As confidentially submitted to the Securities and Exchange Commission on [●], 2023

Registration No. 333-[●]

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Ten-League International Holdings Limited

(Exact name of registrant as specified in its charter)

Not Applicable

(Translation of Registrants name into English)

| Cayman Islands | 5080 | Not Applicable | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

16 Gul Drive

Singapore 629467

+65 6862 0769

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive office)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

(212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

Louise L. Liu, Esq. Morgan Lewis & Bockius Suite 1902-09, Edinburgh Tower The Landmark 15 Queen’s Road Central Hong Kong Telephone: (852) 3551 8500 |

Henry F. Schlueter, Esq. Celia Velletri, Esq. Schlueter & Associates, P.C. 5290 DTC Parkway, Suite 150 Greenwood Village, CO 80111 USA Telephone: (303) 292 3883

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.

☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

☐

The term new or revised financial accounting standard refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Registration Statement contains two prospectuses, as set forth below.

| ● | Public offering prospectus. A prospectus to be used for the initial public offering by us of [●] of our ordinary shares, or the public offering prospectus, through the underwriter named in the Underwriting section of the public offering prospectus. | |

| ● | Resale prospectus. A prospectus to be used for the potential resale by LJSC Holdings Limited, or LJSC Holdings, which is a company incorporated in the British Virgin Islands on June 9, 2023 and wholly-owned by Mr. Ng Hong Whee, an independent third party which owns 4.90% of our issued and outstanding shares prior to this offering and one of the selling shareholders, Undersea Capital Holdings Limited, or Undersea Capital, which is a company incorporated in the British Virgin Islands on June 9, 2023 and wholly-owned by Mr. Lay Kok Weng, an independent third party which owns 4.60% of our issued and outstanding shares prior to this offering and one of the selling shareholders, and Jules Verne Investments Limited, or Jules Verne, which is a company incorporated in the British Virgin Islands on June 9, 2023 and wholly-owned by Mr. Chua Wee Ming, an independent third party which owns 4.50% of our issued and outstanding shares prior to this offering and one of the selling shareholders, of [●], [●] and [●] ordinary shares of the registrant respectively, or the resale prospectus. |

The resale prospectus is substantively identical to the public offering prospectus, except for the following principal points:

| ● | they contain different outside and inside front covers; | |

| ● | the “Offering” section in the “Prospectus Summary” section on page 9 of the public offering prospectus is removed and replaced with the “Offering” section on page 3 of the resale prospectus; | |

| ● | they contain different “Use of Proceeds” sections on page 35 of the public offering prospectus is removed and replaced with the “Use of Proceeds” section on page 3 of the resale prospectus; | |

| ● | the “Capitalization” and “Dilution” sections on page 36 and page 37 of the public offering prospectus are deleted from the resale prospectus respectively; | |

| ● | a “Resale Shareholders” section is included in the resale prospectus beginning on page 3 of the resale prospectus; | |

| ● | references in the public offering prospectus to the resale prospectus will be deleted from the resale prospectus; | |

| ● | the “Underwriting” section on page 140 of the public offering prospectus is removed and replaced with a “Plan of Distribution” section on page 4 of the resale prospectus; | |

| ● | the “Legal Matters” section on page 144 of the public offering prospectus is removed and replaced with the “Legal Matters” on page 5 of in the resale prospectus; and | |

| ● | the outside back cover of the public offering prospectus is deleted from the resale prospectus. |

The Registrant has included in this Registration Statement, after the financial statements, a set of alternate pages to reflect the foregoing differences of the resale prospectus as compared to the public offering prospectus.

The public offering prospectus will exclude the alternate pages and will be used for the public offering by the Registrant. The resale prospectus will be substantively identical to the public offering prospectus except for the addition or substitution of the alternate pages and will be used for the resale offering by LJSC Holdings, Undersea Capital and Jules Verne.

| ii |

The information in this prospectus is not complete and may be changed or supplemented. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where such offer or sale is not permitted.

| PRELIMINARY PROSPECTUS DATED [●], 2023 | SUBJECT TO COMPLETION |

Ten-League International Holdings Limited

[●] Ordinary shares

This is an initial public offering of our ordinary shares, par value US$0.001 per share, of Ten-League International Holdings Limited, or the Company. We are offering, on a firm commitment engagement basis, [●] ordinary shares. In addition, our selling shareholders are offering an aggregate of [●] ordinary shares to be sold in the offering pursuant to this prospectus. We will not receive any proceeds from the sale of the ordinary shares to be sold by the selling shareholders. We anticipate that the initial public offering price of the ordinary shares will be between US$[●] and US$[●] per ordinary share.

Prior to this offering, there has been no public market for our shares. We intend to apply to list our ordinary shares on Nasdaq Capital Market, or Nasdaq, under the symbol “[●]”. This offering is contingent upon the listing of our ordinary shares on the Nasdaq or another national securities exchange. There can be no assurance that we will be successful in listing our ordinary shares on the Nasdaq or another national securities exchange.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Investing in our ordinary shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 10 to read about factors you should consider before buying our ordinary shares.

We are an “Emerging Growth Company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, and a “Foreign Private Issuer” under applicable U.S. federal securities laws and, as such, are eligible for reduced public company reporting requirements. Please see “Implications of Our Being an Emerging Growth Company” and “Implications of Our Being a Foreign Private Issuer” beginning on page 7 of this prospectus for more information.

We are a holding company that is incorporated in the Cayman Islands as an exempted company with limited liability. As a holding company with no operations, we conduct all of our operations through our wholly-owned subsidiaries in Singapore. The ordinary shares offered in this offering are shares of the holding company that is incorporated in the Cayman Islands as an exempted company with limited liability. Investors of our ordinary shares should be aware that they may never directly hold equity interests in our subsidiaries.

Upon completion of this offering, our issued and outstanding shares will consist of [●] ordinary shares. We will be a “controlled company” as defined under Nasdaq Marketplace Rule 5615(c) because, immediately after the completion of this offering, Ten-League Corporations Pte. Ltd., or Ten-League Corp, will own approximately [●]% of our total issued and outstanding ordinary shares, representing approximately [●]% of the total voting power and as a result, Mr. Lim Jison, who controls Ten-League Corp, will have the ability to determine all matters of the Company requiring approval by its shareholders. As a “controlled company”, we are permitted to elect not to comply with certain corporate governance requirements. If we rely on these exemptions, you will not have the same protection afforded to shareholders of companies that are subject to these corporate governance requirements.

| Per Share | Total(4) | |||||||

| Initial public offering price(1) | US$ | [●] | US$ | [●] | (4) | |||

| Underwriting discounts and commissions(2) | US$ | [●] | US$ | [●] | ||||

| Proceeds to the Company before expenses(3) | US$ | [●] | US$ | [●] | ||||

| Proceeds to the selling shareholders before expenses(3) | US$ | [●] | US$ | [●] | ||||

(1) Initial public offering price per share is assumed to be US$[●].

(2) We have agreed to pay the underwriter a discount equal to 6% of the gross proceeds of the offering. This table does not include a non-accountable expense allowance equal to 1% of the gross proceeds of this offering payable to the underwriter. For a description of the other compensation to be received by the underwriter, see “Underwriting” beginning on page 140.

(3) Excludes fees and expenses payable to the underwriter. The total amount of underwriter expenses related to this offering is set forth in the section entitled “Expenses Related to This Offering” on page 133.

(4) Includes US$[●] gross proceeds from the sale of [●] ordinary shares offered by our Company and US$[●] gross proceeds from the sale of [●] ordinary shares offered by the selling shareholders.

If we complete this offering, net proceeds will be delivered to us and the selling shareholders on the closing date.

The underwriter expects to deliver the ordinary shares to the purchasers against payment on or about [●], 2023.

You should not assume that the information contained in the registration statement to which this prospectus is a part is accurate as of any date other than the date hereof, regardless of the time of delivery of this prospectus or of any sale of the ordinary shares being registered in the registration statement of which this prospectus forms a part.

No dealer, salesperson or any other person is authorized to give any information or make any representations in connection with this offering other than those contained in this prospectus and, if given or made, the information or representations must not be relied upon as having been authorized by us. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any security other than the securities offered by this prospectus, or an offer to sell or a solicitation of an offer to buy any securities by anyone in any jurisdiction in which the offer or solicitation is not authorized or is unlawful.

EDDID SECURITIES USA INC.

The date of this prospectus is [●], 2023.

| iii |

TABLE OF CONTENTS

Until [●], 2023 (the 25th day after the date of this prospectus), all dealers that effect transactions in these ordinary shares, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as an underwriter and with respect to their unsold allotments or subscriptions.

| iv |

Except where indicated or where the context otherwise requires, the terms “Company”, “Group”, “we”, “us” and “our” refer to Ten-League International Holdings Limited, an exempted company incorporated in the Cayman Islands with limited liability under the Companies Act (as amended) of the Cayman Islands, or the Companies Act, and its subsidiaries or any of them, or where the context so requires, in respect of the period before our Company becoming the holding company of its present subsidiaries, such subsidiaries as if they were subsidiaries of our Company at the relevant time or the businesses which have since been acquired or carried on by them or as the case may be their predecessors. For other conventions that apply to this prospectus, see “Prospectus Summary — Conventions That Apply to This Prospectus”.

Neither we, the selling shareholders nor the underwriter have authorized anyone to provide you with any information or to make any representations other than as contained in this prospectus or in any related free writing prospectus. Neither we, the selling shareholders nor the underwriter take responsibility for, and provide no assurance about the reliability of, any information that others may give you. This prospectus is an offer to sell only the securities offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the securities. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: Neither we, the selling shareholders nor the underwriter have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the ordinary shares and the distribution of this prospectus outside the United States.

We obtained statistical data, market data and other industry data and forecasts used in this prospectus from market research, publicly available information and industry publications. While we believe that the statistical data, industry data, forecasts and market research are reliable, we have not independently verified the data.

Certain amounts, percentages and other figures included in this prospectus have been subject to rounding adjustments. Accordingly, amounts, percentages and other figures shown as totals in certain tables or charts may not be the arithmetic aggregation of those that precede them, and amounts and figures expressed as percentages in the text may not total 100% or, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

Certain market data and forecasts used throughout this prospectus were obtained from internal company surveys, market research, consultant surveys, reports of governmental and international agencies and industry publications and surveys, including the report of Frost & Sullivan, a third-party legal global research organization, commissioned by our Company. Industry publications and third-party research, surveys and reports generally indicate that their information has been obtained from sources believed to be reliable. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. Our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” in this prospectus.

| 1 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements that relate to our current expectations and views of future events. These forward-looking statements are contained principally in the sections entitled “Prospectus Summary,” “Risk Factors,” “Use of Proceeds,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Industry Overview” and “Business.” These statements relate to events that involve known and unknown risks, uncertainties and other factors, including those listed under “Risk Factors,” which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, these forward-looking statements can be identified by words or phrases such as “believe”, “plan”, “expect”, “intend”, “should”, “seek”, “estimate”, “will”, “aim” and “anticipate”, or other similar expressions, but these are not the exclusive means of identifying such statements. All statements other than statements of historical facts included in this document, including those regarding future financial position and results, business strategy, plans and objectives of management for future operations (including development plans and dividends) and statements on future industry growth are forward-looking statements. In addition, we and our representatives may from time to time make other oral or written statements which are forward-looking statements, including in our periodic reports that we will file with the SEC, other information sent to our shareholders and other written materials.

These forward-looking statements are subject to risks, uncertainties and assumptions, some of which are beyond our control. In addition, these forward-looking statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual outcomes may differ materially from the information contained in the forward-looking statements as a result of a number of factors, including, without limitation, the risk factors set forth in “Risk Factors” and the following:

| ● | our business and operating strategies and our various measures to implement such strategies; | |

| ● | our operations and business prospects, including development and capital expenditure plans for our existing business; | |

| ● | changes in policies, legislation, regulations or practices in the industry and those countries or territories in which we operate that may affect our business operations; | |

| ● | our financial condition, results of operations and dividend policy; | |

| ● | changes in political and economic conditions and competition in the area in which we operate, including a downturn in the general economy; | |

| ● | the regulatory environment and industry outlook in general; | |

| ● | future developments in the provision of equipment, value added solutions and maintenance and repair services market and actions of our competitors; | |

| ● | catastrophic losses from man-made or natural disasters, such as fires, floods, windstorms, earthquakes, diseases, epidemics, other adverse weather conditions or natural disasters, war, international or domestic terrorism, civil disturbances and other political or social occurrences; | |

| ● | the loss of key personnel and the inability to replace such personnel on a timely basis or on terms acceptable to us; | |

| ● | the overall economic environment and general market and economic conditions in the jurisdictions in which we operate; |

| 2 |

| ● | our ability to execute our strategies; | |

| ● | changes in the need for capital and the availability of financing and capital to fund those needs; | |

| ● | our ability to anticipate and respond to changes in the markets in which we operate, and in client demands, trends and preferences; | |

| ● | exchange rate fluctuations, including fluctuations in the exchange rates of currencies that are used in our business; | |

| ● | changes in interest rates or rates of inflation; and | |

| ● | legal, regulatory and other proceedings arising out of our operations. |

The forward-looking statements made in this prospectus relate only to events or information as of the date on which the statements are made in this prospectus. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this prospectus and the documents that we reference in this prospectus and have filed as exhibits to the registration statement, of which this prospectus is a part, completely and with the understanding that our actual future results or performance may be materially different from what we expect.

This prospectus contains certain data and information that we obtained from various government and private publications. Statistical data in these publications also include projections based on a number of assumptions. The markets for the supply of heavy machinery may not grow at the rate projected by such market data, or at all. Failure of this industry to grow at the projected rate may have a material and adverse effect on our business and the market price of our ordinary shares. Furthermore, if any one or more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based on these assumptions. You should not place undue reliance on these forward-looking statements.

| 3 |

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you, and we urge you to read this entire prospectus carefully, including the “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections and our consolidated financial statements and notes to those statements, included elsewhere in this prospectus, before deciding to invest in our ordinary shares. This prospectus includes forward-looking statements that involve risks and uncertainties. See “Special Note Regarding Forward-Looking Statements.”

Our Mission

Our mission is to provide high-quality equipment, value-added engineering solutions as well as maintenance and repair services through continuous adaptation and application of new technologies.

Overview

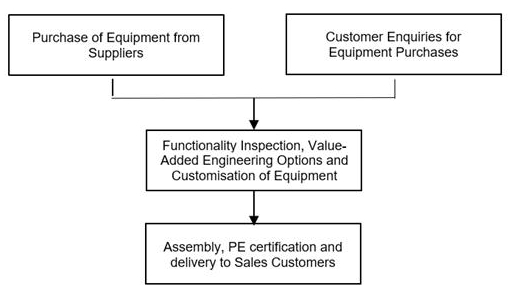

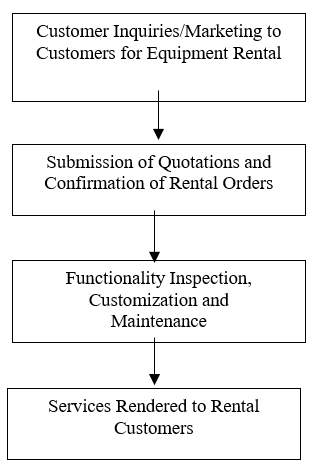

We are a Singapore-based provider of turnkey project solutions. Our business primarily consists of sales of heavy equipment and parts, heavy equipment rental and provision of engineering consultancy services to port, construction, civil engineering and underground foundation industries. We currently conduct our operations through our wholly-owned subsidiaries, Ten-League Engineering & Technology Pte. Ltd., or Ten-League (E&T), and Ten-League Port Engineering Solutions Pte. Ltd., or Ten-League (PES), which were previously held by Ten-League Corp prior to our group reorganization for the listing of our ordinary shares. Together with the operating history of Ten-League Corp, we have a total of over 24 years of history operating our business. Our core business activities consist of the following segments:

| (a) | equipment sales, which involves sale of various new and used heavy equipment and parts, or Equipment Sales Business; | |

| (b) | equipment rental, which involves the rental of various new and used heavy equipment, or Equipment Rental Business; and | |

| (c) | engineering consultancy services, which primarily includes the provision of value-added engineering solutions, including equipment retrofitting, upgrading, modernization, fleet management and other enhancement on equipment through the replacement or application of, among others, mechanical parts, sensor fusion, software and remote control system. Our engineering consultancy services complements our Equipment Sales Business and Equipment Rental Business. We do not provide such service to third-party equipment sales/rental companies. |

The equipment we provide is categorized into (i) foundation equipment; (ii) hoist equipment; (iii) excavation equipment; and (iv) port machinery.

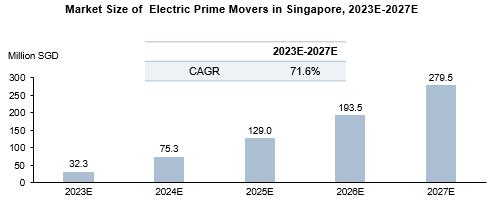

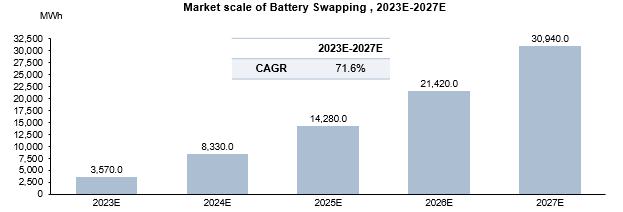

We have been supplying fully electric reach stacker and empty container handler to port operators in Singapore since 2021 and have been contracted to supply electric prime movers with swappable battery pack and build charging infrastructure since October 2022 by a leading port operator based in Singapore, or the Leading Port Operator. Meanwhile, we are actively exploring the market for fully electric wheel loader, excavator and forklift, and offering them as a part of our fleet of electrified equipment.

Our Competitive Strengths

We believe that the following competitive strengths have contributed to our past success and will continue to distinguish us from our competitors:

| ● | We have a well-established market position as an engineering solutions provider in the port, construction, civil engineering and underground foundation industries and possess a strong and proven track record | |

| ● | We are able to provide “one-stop solution” including heavy equipment sales and rental, engineering consultancy services and equipment maintenance and repair services | |

| ● | We have a strong long-term relationship with our major suppliers, all of which belong to a group of companies considered as one of the world’s largest heavy equipment manufacturers, or Major Supplier, and a wide customer base across the construction and infrastructure, civil engineering and foundation industries in Singapore | |

| ● | We have a strong management team with in-depth knowledge and expertise |

| 4 |

Our Business Strategies

To achieve our business objectives, we plan to adopt the following strategies to drive our future growth:

| ● | We intend to offer more environmentally friendly heavy equipment | |

| ● | We intend to expand our engineering, procurement, construction and commissioning, or EPCC, service for deploying charging solutions in Singapore | |

| ● | Expansion and diversification of our operations and product and service offerings through investments, mergers and acquisitions, joint ventures and/or strategic collaborations | |

| ● | Deepen collaboration with our strategic partners and further expand and diversify our value-added engineering solutions and options | |

| ● | Attract, cultivate and retain a talented and professional workforce |

Risks and Challenges

Investing in our ordinary shares involves risks. The risks summarized below are qualified by reference to “Risk Factors” beginning on page 10 of this prospectus, which you should carefully consider before making a decision to purchase ordinary shares. If any of these risks actually occurs, our business, financial condition or results of operations would likely be materially adversely affected. In such case, the trading price of our ordinary shares would likely decline, and you may lose all or part of your investment.

These risks include but are not limited to the following:

| ● | We are dependent on our Major Supplier. There can be no assurance that we will be able to renew our distribution agreements with our Major Supplier on the same terms or at all, or that the distribution arrangements will not be terminated prematurely. | |

| ● | We are subject to certain legal and operational risks associated with relying on a major supplier based in the PRC. | |

| ● | We are dependent on our key management and skilled personnel for our continued success and growth. | |

| ● | We operate in a competitive environment and face competition from existing and new industry players. | |

| ● | We are dependent on foreign labor and may face labor shortages or increased costs of labor for our Singapore operations. |

| 5 |

| ● | We are subject to a number of operating risks. | |

| ● | We may be unsuccessful in implementing our business strategies and future plans. | |

| ● | We are dependent on the level of activities in the construction and infrastructure, civil engineering and foundation industries. | |

| ● | We do not have long term contracts with our customers. | |

| ● | We are dependent on the timely delivery of the heavy equipment and other products which we distribute. | |

| ● | We may experience work safety-related accidents that may expose us to liability claims. | |

| ● | Our rental fleet is subject to residual value risk upon disposition. | |

| ● | If our rental fleet ages, our operating costs may increase, we may be unable to pass along such costs, and our earnings may decrease. | |

| ● | We incur maintenance and repair costs associated with our rental fleet equipment that could have a material adverse effect on our business in the event these costs are greater than anticipated. | |

| ● | Climate change, climate change regulations and greenhouse effects may materially adversely impact our operations and markets. | |

| ● | We may require additional funding for our future growth and are dependent on financing to fund our purchase of equipment for our Equipment Rental Business. | |

| ● | We may be exposed to risks associated with joint ventures or strategic alliances. | |

| ● | We may be affected by any adverse impact on our reputation and goodwill. | |

| ● | Adverse conditions in the global financial markets and the general economy may adversely affect our business, financial condition, results of operations and prospects. | |

| ● | We cannot assure you that our future plans will be successful. |

Corporate Information

We were incorporated in the Cayman Islands as an exempted company with limited liability on March 17, 2023. Our registered office in the Cayman Islands is at Walkers Corporate Limited, 190 Elgin Avenue, George Town, Grand Cayman KY1-9008, Cayman Islands. Our principal executive office is at 16 Gul Drive, Singapore 629467. Our telephone number at this location is +65 6862 0769. Our principal website address is https://www.ten-league.com.sg. The information contained on our website does not form part of this prospectus. Our agent for service of process in the United States is Cogency Global Inc., 122 East 42nd Street, 18th Floor, New York, NY 10168.

Because we are incorporated under the laws of the Cayman Islands, you may encounter difficulties in protecting your interests as a shareholder, and your ability to protect your rights through the U.S. federal court system may be limited.

| 6 |

Implications of Our Being an Emerging Growth Company

As a company with less than US$1.235 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include:

| ● | being permitted to provide only two years of audited financial statements (rather than three years), in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; and |

| ● | an exemption from compliance with the auditor attestation requirement of the Sarbanes-Oxley Act of 2002, on the effectiveness of our internal control over financial reporting. |

We may take advantage of these reporting exemptions until we are no longer an emerging growth company. We will remain an emerging growth company until the earliest of (1) the last day of the fiscal year in which the fifth anniversary of the completion of this offering occurs, (2) the last day of the fiscal year in which we have total annual gross revenue of at least US$1.235 billion, (3) the date on which we are deemed to be a “large accelerated filer” under the United Sates Securities Exchange Act of 1934, as amended, or the Exchange Act, which means the market value of our ordinary shares that are held by non-affiliates exceeds US$700.0 million as of the prior December 31, and (4) the date on which we have issued more than US$1.0 billion in non-convertible debt during the prior three-year period. We may choose to take advantage of some, but not all, of the available exemptions. We have included two years of selected financial data in this prospectus in reliance on the first exemption described above. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold stock.

Implications of Our Being a Foreign Private Issuer

Upon completion of this offering, we will report under the Exchange Act as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| ● | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| ● | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission, or the SEC, of quarterly reports on Form 10-Q containing unaudited financial and other specified information, or current reports on Form 8-K, upon the occurrence of specified significant events. |

Both foreign private issuers and emerging growth companies are also exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosures required of companies that are neither emerging growth companies nor foreign private issuers.

In addition, as a company incorporated in the Cayman Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from the corporate governance listing requirements of the Nasdaq. These practices may afford less protection to shareholders than they would enjoy if we complied fully with corporate governance listing requirements of the Nasdaq. Following this offering, we will rely on home country practice to be exempted from certain of the corporate governance requirements of the Nasdaq, such that a majority of our directors, or directors on our board of directors, or the Board, are not required to be independent directors.

| 7 |

Conventions That Apply to This Prospectus

| Except where the context otherwise requires and for purposes of this prospectus only: | ||

| ● | “Amended Memorandum of Association” or “Amended Memorandum” means the amended and restated memorandum of association of our Company adopted on [●], 2023 and as supplemented, amended or otherwise modified from time to time. | |

| ● | “Amended and Restated Articles of Association” means the amended and restated articles of association of our Company adopted on [●], 2023, as amended from time to time. A copy of the Amended Memorandum of Association and Amended and Restated Articles of Association are filed as Exhibit 3.2 to our Registration Statement of which this prospectus forms a part. | |

| ● | “bizSAFE” means a five-step program that assists companies to build up their workplace safety and health capabilities in order to achieve quantum improvements in safety and health standards at the workplace, and organized under Workplace Safety and Health Council of Singapore. | |

| ● | “ordinary shares” or “shares” means our ordinary shares of par value of US$0.001 per share. | |

| ● | “S$” or “SGD” or “Singapore Dollars” means Singapore dollar(s), the lawful currency of Singapore. | |

| ● | “US$”, “$” or “USD” or “United States Dollars” means United States dollar(s), the lawful currency of the United States of America. | |

| ● | “U.S. GAAP” are to generally accepted accounting principles in the United States. |

| 8 |

| Offering Price | The initial public offering price will be between US$[●] and US$[●] per ordinary share | |

| Ordinary shares offered by us | [●] ordinary shares | |

| Ordinary shares offered by the selling shareholders | [●] ordinary shares (of which Ten-League Corp is selling [●] shares, LJSC Holdings is selling [●] shares, Undersea Capital is selling [●] shares and Jules Verne is selling [●] shares) | |

Ordinary shares issued and outstanding prior to this offering |

[●] ordinary shares | |

Ordinary shares to be issued and outstanding immediately after this offering |

[●] ordinary shares | |

| Use of proceeds | We currently intend to use the net proceeds from this offering (i) to expand our product offering; (ii) to improve our automation process and invest in equipment and technology; (iii) to expand through strategic targeted acquisitions and investments; (iv) to market and brand build; (v) for the repayment of bank borrowing; and (v) for working capital and other general corporate purposes. See “Use of Proceeds” | |

Lock-up

|

We, each of our directors and executive officers and certain principal shareholders, except for the selling shareholders with respect to its ordinary shares sold in this offering, have agreed, subject to certain exceptions, for a period of 180 days after the date of this prospectus, not to, except in connection with this offering, offer, pledge, sell, contract to sell, sell any option or contract to purchase, purchase any option or contract to sell, grant any option, right or warrant to purchase, lend or otherwise transfer or dispose of, directly or indirectly, any ordinary shares or any other securities convertible into or exercisable or exchangeable for ordinary shares, or enter into any swap or other arrangement that transfers to another, in whole or in part, any of the economic consequences of ownership of ordinary shares. See “Shares Eligible for Future Sale” and “Underwriting — Lock-Up Agreements” | |

| Risk factors | Investing in our ordinary shares involves risks. See “Risk Factors” beginning on page 10 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ordinary shares | |

| Listing | We plan to apply to list the ordinary shares on the Nasdaq | |

| Proposed trading symbol | [●] | |

| Transfer agent | [●] | |

| Payment and settlement | The underwriter expects to deliver the ordinary shares against payment therefor through the facilities of the Depository Trust Company on [●], 2023 |

| 9 |

Investing in our shares is highly speculative and involves a significant degree of risk. You should carefully consider the following risks, as well as other information contained in this prospectus, before making an investment in our Company. The risks discussed below could materially and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the trading price of our shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability to pay dividends, and you may lose all or part of your investment.

This prospectus also contains forward-looking statements having direct and/or indirect implications on our future performance. Our actual results may differ materially from those anticipated by these forward-looking statements due to certain factors, including the risks and uncertainties faced by us, as described below and elsewhere in this prospectus.

Risks Related to Our Business and Industry

We are dependent on our Major Supplier. There can be no assurance that we will be able to renew our distribution agreements with our Major Supplier on the same terms or at all, or that the distribution arrangements will not be terminated prematurely.

We purchase substantially all of our equipment from our Major Supplier. Our Major Supplier is one of the world’s largest heavy equipment manufacturers and the first in its industry in China to be ranked among the FT Global 500 and the Forbes Global 2000. Our purchases from our Major Supplier represented 71.3% and 60.4%, respectively, of our cost of revenue for the years ended December 31, 2021 and 2022. We have entered into a service dealer agreement with our Major Supplier on January 1, 2021, with an initial term of one year which is automatically renewable on an annual basis unless the Major Supplier terminates it. In addition, each of our operating subsidiaries, namely, Ten-League (E&T) and Ten-League (PES), entered into a non-exclusive dealership agreement with our Major Supplier in 2019. Both dealership agreements expired in 2021. We are currently in the process of renewing such dealership agreements with our Major Supplier and have been conducting business with the Major Supplier on the same terms as those described in such dealership agreements. During the term of the dealership agreements, we did not encounter any material supply chain disruptions as a result of our reliance on the Major Supplier. For further information regarding our relationship with the Major Supplier, see “Business — Major Suppliers” in this prospectus.

Our distribution arrangements with our Major Supplier are non-exclusive in nature, and our Major Supplier reserves the right to directly supply the same products in Singapore or to engage other distributors to supply the same products in Singapore, which would increase our competition for customers. In this case, our business, results of operations and prospects may be adversely affected.

In addition, our distribution arrangements with our Major Supplier are subject to renewal and may be terminated by our Major Supplier upon giving the requisite notice or upon the occurrence of certain stipulated events, some of which are not entirely within our control. As such, there can be no assurance that we will be able to renew these arrangements on terms acceptable to us or at all or that these arrangements will not be terminated prematurely or modified to our detriment. Although we believe that we have alternative sources of supply for the equipment, the loss of the distributorship with our Major Supplier may have a material adverse impact on our financial condition and results of operations if we are unable to obtain comparable equipment in an adequate or timely manner.

We are subject to certain legal and operational risks associated with relying on a major supplier based in the PRC.

Although we have not experienced any supply chain disruptions that have had a material impact on our business operations due to our reliance on the Major Supplier, in the event of disruption or total cessation of business relationship with the Major Supplier, we may have to seek alternative sources for heavy equipment and related products which may incur additional time and cost for us and until such alternative is found on reasonable or similar terms to those with the Major Supplier. Such disruption or total cessation will have a material adverse affect on our operations which in turn may cause our share price to decline.

The PRC legal system is a civil law system based on written statutes, and prior court decisions can only be cited as references. The PRC government has been developing a comprehensive system of laws and regulations governing economic matters in general such as foreign investment, corporate organization and governance, commerce, taxation, finance, foreign exchange and trade. However, due to the continuous and rapid development of the PRC legal system and the limited volume of published court decisions which are non-binding in nature, the interpretations and enforcement of laws, regulations and rules may be inconsistent and involve uncertainties, which may limit legal protections available to us in the event of dispute arising with our Major Supplier. Enacted laws and regulations may not sufficiently cover all aspects of economic activities in the PRC, or may be unclear or inconsistent. Even where adequate laws exist in the PRC, the enforcement of existing laws or contracts may be uncertain or sporadic, and it may be difficult to obtain swift and equitable enforcement of a judgment by a court.

In addition, we cannot predict future developments in the PRC legal system, including the promulgation of new laws, changes to existing laws and the interpretation or enforcement thereof, and the effects of such developments on our Major Supplier’s industry which in turn may affect our ability to obtain heavy equipment and parts from them. Therefore, notwithstanding that we have no presence in the PRC and the above does not directly apply to us or directly affect our daily operations, such future developments would have implications on our Major Supplier, which in turn could affect the supply of heavy equipment and related products to us.

| 10 |

We are dependent on our key management and skilled personnel for our continued success and growth.

We attribute our success and growth to-date largely to the contributions and expertise of our directors and executive officers, all of whom have extensive experience in our business or relevant industries. Our founder, Mr. Lim Jison, or Mr. Lim, has worked in the industry for over 25 years, has grown our business since our inception, and is instrumental to our continued success, formulating business strategies and spearheading the growth of our business. He possesses extensive industry knowledge and comprehensive global and local industry network, is familiar with all aspects of our business operations and has established good relationships with customers and suppliers. He is supported by our executive officers, who play an important role in implementing our overall business strategy, managing our operations and executing our corporate development activities.

However, there is no assurance that we will be able to continue to retain the services of our key personnel. Even though we have obtained a keyman insurance for Mr. Lim upon listing, the resignation or the loss of the services of Mr. Lim or any of our directors, executive officers or other key personnel without suitable and timely replacement or the inability to attract and retain qualified management personnel, may materially and adversely affect our business, results of operations and prospects. Further, in the event that we need to increase employee compensation levels substantially to attract and/or retain any key management personnel, our costs may increase, and our results of operations may be materially and adversely affected.

Our continued success and growth are also dependent upon our ability to recruit and retain skilled and qualified personnel such as design, engineering and technical personnel. Skilled personnel with the appropriate experience in the industries we operate in are limited and competition for the employment of such personnel is intense. Even though we intend to continue to devote significant resources to recruit, train and retain such personnel, there is no assurance that we will be able to attract the necessary skilled personnel to work for us or that we will be able to retain the skilled personnel or that suitable and timely replacements can be found for skilled personnel who leave us. Further, competition for skilled qualified employees may result in us having to pay higher wages to attract and retain our employees, which may result in higher labor costs, which in turn may materially and adversely affect our results of operations. If we are unable to continue to attract and retain skilled employees, this will adversely affect our business and prospects.

We operate in a competitive environment and face competition from existing and new industry players.

We operate in a competitive environment and our success depends to a large extent on our ability to compete against other industry players on, among other things, reputation, track record, pricing, product range, delivery times and customer service.

We cannot assure you that we will be able to compete effectively against our existing and future competitors and adapt quickly to changing market conditions and trends. Failure to keep abreast of technological advancements and industry developments may result in failure to provide services in a cost-effective and efficient manner compared to our competitors, which may lead to loss of customers. Our business and results of operations may be adversely affected if competition intensifies. Any failure by us to remain competitive will adversely affect our business, financial condition and results of operations.

In addition, new competitors may enter the industry, resulting in increased competition, which in turn may result in us losing our existing customers and not being able to secure new customers. There is no assurance that we will be able to compete successfully in the future against our existing or potential competitors or that our business, financial condition and results of operations will not be adversely affected by increased competition.

| 11 |

We are dependent on foreign labor and may face labor shortages or increased costs of labor for our Singapore operations.

We employ a significant number of foreign workers (including skilled workers) for our Singapore operations, and we are vulnerable to changes in the availability and costs of employing foreign workers. As of August 10, 2023, out of our total employees in Singapore, approximately 42.9% are foreign workers who mainly work in servicing and operations. The supply and costs of skilled workers are subject to demand and supply conditions in the labor market and the local and foreign governments’ labor regulations and visa restrictions.

In addition, the availability of both skilled and unskilled foreign labor is subject to policies imposed by the Ministry of Manpower of Singapore, or MOM, and the foreign affairs and labor policies of the countries in which these foreign workers are domiciled. For instance, the availability of foreign employees in Singapore is regulated by MOM through policy measures such as the imposition of levies and quotas known as dependency ratio ceilings, being the percentage of foreign employees permitted in a company’s total workforce. We are susceptible to any increase in such levies and any changes in the supply and/or quota of foreign employees that it is permitted to hire. The availability, requirements and cost of housing for such workers are also subject to government policies. Any changes in such policies may affect the supply of foreign manpower and cause disruptions to our operations which will result in an increase in our labor costs and may have a material adverse impact on our results of operations. See “Regulatory Environment – Employment of Foreign Manpower Act 1990 of Singapore, or the EFMA” in this prospectus for further information on the main foreign employment laws and regulations governing our business.

Any increase in competition for foreign workers, especially skilled workers, will increase our labor costs. Consequently, if we are not able to pass on the increase in labor costs to our customers, our results of operations will be adversely affected.

We are subject to a number of operating risks.

Our operations are exposed to the risk of equipment failure, risk of failure by employees to follow procedures and protocols as well as inherent risks in operating equipment and machinery, resulting in damage to or loss of any relevant machines, equipment or facilities required in a project or personal injury. A major operational failure could result in loss of life and/or serious injury, damage to or loss of the machines, equipment or facilities and protracted legal disputes and damage to our reputation. In the event of an operational or equipment failure, we may be forced to cease part of our operations and/or be subject to a penalty or incur extra costs or expenses in any dispute as a result of such operational or equipment failure.

In addition, the industry we operate in is highly regulated by the Land Transport Authority of Singapore, or LTA, MOM, the National Environment Agency of Singapore, or NEA, and other regulatory authorities in Singapore. Where there is a non-compliance of any regulatory requirements of LTA, MOM, NEA or other regulatory authorities, we will be subject to penalties as may be imposed by them and/or may be required to cease operations until we comply with the requirements of the relevant authorities. This may have an adverse impact on our business and results of operations.

We may be unsuccessful in implementing our business strategies and future plans.

As part of our business strategies and future plans, we intend to further expand our product portfolio to include additional models of fully electric equipment, expand our engineering, procurement, construction and commissioning, or EPCC, service for deploying charging solutions in Singapore and deepen collaboration with our strategic partners and further expand and diversify our engineering solutions and options, among others. While such plans are based on our outlook regarding our business prospects, there is no assurance that such expansion plans will be commercially successful or that the actual outcome of those plans will match our expectations. The success and viability of our plans are dependent upon our ability to successfully carry out our overall electrification strategy and implement corresponding strategic business development and marketing plans effectively and upon an increase in demand for our products and services by existing and new customers in the future.

| 12 |

Further, the implementation of our business strategies and future plans may require substantial capital expenditure and additional financial resources and commitments. There is no assurance that these business strategies and future plans will achieve the expected results or outcome such as an increase in revenue that will be commensurate with our investment costs or the ability to generate any costs savings, increased operational efficiency and/or productivity improvements to our operations. There is also no assurance that we will be able to obtain financing on terms that are favorable, if at all. If the results or outcome of our future plans do not meet our expectations, if we fail to achieve a sufficient level of revenue or if we fail to manage our costs efficiently, we may be unable to recover our investment costs and our business, financial condition, results of operation and prospects may be adversely affected.

We are dependent on the level of activities in the construction and infrastructure, civil engineering and foundation industries.

Our customers are mainly in the construction and infrastructure, civil engineering and foundation industries in Singapore. In particular, a significant portion of our customer base consists of those who are heavily involved in infrastructure and government projects. Thus, the demand for our products and services is dependent, to a large extent, on the level of business activities in these industries and the business activities emerging from such infrastructure and government-related projects in Singapore. These industries are cyclical in nature. Any decline in the businesses of these industries or a broad economic downturn in Singapore may lead to a decrease in the demand for equipment or depress rental rates and the sales prices for our equipment, which in turn, will have an adverse effect on our business, results of operations and prospects. We may be unable to predict the timing, extent or duration of such activity cycles of these industries. In addition, our business may be negatively impacted, either temporarily or long-term, by a number of factors out of our control, including:

| ● | a reduction in spending levels by customers; | |

| ● | unfavorable credit markets affecting end-user access to capital; | |

| ● | adverse changes in government infrastructure spending; | |

| ● | an increase in the cost of construction materials; | |

| ● | adverse weather conditions or natural disasters which may affect a particular region; | |

| ● | an increase in interest rates; | |

| ● | supply chain disruptions; or | |

| ● | public health crises and epidemics, such as COVID-19. |

If we fail to react to the cyclical downturn or the factors that are out of our control effectively, our business, financial condition, results of operations and prospects may be adversely affected.

| 13 |

We do not have long term contracts with our customers.

We do not have definite and long-term purchase or rental contracts with our customers for the various products and services we provide, and our customers typically make their purchases or rentals on a project needs basis. These customers may also decide to make purchases or rentals from our competitors. While we have good business relationships with our customers, there can be no assurance that they will not significantly reduce and/or delay their orders or stop making purchases or rentals from us in the future. There also can be no assurance that business relationships with these customers would remain cordial or that they would continue to be satisfied with our quality of service. If our major customers or a significant number of our other customers were to make purchases or rentals from sources other than us and if we are unable to secure alternative orders of comparable size, whether from new or existing customers, our business, financial condition, results of operations and prospects may be adversely affected.

In addition, in the event that our heavy equipment fleet for our Equipment Rental Business is not being rented out, we will have to bear the costs incurred the maintenance of such heavy equipment which are not being deployed or rented. It is also difficult for us to accurately anticipate the level of heavy equipment that is required due to the fact that most of our rentals are made on a short term or project needs basis. There can be no assurance that our rental equipment fleet will be fully and efficiently utilized. In the event that we have to incur additional fixed costs towards the maintenance of the rental equipment fleet, it may result in a material adverse impact on our business, results of operations and prospects. We may also have to take into account depreciation charges incurred for our heavy equipment.

We are dependent on the timely delivery of the heavy equipment and other products which we distribute.

We typically do not maintain significant levels of inventories and typically only place orders based on our forecasted demand. However, due to recent market conditions, we have been maintaining inventories in order to fulfil market demand on short notice. There can also be no assurance that our suppliers will be able to fulfill our purchase requirements in adequate quantities on a timely basis or at all. If any of these events were to occur, we will be unable to fulfill our customers’ orders on a timely basis or at all or we may have to satisfy our purchase requirements from alternative sources in limited quantities or at higher costs, and may be liable for breach of contract with our customers pursuant to the non-fulfilment or partial fulfilment of the contract terms. Further, any significant delay or disruption in the delivery of products by our suppliers may affect our ability to fulfill our customers’ orders which in turn could result in loss of sales and could affect customer satisfaction and our reputation. In any of such events, our business, financial condition, results of operations and prospects will be adversely affected.

We may experience work safety-related accidents that may expose us to liability claims.

Due to the nature of our operations, it is also subject to the risk of our employees or third parties being involved in accidents or mishaps at our premises or our customers’ premises. These accidents may occur as a result of non-compliance with safety measures or various other reasons, and may have a material adverse impact on our track record and reputation. In the event of such accidents, we will have to incur costs to make good our premises, machinery, equipment or inventory or to relocate to alternative premises. Such accidents or mishaps may also disrupt our operations and lead to delays in the completion of our projects, and in the event of such delays, we could be liable to pay liquidated damages under the terms of contracts with our customers.

| 14 |

Further, in the event we are found to be liable for any such accidents, penalties or damages may be imposed upon us. Our business, financial condition and results of operations may also be affected if we have to incur a significant amount of legal costs in the event that we are involved in legal proceedings, even if we are not found to be liable for any claims as a result of such proceedings.

In the event of accidents which are not covered by the insurance or work injury compensation policies taken by us, or if claims arising from such accidents are in excess of our insurance coverage and/or any of our insurance claims is contested by the insurance companies, we will be required to pay such compensation and our results of operations may be materially and adversely affected as a result. In addition, such insurance claims may result in increases in our insurance premiums.

Our rental fleet is subject to residual value risk upon disposition.

The market value of any given piece of rental equipment could be less than its depreciated value at the time it is sold. The market value of used rental equipment depends on several factors, including:

| ● | the market price for new equipment of a like kind; | |

| ● | wear and tear on the equipment relative to its age; | |

| ● | the timing when it is sold ; | |

| ● | worldwide and domestic demands for used equipment; | |

| ● | the supply of used equipment on the market; and | |

| ● | general economic conditions. |

As to the timing of when the equipment is sold, prices are generally higher when contracts/projects are awarded by the Building and Construction Authority of Singapore, or the BCA. That is because when the BCA awards more contracts/projects, it is expected to drive up demand for heavy equipment resulting in a corresponding increase in the price of the equipment.

Any significant decline in the selling prices for used equipment could have a material adverse effect on our business, financial condition, results of operations or cash flows.

If our rental fleet ages, our operating costs may increase, we may be unable to pass along such costs, and our earnings may decrease.

The costs of new equipment we use in our fleet may increase, requiring us to spend more for replacement equipment or preventing us from procuring equipment on a timely basis. If our rental equipment ages, the costs of maintaining such equipment, if not replaced within a certain period of time, will likely increase. The costs of maintenance may materially increase in the future and could lead to material adverse effects on our results of operations.

The cost of new equipment for use in our rental fleet could also increase due to increased material costs for our suppliers (including tariffs on raw materials) or other factors beyond our control. Such increases could materially adversely impact our financial condition and results of operations in future periods. Furthermore, changes in customer demand could cause certain of our existing equipment to become obsolete and require us to purchase new equipment at increased costs.

| 15 |

We incur maintenance and repair costs associated with our rental fleet equipment that could have a material adverse effect on our business in the event these costs are greater than anticipated.

As our fleet of rental equipment ages, the cost of maintaining such equipment, if not replaced within a certain period of time, generally increases. Determining the optimal age for our rental fleet equipment is subjective and requires considerable estimates by management. We have made estimates regarding the relationship between the age of our rental fleet equipment, maintenance and repair costs, and the market value of used equipment. Our future operating results could be adversely affected because our maintenance and repair costs may be higher than estimated and market values of used equipment may fluctuate.

Climate change, climate change regulations and greenhouse effects may materially adversely impact our operations and markets.

Although we have been introducing fully electric equipment and are currently building our first battery swap station in Singapore as a part of our overall electrification strategy of adopting to a greener future, the majority of our equipment currently on offer for sales and rental remains powered by internal combustion engine. Climate change and its association with greenhouse gas emissions is receiving increased attention from the scientific and political communities. Singapore and other countries and regions have adopted or are considering legislation or regulation imposing overall caps or taxes on greenhouse gas emissions from certain sectors or facility categories. Such new laws or regulations, or stricter enforcement of existing laws and regulations, could increase the costs of operating our businesses, reduce the demand for our products and services and impact the prices we charge our customers, any or all of which could adversely affect our results of operations. Failure to comply with any legislation or regulation could potentially result in substantial fines, criminal sanctions or operational changes. Moreover, even without such legislation or regulation, the perspectives of our customers, stockholders, employees and other stakeholders regarding climate change are continuing to evolve, and increased awareness of, or any adverse publicity regarding, the effects of greenhouse gases could harm our reputation or reduce customer demand for our products and services.

| 16 |

Additionally, as severe weather events become increasingly common, our or our customers’ operations may be disrupted, which could result in increased operational costs or reduced demand for our products and services and extended periods of disruptions could have an adverse effect on our results of operations. In addition, climate change may also reduce the availability or increase the cost of insurance for weather-related events as well as may impact the global economy, including as a result of disruptions to supply chains. We anticipate that climate change-related risks will increase over time.

We may require additional funding for our future growth and are dependent on financing to fund our purchase of equipment for our Equipment Rental Business.

We have identified our future plans as set out in this prospectus. Under such circumstance, we may need to obtain debt or equity financing to fund our business and future growth. There is no assurance that we will be able to obtain additional financing on terms that are acceptable to us or at all. If we are unable to do so, our future plans and growth prospects may be adversely affected. In addition, we require financing to fund our purchase of heavy equipment for our Equipment Rental Business. If we are unable to secure financing for this purpose, our ability to renew or expand our fleet to meet our equipment rental requirements may be adversely affected and could have a material and adverse effect on our business and results of operations.

If such financing requirements are met by way of debt financing, apart from increasing our interest expense and gearing, we may have restrictions placed on us through such debt financing arrangements which may (a) limit our ability to pay dividends or require us to seek consents for the payment of dividends; (b) increase our vulnerability to general adverse economic and/or industry conditions; (c) require us to dedicate a substantial portion of our cash flow from operations to payments on our debt, thereby reducing the availability of our cash flows to fund capital expenditure, working capital and other requirements; and/or (d) limit our flexibility in planning for, or reacting to, changes in our business and our industry.

Furthermore, our borrowing facilities bear interests at fixed and variable rates. Any significant increase in prevailing interest rates or at the time of refinancing of our borrowing facilities could have a material and adverse effect on our business and results of operations.

There is no assurance that sufficient credit facilities will be available when needed or that, if available, such credit facilities will be obtained on terms that are acceptable to us. There is also no guarantee that the terms for credit facilities will be as favorable as those previously obtained. Our ability to obtain credit facilities for our requirements depends, among other things, on the prevailing economic conditions, our results of operations and the general condition of our industry. Inability to secure additional financing may materially and adversely affect our business, implementation of our business strategies and future plans as well as results of operations.

| 17 |

We may be exposed to risks associated with joint ventures or strategic alliances.

We may seek opportunities for growth through acquisitions, joint ventures, investments and partnerships. There is no assurance that any of these efforts will be successful. The acquisitions and investments that we may make, or joint ventures and partnerships that we may enter into, may expose us to additional business or operating risks or uncertainties, including but not limited to the following:

| ● | inability to effectively integrate and manage the acquired businesses; | |

| ● | inability of us to exert control over the actions of our joint venture partners, including any non-performance, default or bankruptcy of the joint venture partners; | |

| ● | time and resources expended to coordinate internal systems, controls, procedures and policies; | |

| ● | disruption to ongoing business and diversion of our management’s time and attention from its day-to-day operations and other business concerns; | |

| ● | risk of entering markets that we may have no or limited prior experience or dealing with new counterparties; | |

| ● | potential loss of key employees and customers of our existing business and acquired businesses; | |

| ● | risk that an investment or acquisition may reduce our future earnings; and | |

| ● | exposure to unknown liabilities. |

If there are disagreements between us and our joint venture partners (if any) regarding the business and operations of our joint ventures, there is no assurance that we will be able to resolve them in a manner that will be favorable to us. In addition, such joint venture partners may (i) have economic or business interests or goals that are inconsistent with that of ours; (ii) take actions contrary to our instructions, requests, policies or objectives; (iii) be unable or unwilling to fulfil their obligations; (iv) have financial difficulties; or (v) have disputes with us as to the scope of their responsibilities and obligations. Any of these and other factors may adversely affect the business and operations of our joint ventures, which may in turn adversely affect our business, financial condition, results of operations and prospects.

If we are unable to successfully implement our growth strategy or are unable to address the risks associated with our acquisitions, joint ventures, investments and partnerships, or if we encounter unforeseen difficulties, complications or delays frequently encountered in connection with the integration of acquired businesses and the expansion of operations, or fail to achieve acquisition synergies, our business, financial condition, results of operations and prospects may be materially and adversely affected.

We may be affected by any adverse impact on our reputation and goodwill.

We have built a reputation as one of the reliable providers of turnkey project solutions in Singapore to port, construction, civil engineering and underground foundation industries. Any negative publicity about us, our directors, our executive officers or our substantial shareholders, whether founded or unfounded, may tarnish our reputation and goodwill with our customers and suppliers. Such negative publicity may include, among other things, unsuccessful attempts in joint ventures, acquisitions or take-overs, or involvement in litigation, insolvency proceedings or investigations by government authorities.

| 18 |

Under these circumstances, our customers and suppliers may lose confidence in our business, our directors, our executive officers or our substantial shareholders, and this could affect our business relationships with them and their referral of new business opportunities to us. This may have a material and adverse impact on our business, results of operations and prospects.

Adverse conditions in the global financial markets and the general economy may adversely affect our business, financial condition, results of operations and prospects.

While our current business operates in Singapore, our business, financial condition, results of operations and prospects may be adversely affected by political, economic, social and legal developments in Singapore and globally that are beyond our control. Such political and economic uncertainties include, but are not limited to, the risks of war, terrorism, changes in interest rates, rates of economic growth, fiscal and monetary policies of the government, inflation, deflation, methods of taxation and tax policy, unemployment trends, and other matters that influence consumer confidence, spending and tourism.

Further, negative developments in geo-political events such as the US-China trade issues may bring uncertainty to the global economy. Any of such issues may lead to retaliatory and/or threat of retaliatory measures being imposed on the relevant countries. This may lead to volatility in the financial markets. The nature and extent of such changes are difficult to predict, and may bring uncertainty to the global economy and/or political environment. There is no assurance that we will be able to grow our business, or that we will be able to react promptly to any change in economic conditions. If we fail to react promptly to the changing economic conditions, our performance and profitability could be adversely affected. Our business, financial condition, results of operations and prospects may be materially and adversely affected if these conditions deteriorate in the future.

We cannot assure you that our future plans will be successful.