UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

For the transition period from ______ to ______

Commission

file number

(Exact Name of Registrant as Specified in Its Charter)

| Not applicable | ||

| (State

or other jurisdiction of incorporation) |

(I.

R. S. Employer Identification No.) |

| (Address of principal executive offices, including ZIP code) |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol | Name of exchange on which registered | ||

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act) Yes ☐

The registrant was

Number of shares of common shares outstanding as of December 11, 2023 was .

Documents

Incorporated by Reference:

TABLE OF CONTENTS

| i |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Any statements in this Annual Report on Form 10-K about our expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as “believe,” “will,” “expect,” “anticipate,” “estimate,” “intend,” “plan” and “would.” For example, statements concerning financial condition, possible or assumed future results of operations, growth opportunities, industry ranking, plans and objectives of management, markets for our common stock and future management and organizational structure are all forward-looking statements. Forward-looking statements are not guarantees of performance. They involve known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to differ materially from any results, levels of activity, performance or achievements expressed or implied by any forward-looking statement.

Any forward-looking statements are qualified in their entirety by reference to the risk factors discussed throughout this Annual Report on Form 10-K. Some of the risks, uncertainties and assumptions that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include, but are not limited to:

| ● | the timing of the development of future services, |

| ● | projections of revenue, earnings, capital structure and other financial items, |

| ● | statements regarding the capabilities of our business operations, |

| ● | statements of expected future economic performance, |

| ● | statements regarding competition in our market, and |

| ● | assumptions underlying statements regarding us or our business. |

The foregoing list sets forth some, but not all, of the factors that could affect our ability to achieve results described in any forward-looking statements. You should read this Annual Report on Form 10-K and the documents that we reference herein and have filed as exhibits to the Annual Report on Form 10-K, completely and with the understanding that our actual future results may be materially different from what we expect. You should assume that the information appearing in this Annual Report on Form 10-K is accurate as of the date hereof. Because the risk factors referred to on page 10 of Annual Report on Form 10-K could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us or on our behalf, you should not place undue reliance on any forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of the information presented in this Annual Report on Form 10-K, and particularly our forward-looking statements, by these cautionary statements.

| ii |

SUMMARY OF RISK FACTORS

Our business is subject to numerous risks described in the section titled “Risk Factors” and elsewhere in this prospectus. The main risks set forth below and others you should consider are discussed more fully in the section entitled “Risk Factors” beginning on page 8, which you should read in its entirety.

● our operations could be adversely affected by possible future government legislation, policies and controls or by changes in applicable laws and regulations;

● public health crises such as the COVID-19 pandemic may adversely impact our business;

● the volatility of global capital markets over the past several years has generally made the raising of capital more difficult;

● risks associated with political instability and changes to the regulations governing our business operations;

● our success is largely dependent on the performance of our directors and officers, Field Agents, and employees;

● our Common Shares may be subject to significant price volatility;

● internal controls cannot provide absolute assurance with respect to the reliability of financial reporting and financial statement preparation;

● we may be unable to manage our growth;

● risks associated with security breaches;

● risks associated with software errors or defects;

● our operations depend on information technology systems; and on continuous reliable internet access;

● our business now or in the future may be adversely affected by risks outside our control;

● risks associated with the Company’s reliance on strategic partnerships;

● reputational risk, and

● risks associated with protection of intellectual property.

| iii |

ITEM 1. BUSINESS

General

We are a Canadian-based mortgage technology and brokerage company that provides mortgage brokerage services and technology solutions to Canadian mortgage agents, brokers, sub-brokers, brokerages and consumers. Through data-driven systems together with cloud-based tools, we believe we offer competitive advantages in the Canadian mortgage industry relative to alternative mortgage broker arrangements.

We also provide back office services, together with pre-underwriting support services (collectively the “Brokerage Services”) to Canadian mortgage brokerages (the “Brokerages”). In connection with the provision of the Brokerage Services, we employ and engage several licensed mortgage brokers and agents (collectively, “Field Agents”). We have a total of full-time employed staff of 55. In addition, we also enter into affiliation agreements with certain licensed mortgage brokers (collectively, “Affiliate Brokers” and, together with Field Agents and Brokerages, the “Users”), pursuant to which the Company and the Affiliate Broker enter into an affiliation relationship with the intention of jointly marketing mortgage brokerage and other financial services as affiliated entities, sometimes referred to as “white labelling”, which allows the Affiliate Broker to sell a mortgage that is branded with its company name to its own client base.

Our services distribution and fee structure for each stream is detailed hereunder:

| 1. | The fee for the subscription service revenue stream is $117 for use of our platforms by our agents to complete the mortgage deal from initiation to funding by the lender partner and is about 3% of total gross revenue. | |

| 2. | Our pre-risk assessment services revenue is about 1.3% of our total gross revenue and the structure for this service is $390 per deal for a mortgage funded amount of $390,000 and over. For a mortgage funded amount under $390,000 the fee is $273. | |

| 3. | The balance of our total gross revenue at 95% comes from our lender partner service commissions and the structure varies by rate and amount based on the season, special promotions at that particular time, bonus applicable, funded volume, etc. The lender partners comprise of banks, trust companies, mortgage loan companies, building societies and other lending financial institutions, including but not limited to the Bank of Nova Scotia (Scotiabank), Manulife Bank of Canada, Toronto-Dominion Bank (TD Bank), The Mortgage Alliance Company of Canada Inc. (MCAP), First National Financial LP, Home Trust Company, The Equitable Trust Company (Equitable Bank), ICICI Bank Canada and Desjardins Mortgage Financing Services. |

We currently operate exclusively in Canada, specifically in the provinces of Ontario, Newfoundland and Labrador, New Brunswick, Nova Scotia, British Columbia, Prince Edward Island and Alberta. We launched our first brokerage in Ontario in November 2016. We have been approved by each of the applicable provincial mortgage regulators to operate in 11 provinces and territories namely Alberta, British Columbia, New Brunswick, Newfoundland and Labrador, Northwest Territories, Nova Scotia, Nunavut, Prince Edward Island, Quebec, and Yukon, and 2 provinces to follow are Manitoba and Saskatchewan. We launched our first brokerage office in Alberta on July 1, 2021. We also launched our first brokerage office in Newfoundland and Labrador, Nova Scotia, New Brunswick, and Prince Edward Island on May 4, 2022. Thereafter, we expect to open our first British Columbia brokerage office and our first Quebec brokerage office sometime in late 2022 or early 2023. We provide our Brokerage Services to both residential and commercial mortgage opportunities and, in each case, through a proprietary technology called MyPineapple, as discussed in further detail below.

MyPineapple

At the heart of our Brokerage Services is an innovative technology system, MyPineapple, that provides real time data management and reporting, lead generation opportunities, customer relationship management, deal processing, education and knowledge center, payroll, regulatory compliance, data analytics, document collection and storage, automated onboarding, lender access, back office support and direct underwriting support, all in one. MyPineapple offers network management capabilities for Users, including hundreds of qualified Field Agents, to create an efficient marketplace for the provision of mortgage lending and insurance industry services. MyPineapple integrates directly with Salesforce, Equifax, OneSpan, G Suite and Filogix and manages Users’ day-to-day business through automated triggers and tasks, ensuring nothing falls through the cracks. Backed by Salesforce, pursuant to the Salesforce Agreement (defined herein), and built with proprietary code deep data analytics, MyPineapple syncs up with Users’ calendar and emails, produces robust reporting, advanced analytics, and real-time notifications on marketing communications, and more. MyPineapple is a sophisticated and fundamental tool for revenue growth and relationship development. It plays a significant role in what we believe makes our Brokerage Services distinct and cutting-edge.

MyPineapple was created to address key issues within the mortgage brokerage industry. We built MyPineapple to create a long-term competitive advantage relative to traditional service providers, who have comparatively high-touch, labor intensive and costly operations. We believe that, through MyPineapple, we are able to deliver faster services and with fewer errors. Our MyPineapple platform is completely automated, simplifying the mortgage process while providing efficiencies to and alleviating pressure on Users’ staff in completing traditional administrative tasks, which in turn reduces the Users’ cost structure and results in increased profit margins and scalability. MyPineapple reduces manual processes through robust quality control mechanisms, logistics management capabilities, capacity planning tools and end-to-end transaction management. MyPineapple also includes a leading education technology platform, which enables Users to continuously stay informed and educated on what mortgage solutions and market conditions could impact Canadian consumers.

| 1 |

Our primary objectives and goals include, but are not limited to, the following:

| ● | Grow our mortgage broker distribution channel to gain further market share and consumer adoption, including increasing organic (non-acquisition related) market share and to achieve growth on the number of mortgages funded annually; | |

| ● | Become the go-to mortgage experience platform for mortgage agents, lenders and homebuyers; | |

| ● | For Pineapple Insurance to provide an insurance option for all our mortgage approvals; | |

| ● | To ensure that we are providing a well-rounded and custom-tailored approach to insurance solutions that may best suit the clients’ needs; | |

| ● | To leverage the power of our growing database and brand recognition to open further insurance opportunity channel; and |

Streamline the insurance approval and application process for mortgage clients using technology.

Services and Products

Brokerage Services

The following is a detailed description of the Brokerages Services that we offer:

| 1. | Mortgage Brokering: We employ and engage a number of licensed Field Agents who originate clients, provide mortgage consultation services, advise clients on the various mortgage products offered by financial institutions in Canada, offer clients access to rate information and mortgage options from a range of lenders, including major banks and lending institutions and assist clients in selecting the most appropriate and effective mortgage solution for their particular needs. |

| 2. | Technology: MyPineapple is a full spectrum, robust and comprehensive technology system, which allows Users to conduct their brokerage services more effectively and efficiently. Amongst other things, MyPineapple syncs up with Users’ calendar and emails, produces robust reporting, advanced analytics, and real-time notifications for email opens, and link clicks. MyPineapple also provides Users with cloud storage. We also provide marketing support to Users in order to systematically manage the marketing process, segmentation and client conversions. We ensure that all clients stay well informed with highly relevant information; it also increases the conversion ratios and engagement metric for its Users. This provides Users the ability to focus on higher probability clients and deliver a high level of value and service while the system manages the relationship with others. |

| 3. | Back Office Support Services: Through MyPineapple, we offer our Users back office support services, including digital and automated onboarding and set up, loan packaging and processing, digital document collection and client portals, loan maintenance activities, payroll, lender communication, reporting requirements for regulators and business management, cloud services, expense collections, document preparation, compliance, training, administration and marketing. |

| 4. | Pre-Underwriting Support: Technology enabled and together with back-office support, we offer our Users pre-underwriting support services that establish appropriate qualifying processes in a mortgage application, providing borrowers a digital environment ensuring mortgage agents has the necessary data and providing borrowers with an instant pre-qualification. We use our diverse exposure to the mortgage industry to save Users from spending valuable resources on mortgage applications that have fewer chances of reaching approval. In particular, we offer our Users the following pre-underwriting services, aimed at speeding up the underwriting process and helping mortgage lenders make accurate decisions: |

| ● | Credit Review: We verify all information that is supplied by the client in vital loan documents and other personal information. Thereafter, we meticulously review client credit records and tax return documents to ensure the client has the required financial stability to make monthly payments for the mortgage. We follow checklist-based system to ensure that all the critical aspects pertaining to underwriting are covered. |

| 2 |

| ● | Data Validation: Our pre-underwriting support services include recording and digitizing our findings in the data validation process. By digitizing these vital information sets about the client, we are able to establish the accuracy and speed needed to expedite the underwriting process. | |

| ● | Fraud Analysis and Compliance: We pride ourselves in diligently checking for identity fraud and ensuring that applications are compliant and contain complete information. Our mortgage experts have the experience and acumen to spot missing or mala fide information. This obviates the need for the underwriter to send client files back for incomplete information and thereby speeds up the underwriting process. Our fraud analysis encompasses all aspects of the client file review process including running third-party reports. This ensures the underwriter has to focus only on decision-making. | |

| ● | Appraisal Ordering and Review: We take charge of title ordering and dispatching verified property information to the appraiser to boost the turnaround times of the appraisal process. Once the appraisal is over, we carefully review the appraisal report to ensure that the process has been completed in a fair and error-free manner. | |

| ● | Data Analytics: Through MyPineapple, we are able to use data to analyze customer benefit opportunities as they become available. In particular, MyPineapple allows us to utilize the data that has been acquired through the mortgage approval process along with real time real estate and credit data to thereby reduce costs and overall debt process timelines. |

Insurance Products

Pineapple Insurance Inc. (“Pineapple Insurance”) is a wholly owned subsidiary of Pineapple Financial Inc. This entity is to serve the insurance needs of our brand mortgage brokers and agents across Canada. Pineapple Insurance is to act as an Managing General Agent (MGA) supported by Industrial Alliance. This entity will create both a revenue channel and retention strategy for borrowers that live within our database. This will also allow a growth opportunity and an overall holistic financial services opportunity for us. We are currently in the early stages of development of Pineapple Insurance Inc. Operational infrastructure and a budget has been prepared alongside technology modifications to our MyPineapple system in order to manage the delivery of this product. We have also created a sales and marketing plan alongside assets and materials, which will be used for initial launch. Our next steps are staffing and human capital requirements in order to execute on the business plan and goals of developing Pineapple Insurance.

Pineapple Insurance provides the following services:

| ● | We will complete a needs analysis on each client to ensure the most suitable product to meet both their needs and their goals. In our product suite, we will offer term life insurance which will provide a low-cost coverage at a fixed rate of payments for a limited period of time for the life of the mortgage. The goal of this product is to ensure that in the event of the insurer’s untimely death with their term policy their beneficiaries will be covered in the amount of the policy during the life of the term. No insurance will be paid to the beneficiary should the insured pass away after the end of the term or if the insured did not make the required payments. | |

| ● | Whole Life Insurance is a life insurance policy which is guaranteed to remain in force for the insured’s entire lifetime, provided required premiums are paid, or to the maturity date. In addition to paying a death benefit, whole life insurance also contains a savings component in which cash value may accumulate on a tax-advantaged basis. The policies can be leveraged as collateral or an asset with our lenders through the Company. |

| 3 |

| ● | For both our personal and our business clients, we offer permanent life insurance policies, which offer a death benefit and cash value. The death benefit is money that is paid to your beneficiaries when you pass away. Cash value is a separate savings component that you may be able to access while you are still alive. Permanent insurance can help cover the business owner for their entire life. And unlike term insurance, it includes the potential for a cash accumulation fund. Investments in the fund are tax-preferred, including at death when the tax-free death benefit is paid out to a named beneficiary. An additional benefit of permanent life insurance is that allocating funds in a corporation away from taxable investments to a permanent life insurance policy can help reduce overall annual taxable investment income. Permanent life insurance lasts from the time you buy a policy to the time you pass away, as long as you pay the required premiums. The policies can be leveraged as collateral or an asset with our lenders through the Company. | |

| ● | Critical Illness Insurance provides additional coverage for medical emergencies like heart attacks, strokes, or cancer. Because these emergencies or illnesses often incur greater-than-average medical costs, these policies pay out cash to help cover those overruns where traditional health insurance may fall short and help cover living expenses while the client recovers. These policies come at a relatively low cost. However, the instances that they will cover are generally limited to a few illnesses or emergencies. The key element is to ensure that the mortgagor does not fall behind in their mortgage payments. | |

| ● | Credit Insurance is a type of life insurance that can cover the remaining amount of your loan in the event of your death. Your insurance company will use the death benefit to pay down or pay off the remaining balance on the loan, up to a maximum amount outlined in the certificate of insurance. The money from your death benefit will go to your creditor. The money will not go to your family or beneficiaries. |

We offer a wide range of investment options to suit clients risk tolerance and investment preferences. A financial advisor will review and assess the needs of each client to determine the short- and long-term goals for financial success. Such options may include segregated funds or mutual funds for registered (registered education savings plans (RESPs), registered retirement savings plans (RRSPs), tax-free savings accounts (TFSAs), etc.) and non-registered accounts. A segregated fund, or seg fund, is a type of investment fund administered by Canadian insurance companies in the form of individual, variable life insurance contracts offering certain guarantees to the policyholder such as reimbursement of capital upon death and mutual funds. As a regulatory requirement, all Canadian mortgage approvals being presented by the mortgage broker channel must include the option for a client to consider an insurance option in an effort to protect the liability in the case of death or disability. Pineapple Insurance Inc. will be presenting this insurance option for a client to accept or not via the products that we have available. This will be presented to all mortgage approvals being offered via our parent company, Pineapple Financial Inc.

As a complementary service to our parent company, Pineapple Financial Inc., this insurance subsidiary was created to easily serve the needs of the homeowners whose mortgages originate with us. With any mortgage product in Canada, an insurance component is a requirement, hence the diversification and business development into insurance.

Our insurance services identified above currently are provided by a third-party insurance company, Industrial Alliance Inc., with whom we are affiliated as a managing general agent (MGA). We, therefore, act as an agent earning commissions from the premiums charged by the insurance company.

We believe the material steps for Pineapple Insurance to grow form its early stages of development are as follow:

| 1. | To introduce the services offered by Industrial Alliance and to serve the Users on our platform, MyPineapple, is to market these services, create a knowledge base for them to understand and pass on the learning to their customers, create a support structure for both Users and Users’ customers. | |

| 2. | Set up an internal infrastructure for the management and offering of these services i.e. hire a senior management person to manage the operational affairs and thereafter additional personnel, as needed when the business grows. The additional personnel will be mostly sales commissionable personnel with a retainer. |

The costs we anticipate relate to mostly the marketing efforts undertaken, human capital which will be a fixed cost for the senior person and variable for additional personnel. As we develop and progress this business, it is anticipated that our major expenses will be payroll, marketing, and platform development. We have identified approximately 15% of the use of the proceeds from the shares offering to be dedicated to developing this business.

| 4 |

The timeline we feel to grow this subsidiary would be approximately 12 to 36 months depending upon the marketing efforts, acceptance of the products and services offered by Industrial Alliance, the prices / premiums for these products and services, and the understanding of the products because of the many variations that are inherent in the insurance products and services.

InsurTech

MyPineapple is a key reason for our success and has the ability to drive interested and timely insurance prospects to a replicated module that we have built in order to streamline and manage the customer flow for insurance products. The process is designed to create a unique synchronicity between the client obtaining a mortgage approval and insurance approval.

Combined, the simplicity of the two platforms with its connectivity and integrations will allow Pineapple Insurance to successfully process and approve insurance applications.

We have also created client segmentations and retention programs to ensure that we can maximize our database of over 150,000 potential clients.

Growth Strategy

Brokerage Services

We aim to gain further market share and consumer adoption by focusing on the following areas of growth:

| 1. | Increase Agent Revenue From Optimized Analytics: We will continue to analyze past borrower data to determine opportunities to beneficially re-service them in the future, potentially creating revenue generating activities and significantly enhancing the borrower experience. | |

| 2. | Added Product Suite – Insurance. As discussed above, we are establishing an insurance channel that provides borrowers with a full suite of insurance products, which we believe will increase revenue. | |

| 3. | National Expansion: We expect to continue to expand our business and operations into current jurisdictions along with new provinces such as British Colombia and Quebec. | |

| 4. | Borrower-Facing Technology. We believe MyPineapple will be a marketplace where clients can select from a variety of mortgage products that will suit their individual needs while tracking the progress and status of the transaction for the life of the mortgage and beyond. |

Insurance Products

In order to achieve our objectives and goals, Pineapple Insurance will focus on four main areas:

| 1. | Insurance originations: Our files will be obtained exclusively through the Pineapple Financial referral network. This will be achieved through technology integration where Pineapple Insurance agents are immediately notified of a mortgage approval which requires an insurance option. Our agents will be highly trained in an effort to service the growth of our referral network. Consistency in service level and approach is key to building our brand. | |

| 2. | Emphasizing core values: Servicing our clients, maintaining relationships, ongoing and continued support, education and training, ongoing lines of communication between mortgage agent and insurance agent and ensuring a smooth and efficient closing process. We expect our agents to conduct themselves with the highest level of professionalism and carry out the fundamental and core values of Pineapple Insurance at all times. |

| 5 |

| 3. | Hiring and training insurance agents: We will follow and adhere to strict hiring and training policies as set out in our training manuals. Development of education and training programs working in conjunction with our partners. Ensuring that we are consistently working on recruiting top performing insurance agents that will be able to meet the growth and scale of the needs of the Company. | |

| 4. | Technologies and relationship management tools: We will be replicating and customizing our robust MyPineapple system for data transfer and client management. This will be broken into the following areas: |

| ● | Operational Excellence: notifying insurance agents at the optimal time to increase conversion metrics and customer satisfaction. Integration of client data so the process is convenient for all involved parties. Visibility of status and automations of workflow and requirements; | |

| ● | Client Relationship Management (CRM): Advancing client relationships towards application indication, application completion and client retention; and | |

| ● | Acquisition: marketing funnels to leverage the overall database and identity opportunities from older missed opportunities. |

Markets for our Services

Brokerage Services

The clients for our Brokerage Services include mortgage agents, brokers, sub-brokers, brokerages and consumers. Our customer activity is intrinsically linked to the health of the real estate or commercial markets generally, particularly in Canada.

Strong housing demand during 2020, 2021 and the first quarter of 2022 positively impacted the seasonal variations. With the onset of inflationary pressures around the globe, not only the seasonality but the normal trends of the housing markets have declined with the increase of interest rates. Although our business may be negatively impacted, we believe our multiple channels of revenue helps to mitigate any such impact.

On April 7, 2022, the 2022 budget was released by the Government of Canada which focuses on affordable housing alternatives for Canadians and additional tax measures to assist first time home buyers. With the continual influx of new immigrants as proposed by the Government of Canada; the renewed demand in home renovations and refurbishments; the users becoming more knowledgeable about additional use of their home equity, and other varying and creative measures, we plan to capitalize on these growth initiatives into the future.

Insurance Products

The insurance market for Pineapple Insurance is focused around growth in the Canadian mortgage landscape as well as market share growth for Pineapple Financial.

| ● | Real estate investors: we are able to consolidate multiple mortgage amounts into one insurance policy to help minimize risk if an investor has multiple properties. | |

| ● | Residential Home purchase: with Canadian housing prices hitting all-time highs, we will help clients provide insurance to fill the gap between their current coverage and the mortgage amount | |

| ● | Refinance: can help clients reduce existing coverage or apply/consolidate if they require additional coverage. | |

| ● | Reverse Mortgage: these clients can use the income from the reverse mortgage to help plan their final expense through insurance as well as enrich their retirement years. |

| 6 |

| ● | Switch: transferring to another lender at renewal. The insurance we offer is not tied to the lender directly and can assist clients in locking in their rates long term when they can still qualify for insurance | |

| ● | Renovation and construction: Clients will be able to access their cash values in their permanent insurance policies to help fund their renovations and construction projects. If additional financing is required, we can provide the added insurance coverage needed. | |

| ● | Self-Employed: As large numbers of Canadians move into business for themselves, we have found a great need for an insurance product that can suit their needs since they generally do not have a company benefits plan. Income protection will also be a key component of our business here. | |

| ● | Commercial Mortgages: We can provide the proper insurance to clients for the right amount of coverage and timeline for one or multiple investors. Coverages can go up to $20 million. | |

| ● | Private Lending: Customized insurance can be provided to private lenders who may have a different set of circumstances in terms of investment type and timeline horizon. | |

| ● | High Risk Health & Uninsurable: We can offer guaranteed issue insurance to clients who may have declining health or were previously declined for insurance in the past. |

Pineapple Financial Inc. and Mortgage Market Dependency

We take a long-term view to manage and measure the success of our ongoing business strategy. In this regard, our principal focus is on market share growth. We seek to achieve increased market share irrespective of residential and commercial mortgage origination market conditions. Market share growth can be achieved through both the onboarding of new Users to MyPineapple and by increasing market share within its existing Users, including recently onboarded Users.

We are confident in our ability to increase the number of Field Agents using MyPineapple in conducting their brokerage services primarily due to the efficiency that MyPineapple brings to the mortgage brokerage process. From August 1, 2022 to August 1, 2023, our active users increased at a rate of 9.35%.

The mortgage market and residential and commercial mortgage originations are subject to the influence of many external factors, such as broader economic conditions and fluctuating interest rates, over which we have no control. We believe we have substantial growth opportunities to expand our market share within our existing total addressable market. In particular, we expect to have access to more opportunities in the commercial mortgage segment through our partnership with MCommercial. Additionally, we expect to gain access to greater market share opportunities as we continue to develop MyPineapple and improve the efficiency of the mortgage approval process.

Industry Overview

The Canadian Mortgage and Mortgage Brokerage Industry

According to the Bank of Canada, as of May 1, 2022, Canada’s chartered banks held over $1.523 trillion of residential mortgages (which amount does not include mortgages held by provincially regulated entities such as credit unions or mortgage investment corporations). Mortgage lenders typically offer a range of products, with options for fixed or variable rates, varying terms and amortization periods, as well as differing ancillary terms for pre-payment, incentives or other matters. Interest rates are typically renegotiated every three (3) years. While mortgage lenders post both fixed and variable interest rates at which the lender offers mortgages of varying terms, typically most lenders are willing to negotiate interest rates lower than those posted, a practice referred to as “discounting”. The practice began in Canada in the early 1990s and is considered the norm in today’s mortgage market. The practice of discounting permits mortgage lenders to improve their ability to price discriminate and offer different rates to different borrowers based on their willingness to pay. Price discrimination allows lenders to increase their profits through negotiating different rates with individual borrowers instead of offering a blanket reduction in rates. The advent of price discrimination in the Canadian mortgage market has increased the importance of the mortgage broker in the lending negotiation process. In return for a fee (paid by the lending institution), the mortgage broker is typically able to negotiate a better rate than the consumer, or to efficiently reduce the time and effort required to be applied by the consumer to achieve similar results. Mortgage brokers are provincially regulated and subject to training and licensing requirements. See “Regulatory Environment” for details. However, there are relatively few barriers to entry in the mortgage brokerage market. Nevertheless, the ability of a given mortgage broker to erode lender price discrimination and secure rates at the lower end of the range at which lenders are prepared to lend is dependent upon a number of factors. While experience and negotiating ability are relevant factors, a key factor in the potential success of a mortgage broker in securing advantageous rates is the bargaining power of the mortgage broker, which varies directly with the volume of mortgages the broker is able to place with lenders.

| 7 |

Industry Growth Strategy

Our overall aim has been to increase market share through organic (non-acquisition related) means and to achieve growth on the number of mortgages funded annually. In an effort to accomplish our growth goals, we maintain a consistent, focus on recruiting Field Agents and overall Users. We have employed a significant number of recruiters which has resulted in growth rate than most of our competitors. Secondly, with ongoing concentrated efforts towards recruiting, it has allowed us to gain a strong understanding of the competitive models that exist and also to continually enhance our offerings in the most effective way to recruit and retain qualified Field Agents. Additionally, through MyPineapple, we are able to support Field Agents growth in sales volume, productivity and efficiency in delivering mortgage solutions and increasing corporate revenue. Our aim has always been to have the leading model on which to recruit and support Field Agents, based on offering them a superior value-proposition.

Competitive Conditions

Mortgage Brokerage Market Conditions

Effective January 1, 2018, the Office of the Superintendent of Financial Institutions Canada (“OSFI”) adopted Guideline B-20 - Residential Mortgage Underwriting Practices and Procedures (the “Guideline B-20”). The revised Guideline B-20 applies to all federally regulated financial institutions. The changes to Guideline B-20 reinforce OSFI’s expectation that federally regulated mortgage lenders remain vigilant in their mortgage underwriting practices. As Guideline B-20 made mortgage borrowing more difficult for many Canadians, management believes more Canadians may have turned to mortgage brokers to help navigate the complex rules. Management expects that mortgage brokers will increase their market share in the coming years due to the following factors:

| ● | Mortgage regulations: Mortgage regulations have become more stringent in recent years, affecting the number of individuals that can qualify for conventional bank mortgages. As a result, these individuals are turned away from banks and seek out mortgage brokers for assistance in obtaining a mortgage. | |

|

● | Additional Offerings: With new products to offer, mortgage brokers will tend to appeal to a larger demographic/population base and also retain clients more effectively. |

| ● | Conditioning and Habits: Twenty years ago, only a minimal percentage of the Canadian population used mortgage brokers, as brokers were viewed generally as a last resort to obtaining a mortgage. Over the years, this perception has shifted, and Canadians are now using mortgage brokers to obtain better mortgage rates and to save money. The generation that was reaching a home-buying age when brokers had little or no market share is aging and continually being replaced by younger, mortgage broker friendly Canadians. | |

| ● | Complexity of Mortgages: Many consumers are not sufficiently financially literate to ask the right questions when applying for a loan at a bank. As financial products become more complicated, more Canadians seek assistance to understand the complexities and alternatives. | |

| ● | Increased Broker Business Sophistication: As mortgage broker business sophistication increases, the Company expects the volume of renewal business funded by mortgage brokers to increase. | |

| ● | Interest Rates May Increase: As interest rates have been at historical lows for a significant period, many believe that interest rates will increase in years to come. In a higher interest rate environment, the Company anticipates that a growing proportion of consumers will likely shop for the best mortgage opportunities, driving the more conservative “single-bank” mortgage consumers to use mortgage brokers. | |

| ● | Technology: By utilizing MyPineapple and other available technologies, mortgage brokers have the ability to access client demographic and credit information and quickly and efficiently disseminate credit applications to various lenders across Canada. Technology provides the mortgage broker and clients with the ability to efficiently access home specific and third-party data such as appraisals, credit reports and related credit application information in a highly efficient and cost-effective manner. |

| 8 |

Primary Competitors

Our primary competitors consist of the following 3 categories:

| 1. | Traditional Mortgage Brokerages: These mortgage companies provide clients a more traditional way of obtaining mortgages by sourcing business through referrals while processing loan applications with limited access to technology and face-to-face meetings. As many of these organizations have been operating for decades, they have had time to cultivate relationships and build strong portfolios of customers. They access Canada’s leading lenders for their products and services. Examples are: Dominion Lending Centres (TSX: DLCG), Verico, Mortgage Alliance and Centum. | |

| 2. | Digital Mortgage Companies: A fairly new breed of mortgage company that is sprouting from the digital evolution currently taking place in our landscape. These companies are focused on a direct-to-consumer model by offering a digital mortgage experience, however, they are still using a more traditional structure in the back office to fund mortgage solutions through Canada’s largest lenders. Examples are: Nesto, Homewise and Motus Bank. | |

| 3. | Mortgage Technology Providers: These are companies that provide software and technology solutions to some of the traditional mortgage brokerages and companies that have not invested or developed their own technology solutions. The providers are typically focused on specific problems and providing solutions to segments of mortgage workflow. They can be expensive and difficult for traditional companies to implement. Examples are: Finmo, Lenders and Lender Spotlight. |

Competitive Advantages

We compete with a number of mortgage brokerage companies. However, we offer competitive advantages relative to alternative mortgage broker arrangements as a result of the following:

| ● | Debt Consolidation: As personal debt levels continue to grow, we offer a unique opportunity of allowing potential borrowers access to their home equity to consolidate debts at lower interest rates. Interest only payments will provide lower and more flexible payment terms which will free clients cash flow for savings and help them establish better control over their personal finances. |

| ● | Residential Home Purchase: With access to Canada’s top lenders, we can help our clients find a mortgage solution best suited for their individual needs. Our Field Agents are trained at finding a mortgage solution that fits into a client’s overall wealth plan and helps the client obtain the lowest overall cost of borrowing. |

| ● | Refinance: We will encourage and assist clients to either take equity out of their homes or refinance into lower interest rates. |

| ● | Switch: We allow clients to easily transfer to another lender upon renewal. |

| 9 |

| ● | Renovation and Construction: With homebuyers seeing historic appreciation in home values the market has seen the “move up” buyer decide to stay and renovate existing property with the equity they have quickly grown. This has provided an opportunity for us to focus on providing the short-term financing required for such home renovation projects, while the major banks have slowly pulled out or limited their exposure in this area with government regulations changes to the home equity line of credit program. |

| ● | Self Employed: As large numbers of Canadians move into business for self, we have found an increase demand for a mortgage product that can suit their needs. Typically these borrowers have good credit ratings and assets but can’t verify their income through traditional means such as tax filings and pay stubs. |

| ● | Damaged Credit: Damaged or challenged credit files are something that needs a financing solution. We take a holistic approach in determining the risk as it maps out a solution. Mortgages for these types of clients will need to improve their situation either by increasing cash flow, reducing debt load or increasing income potential. We will ask referring brokers to maintain close relationships with these clients to work on rehabilitation. |

| ● | Private Lending: With exclusive access and expertise in private lending, we can ensure clients have knowledge of all available resources in the market. |

| ● | Technology: We are able to provide advanced technology solutions to differentiate us from our competitors, including: |

| a) | Data Analytics – Optimized Retention – Enhanced Customer Experience: As a data driven mortgage company MyPineapple harnesses the power of data which we acquire through the mortgage process and use it to help make meaningful decisions which save the client money, time and improve the customer experience. | |

| b) | Unique Customer Profiling – Optimized Retention: Using a proprietary scoring and profiling process, we are able to uniquely segment clients and provide most televant information and resources to them at a meaningful point in the mortgage process. | |

| c) | Internal Processing Centre – Focused Team – Increased Productivity: Having an internal underwriting and mortgage processing center allows us increased conversion, higher funding ratio’s and maximize productivity of our Field Agents. | |

| d) | Actionable Signals - Marketing Efforts – Focused Engagement: Driving real-time signals to our Field Agents when conversion opportunities present themselves. | |

| e) | Knowledge Transfer – Increased Accuracy – Performance: Comprehensive education technologies platform allows us to align the right product to the right lender and client. | |

| f) | Data Integrity – Optimized Decision Making: We have built safeguards to ensure data integrity and accuracy. | |

| g) | Lead Generation and Market Segmentation: MyPineapple quickly segments leads for personalized marketing. It then markets on behalf of the agent, turning cold leads into warm leads for faster customer acquisition. Field Agents receive real-time notifications for email, as well as reminders and scripts to ensure nothing is missed. | |

| h) | Automated Triggers and Enhanced Workflow -–MyPineapple directly syncs to calendars and emails. Tasks can easily be inputted into the system and email reminders ensure Field Agents remember to follow up. Intuitive automation then kicks in to guide Field Agents and all stakeholders through the entire process. | |

| i) | Live Community via Chatter: MyPineapple connects Field Agents directly to the underwriting team, as well as other agents throughout the organization. This creates a support network, sense of work community and ultimately accelerates the response time. | |

| j) | Online database of educational tools known as KNOWLEDGE – This online information resource is an online library with over 2000 resources, containing training videos that cover everything, from lender guidelines, sales and marketing tips, to deals training and more. | |

| k) | Advanced Analytics and Reporting Features that turn data into actionable insights - This maximizes opportunity and creates lifetime customer value which lowers acquisition costs and significantly increases revenue. |

| 10 |

Specialized Skill and Knowledge

Our business requires specialized skills and knowledge, which include, but are not limited to, expertise related to mortgage underwriting, mortgage originations, private lending, business development, marketing and business strategy development. Our executive and management team has a strong background and significant experience and expertise in these areas. Our team also possesses specialized skills in data architecture, software development, programming and coding, finance and accounting, automations and process, training and education. Additionally, we currently rely upon, and expect to continue to rely upon, various legal and financial advisors and consultants and others in the operation and management of our business.

Intangible Assets

Our business is substantially dependent on our proprietary technology platform, MyPineapple, which it licenses from Salesforce. While the Company has not registered any intellectual property rights with respect to MyPineapple, it relies on trade secrets to protect the applicable proprietary information. Additionally, MyPineapple has been built through various development partners, such that no single developer has access to the complete technological architecture. See “Business –– Material Contracts” for more information on the Salesforce Agreement

Additionally, we rely on confidentiality agreements with its employees, consultants and advisors to protect its trade secrets and other proprietary information. Nonetheless, these agreements may not effectively prevent disclosure of confidential information and may not provide an adequate remedy in the event of unauthorized disclosure of confidential information. If we are not able to adequately prevent disclosure of trade secrets and other proprietary information, the value of its business could be significantly diminished.

Material Contracts

Salesforce Agreement

In connection with the development of MyPineapple, we entered into a licensing agreement with Salesforce.com, Inc. dated (NYSE: CRM) December 1, 2020 (the “Salesforce Agreement”) and expires on November 30, 2023. Salesforce is a cloud-based software company headquartered in San Francisco, California. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Pursuant to the Salesforce Agreement, we are licensed to use the Salesforce software as the platform or infrastructure on which we build the various applications such as MyPineapple. The applications we develop on this platform are the core that drive the operational software and applications used by Field Agents to initiate and process mortgage originations, which is the primary basis of our revenue generation. The Company is billed annually at a rate of $500,172 per year, which was during the year ended August 31, 2023

Affiliation Agreements

We enter into affiliation agreements with Affiliate Brokers, pursuant to which we and the Affiliate Broker enter into an affiliation relationship with the intention of jointly marketing mortgage brokerage and other financial services as affiliated entities, sometimes referred to as “white labelling”, which allows the Affiliate Broker to sell a mortgage that is branded with its company name to its own client base. Pursuant to these affiliation agreements, we generally receive a fixed commission from the Affiliate Broker for any mortgage transaction where the Affiliate Broker has acted as the mortgage broker for the borrower. In general, these affiliation agreements have an indefinite term and may be terminated by either party upon thirty days written notice.

Changes to Contracts

The Company does not expect its business to be affected in the current financial year by renegotiation or termination of contracts or sub-contracts.

| 11 |

Regulatory Environment

Brokerage License Requirements

In order to operate its mortgage broker business, we must remain duly licensed as a mortgage broker to deal and trade in mortgages in accordance with the Mortgage Brokerages, Lenders and Administrators Act, 2006 (Ontario), as amended (the “MBLA Act”). We have had our mortgage brokerage license since November 2016 and it has been renewed each year without issue. We will be subject to similar legislation and license requirements in the other provinces in Canada where we intend to expand.

In accordance with the MBLA Act, individuals, including directors, officers, partners, directors and officers of corporate partners, employees or agents of a mortgage brokerage company, such as the Company, who are engaged in dealing mortgages or trading in mortgages on its behalf must obtain a mortgage broker or mortgage agent license. A mortgage broker or agent license authorizes an individual to work for only the mortgage brokerage company named under the license. An individual cannot be licensed to work for more than one mortgage brokerage company. The Superintendent of Financial Services will use the information obtained in a mortgage broker license application to determine whether an applicant meets the prescribed eligibility requirements and is suitable for a license. The applicant will be required to submit documents to support certain pieces of information about the business.

| ● | Application Process. The application must be completed and submitted to certain regulatory authorities in the provinces and territories of Canada (each a “Regulatory Authority”), such as the Financial Services Regulatory Authority Ontario. The Regulatory Authority will send to the applicant an email acknowledgement upon receipt of the application. The Regulatory Authority will advise the applicant if the application is in order to proceed to the next step in the process. In the next step, the applicant will prepare and submit the application to license the mortgage brokerage’s principal broker and prepare and submit the online declarations for all the directors/officers/partners via The Regulatory Authority’s online licensing system. All directors and officers of the mortgage brokerage company applicant (“DOPs”) are required to provide confirmation of their suitability for licensing of the mortgage brokerage. A mortgage brokerage’s license can only be approved or issued when all the declarations from DOPs are received and reviewed by the Regulatory Authority. Once the brokerage’s license has been approved an email will be sent to the principal broker to indicate the brokerage’s license number. No paper license will be issued. At this point, the brokerage may prepare and submit applications to license its other brokers and agents via the online licensing system. |

| ● | Fraud Prevention Measures. FSRA is required to maintain a public registry of licensed mortgage brokerages. Consistent with FSRA’s role in protecting the public interest FSRA collaborates with other organizations, including other regulators, fraud prevention organizations and law enforcement agencies. |

| ● | Fees and Renewal. Fees are payable in respect of all applications for licenses, other than for the mortgage brokerage’s principal broker. The fees are based on a one-year cycle. The fee due is prorated based on when the application is submitted. To simplify the payment and reconciliation process, mortgage brokerages are also required to submit fees on behalf of their agents and brokers. These fees are paid electronically when the mortgage brokerage submits license applications for its brokers and agents through the online licensing system. Once licensed, every mortgage brokerage must pay a regulatory fee in respect of each new one-year cycle. This fee is due every year on March 31. The mortgage brokerage must also pay fees on behalf of each agent and broker, other than the principal broker, when renewing their broker or agent licenses for the same one-year cycle. |

Insurance Regulation

Pineapple Insurance is subject to federal, as well as provincial and territorial, regulation in Canada in the provinces and territories in which they underwrite insurance/reinsurance. The Office of the Superintendent of Financial Institutions (“OSFI”) is the federal regulatory body that, under the Insurance Companies Act (Canada) (the Insurance Companies Act”), prudentially regulates federal Canadian and non-Canadian insurance and reinsurance companies operating in Canada. Pineapple Insurance is licensed to carry on insurance business by OSFI and in each province and territory.

Under the Insurance Companies Act, Pineapple Insurance is required to maintain an adequate amount of capital in Canada, calculated in accordance with a test promulgated by OSFI called the Minimum Capital Test. Under the Insurance Companies Act, approval of the Minister of Finance (Canada) is required in connection with certain acquisitions of shares of, or control of, Canadian insurance companies such as Pineapple Insurance, and notice to and/or approval of OSFI is required in connection with the payment of dividends by or redemption of shares by Canadian insurance companies such as Pineapple Insurance.

| 12 |

Other Regulations

In addition, the Company must comply with all federal, provincial and municipal laws that affect a Canadian business including employment, workers’ compensation, insurance, corporate, and tax laws and regulations.

Bankruptcy and Similar Procedures

The Company has not had any bankruptcy (whether voluntary or otherwise), receivership or other similar proceedings instituted by it or against it since its incorporation nor are any such proceedings being contemplated or threatened in the foreseeable future.

Material Restructuring Transactions

Pineapple has not completed any material restructuring transactions since incorporation.

Incorporation

The Company was incorporated under the OBCA on October 16, 2015 under the name “2487269 Ontario Limited” (doing business under the name of Capital Lending Centre). The Company’s head office is located at Unit 200, 111 Gordon Baker Road, North York, Ontario M2H 3R1 and its registered and records office is located at 67 Mowat Avenue Suite 122, Toronto, Ontario M6K 3E3. On June 16, 2021, the Company changed its name to “Pineapple Financial Inc.”

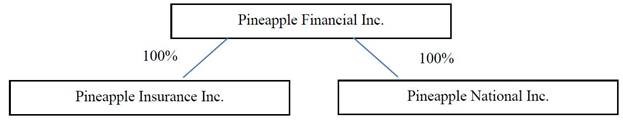

Corporate Structure

The Company has two wholly owned subsidiaries: Pineapple Insurance Inc. (“Pineapple Insurance”) and Pineapple National Inc. (“Pineapple National”). Pineapple Insurance was incorporated under the OBCA on December 14, 2016, under the name “CLC Insurance Inc.” and changed its name to Pineapple Insurance Inc. on July 12, 2021. Pineapple Insurance has a registered and records office located at Suite 200, 111 Gordon Baker Road, Suite 200, North York, Ontario M2H 3R1. Pineapple National was incorporated under the Canada Business Corporations Act on November 9, 2021, with a registered and records office located at 10th Floor, 595 Howe Street, Vancouver, British Columbia V6C 2T5.

ITEM 1A. RISK FACTORS

Risks Related to the Company

We are dependent on the residential real estate market.

Our financial performance is closely connected to the strength of the residential real estate market, which is subject to a number of general business and macroeconomic conditions beyond our control.

| 13 |

Macroeconomic conditions that could adversely impact the growth of the real estate market and have a material adverse effect on our business include, but are not limited to, economic slowdown or recession, increased unemployment, increased energy costs, reductions in the availability of credit or higher interest rates, increased costs of obtaining mortgages, an increase in foreclosure activity, inflation, disruptions in capital markets, declines in the stock market, adverse tax policies or changes in other regulations, lower consumer confidence, lower wage and salary levels, war or terrorist attacks, natural disasters or adverse weather events, or the public perception that any of these events may occur. Unfavorable general economic conditions, such as a recession or economic slowdown, in the United States, Canada or other markets the Company enters and operates within could negatively affect the affordability of, and consumer demand for, its services which could have a material adverse effect on its business and profitability.

In addition, federal and state governments, agencies and government-sponsored entities could take actions that result in unforeseen consequences to the real estate market or that otherwise could negatively impact the Company’s business. Some of the above-mentioned economic factors and conditions are currently adversely affecting Pineapple as the Users and consumer sentiment has waned and has precipitated fears of a possible economic recession. In the event of a continuing market downturn, our results of operations could be adversely affected by those factors in many ways, including making it more difficult for us to raise funds if necessary, and our stock price may further decline.

The real estate market is substantially reliant on the monetary policies of the federal government and its agencies and is particularly affected by the policies of the Bank of Canada, which regulates the supply of money and credit in Canada, which in turn impacts interest rates. The Company’s revenues could be negatively impacted by a rising interest rate environment. As mortgage rates rise, the number of home sale transactions may decrease as potential home sellers choose to stay with their lower mortgage rate rather than sell their home and pay a higher mortgage rate with the purchase of another home. Due to a prospective higher debt assumption with the rise in interest rates, homeowners also may choose to not participate in refinancing or other similar mortgage financing activity that would create revenue for Pineapple. Potential home buyers may choose to rent rather than pay higher mortgage rates. Changes in the interest rate environment and mortgage market are beyond the Company’s control, are difficult to predict and could have a material adverse effect on its business and profitability.

We may not be able to secure additional capital and achieve adequate liquidity to grow and compete.

We will require additional capital to operate, grow and compete, and failure to obtain such additional capital could limit our operations and our growth. When such additional capital is required, we will need to pursue various financing transactions or arrangements, which may include debt financing, equity financing or other means. Additional financing may not be available when needed or, if available, the terms of such financing might not be favorable to us and might involve substantial dilution to existing shareholders. In addition, debt and other debt financing may involve a pledge of assets and may be senior to interests of equity holders. We may incur substantial costs in pursuing future capital requirements, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. The ability to obtain needed financing may be impaired by such factors as the capital markets (both generally and in the mortgage brokerage industry in particular), our status as a relatively new enterprise with a limited history and/or the loss of key management personnel.

We have a limited operating history and, therefore, cannot accurately project our revenues and operating expenses.

We have a relatively limited operating history. As such, we will be subject to all of the business risks and uncertainties associated with any new business enterprise, including under-capitalization, cash shortages, limitations with respect to personnel, financial and other resources. Although we possess an experienced management team, there is no assurance that we will be successful in achieving a return on shareholders’ investment and the likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered in connection with the establishment of any business. There is no assurance that we can continue to generate revenues, operate profitably, or provide a return on investment, or that we will successfully implement our business and growth plans. An investment in our securities carries a high degree of risk and should be considered speculative by investors. Prospective investors should consider any purchase of our securities in light of the risks, expenses and problems frequently encountered by all companies in the early stages of their corporate development.

| 14 |

We may continue to incur substantial losses and negative operating cash flows and may not achieve or maintain positive cash flow or profitability in the future.

Our financial statements have been prepared on a going concern basis under which an entity is considered to be able to realize its assets and satisfy its liabilities in the ordinary course of business. Our future operations are dependent upon the identification and successful completion of equity or debt financings and the continued achievement of profitable operations at an indeterminate time in the future. There can be no assurances that we will be successful in completing equity or debt financings or in achieving profitability. The financial statements do not give effect to any adjustments relating to the carrying values and classifications of assets and liabilities that would be necessary should we be unable to continue as a going concern.

Currency exchange rates fluctuations could adversely affect our operating results.

The Company is exposed to the effects of fluctuations in currency exchange rates, Our functional currency is in Canadian dollars (CAD) and our presentation currency is in US dollars (USD). Due to the currency exchange rates fluctuations between the two currencies, there is a risk the company’s operations and profitability may be affected during the translation. Currently the company does not have many international transactions and the fluctuations are mostly limited to the financial statements currency translation adjustments relating to the movements. The financial statements contain a line disclosing this translation amount.

Our operating results may be subject to seasonality and vary significantly among quarters during each calendar year, making meaningful comparisons of successive quarters difficult.

Seasons and weather traditionally impact the real estate industry in the jurisdictions where we operate. Continuous poor weather or natural disasters negatively impact listings and sales. Spring and summer seasons historically reflect greater sales periods in comparison to fall and winter seasons. We have historically experienced lower revenues during the fall and winter seasons, as well as during periods of unseasonable weather, which reduces the Company’s operating income, net income, operating margins and cash flow.

Real estate listings precede sales and a period of poor listings activity will negatively impact revenue. Past performance in similar seasons or during similar weather events can provide no assurance of future or current performance, and macroeconomic shifts in the markets we serve can conceal the impact of poor weather or seasonality.

Home sales in successive quarters can fluctuate widely due to a wide variety of factors, including holidays, national or international emergencies, the school year calendar’s impact on timing of family relocations, interest rate changes, speculation of pending interest rate changes and the overall macroeconomic market. Our revenue and operating margins each quarter will remain subject to seasonal fluctuations, poor weather and natural disasters and macroeconomic market changes that may make it difficult to compare or analyze our financial performance effectively across successive quarters.

Our growth strategy may not achieve the anticipated results.

Our future growth, profitability and cash flows depend upon our ability to successfully implement our growth strategy, which, in turn, is dependent upon a number of factors, including our ability to:

| ● | expand our customer base; | |

| ● | increase and retain more qualified agents; | |

| ● | expand into additional jurisdictions; | |

| ● | support growth of existing customers; |

| 15 |

| ● | continued financial strength and health; | |

| ● | diversify into additional related businesses; | |

| ● | improve our technological capabilities; | |

| ● | ensure skilled and well-trained employees and agents; | |

| ● | enhance our platforms; and | |

| ● | selectively pursue acquisitions. |

There can be no assurance that we can successfully achieve any or all of the above initiatives in the manner or time period that we expect. Further, achieving these objectives will require investments which may result in short-term costs without generating any current revenue and therefore may be dilutive to our earnings. We cannot provide any assurance that we will realize, in full or in part, the anticipated benefits we expect our strategy will achieve. The failure to realize those benefits could have a material adverse effect on our business, financial condition and results of operations.

We may be unable to effectively manage rapid growth in our business.

We anticipate that growth in demand for our services will place significant demands on our operational infrastructure. The scalability and flexibility of our platform depends on the functionality of our technology and network infrastructure and its ability to handle increased traffic and demand for bandwidth. We anticipate that growth in the number of customers using our platform and the number of requests processed through our platform will increase the amount of data that we process. Any problems with the transmission of increased data and requests could result in harm to our brand or reputation. Moreover, as our business grows, we will need to devote additional resources to improving our operational infrastructure and continuing to enhance its scalability in order to maintain the performance of our platform.

As we grow, we will be required to continue to improve our operational and financial controls and reporting procedures and we may not be able to do so effectively. Furthermore, some members of our management do not have significant experience managing a large national business operation, so our management may not be able to manage such growth effectively. In managing our growing operations, we are also subject to the risks of over-hiring and/or overcompensating our employees and over-expanding our operating infrastructure. As a result, we may be unable to manage our expenses effectively in the future, which may negatively impact our gross profit or operating expenses.

As we continue to grow and develop the infrastructure of a public company, we must effectively integrate, develop and motivate a growing number of new employees. In addition, we must preserve our ability to execute quickly, further developing our platform and implementing new features and initiatives. As a result, we may find it difficult to maintain our corporate culture, which could limit our ability to innovate and operate effectively. Any failure to preserve our culture could also negatively affect our ability to recruit and retain personnel, to continue to perform at current levels or to execute on our business strategy effectively and efficiently.

To grow our business, we will continue to depend on relationships with third parties, such as insurance companies, financial institutions and lenders.

To grow our business, we will continue to depend on relationships with third parties, such as insurance companies, financial institutions and lenders. Identifying partners, and negotiating and documenting relationships with them, requires significant time and resources. Our competitors may be effective in providing incentives to third parties to favor their products or services over ours. In addition, acquisitions our partners by our competitors could result in a decrease in the number of our current and potential customers, as our partners may no longer facilitate the adoption of our applications by potential customers. Although we do maintain a few fixed-term contracts with lending partners, we cannot assure you that we can renew them once they expire, or we can renew them with the term we desire. Even though our business does not substantially depend on any particular third-party lending partner, if we are unsuccessful in establishing and maintaining our relationships with third parties, or if these third parties are unable or unwilling to provide services to us, our ability to compete in the marketplace or to generate revenue could be impaired, and its results of operations may suffer. Even if we are successful, we cannot be sure that these relationships will result in increased customer usage of its services or increased revenue.

| 16 |

Our insurance business is highly regulated, and statutory and regulatory changes may materially adversely affect our business, financial condition and results of operations.

Life insurance statutes and regulations are generally designed to protect the interests of the public and policyholders. Those interests may conflict with the interests of our shareholders. Federal and provincial insurance laws regulate all aspects of our Canadian insurance business. Changes to federal or provincial statutes and regulations may be more restrictive than current requirements or may result in higher costs, which could materially adversely affect our business, financial condition and results of operations. If the Office of the Superintendent of Financial Institutions (“OFSI”) determines that our corporate actions do not comply with applicable Canadian law, Pineapple Insurance could face sanctions or fines, and be subject to increased capital requirements or other requirements. If OSFI determines Pineapple Insurance is not receiving adequate support from Pineapple under applicable Canadian law, Pineapple Insurance may be subject to increased capital requirements or other requirements deemed appropriate by OSFI.

If there are extraordinary changes to Canadian statutory or regulatory requirements, we may be unable to fully comply with or maintain all required insurance licenses and approvals and the regulatory authorities could preclude or temporarily suspend us from carrying on some or all of our insurance activities or impose fines or penalties on us, which could materially adversely affect our business, financial condition and results of operations. We cannot predict with certainty the effect any proposed or future legislation or regulatory initiatives may have on the conduct of our business.

We may be subject to fraudulent activity that may negatively impact our operating results, brand and reputation.