UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from to

Commission file number

(Exact name of registrant as specified in its charter)

| ||

(State or other jurisdiction of | (I.R.S. Employer |

(949) 740-7799

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

|

| The |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ |

| Accelerated filer | ☐ |

☒ | Smaller reporting company | |||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the registrant’s voting and non-voting common equity held by its non-affiliates as of June 30, 2024, the last business day of the registrant’s most recently completed second fiscal quarter, was $

The number of the registrant’s shares of Class A common stock, $0.0001 par value per share, outstanding on March 11, 2025, was

Table of Contents

i

PART I

Item 1. Business.

Overview

For the year ended December 31, 2024, we generated revenues from two sources: parallel-import vehicles sales and logistics and warehousing services, while parallel-import vehicles segment was our only source of revenue in 2023. We began our operations in 2016 as a seller of parallel-import vehicles, sourcing vehicles in the U.S. and selling them in the PRC market. In the PRC, parallel-import vehicles refer to those purchased by dealers directly from overseas markets and imported for sale through channels other than brand manufacturers’ official distribution systems. Parallel-import vehicles used to be popular in the PRC because they were generally priced 10% to 15% cheaper than vehicles sold through distribution systems authorized by brand manufacturers. In addition, some overseas models can only be obtained through this channel rather than through the brand manufacturers’ authorized distribution systems as a result of certain regulations that prohibit their production and sale in the PRC due to environmental protection and emission standards. For the years ended December 31, 2024 and 2023, parallel-import vehicles contributed 78.2% and 100.0% of our total revenue, respectively. However, due to the COVID-19 pandemic, lockdowns in the PRC, and weaker customer demand in the PRC caused by deteriorating macroeconomic conditions and a growing preference for domestically produced electric vehicles (“EVs”), our parallel-import vehicle sales volume has been significantly reduced. We sold 14 and 303 vehicles during the years ended December 31, 2024 and 2023, respectively, generating total revenue of $1.6 million and $38.3 million, respectively, representing a decrease of 95.7% from 2023 to 2024.

To offset the negative impact brought by the decline in the parallel-import vehicle market and to diversify our revenue sources, in February 2024, we acquired Edward Transit Express Group Inc. (“Edward”), a California-based common carrier specializing in ocean transportation services, to start our logistics and warehousing operations. Beginning in the second quarter of 2024, we increased our marketing staff to pursue new business opportunities and focus on international trade flows between the PRC and the U.S. Additionally, in July 2024, we relocated our headquarters from Charlotte, North Carolina, to Irvine, California, which we believe will enable stronger management focus on our logistics and warehousing business due to Irvine’s proximity to the key ports of Los Angeles and Long Beach. In December 2024, we acquired TW & EW Services Inc (“TWEW”), a California-based provider of general labor and logistics services. Through TWEW, we provide general labor services including loading, unloading, and other labor-related activities.

Organizational Structure

Cheetah Net was originally formed on August 9, 2016 under the laws of the State of North Carolina as a limited liability company known as Yuan Qiu Business Group LLC. On March 1, 2022, we filed Articles of Incorporation including Articles of Conversion with the Secretary of State of the State of North Carolina to convert from an LLC to a corporation, and changed our name to Cheetah Net Supply Chain Service Inc. Cheetah Net also conducts business under the trade name of “Elite Motor Group.” As of the date of this annual report, Cheetah Net holds 100% of the equity interests in the following entities:

| ● | (i) Allen-Boy International LLC (“Allen-Boy”), a limited liability company organized on August 31, 2016 under the laws of the State of Delaware, which was acquired by Cheetah Net from Yingchang Yuan, the previous owner of Allen-Boy who beneficially owns 1,200,000 shares of Class A common stock of Cheetah Net, for a total consideration of $100 on January 1, 2017. Allen-Boy did not have any business activities until acquired by Cheetah Net. Currently, Allen-Boy is engaged in the parallel-import vehicle business. |

| ● | (ii) Pacific Consulting LLC (“Pacific”), a limited liability company organized on January 17, 2019 under the laws of the State of New York, which was acquired by Cheetah Net from Yingchang Yuan for a total consideration of $100 on February 15, 2019. Pacific did not have any business activities until acquired by Cheetah Net. Currently, Pacific is engaged in the parallel-import vehicle business. |

| ● | (iii) Entour Solutions LLC (“Entour”), a limited liability company organized on April 8, 2021 under the laws of the State of New York, which was acquired by Cheetah Net from Daihan Ding, the previous owner of Entour, for a total consideration of $100 on April 9, 2021. Entour did not have any business activities until acquired by Cheetah Net. Currently, Entour is engaged in the parallel-import vehicle business. |

1

| ● | (iv) Cheetah Net Logistics LLC (“Logistics”), a limited liability company organized on October 12, 2022 under the laws of the State of New York, whose previous sole member and owner, Hanzhang Li, assigned all his membership interests in Logistics to Cheetah Net for a total consideration of $100 through a membership interest assignment agreement dated October 19, 2022. Currently, Logistics is engaged in the parallel-import vehicle business. |

| ● | (v) Edward, a corporation incorporated on July 14, 2010 under the laws of the State of California, whose previous sole shareholder and owner, Juguang Zhang, transferred all his right, title, and interest in and to all of the issued and outstanding equity interests of Edward to Cheetah Net for a total consideration of $1,500,000, consisting of a $300,000 cash payment and Cheetah Net’s Class A common stock initially valued at $1.2 million through a stock purchase agreement dated January 24, 2024, as amended. The fair value of the stock consideration was determined to be $900,000. (See Note 8 of our audited financial statements as of December 31, 2024.) Currently, Edward is engaged in ocean transportation services. |

| ● | (vi) TWEW, a corporation incorporated on February 27, 2020 under the laws of the State of California, whose previous shareholders and owners transferred all their rights, titles, and interests in and to all of the issued and outstanding equity interests of TWEW to Cheetah Net for a total consideration of $1.0 million, consisting of a $200,000 cash payment and Cheetah Net’s Class A common stock valued at $800,000 through a stock purchase agreement dated November 27, 2024. The TWEW acquisition was closed on December 19, 2024. Currently, TWEW is engaged in logistics and labor services to strengthen Cheetah Net’s position in the logistics sector. |

| ● | (vii) NexTrade International LLC (“NexTrade”), a limited liability company organized on September 13, 2024 under the laws of the State of Delaware. On December 19, 2024, the sole member of NexTrade transferred all his membership interests in NexTrade to Cheetah Net for a total consideration of $1 in cash. NexTrade currently holds 100% of the ownership interests in Naiside (Shenzhen) International Trading Co., Ltd., a limited liability company organized on December 3, 2024, under the laws of the PRC. As of the date of this annual report, NexTrade is not engaged in any business operations. |

On August 3, 2023, we closed our IPO of 78,125 shares of Class A common stock at a price of $64.00 per share. In connection with the IPO, the shares of Class A common stock began trading on the Nasdaq Capital Market under the symbol “CTNT” on August 1, 2023.

On May 15, 2024, we closed a public offering of 825,625 shares of our Class A common stock at a price of $9.92 per share, for gross proceeds of approximately $8.19 million, before deducting placement agent fees and other offering fees and expenses.

On May 23, 2024, the Company dissolved two wholly owned subsidiaries, Canaan International LLC, an LLC organized on December 5, 2018 under the laws of the State of North Carolina, and Canaan Limousine LLC, an LLC organized on February 10, 2021 under the laws of the State of South Carolina.

On July 26, 2024, we closed a public offering of 404,979 shares of our Class A common stock at a price of $3.68 per share, for gross proceeds of approximately $1.49 million, before deducting placement agent fees and other offering fees and expenses.

On September 30, 2024, our stockholders approved our Fourth Amended and Restated Articles of Incorporation, which authorizes a reverse stock split of the issued shares of our common stock, par value $0.0001 per share, at a ratio ranging from 1-for-10 to 1-for-30, as determined at the discretion of our board of directors. On October 7, 2024, our board of directors approved a reverse stock split of our common stock at a ratio of 1-for-16. On October 21, 2024, we effectuated a reverse stock split of our common stock at a ratio of 1-for-16. Following such reverse split, each 16 shares of our common stock outstanding were automatically combined into one new share of common stock. No fractional shares were issued in connection with the reverse split; any fractional shares resulting from the reverse split were rounded up to the nearest whole share. The par value per share of our common stock remained unchanged. Our Class A common stock started trading on a post-split basis on October 24, 2024, at which time the Class A common stock was assigned a new CUSIP number (16307X202). Unless otherwise indicated, all share and per share amounts presented in this document have been retrospectively adjusted to reflect the reverse stock split as if it had occurred as of the earliest period presented.

2

Our Industry and Business Model

(I) Parallel-Import Vehicles

Overview

For the years ended December 31, 2024 and 2023, we generated revenue primarily from the sales of parallel-import vehicles. In the PRC, parallel-import vehicles refer to those purchased directly by dealers from overseas markets and imported into the PRC market for sale through channels other than brand manufacturers’ official distribution systems. Models and prices of parallel-import vehicles vary from mid-range to high-end brands, with a manufacturer’s suggested retail price (“MSRP”) typically not less than $40,000. Parallel-import vehicles used to be popular in China because they were relatively cheaper and offered a wider variety of models and versions with more customization possibilities than regular imported cars. Specifically, because parallel-import vehicles do not have to pass through multiple levels of distributors, such as China general distributors, regional distributors, and 4S stores, to reach their end consumers, they could generally be priced at least 10% to 15% lower than regular-imported vehicles. Parallel-import vehicles were popular also because some overseas models could not be produced and sold in China due to certain regulations concerning environmental protection and emission standards and could only be introduced into the PRC market through parallel imports. As manufacturers frequently arbitrage markets, setting the price according to local market conditions so the same vehicle will have different retail prices in different territories, this enables parallel-import vehicle dealers to utilize a profit maximization strategy to drive profit from the industry.

Parallel-import vehicles in China are generally divided into three categories based on the original country of procurement, including the U.S. version, the Middle East version, and the European version. All of the cars we sold in the past two fiscal years were of the U.S. version with MSRPs typically not less than $80,000. Suppliers of U.S. versions of parallel-import cars are typically unable to purchase large quantities of vehicles, so most of the industry’s participants are small family businesses who purchase cars from local dealers and resell them to local dealers/exporters in the U.S. or to dealers/importers in China. For U.S. dealers of parallel-import vehicles, vehicle sourcing capabilities are critical.

We purchased automobiles from the U.S. market through our team of professional purchasing agents, and resold them to our customers, including both U.S.- and PRC-based parallel-import vehicle dealers. We derived profits primarily from the price difference between our buying and selling prices for parallel-import vehicles. Our parallel-import vehicle operating principle was to maximize sales margins rather than volume, so we mainly focused on luxury vehicle brands in large demand because of the strong purchasing power of the end consumers in the PRC and higher markups for pricing. This strategy allowed us to maintain efficient operations and effective management by keeping the size and scope of our Company within reasonable limits.

From 2016 to the first half of 2022, we experienced significant growth in sales volume, revenue, and gross profit due to our core strengths and a favorable economic climate. However, the parallel-import vehicle market has faced significant challenges in recent years. Since the second half of 2023, the market for new luxury vehicles in the PRC has been negatively impacted by weak economic conditions and a shift in consumer demand towards EVs, mainly those produced domestically by PRC manufacturers. Luxury import brand dealers have responded to these threats by discounting the sale price of their vehicles, which has lately prevented us from generating a profit from the sale of parallel import vehicles. These factors, compounded by the lingering effects of the COVID-19 pandemic and lockdowns in the PRC, have significantly impacted our parallel-import vehicle business. Due to the unfavorable market conditions, our board of directors approved the discontinuation of our parallel-import vehicle business on March 3, 2025.

To offset the negative impact brought by the decline in the parallel-import vehicle market and to diversify our revenue sources, in February 2024, we acquired Edward, a California-based common carrier specializing in ocean transportation services, to start our logistics and warehousing operations. Beginning in the second quarter of 2024, we increased our marketing staff to pursue new business opportunities and focus on international trade flows between the PRC and the U.S. Additionally, in July 2024, we relocated our headquarters from Charlotte, North Carolina, to Irvine, California, which we believe will enable stronger management focus on our logistics and warehousing business due to Irvine’s proximity to the key ports of Los Angeles and Long Beach. Also, in December 2024, we acquired TWEW, a California-based provider of labor and logistics services. Through TWEW, we provide general labor services including loading, unloading, and other labor-related activities. See “—II. Logistics and Warehousing Services.”

3

Our Parallel-Import Vehicles Customers

We primarily served two types of customers in our parallel-import vehicles business in the past two fiscal years: (i) PRC customers and (ii) U.S. domestic customers. Specifically, our PRC customers were Chinese automobile dealers/importers who intended to import automobiles into the PRC market as parallel-import vehicles. Our U.S. domestic customers were parallel-import car dealers/exporters based in the U.S., which were typically the branches or upstream suppliers of Chinese parallel-import vehicle car dealers, who often lack purchasing capabilities in the U.S. market and need to purchase vehicles from us to transport to their PRC branches or sell to their PRC customers. Our parallel-import vehicles customers were willing to work with us because we were able to provide them with a large number of vehicles having a wide variety of models, thus greatly reducing the difficulty of collecting and managing vehicles for them. Our PRC and U.S. parallel-import vehicles customers generated approximately 87.7% and 12.3% of our revenue from parallel-import vehicles, respectively, during the year ended December 31, 2024, and 78.2% and 21.8% of our revenue from parallel-import vehicles, respectively, during the year ended December 31, 2023. We had a total of two and four customers for the years ended December 31, 2024 and 2023, respectively. For the year ended December 31, 2024, our two largest customers accounted for approximately 100% of our total revenue from parallel import vehicles. For the year ended December 31, 2023, our three largest customers accounted for approximately 98.9% of our total revenue from parallel-import vehicles.

As an example of a typical transaction, under a sales contract entered into by and between our Company and a PRC parallel-import vehicle customer, we were required to (i) load the designated automobiles on a vessel by the time of shipment specified in the contract at a U.S. port of loading; (ii) facilitate export customs clearance; (iii) provide the PRC customer with information about the designated automobiles, quantity, invoice amount, vessel name, and departure date, and provide a bill of lading, packaging list, commercial invoice, and other necessary documents; and (iv) ensure that the sold automobiles are brand new. Pursuant to the sales contract, the PRC customer (i) was responsible for import customs clearance and other relevant import issues; (ii) was required to bear all costs and risks once the designated automobiles arrive at the designated port of destination in the PRC; and (iii) was responsible for arranging payment as specified in the contract. In the event of any dispute, controversy, or claim arising out of or relating to such sales contracts, both parties agreed (i) they will first try to resolve such disputes through friendly consultation; and that (ii) the validity, interpretation, and implementation of such contracts shall be governed by the laws of the State of North Carolina in the U.S.

Similarly, our U.S. customers entered into sales agreements for each automobile sold by us. According to a typical sales agreement entered into between our U.S. customers and our Company, we would (i) sell the designated automobile to the U.S. customer for the amount specified in the agreement and certify that all of the information provided therein is true and accurate to the best of our knowledge; (ii) deliver the automobile to the warehouse requested by the U.S. customer; and (iii) provide the automobile title within three weeks of the completion of the transaction. Meanwhile, the U.S. customer acknowledged that the automobile described therein was sold “as is” and that there was no guarantee or warranty either expressed or implied with respect to the automobile.

Our Parallel-Import Vehicles Suppliers

We did not have regular suppliers for our parallel-import vehicles business in the past two fiscal years, because we purchased all of our automobiles via our team of professional purchasing agents from U.S. automobile dealers that had the designated automobile model in stock. The designated brands and models were usually luxury or mid- to high-end vehicles that were in high demand in the PRC market, such as Mercedes GLS450, Mercedes G63, BMW X7, and Lexus 600.

Our Professional Purchasing Agents for Parallel-Import Vehicles

As of December 31, 2024, we did not work with any independent contractors on parallel-import vehicle purchases due to the shrinkage of the parallel-import vehicle market. Due to the unfavorable market conditions, our board of directors approved the discontinuation of our parallel-import vehicle business on March 3, 2025. See “—Overview.”

4

As of December 31, 2023, we worked with 389 independent contractors as our professional purchasing agents, responsible for purchasing designated models of vehicles using the knowledge and negotiating skills they acquired from our training. We developed a standardized system of recruiting, training, and managing professional purchasing agents. Specifically, we posted job listings on various job platforms to attract qualified potential candidates and assigned received resumes to our full-time procurement specialists, who would schedule interviews by telephone or in person. A second interview would be conducted by a procurement manager and/or human resources manager to further review the candidate’s background and qualifications. Upon reviewing the applicant’s experience in the industry, knowledge of our Company, and other qualifications, we would determine whether a candidate is a good fit. In addition, we designed and developed our own referral program that incentivized our agents to utilize their network to attract additional qualified agents and thus further expanded our purchasing agent base. In particular, we encouraged our purchasing agents to introduce such positions to their connections and forward their resumes or contact information to our Company if consent was granted. The candidates so referred, if retained, would receive our training and start working as purchasing agents, and the referral agent would earn a $200 commission for each deal the referred agents closed. There were no limit or cap on how many referrals could be made in our referral program. In the referral program, existing agents acted as mentors to new agents by providing them with initial training and helping them become familiar with our Company.

Since most of the purchasing agents had other part-time employment, training sessions were provided to accommodate their schedules. In a training session, our procurement specialists would outline the details, such as models with specifications, purchasing procedures, commission structures, and agent conduct when visiting a dealership. The agents were trained continuously after each deal was completed to improve their skills and knowledge. To determine whether a new purchasing agent had been fully trained and understood well his or her responsibilities, workflow, and company procedures and policies, a procurement manager would schedule an assessment test or call with the new agent before the agent placed his or her first order with a dealership. We managed our purchasing agents through a variety of communication tools, including texts, phone calls, emails, and Zoom meetings. Each purchasing agent would be assigned to a procurement specialist in charge, who led and trained a group of agents. Depending on the agent’s schedule, the procurement specialists in charge were in direct communication with their agents on a weekly basis for updates on active deals, leads for new potential deals, and scheduling vehicle pick-ups.

In accordance with a typical independent contractor agreement entered between a professional purchasing agent and our Company, the purchasing agent agreed to (i) acquire the automobile identified by our Company and promptly transfer possession of the automobile to us; (ii) diligently execute all documents related to the transfer of title and delivery of the automobile; (iii) deliver the automobile without any physical damage, including all purchasing documents, user manuals, window sticker, keys, spare tires, and interior carpets; and (iv) acknowledge that the automobile was at all times the sole property of our Company insofar as we fulfilled our obligation to fund all related costs of purchasing the automobile and to pay/reimburse all fees owed pursuant to the independent contractor agreement. Pursuant to the independent contractor agreement, we were required to pay the purchasing agent a service fee calculated according to an agreed-upon payment structure specified in the agreement, which included (i) a base fee ranging from $500 to $2,000, depending on the model of the purchased automobile, and (ii) an incentive bonus that amounted to 25% of any further discount achieved by the purchasing agent beyond the pre-determined benchmark discount required for the purchased automobile. Such an agreement also included liability exemption clauses providing that the purchasing agent shall not be liable for any fines or lawsuits imposed by dealerships or manufacturers due to export infractions or infringements, and we agreed to indemnify, defend, and hold harmless the purchasing agent from and against any liability, losses, claims, costs, interests, penalties, expenses, and damages arising from any non-negligent execution of the role as purchasing agents on behalf of our Company.

5

Parallel-Import Vehicles Brands We Supplied

The brands of automobiles we have procured include Mercedes, BMW, Land Rover, Lexus, Ram, and Toyota.

The following table sets forth a breakdown of brands purchased during the years ended December 31, 2024 and 2023.

|

| Percentages |

|

| Percentages |

| |||

Number of | of | Number of | of | ||||||

Automobiles | Total | Automobiles | Total | ||||||

Purchased | Purchase | Purchased | Purchase | ||||||

During the | During the | During the | During the | ||||||

Year | Year |

| Year |

| Year | ||||

Ended |

| Ended | Ended | Ended | |||||

| December 31, | December 31, | December 31, | December 31, | |||||

Brands/Models: | 2024 | 2024 | 2023 | 2023 | |||||

Luxury Brands |

|

|

|

|

| ||||

Mercedes Benz GLS450 | 11 | 78.6 | % | 157 | 51.8 | % | |||

Mercedes Benz G63 | 1 | 7.1 | % | — | — | % | |||

Mercedes Benz GLS600 | — | — | % | 12 | 4.0 | % | |||

BMW X7 |

| — |

| — | % | 5 |

| 1.7 | % |

Lexus LX600 |

| 2 |

| 14.3 | % | 68 |

| 22.4 | % |

Land Rover Range Rover |

| — |

| — | % | 15 |

| 4.9 | % |

Ram 1500 TRX |

| — |

| — | % | 14 |

| 4.6 | % |

Toyota Sequoia |

| — |

| — | % | 32 |

| 10.6 | % |

Total |

| 14 |

| 100.0 | % | 303 |

| 100.0 | % |

Parallel-Import Vehicles Services and Operational Flow

Procurement

We made procurement decisions based on our extensive experience and insights into the PRC parallel-import vehicle industry. In order to avoid overstocking or understocking inventory, we would forecast inventory needs and expenses through meticulous market analysis and weekly sales department meetings. Specifically, our management would estimate, based on the data from the General Administration of Customs of China, that approximately 20,000 parallel-import cars had been exported annually from the U.S. to China in recent years, most of which were of low-end and mid-range brands. Our founding team understood the factors driving the growth of the luxury-car segment in China and the desires of the Chinese consumer. In addition, we had some close business partners in China who were parallel-import car traders or dealers, including some of our PRC customers and some third parties or potential customers. They provided us with timely information on the PRC market and often offered us more favorable terms of settlement. To develop our sales strategy and support our procurement department’s purchasing plans, the sales department met weekly with our procurement department to discuss the latest market needs and dynamics, including sales prices, brand composition, and inventory changes. Nonetheless, in the event that we overstocked or understocked our inventory, our business, financial condition, and results of operations could be adversely harmed.

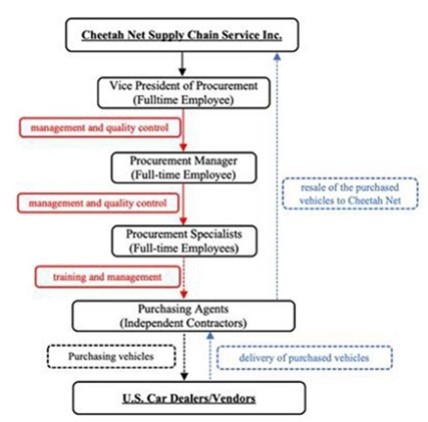

We primarily procured automobiles through our team of professional purchasing agents, who served as independent contractors, from U.S. automobile dealers that had the designated automobile model in stock. Mr. Walter Folker, our previous Vice President of Procurement, oversaw a full-time procurement manager, who in turn supervised our full-time procurement specialists. Those full-time procurement specialists were responsible for training our purchasing agents and providing them with timely phone coaching and on-site support.

6

Our purchasing agents negotiated the best price for our designated automobile models using the knowledge and negotiating skills they received from our training. We decided which automobiles to purchase primarily based on the demand and selling price for specific automobile models in the PRC market and their availability in the U.S. market. We regularly issued instructions about the brands and models of vehicles to be purchased, as well as the maximum acceptable prices and pick-up time limits. Professional purchasing agents could visit dealerships across the U.S. for quotes based on their schedules and convenience and provide us with the price information they obtained. We would then select the lowest prices for models in demand and assist those purchasing agents who provided such quotes in completing the purchases. Once the purchases were completed, the purchasing agents sell automobiles to our Company at their purchase prices and charge us a service fee per automobile based on the model of the vehicle and the discount they obtained from the automobile dealers. See “—Our Professional Purchasing Agents.”

A purchasing agent would usually pay the deposit to automobile dealers using a Company-issued credit and would pay the remaining balance via bank cashier check from our Company’s bank account. The purchasing agents would occasionally advance funds to the automobile dealers, which we would reimburse once they provided a receipt and other required documents. In addition, we would fund other costs, fees, and taxes incurred by purchasing agents related to the purchase and transfer of automobiles. Once the purchasing agents received the titles of the purchased automobiles from the Department of Motor Vehicles, they would immediately sign the titles over to us. Automobiles purchased from U.S. automobile dealers would be picked up by our purchasing agents and delivered to us at a designated warehouse or other agreed delivery locations.

Below is a diagram showing the procurement process:

7

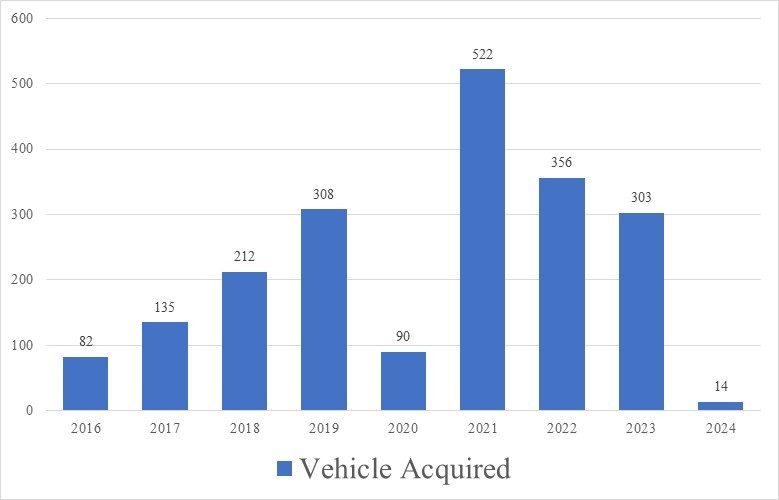

The following chart demonstrates the number of vehicles we acquired each year since 2016. We were able to support an annual purchase volume of 500 to 600 cars with our team size and working capital reserves before our business focus shift to logistics and warehousing services. We discontinued to acquire vehicles since the second quarter of 2024, and discontinued parallel-import vehicle business following the approval of Company’s Board of Director on March 3, 2025 due to unfavorable market conditions.

Note: Year 2020 was affected by the COVID-19 pandemic and China’s Implementation of National VI Standards.

8

Sales and Services

In the past two fiscal years, we sold our automobile inventories to both U.S. customers (parallel-import vehicle exporters based in the U.S.) and PRC customers (Chinese parallel-import car dealers who purchased cars from us and imported them into the PRC to resell them to other dealers or end consumers). A specific vehicle model’s pricing and profitability varied based on the market demand and supply for that model. We set our selling prices based on multiple factors, including the price of the same model sold by authorized dealers in China, normal commercial terms, market pricing adjustments, customer payment methods, operational efficiency of our Company, and anticipated workload for trading activities. The selling price was finalized as the MSRP plus service fees, which were determined upon comprehensive consideration of the overall market adjustments for vehicles as well as the customer’s payment method. The following table sets forth the breakdown of our sales revenue by brands and models during the years ended December 31, 2024 and 2023.

| Sales |

| Revenue Share |

| Sales |

| Revenue Share |

| |||

Revenue | of Total | Revenue | of Total | ||||||||

During the | Sales for | During the | Sales for | ||||||||

Year | the Year | Year | the Year | ||||||||

Ended | Ended | Ended | Ended | ||||||||

December 31, | December 31, | December 31, | December 31, | ||||||||

Brands/Models: | 2024 | 2024 | 2023 | 2023 | |||||||

Luxury Brands |

|

|

|

| |||||||

Mercedes Benz GLS450 | $ | 1,175,116 | 72.0 | % | $ | 17,634,255 | 46.0 | % | |||

Mercedes Benz G63 | $ | 200,297 | 12.3 | % | $ | — | — | % | |||

Mercedes Benz GLS600 | $ | — | — | % | $ | 2,877,516 | 7.5 | % | |||

BMW X7 | $ | — | — | % | $ | 480,210 | 1.2 | % | |||

Lexus LX 600 | $ | 255,835 |

| 15.7 | % | $ | 10,023,386 |

| 26.2 | % | |

Land Rover Range Rover | $ | — |

| — | % | $ | 2,359,979 |

| 6.2 | % | |

Ram 1500 RTX | $ | — |

| — | % | $ | 1,698,061 |

| 4.4 | % | |

Toyota Sequoia | $ | — |

| — | % | $ | 3,242,567 |

| 8.5 | % | |

Total | $ | 1,631,248 |

| 100.0 | % | $ | 38,315,974 | 100.0 | % | ||

Typically, we would enter into sales contracts with our PRC and U.S. customers. See “—Our Parallel-Import Vehicles Customers.” Our U.S. customers usually pay the full amount to us within two days before or after the automobile is delivered to the appointed warehouse. In most cases, our PRC customers would make their payments one or two weeks after we arranged for a freight forwarding company to load the automobile and provided them with the ocean bill of lading and other related documents.

Fulfillment and U.S. Customs Clearance

For our domestic sales, we delivered the purchased vehicles to U.S. customers at their designated warehouses and provided the original copy of the title to them within the agreed timeframe. Our U.S. customers were responsible for export and cross-border transportation matters on their own after purchasing automobiles. In this case, we bore the risk of damage and loss before delivering the automobile to the warehouse designated by the U.S. customer. For our PRC customers, it was our responsibility to arrange for the ocean freight forwarder to load the automobile to be shipped and provide them with the ocean bill of lading and related documents. As such, we bore the risk of damage and loss prior to arranging for the shipping of automobiles by third-party logistics service providers, but these risks passed to our PRC customers once the automobile was dispatched on board. Our PRC customers, namely, Chinese parallel-import car dealers, were responsible for after-sale services for the end consumers of those parallel-import vehicles.

9

Prior to shipping the automobiles, we would generally require PRC customers to make the majority of the amount owed (typically the MSRP amount) upfront via a letter of credit, where the release of payment was contingent upon our submission of a bill of lading and other required documents to the issuing bank underlying the letter of credit for its review. Once we confirmed receipt of the letter of credit, we would settle the loan (if any) and arrange for customs clearance and shipping by third-party logistics service providers. In the event that all customs clearance procedures had been completed with all forms filled out and accepted by U.S. Customs and Border Protection (“Customs”), we would ship the automobiles and provide the issuing bank with the bill of lading and related documents for its review. Upon completion of the review, the issuing bank would release payment to us and the bill of lading and related documents to PRC customers, which were necessary to obtain the automobiles from the freight forwarder. We cooperated with third-party logistics service providers whose primary responsibility was to provide cross-border logistics services, typically by sea, for the delivery of our automobiles to our PRC customers.

(II) Logistics and Warehousing Services

Logistics and warehousing services is a business line we launched in February 2024. Following the downturn in the parallel-import vehicle market, our management decided to pivot toward logistics and warehousing, drawing on the extensive experience we had developed in transporting parallel-import vehicles. In February 2024 and December 2024, we acquired Edward and TWEW, respectively, and have since generated revenue from their existing logistics and warehousing operations. For the year ended December 31, 2024, our logistics and warehousing business contributed 21.8% of our total revenue. As of December 31, 2024, we had an active customer base of 24 customers for our logistics and warehousing business, as compared with seven when we initially launched the business in February 2024. Although, as of the date of this annual report, logistics and warehousing accounts for a relatively small portion of our total revenue, we have taken actions to streamline operations, expand service offering, and enhance market position. Therefore, we anticipate the logistics and warehousing business will become our primary focus in the foreseeable future.

Our logistics and warehousing business focuses on providing freight forwarding services for clients shipping goods from the U.S. to mainland China or Hong Kong. We operate as a Non-Vessel-Operating Common Carrier (“NVOCC”), bridging the gap between shippers and ocean carriers to facilitate the movement of cargo. Generally, our customers lack either the industry knowledge or direct relationships with ocean carriers necessary to secure reliable, cost-effective transportation. By acting as our customers’ U.S. point of contact, we coordinate shipments on their behalf, leveraging our expertise and carrier network to streamline logistics. Our primary responsibilities include: (i) cargo storage, (ii) freight forwarding, (iii) U.S. customs clearance, and (iv) labor services and cargo loading and unloading. Customers may engage us for any combination of these services. For the year ended December 31, 2024, we conducted the first three services exclusively through Edward and handled labor services and cargo loading and unloading solely through TWEW.

Cargo Storage

The workflow of cargo storage begins when a customer submits a shipping request. Our customers are typically U.S.-based merchants needing to ship goods to Asia. They cover the cost of transporting their cargo from their locations to our California warehouse. Once the cargo arrives at our warehouse, our staff inspects it and records details such as contents and final destination in our system. As of the date of this annual report, we lease one warehouse located in Gardena, California, covering approximately 8,800 square feet. See “Item 2. Properties.” Our warehouse is equipped with handling equipment (such as forklifts and pallet jacks) and security measures (such as surveillance cameras and fire sprinkler systems) to protect stored cargo.

Freight Forwarding

After the cargo is received, customers may choose to either have us ship it or engage another service provider to do so. If a customer opts for our ocean freight service, we will secure space for the cargo through our established network of ocean carriers. As of the date of this annual report, we work with three ocean carriers, each of which had a longstanding partnership with Edward prior to its acquisition and continues to work with us after the acquisition.

We enter into master service agreements with ocean carriers, typically lasting for 12 months. These service agreements generally contain a minimum quantity commitment (“MQC”), which is the minimum volume of cargo (often measured in 20 and 40-foot equivalent units), that we, as the shipper, must tender to the carrier within the contractual period. This arrangement allows us to secure favorable rates and enough space while enabling the carrier to allocate its capacity efficiently. Under these agreements, we must submit individual booking requests within the timeframe specified by the agreement. In return for our MQC commitment, the carrier reserves space for our shipments at the agreed-upon rates.

10

Ocean freight fees are generally paid at the estimated time of departure. However, we have credit arrangements with certain ocean carriers and, in some cases, settle multiple transactions together on a periodic basis. If we fail to meet the MQC, we may be subject to a “Dead Freight” penalty, meaning we must pay the contracted rate for any shortfall in the MQC. If the carrier cannot provide sufficient space, the contract permits a reduction of our MQC obligation by the undelivered volume. Because these agreements include a “Dead Freight” penalty, they typically do not offer early termination clauses. Once cargo leaves our warehouse, we coordinate with trucking companies to transport it to the port. According to industry practices, we and the trucking companies typically reach agreements for each service engagement, primarily through email communications, rather than executing formal written service agreements. As of the date of this annual report, we work with nine trucking companies. The ocean carriers and trucking companies serve as our suppliers.

U.S. Customs Clearance

Before cargo departs the United States, we handle U.S. customs clearance on behalf of the client if engaged to do so. Specifically, the customer signs a power of attorney designating us as its legal agent at the U.S. custom, authorizing us to endorse, sign, declare, or certify any entry, withdrawal, declaration, certificate, bill of lading, or other document required by law or regulation in connection with the shipment of the goods.

Labor Services and Cargo Loading and Unloading

We provide general labor and container loading and unloading workforce services to clients through TWEW. We enter into cooperation agreements with customers, which stipulates our obligations such as to supply workers to customers and handle payroll, taxes, and insurances. These workers typically work on terminal loading and unloading operations. We hire workers from independent third parties. Customers payments are generally calculated based on the hours worked by the assigned workers. These agreements can typically be early terminated by either party with prior written notice.

Technology and Intellectual Property

The success of our business depends on our proprietary technologies. Our logistics and warehousing business leverages GoFreight, a freight forwarding management software that streamlines workflows, enhances shipment tracking, and supports multi-modal logistics, with a primary focus on ocean freight. Key features of GoFreight include an automated freight management system that minimizes manual tasks, a centralized dashboard for shipment visibility, and integrated tools for efficient import and export operations.

We previously relied on our Office Automation System (the “OA System”), an information technology system used to track order status and monitor business workflow, to conduct our parallel-import vehicles business. The OA System facilitated the storage, exchange, and management of order data, thereby enhancing our productivity and efficiency. As of the date of this annual report, we have discontinued the use of the OA System. However, we cannot rule out the possibility of reusing it should we resume our parallel-import vehicles operations.

As of the date of this annual report, we own four domain names in the U.S., including (i) Cheetah-net.com, a domain name registered on August 17, 2022 and associated with the Cheetah Net website; (ii) Pacificconsultingusa.com, a domain name registered on January 7, 2019 and associated with the Pacific Consulting LLC website; (iii) Allen-boy.com, a domain name registered on December 5, 2018 and currently not in use; and (iv) edwardtransitusa.com, a domain name associated with the Edward website, which was registered by Edward prior to our acquisition and subsequently transferred to our domain provider on April 17, 2024. We also own the trademark “LOFIRST,” which was originally registered by Edward and later acquired by us following our acquisition of Edward.

We hold an Ocean Transportation Intermediary License (License No. 015545N), which allows us to operate as an NVOCC.

Employees

As of December 31, 2024, we had a total of 15 employees, 13 of whom worked as full-time employees, as set forth in the following table:

| Number of |

| Number of | |

total | full-time | |||

Function: | employees | employees |

11

Warehousing Management | 3 | 3 | ||

Marketing | 2 | 2 | ||

Accounting | 4 | 4 | ||

Legal | 3 | 3 | ||

Administration | 2 | — | ||

Executive officer | 1 | 1 | ||

Total |

| 15 |

| 13 |

Our employment contracts with full-time employees include a confidentiality clause.

Under our logistics and warehousing services, we worked with two independent contractors as of December 31, 2024. These independent contractors provided general labor support for our operations. Under our parallel-import vehicles business, we worked with 389 independent contractors as of December 31, 2023. These independent contractors served as our professional purchasing agents, primarily responsible for visiting the U.S. automobile dealers and negotiating the best vehicle purchase price.

We believe that we maintain a good working relationship with our employees and our independent contractors, and we have not experienced material labor disputes in the past. None of our employees is represented by labor unions.

Competition

The logistics and warehousing industry in the U.S. is highly competitive and rapidly evolving, with many new entrants in recent years and only a few leading companies. We believe our ability to compete effectively for customers depends on several factors: the quality and variety of services we offer in our logistics and warehousing business, our relationships with ocean carriers, customers, customs, and trucking companies, and our ability to recruit and retain talented professionals with industry expertise. Based on these factors and our stable supplier and customer connections, we believe our niche focus on international trade flows between the PRC and U.S., combined with integrated services, provides a differentiated value proposition. However, some of our current or future competitors may have longer operating histories, greater brand recognition, or more extensive financial, technical, or marketing resources than we do. See also “Item 1A. Risk Factors—Economic, Political, and Market Risks—We are in the competitive logistics and warehousing industry, and we may not be able to compete successfully against existing or new competitors, which could reduce our market share and adversely affect our competitive position and financial performance.”

Governmental Regulations

The U.S. Federal Maritime Commission regulations require that all NVOCCs maintain proof of financial responsibility. Most NVOCCs satisfy this requirement by obtaining an NVOCC Bond. Licensed NVOCCs must maintain a bond in the amount of $75,000. As of the date of this annual report, Edward maintains a bond in the amount of $75,000.

12

Item 1A. Risk Factors.

Economic, Political, and Market Risks

We are currently operating in a period of economic uncertainty and capital markets disruption, which has been significantly impacted by geopolitical instability due to the ongoing military conflicts between Russia and Ukraine and in the Middle East and the increasingly strained relationship between the U.S. and China. Our business, financial condition, and results of operations could be materially adversely affected by any negative impact on the global economy and capital markets resulting from the conflicts in Ukraine and the Middle East or any other geopolitical tensions.

U.S. and global markets are experiencing volatility and disruption following the escalation of geopolitical tensions and the military conflicts between Russia and Ukraine and in the Middle East. Although the length and impact of the ongoing military conflicts is highly unpredictable, the conflicts could lead to continuing market disruptions, including significant volatility in commodity prices, credit and capital markets, as well as supply chain interruptions.

The military conflict in Ukraine has led to sanctions and other penalties being levied by the United States, European Union, and other countries against Russia. Additional potential sanctions and penalties have also been proposed or threatened. Russian military actions and the resulting sanctions could adversely affect the global economy and financial markets and lead to instability and lack of liquidity in capital markets, potentially making it more difficult for us to obtain additional funds. Although our business has not been materially impacted by the ongoing military conflicts between Russia and Ukraine and in the Middle East to date, it is impossible to predict the extent to which our operations, or those of our suppliers and manufacturers, will be impacted in the short and long term, or the ways in which the conflict may impact our business. The extent and duration of the military action, sanctions and resulting market disruptions are impossible to predict, but could be substantial. Any such disruptions may also magnify the impact of other risks described in this annual report.

In addition, the U.S.-PRC relationship has recently faced a daunting challenge, contributing to geopolitical instability worldwide. Because our sales to the PRC market represent a significant part of our revenue, our business relies on a stable economic and political relationship between the U.S. and the PRC. However, the tensions between the two countries have intensified since the COVID-19 pandemic, exemplified by the ongoing trade conflicts between U.S. and the PRC, and there is significant uncertainty about the future relationship between the two countries with respect to trade policies, treaties, government regulations, and tariffs. A deteriorating relationship between the U.S. and the PRC, or a prolonged stalemate between them, could materially adversely affect international logistics, as well as our business, results of operations, and financial condition.

Availability and demand for our products and services may be adversely impacted by economic conditions and other factors.

Our success depends on the demand for our logistics and warehousing services. Fluctuations in economic conditions, periods of recession, reduced consumer spending, or volatility in fuel prices can significantly diminish demand for our services. Additionally, changes in political policies, currency exchange rates, and regulatory requirements may disrupt transportation processes, affecting customers’ willingness to engage our services. If we are unable to adapt business strategies or maintain adequate financial and operational flexibility in response to fluctuations caused by these events, our business, financial condition, and results of operations could be materially and adversely affected.

We are in the competitive logistics and warehousing industry, and we may not be able to compete successfully against existing or new competitors, which could reduce our market share and adversely affect our competitive position and financial performance.

The logistics and warehousing industry in the U.S. is competitive and rapidly evolving, with many new companies joining the competition in recent years. We compete directly with other local, regional, national, and international logistics providers on the following bases:

| ● | service pricings; |

| ● | quality of services; |

| ● | transportation speed; and |

| ● | service offerings. |

13

Convenience and reliability are a major concern for logistics and warehousing services users; customers tend to select a brand with a relatively large market share and proven reputation. In addition, our experience in expanding non-vehicle logistics and warehousing revenue is limited, and our success in these areas will depend on our ability to develop and scale an effective salesforce to market these services to international trading companies in the U.S. and the PRC. Our competitors may operate with different business models, have different cost structures, and may ultimately prove to be more successful or more adaptable to new regulatory, technological, and other developments. They may in the future achieve greater market acceptance and recognition and gain a greater market share. It is also possible that potential competitors may emerge and acquire a significant market share. If existing or potential competitors develop or offer services that provide significant performance, price, creative optimization, or other advantages over those offered by us, our business, results of operations, and financial condition would be negatively affected. Our existing and potential competitors may enjoy competitive advantages over us, such as longer operating history, greater brand recognition, larger client base, and better value-added services. We may lose clients if we fail to compete successfully, which could adversely affect our financial performance and business prospects. We cannot guarantee that our strategies will remain competitive or successful in the future. Increasing competition may result in pricing pressure and loss of our market share, either of which could have a material adverse effect on our financial condition and results of operations.

We may be adversely affected by the effects of inflation and a potential recession in the U.S. and by a weakening economy in the PRC.

Inflation has the potential to adversely affect our liquidity, business, financial condition, and results of operations by increasing our overall cost structure, particularly if we are unable to achieve commensurate increases in the prices we charge our customers. The existence of inflation in the U.S. economy has resulted in, and may continue to result in, higher interest rates and capital costs, shipping costs, supply shortages, increased costs of labor, weakening exchange rates, and other similar effects. As a result of inflation, we have experienced and may continue to experience cost increases. In addition, poor economic and market conditions in the U.S. and the PRC, including a potential recession, may negatively impact market sentiment, decreasing the demand for automobiles, which would adversely affect our operating income and results of operations. If we are unable to take effective measures in a timely manner to mitigate the impact of inflation as well as a potential recession, our business, financial condition, and results of operations could be adversely affected.

Fluctuations in exchange rates could have a material and adverse effect on our results of operations and the value of your investment.

The value of Renminbi (“RMB”), PRC’s legal currency, against the USD may fluctuate and is affected by, among other things, changes in political and economic conditions and the foreign exchange policy adopted by the PRC government. On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the RMB to the U.S. dollar, and the RMB appreciated more than 20% against the U.S. dollar over the following three years. Between July 2008 and June 2010, this appreciation halted and the exchange rate between the RMB and the U.S. dollar remained within a narrow band. In August 2015, the People’s Bank of China (the “PBOC”) changed the way it calculates the mid-point price of the RMB against the USD, requiring the market-makers who submit for reference rates to consider the previous day’s closing spot rate, foreign-exchange demand and supply, as well as changes in major currency rates. In 2019, the RMB appreciated by approximately 1.9% against the U.S. dollar. In 2020, RMB appreciated by approximately 6.9% against the U.S. dollar. In 2021, RMB depreciated approximately 2.6% against the U.S. dollar. During the year ended December 31, 2022, RMB rapidly depreciated against the U.S. dollar by approximately 9.0%. It is difficult to predict how market forces or PRC or U.S. government policy, including any interest rate increases by the Federal Reserve, may impact the exchange rate between the RMB and the USD in the future. There remains significant international pressure on the PRC government to adopt a more flexible currency policy, including from the U.S. government, which has threatened to label China as a “currency manipulator,” which could result in greater fluctuation of the RMB against the USD. However, the PRC government may still at its discretion restrict access to foreign currencies for capital account or current account transactions in the future. Therefore, it is difficult to predict how market forces or government policies may impact the exchange rate between the RMB and the USD in the future. In addition, the PBOC regularly intervenes in the foreign exchange market to limit fluctuations in RMB exchange rates and achieve policy goals. To date, we have not entered into any hedging transactions in an effort to reduce our exposure to foreign currency exchange risk. While we may decide to enter into hedging transactions in the future, the availability and effectiveness of these hedges may be limited and we may not be able to hedge our exposure adequately or at all. As of the date of this annual report, we settle all our transactions in USD. Our clients who need to convert RMB into USD for payment may choose not to engage us due to exchange rate considerations. If that occurs, or if the exchange rate between the RMB and USD fluctuates in an unanticipated manner, our business, financial condition, and results of operations could be materially adversely affected.

14

If the PRC government imposes further restrictions and limitations on our PRC customers’ ability to transfer or distribute cash from the PRC to the U.S., our business, financial condition, and results of operations could be materially adversely affected.

The PRC government has imposed controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of the PRC. For instance, the Circular on Promoting the Reform of Foreign Exchange Management and Improving Authenticity and Compliance Review, or “SAFE Circular 3,” issued on January 26, 2017, provides that banks shall, when dealing with dividend remittance transactions from a domestic enterprise to its offshore shareholders of more than $50,000, review the relevant board resolutions, original tax filing form, and audited financial statements of such domestic enterprise based on the principle of genuine transaction. There is no guarantee that the PRC government will not further intervene or impose other restrictions on our PRC customers’ ability to transfer or distribute cash outside the PRC. In the event that the foreign exchange control system prevents our PRC customers from remitting their payments to the U.S., we may not be able to receive a substantial portion of our revenue. As a result, our business, financial condition, and results of operations may be adversely affected.

Operational Risks

We are undergoing a transformation of our business model, which could have a material and adverse effect on our business, financial condition, and results of operations.

We are shifting our business focus from parallel-import vehicle sales to logistics and warehousing services. Since the second half of 2022, our parallel-import vehicle business has been negatively impacted by the COVID-19 pandemic, lockdowns in the PRC, and weaker customer demand in the PRC due to deteriorating macroeconomic conditions. During the year ended December 31, 2024, we sold 14 vehicles, generating revenue of $1.6 million. During the year ended December 31, 2023, we sold 303 vehicles, generating revenue of $38.3 million. In February 2024, we acquired Edward to expand our logistics and warehousing service operations. Beginning in the second quarter of 2024, we increased our marketing staff to pursue new business opportunities and to focus on international trades between the PRC and the U.S. In December 2024, we acquired TWEW to further expand our logistics services. These strategic actions are expected to significantly alter our revenue structure and could, if unsuccessful, materially and adversely affect our business, financial condition, and results of operations.

As we are located in California, we may be subject to catastrophic events, which could have a material adverse impact on our business, financial condition, and results of operations.

We are located in California, a state prone to natural disasters and other catastrophic events due to its coastal location. A disruption or failure of our systems or operations resulting from earthquakes, severe weather, actual or threatened terrorist attacks, strikes, civil unrest, pandemics, or similar catastrophic occurrences could delay our ability to deliver services and carry out other critical functions. Such disruptions could have a materially adverse effect on our business, financial condition, and results of operations.

Service disruption experienced by our warehouse and office may adversely affect our business operations.

Our daily operations rely heavily on the orderly performance of our regional warehouse in Gardena, California, which manages our storage and shipments, and our administrative office in Irvine, California, which oversees our operational activities. Service disruptions due to automated facility failures, insufficient capacity during peak freight periods, force majeure events, third-party interference or disputes, employee misconduct, strikes, government inspections, orders, mandates, and temporary or permanent shutdowns could cause our shipments to be canceled or delayed and increase our storage costs, both of which could have a materially adverse effect on our business, financial condition, and results of operations.

If our clients are able to reduce their logistics and supply chain costs or increase utilization of their internal solutions, our business and results of operations may be materially and adversely affected.

Clients often rely on logistics companies because developing in-house logistics and supply chain capabilities is costly, requires specialized expertise, and can lead to operational inefficiencies. However, if our clients are able to establish their own logistics and supply chain solutions, increase utilization of their internal resources, reduce their logistics spending, or otherwise choose to discontinue our services, our business, financial condition, and results of operations may be materially and adversely affected.

15

We face risks from fuel price fluctuation.

Transportation costs are a major expense in the logistics industry, and fuel is a key component of such expense. As an NVOCC, we depend on international shipping partners to transport our goods. If fuel prices rise significantly, our partners may increase their service fees, thereby passing on higher costs to us.

We face risks associated with the freight handled through our network.

We handle a large volume of freights and face challenges with respect to the protection and examination of freights. Freights within our network may be stolen, damaged, or lost for various reasons, and we or third-party transportation providers or both may be perceived or found liable for such incidents. In addition, we may fail to screen freight and detect unsafe, prohibited, or restricted items. Unsafe items, such as flammables, explosives, toxic, radioactive, or corrosive items and materials, may damage other freights within our network, injure recipients, and harm the personnel and assets of us and/or third-party transportation providers. Furthermore, if we fail to prevent prohibited or restricted items from entering into our network and if we participate in the transportation and delivery of such items, we may be subject to administrative or even criminal penalties, and if any personal injury or property damage is concurrently caused, we may be further liable for civil compensation.

The transportation of freight also involves inherent risks. We are subject to risks associated with transportation safety, and the insurance maintained by us may not fully cover the damages caused by transportation related injuries or loss. From time to time, our vehicles and personnel may be involved in transportation accidents, and the freight carried by them may be lost or damaged. In addition, frictions or disputes may occasionally arise from the direct interactions between our pickup and delivery personnel with freight senders and recipients. Personal injuries or property damages may arise if such incidents escalate.

Any of the foregoing could disrupt our services, cause us to incur substantial expenses, and divert the time and attention of our management. We and third-party transportation providers may face claims and incur significant liabilities if found liable or partially liable for any of injuries, damages, or losses. Claims against us may exceed the amount of our insurance coverage or may not be covered by insurance at all. Governmental authorities may also impose significant fines on us or require us to adopt costly preventive measures. Furthermore, if our services are perceived to be insecure or unsafe by our clients, our business volume may be significantly reduced, and our business, financial condition, and results of operations may be materially and adversely affected.

Failure to renew our current Ocean Transportation Intermediary (“OTI”) License or any delay in doing so could have a material adverse impact on our operations.

We depend on our OTI license to maintain our NVOCC status and maintain our logistics operations. We intend to renew the license before it expires on May 31, 2027; however, there is no guarantee that we will obtain such renewal in a timely manner. Delays or complications in the renewal process may arise due to regulatory changes, unexpected administrative hurdles, or additional requirements imposed by the licensing authority. If we fail to renew such license before the current term ends, or if any delays happen, we may be compelled to temporarily suspend our logistics business. Such an interruption could lead to substantial disruptions in our operations and materially and adversely affect our financial condition and results of operations.

Our business, financial condition, and results of operations may be materially and adversely affected if our third-party transportation providers are unable to provide high-quality services to our clients.

As an NVOCC, we rely on partnerships with various ocean carriers to transport goods. If these partners fail to meet the expected standards of service, such as causing damage to goods during transit, introducing significant delivery delays, or handling goods improperly, both their reputation and ours could be adversely affected. Such incidents may undermine our customers’ confidence in our ability to provide reliable logistics services, which in turn could have a material and adverse effect on our business and financial condition, and results of operations.

Our business relies on a few customers each accounting for more than 10% of our total purchases, and interruption in any of their operations will have an adverse effect on our business, financial condition, and results of operations.

During the years ended December 31, 2024 and 2023, we derived most of our revenue from a few customers. For the year ended December 31, 2024, our two largest clients accounted 87.7% and 12.3% of our total revenue, respectively. For the year ended

16

December 31, 2023, our three largest clients accounted for 53.2%, 25.5%, and 20.2% of our total revenue, respectively. We can lose a major customer due to a variety of factors, including our inability to provide satisfying logistics and warehousing services. We cannot guarantee that we will continue to maintain business cooperation with these major customers at the same level or at all. Some of these major customers are engaged in the parallel-import vehicle business with us, a business we have discontinued. If any significant customer terminates its relationship with us, or if we are unable to find replacements for those who no longer work with us due to our business strategy shift, our business, financial condition, and results of operations could be materially and adversely affected.

We started providing our logistics and warehousing services in February 2024; we may not be successful in this new line of business, which may adversely affect our business, financial condition, and results of operations.

We started providing our own logistics and warehousing services in February 2024 after completing the acquisition of Edward. We have a relatively limited operating history and experience regarding these new services, and we may encounter difficulties as we advance our business operations, such as in marketing, selling, and maintaining our logistics and warehousing systems, and keeping pace with new technological trends and advances in the logistics and warehousing management.

The logistics and warehousing industry is highly competitive. See “—Economic, Political, and Market Risks—We are in the competitive logistics and warehousing industry, and we may not be able to compete successfully against existing or new competitors, which could reduce our market share and adversely affect our competitive position and financial performance.” We may develop an online platform to facilitate our logistics and warehousing services, enabling us to automate and digitalize key steps of supply chain for our customers. These efforts, however, are costly and time-consuming, and may divert our management’s attention. There can be no guarantee that these efforts will be successful and generate the expected return.

We have primarily funded our working capital needs from financing activities historically, and there is no assurance that we will always maintain positive cash flow in the near future or at all.

As of December 31, 2024 and 2023, we had working capital of approximately $10.2 million and $7.5 million, respectively. As of the date of this annual report, we have funded our working capital needs primarily from financing activities. Given that our logistics and warehousing business typically requires significant amounts of working capital, there is no assurance that we will always maintain positive cash flow in the near future or at all, as we expect to continually expand our logistics and warehousing business. Failure to maintain positive cash flow for the near term may adversely affect our ability to raise needed capital for our business on reasonable terms, diminish customer willingness to enter into transactions with us, and have other adverse effects that may decrease our long-term viability.

Our business and results of operations may be harmed by the misconduct of authorized employees that have access to assets of our Company such as inventory, bank accounts, credit cards, and confidential information.

During the course of our business operations, some of our employees have access to certain valuable assets of our Company, such as cargo inventory, bank accounts, and confidential information. In the event of misconduct by such authorized employees, our Company could suffer significant losses. Employee misconduct may include misappropriating cargo inventory or bank accounts, falsifying inventory records or bank accounts, improper use or disclosure of confidential information to the public or our competitors, and failure to comply with our code of conduct or other policies or with federal or state laws or regulations regarding the use and safeguarding of classified or other protected information, import-export controls, and any other applicable laws or regulations. Although we have implemented policies, procedures, and controls to prevent and detect these activities, these precautions may not prevent all intentional or negligent misconduct, and as a result, we could face unknown risks or losses. Furthermore, such unethical, unprofessional, or even criminal behavior by employees could damage our reputation, result in fines, penalties, restitution, or other damages, and lead to the loss of current and future customers, all of which would adversely affect our business, financial condition, and results of operations.

Our insurance does not fully cover all of our operational risks, and changes in the cost of insurance or the availability of insurance could materially increase our insurance costs or result in a decrease in our insurance coverage.

We currently have insurance on our real property, vehicles, and personal property, general liability insurance, workers compensation, and employer liability insurance. In certain instances, our insurance may not fully cover an insured loss depending on the magnitude and nature of the claim. Additionally, changes in the cost of insurance or the availability of insurance in the future could substantially

17

increase our costs to maintain our current level of coverage or could cause us to reduce our insurance coverage and increase the portion of our risks that we self-insure.

Any negative publicity about us, our products and services, and our management may materially and adversely affect our reputation and business.

We may from time to time receive negative publicity about us, our management, or our business. Certain of such negative publicity may be the result of malicious harassment or unfair competitive acts by third parties. We may even be subject to government or regulatory investigations as a result of such third-party conduct and may be required to spend significant time and incur substantial costs to defend ourselves against such third-party conduct, and we may not be able to conclusively refute each of the allegations within a reasonable period of time, or at all. Harm to our reputation and confidence of our customers can also arise for other reasons, including misconduct of our employees or any third-party business partners with whom we conduct business, including purchasing agents and logistics service providers. Our reputation may be materially and adversely affected as a result of any negative publicity, which in turn may cause us to lose market share, customers, industry partners, and other business partnerships.

Cybersecurity incidents could disrupt our business operations, result in the loss of critical and confidential information, adversely impact our reputation, and harm our business.

Cybersecurity threats and incidents directed at us could range from uncoordinated individual attempts to gain unauthorized access to information technology systems to sophisticated and targeted measures aimed at disrupting business or gathering personal data of customers. In the ordinary course of our business, we collect and store business information about our customers such as their names, addresses, and business licenses in Google Drive, a file storage platform developed by Google. The systems of third-party providers, such as Google, may experience material interruptions or failures due to a variety of events beyond our control. See “—We may experience operational system failures or interruptions that could materially harm our ability to conduct our operations.”