Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended 30 September 2010 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to |

Commission file number 1-4534

AIR PRODUCTS AND CHEMICALS, INC.

| 7201 Hamilton Boulevard |

State of incorporation: Delaware | |

| Allentown, Pennsylvania, 18195-1501 |

I.R.S. identification number: 23-1274455 | |

| Tel. (610) 481-4911 |

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: |

Registered on: | |

| Common Stock, par value $1.00 per share |

New York | |

| Preferred Stock Purchase Rights |

New York |

Securities registered pursuant to Section 12(g) of the Act: None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. |

YES x NO ¨ |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. |

YES ¨ NO x |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

YES x NO ¨ |

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). |

YES x NO ¨ |

| Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. |

x |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). |

YES ¨ NO x |

The aggregate market value of the voting stock held by non-affiliates of the registrant on 31 March 2010 was approximately $15.7 billion. For purposes of the foregoing calculations all directors and/or executive officers have been deemed to be affiliates, but the registrant disclaims that any such director and/or executive officer is an affiliate.

The number of shares of common stock outstanding as of 15 November 2010 was 214,275,258.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2011 Annual Meeting of Shareholders are incorporated by reference into Part III.

Table of Contents

AIR PRODUCTS AND CHEMICALS, INC.

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended 30 September 2010

TABLE OF CONTENTS

2

Table of Contents

PART I

| ITEM 1. | BUSINESS |

General Description of Business and Fiscal Year 2010 Developments

Air Products and Chemicals, Inc. (the Company or Air Products), a Delaware corporation originally founded in 1940, serves technology, energy, industrial, and healthcare customers globally with a unique portfolio of products, services, and solutions that include atmospheric gases, process and specialty gases, performance materials, equipment, and services. The Company is the world’s largest supplier of hydrogen and helium and has built leading positions in growth markets such as semiconductor materials, refinery hydrogen, natural gas liquefaction, and advanced coatings and adhesives. As used in this report, unless the context indicates otherwise, the term “Company” includes subsidiaries and predecessors of the registrant and its subsidiaries.

On 11 February 2010, Air Products Distribution, Inc. (Purchaser), a wholly owned subsidiary of Air Products, commenced a cash tender offer for all the outstanding shares of common stock of Airgas, Inc. (Airgas) not already owned by Air Products. Airgas is the largest U.S. distributor of packaged industrial, medical, and specialty gases, and associated hard goods such as welding equipment. The offer is scheduled to expire at midnight, New York City time, on Friday, 3 December 2010, unless further extended.

The Company manages its operations, assesses performance, and reports earnings under four business segments: Merchant Gases, Tonnage Gases, Electronics and Performance Materials, and Equipment and Energy.

Financial Information about Segments

Financial information concerning the Company’s four business segments appears in Note 25, Business Segment and Geographic Information, to the consolidated financial statements, included under Item 8 herein.

Narrative Description of Business by Segments

Merchant Gases

Merchant Gases sells atmospheric gases such as oxygen, nitrogen, and argon (primarily recovered by the cryogenic distillation of air); process gases such as hydrogen and helium (purchased or refined from crude helium); and medical and specialty gases, along with certain services and equipment, throughout the world to customers in many industries, including those in metals, glass, chemical processing, food processing, healthcare, steel, general manufacturing, and petroleum and natural gas industries.

Merchant Gases includes the following types of products:

Liquid bulk—Product is delivered in bulk (in liquid or gaseous form) by tanker or tube trailer and stored, usually in its liquid state, in equipment designed and installed by the Company at the customer’s site for vaporizing into a gaseous state as needed. Liquid bulk sales are typically governed by three- to five-year contracts.

Packaged gases—Small quantities of product are delivered in either cylinders or dewars. The Company operates packaged gas businesses in Europe, Asia, and Brazil. In the United States, the Company’s current packaged gas business sells products only for the electronics and magnetic resonance imaging (principally helium) industries.

Small on-site plants—Customers receive product through small on-sites (cryogenic or noncryogenic generators), either by a sale of gas contract or the sale of the equipment to the customer.

Healthcare products—Customers receive respiratory therapies, home medical equipment, and infusion services. These products and services are provided to patients in their homes, primarily in Europe. The Company has leading market positions in Spain, Portugal, and the United Kingdom, and in Mexico through its equity affiliate.

Electric power is the largest cost component in the production of atmospheric gases—oxygen, nitrogen, and argon. Natural gas is also an energy source at a number of the Company’s Merchant Gases facilities. The Company mitigates energy and natural gas price increases through pricing formulas and surcharges. A shortage or interruption of electricity or natural gas supply, or a price increase that cannot be passed through to customers, possibly for competitive reasons, may adversely affect the operations or results of Merchant Gases. During fiscal year 2010, no significant difficulties were encountered in obtaining adequate supplies of energy or raw materials.

Merchant Gases competes worldwide against three global industrial gas companies: L’Air Liquide S.A.; Linde AG; Praxair, Inc.; and several regional sellers (including Airgas, primarily with respect to liquid bulk sales). Competition in industrial gases is based primarily on price, reliability of supply, and the development of industrial gas applications.

3

Table of Contents

Competition in the healthcare business involves price, quality, service, and reliability of supply. In Europe, primary healthcare competitors include the same three global industrial gas companies mentioned previously, as well as smaller regional service providers. In some countries such as Spain and the United Kingdom, the Company tenders for significant parts of the healthcare business with government agencies and is expecting to participate in tenders in some countries over the coming fiscal year.

Merchant Gases sales constituted 41% of the Company’s consolidated sales in fiscal year 2010, 44% in fiscal year 2009, and 40% in fiscal year 2008. Sales of atmospheric gases (oxygen, nitrogen, and argon) constituted approximately 20% of the Company’s consolidated sales in fiscal year 2010, 21% in fiscal year 2009, and 18% in fiscal year 2008.

Tonnage Gases

Tonnage Gases provides hydrogen, carbon monoxide, nitrogen, oxygen, and syngas principally to the energy production and refining, chemical, and metallurgical industries worldwide. Gases are produced at large facilities located adjacent to customers’ facilities or by pipeline systems from centrally located production facilities and are generally governed by contracts with 15- to 20-year terms. The Company is the world’s largest provider of hydrogen, which is used by oil refiners to facilitate the conversion of heavy crude feedstock and lower the sulfur content of gasoline and diesel fuels to reduce smog and ozone depletion. The energy production industry uses nitrogen injection for enhanced recovery of oil and natural gas and oxygen for gasification. The metallurgical industry uses nitrogen for inerting and oxygen for the manufacture of steel and certain nonferrous metals. The chemical industry uses hydrogen, oxygen, nitrogen, carbon monoxide, and synthesis gas (a hydrogen-carbon monoxide mixture) as feedstocks in the production of many basic chemicals. The Company delivers product through pipelines from centrally located facilities in or near the Texas Gulf Coast; Louisiana; Los Angeles, California; Alberta, Canada; Rotterdam, the Netherlands; Southern England, U.K.; Northern England, U.K.; Western Belgium; Ulsan, Korea; Nanjing, China; Tangshan, China; Kuan Yin, Taiwan; Singapore; and Camaçari, Brazil. The Company also owns less than controlling interests in pipelines located in Thailand and South Africa.

Tonnage Gases also includes a Polyurethane Intermediates (PUI) business. At its Pasadena, Texas facility, the Company produces dinitrotoluene (DNT), which is converted to toluene diamine (TDA) and sold for use as an intermediate in the manufacture of a major precursor of flexible polyurethane foam used in furniture cushioning, carpet underlay, bedding, and seating in automobiles. Most of the Company’s TDA is sold under long-term contracts with raw material cost and currency pass-through to a small number of customers. The Company employs proprietary technology and scale of production to differentiate its polyurethane intermediates from those of its competitors.

Natural gas is the principal raw material for hydrogen, carbon monoxide, and synthesis gas production. Electric power is the largest cost component in the production of atmospheric gases. The Company mitigates energy and natural gas price increases through long-term cost pass-through contracts. Toluene, ammonia, and hydrogen are the principal raw materials for the PUI business and are purchased from various suppliers under multiyear contracts. During fiscal year 2010, no significant difficulties were encountered in obtaining adequate supplies of energy or raw materials.

Tonnage Gases competes in the United States and Canada against three global industrial gas companies: L’Air Liquide S.A.; Linde AG; Praxair, Inc.; and several regional competitors. Competition is based primarily on price, reliability of supply, the development of applications that use industrial gases, and, in some cases, provision of other services or products such as power and steam generation. The Company also derives a competitive advantage from its pipeline networks, which enable it to provide a reliable and economic supply of products to customers. Similar competitive situations exist in the European and Asian industrial gas markets where the Company competes against the three global companies as well as regional competitors. Global competitors for the PUI business are primarily BASF Corporation and Bayer AG.

Tonnage Gases sales constituted approximately 32% of the Company’s consolidated sales in fiscal year 2010, 31% in fiscal year 2009, and 34% in fiscal year 2008. Tonnage Gases hydrogen sales constituted approximately 15% of the Company’s consolidated sales in both fiscal year 2010 and 2009, and 17% in fiscal year 2008.

Electronics and Performance Materials

Electronics and Performance Materials employs applications technology to provide solutions to a broad range of global industries through chemical synthesis, analytical technology, process engineering, and surface science. This segment provides the electronics industry with specialty gases (such as nitrogen trifluoride, silane, arsine, phosphine, white ammonia, silicon tetrafluoride, carbon tetrafluoride, hexafluoromethane, critical etch gases, and tungsten hexafluoride) as well as tonnage gases (primarily nitrogen), specialty chemicals, services, and equipment for the

4

Table of Contents

manufacture of silicon and compound semiconductors, thin film transistor liquid crystal displays, and photovoltaic devices. These products are delivered through various supply chain methods, including bulk delivery systems or distribution by pipelines such as those located in California’s Silicon Valley; Phoenix, Arizona; Tainan, Taiwan; Gumi and Giheung, Korea; and Tianjin and Shanghai, China.

Electronics and Performance Materials also provides performance materials for a wide range of products, including coatings, inks, adhesives, civil engineering, personal care, institutional and industrial cleaning, mining, oil refining, and polyurethanes, and focuses on the development of new materials aimed at providing unique functionality to emerging markets. Principal performance materials include polyurethane catalysts and other additives for polyurethane foam, epoxy amine curing agents, and auxiliary products for epoxy systems, specialty surfactants for formulated systems, and functional additives for industrial cleaning and mining industries.

The Electronics and Performance Materials segment uses a wide variety of raw materials, including silane, amines, alcohols, epoxides, organic acids, and ketones. During fiscal year 2010, no significant difficulties were encountered in obtaining adequate supplies of energy or raw materials.

The Electronics and Performance Materials segment faces competition on a product-by-product basis against competitors ranging from niche suppliers with a single product to larger and more vertically integrated companies. Competition is principally conducted on the basis of price, quality, product performance, reliability of product supply, technical innovation, service, and global infrastructure.

Total sales from Electronics and Performance Materials constituted approximately 21% of the Company’s consolidated sales in fiscal year 2010, 19% in fiscal year 2009, and 21% in fiscal year 2008.

Equipment and Energy

Equipment and Energy designs and manufactures cryogenic equipment for air separation, hydrocarbon recovery and purification, natural gas liquefaction (LNG), and helium distribution (cryogenic transportation containers), and serves energy markets in a variety of ways.

Equipment is sold globally to customers in the chemical and petrochemical manufacturing, oil and gas recovery and processing, and steel and primary metals processing industries. The segment also provides a broad range of plant design, engineering, procurement, and construction management services to its customers.

Energy markets are served through the Company’s operation and partial ownership of cogeneration and flue gas desulfurization facilities, its development of hydrogen as an energy carrier, and oxygen-based technologies to serve energy markets in the future. The Company owns and operates a cogeneration facility in Calvert City, Kentucky and a 49-megawatt fluidized-bed coal and biomass-fired power generation facility in Stockton, California; and operates and owns a 47.9% interest in a 112-megawatt gas-fueled power generation facility in Thailand. The Company also operates and owns a 50% interest in a flue gas desulfurization facility in Indiana.

Steel, aluminum, and capital equipment subcomponents (compressors, etc.) are the principal raw materials in the equipment portion of this segment. Adequate raw materials for individual projects are acquired under firm purchase agreements. Coal, petroleum coke, and natural gas are the largest cost components in the production of energy. The Company mitigates these cost components, in part, through long-term cost pass-through contracts. During fiscal year 2010, no significant difficulties were encountered in obtaining adequate supplies of raw materials.

Equipment and Energy competes with a great number of firms for all of its offerings except LNG heat exchangers, for which there are fewer competitors due to the limited market size and proprietary technologies. Competition is based primarily on technological performance, service, technical know-how, price, and performance guarantees.

The backlog of equipment orders (including letters of intent believed to be firm) from third-party customers (including equity affiliates) was approximately $274 million on 30 September 2010, approximately 30% of which is for cryogenic equipment and 50% of which is for LNG heat exchangers, as compared with a total backlog of approximately $239 million on 30 September 2009. The Company expects that approximately $250 million of the backlog on 30 September 2010 will be completed during fiscal year 2011.

5

Table of Contents

Narrative Description of the Company’s Business Generally

The Company, through subsidiaries, affiliates, and minority-owned ventures, conducts business in over 40 countries outside the United States. Its international businesses are subject to risks customarily encountered in foreign operations, including fluctuations in foreign currency exchange rates and controls; import and export controls; and other economic, political, and regulatory policies of local governments.

The Company has majority or wholly owned foreign subsidiaries that operate in Canada, 17 European countries (including the United Kingdom and Spain), nine Asian countries (including China, Korea, Singapore, and Taiwan), and four Latin American countries (including Mexico and Brazil). The Company also owns less-than-controlling interests in entities operating in Europe, Asia, Africa, the Middle East, and Latin America (including Italy, Germany, China, India, Singapore, Thailand, South Africa, and Mexico).

Financial information about the Company’s foreign operations and investments is included in Notes 8, Summarized Financial Information of Equity Affiliates; 22, Income Taxes; and 25, Business Segment and Geographic Information, to the consolidated financial statements included under Item 8 herein. Information about foreign currency translation is included under “Foreign Currency” in Note 1, Major Accounting Policies, and information on the Company’s exposure to currency fluctuations is included in Note 13, Financial Instruments, to the consolidated financial statements, included under Item 8 below, and in “Foreign Currency Exchange Rate Risk,” included under Item 7A below. Export sales from operations in the United States to unconsolidated customers amounted to $570.5 million, $510.2 million, and $629.1 million in fiscal years 2010, 2009, and 2008, respectively. Total export sales in fiscal year 2010 included $387.8 million in export sales to affiliated customers. The sales to affiliated customers were primarily equipment sales within the Equipment and Energy segment and the Electronic and Performance Materials segment.

Technology Development

The Company pursues a market-oriented approach to technology development through research and development, engineering, and commercial development processes. It conducts research and development principally in its laboratories located in the United States (Trexlertown, Pennsylvania; Carlsbad, California; Milton, Wisconsin; and Phoenix, Arizona); the United Kingdom (Basingstoke, London, and Carrington); Germany (Hamburg); the Netherlands (Utrecht); Spain (Barcelona); and Asia (Tokyo, Japan; Shanghai, China; Giheung, Korea; and Chubei, Taiwan). The Company also funds and cooperates in research and development programs conducted by a number of major universities and undertakes research work funded by others—principally the United States government.

The Company’s corporate research groups, which include science and process technology centers, support the research efforts of various businesses throughout the Company. Technology development efforts for use within Merchant Gases, Tonnage Gases, and Equipment and Energy focus primarily on new and improved processes and equipment for the production and delivery of industrial gases and new or improved applications for all such products. Research and technology development for Electronics and Performance Materials supports development of new products and applications to strengthen and extend the Company’s present positions. Work is also performed in Electronics and Performance Materials to lower processing costs and develop new processes for the new products.

Research and development expenditures were $114.7 million during fiscal year 2010, $116.3 million in fiscal year 2009, and $130.7 million in fiscal year 2008. The Company expended $23.9 million on customer-sponsored research activities during fiscal year 2010, $29.7 million in fiscal year 2009, and $24.8 million in fiscal year 2008.

As of 1 November 2010, the Company owns 932 United States patents, 2,808 foreign patents, and is a licensee under certain patents owned by others. While the patents and licenses are considered important, the Company does not consider its business as a whole to be materially dependent upon any particular patent, patent license, or group of patents or licenses.

Environmental Controls

The Company is subject to various environmental laws and regulations in the countries in which it has operations. Compliance with these laws and regulations results in higher capital expenditures and costs. From time to time, the Company is involved in proceedings under the Comprehensive Environmental Response, Compensation, and Liability Act (the federal Superfund law), similar state laws, and the Resource Conservation and Recovery Act (RCRA) relating to the designation of certain sites for investigation and possible cleanup. Additional information with respect to these proceedings is included under Item 3, Legal Proceedings, below. The Company’s accounting policy for environmental expenditures is discussed in Note 1, Major Accounting Policies, and environmental loss contingencies are discussed in Note 17, Commitments and Contingencies, to the consolidated financial statements, included under Item 8, below.

6

Table of Contents

The amounts charged to income from continuing operations related to environmental matters totaled $31.6 million in fiscal 2010, $52.5 million in 2009, and $49.9 million in 2008. These amounts represent an estimate of expenses for compliance with environmental laws, remedial activities, and activities undertaken to meet internal Company standards. Future costs are not expected to be materially different from these amounts. The 2009 amount included a charge of $16.0 for the Paulsboro site. Refer to Note 17, Commitments and Contingencies, to the consolidated financial statements for additional information on this charge. The 2008 amount included revised cost estimates for several existing sites.

Although precise amounts are difficult to determine, the Company estimates that in both fiscal year 2010 and 2009, it spent approximately $6 million on capital projects to control pollution. Capital expenditures to control pollution in future years are estimated at approximately $6 million in both fiscal year 2011 and 2012. The cost of any environmental compliance generally is contractually passed through to the customer.

The Company accrues environmental investigatory and remediation costs for identified sites when it is probable that a liability has been incurred and the amount of loss can be reasonably estimated. The potential exposure for such costs is estimated to range from $87 million to a reasonably possible upper exposure of $101 million. The accrual on the consolidated balance sheet for 30 September 2010 was $87.0 million and for 30 September 2009 was $95.0 million. Actual costs to be incurred in future periods may vary from the estimates, given inherent uncertainties in evaluating environmental exposures. Subject to the imprecision in estimating future environmental costs, the Company does not expect that any sum it may have to pay in connection with environmental matters in excess of the amounts recorded or disclosed above would have a materially adverse effect on its financial condition or results of operations in any one year.

Employees

On 30 September 2010, the Company (including majority-owned subsidiaries) had approximately 18,300 employees, of whom approximately 17,900 were full-time employees and of whom approximately 11,000 were located outside the United States. The Company has collective bargaining agreements with unions at various locations that expire on various dates over the next four years. The Company considers relations with its employees to be satisfactory and does not believe that the impact of any expiring or expired collective bargaining agreements will result in a material adverse impact on the Company.

Available Information

All periodic and current reports, registration statements, and other filings that the Company is required to file with the Securities and Exchange Commission (SEC), including the Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934 (the 1934 Act Reports), are available free of charge through the Company’s Internet website at www.airproducts.com. Such documents are available as soon as reasonably practicable after electronic filing of the material with the SEC. All 1934 Act Reports filed during the period covered by this report were available on the Company’s website on the same day as filing.

The public may also read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy, and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

Seasonality

Although none of the four business segments are subject to seasonal fluctuations to any material extent, the Electronics and Performance Materials segment is susceptible to the cyclical nature of the electronics industry and to seasonal fluctuations in underlying end-use performance materials markets.

Working Capital

The Company maintains inventory where required to facilitate the supply of products to customers on a reasonable delivery schedule. Merchant Gases inventory consists primarily of industrial, medical, specialty gas, and crude helium inventories supplied to customers through liquid bulk and packaged gases supply modes. Merchant Gases inventory also includes home medical equipment to serve healthcare patients. Electronics inventories consist primarily of bulk and packaged specialty gases and chemicals and also include inventories to support sales of equipment and services. Performance Materials inventories consist primarily of bulk and packaged performance chemical solutions. The Tonnage Gases inventory is primarily Polyurethane Intermediates raw materials and finished goods; the remaining on-site plants and pipeline complexes have limited inventory. Equipment and Energy has limited inventory.

7

Table of Contents

Customers

The Company does not have a homogeneous customer base or end market, and no single customer accounts for more than 10% of the Company’s consolidated revenues. The Company and the Tonnage Gases and Electronics and Performance Materials segments do have concentrations of customers in specific industries, primarily refining, chemicals, and electronics. Within each of these industries, the Company has several large-volume customers with long-term contracts. A negative trend affecting one of these industries, or the loss of one of these major customers, although not material to the Company’s consolidated revenues, could have an adverse impact on the affected segment.

Governmental Contracts

No segment’s business is subject to a government entity’s renegotiation of profits or termination of contracts that would be material to the Company’s business as a whole.

Executive Officers of the Company

The Company’s executive officers and their respective positions and ages on 15 November 2010 follow. Information with respect to offices held is stated in fiscal years.

| Name | Age | Office | ||||

| M. Scott Crocco | 46 | Vice President and Corporate Controller (became Vice President in 2008; Corporate Controller in 2007; and Director of Corporate Decision Support in 2003) | ||||

| Robert D. Dixon (A) |

51 | Senior Vice President and General Manager – Merchant Gases (became Senior Vice President in 2008; Vice President and General Manager – Merchant Gases in 2007; President – Air Products Asia in 2003; and Vice President – Air Products Asia in 2003) | ||||

| Paul E. Huck (A) |

60 | Senior Vice President and Chief Financial Officer (became Senior Vice President in 2008; Vice President and Chief Financial Officer in 2004) | ||||

| Stephen J. Jones (A) |

49 | Senior Vice President and General Manager, Tonnage Gases, Equipment and Energy (became Senior Vice President and General Manager, Tonnage Gases, Equipment and Energy in 2009; Senior Vice President, General Counsel and Secretary in 2008; Vice President and Associate General Counsel in 2007; and Vice President and General Manager – Industrial Chemicals Division in 2003) | ||||

| John W. Marsland (A) |

44 | Senior Vice President, Supply Chain (became Senior Vice President, Supply Chain in 2010; Vice President and General Manager, Global Liquid Bulk, Generated Gases and Helium in 2009; Vice President – Business Services in 2009; Vice President and General Manager – Healthcare in 2007; Vice President and General Manager, Global Healthcare in 2005) | ||||

| John E. McGlade (A)(B)(C) |

56 | Chairman, President, and Chief Executive Officer (became Chairman and Chief Executive Officer in 2008; President and Chief Operating Officer in 2006; Group Vice President – Chemicals in 2003) | ||||

| Lynn C. Minella (A) |

52 | Senior Vice President – Human Resources and Communications (became Senior Vice President – Human Resources and Communications in 2008; Vice President – Human Resources in 2004) | ||||

8

Table of Contents

| Name | Age | Office | ||||

| John D. Stanley (A) |

52 | Senior Vice President and General Counsel (became Senior Vice President and General Counsel in 2009; Assistant General Counsel, Americas and Europe in 2007; Assistant General Counsel, Corporate and Commercial in 2004) | ||||

| (A) | Member, Corporate Executive Committee |

| (B) | Member, Board of Directors |

| (C) | Member, Executive Committee of the Board of Directors |

| ITEM 1A. | RISK FACTORS |

You should read the following risk factors carefully in conjunction with evaluating our business and the forward-looking information contained in this Annual Report on Form 10-K. Any of the following risks could have a materially adverse effect on our business, operating results, financial condition, and the actual outcome of matters as to which forward-looking statements are made in this Annual Report on Form 10-K. While we believe we have identified and discussed below the key risk factors affecting our business, there may be additional risks and uncertainties that are not presently known or that are not currently believed to be significant that may adversely affect our business, performance, or financial condition in the future.

Overall Economic Conditions—Sluggish general economic conditions in certain markets in which the Company does business may decrease the demand for its goods and services and adversely impact its revenues, operating results, and cash flow.

Demand for the Company’s products and services depends in part on the general economic conditions affecting the countries and industries in which the Company does business. Recently, sluggish economic conditions in the U.S. and Europe and in certain industries served by the Company have impacted and may in the future impact demand for the Company’s products and services, in turn negatively impacting the Company’s revenues and earnings. While markets have stabilized relative to the extreme economic contraction in 2008—2009, industry utilization rates and therefore pricing pressure continue to be risks. Excess capacity in the Company’s or its competitors’ manufacturing facilities could decrease the Company’s ability to maintain pricing and generate profits. Unanticipated contract terminations or project delays by current customers can also negatively impact financial results.

Asset Impairments—The Company may be required to record impairment on its long-lived assets.

Weak demand may cause underutilization of the Company’s manufacturing capacity or elimination of product lines; contract terminations or customer shutdowns may force sale or abandonment of facilities and equipment; contractual provisions may allow customer buyout of facilities or equipment; or other events associated with weak economic conditions or specific end market, product, or customer events may require the Company to record an impairment on tangible assets, such as facilities and equipment, as well as intangible assets, such as intellectual property or goodwill, which would have a negative impact on its financial results.

Competition—Inability to compete effectively in a segment could adversely impact sales and financial performance.

The Company faces strong competition from several large global competitors and many smaller regional ones in all of its business segments. Introduction by competitors of new technologies, competing products, or additional capacity could weaken demand for or impact pricing of the Company’s products, negatively impacting financial results. In addition, competitors’ pricing policies could materially affect the Company’s profitability or its market share.

Raw Material and Energy Cost and Availability—Interruption in ordinary sources of supply or an inability to recover increases in energy and raw material costs from customers could result in lost sales or reduced profitability.

Energy, including electricity, natural gas, and diesel fuel for delivery trucks, is the largest cost component of the Company’s business. Because the Company’s industrial gas facilities use substantial amounts of electricity, energy price fluctuations could materially impact the Company’s revenues and earnings. Hydrocarbons, including natural gas, are the primary feedstock for the production of hydrogen, carbon monoxide, and synthesis gas. The Electronics and Performance Materials segment uses a wide variety of raw materials, including alcohols, ethyleneamines,

9

Table of Contents

cyclohexylamine, acrylonitriles, and glycols. Shortages or price escalation in these materials could negatively impact financial results. A disruption in the supply of energy and raw materials, whether due to market conditions, legislative or regulatory actions, natural events, or other disruption, could prevent the Company from meeting its contractual commitments, harming its business and financial results.

The Company typically contracts to pass through cost increases in energy and raw materials to its customers, but cost variability can still have a negative impact on its results. The Company may not be able to raise prices as quickly as costs rise, or competitive pressures may prevent full recovery. Increases in energy or raw material costs that cannot be passed on to customers for competitive or other reasons would negatively impact the Company’s revenues and earnings. Even where costs are passed through, price increases can cause lower sales volume.

Regulatory Compliance—The Company is subject to extensive government regulation in jurisdictions around the globe in which it does business. Changes in regulations addressing, among other things, environmental compliance, import/export restrictions, and taxes, can negatively impact the Company’s operations and financial results.

The Company is subject to government regulation in the United States and foreign jurisdictions in which it conducts its business. The application of laws and regulations to the Company’s business is sometimes unclear. Compliance with laws and regulations may involve significant costs or require changes in business practice that could result in reduced profitability. Determination of noncompliance can result in penalties or sanctions that could also impact financial results. Compliance with changes in laws or regulations can require additional capital expenditures or increase operating costs. Export controls or other regulatory restrictions could prevent the Company from shipping its products to and from some markets or increase the cost of doing so. This area continues to attract external focus by multiple customs and export enforcement authorities. Changes in tax laws and regulations and international tax treaties could affect the financial results of the Company’s businesses.

Greenhouse Gases—Legislative and regulatory responses to global climate change create financial risk.

Some of the Company’s operations are within jurisdictions that have, or are developing, regulatory regimes governing emissions of greenhouse gases (GHG). These include existing and expanding coverage under the European Union Emissions Trading Scheme; mandatory reporting and reductions at manufacturing facilities in Alberta, Canada; and mandatory reporting and anticipated constraints on GHG emissions in California and Ontario. In addition, the U.S. Environmental Protection Agency has taken preliminary actions towards regulating greenhouse gas emissions. Increased public awareness and concern may result in more international, U.S. federal, and/or regional requirements to reduce or mitigate the effects of GHG. Although uncertain, these developments could increase the Company’s costs related to consumption of electric power, hydrogen production, and fluorinated gases production. The Company believes it will be able to mitigate some of the potential increased cost through its contractual terms, but the lack of definitive legislation or regulatory requirements prevents accurate estimate of the long-term impact on the Company. Any legislation that limits or taxes GHG emissions could impact the Company’s growth, increase its operating costs, or reduce demand for certain of its products.

Environmental Compliance—Costs and expenses resulting from compliance with environmental regulations may negatively impact the Company’s operations and financial results.

The Company is subject to extensive federal, state, local, and foreign environmental and safety laws and regulations concerning, among other things, emissions in the air, discharges to land and water, and the generation, handling, treatment, and disposal of hazardous waste and other materials. The Company takes its environmental responsibilities very seriously, but there is a risk of environmental impact inherent in its manufacturing operations and transportation of chemicals. Future developments and more stringent environmental regulations may require the Company to make additional unforeseen environmental expenditures. In addition, laws and regulations may require significant expenditures for environmental protection equipment, compliance, and remediation. These additional costs may adversely affect financial results. For a more detailed description of these matters, see “Narrative Description of the Company’s Business Generally—Environmental Controls,” above.

Foreign Operations, Political, and Legal Risks—The Company’s foreign operations can be adversely impacted by nationalization or expropriation of property, undeveloped property rights, and legal systems or political instability.

The Company’s operations in certain foreign jurisdictions are subject to nationalization and expropriation risk, and some of its contractual relationships within these jurisdictions are subject to cancellation without full compensation for loss. Economic and political conditions within foreign jurisdictions, social unrest, or strained relations between

10

Table of Contents

countries can cause fluctuations in demand, price volatility, supply disruptions, or loss of property. The occurrence of any of these risks could have a material, adverse impact on the Company’s operations and financial results.

Interest Rate Increases—The Company’s earnings, cash flow, and financial position can be impacted by interest rate increases.

At 30 September 2010, the Company had total consolidated debt of $4,128.3 million, of which $468.5 million will mature in the next twelve months. The Company expects to continue to incur indebtedness to fund new projects and replace maturing debt. Although the Company actively manages its interest rate risk through the use of derivatives and diversified debt obligations, not all borrowings at variable rates are hedged, and new debt will be priced at market rates. If interest rates increase, the Company’s interest expense could increase significantly, affecting earnings and reducing cash flow available for working capital, capital expenditures, acquisitions, and other purposes. In addition, changes by any rating agency to the Company’s outlook or credit ratings could increase the Company’s cost of borrowing.

Currency Fluctuations—Changes in foreign currencies may adversely affect the Company’s financial results.

A substantial amount of the Company’s sales are derived from outside the United States and denominated in foreign currencies. The Company also has significant production facilities which are located outside of the United States. Financial results therefore will be affected by changes in foreign currency rates. The Company uses certain financial instruments to mitigate these effects, but it is not cost-effective to hedge foreign currency exposure in a manner that would entirely eliminate the effects of changes in foreign exchange rates on earnings, cash flows, and fair values of assets and liabilities. Accordingly, reported sales, net earnings, cash flows, and fair values have been and in the future will be affected by changes in foreign exchange rates. For a more detailed discussion of currency exposure, see Item 7A, below.

Pension Liabilities—The Company’s results of operations and financial condition could be negatively impacted by its U.S. and non-U.S. pension plans.

Adverse equity market conditions and volatility in the credit markets have had and may continue to have an unfavorable impact on the value of the Company’s pension trust assets and its future estimated pension liabilities, significantly affecting the net periodic benefit costs of its pension plans and ongoing funding requirements for these plans. As a result, the Company’s financial results and cash flow in any period could be negatively impacted. For information about potential impacts from pension funding and the use of certain assumptions regarding pension matters, see the discussion in Note 16, Retirement Benefits, to the consolidated financial statements, included in Item 8, below.

Catastrophic Events—Catastrophic events could disrupt the Company’s operations or the operations of its suppliers or customers, having a negative impact on the Company’s business, financial results, and cash flow.

The Company’s operations could be impacted by catastrophic events outside the Company’s control, including severe weather conditions such as hurricanes, floods, earthquakes, and storms, or acts of war and terrorism. Any such event could cause a serious business disruption that could affect the Company’s ability to produce and distribute its products and possibly expose it to third-party liability claims. Additionally, such events could impact the Company’s suppliers, in which event energy and raw materials may be unavailable to the Company, or its customers may be unable to purchase or accept the Company’s products and services. Any such occurrence could have a negative impact on the Company’s operations and financial results.

Operational Risks—Operational and execution risks may adversely affect the Company’s operations or financial results.

The Company’s operation of its facilities, pipelines, and delivery systems inherently entails hazards that require continuous oversight and control, such as pipeline leaks and ruptures, fire, explosions, toxic releases, mechanical failures, or vehicle accidents. If operational risks materialize, they could result in loss of life, damage to the environment, or loss of production, all of which could negatively impact the Company’s ongoing operations, financial results, and cash flow. In addition, the Company’s operating results are dependent on the continued operation of its production facilities and its ability to meet customer requirements. The Company’s operating facilities for the production of certain product lines, primarily in certain electronic materials products, are highly concentrated. Insufficient capacity may expose the Company to liabilities related to contract commitments. Operating results are also dependent on the Company’s ability to complete new construction projects on time, on budget, and in accordance with performance requirements. Failure to do so may expose the Company to loss of revenue, potential litigation, and loss of business reputation.

11

Table of Contents

Information Security—The security of the Company’s Information Technology systems could be compromised, which could adversely affect its ability to operate.

The Company utilizes a global enterprise resource planning (ERP) system and other technologies for the distribution of information both within the Company and to customers and suppliers. The ERP system and other technologies are potentially vulnerable to interruption from viruses, hackers, or system breakdown. To mitigate these risks, the Company has implemented a variety of security measures, including virus protection, redundancy procedures, and recovery processes. A significant system interruption, however, could materially affect the Company’s operations, business reputation, and financial results.

Litigation and Regulatory Proceedings—The Company’s financial results may be affected by various legal and regulatory proceedings, including those involving antitrust, environmental, or other matters.

The Company is subject to litigation and regulatory proceedings in the normal course of business and could become subject to additional claims in the future, some of which could be material. The outcome of existing legal proceedings may differ from the Company’s expectations because the outcomes of litigation, including regulatory matters, are often difficult to predict reliably. Various factors or developments can lead the Company to change current estimates of liabilities and related insurance receivables, where applicable, or make such estimates for matters previously not susceptible to reasonable estimates, such as a significant judicial ruling or judgment, a significant settlement, significant regulatory developments, or changes in applicable law. A future adverse ruling, settlement, or unfavorable development could result in charges that could have a materially adverse effect on the Company’s results of operations in any particular period. For a more detailed discussion of the legal proceedings involving the Company, see Item 3, below.

Recruiting and Retaining Employees—Inability to attract, retain, or develop skilled employees could adversely impact the Company’s business.

Sustaining and growing the Company’s business depends on the recruitment, development, and retention of qualified employees. Demographic trends and changes in the geographic concentration of global businesses have created more competition for talent. The inability to attract, develop, or retain quality employees could negatively impact the Company’s ability to take on new projects and sustain its operations, which might adversely affect the Company’s operations or its ability to grow.

Portfolio Management—The success of portfolio management activities is not predictable.

The Company continuously reviews and manages its portfolio of assets in order to maximize value for its shareholders. Portfolio management involves many variables, including future acquisitions and divestitures, restructurings and resegmentations, and cost-cutting and productivity initiatives. The timing, impact, and ability to complete such undertakings; the costs and financial charges associated with such activities; and the ultimate financial impact of such undertakings are uncertain and can have a negative short- or long-term impact on the Company’s operations and financial results.

RISK FACTORS RELATED TO THE TENDER OFFER FOR AIRGAS

If the Company is successful in acquiring Airgas, it will incur substantial transaction and merger-related costs.

If the Company is successful in its tender offer for Airgas (see Note 3, Airgas Transaction, to the consolidated financial statements for more information on this transaction), or otherwise succeeds in acquiring Airgas, it will incur substantial nonrecurring transaction and merger-related costs associated with the acquisition of Airgas, combining the operations of the two companies, and achieving desired synergies. Although the Company expects that the elimination of duplicative costs and the realization of other efficiencies related to the integration of the two businesses will offset the incremental transaction and merger-related costs, this net benefit may not be achieved when expected, or at all.

The Company will carry significantly more long-term debt obligations if the acquisition is completed.

At the current tender offer of $65.50 per share, the total value of the Airgas transaction would be approximately $7.4 billion, including $5.7 billion of equity and $1.7 billion of assumed debt. In connection with the tender offer, the Company has secured a $6.7 billion term loan credit facility (the “bridge loan”), and the Company expects to retain approximately $1 billion of existing Airgas debt. If the tender offer is successful, the Company intends to finance the acquisition primarily by issuing public debt securities. If the Company is unable to successfully market this debt issuance, the bridge loan will be drawn. The bridge loan carries a higher cost than is anticipated for the public debt.

12

Table of Contents

The issuance and assumption of this new debt will require a greater proportion of the Company’s cash flow from operations to service this debt than the Company has historically had to allocate to debt.

Changes in our credit ratings may have a negative impact on our financing costs in future periods.

The Company anticipates that the debt issuance to finance the acquisition of Airgas will result in a temporary downgrade of its credit ratings. The Company’s credit rating is a significant factor in determining pricing and availability of its debt. Changes in our credit ratings could increase our borrowing costs. In addition, our current short-term credit rating allows us to participate in a commercial paper market that has a large number of potential investors and a high degree of liquidity. A downgrade in our credit ratings, particularly our short-term credit rating, could likely reduce the amount of commercial paper we could issue, increase our commercial paper borrowing costs, or both. The Company expects that its credit rating would be restored to current levels within a few years following the potential acquisition; however, inability to achieve the anticipated benefits of the transaction or obtain projected prices for assets required to be divested, or other unexpected developments may delay this restoration.

If the acquisition is completed, we will be subject to integration and other risks.

If the Company is successful in acquiring Airgas, the success of the merger will depend, in part, on its ability to realize the anticipated benefits from combining the businesses. To realize these anticipated benefits, the Company must successfully integrate the operations and personnel of Airgas into our business. It is possible that the integration process could take longer than anticipated and could result in the loss of valuable employees or the disruption of each company’s ongoing businesses. Failure to achieve the anticipated benefits could result in increased costs or decreases in the amount of expected revenues and could adversely affect our future business, financial condition, and operating results. Additionally, if the acquisition is successful, the Company will be required to divest certain assets to comply with the Consent Decree approved by the U.S. Federal Trade Commission on 8 October 2010. Failure to find suitable buyers or obtain a reasonable price for the assets could adversely affect the financial condition of the Company.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

The Company has not received any written comments from the Commission staff that remain unresolved.

| ITEM 2. | PROPERTIES |

The Company owns its principal executive offices, which are located at its headquarters in Trexlertown, Pennsylvania, and also owns additional administrative offices in Hersham, England and in Hattingen, Germany. Its regional Asian administrative offices, which are leased, are located in Hong Kong; Shanghai, China; Taipei, Taiwan; Petaling Jaya, Malaysia; and Singapore. Additional administrative offices are leased in Ontario, Canada; Kawasaki, Japan; Seoul, Korea; Brussels, Belgium; Paris, France; Barcelona, Spain; Rotterdam, the Netherlands; São Paulo, Brazil; and Kempton Park, South Africa. Management believes the Company’s manufacturing facilities, described in more detail below, are adequate to support its businesses.

Following is a description of the properties used by the Company’s four business segments:

Merchant Gases

Merchant Gases currently operates over 150 facilities in North and South America (approximately 40 of which sites are owned); over 130 sites in Europe, including healthcare (approximately half of which sites are owned); and over 75 facilities in seven countries within Asia. Helium is recovered at sites in Kansas and Texas and distributed from several transfill sites in the U.S., Canada, Europe, and Asia. Sales support offices are located at its Trexlertown headquarters and in leased properties in three states, at all administrative sites in Europe, and at 15 sites in Asia. Research and development (R&D) activities for this segment are conducted in Trexlertown, Pennsylvania.

Tonnage Gases

Tonnage Gases operates over 50 plants in the United States and Canada that produce over 300 standard tons per day of product. Thirty-five of these facilities produce or recover hydrogen, many of which support the four major pipeline systems located along the Gulf Coast of Texas; on the Mississippi River corridor in Louisiana; in Los Angeles, California; and Alberta, Canada. The Tonnage Gases segment includes a facility in Pasadena, Texas that produces Polyurethane Intermediate products. The segment also operates over 20 tonnage plants in Europe and over 20 tonnage plants within Asia, the majority of which are on leasehold type long-term structured agreements. Sales support offices are located at the Company’s headquarters in Trexlertown, Pennsylvania and leased offices in Texas, Louisiana, California, and Calgary, Alberta in North America, as well as in Hersham, England; Rotterdam, the Netherlands; Shanghai, China; Singapore; and Doha, Qatar in the Middle East.

13

Table of Contents

Electronics and Performance Materials

The electronics business within the Electronics and Performance Materials segment produces, packages, and stores nitrogen, specialty gases, and electronic chemicals at over 44 sites in the United States (the majority of which are leased), nine facilities in Europe, and over 45 facilities in Asia (approximately half of which are located on customer sites).

The performance materials portion of this segment operates facilities in Los Angeles, California; Calvert City, Kentucky; Wichita, Kansas; Milton, Wisconsin; Reserve, Louisiana; Clayton, England; Marl, Germany; Singapore; Isehara, Japan; Changzhou, China and Nanjing, China. Substantially all of the Performance Materials properties are owned.

This segment has five field sales offices in the United States as well as sales offices in Europe, Taiwan, Korea, Singapore, and China, the majority of which are leased. The segment conducts R&D related activities at eight locations worldwide, including Trexlertown, Pennsylvania; Carlsbad, California; Utrecht, the Netherlands; Hamburg, Germany; Chubei, Taiwan; Giheung, South Korea; Shanghai, China; and Kawasaki, Japan.

Equipment and Energy

Equipment and Energy operates eight manufacturing plants and two sales offices in the U.S. The Company manufactures a significant portion of the world’s supply of LNG equipment at its Wilkes-Barre, Pennsylvania site. Air separation columns and cold boxes for Company-owned facilities and third-party sales are produced by operations in Istres, France; Caojing, China; as well as in the Wilkes-Barre facility when capacity is available. Cryogenic transportation containers for liquid helium are manufactured and reconstructed at facilities in eastern Pennsylvania and Liberal, Kansas. Offices in Hersham, England and Shanghai, China house Equipment commercial team members.

Electric power is produced at various facilities, including Stockton, California and Calvert City, Kentucky. Flue gas desulfurization operations are conducted at the Pure Air facility in Chesterton, Indiana. Additionally, the Company owns a 47.9% interest in a gas-fueled power generation facility in Thailand. The Company or its affiliates own approximately 50% of the real estate in this segment and lease the remaining 50%.

| ITEM 3. | LEGAL PROCEEDINGS |

In the normal course of business, the Company and its subsidiaries are involved in various legal proceedings, including contract, product liability, intellectual property, and insurance matters. Although litigation with respect to these matters is routine and incidental to the conduct of the Company’s business, such litigation could result in large monetary awards, especially if a civil jury is allowed to determine compensatory and/or punitive damages. However, the Company believes that litigation currently pending to which it is a party will be resolved without any materially adverse effect on its financial position, earnings, or cash flows.

The Company is also from time to time involved in certain competition, environmental, health, and safety proceedings involving governmental authorities. The Company is a party to proceedings under the Comprehensive Environmental Response, Compensation, and Liability Act (the federal Superfund law); the Resource Conservation and Recovery Act (RCRA); and similar state environmental laws relating to the designation of certain sites for investigation or remediation. Presently there are approximately 30 sites on which a final settlement has not been reached where the Company, along with others, has been designated a Potentially Responsible Party by the Environmental Protection Agency or is otherwise engaged in investigation or remediation, including cleanup activity at certain of its current or former manufacturing sites. The Company does not expect that any sums it may have to pay in connection with these matters would have a materially adverse effect on its consolidated financial position. Additional information on the Company’s environmental exposure is included under “Narrative Description of the Company’s Business Generally—Environmental Controls.”

In 2008, the U.S. Environmental Protection Agency made a referral to the U.S. Department of Justice concerning alleged violations of the Resource Conservation and Recovery Act (RCRA) related to sulfuric acid exchange at the Company’s Pasadena, Texas facility. The Company disputes the allegations, but has agreed to settle the matter for a $1.485 million civil penalty ($1.35 million to the United States and $135,000 to the State of Texas) and payment of $15,000 to the State of Texas for attorneys’ fees. The settlement was memorialized in a Consent Decree which was lodged with the U.S. District Court for the Southern District of Texas, Houston Division, on 25 August 2010 and entered on 29 October 2010.

14

Table of Contents

On 16 February 2010, an unplanned shutdown at the Company’s nitric acid plant in Pasadena, Texas resulted in the release of nitrogen dioxide and nitric acid into the atmosphere. In connection with the incident, the Company has been contacted by federal, state, and local environmental regulatory authorities, and the U.S. Occupational Safety and Health Administration. A complaint alleging various regulatory and air permit violations and seeking unspecified civil penalties, attorneys’ fees, and court costs has been filed by Harris County, Texas. At this time, the Company does not know whether any fines or penalties will be assessed; however, the Company expects that any resulting fines or penalties will be immaterial to its consolidated financial results.

In September 2010, the Brazilian Administrative Council for Economic Defense (CADE) issued a decision against the Company’s Brazilian subsidiary, Air Products Brasil Ltda., and several other Brazilian industrial gas companies for alleged anticompetitive activities. CADE imposed a civil fine of R$179.2 million on Air Products Brasil Ltda. This fine was based on a recommendation by a unit of the Brazilian Ministry of Justice whose investigation began in 2003, alleging violation of competition laws with respect to the sale of industrial and medical gases. The fines are based on a percentage of the Company’s total revenue in Brazil in 2003.

The Company has denied the allegations made by the authorities and filed an appeal in October 2010 to the Brazilian courts. Certain of the Company’s defenses, if successful, could result in the matter being dismissed with no fine against the Company. The Company, with advice of its outside legal counsel, has assessed the status of this matter and has concluded that although an adverse final judgment after exhausting all appeals is reasonably possible, such a judgment is not probable. As a result, no provision has been made in the consolidated financial statements.

While the Company does not expect that any sums it may have to pay in connection with these or any other legal proceeding would have a materially adverse effect on its consolidated financial position or net cash flows, a future charge for regulatory fines or damage awards could have a significant impact on the Company’s net income in the period in which it is recorded.

| ITEM 4. | RESERVED |

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES |

The Company’s common stock (ticker symbol APD) is listed on the New York Stock Exchange. Quarterly stock prices, as reported on the New York Stock Exchange composite tape of transactions, and dividend information for the last two fiscal years appear below. Cash dividends on the Company’s common stock are paid quarterly. The Company’s objective is to pay dividends consistent with the reinvestment of earnings necessary for long-term growth. It is the Company’s expectation that comparable cash dividends will continue to be paid in the future.

Quarterly Stock Information

| 2010 | High | Low | Close | Dividend | ||||||||||||

| First |

$85.44 | $73.76 | $81.06 | $.45 | ||||||||||||

| Second |

83.80 | 65.05 | 73.95 | .49 | ||||||||||||

| Third |

80.24 | 64.47 | 64.81 | .49 | ||||||||||||

| Fourth |

84.43 | 64.13 | 82.82 | .49 | ||||||||||||

| $1.92 | ||||||||||||||||

| 2009 | High | Low | Close | Dividend | ||||||||||||

| First |

$68.51 | $41.46 | $50.27 | $.44 | ||||||||||||

| Second |

60.20 | 43.44 | 56.25 | .45 | ||||||||||||

| Third |

69.93 | 54.73 | 64.59 | .45 | ||||||||||||

| Fourth |

80.60 | 60.52 | 77.58 | .45 | ||||||||||||

| $1.79 | ||||||||||||||||

The Company has authority to issue 25,000,000 shares of preferred stock in series. The Board of Directors is authorized to designate the series and to fix the relative voting, dividend, conversion, liquidation, redemption, and

15

Table of Contents

other rights, preferences, and limitations. When preferred stock is issued, holders of Common Stock are subject to the dividend and liquidation preferences and other prior rights of the preferred stock. There currently is no preferred stock outstanding. The Company’s Transfer Agent and Registrar is American Stock Transfer & Trust Company, 59 Maiden Lane, Plaza Level, New York, New York 10038, telephone (800) 937-5449 (U.S. and Canada) or (718) 921-8124 (all other locations); Internet website www.amstock.com; and e-mail address info@amstock.com. As of 15 November 2010, there were 8,256 record holders of the Company’s common stock.

Purchases of Equity Securities by the Issuer

On 20 September 2007, the Company’s Board of Directors authorized the repurchase of $1.0 billion of common stock. The program does not have a stated expiration date. As of 30 September 2010, the Company had purchased four million of its outstanding shares under this authorization at a cost of $350.8 million. There were no purchases of stock during fiscal year 2010. Additional purchases will be completed at the Company’s discretion while maintaining sufficient funds for investing in its businesses and growth opportunities.

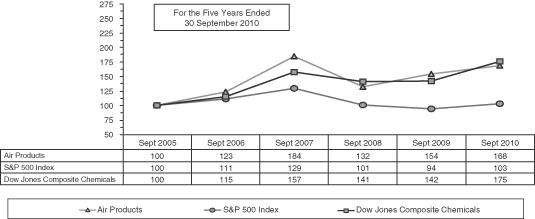

Performance Graph

The performance graph below compares the five-year cumulative returns of the Company’s common stock with those of the Standard & Poor’s 500 and Dow Jones Chemicals Composite Indices. The figures assume an initial investment of $100 and the reinvestment of all dividends.

16

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA |

| (Millions of dollars, except per share) | 2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||

| Operating Results |

||||||||||||||||||||

| Sales |

$9,026 | $8,256 | $10,415 | $9,148 | $7,885 | |||||||||||||||

| Cost of sales |

6,503 | 6,042 | 7,693 | 6,699 | 5,817 | |||||||||||||||

| Selling and administrative |

957 | 943 | 1,090 | 1,000 | 892 | |||||||||||||||

| Research and development |

115 | 116 | 131 | 129 | 140 | |||||||||||||||

| Global cost reduction plan |

— | 298 | — | 14 | 71 | |||||||||||||||

| Acquisition-related costs |

96 | — | — | — | — | |||||||||||||||

| Operating income |

1,389 | 846 | 1,496 | 1,376 | 1,042 | |||||||||||||||

| Equity affiliates’ income |

127 | 112 | 145 | 114 | 92 | |||||||||||||||

| Interest expense |

122 | 122 | 162 | 162 | 118 | |||||||||||||||

| Income tax provision |

340 | 185 | 365 | 287 | 262 | |||||||||||||||

| Income from continuing operations attributable to Air Products |

1,029 | 640 | 1,091 | 1,020 | 734 | |||||||||||||||

| Net income attributable to Air Products |

1,029 | 631 | 910 | 1,036 | 723 | |||||||||||||||

| Basic earnings per common share attributable to Air Products: |

||||||||||||||||||||

| Income from continuing operations |

4.85 | 3.05 | 5.14 | 4.72 | 3.31 | |||||||||||||||

| Net income |

4.85 | 3.01 | 4.29 | 4.79 | 3.26 | |||||||||||||||

| Diluted earnings per common share attributable to Air Products: |

||||||||||||||||||||

| Income from continuing operations |

4.74 | 3.00 | 4.97 | 4.57 | 3.23 | |||||||||||||||

| Net income |

4.74 | 2.96 | 4.15 | 4.64 | 3.18 | |||||||||||||||

| Year-End Financial Position |

||||||||||||||||||||

| Plant and equipment, at cost |

$16,310 | $15,751 | $14,989 | $14,439 | $12,910 | |||||||||||||||

| Total assets |

13,506 | 13,029 | 12,571 | 12,660 | 11,181 | |||||||||||||||

| Working capital |

790 | 494 | 636 | 436 | 289 | |||||||||||||||

| Total debt (A) |

4,128 | 4,502 | 3,967 | 3,668 | 2,846 | |||||||||||||||

| Air Products shareholders’ equity |

5,547 | 4,792 | 5,031 | 5,496 | 4,924 | |||||||||||||||

| Total equity |

5,698 | 4,930 | 5,167 | 5,673 | 5,102 | |||||||||||||||

| Financial Ratios |

||||||||||||||||||||

| Return on average Air Products shareholders’ equity (B) |

19.9 | % | 13.3 | % | 20.1 | % | 19.5 | % | 15.1 | % | ||||||||||

| Operating margin |

15.4 | % | 10.3 | % | 14.4 | % | 15.0 | % | 13.2 | % | ||||||||||

| Selling and administrative as a percentage of sales |

10.6 | % | 11.4 | % | 10.5 | % | 10.9 | % | 11.3 | % | ||||||||||

| Total debt to sum of total debt and total equity (A) |

42.0 | % | 47.7 | % | 43.4 | % | 39.8 | % | 36.3 | % | ||||||||||

| Other Data |

||||||||||||||||||||

| Depreciation and amortization |

$863 | $840 | $869 | $790 | $705 | |||||||||||||||

| Capital expenditures on a GAAP basis (C) |

1,134 | 1,236 | 1,159 | 1,553 | 1,358 | |||||||||||||||

| Capital expenditures on a non-GAAP basis (C) |

1,298 | 1,475 | 1,355 | 1,635 | 1,487 | |||||||||||||||

| Cash provided by operating activities |

1,522 | 1,329 | 1,659 | 1,500 | 1,348 | |||||||||||||||

| Cash used for investing activities |

1,057 | 1,040 | 920 | 1,483 | 947 | |||||||||||||||

| Cash provided by (used for) financing activities |

(580 | ) | 95 | (678 | ) | (15 | ) | (423 | ) | |||||||||||

| Dividends declared per common share |

1.92 | 1.79 | 1.70 | 1.48 | 1.34 | |||||||||||||||

| Market price range per common share |

85–64 | 81–41 | 106–65 | 99–66 | 70–53 | |||||||||||||||

| Weighted average common shares outstanding (in millions) |

212 | 210 | 212 | 216 | 222 | |||||||||||||||

| Weighted average common shares outstanding assuming dilution (in millions) |

217 | 214 | 219 | 223 | 228 | |||||||||||||||

| Book value per common share at year-end |

$25.94 | $22.68 | $24.03 | $25.52 | $22.67 | |||||||||||||||

| Shareholders at year-end |

8,300 | 8,600 | 8,900 | 9,300 | 9,900 | |||||||||||||||

| Employees at year-end (D) |

18,300 | 18,900 | 21,100 | 22,100 | 20,700 | |||||||||||||||

| (A) | Total debt includes long-term debt, current portion of long-term debt, and short-term borrowings as of the end of the year. Calculation based on continuing operations. |

| (B) | Calculated using income and five-quarter average Air Products shareholders’ equity from continuing operations. |

| (C) | Capital expenditures on a GAAP basis include additions to plant and equipment, investment in and advances to unconsolidated affiliates, and acquisitions (including long-term debt assumed in acquisitions). The Company utilizes a non-GAAP measure in the computation of capital expenditures and includes spending associated with facilities accounted for as capital leases and purchases of noncontrolling interests. Certain contracts associated with facilities that are built to provide product to a specific customer are required to be accounted for as leases, and such spending is reflected as a use of cash within cash provided by operating activities. Additionally, the purchase of noncontrolling interests in a subsidiary is accounted for as an equity transaction and will be reflected as a financing activity in the consolidated statement of cash flows. Refer to page 31 for a reconciliation of the GAAP to non-GAAP measure for 2010, 2009, and 2008. For 2007 and 2006, the GAAP measure was adjusted by $83 and $129, respectively, for spending associated with facilities accounted for as capital leases. |

| (D) | Includes full- and part-time employees from continuing and discontinued operations. |

17

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

| 18 | ||||

| 18 | ||||

| 20 | ||||

| 20 | ||||

| 28 | ||||

| 30 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 40 | ||||

| 41 |

The following discussion should be read in conjunction with the consolidated financial statements and the accompanying notes contained in this report. All comparisons in the discussion are to the corresponding prior year unless otherwise stated. All amounts presented are in accordance with U.S. generally accepted accounting principles (GAAP), except as noted. All amounts are presented in millions of dollars, except for share data, unless otherwise indicated.

Captions such as income from continuing operations attributable to Air Products and net income attributable to Air Products are simply referred to as “income from continuing operations” and “net income” throughout this Management’s Discussion and Analysis, unless otherwise stated.

The discussion of results that follows includes non-GAAP financial measures. These non-GAAP measures exclude acquisition-related costs in 2010. For 2009, the non-GAAP measures exclude the global cost reduction plan charge, costs related to customer bankruptcy and asset actions and third quarter 2009 pension settlement costs. For 2008, the non-GAAP measures exclude pension settlement costs. The presentation of non-GAAP measures is intended to enhance the usefulness of financial information by providing measures that the Company’s management uses internally to evaluate the Company’s baseline performance on a comparable basis. The reconciliation of reported GAAP results to non-GAAP measures is presented on pages 28—29.

Air Products and Chemicals, Inc. and its subsidiaries (the Company or Air Products) serves technology, energy, industrial, and healthcare customers globally with a unique portfolio of products, services, and solutions that include atmospheric gases, process and specialty gases, performance materials, equipment, and services. Geographically diverse, with operations in over 40 countries, the Company has sales of $9.0 billion, assets of $13.5 billion, and a worldwide workforce of approximately 18,300 employees.

The Company organizes its operations into four reportable business segments: Merchant Gases, Tonnage Gases, Electronics and Performance Materials, and Equipment and Energy.

In 2010, the Company emerged from the recession and delivered strong growth and productivity. Sales increased 9% and underlying sales increased 8%, due to strong volume growth as the economic environment improved. These results were driven by a significant recovery in the Electronics and Performance Materials segment and new investments and contracts in the Tonnage Gases segment. Operating income increased due to improved performance across all business segments.

The Company delivered significant improvements in 2010 as a result of actions taken to lower costs and position the Company for success coming out of the global recession. These actions included the completion of the Company’s global cost reduction plans and Electronics business restructuring. Additionally, the Company repositioned its manufacturing centers, continued to leverage the SAP system, and further utilized its shared service centers. These actions contributed to increased productivity and improved operating results.

18

Table of Contents

In February 2010, the Company commenced a tender offer to acquire all of the outstanding shares of Airgas, Inc. (Airgas). Airgas is the largest packaged industrial gases distributor in the U.S. Its fiscal year 2010 annual revenues were $3.9 and its total assets as of 31 March 2010 were $4.5. The current offer price is $65.50 per share. At this price, the total value of the transaction would be approximately $7.4 billion, including $5.7 billion of equity and $1.7 billon of assumed debt. The offer and withdrawal rights are scheduled to expire on 3 December 2010, unless further extended.

Highlights for 2010

| • | Sales of $9,026.0 increased 9%, or $769.8. Underlying business increased 8%, primarily due to higher volumes in the Electronics and Performance Materials and Tonnage Gases segments. |

| • | Operating income of $1,389.0 increased 64%, or $542.7. On a non-GAAP basis, operating income of $1,485.0 increased 25%, or $300.4, primarily due to higher volumes, lower costs, and favorable currency and foreign exchange, partially offset by reduced pricing. |