Table of Contents

As filed with the U.S. Securities and Exchange Commission on February 2, 2024.

Registration No. 333-276589

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

BBB Foods Inc.

(Exact Name of Registrant as Specified in its Charter)

| British Virgin Islands | 5411 | N/A | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

Río Danubio 51

Col. Cuauhtémoc

Mexico City, Mexico 06500

+52 (55) 1102-1200

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Cogency Global Inc.

122 East 42nd Street, 18th floor

New York, NY 10168

+1 (212) 947-7200

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

| S. Todd Crider Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 + 1 (212) 455-2000 |

Jorge U. Juantorena Manuel Silva Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 +1 (212) 225-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the U.S. Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling shareholders may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED FEBRUARY 2, 2024

PRELIMINARY PROSPECTUS

28,050,491 Class A common shares

BBB Foods Inc.

(incorporated in the British Virgin Islands)

This is an initial public offering of the Class A common shares, no par value, of BBB Foods Inc. We are offering 28,050,491 of the Class A common shares being sold in this offering.

Prior to this offering, there has been no public market for our Class A common shares. The estimated initial public offering price for the Class A common shares in this offering is expected to be between US$14.50 and US$16.50 per Class A common share. We intend to apply to list our Class A common shares on the New York Stock Exchange under the symbol “TBBB.” This offering is contingent upon receiving authorization to list our Class A common shares on the New York Stock Exchange.

Upon consummation of this offering, we will have three classes of common shares: Class A common shares, Class B common shares and Class C common shares. The rights of the holders of each class of our common shares will be identical, except with respect to voting, conversion, preemptive rights and transfer restrictions applicable to the Class B common shares and conversion and transfer restrictions applicable to our Class C common shares. Each Class A common share will be entitled to one vote. Each Class B common share will be entitled to 15 votes and will be convertible into one Class A common share automatically upon transfer, subject to certain exceptions. Each Class C common share will be entitled to one vote and will be convertible into one Class A common share in certain circumstances, including automatically upon certain transfers and the expiry of the transfer restrictions that will apply to the Class C common shares. Class B common shares and Class C common shares will not be listed on any stock exchange and will not be publicly traded. Holders of Class A common shares, Class B common shares and Class C common shares will vote together as a single class on all matters unless otherwise required by law and subject to certain exceptions set forth in our memorandum and articles of association.

Following this offering, our issued and outstanding Class B common shares, will represent 42.2% of the combined voting power of our outstanding common shares and 4.6% of our total equity ownership, assuming no exercise of the underwriters’ option to purchase additional Class A common shares from the selling shareholders. For further information, see “Description of Share Capital.” Bolton Partners Ltd., a vehicle affiliated with our founder, Chairman and Chief Executive Officer, will, directly or indirectly, own all of our Class B common shares and a portion of our Class C common shares. As a result, Bolton Partners Ltd. will beneficially own approximately 46.7% of the combined voting power of our outstanding common shares following this offering, assuming no exercise of the underwriters’ option to purchase additional Class A common shares from the selling shareholders, and will therefore have significant influence over matters requiring shareholder approval.

We are a “foreign private issuer” under the U.S. federal securities laws and, as a result, have elected to comply with certain reduced public company disclosure and reporting requirements. See “Risk Factors—Risks Relating to this Offering and Our Class A Common Shares—Our status as a foreign private issuer exempts us from certain of the corporate governance standards of the New York Stock Exchange, limiting the protections afforded to investors” and “Risk Factors—Risks Relating to this Offering and Our Class A Common Shares—As a foreign private issuer, we will have different disclosure and other requirements from U.S. domestic registrants. We may take advantage of exemptions from certain corporate governance regulations of the New York Stock Exchange, and this may result in less protection for the holders of our Class A common shares.”

Investing in our Class A common shares involves a high degree of risk. See “Risk Factors” beginning on page 28 of this prospectus.

| Per Class A Common Share |

Total | |||||||

| Initial public offering price |

US$ | US$ | ||||||

| Underwriting discount and commissions(1) |

US$ | US$ | ||||||

| Proceeds to us (before expenses)(2) |

US$ | US$ | ||||||

| (1) | See “Underwriting” for a description of all compensation payable to the underwriters. |

| (2) | See “Expenses of the Offering” for a description of all expenses (other than underwriting discounts and commissions) payable in connection with this offering. |

The selling shareholders have granted the underwriters the right to purchase up to an aggregate of 4,207,573 additional Class A common shares from us and the selling shareholders within 30 days from the date of this prospectus, at the initial public offering price, less underwriting discounts and commissions. We will not receive any proceeds from the sale of Class A common shares by the selling shareholders if the underwriters exercise their option to purchase additional Class A common shares from the selling shareholders in connection with this offering.

One or more funds and/or accounts managed by Capital International Investors (collectively, the “Cornerstone Investors”) have, severally and not jointly, indicated an interest in purchasing up to an aggregate of US$88 million in Class A common shares in this offering at the initial public offering price. The Class A common shares to be purchased by the Cornerstone Investors will not be subject to a lock-up agreement with the underwriters. Because these indications of interest are not binding agreements or commitments to purchase, the Cornerstone Investors may determine to purchase more, less or no shares in this offering or the underwriters may determine to sell more, less or no shares to the Cornerstone Investors. The underwriters will receive the same discount on any of our Class A common shares purchased by the Cornerstone Investors as they will from any other Class A common shares sold to the public in this offering.

Neither the U.S. Securities and Exchange Commission (the “SEC”), nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We expect to deliver the Class A common shares to purchasers against payment in New York, New York, on or about , 2024, through the book-entry facilities of The Depository Trust Company.

Global Coordinators

| J.P. Morgan | Morgan Stanley |

Joint Bookrunners

| BofA Securities | Scotiabank | UBS Investment Bank |

The date of this prospectus is , 2024.

Table of Contents

B BB Tiendas 3B

Table of Contents

We are the pioneers and leaders of hard discount grocery retail in Mexico. Our name, 3B means: “Bueno, Bonito y Barato” or “good, nice and affordable”. It summarizes our mission of offering irresistible value to budget savy consumers.

Table of Contents

Simple yet disruptive business model that drives customer savings and improve our value proposition.

Table of Contents

We have absolute confidence in our product quality, backed up by our no-questions-asked no-receipt-needed money-back return policy.

Table of Contents

Private label products are core to our strategy. High-quality and low prices enhance our customer’s value for money and allow us to maintain everyday low prices.

Table of Contents

Our more than 2,250 stores are strategically located close to our customers’ homes to provide a more efficient and cost-effective shopping experience.

Table of Contents

| Page | ||||

| iii | ||||

| vi | ||||

| 1 | ||||

| 28 | ||||

| 55 | ||||

| 57 | ||||

| 58 | ||||

| 59 | ||||

| 61 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

63 | |||

| 82 | ||||

| 113 | ||||

| 123 | ||||

| 126 | ||||

| 128 | ||||

| 145 | ||||

| 148 | ||||

| 153 | ||||

| 167 | ||||

| 168 | ||||

| 169 | ||||

| 170 | ||||

| 172 | ||||

| F-1 | ||||

None of we, the selling shareholders, the underwriters, nor any of our or their respective agents have authorized anyone to give any information or make any representation about this offering that is different from, or in addition to that contained in the prospectus, the related registration statement, any free writing prospectus prepared by or on behalf of us or we may refer to you. None of we, the selling shareholders, the underwriters, nor any of our or their respective agents will have or take responsibility and can provide no assurance as to the reliability of any other information that others may give you.

This prospectus is being used in connection with this offering of the Class A common shares in the United States and, to the extent described below, elsewhere. This offering is being made in the United States and elsewhere based solely on the information contained in this prospectus. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the Class A common shares. Our business, financial condition, results of operations, cash flows and prospects may have changed since the date on the front cover of this prospectus.

None of we, the selling shareholders, the underwriters, nor any of our or their respective agents are offering or seeking offers to purchase the Class A common shares in any jurisdiction where such offers or sales are not permitted. We have not undertaken any efforts to qualify this offering for offers and sales to the public in any jurisdiction outside the United States, and we do not expect to make offers and sales to the public in jurisdictions located outside the United States (including Mexico). However, we may make offers and sales outside the United States in circumstances that do not constitute a public offer or distribution under applicable laws and regulations.

This offering is being made in the United States and elsewhere based solely on the information contained in this prospectus.

i

Table of Contents

Notice to Investors Outside the United States. None of we, the selling shareholders, the underwriters, nor any of our or their respective agents have done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus in connection with this offering in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus or any such free writing prospectus must inform themselves about, and observe any restrictions relating to, this offering of our Class A common shares and the distribution of this prospectus and any such free writing prospectus outside the United States.

Notice to Mexican Investors. The Class A common shares have not been and will not be registered with the Mexican National Securities Registry (Registro Nacional de Valores, or the “RNV”) maintained by the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores, or the “CNBV”), and therefore, the Class A common shares may not be offered or sold publicly in Mexico or otherwise be subject to brokerage activities in Mexico, the Class A common shares may be offered and sold in Mexico, on a private placement basis, solely to investors that qualify as institutional or qualified investors pursuant to the private placement exemption set forth in Article 8 of the Mexican Securities Market Law (Ley del Mercado de Valores) and regulations thereunder. The information contained in this prospectus is solely our responsibility and has not been reviewed or authorized by the CNBV and may not be publicly distributed in Mexico. In making an investment decision, all investors, including any Mexican investor, who may acquire Class A common shares from time to time, must rely on their own examination of the Issuer and the terms of this offering, including the merits and risks involved.

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Certain Definitions

Unless the context otherwise requires, references in this prospectus to “Tiendas 3B,” the “Company,” “we,” “our,” “us” and similar terms are to BBB Foods Inc., together with its consolidated subsidiaries; references to the “Issuer” are to BBB Foods Inc., the company whose Class A common shares are being offered by this prospectus, and not to any of its subsidiaries; references to our “principal shareholder” are to Bolton Partners Ltd., a vehicle affiliated with Mr. K. Anthony Hatoum, our founder, Chairman and Chief Executive Officer; and references to the “selling shareholders” are to those shareholders listed as selling shareholders under “Principal and Selling Shareholders.”

The term “Companies Act” refers to the BVI Business Companies Act, 2004 (as amended) of the British Virgin Islands.

The term “sales” refers to our Revenue from sales of merchandise.

Currency Information

The term “Mexican peso” and the symbol “Ps.” refer to the legal currency of Mexico, and the term “U.S. dollar” and the symbol “US$” refer to the legal currency of the United States.

This prospectus contains translations of certain Mexican peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the Mexican peso amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rate indicated as of the dates mentioned herein or at any other rate. Unless otherwise indicated, we have translated Mexican peso amounts into U.S. dollars at the rate of Ps.17.62 per US$1.00, the exchange rate to pay foreign currency denominated obligations due on September 30, 2023 published by the Mexican Central Bank in the Mexican Federal Official Gazette (Diario Oficial de la Federación, or the “Official Gazette”). In addition, we have translated the the U.S. dollar amounts outstanding on the Promissory Notes and the Convertible Notes as of September 30, 2023 into Mexican pesos at the rate of Ps.17.62 per US$1.00 (the exchange rate to pay foreign currency denominated obligations due on September 30, 2023, published by the Mexican Central Bank in the Official Gazette) and as of December 31, 2022 at the rate of Ps.19.36 per US$1.00 (the exchange rate to pay foreign currency denominated obligations due on December 31, 2022 published by the Mexican Central Bank in the Official Gazette).

Financial Statement Presentation

The Issuer, the company whose Class A common shares are being offered in this prospectus, was incorporated on July 9, 2004 in the British Virgin Islands with company number 605635.

The financial information presented herein has been derived from our audited consolidated financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, together with the notes thereto, and our unaudited interim condensed consolidated financial statements as of September 30, 2023 and for the nine months ended September 30, 2023 and 2022, together with the notes thereto, prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), and included elsewhere in this prospectus.

The summary consolidated historical financial data should be read in conjunction with “Special Note Regarding Non-IFRS Financial Measures,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our audited consolidated financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, together with the notes thereto, and our unaudited interim condensed consolidated financial statements as of September 30, 2023 and for the nine months ended September 30, 2023 and 2022, together with the notes thereto, included elsewhere in this prospectus.

iii

Table of Contents

Special Note Regarding Non-IFRS Financial Measures

For convenience of investors, this prospectus presents certain non-IFRS financial measures, which are not recognized under IFRS. A non-IFRS financial measure is generally defined as one that purports to measure financial performance but excludes or includes amounts that would not be so adjusted in the most comparable IFRS measure. Specifically we present:

| • | EBITDA |

| • | EBITDA Margin |

For a discussion on the use of these measures and a reconciliation of the most directly comparable IFRS measures, see “Summary Financial and Other Information —Non-IFRS Financial Measures and Key Operating Metrics—Non-IFRS Financial Measures.”

Non-IFRS financial measures do not have standardized meanings and may not be directly comparable to similarly-titled measures adopted by other companies. These non-IFRS financial measures are used by our management for decision-making purposes and to assess our financial and operating performance, generate future operating plans and make strategic decisions regarding the allocation of capital. The non-IFRS measures presented herein have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results of operations presented in accordance with IFRS. Additionally, our calculations of non-IFRS measures may be different from the calculations used by other companies, including our competitors, and therefore, our measures may not be comparable to those of other companies.

Rounding Adjustments

We have made rounding adjustments to certain numbers presented in this prospectus. As a result, numerical figures presented as totals may not always be the exact arithmetic results of their components. Percentage figures included in this prospectus have not, in all cases, been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, certain percentage amounts in this prospectus may vary from those obtained by performing the same calculations using the figures in our audited consolidated financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, together with the notes thereto, and our unaudited interim condensed consolidated financial statements as of September 30, 2023 and for the nine months ended September 30, 2023 and 2022, together with the notes thereto, included elsewhere in this prospectus.

Market and Industry Data

This prospectus contains data related to economic conditions in the market in which we operate. The information contained in this prospectus concerning economic conditions is based on publicly available information from third-party sources that we believe to be reliable. Market data and certain industry forecast data used in this prospectus were derived from our management’s knowledge and our experience in the industry, internal reports and studies, where appropriate, as well as estimates, market research, publicly available information and industry publications. We obtained the information included in this prospectus relating to the industry in which we operate, as well as the estimates concerning market shares, through internal research, public information and publications on the industry prepared by official public sources, such as: the Mexican Central Bank (Banco de México), the World Bank, the National Minimum Wage Commission (Comisión Nacional de Salarios Mínimos), the Mexican Statistic and National Geography Institute (Instituto Nacional de Estadística y Geografía, or “INEGI”), the Central Intelligence Agency World Factbook, Euromonitor International Passport: Retail, 2023 edition, and NielsenIQ México Services.

Industry publications, governmental publications, and other market sources, including those referred to above, generally state that the information they include has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We have no reason to believe any of this information or these reports are inaccurate in any material respect and believe and act as if they are reliable. Neither we, the underwriters, nor their respective agents have independently verified it and they are subject to change based on various factors, including those discussed in the section entitled “Risk Factors.” Estimates of market and industry data are based on statistical models, key assumptions and limited data

iv

Table of Contents

sampling, and actual market and industry data may differ significantly from estimated industry data. In addition, the data that we compile internally, and our estimates have not been verified by an independent source. Information derived from management’s knowledge and our experience is presented on a reasonable, good faith basis. Except as disclosed in this prospectus, none of the publications, reports or other published industry sources referred to in this prospectus were commissioned by us or prepared at our request. Except as disclosed in this prospectus, we have not sought or obtained the consent of any of these sources to include such market data in this prospectus.

Information in this prospectus mentioning “Euromonitor” as a source is from independent market research carried out by Euromonitor International Limited but should not be relied upon in making, or refraining from making, any investment decision. Euromonitor’s forecasted compounded annual growth rate of the Mexican formal grocery market presented in this prospectus is based on Euromonitor’s forecasted growth of the offline grocery retail value, which is estimated by Euromonitor with retail selling prices to consumers, excluding value added tax, in U.S. dollars at year-on-year exchange rates and at current prices for the year.

Trademarks and Trade Names

We own or have rights to trademarks, service marks and trade names that we use in connection with the operation of our business, including our corporate name, logos, and website names. Other trademarks, service marks and trade names appearing in this prospectus are the property of their respective owners. Solely for convenience, some of the trademarks, service marks and trade names referred to in this prospectus are listed without the ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our trademarks, service marks and trade names.

v

Table of Contents

REFLECTIONS FROM OUR CEO

Intro

In 2004, out of the many countries I evaluated, I chose Mexico to start a Hard Discount grocery business. Whatever the metric I considered important for the business to thrive, Mexico always placed in the top three. So Mexico won. Having raised the funds to get started, I moved with my family to Mexico City in September 2004. At the time, I barely spoke Spanish and only knew a handful of people.

It helped to come in fresh and not assume you knew much. I asked a lot of questions to try to understand the Mexican consumer. I went to many neighborhoods in Mexico City, stood in the street with a clipboard and stopped anyone carrying shopping bags to ask them questions about their shopping habits and decisions. Surprisingly, most people talked to me (with my assistant translating), and when I asked, many agreed to host me in their homes for in-depth interviews. These talks with potential customers were invaluable. They allowed me to refine what we would ultimately offer in our first store, which opened in March of 2005. 2,200+ stores down the road, our customers are still telling us what is important to them and we are still listening.

My passion has always been to build things. I studied civil engineering. And I found that I love building businesses. From my previous startups, I have learned that: your business idea has to have at least one strong and sustainable competitive advantage, you have to pull together the strongest team that you can afford and that believes passionately in the idea, and you have to build a strong foundation from day one, one on which you can build that large business you are dreaming of. And that is what we did, our small initial team working out of a two-room office.

Our first store opening (Prohogar, March 2005). We all look much younger. Many of the faces in this photo are still with us. Eliza Zarraga, who started as a cashier, is now running her region. Javier Real, who started as a junior accountant, now runs the accounting department.

vi

Table of Contents

A simple and powerful business model

My introduction to the world of hard discount grocery retail was by chance. I was working in private equity at the time, and our fund invested in a hard discount grocer in Turkey called BIM. I fell in love with this business. As a model, it resonated with a lot of my core beliefs about what makes an enterprise successful:

| • | It is simple and shuns complexity and bureaucracy |

| • | It is laser focused on delivering value to the customer |

| • | It is one that believes that the best decisions are made where the action is |

| • | It empowers its people and rewards an entrepreneurial spirit |

| • | It is a good citizen helping build a better society |

I became convinced of its potential and that it was the right business model for Mexico, a growing retail market with favorable demographics. As such, I left the world of finance and decided to build yet another company. 3B is my most challenging and exciting build yet.

Our Customers

Our customers are what make our business possible.

Talking to our customers during my regular store visits is where I get my best insights. Almost all our good ideas have been sparked by talking to our customers. They are also the first ones to tell us what needs to be improved. And we listen intently.

We strive to give our customers every day the best value for their money in everything we carry. We will do everything to earn and keep their trust. This starts with only selling products of a quality we would gladly consume in our own homes. To that end, we back-up our products with our 100% money back guarantee—no questions asked.

Our Team and Culture

Preserving our can-do and scrappy startup culture has been and will continue to be top of my mind. With over 22,000 people today, our team is large and fast-growing.

Our challenge is to keep a nimble, efficient and cohesive organization while growing rapidly. I believed from day one and more so today that to meet this challenge one needs to:

| • | Instill a culture that despite distance and separation becomes the bond that holds everyone together. |

| • | Hire the best people you can. Go for talent density. Invest the time to develop and retain this talent. It is an investment that takes time to pay off but one that is critical and becomes a formidable competitive advantage. We would not be where we are today without it. |

| • | Trust that you have the right person for the job. Give them the resources and the power to get the job done. Delegate and let them thrive. |

| • | Build a decentralized organization and keep it as flat as possible. |

| • | Make information available to all and keep communications open at all levels. Anyone at any level at 3B can reach out to me directly. |

Our team and culture at 3B are the main driver of our success today and for the future.

vii

Table of Contents

Our private label suppliers

We rely on our private label suppliers to produce the best possible products at the best possible price. And we expect them to improve over time. Our relationship, by nature, is a long-term one. As our demand continually increases, our suppliers benefit and also grow rapidly. As we satisfy demand, control quality and develop products, together we need to make sure that we are thinking of the next production line, the next factory, the next improvement.

Partnering with a private label supplier is a bit like getting married and raising a family. You court, pick carefully, make sure you share the same beliefs, get married, and together design, produce and get to market products that offer great value for money. Together you make sure your products are successful and gain share over time. You plan for future improvements of all types whether in sourcing, manufacturing, logistics, quality or marketing. All this with one goal: to offer the customer the best possible product for their money.

We are lucky and privileged to have found such partners. And look forward for a fruitful relationship for many years to come.

The road ahead

This public offering is a significant milestone for our team and for those who believed in us early on. I am honored and excited to share what we have built with new investors and the public markets.

The road ahead is exciting and full of promise. We have barely scratched the surface of the $124 billion-dollar Mexican grocery market. The more we grow, the more opportunities present themselves for us to do better.

Looking forward, we will keep things simple, we will focus on what we do best and we will continue to be obsessed with improving on everything we do and on offering a continuously improving product to our customers.

We want to help the Mexican consumer live better and be a catalyst for improvement in the neighborhoods in which our stores are located.

We want to help our private label suppliers be successful and become major players.

We want to enchant our clients when they visit us.

We want to help our teammates develop into better people and business people.

We can do it because we believe in what we do, have built a great team, found the right partners, developed the expertise, and are battle tested.

Thank you for considering us.

K. Anthony Hatoum

viii

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. This summary may not contain all the information that may be important or relevant to you in making your investment decision. Before you decide to invest in our Class A common shares, we urge you to read this entire prospectus carefully, including our audited consolidated financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, together with the notes thereto, and our unaudited interim condensed consolidated financial statements as of September 30, 2023 and for the nine months ended September 30, 2023 and 2022, together with the notes thereto, included elsewhere in this prospectus and the information set forth under “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Overview

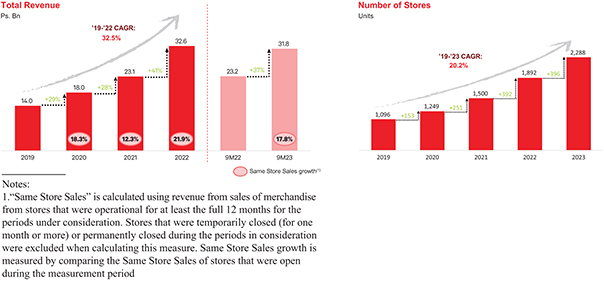

We are pioneers and leaders of the grocery hard discount model in Mexico and one of the fastest growing retailers in the country as measured by our sales and store growth rates. The 3B name, which references “Bueno, Bonito y Barato” – a Mexican saying which translates to “Good, Nice and Affordable”– summarizes our mission of offering irresistible value to budget savvy consumers through great quality products at bargain prices. From 2020 to 2022, our total revenue grew at a compounded annual growth rate (“CAGR”) of 34.4%, reaching Ps.32.6 billion (US$1.85 billion) for 2022, and our number of stores increased from 1,249 as of year-end 2020 to 2,288 as of year-end 2023, which represents a CAGR of 22.4%. Our total revenue for the 12-month period ended September 30, 2023 was Ps.41.2 billion (US$2.3 billion).

Our business model is simple yet disruptive: we offer a limited assortment of products that cover the daily grocery needs of our clients. We price our products to offer what is generally market-leading value for money: the lowest sustainable price in the market for a given quality. Our stores also offer convenience, since they are generally located within central neighborhoods that allow for daily visits and minimize transportation needs for our customers. Our customers visit us on average three to four times per week to fulfill one or two days of groceries.

The Tiendas 3B product range consists of approximately 800 stock keeping units (“SKUs”) of branded, private label and spot products.

| • | Branded products are well known national and international brand label goods that we offer at the lowest sustainable price in the market to attract customers and drive traffic. For 2022 and the nine months ended September 30, 2023, branded products represented 51.8% and 48.8% of our sales, respectively. |

| • | Private label products are products that we have developed ourselves and which we believe are of comparable or better quality than the equivalent branded alternative offered at our stores. For 2022 and the nine months ended September 30, 2023, private label products represented 42.8% and 45.4% of our sales, respectively. |

| • | Spot products are quality food and non-food products that we offer in addition to our regularly stocked products. These are offered in limited amounts and offer exceptional value. The selection changes every two weeks on average. For 2022 and the nine months ended September 30, 2023, our spot products represented 5.4% and 5.8% of our sales, respectively. |

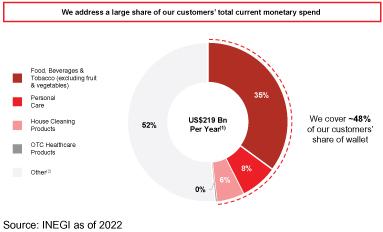

Our stores serve low-to-middle income households, which according to the National Survey of Household Income and Expenditure conducted by INEGI, spent US$219 billion in 2022, or 70.7% of the Mexican population’s total current monetary spend, defined by INEGI as a households’ expenditure on food, beverages

1

Table of Contents

and tobacco, personal care, house cleaning products and over the counter healthcare products, among other categories other than rent and financial expenditures. We believe that our business model, which focuses on both value and convenience, allows us to serve our target market better than incumbent competitors and maintain real and sustainable competitive advantages.

Due to our low number of SKUs and focus on serving daily grocery needs, we have been able to achieve a high ratio of sales per SKU and a ratio of 3.0 Payable Days to Inventory Days during 2022, driving significant cash flow generation. We are also able to benefit from a virtuous cycle, where the ever-increasing scale of our purchases per SKU allows us to negotiate increasingly lower prices with our suppliers and, in turn, we are able to transfer those savings to our customers, therefore increasing customer loyalty and our sales.

The Tiendas 3B business model is highly efficient, allowing us to operate with gross margins that are lower than those of leading grocery retailers in Mexico, based on publicly available information. The strength of our model is underpinned by our limited product assortment, our decentralized organization, and our culture that values efficiency and simplicity. Efficiency translates into savings that can be passed on to our customers.

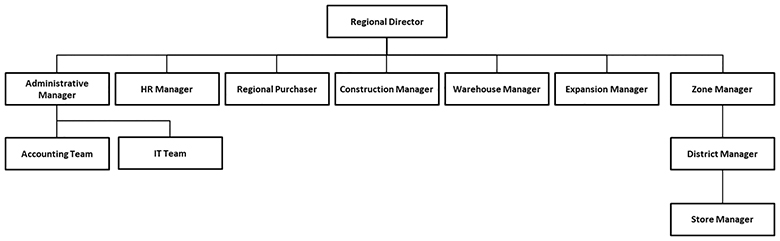

Our management is decentralized and organized into regions, each run by a regional director, and built around a distribution center that serves approximately 150 stores. Each region has sufficient functional resources to operate autonomously and efficiently. This structure, supported by nimble central headquarters, has enabled us to scale efficiently by allowing us to dynamically select new store locations in a constant pursuit of scale and expansion, while achieving positive gross and operating profit. Additionally, it enables suppliers to reach our decision makers quickly, fostering collaboration and accelerating the development of private label products.

Developing and retaining talent, as well as fostering a strong corporate culture, are key components of our business model and essential to sustaining our rapid growth rates and achieving efficiencies. We anticipate our personnel needs several years in advance and invest significant resources to ensure that we have the right talent at the right time.

We believe that the hard discount segment in Mexico has significant entry barriers for new participants, including: (i) the time and capital it takes to achieve scale and profitability given the inherent low gross margins of a hard discounter; (ii) the knowledge required to find competitive real estate and qualified personnel; (iii) the investment and know-how required to develop a meaningful private label product offering; and (iv) obtaining access to highly qualified senior management and experienced teams.

Our Business Model

Our business model is based on the following pillars:

| • | High rotation of products: By limiting our selection of products, we have been able to achieve a high turnover of sales per SKU, which makes us a relevant buyer of the products we sell, in turn allowing for favorable terms with suppliers. In 2022, we had 22 Inventory Days, 65 Payable Days and 0.1 Receivable Days, driving cash flow generation that supports our self-financed growth. |

| • | Strong private label offering: We own 93 different private label brands representing over 385 SKUs, that cover an array of food and non-food products. We outsource the manufacturing of these products to over 100 carefully selected local manufacturers with tested supply reliability and quality controls. We are generally able to offer our private label products at a lower cost than that of the branded products they compete with. Further, our customer satisfaction studies and product analysis indicate that the quality of our private label products is comparable, if not better, than the competing branded products. Our enduring and long-term relationships with our suppliers have created a robust supplier ecosystem that underpins the strength of our private label product offering. |

2

Table of Contents

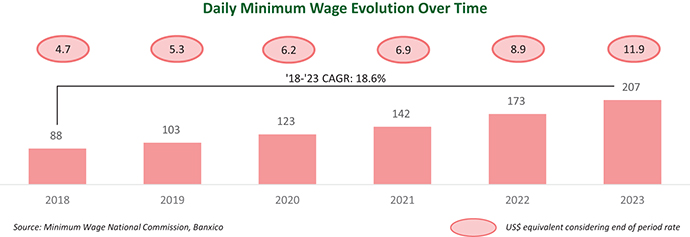

| • | Value for money: By consistently delivering and improving value for money to our customers, including through our private label products, we have earned their trust, increased our wallet share and attracted new customers. As a result, we have achieved Same Store Sales growth of 21.9%, 12.3%, 18.3% during 2022, 2021 and 2020, respectively, well above Mexico’s inflation rates of 7.8%, 7.4% and 3.2% for the same periods. |

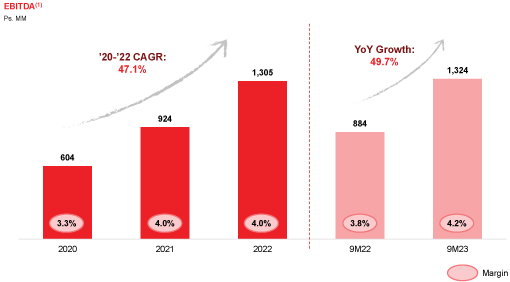

| • | Low-cost operations and virtuous cycle of efficiency: We have built a business model that allows us to generate operating profit while operating at market-leading low gross profit margins, by limiting our SKUs, decentralizing operations, focusing on simplicity, maintaining low capital expenditures per store, having a nimble and agile decision-making process, a horizontal management structure, and promoting a strong culture of efficiency. This allows us to offer and sustain everyday low prices to our customers. Our gross profit margin for 2022 was 15.1%, compared to gross profit margins of 28.1% of La Comer, 23.4% of Walmart de México (“Walmex”), 22.9% of Chedraui and 22.1% of Soriana. For the nine months ended September 30, 2023, our gross profit margin was 15.8%. |

| • | Rapid expansion: In 2023, we averaged a new store opening every 22 hours, which is faster than any other grocery retailer in Mexico. Our operations actively involve our regional personnel in the store opening process, with the goal of locating and securing the most attractive locations for new stores. Further, our low capital expenditure needed per new store which, combined with the attractive cash flow generation capacity of our stores, allows us to achieve attractive Payback Periods on average. In addition, our negative working capital dynamics allow us to self-fund these investments. We are systematic in our approach to opening stores, and our recent vintages are showing a faster sales ramp-up and higher profitability vis-à-vis our older vintages for the same comparable period. With an estimated white space for at least 12,000 additional Tiendas 3B stores in Mexico, we are constantly looking to increase our number of stores and expand into new regions. |

The Grocery Retail Industry in Mexico

Large and growing market

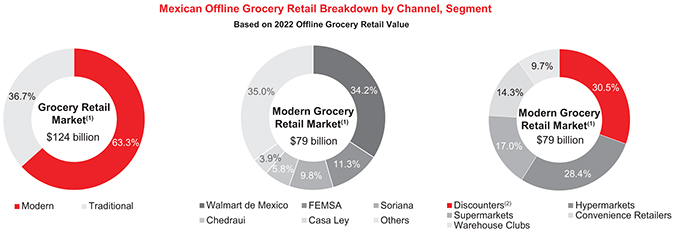

The Mexican formal grocery market had approximately US$124 billion annual sales for 2022 and is projected to grow at a 7.6% compounded annual rate from 2022 to 2027, according to Euromonitor. The market is expected to reach US$179 billion in annual sales by 2027.

Fragmented market: One dominant player but otherwise highly fragmented

The grocery market in Mexico is best viewed in two channels: the Modern (or organized) channel, which is a sub-set of the formal grocery market and which we define to include discounters, hypermarkets, supermarkets, convenience stores and warehouse clubs, and the Traditional (or informal) channel, which we define to include, among others, local grocers and food, drink, and tobacco specialty stores. The Modern channel, which we calculate represented US$79 billion in annual sales for 2022 based on data from Euromonitor, can be further divided into full-price retailers and discounters (including soft discounters and hard discounters, such as Tiendas 3B). Discounters represented 30.5% of the Modern channel for the year ended December 31, 2022, according to data from Euromonitor.

Walmex is the dominant player in the Modern channel, representing 34.2% of that channel’s total sales for 2022 based on data from Euromonitor. Walmex’s most successful format is Bodega Aurrera, a discounter which represented 16.7% of sales in the Modern channel. Beyond that, the market is highly fragmented.

3

Table of Contents

The hard discount business model

Hard discount is still a nascent business model in Mexico within the Modern channel. According to NielsenIQ, hard discounters, such as Tiendas 3B and Tiendas Neto, only represented 2.3% of sales in the Mexican grocery market for 2022. Although large retail players, such as Walmex (through Bodega Aurrera Express) or FEMSA (through Tiendas BARA), have presence in discount formats, since inception, Tiendas 3B has successfully competed with those formats as well as with other established grocery players as shown by our growth track record.

Hard discount grocery retailers, like ourselves, are different from other retailers in the Modern channel. The hard discount model focuses on a limited assortment of high value for money, high rotation branded and private label products that address the consumer’s essential daily needs. A hard discounters operations seek to be highly efficient and simple, with streamlined logistics, distribution, storefront operations and standardized no-frill store layouts with flexible locations. As a result of the efficiencies in the business model, hard discounters who achieve scale tend to have low gross margins and yet can achieve high returns on invested capital.

Tiendas 3B’s addressable market

Our stores serve low-to-middle income households, which according to the National Survey of Household Income and Expenditure conducted by INEGI, spent US$219 billion in 2022, or 70.7% of the Mexican population’s total current monetary spend. According to data from INEGI, approximately 48.4% of annual average Mexican household total current monetary spend within the second to ninth income decile is destined to food (excluding fruits and vegetables), beverages and tobacco, personal care products, house cleaning products and over the counter medicines. Our product offering covers all of these categories. Further, approximately 35.1% of annual average Mexican household current monetary spend within the second to ninth income decile is destined to food (excluding fruits and vegetables) and beverage products alone, such as the ones we sell.

|

|

|

Notes: |

Notes: | |||

| 1. Considers an exchange rate of Ps$19.36 per USD 2. Each household has on average 3.43 members 3. Range considers average income by income decile |

4. Excludes non-monetary expenses with an estimated value of US$84.9 Bn. Non-monetary expenses include self-consumption, payments in kind, gifts, and the estimated rent households would have had to pay if they did not own their house |

1. Total current monetary spend for income deciles II to IX 2. Includes transportation & communications, education, housing, clothing, fruit and vegetables, and healthcare (excl. OTC products) |

4

Table of Contents

Tiendas 3B’s whitespace opportunity

We believe that there is a large whitespace opportunity for Tiendas 3B. This opportunity will be driven by market expansion as a result of favorable demographic trends, the under-penetration of hard discount stores in the Mexican grocery market, and hard discount’s growing appeal with the Mexican consumers. Tiendas 3B’s addressable market is large and poised for continued growth.

Based on our estimates at December 31, 2022, we believe there is a potential to open at least 12,000 additional Tiendas 3B stores in Mexico at current population levels in urban areas alone. We have mapped out whitespace by identifying communities with over 10,000 inhabitants as our stores are designed to adequately serve that number of people in a trade area of 800 meters from each store. This would represent almost a six-fold increase over our 2,288 stores as of December 31, 2023.

Hard discount in Mexico has significant growth potential when compared to other countries

The hard discount retail market in Mexico appears to be underpenetrated when compared to other countries with more established hard discount retail markets.

5

Table of Contents

According to NielsenIQ, in 2022, the hard discount market in Mexico represented only 2.3% of NielsenIQ’s measurement of the Mexican grocery market. In contrast, grocery retailers which we consider hard discounters in Germany (i.e., Aldi and Lidl), in Poland (i.e., Biedronka, Aldi and Lidl), and in Turkey (i.e., BIM and A101), which are countries with succesful and mature hard-discount markets, represented 23.6%, 33.6% and 24.1%, respectively, of their corresponding grocery market’s annual sales in 2022 based on data from Euromonitor.

Source: Euromonitor, NielsenIQ, Company Information, INEGI, World Bank

Notes:

| 1. | Considers Biedronka, Lidl and Aldi |

| 2. | Considers BIM and A101 |

| 3. | Considers Aldi and Lidl |

| 4. | Information from NielsenIQ “Hard Discounters” report |

Although the Mexican food retail market has other features that differentiates it from that of Germany, Poland and Turkey at the time the hard discount model was introduced in those countries, including having a highly developed and efficient food retailers, we believe that these markets exemplify how the hard discount model can prosper even as countries grow richer. Initially, similar to Mexico, German and Polish consumers were attracted to hard discount given the great value proposition. At the time hard discount was introduced in Germany (1946 following the Second World War), in Poland (1990 following the fall of the Soviet Union) and Turkey (in 1995), German real GDP per capita, adjusted for inflation to date and price differences between countries was US$7,195, Poland’s was US$8,150 and Turkey’s was US$9,963. Even as per capita income ramped up in those countries, hard discounter penetration continued to increase. Although there is no assurance that the Mexican market will develop in the same fashion, we believe Mexican consumers are increasingly attracted to the hard discount model’s value proposition.

Our Competitive Strengths

Since inception, we have successfully competed with well-established grocery retailers and our sustainable competitive advantages have allowed us to thrive. We believe that as we continue to grow, our advantages will become more pronounced:

Rapid store expansion capacity

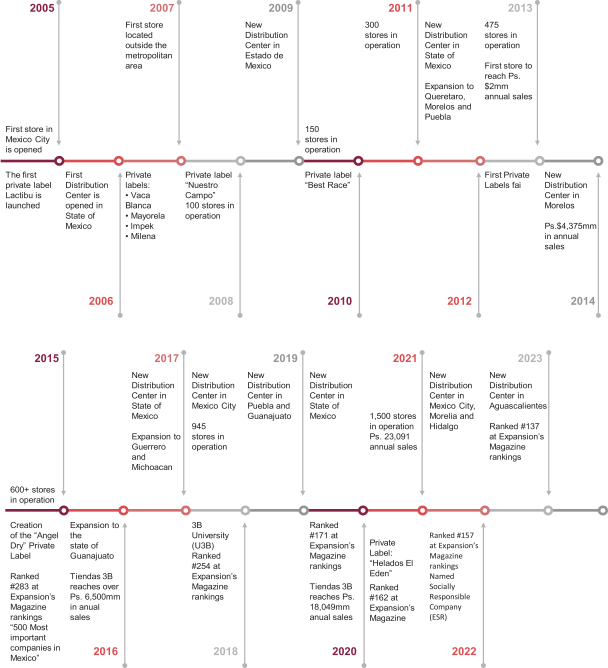

We opened our first store in February 2005, and as of December 31, 2023, we had 2,288 stores and 14 distribution centers. As our sales have grown, the pace of our store openings has accelerated naturally, as

6

Table of Contents

illustrated in the chart below. We had 392 net new store openings during 2022 and 396 net new store openings during 2023, which translates into a new store opening every 22 hours.

We are the fastest growing retailer in Mexico in terms of sales, based on a comparison of our sales figures with Euromonitor’s analysis of sales growth for the fastest growing retail players in Mexico. As shown below, Tiendas 3B has significantly outpaced incumbent retailers, with a total revenue CAGR of 34.4% from 2020 to 2022.

| Source: Based on a comparison of Tiendas 3B’s sales figures with Euromonitor’s analysis of sales growth for competitors

Notes: |

| 1. Considers Tiendas 3B’s total revenue CAGR. CAGRs of incumbent retail players according to Euromonitor’s estimated offline grocery retail value estimated with retail selling prices to consumers, excluding value added tax, in Mexican pesos and at current prices for the year 2. Only includes Walmart Supercenter format in Mexico |

7

Table of Contents

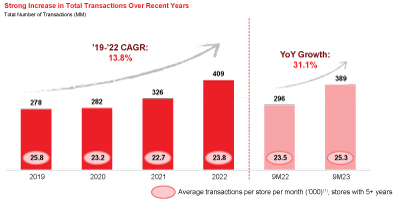

Sales growth underpinned by strong fundamentals

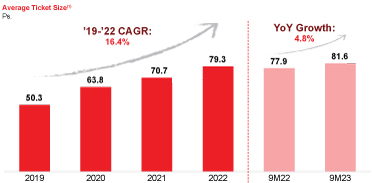

Our Same Store Sales growth and expansion are underpinned by strong store level fundamentals. Although growth through geographic expansion and store openings is a strong component of our expansion strategy, we believe our model is sustainable and scalable given the combined effect of growing average ticket size and a growing volume of transactions per store at our existing stores.

|

|

|

|

Notes: |

Notes: | |

| 1. We calculate Average Ticket Size by dividing revenue from sales of merchandise by total number of transactions |

1. Average transactions per store per month, only considering stores from vintages with five or more years of operations |

High rotation of our inventory to generate significant negative working capital

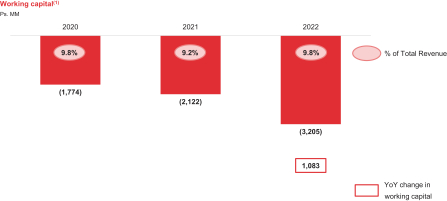

By focusing on high rotation items and limiting them to one-brand one-size, curated to satisfy most grocery needs of the average Mexican family, we are able to keep low Inventory Days. In 2022, we had 22 Inventory Days.

Our supplier payment terms (65 Payable Days for 2022) and low Inventory Days (22 Inventory Days for 2022), create a favorable negative working capital cycle that has enabled us to self-fund our rapid expansion. Our working capital for 2021, 2022 and the nine months ended September 30, 2023 was Ps.(2,121,704) thousand, Ps.(3,205,200) thousand and Ps.(4,243,026) thousand, respectively. Cash flows provided by our operating activities were Ps.1,082,703 thousand, Ps.1,366,308 thousand, Ps.2,116,335 thousand and Ps.1,942,839 thousand for 2020, 2021, 2022 and the nine months ended September 30, 2023, respectively, compared to our capital expenditures of Ps.297,028 thousand, Ps.532,173 thousand, Ps.1,122,877 thousand and Ps.940,202 thousand for 2020, 2021, 2022 and the nine months ended September 30, 2023, respectively.

|

Notes: |

||

| 1. We calculate working capital as total current assets minus total current liabilities. | ||

8

Table of Contents

Lean operational model designed to maximize efficiency and minimize costs

Our limited assortment of products allows us to simplify and optimize operations leading to low sales expense as a percentage of total revenue, which was 10.6% for 2022 and 10.8% for the nine months ended September 30, 2023.

Every aspect of our operations has been carefully optimized for efficiency. We reduce working hours and operating costs by designing our products and packaging with efficiency in mind, choosing the right truck sizes and equipment, making judicious use of technology and efficiently distributing refrigerated goods, store orders, and managing our proprietary logistics infrastructure. For example, we reduce time and costs from stocking shelves by selling directly from the box (usually lidless) that arrives from our distribution centers. Our trucks and stores are designed to allow one driver to unload a store delivery single-handedly in 30 minutes or less and our distribution centers are strategically located to allow optimal re-stocking efficiency and route planning.

Standard supermarkets, with a larger number of SKUs are more complex and costly to run. They need higher gross margins to sustain their operations. By being able to operate at lower costs, we can achieve positive operating profit even with low gross margins, and can offer sustainable lower prices, which we believe is very hard to replicate for traditional grocery retailers.

Significant purchasing power

As our sales have grown, so has our purchasing power. We believe we can buy at very competitive prices since our sales are concentrated in a relatively lower number of SKUs. This allows us to continually lower our purchase costs, improve our payment terms and develop strong supplier relationships, which in turn enables us to transfer generated savings on to our customers. Further, we cooperate closely with our private label suppliers to help them negotiate better terms on their own supplies and raw materials, which also translates into savings for our customers.

Building and constantly reinforcing customer trust and loyalty

We have built enduring customer relationships based on trust in our pricing and quality. We believe that this trust is a cornerstone of our business, allowing us to accelerate our sales growth and eventually expand into higher ticket items and additional product categories (so long as they also deliver our characteristic value-for-money). We offer a no-questions-asked no-receipt-needed money-back return policy on all products we sell. This guarantee helps build trust and encourages our customers to try our private label products.

Decentralized and nimble organization that is close to the action

We have a decentralized and lean organizational structure built around autonomous regions each led by a regional director. As of December 31, 2023, we had 14 operating regions. Each region consists of approximately 150 stores supported by a single distribution center with functional support areas, such as human resources, real estate, logistics, IT and regional purchasing and accounting. For example, the regional directors decide which new stores to open (within company guidelines) without requiring headquarters’ approval. All regions are similarly sized and configured in terms of operations and the model is readily replicable. As each region increases the number of stores it operates beyond 150 and up to 200, a new region is formed in adjacent geographies and stores are shifted accordingly to optimize logistics.

We believe this approach has many benefits. Decisions are closer to the action and therefore nimble. There is less bureaucracy. Opening new regions is rapid, efficient, and cost effective. Benchmarking among similar regions makes managing the entire business efficient and allows us to maintain a small central office even at scale.

9

Table of Contents

We invest significantly in human resource development and our culture. We believe this is essential to maintaining sustainable profitable growth and managing a decentralized structure. We achieve these goals by: long-term planning, a belief in the concept of talent density, and investing in in-person training, which is supplemented by more than 100 training modules found in our online “Universidad 3B,” which is designed to foster a strong cultural affinity and operational excellence across the organization.

Founder-led management team with leading industry expertise

We are a founder-led company with a solid management team, the majority of which has been working together for more than 15 years, most since inception. Our management team has 130+ years of combined experience in the retail and hard discount industry, has extensive knowledge of the Mexican grocery market, and has held relevant positions within local and international players. The trajectory and continuity of our management team contributes to a strong and stable corporate culture that is both customer and employee-centric. Our management team has developed highly specialized know-how that we believe is hard to replicate and a key differentiating factor that has propelled our success.

Our Strategy

Unrelenting focus on lean operating model to support profitable growth

Our business model has proven to be sustainable and resilient through different economic cycles, which we expect to continue. We believe we still have room to continue to improve our operating margins through the scalability of our platform. We have sustainably low operating costs as a percentage of sales, driven by scale, rigorous cost discipline, the judicious use of technology, making our processes even more efficient, and better integrating with our private label suppliers. We believe our current operational structure will allow us to continue supporting our expansion efforts at marginal incremental costs.

Rapidly expanding number of stores in contiguous regions, while maintaining low investment requirements per new store

We aim to open stores in places that are convenient for our customers, most of which access our stores on foot. We follow a disciplined approach to our geographic expansion without compromising our supply and distribution capabilities. Our standardized format and requirements assure that our capital requirements for new stores remain low, an important component as we fund our rapid expansion.

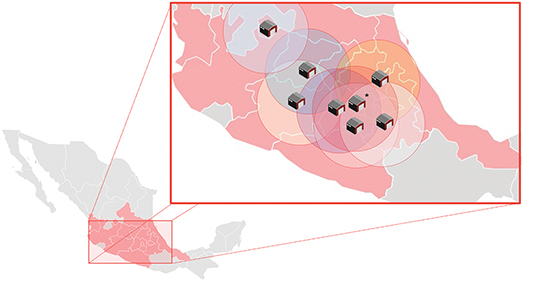

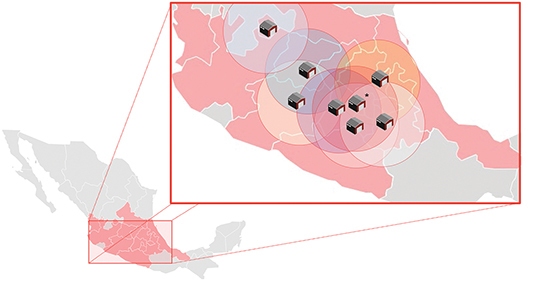

As of December 31, 2023, our stores were concentrated in 15 states in the central region of Mexico, including: Mexico City, State of Mexico, Hidalgo, Puebla, Tlaxcala, Morelos, Queretaro, Guanajuato, Michoacán, Guerrero, Veracruz, Aguascalientes, Nayarit, Jalisco, and San Luis Potosí. This geographic footprint has resulted from progressive expansion as we add new distribution centers to support stores in new areas, in each case targeting critical density to support the efficiencies of our structure. Our store location map reflects our disciplined expansion approach.

10

Table of Contents

| (*Mexico City Metropolitan Area has 7 DCs) Illustrative DCs coverage areas |

Developing new private label product lines

We intend to consolidate our private label leadership by continuing to develop new private label product lines that offer higher value for money than branded alternatives to our customers. We work closely with over 100 local suppliers of our private label products to develop new and innovative product lines. Our close relationship and integration allow us to adapt our offering to changing customer needs and preferences. As we increase our private label sales penetration going forward, we will drive greater value to our customers, which we expect will translate into sales growth, while also increasing control of our margins and improving our profitability.

Our frequent client interactions, extensive market studies, and ongoing testing of products, allow us to understand and anticipate customer preferences, and to meet their evolving needs. Our team of 30 purchasers as of September 30, 2023 work hand in hand with our suppliers to continuously innovate and improve our portfolio of products.

We help our suppliers grow alongside us by providing transparency of our growth plans, paying them on time and facilitating access to our wide network of other supplier relationships. We see suppliers as strategic partners because we often find opportunities to develop brands and product presentations, aiming to increase the quality and improve the price of our products. We also help suppliers by sharing best practices we see from suppliers of other of our products (for example access to better packaging and labeling alternatives), which creates efficiencies across our business. Our annual private label supplier fair assists this exchange of ideas and solidifies our supplier ecosystem.

Increasing our sales of “Los Irrepetibles”

We intend to increase the sales contribution of “Los Irrepetibles,” our spot product offering that includes grocery and non-grocery products such as, electronics, apparel, home goods, and others. We offer a changing selection of approximately 50 spot products every two weeks on average. These products offer notably high value for money and add a treasure hunt factor to the shopping experience. We call them “Los Irrepetibles” because they are offered at prices so low that they will not be “repeated” (replenished) once we sell out.

Part of our strategy is to selectively offer higher ticket spot items that still offer tremendous value for money. We are currently conducting tests on a limited scale to assess our customers’ acceptance of these price points and product price elasticity. Going forward, we plan to expand our spot product purchasing division to improve purchasing capacity and product sourcing.

11

Table of Contents

Introducing new categories of products and services

We plan to selectively introduce new product categories to meet our customers’ needs. At any moment we are actively testing several new product categories. As a result of these efforts, we recently introduced the beauty category in our stores. Additionally, we plan to expand our assortment in certain categories, including ice creams and fresh and frozen meats. Based on our internal analysis, we believe there is sufficient demand to introduce SKUs to our offering and drive additional sales and wallet penetration.

Additionally, we believe that our increasingly ubiquitous store footprint can be leveraged to increase the services we offer to our customers at our locations. Currently we offer utility and service payments, top-ups, amongst others. We see opportunities to expand our service offering given our customers’ frequent store visits each week.

Recent Developments

Our results for the year ended December 31, 2023 are not yet available as of the date of this prospectus. We expect to finalize our consolidated financial results as of and for the year ended December 31, 2023 after this offering is completed.

Based upon the preliminary information available to us as of the date of this prospectus, we expect our consolidated financial results as of and for the year ended December 31, 2023 to be substantially consistent with the trends and performance reflected in the historical financial information included in this prospectus.

The preceding statement is based on our reasonable estimates and preliminary unaudited information available as of the date of this prospectus. Internal reviews and procedures necessary to complete our consolidated financial results as of and for the year ended December 31, 2023 are ongoing as of the date of this prospectus and they have not been audited, reviewed, examined or compiled by PricewaterhouseCoopers, S.C. Management is responsible for the preparation and presentation of such preliminary information. PricewaterhouseCoopers, S.C. expresses no opinion or any other form of assurance on such preliminary information referred to above. Accordingly, we cannot provide any assurances that our consolidated financial results as of and for the year ended December 31, 2023 will be consistent with the trends and financial and operating performance shown in the financial information included in this prospectus, or that such results (or the market perception of such results) will not adversely affect the trading price of our Class A common shares.

Summary of Risk Factors

An investment in our Class A common shares is subject to a number of risks, including risks relating to our business and industry, risks related to Mexico and risks related to this offering and our Class A common shares. Please read the information under “Risk Factors” for a more thorough description of these and other risks. Below is a summary of the principal risks we face:

| • | economic factors reducing our customers’ spending, impairing our ability to execute our strategies and initiatives, and increasing our costs and expenses, resulting in materially decreased sales or profitability; |

| • | failure to achieve or sustain our strategies and initiatives, including those relating to store openings, sourcing and supplier relationships, private label product development and cost initiatives, inventory management, supply chain, store operations, expense reduction and technology; |

| • | risks associated with our private label products, including, but not limited to, our level of success in improving their margins; |

| • | our ability to successfully identify, lease, obtain permits for and adapt real estate spaces for stores and distribution centers; |

| • | our ability to renew our existing leases on terms that are not detrimental to us; |

12

Table of Contents

| • | competitive pressures and changes in the business environment and the geographic and product markets where we operate, including, but not limited to, pricing, promotional activity, expanded availability of mobile, web-based and other digital technologies, and alliances or other business combinations; |

| • | our failure to attract, train and retain qualified employees while controlling labor costs and other labor issues; |

| • | our loss of key personnel, including regional management, or inability to hire additional qualified personnel; |

| • | sustainability of negative levels of working capital; |

| • | product liability, product recall or other product safety or labeling claims; |

| • | risks and challenges associated with sourcing merchandise from suppliers, including, but not limited to, those related to international trade; |

| • | failure to successfully manage inventory balances; |

| • | a significant disruption to our distribution network, the capacity of our distribution centers or the timely receipt of inventory, or delays in constructing or opening new distribution centers; |

| • | damage or interruption to our information systems as a result of external factors, staffing shortages or challenges in maintaining or updating our existing technology or developing or implementing new technology; |

| • | failure to maintain the security of our business, customer, employee or vendor information or to comply with privacy laws; |

| • | the impact of changes in or noncompliance with laws and governmental regulations and requirements (including, but not limited to, those relating to environmental compliance, product and food safety or labeling, information security and privacy, labor and employment, employee wages, and those governing the sale of products, as well as tax laws, the interpretation of existing tax laws, or our failure to sustain our reporting positions, in each case negatively affecting our tax rate) and developments in or outcomes of private actions, class actions, multi-district litigation, arbitrations, derivative actions, administrative proceedings, regulatory actions or other litigation; |

| • | incurrence of material uninsured losses, excessive insurance costs or accident costs; |

| • | deterioration in market conditions, including market disruptions, limited liquidity and interest rate fluctuations, or changes in our credit profile; |

| • | risks related to public health crises such as the COVID-19 outbreak, including but not limited to, the effects on our supply chain, distribution network, store and distribution center growth or customers’ spending patterns; |

| • | natural disasters, unusual weather conditions (whether or not caused by climate change), pandemic outbreaks or other health crises, acts of violence or terrorism, and global political events; |

| • | changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement (the “USMCA”) to which Mexico is a party; and |

| • | difficulties you may experience because we are a British Virgin Islands company in obtaining or enforcing judgments against us or our executive officers and directors in the United States. |

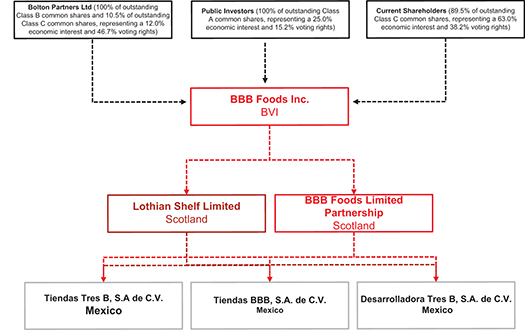

Our Corporate Structure

The Issuer is a holding company incorporated in the British Virgin Islands. The Issuer has no material operations of its own and substantially all of its operations are conducted through the Issuer’s Mexican subsidiaries. Investors in the Class A common shares are purchasing equity interests in the British Virgin Islands holding company, and not in such Mexican subsidiaries. We indirectly hold 100% equity interests in our Mexican subsidiaries.

13

Table of Contents

The following chart and the information set forth in the following paragraph presents our corporate structure, including our principal shareholder and principal subsidiaries immediately after the completion of this offering, assuming no exercise of the underwriters’ option to purchase additional Class A common shares.

Bolton Partners Ltd., our principal shareholder, will beneficially own approximately 46.7% of the combined voting power of our outstanding common shares following this offering, and will therefore have significant influence over matters requiring shareholder approval. However, the foregoing does not include Class C common shares that will be held by our principal shareholder and our directors and officers in respect of both unvested and vested (but currently unexercisable) stock options or delayed-delivery awards under the Liquidity Event Bonus Plan and the Founder Liquidity Bonus, as applicable. Taking into account such Class C common shares which our principal shareholder, directors and officers will be entitled to receive at later dates, and assuming net settlement at their respective strike prices, our principal shareholder would beneficially own approximately 45.4% of the combined voting power of our outstanding common shares following this offering. See “Principal and Selling Shareholders.”

Corporate Information

We were incorporated on July 9, 2004 under the laws of the British Virgin Islands with company number 605635. Our principal executive offices are located at Río Danubio 51, Col. Cuauhtémoc, Mexico City, Mexico 06500. Our registered office is located at Commerce House, Wickhams Cay 1, P.O. Box 3140, Road Town, Tortola VG1110, British Virgin Islands. Our website is www.tiendas3b.com. The information contained in, or accessible through, our website is not incorporated into this prospectus or the registration statement of which it forms a part and does not form part of, this prospectus, and you should not consider such information in deciding whether to invest in our Class A common shares.

Conventions that Apply to this Prospectus

Except as otherwise indicated or the context requires, all information in this prospectus assumes:

| • | the filing and amendment and restatement of our memorandum and articles of association and the redesignation of our existing shares into Class A common shares, Class B common shares and Class C common shares, each of which will occur immediately prior to the completion of this offering, and which we refer to as the “IPO Reorganization”; |

14

Table of Contents

| • | an initial public offering price of US$15.50 per Class A common share, the midpoint of the estimated offering price range per Class A common share set forth on the cover page of this prospectus; and |

| • | a 3-for-1 forward share split of our common shares that will be effected immediately prior to the completion of this offering; and |

| • | no exercise by the underwriters of their option to purchase up to 4,207,573 additional Class A common shares from the selling shareholders in connection with this offering. |

In addition, except as otherwise indicated or the context requires, this prospectus does not reflect the issuance of any common shares issuable upon exercise of options granted under our 2004 Option Plan, any common shares reserved for issuance under our Equity Incentive Plan, or any Class C common shares awarded under the Liquidity Event Bonus Plan and the Founder Liquidity Bonus. As of the date of this prospectus, and after giving effect to the IPO Reorganization:

| • | 14,395,408 Class C common shares are issuable upon the exercise of options granted, 8,565,408 of which are subject to fully vested options; |

| • | 8,300,000 Class A common shares have been reserved for issuance under our Equity Incentive Plan adopted in connection with this offering; |

| • | 4,087,408 Class C common shares will be awarded under the Founder Liquidity Bonus to Bolton Partners Ltd.; and |

| • | 7,500,000 Class C common will be awarded under the Liquidity Event Bonus Plan, 6,000,000 of which will be awarded to our principal shareholder and the remainder to the direct reports of the Chief Executive Officer. |

All of such Class C common shares are subject to the restrictions on transfer of Class C common shares described under “Description of Our Share Capital—Class C Common Shares” or, in the case of vested options and Class C common shares awarded under the Founder Liquidity Bonus and Liquidity Event Bonus Plan, subject to restrictions on exercise and delayed delivery, respectively, for the same time frame as such restrictions on transfer (subject to certain exceptions). For additional information, see “Management—2004 Option Plan,” “Management—Liquidity Event Bonus Plan” and “Management—Founder Liquidity Bonus.”