UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM

_________________

| (Mark One) | ||

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended |

or

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to |

Commission File Number:

_____________________

(Exact name of registrant as specified in its charter)

_____________________

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| OTC |

_________________

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Smaller reporting company | ||

| Emerging Growth Company | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as

defined in Rule 12b-2 of the Act). Yes ☐

The aggregate market value of the voting

and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the

average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second

fiscal quarter was $

As of April 15, 2023, there were shares outstanding of the registrant’s common stock.

TABLE OF CONTENTS

PART I

| Item 1. | Business |

(a) Business Development

The Company was organized under the laws of the State of Nevada on September 19, 2009, under its current name. The Company was a development stage company with the goal of becoming a design, engineer, construct, market and sell high-quality PV SEFs for commercial and utility applications to local markets.

Prior to June 1, 2012, we were engaged in exploration for commercially recoverable metal-bearing mineral deposits. On June 1, 2012, we entered into an agreement with Xunyang Yongjin Mining Co., Ltd. to transfer our mining exploration rights for a cash payment. Further, on December 30, 2013, our subsidiary, Shaanxi Changjiang Mining & New Energy Co., Ltd (“Shaanxi Changjiang”), entered into Equity Transfer Agreements with officers of the Company, whereby the Company’s subsidiaries were sold off.

Business operations for China Chingjiang Mining & New Energy Energy Co., Ltd. and its subsidiaries were abandoned by former management and a custodianship action, as described in the subsequent paragraph, was commenced in 2020. The Company filed its last 10-Q in 2017, this financial report included liabilities and debts. As of the date of this filing, these liabilities and debts have not been addressed and remain on the Company’s books.

On February 3, 2020, the Eighth District Court of Clark County, Nevada granted the Application for Appointment of Custodian as a result of the absence of a functioning board of directors and the revocation of the Company’s charter. The order appointed Small Cap Compliance, LLC (“SCC”) custodian with the right to appoint officers and directors, negotiate and compromise debt, execute contracts, issue stock, and authorize new classes of stock.

The court awarded custodianship to Small Cap Compliance, LLC (sole member is Rhonda Keaveney) based on the absence of a functioning board of directors, revocation of the company’s charter, and abandonment of the business. At this time, Ms. Keaveney was appointed sole officer and director.

Upon appointment as custodian of CHJI and under its duties stipulated by the Nevada court, SCC took initiative to organize the business of the issuer. As custodian, the duties were to conduct daily business, hold shareholder meetings, appoint officers and directors, reinstate the company with the Nevada Secretary of State. SCC also had authority to enter into contracts and find a suitable merger candidate. SCC was compensated for its role as custodian in the amount of 1,000,000 shares of Convertible Series C Preferred Stock. SCC did not receive any additional compensation, in the form of cash or stock, for custodian services. The custodianship was discharged on May 18, 2020.

On August 23, 2020, SCC entered into a Stock Purchase Agreement with Bridgeview Capital Partners, LLC whereby Bridgeview Capital Partners, LLC purchased 1,000,000 shares of Convertible Series C Preferred Stock. These shares represent the controlling block of stock. Ms. Keaveney resigned his position of sole officer and director and appointed Dr. Chongyi Yang as CEO, Treasurer, Secretary, and Director of the Company.

Bridgeview Capital Partners, LLC is controlled by Michael Dobbs and Sean Lanci.

On August 23, 2020, Bridgeview Capital Partners, LLC entered into a Stock Purchase with Cathay Capital Management Inc. (“Cathay”) whereby Cathay purchased 1,000,000 shares of Convertible Series C Preferred Stock. Chongyi Yang is the control person for Cathay.

The Company transitioned from mining to clean new energy. Our current business is focused on the solar photovoltaic, or “PV”.

When the sun shines onto a solar panel, energy from the sunlight is absorbed by the PV cells in the panel. This energy creates electrical charges that move in response to an internal electrical field in the cell, causing electricity to flow.

Concentrating solar-thermal power (CSP) systems use mirrors to reflect and concentrate sunlight onto receivers that collect solar energy and convert it to heat, which can then be used to produce electricity or stored for later use. It is used primarily in very large power plants.

| 1 |

The Company’s green energy business unit is committed to providing customers and partners with professional and comprehensive green new energy project solution services.

We build rural revitalization smart new energy photovoltaic. Specifically we will focus on 5G smart street lamp energy storage and charging, integrated charging stations and rural new energy vehicles, low-carbon parks, and commercial and household rooftop photovoltaic green power.

Industry overview

Solar photovoltaic energy is an emerging, clean energy industry with a growing market share. Application of solar energy in developed countries such as Germany and Japan, are relatively comprehensive and mature. At the present time, the Chinese PV downstream market is still in the initial stages of development, though most of the PV modules are manufactured in China.

China's solar PV module manufacturers were hit by the European Union and the United States anti-dumping sanctions. Businesses and governments are trying to find better alternative applications market to absorb the huge domestic surplus solar PV capacity. The untapped domestic PV downstream market is one of the best ways to absorb the surplus production capacity.

The Chinese government is encouraging the construction of a large PV base and the development of distributed photovoltaic. Currently, we mainly focus on the development of distributed photovoltaic power generation projects.

We believe the next few years will show protracted continued growth in the PV solar market. Government policies, in the form of both regulation and incentives, have accelerated the adoption of solar technologies by businesses and consumers and have provided opportunities for developers to construct PV systems as an alternative to more traditional forms of power generation.

Our Industry and Principal Market

Sales and Marketing

We are establishing a sales and marketing department which is focused on identifying and establishing relationships with entities that are likely to have a need for our products and services.

Our products and services are expected to be largely represented through our Company's sales force located in China

Current Business Operations

At the present time, our focus is on serving the local solar PV generation market.

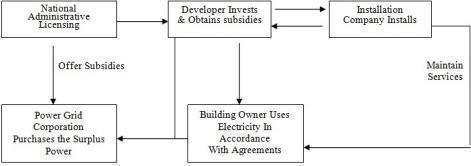

The following chart illustrates our distributed solar PV business model.

| 2 |

Solar PV Industry

General

Though we may be a new participant in solar PV industry, we also realized that the local downstream market of solar PV industry was as new as we are. Experience in some developed countries has shown that there should be a business opportunity in China's PV downstream market in the near future.

Each of our EPC projects is a strategic long-term investment, with relatively low risk, a stable cash inflow can be generated and little ongoing maintenance costs would be incurred once the project begins operations.

Competition

We anticipate that our competitors in the solar PV markets will be local and regional EPC contractors and developers. Other companies in China that engage in solar PV power generation that we consider to be likely competitors, include: Xi'an Huanghe Photovoltaic Technology Co., Ltd., Shaanxi Tuori New Energy Technology Limited, and Shaanxi Changling Electric Co., Ltd., etc. These competitors have more experience in the operation of solar PV energy and have superior financial resources than we do.

The entire solar industry also faces competition from other power generation sources, both conventional sources as well as other emerging technologies. Solar power has certain advantages and disadvantages when compared to other power generating technologies. The advantages include the ability to deploy products in many sizes and configurations, provide reliable power for many applications, serve as both a power generator and the skin of a building and eliminate air, water and noise emissions. The disadvantages mainly came from the relatively high cost of power generation.

The cost of electricity generated by PV products currently is very close to the cost of electricity generated from conventional power such as coal and hydropower in Chinese markets. A significant reduction in the scope or discontinuation of government incentive programs could cause demand for our products and our revenue to decline, and have a material adverse effect on our business, financial condition, results of operations and prospects.

As an emerging industry, the rapid growth of the solar PV could reduce the intensity of competition from alternative products and services.

In the near term, mature government subsidy roadmaps from the government have led developers to be aggressive with their solar installations so that they can enjoy better economic returns. Cost reductions of solar installations have proven to be viable and have also led to aggressive solar installation. In the long run, we believe that solar energy continues to have significant future growth potential and that demand for our products and services will continue to grow significantly for the following reasons:

| · | increasing demand for renewable energies, including solar energy, due to the finiteness of fossil fuels and concerns over nuclear power; | |

| · | increasing environmental awareness leading to regulations and taxes aimed at limiting emissions from fossil fuels; | |

| · | continued adoption or maintenance of government incentives for solar energy at all level of Chinese government; | |

| · | narrowing cost differentials between solar energy and conventional energy sources due to market-wide decreases in the average selling prices for PV products driven by lower raw materials costs and increased production efficiencies; and | |

| · | continued improvements in the conversion efficiency of PV products leading to lower costs per watt of electricity generated, making solar energy more efficient and cost-effective. |

| 3 |

PV Government Regulation

This section sets forth a summary of the most significant regulations or requirements that affect our business activities in China.

Regulations issued or implemented by the State Council, China's National Development and Reform Commission ("NDRC"), and other relevant government authorities cover many aspects of new energy industry, including, but not limited to the following principal regulations:

Renewable Energy Law

On December 26, 2009, China revised its Renewable Energy Law, which originally became effective on January 1, 2006. The revised Renewable Energy Law became effective on April 1, 2010 and has laid the legal foundation for developing renewable energy in China. These laws lay the foundation for future regulation.

Renewable Energy Law clearly stipulates the following principles for the development of new energy:

| · | To encourage and support the use of solar and other renewable energy and the use of on-grid generation. | |

| · | To encourage the installation and use of solar energy water-heating systems, solar energy heating and cooling systems, solar PV systems and other solar energy utilization systems. | |

| · | To authorize the relevant pricing authorities to set favorable prices for the purchase of electricity generated by solar and other renewable power generation systems. | |

| · | To provide financial incentives, such as national funding, preferential loans and tax preferences for the development of renewable energy projects. |

Historical Government Directives

In January 2006, the NDRC promulgated two implementation directives of the Renewable Energy Law. These directives set forth specific measures in setting prices for electricity generated by solar and other renewal power generation systems and in sharing additional expenses occurred. The directives further allocate the administrative and supervisory authorities among different government agencies at the national and provincial levels and stipulate responsibilities of electricity grid companies and power generation companies with respect to the implementation of the Renewable Energy Law.

China's Ministry of Construction issued a directive in June of 2005, which seeks to expand the use of solar energy in residential and commercial buildings and encourages the increased application of solar energy in townships. In addition, China's State Council promulgated a directive in June of 2005, which sets forth specific measures to conserve energy resources and encourage exploration, development and use of solar energy in China's western areas, which are not fully connected to electricity transmission grids, and other rural areas.

In July 2007, the PRC State Electricity Regulatory Commission issued the Supervision Regulations on the Purchase of All Renewable Energy by Power Grid Enterprises which became effective on September 1, 2007. To promote the use of renewable energy for power generation, the regulations require that electricity grid enterprises must in a timely manner set up connections between the grids and renewable power generation systems and purchase all the electricity generated by renewable power generation systems. The regulations also provide that power dispatch institutions shall give priority to renewable power generation companies in respect of power dispatch services provision.

On September 4, 2006, China's Ministry of Finance and Ministry of Construction jointly promulgated the Interim Measures for Administration of Special Funds for Application of Renewable Energy in Building Construction, which provides that the Ministry of Finance will arrange special funds to support the application of renewable energy in building construction in order to enhance building energy efficiency, protect the ecological environment and reduce the consumption of fossil energy. These special funds provide significant support for the application of solar energy in hot water supply, refrigeration and heating, PV technology and lighting integrated into building construction materials.

| 4 |

On October 28, 2007, the Standing Committee of the National People's Congress adopted amendments to the PRC Energy-saving Law, which sets forth policies to encourage the conservation of energy in manufacturing, civic buildings, transportation, government agents and utilities sectors. The amendments also seek to expand the use of the solar energy in construction areas.

In March 2009, China's Ministry of Finance promulgated the Interim Measures for Administration of Government Subsidy Funds for Application of Solar Photovoltaic Technology in Building Construction, or the Interim Measures, to support the demonstration and the promotion of solar PV applications in China. Local governments are encouraged to issue and implement supporting policies for the development of solar PV technology. These Interim Measures set forth subsidy funds set at RMB 20 per watt for 2009 to cover solar PV systems integrated into building construction that have a minimum capacity of 50 kilowatt peak.

In April 2009, the Ministry of Finance and the Ministry of Housing and Urban-Rural Development jointly issued the "Guidelines for Declaration of Demonstration Project of Solar Photovoltaic Building Applications." These guidelines created a subsidy of up to RMB 20 per watt for building integrated PV or BIPV projects using solar-integrated building materials and components and up to RMB 15 per watt for BIPV projects using solar-integrated materials for rooftops or walls.

In July 2010, the Ministry of Housing and Urban-Rural Development issued the "City Illumination Administration Provisions" or the Illumination Provision. The Illumination Provisions encourage the installation and use of renewable energy system such as PV systems in the process of construction and re-construction of city illumination projects.

On March 8, 2011, the Ministry of Finance and the Ministry of Housing and Urban-Rural Development jointly promulgated the Notice on Further Application of Renewable Energy in Building Construction, which aims to raise the percentage of renewable energy used in buildings.

On March 27, 2011, the NDRC promulgated the revised Guideline Catalogue for Industrial Restructuring which categorizes the solar power industry as an encouraged item.

On March 14, 2012, the Ministry of Finance, the NDRC and the National Energy Bureau jointly issued the interim measures for the management of additional subsidies for renewable-energy power prices, according to which relevant renewable-energy power generation enterprises are entitled to apply for subsidies for their renewable power generation projects that satisfy relevant requirements set forth in the measures.

On March 1, 2013, China's State Council issued the "Twelfth Five Year Plan." The plan supports the promotion and development of renewable energy, including the solar energy. The plan also encourages the development of solar PV power stations in the areas with abundant solar power resource.

On November 18, 2013, the National Energy Bureau issued "The Interim Measures for the management of distributed photovoltaic power generation projects". The regulation contributes to promote the application of distributed photovoltaic power and regulate the projects management.

On November 26, 2013, the Ministry of Finance announced that the power generated by its own distributed PV power generation project could be exempted from imposing government fee, such as renewable energy surcharges, fee for major national water conservancy construction, etc.

In January, 2014, the National Energy Administration of China announced the PV installation target for 2014 to be 14GW, which includes 8GW for distributed PV systems and 6GW for large scale PV power plants.

In the same month, the National Energy Administration of China released a list of 81 "New Energy Demonstration Cities" and eight "industrial demonstration parks" in 28 and 8 provinces respectively. These cities and zones are required to achieve their respective mandatory targets in terms of solar PV installations and the percentage of installed renewable energy power generation capacities by the end of 2015, or the end of the 12th Five-Year-Plan.

In February 2014, the Certification and Accreditation Administration and the National Energy Administration jointly issued the "Implementation Opinions on Strengthening the Testing and Certification of PV Products." The implementation opinions provide that only certified PV products may be connected to the public grid or receive government subsidies. The institutions that certify PV products must be approved by the Certification and Accreditation Administration. According to the implementation opinions, PV products that are subject to certification include PV battery parts, inverters, control devices, confluence devices, energy storage devices and independent PV systems.

| 5 |

In December, 2014, the National Energy Administration of China released a list of 30 "distributed solar photovoltaic industrial application demonstration zone" to encourage the development of distributed solar PV industry.

On January 28, 2015, the NEA of China announced the target for national solar installations in 2015 to be 15GW, 8GW of which would be targeted for utility scale, 7GW for distributed generation.

On December 24, 2015, the National Development and Reform Commission promulgated the Notice on the improvement of photovoltaic electricity price, which announced a new standard on-grid price implemented from January 1, 2016 for solar PV electricity.

On December 15, 2015, the National Energy Bureau announced the annual plan for the development of solar PV. The solar power installed capacity will reach 160GW, and total annual investment will reach 200 billion RMB for 2016, in the light of the plan.

Effect of Existing Securities and Exchange Commission Regulations on the Business

We were subject to the Exchange Act and the Sarbanes-Oxley Act of 2002. Under the Exchange Act, we are required to file with the SEC annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. The Sarbanes-Oxley Act creates a strong and independent accounting oversight board to oversee the conduct of auditors of public companies and to strengthen auditor independence. It also (1) requires steps be taken to enhance the direct responsibility of senior members of management for financial reporting and for the quality of financial disclosures made by public companies; (2) establishes clear statutory rules to limit, and to expose to public view, possible conflicts of interest affecting securities analysts; (3) creates guidelines for audit committee members’ appointment, and compensation and oversight of the work of public companies’ auditors; (4) prohibits certain insider trading during pension fund blackout periods; and (5) establishes a federal crime of securities fraud, among other provisions.

We are also subject to Section 14(a) of the Exchange Act, which requires all companies with securities registered pursuant to Section 12(g) of the Exchange Act to comply with the rules and regulations of the SEC regarding proxy solicitations, as outlined in Regulation 14A. Matters submitted to our stockholders at a special or annual meeting thereof or pursuant to a written consent requires us to provide our stockholders with the information outlined in Schedules 14A or 14C of Regulation 14A. Preliminary copies of this information must be submitted to the SEC at least 10 days prior to the date that definitive copies of this information are provided to our stockholders.

Employees

The Company currently has two executive officers Dr. Chongyi Yang serves as Chief Executive Officer, Treasurer, and Secretary. Chunsheng Qin services as President.

Management of the Company expects to use consultants, attorneys and accountants as necessary, and it is not expected that the Company will have any full-time or other employees, except as may be the result of completing a transaction.

Intellectual Property

As of the date of this report, we do not own any patents, trademarks, licenses, franchises, concessions, and royalty agreements, or other intellectual property contracts.

Available Information

Our Periodic Reports including Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports, and amendments to those reports, and other forms that we file with or furnish to the Securities and Exchange Commission (SEC) are available to review on the SEC’s EDGAR website.

Corporate Governance

In accordance with and pursuant to relevant related rules and regulations of the SEC, the Board of Directors of the Company has established and periodically update our corporate governance guide, which is applicable to all directors, officers and employees of the Company. We have not yet established an audit committee of our board of directors.

| 6 |

| Item 1A. | Risk Factors |

Not applicable to a smaller reporting company.

| Item 1B. | Unresolved Staff Comments |

None

| Item 2. | Properties |

We do not own any property but rent office space.

| Item 3. | Legal Proceedings |

There are not any material pending legal proceedings to which the Registrant is a party or as to which any of its property is subject, and no such proceedings are known to the Registrant to be threatened or contemplated against it.

| Item 4. | Mine Safety Disclosures |

N/A

| 7 |

PART II

| Item 5. | Market Price and Dividends on the Registrant’s Common Equity and Related Stockholder Matters |

(a) Market information.

Our Common Stock is not trading on any stock exchange. It is listed, but not quoted, OTC Markets under the symbol CHJI and there is no established public trading market for the class of common equity.

| Fiscal Year 2022 | HIGH | LOW | ||||||

| First Quarter (Jan.1, 2022 – March 31, 2022) | $ | .02 | $ | .019 | ||||

| Second Quarter (April 1, 2022– June 30, 2022) | .058 | .011 | ||||||

| Third Quarter (July 1, 2022 – Sept. 30, 2022) | .058 | .016 | ||||||

| Fourth Quarter (Oct. 1, 2022 – Dec. 31, 2022) | .125 | .016 | ||||||

| Fiscal Year 2021 | ||||||||

| First Quarter (Jan.1, 2021 – March 31, 2021) | $ | .09 | $ | .07 | ||||

| Second Quarter (April 1, 2021– June 30, 2021) | .09 | .02 | ||||||

| Third Quarter (July 1, 2021 – Sept. 30, 2021) | .05 | .013 | ||||||

| Fourth Quarter (Oct. 1, 2021 – Dec. 31, 2021) | .06 | .02 | ||||||

Holders

(b) Holders.

As of April 15, 2022, there are approximately 3,581 holders of an aggregate of 64,629,559 shares of our Common Stock issued and outstanding.

(c) Dividends.

We have not declared any cash dividends on our Common Stock since our inception and do not anticipate paying such dividends in the foreseeable future. We plan to retain any future earnings for use in our business. Any decisions as to future payments of dividends will depend on our earnings and financial position and such other facts, as the Board of Directors deems relevant.

(d) Securities authorized for issuance under equity compensation plans.

We have not adopted an equity compensation plan and no securities have been authorized or reserved for issuance under any equity compensation plan.

Description of Securities

The following description is a summary of the material terms of the provisions of our Articles of Incorporation and Bylaws. The Articles of Incorporation and Bylaws have been filed with the SEC as exhibits to our registration statement on Form 10.

Common Stock

We are authorized to issue 500,000,000 shares of Common Stock with $0.01 par value per share. As of our fiscal year ended December 31, 2022, there were 64,629,559 shares of Common Stock issued and outstanding.

Each share of Common Stock entitles the holder to one vote, either in person or by proxy, at meetings of stockholders. Accordingly, the holders of our Common Stock who hold, in the aggregate, more than fifty percent of the total voting rights can elect all of our directors and, in such event, the holders of the remaining minority shares will not be able to elect any of such directors. The vote of the holders of a majority of the issued and outstanding shares of Common Stock entitled to vote thereon is sufficient to authorize, affirm, ratify or consent to such act or action, except as otherwise provided by law.

| 8 |

Holders of Common Stock are entitled to receive ratably such dividends, if any, as may be declared by the Board of Directors out of funds legally available. We have not paid any dividends since our inception, and we presently anticipate that all earnings, if any, will be retained for development of our business. Any future disposition of dividends will be at the discretion of our Board of Directors and will depend upon, among other things, our future earnings, operating and financial condition, capital requirements, and other factors.

Holders of our Common Stock have no preemptive rights or other subscription rights, conversion rights, redemption or sinking fund provisions. Upon our liquidation, dissolution or windup, the holders of our Common Stock will be entitled to share ratably in the net assets legally available for distribution to stockholders after the payment of all of our debts and other liabilities. There are not any provisions in our Articles of Incorporation or our Bylaws that would prevent or delay change in our control.

Our stock transfer agent is Securities Transfer Corporation., located at 2901 N. Dallas Parkway, Suite 380, Plano, TX 75093.

Preferred Stock

Our Articles of Incorporation, as amended, authorizes the issuances of up to 10,000,000 shares of Preferred Stock with the following designations, rights and preferences:

One (1) share of the as Convertible Series C Preferred Stock shall be converted into one thousand (1,000) shares of common stock of the Corporation and entitled to one thousand (1,000) votes of common stock for every one (1) share of as Convertible Series A Preferred Stock owned. The holders of the Convertible Series C Preferred Stock shall not be entitled to receive dividends.

From time to time its Board of Directors may amend the Preferred class of stock. Accordingly, our Board of Directors is empowered, without stockholder approval, to issue Preferred Stock with dividend, liquidation, conversion, voting, or other rights, which could adversely affect the voting power or, other rights of the holders of the Common Stock. In the event of issuance, the Preferred Stock could be utilized, under certain circumstances, as a method of discouraging, delaying or preventing a change in control of the Company.

At this time there are 10,000,000 shares of Preferred Stock authorized as Convertible Series C Preferred Stock and 1,000,000 are issued and outstanding.

Emerging Growth Company

We are an emerging growth company under the JOBS Act. We shall continue to be deemed an emerging growth company until the earliest of:

| 1. | the last day of our first fiscal five years after filing the Form 10 |

| 2. | the last day of our fiscal year during which we had annual gross revenues are $1 billion or more; |

| 3. | the date on which we have, during the previous 3-year period, issued more than $1 billion in non-convertible debt securities; or |

| 4. | the date on which we are deemed to be a “large accelerated filer”, as defined in section 240.12b-2 of title 46, Code of Federal Regulations, or any successor thereto. |

As an emerging growth company, we are exempt from Section 404(a) and (b) of Sarbanes Oxley. Section 404(a) requires issuers to publish information in their annual reports concerning the scope and adequacy of the internal control structure and procedures for financial reporting. This statement shall also assess the effectiveness of such internal controls and procedures. Section 404(b) requires that the registered accounting firm shall, in the same report, attest to and report on the assessment and the effectiveness of the internal control structure and procedures for financial reporting.

As an emerging growth company, we are also exempt from Section 14A(a) and (b) of the Exchange Act, which require the stockholder approval of executive compensation and golden parachutes. These exemptions are also available to us as a Smaller Reporting Company.

| 9 |

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of the Jobs Act, that allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

| Item 6. | [Reserved] |

N/A

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

INTRODUCTION

This section provides management’s discussion of the financial condition, changes in financial condition and results of operations of China Changjiang Mining & New Energy Company, Ltd. with specific information on results of operations and liquidity and capital resources. It includes management’s interpretation of our financial results, the factors affecting these results, the major factors expected to affect future operating results and future investment and financing plans. This discussion should be read in conjunction with our consolidated financial statements and notes thereto.

Cautionary Statement for the Purposes of the Safe Harbor under the Private Securities Litigation Reform Act of 1995

The statements contained in this Annual Report on Form 10-K may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact included in this Report are forward-looking statements made in good faith by us and are intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. When used in this Report, or any other of our documents or oral presentations, the words “anticipate”, “believe”, “estimate”, “expect”, “forecast”, “goal”, “intend”, “objective”, “plan”, “projection”, “seek”, “strategy” or similar words are intended to identify forward-looking statements. Such forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the statements relating to our strategy, operations, markets, services, and other factors all of which are difficult to predict and many of which are beyond our control. Accordingly, while we believe these forward-looking statements to be reasonable, there can be no assurance that they will approximate actual experience or that the expectations derived from them will be realized. Further, we undertake no obligation to update or revise any of our forward-looking statements whether as a result of new information, future events or otherwise.

Results of Operations for China Changjiang Mining & New Energy Company, Ltd.. —Comparison of the Years ended December 31, 2022 and 2021

Revenue

We had no revenues from operations during either 2022 or 2021.

Selling and General & Administrative Expense

General and Administrative Expenses were $0 for the year ended December 31, 2022 compared to $0 for the year ended December 31, 2021, an decrease of $0.

Other Income(expense)

During the year ended December 31, 2022 and 2021, we gained $371,024 from foreign exchange compared to loss of 119,757 for the year ended December 31, 2021, an increase of 490,781.

| 10 |

Net Profit/Loss

We had a net profit of $371,024 for the year ended December 31, 2022, compared to a net loss $119,757 for the year ended December 31, 2021.

Liquidity and Capital Resources

As of December 31, 2022, we had $0 of cash, 3,728,658 in liabilities, and an accumulated deficit of $19,918,801. We used zero of cash in operations for the year ended December 31, 2022 and received net proceeds from financing of $0.

The financial statements accompanying this Report have been prepared on a going concern basis, which contemplates the realization of assets and settlement of liabilities and commitments in the normal course of our business. As reflected in the accompanying financial statements, we have not yet generated any revenue, had a net profit of $371,024 and have an accumulated stockholders’ deficit of $19,918,801 as of December 31, 2022. These factors raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent on our ability to raise additional funds and implement our business plan. The financial statements do not include any adjustments that might be necessary if we are unable to continue as a going concern.

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. |

As of December 31, 2022, we were not subject to any market or interest rate risk.

| Item 8. | Financial Statements and Supplementary Data. |

This information appears following Item 15 of this Report and is included herein by reference.

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. |

N/A

| Item 9A. |

Controls and Procedures |

Management’s Evaluation of Disclosure Controls and Procedures

Our disclosure controls and procedures are designed to provide reasonable assurance that the information required to be disclosed by us in reports that we file or submit under the Exchange Act is accumulated and communicated to our management, including our principal executive officer and principal financial officer, as appropriate to allow timely decisions regarding required disclosure and is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the SEC. Based upon that evaluation, our principal executive officer and principal financial officer concluded that, as of the end of the period covered by this report, our disclosure controls and procedures were effective at the reasonable assurance level.

Management’s Report on Internal Control over Financial Reporting

Our management, with the participation of our principal executive officer and principal financial officer, is responsible for establishing and maintaining adequate internal control over our financial reporting. Our internal control system was designed to provide reasonable assurance to management regarding the preparation and fair presentation of published financial statements.

| 11 |

Our management, consisting of our principal executive officer and principal financial officer, does not expect that our disclosure controls and procedures or our internal controls over financial reporting will prevent all error and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues, misstatements, errors, and instances of fraud, if any, within our company have been or will be prevented or detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns can occur because of simple error or mistake. The design of any system of controls is based in part on certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Projections of any evaluation of controls effectiveness to future periods are subject to risks that internal controls may become inadequate as a result of changes in conditions, or through the deterioration of the degree of compliance with policies or procedures.

Changes in Internal Control over Financial Reporting

There was no change in the Company’s internal control over financial reporting that occurred during the year ended December 31, 2022 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

Management's Assessment Regarding Internal Control Over Financial Reporting

At the end of the period covered by this Annual Report on Form 10-K, an evaluation was carried out under the supervision of and with the participation of our management, including the Principal Executive Officer and the Principal Financial Officer of the effectiveness of the design and operations of our disclosure controls and procedures (as defined in Rule 13a – 15(e) and Rule 15d – 15(e) under the Exchange Act) as of the end of the period covered by this report. Based on that evaluation, the Principal Executive Officer and the Principal Financial Officer have concluded that our disclosure controls and procedures were not effective in ensuring that: (i) information required to be disclosed by the Company in reports that it files or submits to the Securities and Exchange Commission under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in applicable rules and forms and (ii) material information required to be disclosed in our reports filed under the Exchange Act is accumulated and communicated to our management, including our CEO and CFO, as appropriate, to allow for accurate and timely decisions regarding required disclosure.

Disclosure controls and procedures were not effective due primarily to a material weakness in the segregation of duties in the Company’s internal control of financial reporting as discussed below.

Internal Control over Financial Reporting

Management is responsible for establishing and maintaining adequate internal control over financial reporting for the Company (including its consolidated subsidiaries) and all related information appearing in our Annual Report on Form 10-K. Our internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with accounting principles generally accepted in the United States of America

Management conducted an evaluation of the design and operation of our internal control over financial reporting as of the end of the period covered by this report, based on the criteria in a framework developed by the Company’s management pursuant to and in compliance with the criteria established. This evaluation included review of the documentation of controls, evaluation of the design effectiveness of controls, walkthroughs of the operating effectiveness of controls and a conclusion on this evaluation. Based on this evaluation, management has concluded that our internal control over financial reporting was not effective, because management identified a material weakness in the Company’s internal control over financial reporting related to the segregation of duties as described below.

While the Company does adhere to internal controls and processes that were designed, it is difficult with a very limited staff to maintain appropriate segregation of duties in the initiating and recording of transactions, thereby creating a segregation of duties weakness. Due to: (i) the significance of segregation of duties to the preparation of reliable financial statements; (ii) the significance of potential misstatement that could have resulted due to the deficient controls; and (iii) the absence of sufficient other mitigating controls, we determined that this control deficiency resulted in more than a remote likelihood that a material misstatement or lack of disclosure within the annual or interim financial statements may not be prevented or detected.

| 12 |

Management’s Remediation Initiatives

Management has evaluated, and continues to evaluate, avenues for mitigating our internal controls weaknesses, but mitigating controls to completely mitigate internal control weaknesses have been deemed to be impractical and prohibitively costly, due to the size of our organization at the current time. Management expects to continue to use reasonable care in following and seeking improvements to effective internal control processes that have been and continue to be in use at the Company.

Changes in internal controls over financial reporting

There were no changes in the Company’s internal control over financial reporting that occurred prior to the Company’s most recent financial quarter that materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

| Item 9B. | Other Information. |

N/A

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections.

N/A

| 13 |

PART III

| Item 10. | Directors, Executive Officers and Corporate Governance |

Our Officers and directors and additional information concerning them are as follows:

| Name | Age | Position | ||||

| Dr. Chongyi Yang | 61 | CEO, Secretary, Treasurer, Director | ||||

Officer Bios

Dr. Yang Chong Yi, Chief Executive Officer

Dr. Yang Chong Yi is experienced in both governmental and private sectors, specializing in investment banking, and merger and acquisitions. Dr. Yang has held the following positions:

| · | Deputy Chief in the Bureau of Commodity Price in Shanghai Development and Reform Center | |

| · | Associate Director in Hongkong First Eastern Investment Group | |

| · | General Manager in Shanghai First Food Investment Management Company | |

| · | Managing Director of a state-owned private equity fund |

Dr. Yang also has experience consulting businesses in preparation for IPOs on listings on NASDAQ in addition to consulting commercial complex projects in the cities of New York and Los Angeles.

Dr. Yang Chong Yi is the author of “Winning at Quitting” and “The Economics of Popularity” and Visiting Professor at Shanghai Lixin Institute of Finance and Accounting, a Distinguished Research Institution at the Economic Development Research Center of the Shanghai Municipal Government. Lastly, Dr. Yang is Executive Secretary of the Financial and Economic Committee (Shanghai) of the US-China International Chamber of Commerce.

| Item 11. | Executive Compensation |

For each of the fiscal years ended December 31, 2022, and 2021 there was no direct compensation awarded to, earned by, or paid by us to any of our executive officers.

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

(a) Security ownership of certain beneficial owners.

The following table sets forth, as of December 31, 2022, the number of shares of common stock owned of record and beneficially by our executive officer, director and persons who beneficially own more than 5% of the outstanding shares of our common stock

| Name and Address of Beneficial Owner |

Amount and Nature of Beneficial Ownership |

Percentage of Class |

|||

| Cathay Capital Management Inc./Dr. Congyi Yang is the control person | 1,000,000 Preferred C Shares | 100% | |||

| 19F, No.38 West Nanjing Road | |||||

| Jing’An District, Shanghai | |||||

| China 200041 |

| 14 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

N/A

| Item 14. | Principal Accounting Fees and Services |

BFBorgers CPA PC (“BFB”) served as the Company’s independent auditor for the years ended December 31, 2022 and 2021.

The following table presents fees billed for professional audit services rendered by BFB in connection with its audits of the Company’s annual financial statements for the years ended December 31, 2022 and 2021. The fees billed to the CHJI by BFB during 2022 and 2021 were the following:

| December 31, | December 31, | |||||||

| 2022 | 2021 | |||||||

| ASSETS | ||||||||

| Audit Fees | $ | 16,500 | $ | 12,000 | ||||

| Audit Related Fees (auditor admin. Fees) | – | – | ||||||

| Tax Fees | – | – | ||||||

| All Other Fees | – | – | ||||||

| Total Fees | $ | 16,500 | $ | 12,000 | ||||

As used in the table above, the following terms have the meanings set forth below.

Audit Fees

The fees for professional services rendered in connection with the audit of the Company’s annual financial statements, for the review of the financial statements included in our Quarterly Reports on Form 10 and for services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements.

Audit-Related Fees

The fees for assurance and related services that are reasonably related to the performance of the audit or review of our financial statements.

Tax Fees

The fees for professional services rendered for tax compliance, tax advice and tax planning.

All Other Fees

The fees for products and services provided, other than for the services reported under the headings “Audit Fees,” “Audit Related Fees” and “Tax Fees.” The Company has adopted a policy regarding the services of its independent auditors under which our independent accounting firm is not allowed to perform any service which may have the effect of jeopardizing the registered public accountant’s independence. Without limiting the foregoing, the independent accounting firm shall not be retained to perform the following:

| · | Bookkeeping or other services related to the accounting records or financial statements |

| · | Financial information systems design and implementation |

| · | Appraisal or valuation services, fairness opinions or contribution-in-kind reports |

| · | Actuarial services |

| · | Internal audit outsourcing services |

| · | Management functions |

| · | Broker-dealer, investment adviser or investment banking services |

| · | Legal services |

| · | Expert services unrelated to the audit |

| 15 |

PART IV

| Item 15. | Exhibits, Financial Statement Schedules. |

| No. | Description | |

| 31.1 | Rule 13a-14(a)/15d-14(a) Certification of Chief Executive Officer | |

| 31.2 | Rule 13a-14(a)/15d-14(a) Certification of Chief Financial Officer | |

| 32.1 | Section 1350 Certification of Chief Executive Officer | |

| 32.2 | Section 1350 Certification of Chief Financial Officer | |

| 101 | The following financial statements from the Company’s Quarterly Report on Form 10-K for the year ended December 31, 2021, formatted in inline XBRL, include: (i) Condensed Consolidated Balance Sheets, (ii) Condensed Consolidated Statements of Operations, (iii) Condensed Consolidated Statements of Stockholders’ Equity, (iv) Condensed Consolidated Statements of Cash Flows and (v) the Notes to the Condensed Consolidated Financial Statements. |

| 16 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

CONSOLIDATED FINANCIAL STATEMENTS

(Audited)

| 17 |

Report of Independent Registered Public Accounting Firm

To the shareholders and the board of directors of China Changjiang Mining & New Energy Company, Ltd.

Opinion on the Financial Statements

We have audited the accompanying balance sheets of China Changjiang Mining & New Energy Company, Ltd. as of December 31, 2022 and 2021, the related statements of operations, stockholders' equity (deficit), and cash flows for the years then ended, and the related notes (collectively referred to as the "financial statements"). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2022 and 2021, and the results of its operations and its cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States.

Substantial Doubt about the Company’s Ability to Continue as a Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 3 to the financial statements, the Company has suffered recurring losses from operations and has a significant accumulated deficit. In addition, the Company continues to experience negative cash flows from operations. These factors raise substantial doubt about the Company's ability to continue as a going concern. Management's plans in regard to these matters are also described in Note 3. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on the Company's financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) ("PCAOB") and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

Critical Audit Matter

Critical audit matters are matters arising from the current-period audit of the financial statements that were communicated or required to be communicated to the audit committee and that (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments.

We determined that there are no critical audit matters.

/S/

We have served as the Company's auditor since 2021

April 13, 2023

| 18 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

BALANCE SHEETS

| As at | ||||||||

| Dec. 31, 2022 | Dec. 31, 2021 | |||||||

| Assets | ||||||||

| Cash and equivalents | $ | $ | ||||||

| Total current assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

| Other payable and accrued liabilities | $ | $ | ||||||

| Total current liabilities | ||||||||

| Due to related parties | ||||||||

| Due to Shareholders | ||||||||

| Total non-current liabilities | ||||||||

| TOTAL LIABILITIES | ||||||||

| STOCKHOLDERS' DEFICIT | ||||||||

| Series C convertible preferred stock ($ par value, shares authorized, shares outstanding as of December 31, 2022 and 2021) | ||||||||

| Common stock ($ par value, shares authorized, shares issued and outstanding as of December 31, 2022 and 2021) | ||||||||

| Treasury stock | ( | ) | ( | ) | ||||

| Additional paid-in capital | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| TOTAL STOCKHOLDERS' DEFICIT | ( | ) | ( | ) | ||||

| TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited financial statements

| 19 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

STATEMENTS OF OPERATIONS

| For the years ended | ||||||||

| Dec. 31, 2022 | Dec. 31, 2021 | |||||||

| OTHER INCOME/(EXPENSE) | ||||||||

| Compensation expenses | $ | $ | ||||||

| Foreign exchange gains/ (losses), net | ( | ) | ||||||

| Other income | ||||||||

| Total other income/(expense) | ( | ) | ||||||

| Net profit/ (loss) | $ | $ | ( | ) | ||||

| Net loss per share - basic and diluted | $ | ) | $ | ) | ||||

| Weighted average number of common shares outstanding | ||||||||

The accompanying notes are an integral part of these unaudited financial statements

| 20 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

STATEMENTS OF CHANGES IN STOCKHOLDERS’ DEFICIT

| Series C convertible preferred stock | Common Stock | Treasury | Additional Paid in | Accumulated | ||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Stock | Capital | Deficit | Total | |||||||||||||||||||||||||

| Balance, January 1, 2021 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||

| Net loss for the year ended December 31, 2021 | – | – | ( | ) | ( | ) | ||||||||||||||||||||||||||

| Balance, December 31, 2021 | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||||||||

| Net loss for the year ended December 31, 2022 | – | – | ||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||

The accompanying notes are an integral part of these unaudited financial statements

| 21 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

STATEMENTS OF CASH FLOWS

| For the years ended | ||||||||

| Dec. 31, 2022 | Dec. 31, 2021 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

| Net loss | $ | $ | ( | ) | ||||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Compensation expenses for Preferred C Shares | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts payable and accrued expenses | ( | ) | ||||||

| Due to related parties | ( | ) | ||||||

| Due to shareholders | ( | ) | ||||||

| Cash used in operating activities | ||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

| Investment received from Preferred C shares issued | ||||||||

| Cash generated from financing activities | ||||||||

| Net change in cash and equivalents | ||||||||

| Cash and equivalents, beginning of period | ||||||||

| Cash and equivalents, end of period | $ | $ | ||||||

| Cash paid for interest | $ | $ | ||||||

| Cash paid for income taxes | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited financial statements

| 22 |

CHINA CHANGJIANG MINING & NEW ENERGY COMPANY, LTD.

Notes to Financial Statements

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS

China Changjiang Mining & New Energy Company, Ltd. (“China Changjiang”, “we”, the “Company”) was incorporated under the laws of the State of Delaware in 1969.

Hong Kong Wah Bon Enterprise Limited (“Wah Bon”) was incorporated in Hong Kong on July 7, 2006 as an investment holding company.

Shaanxi Pacific New Energy Development Company Limited (“Shaanxi Pacific”) was incorporated as a limited liability company in the People's Republic of China ("PRC") on July 20, 2007 as an investment holding company.

Shaanxi Changjiang Mining & New Energy Company, Ltd (“Shaanxi Changjiang”) (formerly Weinan Industrial and Commercial Company Limited) was incorporated as a limited liability company in the PRC on March 19, 1999. The Company became a joint stock company in January 2006 with its business activities in investment holding and the development of a theme park in Xi'An, PRC.

In August 2005, Shaanxi Changjiang contributed land use rights valued at $7,928,532 in lieu of cash to the registered capital of Huanghe representing 92.93% of the equity of Huanghe. Huanghe was incorporated as a limited liability company in the PRC on August 9, 2005 as Shaanxi Changjiang Petroleum and Energy Development Co., Limited and is engaged in the development of a theme park in Huanghe Bay (Huanghe Nantan), Heyang County, Shaanxi Province, PRC.

On February 5, 2007, Shaanxi Changjiang entered into an agreement with a third party to acquire 40% of the equity interest in East Mining Company Limited ("East Mining") for $3,117,267 in cash. East Mining is engaged in exploration for lead, zinc and gold for mining in Xunyan County, Shaanxi Province, PRC.

On March 22, 2007, Shaanxi Changjiang entered into an agreement with the majority shareholder of Shaanxi Changjiang to exchange its 92.93% interest in Huanghe for a 20% equity interest in East Mining owned by this related party.

On August 15, 2007, 97.2% of the shareholders of Shaanxi Changjiang entered into a definitive agreement with Shaanxi Pacific and the stockholders of Shaanxi Pacific in which they disposed their ownership in Shaanxi Changjiang to Shaanxi Pacific for 98% of ownership in Shaanxi Pacific and cash of $1,328,940 payable on or before December 31, 2007.

On September 2, 2007, Wah Bon acquired 100% ownership of Shaanxi Pacific for a cash consideration of $128,205.

On May 30, 2007, amended to July 5, 2007, North American Gaming and Entertainment Corporation ("North American") entered into a Material Definitive Agreement, pursuant to which the shareholders of Shaanxi Changjiang exchanged all their shares in Shaanxi Changjiang for 500,000 shares of series C convertible preferred stock ("series C shares") in North American which carried the right of 1,218 votes per share and was convertible to 609,000,000 common shares. In connection with the exchange, Shaanxi Changjiang also delivered $370,000 to North American and certain non-affiliates of North American will transfer to North American or its designee a total of 3,800,000 shares of common stock, par value of $0.01 per share, of North American which had been held for longer than 2 years by such non-affiliates, in exchange for the issuance by North American to each of such non-affiliates of 2,250,000 shares of common stock of North American. Issued and outstanding share of series C preferred stock were automatically converted into that number of fully paid and non-assessable shares of common stock based upon the conversion rate upon the filing by the Company of an amendment to its Certificate of Incorporation, increasing the number of authorized shares of common stock to 800,000,000 shares, changing the Company's name to China Changjiang Mining & New Energy Company Ltd. and implementing a one for ten reverse stock split. The transaction was closed on February 4, 2008 and Wah Bon became a wholly owned subsidiary of North American.

There was a 10 to 1 reverse stock split for the Company's common stock during December 2009 and all the shares information are retroactively restated to reflect the reverse stock split. The preferred stock holders will not convert their C convertible preferred stock until after the completion of the reverse stock split.

| 23 |

On February 9, 2010, we filed a Certificate of Amendment to our Articles of Incorporation to effect a 1-for-10 reverse stock split of our common stock. The 1-for-10 reverse split was approved by FINRA on July 30, 2010, effective August 2, 2010.

The Company was reincorporated from the state of Delaware to the state of Nevada with the intent to effect a statutory merger of the Delaware corporation “North American Gaming and Entertainment Corporation” into China Changjiang and to swap all issued and outstanding shares in the Delaware corporation for comparable shares in China Changjiang and dissolve the Delaware corporation.

The merger of North American and Wah Bon was treated for accounting purposes as a capital transaction and recapitalization by Wah Bon (the “accounting acquirer”) and re-organization by North American (the “accounting acquiree”). The consolidated financial statements have been prepared as if the reorganization had occurred retroactively.

On February 4, 2008, we acquired Wah Bon and its three subsidiaries: Shaanxi Pacific; Shaanxi Changjiang and East Mining. Wah Bon owns 100% of Shaanxi Pacific. Shaanxi Pacific owns 97.2% of Shaanxi Changjiang; and Shaanxi Changjiang owns 60% of East Mining. The minority interests represent the minority shareholders' 2.8% and 40% share of the results of Shaanxi Changjiang and East Mining respectively.

The Company established a subsidiary, named Shaanxi Weinan Changjiang Solar Photovoltaic Energy Applied Science and Technology Co., Ltd. ("Changjiang PV") in April 2012. The Company's subsidiary, Shaanxi Changjiang accounted for 51% shares of Changjiang PV, and Mr. Zhang Hong Jun, the director and principal shareholder of the Company, accounted for the other 49% shares.

On December 30, 2013, the Company transferred all of its 60% equity of East Mining to its director and principal shareholder, Mr. Zhang Hong Jun and one of its shareholders, Mr. Wang Sheng Li with a consideration of $885,696 (RMB 5,400,000). Each of the acquirers obtained 30% equity of East Mining in this transaction. There is no gain or loss recognized because this is a transaction between entities under common control.

Prior to January 1, 2019, the Company divested all of its subsidiaries, and de-registered Wah Bon in 2020.

The Company’s main business is in the transitional period from mining to clean new energy, and mainly focus on the solar photovoltaic, or “PV”, downstream market at present stage. The Company is not actively trading during the current reporting period.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The Company maintains its accounts and prepares its financial statements using the accrual method accounting. The consolidated financial statements and notes are representations of management. Accounting policies adopted by the Company conform to generally accepted accounting principles in the United States of America and have been consistently applied.

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Significant estimates include the estimated useful lives of property and equipment. Actual results could differ from those estimates.

Cash equivalents

The Company considers all highly liquid investments with a maturity of three months or less when purchased to be cash equivalents.

Fair value of financial instruments

The Company follows paragraph 825-10-50-10 of the FASB Accounting Standards Codification for disclosures about fair value of its financial instruments and paragraph 820-10-35-37 of the FASB Accounting Standards Codification (“Paragraph 820-10-35-37”) to measure the fair value of its financial instruments. Paragraph 820-10-35-37 establishes a framework for measuring fair value in accounting principles generally accepted in the United States of America (U.S. GAAP), and expands disclosures about fair value measurements. To increase consistency and comparability in fair value measurements and related disclosures, Paragraph 820-10-35-37 establishes a fair value hierarchy which prioritizes the inputs to valuation techniques used to measure fair value into three (3) broad levels. The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. The three (3) levels of fair value hierarchy defined by Paragraph 820-10-35-37 are described below:

| 24 |

Level 1: Quoted market prices available in active markets for identical assets or liabilities as of the reporting date.

Level 2: Pricing inputs other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date.

Level 3: Pricing inputs that are generally unobservable inputs and not corroborated by market data. The carrying amount of the Company’s financial assets and liabilities, such as prepaid expenses and accrued expenses approximate their fair value because of the short maturity of those instruments.

Foreign Currency Translation

The Company maintains its financial statements in its functional currency, which is US dollar ("USD"). Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency at rates of exchange prevailing at the balance sheet dates. Exchange gains or losses arising from foreign currency transactions or translation of monetary assets and liabilities denominated in foreign currencies are included in the statement of operations for the respective periods.

Exchange rates used in these

financial statements, USD to CNY, are

Related Party

A party is considered to be related to the Company if the party directly or indirectly or through one or more intermediaries, controls, is controlled by, or is under common control with the Company. Related parties also include principal owners of the Company, its management, member of the immediate families of principal owners of the Company and its management and other parties with which the Company may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting party might be prevented from fully pursuing its own separate interests. A party which can significantly influence the management or operating policies of the transacting parties or if it has an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests is also a related party.

Income taxes

The Company follow ASC 740-10-30, which requires recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred tax assets and liabilities are based on the differences between the financial statement and tax bases of assets and liabilities using enacted tax rates in effect for the fiscal year in which the differences are expected to reverse. Deferred tax assets are reduced by a valuation allowance to the extent management concludes it is more likely than not that the assets will not be realized. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the fiscal years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the Statements of Income in the period that includes the enactment date.

On December 22, 2017, the Tax Cuts and Jobs Act (TCJA) was signed into law by the President of the United States. TCJA is a tax reform act that among other things, reduced corporate tax rates to 21 percent effective January 1, 2018. FASB ASC 740, Income Taxes, requires deferred tax assets and liabilities to be adjusted for the effect of a change in tax laws or rates in the year of enactment, which is the year in which the change was signed into law. Accordingly, the Company adjusted its deferred tax assets and liabilities at December 31,2017, using the new corporate tax rate of 21 percent.

The Company adopted ASC 740-10-25 (“ASC 740-10-25”) with regard to uncertainty income taxes. ASC 740-10-25 addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements. Under ASC 740-10-25, we may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement. ASC 740-10-25 also provides guidance on de-recognition, classification, interest and penalties on income taxes, and accounting in interim periods and requires increased disclosures. We had no material adjustments to our liabilities for unrecognized income tax benefits according to the provisions of ASC 740-10-25.

| 25 |

Net income (loss) per common share is computed pursuant to section 260-10-45 of the FASB Accounting Standards Codification. Basic net income (loss) per common share is computed by dividing net income (loss) by the weighted average number of shares of common stock outstanding during the period. Diluted net income (loss) per common share is computed by dividing net income (loss) by the weighted average number of shares of common stock and potentially outstanding shares of common stock during the period. The weighted average number of common shares outstanding and potentially outstanding common shares assumes that the Company incorporated as of the beginning of the first period presented. For the years ended December 31, 2022 and 2021, there are outstanding common shares and potentially dilutive shares, respectively, from convertible preferred stock; however, these shares have not been considered in the weighted average share calculation as their inclusion would be anti-dilutive due to the net loss for the year ended.

Recently issued accounting pronouncements

The Company has implemented all new accounting pronouncements that are in effect. These pronouncements did not have any material impact on the financial statements unless otherwise disclosed, and the Company does not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on its financial position or results of operations.

NOTE 3 – GOING CONCERN

The Company’s unaudited

financial statements are prepared using accounting principles generally accepted in the United States of America applicable to a going

concern that contemplates the realization of assets and liquidation of liabilities in the normal course of business. The Company has not

established any source of revenue to cover its operating costs and has an accumulated deficit of $

In addition to operational expenses, as the Company executes its business plan, it is incurring expenses related to complying with its public reporting requirements. In order to finance these expenditures, the Company has raised capital in the form of debt, which will have to be repaid, as discussed in detail below. The Company has depended on loans from related parties and shareholders for most of its operating capital. The Company will need to raise capital in the next twelve months in order to remain in business.