UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended 30 September 2021 | |||||

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _______________________ to ______________________ | |||||

Commission file number 001-04534

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

(Address of principal executive offices) (Zip Code)

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ☒ | No | ☐ | |||||||||||||||||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | ☐ | ☒ | |||||||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ☒ | No | ☐ | |||||||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☒ | No | ☐ | |||||||||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||||||||||||||||||

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. | ||||||||||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | No | ☒ | |||||||||||||||||

The aggregate market value of the voting stock held by non-affiliates of the registrant on 31 March 2021 was approximately $62.1 billion. For purposes of the foregoing calculations, all directors and/or executive officers have been deemed to be affiliates, but the registrant disclaims that any such director and/or executive officer is an affiliate.

The number of shares of common stock outstanding as of 31 October 2021 was 221,460,382 .

DOCUMENTS INCORPORATED BY REFERENCE

AIR PRODUCTS AND CHEMICALS, INC.

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended 30 September 2021

TABLE OF CONTENTS

| PART I | ||||||||

| ITEM 1. | ||||||||

| ITEM 1A. | ||||||||

| ITEM 1B. | ||||||||

| ITEM 2. | ||||||||

| ITEM 3. | ||||||||

| ITEM 4. | ||||||||

| PART II | ||||||||

| ITEM 5. | ||||||||

| ITEM 6. | ||||||||

| ITEM 7. | ||||||||

| ITEM 7A. | ||||||||

| ITEM 8. | ||||||||

| ITEM 9. | ||||||||

| ITEM 9A. | ||||||||

| ITEM 9B. | ||||||||

| PART III | ||||||||

| ITEM 10. | ||||||||

| ITEM 11. | ||||||||

| ITEM 12. | ||||||||

| ITEM 13. | ||||||||

| ITEM 14. | ||||||||

| PART IV | ||||||||

| ITEM 15. | ||||||||

| ITEM 16. | ||||||||

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts and can generally be identified by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” "future," “goal,” “intend,” “may,” “outlook,” “plan,” “positioned,” “possible,” “potential,” “project,” “should,” “target,” “will,” “would,” and similar expressions or variations thereof, or the negative thereof, but these terms are not the exclusive means of identifying such statements. Forward-looking statements are based on management’s expectations and assumptions as of the date of this report and are not guarantees of future performance. You are cautioned not to place undue reliance on our forward-looking statements.

Forward-looking statements may relate to a number of matters, including expectations regarding revenue, margins, expenses, earnings, tax provisions, cash flows, pension obligations, share repurchases or other statements regarding economic conditions or our business outlook; statements regarding plans, projects, strategies and objectives for our future operations, including our ability to win new projects and execute the projects in our backlog; and statements regarding our expectations with respect to pending legal claims or disputes. While forward-looking statements are made in good faith and based on assumptions, expectations and projections that management believes are reasonable based on currently available information, actual performance and financial results may differ materially from projections and estimates expressed in the forward-looking statements because of many factors, including, without limitation:

•the duration and impacts of the ongoing COVID-19 global pandemic and efforts to contain its transmission, including the effect of these factors on our business, our customers, economic conditions and markets generally;

•changes in global or regional economic conditions, inflation, and supply and demand dynamics in the market segments we serve, or in the financial markets that may affect the availability and terms on which we may obtain financing;

•the ability to implement price increases to offset cost increases;

•disruptions to our supply chain and related distribution delays and cost increases;

•risks associated with having extensive international operations, including political risks, risks associated with unanticipated government actions and risks of investing in developing markets;

•project delays, contract terminations, customer cancellations, or postponement of projects and sales;

•our ability to develop, operate, and manage costs of large-scale and technically complex projects, including gasification and hydrogen projects;

•the future financial and operating performance of major customers, joint ventures, and equity affiliates;

•our ability to develop, implement, and operate new technologies;

•our ability to execute the projects in our backlog and refresh our pipeline of new projects;

•tariffs, economic sanctions and regulatory activities in jurisdictions in which we and our affiliates and joint ventures operate;

•the impact of environmental, tax, or other legislation, as well as regulations and other public policy initiatives affecting our business and the business of our affiliates and related compliance requirements, including legislation, regulations, or policies intended to address global climate change;

•changes in tax rates and other changes in tax law;

•the timing, impact, and other uncertainties relating to acquisitions and divestitures, including our ability to integrate acquisitions and separate divested businesses, respectively;

•risks relating to cybersecurity incidents, including risks from the interruption, failure or compromise of our information systems;

3

FORWARD-LOOKING STATEMENTS (CONTINUED)

•catastrophic events, such as natural disasters and extreme weather events, public health crises, acts of war, or terrorism;

•the impact on our business and customers of price fluctuations in oil and natural gas and disruptions in markets and the economy due to oil and natural gas price volatility;

•costs and outcomes of legal or regulatory proceedings and investigations;

•asset impairments due to economic conditions or specific events;

•significant fluctuations in inflation, interest rates and foreign currency exchange rates from those currently anticipated;

•damage to facilities, pipelines or delivery systems, including those we own or operate for third parties;

•availability and cost of electric power, natural gas, and other raw materials; and

•the success of productivity and operational improvement programs.

In addition to the foregoing factors, forward-looking statements contained herein are qualified with respect to the risks disclosed elsewhere in this document, including in Item 1A, Risk Factors, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 7A, Quantitative and Qualitative Disclosures About Market Risk. Any of these factors, as well as those not currently anticipated by management, could cause our results of operations, financial condition or liquidity to differ materially from what is expressed or implied by any forward-looking statement. Except as required by law, we disclaim any obligation or undertaking to update or revise any forward-looking statements contained herein to reflect any change in assumptions, beliefs, or expectations or any change in events, conditions, or circumstances upon which any such forward-looking statements are based.

PART I

Item 1. Business.

Air Products and Chemicals, Inc., a Delaware corporation originally founded in 1940, serves customers globally with a unique portfolio of products, services, and solutions that include atmospheric gases, process and specialty gases, equipment, and services. Focused on serving energy, environment and emerging markets, we provide essential industrial gases, related equipment, and applications expertise to customers in dozens of industries, including refining, chemicals, metals, electronics, manufacturing, and food and beverage. We are the world’s largest supplier of hydrogen and have built leading positions in growth markets such as helium and liquefied natural gas ("LNG") process technology and equipment. We develop, engineer, build, own, and operate some of the world’s largest industrial gas projects, including gasification projects that sustainably convert abundant natural resources into syngas for the production of high-value power, fuels, and chemicals and are developing carbon capture projects and world-scale low carbon and carbon-free hydrogen projects that will support global transportation and energy transition away from fossil fuels.

As used in this report, unless the context indicates otherwise, the terms “we,” “our,” “us,” the “Company,” "Air Products," or “registrant” include controlled subsidiaries, affiliates, and predecessors of Air Products and our controlled subsidiaries and affiliates.

Except as otherwise noted, the description of our business below reflects our continuing operations. Refer to Note 5, Discontinued Operations, to the consolidated financial statements for activity associated with discontinued operations.

4

During the fiscal year ended 30 September 2021 (“fiscal year 2021”), we reported our continuing operations in five reporting segments under which we managed our operations, assessed performance, and reported earnings: Industrial Gases – Americas; Industrial Gases – EMEA (Europe, Middle East, and Africa); Industrial Gases – Asia; Industrial Gases – Global; and Corporate and other. The discussion that follows is based on those operations. Refer to Note 23, Business Segment and Geographic Information, to the consolidated financial statements for additional details on our reportable business segments.

On 4 November 2021, we announced the reorganization of our industrial gases segments effective 1 October 2021. Refer to Note 24, Subsequent Events, for additional information.

Industrial Gases Business

Our Industrial Gases business produces atmospheric gases, such as oxygen, nitrogen, and argon; process gases, such as hydrogen, helium, carbon dioxide (CO2), carbon monoxide, and syngas; and specialty gases. Atmospheric gases are produced through various air separation processes, of which cryogenic is the most prevalent. Process gases are produced by methods other than air separation. For example, hydrogen, carbon monoxide, and syngas are produced by steam methane reforming of natural gas and by the gasification of liquid and solid hydrocarbons. Hydrogen is produced by purifying byproduct sources obtained from the chemical and petrochemical industries. Helium is produced as a byproduct of gases extracted from underground reservoirs, primarily natural gas, but also CO2 purified before resale. The Industrial Gases business also develops, builds, and operates equipment for the production or processing of gases, such as air separation units and non-cryogenic generators.

Our Industrial Gases business is organized and operated regionally. The regional Industrial Gases segments supply gases, related equipment, and applications in the relevant region to diversified customers in many industries, including those in refining, chemicals, metals, electronics, manufacturing, and food and beverage. Hydrogen is used by refiners to facilitate the conversion of heavy crude feedstock and lower the sulfur content of gasoline and diesel fuels, as well as in the developing hydrogen-for-mobility markets. We have hydrogen fueling stations that support commercial markets in California and Japan as well as demonstration projects in Europe, Saudi Arabia, and other parts of Asia. The chemicals industry uses hydrogen, oxygen, nitrogen, carbon monoxide, and syngas as feedstocks in the production of many basic chemicals. The energy production industry uses nitrogen injection for enhanced recovery of oil and natural gas and oxygen for gasification. Oxygen is used in combustion and industrial heating applications, including in the steel, certain nonferrous metals, glass, and cement industries. Nitrogen applications are used in food processing for freezing and preserving flavor, and nitrogen is used for inerting in various fields, including the metals, chemical, and semiconductor industries. Helium is used in laboratories and healthcare for cooling and in other industries for pressurizing, purging, and lifting. Argon is used in the metals and other industries for its unique inerting, thermal conductivity, and other properties. Industrial gases are also used in welding and providing healthcare and are utilized in various manufacturing processes to make them more efficient and to optimize performance.

Industrial gases are generally produced at or near the point of use given the complexity and inefficiency with storing molecules at low temperatures. Helium, however, is generally sourced globally, at long distances from point of sale. As a result, we maintain an inventory of helium stored in our fleet of ISO containers as well as at the U.S. Bureau of Land Management underground storage facility in Amarillo, Texas.

5

We distribute gases to our sale of gas customers through different supply modes depending on various factors including the customer's volume requirements and location. Our supply modes are as follows:

•Liquid Bulk—Product is delivered in bulk (in liquid or gaseous form) by tanker or tube trailer and stored, usually in its liquid state, in equipment that we typically design and install at the customer’s site for vaporizing into a gaseous state as needed. Liquid bulk sales are usually governed by three- to five-year contracts.

•Packaged Gases—Small quantities of product are delivered in either cylinders or dewars. We operate packaged gas businesses in Europe, Asia, and Latin America. In the United States, our packaged gas business sells products (principally helium) only for the electronics and magnetic resonance imaging industries.

•On-Site Gases—Large quantities of hydrogen, nitrogen, oxygen, carbon monoxide, and syngas (a mixture of hydrogen and carbon monoxide) are provided to customers, principally in the energy production and refining, chemical, and metals industries worldwide, that require large volumes of gases and have relatively constant demand. Gases are produced and supplied by large facilities we construct or acquire on or near the customers’ facilities or by pipeline systems from centrally located production facilities. These sale of gas contracts are generally governed by 15- to 20-year contracts. We also deliver smaller quantities of product through small on-site plants (cryogenic or non-cryogenic generators), typically via a 10- to 15-year sale of gas contract.

Electricity is the largest cost component in the production of atmospheric gases. Steam methane reformers utilize natural gas as the primary raw material and gasifiers use liquid and solid hydrocarbons as the principal raw material for the production of hydrogen, carbon monoxide, and syngas. We mitigate electricity, natural gas, and hydrocarbon price fluctuations contractually through pricing formulas, surcharges, and cost pass-through and tolling arrangements. During fiscal year 2021, no significant difficulties were encountered in obtaining adequate supplies of power and natural gas.

We obtain helium from a number of sources globally, including crude helium for purification from the U.S. Bureau of Land Management's helium reserve.

The regional Industrial Gases segments also include our share of the results of several joint ventures accounted for by the equity method, which we report in our financial statements as income from equity affiliates. The largest of these joint ventures operate in China, India, Italy, Mexico, Saudi Arabia, South Africa, and Thailand.

Each of the regional Industrial Gases segments competes against three global industrial gas companies: Air Liquide S.A., Messer, and Linde plc, as well as regional competitors. Competition in Industrial Gases is based primarily on price, reliability of supply, and the development of industrial gas applications. We derive a competitive advantage in locations where we have pipeline networks, which enable us to provide reliable and economic supply of products to our larger customers.

Overall regional industrial gases sales constituted approximately 92%, 94%, and 96% of consolidated sales in fiscal years 2021, 2020, and 2019, respectively. Sales of atmospheric gases constituted approximately 47%, 47%, and 46% of consolidated sales in fiscal years 2021, 2020, and 2019, respectively, while sales of tonnage hydrogen, syngas, and related products constituted approximately 22%, 22%, and 26% of consolidated sales in fiscal years 2021, 2020, and 2019, respectively.

6

Industrial Gases Equipment

We design and manufacture equipment for air separation, hydrocarbon recovery and purification, natural gas liquefaction, and liquid helium and liquid hydrogen transport and storage. The Industrial Gases – Global segment includes activity primarily related to the sale of cryogenic and gas processing equipment for air separation. The equipment is sold worldwide to customers in a variety of industries, including chemical and petrochemical manufacturing, oil and gas recovery and processing, and steel and primary metals processing. The Corporate and other segment includes: our LNG equipment business, our Gardner Cryogenics business fabricating helium and hydrogen transport and storage containers, and our Rotoflow business, which manufactures turboexpanders and other precision rotating equipment. Steel, aluminum, and capital equipment subcomponents (compressors, etc.) are the principal raw materials in the manufacturing of equipment. Raw materials for individual projects typically are acquired under firm purchase agreements. Equipment is produced at our manufacturing sites with certain components being procured from subcontractors and vendors. Competition in the equipment business is based primarily on plant efficiency, service, technical know-how and price, as well as schedule and plant performance guarantees. Sale of equipment constituted approximately 8%, 6%, and 4% of consolidated sales in fiscal years 2021, 2020, and 2019, respectively.

Our backlog of equipment orders was approximately $1.3 billion on 30 September 2021 (as compared to a total backlog of approximately $1.6 billion on 30 September 2020). We estimate that approximately half of the total equipment sales backlog as of 30 September 2021 will be recognized as revenue during fiscal year 2022, dependent on execution schedules of the relevant projects.

International Operations

Through our subsidiaries, affiliates, and joint ventures accounted for using the equity method, we conduct business in 53 countries outside the United States. Our international businesses are subject to risks customarily encountered in foreign operations, including fluctuations in foreign currency exchange rates and controls, tariffs, trade sanctions, and import and export controls, and other economic, political, and regulatory policies of local governments described in Item 1A, Risk Factors, below.

We have majority or wholly owned foreign subsidiaries that operate in Canada; 18 European countries (including the Netherlands, Spain, and the United Kingdom); 11 Asian countries (including China, South Korea, and Taiwan); seven Latin American countries (including Brazil and Chile); six countries in the Middle East (including Saudi Arabia), and three African countries. We also own less-than-controlling interests in entities operating in Europe, Asia, Latin America, the Middle East, and Africa (including China, India, Italy, Mexico, Oman, Saudi Arabia, South Africa, and Thailand).

Financial information about our foreign operations and investments is included in Note 7, Summarized Financial Information of Equity Affiliates; Note 21, Income Taxes; and Note 23, Business Segment and Geographic Information, to the consolidated financial statements included under Item 8, below. Information about foreign currency translation is included under “Foreign Currency” in Note 1, Major Accounting Policies, and information on our exposure to currency fluctuations is included in Note 12, Financial Instruments, to the consolidated financial statements, included under Item 8, below, and in “Foreign Currency Exchange Rate Risk,” included under Item 7A, below.

Technology Development

We pursue a market-oriented approach to technology development through research and development, engineering, and commercial development processes. We conduct research and development principally in our laboratories located in the United States (Trexlertown, Pennsylvania), the United Kingdom (Basingstoke and Carrington), Spain (Barcelona), China (Shanghai), and Saudi Arabia (Dhahran). We also fund and cooperate in research and development programs conducted by a number of major universities and undertake research work funded by others, including the United States government.

Development of technology for use within the Industrial Gases business focuses primarily on new and improved processes and equipment for the production and delivery of industrial gases and new or improved applications for industrial gas products.

During fiscal year 2021, we owned approximately 780 United States patents, approximately 3,480 foreign patents, and were a licensee under certain patents owned by others. While the patents and licenses are considered important, we do not consider our business as a whole to be materially dependent upon any particular patent, patent license, or group of patents or licenses.

7

Environmental Regulation

We are subject to various environmental laws, regulations, and public policies in the countries in which we have operations. Compliance with these measures often results in higher capital expenditures and costs. In the normal course of business, we are involved in legal proceedings under the Comprehensive Environmental Response, Compensation, and Liability Act ("CERCLA," the federal Superfund law); Resource Conservation and Recovery Act ("RCRA"); and similar state and foreign environmental laws relating to the designation of certain sites for investigation or remediation. Our accounting policy for environmental expenditures is discussed in Note 1, Major Accounting Policies, and environmental loss contingencies are discussed in Note 16, Commitments and Contingencies, to the consolidated financial statements, included under Item 8, below.

Some of our operations are within jurisdictions that have or are developing regulatory regimes governing emissions of greenhouse gases (“GHG”), including CO2. These include existing coverage under the European Union Emission Trading System, the California Cap-and-Trade Program, China’s Emission Trading Scheme and its nation-wide expansion, and South Korea’s Emission Trading Scheme. In the Netherlands, a CO2 emissions tax was enacted on 1 January 2021. In Canada, Alberta’s Technology Innovation and Emission Reduction System went into effect 1 January 2020. In Ontario, Environment & Climate Change Canada’s Output Based Pricing System (“OBPS”) is currently in effect, however, effective 1 January 2022, Ontario’s GHG Emissions Performance Standards program will be used in lieu of adherence to the OBPS. In addition, the U.S. Environmental Protection Agency (“EPA”) requires mandatory reporting of GHG emissions and is regulating GHG emissions for new construction and major modifications to existing facilities. Some jurisdictions have various mechanisms to target the power sector to achieve emission reductions, which often result in higher power costs.

Increased public concern may result in more international, U.S. federal, and/or regional requirements to reduce or mitigate the effects of GHG emissions. Although uncertain, these developments could increase our costs related to consumption of electric power, hydrogen production and application of our gasification technology. We believe we will be able to mitigate some of the increased costs through contractual terms, but the lack of definitive legislation or regulatory requirements prevents an accurate estimate of the long-term impact these measures will have on our operations. Any legislation that limits or taxes GHG emissions could negatively impact our growth, increase our operating costs, or reduce demand for certain of our products.

Regulation of GHG may also produce new opportunities for us. We continue to develop technologies to help our facilities and our customers lower energy consumption, improve efficiency and lower emissions. We see significant opportunities for gasification, carbon capture technologies and hydrogen for mobility and energy transition.

We estimate that we spent approximately $8 million, $4 million, and $5 million in fiscal years 2021, 2020, and 2019, respectively, on capital projects reflected in continuing operations to control pollution. Capital expenditures to control pollution are estimated to be approximately $8 million in both fiscal years 2022 and 2023.

For additional information regarding environmental matters, refer to Note 16, Commitments and Contingencies, to the consolidated financial statements.

Employees

We believe our employees are our most valuable asset and are critical to our success as an organization. Our goal is to be the safest, most diverse and most profitable industrial gas company in the world, providing excellent service to our customers. Integral to our success is the continued development of our 4S culture (Safety, Speed, Simplicity and Self-Confidence) and creating a work environment where our employees feel that they belong and matter. Our talent related initiatives, including employee recruitment and development, diversity and inclusion and compensation and benefit programs, are focused on building and retaining the world-class and talented staff that is needed to meet our goals.

On 30 September 2021, we had approximately 20,875 employees, of whom approximately 20,625 were full-time and approximately 15,575 were located outside the United States. We have collective bargaining agreements with unions and works councils at certain locations that expire on various dates over the next four years. We consider relations with our employees to be good.

Our 2021 Sustainability Report details our growth strategy and the role our most valuable asset and our competitive advantage, our employees, play in achieving our goals. Rooted in our framework of Grow- Conserve- Care, our higher purpose is to bring people together to collaborate and innovate solutions to the world’s most significant energy and environmental sustainability challenges. Our 2021 Sustainability Report details how we care for our employees.

8

Safety

Safety is fundamental to who we are as a company. Safety is a shared value, and our employees’ commitment to safety is demonstrated in many ways every day. Safety is a critical component of everything we do, everywhere in the world. Our goal is to be the safest industrial gas company in the world.

Diversity, Inclusion, and Belonging

Our 2021 Sustainability Report sets forth our announced goals to further increase the percentage of women and U.S. minorities in professional and managerial roles and the recruitment and talent development strategies we have in place to ensure we meet these goals. Since the publication of our 2021 Sustainability Report, we have announced goals to further increase the percentage of women and U.S. minorities in professional and managerial roles. By 2025, we aim to achieve at least 28 percent female representation in the professional and managerial population globally. Due to significant increase of our U.S. minority representation, our new 2025 diversity goal is to achieve at least 30 percent U.S. minority representation in professional and managerial roles. We established these targets following analysis of our global employee representation metrics and future talent needs, as well as assessing industry benchmarks and peer companies.

Compensation

As detailed in our 2021 Sustainability Report, in order to create a diverse workplace, individuals must be compensated fairly and equitably. A work environment where employees know they belong and matter includes fair and equitable pay. Our pay practices apply equally to all employees irrespective of gender, race, religion, disability, age, or any other form of personal difference. We strive to pay competitively in local markets where we do business and compete for talent. We benchmark our compensation to ensure that we are keeping pace with the market to provide competitive pay and benefits. A gender pay equity analysis completed by a third-party in 2020 resulted in no significant adverse findings for minorities in the U.S. and for females globally.

We value the contributions of our employees, particularly in the face of the challenges posed by the COVID-19 pandemic. Many of our employees are on the front line during the pandemic, keeping our plants running and delivering to our customers the products they need. When possible, employees have been working from home to help maintain their health and safety as well as business continuity. We have not laid off any of our employees or reduced their salaries due to COVID-19.

Seasonality

Our businesses are not subject to seasonal fluctuations to any material extent.

Inventories

We maintain limited inventory where required to facilitate the supply of products to customers on a reasonable delivery schedule. Inventory consists primarily of crude helium, industrial gas, and specialty gas inventories supplied to customers through liquid bulk and packaged gases supply modes.

Customers

We do not have a homogeneous customer base or end market, and no single customer accounts for more than 10% of our consolidated revenues. We do have concentrations of customers in specific industries, primarily refining, chemicals, and electronics. Within each of these industries, we have several large-volume customers with long-term contracts. A negative trend affecting one of these industries, or the loss of one of these major customers, although not material to our consolidated revenue, could have an adverse impact on our financial results.

Governmental Contracts

Our business is not subject to a government entity’s renegotiation of profits or termination of contracts that would be material to our business as a whole.

Available Information

All periodic and current reports, registration statements, proxy statements, and other filings that we are required to file with the Securities and Exchange Commission ("SEC"), including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934 (the "Exchange Act"), are available free of charge through our website at www.airproducts.com. Such documents are available as soon as reasonably practicable after electronic filing of the material with the SEC. All such reports filed during the period covered by this report were available on our website on the same day as filing. In addition, our filings with the SEC are available free of charge on the SEC's website, www.sec.gov.

9

Our Executive Officers

Our executive officers and their respective positions and ages on 18 November 2021 follow. Information with respect to offices held is stated in fiscal years.

| Name | Age | Office | ||||||

| Seifi Ghasemi | 77 | Chairman, President, and Chief Executive Officer (became Chairman, President and Chief Executive Officer in 2014 and previously served as Chairman and Chief Executive Officer of Rockwood Holdings, Inc. from 2001 to 2014). Mr. Ghasemi is a member and Chairman of the Board of Directors and the Chairman of the Executive Committee of the Board of Directors. | ||||||

| Sean D. Major | 57 | Executive Vice President, General Counsel and Secretary (Executive Vice President and General Counsel since May 2017 and Secretary since December 2017). Previously, Mr. Major served as Executive Vice President, General Counsel and Secretary for Joy Global Inc. from 2007 to 2017. | ||||||

| Melissa N. Schaeffer | 42 | Senior Vice President and Chief Financial Officer (became Senior Vice President and Chief Financial Officer in August 2021). Ms. Schaeffer joined the Company in 2016 and most recently served as Vice President, Finance – GEMTE, Americas, Middle East, and India from 2020 to 2021 and previously served as Vice President, Chief Audit Executive from 2016 to 2020. | ||||||

| Dr. Samir J. Serhan | 60 | Chief Operating Officer (Executive Vice President since December 2016 and Chief Operating Officer since May 2020). Dr. Serhan served as President, Global HyCO, from 2014 to 2016 for Praxair Inc. From 2000-2014, he worked in leadership positions in the U.S. and Germany for The Linde Group, including as Managing Director of Linde Engineering from 2008-2014. | ||||||

Item 1A. Risk Factors.

Our operations are affected by various risks, many of which are beyond our control. In evaluating investment in the Company and the forward-looking information contained in this Annual Report on Form 10-K or presented elsewhere from time to time, you should carefully consider the risk factors discussed below. Any of these risks could have a material adverse effect on our business, operating results, financial condition, and the actual outcome of matters as to which forward-looking statements are made and could adversely affect the value of an investment in our securities. The risks described below are not all inclusive but are designed to highlight what we believe are important factors to consider when evaluating our expectations. In addition to such risks, there may be additional risks and uncertainties that adversely affect our business, performance, or financial condition in the future that are not presently known, are not currently believed to be significant, or are not identified below because they are common to all businesses.

Risks Related to Economic Conditions

The COVID-19 global pandemic may materially and adversely impact our business, financial condition and results of operations.

The COVID-19 global pandemic, including resurgences and variants of the virus that causes COVID-19, and efforts to reduce its spread have led, and may continue to lead to, significant changes in levels of economic activity and significant disruption and volatility in global markets. These factors have led, and may continue to lead, to reduced demand for industrial gas products, particularly in our merchant business. In addition, COVID-19 may result in reduced sales in our other businesses, lower returns for certain of our projects, and the potential delay or cancellation of certain projects in our pipeline.

In addition, we are monitoring the health of our employees and many of our employees, including those based at our headquarters, are working remotely in accordance with health safety guidance and applicable governmental orders. Action by health or other governmental authorities requiring the closure of our facilities, recommending other physical distancing measures, or mandating vaccination against COVID-19 could negatively impact our business and those of our service providers and customers. Although we have business continuity and other safeguards in place, we cannot be certain that they will be fully effective for extended periods of time.

10

As the pandemic and responses to it continue to evolve we may experience further adverse impacts on our operations, and our ability to access capital on favorable terms, or at all, may be impaired. In addition, we may face unpredictable increases in demand for certain of our products when restrictions on business and travel end. If demand for our products exceeds our capacity, it could adversely affect our financial results and customer relationships. Although the duration and ultimate impact of these factors is unknown at this time, the decline in economic conditions due to COVID-19, or another disease-causing similar impacts, may adversely affect our business, financial condition and results of operations and such impact may be material.

Further, to the extent COVID-19 adversely affects our business, financial condition, and results of operations and global economic conditions more generally, it may also have the effect of heightening many of the other risks described herein.

Changes in global and regional economic conditions, the markets we serve, or the financial markets may adversely affect our results of operations and cash flows.

Unfavorable conditions in the global economy or regional economies, the markets we serve or financial markets may decrease the demand for our goods and services and adversely impact our revenues, operating results, and cash flows.

Demand for our products and services depends in part on the general economic conditions affecting the countries and markets in which we do business. Weak economic conditions in certain geographies and changing supply and demand balances in the markets we serve have negatively impacted demand for our products and services in the past, including most recently due to COVID-19, and may do so in the future. Reduced demand for our products and services would have a negative impact on our revenues and earnings. In addition, reduced demand could depress sales, reduce our margins, constrain our operating flexibility or reduce efficient utilization of our manufacturing capacity, or result in charges which are unusual or nonrecurring. Excess capacity in our manufacturing facilities or those of our competitors could decrease our ability to maintain pricing and generate profits.

In addition, our operating results in one or more segments may be affected by uncertain or deteriorating economic conditions for particular customer markets within a segment. A decline in the industries served by our customers or adverse events or circumstances affecting individual customers can reduce demand for our products and services and impair the ability of such customers to satisfy their obligations to us, resulting in uncollected receivables, unanticipated contract terminations, project delays or the inability to recover plant investments, any of which may negatively impact our financial results.

Weak overall demand or specific customer conditions may also cause customer shutdowns or defaults or otherwise make us unable to operate facilities profitably and may force sale or abandonment of facilities and equipment or prevent projects from coming on-stream when expected. These or other events associated with weak economic conditions or specific market, product, or customer events may require us to record an impairment on tangible assets, such as facilities and equipment, or intangible assets, such as intellectual property or goodwill, which would have a negative impact on our financial results.

Our extensive international operations can be adversely impacted by operational, economic, political, security, legal, and currency translation risks that could decrease profitability.

In fiscal year 2021, over 60% of our sales were derived from customers outside the United States and many of our operations, suppliers, and employees are located outside the United States. Our operations in foreign jurisdictions may be subject to risks including exchange control regulations, import and trade restrictions, trade policy and other potentially detrimental domestic and foreign governmental practices or policies affecting U.S. companies doing business abroad. Changing economic and political conditions within foreign jurisdictions, strained relations between countries, or the imposition of tariffs or international sanctions can cause fluctuations in demand, price volatility, supply disruptions, or loss of property. The occurrence of any of these risks could have a material adverse impact on our financial condition, results of operation, and cash flows.

11

Our growth strategies depend in part on our ability to further penetrate markets outside the United States, particularly in markets such as China, India, Indonesia, and the Middle East, and involve significantly larger and more complex projects, including gasification and large-scale hydrogen projects, some in regions where there is the potential for significant economic and political disruptions. We are actively investing large amounts of capital and other resources, in some cases through joint ventures, in developing markets, which we believe to have high growth potential. Our operations in these markets may be subject to greater risks than those faced by our operations in mature economies, including political and economic instability, project delay or abandonment due to unanticipated government actions, inadequate investment in infrastructure, undeveloped property rights and legal systems, unfamiliar regulatory environments, relationships with local partners, language and cultural differences and increased difficulty recruiting, training and retaining qualified employees. In addition, our properties and contracts in these locations may be subject to seizure and cancellation, respectively, without full compensation for loss. Successful operation of particular facilities or execution of projects may be disrupted by civil unrest, acts of war, sabotage or terrorism, and other local security concerns. Such concerns may require us to incur greater costs for security or require us to shut down operations for a period of time.

Furthermore, because the majority of our revenue is generated from sales outside the United States, we are exposed to fluctuations in foreign currency exchange rates. Our business is primarily exposed to translational currency risk as the results of our foreign operations are translated into U.S. dollars at current exchange rates throughout the fiscal period. Our policy is to minimize cash flow volatility from changes in currency exchange rates. We choose not to hedge the translation of our foreign subsidiaries’ earnings into dollars. Accordingly, reported sales, net earnings, cash flows, and fair values have been, and in the future will be, affected by changes in foreign exchange rates. For a more detailed discussion of currency exposure, see Item 7A, Quantitative and Qualitative Disclosures About Market Risk, below.

Risks Related to Our Business

Operational and project execution risks, particularly with respect to our largest projects, may adversely affect our operations or financial results.

A significant and growing portion of our business involves gasification and other large-scale projects that involve challenging engineering, procurement and construction phases that may last up to several years and involve the investment of billions of dollars. These projects are technically complex, often reliant on significant interaction with government authorities and face significant financing, development, operational and reputational risks. We may encounter difficulties in engineering, delays in designs or materials provided by the customer or a third party, equipment and materials delivery delays, schedule changes, customer scope changes, delays related to obtaining regulatory permits and rights-of-way, inability to find adequate sources of labor in the locations where we are building new plants, weather-related delays, delays by customers' contractors in completing their portion of a project, technical or transportation difficulties, cost overruns, supply difficulties, geopolitical risks and other factors, many of which are beyond our control, that may impact our ability to complete a project within the original delivery schedule. In some cases, delays and additional costs may be substantial, and we may be required to cancel a project and/or compensate the customer for the delay. We may not be able to recover any of these costs. In addition, in some cases we seek financing for large projects and face market risk associated with the availability and terms of such financing. These financing arrangements may require that we comply with certain performance requirements which, if not met, could result in default and restructuring costs or other losses. All of these factors could also negatively impact our reputation or relationships with our customers, suppliers and other third parties, any of which could adversely affect our ability to secure new projects in the future.

The operation of our facilities, pipelines, and delivery systems inherently entails hazards that require continuous oversight and control, such as pipeline leaks and ruptures, fire, explosions, toxic releases, mechanical failures, vehicle accidents, or cyber incidents. If operational risks materialize, they could result in loss of life, damage to the environment, or loss of production, all of which could negatively impact our ongoing operations, reputation, financial results, and cash flows. In addition, our operating results are dependent on the continued operation of our production facilities and our ability to meet customer requirements, which depend, in part, on our ability to properly maintain and replace aging assets.

12

We are subject to extensive government regulation in the jurisdictions in which we do business. Regulations addressing, among other things, import/export restrictions, anti-bribery and corruption, and taxes, can negatively impact our financial condition, results of operation, and cash flows.

We are subject to government regulation in the United States and in the foreign jurisdictions where we conduct business. The application of laws and regulations to our business is sometimes unclear. Compliance with laws and regulations may involve significant costs or require changes in business practices that could result in reduced profitability. If there is a determination that we have failed to comply with applicable laws or regulations, we may be subject to penalties or sanctions that could adversely impact our reputation and financial results. Compliance with changes in laws or regulations can result in increased operating costs and require additional, unplanned capital expenditures. Export controls or other regulatory restrictions could prevent us from shipping our products to and from some markets or increase the cost of doing so. Changes in tax laws and regulations and international tax treaties could affect the financial results of our businesses. Increasingly aggressive enforcement of anti-bribery and anti-corruption requirements, including the U.S. Foreign Corrupt Practices Act, the United Kingdom Bribery Act and the China Anti-Unfair Competition Law, could subject us to criminal or civil sanctions if a violation is deemed to have occurred. In addition, we are subject to laws and sanctions imposed by the U.S. and other jurisdictions where we do business that may prohibit us, or certain of our affiliates, from doing business in certain countries, or restricting the kind of business that we may conduct. Such restrictions may provide a competitive advantage to competitors who are not subject to comparable restrictions or prevent us from taking advantage of growth opportunities.

Further, we cannot guarantee that our internal controls and compliance systems will always protect us from acts committed by employees, agents, business partners or that businesses that we acquire would not violate U.S. and/or non-U.S. laws, including the laws governing payments to government officials, bribery, fraud, kickbacks and false claims, pricing, sales and marketing practices, conflicts of interest, competition, export and import compliance, money laundering, and data privacy. Any such improper actions or allegations of such acts could damage our reputation and subject us to civil or criminal investigations in the U.S. and in other jurisdictions and related shareholder lawsuits, could lead to substantial civil and criminal, monetary and non-monetary penalties, and could cause us to incur significant legal and investigatory fees. In addition, the government may seek to hold us liable as a successor for violations committed by companies in which we invest or that we acquire.

We may be unable to successfully identify, execute or effectively integrate acquisitions, or effectively disentangle divested businesses.

Our ability to grow revenue, earnings, and cash flow at anticipated rates depends in part on our ability to identify, successfully acquire and integrate businesses and assets at appropriate prices, and realize expected growth, synergies, and operating efficiencies. We may not be able to complete transactions on favorable terms, on a timely basis or at all. In addition, our results of operations and cash flows may be adversely impacted by the failure of acquired businesses or assets to meet expected returns, the failure to integrate acquired businesses, the inability to dispose of non-core assets and businesses on satisfactory terms and conditions, and the discovery of unanticipated liabilities or other problems in acquired businesses or assets for which we lack adequate contractual protections or insurance. In addition, we may incur asset impairment charges related to acquisitions that do not meet expectations.

We continually assess the strategic fit of our existing businesses and may divest businesses that are deemed not to fit with our strategic plan or are not achieving the desired return on investment. These transactions pose risks and challenges that could negatively impact our business and financial statements. For example, when we decide to sell or otherwise dispose of a business or assets, we may be unable to do so on satisfactory terms within our anticipated time frame or at all. In addition, divestitures or other dispositions may dilute our earnings per share, have other adverse financial and accounting impacts, distract management, and give rise to disputes with buyers. In addition, we have agreed, and may in the future agree, to indemnify buyers against known and unknown contingent liabilities. Our financial results could be impacted adversely by claims under these indemnification provisions.

13

The security of our information technology systems could be compromised, which could adversely affect our ability to operate.

We depend on information technology to enable us to operate safely and efficiently and interface with our customers as well as to maintain our internal control environment and financial reporting accuracy and efficiency. Our information technology capabilities are delivered through a combination of internal and external services and service providers. If we do not allocate and effectively manage the resources necessary to build and sustain the proper technology infrastructure, we could be subject to transaction errors, processing inefficiencies, the loss of customers, business disruptions, property damage, or the loss of or damage to our confidential business information due to a security breach. In addition, our information technology systems may be damaged, disrupted or shut down due to attacks by computer hackers, computer viruses, employee error or malfeasance, power outages, hardware failures, telecommunication or utility failures, catastrophes or other unforeseen events, and in any such circumstances our system redundancy and other disaster recovery planning may be ineffective or inadequate. Security breaches of our systems (or the systems of our customers, suppliers or other business partners) could result in the misappropriation, destruction or unauthorized disclosure of confidential information or personal data belonging to us or to our employees, partners, customers or suppliers, and may subject us to legal liability.

As with most large systems, our information technology systems have in the past been, and in the future likely will be subject to computer viruses, malicious codes, unauthorized access and other cyber-attacks, and we expect the sophistication and frequency of such attacks to continue to increase. To date, we are not aware of any significant impact on our operations or financial results from such attempts; however, unauthorized access could disrupt our business operations, result in the loss of assets, and have a material adverse effect on our business, financial condition, or results of operations. Any of the attacks, breaches or other disruptions or damage described above could: interrupt our operations at one or more sites; delay production and shipments; result in the theft of our and our customers’ intellectual property and trade secrets; damage customer and business partner relationships and our reputation; result in defective products or services, physical damage to facilities, pipelines or delivery systems, including those we own or operate for third parties, legal claims and proceedings, liability and penalties under privacy laws, or increased costs for security and remediation; or raise concerns regarding our internal control environment and internal control over financial reporting. Each of these consequences could adversely affect our business, reputation and our financial statements.

Our business involves the use, storage, and transmission of information about our employees, vendors, and customers. The protection of such information, as well as our proprietary information, is critical to us. The regulatory environment surrounding information security and privacy is increasingly demanding, with the frequent imposition of new and constantly changing requirements. We have established policies and procedures to help protect the security and privacy of this information. We also, from time to time, export sensitive customer data and technical information to recipients outside the United States. Breaches of our security measures or the accidental loss, inadvertent disclosure, or unapproved dissemination of proprietary information or sensitive or confidential data about us or our customers, including the potential loss or disclosure of such information or data as a result of fraud, trickery, or other forms of deception, could expose us, our customers, or the individuals affected to a risk of loss or misuse of this information, which could ultimately result in litigation and potential legal and financial liability. These events could also damage our reputation or otherwise harm our business.

Interruption in ordinary sources of raw material or energy supply or an inability to recover increases in energy and raw material costs from customers could result in lost sales or reduced profitability.

Hydrocarbons, including natural gas, are the primary feedstock for the production of hydrogen, carbon monoxide, and syngas. Energy, including electricity, natural gas, and diesel fuel for delivery trucks, is the largest cost component of our business. Because our industrial gas facilities use substantial amounts of electricity, inflation and energy price fluctuations could materially impact our revenues and earnings. A disruption in the supply of energy, components, or raw materials, whether due to market conditions, legislative or regulatory actions, the COVID-19 pandemic, natural events, or other disruption, could prevent us from meeting our contractual commitments and harm our business and financial results.

Our supply of crude helium for purification and resale is largely dependent upon natural gas production by crude helium suppliers. Lower natural gas production resulting from natural gas pricing dynamics, supplier operating or transportation issues, or other interruptions in sales from crude helium suppliers, can reduce our supplies of crude helium available for processing and resale to customers.

14

We typically contract to pass-through cost increases in energy and raw materials to customers, but such cost pass-through results in declining margins, and cost variability can negatively impact our other operating results. For example, we may be unable to raise prices as quickly as costs rise, or competitive pressures may prevent full recovery of such costs. In addition, increases in energy or raw material costs that cannot be passed on to customers for competitive or other reasons may negatively impact our revenues and earnings. Even where costs are passed through, price increases can cause lower sales volume.

New technologies create performance risks that could impact our financial results or reputation.

We are continually developing and implementing new technologies and product offerings. Existing technologies are being implemented in products and designs or at scales beyond our experience base. These technological expansions can create nontraditional performance risks to our operations. Failure of the technologies to work as predicted, or unintended consequences of new designs or uses, could lead to cost overruns, project delays, financial penalties, or damage to our reputation. In addition, gasification and other large-scale projects may contain processes or technologies that we have not operated at the same scale or in the same combination, and although such projects generally include technologies and processes that have been demonstrated previously by others, such technologies or processes may be new to us and may introduce new risks to our operations. Additionally, there is also a risk that our new technologies may become obsolete and replaced by other market alternatives. Performance difficulties on these larger projects may have a material adverse effect on our operations and financial results. In addition, performance challenges may adversely affect our reputation and our ability to obtain future contracts for gasification projects.

Protecting our intellectual property is critical to our technological development and we may suffer competitive harm from infringement on such rights.

As we develop new technologies, it is critical that we protect our intellectual property assets against third-party infringement. We own a number of patents and other forms of intellectual property related to our products and services. As we develop new technologies there is a risk that our patent applications may not be granted, or we may not receive sufficient protection of our proprietary interests. We may also expend considerable resources in defending our patents against third-party infringement. It is critical that we protect our proprietary interests to prevent competitive harm.

Legal and Regulatory Risks

Legislative, regulatory, and societal responses to global climate change create financial risk.

We are the world’s leading supplier of hydrogen, the primary use of which is the production of ultra-low sulfur transportation fuels that have significantly reduced transportation emissions and helped improve human health. To make the high volumes of hydrogen needed by our customers, we use steam methane reforming, which produces carbon dioxide. In addition, gasification enables the conversion of lower value feedstocks into cleaner energy and value-added products; however, our gasification projects also produce carbon dioxide. Some of our operations are within jurisdictions that have or are developing regulatory regimes governing GHG emissions, including CO2, which may lead to direct and indirect costs on our operations. Furthermore, some jurisdictions have various mechanisms to target the power sector to achieve emission reductions, which often result in higher power costs.

Increased public concern and governmental action may result in more international, U.S. federal and/or regional requirements to reduce or mitigate the effects of GHG emissions. Although uncertain, these developments could increase our costs related to consumption of electric power, hydrogen production and application of our gasification technology. We believe we will be able to mitigate some of the increased costs through contractual terms, but the lack of definitive legislation or regulatory requirements prevents an accurate estimate of the long-term impact these measures will have on our operations. Any legislation or governmental action that limits or taxes GHG emissions could negatively impact our growth, increase our operating costs, or reduce demand for certain of our products.

15

Our financial results may be affected by various legal and regulatory proceedings, including antitrust, tax, environmental, or other matters.

We are subject to litigation and regulatory investigations and proceedings in the normal course of business and could become subject to additional claims in the future, some of which could be material. While we seek to limit our liability in our commercial contractual arrangements, there are no guarantees that each contract will contain suitable limitations of liability or that limitations of liability will be enforceable. Also, the outcome of existing legal proceedings may differ from our expectations because the outcomes of litigation, including regulatory matters, are often difficult to predict reliably. Various factors or developments can lead us to change current estimates of liabilities and related insurance receivables, where applicable, or make such estimates for matters previously not susceptible to reasonable estimates, such as a significant judicial ruling or judgment, a significant settlement, significant regulatory developments, or changes in applicable law. A future adverse ruling, settlement, or unfavorable development could result in charges that could have a material adverse effect on our financial condition, results of operations, and cash flows in any particular period.

Costs and expenses resulting from compliance with environmental regulations may negatively impact our operations and financial results.

We are subject to extensive federal, state, local, and foreign environmental and safety laws and regulations concerning, among other things, emissions in the air; discharges to land and water; and the generation, handling, treatment, and disposal of hazardous waste and other materials. We take our environmental responsibilities very seriously, but there is a risk of adverse environmental impact inherent in our manufacturing operations and in the transportation of our products. Future developments and more stringent environmental regulations may require us to make additional unforeseen environmental expenditures. In addition, laws and regulations may require significant expenditures for environmental protection equipment, compliance, and remediation. These additional costs may adversely affect our financial results. For a more detailed description of these matters, see Item 1, Business–Environmental Regulation, above.

A change of tax law in key jurisdictions could result in a material increase in our tax expense.

The multinational nature of our business subjects us to taxation in the United States and numerous foreign jurisdictions. Due to economic and political conditions, tax rates in various jurisdictions may be subject to significant change. Our future effective tax rates could be affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities, or changes in tax laws or their interpretation.

Changes to income tax laws and regulations in any of the jurisdictions in which we operate, or in the interpretation of such laws, could significantly increase our effective tax rate and adversely impact our financial condition, results of operations, or cash flows. Various levels of government, including the U.S. federal government, are increasingly focused on tax reform and other legislative action to increase tax revenue. Further changes in tax laws in the U.S. or foreign jurisdictions where we operate could have a material adverse effect on our business, results of operations, or financial condition.

General Risk Factors

Catastrophic events could disrupt our operations or the operations of our suppliers or customers, having a negative impact on our business, financial results, and cash flows.

Our operations could be impacted by catastrophic events outside our control, including severe weather conditions such as hurricanes, floods, earthquakes, storms, epidemics, pandemics, acts of war, and terrorism. Any such event could cause a serious business disruption that could affect our ability to produce and distribute products and possibly expose us to third-party liability claims. Additionally, such events could impact our suppliers, customers, and partners, which could cause energy and raw materials to be unavailable to us, or our customers to be unable to purchase or accept our products and services. Any such occurrence could have a negative impact on our operations and financial results.

16

The United Kingdom’s (“UK”) exit from European Union (“EU”) membership could adversely affect our European Operations.

Although the UK’s exit from EU membership on 31 January 2021 ("Brexit") did not result in material disruptions to customer demand, our relationships with customers and suppliers, or our European business, the ultimate effects of Brexit on us are still difficult to predict. Adverse consequences from Brexit may include greater restrictions on imports and exports between the UK and EU members and increased regulatory complexities. Any of these factors could adversely affect customer demand, our relationships with customers and suppliers, and our European business overall.

Inability to compete effectively in a segment could adversely impact sales and financial performance.

We face strong competition from large global competitors and many smaller regional competitors in many of our business segments. Introduction by competitors of new technologies, competing products, or additional capacity could weaken demand for, or impact pricing of our products, negatively impacting financial results. In addition, competitors’ pricing policies could affect our profitability or market share.

Item 1B. Unresolved Staff Comments.

We have not received any written comments from the Commission staff that remain unresolved.

Item 2. Properties.

Air Products and Chemicals, Inc. owns its principal administrative offices in Trexlertown, Pennsylvania, and the Company's new global headquarters and co-located research and development facility in Allentown, Pennsylvania, as well as regional offices in Hersham, England; Medellin, Colombia; and Santiago, Chile. We lease the principal administrative offices in Shanghai, China; Pune, India; Vadodara, India; and Dhahran, Saudi Arabia. We lease administrative offices in the United States, Canada, Spain, Malaysia, and China for our Global Business Support organization.

Descriptions of the properties used by our five business segments are provided below. We believe that our facilities are suitable and adequate for our current and anticipated future levels of operation.

Industrial Gases – Americas

This business segment currently operates from over 425 production and distribution facilities in North and South America. Approximately 25% of these facilities are located on owned property and 10% are integrated sites that serve dedicated customers as well as merchant customers. We have sufficient property rights and permits for the ongoing operation of our pipeline systems in the Gulf Coast, California, and Arizona in the United States and Alberta and Ontario in Canada. Management and sales support is based in our Trexlertown, Medellin, and Santiago offices referred to above, and at 12 leased properties located throughout North and South America.

Industrial Gases – EMEA

This business segment currently operates from over 200 production and distribution facilities in Europe, the Middle East, India, and Africa, approximately one-third of which are on owned property. We have sufficient property rights and permits for the ongoing operation of our pipeline systems in the Netherlands, the United Kingdom, Belgium, France, and Germany. Management and sales support for this business segment is based in Hersham, England, referred to above; Barcelona, Spain; and at 16 leased regional office sites and 15 leased local office sites, located throughout the region.

Industrial Gases – Asia

This business segment currently operates from over 200 production and distribution facilities within Asia, approximately 25% of which are on owned property or long-duration term grants. We have sufficient property rights and permits for the ongoing operation of our pipeline systems in China, South Korea, Taiwan, Malaysia, Singapore, and Indonesia. Management and sales support for this business segment is based in Shanghai, China, and Kuala Lumpur, Malaysia, and in 30 leased office locations throughout the region.

17

Industrial Gases – Global

Management, sales, and engineering support for this business segment is based in our principal administrative offices noted above.

Equipment is manufactured in Missouri in the United States and Shanghai, China.

Research and development activities are primarily conducted at owned locations in the United States, the United Kingdom, and Saudi Arabia.

Helium is processed at multiple sites in the United States and then distributed to and from transfill sites globally.

Corporate and other

Corporate administrative functions are based in our administrative offices referred to above.

The LNG business operates a manufacturing facility in Florida in the United States with management, engineering, and sales support based in the Trexlertown offices referred to above.

The Gardner Cryogenic business operates at facilities in Pennsylvania and Kansas in the United States.

The Rotoflow business operates manufacturing and service facilities in Texas and Pennsylvania in the United States with management, engineering, and sales support based in the Trexlertown offices referred to above and a nearby leased office.

Item 3. Legal Proceedings.

In the normal course of business, we and our subsidiaries are involved in various legal proceedings, including commercial, competition, environmental, intellectual property, regulatory, product liability, and insurance matters. Although litigation with respect to these matters is routine and incidental to the conduct of our business, such litigation could result in large monetary awards, especially if compensatory and/or punitive damages are awarded. However, we believe that litigation currently pending to which we are a party will be resolved without any material adverse effect on our financial position, earnings, or cash flows.

From time to time, we are also involved in proceedings, investigations, and audits involving governmental authorities in connection with environmental, health, safety, competition, and tax matters.

We are a party to proceedings under CERCLA, RCRA, and similar state and foreign environmental laws relating to the designation of certain sites for investigation or remediation. Presently there are 31 sites on which a final settlement has not been reached where we, along with others, have been designated a potentially responsible party by the Environmental Protection Agency or is otherwise engaged in investigation or remediation, including cleanup activity at certain of its current and former manufacturing sites. We do not expect that any sums we may have to pay in connection with these environmental matters would have a material adverse impact on our consolidated financial position. Additional information on our environmental exposure is included under Item 1, Business–Environmental Regulation, and Note 16, Commitments and Contingencies, to the consolidated financial statements.

In September 2010, the Brazilian Administrative Council for Economic Defense ("CADE") issued a decision against our Brazilian subsidiary, Air Products Brasil Ltda., and several other Brazilian industrial gas companies for alleged anticompetitive activities. CADE imposed a civil fine of R$179.2 million (approximately $33 million at 30 September 2021) on Air Products Brasil Ltda. This fine was based on a recommendation by a unit of the Brazilian Ministry of Justice, following an investigation beginning in 2003, which alleged violation of competition laws with respect to the sale of industrial and medical gases. The fines are based on a percentage of our total revenue in Brazil in 2003.

18

We have denied the allegations made by the authorities and filed an appeal in October 2010 with the Brazilian courts. On 6 May 2014, our appeal was granted and the fine against Air Products Brasil Ltda. was dismissed. CADE has appealed that ruling and the matter remains pending. We, with advice of our outside legal counsel, have assessed the status of this matter and have concluded that, although an adverse final judgment after exhausting all appeals is possible, such a judgment is not probable. As a result, no provision has been made in the consolidated financial statements. In the event of an adverse final judgment, we estimate the maximum possible loss to be the full amount of the fine of R$179.2 million (approximately $33 million at 30 September 2021) plus interest accrued thereon until final disposition of the proceedings.

Additionally, Winter Storm Uri, a severe winter weather storm in the U.S. Gulf Coast in February 2021, disrupted our operations and caused power and natural gas prices to spike significantly in Texas. We are currently in the early stages of litigation of a dispute regarding energy management services related to the impact of this unusual event, and other disputes may arise from such power price increases. In addition, legislative action may affect power supply and energy management charges. While it is reasonably possible that we could incur additional costs related to power supply and energy management services in Texas related to the winter storm, it is too early to estimate potential losses, if any, given significant unknowns resulting from the unusual nature of this event.

Other than the matters discussed above, we do not currently believe there are any legal proceedings, individually or in the aggregate, that are reasonably possible to have a material impact on our financial condition, results of operations, or cash flows. However, a future charge for regulatory fines or damage awards could have a significant impact on our net income in the period in which it is recorded.

Item 4. Mine Safety Disclosures.

Not applicable.

19

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities.

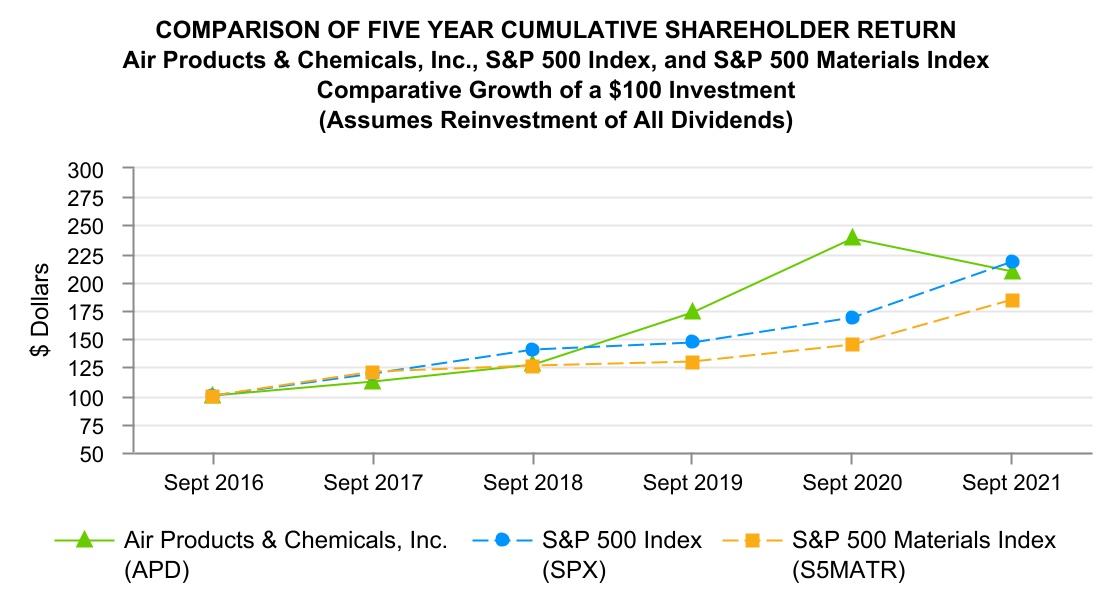

Our common stock is listed on the New York Stock Exchange under the symbol "APD." As of 31 October 2021, there were 4,722 record holders of our common stock.

Cash dividends on our common stock are paid quarterly. It is our expectation that we will continue to pay cash dividends in the future at comparable or increased levels. The Board of Directors determines whether to declare dividends and the timing and amount based on financial condition and other factors it deems relevant. Dividend information for each quarter of fiscal years 2021 and 2020 is summarized below:

| 2021 | 2020 | |||||||

| Fourth quarter | $1.50 | $1.34 | ||||||

| Third quarter | $1.50 | $1.34 | ||||||

| Second quarter | $1.50 | $1.34 | ||||||

| First quarter | $1.34 | $1.16 | ||||||

| Total | $5.84 | $5.18 | ||||||

Purchases of Equity Securities by the Issuer