UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the fiscal year ended

or

For the transition period from to

Commission

file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Trading Symbol(s) | Name of each exchange on which registered: | ||

| The

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| ☒ | Smaller reporting company | |||||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

As of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, the registrant’s common stock was not listed on any exchange or over-the-counter market. The registrant’s common stock began trading on the Nasdaq Stock Market on April 2, 2024.

As of April 12, 2024 there were shares of common stock, par value $0.001 per share of the registrant issued and outstanding.

TABLE OF CONTENTS

| 1 |

Unless otherwise stated in this Annual Report on Form 10-K (this “Report”), references to “we,” “us,” “our,” “Company” or “our Company” are to Massimo Group, a Nevada corporation.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements about us and our industry that involve substantial risks and uncertainties. All statements contained in this Report other than statements of historical fact, including statements regarding our future results of operations and financial position, our business strategy and plans, projected costs and our objectives for future operations, are forward-looking statements. In some cases, you can identify forward-looking statements because they contain words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “should,” “shall,” “intend,” “goal,” “objective,” “seek,” “expect,” and similar expressions or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans, or intentions. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including but not limited to: our limited operating history on which to judge our performance and assess our prospects for future success, risks related to our reliance on a network of independent dealers and distributors to manage the retail distribution of many of our products, our reliance on third-party manufacturers and supplies for our products, risks related to the fact that the majority of the products we purchase are manufactured by suppliers in China and their operations are subject to risks associated with business operations in China, the inexperience of our principal shareholder and senior management in operating a publicly traded company, economic conditions that impact consumer spending may have a material adverse effect on our business, results of operations or financial condition, risks related to face intense competition in all product lines, including from some competitors that have greater financial and marketing resources, risks related to our ability to attract and retain key personnel, potential harm caused by misappropriation of our data and compromises in cybersecurity, changes in laws, regulatory requirements, governmental incentives and fuel and energy prices, litigation, regulatory proceedings, complaints, product liability claims and/or adverse publicity, the inability of our dealers, customers and distributors to secure adequate access to capital or financing, failure to develop brand name and reputation, the significant product repair and/or replacement due to product warranty claims or product recalls, the impact of health epidemics, including the COVID-19 pandemic, on our business, the other risks we face and the actions we may take in response thereto and other risks and uncertainties described in this Report, including those described in the “Risk Factors” section. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this Report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. Except as required by applicable law, we undertake no duty to update any of these forward-looking statements after the date of this Report or to conform these statements to actual results or revised expectations.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, and you are cautioned not to unduly rely upon these statements.

You should read this Report and the documents that we reference in this Report and have filed as exhibits to the registration statement, of which this Report is a part, completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of the forward-looking statements in this Report by these cautionary statements.

| 2 |

PART I

Item 1. Business.

Overview

We believe we are a leading company in the Mid-Tier Band of the powersports vehicles and boats industry in the United States, which comprises the All-Terrain Vehicle (“ATV”), Utility-Terrain Vehicle (“UTV”), and pontoon and tritoon boats (“Pontoon Boats”) subsectors (the “Powersports Vehicles and Boats Industry”). “Mid-Tier Band” means the mid-tier band of the Powersports Vehicles and Boats Industry, which our management considers to be those manufacturers that produce a wide range of products that cater to customer needs but do not yet have the international operations and market share of the Top-Tier Band (as defined below) of the Powersports Vehicles and Boats Industry. “Top-Tier Band” means the top-tier band of the Powersports Vehicles and Boats Industry, which our management considers to include companies such as Polaris, Bombardier Recreational Products (BRP), Arctic Cat, Honda, and Yamaha with international operations and large market shares.

In 2020, we became one of the 15 largest Pontoon Boats manufacturers in Texas. Our emphasis on providing the sports enthusiast with powerful, affordable, and reliable products has enabled us to grow annual revenues and net income to in excess of $86 million and $4 million, respectively, in the fiscal year ended December 31, 2022 and in excess of $115 million and $10 million, respectively, in the fiscal year ended December 31, 2023.

We manufacture, import and distribute a diversified portfolio of products divided into two main lines: (1) UTVs, ATVs, motorcycles, scooters, golf carts and a juvenile line from go karts to balance bikes; and (2) recreational Pontoon Boats. In 2009, we began by distributing electric scooters, our first product. Since that time, we have successfully entered the market for motorcycles, UTVs, ATVs, golf carts and Pontoon Boats, as well as a juvenile line from go karts to balance bikes and snow equipment. We have also been developing new product lines, such as electric vehicle (“EV”) chargers, electric coolers, power stations, portable solar panels and electric Pontoon Boats, all of which are currently available for sale. In addition to distributing our products, we intend to provide unparalleled customer service which includes over 600 motor vehicles and 5,500 marine third-party service providers across the United States, 24-hour customer support and an approximately 40,000 sq. ft. parts facility which enables us to fulfill most parts orders within 48 hours.

We seek to provide our customers with reliable, high-quality products at great value. By doing so, we believe we have developed a loyal customer base and achieved annual revenues and net income in excess of $86 million and $4 million, respectively, in the fiscal year ended December 31, 2022, and in excess of $115 million and $10 million, respectively, in the fiscal year ended December 31, 2023.

We are headquartered in a 286,000 sq. ft. facility of which 220,000 sq. ft. is dedicated to Massimo Motor Sports LLC (“Massimo Motor Sports”) and 66,000 sq. ft. to Massimo Marine LLC, a division of Brunswick Corporation (“Massimo Marine”). Our facility is adjacent to seven acres for boat storage in Dallas, Texas, which houses a design center, two assembly lines, our parts department, a test track, dyno and over 30 loading docks. Our products are sold directly by us, in the e-commerce marketplace, and through a network of dealerships, distributors, and chain stores. We have a significant in-store UTV retail partnership with Tractor Supply Co.

We manufacture and assemble our products in our Dallas facility and rely upon an international network of strategic global partnerships to supply us with parts and components. In 2017, we began a partnership with Linhai Yamaha Motor Co., located in Shanghai, China which allowed us to rapidly expand our product line and increase the performance of our vehicles. Further, we partnered with Kubota, Japan to enter the diesel UTV market in 2019.

Corporate History

Massimo Motor Sports was initially formed as a limited liability company in Texas on June 30, 2009. Massimo Marine was formed as a limited liability company in Texas on January 6, 2020. At the time of the respective formations, Mr. David Shan had held one hundred percent (100%) of the issued and outstanding membership interests of Massimo Motor Sports and Massimo Marine.

| 3 |

On October 10, 2022, Massimo Group, a Nevada corporation, was formed, whereby Mr. David Shan was the sole stockholder. On June 1, 2023, the Company effectuated an internal reorganization whereby (i) Asian International Securities Exchange Co., Ltd. (“AISE”) entered into two separate contribution agreements with Massimo Marine and Massimo Motor Sports, respectively, whereby AISE contributed $1,000,000 to Massimo Marine and $1,000,000 to Massimo Motor Sports in exchange for fifteen percent (15%) of membership interests in both entities, and (ii) simultaneously, on the same date, Mr. David Shan and AISE contributed their membership interests in Massimo Marine and Massimo Motor Sports, which was eighty-five percent (85%) and fifteen percent (15%) respectively, to Massimo Group in exchange for shares of common stock, par value $0.001 (“common stock”) of Massimo Group, the end result being that Mr. David Shan and AISE own eighty-five percent (85%) and fifteen percent (15%) of Massimo Group (the “Reorganization”).

Initial Public Offering

On April 1, 2024, we consummated our initial public offering (“IPO”) of 1,300,000 shares of common stock. The shares of common stock were sold at a price of $4.50 per unit, generating gross proceeds to the Company of approximately $5.85 million. We also granted the underwriters the option, exercisable for 45 days from April 1, 2024, to purchase up to an additional 195,000 shares from our Company at the IPO price less the underwriting discount and commissions to cover over-allotments.

Our common stock began trading on April 2, 2024 on The Nasdaq Capital Market (“Nasdaq”) under the symbol “MAMO.”

Impact of COVID-19

In December 2019, Coronavirus Disease (“COVID-19”) was first reported to have surfaced in Wuhan, China. COVID-19 spread rapidly to many parts of the People’s Republic of China and other parts of the world in the first half of 2020, which caused significant volatility in the domestic and international markets. The COVID-19 pandemic adversely affected many aspects of our business, including the expansion of our customer base and the introduction of new product offerings. We temporarily closed our offices and production facilities partially in March 2020, as required by relevant local authorities. Our offices reopened in April 2020 upon approval from the local governments. Due to the extended lock-down and self-quarantine policies in Dallas, Texas, we experienced a business disruption during the lock-down period from early March to June 2020. In July 2020, due to the effective containment of COVID-19 in the United States, we resumed our full operation. Then, due to the lockdown in China, where most of our suppliers are, our stock supply was disrupted from May to July 2022. Our ability to re-supply our inventory resumed in August 2022. We estimate that we lost about $1.5 million of sales as a result of this supply disruption. However, the COVID-19 pandemic did not have a material net impact on the Company’s financial positions and operating results, and our revenue reached (i) approximately $86 million for the fiscal year ended December 31, 2022, representing an increase of approximately $4 million or 5% from approximately $82 million for the fiscal year ended December 31, 2021 and (ii) approximately $115 million for the fiscal year ended December 31, 2023, representing an increase of approximately $29 million or 32.9% from approximately $86 million for the fiscal year ended December 31, 2022.

Competitive Strengths

We believe we are a leading company in the Mid-Tier Band of the Powersports Vehicles and Boats Industry. The following strengths have enabled us to achieve our growth to date, and we believe will contribute to our ongoing growth:

Diversified and Comprehensive Product Portfolio

We have a robust portfolio of products, including UTVs and ATVs, golf carts, motorcycles, scooters, Pontoon Boats, snow equipment and a line of accessories for the outdoor enthusiast including electric coolers, power stations and portable solar panels. Our products provide enthusiasts with a variety of exhilarating, stylish and powerful vehicles for year-round use on a variety of terrains. The diversity of our products reduces our exposure to changes in consumer behavior in any single category and provides us with multiple avenues for continued growth. Furthermore, certain product lines are sold in offsetting seasons, reducing the overall seasonality of our sales and lowering cash flow influx risk.

| 4 |

In addition to its appeal to consumers, our broad product portfolio provides a compelling value proposition to our dealers and distributors and allows dealers to reduce seasonality, increase operational efficiency and facilitate inventory management.

Multiple Distribution Channels

We have established multiple distribution channels for our products, including our own e-commerce platforms, leading marketplace accounts, an extensive network of independent dealers and distributors, and relationships with some of the largest retailers in the United States including Tractor Supply Co., Lowes, Walmart, Costco, Sam’s Club, Home Depot, Orscheln Farm & Home, and more. Our multiple channels for distribution and large dealer network provide multiple avenues through which we can engage and communicate with consumers.

Strategic Partnerships with Leading Suppliers of High-Quality Products

We benefit from cordial relationships with leading suppliers throughout the world. We have ongoing relationships with leading manufacturers which enable us to offer our customers reliable leading-edge high-quality products at prices which represent great value. For example, our partnership in 2017 with Linhai Yamaha Motor Co., a supplier located in Shanghai, China, has allowed us to increase our vehicles performance and expand our product lines. These relationships also enable us to cut costs while maintaining quality standards and plan shipments to control our inventory levels. Many of our manufacturing partners’ facilities are located in China, which enables them to offer lower cost manufacturing and rapid lead-times for end-market distribution in the United States.

Dedicated Customer Support Team

We have over 600 third-party motor sports service providers across the United States, more than 5,500 third-party marine boat dealers to service our Pontoon Boats and a dedicated staff of full-time employees including trained technicians to provide online and telephone support to our customers and dealers. This is a value-added service we provide, albeit we have not historically generated revenue from providing maintenance services. We carry full lines of parts, accessories and maintenance items across all models in our approximately 40,000 sq. ft. parts department and strive to fill all orders for parts and accessories within 48 hours.

State of the Art Facility

We are headquartered in a 286,000 sq. ft. facility of which 220,000 sq. ft. is dedicated to Massimo Motor Sports and 66,000 sq. ft. to Massimo Marine. Our facility is adjacent to seven acres for boat storage in Dallas, Texas, which houses a design center, two assembly lines, our parts department, a test track, dyno, and over 30 loading docks. In addition to serving as the manufacturing facility for our Pontoon Boats, the facility is equipped to quickly palletize and shrink wrap ATVs and UTVs so that most orders can be shipped to stores or distributors within three days.

Highly Experienced Management Team

Our experienced management team has demonstrated its ability to identify, create and implement new product opportunities, increase revenues, improve financial performance, and maintain a corporate culture dedicated to serving our customers and providing them with premium quality products at great value with unparalleled service.

Strategy

Our goal is to enter the Top-Tier Band of the Powersports Vehicles and Boats Industry and increase our market share through the following initiatives:

| ● | Open New Distribution Centers. A portion of the proceeds of the IPO will be used to open new distribution centers in California and the Southeast of the United States. We expect that this will enable us to reduce the time and expense associated with delivering products, replacement parts and accessories to customers, distributors and retailers located in the western and eastern parts of the United States, thereby enabling us to reduce costs to customers or improve our margins while increasing customer satisfaction. |

| 5 |

| ● | Expand our Internal Sales Capabilities. We will seek to strengthen our marketing efforts by hiring and incentivizing talented marketing professionals and sales personnel to increase our nationwide presence in the dealer, distributor and retailer communities, along with the military of the United States. | |

| ● | Invest in our Infrastructure. We believe our success greatly depends on our ability to maintain our operating efficiencies. To assist in this effort, we will use a portion of the proceeds of our IPO to expand and upgrade portions of our information technology (“IT”) systems, including our online sales and distribution networks. | |

| ● | Expand Our Product Lines. We plan to expand our product lines by introducing new models of UTVs, ATVs and recreational vehicles that cater to different customer needs and preferences. This will include models with advanced features that will include remote diagnostics capabilities and electric lines of our UTVs. We will continue to follow consumer trends and consult with our suppliers and distributors to identify new products and product upgrades we will offer to customers and distributors. Where possible, such as with our Pontoon Boats, we will upgrade our offerings and add new accessories to increase our profit margins. | |

| ● | Expand and Diversify our Supplier Base. To enable us to further diversify our product offerings, drive down our product costs and reduce our supply chain risks and improve quality control, we will seek to establish relationships with new suppliers in countries building their manufacturing capacities as certain buyers seek to reduce their dependence on Chinese manufacturers. Should appropriate opportunities arise, we will seek to vertically integrate our production capabilities by acquiring a manufacturing facility or opening our own plant. | |

| ● | Increase our Personnel. We intend to look to augment our current personnel by adding additional employees with experience to increase sales of our current products, identify and launch new products and increase our operating efficiencies. This will also include hiring experienced engineers, product designers, and sales representatives who can help the Company achieve its growth objectives. | |

| ● | Acquisitions and Consolidation: We will explore potential acquisitions and consolidation opportunities in the Powersports Vehicles and Boats Industry to expand our market share and gain access to new technologies and capabilities. |

Products

We have a diverse product line which includes industrial and recreational UTVs, recreational ATVs, golf carts, motorcycles, Pontoon Boats, juvenile products from go karts to balance bikes, snow equipment and a line of accessories including EV chargers, electric coolers, power stations and portable solar panels. The majority of our products are imported directly from our manufacturer network to our facility in Dallas where they are assembled, accessorized and inspected before shipment to a distributor or direct to the customer, with the exception of our Pontoon Boats, which are wholly manufactured at our Dallas facility. With the exception of our products designed for industry usage, our products are designed to serve and market towards recreational users.

We constantly monitor the consumer market and consult with suppliers to determine what new products we can offer customers. In determining whether to commence distributing a product, among other things, we consider the quality and reliability of the product, the value we believe we can deliver to the consumer based on the price to be paid to the supplier and the reliability of the supplier.

ATV and UTV

An ATV is an all-terrain vehicle—commonly called a four-wheeler or quad—designed for a single rider and typically used for recreation. A UTV is a utility terrain vehicle used for work or recreation. Designed with a cabin for two to four riders, it is often called an SxS or side-by-side.

We currently distribute four models of our MSA line of ATVs with base prices ranging from approximately $2,800 to $9,000, and four lines of UTVs with various models including golf carts, at prices ranging from $6,000 to $22,000. We maintain a full line of accessories and replacement parts for all of our ATVs and UTVs. In the fiscal years ended December 31, 2023 and 2022, the majority of our ATV and UTV sales were gas-powered models. Nevertheless, we offer electric versions of several our UTVs, particularly electric golf carts.

| 6 |

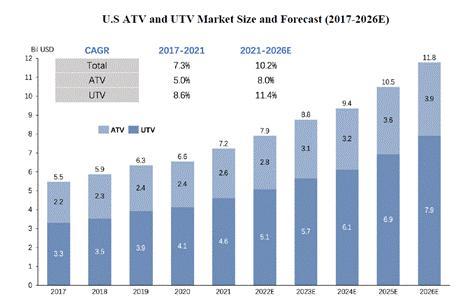

According to Frost & Sullivan, the market size of the ATV industry in the United States in terms of revenue grew at a compound annual growth rate (“CAGR”) of 5.0% from $2.2 billion in 2017 to $2.6 billion in 2021 and is expected to grow further to $3.9 billion in 2026 at a CAGR of 8.0%. The market size of the UTV industry in the United States in terms of revenue grew at a CAGR of 8.6% from $3.3 billion in 2017 to $4.6 billion in 2021 and is expected to grow further to $7.9 billion in 2026 at a CAGR of 11.4 %. ATV market growth rate is expected to be slower compared to UTV market growth partially because of drivers’ preference for a more comfortable and safer driving experience. Of the ATV and UTV vehicles sold in 2021, 63.2% were installed with gasoline propulsion and 34.1% with diesel propulsion with electric propulsion taking up the balance of 2.7% in 2021. It is expected that the percentage of electric propulsion vehicles sold will increase with diesel engines decreasing. However, gasoline propulsion is expected to be the consumers’ choice for the foreseeable future.

According to Frost & Sullivan, in 2021, 45.2% of the ATV and UTV vehicles were used for outdoor sports and recreation activities, 30.1% were used for agricultural activities and 24.7% were used for military purposes. There is an increase in demand for ATVs and UTVs for military activities such as driving on difficult terrains, transporting troops, and others. ATVs and UTVs are expected to experience substantial growth in the military segment, owing to superior mobility provided for tactical missions. Additionally, features such as high maneuverability, flexibility, and superior navigational aids providing instant directions for vehicle operators will help foster further market growth.

U.S ATV and UTV Market Size and Forecast (2017 – 2026E) from Frost & Sullivan

| 7 |

Massimo MSA 450F ATV

Massimo T-Boss 550 UTV

| 8 |

Massimo Warrior 1000

Recreational Pontoon Boats

Pontoon Boats are flat-deck boats propelled by an outboard motor with two or three floating aluminum tubes supporting the deck. They are rectangular in shape, making them generally unsuitable for uneven or rough water and are popular in lakes where they are used for entertainment, fishing, sunbathing and other leisurely activities. Pontoon Boats have a large deck surface, which allows for more seats, luxury, comfort, expanded storage space, and increased capacity for a variety of activities depending on customers’ preferences.

We entered the Pontoon Boats market in 2020 when we successfully launched our first series of Pontoon Boats. By the end of 2023, our sales of Pontoon Boats placed us in approximately the top 15 pontoon manufacturers in Texas by volume. From inception, we have manufactured our Pontoon Boats in our Dallas facility. In terms of our product offerings, we currently offer both gas-powered and electric-powered boats and maintain a complete line of replacement parts and a broad range of accessories. We also intend to implement a “build a boat” program, where customers can select from a variety of models and add accessories.

The Pontoon Boats market has demonstrated remarkable growth since 2008, when the financial crisis resulted in declines across the boating industry. According to data from Statistical Surveys Inc. (“SSI”), Pontoon Boats, second to personal watercraft, have been a leading segment in the recreational boating industry over the last decade. Pontoon Boats made up 22% of total marine units registered in 2021, outperforming others in the main powerboat segment, SSI data reveals that 2021 pontoon registrations were some of the highest seen over the past 10 years. This includes a 16% increase from 2019 (57,287) to 2021 (66,280) when other recreational boat segments saw declines.

According to Frost & Sullivan, the size of the Pontoon Boat market in the United States in terms of revenue grew at a CAGR of 10.7% from $2.2 billion in 2017 to $3.3 billion in 2021 and is expected to grow further to $6.6 billion in 2026 at a CAGR of 14.9 %.

| 9 |

U.S Pontoon Boats Market Size and Forecast (2017 – 2026E) from Frost & Sullivan

Massimo Pontoon Boat

| 10 |

Motorcycles, GO Karts, Youth Market and Accessories

Along with our larger vehicles, we offer a range of gas and electric powered wheeled vehicles for the sports enthusiast. These include lines of minibikes and motorcycles, at prices ranging from $700 to $8,000, including our recently introduced E-Spider 72V Trike, go karts for both children and adults, and a line of go karts, mini-bikes and electric balance bikes especially designed for the juvenile market. Each of these models is designed to appeal to a specific segment within the recreational powersports market, from youth models to electric vehicle enthusiasts.

|

|

|

Massimo Go Kart, Mini 125 and Motorcycles

We offer a wide range of accessories for all of our vehicles including replacement parts and supplies, along with seasonal equipment such as snowplows and enclosures specially designed for our UTVs. Our outdoor accessories include EV chargers, portable solar panels, electric coolers and power stations. All of these products are now available for sale.

Marketing

Our target customers are the growing portion of the United States population participating in outdoor recreational activities, farmers and other industrial users that can benefit from the utility of an ATV or UTV. According to Frost & Sullivan, the number of people in the United States participating in outdoor recreational activities increased from 143 million in 2017 to 163 million people in 2021. This increase is attributed to several factors, including growth in rural areas as people leave the cities and the ability of consumers to work from home with a more flexible schedule allowing more time for outdoor weekend activities. These factors, coupled with new product lines and trendy features helped boost the repurchase rate for older consumers and increase the purchasing rate among new customers.

Major market drivers for ATVs are the greater affordability and ease of operation compared to larger more cumbersome vehicles. ATVs are typically less expensive than UTVs. Further, ATVs are easy to operate, especially if you have driven a motorcycle or snowmobile before.

For UTVs, major market drivers include excellent rideability and higher safety level, more options for customization, more storage room and the ability to hold more passengers. A UTV is controlled by a steering wheel as opposed to handlebars making it much easier to drive and allowing for familiarity for those who have driven a car or truck. Customers are more concerned about safety will likely be more comfortable in a UTV than an ATV. Due to their design, UTVs are more stable and easier to control. They also have additional safety measures not found on ATVs, such as seat belts and roll cages. Customers can now add lift kits, new suspensions, lighting systems, cabin heaters, stereo systems and much more to their UTVs than was previously available. Lastly, people who need a more utilitarian work vehicle tend to choose a UTV. In addition to higher payload capacities, UTVs usually have more storage room to haul around necessary equipment.

| 11 |

Major drivers of the Pontoon Boats industry in the United States include recent increases in disposable income coupled with the rise in watercraft sports activities across multiple states. Boating participation across the United States is growing as a result of escalating customer spending for motorized water sports. Pontoon Boats in particular are benefitting from the consumer preference for the comfort flat decks provide as compared to typical V-hull boats of the same length because of the increased open deck area. The larger decks make it easier to host a family outing, party, or fishing outing. Pontoon Boats also provide a more stable steady ride than a narrow v-hulled craft of similar size. Recent technological improvements, including the introduction of two- and four-stroke engines with direct injection technology, which provide improved fuel economy, lower emissions, and more power, is increasing demand for larger more sophisticated Pontoon Boats.

Multiple Distribution Channels

Our products are sold directly by us, in the e-commerce marketplace and through a network of dealerships, distributors, and retailers.

To reach our target customer, we have established multiple distribution channels for our products, including our own on-line sites, multiple popular e-commerce sites, an extensive network of independent dealers and distributors and relationships with some of the largest retailers in the United States including Tractor Supply Co., Lowes, Walmart, Costco, Sam’s Club, Home Depot, Orscheln Farm & Home, and more. We have a significant UTV retail partnership with Tractor Supply Co. through which we generated approximately $47 million and $10 million in revenue in the fiscal years ended December 31, 2023 and 2022, respectively. Our multiple channels for distribution and large dealer network provide multiple avenues through which we can engage and communicate with consumers.

We have an in-house marketing staff which directs our ad campaigns and social media marketing as well as campaigns targeted at expanding our distributor network. Our marketing personnel work closely with our dealers, distributors and retailers organizing in-store and co-branded marketing programs. Since inception we have sought to develop recognition for our brand name among both consumers and distributors through a variety of advertising campaigns, including paid advertisements, landing page campaigns, co-branded campaigns, displays on YouTube and other forms of social media and industry reviews. Part of our strategy has been to seek out quality suppliers, some with recognized brands of their own, who can provide reliable, high-quality vehicles with the latest features at good value.

Generally, our sales directly to independent dealerships account for the majority of our sales during each fiscal year. Once we establish partnerships with independent dealerships, we then sell our products directly to the dealers. The dealers are strategically located throughout the United States. Once they purchase our product, in the most typical situation, they sell the products out of their brick-and-mortar location to end users. The dealerships become our long-term partners and they work with us to promote our brand across their own networks and channels. Presently, we have established partnerships with dealerships who carry our products in approximately 2,800 locations across the United States and with retail stores such as Tractor Supply Co., Lowes and Home Depot. Over the past several years, we have been actively focusing our efforts on expanding our direct dealer network.

Our partnerships with dealers are critical to expanding our brand awareness in new markets geographically. We are beginning to make inroads into the Canadian market and have initiated a relationship with an independent distributor in Ontario, Canada.

Most dealers and distributors distribute multiple products within our portfolio: ATVs and UTVs, Pontoon Boats, motorcycles, and other smaller vehicles as well as parts and accessories. Unlike our competitors, which market their products principally through their affiliated dealers, we also sell our products through well-known retailers such as Lowes, Tractor Supply Co., and other farm and industrial equipment dealers, boat and marine dealers and lawn and garden dealers.

Before entering into a formal partnership with a dealer, we conduct thorough background and credit checks to ensure the prospective partnership is beneficial for us and our customers. To incentive our partners to promote our brands, we implement performance-based incentive programs, which includes the possibility of obtaining additional benefits, such as promotional pricing.

| 12 |

Dedicated Customer Support Team

Our marketing effort does not stop when the customer purchases one of our products. After sale activities intended to maintain a positive relationship include delivery confirmation calls, review requests, warranty registration cards and reminders for scheduled maintenance and maintenance items. We have a dedicated staff of full-time employees including trained technicians to provide online and telephone support to our customers and dealers. We carry full line of parts, accessories and maintenance items across all models in our approximately 40,000 sq. ft. parts facility and strive to fill all parts orders within 48 hours. We provide extensive parts diagrams and service manuals and our trained technicians are available to both distributors and individual customers to assist with diagnosing and solving any problem that may come up.

Product Warranties

We provide limited warranty coverage for defects in materials and workmanship in our ATVs, UTVs and golf carts for a period of one year and Go-Kart and motorcycles for a period of one year. The warranty is non-transferable for the period of coverage if the vehicle is resold. Our limited warranty is void if the vehicle is used as a rental, racing or any modifications are made to the product. Although we employ quality control procedures, a product is sometimes distributed which needs repair or replacement. Historically, product recalls have not had a material effect on our business.

We have entered into an exclusive arrangement with Mercury Marine, a division of Brunswick corporation (“Mercury Marine” or “Mercury”), so all of our Pontoon Boats come equipped with a Mercury outboard engine and parts. Our Mercury Marine warranty and service program gives our customers access to 5,500 approved service centers in the United States. Like most luxury brands, we offer a ten-year warranty on the deck of the Pontoon Boats and a lifetime warranty on aluminum on many materials and workmanship and a three-year warranty for defects in critical parts including the structure, pontoons, fencing, channels, motor mounts and rotomold seat frames caused by poor workmanship. Because we are Mercury exclusive, our customers receive a three-year warranty offered by Mercury Marine on everything supplied by Mercury, which includes digital control, hydraulic steering, throttle, steering system, engine, cables, and electrical. Our warranty, along with the Mercury Marine are transferable during the original warranty period and are in line with top level original equipment manufacturers.

Financing Arrangements

We have arrangements with Northpoint Commercial Finance and Automotive Finance Corporation to provide floor plan financing for our dealers and distributors. Substantially all of our products, including ATVs, UTVs, golf carts and Pontoon Boats are financed under arrangements in which we are paid within a few days of a product’s shipment. To incentivize our dealers and distributors, we bear the first three month of interest, so they pay no interest if our products are sold within 90 days of receipt.

We do not directly provide finance for the purchase of our products, including ATVs, UTVs, golf carts, or Pontoon Boats. We do, however, have programs where we introduce our customers to lenders, such as Northpoint Commercial Finance and Automotive Finance Corporation, who are willing to provide financing for our UTVs, ATVs, golf carts and Pontoon Boats customer.

We work with several financing companies to offer competitive loans for prime and subprime buyers. Our partners can get prospective buyers prequalified with no impact to credit scores via quick online applications. We do provide promotional support with these partners to offer prime loan rates as low as 2.99%. We also sell select models direct which are paid in full prior to pick up or shipment.

Manufacturing and Sourcing

We manufacture our Pontoon Boats in our 286,000 sq. ft. facility of which 220,000 sq. ft. is dedicated to Massimo Motor Sports and 66,000 sq. ft. to Massimo Marine. Our facility is adjacent to a seven-acre storage area for boats in Dallas, Texas. This space houses a design center, two assembly lines, training rooms, an approximately 40,000 square foot parts department, and over thirty loading docks. Structural components and other materials are sourced locally from a variety of suppliers and electrical components and engines are obtained through an exclusive arrangement with Mercury Marine. We have entered into an exclusive arrangement with Mercury Marine, so all of our Pontoon Boats come equipped with a Mercury Marine outboard engine and parts.

Apart from the brand name items we offer to our customers, such as the outboard motor, depth finder, radio and stereo system, the materials and components used in our pontoons are generally available from multiple suppliers. If any supplier was unable to fulfill our needs, alternate sources are available. More than 60% of the value of our boats are USA sourced, thus limiting our risk for overseas interruption.

| 13 |

Substantially all products other than our boats, in particular our ATVs and UTVs, are sourced from select global manufacturers with which we have ongoing relationships. Our in-house sourcing and logistics personnel reach out to possible vendors, suppliers and raw material providers, and review their products and background to ensure that their products will meet our standards and that they can meet our needs on a timely basis. We review market trends with our major suppliers to coordinate manufacturing volumes and delivery dates and determine whether there is an opportunity to upgrade or accessorize a product to increase its customer appeal, the sales price and our margins. We currently have ongoing supply agreements in place with approximately 30 suppliers, two of which are located in the United States and the majority of which are in China.

In 2017, we entered into a partnership for engines with Linhai Yamaha Motor Co. which enabled us to increase the performance of our vehicles and offer new products. An agreement reached in 2019 with Kubota Japan enabled us to obtain a reliable diesel engine with which to enter the diesel UTV market. Currently, our top three suppliers are Linhai Powersports USA Corporation (“Linhai Powersports”), Huzhou Meiwen Textile Imp. & Exp. Co., Ltd. and Linhai Co., Ltd., all of which are located in China and supplied us with approximately 68% and 66% (by cost) of our products in the fiscal years ended December 31, 2023 and 2022, respectively.

We believe that our relationship with reliable manufacturing partners in China has been one of the factors in our growth as it provided a steady source of quality products at costs which allowed us to deliver value to the ultimate consumer. Our business was affected by the supply chain disruptions caused by the COVID-19 pandemic. For example, due to the city lockdown in China where most of our suppliers are, our stock supply was disrupted from May to July 2022. Our ability to re-supply our inventory resumed in August 2022, but we estimate that we lost about $1.5 million of sales as a result of this supply disruption. In addition, due to the supply chain crisis in 2021 and 2022, the cost of our oversea freights increased significantly, double or even triple times from 2020 and 2019. To offset these price increases, we increased the selling prices for the majority of our products. Since 2023, the cost of overseas freights has decreased substantially, though it still exceeds the cost prior to the supply chain crises.

We do not currently expect to suspend our production, sales or maintenance of any of our products or experience higher costs due to constrained capacity or materially increased commodity prices or challenges sourcing materials. We believe our supply chain can respond to expected consumer demand and we will be able to continue to supply products to our customers at reasonable prices. We have not experienced, and do not currently expect to experience, surges or declines in consumer demand for which we are unable to adjust our supply. We have not been affected by export restrictions or sanctions. Nevertheless, we are focusing on broadening our base of suppliers to reduce our dependence on a limited number of suppliers for the majority of our products, to minimize the risk of relying upon Chinese manufacturers, including the risk of fluctuations in the exchange rate between the U.S. Dollar and the legal currency of China (“Chinese RMB”).

Research and Development

In addition to our own internal research and development (“R&D”), we work closely with our suppliers to design innovative, high-performance products to build strong customer loyalty and sustain our reputation as a leading-edge manufacturer. Our suppliers will bear the expense of upfront engineering and design work, recouping the expense out of the amount charged for their products. We believe our successful development efforts enabled us to grow our annual sales of powersports vehicles and pontoon boats by 32.4% and 37.9% respectively in the fiscal year ended December 31, 2023 compared to the fiscal year ended December 31, 2022.

Information Technology

Our in-house design and logistics personnel rely heavily on IT systems to explore new product offerings, to ensure a smooth workflow, and production quality and control. Our relationships with our customers and distributors rely upon the latest technologies to maintain contact and foster a positive collaborative working relationship. As we grow, we will continue to rely heavily upon IT systems to maintain our operating efficiency.

| 14 |

Intellectual Property

We currently hold eight issued patents in the United States that protect certain aspects of our products, design and technologies. Each of our patents has a term of 14 years with the exception of one which has 15 years. As part of our ongoing efforts to prevent infringements on our intellectual property rights and to keep abreast of critical technology developments by our competitors, we closely monitor patent applications in the United States and China. The following is a summary of our patent portfolio:

| No. | Name of Patents | Patent No. | Grant Date | Expiration Date | ||||

| 1 | Motorbike design patent | US D643783S | August 23, 2011 | August 23, 2025 | ||||

| 2 | Motorbike design patent | US D645791S | September 27, 2011 | September 27, 2025 | ||||

| 3 | ATV design patent | D775563 | January 3, 2017 | January 3, 2031 | ||||

| 4 | ATV design patent | D701143 | March 18, 2014 | March 18, 2028 | ||||

| 5a | Design patents acquired | D691924 | October 22, 2013 | October 22, 2027 | ||||

| 5b | Design patents acquired | D788653 | June 6, 2017 | June 6, 2032 | ||||

| 5c | Design patents acquired | D682750 | May 21, 2013 | May 21, 2027 | ||||

| 5d | Design patents acquired | D709015 | July 15, 2014 | July 15, 2028 |

We also rely upon a combination of registered and unregistered trademarks, service marks, and trade names to strengthen our position as a branded motor sports company with increasing brand recognition. We hold various registered trademarks in the United States with respect to our brands and product lines. We carefully review the brands and trademarks being used by our competitors in the United States and other jurisdictions before using a new trademark and in determining the jurisdictions in which to register any new trademark used by us. As we continue to enter new product categories and develop new models of our current products, we plan to develop and register new trademarks to differentiate such products.

We intend on entering into confidentiality agreements with our suppliers, employees and consultants who may have access to our proprietary information. These agreements will provide that all inventions, ideas, discoveries, improvements, and copyrightable material made or conceived by the individual arising out of the employment or consulting relationship and all confidential information developed or made known to the individual during the term of the relationship are our exclusive property. See “Risk Factors—Risks Relating to Our Business, Strategy, and Industry—We have not made use of confidentiality agreements in the past and, although we intend to rely on such agreements in future dealings with suppliers, employees, consultants, and other parties, the prior lack or the breach of such agreements could adversely affect our business and results of operations.”

Employees

As of March 28, 2024, we had approximately 126 employees, of which approximately 15 were in management and administration, 22 were sales and service personnel, 81 were in manufacturing, 3 were in quality control and 5 were in R&D. None of our employees are represented by a union, and our relationship with our employees is satisfactory.

Competition

ATV and UTV Markets

The ATV and UTV markets in the United States are very concentrated with a limited number of large well capitalized manufacturers representing more than 80% of the market. The major players in the market include Polaris, Bombardier Recreational Products (BRP), Arctic Cat, Honda and Yamaha. We seek to differentiate ourselves by offering products with the latest design features and options and by providing superior aftermarket support to our customers and distributors.

| 15 |

Pontoon Boats Market

The United States Pontoon Boats market is fragmented and there is a significant number of vendors which offer Pontoon Boats across the country. Competition among vendors is based on product offerings and pricing, putting a premium on offering up to date models with high-end accessories.

Seasonality

The ATV and UTV markets do experience some seasonality, but we have developed our product lines to appeal to seasonal customers to minimize any disruptions. In the spring and summer months, we focus on outdoor campaigns tailored to spring cleaning, planting, fishing and family outdoor activities. We promote our complimentary lines of outdoor accessories including electric coolers, outdoor power stations and solar panels. In the fall and winter months, we have a heavy push for hunting season in the United States, and we promote our winter accessories including snow blowers, snowplows and enclosures.

With Pontoon Boats, we are both a distributor and a retailer, which gives us great seasonal protection. Dealers order higher volumes between October to March while retail orders are higher April to September. This gives us an overall balance. While winter months are always slower than summer months, it allows us to maintain cash flow during the winter season.

Product Liability

Product liability claims are made against us from time to time. We do not believe that the outcome of any pending product liability litigation will have a material adverse effect on our operations. However, no assurance can be given as to whether any material product liability claims against us will be made in the future.

Our commercial general liability insurance provides us with coverages of $2,000,000 general aggregate limit and $2,000,000 products-completed operations aggregate limit, with a minimal amount of deductible per claim. We also have umbrella liability insurance with coverage of $7,000,000 aggregate on top of general liability insurance and workers’ compensation insurance. We believe our current coverage is adequate for our existing business and will continue to evaluate the coverages in the future in line with our expanding sales and product breadth.

Insurance

We carry various insurance coverage policies to protect against certain risks consistent with the exposures associated with the nature of our operations. The most significant insurance policies that we carry include:

| ● | commercial general liability insurance for bodily injury and property damage resulting from operations and our products; | |

| ● | property insurance covering the replacement value of all real and personal property damage, including damages arising from earthquake, flood damage and business interruption; | |

| ● | cargo insurance to protect against loss or damage to goods while in transit; | |

| ● | workers’ compensation coverage in the United States to required statutory limits; |

| 16 |

| ● | directors and officers insurance; and | |

| ● | cyber insurance to mitigate risk exposure by offsetting recovery costs following a cyber-related security breach or similar event. |

All policies are subject to certain deductibles, limits or sub-limits and policy terms and conditions.

Inflation

While our business has been impacted by rising inflation, our management does not believe that it has had a material negative impact on our business and results of operations. In recent years, our China-based suppliers have increased the cost of their products as a result of inflation. However, these increases have thus far been offset by the exchange rate fluctuation of the Chinese RMB, which has resulted in there being no material change to our costs. Although we are looking to broaden our supplier base outside of China to reduce our dependence upon Chinese-based suppliers in general, there is no assurance we will be able to broaden our supplier base outside of China or that increases in in our cost of goods will continue to be offset by exchange rate fluctuations.

In addition, to reduce the impact of inflation, we have worked with our suppliers to enter into letters of credit pursuant to which we can make purchases and incur interest and fees at a lower rate than had we made the purchases using our existing bank loan.

Regulatory Issues

We are subject to extensive laws and regulations at many steps in the design, importing, production, marketing and distribution of our products. In addition to the laws and regulations applicable to any business, there are certain requirements applicable only to powersports vehicles, Pontoon Boats, recreational products and outdoor accessories such as those we distribute. These regulations include standards related to safety, construction rules, sound and gaseous emissions, and the sale and marketing of products, and have generally become stricter in recent years.

We endeavor to take appropriate measures to provide a safe, clean working environment for our employees. We strive to ensure and work with our manufacturing partners to ensure that the products we offer comply with current regulations and with more stringent regulations anticipated to become effective in the foreseeable future. Such measures include the development of new engines and vehicle designs, independently and with our supplier partners, as well as the development of new energy-efficiency related technologies. The failure to comply with applicable laws, rules and regulations regarding employees and product safety, health, environmental and noise pollution could cause us to incur fines or penalties and our compliance programs require significant time and expense.

Distributor & Dealer Regulation

Our contractual relationships with distributors and dealerships throughout the country are subject to extensive regulation at the local, state and national level. Each state’s Department of Motor Vehicles sets rules concerning pricing, competition, warranty claims and other aspects of the vehicular dealership business. These laws are further supported by state-wide “lemon laws.” Lemon laws provide remedies for consumers who seek to be compensated for defective vehicles that fall short of accepted standards of quality and performance. The distribution of our vehicles is also regulated by state-wide licensing regimes, federal agency regulation and federal common law pertaining to the Uniform Commercial Code. We have taken efforts to comply with these regulations governing our relationships with our distributors and dealers by vetting our distributors and dealers to ensure their compliance with regulations statewide. The licenses and required compliance to do business in each state can become expensive, and we may allow our licenses to lapse if we ascertain that the costs outweigh the benefits. For example, in 2016, we allowed our Illinois license to expire and then in 2019, we reapplied for our Illinois license once we were confident that we would continue to generate revenue in the state to mitigate the costs.

| 17 |

Safety Regulation

Our products are subject to extensive laws, rules and regulations relating to product safety promulgated by the federal and state governments or regulatory authorities of the United States and the federal and provincial provinces in Canada. These requirements pertain to the design, production, distribution and use of our products. We are a member of several industry and trade associations in Canada, the United States, and other countries whose mandate is to promote safety in the manufacture and use of powersports products. Some of those trade associations promulgate voluntary industry product safety standards with which we and our suppliers comply. While we strive to meet the safety standards set by state and federal authorities, we have been subject to several inquiries by the U.S. Consumer Product Protection Commission regarding defective products. We have also been subject to penalties including a Stop Sale order on one of our electric balance bikes.

Use Regulation

In Canada, the United States and other countries, laws, rules and regulations have been promulgated or are under consideration relating to the use of powersports vehicles and boats. Some countries, provinces, states, municipalities and local regulatory bodies have adopted, or are considering the adoption of, legislation and local ordinances that restrict the use of snowmobiles, ATVs, UTV, Pontoon Boats and outboard engines to specified hours and locations. The use of many of these products has been restricted in some national parks and federal lands in Canada, the United States and other countries. In some instances, this restriction has consisted of a ban on the recreational use of these vehicles in specific locations.

Emissions Regulation

Our products are subject to sound and gaseous emissions laws, rules and regulations promulgated by the governments and regulatory authorities of Canada (Environment and Climate Change Canada), the United States (Environmental Protection Agency), individual American states (such as the California Air Resources Board) and other jurisdictions. Such laws, rules and regulations may require the development of new engines and vehicle designs, as well as the development of new energy-efficient technologies. The failure to comply with the laws, rules and regulations regarding product safety, health, environmental and noise pollution and other issues could result in fines or penalties and our efforts to comply with such regulations require significant time and expense.

Item 1A. Risk Factors.

Any investment in our securities involves a high degree of risk. You should carefully consider the risks described below, which we believe represent certain of the material risks to our business, together with the information contained elsewhere in this Report, before you decide to invest in our shares of common stock. Please note that the risks highlighted here are not the only ones that we may face. For example, additional risks presently unknown to us or that we currently consider immaterial or unlikely to occur could also impair our operations. If any of the following events occur or any additional risks presently unknown to us actually occur, our business, financial condition and operating results may be materially adversely affected. In that event, the trading price of our securities could decline and you could lose all or part of your investment.

Summary of Significant Risks Affecting Our Company

Our significant risks may be summarized as follows:

| ● | We have a limited operating history on which to judge our performance and assess our prospects for future success. |

| ● | Resources devoted to product innovation may not yield new products that achieve commercial success. |

| ● | We rely on independent dealers and distributors to manage the retail distribution of many of our products. |

| ● | We rely on third parties to manufacture many of the products we sell. |

| 18 |

| ● | The majority of the products we purchase are manufactured by in China and their operations are subject to risks associated with business operations in China. Any disruption of these manufacturers to supply us with appropriately priced products on a timely basis could have a material adverse effect on our business. |

| ● | Our management team has no experience operating a company with publicly traded shares. |

| ● | Economic conditions that impact consumer spending may have a material adverse effect on our business, and our partners’ business. |

| ● | We currently maintain all our cash and cash equivalents with three financial institutions. |

| ● | We face intense competition in all product lines, including from some competitors that have greater financial and marketing resources. |

| ● | Any decline in the social acceptability of our products or any increased restrictions on the access or the use of the Company’s products in certain locations could materially adversely affect our business, results operations, or financial condition. |

| ● | Our future expansion plans are subject to uncertainties and risks, and distribution centers we intend to open may not result in increased sales or efficiencies. |

| ● | Our limited investment in R&D of new products may adversely affect our ability to enhance existing products and develop and market new products. |

| ● | The inability of our dealers and distributors to secure adequate access to capital could materially adversely affect our business. |

| ● | We depend upon the successful management of inventory levels, both ours and that of our dealers |

| ● | There is no assurance there will not be disruptions to trade between China and the United States. |

| ● | We may not be able to successfully maintain our strategy of relying upon offshore manufacturers. |

| ● | Supply problems, termination or interruption of supply arrangements or increases in the cost of products could have a material adverse effect on our business. |

| ● | The high cost of delivering our recreational boats may limit the geographic market for these products. |

| ● | Higher fuel costs can materially adversely affect our business. |

| ● | Changes in the credit markets could decrease the ability of consumers to purchase our products and have a material adverse effect on our business. |

| ● | We may require additional capital which may not be available. |

| ● | Our business depends on the continued contributions made by Mr. Shan, our founder, Chairman and Chief Executive Officer. |

| ● | Our business depends on the efforts of our management, and our business may be severely disrupted if we lose their services. |

| ● | If we fail to develop and protect our brand names and reputation, we may not attract and retain new distributors and dealers, or customers. |

| ● | We may be unable to protect our intellectual property or may incur substantial costs as a result of litigation or other proceedings relating to our intellectual property. |

| ● | Significant product repair and/or replacement due to product warranty claims or product recalls could have a material adverse impact on our business. |

| 19 |

| ● | The failure of our IT systems or a security breach involving consumer or employee personal data could have a materially adverse effect on our business. |

| ● | Retail sales of our new products may be materially adversely affected by declining prices for used versions of our products or the supply of new products by competitors in excess of demand. |

| ● | We are subject to laws, rules and regulations regarding product safety, health, environmental and noise pollution, and other issues. |

| ● | If product liability lawsuits are brought against us, we may incur substantial liabilities. |

| ● | Our insurance may not be sufficient. |

| ● | We have been in the past, and may be, in the future subject to several litigation proceedings relating to defective products that have caused property damage, physical injury, and death. |

| ● | Our business requires us to pay licensing fees for each state that we operate in. We may not be able to justify the cost of compliance in a particular state or locality thus necessitating that we allow our license to expire. |

| ● | We have not made use of confidentiality agreements in the past and, although we intend to rely on such agreements in future dealings with suppliers, employees, consultants, and other parties, the prior lack or the breach of such agreements could adversely affect our business and results of operations. |

| ● | Our business could be materially harmed by epidemics, pandemics such as COVID-19 and other public health emergencies. |

| ● | Natural disasters, unusually adverse weather, pandemic outbreaks, boycotts, and geo-political events could materially adversely affect our business. |

| ● | Our ability, or lack thereof, to attract, recruit, and maintain talented sales representatives may adversely affect our business and our plans to expand our market. |

| ● | Our ability, or lack thereof, to establish strategic partnerships and expand our distribution channels may adversely affect our business and our plans. |

| ● | Policies of the United States granting farmers incentives may cease. |

| ● | There is no existing market for our securities, and we do not know if one will develop. |

| ● | The market price of our common stock is likely to be highly volatile, and you could lose all or part of your investment. |

| ● | We have no current plans to pay cash dividends on our common stock for the foreseeable future. |

| ● | Our founder and principal shareholder have substantial influence over our Company. |

| ● | We will incur significant increased costs as a result of operating as a public company and will be required to devote substantial time to compliance initiatives. |

| ● | Changes to estimates related to our property, fixtures and equipment or operating results that are lower than our current estimates may cause us to incur impairment charges on certain long-lived assets, which may adversely affect our results of operations. |

| ● | As an “emerging growth company” under applicable law, we are subject to lessened disclosure requirements, which could leave our stockholders with less information or fewer rights available to stockholders of more mature companies. |

| 20 |

| ● | If securities or industry analysts do not publish or cease publishing research or reports about us, our business, or our market, or if they change their recommendations regarding our common stock adversely, the price of our common stock and trading volume could decline. |

| ● | Anti-takeover provisions in our Articles of Incorporation and Bylaws and Nevada law could discourage, delay, or prevent a change in control of our company and may affect the trading price of our common stock. |

| ● | Failure to establish and maintain effective internal controls in accordance with Section 404 of the Sarbanes-Oxley Act could have a material adverse effect on our business and stock price. |

| ● | Our Bylaws provide that the Second Judicial District Court of Washoe County of the State of Nevada is the sole and exclusive forum for certain stockholder litigation matters. |

Risks Relating to Our Business, Strategy, and Industry

We have a limited operating history on which to judge our performance and assess our prospects for future success.

In 2017, we entered the market and began distributing recreational vehicles, including UTVs and ATVs. In 2020, we began to distribute pontoon and tritoon boats and, more recently, we began to distribute accessories. Consequently, we have a limited operating history on which to evaluate our prospects and those of our products. We may fail to continue our growth. You should not consider our historical growth and expansion of our business as indicative of our ability to grow in the future.

Economic conditions that impact consumer spending may have a material adverse effect on our business, results of operations or financial condition.

Our products compete with a variety of other recreational products and activities for consumers’ discretionary income and leisure time. Our results of operations are therefore sensitive to changes in overall economic conditions, primarily in North America, that impact consumer spending and particularly discretionary spending. Weakening of, and fluctuations in, economic conditions affecting disposable consumer income such as personal income levels, the availability of consumer credit, employment levels, consumer confidence, business conditions, changes in housing market conditions, capital markets, tax rates, savings rates, interest rates, fuel and energy costs, as well as the impacts of natural disasters, extreme weather conditions, acts of terrorism or other similar events could reduce consumer spending generally or discretionary spending in particular. Such reductions could materially adversely affect our business, results of operations or financial condition.

Worldwide economic conditions continue to be challenging as economies recover from the effects of the COVID-19 global pandemic. Demand for our products has been significantly influenced by weak economic conditions and increased market volatility worldwide. Any deterioration in general economic conditions that further diminishes consumer confidence or discretionary income may further reduce our sales and materially adversely affect our business, results of operations or financial condition. We cannot predict the timing or strength of economic recovery, either worldwide or in the specific markets where we compete.

We currently maintain all our cash and cash equivalents with three financial institutions, and, therefore, our cash and cash equivalents could be adversely affected if the financial institutions in which we hold our cash and cash equivalents fails.

We currently maintain all our cash and cash equivalents with three financial institutions. At the current time, our cash balance with such financial institutions is in excess of the Federal Deposit Insurance Corporation insurance (“FDIC Insurance”) limit and, therefore, we may not be able to recover a substantial portion of these cash and cash equivalents, in the event of the failure of any such financial institutions. As a result of the recent inability of certain businesses with accounts at Silicon Valley Bank to gain access to their deposits and the greater focus on the concerns of potential failures of other financial institutions in the future, we are currently diversifying our investments by transferring cash not required for immediate use into short-term treasury bills and also considering transferring a portion of our cash and cash equivalents to other financial institutions in order to reduce the risks associated with maintaining all of our cash and cash equivalents at three financial institutions. Additionally, we are working with our current financial institutions to increase the amount of funds held there that are insured by FDIC Insurance. Notwithstanding these efforts, the failure of one or more of the financial institutions in which our cash and cash equivalents are held, the resulting inability for us to obtain the return of our funds from any of those financial institutions, or any other adverse condition suffered by any of those financial institutions, could impact access to our invested cash or cash equivalents and could adversely impact our operating liquidity and financial performance.

| 21 |

We face intense competition in all product lines, including from some competitors that have greater financial and marketing resources. Failure to compete effectively against competitors could materially adversely impact our business, results of operations or financial condition.

The Powersports Vehicles and Boats Industry is highly competitive. Competition in such markets is based upon several factors, including price, quality, reliability, styling, product features and warranties. At the dealer level, competition is based on several factors including sales and marketing support programs (such as financing joint advertising programs and cooperative advertising). Certain of our competitors are more diversified and have financial and marketing resources which are substantially greater than ours, which allow these competitors to invest more heavily in intellectual property, product development, and sales and marketing support. If we are not able to compete with new products, product features or models comparable to or superior to those of our competitors, or attract new dealers, our business, results of operations or financial condition could be materially adversely affected.

We are subject to competitive pricing. Such pricing pressure may limit our ability to maintain prices or to increase prices for our products in response to raw material, component and other cost increases and so negatively affect our profit margins.

Any decline in the social acceptability of our products or any increased restrictions on the access or the use of the Company’s products in certain locations could materially adversely affect our business, results operations, or financial condition.

Demand for our products depends in part on their social acceptability. Public concerns about the environmental impact of our products or their perceived safety could result in diminished social acceptance. Circumstances outside the Company’s control, such as social actions to reduce the use of fossil fuels, could also negatively impact consumers’ perceptions of our products. Any decline in the social acceptability of our products could negatively impact their sales or lead to changes in laws, rules and regulations that prevent their access to certain locations, including trails and lakes, or restrict their use or manner of use in certain areas or during certain times. Additionally, while we have implemented various initiatives to address these risks, including the improvement of the environmental footprint and safety of our products, there can be no assurance that the perceptions of customers will not change. Consumers’ attitudes towards our products and the activities in which they are used also affect demand. Any failure to maintain the social acceptability of our products could impact our ability to retain existing customers and attract new ones which, in turn, could have a material adverse effect on our business, results of operations or financial condition.

Our future expansion plans are subject to uncertainties and risks, and distribution centers we intend to open may not result in sufficient increased sales of our products or the anticipated efficiencies.