Exhibit 99.1

INVESTOR PRESENTATION Quarter Ended June 30, 2022

SAFE HARBOR STATEMENT In this presentation, we make certain statements and reference other information that are “forward - looking statements” as define d in the Private Securities Litigation Reform Act of 1995 (“PSLRA”). The PSLRA provides a safe harbor under the Securities Act of 193 3, as amended, and the Securities Exchange Act of 1934, as amended, for forward - looking statements that relate to our intentions, beliefs, proj ections, estimations, or forecasts of future events or our future financial performance. Forward - looking statements involve known and un known risks, uncertainties, and other factors that may result in materially differing actual results. We can give no assurance that our e xpe ctations expressed in forward - looking statements will prove to be correct. Factors that could cause our actual results to differ materially from those projected, forecasted, or estimated by us in forw ard - looking statements are discussed in further detail in Selective’s public filings with the United States Securities and Exchange Commi ssi on. We undertake no obligation to publicly update or revise any forward - looking statements – whether as a result of new information, fu ture events or otherwise – other than as the federal securities laws may require. This presentation also includes certain non - GAAP financial measures within the meaning of Regulation G, including “non - GAAP oper ating earnings per share,” “non - GAAP operating income,” and “non - GAAP operating return on equity.” Definitions of these non - GAAP meas ures and a reconciliation to the most comparable GAAP figures pursuant to Regulation G are available in our Annual Report on Form 10 - K an d our Supplemental Investor Package, which can be found on our website < www.selective.com > under “Investors/Reports, Earnings and Presentations.” We believe investors and other interested persons find these measurements beneficial and useful. We have co nsi stently provided these financial measurements in previous investor communications so they have a consistent basis for comparing our r esu lts between quarters and with our industry competitors. These non - GAAP measures, however, may not be comparable to similarly titled measures used outside of the insurance industry. Investors are cautioned not to place undue reliance on these non - GAAP measures in assessing our overall financial performance. 2

OVERVIEW 3

4 2021 Non - GAAP Operating ROE of 14.3%* State Footprint ** 28 Market Cap (as of 9 /6 /2022 ) $4.8B Years of Financial Strength and Superior Execution 95+ 2021 NPW ( up 15% Y/Y ) $3.2B 2021 GAAP Combined Ratio 92.8% A TRACK RECORD OF SUPERIOR EXECUTION An Eight - Year Track Record of Double - Digit Non - GAAP Operating ROEs* and Above Average Industry Growth *Refer to “Safe Harbor Statement” on page 2 of this presentation for further detail regarding certain non - GAAP financial measure s. **State Footprint refers to Commercial Lines only and includes D.C.

OUR SUSTAINABLE COMPETITIVE ADVANTAGES Competitive Position Enhanced by Working Towards the Benefit of all our Stakeholders • Appointment of high - quality independent agent distribution partners with whom we have close relationships • Enables effective management of pricing and retention • Presents significant opportunity for profitable growth • Locally - based underwriting, claims, and safety management specialists • Claims specialists regionally organized by specialty • Enables high - touch approach for customer and agency service • Total attention to customer experience • Developing holistic solutions for 24 - hour omni - channel shared experience • Increased customer engagement • Value - added services Distribution model emphasizing franchise value with high - quality partners Superior omni - channel customer experience Unique locally - based field model S ophisticated tools for risk selection, pricing, and claims management • Our ability to develop and integrate these tools gives us confidence in effectively managing profitability in a more uncertain loss trend environment 5

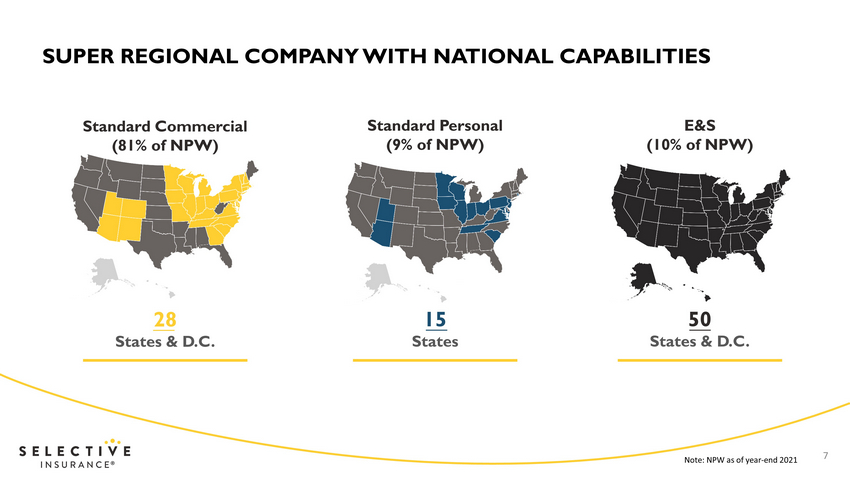

SUMMARY OF OUR OPERATIONS • Focus on disciplined growth • Strong calendar year profitability; Commercial Auto remains an area of focus • Strong new business growth, higher retention, solid renewal pure price increases, and exposure growth • Greater prospective loss trend uncertainty • Competitive dynamics hurting personal auto growth, but market turning • Shifted focus to “mass - affluent” market, where we believe we can be more competitive with our strong coverage and servicing capabilities • Fourth largest “Write Your Own” National Flood Insurance Program writer • Significant loss severity pressure from inflationary forces • Focus on achieving target combined ratio; top - line will depend on market conditions • “E&S light” product mix • Margin improvement through targeted price increases, exiting challenged segments, and claim improvements • Attractive market tailwinds supporting growth Commercial Lines (81% of NPW) Excess & Surplus (10% of NPW) Personal Lines ( 9 % of NPW) Note: NPW as of year - end 2021 6

SUPER REGIONAL COMPANY WITH NATIONAL CAPABILITIES Standard Commercial (81% of NPW) Standard Personal (9% of NPW) E&S (10% of NPW) 28 States & D.C. 15 States 50 States & D.C. Note: NPW as of year - end 2021 7

STRONG ROE OUTPERFORMANCE RELATIVE TO PEERS • 12.1% non - GAAP operating ROE* in 1H 2022 driven by: ̶ Solid underwriting profitability ̶ Manageable CAT losses ̶ Strong investment contribution • Track record of generating ROEs well in excess of our cost of capital and peer group averages 10.3% 8.6% 12.1% 11.3% 0% 5% 10% 15% 2014 2015 2016 2017 2018 2019 2020 2021 1H22 SIGI Peer Avg. Elevated CAT losses Peer index includes TRV, HIG, CNA, CINF, THG, and UFCS Eight consecutive years of double - digit non - GAAP operating ROEs* averaging 11.9% between 2014 and 2021 Historical Non - GAAP Operating ROEs* * Refer to “Safe Harbor Statement” on page 2 of this presentation for further detail regarding certain non - GAAP financial measur es. 8

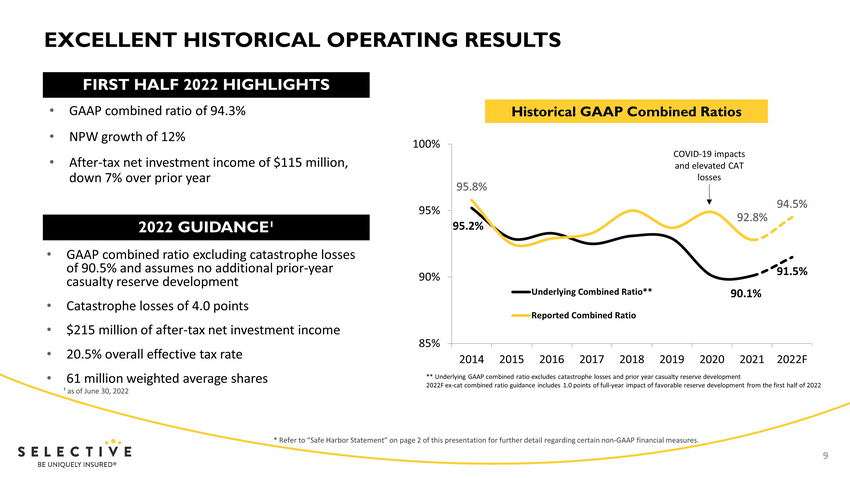

EXCELLENT HISTORICAL OPERATING RESULTS • GAAP combined ratio of 94.3% • NPW growth of 12% • After - tax net investment income of $115 million, down 7% over prior year 95.2% 90.1% 91.5% 85% 90% 95% 100% 2014 2015 2016 2017 2018 2019 2020 2021 2022F Underlying Combined Ratio** Reported Combined Ratio COVID - 19 impacts and elevated CAT losses Historical GAAP Combined Ratios 2022 GUIDANCE¹ • GAAP combined ratio excluding catastrophe losses of 90.5% and assumes no additional prior - year casualty reserve development • Catastrophe losses of 4.0 points • $215 million of after - tax net investment income • 20.5% overall effective tax rate • 61 million weighted average shares ** Underlying GAAP combined ratio excludes catastrophe losses and prior year casualty reserve development 2022F ex - cat combined ratio guidance includes 1.0 points of full - year impact of favorable reserve development from the first hal f of 2022 FIRST HALF 2022 HIGHLIGHTS * Refer to “Safe Harbor Statement” on page 2 of this presentation for further detail regarding certain non - GAAP financial measur es. ¹ as of June 30, 2022 9

OUR STRATEGIC INITIATIVES 10

OUR MAJOR STRATEGIC INITIATIVES Deploy sophisticated underwriting and pricing tools to achieve price increases ≥ loss trends Expanding “share of wallet” and new agent appointments; geo - expansion Continue to deliver superior omni - channel customer experience CONTINUED PROFITABLE GROWTH LEVERAGE SOPHISTICATED TOOLS TO ACHIEVE ADEQUATE PRICING EXCELLENT CUSTOMER SERVICE CULTURE FOCUSED ON INNOVATION AND SUSTAINABILITY A culture of innovation and sustainability, centered around diversity, equity, and inclusion 11

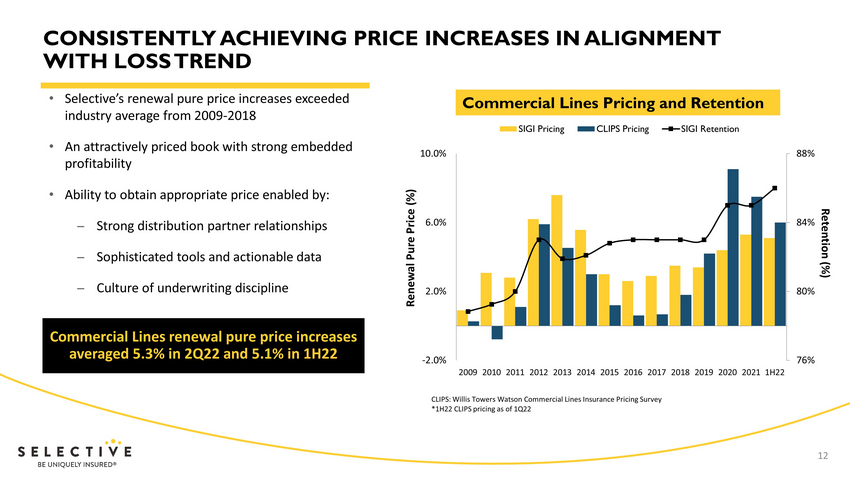

CONSISTENTLY ACHIEVING PRICE INCREASES IN ALIGNMENT WITH LOSS TREND • Selective’s renewal pure price increases exceeded industry average from 2009 - 2018 • An attractively priced book with strong embedded profitability • Ability to obtain appropriate price enabled by: ̶ Strong distribution partner relationships ̶ Sophisticated tools and actionable data ̶ Culture of underwriting discipline 76% 80% 84% 88% -2.0% 2.0% 6.0% 10.0% 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 1H22 SIGI Pricing CLIPS Pricing SIGI Retention Renewal Pure Price (%) Commercial Lines renewal pure price increases averaged 5.3 % in 2Q22 and 5.1% in 1H22 Commercial Lines Pricing and Retention CLIPS: Willis Towers Watson Commercial Lines Insurance Pricing Survey *1H22 CLIPS pricing as of 1Q22 Retention (%) 12

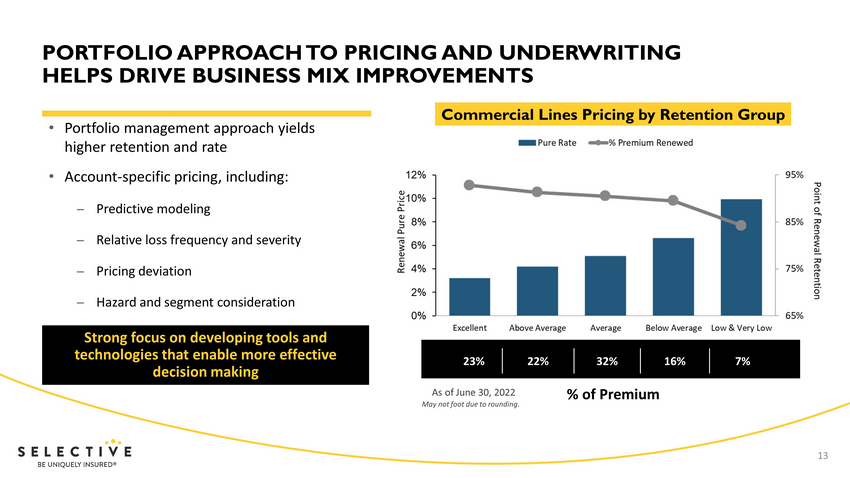

PORTFOLIO APPROACH TO PRICING AND UNDERWRITING HELPS DRIVE BUSINESS MIX IMPROVEMENTS Commercial Lines Pricing by Retention Group % of Premium As of June 30 , 2022 May not foot due to rounding. Strong focus on developing tools and technologies that enable more effective decision making • Portfolio management approach yields higher retention and rate • Account - specific pricing, including: ̶ Predictive modeling ̶ Relative loss frequency and severity ̶ Pricing deviation ̶ Hazard and segment consideration 23% 22% 32% 16% 7% 13

TARGETING PROFITABLE GROWTH OVER TIME Historical Net Premiums Written • Target of growing “share of wallet” to 12% with existing distribution partners • Target of appointments to represent 25% share in existing markets • Geo - expansion • New products and M&A Additional NPW opportunity of about $3B by achieving a 3% commercial lines market share in existing footprint LOWER RISK HIGHER RISK Commercial Lines Growth Drivers 7% NPW CAGR from 2013 - 2021 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 $0B Managed Premium Volume During Soft Market $3.5B 14

INITIATIVES FOCUSED ON PROFITABLE GROWTH Shifting Personal Lines focus towards “mass affluent” market, where we believe we can be more competitive with our strong coverage and servicing capabilities MarketMax ® provides our distribution partners with insights into their portfolio and positions them to expand their relationship with us E&S automation platform enhances competitive position New small business agency interface enhances opportunities by significantly streamlining quoting and issuance process 15

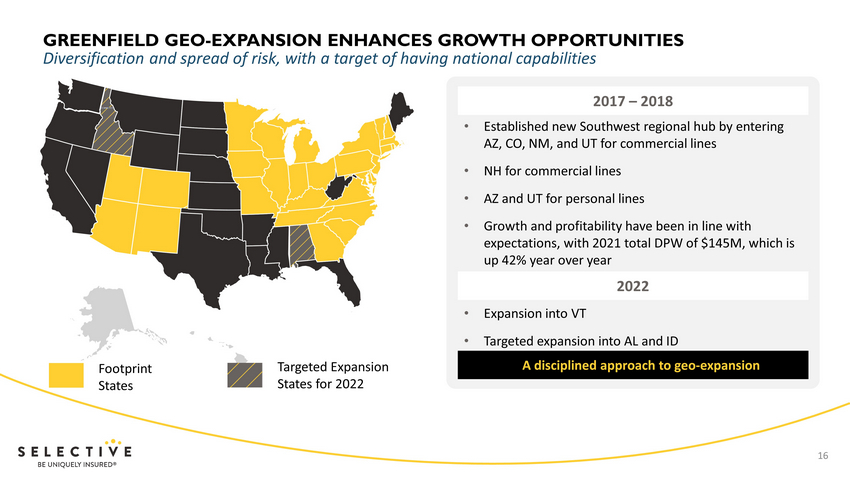

Diversification and spread of risk, with a target of having national capabilities GREENFIELD GEO - EXPANSION ENHANCES GROWTH OPPORTUNITIES A disciplined approach to geo - expansion Footprint States Targeted Expansion States for 2022 2017 – 2018 • Established new Southwest regional hub by entering AZ, CO, NM, and UT for commercial lines • NH for commercial lines • AZ and UT for personal lines • Growth and profitability have been in line with expectations, with 2021 total DPW of $145M, which is up 42% year over year 2022 • Expansion into VT • Targeted expansion into AL and ID 16

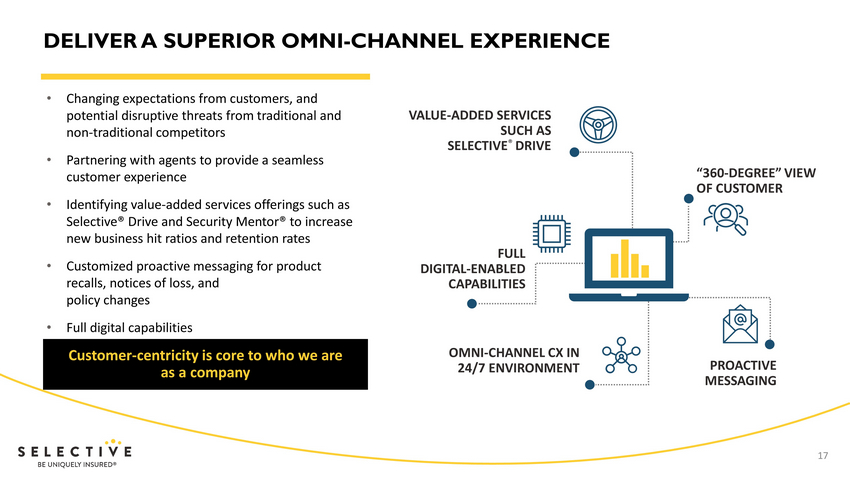

Customer - centricity is core to who we are as a company DELIVER A SUPERIOR OMNI - CHANNEL EXPERIENCE “360 - DEGREE” VIEW OF CUSTOMER PROACTIVE MESSAGING VALUE - ADDED SERVICES SUCH AS SELECTIVE ® DRIVE FULL DIGITAL - ENABLED CAPABILITIES OMNI - CHANNEL CX IN 24/7 ENVIRONMENT • Changing expectations from customers, and potential disruptive threats from traditional and non - traditional competitors • Partnering with agents to provide a seamless customer experience • Identifying value - added services offerings such as Selective® Drive and Security Mentor® to increase new business hit ratios and retention rates • Customized proactive messaging for product recalls, notices of loss, and policy changes • Full digital capabilities 17

DEVELOPING LEADERSHIP IN ENVIRONMENTAL, SOCIAL, AND GOVERNANCE DISCLOSURES A Culture of Strong Governance and Transparency Understanding and Attempting to Mitigate Climate Change Risk Providing Customers with Empathetic Claims Services and Risk Mitigation Solutions Building a Highly Engaged Team of Employees and Leaders Having a Positive Impact on our Communities and Society DRIVING SUSTAINABLE IMPACT Risk oversight and mitigation Capital allocation away from specific environmentally hazardous risks Reducing our carbon footprint Responsive claims service Seamless omni - channel customer experience Value - added tools and technologies to help mitigate customer risk Strong focus on attracting, retaining, and promoting the best talent Emphasis on workplace flexibility Significant initiatives to advance DE&I Financial contributions through The Selective Insurance Group Foundation Investing in strengthening our communities Sustainability Committee overseen by senior management and Corporate Governance and Nominating Committee of the Board Diverse and engaged Board with strong oversight of key areas 18

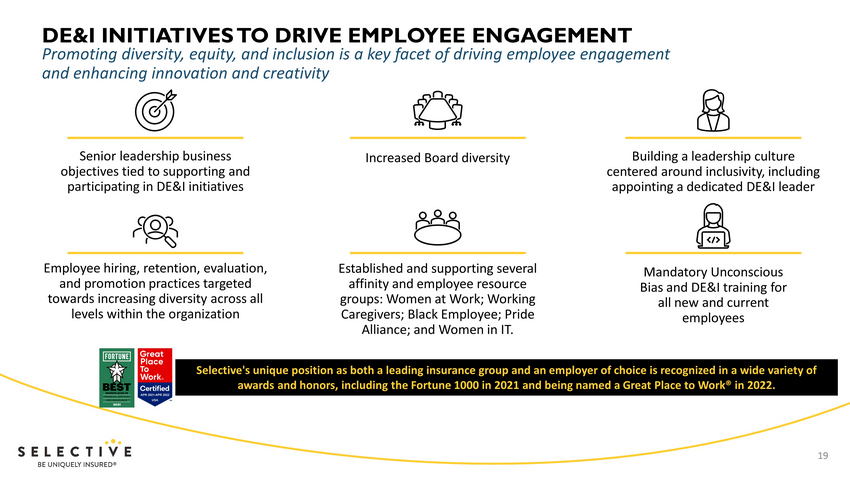

DE&I INITIATIVES TO DRIVE EMPLOYEE ENGAGEMENT Increased Board diversity Building a leadership culture centered around inclusivity, including appointing a dedicated DE&I leader Employee hiring, retention, evaluation, and promotion practices targeted towards increasing diversity across all levels within the organization Senior leadership business objectives tied to supporting and participating in DE&I initiatives Established and supporting several affinity and employee resource groups: Women at Work; Working Caregivers; Black Employee; Pride Alliance; and Women in IT. Mandatory Unconscious Bias and DE&I training for all new and current employees Promoting diversity, equity, and inclusion is a key facet of driving employee engagement and enhancing innovation and creativity Selective's unique position as both a leading insurance group and an employer of choice is recognized in a wide variety of awards and honors, including the Fortune 1000 in 2021 and being named a Great Place to Work® in 2022. 19

FINANCIAL OVERVIEW 20

LOWER RISK PROFILE AND STRONG FINANCIAL STRENGTH A LOWER RISK PROFILE • Strong balance sheet underpinned by a conservative approach to: ̶ Managing the investment portfolio ̶ Purchasing reinsurance protection ̶ Loss reserving • Conservative business and balance sheet profile allows for higher operating leverage • Financial strength rating was upgraded to A+ by AM Best in November 2021 Low to Medium Hazard Writer AM Best A+ S&P A Moody’s A2 Fitch A+ 21

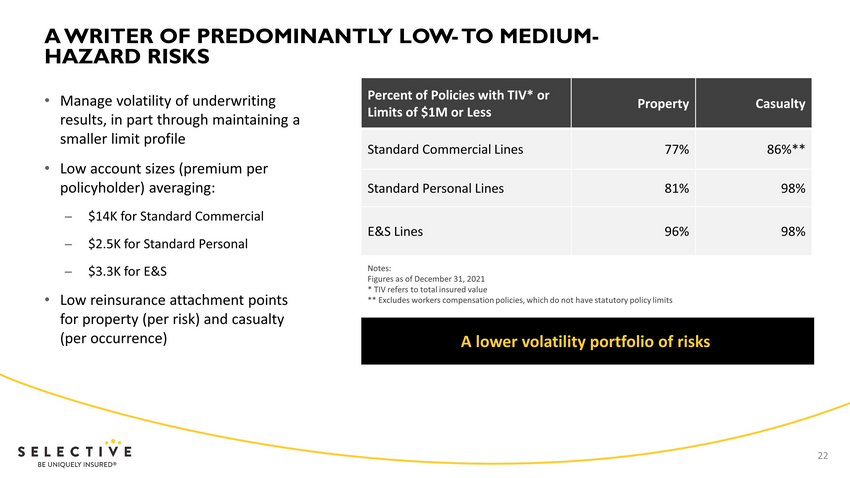

A WRITER OF PREDOMINANTLY LOW - TO MEDIUM - HAZARD RISKS A lower volatility portfolio of risks Percent of Policies with TIV* or Limits of $1M or Less Property Casualty Standard Commercial Lines 77% 86%** Standard Personal Lines 81% 98% E&S Lines 96% 98% Notes: Figures as of December 31, 2021 * TIV refers to total insured value ** Excludes workers compensation policies, which do not have statutory policy limits • Manage volatility of underwriting results, in part through maintaining a smaller limit profile • Low account sizes (premium per policyholder) averaging: ̶ $14K for Standard Commercial ̶ $2.5K for Standard Personal ̶ $3.3K for E&S • Low reinsurance attachment points for property (per risk) and casualty (per occurrence) 22

Fixed Income 87% Short-Term 4% Equities 3% Alternatives & Other 6% CONSERVATIVE INVESTMENT PORTFOLIO Investment Portfolio at 6 /30/22 $7.6B of Investments • Core fixed income and short - term investments comprise 91 % of the investment portfolio in 2Q22: ̶ “A+” average credit quality ̶ Effective duration of 4 .1 years • Risk asset allocation (high yield, public equity, and alternatives) at 10.9 % of invested assets • Ongoing work to further diversify our alternative investments portfolio by strategy and vintage A conservative investment management philosophy, with a focus on highly rated fixed income securities 23

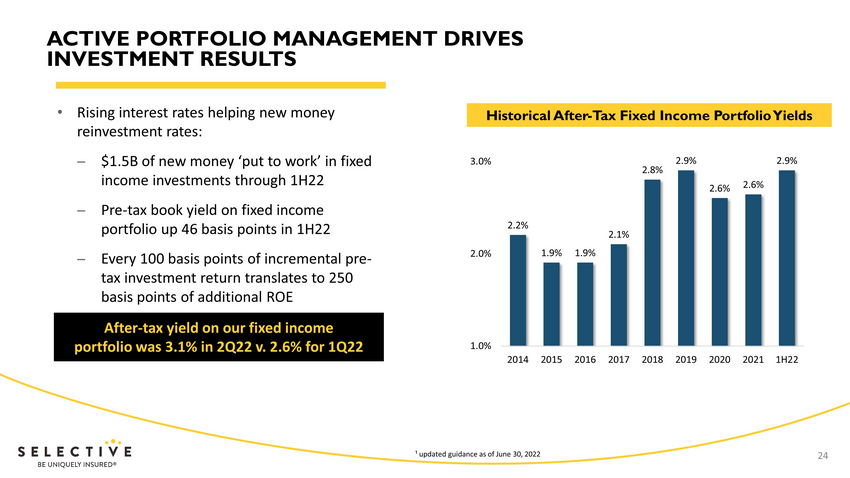

ACTIVE PORTFOLIO MANAGEMENT DRIVES INVESTMENT RESULTS • Rising interest rates helping new money reinvestment rates : ̶ $1.5B of new money ‘put to work’ in fixed income investments through 1H22 ̶ Pre - tax book yield on fixed income portfolio up 46 basis points in 1H22 ̶ Every 100 basis points of incremental pre - tax investment return translates to 250 basis points of additional ROE 2.2% 1.9% 1.9% 2.1% 2.8% 2.9% 2.6% 2.6% 2.9% 1.0% 2.0% 3.0% 2014 2015 2016 2017 2018 2019 2020 2021 1H22 After - tax yield on our fixed income portfolio was 3.1% in 2Q22 v. 2.6% for 1Q22 Historical After - Tax Fixed Income Portfolio Yields ¹ updated guidance as of June 30, 2022 24

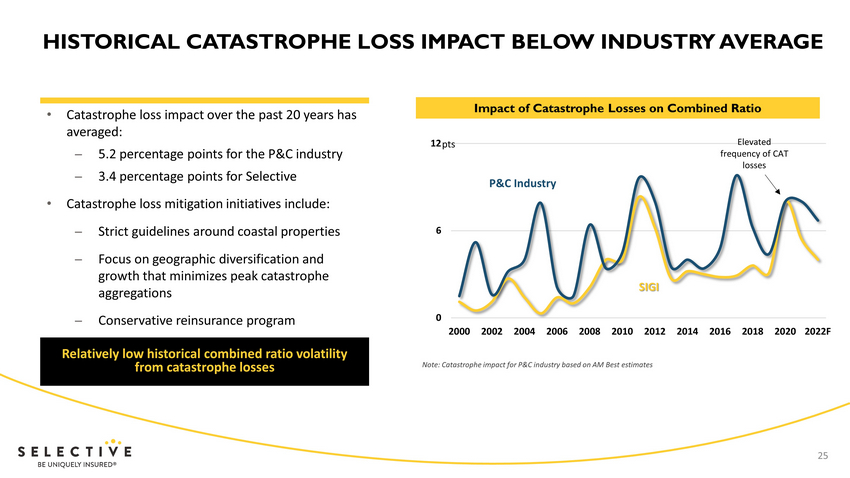

Relatively low historical combined ratio volatility from catastrophe losses HISTORICAL CATASTROPHE LOSS IMPACT BELOW INDUSTRY AVERAGE Impact of Catastrophe Losses on Combined Ratio Note: Catastrophe impact for P&C industry based on AM Best estimates • Catastrophe loss impact over the past 20 years has averaged: ̶ 5.2 percentage points for the P&C industry ̶ 3.4 percentage points for Selective • Catastrophe loss mitigation initiatives include: ̶ Strict guidelines around coastal properties ̶ Focus on geographic diversification and growth that minimizes peak catastrophe aggregations ̶ Conservative reinsurance program 0 6 12 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022F Elevated frequency of CAT losses P&C Industry pts SIGI 25

Balance sheet protection through conservative program and strong panel of reinsurance partners CONSERVATIVE REINSURANCE PROGRAM 1% 1% 1% 2% 2% 4% 15% 0% 6% 12% 18% 25 50 100 150 200 250 500 (Return Period in Years) Net Single - Event Hurricane Loss* as a % of Equity * Single event hurricane losses are net of reinsurance, after tax, and reinstatement premiums as of 1/1/22. GAAP equity as of 12/31/21. • 2022 property catastrophe treaty structure: ̶ Coverage of $835M in excess of $40M retention ̶ $259M in collateralized limit, primarily in the top layer of the program ̶ Additional earnings volatility protection from our non - footprint $30M in excess of $10M layer • Property XOL treaty covers losses up to $ 67 M in excess of $3M retention on a per risk basis • Casualty XOL treaty covers losses up to $88M in excess of $2M retention on a per occurrence basis 26

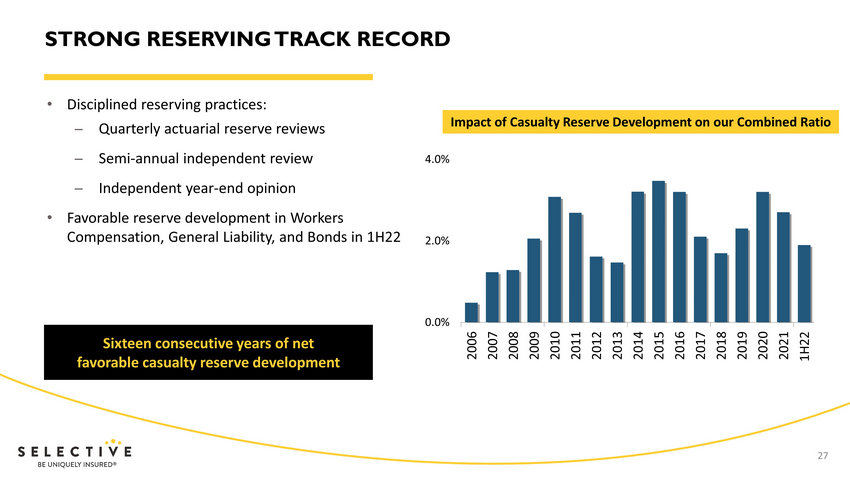

Sixteen consecutive years of net favorable casualty reserve development STRONG RESERVING TRACK RECORD • Disciplined reserving practices: ̶ Quarterly actuarial reserve reviews ̶ Semi - annual independent review ̶ Independent year - end opinion • Favorable reserve development in Workers Compensation, General Liability, and Bonds in 1H22 Impact of Casualty Reserve Development on our Combined Ratio 0.0% 2.0% 4.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 1H22 27

28 • Expecting expense ratio improvement over the next few years Areas for operational enhancements include: • Workflow and process improvements • Robotics and artificial intelligence • Talent development • Product innovation STRONG CAPITAL AND LIQUIDITY POSITION, GREATER FOCUS ON EXPENSES EXPENSE MANAGEMENT • Debt - to - capital ratio of 16.3% • NPW to surplus ratio of ~1.41x at low end of our target range of 1.35x – 1.55x • Parent company cash and investments totaling ~$510M is well in excess of our target of 2x annual recurring outflow • Instituted opportunistic $100M share repurchase authorization • Investing in the business currently provides the most attractive capital deployment opportunities CAPITAL AND LIQUIDITY PLAN Note: Financial statistics are as of June 30 , 2022

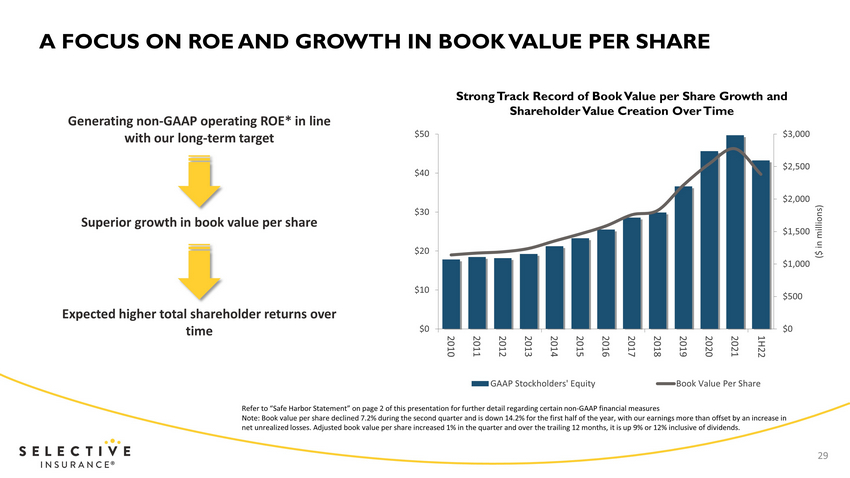

A FOCUS ON ROE AND GROWTH IN BOOK VALUE PER SHARE Strong Track Record of Book Value per Share Growth and Shareholder Value Creation Over Time Generating non - GAAP operating ROE* in line with our long - term target Superior growth in book value per share Expected higher total shareholder returns over time Refer to “Safe Harbor Statement” on page 2 of this presentation for further detail regarding certain non - GAAP financial measures Note: Book value per share declined 7.2% during the second quarter and is down 14.2% for the first half of the year, with our ea rnings more than offset by an increase in net unrealized losses. Adjusted book value per share increased 1% in the quarter and over the trailing 12 months, it is up 9% or 12% inclusive of dividends. $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $0 $10 $20 $30 $40 $50 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 ($ in millions) GAAP Stockholders' Equity Book Value Per Share 29 1H22

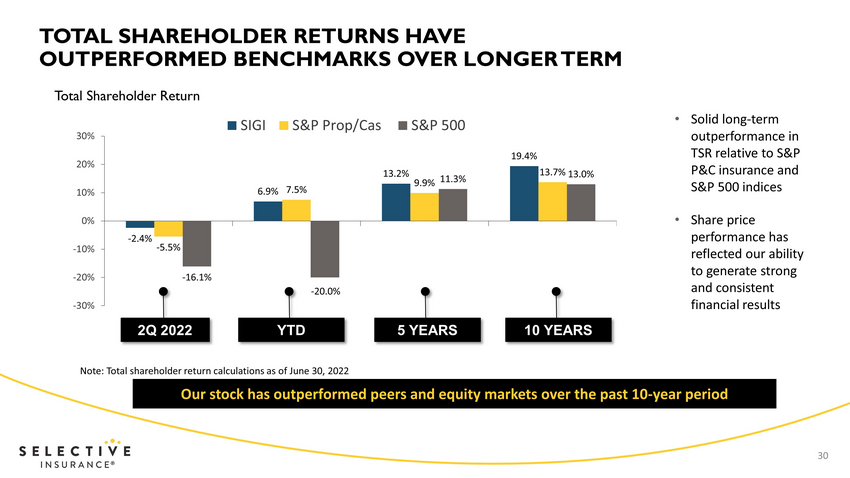

30 TOTAL SHAREHOLDER RETURNS HAVE OUTPERFORMED BENCHMARKS OVER LONGER TERM Total Shareholder Return • Solid long - term outperformance in TSR relative to S&P P&C insurance and S&P 500 indices • Share price performance has reflected our ability to generate strong and consistent financial results Our stock has outperformed peers and equity markets over the past 10 - year period Note: Total shareholder return calculations as of June 30, 2022 - 2.4% 6.9% 13.2% 19.4% - 5.5% 7.5% 9.9% 13.7% - 16.1% - 20.0% 11.3% 13.0% -30% -20% -10% 0% 10% 20% 30% SIGI S&P Prop/Cas S&P 500 2Q 2022 YTD 5 YEARS 10 YEARS

OUR VALUE PROPOSITION A distribution model that emphasizes franchise value, meaning we focus on appointing high - quality independent distribution partners with whom we have meaningful and close business relationships Unique field model enabled by sophisticated technology Strong customer experience * Refer to “Safe Harbor Statement” on page 2 of this presentation for further detail regarding certain non - GAAP financial measur es Leveraging our competitive strengths to generate sustained financial outperformance Excellent growth opportunities within footprint and geo - expansion Solid underwriting margins and non - GAAP operating ROEs* in line with our financial targets Conservative approach to risk selection and balance sheet management 31