UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended | |||||

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from __________ to __________ | |||||

Commission File Number: 001-41710

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (615 ) 514-7339

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |||||||||||

| x | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

1

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes x No

As of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of common stock held by non-affiliates of the registrant was $356.7 million (based on the closing price of $21.96 as reported on the New York Stock Exchange as of that date).

As of February 9, 2024, 83,309,210 shares of the registrant’s common stock, par value $0.0001 per share, were outstanding.

Documents Incorporated by Reference

Part III of this Annual Report on Form 10-K incorporates information from certain portions of the registrant’s definitive proxy statement relating to the registrant’s 2024 annual meeting of shareholders, which will be filed with the Securities and Exchange Commission on Schedule 14A within 120 days after the fiscal year to which this report relates.

2

ATMUS FILTRATION TECHNOLOGIES INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| Page | ||||||||

3

PART I

Item 1. Business

Overview

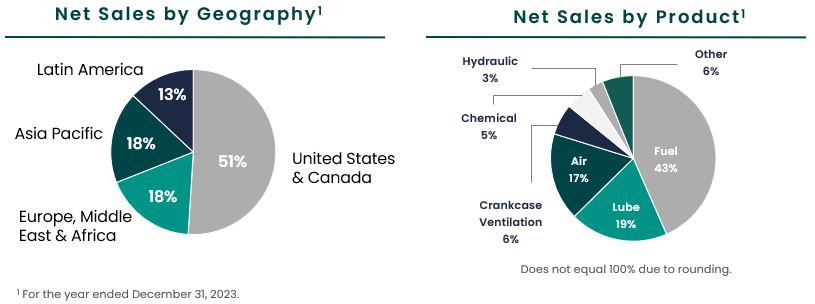

Atmus is one of the global leaders of filtration products for on-highway commercial vehicles and off-highway agriculture, construction, mining and power generation vehicles and equipment. Atmus designs and manufactures advanced filtration products, principally under the Fleetguard brand, that enable lower emissions and provide superior asset protection. Atmus estimates that approximately 19% of Atmus’ net sales in 2023 were generated through first-fit sales to original equipment manufacturers (“OEM”s), where Atmus’ products are installed as components for new vehicles and equipment, and approximately 81% were generated in the aftermarket, where Atmus’ products are installed as replacement or repair parts, leading to a strong recurring revenue base. Building on Atmus’ 65-year history, Atmus continues to grow and differentiate itself through its global footprint, comprehensive offering of premium products, technology leadership and multi-channel path to market.

For the year ended December 31, 2023, Atmus generated $1,628.1 million in Net sales, $171.3 million in Net income and $302.3 million in Adjusted EBITDA. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Non-GAAP Measures” in this Annual Report on Form 10-K for a description of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to Net income, the most directly comparable financial measure calculated in accordance with U.S. GAAP.

Atmus’ Business Strategy

Grow share in first-fit in core markets

Atmus’ organic first-fit growth opportunities are centered on four pillars:

•Grow market share with leading OEMs: Atmus benefits from deep relationships with leading OEMs. Atmus’ technology innovations, global footprint and preferred brand position it well to grow along with the leading OEMs. As Atmus’ OEM partners continue to grow in share and through consolidation of their respective markets, Atmus will partner with them to grow. This growth with OEMs in turn increases the installed base for its products, which drives recurring aftermarket revenue.

•Support technology transitions with leading OEMs: Atmus plans to further build on its relationship with OEMs as they transition to alternate fuel technologies, such as hydrogen-powered internal combustion engines, battery electric vehicles and fuel cell electric vehicles. Based on currently available technology and Atmus’ assessment of products being developed, Atmus believes that, although battery-electric vehicles may have lower levels of filtration content than internal combustion engine vehicles, other technologies such as hydrogen-powered internal combustion engines or fuel cell electric vehicles may have similar levels of filtration content as internal combustion engine vehicles. Some of Atmus’ current developments in the zero emissions space include hydrogen water separators, air filtration products,

4

coolants and deionizing water filters. Atmus currently has a number of alternative fuel development programs underway with its existing customer base in the zero emissions space. Atmus is well positioned for the broader transition of technology through its existing relationships with customers.

•Enhanced product content per vehicle: Atmus has a focus on offering system modules and highly integrated solutions as customers and end-users seek improved filtration performance and quality, which it believes will result in increased first-fit content per vehicle. Atmus is also extending into smart filtration solutions, including embedded sensors, prediction algorithms and data analytics tools.

•Accelerate new product development: Atmus is accelerating its new product development cycle by continued investment in advanced system level testing capabilities, leveraging in-house 3D printing capabilities, utilizing powerful simulation tools and applying machine learning tools throughout its product development cycle.

Accelerate profitable growth in the aftermarket

Atmus estimates that aftermarket net sales represented approximately 81% of its total net sales in 2023, and has significant opportunity for further growth through these strategic initiatives:

•Expand Atmus’ product portfolio: Offering a comprehensive product portfolio provides a ‘one-stop shop’ for Atmus’ customers. Atmus offers a wide range of products to ensure product coverage and continues to release new products on a yearly basis. Atmus has launched approximately 300 new products annually, on average, over the last three years. Atmus has a team dedicated to tracking new filter releases and strategically selecting the type and quantity of products to launch each year to ensure optimal product coverage. Recent product launch focus has trended towards more targeted and focused product releases.

•Use analytics to target and capture growth opportunities: Atmus will continue to develop and enhance analytic tools, including using machine learning and artificial intelligence, to identify cross-sell or up-sell opportunities, and new or underserved customers, and precisely estimate the opportunity for additional sales of its Fleetguard-branded products. Atmus works directly with end-users or through its channel partners to define, track and measure opportunities and conversion rates.

•Expand reach through multi-channel distribution: It is important that Atmus can reach end-users no matter where they are, or how they choose to purchase Atmus products. Atmus continues to expand its presence with OEM dealers, independent distributors, service centers and retail outlets.

•Invest in product technology advantage to enhance value and protect revenue: Where Atmus is the first-fit, it increases customer retention on aftermarket opportunities by using advanced technologies and proprietary product designs that drive improved performance and create preference for its products. Where Atmus is not the first-fit, it continues to develop products that meet or exceed the first-fit product, supporting its brand position as premium quality and performance, and leading to high customer loyalty.

Transform Atmus’ supply chain

Atmus is focused on transforming its supply chain to improve customer experience, which is expected to drive growth and reduce overall cost, leading to margin enhancement. Atmus’ strategic initiatives have four pillars:

•Drive services and availability: Synchronize global planning across the network to focus on on-shelf availability.

•Optimize network: Invest in its physical footprint to provide superior availability while minimizing material and part movement.

•Transform cost structure: Optimize supplier management and spend and increase throughput across Atmus’ network of plants and increase automation.

•Invest in capabilities for the future: Deploy robust processes across the organization from forecasting through customer orders to fulfillment, and invest in critical global systems infrastructure to provide best-in-class functionality.

5

Expand Atmus’ technology and diversify its distribution channels beyond its core markets

Atmus is focused on building sustainable growth by expanding and diversifying into the industrial filtration market, which includes machinery and equipment, oil and gas, pharmaceuticals, food and beverage and metals and mining. Atmus believes it can leverage its global footprint and existing technical capabilities, including its proprietary filtration media technology, into these markets to open new opportunities for growth. Atmus anticipates achieving this by expanding its focus to include non-engine products that it can sell to its current and new customers within its existing markets by utilizing its global footprint. Atmus is working on developing capabilities, whether organically or through acquisitions or strategic partnerships, to enter new markets with long-term growth prospects which will further diversify its revenue base. To the extent that Atmus considers acquisitions, it will apply a disciplined financial framework in assessing these opportunities.

Atmus’ Global Footprint

Atmus serves end-users globally, with approximately 49% of its Net sales in 2023 from outside of the United States and Canada. Atmus believes that it, together with its joint ventures in China and India, has a leading position in its core markets, based on Net sales in 2023. Atmus maintains strong global customer relationships, supported by an established salesforce with work locations in 25 countries as of December 31, 2023. Also, as of December 31, 2023, Atmus operates through 11 distribution centers, 10 manufacturing facilities and five technical facilities plus 10 manufacturing facilities and two technical facilities operated by its joint ventures, giving Atmus presence on six continents.

Atmus’ Premium Products

Atmus offers a full spectrum of filtration solutions that enable lower emissions and provide superior asset protection. Atmus’ filtration products provide comprehensive and differentiated solutions, which allow its end-users to extend service intervals, reduce maintenance costs and increase uptime. Atmus’ products include fuel filters, lube filters, air filters, crankcase ventilation, hydraulic filters and coolants and other chemicals. Atmus’ broad range of products in each of its core markets enables one-stop shopping, which Atmus believes is a key competitive advantage.

6

Atmus’ Markets

Atmus believes the filtration product market is large and attractive, with estimated total product sales of approximately $80 billion in 2022, of which Atmus believes the total engine products market — consisting of its core markets and the passenger car market — was approximately $32 billion. Within the total engine products market, Atmus estimates that its core markets had a total addressable market of approximately $14 billion in 2022, having grown by approximately 4% compounded annual growth rate (“CAGR”) over the last five-year period ending in 2022. Atmus estimates that the passenger car market, which it does not currently and does not expect in the future to focus on, had a total addressable market of approximately $18 billion in 2022. The balance of the filtration product market is made up of industrial filtration markets, which Atmus estimates had a total addressable market of approximately $48 billion in 2022. Atmus’ strategy includes a focus on expanding into industrial filtration markets in the future; these markets have grown by approximately 7% CAGR over the five-year period ending 2022. We believe that inflation was a significant contributor to market growth during the

five-year period ending 2022. Looking ahead, excluding inflationary impact, Atmus expects the industrial filtration markets to grow by approximately 4.5% CAGR and its core markets by approximately 2% CAGR, in each case through the five-year period ending in 2027.

The engine filtration market is impacted by the following key drivers and trends:

•Growth in freight volumes (on-highway) and industrial activity (off-highway): Atmus believes broader economic growth is a strong indicator for its business. The U.S. Bureau of Transportation Statistics’ Freight Analysis Framework forecasted (as of November 2023) that between 2023 and 2050 U.S. freight volume will increase by approximately 50%, and expected that trucks will remain the predominant freight carrier in the near future. Off-highway activity is correlated with the overall construction industry. Dodge Construction Network predicted (as of November 2023) that the overall U.S. construction industry will rise 7% in 2024 after growth slowed to just 1% in 2023. It is expected that the first half of 2024 will see slower growth compared to the second half of the year. The Construction Industry Databook expects (as of October 2023) U.S. construction output to grow at 5.3% CAGR from 2023 to 2027.

•Growth in emerging markets: Global growth in core markets is being driven by macro-economic expansion, including the build-out of infrastructure. Asian markets, including India, are currently positioned for high growth. According to the International Monetary Fund (IMF), from 2018 to 2023, gross domestic product in India has grown at a compounded annual growth rate of 4.0%. The growth in India is primarily driven by the increasing demand for transportation as well as emission regulations. The growth in China was depressed in 2022 due to the COVID-19 response and remained constrained in 2023 due to declining economic conditions. China had experienced high growth in the prior years and Atmus expects a partial recovery over the next few years. Gross domestic product in China has grown at a compounded annual growth rate of 4.9% from 2018 to 2023 according to the IMF.

•More stringent emissions standards: Atmus’ core markets will need to comply with more stringent regulatory standards on emissions driving the requirement for higher quality, increased content and higher priced filtration systems.

•Technology transition: There is broad based recognition that GHG emissions are driving climate change. Increasingly, Atmus’ customers, governments, and investors are making commitments to reduce their GHG emissions, including pledges to achieve net zero GHG emissions by 2050. While the pace of adoption will vary by region, Atmus’ core markets may be impacted by technology transitions, including transition to battery-electric vehicles, fuel cell electric vehicles and alternate power sources.

Atmus’ Competitive Strengths

Technology leadership and deep industry knowledge enable Atmus to deliver better customer solutions

Atmus combines a culture of innovation with deep-seated experience in its industry to deliver superior filtration solutions for its customers. Atmus’ technical team develops a range of filtration technologies, including filtration media, filter element formation, filtration systems integration and service-related solutions such as remote digital diagnostic and prognostic platforms and analytics. Atmus’ technical team of approximately 350 engineers, scientists and technical specialists are located in five technical centers around the world, with approximately 25% holding advanced technical degrees. Atmus’ team draws on a 65-year history focused on

7

filtration and media technologies. Atmus has a broad IP portfolio with over 1,275 worldwide active or pending patents and patent applications and over 600 worldwide trademark registrations and applications as of December 31, 2023.

Atmus has leveraged this expertise not only to develop its cutting-edge filters, filter systems and filtration media but also to manufacture a large portion of its proprietary filtration media. This allows Atmus to move swiftly from development to application of filtration technologies that protect and enhance the operation of its customer’s equipment and machines. StrataPore, NanoNet, NanoForce, and most recently, NanoNet Plus product families have enabled engines and equipment to meet continually changing emissions and performance requirements.

Atmus’ technical team works closely with Atmus’ customers to develop and apply filtration technologies that help them improve their operations. For example, Atmus helped a key customer and partner in China to be one of the first to extend maintenance intervals on both lube and fuel filtration systems from 20,000 kilometers to 100,000 kilometers. Additionally, Atmus’ NanoNet Plus fuel filtration and fluid control systems have delivered fuel system component protection meeting stringent European and North American requirements while still providing enhanced service intervals, and Atmus’ eRCV product families continue to offer crankcase emissions performance control across European, North American, and China-based customers. Atmus’ technology allows it to deliver performance-enabling and customized filtration solutions for its end-users, which creates long-lasting partnerships with its customers.

Iconic Fleetguard brand with premium products

Atmus believes that Fleetguard is a premium, leading brand that is strongly associated with reliability and strong performance. Atmus offers a full suite of Fleetguard-branded filtration products. With its broad line of high-quality filtration products, Atmus’ Fleetguard brand provides filters for nearly all makes of vehicles and equipment in its core markets, which further enhances Atmus’ availability, visibility and brand recognition. Atmus’ Fleetguard brand is further supported by a competitive warranty that gives Atmus’ customers and end-users high confidence in the performance and durability of its products.

Partnering with leading OEMs

Atmus has a strong history as a supplier to leading OEMs, including Cummins, Daimler, Deere, Doosan, Foton, Komatsu, Paccar/DAF, the Traton Group (Navistar/Scania/MAN), Stellantis and Volvo. Atmus sells both first-fit and aftermarket products to these customers and has been selling to each of them for at least 10 years. These customers in the aggregate accounted for approximately 67% of Atmus’ net sales in 2023 and have consistently accounted for more than 67% of Atmus’ net sales in each of the last five years. Atmus has written agreements with most of its key customers that specify certain purchase parameters, but do not obligate them to specific volumes. Atmus invests in its relationships and utilizes its technical strengths to win first-fit business with these OEMs, which drives Atmus’ installed base, yielding strong recurring revenue streams in the aftermarket. The OEMs also provide Atmus with early insight into technological developments and evolving product requirements within the broader engine and industrial application industry, allowing Atmus to be well positioned as the world shifts towards more complex modular filtration systems and filtration for other power sources.

Cummins is Atmus’ largest customer and accounted for approximately 17.4% of Atmus’ net sales in 2023. This relationship is defined by the first-fit supply agreement and the aftermarket supply agreement. These supply agreements will help give Atmus visibility and stability to its future sales within the terms of the agreements. In addition, for 65 years prior to the Separation, Atmus’ sales and technical teams have been embedded with Cummins, allowing Atmus to have a deep understanding of their needs, which enables Atmus to deliver high-quality, high-performance products that deliver value to Cummins. Atmus partners with Cummins in all regions to win end-user accounts in the aftermarket and create a preference for the Fleetguard brand.

Multi-channel path to diverse global markets

Atmus’ global presence provides a diverse and stable customer base across truck, bus, agriculture, construction, mining and power generation vehicles and equipment markets. Atmus’ current core markets are on-highway and off-highway, representing approximately 60% and 40% of Atmus’ net sales in 2023, respectively.

8

Atmus estimates that approximately 81% of Atmus’ net sales in 2023 were generated in the aftermarket.

To drive these net sales, Atmus has developed a multi-channel path to global markets that ensures broad product availability and provides end-users with choice and flexibility in purchasing. Atmus distributes its products through a broad range of OEM dealers, independent distributors, and retail outlets, including truck stops.

The dealers of the OEMs are typically the channel preferred by customers in many markets. Atmus’ close relationships with the OEMs and strong first-fit installed base position Atmus well with the OEM dealer network and large fleet customers. For example, the dealers of four of the largest North America on-highway OEMs carry a significant range of Atmus’ products at their dealerships.

In addition, Cummins distributors, independent distributors and retailers enable Atmus to reach a broader end-user market and create additional points of sale or service. Atmus also works directly with major customers of its channel partners (such as large fleets or mining companies), across its end markets, to create strong brand preference, which, in turn, leads to strong demand for its products and generates recurring revenue. Atmus continues to increase geographic coverage within regions to better serve its customers by investing in distribution expansion.

Atmus typically ships directly from its 11 distribution centers (as of December 31, 2023) worldwide to its channel partners, which provides direct connection and detailed understanding of Atmus’ customer and end-user base. Atmus’ comprehensive distribution and market coverage are vital to maintaining its broad reach, global presence and brand recognition.

Comprehensive aftermarket coverage and large installed base

Atmus has a large installed base driven by first-fit relationships with leading OEMs, leading to long product life cycles and a strong stable revenue base. In the last few years Atmus’ business strategy has put increased focus on releasing first-fit OEM parts, which Atmus believes will increase aftermarket retention. Atmus’ large installed base protects against cyclicality in truck sales and creates a long tail of revenue due to the long lifespans of commercial vehicles and equipment, together with the extensive aftermarket service they require throughout their useful lives. For example, the LF670 filter was first installed on trucks in the 1970s and continues to generate an aftermarket revenue stream approximately 50 years post launch. Aftermarket product sales tend to have a higher profit margin, relative to first-fit systems, driving higher operational cash flow and stability throughout the business cycle.

Atmus’ end-user relationships provide critical market intelligence that help drive up-sell and cross-sell opportunities, while providing Atmus direct visibility to market opportunities. Additionally, these end-user relationships enable Atmus to accelerate the launch of a broad range of products where it is not the first-fit.

Scalable global manufacturing operations

Atmus maintains a global manufacturing footprint with highly capable manufacturing facilities in six continents. As of December 31, 2023, Atmus had 10 manufacturing sites for Atmus, and 10 for its joint ventures, allowing it to maintain proximity with its customers and global scale. All of Atmus’ manufacturing facilities that are currently in production have obtained either ISO 9001 or ISO/TS 16949 quality management certifications. Additionally, Atmus’ global warehousing footprint enhances this proximity with 11 distribution centers (as of December 31, 2023) strategically located around the world.

9

Atmus’ significant volumes allow Atmus to take advantage of economies of scale. Atmus has invested strategically in automation and optimization of core filtration manufacturing processes to deliver cost efficiencies.

Attractive margins and strong operating cash flow generation

Atmus’ business benefits from attractive margins and a track record of strong cash flow generation. Atmus’ high percentage of recurring revenue, relative to other industrial businesses, helps mitigate market cyclicality and revenue volatility. Atmus realized a net income margin of 10.5% and an Adjusted EBITDA margin of 18.6% in 2023. Atmus’ business is resilient, which is evidenced by the fact that, despite the changes in economic conditions due to the COVID-19 pandemic, Atmus’ net sales rebounded with a 16.7% increase in 2021 (as compared to 2020), increased by 8.6% in 2022 (as compared to 2021) and increased by 4.2% in 2023 (as compared to 2022). Atmus generates strong operating cash flow from operations with high cash flow conversion, delivering $564.6 million from 2021 through 2023.

Experienced leadership team with a proven track record of driving growth

Atmus is led by an energized and experienced senior leadership team with extensive industry experience with Cummins and other leading industrial companies. Atmus’ strategic vision and culture are directed by its executive leadership team under the leadership of its Chief Executive Officer, Stephanie J. Disher, its Chief Financial Officer, Jack Kienzler, its Chief People Officer, Renee Swan, its Chief Legal Officer, Toni Y. Hickey and its Vice President, Engine Products, Charles Masters. Stephanie J. Disher joined Cummins in 2013 and has over 20 years of experience in leadership positions, including international assignments in Australia, Asia, and the United States. Most recently, Stephanie J. Disher served as Vice President of Cummins Filtration where she has demonstrated a continued track record of strong business performance, innovation and operational excellence. Jack Kienzler joined Cummins in 2014 and has over 14 years of finance experience. He most recently served as the Executive Director of Investor Relations at Cummins, having formerly led the Corporate Development team. Renee Swan joined Atmus in August 2023 and has over 20 years of experience in human resources and talent management. Toni Y. Hickey joined Cummins in 2012 and has over 24 years of experience as an intellectual property lawyer. Charles Masters joined Cummins in 2003 and has over 20 years of experience in global sales and operational leadership roles within Cummins. Atmus’ leadership team has the ability to develop and execute its strategic vision and aims to create long-term shareholder value. Atmus benefits from its team’s industry knowledge and track record of successful product innovation and financial performance. Additionally, members of Atmus’ senior leadership team have strong experience executing and integrating acquisitions and strategic partnerships to drive accelerated growth and improved profitability.

History

Atmus’ business was founded in 1958, beginning with a single filter production line developed by Cummins Engine Company in Seymour, Indiana to meet the high performance requirements of Cummins diesel engines. As early as 1963, Cummins initiated the Fleetguard brand, which is a well-recognized brand in Atmus’ core markets. In 1987, the India Fleetguard joint venture was established and in 1994 a joint venture in China was formed as Cummins continued to enter emerging markets. In 2006, Atmus’ wholly owned subsidiary China Filtration was established, and in 2010, the Korea media facility was opened. In 2016, an India technology facility was opened and Atmus moved to a new corporate headquarters in Nashville.

Supply

The performance of the end-to-end supply chain, extending through to Atmus’ suppliers, is foundational to its ability to meet customers’ expectations and support long-term growth. Atmus is committed to having a robust strategy for how it selects and manages its suppliers to enable a market focused supply chain. This requires Atmus to continuously evaluate and upgrade its supply base, as necessary, as Atmus strives to ensure it is meeting the needs of its customers.

Atmus uses a combination of proactive and reactive methodologies to enhance its understanding of supply base risks, which guide its development of risk monitoring and sourcing strategies. Atmus’ category sourcing strategy process (a process designed to create the most value for the company) supports the review of its long-term needs and guides decisions on what it makes internally and what it purchases externally. For the items Atmus decides to purchase externally, the strategies also identify the suppliers it should partner with long-term to provide the best technology, the lowest total cost and highest supply chain performance. Key suppliers are

10

managed through long-term supply agreements that secure capacity, delivery, quality and ensure cost requirements are met over an extended period.

Other important elements of Atmus’ sourcing strategy include:

•selecting and managing suppliers to comply with its Supplier Code of Conduct; and

•assuring its suppliers comply with its prohibited and restricted materials policy.

Atmus monitors supply chain disruptions and conducts structured supplier risk and resiliency assessments. Atmus increased the frequency of its formal and informal supplier engagement to address potentially impactful supply base constraints and enhanced collaboration to develop specific countermeasures to mitigate risks. Atmus’ global team, located in different regions of the world, uses various approaches to identify and resolve threats to supply continuity.

Supply chain disruptions can impact Atmus’ business as well as its suppliers and customers, resulting in longer lead times in some areas of its business. Orders are typically issued as rolling releases with a specific lead time. When these orders are on backlog, they are often subject to cancellation on reasonable notice without cancellation charges, and therefore are not considered firm. Atmus is working closely with its customers to meet demand and work through backlogs as efficiently as possible.

Materials

The principal materials that Atmus uses directly in manufacturing its products are steel, filter media and petrochemical-based products, including plastic, rubber and adhesives products. In 2023, material costs represented approximately 57% of Atmus’ cost of sales, compared to 61% of Atmus’ cost of sales in 2022.

Customer Concentration

Atmus has thousands of customers around the world and has developed long-standing business relationships with many of them. Cummins is Atmus’ largest customer, accounting for approximately 17% of Atmus’ net sales in 2023 and 19% in 2022 and 2021, respectively. In connection with the Separation, Atmus entered into a first-fit supply agreement and an aftermarket supply agreement with Cummins for Atmus’ first-fit and aftermarket products. These agreements provide for continuation of Atmus’ supply to Cummins for all of its first-fit applications that Atmus currently supports, commitment to first-fit supply for certain upcoming product launches, and continued supply to Cummins of its full line of aftermarket filtration needs. It does not commit a specific volume of filters or related products. The loss of this customer or a significant decline in the production level of Cummins engines that use Atmus’ filters would have an adverse effect on Atmus’ business, financial condition, results of operations or cash flows.

In addition to the agreement Atmus entered into with Cummins, Atmus has long-term agreements with many of its largest customers. Collectively, Atmus’ net sales from its next four top customers, other than Cummins, was approximately 39% of Atmus’ net sales in 2023, 39% in 2022 and 37% in 2021. Excluding Cummins, two other customers, PACCAR and the Traton Group, accounted for more than 10% of Atmus’ net sales in 2023. Atmus’ customer agreements typically contain standard purchase and sale agreement terms covering filter pricing, quality and delivery commitments, as well as engineering product support obligations. The basic nature of Atmus’ agreements with OEM customers is that they are long-term price and operations agreements that provide for the availability of Atmus’ products to each customer through the duration of the respective agreements. Where Atmus has such agreements in place, its customers typically place purchase orders with it pursuant to these agreements. Agreements with most OEMs contain bilateral termination provisions giving either party the right to terminate in the event of a material breach, change of control or insolvency or bankruptcy of the other party.

Intellectual Property

Atmus owns or controls a broad range of intellectual property rights, including a significant number of patents, trademarks, copyrights, trade secrets and other forms of intellectual property rights in the United States and foreign countries. Atmus has a broad IP portfolio with over 1,275 worldwide active or pending patents and patent applications and over 600 worldwide trademark registrations and applications as of December 31, 2023, which were granted and registered over a period of years. Atmus’ leading brand house trademark is Fleetguard.

11

Atmus protects its innovations that arise from research and development through patent filings, as well as through trade secrets. Although these patents, trademarks and trade secrets are generally considered beneficial to Atmus’ operations, Atmus does not believe any patent, group of patents, trademark or trade secret is solely responsible for protecting its products.

Research and Development

In 2023, Atmus continued to invest in future critical technologies and products. Atmus will continue to make investments to develop new technologies and improve its current products to meet increasing and changing emissions and engine performance requirements globally for diesel and hydrocarbon-powered equipment. In addition to building on its core technologies, Atmus is making investments in filtration and separation technologies required and used by electric powered vehicles, hydrogen production and other industrial systems.

Atmus’ research and development programs are focused on product improvements, product extensions, innovations and cost reductions for its customers. Research and development expenditures include salaries, contractor fees, building costs, utilities, testing, technical IT, administrative expenses and allocation of corporate costs and are expensed when incurred. Research and development expenses were $42.3 million, $38.5 million, and $41.6 million for the years ended December 31, 2023, 2022 and 2021, respectively.

Seasonality

While individual product lines may experience modest seasonal variation in production, there is no material effect on the demand for the majority of Atmus’ products on a quarterly basis.

Competition

Atmus is a leading global participant in the filtration engine products markets. Atmus’ products include fuel filters, lube filters, air filters, crankcase ventilation, hydraulic filters and coolants and other chemicals. Key global participants in this market include MANN+HUMMEL, Donaldson, Parker and MAHLE. The rest of the market is highly fragmented and occupied by various specialized and regional players. Most of the large global players serve both first-fit and aftermarket channels, while smaller, regional players tend to focus on the aftermarket. The filtration market offers a unique multi-channel path to market, and diversification across first-fit, OEM service and aftermarket. The recurring revenue model and mission-critical role of filters drive consistent demand across regions and end markets.

Principal methods of competition in the filtration markets are product quality and performance, price, geographic and application coverage, availability, customer service, ease of doing business and brand reputation. Atmus believes it is a market leader within many of its product lines, including filters in Atmus’ on-highway and off-highway markets, and that its success in the market is due to its technology, its iconic Fleetguard brand, its global footprint, strong customer relationships and the talent within its organization.

Human Capital Resources

As of December 31, 2023, Atmus employed approximately 4,500 persons worldwide. As of December 31, 2023, approximately 53% of Atmus’ employees worldwide were represented by various unions under collective bargaining agreements. Among these collective bargaining agreements, those for the employees in Mexico, Brazil and France are renewed annually after compensation negotiations, while the collective bargaining agreement for the Cookeville, Tennessee plant typically has a four- to five-year term. The collective bargaining agreement for Brazil is in place and active and the compensation negotiations for a new annual term on the collective bargaining agreements for Mexico and France were recently concluded. These collective bargaining agreements have terms that will expire between December 2024 and February 2025. The collective bargaining agreement for the Cookeville, Tennessee plant is expiring at the end of its four year term on February 29, 2024 and negotiations for its renewal started in January 2024.

Throughout Atmus’ 65-year history, Atmus has always recognized that people are the strength of its business and drive its ability to effectively serve its customers and sustain its competitive position. Atmus believes that the composition of its workforce gives it advantages relating to cost and capability when compared to its peers. The global COVID-19 pandemic redefined the way Atmus has traditionally worked and created both new expectations by employees, as well as new ways to work flexibly and seamlessly on a global basis. Atmus is embracing these opportunities as Atmus simplifies its organizational structures and processes, further

12

empowers managers and employees to make decisions and generate positive results, increases employee communication and interaction with senior leadership and enhances a work environment that is inclusive, transparent, agile and team-oriented.

Purpose and Core Values

Atmus is a purpose-driven company. Atmus’ purpose is ‘Creating a better future by protecting what is important.’ Atmus creates and innovates every day. With a forward focus, Atmus never sits still. Atmus realizes the world is bigger than it, and it aspires for a better future for shared humanity. Atmus’ products protect its customers, their equipment and their livelihoods. Atmus protects what’s important to its people, the planet, and its customers.

Atmus’ culture is shaped by its core values:

•Build Trust in every relationship every day.

•Have Courage to speak up, take action and shape the future.

•Be Inclusive by embracing differences and building a community where everyone feels valued.

•Show Caring by engaging with kindness and consideration for the wellbeing of others.

Leadership and Talent Management

The capability of Atmus’ people and their ability to work effectively in agile teams is a primary enabler of Atmus’ success. Atmus strives to create a leadership culture that is authentic, transparent and approachable. By minimizing organizational layers, simplifying its organizational structure and process, Atmus empowers its employees to have an increased impact on its results. Atmus’ leaders are tasked with providing their employees with the support, development and encouragement needed to be successful. Further, Atmus’ leaders connect Atmus’ people and their work to Atmus’ purpose, values, brand promise and strategies. Atmus will continue to invest in leadership development. Atmus will maintain the emphasis that the primary role of leaders at all levels is to focus on people development, supporting the unique needs of each employee in reaching their greatest positive impact at work, in the community and at home.

Atmus’ talent management approach seeks to develop the skills and capabilities of a diverse, global workforce and utilize Atmus’ talent to deliver excellent results. Atmus advances and invests in its people based on strong performance, demonstration of core values in how work is accomplished and the individual motivation to have a larger impact on organization results.

Competitive Pay and Benefits

To attract and retain the best employees, Atmus maintains a positive work environment that is grounded in its core values, a leadership culture that supports the development of its people and competitive pay and benefits.

When designing its base pay compensation ranges, Atmus completes market analyses to maintain pay ranges that are current and related to the work it performs. Atmus also completes annual compensation studies to assess market movement for key skills as well as internal pay equity. Atmus incorporates living wage assessment into its annual compensation reviews to ensure that current and new hires are not below this threshold. Collectively, Atmus’ global wage assessments seek to ensure Atmus is fair, equitable and competitive in its ability to attract and retain the best talent. Everywhere possible, individual performance is the primary path for Atmus’ employees to advance their earning potential. In addition, all employees also participate in annual variable compensation plans that encourage collaboration in the achievement of overall business results.

Atmus’ benefit programs are aligned with Atmus’ values, target market competitiveness and offer flexibility to meet individual needs. Medical benefits include tiered health care costs that are more affordable to junior employees. Also included in Atmus’ offerings are employee assistance programs, vacation time, retirement and savings plans and a variety of paid and unpaid time-off options that seek to address personal needs and important life-events.

Employee Safety and Wellness

13

Atmus has a health, safety and environment commitment to protect what is important - its people, the planet and its customers. Every day, Atmus is committed to continually improve the health and safety of its work environment, taking action to achieve its goal that nobody gets hurt.

In pursuit of this goal, Atmus embraces a positive safety culture that encourages its employees to recognize potentially unsafe situations, report concerns and work together to remove potential hazards from the work environment before incidents occur. Additionally, Atmus’ Global Health and Safety Policy sets the standard for Atmus’ facilities based on best practices that often exceed regulatory requirements. Atmus manages its sites using the International Standards for Health, Safety and Environment to create a strong framework for risk reduction and continual improvement, with certification to ISO45001 and ISO14001.

Atmus encourages its leaders to promote safety through strategic planning, enforcement and accountability, fostering the right environment, and influencing employees and other stakeholders. Atmus encourages its employees to promote safety through personal accountability, managing risk, and adopting positive behaviors. By employing these safety guidelines, Atmus seeks to achieve its goal of zero serious injury fatalities caused by machinery safety hazards due to the lack of or failure of safety control measures.

Where Atmus identifies a risk, it ensures that improvement actions are shared across the organization to promote a learning-oriented culture where Atmus’ employees are empowered to make their work environment safer and better. Using leading indicators of performance, Atmus recognizes the contribution of individuals and teams to reinforce safe work behaviors in the workplace, homes and communities.

Diversity and Inclusion

Diversity and inclusion at all levels of Atmus are critical to its ability to innovate, win in the marketplace and create sustainable success. Having diverse and inclusive workplaces allows Atmus to attract and retain the best employees to deliver results for its shareholders. Building on a long history that has emphasized diversity and inclusion, Atmus will continue to seek opportunities and invest in processes that attract, develop and retain diverse talent, globally. Atmus will measure outcomes and ensure that all employees can benefit from being a part of Atmus. This starts by assuring that the leadership of Atmus is diverse. At this time, five out of Atmus’ 11 directors are female and four out of its 11 directors are ethnically diverse. In addition, 44% of Atmus’ executive team is female, including its Chief Executive Officer, and 22% is ethnically diverse.

Environmental Sustainability

Atmus is committed to ‘Creating a better future by protecting what is important.’ Atmus believes environmental sustainability is central to what it does and it is dedicated to serving as an environmental steward to proactively enable a cleaner and more sustainable world for its employees, its customers and its communities.

Sustainability is a continuous journey. As part of its journey, Atmus has embedded environmental initiatives across Atmus through its policies and procedures. Atmus establishes annual goals that focus on protecting employees while continuously reducing environmental impacts through pollution prevention, energy efficiency improvements and conservation, and water minimization.

From Atmus’ product portfolio choices to its production development processes, Atmus’ focus is on enabling a cleaner and more sustainable world. For Atmus’ customers and end-users, Atmus continues to deliver technology solutions that enable the adoption of cleaner and more efficient energy sources in their operations. Further, Atmus’ approach to product design enables customers and end-users to extend service intervals thereby reducing resource consumption and GHG emissions. In Atmus’ product development processes, Atmus’ intent is to select design and production strategies that enable energy conservation. This includes initiatives to reduce raw material and energy consumption, such as the selection of recycled materials in Atmus’ media and the use of specialized media in some of Atmus’ products to eliminate the need for curing ovens.

Atmus’ operations and facility management programs consistently look for opportunities to reduce Atmus’ impact. Atmus also voluntarily executes global environmental sustainability initiatives, including:

•Implementing green energy alternatives, including installing solar panels at its San Luis Potosi, Mexico plant and other manufacturing sites.

14

•Monitoring water consumption at its sites, setting reduction goals, and implementing water sustainability alternatives, including a rainwater harvest program for its desert garden at its San Luis Potosi plant to reduce water use.

•Implementing energy efficiency improvements at its facilities, including boilers in its Cookeville, TN plant, energy efficient air handling upgrades to its plant in Neillsville, WI and the installation of high efficiency LED lighting throughout Atmus’ site in Kilsyth, Australia.

During 2023, Atmus formally engaged its stakeholders, with the assistance of a third-party sustainability consultant, and completed a double materiality assessment. This assessment is a rigorous, industry-aligned process designed to evaluate and prioritize Environmental, Social and Governance topics based on stakeholders’ own goals and objectives both in terms of its implications for the company's financial value, as well as the company's impact on the world at large. Atmus is reviewing and considering these results as Atmus further refines its sustainability goals and targets.

Joint Ventures

Atmus has entered into three joint ventures with business partners, two in India, and one in China. Atmus’ joint ventures operate either manufacturing facilities or manufacturing and technology centers.

Atmus’ manufacturing joint ventures are primarily intended to allow Atmus to increase its market penetration in geographic regions, reduce capital spending, streamline its supply chain management and develop technologies. Atmus’ largest manufacturing joint ventures are based in China and India, and are included in the list below. The results and investments in Atmus’ joint ventures in which Atmus has 50% or less ownership interest that are discussed below are not consolidated in its financial results and are instead included in “Equity, royalty and interest income from investees” and “Investments and advances related to equity method investees” in its Consolidated Statements of Net Income and Consolidated Balance Sheets, respectively.

•Fleetguard Filters Private Ltd. (FFPL) is a joint venture with its partner, Perfect Sealing Systems Private Ltd., that manufactures and sells industrial filters and coolant for commercial vehicles and generators and operates seven manufacturing facilities throughout India. Atmus directly held 49.491% of the economic interest and 50% of the voting interest during the three-year period ended December 31, 2023.

We previously disclosed that the transactions to implement our initial public offering, the separation and the splitoff would constitute a change in control under the governing documents of FFPL, resulting in the loss of rights to board representation which would effectively result in the loss of the ability to prevent certain significant actions and could result in a reduction or elimination of dividends. Subsequent to the initial public offering, based on mutual commercial agreement between the parties, FFPL and the joint venture partners have amended the FPPL Articles of Association to, among other matters, eliminate the change in control provision and revise certain economic provisions.

•Filtrum Fibretechnologies Pvt. Ltd. (Filtrum) is a joint venture with its joint venture partner, FFPL, and four other individuals (who collectively hold an approximate 25% interest), that manufactures filter media for automotive and industrial applications, and is located in Pune, India. Atmus held a 49.75% economic interest (25% directly and 24.75% indirectly through its proportionate ownership of FFPL’s 50% ownership interest) during the three-year period ended December 31, 2023.

•Shanghai Fleetguard Filter Co, Ltd. (SFG) is a joint venture with its partner, Dongfeng Electronic Technology Co. Ltd., that manufactures and distributes various filter and filter spare parts and operates three manufacturing facilities throughout China. Atmus held a 50% indirect ownership share during the three-year period ended December 31, 2023.

Atmus’ joint venture facilities are as follows:

Manufacturing

China: Wuhan (206,000 square feet), owned

China: Shiyan (47,000 square feet), owned

15

India: Dharwad (157,000 square feet), owned

India: Hosur (90,000 square feet), owned

India: Jamshedpur (26,500 square feet), owned, (21,000 square feet), leased

India: Sitarganj (87,500 square feet), owned

India: Loni (173,000 square feet), leased

India: Wadki (63,000 square feet), leased

Manufacturing and technology

China: Shanghai (148,000 square feet), leased

India: Nandur (97,000 square feet), owned, (33,000 square feet), leased

Financial information about Atmus’ investments in joint ventures and alliances is incorporated by reference from Note 5, Investments in Equity Investees, to Atmus’ historical consolidated financial statements.

Atmus will continue to evaluate joint venture and partnership opportunities in order to penetrate new markets, develop new products and generate manufacturing and operational efficiencies.

Regulatory Matters

Atmus faces extensive government regulation both within and outside the United States relating to the development, manufacture, marketing, sale and distribution of its products, including regulations relating to data privacy, trade compliance, anti-corruption and anti-bribery. These are not the only regulations with which Atmus must comply. For a description of risks related to the regulations that Atmus is subject to, please refer to the section entitled “Risks Related to Government Regulation.”

Legal Proceedings

Atmus is, from time to time, subject to a variety of litigation and other legal and regulatory proceedings and claims incidental to Atmus. Please refer to Note 14, Commitments and Contingencies, to the consolidated financial statements appearing elsewhere in this Annual Report on Form 10-K for more information.

Available Information

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other information, including amendments to those reports, available free of charge through its website at investors.atmus.com, as soon as reasonably practicable after it electronically files such material with, or furnishes such material to, the Securities and Exchange Commission (SEC). These filings are available on the SEC’s website at www.sec.gov.

16

MANAGEMENT OF ATMUS

Executive Officers

The following table sets forth information, as of February 14, 2024, regarding the individuals who serve as Atmus’ executive officers, followed by a biography of each executive officer.

| Name | Age | Position | |||||||||

Stephanie J. Disher | 48 | Chief Executive Officer | |||||||||

| Jack Kienzler | 38 | Chief Financial Officer | |||||||||

| Renee Swan | 43 | Chief People Officer | |||||||||

Charles Masters | 51 | Vice President, Engine Products | |||||||||

Toni Y. Hickey | 50 | Chief Legal Officer and Corporate Secretary | |||||||||

Stephanie J. Disher currently serves as Atmus’ Chief Executive Officer. Ms. Disher previously served as Vice President of Cummins Filtration Inc. Prior to that role, Ms. Disher served in various leadership roles since joining Cummins in 2013, including as Operations Director and Managing Director for Cummins in the South Pacific region. Ms. Disher holds a bachelor’s degree in Commerce from the University of Western Sydney and a Master of Business Administration from the University of Melbourne.

Jack Kienzler currently serves as Atmus’ Chief Financial Officer. Mr. Kienzler previously oversaw the financial activities of Cummins Filtration Inc. as its Chief Financial Officer. Mr. Kienzler served in various leadership roles since joining Cummins in 2014. Mr. Kienzler holds a Bachelor of Science in Finance and Accounting from Indiana University and a Master of Business Administration from the Indiana University Kelley School of Business.

Renee Swan currently serves as Atmus’ Chief People Officer. Ms. Swan previously served as Vice President of Human Resources for the communication systems segment of L3Harris Technologies, Inc. Ms. Swan has over two decades of experience in human resources disciplines, having spent time with Kennametal, Honeywell International, and Eaton Corporation in progressive human resources responsibilities. Ms. Swan has a Master of Professional Studies in Human Resource Management from Cornell University, a Master of Business Administration degree from Point Park University and a Bachelor's in Communications from the University of Pittsburgh.

Charles Masters currently serves as Atmus’ Vice President, Engine Products and previously served as Executive Director of Global Sales and Marketing of Cummins Filtration Inc. Prior to that role, Mr. Masters served in various leadership roles since joining Cummins in 2003, including as General Manager of Eaton Cummins Automated Transmission Technologies from 2018 to 2021 and as President of Cummins Western Canada from 2016 to 2018. Mr. Masters holds a Bachelor of Commerce from the University of Alberta and a Master of Business Administration from Harvard Business School.

Toni Y. Hickey currently serves as Atmus’ Chief Legal Officer and Corporate Secretary. Ms. Hickey previously served as General Counsel of Cummins Filtration Inc., after serving as Deputy General Counsel and Chief Intellectual Property Counsel for Cummins from May 2015 to August 2021. Ms. Hickey has a Bachelor of Science in Finance and Accounting from the University of Colorado — Boulder, and a Juris Doctorate from Southern Methodist University School of Law.

Item 1A. Risk Factors

These risk factors could materially affect our business, financial condition, results of operations and cash flows. These risk factors are not exhaustive and investors are encouraged to perform their own investigation with respect to the business, financial condition and prospects of our business. You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K for the fiscal-year ended December 31, 2023, and should also carefully consider the matters addressed in the section herein entitled “Cautionary Statements and Risk Factor Summary.” We may face additional risks and uncertainties that are not presently known to us, or that we currently deem immaterial, which may also impair our business, financial condition, results of operation or cash flows. The following discussion should be read in conjunction with the “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements and notes to the financial statements included herein.

17

Summary of Risk Factors

The following summarizes the risks facing our business, all of which are more fully described below. This summary should be read in conjunction with the risk factors below and should not be relied upon as an exhaustive summary of the material risks facing our business. The order of presentation is not necessarily indicative of the level of risk that each factor poses to us.

Risks Related to Our Business Operations

•Significant customer concentration among Cummins, PACCAR, and the Traton Group.

•The loss of a top OEM relationship, or changes in the preferences of Atmus' aftermarket end-users.

•Deriving significant earnings from investees that Atmus does not directly control.

•Significant competition in the markets Atmus serves.

•Evolving customer needs and developing technologies.

•Reliance on Atmus’ executive leadership and other key personnel.

•Strategic transactions, such as acquisitions, divestitures, and joint ventures.

•Management of productivity improvements.

•Work stoppages and other labor matters.

•Variability in material and commodity costs.

•Raw material, transportation and labor price increases and supply shortages.

•Complexity of supply chain and manufacturing.

•Atmus’ customers operating in cyclical industries and the current economic conditions in these industries.

•Exposure to potential claims related to warranties and claims for support outside of standard warranty obligations.

•Products being subject to recall for performance or safety-related issues.

•Inability or failure to adequately protect and enforce Atmus’ intellectual property rights and the cost of protecting or enforcing Atmus' intellectual property rights.

•Ineffective internal control over financial reporting.

•Unexpected events, including natural disasters.

Risks Related to Legal and Regulatory Issues

•Sales of counterfeit versions of products, as well as unauthorized sales of products.

•Statutory and regulatory requirements that can significantly increase costs.

•Changes in international, national and regional trade laws, regulations and policies affecting international trade.

18

•Unanticipated changes in Atmus' effective tax rate, the adoption of new tax legislation or exposure to additional income tax liabilities, as well as audits by tax authorities resulting in additional tax payments for prior periods.

•Changes in tax law relating to multinational corporations.

•Significant compliance costs and reputational and legal risks imposed by Atmus' global operations and the laws and regulations to which these are subject.

•Effects of climate change may cause Atmus to incur increased costs.

•Operations being subject to increasingly stringent environmental laws and regulations as well as to laws requiring cleanup of contaminated property.

Risks Related to Cybersecurity and Information Technology Infrastructure

•Potential system or data security breaches or other disruptions.

•Dependence on information technology infrastructure and assets that are increasing in complexity.

Risks Related to Finance and Financial Market Conditions

•Foreign currency exchange rate.

•Potential economic downturns that could cause the balances of recorded goodwill to decrease.

Risks Related to Macroeconomic and Geopolitical Conditions

•Political, economic, and social uncertainty in geographies where Atmus has significant operations or large offerings of products.

•Uncertain worldwide and regional market and economic conditions.

Risks Related to Atmus’ Relationship with Cummins

•The loss of Cummins’ reputation, economies of scale, capital base and other resources as a result of the Separation from Cummins.

•Potential failure of performance by Atmus or Cummins under transaction agreements executed as part of the Separation.

•Actual or potential conflicts of interests for certain of Atmus' executive officers and directors because of their equity interests in Cummins.

•Limited liability to Atmus from Cummins and its directors for breach of fiduciary duty.

•Potential indemnification liabilities to Cummins pursuant to the Separation Agreement.

Risks Related to Atmus’ Capital Structure

•Changes in capital and credit markets.

•Substantial indebtedness consisting of Atmus’ term loan and revolving credit facility, which may impact Atmus' ability to service all its indebtedness and react to changes in the industry.

Risks Related to Ownership of Atmus Common Stock

19

•Substantially all Atmus' assets being pledged as security for its term loan and revolving credit facility.

•Fluctuations in the price of Atmus Common Stock; and

•Applicable laws and regulations, provisions of Atmus' amended and restated certificate of incorporation and Atmus' bylaws and certain contractual rights granted to Cummins that may discourage takeover attempts and business combinations that stockholders might consider in their best interests.

Risks Related to Our Business Operations

We have significant customer concentration, with Cummins, PACCAR and the Traton Group respectively accounting for approximately 17.4%, 15.6% and 11.8% of our net sales for the year ended December 31, 2023. The loss of such net sales to any of such significant customers would have a material and adverse effect on our business, financial condition, results of operations and cash flows.

Cummins is our largest customer. For the year ended December 31, 2023, net sales to Cummins accounted for approximately 17.4% of our net sales. Sales to Cummins joint ventures and to distributors with which Cummins has a relationship also account for a portion of our net sales. A portion of our net sales is dependent upon customer acceptance of, and demand for, Cummins’ engines or generators that use our filters. This customer concentration increases the risk of fluctuations in our operating results and our sensitivity to any material adverse developments experienced by Cummins. While our relationship with Cummins is defined by our first-fit supply agreement and aftermarket supply agreement, we may fail in the future to renew these contracts, and, moreover, even if renewed, Cummins’ purchasing power may give it the ability to make greater demands on us with regard to pricing and contractual terms in general. In addition, Cummins may procure supplemental supply of top volume aftermarket products from alternative suppliers for a limited time if we fail to meet certain delivery performance requirements or if we do not offer a product or similar product for sale.

Cummins historically did not seek competitive bids for filtration products. However, prior to the completion of the IPO, Cummins initiated a competitive process to source a selective group of future first-fit programs and associated aftermarket products from its filtration product suppliers, including us. Subsequently, we were successful in being awarded this business. In the future, we expect that Cummins will continue to seek competitive bids for new filtration products and, while we will have a preferred supplier relationship with Cummins, we will have to successfully win bids through Cummins’ bidding process in order to maintain or grow our current level of sales to Cummins and cannot guarantee that Cummins will always select our products. The loss of, or any substantial reduction in sales to, Cummins would have a material adverse effect on our business, financial condition, results of operations and cash flows.

For the year ended December 31, 2023, net sales to PACCAR and the Traton Group accounted for approximately 15.6% and 11.8%, respectively, of our net sales. We cannot guarantee that PACCAR or the Traton Group will always choose to purchase our products. The loss or substantial reduction of sales to PACCAR or the Traton Group could materially and adversely affect our business, financial condition, results of operations or cash flows.

In addition, our association with Cummins has contributed to the relationships we have with certain significant customers due to the relationship those customers had with Cummins. We may not be able to attract new customers of Cummins, or retain existing customers, without Cummins’ support.

The loss of a top OEM relationship, or changes in the preferences of our aftermarket end-users, could adversely impact the recurring nature of our aftermarket sales.

We supply filtration products to many of the largest OEMs for both first-fit and aftermarket, which results in recurring revenue for our products. Our relationships with these OEMs also allow us to be closely attuned to our customers' requirements and preferences and react quickly to any changes. The use of our filtration products as a standard first-fit component creates a steady demand for that product in the aftermarket, as end-users often return to the OEM for aftermarket service for multiple years and may continue to prefer our products as replacement or repair parts.

We may not be able to maintain our current top OEM relationships in the future or may not become the preferred supplier for additional OEMs. In addition, our channel partners’ and end-users’ preferences for

20

replacement or repair filtration products may change in the future. The loss of a top OEM relationship, or changes in the preferences of our aftermarket end-users, could adversely impact the recurring nature of our aftermarket sales.

We derive significant earnings from investees that we do not directly control.

We earn equity, royalty and interest income from our joint venture in China — Shanghai Fleetguard Filter Co. Ltd., where we indirectly hold 50% of the economic interest. We also earn equity, royalty and interest income from our joint ventures in India — Fleetguard Filter Private Ltd. (“FFPL”), where we directly hold 49.491% of the economic interest (and 50% of the voting interest), and Filtrum Fibretechnologies Pvt. Ltd., where we hold, directly or indirectly, 49.75% of the economic interests (25% directly and 24.75% indirectly through our proportionate ownership of FFPL’s 50% ownership interest). For the year ended December 31, 2023, we recognized $33.6 million of equity, royalty and interest income from investees, compared to $28.0 million for the year ended December 31, 2022 and $32.4 million for the year ended December 31, 2021. Of these amounts, $21.5 million, $17.1 million and $16.4 million, respectively, were from our joint venture in India — FFPL. Although a significant percentage of our net income is derived from these unconsolidated entities (which were approximately 19.6% for the year ended December 31, 2023, approximately 16.4% for the year ended December 31, 2022 and 19.0% for the year ended December 31, 2021, of which approximately 12.6%, approximately 10.0% and approximately 9.6% were from FFPL for the year ended December 31, 2023, 2022 and 2021, respectively), we do not unilaterally control their management or their operations, which puts a substantial portion of our net income and cash flow through dividend payments at risk from the actions or inactions of these entities. A significant reduction in the level of contribution by these entities to our net income would likely have a material adverse effect on our business, financial condition, results of operations or cash flows.

We face significant competition in the markets we serve and maintaining a competitive advantage requires consistent investment with uncertain returns.

The businesses and product lines in which we participate are very competitive and we risk losing business based on a wide range of factors, including price, quality, technological and engineering capability, manufacturing and distribution capability, innovation, performance, reliability and availability, geographic coverage, delivery and customer service. Our customers continue to seek technological innovation, productivity gains and competitive prices from us and our other suppliers. As a result of these and other factors, if we do not meet our customers’ expectations, we may not be able to compete effectively.

Additionally, we operate in highly competitive markets and have numerous competitors who are well-established in those markets. Our competitors include companies that may have greater name recognition or financial, technical, operational, marketing or other resources than us. We expect our competitors to continue improving the design and performance of their products and to introduce new products that could be competitive in both price and performance. We believe that we have certain technological advantages over our competitors in the markets in which we operate, but maintaining these advantages requires us to consistently invest in research and development, sales and marketing and customer service and support. There is no guarantee that we will be successful in maintaining these advantages.

The competitive environment in which we operate is also subject to change. There is no guarantee that we will be successful in implementing new product expansions, as we may fail to successfully complete product development or achieve the level of sales for these products that we expect. There may also be unexpected costs for such new product offerings, which would lower our margins. In addition, certain competitors may have a competitive advantage in these new markets and if they are able to successfully develop a product before we do, they could reach the market before we do or gain broader market acceptance.

Evolving customer needs and developing technologies may threaten our existing business and growth.

The ongoing energy transition away from fossil fuels and the increased adoption of electrified powertrains in some market segments could result in lower demand for current diesel or natural gas engines and components and, over time, reduce the demand for related parts and service revenues. Specifically, our core markets may be impacted by technology transitions, including the transition to battery-electric vehicles, hydrogen-powered internal combustion engines, fuel cell electric vehicles and alternate power sources. Substantially all of our net sales are related to internal combustion engine filtration products. Concerns regarding the effects of emissions of GHG on the climate have driven (and will likely continue to drive) international, national, regional and local

21

legislative and regulatory responses, including those imposing more stringent emissions standards, requiring higher fuel efficiency and/or banning sales of gas-powered vehicles in the future. Such responses may generate or accelerate changes in technology and in customer and end-user preference, including wider adoption of, and preference for, technologies providing alternatives to diesel engines, such as electrification of equipment, which could reduce or eliminate the demand for our products.

Moreover, on November 15, 2019, Cummins, our largest customer, established a new set of goals for 2030 as part of its environmental sustainability strategy and since then has continued to implement such strategy to make progress towards its target of reaching carbon neutrality in its products and operations by 2050. Among Cummins’ new goals for 2030 is reducing its Scope 3 absolute lifetime GHG emissions from newly sold products, and partnering with its customers to reduce its indirect GHG emissions from its products. These goals may result in Cummins preferring products that reduce its direct and/or indirect GHG emissions. As a result of these risks, and as we have seen OEMs begin to invest heavily in these new technologies and launch new non internal combustion engines, we have been working, and continue to work, to expand our product offerings across industries and application types, including electric powertrain, hydrogen internal combustion engines and fuel cells, among others. However, there can be no assurance that we will be successful in doing so, or even if we are successful, that such new products will generate the same revenue or margin as internal combustion engine filtration products. Some of these technologies, such as battery electric vehicles, may not utilize as much filtration content. Additionally, there can be no assurance that our expectations regarding new and developing alternate fuel technologies, including with respect to which technologies will prevail and the development of filtration content for those technologies, will prove to be accurate. Such disruptive innovation could create new markets for others and displace existing companies and products. If we are unsuccessful in adapting our technologies or expanding into adjacent markets, these disruptions could result in significant negative consequences for us. Our future growth is dependent on properly addressing future customer and end-user needs and adapting our products in line with global technology trends.

We rely on our executive leadership team and other key personnel as a critical part of our human capital resources.

We depend on the skills, institutional knowledge, working relationships and continued services and contributions of key personnel, including our executive leadership team, as critical parts of our human capital resources. In addition, our ability to achieve our operating and strategic goals depends on our ability to identify, hire, train and retain qualified individuals. We compete with other companies, both within and outside of our industry, for talented personnel and we may lose key personnel or fail to attract, train and retain other talented personnel. Any such loss or failure could have material adverse effects on our business, financial condition, results of operations or cash flows.