UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| [X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the quarterly period ended January 31, 2019 | ||

| OR | ||

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission file number: 1-08266

U.S. GOLD CORP.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 22-1831409 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 1910 E. Idaho Street, Suite 102-Box 604, Elko, NV | 89801 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(800) 557-4550

(Registrant’s Telephone Number, including Area Code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act (Check One)”

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [X] Smaller reporting company [X] Emerging growth Company [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ] Yes [X] No

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. Common Stock ($0.001 par value): As of March 18, 2019, there were 19,310,009 shares outstanding.

U.S. GOLD CORP.

FORM 10-Q

TABLE OF CONTENTS

| 2 |

U.S. GOLD CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| January 31, 2019 | April 30, 2018 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash | $ | 3,193,548 | $ | 7,646,279 | ||||

| Prepaid expenses and other current assets | 212,880 | 632,038 | ||||||

| Total Current Assets | 3,406,428 | 8,278,317 | ||||||

| NON - CURRENT ASSETS: | ||||||||

| Property, net | 77,283 | - | ||||||

| Reclamation bond deposit | 346,947 | 92,928 | ||||||

| Mineral rights | 4,176,952 | 4,176,952 | ||||||

| Deferred income taxes | - | 438,145 | ||||||

| Total Non - Current Assets | 4,601,182 | 4,708,025 | ||||||

| Total Assets | $ | 8,007,610 | $ | 12,986,342 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Accounts payable | $ | 164,620 | $ | 262,652 | ||||

| Accounts payable - related party | 31,520 | 2,431 | ||||||

| Accrued liabilities | 46,219 | 20,998 | ||||||

| Total Current Liabilities | 242,359 | 286,081 | ||||||

| LONG- TERM LIABILITIES | ||||||||

| Asset retirement obligation | 86,739 | - | ||||||

| Total Liabilities | 329,098 | 286,081 | ||||||

| Commitments and Contingencies | ||||||||

| STOCKHOLDERS’ EQUITY: | ||||||||

| Preferred stock, $0.001 par value; 50,000,000 authorized | ||||||||

| Convertible Series C Preferred stock ($0.001 Par Value; 45,002 Shares Authorized; 0 issued and outstanding as of January 31, 2019 and April 30, 2018) | - | - | ||||||

| Convertible Series E Preferred stock ($0.001 Par Value; 2,500 Shares Authorized; 0 issued and outstanding as of January 31, 2019 and April 30, 2018) | - | - | ||||||

| Common stock ($0.001 Par Value; 200,000,000 Shares Authorized; 19,125,263 issued and 18,600,763 outstanding as of January 31, 2019 and 17,590,574 issued and outstanding as of April 30, 2018) | 19,125 | 17,591 | ||||||

| Additional paid-in capital | 32,443,244 | 30,911,222 | ||||||

| Accumulated deficit | (24,783,857 | ) | (18,228,552 | ) | ||||

| Total Stockholders’ Equity | 7,678,512 | 12,700,261 | ||||||

| Total Liabilities and Stockholders’ Equity | $ | 8,007,610 | $ | 12,986,342 | ||||

The accompanying Notes to Unaudited Condensed Consolidated Financial Statements are an integral part of these financial statements.

| 3 |

U.S. GOLD CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| For the Three Months | For the Three Months | For the Nine Months | For the Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| January 31, 2019 | January 31, 2018 | January 31, 2019 | January 31, 2018 | |||||||||||||

| Net revenues | $ | - | $ | - | $ | - | $ | - | ||||||||

| Operating expenses: | ||||||||||||||||

| Compensation and related taxes | 318,771 | 224,109 | 1,545,967 | 1,875,367 | ||||||||||||

| Exploration costs | 737,164 | 932,182 | 2,503,277 | 2,236,461 | ||||||||||||

| Professional fees | 476,604 | 463,714 | 1,644,607 | 1,990,401 | ||||||||||||

| General and administrative expenses | 102,809 | 148,243 | 423,309 | 544,600 | ||||||||||||

| Total operating expenses | 1,635,348 | 1,768,248 | 6,117,160 | 6,646,829 | ||||||||||||

| Operating loss from continuing operations | (1,635,348 | ) | (1,768,248 | ) | (6,117,160 | ) | (6,646,829 | ) | ||||||||

| Loss from continuing operations before provision for income taxes | (1,635,348 | ) | (1,768,248 | ) | (6,117,160 | ) | (6,646,829 | ) | ||||||||

| Provision for income taxes | (438,145 | ) | - | (438,145 | ) | - | ||||||||||

| Loss from continuing operations | (2,073,493 | ) | (1,768,248 | ) | (6,555,305 | ) | (6,646,829 | ) | ||||||||

| Discontinued operations: | ||||||||||||||||

| Gain (loss) from discontinued operations | - | 3,428 | - | (5,925,640 | ) | |||||||||||

| Gain (loss) from sale of discontinued operations | - | (7,538 | ) | - | 94,485 | |||||||||||

| Total loss from discontinued operations | - | (4,110 | ) | - | (5,831,155 | ) | ||||||||||

| Net loss | $ | (2,073,493 | ) | $ | (1,772,358 | ) | $ | (6,555,305 | ) | $ | (12,477,984 | ) | ||||

| Loss per common share, basic and diluted | ||||||||||||||||

| Loss from continuing operations | $ | (0.11 | ) | $ | (0.12 | ) | $ | (0.36 | ) | $ | (0.55 | ) | ||||

| Discontinuing: | ||||||||||||||||

| Operations | $ | - | $ | 0.00 | $ | - | $ | (0.49 | ) | |||||||

| Gain | $ | - | $ | 0.00 | $ | - | $ | 0.01 | ||||||||

| Total discontinuing operations | $ | - | $ | 0.00 | $ | - | $ | (0.48 | ) | |||||||

| Net loss per share | $ | (0.11 | ) | $ | (0.12 | ) | $ | (0.36 | ) | $ | (1.03 | ) | ||||

| Weighted average common shares outstanding - basic | 18,757,263 | 14,400,023 | 18,173,054 | 12,152,505 | ||||||||||||

The accompanying Notes to Unaudited Condensed Consolidated Financial Statements are an integral part of these financial statements.

| 4 |

U.S. GOLD CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY (UNAUDITED)

FOR THE NINE MONTHS ENDED JANUARY 31, 2019

Preferred Stock- Series C | Preferred Stock- Series E | Common Stock | Additional | Total | ||||||||||||||||||||||||||||||||

| $0.001 Par Value | $0.001 Par Value | $0.001 Par Value | Paid-in | Accumulated | Stockholders’ | |||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||||||||||||||

| Balance, April 30, 2018 | - | $ | - | - | $ | - | 17,590,574 | $ | 17,591 | $ | 30,911,222 | $ | (18,228,552 | ) | $ | 12,700,261 | ||||||||||||||||||||

| Issuance of common stock for cash, net of issuance costs | - | - | - | - | 235,071 | 235 | 178,637 | - | 178,872 | |||||||||||||||||||||||||||

| Issuance of common stock for salaries | - | - | - | - | 91,268 | 91 | 99,909 | - | 100,000 | |||||||||||||||||||||||||||

| Issuance of common stock for exploration expenses | - | - | - | - | 199,159 | 199 | 183,027 | - | 183,226 | |||||||||||||||||||||||||||

| Issuance of common stock for services | - | - | - | - | 1,000,000 | 1,000 | 852,232 | - | 853,232 | |||||||||||||||||||||||||||

| Issuance of common stock for accrued services | - | - | - | - | 9,191 | 9 | 12,491 | - | 12,500 | |||||||||||||||||||||||||||

| Issuance of options for services | - | - | - | - | - | - | 205,726 | - | 205,726 | |||||||||||||||||||||||||||

| Net loss - For the nine months ended January 31, 2019 | - | - | - | - | - | - | - | (6,555,305 | ) | (6,555,305 | ) | |||||||||||||||||||||||||

| Balance, January 31, 2019 | - | $ | - | - | $ | - | 19,125,263 | $ | 19,125 | $ | 32,443,244 | $ | (24,783,857 | ) | $ | 7,678,512 | ||||||||||||||||||||

The accompanying Notes to Unaudited Condensed Consolidated Financial Statements are an integral part of these financial statements.

| 5 |

U.S. GOLD CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| For the Nine Months | For the Nine Months | |||||||

| Ended | Ended | |||||||

| January 31, 2019 | January 31, 2018 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | (6,555,305 | ) | $ | (12,477,984 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation | 4,602 | - | ||||||

| Accretion | 4,854 | - | ||||||

| Stock based compensation | 1,233,574 | 665,210 | ||||||

| Salary paid with shares | 100,000 | - | ||||||

| Exploration expense paid with shares | 183,226 | - | ||||||

| Amortization of prepaid stock-based expenses | - | 242,537 | ||||||

| Deferred income taxes | 438,145 | - | ||||||

| Impairment expense | - | 6,094,760 | ||||||

| Gain on sale of business | - | (94,485 | ) | |||||

| Gain on extinguishment of liabilities | - | (248,684 | ) | |||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other current assets | 244,542 | (404,725 | ) | |||||

| Reclamation bond deposit and other assets | (254,019 | ) | (27,881 | ) | ||||

| Accounts payable and accrued liabilities | (60,311 | ) | (10,385 | ) | ||||

| Accounts payable – related parties | 29,089 | - | ||||||

| NET CASH USED IN OPERATING ACTIVITIES | (4,631,603 | ) | (6,261,637 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Net proceeds received from sale of business | - | 326,404 | ||||||

| Investment in note receivable | - | (20,479 | ) | |||||

| NET CASH PROVIDED BY INVESTING ACTIVITIES | - | 305,925 | ||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Issuance of preferred stock and warrants, net of issuance cost | - | 4,918,620 | ||||||

| Issuance of common stock, net of issuance cost | 178,872 | 2,590,004 | ||||||

| NET CASH PROVIDED BY FINANCING ACTIVITIES | 178,872 | 7,508,624 | ||||||

| NET INCREASE (DECREASE) IN CASH | (4,452,731 | ) | 1,552,912 | |||||

| CASH - beginning of period | 7,646,279 | 6,820,623 | ||||||

| CASH - end of period | $ | 3,193,548 | $ | 8,373,535 | ||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | ||||||||

| Cash paid for: | ||||||||

| Interest | $ | - | $ | - | ||||

| Income taxes | $ | - | $ | - | ||||

| SUPPLEMENTAL DISCLOSURE OF NON-CASH INVESTING AND FINANCING ACTIVITIES: | ||||||||

| Grant of stock options for the acquisition of mineral rights | $ | - | $ | 35,850 | ||||

| Increase in asset retirement obligation | $ | 81,885 | $ | - | ||||

| Issuance of common stock pursuant to merger | $ | - | $ | 5,661,935 | ||||

| Conversion of preferred stock into common stock | $ | - | $ | 43 | ||||

| Issuance of common stock for accrued services | $ | 12,500 | $ | 137,500 | ||||

| Issuance of common stock for prepaid services | $ | 174,616 | $ | 253,937 | ||||

The accompanying Notes to Unaudited Condensed Consolidated Financial Statements are an integral part of these financial statements.

| 6 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

NOTE 1 - ORGANIZATION AND DESCRIPTION OF BUSINESS

Organization

U.S. Gold Corp., formerly known as Dataram Corporation (the “Company”), was originally incorporated in the State of New Jersey in 1967 was subsequently re-incorporated under the laws of the State of Nevada in 2016. Effective June 26, 2017, the Company changed its legal name to U.S. Gold Corp. from Dataram Corporation. On May 23, 2017, the Company merged with Gold King Corp. (“Gold King”), in a transaction treated as a reverse acquisition and recapitalization, and the business of Gold King became the business of the Company. The financial statements are those of Gold King (the accounting acquirer) prior to the merger and include the activity of Dataram Corporation (the legal acquirer) from the date of the merger. Gold King is a gold and precious metals exploration company pursuing exploration and development opportunities primarily in Nevada and Wyoming. None of the Company’s properties contain proven and probable reserves and all of the Company’s activities on all of its properties are exploratory in nature.

On July 6, 2016, the Company filed a certificate of amendment to its Articles of Incorporation with the Secretary of State of Nevada in order to effectuate a reverse stock split of the Company’s issued and outstanding common stock per share on a one for three basis, effective on July 8, 2016. Subsequently, on May 3, 2017, the Company filed another certificate of amendment to its Articles of Incorporation, as amended, with the Secretary of State of the State of Nevada in order to effectuate a reverse stock split of the Company’s issued and outstanding common stock on a one for four basis. All share and per share values of the Company’s common stock for all periods presented in the accompanying condensed consolidated financial statements are retroactively restated for the effect of the reverse stock splits.

Recent developments - Acquisition and Disposition

On June 13, 2016, Gold King, a private Nevada corporation, entered into an Agreement and Plan of Merger (the “Merger Agreement”) with the Company, the Company’s wholly-owned subsidiary, Dataram Acquisition Sub, Inc., a Nevada corporation (“Acquisition Sub”), and all of the principal shareholders of Gold King (the “Gold King Shareholders”). Upon closing of the transactions contemplated under the Merger Agreement (the “Merger”), Gold King merged with and into Acquisition Sub with Gold King as the surviving corporation and became a wholly-owned subsidiary of the Company.

On May 23, 2017, the Company closed the Merger with Gold King. The Merger constituted a change of control, the majority of the Board of Directors changed with the consummation of the Merger. The Company issued shares of common stock to Gold King which represented approximately 90% of the combined company.

On July 31, 2017, the Company’s Board of Directors, or Board, reviewed and approved the recommendation of management to consider strategic options for Dataram Corporation’s legacy business (“Dataram Memory”) including the sale of the legacy business. Upon board approval, the legacy business activities were re-classed and reported as part of “discontinued operations” on the condensed consolidated statements of operations and assets and liabilities were reflected on the condensed consolidated balance sheets as “held for sale”.

On October 13, 2017, the Company sold the Dataram Memory business for a price of $900,000 (see Note 7).

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying interim unaudited condensed consolidated financial statements have been prepared by the Company in accordance with accounting principles generally accepted in the United States of America, the instructions to Form 10-Q, and the rules and regulations of the United States Securities and Exchange Commission for interim financial information, which includes the unaudited condensed consolidated financial statements and presents the unaudited condensed consolidated financial statements of the Company and its wholly-owned subsidiaries as of January 31, 2019. All intercompany transactions and balances have been eliminated. The accounting policies and procedures used in the preparation of these unaudited condensed consolidated financial statements have been derived from the audited financial statements of the Company for the year ended April 30, 2018, which are contained in the Form 10-K filed on July 30, 2018. The unaudited condensed consolidated balance sheet as of April 30, 2018 was derived from those financial statements. It is management’s opinion that all material adjustments (consisting of normal recurring adjustments) have been made, which are necessary for a fair financial statement presentation. Operating results for the nine-month period ended January 31, 2019 are not necessarily indicative of the results to be expected for the year ending April 30, 2019.

| 7 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

Use of Estimates and Assumptions

In preparing the condensed consolidated financial statements, management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the condensed consolidated balance sheet, and revenues and expenses for the period then ended. Actual results may differ significantly from those estimates. Significant estimates made by management include, but are not limited to valuation of mineral rights, goodwill, stock-based compensation, the fair value of common stock issued, asset retirement obligation and the valuation of deferred tax assets and liabilities.

Fair Value Measurements

The Company adopted Accounting Standards Codification (“ASC”) ASC 820, “Fair Value Measurements and Disclosures” (“ASC 820”), for assets and liabilities measured at fair value on a recurring basis. ASC 820 establishes a common definition for fair value to be applied in accordance with accounting principles generally accepted in the United States of America that requires the use of fair value measurements, establishes a framework for measuring fair value and expands disclosure about such fair value measurements.

ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Additionally, ASC 820 requires the use of valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs.

These inputs are prioritized below:

| Level 1: | Observable inputs such as quoted market prices in active markets for identical assets or liabilities. |

| Level 2: | Observable market-based inputs or unobservable inputs that are corroborated by market data. |

| Level 3: | Unobservable inputs for which there is little or no market data, which require the use of the reporting entity’s own assumptions. |

The Company analyzes all financial instruments with features of both liabilities and equity under the Financial Accounting Standard Board’s (“FASB”) accounting standard for such instruments. Under this standard, financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement.

The carrying amounts reported in the unaudited condensed consolidated balance sheets for cash, prepaid expense and other current assets – current, accounts payable, and accrued liabilities, approximate their estimated fair values based on the short-term maturity of these instruments.

Goodwill and other intangible assets

In accordance with ASC 350-30-65, the Company assesses the impairment of identifiable intangibles whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Factors the Company considers to be important which could trigger an impairment review include the following:

| 1. | Significant underperformance relative to expected historical or projected future operating results; | |

| 2. | Significant changes in the manner of use of the acquired assets or the strategy for the overall business; and | |

| 3. | Significant negative industry or economic trends. |

When the Company determines that the carrying value of intangibles may not be recoverable based upon the existence of one or more of the above indicators of impairment and the carrying value of the asset cannot be recovered from projected undiscounted cash flows, the Company records an impairment charge. The Company measures any impairment based on a projected discounted cash flow method using a discount rate determined by management to be commensurate with the risk inherent in the current business model. Significant management judgment is required in determining whether an indicator of impairment exists and in projecting cash flows.

Property

Property is carried at cost. The cost of repairs and maintenance is expensed as incurred; major replacements and improvements are capitalized. When assets are retired or disposed of, the cost and accumulated depreciation are removed from the accounts, and any resulting gains or losses are included in income in the year of disposition. Depreciation is calculated on a straight-line basis over the estimated useful life of the assets, generally ten years.

| 8 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

Impairment of long-lived assets

The Company reviews long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be fully recoverable, or at least annually. The Company recognizes an impairment loss when the sum of expected undiscounted future cash flows is less than the carrying amount of the asset. The amount of impairment is measured as the difference between the asset’s estimated fair value and its book value. During the year ended April 30, 2018, the Company determined that the carrying value of Goodwill (see Note 6) exceeded its fair value, which triggered an impairment analysis. The Company recorded a goodwill impairment expense of $6,094,760 during the year ended April 30, 2018, nonrecurring level 3 fair value measurement. No impairment of goodwill was recorded during the nine months ended January 31, 2019.

Mineral Rights

Costs of lease, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. The Company expenses all mineral exploration costs as incurred as it is still in the exploration stage. If the Company identifies proven and probable reserves in its investigation of its properties and upon development of a plan for operating a mine, it would enter the development stage and capitalize future costs until production is established.

When a property reaches the production stage, the related capitalized costs are amortized on a units-of-production basis over the proven and probable reserves following the commencement of production. The Company assesses the carrying costs of the capitalized mineral properties for impairment under ASC 360-10, “Impairment of long-lived assets”, and evaluates its carrying value under ASC 930-360, “Extractive Activities - Mining”, annually. An impairment is recognized when the sum of the expected undiscounted future cash flows is less than the carrying amount of the mineral properties. Impairment losses, if any, are measured as the excess of the carrying amount of the mineral properties over its estimated fair value.

To date, the Company has not established the commercial feasibility of any exploration prospects; therefore, all exploration costs are being expensed.

ASC 930-805, “Extractive Activities-Mining: Business Combinations” (“ASC 930-805”), states that mineral rights consist of the legal right to explore, extract, and retain at least a portion of the benefits from mineral deposits. Mining assets include mineral rights.

Acquired mineral rights are considered tangible assets under ASC 930-805. ASC 930-805 requires that mineral rights be recognized at fair value as of the acquisition date. As a result, the direct costs to acquire mineral rights are initially capitalized as tangible assets. Mineral rights include costs associated with acquiring patented and unpatented mining claims.

ASC 930-805 provides that in measuring the fair value of mineral assets, an acquirer should take into account both:

● The value beyond proven and probable reserves (“VBPP”) to the extent that a market participant would include VBPP in determining the fair value of the assets.

● The effects of anticipated fluctuations in the future market price of minerals in a manner that is consistent with the expectations of market participants.

Share-Based Compensation

Share-based compensation is accounted for based on the requirements of ASC 718, “Compensation – Stock Compensation’ (“ASC 718”) which requires recognition in the financial statements of the cost of employee and director services received in exchange for an award of equity instruments over the period the employee or director is required to perform the services in exchange for the award (presumptively, the vesting period). ASC 718 also requires measurement of the cost of employee and director services received in exchange for an award based on the grant-date fair value of the award. Pursuant to ASC 505, “Equity – Equity Based Payments to Non-Employees” (“ASC 505-50”), for share-based payments to consultants and other third-parties, compensation expense is determined at the measurement date which is the grant date. Until the measurement date is reached, the total amount of compensation expense remains uncertain.

| 9 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

In June 2018, the FASB issued ASU 2018-07, “Compensation — Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment Accounting”, which expands the scope of Topic 718 to include all share-based payment transactions for acquiring goods and services from nonemployees. ASU 2018-07 specifies that Topic 718 applies to all share-based payment transactions in which the grantor acquires goods and services to be used or consumed in its own operations by issuing share-based payment awards. ASU 2018-07 also clarifies that Topic 718 does not apply to share-based payments used to effectively provide (1) financing to the issuer or (2) awards granted in conjunction with selling goods or services to customers as part of a contract accounted for under ASC 606. ASU 2018-07 is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years, with early adoption permitted, but no earlier than adoption of ASC 606. The Company chose to early adopt ASU 2018-07 in July 2018. The adoption of this standard did not have a material impact on the Company’s unaudited condensed consolidated financial statements and related disclosures.

Accounting for Warrants

The Company classifies as equity any contracts that (i) require physical settlement or net-share settlement or (ii) gives the Company a choice of net-cash settlement or settlement in its own shares (physical settlement or net-share settlement). The Company classifies as assets or liabilities any contracts that (i) require net-cash settlement (including a requirement to net-cash settle the contract if an event occurs and if that event is outside the control of the Company) or (ii) gives the counterparty a choice of net-cash settlement or settlement in shares (physical settlement or net-share settlement).

The Company assessed the classification of its common stock purchase warrants as of the date of each equity offering and determined that such instruments met the criteria for equity classification, as the settlement terms indicate that the instruments are indexed to the entity’s underlying stock.

Convertible Preferred Stock

The Company accounts for its convertible preferred stock under the provisions of ASC 480, “Distinguishing Liabilities from Equity”, which sets forth the standards for how an issuer classifies and measures certain financial instruments with characteristics of both liabilities and equity. ASC 480 requires an issuer to classify a financial instrument that is within the scope of ASC 480 as a liability if such financial instrument embodies an unconditional obligation to redeem the instrument at a specified date and/or upon an event certain to occur.

Convertible Instruments

The Company bifurcates conversion options from their host instruments and account for them as free standing derivative financial instruments according to certain criteria. The criteria includes circumstances in which (a) the economic characteristics and risks of the embedded derivative instrument are not clearly and closely related to the economic characteristics and risks of the host contract, (b) the hybrid instrument that embodies both the embedded derivative instrument and the host contract is not re-measured at fair value under otherwise applicable generally accepted accounting principles with changes in fair value reported in earnings as they occur and (c) a separate instrument with the same terms as the embedded derivative instrument would be considered a derivative instrument. An exception to this rule when the host instrument is deemed to be conventional as that term is described under applicable U.S. GAAP.

When the Company has determined that the embedded conversion options should not be bifurcated from their host instruments, the Company records, when necessary, a beneficial conversion feature (“BCF”) related to the issuance of convertible debt and equity instruments that have conversion features at fixed rates that are in-the-money when issued, and the fair value of warrants issued in connection with those instruments. The BCF for the convertible instruments is recognized and measured by allocating a portion of the proceeds to warrants, based on their relative fair value, and as a reduction to the carrying amount of the convertible instrument equal to the intrinsic value of the conversion feature. The discounts recorded in connection with the BCF and warrant valuation are recognized a) for convertible debt as interest expense over the term of the debt, using the effective interest method or b) for convertible preferred stock as dividends at the time the stock first becomes convertible.

| 10 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

Asset Retirement Obligations

Asset retirement obligations (“ARO”), consisting primarily of estimated reclamation costs at the Company’s Copper King and Keystone properties, are recognized in the period incurred and when a reasonable estimate can be made, and recorded as liabilities at fair value. Such obligations, which are initially estimated based on discounted cash flow estimates, are accreted to full value over time through charges to accretion expense. Corresponding asset retirement costs are capitalized as part of the carrying amount of the related long-lived asset and depreciated over the asset’s remaining useful life. Asset retirement obligations are periodically adjusted to reflect changes in the estimated present value resulting from revisions to the estimated timing or amount of reclamation and closure costs. The Company reviews and evaluates its asset retirement obligations annually or more frequently at interim periods if deemed necessary.

Income taxes

The Company accounts for income taxes pursuant to the provision of ASC 740-10, “Accounting for Income Taxes” (“ASC 740-10”), which requires, among other things, an asset and liability approach to calculating deferred income taxes. The asset and liability approach requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the carrying amounts and the tax bases of assets and liabilities. A valuation allowance is provided to offset any net deferred tax assets for which management believes it is more likely than not that the net deferred asset will not be realized.

The Company follows the provision of ASC 740-10 related to Accounting for Uncertain Income Tax Positions. When tax returns are filed, there may be uncertainty about the merits of positions taken or the amount of the position that would be ultimately sustained. In accordance with the guidance of ASC 740-10, the benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions.

Tax positions that meet the more likely than not recognition threshold are measured at the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefit associated with tax positions taken that exceed the amount measured as described above should be reflected as a liability for uncertain tax benefits in the accompanying balance sheet along with any associated interest and penalties that would be payable to the taxing authorities upon examination. The Company believes its tax positions are all more likely than not to be upheld upon examination. As such, the Company has not recorded a liability for uncertain tax benefits.

The Company has adopted ASC 740-10-25, “Definition of Settlement”, which provides guidance on how an entity should determine whether a tax position is effectively settled for the purpose of recognizing previously unrecognized tax benefits and provides that a tax position can be effectively settled upon the completion and examination by a taxing authority without being legally extinguished. For tax positions considered effectively settled, an entity would recognize the full amount of tax benefit, even if the tax position is not considered more likely than not to be sustained based solely on the basis of its technical merits and the statute of limitations remains open. The federal and state income tax returns of the Company are subject to examination by the IRS and state taxing authorities, generally for three years after they are filed.

The Tax Cuts and Jobs Act (the “Act”) was enacted in December 2017. Among other things, the Act reduced the U.S. federal corporate tax rate from 34 percent to 21 percent as of January 1, 2018 and eliminated the alternative minimum tax (“AMT”) for corporations. Since the deferred tax assets are expected to reverse in a future year, it has been tax effected using the 21% federal corporate tax rate. As a result of the reduction in the corporate tax rate, the Company decreased its gross deferred tax assets by approximately $2.1 million which was offset by a corresponding decrease to the valuation allowance as of April 30, 2018, which had no impact on the Company’s consolidated financial statements for the year ended April 30, 2018. The Company will continue to analyze the Tax Act to assess its full effects on the Company’s financial results, including disclosures, for the Company’s fiscal year ending April 30, 2019, but the Company does not expect the Tax Act to have a material impact on the Company’s unaudited condensed consolidated financial statements.

On December 22, 2017, the Securities and Exchange Commission issued Staff Accounting Bulletin 118, which allows a measurement period, not to exceed one year, to finalize the accounting for the income tax effects of the Act. Until the accounting for the income tax effects of the Act is complete, the reported amounts are based on reasonable estimates, are disclosed as provisional and reflect any adjustments in subsequent periods as estimates are refined or the accounting of the tax effects are completed.

| 11 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

During the quarter ended January 31, 2019, the Company established a valuation allowance of $438,145 to offset any previously recognized net deferred tax assets for which management believes it is more likely than not that the net deferred asset will not be realized.

Recent Accounting Pronouncements

In February 2016, the FASB established Topic 842, “Leases”, by issuing Accounting Standards Update (“ASU”) No. 2016-02, which requires lessees to recognize leases on-balance sheet and disclose key information about leasing arrangements. Topic 842 was subsequently amended by ASU No. 2018-01, “Land Easement Practical Expedient for Transition to Topic 842”; ASU No. 2018-10, “Codification Improvements to Topic 842, Leases”; and ASU No. 2018-11, “Targeted Improvements”. The new standard establishes a right-of-use model (ROU) that requires a lessee to recognize a ROU asset and lease liability on the balance sheet for all leases with a term longer than 12 months. Leases will be classified as finance or operating, with classification affecting the pattern and classification of expense recognition in the income statement. The new standard is effective for the Company on May 1, 2019, with early adoption permitted. The Company expects to adopt the new standard on its effective date.

A modified retrospective transition approach is required, applying the new standard to all leases existing at the date of initial application. An entity may choose to use either (1) its effective date or (2) the beginning of the earliest comparative period presented in the financial statements as its date of initial application. If an entity chooses the second option, the transition requirements for existing leases also apply to leases entered into between the date of initial application and the effective date. The entity must also recast its comparative period financial statements and provide the disclosures required by the new standard for the comparative periods. The Company expects to adopt the new standard on May 1, 2019 and use the effective date as the date of initial application. Consequently, financial information will not be updated and the disclosures required under the new standard will not be provided for dates and periods before May 1, 2019.

While the Company is assessing the effects of adoption, it currently believes the most significant effects relate to the recognition of new ROU assets and lease liabilities on its balance sheet for mineral property operating leases and providing significant new disclosures about our leasing activities. The Company does not expect a significant change in its leasing activities between now and adoption.

Other accounting standards that have been issued or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the financial statements upon adoption. The Company does not discuss recent pronouncements that are not anticipated to have an impact on or are unrelated to its financial condition, results of operations, cash flows or disclosures.

NOTE 3 — GOING CONCERN

The accompanying condensed consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company has incurred significant operating losses since its inception. As of January 31, 2019, the Company had cash of approximately $3.2 million, working capital of approximately $3.2 million, an accumulated deficit of approximately $24.8 million, and cash used in operating activities of approximately $4.6 million. As a result of the utilization of cash in its operating activities, and the development of its assets, the Company has incurred losses since it commenced operations. The Company’s primary source of operating funds since inception has been equity financings. These matters raise substantial doubt about the Company’s ability to continue as a going concern for the twelve months following the issuance of these financial statements.

The condensed consolidated financial statements do not include any adjustments relating to the recoverability and classification of asset amounts or the classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

The Company consummated private placements to several investors for the sale of the Company’s Series B Convertible Preferred Stock (“Series B Preferred Stock”) and Series C Convertible Preferred Stock (“Series C Preferred Stock”) for aggregate net proceeds of approximately $10.9 million between July 2016 and October 2016, received net proceeds from sale of the Company’s common stock of approximately $2.6 million between July 2017 and October 2017 and completed a private placement for the sale of the Company’s Series E Convertible Preferred Stock (“Series E Preferred Stock”) and warrants for aggregate net proceeds of approximately $4.9 million in January 2018. All preferred shares were converted to common shares during the fiscal year ended April 30, 2018.

| 12 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

On November 2, 2018, the Company entered into an At-the-Market Offering Agreement (the “ATM Agreement”) with H.C. Wainwright & Co., LLC (“Wainwright”) as sales manager. Under the terms of the ATM Agreement, the Company will be entitled to sell, at its sole discretion and from time to time as it may choose, common shares in the capital of the Company (“Shares”) through Wainwright, with such sales having an aggregate gross sales value of up to $1,000,000 (the “Offering”). Subject to the terms and conditions of the ATM Agreement, Wainwright will use its commercially reasonable efforts to sell the Shares from time to time, based upon the Company’s instructions. The Company has provided Wainwright with customary indemnification rights, and Wainwright will be entitled to a commission at a fixed commission rate equal to 3.0% of the gross proceeds per Share sold. The ATM Agreement will remain in full force and effect until the ATM Agreement is terminated. For the quarter ended January 31, 2019, the Company has sold 235,071 shares and raised a net of $178,872, net of issuance costs of $60,300, through the ATM Agreement at prices per share averaging $1.02.

There can be no assurance that the Company will be able to raise additional capital or if the terms will be favorable.

NOTE 4 — MINERAL RIGHTS

Copper King Project

The mineral properties consist of the Copper King gold and copper development project located in the Silver Crown Mining District of southeast Wyoming (the “Copper King Project”). On July 2, 2014, the Company entered into an Asset Purchase Agreement whereby the Company acquired certain mining leases and other mineral rights comprising the Copper King project. The purchase price was (a) cash payment in the amount of $1.5 million and (b) closing shares calculated at 50% of the issued and outstanding shares of the Company’s common stock and valued at $1.5 million.

In accordance with ASC 360-10, “Property, Plant, and Equipment”, assets are recognized based on their cost to the acquiring entity, which generally includes the transaction costs of the asset acquisition. Accordingly, the Company recorded a total cost of the acquired mineral properties of $3,091,738 which includes the purchase price ($3,000,000) and related transaction cost.

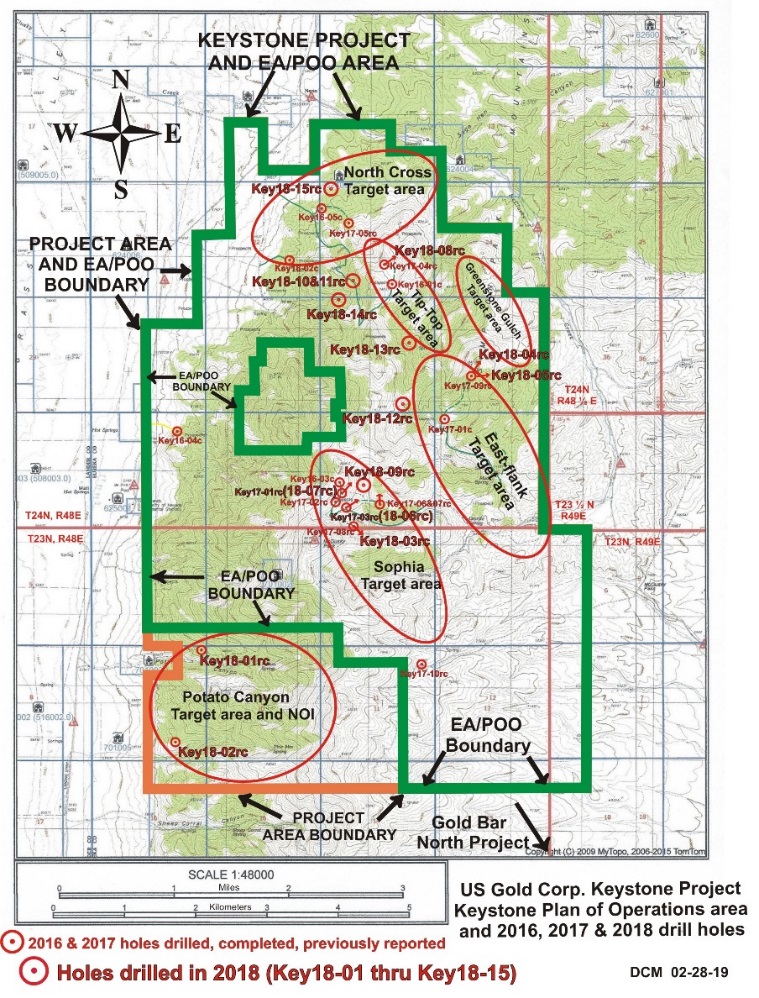

Keystone Project

The Company, through its wholly-owned subsidiary, U.S. Gold Acquisition Corp., acquired the mining claims comprising the Keystone Project on May 27, 2016 from Nevada Gold Ventures, LLC (“Nevada Gold”) and Americas Gold Exploration, Inc. under the terms of a Purchase and Sale Agreement. At the time of purchase, the Keystone Project consisted of 284 unpatented lode mining claims situated in Eureka County, Nevada. The purchase price for the Keystone Project consisted of the following: (a) cash payment in the amount of $250,000, (b) the closing shares which is equivalent to 462,500 shares of the Company’s common stock and (c) an aggregate of 231,458 five-year options to purchase shares of the Company’s common stock at an exercise price of $3.60 per share.

The Company valued the common shares at the fair value of $555,000 or $1.20 per common share based on the contemporaneous sale of its preferred stock in a private placement at $0.10 per common share. The options were valued at $184,968. The options shall vest over a period of two years whereby 1/24 of the options shall vest and become exercisable each month for the next 24 months. The options are non-forfeitable and are not subject to obligations or service requirements.

Accordingly, the Company recorded a total cost of the acquired mineral properties of $1,028,885 which includes the purchase price ($989,968) and related transaction cost ($38,917). Some of the Keystone Project claims are subject to pre-existing net smelter royalty (“NSR”) obligations. In addition, under the terms of the Purchase and Sale Agreement, Nevada Gold retained additional NSR rights of 0.5% with regard to certain claims and 3.5% with regard to certain other claims. Under the terms of the Purchase and Sale Agreement, the Company may buy down one percent (1%) of the royalty from Nevada Gold at any time through the fifth anniversary of the closing date for $2,000,000. In addition, the Company may buy down an additional one percent (1%) of the royalty anytime through the eighth anniversary of the closing date for $5,000,000.

In August 2017, the Company closed on a transaction under a purchase and sale agreement executed in June 2017 with Nevada Gold and the Company’s wholly-owned subsidiary, U.S. Gold Acquisition Corporation, a Nevada corporation, pursuant to which Nevada Gold sold and U.S. Gold Acquisition Corporation purchased all right, title and interest in the Gold Bar North Property, a gold development project located in Eureka County, Nevada. The purchase price for the Gold Bar North Property was: (a) cash payment in the amount of $20,479 which was paid in August 2017 and (b) 15,000 shares of common stock of the Company which were issued in August 2017 valued at $35,850. Mr. David Mathewson, the Company’s Chief Geologist, is a member of Nevada Gold.

| 13 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

As of the date of these condensed consolidated financial statements, the Company has not established any proven or probable reserves on its mineral properties and has incurred only acquisition costs and exploration costs.

Mineral properties consisted of the following:

| January 31, 2019 | April 30, 2018 | |||||||

| (unaudited) | ||||||||

| Copper King project | $ | 3,091,738 | $ | 3,091,738 | ||||

| Keystone project | 1,028,885 | 1,028,885 | ||||||

| Gold Bar North project | 56,329 | 56,329 | ||||||

| Total | $ | 4,176,952 | $ | 4,176,952 | ||||

NOTE 5 — PROPERTY

Property consisted of the following:

| January 31, 2019 | April 30, 2018 | |||||||

| (unaudited) | ||||||||

| Site costs | $ | 81,885 | $ | - | ||||

| Less: accumulated depreciation | (4,602 | ) | - | |||||

| Total | $ | 77,283 | $ | - | ||||

For the nine months ended January 31, 2019 and 2018, depreciation expense amounted to $4,602 and $0, respectively.

NOTE 6 — ASSET RETIREMENT OBLIGATION

In conjunction with various permit approvals permitting the Company to undergo exploration activities at the Copper King project and Keystone project, the Company has recorded an asset retirement obligation based upon the reclamation plans submitted in connection with the various permits.

The following table summarizes activity in the Company’s ARO:

| January 31, 2019 | April 30, 2018 | |||||||

| Balance, beginning of period | $ | - | $ | - | ||||

| Addition and changes in estimates | 81,884 | - | ||||||

| Accretion expense | 4,854 | - | ||||||

| Balance, end of period | $ | 86,739 | $ | - | ||||

| 14 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

NOTE 7 — ACQUISITION AND DISPOSITION

On May 23, 2017, the Company closed the Merger with Gold King. Pursuant to the terms of the Merger Agreement and as consideration for the acquisition of Gold King, on the closing date, 2,446,433 shares of the Company’s common stock, par value $0.001 per share, were issued to holders of Gold King’s common stock, Series A Preferred Stock, Series B Preferred Stock and certain incoming officers. In addition, 45,000.18 shares of the Company’s newly designated Series C Preferred Stock, par value $0.001 per share, convertible into an aggregate of 4,500,180 shares of the Company’s common stock were issued to Copper King LLC, 45,500.18 shares of Series C Preferred Stock were issued to Copper King LLC upon closing, 4,500.01 shares of Series C Preferred Stock were to be held in escrow pursuant to the terms of an escrow agreement and 4,523,589 shares of the Company’s common stock and warrants to purchase up to 452,359 shares of the Company’s common stock were issued to the holders of Gold King’s Series C Preferred Stock. Additionally, 231,458 of the Company’s stock options were issued to the holders of Gold King’s outstanding stock options issued in connection with the closing of the acquisition of the Keystone Project.

As a result of the Merger, for financial statement reporting purposes, the business combination between the Company and Gold King has been treated as a reverse acquisition and recapitalization with Gold King deemed the accounting acquirer and the Company deemed the accounting acquiree under the acquisition method of accounting in accordance with FASB Accounting Standards Codification (“ASC”) Section 805-10-55. At the time of the Merger, both the Company and Gold King have their own separate operating segments. Accordingly, the assets and liabilities and the historical operations that are reflected in the consolidated financial statements after the Merger are those of the Gold King and are recorded at the historical cost basis of the Company. The acquisition process utilizes the capital structure of the Company and the assets and liabilities of Gold King which are recorded at historical cost.

The Company’s assets and liabilities were recorded at their fair values as of the date of the Merger and the results of operations of the Company are consolidated with results of operations of Gold King starting on the date of the Merger. The Company is deemed to have issued 1,204,667 shares of common stock which represents the outstanding common stock of the Company prior to the closing of the Merger. The Company accounted for the value under ASC 805-50-30-2 “Business Combinations” whereby if the consideration is not in the form of cash, the measurement is based on either the cost which shall be measured based on the fair value of the consideration given or the fair value of the assets (or net assets) acquired, whichever is more clearly evident and thus more reliably measurable.

The Company deemed that the fair value of the consideration given was $4.70 per share based on the quoted trading price on the date of the Merger amounting to $5,661,935 which is a more reliable measurement basis. The estimated fair values of assets acquired and liabilities assumed are provisional and are based on the information that was available as of the acquisition date to estimate the fair value of assets acquired and liabilities assumed. The Company believes that information provides a reasonable basis for estimating the fair values of assets acquired and liabilities assumed.

As a result of the reverse merger, the total purchase consideration exceeded the net assets acquired. The Company recorded $6,094,760 of goodwill at the time of the merger. None of the goodwill recognized is expected to be deductible for income tax purposes. The following table summarizes the consideration paid and the amounts of the assets acquired and liabilities assumed recognized at the acquisition date:

The net purchase price paid by the Company was allocated to assets acquired and liabilities assumed on the records of the Company as follows:

| Current assets (including cash of $255,555) | $ | 3,063,059 | ||

| Other assets | 45,984 | |||

| Goodwill | 6,094,760 | |||

| Liabilities assumed (including a note payable – credit line of $1,096,504) | (3,541,868 | ) | ||

| Net purchase price | $ | 5,661,935 |

During the year ended April 30, 2018, the Company recorded an impairment loss of $6,094,760 as the Company determined that the carrying value of the goodwill was not recoverable. The Company determined that if the business combination would have occurred on the first day of the reporting period, there would not have been a material change to the continuing operations of the financial statements presented.

| 15 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

In June 2017, subsequent to the Merger, the Company decided to discontinue its memory product business. The Company sold the Dataram Memory business on October 13, 2017 for a purchase price of $900,000. The Company will focus its activities on its gold and precious metal exploration business. During the year ended April 30, 2018, the Company received net proceeds from the sale of Dataram Memory business of $326,404 after payment of fees related to the sale such as legal and commission expenses and other liabilities assumed.

During the year ended April 30, 2018, the Company recognized a gain on extinguishment of liabilities of $248,684 which is included in the loss from discontinued operations as the Company has settled the distribution payable to the former Dataram Memory shareholders at an amount less than the liability originally recorded at the time of acquisition. Additionally, during the year ended April 30, 2018, the Company recognized gain from sale of discontinued operations of $94,485 related to the sale of the Dataram Memory business on October 13, 2017.

Credit Facility

The Company had a financing agreement (the “Financing Agreement”) with Rosenthal & Rosenthal, Inc. that provides for a revolving loan with a maximum borrowing capacity of $3,500,000. The Financing Agreement renewal date was August 31, 2017 and will renew from year to year unless such Financing Agreement is terminated as set forth in the loan agreement. The amount outstanding under the Financing Agreement bore interest at a rate of the Prime Rate (as defined in the Financing Agreement) plus 3.25% (the “Effective Rate”) or on Over-advances (as defined in the Financing Agreement), if any, at a rate of the Effective Rate plus 3%. The Financing Agreement contained other financial and restrictive covenants, including, among others, covenants limiting the Company’s ability to incur indebtedness, guarantee obligations, sell assets, make loans, enter into mergers and acquisition transactions and declare or make dividends. Borrowings under the Financing Agreement are collateralized by substantially all the assets of the Company. The Financing Agreement provided for advances against eligible accounts receivable and inventory balances based on prescribed formulas of raw materials and finished goods. On October 13, 2017, upon the sale of the Dataram Memory business, the buyer assumed the obligation under this Financing Agreement, therefore, liabilities related to this financing agreement was $0 as of April 30, 2018.

The following table sets forth for the year ended April 30, 2018, indicated selected financial data of the Company’s discontinued operations of its memory product business from the date of merger to April 30, 2018.

| April 30, 2018 | ||||

| Revenues | $ | 7,885,310 | ||

| Cost of sales | 6,653,363 | |||

| Gross profit | 1,231,947 | |||

| Operating and other non-operating expenses (including impairment charge of 6,094,760) | (7,406,271 | ) | ||

| Gain from extinguishment of liabilities | 248,684 | |||

| Loss from discontinued operations | (5,925,640 | ) | ||

| Gain from sale of discontinued operations | 94,485 | |||

| Total loss from discontinued operations | $ | (5,831,155 | ) | |

The following table sets forth for the year ended April 30, 2018, indicated selected financial data of the Company’s gain from sale of the Dataram Memory business.

| Total consideration | $ | 900,000 | ||

| Direct legal and sales commission expenses related to the sale | (201,510 | ) | ||

| Dataram’s accrued expenses to be deducted from the sales proceeds | (174,880 | ) | ||

| Total carrying value of Dataram Memory business on date of sale * | (429,125 | ) | ||

| Net gain from sale of Dataram Memory business | $ | 94,485 |

| Current assets | $ | 3,271,426 | ||

| Other assets | 33,320 | |||

| Current liabilities | (2,866,660 | ) | ||

| Liabilities – long term | (8,961 | ) | ||

| * Total carrying value of Dataram Memory business on date of sale | $ | 429,125 |

| 16 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

NOTE 8 — RELATED PARTY TRANSACTIONS

Accounts payable to related party as of January 31, 2019 and April 30, 2018 was $31,520, and $2,431 respectively and was reflected as accounts payable – related party in the accompanying unaudited condensed consolidated balance sheets. The related parties are a member of the Board of Directors owed $12,500, the Vice President-Head of Exploration owed $12,500 in stock and the Chief Financial Officer owed $6,520 at January 31, 2019.

NOTE 9 — STOCKHOLDERS’ EQUITY

2017 Equity Incentive Plan

In August 2017, the Company’s Board of Directors approved the Company’s 2017 Equity Incentive Plan (the “Plan”) including the reservation of 1,650,000 shares of common stock thereunder.

On January 1st of each year during the term of the Plan (the “Calculation Date”), the aggregate number of shares of Common Stock that are available for issuance shall automatically be increased by such number of shares as is equal to the number of shares sufficient to cause the Share Limit (as defined in the Plan) to equal twenty percent (20%) of the issued and outstanding Common Stock of the Company at such time, provided, however, that if on any Calculation Date the number of shares equal twenty percent (20%) of our total issued and outstanding Common Stock is less than the number of shares of Common Stock available for issuance under the Plan, no change will be made to the aggregate number of shares of Common Stock issuable under the Plan for that year (such that the aggregate number of shares of Common Stock available for issuance under the Plan will never decrease).

Common Stock

In May 2017, in connection with the Merger (see Note 7), the Company issued 37,879 shares of the Company’s common stock having a fair value of $100,000 to the Chief Geologist for services rendered to the Company from June 2016 to January 2017 pursuant to his employment agreement with the Company’s wholly-owned subsidiary Gold King (see Note 11). Consequently, the Company reduced accrued salaries by $100,000 as of July 31, 2017.

In July 2017, the Company sold 179,211 shares of its common stock at $2.79 per common share for proceeds of approximately $500,000.

Between May 2017 and July 2017, the Company issued 3,682,000 shares of the Company’s common stock in exchange for the conversion of 36,820 shares of the Company’s Series C Preferred Stock.

On November 2, 2018, the Company entered into an At-the-Market Offering Agreement (the “ATM Agreement”) with H.C. Wainwright & Co., LLC (“Wainwright”) as sales manager. Under the terms of the ATM Agreement, the Company will be entitled to sell, at its sole discretion and from time to time as it may choose, common stock of the Company (“Shares”) through Wainwright, with such sales having an aggregate gross sales value of up to $1,000,000 (the “Offering”).

Subject to the terms and conditions of the ATM Agreement, Wainwright will use its commercially reasonable efforts to sell the Shares from time to time, based upon the Company’s instructions. The Company has provided Wainwright with customary indemnification rights, and Wainwright will be entitled to a commission at a fixed commission rate equal to 3.0% of the gross proceeds per Share sold.

The ATM Agreement will remain in full force and effect until the ATM Agreement is terminated. For the quarter ended January 31, 2019, the Company sold 235,071 Shares and raised a net of $178,872, net of issuance costs of $60,300, through the ATM Agreement at prices per share averaging $1.02.

Common stock issued for services

During the nine months ended January 31, 2019, the Company issued 91,268 shares of the Company’s common stock to the Chief Geologist for services rendered to the Company from May 2018 to January 2019 pursuant to his employment agreement (see Note 11). The Company valued these common shares at the fair value of $100,000, or $0.93 - $1.36 per common share based on the quoted trading prices on the date of grants.

| 17 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

During the nine months ended January 31, 2019, the Company paid an accrued service liability in the amount of $12,500 by issuing 9,191 shares of common stock at a price of $1.36 per share.

On September 30, 2018, the Company issued an aggregate of 1,000,000 shares of the Company’s common stock to officers, directors, employees and consultants for services rendered. The shares vest 50% on the date of issuance and 50% on the one-year anniversary of the date of issuance. The 1,000,000 shares had a fair value of $990,000 and will be expensed over the vesting period. Additionally, on November 10, 2017, 12,000 shares was issued to a director that vest two years from issue date, and on February 20, 2018, 150,000 shares was issued to a consultant that vest ratably over 12 months, bringing the total of restricted shares issued to 1,162,000. A total of $138,332 and $798,977 was expensed for the three- and nine-month periods ended January 31, 2019.

On December 31, 2018, the Company paid a portion of its accounts payable to a vendor, in the amount of $183,226 by issuing 199,159 shares of common stock at the closing price on December 27, 2018 of $0.92 per share.

During the nine months ended January 31, 2019, the Company has recorded $1,136,458 to the condensed consolidated statements of operations relating to common stock issued for services. A balance of $311,915 remains to be expensed over future vesting periods.

Stock options issued for services

On December 21, 2017, the Company issued four employees an aggregate of 925,000 common stock options for services, having a total fair value of approximately $878,000. 231,250 of the options vest immediately, 231,250 vest on December 21, 2018, 231,250 vest on December 21, 2019 and 231,250 vest on December 21, 2020. These options expire on December 21, 2022. These options have an exercise price of $1.47 per share. Of these options, 37,500 unvested options were forfeited with the departure of an employee on May 1, 2018.

On December 21, 2017, the Company issued four board members an aggregate of 200,000 common stock options for services, having a total fair value of approximately $170,000. 100,000 of the options vest immediately and 100,000 vest on December 21, 2018. These options expire on December 21, 2022. These options have an exercise price of $1.47 per share.

On December 21, 2017, the Company issued three consultants an aggregate of 75,000 common stock options for services, having a total grant date fair value of approximately $76,000. 18,750 of the options vest immediately, 18,750 vest on December 21, 2018, 18,750 vest on December 21, 2019 and 18,750 vest on December 21, 2020. These options expire on December 21, 2022. These options have an exercise price of $1.47 per share.

On April 10, 2018, the Company issued our Chief Financial Officer (“CFO”) 50,000 common stock options for services, having a total fair value of approximately $52,000. 12,500 of the options vest immediately, 12,500 were to vest on April 9, 2019, 12,500 were to vest on April 9, 2020 and 12,500 were to vest on April 9, 2021. These options expire on April 9, 2023. These options have an exercise price of $1.49 per share. Of these options, 37,500 unvested options were forfeited with the departure of the CFO on December 31, 2018.

On April 16, 2018, the Company issued an employee 50,000 common stock options for services, having a total fair value of approximately $47,000. 12,500 of the options vest on July 15, 2018, 12,500 vest on April 16, 2019, 12,500 vest on April 16, 2020 and 12,500 vest on April 16, 2021. These options expire on April 16, 2023. These options have an exercise price of $1.34 per share.

| 18 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

Stock Options

A summary of the Company’s outstanding stock options as of January 31, 2019 and changes during the period then ended are presented below:

| Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (Years) | ||||||||||

| Balance at April 30, 2018 | 1,531,458 | $ | 1.79 | 4.43 | ||||||||

| Granted | — | — | — | |||||||||

| Exercised | — | — | — | |||||||||

| Forfeited | (75,000 | ) | 1.48 | — | ||||||||

| Canceled | — | — | — | |||||||||

| Balance at January 31, 2019 | 1,456,458 | 1.80 | 3.67 | |||||||||

| Options exercisable at end of period | 943,958 | $ | 2.28 | |||||||||

| Options expected to vest | 512,500 | $ | 1.47 | |||||||||

| Weighted average fair value of options granted during the period | $ | — | ||||||||||

At January 31, 2019, the aggregate intrinsic value of options outstanding and exercisable was $0 and $0, respectively.

At April 30, 2018, the aggregate intrinsic value of options outstanding and exercisable was $1,000 and $0, respectively.

Stock-based compensation for stock options has been recorded in the unaudited condensed consolidated statements of operations and totaled $205,726 for the nine months ended January 31, 2019 and $0 for nine months ended January 31, 2018.

Stock Warrants

A summary of the Company’s outstanding stock warrants as of January 31, 2019 and changes during the period then ended are presented below:

| Number of Warrants | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (Years) | ||||||||||

| Balance at April 30, 2018 | 1,702,359 | $ | 3.12 | 3.25 | ||||||||

| Granted | — | — | — | |||||||||

| Exercised | — | — | — | |||||||||

| Forfeited | — | — | — | |||||||||

| Canceled | — | — | — | |||||||||

| Balance at January 31, 2019 | 1,702,359 | $ | 3.12 | 2.49 | ||||||||

| Warrants exercisable at end of period | 1,702,359 | $ | 3.12 | |||||||||

| Weighted average fair value of warrants granted during the period | $ | — | ||||||||||

All warrants as of January 31, 2019 are fully vested.

At January 31, 2019, the aggregate intrinsic value of warrants outstanding and exercisable was $0 and $0, respectively. At April 30, 2018, the aggregate intrinsic value of warrants outstanding and exercisable was $0 and $0, respectively. A balance of $1,137,249 remains to be expensed over future vesting periods.

| 19 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

NOTE 10 — NET LOSS PER COMMON SHARE

Net loss per common share is calculated in accordance with ASC 260, “Earnings Per Share”. Basic loss per share is computed by dividing net loss available to common stockholder, by the weighted average number of shares of common stock outstanding during the period. The following were excluded from the computation of diluted shares outstanding as they would have had an anti-dilutive impact on the Company’s net loss. In periods where the Company has a net loss, all dilutive securities are excluded.

| January 31, 2019 | April 30, 2018 | |||||||

| Common stock equivalents: | ||||||||

| Restricted Stock | 524,500 | - | ||||||

| Stock options | 1,456,458 | 1,531,458 | ||||||

| Stock warrants | 1,702,359 | 1,702,359 | ||||||

| Total | 3,796,317 | 3,233,817 | ||||||

NOTE 11 — COMMITMENTS AND CONTINGENCIES

Mining Leases

The Copper King property position consists of two State of Wyoming Metallic and Non-metallic Rocks and Minerals Mining Leases. These leases were assigned to the Company in July 2014 through the acquisition of the Copper King project.

The Company’s rights to the Copper King Project arise under two State of Wyoming mineral leases:

1) State of Wyoming Mining Lease No. 0-40828 consisting of 640 acres.

2) State of Wyoming Mining Lease No. 0-40858 consisting of 480 acres.

Total lease expense for the nine-month periods ended January 31, 2019 and 2018 was $2,240 and $2,240, respectively.

Lease 0-40828 was renewed in February 2013 for a second ten-year term and Lease 0-40858 was renewed for its second ten-year term in February 2014. Each lease requires an annual payment of $2.00 per acre. In connection with the Wyoming Mining Leases, the following production royalties must be paid to the State of Wyoming, although once the project is in operation, the Board of Land Commissioners has the authority to reduce the royalty payable to the State:

| FOB Mine Value per Ton | Percentage Royalty | |||

| $00.00 to $50.00 | 5 | % | ||

| $50.01 to $100.00 | 7 | % | ||

| $100.01 to $150.00 | 9 | % | ||

| $150.01 and up | 10 | % | ||

The future minimum lease payments under these mining leases are as follows:

| 2019 (remainder of year) | $ | 840 | ||

| 2020 | 2,240 | |||

| 2021 | 2,240 | |||

| 2022 | 2,240 | |||

| 2023 | 2,240 | |||

| Thereafter | 960 | |||

| $ | 10,760 |

The Company may renew the lease for a third ten-year term which will require an annual payment of $3.00 per acre and then $4.00 per acre thereafter.

| 20 |

U.S. GOLD CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2019 and 2018

Executive Employment Agreements

On October 29, 2018, the Company and Mr. Karr executed an employment agreement (the “Karr Employment Agreement”). The material terms of the Karr Employment Agreement include: (i) an annual base salary of $250,000; (ii) eligibility to earn an annual incentive bonus of up to 100% of Mr. Karr’s base salary, payable in cash or stock at Mr. Karr’s discretion; (iii) eligibility to participate in any long term incentive plan adopted by the Company; and (iv) eligibility to participate in any Company employee benefit plans. Mr. Karr is also subject to non-solicitation and confidentiality provisions set forth in the Karr Employment Agreement.

On October 29, 2018, the Company and Mr. Rector executed an employment agreement (the “Rector Employment Agreement”). The material terms of the Rector Employment Agreement include: (i) an annual base salary of $180,000; (ii) eligibility to earn an annual incentive bonus of up to 100% of Mr. Rector’s base salary, payable in cash or stock at Mr. Rector’s discretion; (iii) eligibility to participate in any long term incentive plan adopted by the Company; and (iv) eligibility to participate in any Company employee benefit plans. Mr. Rector is also subject to non-solicitation and confidentiality provisions set forth in the Rector Employment Agreement.

On June 27, 2016, the Company entered into an employment agreement with its Chief Geologist, Mr. David Mathewson. The initial term of the agreement is for one year, with automatic renewals for successive one-year terms unless terminated by written notice at least 30 days prior to the expiration of the term by either party. Mr. Mathewson is to receive a base salary of $200,000 per year. The base salary shall be payable as follows: (a) 25% of the base salary shall be payable in equal monthly cash installments and (b) the remaining 75% of the base salary shall be payable in equal monthly installments in the form of common stock of the Company. Each installment of common stock shall be issued on the first business day of the months and shall be valued at the market price on the trading day immediately prior to the date of issuance. Market price is the closing bid price on the principal securities exchange or trading market. Mr. Mathewson shall be entitled to receive bonus to be paid in cash, stock, or a combination thereof and equity awards.

NOTE 12 — SUBSEQUENT EVENTS

On February 19, 2019, the Company entered into contracts with investor relations firms under which it will be required to pay for services in cash and shares of the Company’s common stock. One agreement is for a six-month term and two agreements are for twelve months. A total of 155,951 shares were issued at a fair value of $160,630 based on the closing price of $1.03 on February 19, 2019 to satisfy the equity component of the agreements.

On February 4, 2019, the Company issued 12,626 shares of common stock to satisfy a stock payable to an employee for services rendered during the quarter ended January 31, 2019. The shares were valued at $12,500 using a share price of $0.99 on the date of issue.

In March 2019, the Company sold 54,995 common shares and raised a net of $45,932, net of issuance costs, through the ATM Agreement at $0.87 per share.

| 21 |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This Quarterly Report on Form 10-Q contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Many of the forward-looking statements are located in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Forward-looking statements can also be identified by words such as “future,” “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “will,” “would,” “could,” “can,” “may,” and similar terms. Forward-looking statements are not guarantees of future performance and the Company’s actual results may differ significantly from the results discussed in the forward-looking statements. Factors that might cause such differences include, but are not limited to, those discussed under the heading “Risk Factors” in Part I, Item 1A of the Company’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “Commission”) which can be reviewed at http://www.sec.gov. The Company assumes no obligation to revise or update any forward-looking statements for any reason, except as required by law.

The interim unaudited consolidated financial statements included herein have been prepared by U.S. Gold Corp. (the “Company”) without audit, pursuant to the rules and regulations of the Commission. Certain information and footnote disclosure normally included in interim unaudited consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) which are duplicate to the disclosures in the audited consolidated financial statement have been omitted pursuant to such rules and regulations, although the Company believes that the disclosures are adequate to make the information presented not misleading. These interim unaudited condensed consolidated financial statements should be read in conjunction with the financial statements and notes thereto in the Form 10-K filed with the Commission on July 30, 2018.

In the opinion of management, all adjustments have been made consisting of normal recurring adjustments and consolidating entries, necessary to present fairly the unaudited interim condensed consolidated financial position of the Company and subsidiaries as of January 31, 2019, the results of their unaudited interim condensed consolidated statements of operations for the nine-month periods ended January 31, 2019 and 2018, and their unaudited interim condensed consolidated cash flows for the nine-month periods ended January 31, 2019 and 2018. The results of unaudited interim condensed consolidated operations for the interim periods are not necessarily indicative of the results for the full year.