Exhibit 10.1

Congratulations on your new assignment!

In addition to the challenges your new position brings, you and your family will encounter many changes as you leave familiar surroundings, find a new place to live and settle into your new location.

The relocation of employees contributes to the Company’s ability to stay flexible and competitive. For that reason, we have partnered with Bristol Global Mobility, as well as a number of other top rate service providers, to provide you with a program of relocation support to reduce normal move disruptions and enable you to get settled in your new home and job as quickly as possible.

This Relocation Guide outlines the services made available to you to help facilitate your move, including selling your current residence and finding a new community and home.

Please take the time to read through this guide and familiarize yourself with the policy and Bristol Global Mobility relocation services before you begin planning your relocation. Recognizing that relocating can be a disruptive time, the Company, through your dedicated Mobility Advisor, will assist you and your family throughout your move.

Our best wishes for success in your new location!

1 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

BENEFITS AT A GLANCE

Policy Component | Description |

Eligibility | · You are eligible for coverage under the relocation program described in this guide if you are classified as an active full-time current or newly-hired, salaried executive level employee or senior officer; homeowner or renter, whose new position increases your commute by 50 miles. It is your responsibility to work with the Sr. Manager Human Resources to monitor your eligibility for benefits and to ensure your status is accurately reflected in the payroll system. Relocation benefits are valid for one year from the date of relocation initiation. Relocation will be paused for any leaves of absence. |

Miscellaneous Allowance | · You will receive an allowance of $10,000 to cover expenses not provided elsewhere in the policy · Such payment will not be grossed-up |

Home Finding Trips | · Professional assistance will be provided by Bristol Global Mobility · The Company will provide you with two home finding trips for up to a total of seven days/six nights, for you, your spouse or one additional family member and for your children. · Reimbursable expenses include reasonable costs associated with: o Airfare (or Mileage/Fuel) o Lodging o Reasonable meal expenses (excludes alcohol) o Rental car · Accompanied rental tours for those who plan to rent |

Temporary Housing | · Professional assistance will be provided by Bristol Global Mobility · The Company will provide you with temporary housing accommodations for up to 120 days · Up to 14 days rental car if automobile is being shipped |

Home Sale Assistance: GBO/Amended Value Sale | · Marketing Assistance · Appraised Value Offer · Amended Value Sale · Independent Sale |

Renter Services | · Lease Cancellation: Up to two months’ rent if required to cover lease cancellation or lease break fees |

New Home Purchase Assistance | · If you decide to purchase a home in the new location, you will be reimbursed for normal and customary new home purchase closing costs |

Movement of Household Goods | · A professional van line will be selected and coordinated by Bristol Global Mobility · Van line will pack, load, transport, unload goods, and unpack, including normal appliance servicing · The Company will provide: o Debris pick up o Storage for up to 120 days o Up to $125,000 of valuation coverage o Shipment for up to two automobiles if the distance to the new location is over 500 miles |

Final Trip to the Destination Location | · You and your family will be reimbursed for en route expenses from the departure location to the destination location. Reimbursable expenses include reasonable costs associated with: o Airfare if vehicle(s) is/are shipped o Lodging – 1 night in origin, en route o Mileage – 1 vehicle if 1 is shipped or 2 vehicles if none are shipped o Reasonable meal expenses (excluding alcohol) · You must travel a minimum of 300 miles per day by the most direct route |

3 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

INTRODUCTION

This handbook has been designed to help you understand Dollar General’s relocation program and to assist you and your family in relocating as quickly as possible with minimal inconvenience. You are encouraged to carefully read this handbook in its entirety. Recognizing that relocating can be a disruptive process, the Company and Bristol Global Mobility will assist you and your family throughout your move.

Eligibility

The relocation program was developed to facilitate the movement of active, full-time newly-hired and current, salaried, executive-level employees or senior officers who are requested to relocate by the Company and designated by the Company to receive the benefits described in this handbook.

In order to be eligible for relocation as described in this handbook, the distance between your former residence and your new job site must be at least 50 miles greater than the distance between your former residence and your former job site.

Family

Your family members eligible for assistance under this policy include your spouse and your dependent household members. In the event an additional member of your household is asked to relocate by the Company, you are eligible to receive only one set of benefits.

Disclaimer

The Company has the sole right at any time to revise, amend or discontinue this policy. This policy shall not be considered or construed as an employment contract and does not constitute a guarantee of employment for any minimum or specified period of time.

Policy Exceptions

If you feel an exception is needed, please submit your request in writing to your Bristol Global Mobility dedicated Mobility Advisor. They will review and forward your request to the Relocation Department at Dollar General for consideration. Upon initial receipt, the Relocation Department will present a recommendation along with facts to the appropriate senior level officer for final approval by the Dollar General Board of Directors’ Compensation Committee. The Compensation Committee may delegate certain waiver authority to the Dollar General CEO under enumerated parameters from time to time. Your dedicated Mobility Advisor will communicate the decision to you.

RELOCATION ADMINISTRATION

Upon notification of your relocation, your dedicated Mobility Advisor will be your main point of contact throughout your move. Your dedicated Mobility Advisor will guide you through each step of the relocation process, answer your questions, and help coordinate all aspects of your move. Listed below are highlights of the services your dedicated Mobility Advisor will provide to you:

| ● | general information |

| ● | expense report reimbursements |

| ● | disposition of your present home |

| ● | assistance in finding a new residence |

4 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

| ● | moving your household goods |

| ● | moving you and your family to the new location |

We encourage you to become fully involved in your move and work closely with the professionals who have been made available to assist you throughout the relocation process. By working closely with your dedicated Mobility Advisor, you will be able to effectively manage your move.

Forms to Complete

Our goal is to have a relocation process that is as simple and easy to use as possible. Therefore, there are only two steps that you must complete before receiving your relocation benefits.

Step 1.Complete and return the Relocation Initiation Form

The Relocation Initiation Form provides us with important information to pass on to the moving company and for relocation check/reimbursement requests.

Step 2.Complete and return the Employee Reimbursement Form.

The Employee Reimbursement Form states that you have read Dollar General’s Relocation policy and understand that you are responsible for any expenses not covered under the policy. This form may also have a reimbursement schedule you would follow to pay back a pro-rated share of your relocation benefits should you leave the company within a year of the date of your last relocation reimbursement or last relocation expense incurred by Dollar General.

Both of these forms can be emailed to Relocation@DollarGeneral.com.

EXPENSES AND REIMBURSEMENT

Most ordinary expenses involved in moving from one location to another are covered under this policy. Any questions of interpretation should be discussed with your dedicated Mobility Advisor in advance.

All relocation expenses must be submitted through the Bristol Global Mobility expense portal and must be separate from any regular business expenses. Expenses submitted through Concur or charged to the corporate credit card will not be eligible for reimbursement. In order to determine the federal and state tax liability for reimbursed expenses, all relocation expenses must be reported accurately.

Where relocation-related expenses are specifically reimbursable, consistent guidelines apply.

| ● | All reimbursable expenses must be reasonable and appropriate. |

| ● | All relocation benefits are reflected in U.S. dollars. |

| ● | All reimbursable moving expenses must be incurred within 24 months from the effective date of employment or transfer and submitted for payment within 90 days from the date the expense is incurred. |

| ● | Only expenses specifically outlined in the policy will be reimbursed. |

5 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

| ● | You must submit original receipts for reimbursement. Your completed expense reports together with your original receipts should be forwarded directly to your dedicated Mobility Advisor. |

| ● | It is important not to include any business expenses on relocation expense forms. |

Miscellaneous Expense Allowance

The Company will provide you with a Miscellaneous Expense Allowance equal to $10,000, to cover many of the incidental expenses not specifically reimbursed under this policy, which may occur as a direct result of your transfer. Some examples of these expenses include:

| ● | driver’s licenses and automobile registrations in the new location, |

| ● | meals during temporary living, |

| ● | duplicate mortgage beyond that covered in the policy, |

| ● | utility deposits, |

| ● | shipment of pets, |

| ● | crating and special shipment of oversized fragile items such as artwork, |

| ● | cleaning or maid service (new or old location), |

| ● | non-refundable tuition, memberships, club dues or subscriptions, |

| ● | piano tuning, |

| ● | tips to movers, |

| ● | drapery and carpet installation or alterations, |

| ● | television or cable installation or adjustments, |

| ● | overnight mail charges, |

| ● | tax consulting, |

| ● | items unique to your personal move not covered by this policy, |

| ● | disassemble/reassemble playground, gym equipment, swimming pools, and similar items. |

For newly hired employees, your miscellaneous expense allowance will be deposited into your account within 2 weeks after your start date.

Tax Assistance

Gross-up will not be provided for the Miscellaneous Expense Allowance.

DESTINATION LOCATION

Home Finding Trips

Whether you are a homeowner or a renter, selecting a new community and home is one of the most important decisions you will make as a result of your job transfer. The Company’s relocation program offers you professional home finding counseling through Bristol Global Mobility. The Company encourages you to take advantage of this valuable service.

Your dedicated Mobility Advisor will discuss your family’s specific needs, preferences, and lifestyle. After review of your requirements, your dedicated Mobility Advisor will select a local real estate professional who is experienced in the areas of interest to you.

Remember to contact your dedicated Mobility Advisor prior to contacting any real estate agent in the new location. |

6 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Your dedicated Mobility Advisor and real estate agent will work together to organize a productive home finding trip. By planning in advance, the agent will be prepared to take you on area tours and discuss items of interest to you and your family. Preparation gives you a better chance of quickly finding a residence to fit your needs at a price you can afford.

Once your real estate agent is contacted, he or she will provide the following information:

| ● | schools, churches, etc., |

| ● | commuting times, |

| ● | child and elder care services, and |

| ● | pre-selected homes for viewing |

If you are a current homeowner, you should delay house hunting in the new location until you have an estimated value on your present home and you have been pre-qualified by a mortgage lender. Home purchase decisions made with unrealistic expectations of current equity may result in over-commitment at the new location.

Dollar General will provide you and your spouse or one additional household member and your children with two (2) home finding trips for a total of seven (7) days. The home finding trip will include the following:

| ● | Hotel accommodations for a maximum six (6) nights total. |

| ● | Airfare or mileage reimbursement at current Company rate if personal vehicle is driven. |

| ● | Reimbursement for rental car for maximum of seven (7) days. |

| ● | Reimbursable meal expenses (excluding alcohol) (original receipts must be submitted). |

Tax Assistance

Gross-up will be provided for home finding trip expenses.

Internet Home Search

Although the Internet can be a useful tool to gain information on housing in the new area, keep in mind you need to use the approved real estate agent assigned to you to obtain information or to view any home you find on the Internet. This will avoid confusion as to which agent you are working with and any possible real estate commission disputes.

Temporary Living

Temporary Living Assistance is intended only for short-term living arrangements at the new location. Dollar General will reimburse you for up to 120 days of temporary living expenses. Temporary living assistance includes the following:

| ● | One bedroom fully furnished corporate apartment for employee only. |

| ● | If trailing family, a two bedroom fully furnished corporate apartment may be requested in lieu of a one bedroom |

| ● | Reimbursement for full size rental car for a maximum of two (2) weeks. |

If you require temporary living assistance, please contact your dedicated Mobility Advisor at least two weeks in advance. He or she will be happy to help you make arrangements and answer any questions you may have.

7 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Return Trip

If you are required to report to work in your new location prior to your family’s final move, Dollar General will reimburse travel expenses for one (1) return trip home per month up to a total of 3 round trips during the temporary living period. One family member may visit you in the new location in lieu of a return trip.

Tax Assistance

Gross-up will be provided for temporary living and return trip expenses.

HOME SALE ASSISTANCE PROGRAM

Your dedicated Mobility Advisor will provide you with the necessary expertise to facilitate the sale of your home through the services described below.

Home Eligibility

A home eligible for home sale assistance is any completed single-family or two-family residence, including a condominium that is used as your principal residence and that is owned by you, your spouse, any of your dependents residing in the same household, or any combination of those persons at the time you are asked to relocate. This also includes land customarily considered part of a residential lot and all personal property normally sold with a residence according to local custom. If your home does not meet these eligibility guidelines, you may qualify for reimbursement of certain home sale closing costs and commission expenses if you sell your primary residence on your own.

Homes considered ineligible for home sale assistance (Guaranteed Buyout Offer/Buyer Value Option) include, but are not limited to, the following:

| ● | cooperative apartments, |

| ● | mobile homes, |

| ● | vacation/secondary homes, |

| ● | investment properties, |

| ● | homes with excessive acreage (+5 acres), |

| ● | homes that are partially completed or under substantial renovation, |

| ● | homes ineligible for conventional financing, |

| ● | houseboats, |

| ● | homes deemed ineligible through building inspections, and |

| ● | vacant lots appraised as contributory value only. |

If you have any questions regarding your home’s eligibility, please contact your dedicated Mobility Advisor prior to beginning the relocation process.

8 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Marketing Your Home

You are required to speak with your dedicated Mobility Advisor prior to taking any steps to list or market your home. You are required to market your home for a minimum of 90 days from the date your home is listed with an approved real estate agent. |

The advantage to successfully marketing your home and selling to an outside buyer is that you may receive a greater cash return than the Appraised Value Offer.

As soon as the Company authorizes your relocation, your dedicated Mobility Advisor will contact you to explain the first step—the listing, marketing, and appraisal of your home. Placing your home on the market as advantageously as possible is a critical element in successfully marketing your home. Your dedicated Mobility Advisor will help you select a qualified real estate agent and together they will determine selling strategies targeted to help you receive the best possible offer for your home. Throughout the home sale process, your dedicated Mobility Advisor will continuously track your agent’s efforts to market your home. The goal of these efforts is to help you obtain the best offer for your home within a reasonable time frame.

Your dedicated Mobility Advisor’s objectives are to:

| ● | help you identify a qualified and active broker to assist you in marketing and listing your home in a highly effective manner |

| ● | work with your real estate agent to develop a strategic marketing plan to sell your home at the best possible market value |

| ● | in conjunction with your real estate agent, suggest any minor repairs and/or improvements that will increase the marketability of your home |

| ● | work with you throughout the process of you selling your home |

Following is a step-by-step process of marketing assistance services provided by your dedicated Mobility Advisor.

Agent Selection

Your dedicated Mobility Advisor will place a referral with two (2) area real estate agents who will visit your home and prepare a complete Employee Relocation Council (ERC) Market Analysis. If you would like to designate a particular real estate agent that has not been recommended, please notify your dedicated Mobility Advisor. As long as the real estate agent agrees to the program’s requirements, he or she will be able to work with you as one of your two selected agents. You may not utilize or ask to have qualified any real estate agent that is a family member, i.e., spouse, child, mother, father, brother, sister, or in-laws. If you have no preference or are not familiar with local brokers, your dedicated Mobility Advisor will assist you in the selection.

Listing Your Home

Your dedicated Mobility Advisor will ask you to select one real estate agent from the two you have interviewed. He or she will then work with you and your selected agent to develop a marketing strategy and establish a list price that is both attractive and realistic in the local market.

9 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

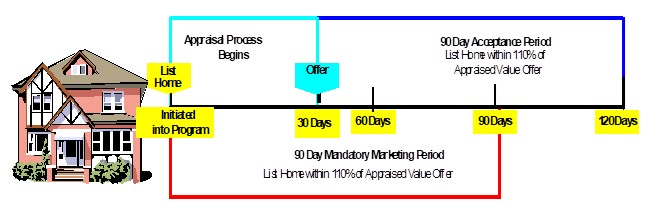

Listing Exclusion Clause

You are required to list your home within 110% Appraised Value. You are required to list your home for a minimum of 90 days from the initial list date before you are eligible to accept the Appraised Value Offer. |

When you speak with your dedicated Mobility Advisor, he or she will discuss the necessity of including the following language in the listing agreement with your broker. The reason for this clause is to allow for cancellation of the listing agreement if necessary for Bristol Global Mobility to close with the buyer. This clause is considered “standard operating procedure” among agents who work with corporate transferees. The following Exclusion Clause should be attached as an addendum to the Listing Agreement.

“In the event of any conflict or inconsistency between this Addendum and the Listing Agreement, the terms of this Addendum shall control. It is understood and agreed that regardless of whether or not an offer is presented by a ready, willing, and able buyer: 1.No commission or compensation shall be earned by, or be due and payable to, broker until the sale of the property has been consummated between seller and buyer, the deed delivered to the buyer and the purchase price delivered to the seller; and 2.The seller reserves the right to sell the property to Bristol Global Mobility or to: ____________ (individually and collectively a “Named Prospective Purchaser”) at any time. Upon the execution by a Named Prospective Purchaser and me (us) of an Agreement of Sale with respect to the property, this listing agreement shall immediately terminate without obligation of my (our) part or on the part of any Named Prospective Purchaser to either pay a commission or to continue this listing.” | ||

| | |

Real Estate Agent | | Date |

| | |

| | |

Seller | | Date |

| | |

| | |

Seller | | Date |

Monitoring the Marketing Process

Your dedicated Mobility Advisor will work with you and your real estate agent throughout the marketing process to ensure maximum exposure for your home, provide feedback on the marketing process, and recommend strategy modifications, if needed.

10 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Negotiating a Sale

When you have an interested buyer and receive an offer, your dedicated Mobility Advisor will be a valuable resource as you negotiate a price and an Offer Letter. You must submit ALL offers received to your dedicated Mobility Advisor for review and consideration. DO NOT SIGN a contract (or any other document) with the buyers or take any money as a deposit from the real estate agent or prospective buyer. |

Amended Value Sale

If you receive a qualified offer on your home from an outside buyer, you have an opportunity to “amend” the Appraised Value Offer from Bristol Global Mobility to reflect your buyer’s offer.

Finalizing a Sale

Your dedicated Mobility Advisor will handle the details of the real estate transaction once the terms of the sales agreement have been finalized.

APPRAISED VALUE OFFER

Your decision to relocate should not be hampered by concerns about selling your home. Bristol Global Mobility will assist you by making an Appraised Value Offer to purchase your home at a value established by independent fee appraisers. The appraisal process will begin immediately after entering the relocation program. This offer will be your “safety net” providing you with a guaranteed price, should your home not sell on the open market.

Appraiser Selection

Your dedicated Mobility Advisor will provide a list of ERC endorsed appraisers in your area to choose from. Once you have notified your dedicated Mobility Advisor of your choice of two appraisers, your dedicated Mobility Advisor will notify the approved appraisers to contact you in order schedule a convenient time to survey your home.

Relocation Appraisal

A relocation appraisal is an estimate of the anticipated sales price of your home over a reasonable selling period. Relocation Appraisers estimate value primarily by comparing your home to the sales of similar properties making detailed adjustments for the differences between those properties and your home. The appraisers consider location, size, age, condition, and marketability.

When the appraisers arrive to inspect your home, you should be prepared to discuss any facts that may be important in determining the value of your home:

| ● | any improvements you have made to the home that may or may not be visible to the appraisers; and |

| ● | any information on similar homes that have recently sold in your area. |

Your home will be appraised in “as is” condition, so it is important your home shows favorably to maximize the appraised value and resale efforts. Your dedicated Mobility Advisor and your real estate agent will assist in suggesting specific fix-up items to help maximize your marketing efforts.

11 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

The appraisers may also ask for a copy of the land survey and a copy of the title policy that you received when you closed on your home. They will need these items to obtain the correct legal description.

Determining the Appraised Value Offer

Your Appraised Value Offer will be equal to the average of two independent relocation appraisals. However, if the variance between the two appraisals is greater than 5% of the higher amount, a third relocation appraisal will be ordered. In this case, your offer will be determined by averaging the two closest appraisals. Normal and customary home inspections will be ordered at the time of the appraisals.

Your dedicated Mobility Advisor will present you with your Appraised Value Offer once the inspection and appraisal reports have been received and reviewed. Your home will have to

You are required to list your home at no more than 110% of the Appraised Value Offer. This may require you to make an adjustment to your most current list price. |

pass all inspections and/or you must satisfactorily remedy any deficiencies before your offer is finalized. The entire process should be completed within 30 days from the date of the last inspection.

Title Search

In addition to arranging for the appraisals and inspections, a title search will be initiated in order to prepare for closing. You may need to be involved in clearing any title issues should they appear on the title report. Please inform your real estate agent that Bristol Global Mobility is bringing the title up-to-date. This can avoid a duplicate title search. Often an agent will arrange for a title search upon notification from a lender of a buyer’s loan approval.

Offer Period

Your dedicated Mobility Advisor will call you with your Appraised Value Offer and outline the timing and process of the home sale program. The Appraised Value Offer has a 90-day acceptance period—90 days to continue marketing your home knowing you have a set “safety net”. Your 90-day acceptance period begins the day your Offer Letter is postmarked. You may accept the appraised value offer at any time after marketing your home for 90 days.

12 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

You are required to market your home for 90 days from the list date before you can accept the Appraised Value Offer. |

Accepting the Appraised Value Offer

If you are unable to sell your home during the 90-day offer period and accept the Appraised Value Offer, you and your spouse should sign the Bristol Global Mobility Offer Letter and return both copies to your dedicated Mobility Advisor along with the other supporting documents. Your execution of the Offer Letter is a legal transaction. You will need to sign and notarize the Offer Letter and other related documents.

The signed Bristol Global Mobility Offer Letter and related documents must be received by your dedicated Mobility Advisor on or prior to the expiration date of your offer. The contract will be dated on the day all necessary documents are completed and signed by you and your dedicated Mobility Advisor.

Vacating the Home

You have 60 days from the date you sign the Bristol Global Mobility Offer Letter in which to vacate the property provided a resale closing does not occur sooner. If you cannot move within 60 days, please let your dedicated Mobility Advisor know and you may be granted additional time to vacate if circumstances warrant.

After you and Bristol Global Mobility have signed the Offer Letter, you will continue to be responsible for the costs of maintenance, repairs, utilities, insurance, etc., until you actually vacate. Prior to vacating, you will be expected to cooperate fully with all attempts by Bristol Global Mobility to market the home by allowing prospective purchasers to view the premises by appointment during reasonable hours.

From the date you vacate, Bristol Global Mobility will make all future mortgage, tax, and other carrying payments on your home. It will also assume payment of maintenance and utility costs. Your equity statement will reflect mortgage interest through your executed Bristol Global Mobility contract or vacate date, whichever comes last.

Utilities

Since sudden cold weather can cause damage due to freezing, do not turn off any utilities when you vacate the home. The utilities must be left in your name until you contract with Bristol Global Mobility or vacate the home, whichever is later. At that time, you should request final readings from the utility companies serving your home. Your dedicated Mobility Advisor will instruct your real estate agent to transfer the utilities into the real estate company’s name until the home closes with new buyers. The day you vacate is customarily the date utilities are transferred to the real estate company. If you receive a utility bill covering a period of time when payment was not your responsibility, please submit the invoice to your dedicated Mobility Advisor for payment.

Insurance

You will need to cancel your homeowner’s insurance policy effective when Bristol Global Mobility signs the Offer Letter or you vacate, whichever is later. Any refund due to you from

13 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

the insurance company will be paid directly to you. Make note to discuss this with your insurance agent and follow-up if necessary.

If you are vacating your home prior to contracting with Bristol Global Mobility, contact your insurance agent to arrange coverage during any periods the home will be unoccupied. Most homeowner’s insurance policies state coverage is void if the dwelling is unoccupied for a specific period of time.

AMENDED VALUE SALE

Achieving an Amended Value Sale is of benefit to you and the Company. The Company avoids the significant expense of purchasing, maintaining, and reselling your home through

If at any time during your marketing period, you receive an offer through the efforts of your real estate agent, you must submit the offer to your dedicated Mobility Advisor. DO NOT SIGN a contract (or any other document) with the buyers or take any money as a deposit from the real estate agent or prospective buyer. |

Bristol Global Mobility and you receive the highest possible price for your home.

Advantages of an Amended Value Sale

| ● | You may receive a greater cash net return than the Appraised Value Offer. |

| ● | You will be relieved of the responsibilities of property ownership upon vacate or contract date with Bristol Global Mobility, whichever is later. |

| ● | You will be relieved of the necessity of closing with the buyer. |

| ● | After contracting with Bristol Global Mobility, you will be assured of receiving the net proceeds based upon the Amended Value Sale even if the original sale falls through and does not close. |

Analyzing the Offer

Your dedicated Mobility Advisor will review the terms of the offer in an effort to determine whether the offer is bona fide (made in good faith), and to confirm that it is not subject to the sale of the buyer’s property, does not contain any unusual or unreasonable terms, and is not subject to interim financing.

Amending the Offer Letter

Once the final offer has been approved, your dedicated Mobility Advisor will ask you to “amend” the amount in your Bristol Global Mobility Offer Letter to reflect the buyer’s offer and to sign and return the Offer Letter.

Buyer’s Offer Less Than Appraised Value Offer

At its discretion, the Company may also accept offers which are lower than your Appraised Value Offer. You will remain eligible to receive your equity calculation based on the Appraised Value Offer.

14 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Closing an Amended Value Sale

Bristol Global Mobility will acquire your home, according to the terms of the amended Bristol Global Mobility Offer Letter with you. Bristol Global Mobility will also fully honor the terms of the Purchase Agreement with the buyers.

Bristol Global Mobility will make every effort to close the transaction with the buyer. However, since Bristol Global Mobility has already purchased your home, you will not be impacted if the sale to the buyer is not eventually consummated. Your equity payment will be based upon the Amended Value Sale Price.

Responsibility for your property remains with you until you contract with Bristol Global Mobility or vacate, whichever is later. This includes maintenance of your home, payments for utilities, mortgage, taxes, and premiums for insurance.

Equity

Your equity is calculated as of the Bristol Global Mobility contract date or your scheduled vacate date, whichever is later, and is based upon the Amended Value sale price or guaranteed offer price, whichever is greater. You will need to coordinate the timing of your equity check with your dedicated Mobility Advisor. You may be eligible to receive an equity advance once you have signed the Bristol Global Mobility Offer Letter and when there is a specific need for funds to close on a new home in the destination area.

It is important to note that certain items are not covered under the policy and will be deducted from your final equity, if you have agreed to any of these additional seller’s expenses:

| ● | repairs and improvements requested by the buyer |

| ● | buyer’s closing costs |

| ● | homeowner warranties |

| ● | buyer’s incentives |

| ● | real estate commission above the standard rate for your area |

| ● | closing dates beyond 60 days of vacating or contracting with Bristol Global Mobility |

INDEPENDENT SALE

If your home is considered ineligible for the Company’s Home Sale Assistance Program (Buyer Value Option or Amended Value Offer) or you elect to sell your home independently prior to initiation into Bristol Global Mobility’s Home Sale Assistance Program, you may be eligible to receive direct reimbursement of normal and customary home sale closing costs and commission when you sell your home on your own. Contact your dedicated Mobility Advisor to determine if your home qualifies for this home sale option.

If your home is eligible for Bristol Global Mobility’s home sale assistance (Buyer Value Option or Amended Value Offer) and you sell your home on your own, the Company will not provide tax assistance for your home sale commission and closing cost expenses. |

15 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Reimbursement of Home Sale Expenses

Normal and customary home sale closing costs and real estate commission at the prevailing rate in your current location (maximum of 6%) will be reimbursed if you sell your home independently within twenty-four (24) months of your effective date of transfer.

Discount points incurred through negotiation with FHA, VA and conventional financing are not reimbursable.

Tax Assistance

You will receive tax assistance for normal and customary home sale closing costs and eligible commission expenses only if your home is ineligible for the Home Sale Assistance Program (Buyer Value Option or Amended Value Offer). If you choose to sell your home on your own, no tax assistance will be provided to you.

HOME PURCHASE CLOSING COST ASSISTANCE

If you are purchasing a residence in the new location, you will be reimbursed for reasonable and actual home purchase closing costs provided you sign a contract to purchase a home in the new area and close within one year of your employment effective date or effective date of transfer.

One time closing costs for permanent financing will be reimbursed including:

| ● | normal attorney’s fees, |

| ● | appraisal fees, |

| ● | tax service fees, |

| ● | title insurance (lender’s coverage, only), |

| ● | recording fees (including tax stamps), |

| ● | credit reports, |

| ● | survey fees, |

| ● | flood certification, and |

| ● | inspections required by the lender |

The Company does not cover one-time closing adjustments such as property taxes, home hazard insurance, fuel adjustments, or private mortgage insurance (PMI). The Company does not cover the costs associated with establishing second mortgages, home equity lines of credit or construction loans.

Tax Assistance

Gross-up will be provided for home purchase closing costs.

National Mortgage Lender Program

The Company has selected national mortgage lenders to provide you with a wide variety of mortgage services. Your dedicated Mobility Advisor will provide you with information on participating mortgage companies.

16 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

Using the services of these preferred lenders offers many advantages:

| ● | familiarity with the Company’s program, |

| ● | mortgage loan pre-approval process, |

| ● | direct billing of closing costs to the Company, and |

| ● | consideration of current spousal income |

New Construction

If you elect to build a home in the new location, you may incur additional expenses as opposed to purchasing an existing home. Be aware in making your decision that policy benefits will not be extended if you decide to build.

RENTERS’ ASSISTANCE

Lease Cancellation

If you are presently renting your home or apartment at the origination location, you should immediately notify your landlord or lease holder of your move to avoid or minimize penalty charges. You should attempt to obtain a written waiver of any provisions of the lease requiring fees or penalties due to your transfer. The Company asks that you make every effort to minimize the penalties by making the best possible arrangements with your landlord.

Should you be required to pay a penalty, the Company reimburses up to a maximum of two (2) months’ rent for any combination of lease termination penalty charges, forfeiture of lease deposit, and/or duplicate rent on your former home or apartment. If necessary, your dedicated Mobility Advisor can assist you with lease cancellation arrangements.

New Lease Agreement

Should you decided to rent a home or apartment in the destination location your new lease should be examined carefully before it is signed. You should negotiate a cancellation clause that would give you the right to cancel the lease without penalty after giving 30 days’ notice, in the event of a company-initiated transfer.

Sample Clause:

If tenant’s employer relocates tenant to a location more than fifty (50) miles from the premises that are the subject of this lease, this lease will be automatically terminated without further liability at any time. Tenant agrees to give landlord at least 30 days’ notice of his/her intention to terminate this lease along with proof of such transfer of employment.

Tax Assistance

Gross-up will be provided for renters’ assistance reimbursements.

MOVING TO THE NEW LOCATION

To enable you and your family to make an effective transition to the new area, the Company’s relocation program provides for a range of move-related assistance:

| ● | pre-move survey of your household goods by the moving company |

| ● | complete packing of all items |

| ● | transportation of your household goods to your new residence |

| ● | up to $125,000 in full replacement valuation coverage for your household goods |

17 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

| ● | unloading, unpacking, and placement of all furniture in your new residence |

| ● | storage of your household goods for up to 90 days, if required |

Shipment of Household Goods

You, or a representative appointed by you, will need to plan to be present during all phases of your move—pack, load, delivery, and unpacking. Your own planning, preparation, and involvement during the process will contribute to a successful move.

Items Excluded From Shipment

The items listed below are not ordinarily considered household goods and are your responsibility. The Company, Bristol Global Mobility, and the moving company will not be able to take responsibility for these items.

The Miscellaneous Expense Allowance is intended to assist you with expenses unique to your personal move and for items not covered by this policy. Please note the Company will not pay for the shipping of the following items. If you have any questions, contact your dedicated Mobility Advisor.

à boats à campers, trailers, motor homes à farm machinery à firewood, rocks, sand, soil, etc. à perishable food items, refrigerated or frozen à aerosol cans, flammable liquids, and other hazardous materials à lumber, bricks, blocks, cement, tiles and building materials | à airplanes à plants, animals à large playground equipment à tool or storage sheds, outdoor buildings à valuables such as jewelry, money, coins, coin and stamp collections, irreplaceable photos, stocks, bonds, deeds, wills, and other legal documents |

Playground and Similar Equipment

Playground, gym equipment, swimming pools, and similar items must be disassembled prior to your move day. If the movers disassemble and reassemble these items, you will be responsible for payment of these costs at the time of service.

Insurance

Your household goods are protected with up to $125,000 of full replacement valuation coverage.

Items of Extraordinary Value (Including Antiques)

It is recommended that items of extraordinary value such as antiques, fine art, furs, silver, china, crystal, photography equipment, oriental rugs, baseball cards, comics, other collectibles, etc. be professionally appraised prior to your move. If purchased within the last year, the value can be substantiated with a sales receipt. The Company will not pay for appraisals or any special handling and packaging of antiques or other high-value items.

Packing and Loading

Careful packing and proper loading are very important steps in assuring a successful move. It is important that the mover packs all your household goods. The driver will prepare a

18 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

complete inventory list of your household goods describing the condition of each item (nicks, scratches, dents, etc.). Review the inventory carefully to make sure you agree with the driver’s description before you sign the inventory. The inventory is an important document in the settlement of claims for loss and damage.

Unloading

Check with the van driver about delivery times at the new location. Be sure to give them all possible telephone numbers where you can be reached en route and in the new location.

As your goods are being unloaded, you must check off each item on your inventory sheets. Make notations on the sheets of missing or damaged items immediately and have the driver sign it. Assembly of furniture will be completed prior to the driver leaving your home. Unpacking of your goods consists of removing the items from the cartons in the room for which they are labeled. This does not include putting items away. Disposal of cartons is included in the move services.

Billing

The van line will send the invoice for your move directly to Bristol Global Mobility. If you transport household goods not covered by the policy or incur unauthorized charges, you will be expected to pay for these items at the time of delivery.

Tipping

Tips to the movers are not covered under this policy. Your Miscellaneous Expense Allowance is designed to offset costs associated with tipping.

Shipment of Automobiles

The Company will reimburse mileage at the current business rate for up to two (2) automobiles to be driven to the new location. In lieu of driving, the Company will pay to ship up to two automobiles if the distance to the new location exceeds 500 miles.

Storage in the New Location

You should make every effort to move directly to your permanent residence. If necessary, you may store your household goods for up to 120 days.

Time Off for Moving

Dollar General understands that moving can be a time-consuming and stressful project. Therefore, you may need to take some time off from work for this purpose. At your manager’s approval, Dollar General will allow you up to one week of paid time off for relocation. During this time, it is suggested that you take care of anything relating to your relocation so that you are able to become settled in your new residence and be fully focused on your job upon your return. Please discuss your plans to take time off for moving with your manager well in advance, so that he or she may plan for your absence.

Travel to the New Location

You will be reimbursed for one-way transportation for you and your family to travel to the new location. If you drive, you will be expected to drive a minimum of 300 miles per day and via the most direct route as established by a standard Rand McNally table or equivalent.

19 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |

You will be reimbursed for the following reasonable and actual en route expenses:

à | lodging (one night in departure or destination location or en route night as needed), |

à | reasonable meal expenses (no alcohol) (original receipts must be submitted), |

à | mileage (current business mileage rate), parking, and tolls, and |

à | airfare, if necessary (14-day advance purchase required). |

TAX ASSISTANCE

Many reimbursements made to you are considered taxable income. The Company is required to report all relocation reimbursements as compensation. For informational purposes, the Company will provide you with a tax assistance sheet that will be prepared and mailed to you in January following your move.

The Company will assist in paying the additional tax resulting from taxable relocation reimbursements. Payments will be made directly to the federal, state, and FICA tax authorities. It is recommended you seek guidance from a tax professional for any year in which you receive relocation-related services or expense reimbursements. Accurate expense documentation is very important.

The tax assistance provided to you is based solely on your Company derived income, your filing status, and number of 1040 exemptions. Spouse income, investment income or any other outside income will not be included in the calculations. Individual variances from the program’s calculations will not be reimbursed.

The additional taxes as calculated by the gross-up program and paid on your behalf will be included on your W-2 as income.

Keep in mind some relocation items are not eligible for gross-up. The table below outlines which relocation payments will be tax assisted.

Relocation Provision | Taxable | Grossed Up |

Miscellaneous Expense Allowance | ✓ | No |

Home Finding | ✓ | Yes |

Temporary Living and Allowable return trips | ✓ | Yes |

Home Sale Assistance | Billed directly to Company | |

Independent Sale - eligible home Independent Sale - ineligible home | ✓ ✓ | No Yes |

Renters’ Assistance | ✓ | Yes |

Home Purchase Closing Cost | ✓ | Yes |

Household Goods Move | ✓ | Yes |

Storage | ✓ | Yes |

Travel to the New Location | ✓ | Yes |

20 | Page | Executive Relocation Policy |

| Updated 11/29/22 | |