| Business Combination Agreement and such Order or other action shall have become final and non-appealable; or |

| • | by either MAC or DePalma, if the Acquiror Shareholders Meeting has been held (including any adjournment or postponement thereof), has concluded, MAC’s stockholders have duly voted and the Acquiror Shareholder Approvals were not obtained. |

In the event of termination of the Business Combination Agreement, the Business Combination Agreement will become void (and there shall be no liability or obligation on the part of the parties and their respective non-party affiliates), with the exception of the parties’ confidentiality obligations, and certain other provisions required under the Business Combination Agreement that shall, in any case, survive any termination of the Business Combination Agreement; provided, however, that termination of the Business Combination Agreement in accordance with its terms shall not relieve any party from liability for any intentional and Willful Breach (as defined in the Business Combination Agreement) of any covenant or agreement set forth in the Business Combination Agreement prior to such termination or fraud.

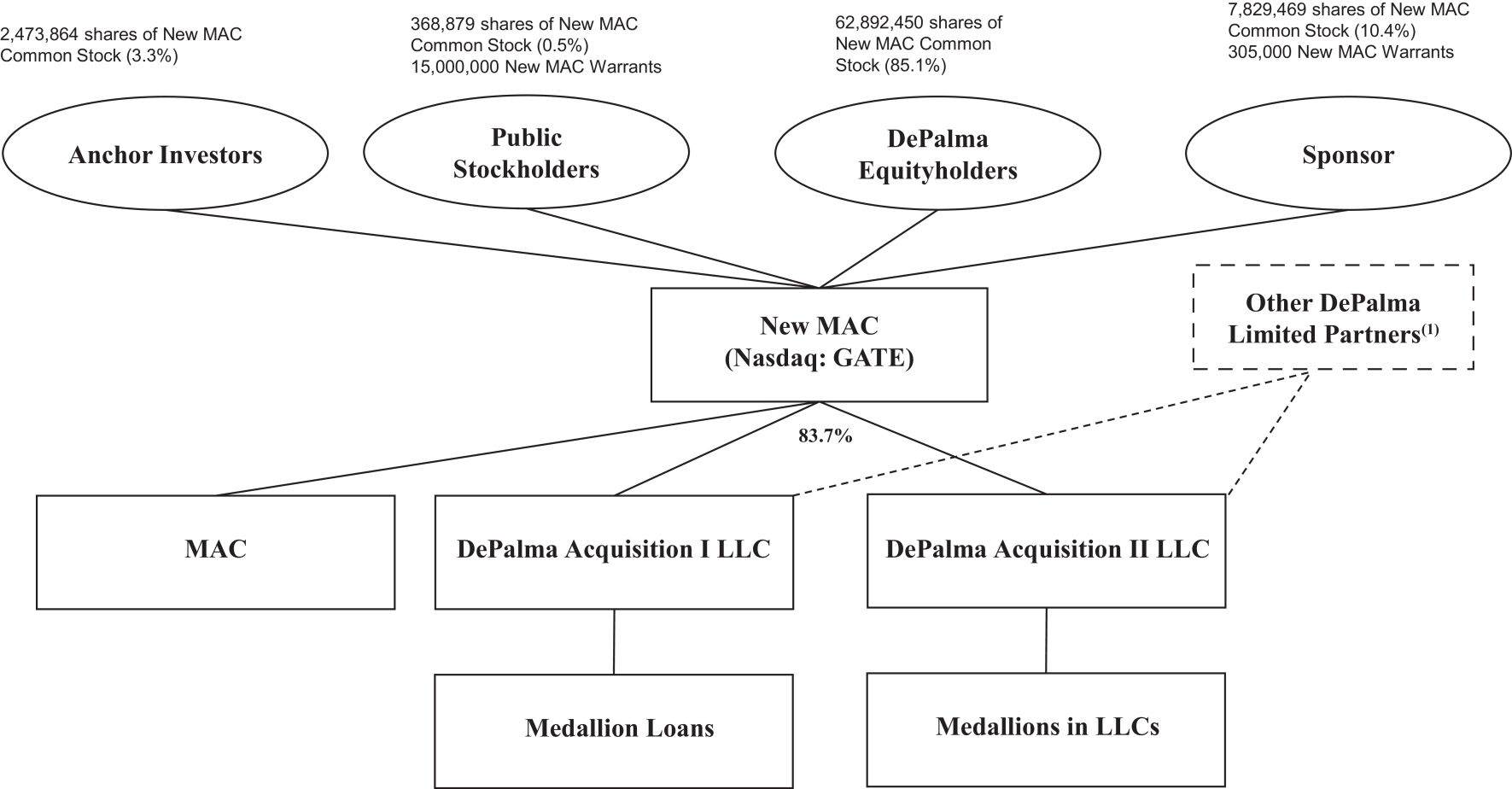

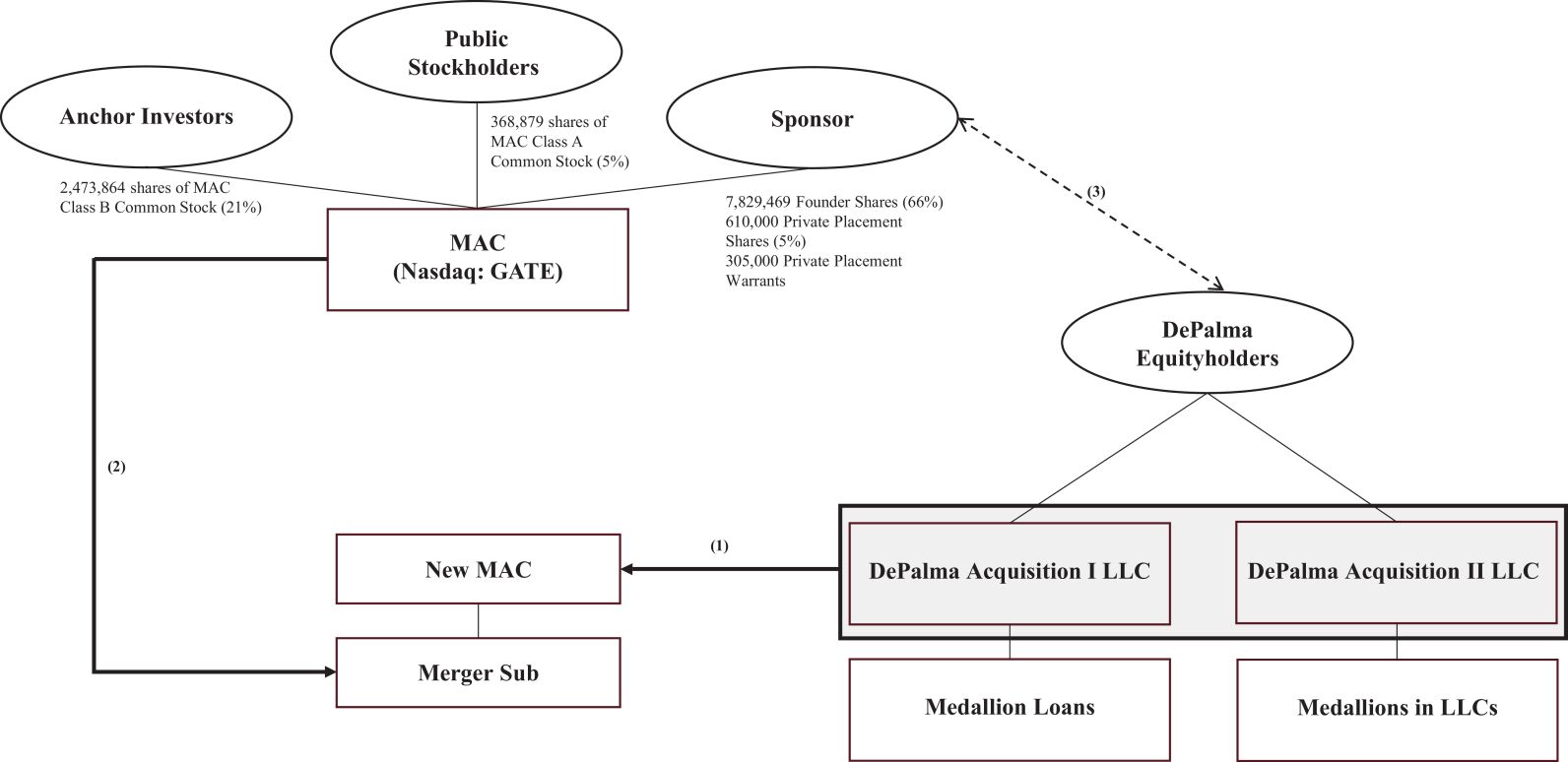

Organizational Structure

Prior to the Business Combination

The following diagram illustrates a simplified version of the ownership structure of MAC prior to the Business Combination. This diagram is provided for illustrative purposes only and does not represent all equityholders of MAC or legal entities of DePalma and its affiliates.

| (1) | Immediately prior to the transactions contemplated by the Business Combination Agreement, New MAC and the DePalma Companies will effect the Pre-Closing Transactions, resulting in New MAC becoming the owner of approximately 83.7% of the DePalma Companies, with the remaining 16.3% continuing to be owned by certain current limited partners of the DePalma Companies. |

| (2) | Merger Sub will merge with and into MAC with MAC surviving as a wholly-owned subsidiary of New MAC. |

| (3) | The DePalma Companies are directly owned by the DePalma Equityholders and are managed by MAM. One of the DePalma Equityholders is the Master Fund, Marblegate Special Opportunities Master Fund, L.P., which has an indirect interest in the Sponsor. The Sponsor in turn owns a majority of MAC Common Stock. As a result, through their positions as managing partners of the general partner of the Master Fund and their control over the Master Fund’s portfolio, Messrs. Andrew Milgram and Paul Arrouet may be deemed to have an interest in the DePalma Companies and MAC. |

37