Exhibit 99.1

Collective Mining Ltd.

Annual Information Form

For the year ended December

31, 2024

Dated March 24, 2025

TABLE OF CONTENTS

MEANING OF CERTAIN REFERENCES AND CURRENCY

INFORMATION

In this annual information form

(“AIF” or “Annual Information Form”), unless the context otherwise requires, “Collective”

refers to Collective Mining Ltd.; the “Bermuda Subsidiary” refers to Collective Mining Limited (Bermuda), the “Branch”

refers to Collective Mining Limited Sucursal, a Colombian branch (Colombia); “Minerales Provenza” refers to the Company’s

subsidiary Minerales Provenza S.A.S. (Colombia); “Minera Campana” refers to the Company’s subsidiary Minera Campana

S.A.S. (Colombia); and the “Company” refers to Collective Mining Ltd. and its subsidiaries. References to “POCML5”

refer to the Company prior to completion of the Business Combination (as defined herein).

This AIF applies to the business

activities and operations of the Company for the year ended December 31, 2024, as updated to March 24, 2025. Unless otherwise indicated,

the information in this AIF is given as of the date hereof.

Unless otherwise indicated,

all references to “US$” in this AIF refer to United States dollars and all references to “$” or

“C$” in this AIF refer to Canadian dollars.

CAUTIONARY STATEMENT REGARDING FORWARD LOOKING

INFORMATION

This AIF contains “forward-looking statements”

or “forward-looking information” within the meaning of applicable securities legislation (collectively referred to herein

as “forward-looking information” or “forward-looking statements”). Forward-looking information includes,

but is not limited to, statements with respect to: the future price of commodities; the estimation of mineral resources; the realization

of mineral resource estimates; regulatory compliance; capital expenditures; planned exploration activities, including but not limited

to, costs and timing of the development of new deposits and the future acquisitions of properties or mineral rights; the interpretation

of geological information; success of exploration activities; the payment of net smelter return royalties; permitting time lines; currency

fluctuations; requirements for additional capital, including but not limited to, future financings; future profitability; government regulation

of mining operations; the obtaining of required licenses and permits and regulatory approvals; ability to generate a mineral resource

estimate and a preliminary economic assessment; reclamation expenses; the acquisition of new properties; other statements relating to

the financial and business prospects of the Company; information as to the Company’s strategy, plans or future financial or operating

performance; and other events or conditions that may occur in the future. Often, but not always, forward-looking statements can be identified

by the use of words and phrases such as “plans”, “expects”, “is expected”, “budget”, “scheduled”,

“estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or variations

(including negative variations) of such words and phrases, or statements that certain actions, events or results “may”, “could”,

“would”, “should”, “might” or “will” be taken, occur or be achieved.

Forward-looking information involve known

and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to

be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

Such factors include, among others: results of exploration activities not being supportive of further development of our projects;

the future price of commodities; the estimation of mineral resources, the realization of mineral resource estimates; regulatory

compliance; capital expenditures; planned exploration activities, including but not limited to, costs and timing of the development

of new deposits and the future acquisitions of properties or mineral rights; the interpretation of geological information; success

of current drill programs; conducting operations in a foreign country; the assurance of titles or boundaries; uncertainties of

project costs; the presence of artisanal/illegal miners; the process of formalization of artisanal miners and the closure of illegal

mines; the environmental permitting process in Colombia; title regarding the ownership of the Company’s projects and the

related surface rights and to the boundaries of the Company’s projects and other risks related to maintaining land surface

rights; maintaining the security of the Company’s information technology systems; the Company’s limited operating

history; the payment of net smelter return royalties; the significant influence exercised by the Executive Chairman of the Company

over the Company; permitting time lines; currency fluctuations; requirements for additional capital, including but not limited to,

future financings; future profitability; government regulation of mining operations; the obtaining of required licenses and permits

and regulatory approvals; delays in obtaining, or the inability to obtain, third party contracts, equipment, supplies and

governmental or other approvals; accidents, labour disputes, unavailability of appropriate land use permits, changes to land usage

agreements and other risks of the mining industry generally and specifically in Colombia; reclamation expenses; the inability to

obtain financing required for the completion of exploration and development activities; changes in business and economic conditions; price

volatility of the common shares of the Company (the “Common Shares”); socio and geopolitical factors;

international conflicts; other factors beyond the Company’s control; and as well as those factors included herein and

elsewhere in the Company’s public disclosure. Readers are cautioned that the foregoing list is not exhaustive of all factors

and assumptions which may have been used. Although the Company has attempted to identify important factors that could cause actual

results to differ materially from those contained in forward-looking information, there may be other factors that cause results not

to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual

results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place

undue reliance on forward-looking information. The forward-looking information contained herein is presented for the purposes of

assisting investors in understanding the Company’s expected financial and operating performance and the Company’s plans

and objectives and may not be appropriate for other purposes. The Company does not undertake to update any forward-looking

information, except in accordance with applicable securities laws.

Readers are cautioned that the

foregoing list is not exhaustive of all factors and assumptions which may have been used. Although the Company has attempted to identify

important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated,

estimated or intended. There can be no assurance that such forward-looking information and statements will prove to be accurate as actual

results and future events could differ materially from those anticipated in such information and statements. Accordingly, readers should

not place undue reliance on forward-looking information and statements. The forward-looking information and statements contained herein

are presented for the purposes of assisting readers in understanding the Company’s expected financial and operating performance

and the Company’s plans and objectives and may not be appropriate for other purposes. See the section entitled “Risk Factors”

below, for additional risk factors that could cause results to differ materially from forward-looking statements.

The forward-looking information

and statements contained in this AIF represent the Company’s views and expectations as of the date of this AIF. The Company anticipates

that subsequent events and developments may cause its views to change. However, while the Company may elect to update such forward-looking

information and statements at a future time, it has no current intention of doing so except to the extent required by applicable law.

SCIENTIFIC AND TECHNICAL INFORMATION

Unless otherwise indicated, scientific and technical

information in this AIF relating to the Company’s mineral properties has been reviewed and approved by David J. Reading, MSc in

Economic Geology and a Fellow of the Institute of Materials, Minerals and Mining and of the Society of Economic Geology (SEG), and a special

advisor to the Company, who is a “qualified person” within the meaning of National Instrument 43-101 – Standards

of Disclosure for Mineral Projects (“NI 43- 101”).

GLOSSARY OF GEOLOGICAL, TECHNICAL AND MINERAL

TERMS

“Ag” means the chemical symbol

for silver.

“Alteration” means changes

in the mineral composition of a rock brought about by physical or chemical means, especially the local action of hydrothermal solutions

that can be related to mineralization.

“Assay” means to analyze the

proportions of metal in a rock or overburden sample and to test an ore or mineral for composition, purity, weight or other properties

of commercial interest.

“Au” means the chemical symbol

for gold.

“Base Metal” means industrial

non-ferrous metals excluding precious metals.

“Chalcopyrite” means a copper

sulphide mineral, the most common ore mineral of copper.

“Claim” means the area that

confers mineral exploration/exploitation rights to the registered (mineral/mining) holder under the laws of the governing jurisdiction.

“Cu” means the chemical symbol

for copper.

“Deposit” means a mineralized

body which has been physically delineated by sufficient drilling, trenching and/or underground work, and found to contain a sufficient

average grade of metal or metals to warrant further exploration and/or development expenditures; however, a deposit does not qualify as

a commercially mineable or body or as containing reserves of ore, until final legal, technical and economic factors have been resolved.

“Diamond Drilling” means drilling

with a hollow bit with a diamond cutting rim to produce a cylindrical core that is used for geological study and assays as used in mine

exploration.

“Dip” means the maximum angle

that a structural surface makes with the horizontal, measured perpendicular to the strike of the structure and in the vertical plane.

“Disseminated” means the distribution

of mineralization usually as small grains randomly distributed throughout a rock mass.

“Exploration” means prospecting,

sampling, mapping, diamond drilling and other work involved in searching for ore.

“Fault” means a fracture in

a rock across which there has been displacement.

“Fe” means the chemical symbol

for iron.

“Grade” means the concentration

of an ore metal in a rock sample, given either as weight percent for base metals (e.g. Cu, Zn, Pb) or in grams per tonne (g/t) or ounces

per short ton (oz/t) for gold, silver, and platinum group metals.

“ICP” means induced coupled

plasma.

“Indicated Mineral Resource”

means that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated

with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning

and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information

gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely

enough for geological and grade continuity to be reasonably assumed.

“Lithology” means the physical

character of a rock.

“Measured Mineral Resource”

means that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are so well

established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters,

to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable

exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits,

workings and drill holes that are spaced closely enough to confirm both geological and grade continuity.

“Mineral” means a naturally

occurring chemical compound or limited mixture of chemical compounds. Minerals generally form crystals and have specific physical and

chemical properties which can be used to identify them.

“Mineralization” means the

process or processes by which a mineral or minerals are introduced into a rock resulting in concentration of metals and their chemical

compounds within a body of rock.

“Mineral Project” means any

exploration, development or production activity, including a royalty interest or similar interest in these activities, in respect of diamonds,

natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial

minerals.

“mineral reserve” means the

economically mineable part of a Measured Mineral Resource or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility

Study. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined.

“mineral resource” means a

concentration or occurrence of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base

and precious metals, coal, and industrial minerals in or on the earth’s crust in such form and quantity and of such grade or quality

that it has reasonable prospects for economic extraction. The lovation, quantity, grade, geological characteristics and continuity of

a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge.

“Mo” means the chemical symbol

for molybdenum.

“Ore” means a mixture of ore

minerals and gangue (worthless minerals) from which there are reasonable and realistic prospects for the economic extraction of at least

one ore mineral.

“Pb” means the chemical symbol

for lead.

“Preliminary Feasibility Study”

means a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a

stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established

and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on mining,

processing, metallurgical, economic, marketing, legal, environmental, social and governmental considerations and the evaluation of any

other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the mineral resource

may be classified as a Mineral Reserve.

“Qualified Person” means an

individual who: (i) is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or

operation or mineral project assessment; (ii) has experience relevant to the subject matter of the mineral project and the technical report;

and (ii) is in good standing with a professional association or foreign association and has the corresponding designation.

“Sample” means a small portion

of rock or a mineral deposit taken so that the metal content can be determined by assaying.

“Sampling” means selecting

a fractional by representative part of a mineral deposit for analysis.

“Strike” means the course or

bearing of the outcrop of an inclined bed, vein, or fault plane on a level surface; the direction of a horizontal line perpendicular to

the direction of the Dip.

“Zn” means the chemical symbol

for zinc.

| METRIC EQUIVALENTS |

| For ease of reference, the following conversion factors are provided: |

| Imperial Measure |

|

Metric Unit |

|

Metric Unit |

|

Imperial Measure |

| 2.47 acres |

|

1 hectare (ha) |

|

0.4047 hectares (ha) |

|

1 acre |

| 3.28 feet (ft) |

|

1 metre (m) |

|

0.3048 metres (m) |

|

1 foot (ft) |

| 0.62 miles |

|

1 kilometer (Km) |

|

1.609 kilometers (Km) |

|

1 mile |

| 0.032 troy ounces |

|

1 gram (g) |

|

31.1 grams (g) |

|

1 troy ounce |

| 2.205 pounds (lb) |

|

1 kilogram (kg) |

|

0.454 kilograms (kg) |

|

1 pound (lb) |

| 1.102 short tons |

|

1 tonne (t) |

|

0.907 tonnes (t) |

|

1 short ton |

| 0.029 troy ounces/ton |

|

1 gram/tonne (g/t) |

|

34.28 grams/tonne (g/t) |

|

1 troy ounce/ton |

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated

under the Business Corporations Act (Ontario) (the “OBCA”) on February 21, 2018 under the name “POCML

5 Inc.” (“POCML5”). On December 10, 2018, POCML5 completed an initial public offering by way of a capital pool

company prospectus.

On May 20, 2021, POCML5 completed

its “Qualifying Transaction” (as such term is defined under the policies of the TSX Venture Exchange) with Collective Mining

Inc. and filed Articles of Amendment to effect a name change from “POCML 5 Inc.” to “Collective Mining Ltd.”

The registered and head office

of Collective is located at 82 Richmond St. E., Toronto, Ontario M5C 1P1.

Inter-corporate Relationships

The following diagram presents

the inter-corporate relationships among Collective and its subsidiaries, as at the date hereof.

| 1 | Includes the Collective Mining Limited Sucursal Colombia,

a Colombian branch (“Branch”). |

GENERAL DEVELOPMENT OF THE BUSINESS

Collective is a Canadian company

listed on the TSX (the “TSX”) and the NYSE American LLC (“NYSE American”) under the symbol “CNL”.

The Company’s long-term focus is on the acquisition, exploration, development and exploitation of mineral properties in which the

Company’s exploration, development and operating expertise could substantially enhance shareholder value. The Company currently

has one material exploration project which is the 4,398-hectare Guayabales project (the “Guayabales Project”) located

in the Caldas department of Colombia. The Company also owns the 4,797-hectare San Antonio project also located in a historical gold district

in the Caldas department of Colombia (the “San Antonio Project” and, together with the Guayabales Project, the “Colombia

Projects”), however, the focus of the Company is on the Guayabales Project, which is currently its only material project. As

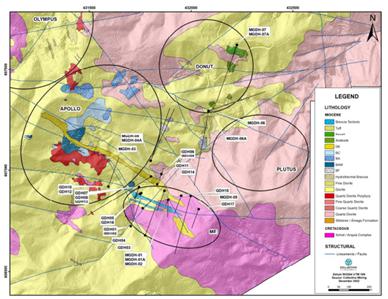

at the date of this AIF, the Company has made a significant gold, copper, silver, tungsten discovery called the Apollo system, made other

earlier stage discoveries such as the Trap target and generated a number of other targets at the Guayabales Project.

Three-Year History and Significant Acquisitions

2022

On July 18, 2022, the Common Shares commenced

trading on the OTCQX® Best Market under the symbol “CNLMF”. The Company upgraded to the OTCQX from the Pink® market

and its Common Shares became eligible for electronic clearing and settlement through The Depository Trust Company in the United States.

On October 25, 2022, the Company completed a “bought

deal” offering of units (the “2022 Units”) for aggregate gross proceeds of approximately C$10.7 million. The

offering was conducted by a syndicate of underwriters led by Clarus Securities Inc., and including BMO Nesbitt Burns Inc. and TD Securities

Inc., and consisted of the sale of 4,783,400 2022 Units (including the partial exercise of an overallotment option) at a price of C$2.25

per 2022 Unit. Each 2022 Unit was comprised of one Common Share and one-half of one Common Share purchase warrant, with each whole warrant

entitling the holder thereof to acquire one Common Share at a price of $3.25 until April 25, 2024.

2023

On March 22, 2023, the Company completed a “bought

deal” offering of Common Shares for aggregate gross proceeds of approximately C$30 million. The offering was conducted by a syndicate

of underwriters co-led by BMO Capital Markets and Clarus Securities Inc., and including Canaccord Genuity Corp., Cormark Securities Inc.

and PI Financial Corp., and consisted of the sale of 7,060,000 Common Shares at a price of C$4.25 per Common Share.

On May 2, 2023, the Company

filed an updated NI 43-101 technical report for the Guayabales Project. See “Guayabales Project”.

On September 6, 2023, the Company

graduated from the TSX Venture Exchange to the TSX and the Common Shares commenced trading on the TSX effective market open on September

6, 2023 under its current stock symbol “CNL”.

On November 8, 2023,

the Company appointed Angela María Orozco Gómez as a director of the Company. Mrs. Orozco Gómez is a seasoned executive

with over 30 years of government and international experience. Most recently, Mr. Orozco Gómez was the Minister of Transport

and Infrastructure, Colombia where she led various initiatives that secured public and private investments in the transportation and infrastructure

industries. Mrs. Orozco Gómez has also been a partner in various private ventures that helped to represent industries in

international trade disputes.

On December 6, 2023,

the Company filed a final short form base shelf prospectus (the “Shelf Prospectus”) with the securities regulatory

authorities in each of the provinces and territories of Canada (other than Québec), following the completion of a regulatory review

of the preliminary base shelf prospectus of the Company. The Shelf Prospectus filing will permit the Company to make offerings of common

shares, warrants, subscription receipts, units or debt securities, or a combination thereof (the “Securities”), up

to an aggregate total of C$200 million during the 25-month period that the Shelf Prospectus remains effective until January 2026.

Securities may be offered in amounts, at prices and on terms to be determined based on market conditions at the time of sale and set forth

in one or more shelf prospectus supplement(s). Information regarding the use of proceeds from a sale of any Securities will be included

in the applicable prospectus supplement(s).

2024

On March 4, 2024,

the Company completed a strategic investment with Agnico Eagle Mines Ltd. (“Agnico Eagle”) on a non-brokered

private placement basis consisting of the sale of 4,500,000 units (each a “March 2024 Unit”), at a price of $4.20

per March 2024 Unit for gross proceeds of C$18.9 million (the “March 2024 Private Placement”). Each March 2024

Unit was comprised of one Common Share and one-half of one Common Share purchase warrant (each whole warrant, a

“Warrant”). Each Warrant will entitle the holder thereof to acquire one Common Share (a “Warrant

Share”), subject to standard anti-dilution provisions, at a price of $5.01 per Warrant Share exercisable until 5:00 p.m.

(Toronto time) on the date that is 36 months following the closing date of the offering (the “Warrant Term”),

provided, however, that should the closing price at which the Common Shares trade equal to or exceed $6.00 for 20 consecutive

trading days following the date that is 24 months after the Closing Date, the Company may accelerate the Warrant Term to the date

which is 30 trading days following the date a notice is provided to holders of Warrants and a press release is issued by the Company

announcing the accelerated Warrant Term.

In connection with the

March 2024 Private Placement, the Company and Agnico Eagle entered into an investor rights agreement (the “Investor Rights Agreement”),

pursuant to which Agnico Eagle is entitled to certain rights, provided Agnico Eagle maintains certain ownership thresholds in the Company,

including: (a) the right to participate in equity financings and top-up its holdings in relation to dilutive issuances in order to maintain

its pro rata ownership interest at the time of such financing or issuance or acquire up to a 9.99% ownership interest in the Company on

a partially-diluted basis; and (b) the right to nominate one person (and in the case of an increase in the size of the board of directors

of the Company (the “Board”) to eight or more directors, two persons) to the Board in the event that Agnico Eagle’s

ownership interest in the Company exceeds and remains at or above 10%, on a partially-diluted basis.

On March 26, 2024, the Company announced the retirement

of Dr. Ken Thomas from its Board effective April 10, 2024.

On July 22, 2024, the Common Shares commenced

trading on NYSE American under the symbol “CNL” and ceased trading on the OTCQX.

On October 31, 2024, the Company completed a (i)

“bought deal” offering of Common Shares, pursuant to a public offering in Canada (the “Public Offering”)

and a private placement in the U.S. (together with the Public Offering, the “Offering”) and (ii) completed a non-brokered

private placement (the “Concurrent Private Placement”) with Agnico Eagle for aggregate gross proceeds of approximately

C$46.4 million including the exercise of the overallotment option. The Public Offering was conducted by a syndicate of underwriters led

by BMO Capital Markets, as sole bookrunner, and including Clarus Securities Inc., Scotia Capital, among others. In aggregate, the Company

issued 9,276,235 Common shares at a price of C$5.00 per share. The Concurrent Private Placement was completed to enable Agnico Eagle to

top-up its ownership interest in the Company to approximately 9.99% on a partially-diluted basis after giving effect to the Offering,

as required pursuant to the terms of the Investor Rights Agreement.

On December 16, 2024, the Company announced that

Mr. Paul Murphy, a valued member of Collective’s Board, passed away.

Events Subsequent to Year

ended December 31, 2024

On February 6, 2025,

the Company announced the appointment of Jasper Bertisen to its Board of Directors. Mr. Bertisen is a seasoned leader in the mining

industry with a proven track record of successfully driving strategic initiatives. He has spent the majority of his career in mining private

equity with Resource Capital Funds, overseeing due diligence and strategy execution for investments spanning development-stage to producing

assets across various commodities and global markets. With extensive governance experience, Jasper has served on the boards of both private

and public mining companies, as well as on the advisory boards of several mining technology companies. He is also an Adjunct Professor

at the Colorado School of Mines and holds M.Sc. degrees in Mining Engineering and Mineral Economics.

On March 20, 2025, the

Company completed a non-brokered private placement with Agnico Eagle pursuant to which Agnico Eagle subscribed for 4,741,984 Common Shares

at a price of C$11.00 per Common Share for gross proceeds of C$52,161,824 (the “March 2025 Private Placement”). Concurrently

with the closing of the March 2025 Private Placement, Agnico Eagle exercised all of the 2,250,000 Warrants it acquired in the March 2024

Private Placement at a price of $5.01 per Warrant Share for additional, aggregate consideration to the Company of C$11,272,500. On closing

of the March 2025 Private Placement (and the exercise of the Warrants), Agnico Eagle owned 12,718,219 Common Shares, and no other securities

of the Company, representing approximately 14.99% of the issued and outstanding Common Shares on a non-diluted basis.

Concurrent with the closing of the March

2025 Private Placement, the Investor Rights Agreement was amended (the “Amended and Restated Investor Rights

Agreement”) to increase the ownership interest ceiling in the participation right and top-up right described above from

9.99% to 14.99% on a partially-diluted basis to match Agnico Eagle’s ownership level as at the closing of the March 2025

Private Placement.

DESCRIPTION OF THE BUSINESS

Summary

As

described above under “General Development of the Business”, the Company is a natural resource exploration company

engaged in the business of acquisition, exploration, development and exploitation of mineral properties whose current efforts are focused

on the exploration of the Colombian Projects. See “Guayabales Project”.

Specialized Skill and Knowledge

All

aspects of the Company’s business require specialized skills and knowledge. Such skills and knowledge include the areas of geology,

mining, metallurgy, environmental permitting, corporate social responsibility, finance, and accounting. The Company faces competition

for qualified personnel with these specialized skills and knowledge, which may increase costs of operations or result in delays.

Competitive Conditions

The

mineral exploration and mining business are extremely competitive. Competition is primarily for: (a) mineral properties that can be developed

and operated economically; (b) technical experts that can find, develop and mine such mineral properties; (c) labour to operate the mineral

properties; and (d) capital to finance development and operations. The Company competes with other mining companies, some of which have

greater financial resources and technical facilities, for the acquisition of mineral concessions, claims, leases, and other interests,

to finance its activities and in the recruitment and retention of qualified employees. The ability of the Company to acquire and develop

precious metal properties will depend not only on its ability to raise the necessary funding but also on its ability to select and acquire

suitable prospects for precious metal development and operation or metal exploration. See “Financing Risk” and “Competition”

under “Risk Factors”.

Cycles

The

Company’s business does not have any material cyclical or seasonal business lines.

Renegotiation or Termination

of Contracts

Management

of the Company does not anticipate that there will be any material renegotiations or terminations of existing contracts within the next

12 months.

Employees

As

at the date of this AIF, the Company had 102 employees, which includes employees located in Canada, United States and Colombia. In addition,

there were 337 contractors working on the Guayabales Project and 25 contractors working on the San Antonio Project.

Bankruptcy and Similar

Procedures

There

have been no bankruptcy, receivership, or similar proceedings against the Company or any of its subsidiaries, or any voluntary bankruptcy,

receivership, or similar proceedings by the Company or any of its subsidiaries, within the three most recently completed financial years

or during or proposed for the current financial year.

Reorganizations

Other

than the Business Combination, there have been no material reorganizations of the Company or any of its subsidiaries within

the three most recently completed financial years or during or proposed for the current financial year.

Emerging Market Disclosure

Operations

in an Emerging Market Jurisdiction

The

Company’s mineral properties and principal business operations are located in a foreign jurisdiction, namely the Republic of Colombia.

Operating in Colombia exposes the Company to various degrees of political, economic and other risks and uncertainties.

Board

and Management Experience and Oversight

Key

members of the Company’s management team and Board of directors have extensive experience running business operations in Colombia.

Mr. Ari Sussman, the Executive Chairman of the Company, was Chief Executive Officer and a director of Continental Gold Inc. (“Continental

Gold”), and Mr. Paul Begin, the Chief Financial Officer and Corporate Secretary of the Company,

was Chief Financial Officer of Continental Gold, which was the largest gold mining company in Colombia and the first to successfully permit

and construct a modern large-scale underground gold mine in the country. Continental Gold was a former Toronto Stock Exchange-listed issuer,

from March 2010 until it was acquired by Zijin Mining Group Co., Ltd. in March 2020 for over C$1.4 billion.

Mr.

Omar Ossma, the President and Chief Executive Officer of the Company, was the former Vice President, Legal of Continental Gold, and has

over 20 years of legal experience in Colombian corporate, environmental, mining and energy law. As Vice President, Legal of Continental

Gold, he oversaw the Colombian legal team and was responsible for all legal support efforts in the country.

Ms.

Maria Constanza García Botero, an independent director of the Company, is a resident of Colombia, and has worked in public finance,

urban development, infrastructure, mining, energy, and public-private partnerships (PPPs) as an advisor or in various management positions

at the National Planning Department, the Ministry of Finance, and the National Hydrocarbons Agency. From 2010 to 2012 she served as the

Deputy Minister of Infrastructure at the Ministry of Transport (Colombia), and from 2012 to 2014, served as President of the National

Mining Agency, Ministry of Mining and Energy (Colombia).

Mrs. Angela María

Orozco Gómez, an independent director of the Company, is a resident of Colombia and has 30 years of government and international

experience. Most recently, Mrs. Orozco Gómez was the Minister of Transport and Infrastructure, Colombia where she led various

initiatives that secured public and private investments in the transportation and infrastructure industries. Mrs. Orozco Gómez

has also been a partner in various private ventures that helped to represent industries in international trade disputes.

Mr.

Ashwath Mehra is a seasoned executive with over 35 years’ experience in the mineral industry. Mr. Mehra spent many years in the

commodity trading and mining business as well as owning, buying and selling companies globally.

Mr.

Jasper Bertisen is a seasoned leader in the mining industry with a proven track record of successfully driving strategic initiatives.

He has spent the majority of his career in mining private equity with Resource Capital Funds, overseeing due diligence and strategy execution

for investments spanning development-stage to producing assets across various commodities and global markets.

The

Board, as well as management and consultants, are actively involved in technical activities, risk assessments and progress reports in

connection with the Company’s exploration activities. The Colombian-resident Board and management members work directly with local

contractors in an operational capacity, and are familiar with the laws, business culture and standard practices in Colombia, are fluent

in Spanish, and are experienced in dealing with Colombian government authorities, including with respect to mineral exploration licensing,

maintenance, and operations.

Communication

While

the reporting language of the head office of the Company is English, the primary operating language in Colombia is Spanish. The senior

management team in Colombia together with Ms. García Botero and Mrs. Orozco Gómez,

are bilingual in English and Spanish, and Mr. Sussman is fluent in English and conversationally fluent in Spanish. The Company maintains

open communication with its Colombian operations through its partially bilingual Board, such that there are no language barriers between

the Company’s management and local operations.

The

Company’s management communicates with its in-country operations through phone and video calls and conferences, in-country work,

meetings, e-mails, and regular reporting procedures. In addition, Collective retained Lloreda Camacho & Co., a law firm based in Bogota,

Colombia, as its legal advisors for all Colombian related matters. Professionals at Lloreda Camacho & Co. acting on behalf of Collective

are bilingual in both English and Spanish.

Controls

Relating to Corporate Structure Risk

The

Company has implemented a system of corporate governance, internal controls over financial and disclosure controls and procedures that

apply to the Company, Collective Mining Limited (Bermuda) including the Branch and its two indirect Colombian subsidiaries, Minerales

Provenza and Minera Campana (together with Minerales Provenza, the “Colombian Subsidiaries”),

which are overseen by the Board and implemented by senior management.

The

relevant features of these systems include direct oversight over the Branch and the Colombian Subsidiaries’ operations by Omar Ossma,

as the principal representative of each of the Colombian Subsidiaries and who is also the President and Chief Executive Officer of the

Company. Since the Company indirectly holds all of the issued and outstanding equity interests of the legal entity that comprises the

Branch and the Colombian Subsidiaries, the Company exercises effective control over the Branch and the management of each of the Colombian

Subsidiaries, as well as its composition.

Executive

management and the Board prepare and review the Colombian Subsidiaries’ financial reporting as part of preparing its consolidated

financial reporting, and the Company’s independent auditors review the consolidated financial statements under the oversight of

the Company’s Audit Committee.

Local

Records Management

The

minute books and corporate records of each of the Colombian Subsidiaries are maintained and held by the Company at Avenida El Poblado,

Carrera 43 No. 9 Sur 195, Oficina 1034, Edificio Square, Medellin, Colombia. Senior management control these records and the Board and

management team have full access.

Strategic

Direction

While

the exploration operations of each of the Branch and the Company’s subsidiaries are managed locally, the Board is responsible for

the overall stewardship of the Company and, as such, supervises the management of the business and affairs of the Company. More specifically,

the Board is responsible for reviewing the strategic business plans and corporate objectives, and approving acquisitions, dispositions,

investments, capital expenditures and other transactions and matters that are material to the Company including those of its material

subsidiaries.

Disclosure

Controls and Procedures

The

Company has a disclosure policy that establishes the protocol for the preparation, review and dissemination of information about the Company.

This policy provides for multiple points of contact in the review of important disclosure matters, which includes input from Board members

in Colombia.

CEO

and CFO Certifications

In

order for the Company’s Chief Executive Officer and Chief Financial Officer to be in a position to attest to the matters

addressed in the quarterly and annual certifications required by National Instrument 52-109 – Certification of Disclosure

in Issuers’ Annual and Interim Filings, the Company has developed internal procedures and responsibilities throughout the

organization for its regular periodic and special situation reporting, in order to provide assurances that information that may

constitute material information will reach the appropriate individuals who review public documents and statements relating to the

Company and its subsidiaries containing material information, is prepared with input from the responsible officers and employees,

and is available for review by the Chief Executive Officer and Chief Financial Officer of the Company in a timely manner.

Managing

Cultural Differences

Differences

in cultures and practices between Canada and Colombia are addressed by the engagement of Colombian-resident Board and management members,

as well as local advisors, who have deep operational experience with the mineral exploration industry in Colombia and are familiar with

the local laws, business culture and standard practices, have local language proficiency, are experienced in working in Colombia and in

dealing with the relevant government authorities and have experience and knowledge of the local banking systems and treasury requirements.

In addition, most of the Company’s management team members that are non Colombians have been involved in the Colombian mineral exploration

and development industry for over 10 years through their involvement with Continental Gold (as further described above), developing an

understanding of the relevant cultural differences and helping in mitigating potential risks from cultural differences.

Transactions

with Related Parties

The

Company is subject to applicable Canadian and United States securities laws and applicable exchange rules and Canadian accounting rules

with respect to approval and disclosure of potential related party transactions and has procurement and other policies in place which

it follows to mitigate risks associated with potential related party transactions. The Company may in the future transact with related

parties from time to time, in which case such related party transactions may require disclosure in the consolidated financial statements

of the Company and in accordance with applicable Canadian securities laws and accounting rules.

Controls

Relating to Verification of Property Interests

The

Company engaged a local team with broad experience in mining exploration in Colombia, as well as in legal, social, and environmental matters.

The lead team in Colombia was previously successful in licensing, building, and putting into operation other mining projects in Colombia.

This contributed to obtaining an understanding of the framework surrounding the good standing of the Company’s properties and assets,

from a legal, social, and environmental perspective.

The

lead team was tasked with the negotiation and acquisition of properties that comprise the Colombian Projects. The current President and

Chief Executive Officer of the Company, Mr. Omar Ossma, who led the negotiations and acquisitions of the Company’s current projects,

is a licensed lawyer in Colombia, with more than 20 years of professional experience in Colombian corporate, environmental, mining and

energy law, 15 of which have been dedicated to the mining and energy sectors. His knowledge of the legal framework of mineral properties

and assets assisted the Company in negotiating and entering into legally binding agreements under Colombian law, ensuring the good standing

of the Company’s rights over the acquired assets and properties.

The

Company also retained an established and leading law firm based in Bogota, Colombia, as its legal advisors for all Colombian related matters,

that is widely known for their mining practice. In addition to providing a wide array of legal services beginning from the date of incorporation

of the Company’s Colombian subsidiaries, the law firm also prepared and delivered title opinions with respect to the Company’s

current Colombian properties.

In

addition, the Company retained two independent consulting firms specializing in the mining sector, with significant experience in social,

engineering, environmental and other sustainability matters that prepared and delivered a due diligence report on the socio-economic and

environmental conditions of the properties comprising the San Antonio option, as well as the first and second Guayabales options, and

a baseline study report on the performance of certain socio-economic, health and safety measures in the property area.

License,

Permitting and other Regulatory Approvals

Based

on consultations with its local advisers and government authorities, the Company satisfied itself that it has obtained all required permits,

licenses and other regulatory approvals to carry out its business in Colombia. The table set out below details which material permits,

business licenses and other regulatory approvals are required for the Company to carry out its business operations in Colombia.

| Material permit, license and/or other regulatory approval required to conduct operations |

|

Material permit, license and/or regulatory approval obtained by the Company |

| Operating as a company requires a Public commercial registry before the Chamber of Commerce. This registry also activates a Tax Registry. |

|

Obtained. |

| |

|

|

| Prospecting activities (all exploration excluding drilling) are free activities in Colombia, and require no permit, other than authorization for land access from private owner. |

|

The Company generally negotiates land access permits in advance to its operations. Currently, the Company has all required land access permits for its current prospecting campaign. |

| |

|

|

| Drilling activities require a valid mining right and/or mining title granted by the National Mining Authority. |

|

The Company is conducting exploration activities on mining titles LH0071-17, 781-17, HI8-15231, 501712 and IIS-10401 which are validly granted mining titles. |

| |

|

|

| Drilling activities will require authorization for land access from private owner. |

|

The Company generally negotiates land access permits in advance to its operations. Currently, the Company has all required land access permits for its current drilling campaign. |

| |

|

|

| Exploration activities are not subject to environmental license. However, if the activities require the use of natural renewable resources (such as water catchments, dumpings and timbering, amongst others) the Company will require a filing, and further permission, before the regional environmental corporation in the territory. |

|

The Company has been granted water rights for its drilling campaign, both in San Antonio and Guayabales projects, and may also recur to purchase water in bulk to perform its drilling campaign. |

| |

|

|

| Construction of a mining project, and its operation requires an environmental license granted by an environmental authority. |

|

The Company is not currently in a position to advance either of its properties to the development and construction phase of a mining project, therefore it does not require an environmental license at this time. |

| |

|

|

| Construction of a mining project, and its operation requires a work plan approved by the applicable mining authority. |

|

The Company is not currently in a position to advance either of its properties to the development and construction phase of a mining project, therefore it does not require a work plan at this time. |

As

at the date of this AIF, no restrictions or conditions have been imposed by the government of Colombia on the Company’s ability

to operate in Colombia. The Company’s continued ability to operate in Colombia could be impacted as a result of: (i) a drastic change

in water conditions which may result in restrictions on already granted water rights; (ii) a breach of environmental commitments and/or

regulations by the Company; (iii) the declaration of environmentally protected areas which could restrict mining activities on the Company’s

current projects; or (iv) court ordered public hearings in regards to the presence of ethnic minorities on the Company’s properties.

See “Risk Factors”.

RISK FACTORS

The

Company is engaged in the exploration, development and acquisition of mining properties and projects. Due to the high-risk nature of the

Company’s business, the Company’s operations are speculative. The Company’s operations, properties and projects are

subject to various risks and uncertainties, including but not limited to, those listed below. The risks described herein are not the only

risk factors facing the Company and should not be considered exhaustive. Additional risks and uncertainties not currently known to the

Company, or that the Company currently considers immaterial, may also materially and adversely affect the business, operations and condition,

financial or otherwise, of the Company. These risk factors, together with all other information included or incorporated by reference

in this AIF, including, without limitation, information contained in the section “Cautionary Statement Regarding Forward Looking

Information” as well as the risk factors set out below, should be carefully reviewed by readers.

Some

of the factors described herein, in the documents incorporated or deemed incorporated by reference herein, are interrelated and, consequently

readers should treat such risk factors as a whole. If any of the adverse effects set out in the risk factors described herein or in another

document incorporated or deemed incorporated by reference herein occur, it could have a material adverse effect on the business, financial

condition and results of operations of the Company. The Company cannot assure you that it will successfully address any or all of these

risks. There is no assurance that any risk management steps taken will avoid future loss due to the occurrence of the adverse effects

set out in the risk factors herein, in other documents incorporated or deemed incorporated by reference herein or other unforeseen risks.

These risk factors could materially affect the Company’s future operating results and could cause actual events to differ materially

from those described in the Company’s forward-looking statements. Unless the context indicates or implies otherwise, references

in this section to the “Company” include the Company and its subsidiaries.

Nature of Mineral Exploration

Resource

exploration and development is a speculative business and involves a high degree of risk which even a combination of experience, knowledge

and careful evaluation may not be able to overcome. The properties in which the Company holds an interest are without a known mineral

resource or reserve. Each of the proposed programs on the properties is an exploratory search for resources or additional resources. There

is no assurance that commercial quantities of resources will be discovered. There is also no assurance that even if commercial quantities

of resources are discovered, a mineral property will be brought into commercial production. The discovery of mineral deposits is dependent

upon a number of factors, not the least of which is the technical skill of the exploration personnel involved. The commercial viability

of a mineral deposit, once discovered, is also dependent upon a number of factors, some of which are the particular attributes of the

deposit, such as size, grade, ground conditions, metallurgy, proximity to infrastructure, community relations, metal prices and government

regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals, and environmental

protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in the Company

not receiving an adequate return on invested capital. There is no certainty that the expenditures made by the Company towards the search

and evaluation of mineral deposits will result in discoveries of economic commercial quantities of ore.

Foreign Country Risk

The

Company’s principal mineral properties are located in rural Colombia. Over the past 15 to 20 years, the Government of Colombia

has made strides in improving the social, political, economic, legal and fiscal regimes. However, operations in Colombia are still

subject to risk due to the potential for social, political, economic, legal and fiscal instability. The government in Colombia faces

ongoing problems including, but not limited to, unemployment and inequitable income distribution and unstable neighboring countries.

The instability in neighboring countries could result in, but not be limited to, an influx of immigrants which could result in a

humanitarian crisis and/or increased illegal activities. Colombia is also home to a number of insurgency groups and large swaths of

the countryside are under guerrilla influence. In addition, Colombia experiences narcotics-related violence, a prevalence of

kidnapping, extortion and thefts and civil unrest in certain areas of the country. Such instability may require the Company to

suspend operations on its properties. There is a risk that agreements with the police and/or army are required and cannot be

reached on time or on terms that are acceptable to the Company, which could result in an increase in security threats or loss of

control at the project site that could have a material adverse effect on the Company.

Although

the Company is not presently aware of any circumstances or facts which may cause the following to occur, other risks may involve matters

arising out of the evolving laws and policies in Colombia, any future imposition of special taxes or similar charges, as well as foreign

exchange fluctuations and currency convertibility and controls, the unenforceability of contractual rights or the taking or nationalization

of property without fair compensation, restrictions on the use of expatriates in the Company’s operations, renegotiation or nullification

of existing concessions, licenses, permits and contracts, illegal mining, changes in taxation policies, changes in mining and environmental

laws or other matters.

Guerilla

Activity

Colombia

has experienced, and continues to experience, internal security issues, primarily due to the activities of guerrilla groups, drug cartels

and criminal gangs. In rural regions of the country with minimal governmental presence, these groups have exerted influence over the local

population, assassinated local social leaders, and funded their activities by protecting and rendering services to drug traffickers and

participating in drug trafficking activities. Certain areas in which the Company operates have been historically impacted by the activities

of these groups. Even though the Colombian Government’s programs and policies have reduced guerrilla and criminal activity, particularly

in the form of terrorist attacks, homicides, kidnappings and extortion, such criminal activity persists in Colombia. Possible escalation

of such activity and the effects associated with it may have a negative effect on the Colombian economy and on the Company, its employees,

financial condition and results of operations The Government of Colombia reached a peace accord in 2016 with the country’s largest

guerrilla group. During 2023, the Government of Colombia entered into formal discussions with another guerrilla group for a future peace

accord, as well as seeking such agreements with other relevant illegal armed groups. Subsequent to year end, the Government of Colombia

suspended discussions with the referred guerrilla group on account of disturbances in certain regions of Colombia. There is no clear agenda

or date to initiate discussions. There is no certainty that the agreements will be adhered to by all of the members of the guerrilla groups

or that a peace agreement will be ultimately reached with the country’s largest guerrilla group or the other existing illegal armed

groups. There can also be no assurance that continuing attempts to reduce or prevent guerilla, drug trafficking or criminal activity will

be successful or that guerilla, drug trafficking and/or criminal activity will not disrupt the Company’s operations in the future.

There is a risk that any peace agreement might contain new laws or change existing laws that could have a material adverse effect on the

Company’s projects. Furthermore, the achievement of peace with the country’s guerrilla groups or other illegal armed groups

could create additional social or political instability in the immediate aftermath, which could have a material adverse effect on the

Company as, among other things, the perception that matters have not improved in Colombia may hinder the Company’s ability to access

capital in a timely or cost-effective manner.

See

“Description of the Business – Emerging Market Disclosure”.

Foreign Operations

The

Company’s exploration operations are located in Colombia. Colombia’s legal and regulatory requirements in connection with

companies conducting mineral exploration and mining activities, banking system and controls as well as local business culture and practices

are different from those in Canada. The officers and directors of the Company must rely, to a great extent, on the Company’s Colombian

management, legal counsel and local consultants retained by the Company in order to keep abreast of material legal, regulatory and governmental

developments as they pertain to and affect the Company’s business operations, and to assist the Company with its governmental relations.

The Company must rely, to some extent, on the members of management and the Board who have previous experience working and conducting

business in Colombia to enhance its understanding of and appreciation for the local business culture and practices in Colombia. The Company

also relies on the advice of local experts and professionals in connection with current and new regulations that develop in respect of

banking, financing and tax matters in Colombia. Any developments or changes in such legal, regulatory or governmental requirements or

in local business practices in Colombia are beyond the control of the Company and may adversely affect its business.

The

Company also bears the risk that changes can occur to the Government of Colombia and a new government may void or change the

laws and regulations that the Company is relying upon. Currently, there are no restrictions on the repatriation from Colombia of

earnings to foreign entities and Colombia has never imposed such restrictions. However, there can be no assurance that restrictions

on repatriation of earnings from Colombia will not be imposed in the future. Exchange control regulations require that any proceeds

in foreign currency originated on exports of goods from Colombia (including minerals) be repatriated to Colombia. However, purchase

of foreign currency is allowed through any Colombian authorized financial entities for purposes of payments to foreign suppliers,

repayment of foreign debt, payment of dividends to foreign stockholders and other foreign expenses.

Due

to its locations in Colombia, the Company depends in part upon the performance of the Colombian economy. As a result, the Company’s

business, financial position and results of operations may be affected by the general conditions of the Colombian economy, price instabilities,

currency fluctuations, inflation, interest rates, regulatory changes, taxation changes, social instabilities, political unrest and other

developments in or affecting Colombia over which the Company does not have control. Because international investors’ reactions to

the events occurring in one emerging market country sometimes appear to demonstrate a “contagion” effect in which an entire

region or class of investment is disfavoured by international investors, Colombia could also be adversely affected by negative economic

or financial developments in other emerging market countries.

See

“Description of the Business – Emerging Market Disclosure”.

Financing Risk

The

Company has limited financial resources and has limited sources of operating cash flow. The Company will require additional funds to finance

exploration and future acquisitions. The exploration and development of the various mineral properties in which the Company holds interests

and the acquisition of additional properties depend upon the Company’s ability to obtain financing through equity financings, joint

ventures of projects, stream financing, debt financing or other means. The perception that security conditions in Colombia have not improved

and the decline in the capital markets for the extractive industry could hinder the Company’s ability to access capital in a timely

or cost-effective manner. Although the Company has been successful in raising funds, including an aggregate of approximately C$87.0 million

raised pursuant to three “bought deal” offerings completed in October, 2022, March, 2023 and October, 2024 (including the

Concurrent Private Placement) and approximately C$71 million raised pursuant to March 2024 Private Placement and the March 2025 Private

Placement, there can be no assurance that the Company will be able to raise additional financing required or that such financing will

be available on terms acceptable to the Company. Failure to obtain additional financing on a timely basis may result in delays or an indefinite

postponement of exploration, development, or production on any or all of the Company’s properties, could cause the Company to reduce

or terminate its operations or lose its interests in its properties and cease to continue as a going concern.

In

addition, there can be no assurance that future financing can be obtained without substantial dilution to existing shareholders. The issuance

of additional securities and the exercise of common share purchase warrants, stock options and other convertible securities will result

in dilution of the equity interests of any persons who are or may become holders of Common Shares.

Property Interests

The

ability of the Company to carry out successful mineral exploration, development and production activities will depend on a number of factors.

The Company has a number of obligations with respect to acquiring and maintaining the Company’s interest in certain of its current

properties. No guarantee can be given that the Company will be in a position to comply with all such conditions and obligations, or to

require third parties to comply with their obligations with respect to such properties. Furthermore, while it is common practice that

permits and licenses may be renewed, extended or transferred into other forms of licenses appropriate for ongoing operations, no guarantee

can be given that any such renewal, extension or transfer will be granted to the Company or, if they are granted, that the Company will

be in a position to comply with all conditions that are imposed. Some of the Company’s interests are the subject of pending applications

to register assignments, extend the term, and increase the area or to convert licenses to concession contracts and there is no assurance

that such applications will be approved as submitted.

There

is no assurance that the Company’s rights and foreign interests will not be revoked or significantly altered to the detriment of

the Company.

No Assurance of Titles

or Boundaries

The

Company is not the registered holder of all of the licences or concessions that comprise its projects in Colombia. Some of the licences

and concessions that comprise the Company’s projects in Colombia are registered in the names of certain third-party entities. The

Company’s interest in the Colombia Projects is partially derived from option agreements. Under the option agreements, third parties

have agreed to transfer the licences and concessions that comprise such properties to the Company upon satisfaction of certain conditions

including but not limited to the receipt of all of the option payments. In the meantime, in certain circumstances, the third parties are

allowed to continue to operate under certain restrictive conditions. There can be no assurance, however, that the third parties will operate

under the agreed upon conditions and that such transfers will be effected. Failure to operate under the agreed conditions could result

in a material loss and have a materially negative impact on the Company’s operations. Also, events may occur that would prevent

the third-party entities from being able to transfer such licences and concessions to the Company. In addition, in the event of a dispute

between the parties, the Company’s only recourse would be to commence legal action in Colombia. If the Company is required to commence

legal proceedings, there is no assurance that the Company will succeed in such proceedings, and, therefore, may never obtain title to

such properties.

Other

parties may dispute title to any of the Company’s mineral properties or land titles, any of the Company’s properties may be

subject to prior unregistered agreements, transfers or claims, and title may be affected by, among other things, undetected encumbrances

or defects or governmental actions or errors. A successful challenge to the precise area and location of the Company’s projects

could result in the Company being unable to operate on its properties as permitted or being unable to enforce its rights with respect

to its properties.

Land Surface and Access

Rights

Even

though the Company has advanced in the acquisition of surface rights relevant to its ongoing operations, as well as a future mine, it

does not own all of the surface rights required to build a future project. There is a risk that the Company will not be able to purchase

all of the surface rights from third parties or on terms that are acceptable to the Company. Additionally, Colombia Law 1448/2011 compensates,

with land restitution, communities that have been displaced as a result of political violence. In the event that the Company is impacted

by application of Law 1448/2011, it has the right to begin an expropriation process available under Colombian law, although the process

could take longer than expected. Although the Company does not expect the effects of Law 1448/2011 to impact the Company, there is a risk

that land near or on the Company’s projects could be impacted, which could have a material adverse effect on the Company.

In

order for the Company to conduct exploration including but not limited to surface reconnaissance work, mapping and drilling, it requires

permission from third party owners of land. There is a risk that the Company will not be able to negotiate land access rights from third

party landowners, which would have a material adverse effect on the Company’s exploration activities. Even though not a common practice,

the Company may rely on judicial proceedings to obtain rights of way on third party land.

The

Company has a number of option agreements with third parties for surface rights (property and/or adverse possession) which are payable

over a number of years. There is a risk that title will not be transferred to the Company by the third party at the termination of the

option agreements in which case the Company’s only recourse would be through legal actions, or by application of mining expropriation.

Enforcing contracts through legal avenues, or applying expropriation will take years to resolve. If any of these events occur, it could

have a material negative impact on the Company.

In

addition, the Company is purchasing surface rights or entering into option agreements for surface rights in rural Colombia where land

titles are characterized by adverse possession rights and not necessarily by land deeds. Although the Company performs due diligence to

ensure that adverse possession rights belong to the third parties that it enters into contracts with, there is a chance that another third

party could claim the same possession rights or ownership with a deed which could have a material negative effect on the Company.

Decree 044

On

January 30, 2024, the Colombian Ministry of Environment issued Decree 044 which allows the Ministry to declare temporary reserve areas

in certain parts of Colombia. To declare a temporary reserve area, a resolution must be issued by the Ministry detailing the area that

is to be temporarily reserved. Pursuant to this decree, a subsequent resolution may mandate a five-year suspension of environmental license

awards, extendable for a further five years, while studies are conducted to determine if an area should be restricted or excluded from

mining. However, this decree does not limit the possibility to continue environmental studies in a mandated area. Decree 044 is presently

being challenged at constitutional and administrative courts, led by the Colombian Disciplinary Office, artisanal and small mining units,

the Colombian Mining Trade Association and the National trade association. Decree 044 does not currently adversely impact operations at

Guayables or San Antonio.

Artisanal Mining

The

Company’s properties are located in Colombia in an area that has a long history of artisanal mining. A portion of the Company’s

property include artisanal groups that are mining informally on a small-scale basis. The Company is committed to respecting their rights

and to assist them in formalizing, however, there is no assurance that this process will be successful or that they will not oppose the

Company’s exploration activities or potential future development. There is also a risk that the number of informal miners could

increase in the future resulting in a material adverse effect on the Company. In addition, artisanal mining accidents occur and, in some

cases, result in serious injury or death. While the Company is not responsible for artisanal mining operations including their health

and safety standards, an artisanal mining accident could be perceived as the Company’s responsibility which could have a material

adverse effect on the Company.

Community Relations

Maintaining

a positive relationship with the communities in which the Company operates is critical to continuing successful exploration and development.

There can be no assurances that the Company will be successful at managing these impacts and that actions of other mining companies will

not have a negative impact on the Company’s ability to manage these impacts. Community support for operations is a key component

of a successful exploration or development project. Various international and national laws, codes, resolutions, conventions, guidelines

and other materials relating to corporate social responsibility (including rights with respect to health and safety and the environment)

may also require government consultation with communities on a variety of issues affecting local stakeholders, including the approval

of mining rights or permits. The Company may come under pressure in the jurisdictions in which it explores or develops to demonstrate

that other stakeholders benefit and will continue to benefit from its commercial activities. Local stakeholders and other groups may oppose

the Company’s current and future exploration, development and operational activities through legal or administrative proceedings,

protests, roadblocks or other forms of public expression against the Company’s activities. Opposition by such groups may have a

negative impact on the Company’s reputation and its ability to receive necessary mining rights or permits. Opposition may also require

the Company to modify its exploration and development plans or enter into agreements with local stakeholders or governments with respect

to its projects. Any of these outcomes could have a material adverse effect on the Company’s business, financial condition, results

of operations and Common Share price.

Minority Ethnic Groups

Various

international and national laws, codes, resolutions, conventions, guidelines, and other materials relate to the rights of minority

ethnic groups. Many of these materials impose obligations on government to respect the rights of minority ethnic groups. Some

mandate that government consult with minority ethnic groups regarding government actions which may affect minority ethnic groups,

including actions to approve or grant mining rights or permits. The obligations of government and private parties under the various

international and national materials pertaining to Minority Ethnic Groups continue to evolve and be defined. The Company’s

current or future operations are subject to a risk that one or more groups of minority ethnic groups may oppose continued operation,

further development, or new development on those projects or operations on which the Company holds an exploration right. Such

opposition may be directed through legal or administrative proceedings or protests, roadblocks, public hearings or other forms of

public expression against the Company or the owner/operator’s activities. Opposition by minority ethnic groups to such

activities may require modification of or preclude operation or development of projects or may require entering into agreements with

minority ethnic groups. Claims and protests of minority ethnic groups may disrupt or delay activities of the owners/operators of the

Company’s exploration assets.

Dependence on Key Management

Employees

The

Company’s exploration programs will depend on the business and technical expertise of key executives, including the directors of

the Company and a small number of highly-skilled and experienced executives and personnel. Due to the relatively small size of the Company,

the loss of any of these individuals or the Company’s inability to attract and retain additional highly skilled employees may adversely

affect its business and future operations. The Company does not have key man insurance in place with respect to any of these individuals.

Labour and Employment Matters

While

the Company has good relations with its employees, these relations may be impacted by changes in labour laws which may be introduced by

the relevant governmental authorities in jurisdictions in which the Company carries on business. Adverse changes in such legislation may

have a material adverse effect on the Company’s business, results of operations and financial condition.

The

Company’s workforce is not governed by a minority union or a cooperative agreement. Although labour relations with its employees

have been good, there is no assurance that this will continue in the future or that employees will not attempt to organize in the future.

Any significant disruption in labour arrangements could have a material adverse effect on the Company’s reputation and its ability

to continue to operate.

Non-Governmental Organization

Intervention

The

Company’s relationship with the communities in which it operates is critical to ensure the future success of its existing operations.

A number of non-governmental organizations are becoming increasingly active in Colombia as the security and safety in Colombia increases

and the Government implements the peace accords. These organizations may create or inflame public unrest and anti-mining sentiment among

the inhabitants in areas of mineral development. Such organizations have been involved, with financial assistance from various groups,

in mobilizing sufficient local anti-mining sentiment to protest and even prevent the issuance of required permits for the development

of mineral projects of other companies. While the Company is committed to operating in a socially responsible manner, there is no guarantee

that the Company’s efforts in this respect will mitigate this potential risk.

Open Pit Mining

The

Company operates in Colombia which has a long history of open pit mining operations, as well as a current and in force legal framework

which allows for open pit mining. Despite this and the fact that the government has recently issued a number of open pit mining permits,

there can be a perception or misinformation that is prevalent in the media or social media that insinuates that open pit mining is banned