UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________

FORM 10-K

______________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31, 2023

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number: 001-41603

______________________

(Exact name of registrant as specified in its charter)

______________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

(406 ) 813-0079

(Registrant’s telephone number, including area code)

______________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbols | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

______________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. (See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act).

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

☒ | ☒ | |||||||||||||

☒ | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of Common Stock held by non-affiliates on June 30, 2023, was approximately $38.3 million.

As of March 15, 2024, there were 44,842,587 shares of Common Stock, $0.0001 par value, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the 2024 Annual Meeting of Stockholder, to be filed no later than 120 days after the end of the fiscal year to which this Annual Report on Form 10-K relates, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| Page | |||||

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws. Statements that are not historical facts, including statements about the beliefs and expectations of Bridger Aerospace Group Holdings, Inc. (the “Company,” “Bridger,” “we” or “us”), are forward-looking statements, including for purposes of the safe harbor provisions under the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “forecast,” “predict,” “poised,” “positioned,” “potential,” “seem,” “seek,” “future,” “outlook,” “target,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters, but the absence of these words does not mean that a statement is not forward-looking. These forward-looking statements include, but are not limited to, (1) anticipated expansion of Bridger’s operations and increased deployment of Bridger’s aircraft fleet, including references to Bridger’s acquisition of and/or right to use the four Super Scoopers from the Spanish government, including the expected closing timings thereof, the anticipated benefits therefrom, and the ultimate structure of such acquisitions and/or right to use arrangements; (2) Bridger’s business and growth plans and future financial performance; (3) current and future demand for aerial firefighting services, including the duration or severity of any domestic or international wildfire seasons; (4) the magnitude, timing, and benefits from any cost reduction actions; (5) Bridger’s exploration of, need for, or completion of any future financings; and (6) anticipated investments in additional aircraft, capital resources, and research and development and the effect of these investments. These statements are based on various assumptions and estimates, whether or not identified in this Annual Report on Form 10-K, and on the current expectations of Bridger’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of Bridger. These forward-looking statements are subject to a number of risks and uncertainties, including: Bridger’s ability to identify and effectively implement any current or future anticipated cost reductions, including any resulting impacts to Bridger’s business and operations therefrom; the duration or severity of any domestic or international wildfire seasons; changes in domestic and foreign business, market, financial, political and legal conditions; Bridger’s failure to realize the anticipated benefits of any acquisitions; Bridger’s successful integration of any aircraft (including achievement of synergies and cost reductions); Bridger’s ability to successfully and timely develop, sell and expand its services, and otherwise implement its growth strategy; risks relating to Bridger’s operations and business, including information technology and cybersecurity risks, loss of requisite licenses, flight safety risks, loss of key customers and deterioration in relationships between Bridger and its employees; risks related to increased competition; risks relating to potential disruption of current plans, operations and infrastructure of Bridger, including as a result of the consummation of any acquisition; risks that Bridger is unable to secure or protect its intellectual property; risks that Bridger experiences difficulties managing its growth and expanding operations; Bridger’s ability to compete with existing or new companies that could cause downward pressure on prices, fewer customer orders, reduced margins, the inability to take advantage of new business opportunities, and the loss of market share; the ability to successfully select, execute or integrate future acquisitions into Bridger’s business, which could result in material adverse effects to operations and financial conditions; and those factors discussed in the section of this Annual Report on Form 10-K entitled “Risk Factors” contained in this Annual Report on Form 10-K. If any of these risks materialize or Bridger management’s assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. The risks and uncertainties above are not exhaustive, and there may be additional risks that Bridger presently does not know or that Bridger currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect Bridger’s expectations, plans or forecasts of future events and views as of the date of this Annual Report on Form 10-K. Bridger anticipates that subsequent events and developments will cause Bridger’s assessments to change. However, while Bridger may elect to update these forward-looking statements at some point in the future, Bridger specifically disclaims any obligation to do so. These forward-looking statements should not be relied upon as representing Bridger’s assessments as of any date subsequent to the date of this Annual Report on Form 10-K. Accordingly, undue reliance should not be placed upon the forward-looking statements contained in this Annual Report on Form 10-K.

ii

PART I

ITEM 1. BUSINESS.

Business Overview

Bridger provides aerial wildfire surveillance, relief and suppression and aerial firefighting services using next-generation technology and environmentally friendly and sustainable firefighting methods primarily throughout the United States. Our mission is to save lives, property and habitats threatened by wildfires, leveraging our high-quality team, specialized aircraft and innovative use of technology and data. We are meeting an underserved and growing need for next-generation full-service aerial firefighting platforms.

Bridger was founded by our Chief Executive Officer and former Navy SEAL officer Timothy Sheehy, in Bozeman, Montana in 2014 with one aircraft and a vision to build a global enterprise to fight wildfires. Bridger has since grown into a full-spectrum aerial firefighting service provider in the U.S. and in the field of aerial wildfire management, offering technology and services to provide front-line firefighters and fire suppression decision-makers access to key fire data in order to effectively combat wildfires.

On January 24, 2023, Bridger completed a reverse recapitalization (the “Reverse Recapitalization”) with Jack Creek Investment Corp (“JCIC”). As a result of the Reverse Recapitalization, Bridger and its subsidiaries prior to the consummation of the Reverse Recapitalization (“Legacy Bridger”) and JCIC each became wholly-owned subsidiaries of the Company.

As of December 31, 2023, the Company has a team of 148 employees and has developed an ecosystem of solutions, services and technologies supporting firefighting ground crews and the public.

The areas in which human development meets or intermingles with undeveloped wildland and vegetative fuels that are both fire-dependent and fire-prone (“wildland-urban interface” or “WUI”) have grown by more than 179,000 square kilometers in the U.S. from 1990 to 2020, according to a 2023 article by the United States Forest Service (the “USFS” and the “USFS WUI Increase Article”). WUI areas, which comprise 9.4% of the U.S. land area, now include nearly one-third of all residences, according to the USFS WUI Increase Article. At the same time, the annual acres burned per fire between 1985 and 2022 have increased by more than three-fold according to data published by the National Interagency Fire Center (the “NIFC”). As the WUI areas continue to grow and wildfires grow larger, more aggressive firefighting strategies are necessary to ensure public safety. Additionally, data published by the NIFC shows that the total number of U.S. acres burned annually has increased by more than two-fold from 1985 to 2022.

These trends have led to a response by the U.S. federal government to increase spending on fire suppression since 1985 with a compound annual growth rate of 7.6% to $3.5 billion in 2022, according to the NIFC Suppression Costs Data. Even with this increased spending and demand, unfulfilled requests for fixed wing aircraft for aerial firefighting grew at a compound annual growth rate of 4.7% between 2002 and 2022, with 654 unfulfilled requests in 2022, according to National Interagency Coordination Center (“NICC”).

Bridger’s management estimates that aerial suppression spend represented approximately 42.7% of an estimated $21.9 billion firefighting market (defined as the sum of air-based suppression, ground, and fire data, aerial imagery-related, and emergency mobile application markets) globally in 2021. There is a rapidly growing global need for fire suppression assets, and Bridger’s management believes that a shift away from ground services to air-based suppression has already commenced. The market is anticipated to continue to expand as wildfires rage across Europe and the U.S.

Business Description

Our portfolio is organized across two core offerings:

Fire Suppression: Consists of deploying specialized Viking CL-415EAF (“Super Scooper”) aircraft to drop large amounts of water quickly and directly on wildfires.

Aerial Surveillance: Consists of providing aerial surveillance via manned (“Air Attack”) aircraft for fire suppression aircraft over an incident and providing tactical coordination with the incident commander.

1

Fire Suppression

We provide direct fire suppression aerial firefighting support for ground crews by operating the Super Scoopers. Aerial fire suppression is provided in conjunction with traditional ground firefighting approaches, and specialized aircraft drop high volumes of water directly onto active wildfires. Because wildfires largely occur within close proximity to a major water source, leveraging readily available resources is more time- and fuel-efficient in combating wildfires when time is of the essence. The Super Scoopers allow for rapid delivery of water strikes to extinguish wildfires, particularly when deployed in tandem or larger groups to allow for continuous water delivery as aircraft return to the water source.

Aerial Surveillance

Wildfires can spread quickly and change course in an instant. Our aerial surveillance services provide decision-makers rapid, current intelligence from useful aerial vantage points, giving them access to key information to support more effective deployment of ground firefighters and improved safety for the public at large. Our aerial surveillance services leverage Air Attack aircraft.

Our Air Attack fleet comprises twelve aircraft, including four Twin Commanders (“Twin Commanders”), four Daher Kodiak 100s (“Daher Kodiaks”), three Pilatus PC-12 (“Pilatus”) and one DeHaviland Twin Otter (“Twin Otter”). We have seven years of experience in providing USFS Type 1 Air Tactical Group Supervisors (“ATGS”), and the aerial platform to relay the necessary information, to ground-based Interagency Incident Commanders (“Incident Commanders”), who are responsible for the overall management of the wildfire and determine how resources are deployed. We are one of the largest ATGS platform providers in the U.S. and have contracts covering 100% of the U.S.

Our Aircraft

We deploy modern technology to track and attack wildfires and have an expansive fleet of specialized firefighting aircraft stationed in three hangars at the Bozeman Yellowstone International Airport in Belgrade, Montana. Our aircraft form the basis of our service offerings and, as such, we strive to continually invest in advancements in aerial firefighting platforms. We continually invest in our fleet to expand our capabilities while assessing opportunities to acquire next-generation firefighting assets to combat the rising threat of wildfires.

We currently operate an aircraft fleet of 18 planes, comprised of the following:

•Six Super Scoopers

•Four Twin Commanders

•Four Daher Kodiaks

•Three Pilatus (one owned and two leased)

•One Twin Otter (leased)

Super Scooper Fleet

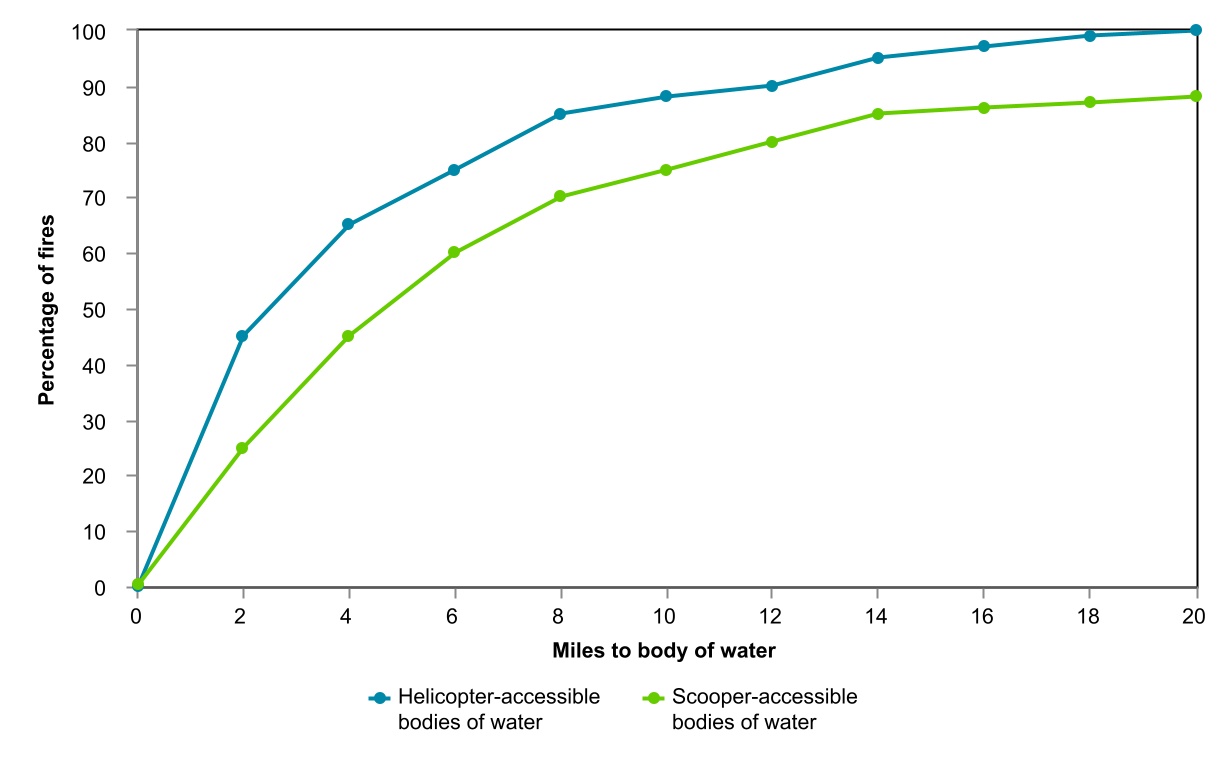

The Super Scooper is the only aircraft designed and built to fight fires and can fly more aggressively in extreme terrains than all other aircraft with equal or greater water capacity. The Super Scooper is an amphibious aircraft that skims the surface of a body of water to scoop water into onboard tanks to drop on a fire. The specific design of the Super Scooper allows for an aggressive low-altitude flight profile, which enables pilots to deliver their drops with more precision, hitting the fire harder and extinguishing it faster. Super Scoopers can scoop up to 1,412 gallons of water in approximately 12 seconds, and with 90% of wildfires within 20 miles of a major water source (see graph below), Super Scoopers provide an extremely effective tool to economically and expeditiously deliver water to a fire without having to return to an airport to refill the water tanks. With a water source within a five-mile radius, the Super Scooper can drop on its target up to every seven minutes for a total of approximately 35 drops, or 50,000 gallons of water, before needing to refuel. As a result of our operations of these Super Scooper assets, in conjunction with our Air Attack fleet, we believe that we are one of the most full-spectrum aerial fire service providers in North America.

2

Source: 2012 Air Attack Against Wildfire Study by the Rand Homeland Security and Defense Center.

The Super Scooper aircraft has an impeccable safety record, direct support from the original equipment manufacturer (the “OEM”), short take-off and landing capabilities (“STOL”) and a multi-crew flight deck. The Super Scooper has a cruising speed of 207 miles per hour. Additionally, the Super Scooper is a highly efficient aircraft when fighting wildland fires and has the ability to drop a higher volume of liquid than retardant-dropping fixed-wing aircraft over the same amount of time due to its ability to gather water from nearby bodies of water.

Our Super Scoopers have an immaculate safety record, as we have never been assessed with any safety violations and/or citations, nor have any of our aircraft ever been involved in any crashes or serious injuries. We have also adopted a safety management system (“SMS”) designed to reduce the likelihood of safety-related issues arising in the course of our overall operations. The SMS program has been audited by both the Federal Aviation Administration (the “FAA”) and the USFS.

Furthermore, the Super Scooper has the ability to operate from smaller airports with runways as short as 2,500 feet in length while larger jet-powered aerial firefighting aircraft often need a runway of at least 4,000 feet in length. The Super Scooper is capable of scooping water in 12 seconds from bodies of water of 4,900 feet or more in length and can empty the water load in 3 seconds in one drop or split the drop into two. The Super Scooper’s water tank capacity is shown in the table below:

| Volume | Weight | |||||||||||||||||||||||||||||||

| Liters | Imp Gal | U.S. Gal | Kg | Lbs | ||||||||||||||||||||||||||||

Each tank | 2,673 | 588 | 706 | 2,722 | 6,000 | |||||||||||||||||||||||||||

Total both tanks | 5,346 | 1,176 | 1,412 | 5,443 | 12,000 | |||||||||||||||||||||||||||

3

A summary graphic of the Super Scooper and its efficiency in collecting water is provided below.

Source: United States Department of Agriculture Amphibious Water Scooper Aircraft Operations Plan 2016.

Air Attack Fleet

Our Air Attack fleet provides high level situational awareness of fire growth, ground firefighting elements, other aircraft within the fire traffic area, and changing weather conditions to Incident Commanders. Each aircraft is outfitted with a broad suite of communication technologies. The Daher Kodiaks and Pilatus, the newest additions to our Air Attack fleet, are particularly renowned for their rugged build and versatility in landing on challenging terrain which is an asset given the inconsistent and harsh flying conditions that challenge aerial firefighting. Our Air Attack fleet is suitable for STOL, allowing for deployment in a greater range of scenarios. A high level of reliability allows the aircraft to be serviced and available for contract for more days, with fewer unscheduled in-field maintenance events. Above active wildfires, the aircraft can maintain the fuel efficiency required to loiter for four to seven hours with slow and stable flight characteristics, offering the ATGS greater visibility.

Key Market Drivers and Opportunities

There are several key market drivers and opportunities for our business, including:

Longer and more severe fire seasons drive demand for fire suppression and aerial surveillance services

NIFC Suppression Costs Data supports that the acreage burned in the U.S. has increased over time. While there is variability in the acreage burned in any given year, the annual average of 7.1 million acres burned from 2000 to 2022 has more than doubled the annual average acreage burned from 1985 to 1999 of 3.2 million.

While the North American wildfire off-season is typically between October and May, fires are starting earlier in the spring and lasting deeper into the fall according to the United States Environmental Protection Agency (the “EPA”). The U.S. fire season is also lengthening on a consistent basis – according to Climate Central, the U.S. fire season is on average 105 days longer than it was in 1970. Climate Central also reported that the average number of large fires (greater than 1,000 acres) burning each year had tripled between the period of the 1970s to the 2010s, and the acres burned by such fires showed a six-fold increase in the 2010s compared to the 1970s. Climate Central attributes the lengthening wildfire season to factors including warmer springs, longer summer dry seasons and drier soils and vegetation, with climate change threatening to increase the extent and severity of these fires. The United States national fire preparedness level has increased over time. The five preparedness levels range from the lowest (1) to the highest (5); and are dictated by fuel and weather conditions, fire activity and fire suppression resource availability throughout the country. Level 5 represents that several geographic areas are experiencing large, complex wildfire incidents, which have the potential to exhaust national wildland firefighting resources, while Level 1 represents that there is very minimal fire activity. According to data provided by the NIFC, the average U.S. fire preparedness level during the main wildfire season (June through September) has increased over time by almost half of a level: during the past five years (2019 – 2023) the average U.S. fire preparedness level was 3.09, while the average U.S. fire preparedness level since 1990 was 2.80.

4

Federal and state funding for wildfire control

National funding for wildfire management is appropriated by the U.S. Congress (“Congress”) and each state pays for wildland firefighting slightly differently. While fire suppression activities on wildlands in the U.S. are financed through federal funds, budget-making processes may restrict the amount allocated. According to the NIFC Suppression Costs Data, the average annual federal government fire suppression spending was $3.0 billion for the five-year period from 2018 to 2022, an increase of 45%, compared to $2.1 billion of average annual spending for the previous five-year period from 2013 to 2017. The funding is allocated to the Department of the Interior (the “DOI”) and the USFS. Our company then enters into short, medium and long-term contracts with federal agencies during the firefighting season. On the state level, we are generally seeing significant increases in several state governments and private entities who are preparing themselves for the new fire reality. For example, in July 2023, the federal government announced the allocation of $185.0 million to support wildland fire management nationwide in 2023 and to assist land managers in planning for wildfire management activities in fiscal year 2024. This investment builds on $278.0 million, announced in March 2023 and December 2022, already allocated in 2023. In 2021, Washington State invested $328.0 million over the five following years to fight wildfires. While this level of commitment is unique, it is reflective of the increased awareness across many levels of government and private entities that wildfire risk has entered a new era of severity.

Given our long-standing customer relationships with governmental bodies, we have an opportunity to fulfill this increased demand for firefighting services driven by longer and more severe fire seasons. We view the increased demand as a means to further government agency ties and to capitalize on new aircraft investments.

Increased demand and limited supply of purpose-built suppression aircraft

According to the reports published by the NICC, demand for Type 3 multi-engine airtankers, which includes our Super Scooper aircraft, increased by over 56% for the two-year period of 2021 and 2022 compared to the prior two-year period of 2019 and 2020. The Wildland Fire Reports showed that the increase in demand led to a higher percentage of unfulfilled requests, and in 2022, 34.9% of Type 3 multi-engine airtankers requests were unfulfilled compared to 8.9% in 2020.

Super Scoopers are multi-engine airtankers built specifically for aerial firefighting. They are highly effective at fighting fires and have historically been owned and operated by foreign governments throughout Europe (there are approximately 40 amphibious scooping aircraft owned by France, Greece, Italy and Spain) and as a result, used amphibious scooping aircraft are difficult to locate and obtain in the United States. We are an original customer for Longview Aviation Services Inc.’s (“LAS”) launch of their Super Scooper CL-415EAF (Enhanced Aerial Firefighter) Program. LAS has only manufactured a limited number of Super Scoopers available for sale between 2020 and 2025, and pursuant to our purchase agreement with LAS and Viking, dated April 13, 2018 (as amended and supplemented from time to time, the “LAS Purchase Agreement”), which has been amended numerous times to add additional planes and upgrades, we agreed to purchase six of the limited number of Super Scoopers. On February 17, 2023, we received our sixth Super Scooper, which allows greater deployment of the Bridger aircraft fleet across the U.S. As we are a long-standing customer of LAS, and as LAS develops their next generation of aerial firefighting solutions, our continuous feedback informs advancements in firefighting technology.

On November 17, 2023, the Company entered into a series of agreements with MAB Funding, LLC (“MAB”) and its subsidiary designed to facilitate the purchase and return to service of four Canadair CL-215T Amphibious Aircraft (the “Spanish Scoopers”) originally awarded to the Company in September 2023 via a public tender process from the Government of Spain for €40.3 million. The terms of the agreements provide that the Company will manage the return to service upgrades of the Spanish Scoopers while they are owned and funded by MAB. The Company has the right, but not the obligation, to acquire each plane as it is ready to be contracted and returned to service. The Company plans to acquire the Spanish Scoopers in a sequential manner as they are modified and subsequently contracted for service.

Given the limited supply of purpose-built multi-engine airtankers, upkeep and maintenance of existing aircraft is vital to minimize lapses in firefighting services occurring during wildfire season and to reduce the impact of any disruptions that occur. The Super Scooper is the only aerial fire suppression aircraft with factory OEM support which aids in reducing downtime.

5

Our Competitive Strengths

Full spectrum of aerial firefighting services

We provide full-spectrum aerial firefighting services, offering both fire suppression and aerial surveillance services in the U.S. and internationally. We emphasize continued investment in new aerial surveillance and aerial fire suppression aircraft. Our aerial surveillance fleet has evolved since our inception from a single aircraft and pilot to the fleet operated today. The diversity of our service offerings affords customers the opportunity to select the appropriate services for their specific needs.

Purpose-built aircraft that can drop higher volumes of water

Our six Super Scooper aircraft are the latest model in the LAS production line and feature enhanced industry technology. Viking, a subsidiary of LAS, purchased the type certificate and is the OEM for the design of all the CL-215 and CL-415 models from Bombardier Aerospace. LAS then made significant improvements and introduced the Super Scooper, which includes the following improvements over the CL-415:

•Higher cruising speed;

•Improved air safety;

•Latest-generation technological reliability;

•New avionics and instrumentation;

•More accurate water discharge technology;

•Suitability for mountainous terrain;

•STOL on asphalt, gravel and water;

•Lower speed during water-bombing (low and slow flight);

•Improved operational efficiency; and

•Structural integrity.

The Super Scooper leverages modern turbine engines to deliver superior high-altitude performance. The Super Scooper is able to reload in under a minute, compared to a reload time of approximately 30 minutes to one hour, depending on base capabilities, for other air tankers enabling the Super Scooper to make more drops in the same amount of time. The Super Scooper can drop approximately 50,000 gallons before requiring refueling, while the largest tanker in the market can only drop 30,000 gallons of retardant before needing to refuel and reload retardant. The Super Scooper aircraft allow for rapid delivery of water strikes to extinguish wildfires, particularly when deployed in tandem or larger groups to allow for continuous water-delivery as aircraft return to the water source.

Highly-skilled crew of pilots and maintenance personnel

As of December 31, 2023, we have 15 captains on staff as part of the Super Scooper flight crew. Each captain has thousands of hours of flight time in the Super Scooper conducting firefighting operations. All flight crew have a minimum of four years of aerial firefighting experience. Recurrent training for all flight crew is required in a Level D full motion flight simulator.

Each of our pilots attends annual and recurrent training specific to the aircraft they operate and to meet our standards of safety and standard operating procedures. Each pilot that flies an aircraft on contract for a government agency receives a certification card on an annual basis that validates they are qualified by the government to safely operate the aircraft while on contract.

As of December 31, 2023, we have 10 crew chiefs on staff as part of the Super Scooper maintenance crew. Each crew chief has thousands of hours maintaining aircraft in the Viking family and are familiar with firefighting operations. Factory training is mandatory for all of the maintenance team specific to the aircraft and components they maintain. They are also required to complete company-specific training courses regarding safety, standard operating procedures and systems in which they track and sign-off on maintenance logs.

6

Long-standing client relationships

We have provided aerial firefighting services since 2015 to government agencies, including the USFS, California Department of Forestry and Fire Protection (“Cal Fire”) and multiple other state governments. We have been praised as an industry leader, specifically by the USFS, with regards to the SMS program and have been recommended by the USFS as a model for safe aircraft operations. Currently, we maintain active contracts with multiple federal agencies and the state governments of many high wildfire risk states. Historically, we have experienced a 100% renewal rate on our federal and state contracts. We bid upon and were awarded a USFS multi-year contract beginning with the 2021 fire season through the beginning of the 2025 fire season for the use of our Super Scooper planes.

Our relationship with the USFS involves three material service agreements: Contract No. 1202SA21T9009, dated as of June 3, 2021 (“Call-When-Needed Water Scooper Contract”), Contract No. 12024B19C9025, dated as of May 15, 2019 (“Exclusive Use Light Fixed Wing Contract”) and Contract No. 1202SA21G5100, dated as of February 22, 2021 (“Call-When-Needed Light Fixed Wing Contract”). Under the Call-When-Needed Water Scooper Contract, we provide Super Scooper aircraft services for wildland firefighting on a national basis for a period of four years from June 3, 2021. We generate revenue under the Call-When-Needed Water Scooper Contract from task orders placed by the USFS. Under the terms of the Call-When-Needed Water Scooper Contract, the USFS reserves the right to terminate the Call-When-Needed Water Scooper Contract, or any part thereof, for its sole convenience or in the event of any default by us. Under the Exclusive Use Light Fixed Wing Contract, we provide light fixed wing aircraft firefighting services on an exclusive use basis for the Northern, Rocky Mountain, Southwestern, Intermountain and Pacific Southwest regions, as defined by the U.S. Department of Agriculture. The original term of the Exclusive Use Light Fixed Wing Contract was for 12 months from May 15, 2019; however, the contract included an option to extend the contract for four additional periods of one year each, and the USFS has exercised its annual option to extend the contract for 12-month periods on each of March 18, 2020, April, 21, 2021, April 18, 2022, and March 14, 2023. We generate revenue under the Exclusive Use Light Fixed Wing Contract by providing guaranteed availability of our services for 120 calendar days per year, with different rates charged for standby hours and flight hours. Under the terms of the Exclusive Use Light Fixed Wing Contract, the USFS reserves the right to terminate the Exclusive Use Light Fixed Wing Contract, or any part thereof, for its sole convenience or in the event of any default by us. Under the Call-When-Needed Light Fixed Wing Contract, we provide light fixed wing aircraft firefighting services, on a call-when-needed basis, for the air tactical group supervision mission on behalf of the Northern Region, as defined by the USFS. The term of the Call-When-Needed Light Fixed Wing Contract is for a period of four years. We generate revenue under the Call-When-Needed Light Fixed Wing Contract by providing our services when called upon by the USFS, if available at time of call, with different rates charged for standby hours and flight hours. Under the terms of the Call-When- Needed Light Fixed Wing Contract, the USFS reserves the right to terminate the Call-When-Needed Light Fixed Wing Contract, or any part thereof, for its sole convenience or in the event of any default by us.

In 2023, the USFS discontinued the future use of multiple discrete contracts and instead consolidated its contracts into a National Multiple Award Task Order Contract (“MATOC”). Under this contract, it can award task orders for exclusive use aircraft instead of awarding multiple contracts. All of our light fixed-wing Air Attack aircraft and the multi-mission Pilatus are available under the MATOC subsequent to the expiration of the Exclusive Use Light Fixed Wing Contract in May 2024 .

Our Growth Strategy

Acquire and deploy additional aircraft to meet increased demand

We are an original customer for LAS’s launch of its Super Scooper CL-415EAF Program. There are approximately 40 amphibious scooping aircraft owned by France, Greece, Italy and Spain and as a result, used amphibious scooping aircraft are difficult to locate and obtain. LAS has only made a limited number available for sale between 2020 and 2025, of which the Company has purchased six.

Expanding our services

Fire Monitoring Technology: With roughly 70,000 wildfires occurring each year in the U.S. (according to the NIFC Suppression Costs Data), news feeds are saturated with reports of wildfires that have grown quickly and are out of control. Current consolidated fire data is controlled by wildfire agencies with limited to no access publicly available. On September 14, 2023, we acquired Ignis Technologies (“Ignis”) to develop a pioneering mobile and web platform that elevates firefighter situational awareness, creates an interoperable common operating picture across firefighting units, and produces real time, high value data to help fire organizations better manage wildfire risk.

7

Maintenance, Repair, Overhaul: We have an experienced and well-trained crew of maintenance professionals. Maintenance personnel and their maintenance support staff are current on all general aviation standards and requirements and are specifically trained to service our fleet of aircraft. We ensure our maintenance team has all the necessary equipment needed to exceed FAA maintenance standards and maintain USFS and DOI contract aircraft requirements. We are a FAA Certified Part 145 Repair Station offering in-house airframe and avionics repair capabilities for our aerial firefighting fleet. In April 2022, our Part 145 Certified Repair Station was awarded an ISO 9110, certification which is one of the highest standards in a repair organization recognized by the FAA. This certification was completed by the British Standards Institution, recognized as an industry leader in quality management systems.

Domestic and international expansion

We are committed to increasing our market share and service offering domestically and internationally. Given our competitive strengths, we believe we are well-positioned to take advantage of the growth in domestic demand for fire safety and environmental awareness. We currently have contracts in place with the USFS, the DOI, Bureau of Indian Affairs, Bureau of Land Management, Washington State Department of Natural Resources, Alaska Division of Forestry, Cal Fire, Colorado Department of Public Safety Division of Fire Prevention and Control, Idaho Department of Lands, Minnesota Department of Natural Resources, Montana Department of Natural Resources and Conservation, Nevada Department of Conservation and Natural Resources and Oregon Department of Forestry.

We intend to penetrate certain additional domestic markets through leveraging existing relationships and building local market teams. We have established this historically by maintaining relationships in the field with customers, gathering near real-time feedback to improve operations, as well as holding regular feedback sessions to incorporate points of improvement and planning for subsequent years.

We are exploring the possibility of operating internationally during the North American wildfire off-season, which generally occurs between October and May. We seek to become a global entity that provides aerial firefighting services worldwide. Our goal is to bring the Super Scooper to Europe through the agreement entered into for the Spanish Scoopers in November 2023. Additionally, we plan to bring the Super Scooper to Asia and/or South America in the future and to demonstrate the platform’s effectiveness. Currently, Super Scoopers are either not utilized on wildland fires in these areas or are not operated in a contractor-owned, contractor-operated business model. We plan to fill an underserved need to provide an alternative solution to aging and obsolete government-owned, government-operated fleets.

Pursuing Opportunistic Mergers & Acquisitions (“M&A”)

We intend to continue to evaluate M&A opportunities to expand our fleet, add new geographies or add additional services. Consistent with this strategy, we regularly evaluate potential acquisition opportunities, including ones that would be significant to us. We cannot predict the timing of any contemplated transactions, and none are currently probable.

Seasonality

Our operating results are impacted by seasonality. Climate conditions and other factors that may influence our revenues may vary each quarter and year. Many of these factors are outside of our control, including but not limited to:

•forest fires tend to have a higher occurrence during the summer months and during times of drought, but are ultimately unpredictable;

•climate change and changes in global temperatures occur over time;

•unexpected weather patterns, natural disasters or other events that increase or decrease the rate or intensity of wildfires or impair our ability to perform firefighting services; and

•changes in governmental regulations or in the status of our regulatory approvals or applications.

Historically, the demand for our services has been higher in the second and third quarters of each fiscal year due to the timing and duration of the North American wildfire season. Consequently, revenues, expenses, and operating cash flows from our services are generated mostly in the second and third quarters of our fiscal year. However, the seasonal fluctuation in the need to fight wildfires based upon location and the varying intensity of the wildfire season may lead our operating results to fluctuate significantly from quarter to quarter and year to year.

8

Our Customers

Our high-performing aircraft, including the Super Scooper, and full-service support platform have allowed us to enter into contracts with U.S. federal, state and local governmental entities and focus on growth while building additional services to map and analyze fire boundaries. Currently, we are engaged in short, medium and long-term contracts with multiple federal agencies such as the USFS and DOI and the state governments of many of the states most endangered by wildfires. Automatically renewing contracts with governmental entities provide stable revenue streams, allowing us to innovate in the aerial firefighting industry and diversify offerings to customers. We bid upon and were awarded a contract with the USFS for use of our Super Scooper aircraft, beginning in 2021 into 2025.

While a majority of our existing contracts are for a one-year base term, we enter into short, medium and long-term contracts with customers, primarily with the aforementioned government agencies during the firefighting season, to deploy aerial fire management assets. Contracts are based on either a Call-When-Needed (“CWN”) or Exclusive Use (“EU”) basis.

Rates established for CWN contracts are generally higher based on a customer's need for urgent or unanticipated deployment of our aerial fire management assets compared to EU contract rates which are generally more competitive based on the security of the revenue from the contract. Historically, we have experienced a 100% renewal rate on our federal and state contracts.

Facilities

Our headquarters are located in Belgrade, Montana, and our aircraft fleet resides at the Bozeman Yellowstone International Airport. We own three hangars and lease five existing lots at the airport on 20-year and 10-year ground leases.

Our international operations’ headquarters are located in Albacete, Spain. We currently own one hangar and lease one existing lot on a short-term ground lease at the Albacete Airport, where the return to service upgrades for the four Spanish Scoopers are being performed.

Our Competitors

Our primary competition is a private aerial firefighting operator that currently manages four CL-415s, three Type II Dash 8-400ATs and seven Avro RJ85s, which are designed to drop fire retardant. Additionally, from time-to-time we may compete with aerial firefighting companies that drop water from helicopters. However, our management does not view helicopters as a direct threat to our operations because while many helicopters are only able to pursue two-hour missions due to fuel capacity, our Super Scooper aircraft have four-hour fuel capacity.

Our Super Scooper program is not designed to replace the use of aircraft that drop fire retardant on wildfires. Fire retardant is a substance frequently deployed by large air tankers to slow down or stop the spread of fire and is frequently used to create a perimeter or border around a fire. While it is possible for a fire to burn through a fire line created by fire retardant, fire retardant remains a valuable tool in the fight and management of wildfires, and when combined with the deployment of Super Scoopers dropping water, can be effective in managing, controlling and slowing the spread of wildfires.

We believe our ability to compete successfully as an aerial firefighting service will depend on a number of factors, which may change in the future due to increased competition, including the price of our offerings, consumer confidence in the safety and efficacy of our offerings and consumer satisfaction for the solutions we offer. Additionally, we may compete with other aerial firefighting operators for federal and state budget dollars, and for various governmental service programs that support aerial firefighting programs.

Our Environmental Impact

According to an article on Climate Change Indicators by the United States Environmental Protection Agency, multiple studies have found that “climate change has already led to an increase in wildfire season length, wildfire frequency and burned area”, “climate change threatens to increase the frequency, extent and severity of fires through increased temperatures and drought” and wildfires release a significant amount of carbon emissions each year.

Amid raging wildfires and changing climate, we use sustainable and environmentally friendly firefighting methods. By sourcing water near the fire for our fire suppression services, we minimize harm to the local water system by keeping water in the local ecology and reducing flight time between scoops and drops. Our mission is to save lives, property, and habitats through our world-class team, specialized aircraft, and innovative use of technology and data.

9

Human Capital

Our employees are critical to our success. On December 31, 2023, we had 148 employees. We have high selection standards, recruiting individuals with specific technical skills and demonstrated ability to work independently in a wide variety of work environments. Prior to joining our company, many of our employees had prior experience working for a wide variety of reputed research, commercial and military aerospace and non-aerospace organizations. As a company founded by veterans, we seek to employ qualified veterans and draw upon the experiences of their shared military background including their strategic mindset, management skillset and high level of discipline. As of December 31, 2023, approximately one out of seven of our employees is a veteran of the U.S. military.

To date, we have not experienced any work stoppages, and we consider our relationship with our employees to be good. We routinely solicit feedback from our entire employee base and empower individuals by encouraging them to formulate solutions and process improvements no matter the level of role. Accordingly, our voluntary turnover is very low, employee engagement is high, and we have not experienced any interruptions of operations due to labor disagreements. Our employees are not subject to collective bargaining agreements or represented by labor union.

Health and Safety

We are committed to the safety of our employees. We maintain environmental, health and safety policies that seek to promote the operation of our business in a manner that is protective of the health and safety of the public and its employees. Our operations offer several health and welfare programs to employees to promote fitness and wellness and to encourage preventative healthcare. In addition, our employees are offered a confidential employee assistance program that provides professional counseling to employees and their family members. We have a holistic philosophy for our benefits offerings, supporting physical health, mental health, financial health, community support and a wide variety of insurance plans to hedge against uncertain losses (e.g., accident, short term disability, paid leaves, and life insurance).

Employee Trainings

To address the inherently dangerous nature of the job, we adhere to achieving operational excellence and providing our employees with the means to further their development. All of our pilots are given extensive training during the winter months, regardless of tenure or previous experience. The trainings include classroom and online courses, simulators, and in-plane time. We strive to have high industry standards and employ several dedicated pilot and airframe-specific trainers. Routinely, we fund enhanced workforce training in specific technical fields related to those employees’ desires. In one instance, we have had an employee who was hired as a facility cleaner. With further training and investment, the employee became a ground vehicle support manager and is now an aircraft mechanic. We also hire entry level mechanics and train them to obtain their airframe and powerplant certification, which allows them to perform maintenance on any aircraft unsupervised.

In addition to technical training, we invest heavily in leadership and management training as well as some of the most advanced safety training available in our industry. The State of Montana Job Grant program has been a tremendous help to us through our early years by providing state funded training to employees attending schooling to better their position as employees within the State of Montana. Before hiring externally as needs are identified, a careful analysis is done of our current staff to determine if the aptitude and interest is already in our employee base. By prioritizing training and promoting current employees, we enhance employee engagement and cut costs simultaneously.

Employee Retention and Opportunity

We believe that attraction and retention of top talent from a variety of backgrounds is important and we employ policies and procedures to recruit diverse talent as well as policies to ensure pay equality. We have an Equal Employment Opportunity Policy whereby we commit to providing equal employment opportunity, promotion, services, or activities which operates for all qualified employees and applicants without regard to race, color, sex, sexual orientation, gender identity, gender expression, parental status, citizenship status, religion, national origin, disability, veteran status, age, marital status, pregnancy, genetic information or other legally protected status. We drive a culture that understands and respects differences. We rely heavily on recruiting internationally to work on our purpose-built aerial firefighting aircraft and identify the cultural benefits that these individuals bring to our company.

10

Governmental Regulation

Federal Aviation Administration

The regulations, policies and guidance issued by the FAA apply to the use and operation of our aircraft. Operators of aircraft are required to have proper licenses, permits and authorizations from the FAA and comply with the FAA’s insurance requirements for third-party liability and government property. While our aircraft are currently registered with the FAA, in the event of a change in ownership, the FAA license will be updated with current information. In that instance, once any such new vehicle registration applications are filed, the applications will serve as registrations until the FAA issues the new vehicle registrations, which will allow operations to continue during that period.

Failure to comply with the FAA’s aviation or space transportation regulations may result in civil penalties or private lawsuits, or the suspension or revocation of licenses or permits, which would prevent operating our aircraft.

In addition to the FAA, our industry is regulated by multiple federal agencies who, in some cases, act as both customer and regulator. We are proud to have a stellar record of performance both in flight and on the ground with respect to all of our regulatory bodies.

ITEM 1A. RISK FACTORS.

Summary of Risk Factors

Below is a summary of the principal factors that could adversely affect our business, operations and financial results. This summary does not address all of the risks that we face. Additional discussion of the risks summarized in this summary, and other risks that we face (including general risk factors), can be found below following this summary.

Aviation and Firefighting Risks

•Our operation of aircraft involves a degree of inherent risk, and we could suffer losses and adverse publicity stemming from any accident, whether related to us or not, involving aircraft, helicopters, or commercial drones similar to the assets we use in our operations.

•Our business is inherently risky in that it is fighting wildfires which are powerful and unpredictable.

•The unavailability of an aircraft due to loss, mechanical failure, lack of pilots or maintenance personnel, especially one of the Viking Air CL-415EAFs, would result in lower operating revenues for us for a period of time that cannot be determined and would likely be prolonged.

•Our pilots and mechanics are required by contract to meet a minimum standard of operational experience. Finding and employing individuals with the necessary level of experience and certification has required us to hire Canadian personnel in addition to U.S. personnel. Inability to source and hire personnel with appropriate skills and experience would inhibit operations.

•The development of superior alternative firefighting tactics or technology that do not rely on our existing and planned capital assets could reduce demand for our services and result in a material reduction in our revenue and results of operations.

Operations Risks

•A cyber-based attack of our IT systems could disrupt our ability to deliver services to our customers and could lead to increased overhead costs, decreased sales, and harm to our reputation.

•Any failure to offer high-quality aerial firefighting services to customers may harm our relationships with our customers and could adversely affect our reputation, brand, business, financial condition and results of operations.

•We are subject to risks associated with climate change, including the potential increased impacts of severe weather events on our operations and infrastructure, and changes in weather patterns may result in lower demand for our services if such changes result in a reduced risk of wildfires.

•We are highly dependent on our senior management team and other highly skilled personnel with unique skills.

11

Seasonality Risks

•There is a seasonal fluctuation in the need to fight forest fires based upon location and a substantial majority of our revenue is currently concentrated in the Western United States. As a result, our operating results may fluctuate significantly from quarter to quarter and from year to year.

Sales and Customer Risks

•The aerial firefighting industry is expected to grow in the near future and is volatile, and if it does not develop, if it develops slower than we expect, if it develops in a manner that does not require use of our services, if it encounters negative publicity or if our solution does not drive commercial or governmental engagement, the growth of our business will be harmed.

•We depend significantly on government customers, which subjects us to risks including early termination, audits, investigations, sanctions and penalties. We are also subject to regulations applicable to government contractors which increase our operating costs and if we fail to comply, could result in the termination of our contracts with government entities.

•We may be unable to manage our future growth effectively, which could make it difficult to execute our business strategy.

•We rely on a few large customers for a majority of our business, and the loss of any of these customers, significant changes in the prices, marketing allowances or other important terms provided to any of these customers or adverse developments with respect to the financial condition of these customers could materially reduce our net income and operating results.

Supplier Risks

•We rely on a limited number of suppliers for certain raw materials and supplied components. We may not be able to obtain sufficient raw materials or supplied components to meet our maintenance or operating needs or obtain such materials on favorable terms or at all, which could impair our ability to provide our services in a timely manner or increase our costs of services and maintenance.

•There is a limited supply of new CL-415EAF aircraft to purchase, and an inability to purchase additional CL-415EAF aircraft could impede our ability to increase our revenue and net income.

•We currently rely and will continue to rely on third-party partners to provide and store the parts and components required to service and maintain our aircraft, and to supply critical components and systems, which exposes us to a number of risks and uncertainties outside our control.

Financial and Capital Strategy Risks

•We may require substantial additional funding to finance our operations and growth strategy, but adequate additional financing may not be available when we need it, on acceptable terms, or at all, and our ability to pursue equity financings may depend in part, on the market price of our shares of common stock, $0.0001 par value per share (“Common Stock”).

•Our systems, aircraft, technologies and services and related equipment may have shorter useful lives than we anticipate.

•We have a substantial amount of debt and servicing future interest or principal payments may impair our ability to operate our business or require us to change our business strategy to accommodate the repayment of our debt.

Early-Stage Company Risks

•Our liquidity position raises substantial doubt about our ability to continue as a going concern.

•We have incurred significant losses since inception, and we may not be able to achieve, maintain or increase profitability or positive cash flow.

•The requirements of being a public company may strain our resources, divert our management’s attention and affect our ability to attract and retain additional executive management and qualified board members.

•We have identified material weaknesses in our internal control over financial reporting, which we are in the process of, and are focused on, remediating.

12

Risks Related to the Ownership of Our Securities

•The price of our Common Stock and Warrants are likely to be highly volatile.

•Our Common Stock is subject to restrictions on ownership by non-U.S. citizens, which could require divestiture by non-U.S. citizen stockholders and could have a negative impact on the transferability of our Common Stock, its liquidity and market value, and such restrictions may deter a potential change of control transaction.

•We may issue additional shares of our Common Stock or other equity securities, which would dilute your ownership interest in us and may depress the market price of our Common Stock.

•There can be no assurance that we will be able to comply with the continued listing standards of Nasdaq.

•The holders of shares of Series A Preferred Stock have rights, preferences and privileges that are not held by, and are preferential to, the rights of holders of our Common Stock.

•A small number of Bridger’s stockholders could significantly influence its business.

•Future sales, or the perception of future sales, of a substantial number of shares of our Common Stock and Warrants, by us or our stockholders in the public market may cause the price of our Common Stock and Warrants to decline.

•Warrants are exercisable for our Common Stock and if exercised will increase the number of shares eligible for future resale in the public market and result in dilution to our stockholders.

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not currently known to us or that we currently deem less significant may also affect our business operations or financial results. If any of the following risks actually occur, our stock price, business, operating results and financial condition could be materially adversely affected and the market price of our securities could decline, causing our equityholders to lose all or a portion of their investment.

Aviation and Firefighting Risks

Our operation of aircraft involves a degree of inherent risk, and we could suffer losses and adverse publicity stemming from any accident, whether related to us or not, involving aircraft, helicopters, or commercial drones similar to the assets we use in our operations.

The operation of aircraft is subject to various risks, and demand for firefighting services, may in the future be impacted by accidents or other safety issues regardless of whether such accidents or issues involve Bridger flights, our aircraft operators, or aircraft flown by our aircraft operators. Air transportation hazards, such as adverse weather conditions and fire and mechanical failures, may result in death or injury to personnel and passengers which could impact client confidence in a particular aircraft type. Safety statistics for air travel are reported by multiple parties, including the Department of Transportation (the “DOT”) and National Transportation Safety Board, and are often separated into categories of transportation. Because our aerial firefighting services include a variety of aircraft, our clients may have a hard time determining how safe aerial firefighting services are, and their confidence in aerial firefighting may be impacted by, among other things, the classification of accidents in ways that reflect poorly on aerial firefighting services or the methods that aerial firefighting services utilize.

As the owners and operators of certain aircraft, including the CL-415EAFs, we believe that safety and reliability are two of the primary attributes that customers consider when selecting aerial firefighting services. Our failure to maintain standards of safety and reliability that are satisfactory to our customers may adversely impact our ability to retain current customers and attract new customers. We are at risk of adverse publicity stemming from any public incident involving our company, our people, or our brand. Such an incident could involve the actual or alleged behavior of any of our employees.

13

Increased accident history could bar us from certain contracts, thereby reducing demand for our services. Further, if our personnel or one of the aircraft models that is used by us is involved in a public incident, accident, catastrophe, or regulatory enforcement action, we could be exposed to significant reputational harm and potential legal liability. The insurance we carry may be inapplicable or inadequate to cover any such incident, accident, catastrophe, or action. In the event that our insurance is inapplicable or inadequate, we may be forced to bear substantial losses from an incident or accident. In addition, any such incident, accident, catastrophe, or action involving our employees or one of the aircraft models used by us could create an adverse public perception, which could harm our reputation, resulting in existing or potential customers being reluctant to use our services and adversely impacting our business, results of operations, and financial condition. If one or more of our operators were to suffer an accident or lose the ability to fly certain aircraft due to safety concerns or investigations, we may be required to cancel or delay certain aerial firefighting services until replacement aircraft and personnel are obtained.

Our operations may also be negatively impacted by accidents or other safety-related events or investigations that occur in or near the airports and the hangars we utilize for our aerial firefighting services. For example, if an accident were to occur at or near one of our hangars that we rely on for certain flights, we may be unable to utilize that hangar until the accident has been cleared, any damages to the facilities have been repaired, and any insurance, regulatory, or other investigations have been completed. Similarly, an adverse safety event by a third- party with respect to the CL-415EAF or any of the other planes in our fleet could result in temporary or permanent bans on certain aircraft models by our current or future customers.

Our business is inherently risky in that it is fighting wildfires which are powerful and unpredictable.

The performance of our services necessitates that we interact with wildfires. Wildfires can be massively unpredictable, and while we have implemented safety protocols and systems, these protocols and systems cannot eliminate the risk of accidents. Further, to effectively fight fires, flight operations often require low-level flights and involve performing services in mountainous terrain, both of which increase the risks involved with our services. To protect against these dangers, we may be required to incur more expenses and/or implement time- consuming safety protocols and systems, which could cause our expenses to be higher than anticipated. We may also be more likely to experience an adverse safety event.

The unavailability of an aircraft due to loss, mechanical failure, lack of pilots or maintenance personnel, especially one of the Viking Air CL-415EAFs, would result in lower operating revenues for us for a period of time that cannot be determined and would likely be prolonged.

Aircraft loss for any reason could impact our ability to provide services. Short- or long-term unavailability of an aircraft may also result from an aging fleet or parts obsolescence. Replacement aircraft or replacement parts may not be available or only available with significant delays.

Our revenues are disproportionately derived from the services of our Super Scoopers. The unavailability of one or more of our Super Scoopers could result in a significant reduction in our revenues and adversely affect our results of operations. For example, in 2022, we experienced a delay with the delivery of our fifth and sixth Super Scooper aircraft. We originally expected that the fifth Super Scooper and sixth Super Scooper would be delivered in May and July 2022, respectively, but ultimately, the delivery and subsequent preparation for deployment of the fifth Super Scooper was delayed until September 2022 and the sixth Super Scooper was not delivered until February 2023. As a result of such delays, our results of operations for the 2022 wildfire season were materially affected. Additionally, only pilots with significant flight hours can operate Super Scoopers, and there is a limited number of available pilots due to the demanding levels of training. There is a limited number of Super Scoopers in operation globally. Certain replacement parts may be unavailable or difficult to obtain, and we may be unable to hire sufficient mechanics trained to service Super Scoopers.

Our pilots and mechanics are required by contract to meet a minimum standard of operational experience. Finding and employing individuals with the necessary level of experience and certification has required us to hire Canadian personnel in addition to U.S. personnel. Inability to source and hire personnel with appropriate skills and experience would inhibit operations.

Our business’s success depends on our continued ability to attract, retain, and motivate highly qualified personnel with experience in the aviation space, including pilots and mechanics. However, competition for qualified personnel is intense. Our business may not be successful in attracting qualified personnel to fulfill our current or future needs. In the event that we are unable to fill critical open employment positions, we may need to delay our operational activities and goals, including the development and expansion of our business, and may have difficulty in meeting our obligations as a public company.

14

In addition, competitors and others may attempt to recruit our employees. The loss of the services of any of our key personnel, the inability to attract or retain highly qualified personnel in the future or delays in hiring such personnel, particularly senior management, pilots, and other technical personnel, could materially and adversely affect our business, financial condition and results of operations. In addition, the replacement of key personnel likely would involve significant time and costs and may significantly delay or prevent the achievement of our business objectives.

The development of superior alternative firefighting tactics or technology that do not rely on our existing and planned capital assets could reduce demand for our services and result in a material reduction in our revenue and results of operations.

Our aircraft have been modified to deploy our technology and support our existing firefighting tactics to fight wildfires. In particular, the Super Scooper is specially designed to fight forest fires with water and to refill from open bodies of water. If new technology or firefighting tactics are created or discovered that provide more powerful, more economic, faster, safer, more environmentally friendly or services that are otherwise superior in certain aspects to our current services, then we may see reduced demand for our services or be required to incur additional costs to adapt our fleet to such technologies or firefighting tactics. Additionally, current and potential government customers may push towards contracting services from customers with modernized fleets. All of these changes could narrow the scope of future contracts to exclude our existing assets, which could reduce demand for our services, our revenues, and earnings.

Operations Risks

We rely on our IT systems to manage numerous aspects of our business. A cyber-based attack of these systems could disrupt our ability to deliver services to our customers and could lead to increased overhead costs, decreased sales, and harm to our reputation.

We rely on IT networks and systems to operate and manage our business. Our IT networks and systems process, transmit and store personal and financial information, and proprietary information of our business. The technology also allows us to coordinate our business across our operation bases and communicate with our employees and externally with customers, suppliers, partners, and other third parties. While we believe we take reasonable steps to secure these IT networks and systems, and the data processed, transmitted, and stored thereon, such networks, systems, and data may be susceptible to cyberattacks, viruses, malware, or other unauthorized access or damage (including by environmental, malicious, or negligent acts), which could result in unauthorized access to, or the release and public exposure of, our proprietary information or our users’ personal information. In addition, cyberattacks, viruses, malware, or other damage or unauthorized access to our IT networks and systems could result in damage, disruptions, or shutdowns to our platform. Any of the foregoing could cause substantial harm to our business, require us to make notifications to our customers, governmental authorities, or the media, and could result in litigation, investigations or inquiries by government authorities, or subject us to penalties, fines, and other losses relating to the investigation and remediation of such an attack or other unauthorized access or damage to our IT systems and networks.

Our service, data and systems may be critical to operations or involve the storage, processing and transmission of sensitive data, including valuable intellectual property, other proprietary or confidential data, regulated data, and personal information of employees, and others. Successful breaches, employee malfeasance, or human or technological error could result in, for example, unauthorized access to, disclosure, modification, misuse, loss, or destruction of our or other third-party data or systems; theft of sensitive, regulated, or confidential data including personal information and intellectual property; the loss of access to critical data or systems; service or system disruptions or denials of service.

Our ability to attract and retain customers, to efficiently operate our business, and to compete effectively depends in part upon the sophistication, security, and reliability of our technology network, including our ability to provide features of service that are important to our customers, to protect our confidential business information and the information provided by our customers, and to maintain customer confidence in our ability to protect our systems and to provide services consistent with their expectations. As a result, we are subject to risks imposed by data breaches and operational disruptions, including through cyberattack or cyber-intrusion, by computer hackers, foreign governments, cyber terrorists and activists, cyber criminals, malicious employees or other insiders of the Company or third-party service providers, and other groups and individuals.

Data breaches of companies and governments continue to increase as the number, intensity, and sophistication of attempted attacks and intrusions from around the world have increased and we, our customers, and third parties increasingly store and transmit data by means of connected IT systems. Additionally, risks such as code anomalies, “Acts of God”, data leakage, cyber-fraud, and human error pose a direct threat to our services, systems, and data and could result in unauthorized or block legitimate access to sensitive or confidential data regarding our operations, customers, employees, and suppliers, including personal information.

15

We also depend on and interact with the technology and systems of third parties, including our customers and third-party service providers such as cloud service providers. Such third parties may host, process, or have access to information we maintain about our company, customers, employees, and vendors or operate systems that are critical to our business operations and services. Like us, these third parties are subject to risks imposed by data breaches, cyberattacks, and other events or actions that could damage, disrupt, or close down their networks or systems. We have security processes, protocols, and standards in place, including contractual provisions requiring such security measures, that are applicable to such third parties and are designed to protect information that is held by them, or to which they have access, as a result of their engagements with us. Nevertheless, a cyberattack could defeat one or more of such third parties’ security measures, allowing an attacker to obtain information about our company, customers, employees, and vendors or disrupt our operations. These third parties may also experience operational disruptions or human error that could result in unauthorized access to sensitive or confidential data regarding our operations, customers, employees, and suppliers, including personal information.

A disruption to our complex, global technology infrastructure, including those impacting our computer systems and website, could result in the loss of confidential business or customer information, require substantial repairs or replacements, resulting in significant costs, and lead to the temporary or permanent transfer by customers of some or all of their business to our competitors. The foregoing could harm our reputation and adversely impact our operations, customer service, and results of operations. Additionally, a security breach could require us to devote significant management resources to address the problems created. A significant data breach or any failure, or perceived failure, by us to comply with any federal, state, or foreign privacy laws, regulations, or other principles or orders to which we may be subject could adversely affect our reputation, brand, and business, and may result in claims, investigations, proceedings, or actions against us by governmental entities, litigation, including class action litigation, from our customers, fines, penalties, or other liabilities, or require us to change our operations or cease using certain data sets. Depending on the nature of the information compromised, we may also have obligations to notify users, law enforcement, government authorities, payment companies, consumer reporting agencies, or the media about the incident and may be required to expend additional resources in connection with investigating and remediating such an incident, and otherwise complying with applicable privacy and data security laws.

These types of adverse impacts could also occur in the event the confidentiality, integrity, or availability of company and customer information was compromised due to a data loss by us or a trusted third party. We or the third parties with which we share information may not discover any security breach and loss of information for a significant period of time after the security breach occurs.