UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended August 31, 2018

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number 0-8814

PURE CYCLE CORPORATION

(Exact name of registrant as specified in its charter)

|

Colorado

|

84-0705083

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

34501 E. Quincy Ave., Bldg. 34, Box 10 Watkins, CO 80137

|

(303) 292-3456

|

|

|

(Address of principal executive offices) (Zip Code)

|

(Registrant’s telephone number, including area code)

|

Securities registered pursuant to Section 12(b) of the Act:

|

Common Stock 1/3 of $.01 par value

|

The NASDAQ Stock Market

|

|

|

(Title of each class)

|

(Name of each exchange on which registered)

|

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of

Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒

No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein,

and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or

an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☒

|

|

Non-accelerated filer ☐

|

Smaller reporting company ☒

|

|

Emerging growth company ☐

|

If an emerging growth company, indicate by check mark if the registrant has elected to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common

equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $134,634,077

Indicate the number of shares outstanding of each of the registrant’s classes of

common stock, as of the latest practicable date: November 8, 2018 - 23,764,098

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III is incorporated by reference from the

registrant’s definitive proxy statement for the Annual Meeting of Shareholders to be held in January 2019, which will be filed with the SEC within 120 days of the close of the fiscal year ended August 31, 2018.

|

Item

|

Page

|

|

|

Part I

|

||

|

1

|

4

|

|

|

1A.

|

19

|

|

|

1B.

|

28 | |

|

2

|

28 | |

|

3

|

28

|

|

|

4

|

28 | |

|

Part II

|

||

|

5

|

29 | |

|

6

|

31 | |

|

7

|

32 | |

|

7A.

|

44 | |

|

8

|

45 | |

|

9

|

46 | |

|

9A.

|

46 | |

|

9B.

|

47 | |

|

Part III

|

||

|

10

|

48 | |

|

11

|

48 | |

|

12

|

48 | |

|

13

|

48 | |

|

14

|

48 | |

|

Part IV

|

||

|

15

|

49 | |

|

16

|

49 | |

| 54 |

FORWARD-LOOKING STATEMENTS

Statements that are not historical facts contained in this Annual Report on Form 10-K, or incorporated by reference into this Annual Report on Form 10-K,

are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as

amended (the “Exchange Act”). The words “anticipate,” “seek,” “project,” “future,” “likely,” “believe,” “may,” “should,” “could,” “will,” “estimate,” “expect,” “plan,” “intend” and similar expressions, as they relate to us, are intended to identify

forward-looking statements. Forward-looking statements include statements relating to, among other things:

| ● |

factors affecting demand for water;

|

| ● |

our competitive advantage;

|

| ● |

plans to develop additional water assets within the Denver area;

|

| ● |

future water supply needs in Colorado and how such needs will be met;

|

| ● |

anticipated increases in residential and commercial demand for water services and competition for these services;

|

| ● |

estimated population increases in the Denver metropolitan area and the South Platte River basin;

|

| ● |

plans for the use and development of our water assets and potential delays;

|

| ● |

plans to provide water for drilling and hydraulic fracturing of oil and gas wells;

|

| ● |

changes in oil and gas drilling activity on our property, on the Lowry Range, or in the surrounding areas;

|

| ● |

regional cooperation among area water providers in the development of new water supplies and water storage, transmission and distribution systems as the most cost-effective

way to expand and enhance service capacities;

|

| ● |

the impact of individual housing and economic cycles on the number of connections we can serve with our water;

|

| ● |

increases in future water tap fees;

|

| ● |

negotiation of payment terms for fees;

|

| ● |

plans for development of our Sky Ranch property;

|

| ● |

the number of units planned for the first phase of development at Sky Ranch;

|

| ● |

the timing for the completion of construction of finished lots at Sky Ranch;

|

| ● |

the number of lots for which delivery is expected in calendar year 2019;

|

| ● |

estimated costs of earthwork, erosion control, streets, drainage and landscaping at Sky Ranch for calendar years 2018 and 2019;

|

| ● |

the estimated amount of reimbursable costs for Sky Ranch;

|

| ● |

capital required and costs to develop the first phase of Sky Ranch;

|

| ● |

estimated costs of improvements to be funded by Pure Cycle and constructed by the CAB;

|

| ● |

anticipated revenues and margins from development of our Sky Ranch property;

|

| ● |

estimated time period for build out of Sky Ranch and sufficiency of tap fees to fund infrastructure costs;

|

| ● |

the impact of any downturn in the homebuilding and credit markets on our business and financial condition;

|

| ● |

the sufficiency of our working capital and financing sources to fund our operations;

|

| ● |

estimated supply capacity of our water assets;

|

| ● |

need for additional production capacity;

|

| ● |

costs and plans for treatment of water and wastewater;

|

| ● |

plans to use raw water, effluent water or reclaimed water for agricultural and irrigation uses;

|

| ● |

participation in regional water projects, including “WISE” and the timing and availability of water from, and projected costs related to, WISE;

|

| ● |

our ability to assist Colorado “Front Range” water providers in meeting current and future water needs;

|

| ● |

timing of and interpretation of Land Board royalties;

|

| ● |

the number of new water connections needed to recover the costs of our water supplies;

|

| ● |

the adequacy of the provisions in the “Lease” for the Lowry Range to cover present and future circumstances;

|

| ● |

factors that may impact labor and material costs;

|

| ● |

loss of key employees and hiring additional personnel for our operations;

|

| ● |

anticipated timing and amount of, and sources of funding for, (i) capital expenditures to construct infrastructure and increase production capacities, (ii) compliance with

water, environmental and other regulations, and (iii) operations, including delivery and treatment of water and wastewater;

|

| ● |

the ability of our deep water well enhancement tool and process to increase efficiency of wells and our plans to use the tool when we drill new water wells and to market

the tool to area water providers;

|

| ● |

plans to drill water walls into aquifers located beneath the Lowry Range and the timing and estimated costs of such a build out;

|

| ● |

our ability to reduce the amount of up-front construction costs for water and wastewater systems;

|

| ● |

ability to generate working capital and market our water assets;

|

| ● |

plans to sell and estimated value of certain farms;

|

| ● |

service life of constructed facilities;

|

| ● |

use of third parties to construct water and wastewater facilities and Sky Ranch lot improvements;

|

| ● |

plans to utilize fixed-price contracts;

|

| ● |

payment of amounts due from the Rangeview District and the Sky Ranch Districts;

|

| ● |

capital expenditures for investing in expenses and assets of the Rangeview District;

|

| ● |

the impact of water quality, solid waste disposal and environmental regulations on our financial condition and results of operations;

|

| ● |

environmental clean-up at the Lowry Range by the U.S. Army Corps of Engineers;

|

| ● |

our ability to comply with permit requirements and environmental regulations and the cost of such compliance;

|

| ● |

our ability to meet customer demands in a sustainable and environmentally friendly way;

|

| ● |

the recoverability of construction and acquisition costs from rates;

|

| ● |

our belief that we are not a public utility under Colorado law;

|

| ● |

changes in unrecognized tax positions;

|

| ● |

plans to retain earnings and not pay dividends;

|

| ● |

forfeitures of option grants, vesting of non-vested options and the fair value of option awards;

|

| ● |

the effectiveness of our disclosure controls and procedures and our internal controls over financial reporting;

|

| ● |

accounting estimates and the impact of new accounting pronouncements;

|

| ● |

future fluctuations in the price and trading volume of our common stock; and

|

| ● |

timing of the filing of our proxy statement.

|

Forward-looking statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions. We

cannot assure you that any of our expectations will be realized. Our actual results could differ materially from those in such statements. Factors that could cause actual results to differ from those contemplated by such forward-looking statements

include, without limitation:

| ● |

the timing of new home construction and other development in the areas where we may sell our water, which in turn may be impacted by credit availability;

|

| ● |

population growth;

|

| ● |

changes in employment levels, job and personal income growth and household debt-to-income levels;

|

| ● |

changes in consumer confidence generally and confidence of potential homebuyers in particular;

|

| ● |

the ability of existing homeowners to sell their existing homes at prices that are acceptable to them;

|

| ● |

changes in the supply of available new or existing homes and other housing alternatives, such as apartments and other residential rental property;

|

| ● |

timing of oil and gas development in the areas where we sell our water;

|

| ● |

general economic conditions;

|

| ● |

the market price of water;

|

| ● |

the market price of oil and gas;

|

| ● |

changes in customer consumption patterns;

|

| ● |

changes in applicable statutory and regulatory requirements;

|

| ● |

changes in governmental policies and procedures, including with respect to land use and environmental and tax matters;

|

| ● |

changes in interest rates;

|

| ● |

private and federal mortgage financing programs and lending practices;

|

| ● |

uncertainties in the estimation of water available under decrees;

|

| ● |

uncertainties in the estimation of costs of delivery of water and treatment of wastewater;

|

| ● |

uncertainties in the estimation of the service life of our systems;

|

| ● |

uncertainties in the estimation of costs of construction projects;

|

| ● |

the strength and financial resources of our competitors;

|

| ● |

our ability to find and retain skilled personnel;

|

| ● |

climatic and weather conditions, including floods, droughts and freezing conditions;

|

| ● |

labor relations;

|

| ● |

turnover of elected and appointed officials and delays caused by political concerns and government procedures;

|

| ● |

availability and cost of labor, material and equipment;

|

| ● |

delays in anticipated permit and construction dates;

|

| ● |

engineering and geological problems;

|

| ● |

environmental risks and regulations;

|

| ● |

our ability to raise capital;

|

| ● |

our ability to negotiate contracts with new customers;

|

| ● |

uncertainties in water court rulings;

|

| ● |

unauthorized access to confidential information and data on our information technology systems and security and data breaches; and

|

| ● |

the factors described under “Risk Factors” in this Annual Report on Form 10-K.

|

We undertake no obligation, and disclaim any obligation, to publicly update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise. All forward-looking statements are expressly qualified by this cautionary statement.

Glossary of terms

The following terms are commonly used in the water industry and are used throughout our annual report:

| ● |

Acre Foot – approximately 326,000 gallons of water, or enough water to cover an acre of ground with one foot of water. For some instances herein, as context dictates, the

term “acre feet” is used to designate an annual decreed amount of water available during a typical year.

|

| ● |

Customer Facilities – facilities that carry potable water and reclaimed water to customers from the retail water distribution system (see “Retail Facilities” below) and

collect wastewater from customers and transfer it to the retail wastewater collection system. Water and wastewater service lines, interior plumbing, meters and other components are typical examples of Customer Facilities. In many cases,

portions of the Customer Facilities are constructed by the developer. Customer Facilities are typically owned and maintained by the customer.

|

| ● |

Non-Tributary Groundwater – groundwater located outside the boundaries of any designated groundwater basins in existence on January 1, 1985, the withdrawal of which will

not, within one hundred years of continuous withdrawal, deplete the flow of a natural stream at an annual rate greater than one-tenth of one percent of the annual rate of withdrawal.

|

| ● |

Not Non-Tributary Groundwater – statutorily defined as groundwater located within those portions of the Dawson, Denver, Arapahoe, and Laramie Fox-Hill aquifers outside of

designated basins that does not meet the definition of “non-tributary.”

|

| ● |

Retail Facilities – facilities that distribute water to and collect wastewater from an individual subdivision or community. Developers are typically responsible for the

funding and construction of Retail Facilities. Once we certify that the Retail Facilities have been constructed in accordance with our design criteria, the developer dedicates the Retail Facilities to a quasi-municipal political

subdivision of the state, and we operate and maintain the facilities on behalf of such political subdivision.

|

| ● |

Section – a parcel of land equal to one square mile and containing 640 acres.

|

| ● |

SFE – a single family equivalent unit. One SFE is a customer – whether residential, commercial or industrial – that imparts a demand on our water or wastewater systems

similar to the demand of a family of four persons living in a single-family house on a standard sized lot. One SFE is assumed to have a water demand of approximately 0.4 acre feet per year and to contribute wastewater flows of

approximately 300 gallons per day.

|

| ● |

Special Facilities – facilities that are required to extend services to an individual development and are not otherwise classified as a typical “Wholesale Facility” or

“Retail Facility.” Temporary infrastructure required prior to construction of permanent water and wastewater systems or transmission pipelines to transfer water from one location to another are examples of Special Facilities. We

typically design and construct the Special Facilities using funds provided by the developer in addition to the normal rates, fees and charges that we collect from our customers. We are typically responsible for the operation and

maintenance of the Special Facilities upon completion.

|

| ● |

Tributary Groundwater – all water located in an aquifer that is hydrologically connected to a natural stream such that depletion has an impact on the surface stream.

|

| ● |

Tributary Surface Water – water on the surface of the ground flowing in a stream or river system.

|

| ● |

Wholesale Facilities – facilities that serve an entire service area or major regions or portions thereof. Wells, treatment plants, pump stations, tanks, reservoirs,

transmission pipelines, and major sewage lift stations are typical examples of Wholesale Facilities. We own, design, construct, operate, maintain and repair Wholesale Facilities which are typically funded using rates, fees and charges

that we collect from our customers.

|

PART I

Pure Cycle Corporation, a Colorado corporation (“we,” “us” or “our”), is a vertically integrated water company that:

| ● |

provides wholesale water and wastewater services;

|

| ● |

designs, constructs, operates and maintains water and wastewater systems;

|

| ● |

supplies untreated water for hydraulic fracturing and other commercial/industrial uses; and

|

| ● |

is developing a master planned mixed-use community as part of our plan to monetize our land and water assets.

|

As a vertically integrated water company, we own or control substantially all assets necessary to provide wholesale water and wastewater services to our

customers. We own or control the water rights that we use to provide domestic and irrigation water to our wholesale customers (including surface water, groundwater, reclaimed water rights and water storage rights). We own the infrastructure

required to (i) withdraw, treat, store and deliver water (such as wells, diversion structures, pipelines, reservoirs and treatment facilities); (ii) collect, treat, store and reuse wastewater; and (iii) treat and deliver reclaimed water for

irrigation use. We are principally targeting the “I-70 corridor,” a largely undeveloped area located east of downtown Denver and south of Denver International Airport along Interstate 70, as we expect the I-70 corridor to experience substantial

growth over the next 30 years.

We provide wholesale water and wastewater services predominantly to two local governmental entities that in turn provide residential and commercial water

and wastewater services to communities along the eastern slope of Colorado in the area referred to as the “Front Range,” extending essentially from Fort Collins on the north to Colorado Springs on the south. Our largest customer is the Rangeview

Metropolitan District (the “Rangeview District”), which is a quasi-municipal political subdivision of the State of Colorado. We have the exclusive right to provide wholesale water and wastewater services to the Rangeview District and its end-use

customers pursuant to the “Rangeview Water Agreements” and the “Off-Lowry Service Agreement” (each as defined below). Through the Rangeview District, we currently provide wholesale service to 391 SFE water connections and 157 SFE wastewater

connections located in the Rangeview District’s service area of southeastern metropolitan Denver in an area called the Lowry Range and other nearby areas where we have acquired service rights.

We supply untreated water to industrial customers for various purposes and to oil and gas companies for hydraulic fracturing on properties located within

or adjacent to our service areas. Oil and gas operators have leased more than 135,000 acres within and adjacent to our service areas to explore and develop oil and gas interests in the oil-rich Niobrara and other formations. We have capitalized on

the need for significant water supplies for hydraulic fracturing in proximity to our existing water supplies and infrastructure.

In addition to our water and wastewater operations, we are developing 931 acres of land we own along Denver’s I-70 corridor as a master planned community

known as Sky Ranch. In June 2017, we entered into agreements to sell a total of 506 residential lots at Sky Ranch to three national home builders. In March 2018, we began construction of finished lots at Sky Ranch and in July 2018, we achieved the

first payment milestone for the sale of 150 platted lots to two of our home builders pursuant to agreements with each builder. Pursuant to agreements with the Rangeview District, we are the exclusive provider of wholesale water and wastewater

services to the future residents of Sky Ranch.

Pure Cycle Corporation was incorporated in Delaware in 1976 and reincorporated in Colorado in 2008. Unless otherwise specified or the context otherwise

requires, all references to “we,” “us,” or “our” are to Pure Cycle Corporation and its subsidiaries on a consolidated basis. Pure Cycle’s common stock trades on The NASDAQ Stock Market under the ticker symbol “PCYO.”

Our Water and Land Assets

This section should be read in conjunction with Item 1A – Risk Factors,

Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations – Critical Accounting Policies and Use of Estimates, and Note 4 – Water and Land Assets.

The $36.7 million of capitalized water costs on our balance sheet represents the

costs of the water rights we own or have the exclusive right to use and the related infrastructure developed to provide wholesale water and wastewater services. Our water assets are as follows:

Table A - Water Assets

|

Water Source

|

Groundwater

(acre feet)

|

|||

|

Lowry (Rangeview Water Supply)

|

||||

|

Export (1)

|

11,650

|

|||

|

Non-Export (1)

|

12,035

|

|||

|

Fairgrounds

|

321

|

|||

|

Sky Ranch

|

828

|

|||

|

24,834

|

||||

|

Surface Water

(acre feet)

|

||||

|

Lowry (1)

|

3,300

|

|||

|

WISE

|

500

|

|||

|

3,800

|

||||

|

Total (Groundwater and Surface Water)

|

28,634

|

|||

| (1) |

The combined Lowry water rights are 26,985 acre feet.

|

We believe we can serve approximately 60,000 SFEs.

Our service areas and water and land assets are described in greater detail in the maps and discussion that follow.

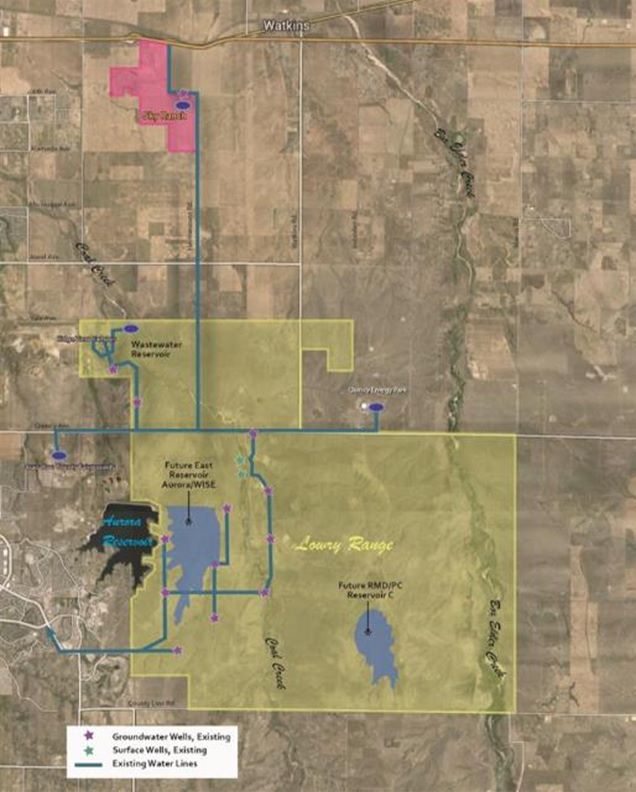

The map below indicates the location of our Denver area assets.

Rangeview Water Supply and the Lowry Range

Our Rangeview Water – We own or control a

total of approximately 3,300 acre feet of tributary surface water, 23,685 acre feet of non-tributary and not non-tributary groundwater rights, and approximately 26,000 acre feet of adjudicated reservoir sites that we refer to as our “Rangeview

Water Supply.” This water is located in the southeast Denver metropolitan area at the “Lowry Range,” which is owned by the State Board of Land Commissioners (the “Land Board”) and is described below.

Rangeview Water Agreements – We acquired our

Rangeview Water Supply in April 1996 pursuant to the following agreements:

| (i) |

The 1996 Amended and Restated Lease Agreement between the Land Board and the Rangeview District, which was superseded by the 2014 Amended and Restated Lease Agreement,

dated July 10, 2014 (the “Lease”), among the Land Board, the Rangeview District and us;

|

| (ii) |

The Agreement for Sale of non-tributary and not non-tributary groundwater which we can “export” from the Lowry Range to supply water to nearby communities (this portion of

the Rangeview Water Supply is referred to as our “Export Water”) between us and the Rangeview District (the “Export Agreement”); and

|

| (iii) |

The 1996 Service Agreement between us and the Rangeview District for the provision of water service to the Rangeview District’s customers located on the Lowry Range, which

was superseded by the Amended and Restated Service Agreement, dated July 11, 2014 (the “Lowry Service Agreement”), between us and the Rangeview District.

|

Additionally, in 1997 we entered into a Wastewater Service Agreement (the “Lowry Wastewater Agreement”) with the Rangeview District to provide wastewater

service to the Rangeview District’s customers on the Lowry Range.

The Lease, the Export Agreement, the Lowry Service Agreement and the Lowry Wastewater Agreement are collectively referred to as the “Rangeview Water

Agreements.”

Pursuant to the Rangeview Water Agreements, we design, construct, operate and maintain the Rangeview District’s water and wastewater systems to allow the

Rangeview District to provide water and wastewater service to its customers located within the Rangeview District’s service area at the Lowry Range. Subject to

the terms and conditions of the Lease, we are the exclusive water and wastewater provider on the Lowry Range, and we operate both the water and the wastewater systems during our contract period on behalf of the Rangeview District, which owns the

facilities for both systems. At the expiration of our contract term in 2081, ownership of the water system facilities located on the Lowry Range used to deliver non-Export Water to customers will revert to the Land Board, with the Rangeview

District retaining ownership of the wastewater facilities. Through facilities we own, we use our Export Water, and we intend to use other supplies owned by us, to provide wholesale water service and wastewater service to customers located outside

of the Lowry Range, including customers of the Rangeview District and other governmental entities and industrial and commercial customers.

Of the approximately 26,985 acre feet of water comprising our Rangeview Water Supply, we own 11,650 acre feet of Export Water, which consists of 10,000

acre feet of groundwater and 1,650 acre feet of average yield surface water, pending completion by the Land Board of documentation related to the exercise of our right to substitute 1,650 acre feet of our groundwater for a comparable amount of

surface water. Additionally, assuming the completion of the substitution of groundwater for surface water, we hold the exclusive right to develop and deliver through the year 2081 the remaining 13,685 acre feet of groundwater and approximately

1,650 acre feet of average yield surface water to customers either on or off of the Lowry Range. The Rangeview Water Agreements also grant us the right to use surface reservoir capacity to provide water service to customers both on and off the

Lowry Range.

The Lowry Range Property – The Lowry Range is

located in unincorporated Arapahoe County, about 20 miles southeast of downtown Denver. The Lowry Range is one of the largest contiguous parcels under single ownership next to a major metropolitan area in the United States. The Lowry Range is

approximately 27,000 acres in size or about 40 square miles of land. Of the 27,000 acres, pursuant to our agreements with the Land Board and the Rangeview District, we have the exclusive rights to provide water and wastewater services to

approximately 24,000 acres of the Lowry Range.

Rangeview Metropolitan District – The

Rangeview District is a quasi-municipal corporation and political subdivision of Colorado formed in 1986 for the purpose of providing water and wastewater service to the Lowry Range and other approved areas. The Rangeview District is governed by an

elected board of directors. Eligible voters and persons eligible to serve as directors of the Rangeview District must own an interest in property within the boundaries of the Rangeview District. We own certain rights and real property interests

which encompass the current boundaries of the Rangeview District. The current directors of the Rangeview District are Mark W. Harding (our President, Chief Financial Officer and a director), Scott E. Lehman (a Pure Cycle employee), and Dirk

Lashnits (a Pure Cycle employee), and one independent board member. Pursuant to Colorado law, directors may receive $100 for each board meeting they attend, up to a maximum of $1,600 per year. Mr. Harding, Mr. Lehman, and Mr. Lashnits have all

elected to forego these payments.

South Metropolitan Water Supply Authority (“SMWSA”)

and Water Infrastructure Supply Efficiency Partnership (“WISE”) – SMWSA is a municipal water authority in the State of Colorado organized to pursue the acquisition and development of new water supplies on behalf of its members, including

the Rangeview District. SMWSA members include 14 Denver area water providers in Arapahoe and Douglas Counties. The Rangeview District became a member of SMWSA in 2009 in an effort to participate with other area water providers in developing

regional water supplies along the Front Range. We entered into a Participation Agreement with the Rangeview District on December 16, 2009, whereby we agreed to provide funding to the Rangeview District in connection with its membership in the SMWSA

(the “SMWSA Participation Agreement”). SMWSA members have been working with the City and County of Denver acting through its Board of Water Commissioners (“Denver Water”) and the City of Aurora acting by and through its utility enterprise (“Aurora

Water”) on a cooperative water project known as the WISE, which seeks to develop regional infrastructure that would interconnect members’ water transmission systems to be able to develop additional water supplies from the South Platte River in

conjunction with Denver Water and Aurora Water. In July 2013, the Rangeview District together with nine other SMWSA members formed the South Metro WISE Authority (“SMWA”) pursuant to the South Metro WISE Authority Formation and Organizational

Intergovernmental Agreement (the “SM IGA”) to enable its members to participate in WISE. The SM IGA specifies each member’s pro rata share of WISE and the members’ rights and obligations with respect to WISE. On December 31, 2013, SMWA, Denver

Water and Aurora Water entered into the Amended and Restated WISE Partnership – Water Delivery Agreement (the “WISE Partnership Agreement”), which provides for the purchase and construction of certain infrastructure (pipelines, water storage

facilities, water treatment facilities, and other appurtenant facilities) to deliver water to and among the 10 members of the SMWA, Denver Water and Aurora Water. We have entered into the Rangeview/Pure Cycle WISE Project Financing and Service

Agreement with the Rangeview District dated November 19, 2014 (effective as of December 22, 2014), which obligates us to fund the Rangeview District’s cost of participating in WISE (the “WISE Financing Agreement”). In exchange for funding the

Rangeview District’s obligations in WISE, we have the sole right to use and reuse the Rangeview District’s approximate 7% share of the WISE water and infrastructure to provide water service to the Rangeview District’s customers and to receive the

revenue from such service. Our current WISE subscription entitles us to approximately three million gallons per day of transmission pipeline capacity and 500 acre feet per year of water. In accordance with the WISE Financing Agreement and the SMWSA

Participation Agreement, to date we have provided approximately $3.1 million of financing to the Rangeview District to fund its obligation to finance the purchase of infrastructure for WISE, its obligations related to SMWSA, and the construction of

a connection to the WISE system. We anticipate that we will be spending the following over the next five fiscal years to fund the Rangeview District’s purchase of its share of the water transmission line and additional facilities, water and related

assets for WISE and to fund operations and water deliveries related to WISE:

Table B – Estimated WISE Costs

|

For the Fiscal Years Ended August 31,

|

||||||||||||||||||||

|

2019

|

2020

|

2021

|

2022

|

2023

|

||||||||||||||||

|

Subscription (Operations)

|

$

|

99,478

|

$

|

99,478

|

$

|

99,478

|

$

|

99,478

|

$

|

99,478

|

||||||||||

|

Water Deliveries

|

362,500

|

543,800

|

725,000

|

906,300

|

906,300

|

|||||||||||||||

|

Capital (Infrastructure)

|

2,528,400

|

50,000

|

50,000

|

50,000

|

50,000

|

|||||||||||||||

|

Other

|

20,000

|

25,000

|

30,000

|

35,000

|

40,000

|

|||||||||||||||

|

$

|

3,010,378

|

$

|

718,278

|

$

|

904,478

|

$

|

1,090,778

|

$

|

1,095,778

|

|||||||||||

Land Board Royalties – Pursuant to the

Rangeview Water Agreements, the Land Board is entitled to royalty payments based on a percentage of revenues earned from water sales that utilize water from the Rangeview Water Supply. The calculation of royalties depends on the water source,

whether the customer is a public or private entity, and the location of the customer. Royalties were modified in July 2014 pursuant to the terms of the Lease. The Land Board does not receive a royalty from wastewater services.

Water Customers – When we develop, operate and deliver water service utilizing water from our Rangeview Water Supply, payments from customers generate royalties to the Land Board at a rate of 12%

of gross revenues from private customers and customers on the Lowry Range and 10% from public entity customers. In the event that either (i) metered production of water used on the Lowry Range in any calendar year exceeds 13,000 acre feet or (ii)

10,000 surface acres on the Lowry Range have been rezoned to non-agricultural use, finally platted and water tap agreements have been entered into with respect to all improvements to be constructed on such acreage, the Land Board may elect, at its

option, to receive, in lieu of its royalty of 12% of gross revenues, 50% of the collective net profits (ours and the Rangeview District’s) derived from the sale or other disposition of water on the Lowry Range. To date, neither of these conditions

has been met, and such conditions are not likely to be met any time soon. In addition to royalties on the sale of metered water deliveries, the Land Board will receive a royalty on the sale of water taps, except for the sale of any taps to Sky

Ranch, at the rate of two percent of the gross amount received from the sale of a water tap.

We are also required to pay the Land Board a minimum annual water production fee of $45,600 per year, which is to be credited against

future royalties.

Sale of Water Rights – In the event we sell our Export Water right outright rather than developing and delivering water service, royalties to the Land Board escalate based on the amount of

gross revenue we receive and are lower for sales to a water district or similar municipal or public entity than for sales to a private entity as defined under the Lease. The Company does not currently contemplate selling its rights to the Export

Water.

East Cherry Creek Valley System – Pursuant to

a 1982 contractual right, the Rangeview District may purchase water produced from East Cherry Creek Valley Water and Sanitation District’s (“ECCV”) Land Board system. ECCV’s Land Board system is comprised of eight wells and more than 10 miles of

buried water pipeline located on the Lowry Range. In May 2012, in order to increase the delivery capacity and reliability of these wells, in our capacity as the Rangeview District’s service provider and the Export Water Contractor (as defined in

the Lease among us, the Rangeview District and the Land Board), we entered into an agreement to operate and maintain the ECCV facilities allowing us to utilize the system to provide water to commercial and industrial customers, including customers

providing water for drilling and hydraulic fracturing of oil and gas wells. Our costs associated with the use of the ECCV system are a flat monthly fee of $8,000 per month from January 1, 2013 through December 31, 2020 and will decrease to $3,000

per month from January 1, 2021 through April 2032. Additionally, we pay a fee per 1,000 gallons of water produced from ECCV’s system, which is included in the water usage fees charged to customers.

Revenues from our Rangeview Water Supply – We

generate revenues through our wholesale water and wastewater operations predominantly from three sources: (i) monthly water usage and wastewater treatment fees, (ii) one-time water and wastewater tap fees and construction fees/Special Facility

funding, and (iii) consulting fees. Our revenue sources and how we account for them are described in greater detail below. We typically negotiate the payment terms for tap fees, construction fees, and other water and wastewater service fees with

our wholesale customers as a component of our service agreements prior to construction of the project. However, with respect to customers on the Lowry Range, pursuant to the Lease, the Rangeview District’s rates and charges to such end-use

customers may not exceed the average of similar rates and charges of three nearby water providers.

| (i) |

Monthly Water Usage and Wastewater Treatment Fees – Monthly wholesale water usage fees are assessed to our customers based on actual metered deliveries to their end-use customers each month. Water usage fees are based

on a tiered pricing structure that provides for higher prices as customers use greater amounts of water. The water usage fees for end-use customers on the Lowry Range are noted below in Table C:

|

Table C – Lowry Range Tiered Water Usage Pricing Structure

|

Price ($ per thousand gallons)

|

||||

|

Base charge per SFE

|

$

|

32.27

|

||

|

0 gallons to 10,000 gallons

|

$

|

3.91

|

||

|

10,001 gallons to 20,000 gallons

|

$

|

5.14

|

||

|

20,001 gallons to 40,000 gallons

|

$

|

8.08

|

||

|

40,001 gallons and above

|

$

|

9.87

|

||

The figures in Table C reflect the amounts charged to the Rangeview District’s end-use customers on the Lowry Range. In exchange for

providing water service to the Rangeview District’s Lowry Range customers, we receive 98% of the usage charges received by the Rangeview District relating to water services after deducting the required royalty to the Land Board (described above at

Rangeview Water Supply and Lowry Range – Land Board Royalties).

The amounts charged by the Rangeview District to its end-use customers off the Lowry Range are determined pursuant to the Rangeview

District’s service agreements with such customers and such rates may vary. In exchange for providing water service to the Rangeview District’s customers off the Lowry Range, we receive 98% of the usage charges received by the Rangeview District

relating to water services after deducting any required royalty to the Land Board. The royalty to the Land Board is required for water service provided utilizing our Rangeview Water Supply, which includes most of our current customers off the Lowry

Range except those at Wild Pointe.

In addition to the tiered water usage pricing structure, we currently charge a hydrant rate of $10.50 per thousand gallons for

commercial and industrial customers. We also collect other immaterial fees and charges from customers and other users to cover miscellaneous administrative and service expenses, such as application fees, review fees and permit fees.

In exchange for providing wastewater services, we receive 90% of the Rangeview District’s monthly wastewater treatment fees, as well as

the right to use or sell the reclaimed water.

| (ii) |

Water and Wastewater Tap Fees and Construction Fees/Special Facility Funding – Tap fees are typically paid by developers in advance of construction activities and are non-refundable. Tap fees are typically

used to fund construction of the Wholesale Facilities and defray the acquisition costs of obtaining water rights.

|

The Rangeview District’s 2018 water tap fees are

$24,974, and its wastewater tap fees are $4,659.

In exchange for providing water service to the Rangeview District’s customers on the Lowry Range, we receive 100% of the Rangeview

District’s tap fees after deducting the two percent royalty to the Land Board described above. If water taps are sold to customers not located on the Lowry Range that are to be serviced utilizing the Rangeview Water Supply (other than taps to Sky

Ranch, which are exempt), the two percent royalty to the Land Board would be deducted from the amount we receive. In exchange for providing wastewater services, whether to customers on or off the Lowry Range, we receive 100% of the Rangeview

District’s wastewater tap fees.

Construction fees are fees we receive, typically in advance, from developers for us to build certain infrastructure such as Special

Facilities, which are normally the responsibility of the developer.

| (iii) |

Consulting Fees – Consulting fees are fees we receive, typically on a monthly basis, from

municipalities and area water providers along the I-70 corridor, for systems with respect to which we provide contract operations services.

|

|

Arapahoe County Fairgrounds Agreement for Water Service

|

|

|

|

In 2005, we entered into an Agreement for Water Service (the “County Agreement”) with Arapahoe County to design, construct,

operate and maintain a water system for, and provide water services to, the county for use at the Arapahoe County fairgrounds (the “Fairgrounds”), which are located west of the Lowry Range. Pursuant to the County Agreement, we purchased

321 acre feet of water from the county in 2008. Further details of the arrangements with the county are described in Note 4 – Water and Land Assets

to the accompanying financial statements.

|

||

|

Pursuant to the County Agreement, we constructed and own a deep water well, a 500,000-gallon water tank and pipelines to

transport water to the Fairgrounds. The construction of these items was completed in our fiscal 2006, and we began providing water service to the county in 2006.

|

Water Sales for Fracking

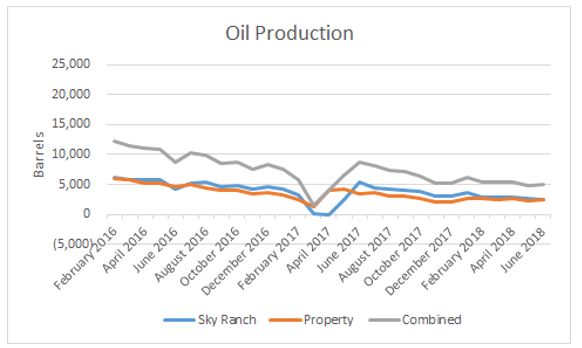

We provide water for hydraulic fracturing (“fracking”) of oil and gas wells being developed in the Niobrara Formation to and around the Land Board’s

Lowry Range property and our Sky Ranch property. Oil and gas drilling in our area is affected by the price of oil, and the number of wells drilled and fracked can vary from year to year. Each well developed in the Niobrara Formation utilizes

between 10 and 20 million gallons of water to drill and frack, which equates to selling water to between approximately 100 and 200 homes for an entire year.

Water revenues from sales of water for the construction of well sites, drilling and fracking wells developed in the Niobrara Formation were approximately

$4,044,300 and $478,500 during the fiscal years ended August 31, 2018 and 2017,

respectively. With a large percentage of the acreage surrounding the Lowry Range in Arapahoe, Adams, Elbert, and portions of Douglas Counties already leased by oil companies, we anticipate providing additional water for drilling and fracking of

oil and gas wells in the future. Previously, nearly all oil and gas development was attributable to our largest fracking customer ConocoPhillips Company (“ConocoPhillips”). However, in the past year, there have been three other oil and gas

companies acquiring lease interests in the area, and each of these companies has drilled and fracked wells. We anticipate continued development of oil and gas wells at the Lowry Range, Sky Ranch and the surrounding area by multiple operators. See

“Sales to the fracking industry can fluctuate significantly” in Item 1A – Risk Factors of this Annual Report on Form 10-K.

Service to Customers Not on the Lowry Range

Since January 2017, we have had an agreement with the Rangeview District to be the Rangeview District’s exclusive provider of water and wastewater

services to the Rangeview District’s customers located outside of its Lowry Range service area. This agreement was confirmed in the Export Service Agreement, dated June 16, 2017 (the “Off-Lowry Service Agreement”), between us and the Rangeview

District. Pursuant to the Off-Lowry Service Agreement, we design, construct, operate and maintain the Rangeview District’s water and wastewater systems and the systems of other communities that have service contracts with the Rangeview District

to provide water and wastewater services to the Rangeview District’s customers that are not on the Lowry Range (currently, Wild Pointe and Sky Ranch). In exchange for providing water and wastewater services to the Rangeview District’s customers

that are not on the Lowry Range, we receive 100% of water and wastewater tap fees, 98% of the water usage fees, and 90% of the monthly wastewater service and usage fees received by the Rangeview District from its customers that are not located on

the Lowry Range, after deduction of royalties due to the Land Board, if applicable. See Rangeview Water Supply and Lowry Range – Land Board Royalties

above. The water usage fees to be collected for service at Sky Ranch are the only fees that would currently be subject to the Land Board royalty.

Wild Pointe – Elbert & Highway 86 Commercial

Metropolitan District – In 2017, we entered into an agreement with the Rangeview District, which had entered into an agreement with Elbert & Highway 86 Commercial Metropolitan District (the “Elbert 86 District”) to operate and

maintain a water system for residential and commercial customers at the Wild Pointe development in Elbert County. The water system includes two deep water wells, a pump station, treatment facility, storage facility, over eight miles of

transmission lines, and approximately 457 acre feet of water rights serving the development. We provided $1.6 million in funding to acquire the exclusive rights to operate and maintain all the water facilities in exchange for payment of the

remaining residential and commercial tap fees and annual water use fees. Service to Wild Pointe is governed by the Off-Lowry Service Agreement.

Sky Ranch Water and Wastewater Service – As

described in more detail below, we are developing 931 acres of land we own as a master planned community known as Sky Ranch. Pursuant to

the Sky Ranch Water and Wastewater Service Agreement, dated June 19, 2017, between PCY Holdings, LLC, our wholly owned subsidiary and the owner of the Sky Ranch property (“PCY Holdings”), and the Rangeview District, PCY Holdings agreed to

construct certain facilities necessary to provide water and wastewater service to Sky Ranch, and the Rangeview District agreed to provide water and wastewater services for the Sky Ranch development. Pursuant to the Off-Lowry Service Agreement, we

are the exclusive provider of water and wastewater services to future residents of the Sky Ranch development.

Sky Ranch Development

In 2010, we purchased approximately 931 acres of undeveloped land located in unincorporated Arapahoe County known as Sky Ranch. Sky Ranch is located

directly adjacent to I-70, 16 miles east of downtown Denver, four miles north of the Lowry Range, and four miles south of Denver International Airport.

The property includes rights to approximately 830 acre feet of water and approximately 640 acres of oil and gas mineral rights and has been zoned for

residential, commercial and retail uses that may include up to 4,850 SFEs. Sky Ranch is zoned for 4,400 homes and 1.6 million square feet of commercial, retail and light industrial development. Sky Ranch will develop in multiple phases over a

number of years. Our first phase of 151 acres is platted for 506 detached single-family residential lots. We have entered into purchase and sale agreements (described in more detail below) with three national home builders pursuant to which the

Company agreed to sell, and the builders agreed to purchase, the initial 506 residential lots at the property. We began construction of 250 residential lots for entry-level housing (houses costing in the $300,000 range) on March 1, 2018, with

model homes scheduled for construction in late 2018. We expect to phase the development of our initial 506 lots beginning with delivery of approximately 150 finished lots in early 2019, delivering an additional 100 lots in mid-2019 and the

balance of the lots to each builder depending on home sales. We estimate that build out of our initial 506 lots will take between three and four years. We have leased the oil and gas minerals underlying the land to a major independent exploration

and production company.

In June 2017, we entered into purchase and sale agreements (collectively, the “Purchase and Sale Contracts”) with three separate home builders pursuant

to which we agreed to sell, and each builder agreed to purchase, a certain number (totaling 506) of single-family, detached residential lots at Sky Ranch. We will be developing finished lots for each of the three home builders (which are lots on

which homes are ready to be built that include roads, curbs, wet and dry utilities, storm drains and other improvements). Each builder is required to purchase water and sewer taps for the lots from the Rangeview District, the cost of which

depends on the size of the lot, the size of the house, and the amount of irrigated turf. Pursuant to the Off-Lowry Service Agreement, we will receive all of the water tap fees and wastewater tap fees. We will receive the monthly service fees and

usage fees for wastewater services received by the Rangeview District from customers at Sky Ranch net of a 10% fee retained by the Rangeview District. We will also receive the usage fees for water services received by the Rangeview District from

customers at Sky Ranch, after deduction, in most instances, of the royalty to the Land Board related to the use of the Rangeview Water Supply, net of a 2% fee retained by the Rangeview District.

In November 2017, each builder completed its due diligence under the Purchase and Sale Contracts, at which time certain earnest money deposits by each

builder became non-refundable. In July 2018, we obtained final approval of the entitlements for the property and achieved the first payment milestone for 150 platted lots to two of our builders. We received a payment of $2,500,000, and the two

builders posted letters of credit for an additional $7,775,000. We are working to complete construction of finished lots in fiscal year 2019 and will receive two additional payments, to be distributed from the escrowed funds, from each of these

builders. The first additional payment will be distributed upon completion of construction of wet utilities, and the final payment will be distributed upon completion of finished lots. Additionally, we will receive payment from our third builder

upon completion of finished lots.

We are obligated pursuant to the Purchase and Sale Contracts, or separate Lot Development Agreements (the “Lot Development Agreements” and, together with

the Purchase and Sale Contracts, the “Builder Contracts”), to construct infrastructure and other improvements, such as roads, curbs and gutters, park amenities, sidewalks, street and traffic signs, water and sanitary sewer mains and stubs, storm

water management facilities, and lot grading improvements for delivery of finished lots to each builder. Pursuant to the Builder Contracts, we must cause the Rangeview District to install and construct off-site infrastructure improvements (i.e.,

a wastewater reclamation facility and wholesale water facilities) for the provision of water and wastewater service to the property. In conjunction with our approvals with Arapahoe County for the Sky Ranch project, we and/or the Rangeview

District and the Sky Ranch Districts or the CAB (each as defined and described in more detail below) are obligated to deposit into an account the anticipated costs to install and construct substantially all the off-site infrastructure

improvements (which include drainage, wholesale water and wastewater facilities, and entry roadway), which we estimate will be approximately $10.2 million.

The improvements, such as roads, parks, and water and sanitary sewer mains, that will be shared by all homeowners in the development and not specific to

a finished lot will ultimately be owned by the Sky Ranch Districts or the CAB. Upon completion of the improvements and acceptance by the Sky Ranch Districts or the CAB, we will be entitled to reimbursement for the verified costs incurred with

respect to such improvements. We estimate that the total capital required to develop lots in the first phase (506 lots) of Sky Ranch will be approximately $35 million, which includes estimated reimbursable costs of approximately of $27 million

that will be reimbursable to us by the CAB, and that lot sales to home builders will generate approximately $36 million in revenues, providing a margin on lots of approximately $1 million prior to receipt of reimbursable expenses. The Company and

the CAB have agreed that no payment is required by the CAB with respect to reimbursable costs unless and until the CAB and/or the Sky Ranch Districts issue bonds in an amount sufficient to reimburse us for all or a portion of advances provided,

or expenses incurred for reimbursables. Due to this contingency, the reimbursable costs will be included in lot development capitalized costs until the point in time when bonding is obtained. At that point, all reimbursable costs will be reversed

and recorded as a note receivable and will reduce any remaining capitalized costs. Any excess will be recognized as other income from CAB reimbursement.

Utility revenues will be derived from tap fees (which vary depending on lot size, house size, and amount of irrigated turf) and usage fees (which are

monthly water usage and wastewater treatment fees). Our current Sky Ranch water tap fees are $26,650 (per SFE), and wastewater taps fees are $4,659 (per SFE).

We have begun design and preliminary engineering for our second phase, which will include approximately 320 acres of residential development and 160

acres of commercial, retail, and industrial development along the I-70 frontage. We expect to have multiple phases being developed concurrently and would expect the development of the Sky Ranch project to occur over 10–14 years, depending on

demand.

Sky Ranch Metropolitan District Nos. 1, 3, 4, and 5

– The Sky Ranch Metropolitan District Nos. 1, 3, 4 and 5 are quasi-municipal corporations and political subdivisions of Colorado formed in 2004 for the purpose of providing service to the approximately 930 acres of the Sky Ranch property

(the “Sky Ranch Districts”). The Sky Ranch Districts are governed by an elected board of directors. Eligible voters and persons eligible to serve as directors of the Sky Ranch Districts must own an interest in property within the boundaries of

the district. We own certain rights and real property interests which encompass the current boundaries of the districts. The current directors of the districts are Mark W. Harding (our President, Chief Financial Officer and a director), Scott E.

Lehman (a Pure Cycle employee), and Dirk Lashnits (a Pure Cycle employee), and one independent board member. Pursuant to Colorado law, directors may receive $100 for each board meeting they attend, up to a maximum of $1,600 per year. Mr. Harding,

Mr. Lehman, and Mr. Lashnits have all elected to forego these payments.

Sky Ranch Community Authority Board

Pursuant to a certain Community Authority Board Establishment Agreement, as the same may be amended from time to time, Sky Ranch Metropolitan District

No. 1 and Sky Ranch Metropolitan District No. 5 formed the CAB to, among other things, design, construct, finance, operate and maintain certain public improvements for the benefit of the property within the boundaries and/or service area of the

Sky Ranch Districts. In order for the public improvements to be constructed and/or acquired, it is necessary for each Sky Ranch District, directly or through the CAB, to be able to fund the improvements and pay its ongoing operations and

maintenance expenses related to the provision of services that benefit the property. We have entered into agreements, first with Sky Ranch Metropolitan District No. 5 in 2014, and later with the CAB in November 2017 and June 2018, requiring us to

fund expenses related to the construction of an agreed upon list of improvements for the Sky Ranch property.

On September 18, 2018, the parties entered into a series of agreements, including a Facilities Funding and Acquisition Agreement with an effective date

of November 13, 2017 (the “2018 FFAA”), which supersedes and consolidates the previous agreements and pursuant to which

| ● |

the CAB agreed to repay the amounts owed by Sky Ranch Metropolitan District No. 5 to Pure Cycle, and the previous Facilities Funding and Acquisition Agreement entered

into between Pure Cycle and Sky Ranch Metropolitan District No. 5 in 2014 was terminated;

|

| ● |

the November 2017 Project Funding and Reimbursement Agreement and the June 2018 Funding Acquisition Agreement between the CAB and Pure Cycle were terminated;

|

| ● |

the CAB acknowledged all amounts owed to Pure Cycle under the terminated agreements, as well as amounts we incurred to finance the formation of the CAB; and

|

| ● |

Pure Cycle agreed to fund expenses related to the construction of an agreed upon list of improvements to be constructed by the CAB with an estimated cost of $30 million

(including improvements already funded) on an as-needed basis for calendar years 2018–2023.

|

Advances and verified costs expended by us for expenses related to the construction of the agreed upon improvements are reimbursable to us by the CAB.

All amounts owed under the terminated agreements and each reimbursable expense incurred under the 2018 FFAA accrues interest at a rate of 6% per annum from the time funds are advanced by us to the CAB or costs are incurred by us for expenses

related to the construction of improvements, as applicable. No repayment is required of the CAB for advances made to the CAB or expenses incurred related to the construction of improvements unless and until the CAB and/or Sky Ranch Districts

issue bonds in an amount sufficient to reimburse us for all or a portion of advances or other expenses incurred. The CAB agrees to exercise reasonable efforts to issue bonds to reimburse us subject to certain limitations. In addition, the CAB

agrees to utilize any available moneys not otherwise pledged to payment of debt, used for operation and maintenance expenses, or otherwise encumbered, to reimburse us. Any advances or expenses not paid or reimbursed by the CAB by December 31,

2058, shall be deemed forever discharged and satisfied in full. We have funded reimbursable expenses for improvements, including improvements with respect to earthwork, erosion control, streets, drainage, and landscaping, at an estimated cost of

$2.3 million and expect to fund an additional estimated $25 million in reimbursable buildout costs.

The current directors of the CAB are Mark W. Harding (our President, Chief Financial Officer and a director), Scott E. Lehman (a Pure Cycle employee),

and Dirk Lashnits (a Pure Cycle employee), and one independent board member. Pursuant to Colorado law, directors may receive $100 for each board meeting they attend, up to a maximum of $1,600 per year. Mr. Harding, Mr. Lehman, and Mr. Lashnits

have all elected to forego these payments.

|

Oil and Gas Leases

|

||

|

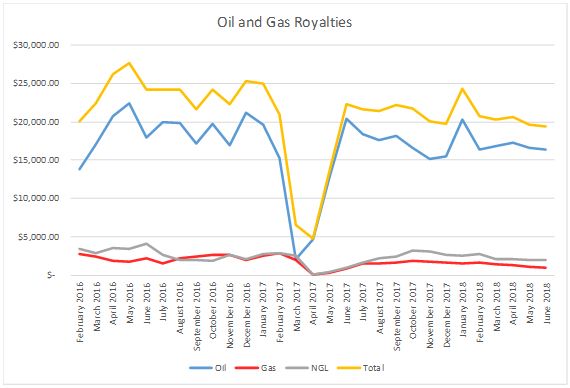

In 2011, we entered into a three-year Oil and Gas Lease (the “O&G Lease”) and Surface Use and Damage Agreement (the “Surface Use Agreement”)

and received an up-front payment of $1,243,400 ($1,900 per mineral acre) and a 20% of gross proceeds royalty (less certain taxes) from the sale of any oil and gas produced from the approximately 634 acres of mineral estate we own at Sky

Ranch. In 2014, the O&G Lease was extended for an additional two (2) years, and we received an additional up-front payment of $1,243,400 for the extension. The O&G Lease is now held by production, and we have been receiving

royalties from the oil and gas production from two wells drilled within our mineral interest. During the fiscal year ended August 31, 2018, we received

$191,300 in royalties attributable to these two wells.

|

|

|

In 2015, we received an up-front payment of $72,000, pursuant to a lease (which expired in fiscal 2017) for the purpose of exploring for,

developing, producing, and marketing oil and gas of 40 acres of mineral estate we own adjacent to the Lowry Range (the “Rangeview Lease”). In September 2017, we entered into a three-year Paid-Up Oil and Gas Lease with Bison Oil and Gas,

LLP (the “Bison Lease”) for this 40-acre mineral estate, and we received an up-front payment of $167,200.

|

Arkansas River Land and Minerals

We own three farms totaling 700 acres in the Arkansas River Valley. The farms were acquired in order to correct dry-up covenant issues related to

water-only farms, and we currently lease all three farms for dry land grazing. We intend to sell the farms in due course and have classified the farms as long-term investments. We also own approximately 13,900 acres of mineral interests in the

Arkansas River Valley, which have an estimated value of approximately $1.4 million. We currently have no plans to sell our mineral interests.

Well Enhancement and Recovery Systems

In 2007, we, along with two other parties, formed Well Enhancement and Recovery Systems LLC (“Well Enhancement LLC”), to develop a new deep water well

enhancement tool and process that we believe will increase the efficiency of wells completed into the Denver Basin groundwater formations. According to results from studies performed by an independent hydro-geologist, the well enhancement tool

effectively increased the production of the two test wells by 80% and 83% when compared to that of nearby wells developed in similar formations at similar depths. Based on the positive results of the test wells, we continue to refine the process

of enhancing deep water wells and are marketing the tool to area water providers. We currently hold a 50% interest in Well Enhancement LLC. We have not drilled any new wells in the past three years and have not used the tool during this period,

but we intend to continue to use the tool when we drill new water wells.

Significant Customers

Water and Wastewater

Our wholesale water and wastewater sales to the Rangeview District pursuant to the Rangeview Water Agreements accounted for 6%, 26% and 67% of our total

water revenues for the fiscal years ended August 31, 2018, 2017 and 2016, respectively. The Rangeview District has one significant customer, the Ridgeview Youth Services Center (“Ridgeview”). Pursuant to our Rangeview Water Agreements, we

are providing water and wastewater services to Ridgeview on behalf of the Rangeview District. Ridgeview accounted for 4%, 21% and 55% of our total water revenues for the fiscal years ended August 31, 2018, 2017 and 2016, respectively.

Our industrial water sales (i) directly and indirectly to ConocoPhillips accounted for approximately 68%, 30% and less than 1% and (ii) to other oil and

gas operators accounted for approximately 21%, 25%, and nil, of our total water revenues for the fiscal years ended August 31, 2018, 2017 and 2016, respectively.

Land Development

Revenues from two customers represented 98% of the Company’s land development revenues for the fiscal year ended August 31, 2018. Richmond America Homes

of Colorado, Inc. represented 66% and Taylor Morrison of Colorado, Inc. represented 32% of the Company’s land development revenues for the fiscal year ended August 31, 2018. No revenues were recognized from the Company’s land development

activities for the fiscal years ended August 31, 2017 and 2016.

Our Projected Operations

This section should be read in conjunction with Item 1A – Risk

Factors.

Along the Colorado Front Range, there are over 70 water providers with varying needs for replacement and new water supplies. We believe that we are well

positioned to assist certain of these providers in meeting their current and future water needs.

We design, construct and operate our water and wastewater facilities using advanced water treatment and wastewater treatment technologies, which allow us

to use our water supplies in an efficient and environmentally sustainable manner. We plan to develop our water and wastewater systems in stages to efficiently meet demands in our service areas, thereby reducing the amount of up-front capital

costs required for construction of facilities. We use third-party contractors to construct our facilities as needed. We employ licensed water and wastewater operators to operate our water and wastewater systems. As our systems expand, we expect

to hire additional personnel to operate our systems, which include water production, treatment, testing, storage, distribution, metering, billing, and operations management.

Our water and wastewater systems conjunctively use surface and groundwater supplies and storage of raw water and highly treated effluent supplies to

provide a balanced sustainable water supply for our wholesale customers and their end-use customers. Integrating conservation practices and incentives together with effective water reuse demonstrates our commitment to providing environmentally

responsible and sustainable water and wastewater services. Water supplies and water storage reservoirs are competitively sought throughout the west and along the Front Range of Colorado. We believe that regional cooperation among area water

providers in developing new water supplies, water storage, and transmission and distribution systems provides the most cost-effective way of expanding and enhancing service capacities for area water providers. We continue to discuss developing

water supplies and water storage opportunities with area water providers.

We expect the development of our Rangeview Water Supply to require a significant number of high capacity deep water wells. We anticipate drilling

separate wells into each of the three principal aquifers located beneath the Lowry Range. Each well is intended to deliver water to central water treatment facilities for treatment prior to delivery to customers. Development of our Lowry Range

surface water supplies will require facilities to divert surface water to storage reservoirs to be located on the Lowry Range and treatment facilities to treat the water prior to introduction into our distribution systems. Surface water diversion

facilities will be designed with capacities to divert the surface water when available (particularly during seasonal events such as spring run-off and summer storms) for storage in reservoirs to be constructed on the Lowry Range. Based on

preliminary engineering estimates, the full build-out of water facilities (including diversion structures, transmission pipelines, reservoirs, and water treatment facilities) on the Lowry Range will cost in excess of $750 million, based on

estimated costs, and will accommodate water service to customers located on and outside the Lowry Range. We expect this build out to occur in phases over an extended period of at least 50 years, and we expect that tap fees will be sufficient to

fund the infrastructure costs.

Our Denver-based supplies are a valuable, locally available resource located near the point of use. This enables us to incrementally develop

infrastructure to produce, treat and deliver water to customers based on their growing demands.

During fiscal 2018, we invested approximately $1.8 million to construct

pipelines that interconnect the Rangeview District, WISE, and Sky Ranch water systems. We expect to continue to invest in pipelines at the Sky Ranch property in anticipation of the first phase of development. We also expect to add additional

wells as demand for water grows.

The Rangeview District is a participant in the WISE project. This project is developing infrastructure to interconnect providers’ water systems and to

extend renewable water sources owned by Denver Water and Aurora Water to participating South Metro water providers, including the Rangeview District and, through our agreements with the Rangeview District, us. This system will diversify our

sources of water and will enable providers to move water among themselves, which will increase the reliability of our and others’ water systems. Through the WISE Financing Agreement, we funded the Rangeview District’s purchase of certain rights

to use existing water transmission and related infrastructure acquired and constructed by the WISE project. We have invested approximately $3.1 million into the WISE water supply to date. We anticipate that we will be spending approximately $3.0

million on this system during fiscal 2019 and $3.8 million during the next four years to fund the Rangeview District’s purchase of its share of the water

transmission line and additional facilities, water and related assets for WISE and to fund operations and water deliveries related to WISE. Timing of the investment will vary depending on the schedule of projects within WISE and the amount of

water purchased.

We are in the process of developing our Sky Ranch property, including building finished lots for home builders and building the water and wastewater

infrastructure for residential and commercial development of the property. In March 2018, we began construction of improvements for finished lots and will phase the construction of finished lots consistent with builder purchases of finished lots

as defined in our agreements. The timing for us to develop the remaining phases of the property will be largely dependent on the Denver real estate market and the interest we receive from home builders and developers. During fiscal 2018, we invested approximately $5.3 million in our Sky Ranch property, which consisted of planning, preliminary and final engineering designs, grading, erosion, sediment

control, drainage design, water and wastewater facility designs, and construction of approximately 10 miles of new transmission lines.

We plan to develop additional water assets within the Denver area and are exploring opportunities to utilize our water assets in areas adjacent to our

existing water supplies.

Water and Growth in Colorado

Colorado has experienced a robust housing market over the past 24 months. The key drivers to housing in the area are:

| ● |

Housing Starts – From September 2017 to September 2018, annual housing starts increased by 13.3%. From September 2016 to September 2017, annual housing starts increased by 6%.

|

| ● |

Unemployment – The unemployment rate in Colorado was 2.9% at

August 31, 2018, compared to a national unemployment rate of 3.9%.

|

| ● |

Population – The Denver Regional Council of Governments, a

voluntary association of over 50 county and municipal governments in the Denver metropolitan area, estimates that the Denver metropolitan area population will increase by about 38% from today’s 3.4 million people to 4.7 million people

by the year 2040. A Statewide Water Supply Initiative report by the Colorado Water Conservation Board estimates that the South Platte River basin, which includes the Denver metropolitan region, will grow from a current population of

3.9 million to 4.9 million by the year 2030, while the state’s population will increase from 5.7 million to 7.2 million.

|

| ● |

Demand – Approximately 70% of the state’s projected

population increase is anticipated to occur within the South Platte River basin. Significant increases in Colorado’s population, particularly in the Denver metro region and other areas in the water-short South Platte River basin,

together with increasing agricultural, recreational, and environmental water demands, will intensify competition for water supplies. The estimated population increases are expected to result in demands for water services in excess of

the current capabilities of municipal service providers, especially during drought conditions.

|

| ● |

Supply – The Statewide Water Supply Initiative estimates that

population growth in the Denver region and the South Platte River basin could result in additional water supply demands of over 400,000 acre feet by the year 2030.

|

| ● |

Development – Colorado law requires property developers to

demonstrate that they have sufficient water supplies for their proposed projects before rezoning applications will be considered. These factors indicate that water and availability of water will continue to be critical to growth