensify. Corteva competes based on germplasm and trait leadership, price, quality and cost competitiveness and the offering of a holistic solution. The company’s key competitors include BASF, Bayer, FMC and ChemChina, as well as companies trading in generic crop protection chemicals and regional seed companies.

Environmental Matters

Information related to environmental matters is included in several areas of this report: (1) Environmental Proceedings beginning on page 28, (2) Management's Discussion and Analysis of Financial Condition and Results of Operations beginning on pages 61, 66-68 and (3) Note 2 - Summary of Significant Accounting Policies, and Note 18 - Commitments and Contingent Liabilities, to the Consolidated Financial Statements.

10

Part I

ITEM 1. BUSINESS, continued

Regulatory Considerations

Our seed and crop protection products and operations are subject to certain approval procedures, manufacturing requirements and environmental protection laws and regulations in the jurisdictions in which we operate. We evaluate and test products throughout the research and development phases, and each new technology undergoes further rigorous scientific studies and tests to validate that the product can be used effectively and that use of the technology is safe for humans and animals and does not cause undue harm to the environment when used in accordance with the directions for use.

The regulatory approval processes and procedures globally are becoming increasingly more complex, which has resulted in additional testing needs, difficult to predict and longer approval timelines, and higher development and maintenance costs. We continue to invest on an ongoing basis to keep dossiers current, respond to regulators and meet evolving regulatory standards required by global regulatory frameworks. Failure to comply with these regulations or future regulatory bans and requirements related to our products and their use may materially impact our financial performance. The increase in timelines for regulatory approvals may result in the company not achieving its sustainability targets, or its anticipated returns on research and development investments.

Regulation of Genetically Modified Organisms (“GMOs”)

Genetically modified seed products are subject to regulatory approval processes and procedures. For example, in the United States, the Coordinated Framework for Regulation of Biotechnology governs genetically modified organisms, using existing U.S. legislation and legal authorities on food, feed and environmental safety. Plant GMOs are regulated by the U.S. Department of Agriculture’s (the “USDA”) Animal and Plant Health Inspection Service (the “APHIS”) under the Plant Protection Act. The APHIS assesses the trait to ensure that the trait will not pose a plant pest and is not a noxious weed. GMOs in food are regulated by the Food and Drug Administration (the “FDA”) under the Federal Food, Drug, and Cosmetic Act (the “FFDCA”). The FDA ensures that the food is safe for food and feed. Pesticides and microorganisms containing GMOs are regulated by the Environmental Protection Agency (the “EPA”) pursuant to the Federal Insecticide, Fungicide and Rodenticide Act (the “FIFRA”) and the Toxic Substances Control Act. The EPA assesses the trait or the stack containing the traits to ensure that there is no unreasonable adverse effect to the environment.

Other countries also have rigorous approval processes, procedures, and scientific testing requirements for the cultivation or import of genetically modified seed products. In the United States and other countries that have functioning regulatory systems, a rigorous scientific review is conducted by these agencies to demonstrate that genetically modified products are as safe as traditionally bred, non-biotech/GMO counterparts for food, feed and the environment. Various countries in EMEA, Latin America, and Asia have banned GMOs entirely.

Regulation of Crop Protection Products

Globally, manufacturers of crop protection products, including herbicides, fungicides and insecticides are required to submit an application/dossier and obtain government regulatory approval prior to selling products in a particular country. In the United States, the EPA is responsible for registering and overseeing the approval and marketing of pesticides, pursuant to the FIFRA, the FFDCA and the Food Quality Protection Act. Also, the USDA and the FDA monitor levels of pesticide residue that is allowed on or in crops. Already registered pesticides are required to be re-registered every 15 years to ensure that those products continue to meet the rigorous safety standards set by the regulators. The EPA reevaluates pesticide tolerances at least every 10 years, taking into account ecological and human health risks, in addition to cumulative risks as a result of multiple routes of and sources of exposure.

As of January 2022, before registering any new conventional pesticide active ingredient, the EPA will evaluate the potential effects on listed species and their designated critical habitats under the Endangered Species Act (the “ESA”). EPA also has initiated such evaluations for certain other active ingredients in response to existing or threatened litigation. Where the EPA determines that a pesticide in the registration and re-evaluation processes “may affect” a listed species, the EPA must consult with the U.S. Fish and Wildlife Service and the National Marine Fisheries Service. As part of its approval, registration, and reevaluation processes, the EPA may impose certain use restrictions on crop protection products under the ESA. Under the citizen suit provisions, the ESA also includes citizen suit provisions that allow the public to bring suit in court against federal agencies when they believe a listed species is not being adequately protected by the EPA.

The company's European operations are subject to the European chemical regulation REACH (“Registration, Evaluation, Authorisation, and Restriction of Chemicals”) and the CLP (“Classification, Labeling, and Packaging of Substances and Mixtures”). Other jurisdictions also have rigorous approval processes, procedures and scientific testing requirements for the approval of crop protection products. We continue to monitor legislative and regulatory developments related to pollution and other environmental health and safety matters.

European Farm to Fork Strategy

In October 2021, a majority of the European Parliament adopted the Farm to Fork Strategy setting forth the European Union’s plans to increase organic farming. As part of this strategy, the E.U. Commission has set aggressive 2030 targets to reduce by 50% the use and risk of chemical pesticides and the use of more hazardous pesticides by 50%. Additionally, as part of this strategy, the E.U. Commission is targeting having 25% of the European Union’s agricultural land under organic farming by

11

Part I

ITEM 1. BUSINESS, continued

2030. The E.U. Commission is also expected to propose mandatory front-of-pack nutrition labelling and develop a food labelling framework covering the nutritional, climate, environmental and social aspects of food products. While the company has a growing product portfolio supportive to organic agriculture, the implementation of this strategy may decrease the size of the market for its products within the European Union.

Available Information

The company's annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are accessible on Corteva's website at http://investors.corteva.com by clicking on the section labeled "Financial Information", then on "SEC Filings." These reports are made available, without charge, as soon as is reasonably practicable after the company files or furnishes them electronically with the Securities and Exchange Commission. No portion of the company's website mentioned in this report, or the materials contained on it, have been made part of this annual report on Form 10-K or incorporated herein by reference, unless such incorporation is specifically mentioned herein.

12

Part I

ITEM 1A. RISK FACTORS

Risks Related to our Industry

The successful development and commercialization of Corteva's pipeline products will be necessary for Corteva's growth.

Corteva uses advanced breeding technologies to produce hybrids and varieties with superior performance in farmers’ fields and uses biotechnology to introduce traits that enhance specific characteristics of its crops. Corteva also uses advanced analytics, software tools, mobile communications and new planting and monitoring equipment to provide agronomic recommendations to growers. Additionally, Corteva conducts research into biological and chemical products to protect farmers’ crops from pests and diseases and enhance plant productivity.

New product concepts may be abandoned for many reasons, including greater anticipated development costs, technical difficulties, lack of efficacy, regulatory obstacles or inability to market under regulatory frameworks, competition, inability to prove the original concept, lack of demand and the need to divert focus, from time to time, to other initiatives with perceived opportunities for better returns. The processes of active ingredient development or discovery, breeding, biotechnology trait discovery and development and trait integration are lengthy, and a very small percentage of the chemicals, genes and germplasm Corteva tests is selected for commercialization. Furthermore, the length of time and the risk associated with the breeding and biotech pipelines are interlinked because both are required as a package for commercial success in markets where biotech traits are approved for growers. For example, the commercial transition to the company’s Enlist E3™ and Conkesta E3® soybean technologies, which are packaged with its Enlist One® and Enlist Duo® herbicides, is expected to take the company several years to complete. In countries where biotech traits are not approved for widespread use, Corteva’s seed sales depend on the quality of its germplasm. While initial commercialization efforts have been promising, there are no guarantees that anticipated levels of product acceptability within Corteva's markets will be achieved or that higher quality products will not be developed by Corteva's competitors in the future.

Speed in discovering, developing, protecting and responding to new technologies, including new technology-based distribution channels that could facilitate Corteva’s ability to engage with customers and end users, and bringing related products to market is a significant competitive advantage. Commercial success frequently depends on being the first company to the market, and many of Corteva’s competitors are also making considerable investments in similar new biotechnology products, improved germplasm products, biological and chemical products and agronomic recommendation products.

Corteva may not be able to obtain or maintain the necessary regulatory approvals for some of its products, including its seed and crop protection products, which could restrict its ability to sell those products in some markets.

Regulatory and legislative requirements affect the development, manufacture and distribution of Corteva’s products, including the testing and planting of seeds containing Corteva’s biotechnology traits and the import of crops grown from those seeds, and non-compliance can harm Corteva’s sales and profitability.

Seed products incorporating biotechnology derived traits and crop protection products must be extensively tested for safety, efficacy and environmental impact before they can be registered for production, use, sale or commercialization in a given market. In certain jurisdictions, Corteva must periodically renew its approvals for both biotechnology and crop protection products, which typically require Corteva to demonstrate compliance with then-current standards which generally are more stringent since the prior registration. The regulatory approvals process is lengthy, costly, complex and in some markets unpredictable, with requirements that can vary by product, technology, industry and country. The regulatory approvals process for products that incorporate novel modes of action or new technologies can be particularly unpredictable and uncertain due to the then-current state of regulatory guidelines and objectives, as well as governmental policy considerations and non- governmental organization and other stakeholder considerations. The uncertainty and increased length of regulatory approvals may reduce Corteva’s return on its research and development investments, and impede its ability to meet sales, profitability, or sustainability metrics.

Furthermore, the detection of biotechnology traits or chemical residues from a crop protection product not approved in the country in which Corteva sells or cultivates its product, or in a country to which Corteva imports its product, may affect Corteva’s ability to supply its products or export its products, or even result in crop destruction, product recalls or trade disruption, which could result in lawsuits and termination of licenses related to biotechnology traits and raw material supply agreements. Delays in obtaining regulatory approvals to import, including those related to the importation of crops grown from

13

Part I

ITEM 1A. RISK FACTORS, continued

seeds containing certain traits or treated with specific chemicals, may influence the rate of adoption of new products in globally traded crops.

Additionally, the regulatory environment may be impacted by the activities of non-governmental organizations and special interest groups and stakeholder reaction to actual or perceived impacts of new and existing technology, products or processes on safety, health and the environment. Obtaining and maintaining regulatory approvals requires submitting a significant amount of information and data, which may require participation from technology providers. Regulatory standards and trial procedures are continuously changing. In addition, Corteva has seen an increase in recent years in the number of lawsuits filed by those who identify themselves as public or environmental interest groups seeking to invalidate pesticide product registrations and/or challenge the way federal or state governmental entities apply the rules and regulations governing pesticide produce use. The pace of change together with the lack of regulatory harmony could result in unintended noncompliance. Responding to these changes and meeting existing and new requirements may involve significant costs or capital expenditures or require changes in business practice that could result in reduced profitability. The failure to receive necessary permits or approvals could have near- and long-term effects on Corteva’s ability to produce and sell some current and future products.

The degree of public understanding and acceptance or perceived public acceptance of Corteva’s biotechnology and other agricultural products and technologies can affect Corteva’s sales and results of operations by affecting planting approvals, regulatory requirements and customer purchase decisions.

Concerns and claims regarding the safe use of seeds with biotechnology traits and crop protection products in general, their potential impact on health and the environment, and the perceived impacts of biotechnology on health and the environment, reflect a growing trend in societal demands for increasing levels of product safety and environmental protection. These include concerns and claims that increased use of crop protection products, drift, inversion, volatilization and the use of biotechnology traits meant to reduce the resistance of weeds or pests to control by crop protection products, could increase or accelerate such resistance and otherwise negatively impact health and the environment. These and other concerns could manifest themselves in stockholder proposals, preferred purchasing, delays or failures in obtaining or retaining regulatory approvals, delayed product launches, lack of market acceptance, product discontinuation, continued pressure for and adoption of more stringent regulatory intervention and litigation, termination of raw material supply agreements and legal claims. These and other concerns could also influence public perceptions, the viability or continued sales of certain of Corteva’s products, Corteva’s reputation and the cost to comply with regulations. As a result, such concerns could have a material adverse effect Corteva’s business, results of operations, financial condition and cash flows.

Changes in agricultural and related policies of governments and international organizations may prove unfavorable.

In many markets there are various pressures to reduce government subsidies to farmers, which may inhibit the growth in these markets of products used in agriculture. In addition, government programs that create incentives for farmers may be modified or discontinued. However, it is difficult to predict accurately whether, and if so when, such changes will occur. Corteva expects that the policies of governments and international organizations will continue to affect the planting choices made by growers as well as the income available to growers to purchase products used in agriculture and, accordingly, the operating results of the agriculture industry.

Corteva participates in an industry that is highly competitive and has undergone consolidation, which could increase competitive pressures.

Corteva currently faces significant competition in the markets in which it operates. In most segments of the market, the number of products available to the grower is steadily increasing as new products are introduced. At the same time, certain products are coming off patent and are thus available to generic manufacturers for production and commercialization. Additionally, data analytic tools and web-based new direct purchase models offer increased transparency and comparability, which creates price pressures. Corteva cannot predict the pricing or promotional actions of its competitors. Aggressive marketing or pricing by Corteva’s competitors could adversely affect Corteva’s business, results of operations and financial conditions. As a result, Corteva continues to face significant competitive challenges.

Corteva’s business may be materially affected by competition from manufacturers of generic products.

Competition from manufacturers of generic products is a challenge for Corteva’s branded products around the world, and the loss or expiration of intellectual property rights can have a significant adverse effect on Corteva’s revenues. The date at which

14

Part I

ITEM 1A. RISK FACTORS, continued

generic competition commences may be different from the date that the patent or regulatory exclusivity expires. However, upon the loss or expiration of patent protection for one of Corteva’s products or of a product that Corteva licenses, or upon the “at- risk” launch (despite pending patent infringement litigation against the generic product) by a generic manufacturer of a generic version of one of Corteva’s patented products or of a product that Corteva licenses, Corteva can lose a major portion of revenues for that product, which can have a material adverse effect on Corteva’s business.

The costs of complying with evolving regulatory requirements could negatively impact Corteva’s business, results of operations and financial condition. Actual or alleged violations of environmental laws or permit requirements could result in restrictions or prohibitions on plant operations, substantial civil or criminal sanctions, as well as the assessment of strict liability and/or joint and several liability.

Corteva is subject to extensive federal, state, local and foreign laws, regulations, rules and ordinances relating to pollution, protection of the environment, waste water discharges, the generation, storage, handling, transportation, treatment, disposal and remediation of hazardous substances and waste materials and the use of genetically modified seeds and crop protection active ingredients by growers.

Environmental and health and safety laws, regulations and standards expose Corteva to the risk of substantial costs and liabilities, including liabilities associated with Corteva’s business and the discontinued and divested businesses and operations of EID. As is typical for businesses like Corteva’s, soil and groundwater contamination has occurred in the past at certain sites and may be identified at other sites in the future. Disposal of waste from Corteva’s business at off-site locations also exposes it to potential remediation costs. Consistent with past practice, Corteva is continuing to monitor, investigate and remediate soil and groundwater contamination at several of these sites.

Costs and capital expenditures relating to environmental, health or safety matters are subject to evolving regulatory requirements and depend on the timing of the promulgation and enforcement of specific standards which impose the requirements. Moreover, changes in environmental regulations, including those related to climate change, could inhibit or interrupt Corteva’s operations, or require modifications to its facilities in the future. Accordingly, environmental, health or safety regulatory matters could result in significant unanticipated costs or liabilities, which may be materially higher than Corteva’s accruals.

Climate change and unpredictable seasonal and weather factors could impact Corteva’s sales and earnings.

The agriculture industry is subject to seasonal and weather factors, which can vary unpredictably from period to period. Weather factors can affect the presence of disease and pests on a regional basis and, accordingly, can positively or adversely affect the demand for crop protection products, including the mix of products used or the level of returns. The weather also can affect the quality, volume and cost of seed produced for sale as well as demand and product mix. Seed yields can be higher or lower than planned, which could lead to higher inventory and related write-offs. Climate change may increase the frequency or intensity of extreme weather such as storms, floods, heat waves, droughts and other events that could affect the quality, volume and cost of seed produced for sale as well as demand and product mix. Climate change may also affect the availability and suitability of arable land and contribute to unpredictable shifts in the average growing season and types of crops produced.

Corteva’s business is subject to various competition and antitrust, rules and regulations around the world, and as the size of its business grows, scrutiny of its business by legislators and regulators in these areas may intensify.

On July 9, 2021, President Biden issued an executive order promoting competition in the American economy. The order encouraged further examination and efforts by U.S. regulatory agencies to avoid market concentrations for agricultural inputs, that could challenge the survival of family farms. The executive order also directs the U.S. Secretary of Agriculture to take action to ensure that the intellectual property system, while still incentivizing innovation, does not also unnecessarily reduce competition in seed and other agricultural input markets beyond what is reasonably contemplated by the U.S. Patent Act and propose strategies for addressing those concerns across intellectual property, antitrust, and other relevant laws. While the ultimate impact of the executive order will depend on the actions ultimately resulting from the U.S. regulatory authorities, actions taken by such authorities may increase the regulation and regulatory costs associated with the agriculture industry in the future and restrict the company from pursuing certain growth opportunities, including mergers and acquisitions.

Scrutiny from regulators in the U.S. and abroad may intensify as Corteva’s business presence grows. This scrutiny and related investigations, even when not resulting in an enforcement action, may result in damage to a company’s reputation, significant

15

Part I

ITEM 1A. RISK FACTORS, continued

defense expense, as well as become a distraction to management. Antitrust and competition enforcement actions may result in regulators imposing fines, penalties, or restrictions on a company’s business practices in a manner that may significantly impact its results of operations.

Corteva’s sales to its customers may be adversely affected should a company successfully establish an intermediary platform for the sale of Corteva’s products or otherwise position itself between Corteva and its customers.

Corteva services customers primarily through the Pioneer direct sales channel in key agricultural geographies, including the United States. In addition, Corteva supplements this approach with strong retail channels, including distributors, agricultural cooperatives and dealers, and with digital solutions that assist farmer decision-making with a view to optimize their product selection and maximize their yield and profitability. While Corteva expects the indirect channels and its digital platform will extend its reach and increase exposure of its products to other potential customers, including smaller farmers or farmers in less concentrated areas, there can be no assurance that Corteva will be successful in this regard. If a competitor were to successfully establish an intermediary platform for distribution of Corteva’s products, especially with respect to Corteva’s digital platform, it may disrupt Corteva’s distribution model and inhibit Corteva’s ability to provide a complete go-to-market strategy covering the direct, dealer and retail channels. In such a circumstance, Corteva’s sales may be adversely affected.

Risks Related to Our Operations

Corteva is dependent on its relationships or contracts with third parties with respect to certain of its raw materials or licenses and commercialization.

Corteva is dependent on third parties in the research, development and commercialization of its products and enters into transactions including, but not limited to, supply agreements and licensing agreements in connection with Corteva’s business. The majority of Corteva’s corn hybrids and soybean varieties sold to customers contain biotechnology traits that Corteva licenses from third parties under long-term licenses. If Corteva loses its rights under such licenses, it could negatively impact Corteva’s ability to obtain future licenses on competitive terms, commercialize new products and generate sales from existing products. To maintain such licenses, Corteva may elect to out-license its technology, including germplasm. There can be no guarantee that such out-licensing will not ultimately strengthen Corteva’s competition thereby adversely impacting Corteva’s results of operations.

While Corteva relies heavily on third parties for multiple aspects of its business and commercialization activities, Corteva does not control many aspects of such third parties’ activities. Third parties may not complete activities on schedule or in accordance with Corteva’s expectations. Failure by one or more of these third parties to meet their contractual or other obligations to Corteva or to comply with applicable laws or regulations, or any disruption in the relationship between Corteva and one or more of these third parties could delay or prevent the development, approval or commercialization of Corteva’s products and could also result in non-compliance or reputational harm, all with potential negative implications for Corteva’s business.

In addition, Corteva’s agreements with third parties may obligate it to meet certain contractual or other obligations to third parties. For example, Corteva may be obligated to meet certain thresholds or abide by certain boundary conditions. If Corteva were to fail to meet such obligations to the third parties, its relationship with such third parties may be disrupted. Such a disruption could negatively impact certain of Corteva’s licenses on which it depends, could cause reputational harm, and could negatively affect Corteva’s business, results of operations and financial condition.

Corteva’s business, results of operations and financial condition could be adversely affected by industrial espionage and other disruptions to its supply chain, information technology or network systems.

Business and/or supply chain disruptions, plant and/or power outages and information technology system and/or network disruptions, regardless of cause including acts of sabotage, employee error or other actions, geo-political activity, military conflict, local epidemics or pandemics, weather events and natural disasters could seriously harm Corteva’s operations as well as the operations of its customers and suppliers. For example, a pandemic in locations where Corteva has significant operations, sales, or key suppliers could have a material adverse effect on Corteva’s results of operations. In addition, terrorist attacks and natural disasters have increased stakeholder concerns about the security and safety of chemical production and distribution.

Business and/or supply chain disruptions may also be caused by security breaches, which could include, for example, ransomware attacks and attacks on information technology and infrastructure by hackers, viruses, breaches due to employee

16

Part I

ITEM 1A. RISK FACTORS, continued

error or actions or other disruptions. Corteva and/or its suppliers may fail to effectively prevent, detect and recover from these or other security breaches and, as a consequence, such breaches could result in misuse of Corteva’s assets, business disruptions, loss of property including trade secrets and confidential business information, legal claims or proceedings, reporting errors, processing inefficiencies, negative media attention, loss of sales and interference with regulatory and data privacy compliance.

Like most major corporations, Corteva is the target of industrial espionage, including cyber-attacks, from time to time. Corteva has determined that these incidents have resulted, and could result in the future, in unauthorized parties gaining access to certain confidential business information. However, to date, Corteva has not experienced any material financial impact, changes in the competitive environment or impact on business operations from these events. Although management does not believe that Corteva has experienced any material losses to date related to industrial espionage and security breaches, including cybersecurity incidents, there can be no assurance that Corteva will not suffer such losses in the future.

Corteva actively manages the risks within its control that could lead to business disruptions and security breaches. As these threats continue to evolve, particularly around cybersecurity, Corteva may be required to expend significant resources to enhance its control environment, processes, practices and other protective measures. Despite these efforts, such events could also have a material adverse effect on Corteva’s business, financial condition, results of operations and reputation. Additionally, any losses from such an event may be excluded from, or in excess of the coverages provided by Corteva's insurance policies.

Volatility in Corteva’s input costs, which include raw materials and production costs, could have a significant impact on Corteva’s business, results of operations and financial condition.

Corteva’s input costs are variable based on the costs associated with production or with raw materials Corteva uses. For example, Corteva’s production costs vary, especially on a seasonal basis where changes in weather influence supply and demand. In addition, Corteva’s manufacturing processes consume significant amounts of raw materials, the costs of which are subject to worldwide supply and demand as well as other factors beyond Corteva’s control. Corteva refers to these costs collectively as input costs. Significant variations in input costs affect Corteva’s operating results from period to period.

When possible, Corteva purchases raw materials through negotiated long-term contracts to minimize the impact of price fluctuations. Corteva also enters into over-the-counter and exchange traded derivative commodity instruments to hedge its exposure to price fluctuations on certain raw material purchases. In addition, Corteva takes actions to offset the effects of higher input costs through selling price increases, productivity improvements and cost reduction programs. Success in offsetting higher input costs with price increases is largely influenced by competitive and economic conditions and could vary significantly depending on the market served. If Corteva is not able to fully offset the effects of higher input costs, it could have a significant impact on its financial results.

Corteva’s liquidity, business, results of operations and financial condition could be impaired if it is unable to raise capital through the capital markets or short-term debt borrowings.

Any limitation on Corteva’s ability to raise money in the capital markets or through short-term debt borrowings could have a substantial negative effect on Corteva’s liquidity. Corteva’s ability to affordably access the capital markets and/or borrow short- term debt in amounts adequate to finance its activities could be impaired as a result of a variety of factors, including factors that are not specific to Corteva, such as a severe disruption of the financial markets and, in the case of debt securities or borrowings, interest rate fluctuations. Due to the seasonality of Corteva’s business and the credit programs Corteva may offer its customers, net working capital investment and corresponding debt levels will fluctuate over the course of the year.

Corteva regularly extends credit to its customers to enable them to purchase seeds or crop protection products at the beginning of the growing season. The customer receivables may be used as collateral for short-term financing programs. Any material adverse effect upon Corteva’s ability to own or sell such customer receivables, including seasonal factors that may impact the amount of customer receivables Corteva owns, may materially impact Corteva’s access to capital.

Corteva has additional agreements with financial institutions to establish programs that provide financing for select customers of Corteva’s seed and crop protection products in the United States, Latin America, Europe and Asia. The programs are renewed on an annual basis. In most cases, Corteva guarantees the extension of such credit to such customers. If Corteva is unable to renew these agreements or access the debt markets to support customer financing, Corteva’s sales may be negatively impacted, which could result in increased borrowing needs to fund working capital.

17

Part I

ITEM 1A. RISK FACTORS, continued

Corteva’s earnings, operations and business, among other things, will impact its credit ratings, costs and availability of financing. There can be no assurance that Corteva or EID will maintain its current or prospective credit ratings. A decrease in the ratings assigned to Corteva or EID by the ratings agencies may negatively impact Corteva’s liquidity, access to the debt capital markets and increase Corteva’s cost of borrowing and the financing of its seasonal working capital.

Corteva’s customers may be unable to pay their debts to Corteva, which could adversely affect Corteva’s results.

Corteva offers its customers financing programs with credit terms generally less than one year from invoicing in alignment with the growing season. Due to these credit practices as well as the seasonality of Corteva’s operations, Corteva may need to issue short-term debt at certain times of the year to fund its cash flow requirements. Corteva’s customers may be exposed to a variety of conditions that could adversely affect their ability to pay their debts. For example, customers in economies experiencing an economic downturn or in a region experiencing adverse growing conditions may be unable to repay their obligations to Corteva, which could adversely affect Corteva’s results.

Increases in pension and other post-employment benefit plan funding obligations may adversely affect Corteva’s results of operations, liquidity or financial condition.

Through Corteva's ownership of EID, Corteva maintains EID defined benefit pension and other post-employment benefit plans. For some of these plans, including EID’s principal U.S. pension plan, Corteva continues as sponsor for the entire plan regardless of whether participants, including retirees, are or were associated with EID’s agriculture business. Corteva uses many assumptions in calculating its expected future payment obligations under these plans. Significant adverse changes in credit or market conditions could result in actual rates of returns on pension investments being lower than assumed. In addition, expected future payment obligations may be adversely impacted by changes in assumptions regarding participants, including retirees. In 2022, Corteva expects to contribute approximately $60 million to its pension plans other than the principal U.S. pension plan, and about $140 million for its other post-employment benefit ("OPEB") plans. While not anticipated for 2022, Corteva may make potential discretionary contributions to the principal U.S. pension plan. Corteva, furthermore, may be required to make significant contributions to its pension plans in the future, which could adversely affect Corteva’s results of operations, liquidity and financial condition.

Corteva’s business, results of operations and financial condition could be adversely affected by environmental, litigation and other commitments and contingencies.

As a result of Corteva’s operations, including past operations and those related to divested businesses and discontinued operations of EID, Corteva incurs environmental operating costs for pollution abatement activities including waste collection and disposal, installation and maintenance of air pollution controls and wastewater treatment, emissions testing and monitoring and obtaining permits. Corteva also incurs environmental operating costs related to environmental related research and development activities including environmental field and treatment studies as well as toxicity and degradation testing to evaluate the environmental impact of products and raw materials. In addition, Corteva maintains and periodically reviews and adjusts its accruals for probable environmental remediation and restoration costs.