Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

As confidentially submitted to the U.S. Securities and Exchange Commission on February 11, 2019

This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Parsons Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 7373 | 95-3232481 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

5875 Trinity Parkway #300

Centreville, Virginia 20120

(703) 988-8500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Charles L. Harrington

Chairman, Chief Executive Officer and President

5875 Trinity Parkway #300

Centreville, Virginia 20120

(703) 988-8500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Steven B. Stokdyk, Esq. Cathy A. Birkeland, Esq. Latham &

Watkins LLP |

Peter W. Wardle, Esq. Stewart McDowell, Esq. Gibson, Dunn & Crutcher LLP 333 South Grand Avenue Los Angeles, California 90071 (213) 229-7000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate |

Amount of Registration Fee | ||

| Common Stock, par value $1.00 per share |

$ | $ | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase from the registrant. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated February 11, 2019.

Shares

Parsons Corporation

Common Stock

This is an initial public offering of shares of common stock of Parsons Corporation. All of the shares of common stock are being sold by the company.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . Parsons Corporation intends to apply to list the common stock on the under the symbol “PRSN”.

Following this offering, we will be a “controlled company” within the meaning of the corporate governance rules of the . See “Management—Controlled Company Exception.”

See “Risk Factors” on page 20 to read about factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial Public Offering Price |

$ | $ | ||||||

| Underwriting Discount(1) |

$ | $ | ||||||

| Proceeds Before Expenses(1) |

$ | $ | ||||||

| (1) | See “Underwriting”. |

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares from us at the initial price to the public less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2019.

| Goldman Sachs & Co. LLC | BofA Merrill Lynch |

Morgan Stanley

Prospectus dated , 2019

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

| 1 | ||||

| 20 | ||||

| 50 | ||||

| 52 | ||||

| 54 | ||||

| 55 | ||||

| 57 | ||||

| 60 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

64 | |||

| 89 | ||||

| 106 | ||||

| 116 | ||||

| 140 | ||||

| 141 | ||||

| 143 | ||||

| 146 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK |

148 | |||

| 153 | ||||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| F-1 |

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only under circumstances and in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospectus may have changed since that date.

For investors outside the U.S., we have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the U.S. Persons outside the U.S. who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the U.S. See “Underwriting.”

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

BASIS OF PRESENTATION

Prior to fiscal 2018, Parsons was on a 52- or 53-week fiscal year ending on the last Friday on or before the end of the calendar year. In 2018, our board of directors approved a change in our fiscal year end from the last Friday on or before the calendar year to December 31st. Accordingly, references to fiscal 2018, fiscal 2017, fiscal 2016, fiscal 2015 and fiscal 2014 represent the financial results of Parsons Corporation and its subsidiaries for the fiscal years ended December 31, 2018, December 29, 2017, December 30, 2016, December 25, 2015 and December 26, 2014, respectively. In a 52-week fiscal year, each quarter contains 13 weeks of operations; in a 53-week fiscal year, three of the quarters include 13 weeks of operations and one of the quarters includes 14 weeks of operations. Fiscal 2017, fiscal 2015 and fiscal 2014 were all 52-week years. Fiscal 2016 was a 53-week year, which may have caused our revenue, expenses and other results of operations to be higher due to an additional week of operations.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

Parsons, Polaris Alpha, iNET and Domain6 and our other registered or common law trademarks, service marks or trade names appearing in this prospectus are the property of Parsons Corporation. Other trademarks, service marks or trade names appearing in this prospectus are the property of their respective owners. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. We have omitted the ® and ™ designations, as applicable, for the trademarks used in this prospectus.

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size, is based on reports from various sources. In some cases, we do not expressly refer to the sources from which this data is derived. In that regard, when we refer to one or more sources of this type of data in any paragraph, you should assume that other data of this type appearing in the same paragraph is derived from the same sources, unless otherwise expressly stated or the context otherwise requires.

Because this information involves a number of assumptions and limitations, you are cautioned not to give undue weight to such information. We have not independently verified market data and industry forecasts provided by any of these or any other third-party sources referred to in this prospectus.

In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section captioned “Risk Factors” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the estimates made by third parties and by us.

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes included elsewhere in this prospectus. You should also consider the matters described under the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Unless the context otherwise requires, the terms “Parsons,” “the Company,” “we,” “us” and “our” refer to Parsons Corporation and its consolidated subsidiaries.

Overview

We are a leading provider of technology-driven solutions in the defense, intelligence and critical infrastructure markets. We provide technical design and engineering services and software to address our customers’ challenges. We have developed significant expertise and differentiated capabilities in key areas of cybersecurity, intelligence, defense, military training, connected communities, physical infrastructure and mobility solutions. By combining our talented team of professionals and advanced technology, we help solve complex technical challenges to enable a safer, smarter and more interconnected world.

Since our founding 75 years ago, we have built our reputation and business on our ability to successfully transform and innovate our services while leveraging cutting-edge technologies in order to expand our offerings. Whether our customers need a first-of-its-kind advanced missile development and testing facility, or an artificial intelligence enabled cloud platform to defend against cybersecurity threats, we deliver for our customers. We seek to grow by offering our clients innovative solutions supported by research and development, as well as acquisitions of emerging technologies. We have developed longstanding relationships with customers such as the U.S. military and intelligence agencies and state and local governments and agencies.

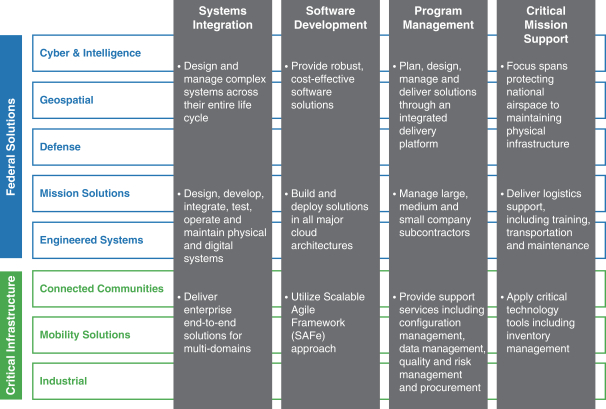

Advances in technology are dramatically shifting the operating landscape across our markets. Governments and companies are grappling with pressing challenges ranging from confronting increasingly sophisticated cybersecurity threats to upgrading aging systems and infrastructure. To address these challenges, our customers are actively seeking technology-enabled solutions to enhance and transform their operations and assets. Our wide-ranging capabilities enable us to provide our services and solutions across the defense, intelligence and critical infrastructure markets. As a leading technology-driven solutions provider with a proven track record, we believe we are well positioned to benefit from these trends and serve our customers’ evolving needs. We have capabilities in the following four areas that cut across our segments and business lines:

Systems Integration: We provide engineering services and technology for large digital and physical systems with high technical complexity. We lead projects from concept development through design, implementation, testing and verification, ensuring interoperability of these complex, disparate systems.

Software Development: We develop software and systems across many domains and mission-specific applications. Our experienced software engineers and developers design, develop, integrate, operate and sustain mission-critical software applications and systems across cyber, intelligence, defense and commercial customers.

1

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Program Management: We provide expertise and technology to advance our customers’ execution of large, complex projects within their defined time and cost parameters.

Critical Mission Support: We provide a diverse set of technical services to help our nation’s military on land, sea, air and space. These services include mission training, protecting national airspace, fighting infectious diseases, digitizing the health environment, performing contingency operations and providing operations and maintenance for physical infrastructure.

Our customer relationships, which are based on a long history of successfully delivering complex technical services, are key to our success. We are often involved in the early stages of our customers’ planning processes, which allows us to efficiently optimize our service delivery model. These relationships, along with our technical expertise and access to talented human capital, allow us to successfully deliver solutions that meet our customers’ demanding technical and execution requirements.

Technology and our people are our most important assets, allowing us to consistently deliver for our customers and help them solve their most pressing challenges. Investment in key technological capabilities is core to our business and helps us to stay at the forefront of the evolving trends across our end markets. To meet the challenges of tomorrow, we are focusing our technology investment on cybersecurity, machine learning, big data analytics and cloud applications. The work of our highly skilled and dedicated employees has enabled our long track record of continued innovation and execution on behalf of our customers. Our team of engineers, scientists, programmers and other specialists include PhDs and certified hackers and a large number of our skilled workforce hold government security clearances, which provides a significant competitive advantage for the highly technical and demanding work we perform.

We operate in two reporting segments, Federal Solutions and Critical Infrastructure, with revenue contribution of % and % and Adjusted EBITDA attributable to Parsons Corporation contribution of % and % for fiscal 2018. See "Summary Consolidated Financial Data" below for further discussion.

Federal Solutions: Our Federal Solutions segment is a high-end services and technology provider to the U.S. government, delivering timely, cost-effective solutions for mission-critical projects. We provide advanced technologies, including cybersecurity, missile defense systems, military training, subsurface munitions detection, military facility modernization, logistics support, chemical weapon remediation and engineering services. We serve a broad set of U.S. government agencies, including the Missile Defense Agency, the United States intelligence community, the U.S. military, the Department of Energy and the Federal Aviation Administration.

Critical Infrastructure: Our Critical Infrastructure segment provides integrated design and engineering services for complex physical and digital infrastructure around the globe. We are a technology innovator focused on next generation infrastructure. Our capabilities in design and project management allow us to deliver significant value to our customers by employing cutting-edge technologies, improving timelines and reducing costs. We serve a diverse global customer base including federal, state, municipal and industry customers such as Los Angeles World Airports, Canada’s Metrolinx, Dubai’s Roads and Transport Authority and the Port Authority of New York and New Jersey.

2

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

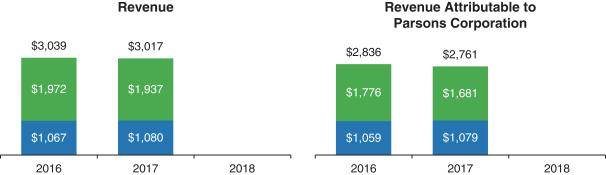

We have successfully grown our business in each segment and on a consolidated basis. In fiscal 2018, we generated revenues of $ billion, Revenue attributable to Parsons Corporation of $ billion, net income (loss) attributable to Parsons Corporation of $ million and Adjusted EBITDA attributable to Parsons Corporation of $ million. In fiscal 2018, our Federal Solutions segment had % year-over-year revenue growth, or % excluding the results of Polaris Alpha, LLC, or Polaris Alpha, which we acquired in May 2018, and our Critical Infrastructure segment had % year-over-year revenue growth. The following table shows our growth over the last three years (in millions):

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment Results” and “Note 19—Segments Information” in the notes to our consolidated financial statements included elsewhere in this prospectus for further discussion regarding our segment Revenue attributable to Parsons Corporation and segment Adjusted EBITDA attributable to Parsons Corporation.

In fiscal 2018, we achieved an overall win rate of % on new contracts and task orders for which we competed and a win rate of more than % on re-competed contracts and task orders (i.e., existing contracts or tasks orders which are up for bid) for existing or related business. As of December 31, 2018, our total backlog was $ million, an increase of % from December 29, 2017.

Our Services and Solutions

Within each of our segments, we focus our services and solutions on the needs of customers in each of our business lines. Our capabilities of systems integration, software development, program management and critical mission support apply across our segments and business lines.

3

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Federal Solutions

Our Federal Solutions business provides engineering, software and hardware solutions and services. It is focused on five business lines: Cyber & Intelligence, Geospatial, Defense, Mission Solutions, and Engineered Systems.

| • | Cyber & Intelligence—Focuses on two related, but discrete markets: cybersecurity and intelligence. Our customers include the U.S. Army and the United States intelligence community, which consists of 16 separate United States government intelligence agencies. We provide cybersecurity software and engineering services, rapid hardware prototyping and other technical services. An example is ThunderRidge, our tool that assists cyber operational users to develop action plans, assess cyber threats and disseminate situational awareness in real-time. |

| • | Geospatial—Focuses on providing geospatial intelligence, big data analytics and threat mitigation technology services to the defense, intelligence, space and command, control, communications, computer, cyber, intelligence, surveillance and reconnaissance, or C5ISR, end markets. An example is our work with the National Geospatial-Intelligence Agency, or NGA, in providing automated capabilities to analyze, collect and expose geospatial intelligence content from the open source environment. |

| • | Defense—Focuses on the missile defense, space and C5ISR end markets. Our customer portfolio includes the Missile Defense Agency, or MDA, the U.S. Air Force and the U.S. Army. We provide mission planning for space situational awareness, small satellite systems integration, electronic warfare, directed energy modeling and simulation and command and control systems and support. An example is our role as the prime systems engineering technical assistance, or SETA, contractor for the MDA where we provide weapons and missile defense systems engineering and command and control, battle management and communications (C2BMC) system support. |

| • | Mission Solutions—Supports military training and readiness and associated infrastructure. Our services and solutions include converged cyber-physical solutions for critical infrastructure, and global military mission readiness and training. Customers include the Federal Aviation Administration and the U.S. Army. Representative offerings include live, virtual, constructive and gaming training, converged cyber-physical security for industrial control systems and infrastructure upgrades, connected devices and smart meters. Differentiated technologies include our information assurance and compliance qualifications and our Domain6 cybersecurity toolset for industrial control systems protection. |

| • | Engineered Systems—Focuses on advanced technology services for advanced energy production systems, healthcare systems, environmental systems and associated infrastructure. Customers include the U.S. Department of Energy, the U.S. Army Corps of Engineers and the U.S. Air Force. Representative offerings include nuclear waste processing and treatment, weapons of mass destruction elimination, program and project management, infectious disease control analytics and data protection. Our expertise includes fluorinated organic chemicals, advanced digital classification and complex program and engineering management. |

4

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Critical Infrastructure

Our Critical Infrastructure business provides engineering, program management, systems engineering and software solutions. It is focused on three business lines: Connected Communities, Mobility Solutions and Industrial.

| • | Connected Communities—Provides intelligent transportation system management, advanced train controls integration, smart cities software and critical infrastructure cyber protection. Our customers include the transportation authorities for the cities of Los Angeles, New York and Paris, the states or provinces of Georgia, Ontario and Texas and rail and transit entities including AMTRAK, CSX and the Washington Metropolitan Area Transit Authority, or WMATA. Technology capabilities include positive and communications-based train controls systems integration, intelligent transportation network software, vehicle inspection data analytics software, tolling systems software and autonomous vehicle integration. An example is our role as provider of Advanced Traffic Management Systems, or ATMS, for transportation systems in seven U.S. states through our Intelligent NETworks, or iNET, platform. Our deployment for the Georgia Department of Transportation of this platform connects over 8,500 sensors and improves transportation efficiency by reducing commutes through solutions such as the new reversible toll lanes in Atlanta’s Northwest Corridor. |

| • | Mobility Solutions—Provides engineering services for complex infrastructure including bridges and tunnels, roads and highways, airports and rail and transit. Within our diverse customer base, our customer relationships include the Port Authority of New York and New Jersey and Dubai’s Roads and Transport Authority. Our capabilities include technologies in long-span bridges, tunnels, international airports and automated people mover and baggage handling systems. An example is our role as the sole program manager of the recently awarded Diamond Head Extension Program at Honolulu International Airport. |

| • | Industrial—Delivers engineering, program management and environmental solutions to private-sector industrial clients and public utilities. Customers are diverse with limited concentration, and include chemical, energy, utility, communications and manufacturing companies and some provincial agencies. Our capabilities include environmental remediation engineering, process engineering, cyber-physical security software and program management of capital projects. Differentiated technology solutions include our Domain6 cybersecurity toolset, advanced environmental analytics and modeling and the application of augmented and virtual reality. |

Our Market Opportunities

Technological progress is driving a swift pace of change, resulting in ongoing societal transformation, complicated geopolitical dynamics, a shifting threat landscape and the globalization of commerce. To address this evolving landscape, our customers are actively seeking technology-enabled solutions to upgrade and transform assets and operations. The below trends are key drivers of activity and growth in both our Federal Solutions and Critical Infrastructure segments.

Defense Spending Remains a Key Focus of the national agenda due to the reemergence of long-term strategic competition, which has been cited in the National Defense Strategy as the primary concern for U.S. national prosperity and security. This reemergence has resulted in increased global disorder and a security environment defined by rapid technological change, which may be more complex than ever before.

Cybersecurity is Mission Critical to U.S. National Security and cybersecurity threats are increasing in volume and sophistication as global connectivity and the rise of social media have led to

5

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

an explosion in the amount of available and exploitable data. The proliferation of mobile devices, smart devices and cloud computing has vastly increased the need for enterprise-wide risk-based cybersecurity programs and governments have become increasingly aware of the need for a proactive approach to the risk of cyber-attacks.

Consistent Need for Actionable Intelligence to Support U.S. Priorities is driving a shifting threat landscape that necessitates a greater need for collaboration and cooperation between intelligence agencies. There is a new demand for multi-domain command and control systems that are not designed for one particular warfighting domain, but are instead optimized to function cohesively across a spectrum of domains. This in turn drives a need for sophisticated data analytics to parse data into useful formats in real-time.

Global Infrastructure Needs Significant Replacements and Technology-Driven Upgrades. Aging physical infrastructure is strained by the swift pace of technological change. Critical infrastructure, specifically transportation infrastructure that is essential to national economic and security concerns including airports, bridges, and rail and transit systems, is particularly vulnerable. We believe aging infrastructure will continue to be replaced and supplanted by newer, smarter infrastructure with an increased focus on connectivity.

Urbanization Creates Demand for Smart Cities with Connected Populations. Cities around the globe increasingly demand new capabilities, such as sensor networks and communication strategies to connect streetlights, security cameras and emergency systems, to provide important real-time information and better serve their citizens. Better integrated corridor management solutions, intelligent transportation systems, advanced rail systems and updated telecommunication networks will keep cities around the world functioning as smart cities and serve as engines for economic growth.

Disruption of Legacy Service Delivery Models from Technology. Historical capital project management is changing with the introduction of cloud-connected computer-aided design, automation, big data, machine learning and other technologies. The introduction of these new technologies allows industry participants to reimagine existing value chains, address integrated lifecycle objectives, boost productivity and streamline project management. Industry participants that have the capability to embrace these new technologies to enhance their capability and service offering to higher value solutions will be well positioned to assist governments and communities in their transformation.

Amidst this disruption, we believe we are well-positioned to serve a large array of governments and companies. Across a diverse set of industries, we provide smart and agile solutions that address our customers’ concerns as they adapt to the rapid changes of a more interconnected and technology-driven world.

Our Competitive Strengths

Proven Track Record

Our 75 year proven track record is a result of our strong performance, the dedication of our employees and our longstanding customer relationships. We focus on being a company that delivers on its promises, holds integrity at the highest level and successfully assists our clients as they execute their most complex missions. Driven by our integrated people, process and technology approach, we have a reputation for innovation and are trusted with our customers’ most important endeavors.

Our differentiated business model has driven high win rates and strong financial performance, characterized by solid top and bottom line growth, high and growing backlog levels and low capital

6

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

requirements. In fiscal 2018, we won % of our re-competed assignments, achieved an average of % of award fees and achieved a win rate of % on assignments that we pursued. In fiscal 2018, our Federal Solutions revenues grew % and our Critical Infrastructure revenues grew % year-over-year. As of December 31, 2018, our backlog was $ , up % from year end fiscal 2017.

Long-Term Customer Relationships

We maintain long-term relationships with key government and commercial customers, many of which span over 40 years. For example, in the Federal Solutions segment, we have been providing support to the MDA for over 30 years. In the Critical Infrastructure segment, we have supported the WMATA for over 50 years. These longstanding relationships give us the insight and customer intimacy to align our research and development investments based on customer needs and enable high win rates for prime contract positions on the most technically demanding assignments.

Technology Innovation

We are on the forefront of developing sophisticated engineering and technical services products for our customers, such as our iNET and Domain6 technology offerings. Our technical and management teams have a deep understanding of the products, their ecosystems and deployments, the customer and the processes necessary to create tailored solutions.

Our competencies include delivering advanced technologies in cybersecurity, data and video analytics, cloud applications and migration and artificial intelligence. Our approach of agile development, rapid prototyping, quick reaction capability and low rate initial production delivers customers solutions from concept to full life cycle support. By leveraging people, processes and technologies, we focus on continually delivering innovative solutions to address our customers’ immediate and long-term challenges.

Scalable and Agile Business Offerings

Our scalable and agile offerings enable us to satisfy robust and evolving customer needs. The demanding environments where we operate are characterized by a need for high-confidence solutions, widespread application needs and mission critical outcomes. We pride ourselves on providing agile technologies through inventive and refined processes that provide quality outcomes to our customers.

Our technologies and platforms are designed to be applicable across end user markets and sub markets. This approach allows for scalable solutions that can be quickly and seamlessly integrated into multiple customer applications, regardless of geography or industry, allowing us to deploy a given service or platform across multiple markets.

World Class Talent

Our most important asset is our team of talented employees, 15,633 as of January 31, 2019, whose technical expertise is sought by our clients for their most sophisticated applications and challenges. Engineers, scientists, programmers and other employees choose us and stay with us for the opportunity to collaborate with our customers, deploy our expansive technical resources, rapidly bring bold ideas to market and work on leading solutions that enable a better world.

Our professionals are highly educated, with a wide range of technical acumen and in-depth domain knowledge and expertise. We have more than 10,300 degreed employees and over 3,100

7

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

highly credentialed employees as of January 31, 2019. Our management team has significant experience executing strategies for delivering profitable growth and is recognized for operational excellence and leadership integrity. Our executive management team has an average tenure of 17 years with the company and averages over 32 years of industry or functional experience.

Demonstrated Ability to Identify and Execute Acquisitions to Transform our Business

Strategic acquisitions that augment our technology offerings and capabilities are a key tenet of our growth strategy. We have completed five strategic acquisitions (four in Federal Solutions and one in Critical Infrastructure) since 2011, which collectively provided us with a wide variety of complementary technology capabilities, with an aggregate purchase price of $1.4 billion. This highlights our ability to successfully identify and execute on attractive opportunities to augment our leading technical offerings. These acquisitions include:

| • | OGSystems: Acquired in 2019, OGSystems, LLC, or OGSystems, is a disruptive geo-intelligence solutions and immersive engineering provider that creates technology solutions for the United States intelligence community and the Department of Defense. |

| • | Polaris Alpha: Acquired in 2018, Polaris Alpha Holdings, LLC, or Polaris Alpha, is an advanced, technology-focused provider of innovative mission solutions for national security, intelligence, defense and other U.S. federal customers. |

| • | Delcan Technologies: Acquired in 2014, Delcan Technologies is a multidisciplinary provider of engineering, planning, management and technology services offering a broad range of integrated systems and infrastructure solutions focused on mobility and urban autonomy. |

We maintain a robust acquisition pipeline and are continually evaluating potential opportunities for disciplined growth by acquisition to further transform our business.

Our Strategy for Growth

Our growth strategy is focused on three pillars: Enhance, Extend and Transform. These include continually enhancing and optimizing our core business processes, extending our core business into high-growth and opportunity-rich adjacent markets and acquiring and integrating companies that possess transformative and disruptive technologies.

Enhance and Optimize our Core Operations

We are committed to enhancing and optimizing our core business and improving financial performance, including revenue growth, margin expansion and positive cash flow, using the following strategies:

| • | Focusing on cross-selling a wide range of applicable services and solutions to our customers, including those added to our portfolio through acquisition. |

| • | Continuing research and development investments in cybersecurity software, iNET, our intelligent transportation system connected city platform, modeling and simulation, data analytics and our software and security-as-a-service platforms. |

| • | Continuously evaluating and shaping our portfolio to divest, exit and de-emphasize lower-performing businesses and markets. |

| • | Rigorously managing our working capital to maximize cash flow. |

8

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Extend into Opportunity-Rich Adjacent Markets

We are extending our core markets through organically penetrating and expanding in market adjacencies requiring our core services and solutions, with key market focuses that include:

| • | Space—Extend our space situational awareness, small satellite integration, command and control and critical infrastructure solutions to our current and new space customers in the government and commercial space markets. |

| • | Energy—Extend our cyber-physical security, energy efficiency, owner’s engineer, and critical infrastructure solutions to regulated utilities, oil and gas energy companies and federal energy customers. |

| • | Health—Extend our data analytics, artificial intelligence and cloud computing solutions to the federal disease research and greater federal healthcare ecosystem. |

| • | Smart Cities—Extend our iNET platform to include enhanced cybersecurity, data analytics, machine learning and cloud computing to expand coverage to additional global cities and regions. |

| • | Critical Infrastructure Protection—Leverage our installed customer base and pursue market segments that are driven by high threat levels and regulatory concerns. |

Continued Acquisition and Integration of Transformative, Disruptive Technologies

We are transforming our business capabilities and business models through the acquisition of companies with additional software and hardware intellectual property in:

| • | Cybersecurity software leveraging artificial intelligence algorithms across large data sets to further expand our coverage with large infrastructure and mobility systems. |

| • | Intelligence software focused on data capture, processing and configuration to produce actionable intelligence from large data sets. |

| • | Internet of Things, or IoT, sensor systems integration, data capture and processing focused on mobility solutions for connected and smart cities. |

| • | Space and geospatial software to expand our small satellite command and control coverage, large data capture and analysis with embedded artificial intelligence to improve space operations. |

Our objective is to continue to transform our business into a highly-scalable defense and infrastructure platform and increase revenue growth rates, margins and cash flows. We seek to expand opportunities for long-term revenue growth, both by developing and acquiring capabilities that will allow us to reach new customers and by expanding our offerings for existing customers. We build on the foundation of our Enhance and Extend strategies and reinforce these strategies with acquisitions of companies with software, hardware and expertise in our target markets, services and solutions.

Summary Risk Factors

Our business is subject to numerous risks and uncertainties, including those in the section entitled “Risk Factors” and elsewhere in this prospectus. These risks include, but are not limited to, the following:

| • | Government spending and priorities could change in a manner that adversely affects our future revenue and limits our growth prospects. |

9

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

| • | The U.S. federal government and its agencies collectively are our largest single customer. |

| • | Our failure to comply with a variety of complex procurement rules and regulations could result in our being liable for penalties, including termination of our government contracts, disqualification from bidding on future government contracts and suspension or debarment from government contracting. |

| • | Government entities may adopt new contract rules and regulations or revise their procurement practices in a manner adverse to us at any time. |

| • | A substantial portion of our business is subject to reviews, audits and cost adjustments by government agencies, which, if resolved unfavorably to us, could adversely affect our profitability, cash flows or growth prospects. |

| • | Our government contracts may be terminated by the government counterparty at any time and may contain other provisions permitting the government to discontinue contract performance. |

| • | We face aggressive industry competition that can impact our ability to obtain contracts and may affect our future revenues, profitability and growth prospects. |

| • | Our ability to attract, train, retain and utilize skilled employees and senior management. |

| • | Changes in the mix of our contracts and in our estimates and management of costs, time and resources for our contracts. |

| • | Required compliance with numerous legal and regulatory requirements. |

| • | Our operations through joint venture entities, some of which we do not have management control over, and with which we typically have joint and several liability with our joint venture partners. |

Recent Developments

On January 7, 2019, we acquired OGSystems for $304.8 million. OGSystems provides geospatial intelligence, big data analytics and threat mitigation for defense and intelligence customers. The acquisition was funded by $44.8 million of cash on hand, $150.0 million of borrowings under our $150.0 million unsecured term facility, or Term Loan, pursuant to a term loan agreement between us and certain lenders dated January 4, 2019, as amended, or Term Loan Agreement, and $110.0 million of borrowings under our $550.0 million unsecured credit facility, or Revolving Credit Facility, pursuant to a credit agreement between us and certain lenders dated November 15, 2017, as amended, or Credit Agreement. In 2018, OGSystems had revenues of $ million and net income of $ million. The financial results of OGSystems are not included in our consolidated results of operations for the periods presented in this prospectus.

Corporate Information

We are a Delaware corporation and commenced our principal operations in 1944. Our principal executive offices are located at 5875 Trinity Parkway #300, Centreville, Virginia 20120, and our telephone number is (703) 988-8500. Our website address is www.parsons.com. The information on or that can be accessed through our website is not incorporated by reference into this prospectus, and you should not consider any such information as part of this prospectus or in deciding whether to purchase our common stock.

10

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Parsons Employee Stock Ownership Plan

In 1984, we became 100% owned by the Parsons Employee Stock Ownership Plan, which we refer to as the ESOP. The ESOP is Parsons’ sole shareholder prior to the consummation of this offering. The ESOP is a tax qualified retirement plan and trust subject to the requirements of the Internal Revenue Code, as amended, or the Code, and the Employee Retirement Income Security Act of 1974, as amended, or ERISA. The trustee of the ESOP is Newport Trust Company, which we refer to as the ESOP Trustee. Following consummation of this offering, each ESOP participant (or his or her beneficiaries) will have the right to direct the ESOP Trustee on how to vote the shares of common stock allocated to his or her account under the ESOP. The ESOP Trustee will vote any shares of common stock held in the ESOP, but not allocated to any ESOP participant’s account and any allocated shares for which no voting directions are timely received by the ESOP Trustee, in its independent fiduciary discretion.

S Corporation Status

Since 1999, we have elected to be taxed for U.S. federal income tax purposes as an “S” Corporation under the provisions of Sections 1361 through 1379 of the Code. As a result, our earnings have not been subject to, and we have not paid, U.S. federal income tax, and no provision or liability for U.S. federal income tax has been included in our consolidated financial statements. Instead, for U.S. federal income tax purposes our taxable income is “passed through” to our sole shareholder, the ESOP. As the ESOP is a tax qualified plan exempt from federal income taxes, we have not previously had to make any distributions to the ESOP for taxes. Unless specifically noted otherwise, no amount of our consolidated net income or our earnings per share presented in this prospectus, including in our consolidated financial statements and the accompanying notes appearing in this prospectus, reflects any provision for or accrual of any expense for U.S. federal income tax liability for any period presented. In connection with this offering, our status as an “S” Corporation will terminate. Thereafter, our taxable earnings will be subject to U.S. federal income tax and we will bear the liability for those taxes.

11

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

THE OFFERING

| Common stock offered by Parsons |

shares | |

| Common stock outstanding after this offering |

shares | |

| Underwriters’ option to purchase additional shares of common stock from Parsons |

shares | |

| Use of proceeds |

We estimate that the net proceeds to us from the sale of shares of our common stock in this offering will be approximately $ million based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. | |

| We intend to use the net proceeds to us from this offering to repay the outstanding principal balance of approximately $150.0 million under our Term Loan (plus any accrued interest), the outstanding principal balance of approximately $ million under our Revolving Credit Facility (plus any accrued interest), to fund future acquisitions and for working capital and other general corporate purposes. See the section captioned “Use of Proceeds” for a more complete description of the intended use of proceeds from this offering. | ||

| Dividend Policy |

We currently do not intend to declare or pay any cash dividends in the foreseeable future. Any further determination to pay dividends on our capital stock will be at the discretion of our board of directors, subject to applicable laws, and will depend on our financial condition, results of operations, capital requirements, restrictions under our senior notes issued in a private placement in 2014, or the Senior Notes, Credit Agreement and Term Loan Agreement, and other factors that our board of directors considers relevant. See “Dividend Policy” for further information. | |

| Voting Rights |

Shares of common stock are entitled to one vote per share. See the section captioned “Description of Capital Stock”. Assuming no exercise of the underwriters’ option to purchase additional shares, following this offering, outstanding shares of common stock beneficially held by our executive officers and the ESOP, the | |

12

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

| only holder of more than 5% of our capital stock, will represent approximately % of the voting power of our outstanding capital stock. The ESOP participants (or their beneficiaries) have the right to direct the ESOP Trustee on how to vote the shares of common stock allocated to his or her account under the ESOP. The ESOP Trustee will vote in its independent fiduciary discretion any shares of common stock held in the ESOP, but not allocated to any ESOP participant’s account, and any allocated shares for which no voting directions are timely received from participants. | ||

| Risk Factors |

You should carefully read and consider the information set forth in the section entitled “Risk Factors” beginning on page 18, together with all of the other information set forth in this prospectus, before deciding whether to invest in our common stock. | |

| Conflicts of Interest |

An affiliate of Merrill Lynch, Pierce, Fenner & Smith Incorporated is a lender under the Term Loan and Revolving Credit Facility. As described in the section entitled “Use of Proceeds,” a portion of the net proceeds from this offering will be used to repay borrowings under the Term Loan and Revolving Credit Facility. Because we expect that more than 5% of the proceeds of this offering will be received by an affiliate of Merrill Lynch, Pierce, Fenner & Smith Incorporated, a lender under the Term Loan and Revolving Credit Facility, this offering is being conducted in compliance with Rule 5121, as administered by the Financial Industry Regulatory Authority, or FINRA. has agreed to act as the qualified independent underwriter with respect to this offering and has performed due diligence investigations and participated in the preparation of this registration statement. See the section entitled “Underwriting—Conflicts of Interest.” | |

| Proposed trading symbol |

“PRSN”. | |

The total number of shares of our common stock that will be outstanding after this offering will be shares, and excludes, as of December 31, 2018:

| • | shares of common stock reserved for future grant or issuance under our 2019 Incentive Award Plan, or the 2019 Plan, which will become effective upon the completion of this offering; and |

| • | shares of our common stock that may be issued upon settlement of awards granted in 2019 under our Long Term Growth Plan, Shareholder Value Plan or Restricted Award Plan. |

13

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Except as otherwise indicated, all information in this prospectus assumes:

| • | the filing and effectiveness of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws immediately prior to the closing of this offering; and |

| • | no exercise by the underwriters of their right to purchase up to an additional shares of common stock from us to cover overallotments, if any. |

14

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present summary consolidated financial and other data and pro forma information to reflect our conversion from an “S” Corporation to a “C” Corporation for income tax purposes. The consolidated statements of operations data for the fiscal years ended December 30, 2016, December 29, 2017 and December 31, 2018 and the consolidated balance sheet data as of December 29, 2017 and December 31, 2018 are derived from our consolidated financial statements included elsewhere in this prospectus.

You should read this data together with our audited consolidated financial statements and related notes, as well as the information under the captions “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included elsewhere in this prospectus. Our historical results are not necessarily indicative of our future results.

| Fiscal Year Ended | ||||||||||||

| (U.S. dollars in thousands, except per share data) | December 30, 2016 |

December 29, 2017 |

December 31, 2018 |

|||||||||

| Consolidated Statements of Operations Data: |

||||||||||||

| Revenue |

$ | 3,039,191 | $ | 3,017,011 | $ | |||||||

| Direct costs of contracts |

2,431,193 | 2,400,140 | ||||||||||

| Equity in earnings of unconsolidated joint ventures |

35,462 | 40,086 | ||||||||||

| Indirect, general and administrative expenses |

522,920 | 506,255 | ||||||||||

| Impairment of goodwill, intangible and other assets |

85,133 | — | ||||||||||

|

|

|

|

|

|

|

|||||||

| Operating income |

35,407 | 150,702 | ||||||||||

|

|

|

|

|

|

|

|||||||

| Interest income |

1,190 | 2,465 | ||||||||||

| Interest expense |

(16,509 | ) | (15,798 | ) | ||||||||

| Other income, net |

1,340 | 5,658 | ||||||||||

| Interest and other expense associated with claim on long-term contract |

(9,422 | ) | (10,026 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Total other expense |

(23,401 | ) | (17,701 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Income before tax expense |

12,006 | 133,001 | ||||||||||

| Income tax expense |

(13,992 | ) | (21,464 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Net (loss) income including noncontrolling interests |

(1,986 | ) | 111,537 | |||||||||

| Net income attributable to noncontrolling interests |

(11,161 | ) | (14,211 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Net (loss) income attributable to Parsons Corporation |

$ | (13,147 | ) | $ | 97,326 | $ | ||||||

|

|

|

|

|

|

|

|||||||

| Net (loss) income attributable to Parsons Corporation per share(1): |

||||||||||||

| Basic and diluted |

$ | (0.45 | ) | $ | 3.49 | $ | ||||||

| Weighted-average number of shares: |

||||||||||||

| Basic and diluted |

29,499 | 27,858 | ||||||||||

| Pro Forma Income (Loss) Information (unaudited)(2): |

||||||||||||

| Historical income (loss) before provision for income taxes |

$ | |||||||||||

| Pro forma provision for income taxes |

||||||||||||

| Pro forma net income (loss) |

$ | |||||||||||

| Pro forma net income (loss) attributable to Parsons Corporation |

||||||||||||

| Pro forma basic and diluted net income (loss) attributable to Parsons Corporation per common share |

$ | |||||||||||

| Weighted-average number of shares used in computing pro forma net income (loss) attributable to Parsons Corporation per share |

||||||||||||

| Basic and diluted |

||||||||||||

| (1) | See “Note 18—Earnings Per Share” to our audited consolidated financial statements in this prospectus for more information regarding net income (loss) per share, basic and diluted. |

15

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

| (2) | The unaudited pro forma income (loss) information for 2018 gives effect to an adjusted income tax expense as if we had been a “C” Corporation at an assumed combined federal, state and local statutory income tax rate of % for the fiscal year ended December 31, 2018. |

| As of December 29, 2017 | As of December 31, 2018 | |||||||||||

| (U.S. dollars in thousands) | Actual | Actual | Pro Forma(1) | |||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents(2) |

$ | 376,368 | $ | $ | ||||||||

| Total assets |

2,272,718 | |||||||||||

| Total debt |

249,407 | |||||||||||

| Noncontrolling interests |

27,494 | |||||||||||

| Redeemable common stock held by the ESOP |

1,855,305 | |||||||||||

| Total shareholders’ deficit |

(1,049,916 | ) | ||||||||||

| (1) | This column gives effect to (i) the elimination of our obligation to redeem eligible ESOP shares for cash and the related reclassification of redeemable common stock held by the ESOP to common stock and additional paid-in capital, as well as (ii) the termination of our “S” Corporation status in connection with our initial public offering and our election to be treated as a “C” Corporation under the Code, including an in net deferred tax assets of $ million and the reclassification of undistributed accumulated deficit to additional paid-in capital, assuming our “S” Corporation status terminated on December 31, 2018. This column does not give effect to the payment of $44.8 million of cash on hand and $260.0 million of aggregate borrowings under our Term Loan and Revolving Credit Facility in connection with consummation of our acquisition of OGSystems in January 2019. |

| (2) | Does not include $68.8 million of consolidated joint ventures and $1.0 million of restricted cash and investments as of December 29, 2017. |

| Fiscal Year Ended | ||||||||||||

| (U.S. dollars in thousands) | December 30, 2016 |

December 29, 2017 |

December 31, 2018 |

|||||||||

| Other Information: |

||||||||||||

| Revenue attributable to Parsons Corporation(1) |

$ | 2,835,529 | $ | 2,760,819 | $ | |||||||

| Adjusted EBITDA attributable to Parsons Corporation(2) |

$ | 160,582 | $ | 175,740 | $ | |||||||

| Adjusted EBITDA Margin(3) |

5.7% | 6.4% | % | |||||||||

| (1) | A reconciliation of revenue to Revenue attributable to Parsons Corporation is set forth below: |

| Fiscal Year Ended | ||||||||||||

| (U.S. dollars in thousands) | December 30, 2016 |

December 29, 2017 |

December 31, 2018 |

|||||||||

| Revenue |

$ | 3,039,191 | $ | 3,017,011 | $ | |||||||

| Revenue attributable to noncontrolling interests |

(203,662) | (256,192) | ||||||||||

|

|

|

|

|

|

|

|||||||

| Revenue attributable to Parsons Corporation |

$ | 2,835,529 | $ | 2,760,819 | $ | |||||||

|

|

|

|

|

|

|

|||||||

Revenue attributable to Parsons Corporation is a supplemental measure of our operating performance that is not recognized under generally accepted accounting principles in the United States, or GAAP. Revenue attributable to Parsons Corporation is included in this prospectus because it is used by management and our board of directors to assess the operating performance of our business both on a segment and on a consolidated basis. We view Revenue attributable to Parsons Corporation as a useful measure of our operating business because it excludes the impact of revenue that is not attributable to Parsons Corporation. Revenue attributable to Parsons Corporation is calculated by excluding revenue attributable to noncontrolling interests from revenue. Revenue

16

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

attributable to noncontrolling interests is the portion of revenue from joint ventures that is consolidated into our financial statements and is not attributable to Parsons Corporation. Revenue attributable to Parsons Corporation is not required by, or presented in accordance with, GAAP. Our calculations of Revenue attributable to Parsons Corporation may not be comparable to similarly titled captions reported by other companies. Revenue attributable to Parsons Corporation should not be considered as a substitute for analysis of our revenue as reported under GAAP.

| (2) | A reconciliation of net income (loss) attributable to Parsons Corporation to Adjusted EBITDA attributable to Parsons Corporation is set forth below: |

| Fiscal Year Ended | ||||||||||||

| (U.S. dollars in thousands) | December 30, 2016 |

December 29, 2017 |

December 31, 2018 |

|||||||||

| Net (loss) income attributable to Parsons Corporation |

$ | (13,147) | $ | 97,326 | $ | |||||||

| Net income attributable to noncontrolling interests |

11,161 | 14,211 | ||||||||||

|

|

|

|

|

|

|

|||||||

| Net (loss) income including noncontrolling interests |

(1,986) | 111,537 | ||||||||||

| Interest expense, net |

15,319 | 13,333 | ||||||||||

| Income tax expense |

13,992 | 21,464 | ||||||||||

| Depreciation and amortization |

42,262 | 35,303 | ||||||||||

| Impairment of goodwill, intangible and other assets |

85,133 | — | ||||||||||

| Litigation related expenses (income)(a) |

9,422 | 10,026 | ||||||||||

| Amortization of deferred gain resulting from sale-leaseback transactions(b) |

(7,283) | (7,283) | ||||||||||

| Acquisition related costs(c) |

2,552 | 1,190 | ||||||||||

| Restructuring(d) |

12,407 | — | ||||||||||

| Other(e) |

1,334 | 5,061 | ||||||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA |

173,152 | 190,631 | ||||||||||

| Adjusted EBITDA attributable to noncontrolling interests |

(12,570) | (14,891) | ||||||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA attributable to Parsons Corporation |

$ | 160,582 | $ | 175,740 | $ | |||||||

|

|

|

|

|

|

|

|||||||

| (a) | Fiscal 2016 and fiscal 2017 reflect the post-judgment interest expense recorded in “Interest and other expenses associated with claim on long-term contract” in our results of operations related to the judgment entered against us in 2014 in connection with a lawsuit by the Los Angeles Metropolitan Transportation Authority. For fiscal 2018, due to the judgment being vacated, the Company reversed the accrued liability with an offset to , in the amount of $ million. |

| (b) | Reflects amortization of the deferred gain on prior sale-leaseback transactions in fiscal 2011. See “Note 8—Sale-Leasebacks” in the notes to our consolidated financial statements included elsewhere in this prospectus. |

| (c) | Reflects costs incurred in connection with acquisitions, including primarily fees paid for professional services and employee retention. |

| (d) | Reflects costs associated with and related to our corporate restructuring initiatives, including expenses incurred in connection with a restructuring program we began implementing in 2015. See “Note 2—Summary of Significant Accounting Policies—Restructuring” in the notes to our consolidated financial statements included elsewhere in this prospectus. |

17

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

| (e) | Fiscal 2016 includes a $3.5 million loss from the sale of a subsidiary, a $0.9 million gain on the sale of fixed assets, a $0.8 million gain related to disposed businesses and a $0.5 million gain related to settlement proceeds received for an already completed contract. Fiscal 2017 includes non-operating lease termination costs of $1.8 million, a $1.8 million loss related to disposed businesses, a $1.0 million loss from the sale of fixed assets and a $0.5 million loss related to several individually insignificant items that are non-recurring, infrequent or unusual in nature. |

Adjusted EBITDA attributable to Parsons Corporation is a supplemental measure of our operating performance included in this prospectus because it is used by management and our board of directors to assess our financial performance both on a segment and on a consolidated basis. We discuss Adjusted EBITDA attributable to Parsons Corporation because our management uses this measure for business planning purposes, including to manage the business against internal projected results of operations and measure the performance of the business generally. Adjusted EBITDA is frequently used by analysts, investors and other interested parties to evaluate companies in our industry.

Adjusted EBITDA attributable to Parsons Corporation is not a GAAP measure of our financial performance or liquidity and should not be considered as an alternative to net income (loss) as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP. We define Adjusted EBITDA attributable to Parsons Corporation as net income (loss) attributable to Parsons Corporation, adjusted to exclude interest expense (net of interest income), provision for income taxes, depreciation and amortization and certain other items that we do not consider in our evaluation of ongoing operating performance. These other items include, among other things, impairment of goodwill, intangible and other assets, interest and other expenses recognized on litigation matters, amortization of deferred gain resulting from sale-leaseback transactions, expenses incurred in connection with acquisitions and expenses related to our corporate restructuring initiatives. Adjusted EBITDA attributable to Parsons Corporation should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Additionally, Adjusted EBITDA attributable to Parsons Corporation is not intended to be a measure of free cash flow for management’s discretionary use, as it does not reflect tax payments, debt service requirements, capital expenditures and certain other cash costs that may recur in the future, including, among other things, cash requirements for working capital needs and cash costs to replace assets being depreciated and amortized. Management compensates for these limitations by relying on our GAAP results in addition to using Adjusted EBITDA attributable to Parsons Corporation supplementally. Our measure of Adjusted EBITDA attributable to Parsons Corporation is not necessarily comparable to similarly titled captions of other companies due to different methods of calculation.

The following table shows the composition of consolidated Adjusted EBITDA attributable to Parsons Corporation by the Adjusted EBITDA attributable to Parsons Corporation of each of our reportable segments:

| Fiscal Year Ended | ||||||||||||

| (U.S. dollars in thousands) | December 30, 2016 |

December 29, 2017 |

December 31, 2018 |

|||||||||

| Federal Solutions Adjusted EBITDA attributable to Parsons Corporation |

$ | 79,376 | $ | 89,269 | $ | |||||||

| Critical Infrastructure Adjusted EBITDA attributable to Parsons Corporation |

81,206 | 86,471 | ||||||||||

|

|

|

|

|

|

|

|||||||

| Consolidated Adjusted EBITDA attributable to Parsons Corporation |

$ | 160,582 | $ | 175,740 | $

|

|

| |||||

|

|

|

|

|

|

|

|||||||

18

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment Results," and "Note 19—Segments Information” in the notes to our consolidated financial statements included elsewhere in this prospectus for further discussion regarding our segment Adjusted EBITDA attributable to Parsons Corporation.

| (3) | Adjusted EBITDA Margin is calculated as Adjusted EBITDA attributable to Parsons Corporation divided by Revenue attributable to Parsons Corporation in the applicable period. |

19

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

You should carefully consider the risks described below and the other information contained in this prospectus, including our consolidated financial statements and the related notes, before making an investment decision. Our business, financial condition and results of operations could be materially and adversely affected by any of these risks or uncertainties. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Business

Government spending and priorities could change in a manner that adversely affects our future revenue and limits our growth prospects.

We derive, and expect to continue to derive, a significant portion of our revenue from contracts with government entities. As a result, our business depends upon continued government expenditures on defense, intelligence, civil and engineering programs for which we provide support, both among foreign governments and at federal, state and local levels domestically. These expenditures have not remained constant over time and have been reduced in some periods. In particular, these expenditures have recently been affected by efforts to improve efficiency and reduce costs affecting government programs generally. Our business, prospects, financial condition or operating results could be materially harmed, among other causes, by the following:

| • | budgetary constraints, including mandated automatic spending cuts, affecting across-the-board government spending, or specific agencies in particular, and changes in available funding; |

| • | a shift in expenditures away from agencies or programs that we support; |

| • | reduced government outsourcing of functions that we are currently contracted to provide, including as a result of increased insourcing by various U.S. government agencies due to changes in the definition of “inherently governmental” work, including proposals to limit contractor access to sensitive or classified information and work assignments; |

| • | further efforts to improve efficiency and reduce costs affecting government programs; |

| • | changes or delays in government programs that we support or the programs’ requirements; |

| • | a continuation of recent efforts by the U.S. government in particular to decrease spending for management support service contracts; |

| • | U.S. government shutdowns due to, among other reasons, a failure by elected officials to fund the government, such as the shutdowns which occurred during government fiscal years 2019 and 2014 and, to a lesser extent, government fiscal year 2018, and other potential delays in the appropriations process; |

| • | U.S. government agencies awarding contracts on a technically acceptable/lowest cost basis in order to reduce expenditures; |

| • | delays in the payment of our invoices by government payment offices; |

| • | an inability by the U.S. government to fund its operations as a result of a failure to increase the federal government’s debt ceiling, a credit downgrade of U.S. government obligations or for any other reason; and |

| • | changes in the political climate and general economic conditions, including a slowdown of the economy or unstable economic conditions and responses to conditions, such as emergency spending, that reduce funds available for other government priorities. |

20

Table of Contents

Confidential Treatment Requested by Parsons Corporation

Pursuant to 17 C.F.R. Section 200.83

Any disruption in the functioning of government agencies, including as a result of government closures and shutdowns, terrorism, war, natural disasters, destruction of government facilities, and other potential calamities could have a negative impact on our operations and cause us to lose revenue or incur additional costs due to, among other things, our inability to deploy our staff to client locations or facilities as a result of such disruptions.

In particular, with regard to our largest single customer, the U.S. federal government, budget deficits, the national debt and the prevailing economic condition, and actions taken to address them, could continue to negatively affect the U.S. government expenditures on defense, intelligence and civil programs for which we provide support. The Department of Defense is one of our significant clients and cost cutting, including through consolidation and elimination of duplicative organizations and insourcing, has become a major initiative for the Department of Defense. In particular, the Budget Control Act of 2011 provides for automatic spending cuts (referred to as sequestration) totaling approximately $1.2 trillion between 2013 and 2021, including an estimated $500.0 billion in federal defense spending cuts over this time period. Most recently, the Bipartisan Budget Act of 2018 amended the discretionary spending limits established by the Budget Control Act of 2011 for the government fiscal 2018 and 2019 budgets across the federal government and increased the prior discretionary spending cap in both defense and non-defense. Pursuant to the Consolidated Appropriations Act, 2018, the new Department of Defense spending limit is approximately $660.0 billion for government fiscal 2018, including an allocation of $65.0 billion in overseas contingency operations funding. While recent budget actions reflect a more measured and strategic approach to addressing the U.S. government’s fiscal challenges, there remains uncertainty as to how exactly budget cuts, including sequestration, will impact us, and we are therefore unable to predict the extent of the impact of such cuts on our business and results of operations. However, a reduction in the amount of or delays or cancellations of funding for, services that we are contracted to provide to the Department of Defense as a result of any of these initiatives, legislation or otherwise could have a material adverse effect on our business, financial condition and results of operations. In addition, in response to an Office of Management and Budget mandate, government agencies have reduced management support services spending in recent years. If federal awards for management support services continue to decline, our revenue and operating profits may materially decline and further efforts by the Office of Management and Budget to decrease federal awards for management support services could have a material and adverse effect on our business, financial condition and results of operations.