Use these links to rapidly review the document

Table of Contents

INDEX OF FINANCIAL STATEMENTS DILLARD'S, INC. AND SUBSIDIARIES Year Ended January 28, 2012

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark one) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended January 28, 2012 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to . |

||

Commission file number 1-6140

DILLARD'S, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE State or other jurisdiction of incorporation or organization |

71-0388071 (IRS Employer Identification No.) |

|

1600 CANTRELL ROAD, LITTLE ROCK, ARKANSAS (Address of principal executive offices) |

72201 (Zip Code) |

Registrant's telephone number, including area code (501) 376-5200

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Class A Common Stock | New York Stock Exchange |

Securities

registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ý Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes ý No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ý | Accelerated Filer o | Non-Accelerated Filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of July 30, 2011: $2,606,181,433.

Indicate the number of shares outstanding of each of the registrant's classes of common stock as of February 25, 2012:

CLASS A COMMON STOCK, $0.01 par value 45,430,606

CLASS B COMMON STOCK, $0.01 par value 4,010,929

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Stockholders to be held May 19, 2012 (the "Proxy Statement") are incorporated by reference into Part III of this Form 10-K.

Dillard's, Inc. ("Dillard's", the "Company", "we", "us", "our" or "Registrant") ranks among the nation's largest fashion apparel, cosmetics and home furnishing retailers. The Company, originally founded in 1938 by William T. Dillard, was incorporated in Delaware in 1964. As of January 28, 2012, we operated 304 Dillard's stores, including 16 clearance centers, and an Internet store offering a wide selection of merchandise including fashion apparel for women, men and children, accessories, cosmetics, home furnishings and other consumer goods. The Company also operates a general contracting construction company, CDI Contractors, LLC and CDI Contractors, Inc. ("CDI"), whose business includes constructing and remodeling stores for the Company.

The following table summarizes the percentage of net sales by segment and major product line:

| |

Percentage of Net Sales | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Fiscal 2011 |

Fiscal 2010 |

Fiscal 2009 |

|||||||

Retail operations segment: |

||||||||||

Cosmetics |

15 | % | 15 | % | 15 | % | ||||

Ladies' apparel and accessories |

37 | 37 | 36 | |||||||

Juniors' and children's apparel |

8 | 8 | 8 | |||||||

Men's apparel and accessories |

17 | 17 | 17 | |||||||

Shoes |

16 | 15 | 14 | |||||||

Home and furniture |

6 | 6 | 7 | |||||||

|

99 | 98 | 97 | |||||||

Construction segment |

1 | 2 | 3 | |||||||

Total |

100 | % | 100 | % | 100 | % | ||||

Additional information regarding our business, results of operations and financial condition, including information pertaining to our reporting segments, can be found in Management's Discussion and Analysis of Financial Condition and Results of Operations in Item 7 hereof and in Note 2 of "Notes to Consolidated Financial Statements" in Item 8 hereof.

Most of our stores are located in suburban shopping malls and open-air centers. Our customers may also purchase merchandise on-line at our website, www.dillards.com, which features on-line gift registries and a variety of other services. We operate retail department stores located primarily in the southwest, southeast and midwest regions of the United States. Our stores are located in 29 states.

We conduct our retail merchandise business under highly competitive conditions. Although we are a large regional department store, we have numerous competitors at the national and local level that compete with our individual stores, including specialty, off-price, discount and Internet retailers. Competition is characterized by many factors including location, reputation, assortment, advertising, price, quality, service and credit availability. We believe that our stores are in a strong competitive position with regard to each of these factors. Other retailers may compete for customers on some or all of these factors, or on other factors, and may be perceived by some potential customers as being better aligned with their particular preferences.

Our merchandise selections include, but are not limited to, Dillard's lines of exclusive brand merchandise such as Antonio Melani, Gianni Bini, Roundtree & Yorke and Daniel Cremieux. Dillard's exclusive brands/private label merchandise program provides benefits for Dillard's and our customers. Our customers receive fashionable, higher quality product often at a savings compared to national

1

brands. Dillard's private label merchandise program allows us to ensure Dillard's high standards are achieved, while minimizing costs and differentiating our merchandise offerings from other retailers.

We have made a significant investment in our trademark and license portfolio, in terms of design function, advertising, quality control, manufacturing process and quick response to market trends in a quality manufacturing environment. Dillard's trademark registrations are maintained for as long as Dillard's holds the exclusive right to use the trademarks on the listed products.

Our merchandising, sales promotion and store operating support functions are conducted primarily at our corporate headquarters. Our back office sales support functions, such as accounting, product development, store planning and information technology, are also centralized.

We have developed a knowledge of each of our trade areas and customer bases for our stores. This knowledge is enhanced through regular store visits by senior management and merchandising personnel and through the use of on-line merchandise information and is supported by our regional merchandising offices. We will continue to use existing technology and research to edit assortments by store to meet the specific preference, taste and size requirements of each local operating area.

Certain departments in our stores are licensed to independent companies in order to provide high quality service and merchandise where specialization, focus and expertise are critical. The licensed departments vary by store to complement our own merchandising departments. The principal licensed department is an upscale women's apparel vendor in certain stores. The terms of the license agreements typically range between three and five years with one year renewals and require the licensee to pay for fixtures and to provide their own employees. We regularly evaluate the performance of the licensed departments and require compliance with established customer service guidelines. The licensee for the fine jewelry department ceased operation of all licensed outlets during fiscal 2009.

GE Consumer Finance ("GE") owns and manages Dillard's proprietary credit cards ("proprietary cards") under a long-term marketing and servicing alliance ("Alliance") that expires in fiscal 2014. GE establishes and owns proprietary card accounts for our customers, retains the benefits and risks associated with the ownership of the accounts, provides key customer service functions, including new account openings, transaction authorization, billing adjustments and customer inquiries, receives the finance charge income and incurs the bad debts associated with those accounts. Pursuant to the Alliance, we receive on-going cash compensation from GE based upon the portfolio's earnings. The compensation earned on the portfolio is determined monthly and has no recourse provisions. Furthermore, pursuant to this agreement, we have no continuing involvement other than to honor the proprietary cards in our stores. Although not obligated to a specific level of marketing commitment, we participate in the marketing of the proprietary cards and accept payments on the proprietary cards in our stores as a convenience to customers who prefer to pay in person rather than by paying online or mailing their payments to GE.

We seek to expand the number and use of the proprietary cards by, among other things, providing incentives to sales associates to open new credit accounts, which generally can be opened while a customer is visiting one of our stores. Customers who open accounts are rewarded with discounts on future purchases. Proprietary card customers are sometimes offered private shopping nights, direct mail catalogs, special discounts and advance notice of sale events. GE has created various loyalty programs that reward customers for frequency and volume of proprietary card usage.

Our earnings depend to a significant extent on the results of operations for the last quarter of our fiscal year. Due to holiday buying patterns, sales for that period average approximately one-third of annual sales.

As of January 28, 2012, we employed approximately 38,900 full-time and part-time associates, of which approximately 23% were part-time. The number of associates varies during the year, especially during peak seasonal selling periods.

2

We purchase merchandise from many sources and do not believe that we are dependent on any one supplier. We have no long-term purchase commitments or arrangements with any of our suppliers and consider our relationships to be strong and mutually beneficial.

Our fiscal year ends on the Saturday nearest January 31 of each year. Fiscal years 2011, 2010, and 2009 ended on January 28, 2012, January 29, 2011 and January 30, 2010, respectively, and each included 52 weeks.

The information contained on our website is not incorporated by reference into this Form 10-K and should not be considered to be a part of this Form 10-K. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, statements of changes in beneficial ownership of securities on Form 4 and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge (as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC) on the Dillard's, Inc. website: www.dillards.com.

We have adopted a Code of Business Conduct and Corporate Governance Guidelines, as required by the listing standards of the New York Stock Exchange and the rules of the SEC. We have posted on our website our Code of Conduct, Corporate Governance Guidelines, Social Accountability Policy and committee charters for the Audit Committee of the Board of Directors and the Stock Option and Executive Compensation Committee.

Our corporate offices are located at 1600 Cantrell Road, Little Rock, Arkansas 72201, telephone: 501-376-5200.

The risks described in this Item 1A, Risk Factors, of this Annual Report on Form 10-K for the year ended January 28, 2012, could materially and adversely affect our business, financial condition and results of operations.

The Company cautions that forward-looking statements, as such term is defined in the Private Securities Litigation Reform Act of 1995, contained in this Annual Report on Form 10-K are based on estimates, projections, beliefs and assumptions of management at the time of such statements and are not guarantees of future performance. The Company disclaims any obligation to update or revise any forward-looking statements based on the occurrence of future events, the receipt of new information, or otherwise. Forward-looking statements of the Company involve risks and uncertainties and are subject to change based on various important factors. Actual future performance, outcomes and results may differ materially from those expressed in forward-looking statements made by the Company and its management as a result of a number of risks, uncertainties and assumptions.

The retail merchandise business is highly competitive, and that competition could lower revenues, margins and market share.

We conduct our retail merchandise business under highly competitive conditions. Although we are a large regional department store, we have numerous competitors at the national and local level that compete with our individual stores, including specialty, off-price, discount, Internet and mail-order retailers. Competition is characterized by many factors including location, reputation, fashion, merchandise assortment, advertising, price, quality, service and credit availability. We anticipate that intense competition will continue. If we are unable to maintain our competitive position, we could experience downward pressure on prices, lower demand for products, reduced margins, the inability to take advantage of new business opportunities and the loss of market share.

3

Changes in economic, market and other conditions could adversely affect our operating results.

The retail merchandise business is affected by changes in international, national, regional, and local economic conditions, consumer preferences and spending patterns, demographic trends, consumer confidence, consumer credit availability, weather, traffic patterns, the type, number and location of competing stores, and the effects of war or terrorist activities and any governmental responses thereto. Factors such as inflation, apparel costs, labor and benefit costs, legal claims, and the availability of management and hourly employees also affect store operations and administrative expenses. Our ability to finance new store development, improvements and additions to existing stores, and the acquisition of stores from competitors is affected by economic conditions, including interest rates and other government policies impacting land and construction costs and the availability of borrowed funds.

Current store locations may become less desirable, and desirable new locations may not be available for a reasonable price, if at all, either of which could adversely affect our results of operations.

The success of any store depends substantially upon its location. There can be no assurance that current locations will continue to be desirable as demographic patterns change. Neighborhood or economic conditions where stores are located could decline in the future, thus resulting in potentially reduced sales in those locations. If we cannot obtain desirable locations at reasonable prices, our cost structure will increase and our revenues will be adversely affected.

Ownership and leasing of significant amounts of real estate exposes us to possible liabilities and losses.

We own the land and building, or lease the land and/or the building, for all of our stores. Accordingly, we are subject to all of the risks associated with owning and leasing real estate. In particular, the value of the assets could decrease, and their operating costs could increase, because of changes in the investment climate for real estate, demographic trends and supply or demand for the use of the store, which may result from competition from similar stores in the area, as well as liability for environmental conditions. If an existing owned store is not profitable, and we decide to close it, we may be required to record an impairment charge and/or exit costs associated with the disposal of the store. We generally cannot cancel our leases. If an existing or future store is not profitable, and we decide to close it, we may be committed to perform certain obligations under the applicable lease including, among other things, paying the base rent for the balance of the lease term. In addition, as each of the leases expires, we may be unable to negotiate renewals, either on commercially acceptable terms or at all, which could cause us to close stores in desirable locations. We may not be able to close an unprofitable owned store due to an existing operating covenant which may cause us to operate the location at a loss and prevent us from finding a more desirable location. We have approximately 75 stores along the Gulf and Atlantic coasts that are covered by third party insurance but are self-insured for property and merchandise losses related to "named storms"; therefore, repair and replacement costs will be borne by us for damage to any of these stores from "named storms".

We rely on third party suppliers to obtain materials and provide production facilities from which we source our merchandise.

We may experience supply problems such as unfavorable pricing or untimely delivery of merchandise. The price and availability of materials from suppliers can be adversely affected by factors outside of our control, such as increased worldwide demand. Further, our suppliers may experience financial difficulties due to a downturn in the industry or in other macroeconomic environments, such as credit markets, stifling their ability to obtain borrowed funds necessary to finance their operations. These supplier risks may have a material adverse effect on our business and results of operations.

4

We may evaluate acquisitions, joint ventures and other strategic initiatives, any of which could distract management or otherwise have a negative effect on revenues, costs and stock price.

Our future success may depend on opportunities to buy or obtain rights to other businesses or technologies that could complement, enhance or expand our current business or products or that might otherwise offer growth opportunities. In particular, we intend to evaluate potential mergers, acquisitions, joint venture investments, strategic initiatives, alliances, vertical integration opportunities and divestitures. Our attempt to engage in these transactions may expose us to various inherent risks, including:

- •

- assessing the value, future growth potential, strengths, weaknesses, contingent and other liabilities and potential

profitability of acquisition candidates;

- •

- the potential loss of key personnel of an acquired business;

- •

- the ability to achieve projected economic and operating synergies;

- •

- difficulties successfully integrating, operating, maintaining and managing newly acquired operations or employees;

- •

- difficulties maintaining uniform standards, controls, procedures and policies;

- •

- unanticipated changes in business and economic conditions affecting an acquired business;

- •

- the possibility of impairment charges if an acquired business performs below expectations; and

- •

- the diversion of management's attention from the existing business to integrate the operations and personnel of the acquired or combined business or to implement the strategic initiative.

Our annual and quarterly financial results may fluctuate depending on various factors, many of which are beyond our control, and if we fail to meet the expectations of securities analysts or investors, our share price may decline.

Our sales and operating results can vary from quarter to quarter and year to year depending on various factors, many of which are beyond our control. Certain events and factors may directly and immediately decrease demand for our products or increase operating costs. If customer demand decreased or if operating costs increased rapidly, our results of operations would also decline precipitously. The recent passage of health care legislation will cause the Company's operating costs to rise in fiscal 2014 and beyond. The Company is currently in the process of assessing the extent of the effect of the legislation on its operating costs. Other events and factors include:

- •

- changes in competitive and economic conditions generally;

- •

- variations in the timing and volume of our sales;

- •

- sales promotions by us or our competitors;

- •

- changes in average same-store sales and customer visits;

- •

- changes in legislation, affecting such matters as credit card income;

- •

- variations in the price (including purchase discounts), availability and shipping costs of merchandise;

- •

- seasonal effects on demand for our products;

- •

- changes in the cost or availability of material or labor; and

- •

- weather and acts of God.

5

Litigation with customers, employees and others could harm our reputation and impact operating results.

Lawsuits have been filed, and may continue to be filed, by customers and employees alleging discrimination. We are also susceptible to claims filed by customers alleging responsibility for injury suffered during a visit to a store. Further, we may be subject to other claims in the future based on, among other things, employee discrimination, harassment, wrongful termination and wage issues, including those relating to overtime compensation. These types of claims, as well as other types of lawsuits to which we are subject from time to time, can distract management's attention from core business operations and/or negatively impact operating results.

Catastrophic events may disrupt our business.

Unforeseen events, including war, terrorism and other international conflicts, public health issues, and natural disasters such as earthquakes, hurricanes or other adverse weather and climate conditions, whether occurring in the United States or abroad, could disrupt our operations, disrupt international trade and supply chain efficiencies, suppliers or customers, or result in political or economic instability. These events could result in property losses, reduce demand for our products or make it difficult or impossible to receive products from suppliers.

Variations in the amount of vendor allowances received could adversely impact our operating results.

We receive vendor allowances for advertising, payroll and margin maintenance that are a strategic part of our operations. A reduction in the amount of cooperative advertising allowances would likely cause us to consider other methods of advertising as well as the volume and frequency of our product advertising, which could increase/decrease our expenditures and/or revenue. Decreased payroll reimbursements would either cause payroll costs to rise, negatively impacting operating income, or cause us to reduce the number of employees, which may cause a decline in sales. A decline in the amount of margin maintenance allowances would either increase cost of sales, which would negatively impact gross margin and operating income, or cause us to reduce merchandise purchases, which may cause a decline in sales.

A privacy breach could adversely affect our business, reputation and financial condition.

The protection of customer, employee and Company data is critical to us. The regulatory environment surrounding information security and privacy is increasingly demanding, with the frequent imposition of new and constantly changing requirements. We receive certain personal information about our customers and employees. In addition, our online operations at www.dillards.com depend upon the secure transmission of confidential information over public networks, including information permitting cashless payments. A compromise of our security systems that results in personal information being obtained by unauthorized persons could adversely affect our reputation with our customers, employees and others, as well as our operations, results of operations, financial condition and liquidity, and could result in litigation against us or the imposition of penalties. In addition, a security breach could require that we expend significant additional resources related to our information security systems and could result in a disruption of our operations, particularly our online sales operations.

Reductions in the income and cash flow from our long-term marketing and servicing alliance related to our proprietary credit cards could impact operating results and cash flows.

GE owns and manages our proprietary credit cards under the Alliance that expires in fiscal 2014. The Alliance provides for certain payments to be made by GE to the Company, including a revenue sharing and marketing reimbursement. The income and cash flow that the Company receives from the Alliance is dependent upon a number of factors including the level of sales on GE accounts, the level of balances carried on the GE accounts by GE customers, payment rates on GE accounts, finance

6

charge rates and other fees on GE accounts, the level of credit losses for the GE accounts, GE's ability to extend credit to our customers as well as GE's funding costs, all of which can vary based on changes in federal and state banking and consumer protection laws and from a variety of economic, legal, social and other factors that we cannot control. If the income or cash flow that the Company receives from the Alliance decreases, our operating results and cash flows could be adversely affected.

The percentage-of-completion method of accounting for contract revenues may result in material adjustments, which could result in a charge against our earnings.

Our construction segment recognizes contract revenues using the percentage-of-completion method. Under this method, estimated contract revenues are recognized by applying the percentage of completion of the project for the period to the total estimated revenues for the contract. Estimated contract losses are recognized in full when determined. Total contract revenues and cost estimates are reviewed and revised at a minimum on a quarterly basis as the work progresses and as change orders are approved. Adjustments based upon the percentage of completion are reflected in contract revenues in the period when these estimates are revised. To the extent that these adjustments result in an increase, a reduction or an elimination of previously reported contract profit, we recognize a credit or a charge against current earnings, which could be material.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

7

All of our stores are owned by us or leased from third parties. At January 28, 2012, we operated 304 stores in 29 states totaling approximately 52.7 million square feet of which we owned approximately 46.2 million square feet. Our third-party store leases typically provide for rental payments based on a percentage of net sales with a guaranteed minimum annual rent. In general, the Company pays the cost of insurance, maintenance and real estate taxes related to the leases.

The following table summarizes by state of operation the number of retail stores we operate and the corresponding owned and leased footprint at January 28, 2012:

Location

|

Number of stores |

Owned Stores |

Leased Stores |

Owned Building on Leased Land |

Partially Owned and Partially Leased |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Alabama |

10 | 10 | — | — | — | |||||||||||

Arkansas |

8 | 7 | — | — | 1 | |||||||||||

Arizona |

17 | 16 | — | 1 | — | |||||||||||

California |

3 | 3 | — | — | — | |||||||||||

Colorado |

8 | 8 | — | — | — | |||||||||||

Florida |

42 | 39 | — | 3 | — | |||||||||||

Georgia |

12 | 7 | 3 | 2 | — | |||||||||||

Iowa |

5 | 5 | — | — | — | |||||||||||

Idaho |

2 | 1 | 1 | — | — | |||||||||||

Illinois |

3 | 3 | — | — | — | |||||||||||

Indiana |

3 | 3 | — | — | — | |||||||||||

Kansas |

7 | 3 | 2 | 2 | — | |||||||||||

Kentucky |

6 | 5 | 1 | — | — | |||||||||||

Louisiana |

14 | 13 | 1 | — | — | |||||||||||

Missouri |

10 | 7 | 1 | 2 | — | |||||||||||

Mississippi |

6 | 4 | 1 | 1 | — | |||||||||||

Montana |

2 | 2 | — | — | — | |||||||||||

North Carolina |

16 | 14 | 1 | 1 | — | |||||||||||

Nebraska |

3 | 2 | 1 | — | — | |||||||||||

New Mexico |

6 | 3 | 3 | — | — | |||||||||||

Nevada |

4 | 4 | — | — | — | |||||||||||

Ohio |

15 | 10 | 5 | — | — | |||||||||||

Oklahoma |

10 | 6 | 4 | — | — | |||||||||||

South Carolina |

8 | 8 | — | — | — | |||||||||||

Tennessee |

10 | 8 | 1 | — | 1 | |||||||||||

Texas |

60 | 43 | 10 | 2 | 5 | |||||||||||

Utah |

6 | 4 | 2 | — | — | |||||||||||

Virginia |

7 | 5 | 1 | 1 | — | |||||||||||

Wyoming |

1 | 1 | — | — | — | |||||||||||

Total |

304 | 244 | 38 | 15 | 7 | |||||||||||

8

At January 28, 2012, we operated the following additional facilities:

Facility

|

Location | Square Feet | Owned / Leased |

||||

|---|---|---|---|---|---|---|---|

Distribution Centers: |

Mabelvale, AR | 400,000 | Owned | ||||

|

Gilbert, AZ | 295,000 | Owned | ||||

|

Valdosta, GA | 370,000 | Owned | ||||

|

Olathe, KS | 500,000 | Owned | ||||

|

Salisbury, NC | 355,000 | Owned | ||||

|

Ft. Worth, TX | 700,000 | Owned | ||||

Internet Fulfillment Center |

Nashville, TN | 285,000 | Leased | ||||

Dillard's Executive Offices |

Little Rock, AR | 333,000 | Owned | ||||

CDI Contractors, LLC Executive Office |

Little Rock, AR | 25,000 | Owned | ||||

CDI Storage Facilities |

Maumelle, AR | 66,000 | Owned | ||||

Total |

3,329,000 | ||||||

The Company's new 850,000 square foot internet fulfillment center located in Maumelle, Arkansas is expected to be fully operational by the end of the first fiscal quarter of 2012. Additional property information is contained in Notes 1, 12 and 13 of "Notes to Consolidated Financial Statements," in Item 8 hereof.

From time to time, the Company is involved in litigation relating to claims arising out of the Company's operations in the normal course of business. This may include litigation with customers, employment related lawsuits, class action lawsuits, purported class action lawsuits and actions brought by governmental authorities. As of March 22, 2012, the Company is not a party to any legal proceedings that, individually or in the aggregate, are reasonably expected to have a material adverse effect on the Company's business, results of operations, financial condition or cash flows.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

9

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table lists the names and ages of all executive officers of the Registrant, the nature of any family relationship between them and all positions and offices with the Registrant presently held by each person named. Each is elected to serve a one-year term. There are no other persons chosen to become executive officers.

Name

|

Age | Position & Office | Held Present Office Since |

Family Relationship to CEO | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

William Dillard, II |

67 |

Director; Chief Executive Officer |

1998 |

Not applicable |

||||||

Alex Dillard |

62 |

Director; President |

1998 |

Brother of William Dillard, II |

||||||

Mike Dillard |

60 |

Director; Executive Vice President |

1984 |

Brother of William Dillard, II |

||||||

Drue Matheny |

65 |

Director; Executive Vice President |

1998 |

Sister of William Dillard, II |

||||||

James I. Freeman |

62 |

Director; Senior Vice President; Chief Financial Officer |

1988 |

None |

||||||

Steven K. Nelson |

54 |

Vice President |

1988 |

None |

||||||

Robin Sanderford |

65 |

Vice President |

1998 |

None |

||||||

Paul J. Schroeder, Jr. |

64 |

Vice President; General Counsel |

1998 |

None |

||||||

Burt Squires |

62 |

Vice President |

1984 |

None |

||||||

Julie A. Taylor |

60 |

Vice President |

1998 |

None |

||||||

Richard B. Willey* |

61 |

Vice President |

2010 |

None |

||||||

- *

- Mr. Willey joined the Company in 1987. He served as Regional Vice President of Stores from 1987 to 2001. From 2001 to 2010, he served as Vice President of Store Planning and Construction. In 2010, he was promoted to Corporate Vice President of Stores.

10

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Market and Dividend Information for Common Stock

The Company's Class A Common Stock trades on the New York Stock Exchange under the Ticker Symbol "DDS". No public market currently exists for the Class B Common Stock.

The high and low sales prices of the Company's Class A Common Stock, and dividends declared on each class of common stock, for each quarter of fiscal 2011 and 2010 are presented in the table below:

| |

2011 | 2010 | Dividends per Share |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | 2011 | 2010 | |||||||||||||

First |

$ | 48.57 | $ | 37.87 | $ | 31.22 | $ | 14.94 | $ | 0.04 | $ | 0.04 | |||||||

Second |

61.08 | 45.27 | 29.88 | 19.91 | 0.05 | 0.04 | |||||||||||||

Third |

57.58 | 38.99 | 27.80 | 19.26 | 0.05 | 0.04 | |||||||||||||

Fourth |

56.30 | 42.54 | 44.50 | 25.31 | 0.05 | 0.04 | |||||||||||||

While the Company expects to continue paying quarterly cash dividends during fiscal 2012, all dividends will be reviewed quarterly and declared by the Board of Directors.

Stockholders

As of February 25, 2012, there were 3,270 holders of record of the Company's Class A Common Stock and 8 holders of record of the Company's Class B Common Stock.

Repurchase of Common Stock

Issuer Purchases of Equity Securities

Period

|

(a) Total Number of Shares Purchased |

(b) Average Price Paid per Share |

(c)Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

(d) Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

October 30, 2011 through November 26, 2011 |

1,264,663 | $ | 49.26 | 1,264,663 | $ | 63,986,630 | |||||||

November 27, 2011 through December 31, 2011 |

299,800 | 47.88 | 299,800 | 49,632,387 | |||||||||

January 1, 2012 through January 28, 2012 |

487,318 | 45.39 | 487,318 | 27,511,684 | |||||||||

Total |

2,051,781 | $ | 48.14 | 2,051,781 | $ | 27,511,684 | |||||||

In May 2011, the Company announced that the Board of Directors authorized the repurchase of up to $250 million of its Class A Common Stock. This authorization permits the Company to repurchase its Class A Common Stock in the open market, pursuant to preset trading plans meeting the requirements of Rule 10b5-1 under the Securities Exchange Act of 1934 or through privately negotiated transactions. The plan has no expiration date, and remaining availability pursuant to the Company's share repurchase program was $27.5 million as of January 28, 2012.

In February 2012, the Company announced that the Board of Directors authorized the repurchase of up to $250 million of its Class A Common Stock. This additional authorization permits the Company

11

to repurchase its Class A Common Stock in the open market, pursuant to preset trading plans meeting the requirements of Rule 10b5-1 under the Securities Exchange Act of 1934 or through privately negotiated transactions. The plan has no expiration date.

Securities Authorized for Issuance under Equity Compensation Plans

The information concerning the Company's equity compensation plans is incorporated by reference here to Item 12 of this Annual Report on Form 10-K under the heading "Equity Compensation Plan Information".

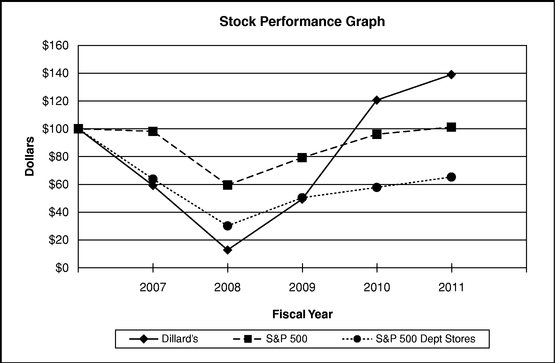

Company Performance

For each of the last five fiscal years, the graph below compares the cumulative total returns on the Company's Class A Common Stock, the Standard & Poor's 500 Index and the Standard & Poor's 500 Department Stores Index. The cumulative total return on the Company's Class A Common Stock assumes $100 invested in such stock on February 4, 2007 and assumes reinvestment of dividends.

| |

2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Dillard's, Inc. |

$ | 59.15 | $ | 12.77 | $ | 49.37 | $ | 120.62 | $ | 138.99 | ||||||

S&P 500 |

98.17 | 59.52 | 79.24 | 96.08 | 101.20 | |||||||||||

S&P 500 Department Stores |

63.85 | 30.16 | 50.42 | 57.83 | 65.29 | |||||||||||

12

ITEM 6. SELECTED FINANCIAL DATA.

The selected financial data set forth below should be read in conjunction with our "Management's Discussion and Analysis of Financial Condition and Results of Operations", our consolidated audited financial statements and notes thereto and the other information contained elsewhere in this report.

(Dollars in thousands of dollars, except per share data)

| |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Net sales |

$ | 6,263,600 | $ | 6,120,961 | $ | 6,094,948 | $ | 6,830,543 | $ | 7,207,417 | ||||||

Percent change |

2 | % | 0 | % | -11 | % | -5 | % | -6 | % | ||||||

Cost of sales |

4,041,550 | 3,976,063 | 4,102,892 | 4,827,769 | 4,786,655 | |||||||||||

Percent of sales |

64.5 | % | 65.0 | % | 67.3 | % | 70.7 | % | 66.4 | % | ||||||

Interest and debt expense, net |

72,059 | 73,792 | 74,003 | 88,821 | 91,556 | |||||||||||

Income (loss) before income taxes and income on (equity in losses of) joint ventures |

396,669 | 268,716 | 84,525 | (380,005 | ) | 60,518 | ||||||||||

Income taxes (benefit) |

(62,518 | ) | 84,450 | 12,690 | (140,520 | ) | 13,010 | |||||||||

Income on (equity in losses of) joint ventures |

4,722 | (4,646 | ) | (3,304 | ) | (1,580 | ) | 6,253 | ||||||||

Net income (loss) |

463,909 | 179,620 | 68,531 | (241,065 | ) | 53,761 | ||||||||||

Net income (loss) per diluted common share |

8.52 | 2.67 | 0.93 | (3.25 | ) | 0.68 | ||||||||||

Dividends per common share |

0.19 | 0.16 | 0.16 | 0.16 | 0.16 | |||||||||||

Book value per common share |

41.50 | 34.79 | 31.21 | 30.65 | 33.45 | |||||||||||

Average number of diluted shares outstanding |

54,448,065 | 67,174,163 | 73,783,960 | 74,278,461 | 79,103,423 | |||||||||||

Accounts receivable(1) |

28,708 | 25,950 | 63,222 | 87,998 | 10,880 | |||||||||||

Merchandise inventories |

1,304,124 | 1,290,147 | 1,300,680 | 1,374,394 | 1,779,279 | |||||||||||

Property and equipment, net |

2,440,266 | 2,595,514 | 2,780,837 | 2,973,151 | 3,190,444 | |||||||||||

Total assets |

4,306,137 | 4,374,166 | 4,606,327 | 4,745,844 | 5,338,129 | |||||||||||

Long-term debt |

614,785 | 697,246 | 747,587 | 757,689 | 760,165 | |||||||||||

Capital lease obligations |

9,153 | 11,383 | 22,422 | 24,116 | 25,739 | |||||||||||

Other liabilities |

245,218 | 205,916 | 213,471 | 220,911 | 217,403 | |||||||||||

Deferred income taxes |

314,598 | 341,689 | 349,722 | 378,348 | 436,541 | |||||||||||

Subordinated debentures |

200,000 | 200,000 | 200,000 | 200,000 | 200,000 | |||||||||||

Total stockholders' equity |

2,052,019 | 2,086,720 | 2,304,103 | 2,251,115 | 2,514,111 | |||||||||||

Number of stores |

||||||||||||||||

Opened(2) |

0 | 2 | 0 | 10 | 9 | |||||||||||

Closed |

4 | 3 | 6 | 21 | 11 | |||||||||||

Total—end of year |

304 | 308 | 309 | 315 | 326 | |||||||||||

- (1)

- In

August 2008, the Company purchased the remaining interest in CDI, a former 50% equity method joint venture investment of the Company.

- (2)

- One store in Biloxi, Mississippi, not in operation during fiscal 2007 due to the hurricanes of 2005, was re-opened in early fiscal 2008.

13

The items below are included in the Selected Financial Data.

2011

The items below amount to a net $50.9 million pretax gain ($234.5 million after tax gain or $4.31 per share).

- •

- a $201.6 million income tax benefit ($3.70 per share) due to a reversal of a valuation allowance related to the

amount of the capital loss carryforward used to offset the capital gain income recognized on the taxable transfer of properties to our REIT (see Note 6 of Notes to Consolidated Financial

Statements).

- •

- a $44.5 million pretax gain ($28.7 million after tax or $0.53 per share), net of settlement related

expenses, related to the settlement of a lawsuit with JDA Software Group for $57.0 million.

- •

- a $4.2 million pretax gain ($2.7 million after tax or $0.05 per share) related to a distribution from a mall

joint venture (see Note 1 of Notes to Consolidated Financial Statements).

- •

- a $2.1 million pretax gain ($1.4 million after tax or $0.03 per share) related to the sale of an interest in

a mall joint venture (see Note 1 of Notes to Consolidated Financial Statements).

- •

- a $1.3 million pretax gain ($0.9 million after tax or $0.02 per share) related to the sale of two former

retail store locations.

- •

- a $1.2 million pretax charge ($0.8 million after tax or $0.01 per share) for asset impairment and store closing charges related to the write-down of one property held for sale (see Note 13 of the Notes to Consolidated Financial Statements).

2010

The items below amount to a net $10.4 million pretax gain ($16.4 million after tax gain or $0.24 per share).

- •

- a $2.2 million pretax charge ($1.4 million after tax or $0.02 per share) for asset impairment and store

closing charges related to the write-down of one property held for sale (see Note 13 of the Notes to Consolidated Financial Statements).

- •

- a $7.5 million pretax gain ($4.8 million after tax or $0.07 per share) on proceeds received for final

payment related to hurricane losses.

- •

- a $5.1 million pretax gain ($3.3 million after tax or $0.05 per share) related to the sale of five retail

store locations.

- •

- a $9.7 million income tax benefit ($0.14 per share) primarily related to net decreases in unrecognized tax benefits, interest and penalties due to resolutions of federal and state examinations; decreases in state net operating loss valuation allowances; and a decrease in a capital loss valuation allowance.

2009

The items below amount to a net $6.6 million pretax gain ($14.7 million after tax gain or $0.19 per share).

- •

- a $3.1 million pretax charge ($2.0 million after tax or $0.03 per share) for asset impairment and store closing charges related to certain stores (see Note 13 of the Notes to Consolidated Financial Statements).

14

- •

- a $5.7 million pretax gain ($3.6 million after tax or $0.05 per share) related to proceeds received from

settlement of the Visa Check/Mastermoney Antitrust litigation.

- •

- a $10.6 million income tax benefit ($0.14 per share) primarily due to state administrative settlement and a

decrease in a capital loss valuation allowance.

- •

- a $1.7 million pretax gain ($1.0 million after tax or $0.01 per share) on the early extinguishment of debt

related to the repurchase of certain unsecured notes (see Note 4 of the Notes to Consolidated Financial Statements).

- •

- a $2.3 million pretax gain ($1.5 million after tax or $0.02 per share) related to the sale of a vacant store location in Kansas City, Missouri.

2008

The items below amount to a net $180.4 million pretax charge ($125.5 million after tax charge or $1.69 per share).

- •

- a $197.9 million pretax charge ($136.5 million after tax or $1.84 per share) for asset impairment and store

closing charges related to certain stores.

- •

- a $7.3 million pretax charge ($4.6 million after tax or $0.06 per share) related to hurricane losses and

remediation expenses incurred during the 2008 hurricane season.

- •

- a $24.8 million pretax gain ($15.6 million after tax or $0.21 per share) related to the sale of an aircraft and the sale of a store located in San Antonio, Texas.

2007

The items below amount to a net $2.3 million pretax charge ($10.7 million after tax gain or $0.13 per share).

- •

- a $20.5 million pretax charge ($12.8 million after tax or $0.16 per share) for asset impairment and store

closing charges related to certain stores.

- •

- an $18.2 million pretax gain ($11.5 million after tax or $0.14 per share) related to reimbursement for

inventory and property damages incurred during the 2005 hurricane season.

- •

- a $12.0 million income tax benefit ($0.15 per share) primarily due to state administrative settlement, federal credits and the change in a capital loss valuation allowance.

15

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

EXECUTIVE OVERVIEW

Dillard's, Inc. operates 304 retail department stores spanning 29 states and an Internet store. Our retail stores are located in fashion-oriented shopping malls and open-air centers and offer a broad selection of fashion apparel, cosmetics and home furnishings. We offer an appealing and attractive assortment of merchandise to our customers at a fair price, including national brand merchandise as well as our exclusive brand merchandise. We seek to enhance our income by maximizing the sale of this merchandise to our customers by promoting and advertising our merchandise and by making our stores an attractive and convenient place for our customers to shop.

The Company also operates CDI, a general contractor whose business includes constructing and remodeling stores for the Company, which is a reportable segment separate from our retail operations.

In accordance with the National Retail Federation fiscal reporting calendar, the fiscal 2011, 2010 and 2009 reporting periods presented and discussed below ended January 28, 2012, January 29, 2011 and January 30, 2010, respectively, and each contained 52 weeks.

Fiscal 2011

Our operating results improved during fiscal 2011 with continued consumer confidence. Retail sales were up over last year, with comparable store sales increases recognized in all four quarters of the year. Gross margin improved slightly over last year, mainly from improvement in the first half of the year, and operating expenses were leveraged. We repurchased 11.4 million shares of our Class A Common Stock during the year, helping to reduce our total outstanding shares by almost 18% from last year. Net income increased to $463.9 million, or $8.52 per share during fiscal 2011—our highest historical fiscal year earnings per share—compared to $179.6 million, or $2.67 per share, during fiscal 2010.

Included in net income for fiscal 2011 are:

- •

- a $201.6 million income tax benefit ($3.70 per share) due to a reversal of a valuation allowance related to the

amount of the capital loss carryforward used to offset the capital gain income recognized on the taxable transfer of properties to our REIT.

- •

- a $44.5 million pretax gain ($28.7 million after tax or $0.53 per share), net of settlement related

expenses, related to the settlement of a lawsuit with JDA Software Group for $57.0 million.

- •

- a $4.2 million pretax gain ($2.7 million after tax or $0.05 per share) related to a distribution from a mall

joint venture.

- •

- a $2.1 million pretax gain ($1.4 million after tax or $0.03 per share) related to the sale of an interest in

a mall joint venture.

- •

- a $1.3 million pretax gain ($0.9 million after tax or $0.02 per share) related to the sale of two former

retail store locations.

- •

- a $1.2 million pretax charge ($0.8 million after tax or $0.01 per share) for asset impairment and store closing charges related to the write-down of one property held for sale.

Included in net income for fiscal 2010 are:

- •

- a $2.2 million pretax charge ($1.4 million after tax or $0.02 per share) for asset impairment and store

closing charges related to the write-down of one property held for sale;

- •

- a $7.5 million pretax gain ($4.8 million after tax or $0.07 per share) on proceeds received for final payment related to hurricane losses;

16

- •

- a $5.1 million pretax gain ($3.3 million after tax or $0.05 per share) related to the sale of five retail

store locations; and

- •

- a $9.7 million income tax benefit ($0.14 per share) primarily related to net decreases in unrecognized tax benefits, interest and penalties due to resolutions of federal and state examinations; decreases in state net operating loss valuation allowances; and a decrease in a capital loss valuation allowance.

Highlights of fiscal 2011 as compared to fiscal 2010 are:

- •

- Record earnings per share of $8.52 compared to $2.67 for the prior year. Net income was $463.9 million for fiscal

2011 compared to $179.6 million for fiscal 2010;

- •

- A comparable store sales increase of 4% over the prior year;

- •

- Operating expense leverage of 60 basis points of sales. Operating expenses as a percent of sales were 26.0% and 26.6% for

fiscal 2011 and fiscal 2010, respectively; and

- •

- Cash flow from operations of $501.1 million allowed the repurchase of approximately $491.2 million (11.4 million shares) of Class A Common Stock under the Company's share repurchase programs. Total shares outstanding at January 28, 2012 were 49.4 million shares compared to 60.0 million shares at January 29, 2011.

As of January 28, 2012, we had working capital of $721.4 million, cash and cash equivalents of $224.3 million and $891.6 million of total debt outstanding. We operated 304 total stores as of January 28, 2012, a decrease of four stores from the same period last year.

Key Performance Indicators

We use a number of key indicators of financial condition and operating performance to evaluate the performance of our business, including the following:

| |

Fiscal Year Ended | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

(retail segment only, excluding cash flow data)

|

January 28, 2012 |

January 29, 2011 |

January 30, 2010 |

|||||||

Net sales (in millions) |

$ | 6,193.9 | $ | 6,020.0 | $ | 5,890.0 | ||||

Gross profit (in millions) |

$ | 2,221.0 | $ | 2,142.9 | $ | 1,982.9 | ||||

Gross profit as a percentage of net sales |

35.9 | % | 35.6 | % | 33.7 | % | ||||

Cash flow from operations (in millions) |

$ | 501.1 | $ | 512.9 | $ | 554.0 | ||||

Total store count at end of period |

304 | 308 | 309 | |||||||

Sales per square foot |

$ | 118 | $ | 113 | $ | 110 | ||||

Net sales trend |

3 | % | 2 | % | (13 | )% | ||||

Comparable store sales trend |

4 | % | 3 | % | (10 | )% | ||||

Comparable store inventory trend |

3 | % | (2 | )% | (5 | )% | ||||

Merchandise inventory turnover |

2.8 | 2.8 | 2.6 | |||||||

Trends and Uncertainties

Fluctuations in the following key trends and uncertainties may have a material effect on our operating results.

- •

- Cash flow—Cash from operating activities is a primary source of liquidity that is adversely affected when the

industry faces economic challenges. Furthermore, operating cash flow can be negatively affected when new and existing competitors seek areas of growth to expand their businesses.

- •

- Pricing—If our customers do not purchase our merchandise offerings in sufficient quantities, we respond by taking markdowns. If we have to reduce our retail selling prices, the cost of sales on

17

- •

- Success of brand—The success of our exclusive brand merchandise as well as merchandise we source from national

vendors is dependent upon customer fashion preferences and how well we can predict and anticipate trends.

- •

- Sourcing—Our store merchandise selection is dependent upon our ability to acquire appealing products from a

number of sources. Our ability to attract and retain compelling vendors as well as in-house design talent, the adequacy and stable availability of materials and production facilities from

which we source our merchandise and the speed at which we can respond to customer trends and preferences all have a significant impact on our merchandise mix and, thus, our ability to sell merchandise

at profitable prices.

- •

- Store growth—Although store growth is presently not a near-term goal, such growth is dependent upon a number of factors which could impede our ability to open new stores, such as the identification of suitable markets and locations and the availability of shopping developments, especially in a weak economic environment.

our consolidated statement of income will correspondingly rise, thus reducing our income and cash flow.

Seasonality and Inflation

Our business, like many other retailers, is subject to seasonal influences, with a significant portion of sales and income typically realized during the last quarter of our fiscal year due to the holiday season. Because of the seasonality of our business, results from any quarter are not necessarily indicative of the results that may be achieved for a full fiscal year.

We do not believe that inflation has had a material effect on our results during the periods presented; however, our business could be affected by such in the future. In response to economic volatility in Asia and to increased fabric prices (including cotton) and overseas wages, during fiscal 2011 we sought solutions to help minimize the effects of these events on our operations by (1) negotiating efficiencies through our longstanding relationships with our current suppliers, (2) considering alternative manufacturing sources, (3) redesigning our garments and incorporating other types of fibers where appropriate and (4) adjusting price points as necessary. With the help of these mitigating steps, the effects of the negative economic events did not have a material negative impact on our fiscal 2011 gross margins, and we believe they will not have a material negative impact on our fiscal 2012 gross margins as these same pressures have moderated since last year.

2012 Guidance

A summary of estimates on key financial measures for fiscal 2012 is shown below.

(in millions of dollars)

|

Fiscal 2012 Estimated | Fiscal 2011 Actual | |||||

|---|---|---|---|---|---|---|---|

Depreciation and amortization |

$ | 256 | $ | 258 | |||

Rentals |

34 | 48 | |||||

Interest and debt expense, net |

71 | 72 | |||||

Capital expenditures |

175 | 116 | |||||

General

Net sales. Net sales include merchandise sales of comparable and non-comparable stores and revenue recognized on contracts of CDI, the Company's general contracting construction company. Comparable store sales include sales for those stores which were in operation for a full period in both the current month and the corresponding month for the prior year. Non-comparable store sales include: sales in the current fiscal year from stores opened during the previous fiscal year before they are considered comparable stores; sales from new stores opened during the current fiscal year; sales in

18

the previous fiscal year for stores closed during the current or previous fiscal year that are no longer considered comparable stores; and sales in clearance centers.

Service charges and other income. Service charges and other income include income generated through the Alliance with GE. Other income includes rental income, shipping and handling fees and lease income on leased departments.

Cost of sales. Cost of sales includes the cost of merchandise sold (net of purchase discounts), bankcard fees, freight to the distribution centers, employee and promotional discounts, non-specific margin maintenance allowances and direct payroll for salon personnel. Cost of sales also includes CDI contract costs, which comprise all direct material and labor costs, subcontract costs and those indirect costs related to contract performance, such as indirect labor, employee benefits and insurance program costs.

Advertising, selling, administrative and general expenses. Advertising, selling, administrative and general expenses include buying, occupancy, selling, distribution, warehousing, store and corporate expenses (including payroll and employee benefits), insurance, employment taxes, advertising, management information systems, legal and other corporate level expenses. Buying expenses consist of payroll, employee benefits and travel for design, buying and merchandising personnel.

Depreciation and amortization. Depreciation and amortization expenses include depreciation and amortization on property and equipment.

Rentals. Rentals include expenses for store leases, including contingent rent, and data processing and other equipment rentals.

Interest and debt expense, net. Interest and debt expense includes interest, net of interest income, relating to the Company's unsecured notes, mortgage notes, term note, subordinated debentures and borrowings under the Company's credit facility. Interest and debt expense also includes gains and losses on note repurchases, amortization of financing costs and interest on capital lease obligations.

Gain on litigation settlement. Gain on litigation settlement includes the proceeds received, net of related expenses, from the settlement of a lawsuit with JDA Software Group.

Gain on disposal of assets. Gain on disposal of assets includes the net gain or loss on the sale or disposal of property and equipment and the gain on the sale of an interest in a mall joint venture.

Asset impairment and store closing charges. Asset impairment and store closing charges consist of write-downs to fair value of under-performing or held for sale properties and exit costs associated with the closure of certain stores. Exit costs include future rent, taxes and common area maintenance expenses from the time the stores are closed.

Income on (equity in losses of) joint ventures. Income on (equity in losses of) joint ventures includes the Company's portion of the income or loss of the Company's unconsolidated joint ventures as well as a distribution of excess cash from one of the Company's mall joint ventures.

Critical Accounting Policies and Estimates

The Company's accounting policies are also described in Note 1 of Notes to Consolidated Financial Statements. As disclosed in this note, the preparation of financial statements in conformity with accounting principles generally accepted in the United States of America ("GAAP") requires management to make estimates and assumptions about future events that affect the amounts reported in the consolidated financial statements and accompanying notes. The Company evaluates its estimates and judgments on an ongoing basis and predicates those estimates and judgments on historical experience and on various other factors that are believed to be reasonable under the circumstances.

19

Since future events and their effects cannot be determined with absolute certainty, actual results will differ from those estimates.

Management of the Company believes the following critical accounting policies, among others, affect its more significant judgments and estimates used in preparation of the Consolidated Financial Statements.

Merchandise inventory. Approximately 97% of the inventories are valued at the lower of cost or market using the last-in, first-out retail inventory method ("LIFO RIM"). Under LIFO RIM, the valuation of inventories at cost and the resulting gross margins are calculated by applying a calculated cost to retail ratio to the retail value of inventories. LIFO RIM is an averaging method that is widely used in the retail industry due to its practicality. Inherent in the LIFO RIM calculation are certain significant management judgments including, among others, merchandise markon, markups, and markdowns, which significantly impact the ending inventory valuation at cost as well as the resulting gross margins. During periods of deflation, current replacement cost could result in inventory values on the first-in, first-out ("FIFO") retail inventory method being lower than the LIFO method. At January 28, 2012 and January 29, 2011, the LIFO method, after a lower of cost or market adjustment, approximated the cost of inventories using the FIFO method. The application of LIFO did not impact cost of sales during fiscal 2011, 2010 or 2009. The remaining 3% of the inventories are valued at the lower of cost or market using the average cost or specific identified cost methods. A 1% change in the dollar amount of markdowns would have impacted net income by approximately $9 million for fiscal 2011.

The Company regularly records a provision for estimated shrinkage, thereby reducing the carrying value of merchandise inventory. Complete physical inventories of all of the Company's stores and warehouses are performed no less frequently than annually, with the recorded amount of merchandise inventory being adjusted to coincide with these physical counts. The differences between the estimated amounts of shrinkage and the actual amounts realized during the past three years have not been material.

Revenue recognition. The Company's retail operations segment recognizes revenue upon the sale of merchandise to its customers, net of anticipated returns of merchandise. The provision for sales returns is based on historical evidence of our return rate. We recorded an allowance for sales returns of $9.0 million and $7.3 million as of January 28, 2012 and January 29, 2011, respectively. Adjustments to earnings resulting from revisions to estimates on our sales return provision were not material for the years ended January 28, 2012, January 29, 2011 and January 30, 2010.

The Company's share of income earned under the Alliance with GE involving the Dillard's branded proprietary credit cards is included as a component of service charges and other income. The Company received income of approximately $96 million, $85 million and $89 million from GE in fiscal 2011, 2010 and 2009, respectively. Pursuant to this Alliance, the Company has no continuing involvement other than to honor the proprietary cards in its stores. Although not obligated to a specific level of marketing commitment, the Company participates in the marketing of the proprietary credit cards and accepts payments on the proprietary credit cards in its stores as a convenience to customers who prefer to pay in person rather than by paying online or mailing their payments to GE.

Revenues from CDI construction contracts are generally recognized by applying percentages of completion for each period to the total estimated revenue for the respective contracts. The length of each contract varies but is typically nine to eighteen months. The percentages of completion are determined by relating the actual costs of work performed to date to the current estimated total costs of the respective contracts. Any anticipated losses on completed contracts are recognized as soon as they are determined.

20

Vendor allowances. The Company receives concessions from vendors through a variety of programs and arrangements, including co-operative advertising, payroll reimbursements and margin maintenance programs.

Cooperative advertising allowances are reported as a reduction of advertising expense in the period in which the advertising occurred. If vendor advertising allowances were substantially reduced or eliminated, the Company would likely consider other methods of advertising as well as the volume and frequency of our product advertising, which could increase or decrease our expenditures. Similarly, we are not able to assess the impact of vendor advertising allowances on creating additional revenues, as such allowances do not directly generate revenues for our stores.

Payroll reimbursements are reported as a reduction of payroll expense in the period in which the reimbursement occurred.

Amounts of margin maintenance allowances are recorded only when an agreement has been reached with the vendor and the collection of the concession is deemed probable. All such merchandise margin maintenance allowances are recognized as a reduction of cost purchases. Under LIFO RIM, a portion of these allowances reduces cost of goods sold and a portion reduces the carrying value of merchandise inventory.

Insurance accruals. The Company's consolidated balance sheets include liabilities with respect to claims for self-insured workers' compensation (with a self-insured retention of $4 million per claim) and general liability (with a self-insured retention of $1 million per claim and a one-time $1 million corridor). The Company's retentions are insured through a wholly-owned captive insurance subsidiary. The Company estimates the required liability of such claims, utilizing an actuarial method, based upon various assumptions, which include, but are not limited to, our historical loss experience, projected loss development factors, actual payroll and other data. The required liability is also subject to adjustment in the future based upon the changes in claims experience, including changes in the number of incidents (frequency) and changes in the ultimate cost per incident (severity). As of January 28, 2012 and January 29, 2011, insurance accruals of $50.3 million and $52.9 million, respectively, were recorded in trade accounts payable and accrued expenses and other liabilities. Adjustments resulting from changes in historical loss trends have helped control expenses during fiscal 2011 and 2010, partially due to Company programs that have helped decrease both the number and cost of claims. Further, we do not anticipate any significant change in loss trends, settlements or other costs that would cause a significant change in our earnings. A 10% change in our self-insurance reserve would have affected net earnings by $3.2 million for fiscal 2011.

Long-lived assets. The Company's judgment regarding the existence of impairment indicators is based on market and operational performance. We assess the impairment of long-lived assets, primarily fixed assets, whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Factors we consider important which could trigger an impairment review include the following:

- •

- Significant changes in the manner of our use of assets or the strategy for the overall business;

- •

- Significant negative industry or economic trends;

- •

- A current-period operating or cash flow loss combined with a history of operating or cash flow losses; or

- •

- Store closings.

The Company performs an analysis of the anticipated undiscounted future net cash flows of the related finite-lived assets. If the carrying value of the related asset exceeds the undiscounted cash flows, the carrying value is reduced to its fair value. Various factors including future sales growth and profit

21

margins are included in this analysis. To the extent these future projections or the Company's strategies change, the conclusion regarding impairment may differ from the current estimates.

Income taxes. Temporary differences arising from differing treatment of income and expense items for tax and financial reporting purposes result in deferred tax assets and liabilities that are recorded on the balance sheet. These balances, as well as income tax expense, are determined through management's estimations, interpretation of tax law for multiple jurisdictions and tax planning. If the Company's actual results differ from estimated results due to changes in tax laws, changes in store locations or tax planning, the Company's effective tax rate and tax balances could be affected. As such, these estimates may require adjustment in the future as additional facts become known or as circumstances change.

The total amount of unrecognized tax benefits as of January 28, 2012 and January 29, 2011 was $8.5 million and $9.1 million, respectively, of which $5.8 million and $6.3 million, respectively, would, if recognized, affect the effective tax rate. The Company classifies accrued interest expense and penalties relating to income tax in the consolidated financial statements as income tax expense. The total interest and penalties recognized in the consolidated statements of income as of January 28, 2012, January 29, 2011 and January 30, 2010 was $(0.2) million, $(2.3) million, and $(2.0) million, respectively. The total accrued interest and penalties in the consolidated balance sheets as of January 28, 2012 and January 29, 2011 was $3.4 million and $3.7 million, respectively.

During fiscal 2011, the Internal Revenue Service ("IRS") concluded its examination of the Company's federal income tax returns for the fiscal tax years 2008 and 2009, and no significant changes occurred in these tax years as a result of such examination. The Company is currently under examination by various state and local taxing jurisdictions for various fiscal years. The tax years that remain subject to examination for major tax jurisdictions are fiscal tax years 2008 and forward, with the exception of fiscal 2003 through 2007 amended state and local tax returns related to the reporting of federal audit adjustments. At this time, the Company does not expect the results from any income tax audit to have a material impact on the Company's consolidated financial statements.

The Company has taken positions in certain taxing jurisdictions for which it is reasonably possible that the total amounts of unrecognized tax benefits may decrease within the next twelve months. The possible decrease could result from the finalization of the Company's various state income tax audits and lapse of statutes of limitation. The Company's federal income tax audit uncertainties primarily relate to research and development credits, while various state income tax audit uncertainties primarily relate to income from intangible assets. The estimated range of the reasonably possible uncertain tax benefit decrease in the next twelve months is between $0.5 million and $2.0 million. Changes in the Company's assumptions and judgments can materially affect amounts recognized in the consolidated balance sheets and statements of income.

Pension obligations. The discount rate that the Company utilizes for determining future pension obligations is based on the Citigroup Above Median Pension Index Curve on its annual measurement date and is matched to the future expected cash flows of the benefit plans by annual periods. The discount rate decreased to 4.3% as of January 28, 2012 from 5.5% as of January 29, 2011. We believe that these assumptions have been appropriate and that, based on these assumptions, the pension liability of $174 million is appropriately stated as of January 28, 2012; however, actual results may differ materially from those estimated and could have a material impact on our consolidated financial statements. A further 50 basis point change in the discount rate would increase or decrease the pension liability by approximately $10.4 million. The Company expects to make a contribution to the pension plan of approximately $7.9 million in fiscal 2012. The Company expects pension expense to be approximately $16.3 million in fiscal 2012 with a liability of $182.5 million at February 2, 2013.

22

RESULTS OF OPERATIONS

The following table sets forth the results of operations and percentage of net sales, for the periods indicated:

| |

For the years ended | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

January 28, 2012 | January 29, 2011 | January 30, 2010 | ||||||||||||||||

(in thousands of dollars)

|

Amount | % of Net Sales |

Amount | % of Net Sales |

Amount | % of Net Sales |

|||||||||||||

Net sales |

$ | 6,263,600 | 100.0 | % | $ | 6,120,961 | 100.0 | % | $ | 6,094,948 | 100.0 | % | |||||||

Service charges and other income |

136,165 | 2.2 | 132,574 | 2.2 | 131,680 | 2.2 | |||||||||||||

|

6,399,765 | 102.2 | 6,253,535 | 102.2 | 6,226,628 | 102.2 | |||||||||||||

Cost of sales |

4,041,550 | 64.5 | 3,976,063 | 65.0 | 4,102,892 | 67.3 | |||||||||||||

Advertising, selling, administrative and general expenses |

1,630,907 | 26.0 | 1,625,793 | 26.6 | 1,644,091 | 27.0 | |||||||||||||

Depreciation and amortization |

257,685 | 4.1 | 261,550 | 4.3 | 262,877 | 4.3 | |||||||||||||

Rentals |

48,110 | 0.8 | 51,045 | 0.8 | 58,363 | 1.0 | |||||||||||||

Interest and debt expense, net |

72,059 | 1.2 | 73,792 | 1.2 | 74,003 | 1.2 | |||||||||||||

Gain on litigation settlement |

(44,460 | ) | (0.7 | ) | — | 0.0 | — | 0.0 | |||||||||||

Gain on disposal of assets |

(3,955 | ) | 0.0 | (5,632 | ) | (0.1 | ) | (3,207 | ) | (0.1 | ) | ||||||||

Asset impairment and store closing charges |

1,200 | 0.0 | 2,208 | 0.0 | 3,084 | 0.1 | |||||||||||||

Income before income taxes and income on (equity in losses of) joint ventures |

396,669 | 6.3 | 268,716 | 4.4 | 84,525 | 1.4 | |||||||||||||

Income taxes (benefit) |

(62,518 | ) | (1.0 | ) | 84,450 | 1.4 | 12,690 | 0.2 | |||||||||||

Income on (equity in losses of) joint ventures |

4,722 | 0.1 | (4,646 | ) | (0.1 | ) | (3,304 | ) | (0.1 | ) | |||||||||

Net income |

$ | 463,909 | 7.4 | % | $ | 179,620 | 2.9 | % | $ | 68,531 | 1.1 | % | |||||||

23

Sales

(in thousands of dollars)

|

Fiscal 2011 | Fiscal 2010 | Fiscal 2009 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

Net sales: |

||||||||||

Retail operations segment |

$ | 6,193,903 | $ | 6,020,043 | $ | 5,889,961 | ||||

Construction segment |

69,697 | 100,918 | 204,987 | |||||||

Total net sales |

$ | 6,263,600 | $ | 6,120,961 | $ | 6,094,948 | ||||

The percent change by category in the Company's retail operations segment sales for the past two years is as follows:

| |

Percent Change | ||||||

|---|---|---|---|---|---|---|---|

| |

Fiscal 2011 - 2010 |

Fiscal 2010 - 2009 |

|||||

Cosmetics |

4.7 | % | (0.1 | )% | |||

Ladies' apparel and accessories |

2.1 | 2.4 | |||||

Juniors' and children's apparel |

3.7 | 1.6 | |||||

Men's apparel and accessories |

2.8 | 1.8 | |||||

Shoes |

5.6 | 7.3 | |||||

Home and furniture |

(2.8 | ) | (3.6 | ) | |||

2011 Compared to 2010

Net sales from the retail operations segment increased $173.9 million or 3% during fiscal 2011 as compared to fiscal 2010 while sales in comparable stores improved 4%. Sales of shoes and cosmetics were up significantly while sales of juniors' and children's apparel, men's apparel and accessories and ladies' apparel and accessories increased moderately. Sales in the home and furniture category were down moderately.

The number of sales transactions decreased 2% over the prior year while the average dollars per sales transaction increased significantly.