UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

| Not applicable | ||

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) |

+65 6322 4392

(Address of Principal Executive Offices)

Rohith Murthy

Chief Executive Officer

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”):

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The Nasdaq Stock Market LLC (The | ||||

| The Nasdaq Stock Market LLC (The |

Securities registered or to be registered pursuant to Section 12(g) of the Exchange Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Exchange Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2024, there were

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If this report is an annual or transition report,

indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act

of 1934. Yes ☐

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange

Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting over Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report. Yes ☐ No

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| US GAAP | ☐ | ☒ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check

mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

TABLE OF CONTENTS

i

CONVENTIONS AND FREQUENTLY USED TERMS

Unless otherwise indicated or unless the context otherwise requires in this annual report on Form 20-F:

“Assignment, Assumption and Amendment Agreement” means the amendment, dated May 25, 2023, to that certain warrant agreement, dated October 15, 2020, by and among the Company, Bridgetown and Continental Stock Transfer & Trust Company (the “Existing Warrant Agreement”), pursuant to which, among other things, Bridgetown assigned all of its rights, interests and obligations in and under the Existing Warrant Agreement to the Company;

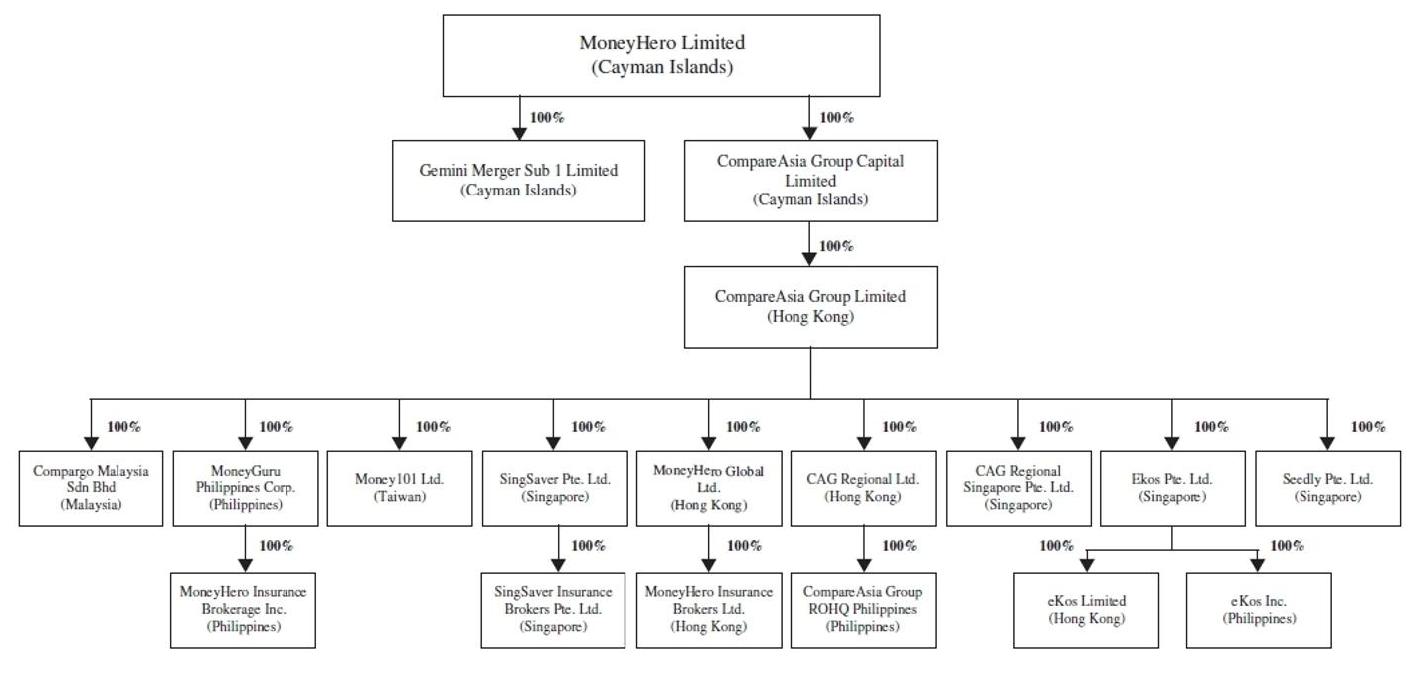

“Bridgetown” means Bridgetown Holdings Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands;

“Bridgetown Merger Sub” means Gemini Merger Sub 1 Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands;

“Business Combination Agreement” means the business combination agreement, dated May 25, 2023, (as it may be amended, supplemented, or otherwise modified from time to time), by and among the Company, Bridgetown Merger Sub, CGCL Merger Sub, Bridgetown and CGCL;

“Bridgetown Public Warrants” means the warrants issued to holders of Class A ordinary shares of Bridgetown as part of the units issued in Bridgetown’s initial public offering;

“Cayman Companies Act” means Cayman Companies Act (As Revised);

“CGCL” means CompareAsia Group Capital Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands, or as the context requires, CompareAsia Group Capital Limited and its subsidiaries and consolidated affiliated entities;

“CGCL Class A Ordinary Shares” means the shares of CGCL designated as Class A ordinary shares, of a nominal or par value of $0.0001, each with one vote per share;

“CGCL Class A Warrant” means warrants to purchase CGCL Class A Ordinary Shares issued pursuant to the CGCL Class A Warrant Instrument, dated October 14, 2022, as amended;

“CGCL Merger Sub” means Gemini Merger Sub 2 Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands;

“China” or “PRC,” in each case, means the People’s Republic of China, excluding, solely for the purpose of this annual report, Taiwan. The term “Chinese” has a correlative meaning for the purpose of this annual report;

“Class A Ordinary Shares” means the Class A ordinary shares of our Company with a par value of $0.0001 per share;

“Class B Ordinary Shares” means the Class B ordinary shares of our Company with a par value of $0.0001 per share;

ii

“Class A Warrants” means the warrants issued by us in connection with the merger between CGCL and CGCL Merger Sub pursuant to the Class A Warrant Instrument;

“Company” means MoneyHero Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands, or as the context requires, MoneyHero Limited and its subsidiaries and consolidated affiliated entities;

“FWD” means a pan-Asian life insurance company majority owned by Pacific Century;

“Hong Kong” means the Hong Kong Special Administrative Region of the People’s Republic of China;

“Initial Merger” means the merger between Bridgetown and Bridgetown Merger Sub, with Bridgetown Merger Sub being the surviving company;

“Mainland China” means the People’s Republic of China, excluding, solely for the purpose of this annual report, Hong Kong, the Macau Special Administrative Region of the People’s Republic of China and Taiwan;

“MoneyHero Group,” “we,” “our” or “us” means MoneyHero Limited and its subsidiaries;

“MoneyHero Group Members” means users who have login IDs with the MoneyHero Group’s platforms in Singapore, Hong Kong and Taiwan, users who subscribe to its email distributions in Singapore, Hong Kong, Taiwan and the Philippines, and users who are registered in its rewards database in Singapore and Hong Kong. Any duplications across the three sources above are deduplicated;

“Monthly Unique User” (i) users who have login IDs with us in Singapore, Hong Kong and Taiwan, (ii) users who subscribe to our email distributions in Singapore, Hong Kong, Taiwan, the Philippines and Malaysia, and (iii) users who are registered in our rewards database in Singapore and Hong Kong. Any duplications across the three sources above are deduplicated;

“Mr. Li” means Mr. Richard Tzar Kai Li;

“Nasdaq” means the Nasdaq Stock Market;

“Pacific Century” means Pacific Century Group, an affiliate of Sponsor;

“PCAOB” means the U.S. Public Company Accounting Oversight Board;

iii

“PMIL” means PCCW Media International Limited, a company incorporated in Hong Kong with limited liability and a wholly-owned subsidiary of PCCW Limited. PCCW Limited is a company incorporated in Hong Kong with limited liability, the shares of which are listed on the main board of the Hong Kong Stock Exchange (stock code: 0008) and traded in the form of American Depositary Receipts on the OTC Markets Group Inc. (ticker: PCCWY);

“Preference Shares” means the preference shares of our Company with a par value of $0.0001 per share having the rights, preferences and restrictions set forth in the second amended and restated memorandum and articles of association of our Company, dated October 12, 2023;

“Public Warrants” means the warrants issued by us upon the conversion of Bridgetown Public Warrants at the effective time of the Initial Merger;

“SEC” means the U.S. Securities and Exchange Commission;

“Shares” means the Class A Ordinary Shares, Class B Ordinary Shares and Preference Shares;

“Sponsor” means Bridgetown LLC, a limited liability company incorporated under the laws of the Cayman Islands;

“Sponsor Warrants” means the warrants to be issued by us upon the conversion of Bridgetown’s private placement warrants at the effective time of the Initial Merger;

“Sponsor Permitted Transferees” means (i) our officers or directors, any affiliate or family member of any of our officers or directors, any affiliate of Sponsor or any member(s) of Sponsor or any of their affiliates and (ii) anyone who acquired Sponsor Warrants from Sponsor in one of the following manners: (a) in the case of an individual, by gift to a member such individual’s immediate family or to a trust, the beneficiary of which is a member of such individual’s immediate family, an affiliate of such individual, or to a charitable organization; (b) in the case of an individual, by virtue of the laws of descent and distribution upon death of such person; (c) in the case of an individual, pursuant to a qualified domestic relations order; or (d) by virtue of the laws of the Cayman Islands or Sponsor’s memorandum and articles of association upon dissolution of Sponsor;

“Traffic” means the total number of unique sessions in GA4. A unique session is a group of user interactions recorded when a user accesses a website or app within a 30-minute window. The current session concludes when there is 30 minutes of inactivity or users have a change in traffic source;

“U.S. Dollars,” “US$” and “$” means United States dollars, the legal currency of the United States;

“Warrants” means our Public Warrants, Sponsor Warrants and Class A Warrants;

iv

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements that involve risks and uncertainties. These forward-looking statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. All statements other than statements of current or historical facts are forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors, including those listed under “Item 3. Key Information—D. Risk Factors,” that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

In some cases, you can identify these forward-looking statements by words or phrases such as “may,” “might,” “would,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but not limited to, statements about:

| ● | our ability to grow market share in our existing markets or any new markets we may enter; |

| ● | our ability to execute our growth strategy, manage growth and maintain our corporate culture as we grow; |

| ● | our ability to successfully execute on acquisitions, integrate acquired businesses and realize efficiencies or meet growth aspirations inherent in the decision to make a specific acquisition; |

| ● | our ability to retain existing commercial partners or attract new commercial partners, or maintain favorable fee arrangements with our commercial partners; |

| ● | our ability to cost-effectively attract new, and retain existing, users and maintain and enhance user engagement; |

| ● | our ability to continue to diversify and optimize our offerings, offer high-quality content and provide strong customer support; |

| ● | the global economic environment and general market and economic conditions in the jurisdictions in which we operate; |

| ● | changes in the consumer lending and insurance markets; |

| ● | changes in interest rates or rates of inflation; |

| ● | ongoing geopolitical uncertainties and conflicts; |

| ● | various risks inherent in operating and investing in Greater Southeast Asia; |

| ● | the regulatory environment and changes in laws, regulations or policies in the jurisdictions in which we operate; |

| ● | increased competition in our industry; |

| ● | anticipated technology trends and developments and our ability to address those trends and developments with our products and offerings; |

v

| ● | our ability to protect information technology systems and platforms against security breaches (which includes physical and/or cybersecurity breaches either by external actors or rogue employees) or otherwise protect the confidential information or personally identifiable information of its users and business partners; |

| ● | developments related to COVID-19 and other pandemics, epidemics or public health threats; |

| ● | man-made or natural disasters, including war, acts of international or domestic terrorism, civil disturbances, occurrences of catastrophic events and acts of God such as floods, earthquakes, wildfires, typhoons and other adverse weather and natural conditions that affect our business or assets; |

| ● | the loss of key personnel and the inability to replace such personnel on a timely basis or on acceptable terms; |

| ● | exchange rate fluctuations; |

| ● | legal, regulatory and other proceedings; |

| ● | changes in tax laws and the interpretation and application thereof by tax authorities in the jurisdictions where we operate; and |

| ● | our ability to maintain the listing of our securities on Nasdaq. |

You should read this annual report and the documents that we refer to in this annual report thoroughly with the understanding that our actual future results may be materially different from and worse than what we expect. Important risks and factors that could cause our actual results to be materially different from our expectations are generally set forth in “Item 3. Key Information—D. Risk Factors,” “Item 4. Information on the Company—B. Business Overview,” “Item 5. Operating and Financial Review and Prospects,” and other sections in this annual report. You should read thoroughly this annual report and the documents that we refer to with the understanding that our actual future results may be materially different from and worse than what we expect. We qualify all of our forward-looking statements by these cautionary statements. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

This annual report also contains statistical data and estimates that we obtained from industry publications and reports generated by government or third-party providers of market intelligence, which we have not independently verified. The statistical data and estimates in these publications and reports are based on a number of assumptions and if any one or more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based on these assumptions. In addition, due to the rapidly evolving nature of the industry in which we operate, projections or estimates about our business and financial prospects involve significant risks and uncertainties.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we refer to in this annual report and exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect.

vi

PART I.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Founded in 2014 and dual-headquartered in Singapore and Hong Kong, MoneyHero Group, formerly known as the Hyphen Group or CompareAsia Group, is a leading personal finance aggregation and comparison platform, as well as a digital insurance brokerage provider in Greater Southeast Asia, operating in Singapore, Hong Kong, Taiwan and the Philippines with respective local market brands. With a portfolio of six well-known and trusted brands, we are primarily involved in the operation of online financial comparison platforms and related services for credit cards, personal loans, mortgages, wealth, insurance and other financial products, connecting the providers of these products with well- matched and ready-to-transact consumers and generating revenue directly from these providers for placing their products on our platforms and engaging us to provide insurance brokerage, marketing and events-related services. These providers, which we refer to as our commercial partners in this prospectus, primarily consist of regional and international brick-and-mortar banking institutions, insurance providers and investment brokers, many of which are subsidiaries and branches of blue-chip global financial institutions that are based in Asia. In addition to our own platforms, we also help our commercial partners expand their user reach by partnering with third-party online content creators and channel partners via Creatory, a self-service portal that helps content and channel partners monetize their online traffic and user base. These content and channel partners earn commission from us for promoting the financial products on our platforms, either on a fixed fee basis or conversion-based fee basis.

We help consumers with effective decision making by providing guidance through informative content and easy-to-use product comparison tools. As of December 31, 2024, we had approximately 7.5 million MoneyHero Group Members, which include users who have login IDs with us in Singapore, Hong Kong and Taiwan, users who subscribe to our email distributions in Singapore, Hong Kong, Taiwan and the Philippines, and users who are registered in our rewards database in Singapore and Hong Kong. We also retain an equity stake in Malaysian fintech company, Jirnexu Pte. Ltd., parent company of Jirnexu Sdn. Bhd., the operator of RinggitPlus, Malaysia’s largest operating B2C financial comparison platform.

As of December 31, 2024, we had over 290 commercial partner relationships, which are measured based on relationships with different business lines within a given financial institution. Our platforms address nearly all aspects of customer needs for financial products, making us a vital partner for financial product providers. In 2024, we had over 1.7 million Applications for financial product purchases and over 0.7 million Approved Applications, compared to over 1.7 million Applications for financial product purchases and over 0.6 million Approved Applications in 2023. In addition, in 2024, we published over 180 articles per month on our blogs, and our platforms averaged over 5.2 million page views per month by our users. In the quarter ended December 31, 2024, we had approximately 6.2 million Monthly Unique Users, 18.6 million Traffic sessions, with 70% of our Traffic sessions and 72% of our Monthly Unique Users engaged with our online platforms organically through unpaid channels. The volume of user activities on our platforms provides visibility into our future growth and has also encouraged us to continue to improve user experience and drive up conversions.

Our main business pillars are (i) online financial comparison platforms, where we provide financial guidance to consumers by offering a broad range of financial and lifestyle content, product comparison tools, and financial product marketplaces on its websites, and (ii) B2B business (Creatory), where we expand our user reach by partnering with other third-party online content and channel partners. The MoneyHero Group conducts its business mainly through the following websites: https://www.moneyherogroup.com, https://www.moneyhero.com.hk, https://www.singsaver.com.sg, https://www.money101.com.tw, https://www.moneymax.ph and https://creatory.biz.

1

For the years ended December 31, 2022, 2023 and 2024, our revenue was US$68.1 million, US$80.7 million and US$79.5 million, respectively. We generate revenue in the form of (i) internet leads generation and marketing service income related to credit cards, personal loans, mortgages, wealth, insurance and other financial products, whereby we charge the providers of these products on a revenue per click (“RPC”), revenue per lead (“RPL”), revenue per application (“RPA”) or revenue per approved application (“RPAA”) basis; (ii) insurance commission income through providing insurance brokerage services; (iii) marketing income through providing marketing services; and (iv) event income from holding financial events and festivals. In 2024, internet leads generation and marketing service income, insurance commission income, marketing income, and events income accounted for approximately 89.5%, 6.5%, 2.7% and 1.3% of our total revenue, respectively, compared to 94.0%, 4.2%, 1.3% and 0.6% of our total revenue in 2023, respectively. We recorded a loss of US$49.4 million, US$172.6 million, and US$37.8 million for the years ended December 31, 2022, 2023 and 2024, respectively.

In 2022, approximately 34.4%, 32.7%, 16.2%, 14.5%, 1.9% and 0.3% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines, Malaysia and Thailand, respectively. We ceased our operations in Thailand in 2022. In 2023, approximately 39.8%, 33.4%, 8.4%, 17.6% and 0.9% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines and Malaysia, respectively. In 2024, approximately 38.9%, 38.3%, 6.5%, 16.2% and 0.2% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines and Malaysia, respectively. As of December 31, 2024, approximately 30.9%, 50.8%, 4.1% and 13.7% of our assets were located in Singapore, Hong Kong, Taiwan and the Philippines, respectively. We ceased our customer-facing operations in Malaysia in the third quarter of 2024.

Cash Flows through Our Organization

Cash is transferred within the MoneyHero Group mainly in the following manners:

| ● | Intercompany working capital loans; |

| ● | Repayment of intercompany working capital loans; |

| ● | Service fees and recharges in connection with various types of management, administrative, technical support and marketing services; and |

| ● | Capital contributions into group companies that are engaged in insurance brokerage business. |

The table below sets forth a breakdown of the amounts transferred, the parties and regions involved and the currencies in which the transfers were made during the period from January 1, 2022 to December 31, 2024.

| Source of Funds | Nature of Transfer | Payor | Payee | Currency of Transfer | Amount (US$, in thousands) |

| Cayman Islands | Working Capital Loan | Moneyhero Limited (“MHL”) | CompareAsia Group Limited (“CAGL”) | USD | 17,280 |

| CompareAsia Group Capital Limited (“CGCL”) | CAGL | USD | 60,804 | ||

| Transfer of listing proceeds received on behalf | CGCL | MHL | USD | 40,001 | |

| Singapore | Working Capital Loan | Ekos Pte. Ltd. | CAGRSG | SGD | 1,281 |

| Singsaver Pte. Ltd. | CAGRSG | SGD | 1,463 | ||

| Seedly Pte. Ltd | SGD | 443 | |||

| Service Fee | Singsaver Pte. Ltd. | CAGRL | USD | 653 | |

| CAGRSG | USD | 699 |

2

| CAGRSG | SGD | 118 | |||

| Ekos Pte. Ltd. | SGD | 2,091 | |||

| Seedly Pte. Ltd | SGD | 341 | |||

| Seedly Pte. Ltd | Singsaver Pte. Ltd. | SGD | 29 | ||

| Ekos Pte. Ltd. | Seedly Pte. Ltd | SGD | 397 | ||

| CAGRSG | SGD | 52 | |||

| Singsaver Pte. Ltd. | SGD | 47,577 | |||

| CAGL | USD | 8 | |||

| CAGRL | USD | 2 | |||

| Singsaver Insurance Brokers Pte. Ltd. | CAGRL | USD | 21 | ||

| CAGRSG | USD | 315 | |||

| Singsaver Pte. Ltd. | SGD | 253 | |||

| Settlement of payment on behalf | Singsaver Pte. Ltd. | CAGL | USD | 8,797 | |

| CAGRSG | USD | 10 | |||

| Capital Contribution | Singsaver Pte. Ltd. | Singsaver Insurance Brokers Pte. Ltd. | SGD | 717 | |

| Loan Repayment | Singsaver Pte. Ltd. | CAGL | USD | 2,976 | |

| CAGRSG | Ekos Pte. Ltd. | SGD | 557 | ||

| Hong Kong | Working Capital Loan | CAGL | CAGRL | USD | 10,938 |

| CompareAsia Group ROHQ Philippines | 80 | ||||

| CAGRSG | 42,356 | ||||

| Compargo Malaysia Sdn. Bhd. | 590 | ||||

| Ekos Limited | 7,784 | ||||

| MoneyGuru Philippines Corporation | 884 | ||||

| MoneyHero Global Limited | 2,689 | ||||

| Seedly Pte. Ltd | 1,043 | ||||

| Singsaver Pte. Ltd. | 6,433 | ||||

| Certain historic subsidiaries | 765 | ||||

| CAGRL | HKD | 864 | |||

| Ekos Limited | 955 | ||||

| MoneyHero Global Limited | 1,274 | ||||

| MoneyHero Global Limited | CAGRL | USD | 350 | ||

| MoneyHero Global Limited | Ekos Limited | HKD | 7 | ||

| Loan Repayment | CAGRL | CAGL | USD | 869 | |

| MoneyHero Global Limited | CAGL | 4,329 | |||

| MoneyHero Global Limited | CAGL | HKD | 1,274 |

3

| CAGL | CGCL | USD | 1,540 | ||

| Ekos Limited | MoneyHero Global Limited | HKD | 15 | ||

| Service Fee | MoneyHero Global Limited | CAGL | USD | 446 | |

| CAGRL | HKD | 536 | |||

| MoneyHero Insurance Brokers Limited | CAGL | USD | 4 | ||

| CAGRL | USD | 45 | |||

| CAGRSG | USD | 14 | |||

| CAGRL | HKD | 37 | |||

| MoneyHero Insurance Brokers Limited | MoneyHero Global Limited | HKD | 1,855 | ||

| Ekos Limited | MoneyHero Global Limited | HKD | 1 | ||

| Settlement of payment on behalf | MoneyHero Global Limited | CAGL | USD | 3,713 | |

| HKD | 2,636 | ||||

| Capital Contribution | MoneyHero Global Limited | MoneyHero Insurance Brokers Limited | HKD | 502 | |

| The Philippines | Working Capital Loan | MoneyGuru Philippines Corporation | CompareAsia Group ROHQ Philippines | PHP | 435 |

| Loan Repayment | MoneyGuru Philippines Corporation | CAGL | USD | 2,467 | |

| CompareAsia Group ROHQ Philippines | MoneyGuru Philippines Corporation | USD | 75 | ||

| Service Fee | MoneyGuru Philippines Corporation | CAGL | USD | 1,332 | |

| CAGRL | 2,571 | ||||

| CAGRSG | 1,956 | ||||

| MoneyHero Insurance Brokerage, Inc. | MoneyGuru Philippines Corporation | PHP | 827 | ||

| Capital Contribution | MoneyGuru Philippines Corporation | MoneyHero Insurance Brokerage, Inc. | PHP | 976 |

As of the date of this annual report, no cash dividend or distribution had been made by our Company or any of our subsidiaries to our respective investors. It is expected that we will retain most, if not all, of our available funds and any future earnings to fund the development and growth of our business. As a result, it is not expected that we will pay any cash dividends in the foreseeable future. The payment of any cash dividends will be dependent upon the revenue, earnings and financial condition of our Company and our subsidiaries from time to time and will be within the discretion of our board of directors. We believe that there are no additional limitations or foreign exchange restrictions on our ability to transfer cash between our Company and our subsidiaries, or among our subsidiaries, either within a certain region or cross borders, and our ability to distribute earnings or declare dividends to U.S. and non-U.S. investors, other than the laws and regulations described under the sections titled “Regulations on Foreign Investment and Exchange Control” and “Regulations on Dividend Distribution” under “Item 4. Information on the Company—B. Business Overview—Regulations—Regulations in Singapore,” the sections titled “Regulations on Foreign Ownership Restrictions,” “Regulations on Exchange Control” and “Regulations on Dividend Distributions” under “Item 4. Information on the Company—B. Business Overview—Regulations—Regulations in the Philippines,” the sections titled “Regulations on Foreign Investment,” “Regulations on Financial Support Provided by Offshore Entities,” “Regulations on Exchange Control” and “Regulations on Dividend Distributions” under the section titled “Item 4. Information on the Company—B. Business Overview—Regulations—Regulations in Taiwan,” the sections titled “Regulations on Foreign Investment” and “Regulations on Exchange Control” under “Item 4. Information on the Company—B. Business Overview—Regulations—Regulations in Malaysia” and “Item 10. Additional Information—B. Memorandum and Articles of Association—Ordinary Shares and Preference Shares—Dividends.”

4

In addition, there are various restrictions under current PRC laws and regulations on intercompany fund transfers and foreign exchange control, which mainly include the following:

| ● | Dividends. PRC companies may pay dividends only out of their accumulated after-tax profits upon satisfaction of relevant statutory conditions and procedures, if any, determined in accordance with PRC accounting standards and regulations, and must first set aside at least 10% of their after-tax profits each year, if any, to fund certain reserve funds until the total amount set aside reaches 50% of its registered capital. In addition, PRC companies are required to complete certain procedural requirements related to foreign exchange control in order to make dividend payments in foreign currencies; and a withholding tax, at the rate of 10% or lower, is payable by a PRC subsidiary upon dividend remittance. |

| ● | Capital expenses. Approval from or registration with competent government authorities is required where Renminbi is to be converted into foreign currency and remitted out of Mainland China to pay capital expenses, such as the repayment of loans denominated in foreign currencies. As a result, PRC companies are required to obtain approval from the State Administration of Foreign Exchange (the “SAFE”) or complete certain registration process in order to use cash generated from their operations to pay off their respective debt in a currency other than Renminbi owed to entities outside Mainland China, or to make other capital expenditure payments outside Mainland China in a currency other than Renminbi. |

| ● | Shareholder loans and capital contributions. Loans by an offshore holding company to its PRC subsidiaries to finance their operations shall not exceed certain statutory limits and must be registered with the local counterpart of the SAFE, and any capital contribution from such holding company to its PRC subsidiaries is required to be registered with the competent PRC governmental authorities. |

As we do not currently have, or expect to have, any subsidiaries or business operations in Mainland China or any revenue from Mainland China, and none of its assets, directors, officers or members of senior management are, or are expected to be, located in Mainland China, we believe, based on the experience of our management, that there are no restrictions on foreign investments or foreign ownership applicable to the businesses currently conducted by our Hong Kong subsidiaries, and that no foreign exchange controls are currently in force in Hong Kong. However, funds or assets located in Hong Kong may not be available to fund operations or for other use outside of Hong Kong due to the PRC government authorities’ interventions in, or the imposition of restrictions and limitations on, the ability of our Company or our subsidiaries to transfer cash or assets. However, there remains uncertainty as to how the relevant laws and regulations will be implemented, and we cannot assure you that PRC regulatory agencies, including the SAFE, will take the same position. If our Company or any of our subsidiaries were to be deemed by PRC regulatory authorities to be subject to these restrictions, there is no assurance that we can fully or timely comply with the relevant requirements or complete the required registration, which could have a material and adverse effect on our business, financial condition and results of operations.

We maintain a Finance and Accounting Manual, which sets forth certain rules and procedures relating to cash management. All the group companies are required to perform monthly bank reconciliation. The Group Finance Director prepares a group-level cash position report on a monthly basis for the group’s Chief Executive Officer to review, with a summary of the balances of bank accounts in each of our four markets, analysis on the fluctuations for the month, information about conversion of trade receivables to cash, explanation on the sources and uses of cash and other information required to forecast, schedule and allocate cash. In addition, for purposes of working capital budgeting, local financial managers are required to send a monthly cashflow forecast of their respective region for the Group Finance Director and Chief Financial Officer to review, and variances from previous forecasts are also analyzed as part of this process. Local entities that need funds for operations are required to submit cash requests to the Group Finance Director and Chief Financial Officer for assessment and approval. Repayments of working capital loans and regional recharges are initiated at the group level, taking into account factors such as the funding needs of the entities and foreign exchange exposure, and require approval from the Chief Financial Officer.

5

A. Selected Financial Data

The following tables present our selected consolidated financial information. The selected consolidated statements of loss and other comprehensive income/(loss) data and cash flow data for the three years ended December 31, 2024, 2023 and 2022 and the consolidated statements of financial position data as of December 31, 2024 and 2023 have been derived from our audited consolidated financial statements included elsewhere in this annual report.

The financial data set forth below should be read in conjunction with, and is qualified by reference to, “Item 5. Operating and Financial Review and Prospects” below and the audited consolidated financial statements and notes thereto included elsewhere in this annual report. Our audited consolidated financial statements are prepared and presented in accordance with IFRS. IFRS differs from U.S. GAAP in certain material respects and thus may not be comparable to financial information presented by U.S. companies. The historical results included below and elsewhere in this prospectus are not indicative of our future performance.

Consolidated Statements of Loss and Other Comprehensive Income/(Loss)

| For the Year Ended December 31, | ||||||||||||

| 2024 | 2023 | 2022 | ||||||||||

| (US$ in thousands, except for loss per share) | ||||||||||||

| Revenue | 79,511 | 80,671 | 68,132 | |||||||||

| Costs and expenses | (119,702 | ) | (110,698 | ) | (109,105 | ) | ||||||

| Operating loss | (40,192 | ) | (30,026 | ) | (40,973 | ) | ||||||

| Other income/(expenses) | 2,513 | (142,511 | ) | (8,721 | ) | |||||||

| Loss before income tax | (37,678 | ) | (172,538 | ) | (49,694 | ) | ||||||

| Tax (expenses)/credit | (109 | ) | (63 | ) | 252 | |||||||

| Loss for the year | (37,787 | ) | (172,601 | ) | (49,442 | ) | ||||||

| Other comprehensive income/(loss), net of tax | 3,750 | (850 | ) | 3,130 | ||||||||

| Total comprehensive loss, net of tax | (34,037 | ) | (173,451 | ) | (46,312 | ) | ||||||

| Basic and diluted loss per share | (0.9 | ) | (17.9 | ) | (102.4 | ) | ||||||

Consolidated Statements of Financial Position

| As of December 31, | ||||||||

| 2024 | 2023 | |||||||

| (US$ in thousands) | ||||||||

| Assets | ||||||||

| Current assets | 78,282 | 106,947 | ||||||

| Non-current assets | 2,601 | 8,100 | ||||||

| Total assets | 80,883 | 115,047 | ||||||

| Liabilities | ||||||||

| Current liabilities | 32,147 | 35,708 | ||||||

| Non-current liabilities | 509 | 255 | ||||||

| Total liabilities | 32,656 | 35,963 | ||||||

| Net assets | 48,227 | 79,084 | ||||||

| Shareholders’ equity | ||||||||

| Total shareholders’ equity | 48,227 | 79,084 | ||||||

Consolidated Statements of Cash Flows

| For the Year Ended December 31, | ||||||||||||

| 2024 | 2023 | 2022 | ||||||||||

| (US$ in thousands) | ||||||||||||

| Net cash flows used in operating activities | (24,888 | ) | (17,043 | ) | (14,609 | ) | ||||||

| Net cash flows used in investing activities | (257 | ) | (1,342 | ) | (4,976 | ) | ||||||

| Net cash flows (used in)/from financing activities | (722 | ) | 63,062 | 34,790 | ||||||||

| Net increase/(decrease) in cash and cash equivalents | (25,867 | ) | 44,677 | 15,205 | ||||||||

| Cash and cash equivalents at the beginning of the year | 68,641 | 24,078 | 9,190 | |||||||||

| Effect of foreign exchange rate changes, net | (253 | ) | (113 | ) | (317 | ) | ||||||

| Cash and cash equivalents at the end of the year | 42,522 | 68,641 | 24,078 | |||||||||

6

Non-IFRS Financial Measures

| For the Year Ended December 31, | ||||||||||||

| 2024 | 2023 | 2022 | ||||||||||

| (US$ in thousands) | ||||||||||||

| Loss for the year | (37,787 | ) | (172,601 | ) | (49,442 | ) | ||||||

| Tax expenses/(credit) | 109 | 63 | (252 | ) | ||||||||

| Depreciation and amortization | 4,043 | 7,165 | 4,789 | |||||||||

| Interest income | (1,478 | ) | (873 | ) | (28 | ) | ||||||

| Finance costs | 25 | 19,028 | 7,801 | |||||||||

| EBITDA | (35,088 | ) | (147,217 | ) | (37,132 | ) | ||||||

| Non-cash items: | ||||||||||||

| Changes in fair value of financial instruments | (447 | ) | 57,333 | 1,101 | ||||||||

| Impairment of goodwill | — | — | 4,383 | |||||||||

| Impairment of intangible assets | 4,541 | 3,106 | 1,451 | |||||||||

| Equity settled share-based payment arising from employee share incentive scheme | 3,179 | 6,629 | 14,431 | |||||||||

| Unrealized foreign exchange loss/(gain), net | 4,197 | (895 | ) | 3,389 | ||||||||

| Listing and other non-recurring strategic exercises related items: | ||||||||||||

| Share-based payment on listing | — | 67,027 | — | |||||||||

| Equity settled share-based payment arising from professional services in relation to listing | — | 500 | — | |||||||||

| Transaction expenses | 29 | 6,643 | 1,139 | |||||||||

| Gain on disposal of assets in Malaysian operations | (600 | ) | — | — | ||||||||

| Other non-recurring costs related to strategic exercises | 61 | 1 | 528 | |||||||||

| Gain on derecognition of convertible loan and bridge loan | — | — | (135 | ) | ||||||||

| Equity-settled share-based payment expense arising from other fundraising activities | — | — | 882 | |||||||||

| Other non-recurring items: | ||||||||||||

| Other long-term employee benefits expense/(credit) | — | 110 | (4,951 | ) | ||||||||

| Non-recurring legal fees | 462 | — | — | |||||||||

| Adjusted EBITDA(1) | (23,666 | ) | (6,763 | ) | (14,915 | ) | ||||||

| Revenue | 79,511 | 80,671 | 68,132 | |||||||||

| Adjusted EBITDA | (23,666 | ) | (6,763 | ) | (14,915 | ) | ||||||

| Adjusted EBITDA Margin(1) | (29.8 | )% | (8.4 | )% | (21.9 | )% | ||||||

Note:

| (1) | In addition to our results determined in accordance with IFRS, we believe that the above non-IFRS measures are useful in evaluating its operating performance. We use these measures, collectively, to evaluate ongoing operations and for internal planning and forecasting purposes. We believe that non-IFRS information, when taken collectively, may be helpful to investors because it provides consistency and comparability with past financial performance and may assist in comparisons with other companies to the extent that such other companies use similar non-IFRS measures to supplement their IFRS results. These non-IFRS measures are presented for supplemental informational purposes only and should not be considered a substitute for financial information presented in accordance with IFRS and may be different from similarly titled non-IFRS measures used by other companies. Accordingly, non-IFRS measures have limitations as analytical tools, and should not be considered in isolation or as substitutes for analysis of other IFRS financial measures, such as loss for the year and loss before income tax. |

7

Adjusted EBITDA is a non-IFRS financial measure defined as loss for the year plus depreciation and amortization, interest income, finance costs, income tax expenses/(credit), impairments of non-financial assets, equity-settled share-based payment expenses, other long-term employee benefits expense/(credit), non-recurring costs related to strategic exercises, gain on disposal of assets in Malaysian operations, transaction expenses, changes in the fair value of financial instruments, non-recurring legal fees, gain on derecognition of convertible loan and bridge loan and unrealized foreign exchange differences. Adjusted EBITDA Margin is defined as Adjusted EBITDA as a percentage of revenue.

A reconciliation is provided above for each non-IFRS measure to the most directly comparable financial measure stated in accordance with IFRS. Investors are encouraged to review the related IFRS financial measures and the reconciliations of these non-IFRS measures to their most directly comparable IFRS financial measures. IFRS differs from U.S. GAAP in certain material respects and thus may not be comparable to financial information presented by U.S. companies. For additional information on related risks, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Securities—We currently, and will continue to, report financial results under IFRS, which differs in certain significant respects from U.S. GAAP.”

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Summary of Risk Factors

An investment in our Class A Ordinary Shares and Warrants involves significant risks. Below is a summary of certain material risks we face, organized under the relevant headings. You should carefully consider the risks below and further discussed under “Item 3. Key Information—D. Risk Factors” before making an investment decision. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations. Our business, financial condition, results of operations or prospects could be materially and adversely affected by any of these risks.

Risks Related to Our Business and Industry

| ● | Our historical revenue growth and financial performance may not be indicative of our future performance; |

| ● | We have a history of losses, and we may not achieve or maintain profitability in the future; |

| ● | Economic conditions, including changes in the consumer lending and insurance markets, and ongoing geopolitical uncertainties and conflicts could materially and adversely affect our business, financial condition and results of operations; |

| ● | Our operations are located in Greater Southeast Asia, which subjects us to various risks inherent in operating and investing in this region, such as uncertainties with respect to the local economic, legal and political environment; |

| ● | If we fail to retain existing commercial partners, especially commercial partners from which we generate a substantial portion of our revenue, or attract new commercial partners, or maintain favorable fee arrangements with our commercial partners, our business, financial condition and results of operations could be materially and adversely affected; |

| ● | Our business relies heavily on our ability to cost-effectively attract new, and retain existing, users and maintain and enhance user engagement; |

| ● | Our business is highly dependent on our ability to offer high-quality content that meets our users’ preferences and demands; |

| ● | We compete in a highly competitive and rapidly evolving market with a number of other companies, and we face the possibility of new entrants disrupting our market over time; |

8

| ● | If we are not able to keep pace with technological developments or respond to future disruptive technologies, we might not remain competitive and our business could be adversely affected; |

| ● | We rely on the data provided by our users and third parties to operate our business and enhance our products and services, and failure to maintain and grow the use of such data may adversely affect our business, financial condition and results of operations; |

| ● | Our actual or perceived failure to protect information provided by our users and commercial partners, or other confidential information, and to comply with the relevant laws and regulations could adversely affect our business, financial condition and results of operations; |

| ● | Our business depends on a strong reputation and brand, and any failure to maintain, protect and enhance our brand could have a material adverse effect on our business, financial condition and results of operations; |

| ● | We may be subject to complaints, litigation, arbitration proceedings and regulatory investigations and inquiries from time to time; and |

| ● | We may fail to obtain, maintain or renew the requisite licenses and approvals. |

Risks Related to Doing Business in Singapore

| ● | Our business, financial condition and results of operations may be influenced by the political, economic and legal environments in Singapore, and by the general state of the Singapore economy. |

Risks Related to Doing Business in Hong Kong

| ● | Potential political and economic instability in Hong Kong may adversely impact our results of operations; |

| ● | The business, financial condition and results of operations of our Hong Kong subsidiaries and/or the value of our securities or our ability to offer or continue to offer securities to investors may be materially and adversely affected to the extent the laws, rules and regulations of the PRC become applicable to us; |

| ● | The PRC government has significant oversight, discretion and control over the manner in which companies incorporated under the laws of the PRC or companies that operate in, or generate revenue from, Mainland China must conduct their business activities. Because of our substantial operations in Hong Kong and given the PRC government’s significant oversight and authority over the conduct of business in Hong Kong generally, if we were to become subject to such oversight, discretion or control, including over overseas offerings of securities and/or foreign investments, it may result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or become worthless, which would materially affect the interests of our investors; |

9

| ● | Our Hong Kong subsidiaries may be subject to various restrictions on intercompany fund transfers and foreign exchange control under current PRC laws and regulations and could be subject to additional, more onerous restrictions under new PRC laws and regulations that may come into effect in the future, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, financial condition and results of operations; |

| ● | We and our subsidiaries may be subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, financial condition and results of operations; |

| ● | The future development of national security laws and regulations in Hong Kong could materially impact our business by possibly triggering sanctions and other measures that can cause economic harm to our business; |

| ● | If we are identified by the SEC as a Commission-Identified Issuer for two consecutive years due to the PCAOB’s inability to inspect our auditors, our securities will likely be delisted. The delisting of our securities, or the threat of our securities being delisted, may materially and adversely affect the value of your investment. Additionally, the inability of the PCAOB to conduct inspections will deprive investors of the benefits of such inspections; |

| ● | There may be difficulties in effecting service of legal process, conducting investigations, collecting evidence, enforcing foreign judgments or bringing original actions in Hong Kong based on United States or other foreign laws against our directors, officers and members of senior management who are located in Hong Kong; |

| ● | We and our Hong Kong subsidiaries may be affected by the currency pegging system in Hong Kong and other exchange rate fluctuations; and |

| ● | Increases in labor costs may adversely affect our business and results of operations. |

Risks Related to Our Securities

| ● | Our failure to meet Nasdaq’s continued listing requirements could result in a delisting of our Class A Ordinary Shares and/or Public Warrants; |

| ● | The market price and trading volume of our securities may be volatile and could decline significantly in the future, which could subject us to securities class action litigation; |

10

| ● | If securities or industry analysts do not publish research, publish inaccurate or unfavorable research or cease publishing research about us, our share price and trading volume could decline significantly; |

| ● | A market for our securities may not be sustained, which would adversely affect the liquidity and price of our securities and make it difficult for holders to sell the securities; |

| ● | Future resales of a large number of our Class A Ordinary Shares or Warrants may cause the market price of our Class A Ordinary Shares to drop significantly, even if our business is doing well; |

| ● | Certain of our shareholders may have substantial influence over us, and their interests may not be aligned with the interests of our other shareholders; |

| ● | We are a “controlled company” within the meaning of the Nasdaq rules and, as a result, qualifies for, and could elect to rely on, exemptions from certain corporate governance requirements; and |

| ● | Our issuance of additional share capital in connection with acquisitions, investments, financings, its equity incentive plans, the exercise of Warrants or otherwise will dilute all other shareholders and could cause the market price of our securities to decline. |

Risks Related to Our Business and Industry

Our historical revenue growth and financial performance may not be indicative of our future performance.

As a relatively young company, we have experienced rapid growth in the past, which may not be sustainable or representative of our future growth trajectory. Additionally, the COVID-19 pandemic has accelerated the shift towards digital acquisition of financial services, leading to an exceptional period of growth that may not be maintained in the future. As the effects of the pandemic subside and market conditions change, we may face new challenges that could impact our growth rate and financial performance. These challenges may include increased competition, evolving user preferences, adverse market conditions or regulatory changes, and other factors beyond our control. Consequently, our historical growth and financial performance may not be indicative of our future prospects. If we are unable to maintain our growth momentum, adapt to changing market conditions or address new challenges effectively, our business, financial condition and results of operations could be materially and adversely affected.

We have a history of losses, and we may not achieve or maintain profitability in the future.

We have a history of losses, including losses of US$49.4 million, US$172.6 million and US$37.8 million for the years ended December 31, 2022, 2023 and 2024, respectively. We expect to continue to make investments in developing and expanding our business, including, but not limited to, in technology, recruitment and training, marketing, and for the purpose of pursuing strategic opportunities. Our growth efforts may result in significant costs and expenses before generating any incremental revenue from acquisitions or investments. Moreover, we may experience more expenses than we anticipate or fail to generate enough revenue to offset costs, leading to increased losses. Additionally, we may continue to incur significant losses in the future for a number of reasons, including, but not limited to:

| ● | our inability to grow market share in our existing markets or any new markets we may enter; |

| ● | our expansion into new markets or adjacent lines of business, for which we typically incur more significant losses in the early stages following entry; |

| ● | our inability to successfully execute on acquisitions, integrate acquired businesses and realize efficiencies or meet growth aspirations inherent in the decision to make a specific acquisition; |

| ● | increased competition in the financial comparison industry and insurance brokerage industry in our main markets; |

11

| ● | failure to realize effective marketing campaigns and product and technology enhancements; |

| ● | failure to execute our growth strategies; |

| ● | changes in the macroeconomic and geopolitical environment and a subsequent reduction in our commercial partners’ customer acquisition budgets for, and our users’ demand for, financial products across our markets; |

| ● | increased marketing costs; |

| ● | challenges in hiring additional personnel to support our overall growth; |

| ● | increased labor costs as a result of rising inflation and increasing competition; |

| ● | changes in laws, regulations and government policies that directly or indirectly impact our industries and business operations; |

| ● | public health threats, natural disasters or other catastrophic events; |

| ● | changes in accounting policies; and |

| ● | unforeseen expenses, difficulties, complications and delays, and other unknown factors. |

In addition, as a public company, we will also incur significant legal, accounting, insurance, compliance and other expenses that we did not incur as a private company. These expenses may increase even more if we no longer qualify as an “emerging growth company,” as defined in Section 2(a) of the Securities Act. We cannot predict or estimate the amount of additional costs we will incur as a public company or the specific timing of such costs. If we fail to manage our losses or to grow our revenue sufficiently to keep pace with our investments and other expenses, our business will be harmed, and we may not achieve or maintain profitability in the future.

Economic conditions, including changes in the consumer lending and insurance markets, and ongoing geopolitical uncertainties and conflicts could materially and adversely affect our business, financial condition and results of operations.

Our business operations and financial performance are influenced by the overall condition of the markets in which we operate. Each of the markets in which we operate is affected by various macroeconomic factors outside our control, which by their nature are cyclical and subject to change. These factors include, among other things, interest rates, the general market outlook for economic growth, unemployment and consumer confidence. These factors are also affected by government policy and regulations that may change.

The current global economic slowdown, adverse changes in the consumer lending and insurance markets and the possibility of continued turbulence or uncertainty in global financial markets and economies have had, continue to have, and may increasingly have a negative impact on our users and commercial partners, the demand for, and supply of, the financial products on our platforms, our ability to generate revenue from our commercial partners and grow our business, and our access to and the availability of financing on acceptable terms. For example, while rising inflation could cause consumers to seek increased credit both in the form of credit cards and personal loans, our commercial partners may tighten their underwriting standards as they see higher rates of default from consumers, which could result in decreased supply of credit card or personal loan products on our platforms and lower approval rates. Inflationary pressures have increased our operating costs in 2023 and 2024 and could continue to have an adverse impact on our costs, margins and profitability in the future. Factors such as increased interest rates, economic uncertainties, recessionary conditions, increased unemployment or stagnant or declining wages also can cause consumers to become more cautious in their borrowing behavior, seek alternative financing options or postpone borrowing decisions altogether. While we closely monitor market conditions and have adopted vertical diversification strategies, there is no guarantee that our efforts will be successful in countering the potential negative impacts of macroeconomic risks on our business. Furthermore, macroeconomic conditions could adversely affect the financial strengths of our commercial partners, causing them to cease participating, or participating less, on our platform, tighten underwriting standards, become less willing or able to issue credit, reduce approval rates, implement cost-reduction initiatives that reduce or eliminate their marketing budgets available to our platforms, requiring them to drop the quality of their products and services, or rendering them unable to pay us fees on time, or at all. We cannot predict the timing or duration of an economic slowdown or the timing or strength of a subsequent economic recovery generally or in our industries. If macroeconomic conditions worsen or the current global economic conditions continue for a prolonged period of time, our business, financial condition and results of operations could be materially and adversely affected.

12

Our operations also could be disrupted by geopolitical risks, including those arising from geopolitical conditions, political and social instability, acts of war or other similar events, which may negatively impact economic growth, cause uncertainty and volatility in the financial markets, and adversely affect our business, financial condition and results of operations. For example, in February 2022, Russia initiated significant military actions against Ukraine, and the tension between Israel and Iran may escalate in the future and turn violent. In response, the U.S. and certain other countries imposed sanctions and export controls against Russia, Belarus and certain individuals and entities connected to Russian or Belarusian political, business and financial organizations. It is not possible to predict the broader consequences of the conflict, its future development, the extent of further sanctions, and their impact on our business operations and our ability to raise capital. These and any adverse changes or instabilities in the geopolitical environment could increase our costs and our exposure to legal and business risks and disrupt the operations of our company, our content and channel partners and our commercial partners.

Our operations are located in Greater Southeast Asia, which subjects us to various risks inherent in operating and investing in this region, such as uncertainties with respect to the local economic, legal and political environment.

We are dual-headquartered in Singapore and Hong Kong and have operations in four Greater Southeast Asia markets. In 2022, approximately 34.4%, 32.7%, 16.2%, 14.5%, 1.9% and 0.3% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines, Malaysia and Thailand, respectively. We ceased our operations in Thailand in 2022. In 2023, approximately 39.8%, 33.4%, 8.4%, 17.6% and 0.9% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines and Malaysia, respectively. In 2024, approximately 38.9%, 38.3%, 6.5%, 16.2% and 0.2% of our total revenue was generated from Singapore, Hong Kong, Taiwan, the Philippines and Malaysia, respectively. We ceased our customer-facing operations in Malaysia in the third quarter of 2024.

Each of our markets has its own set of political, policy, legal, economic, taxation and other risks and uncertainties that may impact our performance. Therefore, operating in our current markets often requires bespoke business models for each market in which we operate, which adds complexity and reduces economies of scale. In addition, volatile political situations, policy instabilities or changes in policy directions in these markets could negatively affect the local economy, operating environment and investor confidence, which in turn could have a material adverse effect on our business, financial condition and results of operations. Furthermore, emerging market countries, such as the Philippines, tend to have less sophisticated legal, taxation and regulatory frameworks than developed markets and are typically subject to greater risks and uncertainties, including, but not limited to, the risks of expropriation, nationalization, commercial or governmental disputes, inflation, interest rate and currency fluctuations, and greater difficulty in enforcing or collecting payment against contracts and ensuring that all required governmental and regulatory approvals necessary to operate our business are in place and will be renewed. In addition, the laws and regulations in these markets are more susceptible to unexpected changes and inconsistent application, interpretation or enforcement.

For a more detailed description of these risks, see “—Risks Related to Doing Business in Singapore,” “—Risks Related to Doing Business in Hong Kong,” “—Risks Related to Doing Business in Taiwan,” and “—Risks Related to Doing Business in the Philippines.”

If we fail to retain existing commercial partners, especially commercial partners from which we generate a substantial portion of our revenue, or attract new commercial partners, or maintain favorable fee arrangements with our commercial partners, our business, financial condition and results of operations could be materially and adversely affected.

Our ability to offer a substantial spectrum of relevant and competitively priced financial products for our users to search, compare and procure is essential to our business, and we generate revenue directly from commercial partners who place financial products on our platforms and engage us for insurance brokerage, marketing and events-related services. As of December 31, 2024, we had over 290 commercial partner relationships.

13

Our commercial partners typically do not have exclusive commercial relationships with us. Our agreements with our commercial partners typically have a term of one to three years on average, which may be terminated by either party for any reason with adequate notice. Our ability to attract and retain commercial partners and negotiate favorable fee arrangements with them is largely dependent on our ability to provide them with a large and consistent volume of qualified users ready to transact and our fee arrangements with them. If we fail to consistently deliver a sufficient quantity of reliable and high-quality customer referrals, due to factors such as shifts in consumer behavior or the emergence of new competitors, our commercial partners may choose to allocate their resources towards alternative channels or competitors, which could negatively impact our revenue, business, financial condition and results of operations. Additionally, changes in market conditions or the regulatory environment may further impact our commercial partner network.

The process of establishing new partnerships or expanding existing relationships can be time-consuming and resource intensive. We devote significant resources to developing and maintaining our relationships with commercial partners but there is no guarantee that our efforts will be successful. If we fail to identify and adapt to the evolving needs of our commercial partners, successfully maintain our relationships with existing commercial partners or identify and secure new sources of supply for our platforms, the amount of fees we can generate from commercial partners could decline significantly, and the quality, diversity and competitiveness of the financial products available through our platforms could be harmed, which will in turn make it more difficult for us to attract and retain users and make us less valuable to commercial partners.

In addition, as the financial services industry in Asia is relatively concentrated, our revenue is heavily reliant on a small number of key commercial partners. For example, various entities affiliated with or acting on behalf of Citibank, N.A. across our key markets together contributed to approximately 14% of our revenue in 2024. The services we provide to these entities are governed by master services agreements, with a term of one to three years, and various work orders and marketing agreements covering a variety type of financial products. The work orders and marketing agreements set out the specific commercial terms and have varying terms of duration. The termination of the master services agreements will not result in the termination of any specific work order or marketing arrangement. The concentrated nature of the industry increases our dependency on these key partners and exposes us to risks associated with the loss of business, unfavorable renegotiation of contractual terms and the emergence of new competitors. If we are unable to manage the risks associated with our dependence on a small number of key commercial partners or adapt to changes in the market environment, if our relationships with any of these key commercial partners were to be terminated, or if our level of business with them were to decrease significantly, our business, financial condition and results of operations could be materially and adversely affected.

Our success-based fee model is subject to risks that could have a material adverse effect on our business, financial condition and results of operations.

We generate revenue directly from commercial partners who place financial products on our platforms and engage us for insurance brokerage, marketing and events-related services. For our internet leads generation and marketing service income, which accounted for approximately 95.3%, 94.0% and 89.5% of our total revenue in 2022, 2023 and 2024, respectively, and we charge our commercial partners on a RPC, RPL, RPA or RPAA basis. In 2022, 2023 and 2024, 84%, 90% and 87% of our revenue was realized based on Approved Applications, respectively, with the remaining portion realized primarily based on Clicks, Leads and Applications. Our internet leads generation and marketing service income is tied to Click, Leads, Application or Approved Application, as applicable, and there is no duplication among the pricing models. Our pricing model is product-based, and our arrangements with some of our commercial partners involve more than one pricing model. The success-based nature of our fee structures creates business risks as we incur marketing and other costs involved in generating revenue upfront but will only receive fees from our commercial partners when such efforts and costs successfully result in Clicks, Leads, Applications and Approved Applications. In 2022, 2023 and 2024, over 80% of our revenue was realized based on Approved Applications. As such, fluctuations in approval rates for Applications, which may be influenced by factors such as economic conditions, consumer creditworthiness and competition from other financial services providers, could create significant risks to our ability to generate revenue and earn profit. Our dependency on success-based outcomes requires us to continuously invest in marketing and promotional activities to attract users to our platforms, while also maintaining strong relationships with our commercial partners. Any adverse change in the availability and competitiveness of the financial products on our platforms, the willingness of our commercial partners to approve applications for financial products, our fee arrangements with our commercial partners, or our ability to attract new users, retain existing users and increase user engagement level could have a material and adverse impact on our business, financial condition and results of operations.

14

Trends in the credit card industry and impact of the general economy on the credit card industry could harm our business, financial condition and results of operations.

The credit card market is an important part of our business. In 2022, 2023 and 2024, over 60% of our revenue was derived from credit card products. Our participation in the credit card market is subject to particular risks, each of which could negatively affect our business, financial condition and results of operations:

| ● | adverse conditions in the economy may affect consumer creditworthiness and credit card issuers’ willingness to issue new credit; |

| ● | lower approval rates by credit card issuers due to tighter underwriting or other factors; |

| ● | credit losses among credit card issuers may increase beyond normal and budgeted levels, which could cause a reduction in credit card issuers’ ability to extend credit; |

| ● | decreases in consumer interest in credit card products; |

| ● | increased competition; and |

| ● | our inability to provide competitive service to credit card issuers and to consumers using our platforms. |

Our insurance brokerage businesses pose unique risks.

We hold insurance brokerage licenses in Singapore, Hong Kong and the Philippines. In 2022, 2023 and 2024, we had insurance commission income of US$1.7 million, US$3.4 million and US$5.2 million, respectively, representing approximately 2.4%, 4.2% and 6.5% of our total revenue, respectively. Commission fee rates and premiums can change based on various factors over which we do not have control, such as the prevailing economic, regulatory, taxation and competitive factors, as well as consumer demand for insurance products and the growing availability of alternative methods for consumers to meet their risk-protection needs. Any decrease in commission fee rates or premiums may have an adverse effect on our financial condition and results of operations.

In addition, our insurance brokerage business is subject to various laws and regulations. Any failure to comply with applicable laws or regulations could result in fines, censure, suspensions of business or other sanctions, including revocation of licenses, which could have a material and adverse effect on our business, financial condition and results of operations. For more details on the applicable laws and regulations, see “Item 4. Information on the Company—B. Business Overview—Regulations.” Even if a sanction imposed against us or our personnel is small in monetary amount, the resulting adverse publicity arising could harm our reputation and impair our ability to attract and retain users and commercial partners. In addition, new laws and regulations that impose additional compliance requirements or make it harder for us to renew our licenses could be adopted from time to time.

Our business relies heavily on our ability to cost-effectively attract new, and retain existing, users and maintain and enhance user engagement.

Our financial performance heavily depends on our ability to refer our users to our commercial partners and facilitate transactions between our users and commercial partners. Our ability to attract new, and retain existing, users and maintain and increase levels of user engagement depends on various factors, including, but not limited to:

| ● | changes in market conditions and the regulatory environment; |

| ● | fluctuations in the demand for, and supply of, the financial products on our platforms; |

| ● | our ability to identify the evolving needs of our users and adapt our platforms and product offerings to cater to such needs in a timely and effective manner; |

| ● | the strength and influence of our brands; |

15

| ● | our commercial partners’ ability to offer products and services that meet user demands and to ensure the relevance and attractiveness of their products in response to new and refined financial products available in the market. |

| ● | our ability to offer high-quality content, access to competitive products, personalized user experience and satisfactory customer services; |

| ● | our ability to further diversify our product and service offerings; |

| ● | the effectiveness of our marketing and promotional activities; |

| ● | our ability to continuously invest in research and development, adapt to technological advancements and emerging trends in customer touchpoints, data management and digital marketing, and stay at the forefront of industry innovation; |

| ● | our ability to successfully navigate the competitive landscape by staying ahead of new entrants and the evolving strategies of existing competitors; and |

| ● | our ability to address user concerns regarding the privacy and security of our platforms. |

Negative publicity about our platforms, our commercial partners, or the financial products available on our platforms, whether accurate or inaccurate, disruptions or outages of our or our commercial partners’ platforms or other technical or customer service problems that frustrate the user experience may also adversely affect our ability to attract and retain users.