SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For fiscal year ended December 31, 2015

Or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to_____________

Commission File Number: 000-52807

China Changjiang Mining & New Energy Co., Ltd. |

(Exact name of registrant as specified in its charter) |

Nevada | 75-2571032 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

Twenty-fourth Floor, Block B, Xinhui Mansion, Gaoxin Road Hi-Tech Zone, Xi'An P.R. China 71005 | +86(29) 8833-1685 | |

(Address of Principal Executive Offices; Zip Code) | (Registrant's Telephone Number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

None | None |

Securities registered pursuant to Section 12(g) of the Act:

Title of each class

Common Stock, par value $0.01 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). Yes o No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

(Check one): | |||

Large accelerated filer | o | Accelerated filer | o |

Non-accelerated filer | o | Smaller reporting company | x |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 30, 2015, there were 64,629,559 shares of the registrant's common stock issued and outstanding of these 9,693,685 shares were held by non-affiliates of the registrant. The aggregate market value of the common stock held by non-affiliates of the registrant on June 30, 2015, based on the average bid and ask price of such stock of $0.045 on June 30, 2015, was $436,216

At March 30, 2016, the registrant had outstanding 64,629,559 shares of common stock, $0.01 par value.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Special Notes Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements. We use words such as "believe," "expect," "anticipate," "project," "target," "plan," "optimistic," "intend," "aim," "will" or similar expressions, which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including those identified in Item 1A "Risk Factors" included herein, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to: "we," "us," "our," or the "Company" are to CHINA CHANGJIANG MINING & NEW ENERGY CO., LTD., and its consolidated subsidiaries;

"MT" are to metric tons;

"PRC" and "China" are to the People's Republic of China;

"SEC" are to the Securities and Exchange Commission;

"Securities Act" are to the Securities Act of 1933, as amended;

"Exchange Act" are to the Securities Exchange Act of 1934, as amended;

"Renminbi" and "RMB" are to the legal currency of China; and

"U.S. dollars," "dollars" and "$" are to the legal currency of the United States.

| 2 |

CHINA CHANGJIANG MINING AND NEW ENERGY COMPANY LTD.

For the Fiscal Year Ended December 31, 2015

TABLE OF CONTENTS

PART I |

|

| ||||

|

|

|

|

| ||

Item 1. |

| Business |

|

| 4 |

|

Item 1A. |

| Risk Factors |

|

| 12 |

|

Item 1B. |

| Unresolved Staff Comments |

|

| 18 |

|

Item 2. |

| Properties |

|

| 18 |

|

Item 3. |

| Legal Proceedings |

|

| 18 |

|

Item 4. |

| Mine Safety Disclosures |

|

| 18 |

|

|

|

|

|

|

| |

PART II |

|

| ||||

|

|

|

|

|

| |

Item 5. |

| Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

|

| 19 |

|

Item 6. |

| Selected Financial Data |

|

| 20 |

|

Item 7. |

| Management's Discussion and Analysis of Financial Condition and Results of Operations |

|

| 20 |

|

Item 7A. |

| Quantitative and Qualitative Disclosures About Market Risk |

|

| 25 |

|

Item 8. |

| Financial Statements and Supplementary Data |

|

| 25 |

|

Item 9. |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

| 25 |

|

Item 9A. |

| Controls and Procedures |

|

| 26 |

|

Item 9B. |

| Other Information |

|

| 27 |

|

|

|

|

|

|

| |

PART III |

|

| ||||

|

|

|

|

|

| |

Item 10. |

| Directors, Executive Officers and Corporate Governance |

|

| 28 |

|

Item 11. |

| Executive Compensation |

|

| 30 |

|

Item 12. |

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

| 31 |

|

Item 13. |

| Certain Relationships and Related Transactions, and Director Independence |

|

| 32 |

|

Item 14. |

| Principal Accounting Fees and Services |

|

| 35 |

|

|

|

|

|

|

| |

PART IV |

|

| ||||

|

|

|

|

|

| |

Item 15. |

| Exhibits, Financial Statement Schedules |

|

| 36 |

|

| 3 |

PART I

ITEM 1. BUSINESS.

Overview

China Changjiang Mining & New Energy Co., Ltd. (the "Company") is currently in the development stage with the goal of becoming a turnkey developer and Engineering, Procurement and Construction ("EPC") contractor of photovoltaic ("PV") solar energy facilities ("SEF").We intend to design, engineer, construct, market and sell high-quality PV SEFs for commercial and utility applications to local markets.

Before June 1, 2012, we were engaged in exploration for commercially recoverable metal-bearing mineral deposits. On June 1, 2012, we entered into an agreement with Xunyang Yongjin Mining Co., Ltd. to transfer our mining exploration rights for a cash payment of $2,380,612 (RMB 15,000,000). Further, on December 30, 2013, our subsidiary, Shaanxi Changjiang Mining & New Energy Co., Ltd ("Shaanxi Changjiang"), entered into Equity Transfer Agreements with each of Zhang Hong Jun, a director of the Company and owner of a controlling interest in the Company (holding 54.42% as of December 31, 2015), and Wang Sheng Li, a director and shareholder of the Company (holding 2.36% as of December 31, 2015), to sell Shaanxi Changjiang's entire 60% interest in Shaanxi East Mining Co., Ltd., ("East Mining" and formerly referred to as "Dongfang Mining") for a total consideration of $885,696 (RMB5,400,000). The consideration payable to the Company was used to offset amounts owed to each of the acquirers. Each of the acquirers obtained 30% equity in this transaction.

Together with Mr. Zhang Hong Jun, a director of the Company and owner of a controlling interest in the Company, the Company established a subsidiary, named Shaanxi Weinan Changjiang Solar Photovoltaic Energy Applied Science and Technology Co., Ltd ("Changjiang PV"), to develop the new solar energy business in April 2012. We hold an indirect 51% interest in Changjiang PV. We and Mr. Zhang Hong Jun have invested in new energy industry for several years. With close relations with government departments and extensive personal connections, we devoted our major efforts to the solar photovoltaic downstream market after signing the mines disposing agreement in June 2012.

Our subsidiary, Changjiang PV, concentrates on the development and operation of EPC projects. Our first EPC project, the Weinan Hechuan 137KWp solar PV building applications has generated revenue for the year ended December 31, 2015 in the amount of $16,718.

We also hold land use rights in a land parcel and we lease a portion of the land use rights on the 5.7 square kilometer parcel to Shaanxi Huanghe Bay Ecological Agriculture Co., Ltd (previously Shaanxi Huanghe Bay Spring Lake Park Co., Ltd.), a company with a common control person. The term of the lease agreement is from January 1, 2011 to December 31, 2029 and the annual rent is approximately $1.2 million (RMB 7,500,000). As of December 31, 2015, we had only received rent payments for 2011 and no payments thereafter. Due to the uncertain collectability, we decided to write off all the receivable related to land lease of $3,618,818 (equivalent to RMB 22,500,000) and decided not to recognize any revenue for the year ended December 31, 2015.

Our Corporate History and Background

The Company is the result of a 2008 share exchange transaction among: (i) North American Gaming and Entertainment Corporation, a Delaware corporation ("North American"); (ii) Shaanxi Changjiang Petroleum & Energy Development Stock Co., Ltd. ("CJP"), a limited liability company established and existing under the law of People's Republic of China; and (iii) the shareholders of CJP, among whom the predominant shareholder, holding 97.2% of CJP's shares, was a Hong Kong company, Hong Kong Wah Bon Enterprise Limited ("Wah Bon"). After completion of the share exchange transaction, the Company entered into a reverse merger with North American.

At the time of the share exchange transaction, CJP owned 60%, and the Company continues to control, Shaanxi East Mining Co., Ltd., ("East Mining") which held the Chinese exploration license through which we pursued our exploration activity.

| 4 |

The share exchange was completed on February 4, 2008, resulting in the shareholders of CJP controlling approximately 96% of the equity ownership of North American. At the time of the closing of the share exchange, North American was a shell company domiciled in Delaware which filed reports under the Exchange Act and whose shares traded in the U.S. over-the-counter market. Wah Bon caused its subsidiary, CJP, to pay $370,000 in cash, and Wah Bon delivered shares constituting 97.2% of the outstanding equity of CJP, in exchange for 3,800,000 shares of North American common stock and 500,000 shares of Series C Preferred Stock of North American, which originally were entitled to 1,218 votes per share. Two U.S. individuals, through their advisory company, Capital Advisory Services, Inc., were paid in the aggregate 4,500,000 shares of North American. In June 2008, CJP changed its name to "Shaanxi Changjiang Mining &New Energy Co., Ltd ("Shaanxi Changjiang")."

Following the share exchange transaction, Wah Bon replaced North American's Board of Directors.

China Changjiang Mining & New Energy Co., Ltd. was incorporated in the state of Nevada on September 19, 2008 for the purposes of re-domesticating the Company from Delaware to Nevada, adopting the Company's current name, and to serve as the surviving company of a reverse merger with North American.

Pursuant to Articles of Merger filed with the Secretary of the State of the State of Nevada on December 4, 2008 and the Secretary of the State of Delaware on April 2, 2009, North American was merged with and into the Company, with the Company being the surviving entity.

On February 9, 2010, we filed a Certificate of Amendment to our Articles of Incorporation to effect a 1-for-10 reverse stock split of our common stock, subject to FINRA approval. The 1-for-10 reverse split was approved by FINRA on July 30, 2010, effective August 2, 2010.

On September 15, 2010, the Company filed with the Nevada Secretary of State a Certificate of Designation and a Certificate of Conversion and Elimination of the Series C Convertible Preferred Stock, pursuant to which: (i) all shares of our Series C Preferred Stock were converted into shares of common stock at a rate of 1,218 shares of common stock for each outstanding share of Series C Preferred Stock; and (ii) we canceled and eliminated the Series C Preferred Stock. In the aggregate, the outstanding shares of the Company's Series C Preferred Stock were converted into 609 million shares of common stock.

As a result of these transactions, we currently have 250,000,000 authorized shares of common stock, par value $0.01 per share, of which 64,629,559 shares are issued and outstanding on the date of filing of this Form 10-K, and 10,000,000 authorized shares of preferred stock, of which no shares are presently issued and outstanding. At the time our share exchange transaction was completed, approximately 96% of the outstanding shares of North American were owned by Wah Bon. See Item 12, "Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters."

We established a subsidiary, named Shaanxi Weinan Changjiang Solar Photovoltaic Energy Applied Science and Technology Co., Ltd. ("Changjiang PV"), in April 2012 to develop the new solar energy business. Our subsidiary, Shaanxi Changjiang, owns 51% of Changjiang PV, and Mr. Zhang Hong Jun, the actual controller, owns the other 49%.

On December 30, 2013, we transferred all of the 60% equity of East Mining to our common control person, Mr. Zhang Hong Jun and one of the shareholders, Mr. Wang Sheng Li with a consideration of $885,696 (RMB 5,400,000). Each of the acquirers obtained 30% equity of East Mining in this transaction.

Shaanxi Changjiang held 20% equity of Shaanxi Changjiang Electricity & New Energy Co., Ltd from 2008, with an investment cost of $315,658 (RMB 2, 000,000) and impairment of $183,429 was provided at the year ended December 31, 2013. On December 31, 2014 Shaanxi Changjiang disclaimed this 20% equity interest in exchange for a waiver of the debt of $201,899 owed to Shaanxi Changjiang Electricity & New Energy Co., Ltd.

| 5 |

Our organization chart as of December 31, 2015 is illustrated as follows.

Industry overview

Solar photovoltaic energy is an emerging, clean energy industry with a growing market share. The global solar PV market has grown from 6.1 Gigawatt ("GW") in 2008 to an estimated 49.7GW in 2014 but with imbalanced development. Application of solar energy in developed countries such as Germany and Japan, are relatively comprehensive and mature. At the present time, the Chinese PV downstream market is still in the initial stages of development, though most of the PV modules are manufactured in China.

In the past year, China's solar PV module manufacturers were hit by the European Union and the United States anti-dumping sanctions. Businesses and governments are trying to find better alternative applications market to absorb the huge domestic surplus solar PV capacity. The untapped domestic PV downstream market is one of the best ways to absorb the surplus production capacity.

The Chinese government is encouraging the construction of a large PV base and the development of distributed photovoltaic. Currently, we mainly focus on the development of distributed photovoltaic power generation projects.

It was estimated that, by 2020, if the Building Integrated PV ("BIPV") would be applied for 10% of the roof area and 15% of the facade area in the existing and new buildings in China, the potential market of BIPV applications would reach 1000GW, equivalent to 45 new installed capacity of the Three Gorges Hydropower Station.

Since the first half of 2012, the supply and demand of silicon in the international market has undergone great changes, resulting in obvious decline in the cost of solar modules. With the declining cost of solar modules from RMB 15 to RMB 6 per watt, the cost of PV power generation was significantly reduced.

We believe the next few years will show protracted continued growth in the PV solar market. Government policies, in the form of both regulation and incentives, have accelerated the adoption of solar technologies by businesses and consumers and have provided opportunities for developers to construct PV systems as an alternative to more traditional forms of power generation.

| 6 |

Our Industry and Principal Market

Sales and Marketing

We have established a sales and marketing department which is focused on identifying and establishing relationships with entities that are likely to have a need for our products and services.

Our products and services are expected to be largely represented through our Company's sales force located in Xi'an City and Weinan City, Shaanxi Province, China.

Current Business Operations

At the present time, our focus is on serving the local solar PV generation market.

According to the national policy and because of the favorable market conditions, Weinan City is to develop photovoltaic power generation demonstration area. Weinan city is a prosperous city, adjacent to the capital of Shaanxi province, Xian city. With rich solar radiation and developed business in the Northwest, Weinan city took advantage to accelerate the development of the distributed solar PV.

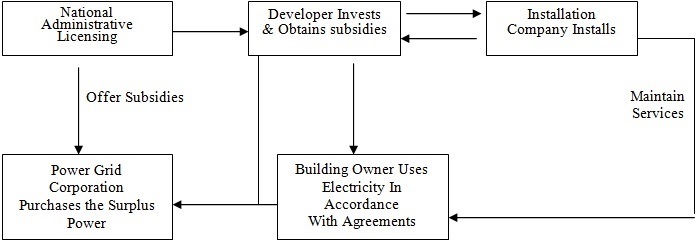

We established a subsidiary, named Shaanxi Weinan Changjiang Solar Photovoltaic Energy Applied Science and Technology Co., Ltd. ("Changjiang PV"), in April 2012 to develop the local distributed solar PV business.

The following chart illustrates our distributed solar PV business model.

In September 2012, Changjiang PV entered into an agreement with Shaanxi Changling Solar Energy & Electric Co., Ltd ("Changling") to outsource the construction of a solar energy project located in Huanghe Bay Springs Lake Theme Park. The project, with a total contract amount of $310,548, was completed by the year end of 2012.

The project was designed to generate electricity preferentially for Huanghe, and sell the surplus power to the grid company. We have received the subsidy funds of $159,096 (RMB 1,000,000) from the local government for the project in December, 2012. For the year ended December 31, 2015, Huanghe Bay Project began to generate revenue of $16,718.

We also hold land use rights in a 5.7 square kilometer parcel located in Huanghe Nantan, Heyang County, in the Shaanxi Province of China. And we lease a portion of the land use rights on the 5.7 square kilometer parcel to Shaanxi Huanghe Bay Ecological Agriculture Co., Ltd (previously Shaanxi Huanghe Bay Spring Lake Park Co., Ltd.), a company with a common control person. The term of the lease agreement is from January 1, 2011 to December 31, 2029 and the annual rent is approximately $1.2 million (RMB 7,500,000). As of December 31, 2015, we had only received rent payments for 2011 and no payments thereafter. Due to the uncertain collectability, we decided to write off all the receivable related to land lease of $3,618,818 (equivalent to RMB 22,500,000) and decided not to recognize any revenue for the year ended December 31, 2015.

| 7 |

Solar PV Industry

General

Though we may be a new participant in solar PV industry, we also realized that the local downstream market of solar PV industry was as new as we are. Experience in some developed countries has shown that there should be a business opportunity in China's PV downstream market in the near future.

Each of our EPC projects is a strategic long-term investment, with relatively low risk, a stable cash inflow can be generated and little ongoing maintenance costs would be incurred once the project begins operations.

Competition

We anticipate that our competitors in the solar PV markets will be local and regional EPC contractors and developers. Other companies in China that engage in solar PV power generation that we consider to be likely competitors, include: Xi'an Huanghe Photovoltaic Technology Co., Ltd., Shaanxi Tuori New Energy Technology Limited, and Shaanxi Changling Electric Co., Ltd., etc. These competitors have more experience in the operation of solar PV energy and have superior financial resources than we do.

The entire solar industry also faces competition from other power generation sources, both conventional sources as well as other emerging technologies. Solar power has certain advantages and disadvantages when compared to other power generating technologies. The advantages include the ability to deploy products in many sizes and configurations, provide reliable power for many applications, serve as both a power generator and the skin of a building and eliminate air, water and noise emissions. The disadvantages mainly came from the relatively high cost of power generation.

The cost of electricity generated by PV products currently is very close to the cost of electricity generated from conventional power such as coal and hydropower in Chinese markets. A significant reduction in the scope or discontinuation of government incentive programs could cause demand for our products and our revenue to decline, and have a material adverse effect on our business, financial condition, results of operations and prospects.

As an emerging industry, the rapid growth of the solar PV could reduce the intensity of competition from alternative products and services.

In the near term, mature government subsidy roadmaps from the government have led developers to be aggressive with their solar installations so that they can enjoy better economic returns. Cost reductions of solar installations have proven to be viable and have also led to aggressive solar installation. In the long run, we believe that solar energy continues to have significant future growth potential and that demand for our products and services will continue to grow significantly for the following reasons:

· | increasing demand for renewable energies, including solar energy, due to the finiteness of fossil fuels and concerns over nuclear power; |

|

|

· | increasing environmental awareness leading to regulations and taxes aimed at limiting emissions from fossil fuels; |

|

|

· | continued adoption or maintenance of government incentives for solar energy at all level of Chinese government; |

|

|

· | narrowing cost differentials between solar energy and conventional energy sources due to market-wide decreases in the average selling prices for PV products driven by lower raw materials costs and increased production efficiencies; and |

|

|

· | continued improvements in the conversion efficiency of PV products leading to lower costs per watt of electricity generated, making solar energy more efficient and cost-effective. |

Government Regulation

This section sets forth a summary of the most significant regulations or requirements that affect our business activities in China.

| 8 |

Regulations issued or implemented by the State Council, China's National Development and Reform Commission ("NDRC"), and other relevant government authorities cover many aspects of new energy industry, including, but not limited to the following principal regulations:

Renewable Energy Law

On December 26, 2009, China revised its Renewable Energy Law, which originally became effective on January 1, 2006. The revised Renewable Energy Law became effective on April 1, 2010 and has laid the legal foundation for developing renewable energy in China.

Renewable Energy Law clearly stipulates the following principles for the development of new energy:

· | To encourage and support the use of solar and other renewable energy and the use of on-grid generation. |

|

|

· | To encourage the installation and use of solar energy water-heating systems, solar energy heating and cooling systems, solar PV systems and other solar energy utilization systems. |

|

|

· | To authorize the relevant pricing authorities to set favorable prices for the purchase of electricity generated by solar and other renewable power generation systems. |

|

|

· | To provide financial incentives, such as national funding, preferential loans and tax preferences for the development of renewable energy projects. |

Government Directives

In January 2006, the NDRC promulgated two implementation directives of the Renewable Energy Law. These directives set forth specific measures in setting prices for electricity generated by solar and other renewal power generation systems and in sharing additional expenses occurred. The directives further allocate the administrative and supervisory authorities among different government agencies at the national and provincial levels and stipulate responsibilities of electricity grid companies and power generation companies with respect to the implementation of the Renewable Energy Law.

China's Ministry of Construction issued a directive in June of 2005, which seeks to expand the use of solar energy in residential and commercial buildings and encourages the increased application of solar energy in townships. In addition, China's State Council promulgated a directive in June of 2005, which sets forth specific measures to conserve energy resources and encourage exploration, development and use of solar energy in China's western areas, which are not fully connected to electricity transmission grids, and other rural areas.

In July 2007, the PRC State Electricity Regulatory Commission issued the Supervision Regulations on the Purchase of All Renewable Energy by Power Grid Enterprises which became effective on September 1, 2007. To promote the use of renewable energy for power generation, the regulations require that electricity grid enterprises must in a timely manner set up connections between the grids and renewable power generation systems and purchase all the electricity generated by renewable power generation systems. The regulations also provide that power dispatch institutions shall give priority to renewable power generation companies in respect of power dispatch services provision.

On September 4, 2006, China's Ministry of Finance and Ministry of Construction jointly promulgated the Interim Measures for Administration of Special Funds for Application of Renewable Energy in Building Construction, which provides that the Ministry of Finance will arrange special funds to support the application of renewable energy in building construction in order to enhance building energy efficiency, protect the ecological environment and reduce the consumption of fossil energy. These special funds provide significant support for the application of solar energy in hot water supply, refrigeration and heating, PV technology and lighting integrated into building construction materials.

| 9 |

On October 28, 2007, the Standing Committee of the National People's Congress adopted amendments to the PRC Energy-saving Law, which sets forth policies to encourage the conservation of energy in manufacturing, civic buildings, transportation, government agents and utilities sectors. The amendments also seek to expand the use of the solar energy in construction areas.

In March 2009, China's Ministry of Finance promulgated the Interim Measures for Administration of Government Subsidy Funds for Application of Solar Photovoltaic Technology in Building Construction, or the Interim Measures, to support the demonstration and the promotion of solar PV applications in China. Local governments are encouraged to issue and implement supporting policies for the development of solar PV technology. These Interim Measures set forth subsidy funds set at RMB 20 per watt for 2009 to cover solar PV systems integrated into building construction that have a minimum capacity of 50 kilowatt peak.

In April 2009, the Ministry of Finance and the Ministry of Housing and Urban-Rural Development jointly issued the "Guidelines for Declaration of Demonstration Project of Solar Photovoltaic Building Applications." These guidelines created a subsidy of up to RMB 20 per watt for building integrated PV or BIPV projects using solar-integrated building materials and components and up to RMB 15 per watt for BIPV projects using solar-integrated materials for rooftops or walls.

In July 2010, the Ministry of Housing and Urban-Rural Development issued the "City Illumination Administration Provisions" or the Illumination Provision. The Illumination Provisions encourage the installation and use of renewable energy system such as PV systems in the process of construction and re-construction of city illumination projects.

On March 8, 2011, the Ministry of Finance and the Ministry of Housing and Urban-Rural Development jointly promulgated the Notice on Further Application of Renewable Energy in Building Construction, which aims to raise the percentage of renewable energy used in buildings.

On March 27, 2011, the NDRC promulgated the revised Guideline Catalogue for Industrial Restructuring which categorizes the solar power industry as an encouraged item.

On March 14, 2012, the Ministry of Finance, the NDRC and the National Energy Bureau jointly issued the interim measures for the management of additional subsidies for renewable-energy power prices, according to which relevant renewable-energy power generation enterprises are entitled to apply for subsidies for their renewable power generation projects that satisfy relevant requirements set forth in the measures.

On March 1, 2013, China's State Council issued the "Twelfth Five Year Plan." The plan supports the promotion and development of renewable energy, including the solar energy. The plan also encourages the development of solar PV power stations in the areas with abundant solar power resource.

On November 18, 2013, the National Energy Bureau issued "The Interim Measures for the management of distributed photovoltaic power generation projects". The regulation contributes to promote the application of distributed photovoltaic power and regulate the projects management.

On November 26, 2013, the Ministry of Finance announced that the power generated by its own distributed PV power generation project could be exempted from imposing government fee, such as renewable energy surcharges, fee for major national water conservancy construction, etc.

In January, 2014, the National Energy Administration of China announced the PV installation target for 2014 to be 14GW, which includes 8GW for distributed PV systems and 6GW for large scale PV power plants.

In the same month, the National Energy Administration of China released a list of 81 "New Energy Demonstration Cities" and eight "industrial demonstration parks" in 28 and 8 provinces respectively. These cities and zones are required to achieve their respective mandatory targets in terms of solar PV installations and the percentage of installed renewable energy power generation capacities by the end of 2015, or the end of the 12th Five-Year-Plan.

| 10 |

In February 2014, the Certification and Accreditation Administration and the National Energy Administration jointly issued the "Implementation Opinions on Strengthening the Testing and Certification of PV Products." The implementation opinions provide that only certified PV products may be connected to the public grid or receive government subsidies. The institutions that certify PV products must be approved by the Certification and Accreditation Administration. According to the implementation opinions, PV products that are subject to certification include PV battery parts, inverters, control devices, confluence devices, energy storage devices and independent PV systems.

In December, 2014, the National Energy Administration of China released a list of 30 "distributed solar photovoltaic industrial application demonstration zone" to encourage the development of distributed solar PV industry.

On January 28, 2015, the NEA of China announced the target for national solar installations in 2015 to be 15GW, 8GW of which would be targeted for utility scale, 7GW for distributed generation.

On December 24,2015, the National Development and Reform Commission promulgated the Notice on the improvement of photovoltaic electricity price, which announced a new standard on-grid price implemented from January 1, 2016 for solar PV electricity.

On December 15, 2015, the National Energy Bureau announced the annual plan for the development of solar PV. The solar power installed capacity will reach 160GW, and total annual investment will reach 200 billion RMB for 2016, in the light of the plan.

Restrictions on Foreign Businesses and Investments

The principal regulation governing foreign ownership of photovoltaic businesses in the PRC is the Foreign Investment Industrial Guidance Catalogue, updated and effective as of January 30, 2012. Under this regulation, industrial activity is categorized as "permitted," "restricted," or "prohibited." and the solar photovoltaic business is listed as an industry of "permitted" where foreign investments are encouraged.

Enterprise Income Tax

On March 16, 2007, the National People's Congress passed the Enterprise Income Tax Law ("the China EIT Law"), which was effective as of January 1, 2008.

The China EIT Law also provides that an enterprise established under the laws of foreign countries or regions but whose "de facto management body" is located in the PRC be treated as a resident enterprise for PRC tax purpose and consequently be subject to the PRC income tax at the rate of 25% for its worldwide income. The Implementing Rules of the new EIT Law merely defines the location of the "de facto management body" as "the place where the exercising, in substance, of the overall management and control of the production and business operation, personnel, accounting, properties, etc., of a non-PRC company is located." On April 22, 2009, the PRC State Administration of Taxation further issued a notice entitled "Notice regarding Recognizing Offshore-Established Enterprises Controlled by PRC Shareholders as Resident Enterprises Based on Their place of Effective Management." Under this notice, a foreign company controlled by a PRC company or a group of PRC companies shall be deemed as a PRC resident enterprise, if ( )the senior management and the core management departments in charge of its daily operations mainly function in the PRC; ( ) its financial decisions and human resource decisions are subject to decisions or approvals of persons or institutions in the PRC; ( ) its major assets, accounting books, company sales, minutes and files of board meetings and shareholders' meetings are located or kept in the PRC; and ( ) more than half of the directors or senior management personnel with voting rights reside in the PRC. Based on a review of surrounding facts and circumstances, the Company does not believe that it is likely that its operations outside of the PRC should be considered a resident enterprise for PRC tax purposes. However, due to limited guidance and implementation history of the China EIT Law, should the Company be treated as a resident enterprise for PRC tax purposes, the Company will be subject to PRC tax on worldwide income at a uniform tax rate of 25% retroactive to September 19, 2008.

The China EIT Law also imposes a withholding income tax of 10% on dividends distributed by a foreign invested enterprise to its immediate holding company outside of China, if such immediate holding company is considered as a non-resident enterprise without any establishment or place within China or if the received dividends have no connection with the establishment or place of such immediate holding company within China, unless such immediate holding company's jurisdiction of incorporation has a tax treaty with China that provides for a different withholding arrangement. Such withholding income tax was exempted under the previous income tax regulations. The United States of America, where the Company is incorporated, has such tax treaty with China.

Our Employees

As of December 31, 2015, we had an aggregate of 12 employees, of whom 11 were full-time employees. This includes two people in marketing, three in maintenance and quality control, three in financial and accounting, and four in general management.

Available Information

We currently do not maintain a web site; however, our annual, periodic and current reports can be accessed on the web site of the SEC at www.sec.gov and printed free of charge.

| 11 |

ITEM 1A. RISK FACTORS.

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition and results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose part or all of your investment. You should read the section entitled "Special Notes Regarding Forward-Looking Statements" above for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this report.

RISKS RELATED TO OUR BUSINESS

WE HAVE TRANSITIONED OUR BUSINESS FROM MINING TO NEW CLEAN ENERGY BUSINESS, WHICH INVOLVED SIGNIFICANT TRANSITION AND INTEGRATION RISK

We disposed of our mining business sector in 2013, and currently we are developing our new clean energy solar business. This change involves significant transition and integration risks, both because we are required to end our participation in mining operations and wind down our existing relationships prior to our being able to participate in a new energy business and because we may incur costs and/or a loss of revenue (or a delay in anticipated increased revenue from the new business) in connection with these changes. The significant transition and integration risks include:

· | an inability to transition our business to clean energy due to a lack of applicable approvals or difficulty in satisfying entrance requirements; |

|

|

· | significant revenue dilution as we terminate our participation in mining operations and/or insufficient, or delay in receipt of, revenue from our participation in current operations, including an inability to maintain our key customer and business relationships as we transition to new energy; and |

|

|

· | difficulties integrating our technology processes, and |

|

|

· | lack of experience in EPC project management. |

If any of these risks or costs materializes, they could have a material adverse effect on our business, results of operations and financial condition.

OUR LIMITED OPERATING HISTORY IN CLEAN NEW ENERGY INDUSTRY MAKE IT DIFFICULT TO EVALUATE OUR RESULTS OF OPERATIONS AND PROSPECTS.

We are a company engaged in the business of local clean solar energy development with two EPC projects under construction and several potential projects. We also hold land use rights in a 5.7 square kilometer parcel located in Huanghe Nantan (Huanghe Bay), Heyang County, in the Shaanxi Province of China, which is held for leasing purpose.

Though we commenced the biomass incineration power business in 2009 by cooperation with our strategic partner, our business change in 2012 was our first time to enter the solar photovoltaic industry and determine the strategy of mainly focusing on PV EPC developing in the future.

| 12 |

We have generated revenue in solar PV business for the years ended December 31, 2014 and 2015 in the amounts of $26,908 and $16,718, respectively. However, our limited operating history makes the prediction of future results of operations difficult, and in addition, we cannot assure that the existing management model is suitable for the EPC project development.

We will devote more resources in our marketing promotion, and attempt to adapt our management to a more flexible operation environment as we have to deal with a variety of competitors due to the relatively lower entrance barrier for solar PV downstream industry.

WE DEPEND ON OUR SENIOR MANAGEMENT AND KEY EMPLOYEES, THE LOSS OF WHOM COULD ADVERSELY AFFECT OUR OPERATIONS.

Our success will depend to a large degree upon our ability to identify, hire, and retain personnel, particularly persons familiar with the marketing, manufacturing and administrative processes associated with the solar energy business. We depend on the skills of our management team and current key employees, such as Mr. Chen Wei Dong, our Chairman, President, and Chief Executive Officer. We may be unable to retain our existing key personnel or attract and retain additional key personnel.

The loss of any of our key employees or the failure to attract, and retain experienced or additional key employees could have a material adverse effect on our business and financial condition.

WE ACT AS THE GENERAL CONTRACTOR FOR OUR CUSTOMERS IN CONNECTION WITH THE INSTALLATION OF OUR SOLAR POWER SYSTEMS AND ARE SUBJECT TO RISKS ASSOCIATED WITH CONSTRUCTION, BONDING, COST OVERRUNS, DELAYS AND OTHER CONTINGENCIES, WHICH COULD HAVE A MATERIAL ADVERSE EFFECT ON OUR BUSINESS AND RESULTS OF OPERATIONS.

We act as the general contractor for our customers in connection with the installation of our solar power systems. All essential costs are estimated at the time of entering into the sales contract for a particular project, and these are reflected in the overall price that we charge our customers for the project. These cost estimates are preliminary and may or may not be covered by contracts between us or the other project developers, subcontractors, suppliers and other parties to the project. In addition, we require qualified, licensed subcontractors to install most of our systems. Shortages of such skilled labor could significantly delay a project or otherwise increase our costs. Should miscalculations in planning a project or defective or late execution occur, we may not achieve our expected margins or cover our costs. Additionally, many systems customers require performance bonds issued by a bonding agency. Due to the general performance risk inherent in construction activities, it is sometimes difficult to secure suitable bonding agencies willing to provide performance bonding. In the event we are unable to obtain bonding, we will be unable to bid on, or enter into sales contracts requiring such bonding.

Delays in solar panel or other supply shipments, other construction delays, unexpected performance problems in electricity generation or other events could cause us to fail to meet these performance criteria, resulting in unanticipated and severe revenue and earnings losses and financial penalties. Construction delays are often caused by inclement weather, failure to timely receive necessary approvals and permits, or delays in obtaining necessary solar panels, inverters or other materials. The occurrence of any of these events could have a material adverse effect on our business and results of operations.

WE ARE A PRIVATE COMPANY MAINLY OPERATING IN CHINA, WHICH MAY RESULT IN A MORE DIFFICULT BUSINESS ENVIRONMENT FOR US, COMPAIRED WITH THE STATE OWNED COMPANY IN PV INDUSTRY

We are a private company operating in China in PV industry, which may incur more cost in obtaining administrative permit, acquiring EPC project, etc, while many competitors are state-owned Companies and operate in a preferable business environment. The PV developer must apply for the PV demonstration project for financial subsidy. Usually the relevant government agencies give priority to the state-owned company under equal conditions.

| 13 |

RISKS RELATED TO OUR PV INDUSTRY

A SIGNIFICANT REDUCTION IN OUR DISCONTINUATION OF GOVERNMENT SUBSIDIES AND ECONOMIC INCENTIVES MAY HAVE A MATERIAL ADVERSE EFFECT ON OUR RESULTS OF OPERATIONS.

Demand for our products and services substantially depends on government incentives aimed to promote greater use of solar power. The PV application markets would not be commercially viable without government incentives. This is because the cost of generating electricity from solar power currently exceeds the cost of generating electricity from conventional or non-solar renewable energy sources.

Usually, the local government bears the financial subsidy. If the local finance is too tight to offer the subsidy, the change of incentive policy may be the only choice. Though we don't think the national incentive policy shall be significant changed in the near future, the local financial subsidy policy adjustment could have a material effect on our business directly.

The scope of the government incentives for solar power depends, to a large extent, on political and policy developments in China related to environmental, economic or other concerns, which could lead to a significant reduction in or a discontinuation of the support for renewable energy sources.

Any new government regulations or utility policies pertaining to our solar power products may result in significant additional expenses to us, our resellers, and our customers and as a result, could cause a significant reduction in demand for our solar power products.

BECAUSE THE MARKETS IN WHICH WE COMPETE ARE HIGHLY COMPETITIVE AND MANY OF OUR COMPETITORS HAVE GREATER RESOURCES THAN US, WE MAY NOT BE ABLE TO COMPETE SUCCESSFULLY AND WE MAY LOSE OR BE UNABLE TO GAIN MARKET SHARE.

We mainly focus on the local solar PV downstream market. Our competitors include Xi'an Huanghe Photovoltaic Technology Co., Ltd., Shaanxi Tuori New Energy Technology Limited, and Shaanxi Changling Electric Co., Ltd., etc. Most of them have a stronger market position than ours, more sophisticated technologies greater resources and better name recognition than we do.

The barriers to entry are relatively low in the PV consumer market. Financial strength and social relations resource were the key barriers to entry for the EPC project acquisition. Because of government's continuous efforts to encourage the PV consumer market, more and more companies with strong financial support commenced their solar PV energy business. It is a challenge for us to establish our competitive market position in the industry. In order to acquire more market share, we must respond more quickly to changing customer demands or market conditions or to devote greater resources to the marketing promotion.

New competitors or alliances among existing competitors could emerge and rapidly acquire a significant market share, which would harm our business. If we fail to compete successfully, our business would suffer and we may lose or be unable to gain market share.

RISKS RELATED TO THE REAL ESTATE INDUSTRY

THE CHINESE GOVERNMENT OWNS ALL LAND IN CHINA, AND CHINA ISSUES LAND USE RIGHTS INSTEAD OF LEGAL TITLE TO THE PROPERTIES. THERE IS NO ASSURANCE THAT OUR RIGHTS TO THE PROPERTIES WILL NOT BE SUBJECT TO IMPAIRMENT OR LOSS.

In China, all property is owned by the central government. Unlike deeds or other evidence of a fee simple ownership interest, land use rights are always subject to fixed periods and permitted land use, usually for long periods of time. These periods are frequently 50 years. Disputes over land use right are common. A loss of our property rights would cause material damage to the Company and the price of its securities and could result in the loss of the entire value of our Company.

| 14 |

RISKS RELATED TO DOING BUSINESS IN THE PEOPLE'S REPUBLIC OF CHINA

WE ARE SUBJECT TO THE POLITICAL AND ECONOMIC POLICIES OF THE PEOPLE'S REPUBLIC OF CHINA, AND GOVERNMENT REGULATION COULD HAVE A MATERIAL ADVERSE EFFECT ON OUR INTENDED BUSINESS.

All of our assets and operations are in the PRC. As a result, our operating results and financial performance as well as the value of our securities could be affected by adverse changes in economic, political and social conditions in China.

The Chinese government adopted a policy to transition from a planned economy to a market driven economy in 1978. Since then, the economy of the PRC has undergone rapid modernization, although the Chinese government still exerts a dominant force in the nation's economy. This continues to include reservation to the state of land use rights, and includes controls on foreign exchange rates and restrictions or prohibitions on foreign ownership in various industries. All lands in China are state owned and only limited "land use rights" are conveyed to business enterprises or individuals.

All of our intended exploration and mining activities require approvals from the local government authorities in China. Obtaining governmental approval is typically a lengthy and difficult process with no guaranty of success. Since the lands where our activities are located were acquired through the grant of a land use right, changes in government policy could adversely affect our business.

The Chinese government operates the economy in many industries through various five-year plans and even annual plans. A large degree of uncertainty is associated with potential changes in these plans. Since China's economic reforms have no precedent, there can be no assurance that future changes will not create materially adverse conditions for our business.

FLUCTUATION OF THE CHINESE CURRENCY COULD MATERIALLY AFFECT OUR FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

We expect that our future revenues and expenses will be generated in China, but our reporting currency is US dollars and reported results will be affected by exchange rate fluctuations between the RMB and the US dollar. We cannot give any assurance that the value of the RMB will continue to appreciate, or even remain stable against the US dollar or any other foreign currency. Accordingly, we may experience economic losses and negative impacts, as reported in U.S. Dollars, as a result of foreign exchange rate fluctuations.

The RMB is currently not a fully convertible currency. The Chinese government may restrict future access to foreign currencies for current account transactions. This may make it difficult for us to transfer money from China to other countries on an economically advantageous basis or even at all. It may also make it difficult for us to pay cash returns on the investment of foreign capital.

THERE ARE RISKS INHERENT IN DOING BUSINESS IN CHINA OVER WHICH WE HAVE NO CONTROL.

The political and economic systems of the PRC are very different from those of the United States and other western countries. China remains volatile with respect to certain social, economic and political issues which could lead to revocation or adjustment of reforms. There are also issues between China and the United States that could result in disputes or instabilities. The role of China and its government remain in flux both domestically and internationally, and could cause shocks or setbacks that may adversely affect our business.

THE CHINESE LEGAL SYSTEM DIFFERS FROM THAT OF THE UNITED STATES, PROVIDING LESS PROTECTION FOR INVESTORS, AND IT MAY BE DIFFICULT FOR INVESTORS TO SEEK LEGAL REDRESS AGAINST US OR OUR OFFICERS AND DIRECTORS, INCLUDING CLAIMS THAT ARE BASED UPON U.S. SECURITIES LAWS.

All of our current operations are conducted in China. All of our current directors and officers are nationals or residents of China. All of the assets of these persons are located in China. The PRC legal system is a civil law system. Unlike the common law system, the civil law system is based on written statutes in which decided legal cases have little value as precedents. Differences in interpretations and rulings can occur with limited opportunity for redress or appeal.

| 15 |

It may not be possible to effect service of process within the U.S. or elsewhere outside China upon our officers and directors. Even if service of process were successful, considerable uncertainty exists as to whether Chinese courts would recognize and enforce U. S. laws or judgments obtained in the U.S. federal and state securities laws as the U. S. laws confer substantial rights to investors and shareholders that have no equivalent in China. Therefore a claim against us or our officers and/or directors or even a final judgment in the U. S. may not be recognized or enforced by Chinese courts.

In 1979, the PRC began to reform its legal system and has enacted numerous laws regulating economic and business development, including those related to foreign investment. Currently many of the approvals required for our business may be obtained at local or provincial level. We believe that it is relatively easier and faster to obtain provincial approval than central government approval. Changes to existing laws that repeal or alter local regulatory authority and preempt it with national laws could negatively affect our business and the value of our securities.

China's regulations and policies regarding investments, including investment in the PV business, are subject to continued reformation and revisions. They may change in a manner adverse to us and our stockholders.

CHINESE LAWS COULD RESTRICT THE PAYMENT OF DIVIDENDS FROM ANY PROCEEDS OBTAINED FROM LIQUIDATION OF OUR ASSETS.

All of our assets are located in China. Chinese law governs the distributions that can be made in the event of liquidation of assets of foreign invested enterprises. While dividend distribution is allowed, some distributions are subject to the approval from the foreign exchange authority in China. Liquidation proceeds would also be subject to foreign exchange control. We are unable to predict the outcome in the event of liquidation insofar as it affects payment to non-Chinese nationals.

RISKS RELATED TO OUR COMMON STOCK

THERE IS CURRENTLY A LARGE MARKET OVERHANG IN OUR COMMON STOCK AND FUTURE SALES OF OUR COMMON STOCK COULD DEPRESS THE MARKET PRICE AND DIMINISH THE VALUE OF YOUR INVESTMENT.

On February 9, 2010, we filed a Certificate of Amendment to our Articles of Incorporation to effect a 1-for-10 reverse split of our common stock, after which all shares of our Series C Preferred Stock were converted into an aggregate of 609 million shares of our common stock. This effectively eliminated the ability of our other common stock holders to have a significant role in the election of directors and other corporate changes. Future sales of shares of our common stock or securities that are convertible into our common stock could adversely affect the market price of our common stock. If any of our principal stockholders sells a large number of shares or if we issue a large number of shares, the market price of our common stock could significantly decline. Moreover, the perception in the public market that our principal stockholders might sell shares of common stock could further depress the market for our common stock.

BECAUSE OUR OFFICERS AND DIRECTORS CONTROL THE MAJORITY OF THE VOTING POWER OF OUR COMMON STOCK, INVESTORS IN OUR COMMON STOCK WILL NOT BE ABLE TO DETERMINE THE OUTCOME OF STOCKHOLDER VOTES.

Our officers and directors currently control approximately 85% of our common stock. So long as they continue to hold, directly or indirectly, shares of common stock representing more than 50% of the combined voting power of our common stock, they will be able to direct the election of all of the members of our board of directors who will determine our strategic plans and financing decisions and appoint top management. They will also be able to determine the outcome of substantially all matters submitted to a vote of our stockholders, including matters involving mergers, acquisitions and other transactions resulting in a change of control of us, and our pursuit of corporate opportunities. They may seek to cause us to take courses of action that, in their judgment, could enhance their investment in us, but which might involve risks to holders of our common stock or adversely affect us or other investors.

| 16 |

THE MARKET FOR SHARES OF OUR COMMON STOCK HAS BEEN LIMITED AND SPORADIC, AND THERE IS NO GUARANTEE THAT A MARKET WILL BE AVAILABLE FOR YOU TO SELL YOUR SHARES.

Shares of our common stock are not listed on any exchange but have been sporadically traded in over the counter transactions or in inter-dealer quotations. There is no assurance that any market makers will in the future post bid and ask prices for our shares of common stock. Our stock has been very thinly traded and there were many days or weeks that the shares did not trade at all. There is no assurance that any market will exist at the time that a shareholder wishes to sell his or her shares and there is no assurance that any market will continue.

OUR COMMON STOCK PRICE IS VOLATILE AND MAY NOT APPRECIATE IN VALUE.

The market price of shares of our common stock fluctuated and is likely to continue to fluctuate significantly. Fluctuations could be rapid and severe and may provide investors little opportunity to react. Factors such as changes in commodity prices, conversion of our preferred shares, results of operations, and a variety of other factors, many of which are beyond the control of the Company, could cause the market price of our common stock to fluctuate substantially. Also, stock markets in penny stock shares tend to have extreme price and volume volatility. The market prices of the securities of many smaller public companies are subject to volatility for reasons that frequently are unrelated to operating performance, earnings or other recognized measurements of value. This volatility may cause declines, including very sudden and sharp declines, in the market price of our common stock. We cannot assure investors that the stock price will appreciate in value, that a market will be available to resell your securities or that the shares will retain any value at all.

WE DO NOT FORESEE PAYING CASH DIVIDENDS IN THE FORESEEABLE FUTURE.

We have not paid cash dividends on our stock and we do not plan to pay cash dividends on our stock in the foreseeable future. We intend to retain any earnings to help fund operations. Therefore an investment in our common stock is not appropriate for investors who require regular and periodic returns on their investments.

OUR STOCK IS A PENNY STOCK. TRADING OF OUR STOCK MAY BE RESTRICTED BY THE SEC'S PENNY STOCK REGULATIONS AND THE FINRA'S SALES PRACTICES, WHICH MAY LIMIT A STOCKHOLDER'S ABILITY TO BUY AND SELL OUR STOCK.

Our stock is a penny stock currently. The SEC has adopted Rule 15g-9 which generally defines "penny stock" to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker- dealers who sell to persons other than established customers and "accredited investors", as defined. Rule 15g-2 requires a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form required by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market, and cautions investors against making a hurried investment decision. The broker-dealer must also provide the customer with the current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction. The broker-dealer must also send a confirmation of these prices after the trade. After a purchase of penny stock, the broker-dealer must send a monthly account statement that gives an estimate of the value of each penny stock purchased.

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules.

Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in, and limit the marketability of, our common stock.

In addition to the "penny stock" rules promulgated by the SEC, the FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative, low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer's financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker- dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock.

| 17 |

ITEM 1B.UNRESOLVED STAFF COMMENTS.

Not applicable to a smaller reporting company.

ITEM 2. PROPERTIES.

Corporate Headquarters

Our corporate headquarters, consisting of 178 square meters, are located at Twenty-fourth Floor,Block B, Xinhui Mansion, Gaoxin Road, Hi-tech Zone, Xi'An, Shaanxi Provence PRC, 710075. Our telephone number is (86)29-88331685 and our fax number is (86)29-88332335. We moved to this office that was owned by Shaanxi Baishui Dukang Liquor Co., Ltd, one of our related parties, in April 2015. We are allowed to occupy the space for free.

Land use right leasing Parcel

All land in China is owned by the state. Individuals and companies are permitted to acquire rights to use land, or "land use rights," for specific purposes. In the case of land used for commercial purposes, the land use rights are granted for a period of 50 years. The original period, and any subsequent periods, may be renewed prior to their expiration. Granted land use rights are transferable and may be used as security for borrowings and other obligations.

We have land use rights (certificate No. (2006) 3240001), in a 5.7 square kilometer parcel in Huanghe Nantan (Huanghe Bay), Heyang County, Shaanxi province. We currently lease a portion of this parcel to Shaanxi Huanghe Bay Ecological Agriculture Co., Ltd, a related party of the Company, for the development and operation of a theme park. The lease expires on December 31, 2029.

The photograph below shows an overview of our land in Huanghe Bay.

The solar PV parcel

We owned a solar PV project, Huanghe Bay Project, as of December 31, 2015, located in the Huanghe Nantan (Huanghe Bay), Heyang County, Shaanxi province.

ITEM 3. LEGAL PROCEEDINGS.

None.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

| 18 |

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Market information

The trading of our stock was suspended on April 1, 2011 by the SEC and resumed on April 17, 2014. Except the suspension period, the Company's common stock was traded over-the-counter and quoted from time to time in the Over-the-Counter ("OTC") Bulletin Board under the trading symbol "CHJI.". There is currently a thinly traded market for the Company's common stock on the OTC Markets Group, Inc. Pink Current Tier. The following table sets forth the range of high and low bid prices as reported by the OTC Bulletin Board for the periods indicated. Such quotations represent inter-dealer prices without retail markup, markdown, or commission, and may not necessarily represent actual transactions.

|

|

|

|

| BID PRICE |

| ||||

CALENDAR YEAR |

| QUARTER |

|

| high |

|

|

| low |

|

2015 |

| Fourth quarter |

|

| 0.0400 |

|

|

| 0.0350 |

|

2015 |

| Third quarter |

|

| 0.0450 |

|

|

| 0.0400 |

|

2015 |

| Second quarter |

|

| 0.0450 |

|

|

| 0.0450 |

|

2015 |

| First quarter |

|

| 0.1300 |

|

|

| 0.0400 |

|

2014 |

| Fourth quarter |

|

| 0.0400 |

|

|

| 0.0400 |

|

2014 |

| Third quarter |

|

| 0.0900 |

|

|

| 0.0200 |

|

2014 |

| Second quarter (from April 17, 2014) |

|

| 0.5100 |

|

|

| 0.0001 |

|

Holders

As of December 31, 2015, we had 3,582 record holders of our common stock.

Dividends

To date, we have not declared or paid any dividends on our common stock. We currently do not anticipate paying any cash dividends in the foreseeable future on our common stock. Although we intend to retain our earnings, if any, to finance the exploration and growth of our business, our board of directors reserves the right to declare and pay dividends in the future, to the extent permitted by law.

Stock Option Grants

None.

Unregistered Sales of Equity Securities

None.

| 19 |

Repurchases of Shares by the Company

None.

ITEM 6. SELECTED FINANCIAL DATA.

Not required for a smaller reporting company.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion and analysis should be read in conjunction with our consolidated financial statements and the related notes thereto as filed with the SEC and other financial information contained elsewhere in this Form 10-K.

Overview

We have transitioned our business from mining to clean new energy, and mainly focus on the solar photovoltaic, or "PV", downstream market at present stage. We are currently in the development stage with the goal of becoming a turnkey developer and Engineering, Procurement and Construction contractor of solar PV energy facilities. We intend to design, engineer, construct, market and sell high-quality PV energy facilities for commercial and utility applications to local markets. Our Huanghe Bay Project has generated revenue for the year ended December 31, 2014 and 2015.

Before June 1, 2012, we were engaged in exploration for commercially recoverable metal-bearing mineral deposits. On June 1, 2012, we entered into an agreement with Xunyang Yongjin Mining Co., Ltd to transfer our mining exploration rights for a cash payment of $2,380,612 (RMB 15,000,000). Further, on December 30, 2013, our subsidiary, Shaanxi Changjiang Mining &New Energy Co., Ltd. ("Shaanxi Changjiang"), entered into Equity Transfer Agreements with each of Zhang Hong Jun, a director of the Company and owner of a controlling interest in the Company (holding 54.43% as of December 31, 2013), and Wang Sheng Li, a director and shareholder of the Company (holding 11.52% as of December 31, 2013), to sell Shaanxi Changjiang's entire 60% interest in Shaanxi East Mining Co., Ltd., ("East Mining" and formerly referred to as "Dongfang Mining") for a total consideration of $885,696 (RMB 5,400,000). The consideration payable to the Company was used to offset amounts owed to each of the acquirers. Each of the acquirers obtained 30% equity in this transaction.

We also hold land use rights in a land parcel and we lease a portion of the land use rights on the 5.7 square kilometer parcel to Shaanxi Huanghe Bay Ecological Agriculture Co., Ltd (previously Shaanxi Huanghe Bay Spring Lake Park Co., Ltd.),, a company with Zhang Hong Jun, a director of the Company and owner of a controlling interest in the Company. The term of the lease agreement is from January 1, 2011 to December 31, 2029. Our land use rights are amortized over their 50 year term. The Land use right was our largest asset, with an annual rent of approximately $1.2 million (RMB 7, 500,000).

As of December 31, 2015, we only received rent payment of 2011 and no any collection afterwards. Due to the uncertain collectability, we decided to write off all the receivable related to land lease of $3,618,818 (equivalent to RMB 22,500,000) and decided not to recognize any revenue for the year ended December 31, 2015.

| 20 |

Our land use rights are amortized over 50-year term. The following is a summary of the book value of our land use rights as of December 31, 2015:

Cost |

| $ | 19,719,353 |

|

Less: Accumulated amortization |

|

| 4,656,915 |

|

Land use rights, net |

| $ | 15,062,438 |

|

The amortization expense for the year ended December 31, 2015 and December 31, 2014 was $411,717 and $416,527, respectively.

As reflected in the accompanying consolidated financial statements, the Company had an accumulated deficit of $7,403,166 as of December 31, 2015, which includes net loss of $4,655,722 for the year ended December 31, 2015. The Company's operations used cash was $133,137 in 2015.

In the past, the Company relied on the loan received from the related parties, and cash generated from operations to meet its operating requirements. Although the Company was successful in the past in obtaining financing, there can be no assurance that it will be able to obtain adequate financing in the future or that the terms of such financings will still be favorable. However in the event that we have insufficient cash to meet our operating requirements, our related companies and shareholders will commit to provide loan to maintain liquidity.

We believe that we have adequate capital to assure that we will be able to meet our obligations or obtain sufficient capital to complete our plan of operations for the next twelve (12) months.

RESULTS OF OPERATIONS

Comparison of the Years Ended December 31, 2015 and December 31, 2014

Sales revenue

We generated revenue of $16,718 from solar PV energy segment for the year ended December 31, 2015, compared with the revenue of $26,908 for the year ended December 31, 2014. We did not recognize land use right leasing revenue for the year ended December 31, 2015, because we could not expect the recovery of this revenue, while we recognized land use right leasing revenue of $1,220,365 for the year ended December 31, 2014. As a result, the revenue was $16,718 for the year ended December 31, 2015, while the total revenue was $1,247,273 for the year ended December 31, 2014.

Operating Expenses

Total operating expenses for the year ended December 31, 2015 increased to $4,674,545 from comparable figure of $748,934 for the year ended December 31, 2014, representing an increase of $3,925,611, or 524%. The operating expenses increased significantly because we wrote off a total balance of $3,897,124 due from related parties and total balance of $71,820 receivable from third parties due to uncertain collectability. And the depreciation expense slightly decreased to $53,174, from comparable figure of $55,324. The amortization expense for the year ended December 31, 2015 remained stable, as no addition or disposal occurred for Land use rights.

| 21 |

Net Income (Loss)

Net Loss for the year ended December 31, 2015 was $4,655,722, as compared to a net income of $429,045 for year ended December 31, 2014. The significant decline in our operating results was mainly attributable to the bad debt expense of $3,968,944 for the year ended December 31, 2015.

Comprehensive Income (Loss)

Our comprehensive loss for the year ended December 31, 2015 was $5,321,924 compared with comprehensive income of $326,210 for the year ended December 31, 2014. The other comprehensive income (loss) for each period only referred to the foreign currencies translation gain (loss), between U.S. Dollar and Chinese Yuan RMB (or Hong Kong Dollar for Wah Bon). The exchange rate of RMB against USD depreciated from 6.1460 as of December 31, 2014 to 6.4907 as of December 31, 2015, resulting in the other comprehensive loss of $666,202 for the year ended December 31, 2015, compared with the other comprehensive loss of $102,835 for the year ended December 31, 2014.

Stockholders' Equity

Stockholders' equity decreased to $10,540,118 as of December 31, 2015, or approximately 31%, from $15,211,685 as of December 31, 2014. The significant decrease was primarily due to the net loss of 4,655,722, the other comprehensive loss of $666,202, and offset by an increase in additional paid-in capital of $495,510 for the year ended December 31, 2015.

The increase in additional paid in capital was mainly due to an exemption from the loan of RMB10,000,000 (approximately $1,572,451) owed to Shaanxi East Mining Co., Ltd, a related party of the Company, an exemption from the salary and rent payable of $97,164 that had been paid by the related parties, offset by a decrease of $770,333 in writing off a receivable due from Shaanxi Jiuzu Shaokang Liquor Co., Ltd., and a decrease of $354,353 in writing off a receivable due from Shaanxi Changfa Industrial Co., Ltd.

LIQUIDITY AND CAPITAL RESOURCES

Cash Flows From Operating Activities

Net cash used in operating activities of $133,138 for the year ended December 31, 2015 was primarily attributable to allowance for doubtful accounts of $4,171,598 occurred in 2015. The adjustments to reconcile our net loss to net cash flow mainly include depreciation and amortization expense of $464,891, imputed expense of $97,164, an increase in due from related party of $16,718, a decrease in operating liability of $200,180, and a decrease in other current assets and prepayment of $5,829.

Net cash used in operating activities of $204,019 for the year ended December 31, 2014 was primarily attributable to its outstanding receivable from related parties of $1,247,273 occurred in 2014. The adjustments to reconcile our net income to net cash flow mainly include depreciation and amortization expense of $471,851, allowance for double accounts of $46,374, an increase in operating liability of $68,568, and a decrease in other current assets and prepayment of $27,416.

Cash Flows From Investing Activities

There is no cash flow in investing activities for the year ended December 31, 2015

Net cash provided by investing activities of $80,683 for the year ended December 31, 2014 was incurred from the decreased balance of due from related parties.

| 22 |

Cash Flows From Financing Activities

Net cash provided by financing activities of $68,426 for the year ended December 31, 2015 was the proceeds from related parties.

Net cash provided by financing activities of $31,404 for the year ended December 31, 2014 was the proceeds from related parties.

General

As in previous year, we have access to short and long term loans of cash from our directors or other related parties.

The Company borrowed $68,426 from related parties for the year ended December 31, 2015.

Our current assets decreased by $137,266 and total assets decreased by $6,899,617 respectively. The decreased current assets were resulted from our decrease in cash in bank and decrease in other current assets and prepayments as of December 31, 2015. And the decreased total assets were mainly due to the writing off receivables due from related parties.