As filed with the Securities and Exchange Commission on February 15, 2024.

Registration No. 333-269028

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 7370 | 35-2503373 | |||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

PodcastOne, Inc.

335 N. Maple Drive, Suite 127

Beverly Hills, California 90210

(310) 858-0888

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Kit Gray

President

PodcastOne, Inc.

335 N. Maple Drive, Suite 127

Beverly Hills, California 90210

(310) 858-0888

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Sasha Ablovatskiy

Jonathan Shechter

Foley Shechter Ablovatskiy LLP

1180 Avenue of the Americas, 8th Floor

New York, NY 10036

(212) 335-0466

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company,

indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised

financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Post-Effective Amendment No. 1 (this “Post-Effective Amendment No. 1”) of PodcastOne, Inc. (the “Company”) to the Company’s Registration Statement on Form S-1, as amended (File No. 333-269028) (the “Registration Statement”), as originally filed by the Company with the U.S. Securities and Exchange Commission (the “SEC”) on December 27, 2022 and as originally declared effective by the SEC on May 15, 2023, is being filed to (i) include the Company’s audited financial statements for the fiscal year ended March 31, 2023 and the Company’s financial statements for the three and nine months ended December 31, 2023 and certain related financial information, (ii) include certain information for the Company’s fiscal year ended March 31, 2023, and (iii) update certain other information in the Registration Statement.

The information included in this Post-Effective Amendment No. 1 amends the Registration Statement and the prospectus contained therein. No additional securities are being registered under this Post-Effective Amendment No. 1. All applicable registration fees were paid at the time of the original filing of the Registration Statement on May 10, 2023.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated February 15, 2024.

10,294,736 Shares

Common Stock

This prospectus relates to the registration of the resale of up to 10,294,736 shares of PodcastOne, Inc.’s (fka Courtside Group, Inc.) (“we,” “us,” “our” “PodcastOne” or the “Company”) common stock, $0.00001 par value per share (the “common stock”), by our stockholders identified in this prospectus, or their permitted transferees (and together with LiveOne, Inc., the “Registered Stockholders”) in connection with our direct listing on The Nasdaq Capital Market (the “Direct Listing”), consisting of (i) 2,514,251 shares of our common stock reserved for issuance upon the conversion of $6,838,500 aggregate principal amount of our outstanding Bridge Notes (as defined in this prospectus) purchased by certain Registered Stockholders, plus the amount of accrued and unpaid interest calculated as of the assumed date of May 5, 2023, if any, that is payable in shares of our common stock in connection with the conversion thereof, (ii) 2,946,167 shares of our common stock that may be issued upon exercise of the Bridge Warrants (as defined in this prospectus) that we issued to certain Registered Stockholders, (iii) 167,833 shares of our common stock that may be issued upon exercise of the Placement Agent Warrants (as defined in this prospectus) that we issued to the placement agent, a Registered Stockholder, in connection with the offering of the Bridge Notes and the Bridge Warrants, and (iv) 346,485 shares of our common stock issued to the Harvest Funds (as defined in this prospectus) pursuant to the terms of the Exchange Agreements (as defined in this prospectus); and (v) the Distribution Shares.

This prospectus is also being furnished to the stockholders of LiveOne, Inc., a Delaware corporation and our parent (Nasdaq: LVO) (together with its subsidiaries other than us, “LiveOne”), in connection with the distribution (the “Distribution”) by LiveOne, a Registered Stockholder, as a special dividend to its stockholders of up to 4,320,000 shares of our common stock (the “Distribution Shares”) out of the 20,000,000 shares of our common stock held by LiveOne immediately prior to the Distribution, consisting of (i) 4,300,000 Distribution Shares distributed as a special dividend in the Distribution and (ii) up to an additional 20,000 Distribution Shares to the extent that any Distribution Shares issued to LiveOne’s stockholders of record in the Distribution were required to be rounded up. The Distribution was completed on or about September 1, 2023.

Unlike an initial public offering, the resale by the Registered Stockholders is not being underwritten by any investment bank. The Registered Stockholders may, or may not, elect to sell their shares of common stock covered by this prospectus, as and to the extent they may determine. Such sales, if any, will be made through brokerage transactions on The Nasdaq Capital Market at prevailing market prices. See “Plan of Distribution.” If the Registered Stockholders choose to sell or distribute, as applicable, their shares of common stock, we will not receive any proceeds from the sale or distribution, as applicable, of shares of our common stock by the Registered Stockholders.

We refer to the Direct Listing and the Distribution herein collectively as the “Spin-Out.” Immediately prior to the time of the Spin-Out, LiveOne held 100% of the outstanding shares of our common stock. The Spin-Out was completed on September 8, 2023. At the time of the Spin-Out, LiveOne distributed the Distribution Shares, constituting of approximately 18.9% of the outstanding shares of our common stock (not including the exercise of the Bridge Warrants or the Placement Agent Warrants and assuming the conversion of all of the Bridge Notes) held by LiveOne on a pro rata basis to holders of record of LiveOne’s common stock, $0.001 par value per share (“LiveOne common stock”), as of August 28, 2023, the final record date set by LiveOne for purposes of such distribution (the “Record Date”). Each 21 shares of LiveOne common stock outstanding as of 5:00 pm New York City, on the Record Date entitled the holder thereof to receive one share of our common stock (the “Distribution Ratio”), with any holder of less than 21 shares of LiveOne common stock receiving one share of our common stock as result of rounding up of any fractional shares of our common stock. The Distribution was made in book-entry form by our transfer agent. Fractional shares of our common stock were rounded up in the Distribution. LiveOne’s board of directors determined that the Distribution on a pro rata basis to holders of record of LiveOne was in the best interests of LiveOne and its stockholders and assisted our Company to comply with the initial listing requirements of The Nasdaq Capital Market. LiveOne’s board of directors and management ultimately concluded that the Distribution of 4,320,000 shares, or approximately 18.9% of the outstanding shares of our common stock at the time of completion of the Spin-Out (not including the exercise of the Bridge Warrants or the exercise of the Placement Agent Warrants and assuming the conversion of all of the outstanding Bridge Notes), struck the balance between providing LiveOne’s stockholders of record an opportunity to participate in unlocking the value of our Company as a stand-alone public company, allowing our Company to comply with such initial listing requirements, and having LiveOne maintain control of our Company positions LiveOne to be able to derive the most value in the future from its then majority ownership of our Company.

After giving effect to the Spin-Out and conversion of the outstanding Bridge Notes (not including the exercise of the Bridge Warrants or the exercise of the Placement Agent Warrants and assuming the conversion of all of the outstanding Bridge Notes), as of the Record Date, LiveOne owned approximately 74.2% of the outstanding shares of our common stock and voting power, the holders of the outstanding Bridge Notes (other than LiveOne) owned approximately 4.7% of the outstanding shares of our common stock, and LiveOne’s stockholders owned approximately 18.9% of outstanding shares of our common stock. Pursuant to the terms of the Bridge Notes, the outstanding Bridge Notes held by the Registered Stockholders (including LiveOne) automatically converted into shares of our common stock as a result of the Direct Listing. As a result of the completion of the Spin-Out, we became a “controlled company” within the meaning of the corporate governance standards of The Nasdaq Capital Market. See “Management — Controlled Company Exemption” and “Description of Capital Stock — General.”

On September 1, 2023, we completed the Distribution in connection with the consummation of the Direct Listing. Immediately after the Spin-Out, we became a publicly-traded company listed on The Nasdaq Capital Market and as of the date of this prospectus continue to be a majority owned subsidiary of LiveOne. Roth Capital Partners, LLC acted as our financial advisor in connection with the Direct Listing (the “Financial Advisor”).

Our common stock began trading on The Nasdaq Capital Market on September 8, 2023 and is currently listed on The Nasdaq Capital Market under the symbol “PODC.” On February 12, 2024, the closing price of our common stock was $1.77 per share.

We are an “emerging growth company” as defined under the federal securities laws and have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company.”

Investing in shares of our shares of common stock involves risks. See “Risk Factors” beginning on page 20 to read about factors you should consider before buying shares of our common stock.

Neither the U.S. Securities and Exchange Commission nor any other regulatory body or state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated ______, 2024.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or contained in any free writing prospectus filed with the U.S. Securities and Exchange Commission (the “SEC”). Neither we nor any of the Registered Stockholders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus we have prepared or that have been prepared on our behalf or to which we have referred you. Neither we nor any of the Registered Stockholders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. The Registered Stockholders are offering to sell, and seeking offers to buy, shares of their common stock but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business, financial condition, and results of operations may have changed since such date.

For investors outside the United States: Neither we nor any of the Registered Stockholders have done anything that would permit the use or possession or distribution of this prospectus or any related free writing prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our common stock by the Registered Stockholders and the distribution of this prospectus outside the United States.

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 (No. 333-269028) that we filed with the SEC. You should read this prospectus and the exhibits filed with or incorporated by reference in the Registration Statement carefully. Such documents contain important information you should consider when making your investment decision. See “Where You Can Find More Information” in this prospectus.

Except as otherwise indicated, all information in this prospectus assumes:

| ● | Exclusion of the 2,000,000 shares of our common stock authorized for issuance under our 2022 Equity Incentive Plan (as amended, the “2022 Plan”), which was adopted by our sole stockholder and our board of directors on December 15, 2022, as well as any future increases in the number of shares of our common stock reserved for issuance under the 2022 Plan. As of December 31, 2023, 779,606 shares of our common stock were reserved for issuance pursuant to awards made under our 2022 Plan, which awards will become effective on the day of the effectiveness of the registration statement of which this prospectus forms a part. See “Description of Capital Stock — 2022 Equity Incentive Plan”; |

| ● | the amendment of our Certificate of Incorporation to decrease the number of our shares of common stock and authorize the issuance of “blank check” preferred stock; |

| ● | the conversion of all of our outstanding Bridge Notes (including interest thereon) into 2,340,707 shares of our common stock as of the Record Date, which reflects the redemption of $3,000,000 of the original amount of Bridge Notes, and which were automatically converted upon the effectiveness of the Direct Listing (the “Bridge Notes Conversion”); |

| ● | the exclusion of 2,946,167 shares of our common stock issuable upon exercise of our warrants outstanding as of the date of this prospectus, which warrants were issued to the holders of the Bridge Notes (the “Bridge Warrants”); |

| ● | the exclusion of 167,833 shares of our common stock issuable upon exercise of our placement agent warrants outstanding as of the date of this prospectus, which warrants were issued to the placement agent in connection with our sale of the Bridge Notes (the “Placement Agent Warrants”); |

| ● | the issuance of 357,036 and 147,044 shares of our common stock to the Harvest Funds and Trinad Capital, respectively, pursuant to the terms of the Exchange Agreements; and |

| ● | the filing and effectiveness of our Amended and Restated Certificate of Incorporation and the adoption of our Amended and Restated Bylaws, each of which occurred on or about September 12, 2023 in connection with the completion of the Direct Listing. |

After giving effect to the Bridge Notes Conversion and assuming no exercise of the Bridge Warrants or the exercise of the Placement Agent Warrants, as of the Record Date, we had a total of 22,844,787 shares of our common stock issued and outstanding.

Certain amounts, percentages, and other figures presented in this prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals, dollars, or percentage amounts of changes may not represent the arithmetic summation or calculation of the figures that precede them.

ii

PROSPECTUS SUMMARY

This summary highlights select information contained elsewhere in this prospectus and does not contain all the information you should consider before making an investment decision. You should read the entire prospectus carefully, including the sections entitled “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the accompanying notes included elsewhere in this prospectus before making an investment decision. Unless otherwise indicated or the context otherwise requires, all references in this prospectus to “we,” “us,” “our,” the “Company,” “PodcastOne” and similar terms refer to PodcastOne, Inc. and its consolidated subsidiaries.

Overview

PodcastOne, Inc. (the “Company,” “PodcastOne,” “we,” “us” or “our”) is a leading podcast platform and publisher that makes its content available to audiences via all podcasting distribution platforms, including PodcastOne’s website (www.podcastone.com), Apple Podcasts, Spotify, Amazon Music and more. We are a majority owned subsidiary of LiveOne, Inc., a Delaware corporation and a Nasdaq-listed company (“LiveOne”). We have recently been ranked #10 on the list of Top Podcast Publishers by the podcast metric company, Podtrac.

We also produce vodcasts (video podcasts), branded podcasts, merchandise and live events on behalf of our talent and clients. With a proven 360-degree advertiser solution for multiplatform integration opportunities and hyper-targeting, we deliver millions of monthly impressions, 14+ million monthly unique listeners, and 60+ million Interactive Advertising Bureau monthly downloads. With content covering all verticals (i.e., sports, entertainment, true-crime, business, society & culture, self-help, etc.), we provide a platform for brands to reach their most sought after targeted audiences.

Our operating model is focused on offering white glove service to our shows, talent and advertising clients. With an in-house sales, production, marketing and tech team, we believe PodcastOne delivers best-in-class services to our clients and talent than any other publisher in the marketplace. This has us well positioned to scale our operations while attracting talent who in turn, will bring in additional brand advertisers and revenue. We earn revenue through the sale of embedded host-read ads, dynamic ads (host-read and otherwise), segment sponsorships and programmatic monetization channels. We also provide the opportunity for clients to have 100% share of voice with branded podcast episodes or series as well as live tours, production, merchandise creation and fulfillment, and IP ownership for original programming.

In addition to our core business, we also built, own and operate a solution for the growing number of independent podcasters: LaunchPadOne. LaunchPadOne is our owned self-publishing podcast platform, created to provide a low or no cost tool for independent podcasters without access to parent podcasting networks or state of the art equipment to create and publish shows. LaunchPadOne serves as a talent pool for us to find new podcasts and talent.

For the fiscal years ended March 31, 2023 and 2022, we generated $34.6 million and $32.3 million in revenue, respectively, representing a compound annual growth rate (“CAGR”) of 7%. For the nine months ended December 31, 2023 and 2022, we generated $31.6 million and $25.8 million in revenue, respectively, representing a CAGR of 22%. For the fiscal years ended March 31, 2023 and 2022, we incurred net losses $7.0 million and $3.6 million, respectively. For the nine months ended December 31, 2023 and 2022, we incurred net losses of $13.7 million and $3.0 million, respectively.

We are more than a podcast company. We are in the relationship business. Brands and creators partner with us to reach consumers who will purchase, listen and subscribe to their favorite PodcastOne podcasts across the audio landscape. We offer content for every type of listener with verticals including reality TV, sports, true crime self-help, and business. The visibility and reach of our network is evident with shows which consistently rank in the top 100 on the Apple Charts.

1

Recent Developments

| ● | On September 21, 2023, we changed our corporate name to “PodcastOne, Inc.” | |

| ● | On September 1, 2023, we completed the Distribution, and on September 8, 2023, we completed the Direct Listing. As a result, we became a publicly-traded company listed on The Nasdaq Capital Market under the symbol “PODC” and as of the date of this prospectus continue to be a majority owned subsidiary of LiveOne. | |

| ● | We have been recently ranked #10 on the list of Top Podcast Publishers by the podcast metric company, Podtrac, as a leading podcast publisher. | |

| ● | In July 2022, we completed our $8.8 million Bridge Notes financing at a valuation of $68.1 million and announced LiveOne’s intention to spin-out our Company as a separate public company. We agreed not to effect any Qualified Financing or Qualified Event (each as defined below), as applicable, unless our post-money valuation at the time of the Qualified Financing or Qualified Event, as applicable, is at least $150 million. In February 2023, in connection with the Direct Listing, LiveOne obtained a valuation report from an independent, third-party valuation firm, which indicates that the fair market value range of our Company’s equity as a wholly-owned subsidiary of LiveOne, on a controlling, marketable interest basis, as of December 31, 2022, is reasonably stated as between $230 million and $274 million. |

| ● | Our President, Kit Gray, has been recently named one of the 22 most influential people in podcasting, and our Vice President of Brand and Talent Partnerships, Eli Dvorkin, has been named to this year’s Top 40 Under 40 in podcasting as chosen by Podcast Magazine. |

| ● | We have an arrangement that allows us and our roster of top performing hosts to integrate unique visual elements into the podcasts they produce and distribute them via YouTube, becoming the first podcast network to utilize Adori, a pioneering interface technology. Adori’s unique YouTube integration technology allows podcast hosts and networks to seamlessly import episodes from RSS feeds, enhance them with visual elements and upload enriched assets directly to YouTube. Adori’s patented technology embeds contextual visuals, multi-format ads, AR experiences, buy buttons, polls, and other “call to action” features in the audio creating a more enhanced and richer listener experience. In creating visually enhanced podcasts, Adori’s YouTube product provides additional monetization avenues for our slate of original programming, increased discoverability and SEO presence. |

| ● | Several of our shows have hit recent milestones: Trust Me released its 100th episode in November 2022 and was featured in Harper’s BAZAAR’s “20 of the Best Podcasts to Download Now.” In October 2022, Coffee Convos was named by Edison Research as the top show delivering women listeners for advertisers. Co-Hosts Kailyn Lowry and Vee Rivera won the 2022 People’s Choice Podcast Award for Influencer of the Year and Podcast Listener Influencer of Year for their podcast, Baby Mama’s No Drama. The show also brought home the Rob Has a Podcast Entertainment award. Southern Tea, hosted by Lindsie Chrisley received a People’s Choice Award in the Kids & Family category. |

| ● | PodcastOne also has a very successful vertical featuring Kail Lowry’s shows Baby Mamas No Drama, Barely Famous and Vibin’ and Kinda’ Thrivin. |

| ● | We also partnered with Hyundai to produce live events with our hosts that provide multiple revenue streams for our Company and our talent while giving Hyundai a platform to promote their new vehicle launches. Two live shows, including one with The LadyGang and one with Jordan Harbinger, were be captured as vodcasts and later streamed on LiveOne’s streaming platform. As part of the branded content partnership, we are also developing an always-on audio plan to further drive promotion for Hyundai. In November 2022, we announced that Hyundai will have share of voice in the first four episodes of our new Friday Night Lights re-watch podcast It’s Not Only Football: Friday Night Lights and Beyond, starring Friday Night Lights stars Scott Porter and Zach Gilford and their celebrity friend, Mae Whitman. |

| ● | We have assembled an experienced Board of Directors consisting of Jay Krigsman, Craig Foster, Ramin Arani, Patrick Wachsberger, James Berk and Robert Ellin, who are distinguished professionals from their respective podcasting, entertainment, new media, business and finance industries, with a wealth of experience in maximizing business growth. |

2

Industry Trends in Our Favor

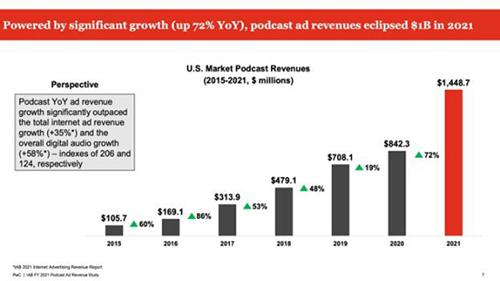

The Podcast Industry Keeps Growing While Radio is Shrinking — For the first time ever, the podcast advertising marketing grew beyond $2.28 billion in 2023 and are expected to exceed $3.25 billion in 2024 and reach $4 billion by 2025. The spoken audio industry has shifted share of voice significantly from 78% radio/13% podcasts/19% other in 2014 to 44% radio/36% podcasts/20% other.

High Growth of Podcasts Audience — In the United States, podcasts have historically been and are expected to continue to develop as a high growth segment within the next five years. An estimated 183 million Americans have listened to a podcast at some point in their life, with “superfans” consuming over 20 hours of content per week in 2023. Driven by product innovations and content accessibility, the podcast market represents significant growth and monetization potential in the long-term.

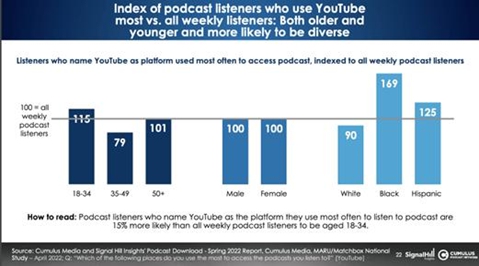

Launch of New Distribution Platforms — Being on the ground floor of a developing platform is another key to our growth strategy. This allows for more discoverability and exclusive feature opportunities. We are currently in beta with YouTube, which announced earlier this year that they are launching their own podcast platform. Approximately 28% of podcasts are consumed on YouTube and that number is quickly growing. When Facebook launched their audio platform, similarly, our shows were a part of their press plan, received exclusive boosting opportunities and were among the first podcasts to streaming on their platform.

Spoken Word is Increasing Among Gen Z — There has been a 214% increase in spoken word consumption since 2014 among the 13-24 year-old demographic, with 21% of that being podcast usage. We deliver content that spans various verticals, preferences and ages, positioning us to be part of that 21% and we expect to see that percentage grow as Gen Z continues to shift their listening habits to podcasts.

Increasing Penetration of Established Marketing — We have a strong opportunity for high growth, even in more in established markets. According to eMarketer, the number of podcast listeners is anticipated to grow to 135 million in 2024 and nearly 150 million listeners are expected to make podcasts a part of their media diet by 2027. Growth is projected to remain in double digits with an average podcast listening time per day topping 25 minutes by 2024.

Key Benefits to Our Listeners

Our Value Propositions

In addition to the highly favorable industry trends set forth above, the following elements denote the fundamental values of our PodcastOne community:

Easy audio making for everyone — We were one of the first online audio communities to provide a one-stop destination for creators to produce, edit, host and distribute audio content to consumer’s mobile and desktop devices. This has given us a wealth of experience to develop the turnkey production, sales and marketing services we offer make it possible for our partners to create high-quality, original podcasts. The monthly average number of downloads by our podcasts decreased from approximately 64.7 million in the third quarter ended December 31, 2022 to approximately 31.3 million in the same period in 2023, driven primarily by Apple iOS 17’s change in download attribution methodology.

Reaching audience and getting paid — PodcastOne shows have access to one of the largest online audio communities with distribution on publicly available platforms (Apple Podcasts, Spotify, Amazon Music, etc.), as well as our proprietary platform. This allows our podcasts, live streaming or interactive audio products available to be shared, further amplifying their reach. Our data-driven marketing strategies and best-in-class sales organization helps increase the content value and motivate content creators to continue to create and share more content on our platform. Our data analytics also provide useful feedback to our hosts to help them create and distribute more unique and high-quality content that truly resonates with their audience and invites new listeners in.

3

“White Glove” Offerings — We differentiate ourselves from our competitors through deeply integrated sales, marketing, production and distribution services offered to creators once onboarded with PodcastOne. Our data driven marketing function range across in network cross promotion, social media best practices, video asset creation and off-network trade opportunities. As a result, we have cultivated a highly engaged listener community across a variety of verticals (True Crime, Sports, TV & Film, etc.). In the quarter ended December 31, 2023, we had recorded a total of 12 million average monthly listeners. We prioritize establishing and maintaining an in-depth relationship with our creators so that we are viewed as a trusted and valued partner.

Podcast Services — Listeners can access our podcasts on their mobile devices and desktops across all major distribution platforms (Apple Podcasts, Spotify, Amazon Music, etc.). We offer all of our podcasts for free to cultivate a broad and loyal user base and generate organic traffic to our audio entertainment which has attractive monetization potential. As we build and scale loyal listeners for our shows, we are also building listeners for our other shows, through our internal cross promotional network. As shows increase in listenership, their value also increases to advertisers, often times resulting in higher cost per thousand impressions (“CPM”), in renewals and ultimately more revenue.

Our Market Opportunity

PodcastOne is a Leading Podcasting Company

PodcastOne is a leading advertiser-supported, on-demand digital audio network. With a 360-degree solution, including content creation, brand integration and distribution, PodcastOne sees more than 436 million downloads annually, across 275 episodes produced weekly. Today, a large global audience has access to over 200 podcasts distributed by PodcastOne whenever and wherever they want. We were one of the first podcast companies and transformed the podcast industry by allowing users to stream audio content (podcasts) on demand. In contrast, traditional radio relies on a linear distribution model in which stations and channels are programmed to deliver a limited programming options with little freedom of choice.

We are one of the largest independent podcast publishers with deep routed relationships with our creators, advertisers and distribution platforms. With over 5.5M unique downloads a month in the US and 29M global streams and downloads, PodcastOne’s portfolio continues to grow with engaged listeners and top tier talent. As illustrated below, we have been recently ranked #10 on the list of Top Podcast Publishers by the podcast metric company, Podtrac, as a leading podcast publisher.

PodcastOne offers content across verticals so there is something for everyone. The power of our network and brands is evident through our shows which consistently rank in the top 100 on the Apple Charts. Furthermore, we have built a promotional strategy that enables discoverability of PodcastOne shows just by being a listener of a show in the same vertical. For example, if you are listening to a PodcastOne true crime show, you will likely hear a promo about another true crime show from PodcastOne.

PodcastOne is more than a podcast company. We are in the relationship business. Every day, brands and creators partner with us to reach consumers who will listen, subscribe to PodcastOne podcasts across the audio landscape. We relentlessly focus on creating entertaining, informative, quality content. Our brand reflects culture by turning a vast portfolio of compelling personalities and stories into entertaining and engaging listening experiences which connect our large audience to the world around them.

4

Podtrac Ranker January 2024

5

What Sets Us Apart

How is PodcastOne Different?

We are a leading US podcast network with nearly 200 podcasts/vodcasts, which have generated more than 3.6 billion downloads to date. We accomplish this through several unique approaches including:

Best In Class Content Portfolio with Deep Talent Relationships — PodcastOne publishes many of the biggest podcasts, including The Adam Carolla Show, Off the Vine with Kaitlyn Bristowe, Coffee Convos, The LadyGang, Nappy Boy Radio with T-Pain, and The Jordan Harbinger Show, spanning all major genres. We have personal relationships with each and every talent, which affords us the opportunity to build extensive multi-year agreements. These agreements provide exclusive rights to their podcasting content and derivative rights to new shows. Additionally, these value-added relationships with talent allow us to negotiate industry-leading participation splits.

Full Ownership of Technology Platform, with Proprietary Data and Insights — We are one of the few podcast networks with proprietary Content Management System (“CMS”)/Content Delivery Network (“CDN”) that allows for optimized programmatic capabilities and improved audience analytics. Our hosts/talent are also able to view their download numbers, trends and analytics on this proprietary software, something many competitors don’t provide. This fully owned and operated enterprise CMS rivals other paid platforms such as Megaphone (Spotify-owned), Art19 (Amazon-owned) and SimpleCast (SiriusXM/Pandora-owned). The CMS day to day operation and maintenance is managed by a vendor we contract with and is constantly being updated to be a best-in-class system. The CMS is the platform where podcast episodes are uploaded, RSS feeds are created and distributed to listening platforms, and the listening data is analyzed and displayed in a dashboard for the hosts / producers to see.

Blue Chip Advertiser Relationships with Targeted Measurable Campaigns and Value-Added Opportunities — We offer and book competitive campaigns with new and legacy brands by: (1) using measurement tools and partners to deploy leading podcast measurement solutions that are tailored to our clients key performance indicators, including brand impact and sales lift; (2) engaging with third party attribution partners to provide greater insight for our clients into the effectiveness of their campaigns across multiple publishers and hosting providers; and (3) conducting brand lift studies that allow us to demonstrate and validate campaign impacts.

In addition, because of our deep-rooted relationships with talent we are able to engage them in host-read embedded spots and coach them through voice-over delivery to increase direct response sales and advertiser satisfaction. Furthermore, these relationships allow us to create value-added opportunities with brands through talent socials, YouTube and other influencer marketing tools.

Advertisers also have the opportunity to brand entire podcast series, as executed by Microsoft and MotorTrend most recently. This would allow advertisers to enter into content development deals for their brand with us, where we would we produce and distribute an entire podcast series for the specific brand. Advertisers benefit from branding a podcast series by getting 100% share of voice ads, which in our experience significantly helps them launch a new product, service or offering. Two podcast series examples that we have recently put together in a similar format are The Inevitable podcast and On the Edge with Microsoft Edge podcast.

White Glove Services for Our Partners — PodcastOne is more than just a hosting platform. Our hands-on approach to launching original content and growing existing shows enables us to support our talent with production, editing, marketing and sales capabilities. We are a one-stop shop for everything creators need for their podcasts to be successful. When it comes to the sales and marketing, we are here to share best practices, allocate in-network promo inventory to their shows and engage in 360-degree sales efforts on their behalf.

LaunchPadOne — LaunchPadOne is a free innovative podcast hosting, distribution, and monetization platform that provides an end-to-end podcast solution. With over 1,000 available podcasts, LaunchPadOne offers creators a 360-degree podcasting ecosystem - a cutting-edge technology hosting platform, customizable design elements, a podcast player, distribution tools to publish on all major listening apps, including Apple Podcasts, Spotify, Google Podcasts, Overcast and Pocket Casts and others, and a deep network of shows. LaunchPadOne’s robust platform technology, promotion and monetization opportunities will allow podcast creators to leverage unique opportunities from PodcastOne, such as the ability to accumulate new listeners, get discovered, and collaborate with the established podcast network. PodcastOne will monetize the audience of the LaunchPadOne network through ad insertion technology platform, which generates revenue for PodcastOne. Simultaneously, LaunchPadOne creators will receive free hosting and also have the opportunity to generate revenue for their own podcasts by embedding any ads they sell on their own.

6

Best-In-Class Management Team with a Track Record of Execution and Growth — we have an unparalleled management team with expertise and resources to produce and manage our podcasts in a turnkey manner. Our list of services include Production studios, Producers, Editors, Social Media, Marketing, Public Relations, Guest Booking, Content Hosting, Nationwide Sales, Host Read Executions, Dynamic Ad Insertion, Programmatic Ads, Vodcasts, Live Events, and Merchandising.

Our best-in-class management team is comprised of the following executives who have scaled PodcastOne to position us as a competitive network in the industry that talent and advertisers want to be a part of:

Kit Gray: Co-Founder & President, PodcastOne — Mr. Gray co-founded PodcastOne in 2012 and attracted high impact podcast talent including Adam Carolla, The LadyGang and Kaitlyn Bristowe. Mr. Gray has been recently named a “Top Influencer in Podcasting” by Podcast Magazine.

Sue McNamara: Chief Revenue Officer — Ms. McNamara has 20 plus years of radio and podcast sales experience. Ms. McNamara is a former CBS radio sales management executive who was responsible for 35% PodcastOne revenue growth in fiscal year ended March 31, 2022.

Eli Dvorkin: VP, Chief Content Officer — Mr. Dvorkin was our first hired employee and joined our Company shortly after our inception. With over 15 years of audio experience, Mr. Dvorkin was recently named one of Podcast Magazine’s 40 Under 40 in podcasting for his ability to create profitable brand partnerships and his ability to grow new and existing talent.

Stacie Parra & Alistair Walford, Co-Heads of Production – with 20+ years of radio and podcast production experience, Ms. Parra has helped us scale a production team that provides a one-stop shop for talent that need production and editing resources for their podcasts.

Benefits for Creators

We provide a large but exclusive stage for creators to connect with existing fans and to be discovered by new fans. In addition to providing creators with access to a free, ad supported podcast marketplace. We also provide creators with a full stack of tools and services, enabling them to grow their podcasts in a turnkey manner.

Creator Services — Our in-house marketing and production teams are responsible for enhancing the growth and success of our talent/creators through various functions by focusing on brand building, audience development, strategy, talent, live events and sweepstakes. At the core of our shows are fundamental and trusted relationships with the hosts which collectively give us the ability to bring their vision to life. The multiple functions of creator services align cross-functionally and throughout PodcastOne to support creators on the platform while attracting new creators to our network.

Monetization — Between July 2020 and December 31, 2023, we have paid more than $34.8 million in minimum guarantee payments (“MGs”) and advertiser revenue shares to creators. We do not pay to distribute our content and we monetize across all listener platforms.

Discovery — We not only help creators connect with existing fans, but we also support creators in connecting with the listeners who are most likely to become fans of their podcasts by running promos for all PodcastOne shows across respective verticals. From our data driven marketing approach that surface new podcasts to Users we offer creators the tools to reach their fans, new and old.

7

Distribution — A creator who makes their podcasts available on PodcastOne gains access to one of the largest publishing and distribution platforms based on our relationships with the top tier podcast apps and platforms. We enable creators to distribute their unique podcasts to this audience. We also pitch creator content for feature opportunities on Apple Podcasts, Spotify, Amazon Music, Stitcher, and iHeart to broaden their reach and discoverability. Additionally we promote our creator content across our social footprint and through email marketing to podcast fans.

Promotion — We empower creators and their managers to personalize and create unique profiles by providing them with best practices to develop their creator image, including featuring podcasts on their profiles and creating podcast playlists. On top of these standard services, we also offer creators specific promotional tools, designed to target specific Users and broad audiences in order to drive engagement.

Analytics — We provide numerous analytics for creators through our service. Analytics that creators can access include the demographics of their audience, users’ anonymized geographical locations, top listening platforms, and podcast performance data such as number of downloads and weekly listening trends. We provide analytical support that creators need to optimize their performance and focus on doing what they do best—creating unique, entertaining experiences to share with fans around the world. For example, many creators have used our analytics to inform tour locations by citing the geographical audience insights provided in the CMS that would otherwise not have been known.

Our Business Model

We are an Ad-Supported Service that provides free content to listeners via their mobile and desktop devices. We generate revenue from the sale of audio, video and social advertising delivered through advertising impressions. We generally enter into arrangements with advertising agencies that purchase advertising on our platform on behalf of the agencies’ clients. These advertising arrangements typically specify the type of advertising product, pricing, insertion dates, and number of impressions in a stated period. Revenue for our Ad-Supported segment is affected primarily by the number of a show’s listeners and our ability to provide innovative advertising products that are relevant to our Ad-Supported Users and enhance returns for our advertising partners. Our advertising strategy centers on the belief that advertising products that are based on content and are relevant to the Ad-Supported User can enhance Ad-Supported Users’ experiences and provide even greater returns for advertisers through the strength of our host-read embedded promos. According to a Super Listener Survey in 2021, an estimated 49% of listeners believe the hosts actually use the products and services they recommend and 60% of podcast listeners say they have bought something from hearing a podcast ad. Offering advertisers additional ways to purchase advertising on a programmatic basis is another key way that we expand our portfolio of advertising products and enhance advertising revenue. Furthermore, we continue to focus on analytics and measurement tools to evaluate, demonstrate, and improve the effectiveness of advertising campaigns on our platform.

8

When we are onboard new talent both parties have the common interest of creating content that advertisers want to purchase. We craft our deals with a percentage split of the advertising revenue (host-read embedded ads, DAI and programmatic) which strengthens our partnerships because when advertisers spend, we all win.

Our Growth Strategies

We believe we are still in the early stages of realizing our goal to connect creators and audiences around the world. Our growth strategies are focused on continuously improving our technology and attracting more listeners in current and new markets in order to collect more behavioral data, which we use to offer our Users, advertisers, and creators to achieve more targeted results. The key elements of our growth strategy are:

Strategically Launch New Podcasts with Culturally Relevant Creators — A creator with an engaged fanbase can strengthen our network and along with it, the PodcastOne brand. There is a lot of strategy that comes from onboarding new creators. Most importantly is how they will impact audience growth across their vertical within the PodcastOne ecosystem. We have seen success in this manner with the Kail Lowry vertical and our Real Housewife-hosted shows.

Acquire Existing Podcasts that will Thrive on Our Network — With the data we collect on show performance and show growth through our in-network promotional strategy we know what shows we can grow on our network. Additionally, this data can guide what is missing and why we may want to acquire a show with large numbers that will provide us with a jumping off point for growing our other shows.

Continue to Invest In Our Advertising Business — We will continue to invest in our advertising products in order to create more value for advertisers and our Ad-Supported Users by enhancing our ability to make advertising content more relevant for our Ad-Supported Users. Our advertising strategy centers on the belief that advertising products that are based in podcasts and are relevant to the Ad-Supported User can enhance Ad-Supported Users’ experiences and provide even greater returns for advertisers. We have introduced a number of new advertising products, including sponsored playlists, a self-serve audio advertising platform, and are testing skippable audio advertising. Offering advertisers additional ways to purchase advertising on a programmatic basis is one example of how we continue to expand our portfolio of advertising products. We also are focused on third party agency relationships and their development of analytics and measurement tools to evaluate, demonstrate, and improve the effectiveness of advertising campaigns on our platform.

Partner with New Distribution Platforms from Day One — Being on the ground floor of a developing platform is another key to our growth strategy. This allows for more discoverability and exclusive feature opportunities. When Facebook launched their audio platform, PodcastOne shows were a part of the press plan, received exclusive boosting opportunities and were among the first podcasts to streaming on their platform. Similarly, we are currently in beta with YouTube, who announced earlier this year that they are launching a podcast platform of their own. Approximately 28% of podcasts are consumed on YouTube and that number is quickly growing.

9

Advertising Solutions for Partners — Our Ad-Supported Service has grown from $34.2 million in revenue for the year ended March 31, 2022 to $34.6 million in revenue for the year ended March 31, 2023, representing an increase of 6%. As more audio content is created and converting listeners to buyers, brands and advertisers are continuing to shift their marketing spends from traditional mediums to podcasting. A March 2022 survey by Advertiser Perceptions shows that “while 31% of agencies and brands have dedicated podcast ad budgets, more than half (54%) are taking the money out of their overall digital allocation including 49% that said it comes from their digital audio budget line.”

Technology innovation and data mining are at the heart of our Ad-Supported Service. From a technology perspective, we continue to adapt to what consumers want and the tools that agencies and partners are building to support these needs. We create content that resonates with listeners and that brands want to be aligned with.

PodcastOne has partnered with third party attribution companies to assist with attribution metrics, click-through data and ROI metrics. Such companies include: Podsights, Chartable, Claritas, Artsai, Podtrac and Extreme Reach.

Our ability to harness our data allows us to know our audiences. We believe we understand people through their mindset, activities, and tastes, and we can serve them relevant advertising catered specifically to them. Our advertising platform is continually moving toward a holistic people-based marketing approach that is better for both our listeners and our advertisers.

By offering advertisers customized opportunities within our programs we are able to deliver results for our brands and advertisers. Taking our podcast brands beyond an audio experience, we also give advertisers the opportunity to scale their buys across our video and social products when aligning with a PodcastOne podcast. We believe we will further strengthen our advertising business, since these are increasingly popular mediums for our advertising partners, the brands they represent and consumer behaviors.

Blue Chip Advertiser Relationships with Targeted Measurable Campaigns and Value-Added Opportunities — Our in-house marketing and production teams are responsible for enhancing the growth and success of our talent/creators through various functions by focusing on brand building, audience development, strategy, talent, live events and sweepstakes. At the core of our shows are fundamental and trusted relationships with the hosts which collectively give us the ability to bring their vision to life. The multiple functions of creator services align cross-functionally and throughout PodcastOne to support creators on the platform while attracting new creators to our network.

10

In addition, because of our deep-rooted relationships with talent we are able to engage them in host read embedded spots and coach them through voice-over delivery to increase direct response sales and advertiser satisfaction. Furthermore, these relationships allow us to create value-added opportunities with brands through talent socials, YouTube and other influencer marketing tools.

Advertisers also have the opportunity to brand entire podcast series, as executed by Microsoft and our MotorTrend podcast most recently. This would allow advertisers to enter into content development deals for their brand with us, where we would we produce and distribute an entire podcast series for the specific brand. Advertisers benefit from branding a podcast series by getting 100% share of voice ads, which in our experience significantly helps them launch a new product, service or offering. Two podcast series examples that we have recently put together in a similar format are The Inevitable podcast and On the Edge with Microsoft Edge podcast.

We also offer comprehensive sales opportunities for advertisers ranging from video, audio and social to live events and merchandise. By scaling across our talent’s networks we can offer exclusive branding opportunities to our clients including higher CPMs for us and value added opportunities for advertisers.

Our Content Strategy

At the core, our content strategy is about partnering with influencers and creators who will not only thrive in the audio space but who complement our current programming. Since July 2020 we have onboarded over 250 shows, increasing downloads by more than 10% for some (On Display with Melissa Gorga, Trust Me) and consistently ranking in the top 12 publishers according to Podtrac. We grow by continuing to identify what resonates with our listeners and delivering content consumers want to listen to.

There is also a surge in video podcasts (vodcasts), a product we have been delivering for some of our shows since 2020. We are encouraging all of our podcasters to create video content, a platform we can support (produce, edit, distribute) on their behalf via YouTube and various social platforms. With YouTube’s recent hyper focus on bringing podcast content to their platform, we expect to see considerable podcast listener growth and AdSense dollars (revenue) from the platform.

Our Technology

We have built an internal Content Management System (“CMS”) system that creators and producers can use to track metrics about shows on an episode-by-episode basis. CMS is the platform where podcast episodes are uploaded, RSS feeds are created and distributed to listening platforms, and the listening data is analyzed and displayed in a dashboard for the creators / producers to see. We are focused on continuously improving our technology so that it is user-friendly and sets us apart from other independent publishers.

We are one of the few podcast networks with a proprietary CMS that allows for a customizable internal system resulting in improved audience analytics. Our hosts/talent are also able to view their own download numbers, trends and analytics on this proprietary software, something many network competitors don’t provide. This fully owned and operated enterprise CMS rivals other paid platforms such as Megaphone (Spotify-owned), Art19 (Amazon-owned) and SimpleCast (SiriusXM/Pandora-owned). The CMS’ day-to-day operation and maintenance is managed by a vendor we contract with and is constantly being updated to be a best-in-class system.

Marketing

Since our inception, we have focused our marketing efforts on enhancing our brand’s authenticity and presence among consumers, creators and advertisers. Initially, our campaigns were designed to educate the market on the concept of on-demand podcast streaming and the navigation functionality we provided. As familiarity with the podcast access model spread, our promotional efforts shifted to promote the specific shows, talent and brands in our portfolio. We’ve found that consumers don’t particularly know or care who is producing the content they are listening to. They are listening because they like what a host or creator represents and has to say.

11

Our Competition

We compete for the time and attention of our users across different forms of media, including traditional broadcast, satellite, and internet radio (iHeartRadio, LastFM, Pandora, and SiriusXM), other providers of on-demand audio streaming services (Spotify, Amazon Prime, Apple Music, Deezer, Google Play Music, Joox, Pandora, and SoundCloud), and other providers of in-home and mobile entertainment such as cable television, video streaming services, and social media and networking websites. Additionally, we compete with midsized publishers creating and distributing ad-supported content for the aforementioned audio platforms (Dear Media, Kast Media, Barstool Sports, etc.). We compete to attract and engage listeners with our content accessibility, perceptions of advertising load in our shows, brand awareness and reputation. Many of our competitors enjoy competitive advantages such as greater name recognition, legacy operating histories, and larger marketing budgets, as well as greater financial, technical, human, and other resources.

Additionally, we compete to attract and retain advertisers and a share of their advertising spend for our Ad-Supported Service. We believe our ability to compete depends primarily on the reputation and strength of our brand as well as our reach and ability to deliver a strong return on investment to our advertisers, which is driven by the size of our show-specific audiences, our advertising products, our targeting, delivery and measurement capabilities, and third party/agency relationships.

We also compete to attract and retain highly talented individuals, including producers, editors, sales executives and marketers. Our ability to attract and retain personnel is driven by compensation, culture, and the reputation and strength of our brand. We believe we provide competitive compensation packages and foster a team-oriented culture where each employee is encouraged to have a meaningful contribution to PodcastOne. We also believe the reputation and strength of our brand helps us attract individuals that are passionate about our Service.

For information on competition-related risks, see “Risk Factors” on page 20.

History and Development of PodcastOne

We are a Delaware corporation incorporated on February 5, 2014. On July 1, 2020, we were acquired by LiveOne and became its wholly owned subsidiary. On July 15, 2022, we completed a private placement offering (the “Notes Financing”) of our unsecured convertible notes to certain accredited investors and institutional investors for gross proceeds of $8,835,800. On September 8, 2023, we completed the Direct Listing and became LiveOne’s majority owned subsidiary. On September 21, 2023, we changed our corporate name to “PodcastOne, Inc.”

Intellectual Property

Our success depends in part upon our ability to protect our technologies and intellectual property. To accomplish this, we rely on a combination of intellectual property rights, including trade secrets, patents, copyrights, and trademarks, as well as contractual restrictions, technological measures, and other methods.

In addition to the forms of intellectual property listed above, we own rights to proprietary processes and trade secrets, including those underlying the PodcastOne platform. We use contractual and technological means to control the use and distribution of our proprietary software, trade secrets, and other confidential information, both internally and externally, including contractual protections with employees, contractors, customers, and partners. Finally, since 2019, PodcastOne has included passive participation in substantially all of its agreements, meaning if a podcast goes to derivative, PodcastOne has creative control but does accrue payment as a passive participant.

LaunchPadOne — LaunchPadOne is a free innovative podcast hosting, distribution, and monetization platform that provides an end-to-end podcast solution. With over 1,000 available podcasts, LaunchPadOne offers creators a 360 podcasting ecosystem - a cutting-edge technology hosting platform, customizable design elements, a podcast player, distribution tools to publish on all major listening apps, including Apple Podcasts, Spotify, Google Podcasts, Overcast and Pocket Casts and others, and a deep network of shows. LaunchPadOne’s robust platform technology, promotion and monetization opportunities will allow podcast creators to leverage unique opportunities from us, such as the ability to accumulate new listeners, get discovered, and collaborate with the established podcast network. We will monetize the audience of the LaunchPadOne network through ad insertion technology platform, which generates revenue for us. Simultaneously, LaunchPadOne creators receive free hosting and also have the opportunity to generate revenue for their own podcasts by embedding any ads they sell on their own.

12

Certain Relationships and Related Party Transactions

Please see section “Certain Relationships and Related Party Transactions — Various Agreements Entered into with LiveOne — Other Agreements” in this prospectus for a summary of material agreements, other than material agreements entered into in the ordinary course of business, to which we are or have been a party.

Concentration of Ownership

LiveOne, which beneficially owned 100% of the outstanding shares of our common stock prior to the Spin-Out, beneficially owned approximately 75.4% of our common stock at the time of the completion of the Spin-Out (not including the exercise of the Bridge Warrants or the exercise of the Placement Agent Warrants and assuming the conversion of all of the Bridge Notes) and, as a result, has the ability to control the outcome of matters submitted to our stockholders for approval, including the election of our directors and the approval of significant corporate transactions. See “Description of Capital Stock.” As a result of the completion of the Spin-Out, we are a “controlled company” within the meaning of the corporate governance standards of Nasdaq. See “Management — Controlled Company Exemption.”

Summary Risk Factors

Our business is subject to a number of risks and uncertainties, as more fully described under “Risk Factors” in this prospectus. We have various categories of risks, including risks related to our business and industry; risks related to our intellectual property; risks related to regulatory compliance and legal matters; risks related to tax and accounting matters; risks related to ownership of our common stock; and general risk factors, which are discussed more fully in the section titled “Risk Factors.” These risks could materially and adversely impact our business, financial condition, and results of operations, which could cause the trading price of our common stock to decline and could result in a loss of all or part of your investment. Additional risks, beyond those summarized below or discussed elsewhere in this prospectus, may apply to our business, activities, or operations as currently conducted or as we may conduct them in the future or in the markets in which we operate or may in the future operate. Some of these risks include:

| ● | We have incurred significant operating and net losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future. | |

| ● | We may require additional capital, including to fund our and/or LiveOne’s current debt obligations and to fund potential acquisitions and capital expenditures, which may not be available on terms acceptable to us or at all and which depends on many factors beyond our control. |

| ● | Our ability to continue as a going concern. |

| ● | If LiveOne does not comply with the provisions of its senior credit facility, its senior lender may terminate its obligations to LiveOne and require LiveOne and/or us to repay all outstanding amounts owed thereunder. |

| ● | We face and will continue to face competition for ad-supported listening time. |

| ● | Our business is dependent upon the performance of the podcasts and their talent. |

| ● | Significant up-front and/or minimum guarantees required under certain of our podcast license agreements may limit our operating flexibility and may adversely affect our business, operating results, and financial condition. |

| ● | If we fail to increase the number of listeners consuming our podcast content, our business, financial condition and results of operations may be adversely affected. |

13

| ● | Our revenue and operating results are highly dependent on the overall demand for advertising. Factors that affect the amount of advertising spending, such as economic downturns, can make it difficult to predict our revenue and could adversely affect our business. |

| ● | Expansion of our operations to deliver additional podcasts subjects us to increased business, legal, financial, reputational and competitive risks. |

| ● | Increases in the costs in relation to podcast content creators, such as higher podcast MGs and/or talent revenue share compensation and costs of discovering and cultivating a top podcast content creator, may have an adverse effect on our business, financial condition and results of operations. |

| ● | We use third-party services and technologies in connection with our business, and any disruption to the provision of these services and technologies to us could result in adverse publicity and a slowdown in the growth of our users, which could materially and adversely affect our business, financial condition and results of operations. |

| ● | We face competition for users’ attention and time. |

| ● | We face significant competition for advertiser and sponsorship spend. |

| ● | We cannot assure you that we will be able to meet Nasdaq’s initial listing requirements to consummate the Direct Listing, and Nasdaq may not permit our shares of common stock to be quoted on its exchange, which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions. |

| ● | Our failure to meet the continued listing requirements of Nasdaq could result in a de-listing of our common stock and penny stock trading. |

| ● | We plan to expand into international markets in the 2025 fiscal year, which would subject us to risks associated with the legislative, judicial, accounting, regulatory, political and economic risks and conditions specific to such markets, which could adversely affect our business, financial condition and results of operations. |

| ● | Our success depends, in significant part, on discretionary consumer and corporate spending on entertainment and factors adversely affecting such spending could have a material adverse effect on our business, financial condition and results of operations. |

| ● | Unfavorable outcomes in legal proceedings may adversely affect our business, financial conditions and results of operations. |

| ● | LiveOne’s debt agreements contain restrictive and financial covenants that may limit our operating flexibility, and LiveOne’s substantial indebtedness may limit cash flow available to us to invest in the ongoing needs of our business. |

| ● | LiveOne may not have the ability to repay the amounts then due under the senior credit facility, which may have a material adverse effect on our business, financial condition and results of operations. |

| ● | The Distribution could result in significant tax liability to LiveOne and its stockholders. | |

| ● | We may be unable to achieve some or all of the benefits that we expect to achieve from the Spin-Out. |

| ● | We have no operating history as an independent publicly-traded company, and our historical financial information is not necessarily representative of the results we would have achieved as an independent publicly-traded company and may not be a reliable indicator of our future results. |

14

| ● | We may not be able to access the credit and capital markets at the times and in the amounts needed on acceptable terms. |

| ● | Certain of LiveOne’s and our agreements contain provisions requiring the consent of third parties in connection with the Spin-Out. If these consents are not obtained, we may be unable to consummate the Spin-Out and/or enjoy the benefit of these agreements in the future. |

| ● | Our listing differs significantly from an underwritten initial public offering. |

| ● | Our stock price may be volatile, and could decline significantly and rapidly. |

| ● | An active, liquid, and orderly market for our common stock may not develop or be sustained. You may be unable to sell your shares of our common stock at or above the price at which you purchased them. |

| ● | LiveOne as our principal stockholders will have the ability to influence the outcome of director elections and other matters requiring stockholder approval. |

| ● | LiveOne’s majority ownership of our common stock has the effect of concentrating voting control with it and its affiliates, which limits your ability to influence the outcome of important transactions and to influence corporate governance matters, such as electing directors, and to approve material mergers, acquisitions, or other business combination transactions that may not be aligned with your interests. |

| ● | Other than our executive officers, none of LiveOne’s stockholders are party to any contractual lock-up agreement or other contractual restrictions on transfer. Following our listing, sales of substantial amounts of our common stock in the public markets, or the perception that sales might occur, could cause the trading price of our common stock to decline. |

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include that:

| ● | we are only required to include two years of audited consolidated financial statements in this prospectus in addition to any required interim financial statements, and correspondingly only required to provide reduced disclosure in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; |

| ● | we are not required to engage an auditor to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”); |

| ● | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency,” and “say-on-golden parachutes”; and |

| ● | we are not required to disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to our median employee compensation. |

We may take advantage of these provisions until the last day of the fiscal year during which the fifth anniversary of this listing occurs or such earlier time that we are no longer an emerging growth company. We will remain an emerging growth company until the earliest of: (i) the last day of the first fiscal year in which our annual gross revenue is $1.07 billion or more; (ii) the last day of the fiscal year during which the fifth anniversary of this listing occurs; (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the SEC.

15

Under the JOBS Act, emerging growth companies also can delay adopting new or revised accounting standards until such time as those standards would otherwise apply to private companies. We currently intend to take advantage of this exemption.

For risks related to our status as an emerging growth company, see “Risk Factors — Risks Related to Ownership of Our Common Stock — We are an “emerging growth company,” and we cannot be certain if the reduced reporting and disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.”

Channels for Disclosure of Information

Investors, the media, and others should note that we intend to announce material information to the public through filings with the SEC, the investor relations page on our website (www.podcastone.com), blog posts on our website, press releases, public conference calls, webcasts, our Twitter feed (@PodcastOne), our Instagram page, our Facebook page and our LinkedIn page. Information contained on or accessible through our website is not incorporated by reference into this prospectus, and inclusion of our website address, Twitter feed, Instagram page, Facebook page and LinkedIn page in this prospectus are inactive textual references only. You should not consider information contained on our website or our social media pages to be part of this prospectus or in deciding whether to purchase shares of our common stock.

The information disclosed by the foregoing channels could be deemed to be material information. As such, we encourage investors, the media, and others to follow the channels listed above and to review the information disclosed through such channels. Any updates to the list of disclosure channels through which we will announce information will be posted on the investor relations page on our website.

Corporate Information

We were incorporated in Delaware as “Courtside Group, Inc.” on February 5, 2014. On July 1, 2020, we were acquired by LiveOne and became its wholly owned subsidiary. On September 8, 2023, we completed the Direct Listing. On September 21, 2023, we changed our corporate name to “PodcastOne, Inc.” As a result of the Direct Listing, we became LiveOne’s majority owned subsidiary. We have two wholly owned subsidiaries, Courtside, LLC, a Delaware limited liability company, and PodcastOne Sales, LLC, a California limited liability company. Our principal executive offices are located at 335 North Maple Drive, Suite 127, Beverly Hills, CA 90210. Our main corporate website address is www.podcastone.com. We make available on or through our website our periodic reports that we file with the SEC. This information is available on our website free of charge as soon as reasonably practicable after we electronically file the information with or furnish it to the SEC. The information contained on, or that can be accessed through, our website is deemed not to be incorporated in this prospectus or to be part of this prospectus and shall not be deemed “filed” under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

SUMMARY UNAUDITED CONDENSED CONSOLIDATED FINANCIAL AND OPERATING DATA

The following tables summarize our unaudited condensed consolidated financial and operating data. The summary consolidated statements of operations and cash flows information for the years ended March 31, 2023 and 2022 and have been derived from our audited consolidated financial statements appearing elsewhere in this prospectus. The summary consolidated statements of operations and cash flows information for the nine months ended December 31, 2023 and 2022 and the summary consolidated balance sheet information as of December 31, 2023 have been derived from our unaudited consolidated financial statements appearing elsewhere in this prospectus. This unaudited condensed consolidated financial data is for informational purposes only. The unaudited interim consolidated financial statements were prepared on a basis consistent with our audited consolidated financial statements and include, in management’s opinion, all adjustments, consisting only of normal recurring adjustments, that we consider necessary for a fair statement of the financial information set forth in those statements. Our historical results are not necessarily indicative of the results that may be expected for any period in the future and our interim results are not necessarily indicative of our expected results for the year ended March 31, 2024. You should read the following summary consolidated financial data together with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

16

There are no pro forma adjustments necessary to reflect our operations and financial position as an autonomous entity from LiveOne as the financial statements reflect all potential adjustments including an allocation of overhead expenses (please refer to Note 2 – Summary of Significant Accounting Policies and Note 15 – Subsequent Events of our audited consolidated financial statements included elsewhere in this prospectus for adjustments made with LiveOne).

| Year Ended March 31, | Year Ended March 31, | Nine Months Ended December 31, | ||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| (Unaudited) | ||||||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||

| Consolidated Statements of Operations Information: | ||||||||||||||||