UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended:

OR

For the transition period from _____________ to ____________

Commission

file number

(Exact name of small business issuer as specified in its charter)

(State or other jurisdiction of incorporation) |

(IRS Employer Identification No.) |

(Address of principal executive offices) (Zip Code)

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Not Applicable | Not Applicable | Not Applicable |

Securities registered under Section 12(g) of the Exchange Act: Common Stock, Par Value $0.001

Indicate

by check mark if registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such files).

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained

herein, and will not be contained, to the best of registrant’s knowledge, in the definitive proxy or information statements incorporated

by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

The

aggregate market value of the voting and non-voting shares of the Company’s common stock held by non-affiliates as

of June 30, 2022 based on the last sale of the Company’s common stock, was $

As of March 30, 2023, there were shares of Common Stock, $0.001 par value, outstanding.

TABLE OF CONTENTS

| i |

CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS

The information contained in this Report includes some statements that are not purely historical and that are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and as such, may involve risks and uncertainties. These forward-looking statements relate to, among other things, expectations of the business environment in which we operate, perceived opportunities in the market and statements regarding our mission and vision. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. You can generally identify forward-looking statements as statements containing the words “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would” and similar expressions, or the negatives of such terms, but the absence of these words does not mean that a statement is not forward-looking.

Forward-looking statements involve risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed in the forward-looking statements. The forward-looking statements contained herein are based on various assumptions, many of which are based, in turn, upon further assumptions. Our expectations, beliefs and forward-looking statements are expressed in good faith on the basis of management’s views and assumptions as of the time the statements are made, but there can be no assurance that management’s expectations, beliefs or projections will result or be achieved or accomplished.

In addition to other factors and matters discussed elsewhere herein, the following are important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements: technological advances, impact of competition, dependence on key personnel and the need to attract new management, effectiveness of cost and marketing efforts, acceptances of products, ability to expand markets and the availability of capital or other funding on terms satisfactory to us. We disclaim any obligation to update forward-looking statements to reflect events or circumstances after the date hereof.

For a discussion of the risks, uncertainties, and assumptions that could affect our future events, developments or results, you should carefully review the “Risk Factors” set forth under “Item 1. Description of Business” below. In light of these risks, uncertainties and assumptions, the future events, developments or results described by our forward-looking statements herein could turn to be materially different from those we discuss or imply.

Unless expressly indicated or the context requires otherwise, the terms “RLI”, “Rubber Leaf”, “Company,” “we,” “us,” and “our” in this document refer to Rubber Leaf Inc, a Nevada corporation.

| ii |

PART I

Item 1. Description of Business.

Corporate History and Structure

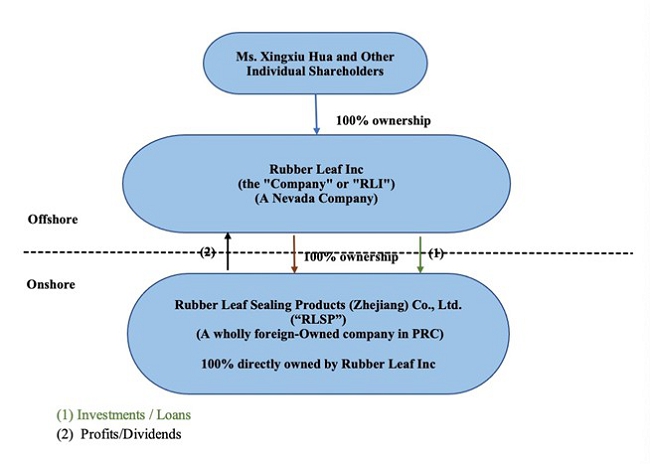

Rubber Leaf Inc (“the Company”) was incorporated under the laws of the State of Nevada on May 18, 2021. It acquired Rubber Leaf Sealing Products (Zhejiang) Co., Ltd. (“RLSP”) on May 27, 2021, through a Share Exchange Agreement between the Company and Xingxiu Hua, the President of the Company and who owned all of the issued and outstanding shares of RLSP. After the acquisition, RLSP became a 100% directly controlled subsidiary of the Company. Currently, all of the Company’s business is conducted through RLSP, our Wholly Foreign-Owned Enterprise (the “WOFE”) in China. RLSP was established in Fenghua, Ningo, China and commenced operations in July 2019. RLSP was the wholly-owned subsidiary of Rubber Leaf LLC, a Delaware company organized on June 1, 2018, and Ms. Xingxiu Hua was the sole member of Rubber Leaf LLC. RLSP’s main business areas include production and sales of synthetic rubber, rubber compound, car window seals, auto parts and etc. We are a well-known auto parts enterprise, and we are also the first-tier supplier of well-known auto brands such as Dongfeng Motor and French Renault.

The Company’s principal business address is Qixing Road, Weng’ao Industrial Zone, Chunhu Subdistrict, Fenghua District Ningbo, Zhejiang, China

The following diagram illustrates our corporate structure as of March 30, 2023.

| ● | Rubber Leaf Inc (“RLI”), a Nevada holding company, was incorporated on May 18, 2021. |

| ● | Rubber Leaf Sealing Products (Zhejiang) Co., Ltd. (“RLSP” or “WOFE”), a wholly foreign-owned enterprise established in the PRC in July 2019, and now is 100% directly owned by Rubber Leaf Inc. |

Business Strategy

Our wholly owned subsidiary RLSP, as an automotive rubber and plastic sealing strip manufacturer, has obtained certificates as first-tier supplier to manufacture sealing strips for some auto Original Equipment Manufacturers (the “OEMs”), such as eGT New Energy Automotive Co., Ltd. (“eGT”), Dongfeng Motor Corporation (“Dongfeng”), French Renault and Volkswagen. RLSP started to supply automotive rubber and plastic sealing strips to eGT, the joint venture of Dongfeng and French Renault since September 2019. Meanwhile, RLSP also obtained certificates as second-tier manufacturer of automotive rubber and plastic sealing strip from some Branded Automobile Manufacturers (the “Auto Manufacturers”). Although RLSP just started to engage in the automotive sealing strip market in China since 2019, high-quality customers and our own unique advantages have allowed us to grow rapidly and accelerate our market share.

| 1 |

| ● | Main Products |

Since its establishment, the Company has been engaged in the research and development, design, production and sales of auto parts such as automobile sealing strips. The Company has strong tooling and mold and special equipment development capabilities, simultaneous development capabilities and overall product design capabilities. It mainly supplies sealing strip products for domestic and foreign automobile manufacturers, as well as supporting research and development and follow-up services.

| ● | Technology development advantage |

With years of exploration in the rubber industry, the Company has formed a strong technical advantage in the field of rubber formulations. The Company’s high-hardness rubber and low-density sponge production technology have reached the domestic leading level. We are also expertise in the areas of rubber vulcanization technology, modular development technology, three-dimensional molding technology, seamless interface technology, surface pre-coating technology and surface flocking. The Company is a leading candidate in the development and application of technology, rubber mixing process technology, CAE, CAD analysis simultaneous development technology and length control technology, and has applied these technologies to mass production. Now we also achieved the experience and technical ability to develop synchronously with the auto OEMs.

| ● | Customer resource advantage |

For auto parts manufacturers that provide supporting supplies to auto OEMs, establishing and maintaining cooperative relationships with as many mainstream auto OEMs as possible is the key to their survival and development. The Company has established a strong cooperative relationship with internationally renowned automobile manufacturers. Become a supplier of Renault, Dongfeng and Nissan. The assessment of qualified suppliers by automobile manufacturers is very strict. The assessment indicators often include enterprise scale, quality system, technology development capabilities, quality capabilities, on-site 5S, procurement management, process management, quality improvement capabilities, human resource training and other aspects. The cycle is usually as long as 1-3 years. With the increasingly fierce competition in the automobile manufacturing industry, auto OEMs have higher and higher requirements for the comprehensive strength and industry experience of their suppliers. The experience of providing supporting services for mainstream auto OEMs has become more and more customers choosing supplies. An important standard for quotient. Therefore, the automobile manufacturing industry has gradually become a relatively closed ecosystem, and only auto parts suppliers with high-quality customer resources can enter a virtuous circle of development.

Sales and Marketing

Our main products are automotive rubber and plastic sealing strips produced for specific models. The products have typical personalized customization features, so the direct sales model is basically adopted. The Company directly contacts the auto OEMs or the first-tier suppliers of the auto OEMs to obtain supplier qualifications, clarify product specifications and models, negotiate product prices, and obtain orders.

All of our executives are excellent industry professionals with extensive experience in the automotive-related industry for more than 20 years. They have a wealth of experience and contacts to help companies to expand the markets. Although it takes a long time to obtain the auto OEMs’ approval, once the company becomes supplier, the order is very stable for years.

Our sales process can generally be divided into two stages: product development and mass supply. In the product development stage, the company first needs to establish contact with customers and enter the list of qualified suppliers through a series of reviews by customers. After obtaining the project through bidding and other methods, the company will develop new models simultaneously with the automaker and its component suppliers or improve the development of seal products for mass-produced models, and develop models that meet the functions and performance of the models’ cost and other requirements. Before confirming the batch supply, the customer will further check the issuer’s factory area, production line, management system, etc., to confirm the issuer’s mass supply capability and product quality consistency. This stage lasts for a long time. The improved development of seals for mass-produced models generally takes about 6 months, and the simultaneous development of new models with auto OEMs and their accessory suppliers often takes a year or more.

Based on considerations such as cost and product consistency, auto OEMs generally choose one or two major suppliers for the same automotive seal product. Therefore, in the batch supply stage, the company can generally obtain continuous and stable orders based on the production and sales volume of this model. At this stage, the company’s main work is to provide timely and stable quality products based on customer orders, provide after-sales service, negotiate quotations, and sign price contracts on a regular or irregular basis. This stage is the main source of company income.

Our sales is substantial dependence on one major customer, Shanghai Xinsen Import & Export Co., Ltd (“Shanghai Xinsen”) for year ended December 31, 2022 which is also our related party. Effective on October 1, 2022, Ms. Xingxiu Hua, the President of the Company, has reduced her direct ownership of Shanghai Xinsen from 90% to 15%, and she is also no longer served as the Legal Representative and General Manager of Shanghai Xinsen pursuant to the board resolution of Shanghai Xinsen at the same date. The changes have been made and certified by the local government on October 11, 2022. The main reason for Ms. Hua’s ownership change in Shanghai Xinsen is due to her personal arrangement to focus more on RLSP’s business strategy improvement and market development. Nevertheless, we expect our future sales to Shanghai Xinsen will not be impacted by Ms. Hua’s ownership change since RLSP has established a matured sales system with Shanghai Xinsen in the past years, and moreover, Shanghai Hongyang and Wuhu Huichi, the customers of Shanghai Xinsen and who indirectly purchased RLSP’s products through Shanghai Xinsen, have been using RLSP’s products stably and consistently for many years.

| 2 |

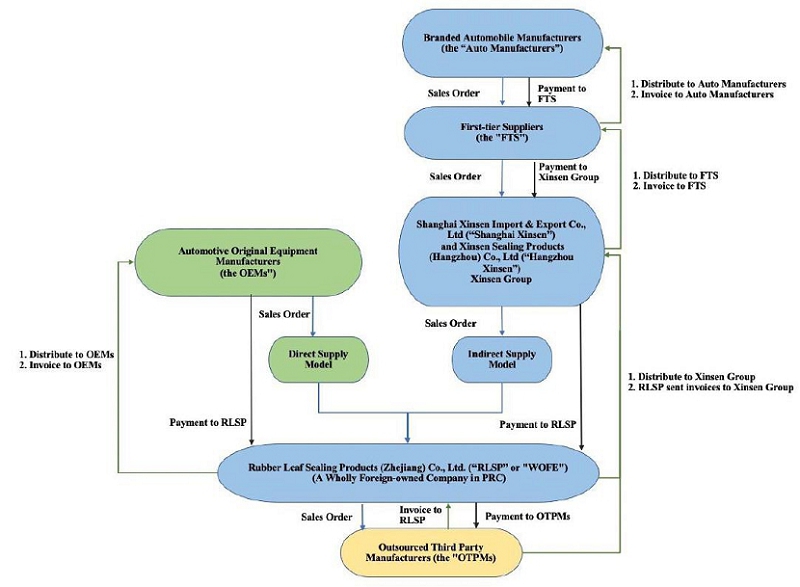

The Company currently operates with two sales models, the direct supply model and indirect supply model:

Model A: Direct supply model. Upon passing the on-site inspections of auto Original Equipment Manufacturers (the “OEMs”), RLSP is listed at the auto OEMs’ directories being one of their first-tier suppliers who will purchase raw materials, produce final products independently, and deliver finished products to the auto OEMs’ warehouses directly. RLSP satisfies its performance obligation when its finished products are delivered to the auto OEMs’ warehouses and a follow-up quality inspection is accepted by the auto OEMs. Meanwhile, the auto OEMs will also request product replacement for disqualified products. The ownership and control of our finished products are transferred to our customers as soon as the products passed the inspection and acceptance into the warehouses of the auto OEMs. Our revenue will be recognized once the control of our products has been transferred to our customers, and the payments will be paid by the auto OEMs directly.

Model B: Indirect supply model. RLSP received the purchase orders from our related parties-Shanghai Xinsen Import & Export Co., Ltd (“Shanghai Xinsen”) and Xinsen Sealing Products (Hangzhou) Co., Ltd (“Hangzhou Xinsen”) (collectively named as “Xinsen Group” for two companies together). The Company’s President, Ms. Xingxiu Hua, previously held 90% ownership of Shanghai Xinsen and Shanghai Xinsen holds 70% ownership of Hangzhou Xinsen, or Ms. Hua owns 63% ownership of Hangzhou Xinsen, respectively. Effective on October 1, 2022, Ms. Hua reduced her ownership of Shanghai Xinsen from 90% to 15%, and so accordingly reduced her indirect ownership of Hangzhou Xinsen from 63% to 10.5%. Branded Automobile Manufacturers (the “Auto Manufacturers”) send a lump sum purchase orders of the whole vehicle rubber and plastic auto parts of one model to their first-tier suppliers, who then subcontract rubber and plastic seals to Xinsen Group. Xinsen Group is a certified second-tier supplier of Auto Manufacturers who then subcontracts some products that they do not have capability to manufacture to RLSP. Once purchase orders received, RLSP purchased rubber materials from our venders and outsourced the purchase orders to third party manufacturer for work-in-process products (“WIP”) or finished products in its entirely based on management’s decision under the operating circumstances. RLSP has two forms of outsourced processing under Model B:

1). RLSP purchases raw materials and subcontracts the third-party manufacturers to produce WIP. Once WIP is finished and delivered to RLSP’s warehouse, RLSP performs some manual processes, such as welding and constructing in order to meet the specification of the purchase orders, the final products are concluded after strict quality inspection.

2). RLSP purchases raw materials and subcontracts third party manufacturers to produce finished products. RLSP will perform the responsibilities to trace and observe each step of production from the third-party manufacturers.

The finished products will be delivered to the first-tier suppliers’ warehouses, the downstream customers of Xinsen Group either from RLSP or third-party manufacturers’ locations. Xinsen Group will assign inspectors and perform quality inspection when the finished products are delivered. RLSP satisfies its performance obligation when the finished products are delivered to Xinsen Group’s customers and the quality inspection is qualified performed by Xinsen Group. Meanwhile, Xinsen Group will also request product replacement for disqualified products. Once the quality and quantity are confirmed and finished products are acceptable into the warehouses of Xinsen Group’s customers, receiving notes will be provided by Xinsen Group’s customers, then to RLSP as proof of delivery. The date of receiving notes signed is the time that RLSP transfers ownership and control of the finished products under model B to Xinsen Group then indirectly to the first-tier suppliers. RLSP recognizes revenue on the dates when receiving notes are signed by Xinsen Group’s customers.

The following diagram shows how sales are generate, how invoices and payments are processed and how the company’s products are manufactured and distributed to its customers, for our direct and indirect supply models.

| 3 |

Vendors

In order to reduce the purchase cost and enhance the purchase power, our subsidiary, RLSP mainly purchases the raw materials from Shanghai Haozong Rubber & Plastic Technology Co., Ltd. (“Shanghai Haozong”) at present. One of the Company’s directors, Mr. Jun Tong holds 30% ownership of Shanghai Haozong. Currently, we have substantial dependence Shanghai Haozong due to our business strategy.

Competition

According to the statistics of the Automobile Industry Branch of the China Association of Automobile Manufacturers, the 33 major automobile rubber sealing strip manufacturers that participated in the statistics in 2020, the scope of supporting cooperation covers almost all automobile manufacturers in China and all automobile manufacturers including passenger cars and commercial vehicles. In 2020, the rubber sealing strip industry achieved a sales income of about 15.53 billion Chinese yuan, of which main business candidates of the industry accounted for about 95% of the market share.

There is significant competition for the rubber sealing strip industry in the PRC. Many of our competitors are probably larger than we are and can devote more resources than we can do to the manufacture, distribution and sale of the rubber sealing strip. In order to successfully compete in our industry, we will need to:

| ● | Expand our customers basis and strive for additional orders; | |

| ● | Raise funds to support our operations and expand our capacities; | |

| ● | Recruit talent to explore high technology; and | |

| ● | That we provide outstanding product quality, customer service and rigid integrity in our business dealings. |

However, there can be no assurance that even if we do these things we will be able to compete effectively with the other companies in our industry. We believe that we have the required management expertise in the rubber sealing strip industry with good development potential and affordable price.

| 4 |

Government Regulations

| ● | Environmental protection |

The production of chemical pollutants in China must obtain a certificate from the relevant department. Rubber compound is a heavily polluting industry and must be approved by the local environmental protection department in China before it can be produced. Our company has qualified for all environmental assessment.

| ● | Production and operation license |

In China, it is necessary to obtain a business license issued by the Chinese Ministry of Commerce to operate the business related to the business license. RLSP’s main business includes to manufacture the rubber and plastic sealing strips for automotive windows and doors, and RLSP had obtained its business license in July 2019.

Our wholly owned subsidiary RLSP is incorporated and operating in the PRC. RLSP has received all permission required to obtain from Chinese authorities to operate its current business in China, including Business license and Approval regarding Environmental Protection.

Description of Property

RLSP entered into one operating lease with approximately 70,000 square feet from an unrelated individual in Fenghua District, Ningbo, Zhejiang Province, China, on November 15, 2019 for a factory building for manufacturing. The operating lease has twenty-five months lease term started from January 15, 2020 to February 14, 2022 and then extended to January 15, 2024, and the current monthly lease amount is about $18,300. We have also purchased a piece of land in Fenghua District, Ningbo City, Zhejiang Province, and are building a new factory at present, which is expected to be completed in August 2022. This new factory is projected to accommodate 15 TPV production lines and 10 EPDM production lines, which can meet the requirements of 3 million vehicles.

Employees

As of December 31, 2022, the Company has total of 53 employees. We do not presently have pension, health, annuity, insurance, profit sharing, or similar benefit plans; however, we may adopt plans in the future. There are presently no personal benefits available to our employees, Officers and/or Directors.

Patents and Trademarks

The Company currently has two patents, which were issued by China National Intellectual Property Administration on October 30, 2020 to our fully-owned subsidiary RLSP. The duration of each patent is ten (10) years.

| ● | For new energy vehicles, the sealing strip is both a first-level exterior part and a first-level functional part. The weight of the sealing strip and environmental protection has also become vital research topics. | |

| ● | The new structure of the parts developed by us that uses new TPV recyclable materials to replace the original EPDM high-polluting materials. This patent helps to reduce the quality of parts and the pollution for new energy vehicles. |

Subsidiary

The Company has a 100% directly controlled subsidiary, Rubber Leaf Sealing Products (Zhejiang) Co., Ltd. (“RLSP”) which locates in Ningbo, Zhejiang, China.

Reports to Security Holders

The Company’s documents filed with the Securities and Exchange Commission may be inspected at the Commission’s principal office in Washington, D.C. Copies of all or any part of the registration statement may be obtained from the Public Reference Section of the Securities and Exchange Commission, 100 F Street N.E., Washington, D.C. 20549. Call the Commission at 1-800-SEC-0330 for further information on the operation of the public reference rooms. The Securities and Exchange Commission also maintains a web site at http://www.sec.gov that contains reports, proxy statements and information regarding registrants that file electronically with the Commission. All of the Company’s filings may be located under the CIK number 0001893657.

| 5 |

Item 1A. Risk Factors.

An investment in our common stock is highly speculative and should only be made by persons who can afford to lose their entire investment in us. You should carefully consider the following risk factors and other information in this Form 10-K before deciding to become a holder of our common stock. If any of the following risks actually occur, our business and financial results could be negatively affected to a significant extent.

Risks Related to Doing Business in the People’s Republic of China (“PRC”)

Because all of our operations are in China, our business is subject to the complex and rapidly evolving laws and regulations there. The Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our common stock.

As a business operating in China, we are subject to the laws and regulations of the PRC, which can be complex and evolve rapidly. The PRC government has the power to exercise significant oversight and discretion over the conduct of our business, and the regulations to which we are subject may change rapidly and with little notice to us or our shareholders. As a result, the application, interpretation, and enforcement of new and existing laws and regulations in the PRC are often uncertain. In addition, these laws and regulations may be interpreted and applied inconsistently by different agencies or authorities, and inconsistently with our current policies and practices. New laws, regulations, and other government directives in the PRC may also be costly to comply with, and such compliance or any associated inquiries or investigations or any other government actions may:

| ● | Delay or impede our development; | |

| ● | Result in negative publicity or increase our operating costs; | |

| ● | Require significant management time and attention; and | |

| ● | Subject us to remedies, administrative penalties and even criminal liabilities that may harm our business, including fines assessed for our current or historical operations, or demands or orders that we modify or even cease our business practices. |

The promulgation of new laws or regulations, or the new interpretation of existing laws and regulations, in each case that restrict or otherwise unfavorably impact the ability or manner in which we conduct our business and could require us to change certain aspects of our business to ensure compliance, which could reduce revenues, increase costs and require us to obtain more licenses, permits, approvals or certificates, or subject us to additional liabilities. To the extent any new or more stringent measures are required to be implemented, our business, financial condition and results of operations could be adversely affected as well as materially decrease the value of our common stock.

Furthermore, if the PRC government determines that our corporate structure does not comply with PRC regulations, or if these regulations change or are interpreted different in the future, our securities may decline in value or become worthless if the determinations, changes or interpretations result in our inability to assert control over the assets of our PRC subsidiary that accordingly conduct all or substantially all of our operations.

PRC regulations relating to investments in foreign companies by PRC residents may subject our PRC-resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary or limit our PRC subsidiary’ ability to increase their registered capital or distribute profits.

As an U.S. holding company of our PRC subsidiary, we may make loans to our PRC subsidiary or may make additional capital contributions to our PRC subsidiary, subject to satisfaction of applicable governmental registration and approval requirements.

| 6 |

Any loans we extend to our PRC subsidiary, which are treated as foreign-invested enterprises under PRC law, cannot exceed the statutory limit and must be registered with the local counterpart of the State Administration of Foreign Exchange (“SAFE”).

In July 2014, SAFE promulgated the Circular on Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Offshore Investment and Financing and Roundtrip Investment through Special Purpose Vehicles, or SAFE Circular 37, which replaces the previous SAFE Circular 75. SAFE Circular 37 requires PRC residents, including PRC individuals and PRC corporate entities, to register with SAFE or its local branches in connection with their direct or indirect offshore investment activities. SAFE Circular 37 is applicable to our shareholders who are PRC residents and may be applicable to any offshore acquisitions that we may make in the future.

Under SAFE Circular 37, PRC residents who make, or have prior to the implementation of SAFE Circular 37 made, direct or indirect investments in offshore special purpose vehicles, or SPVs, are required to register such investments with SAFE or its local branches. In addition, any PRC resident who is a direct or indirect shareholder of an SPV, is required to update its registration with the local branch of SAFE with respect to that SPV, to reflect any material change. Moreover, any subsidiary of such SPV in China is required to urge the PRC resident shareholders to update their registration with the local branch of SAFE to reflect any material change. If any PRC resident shareholder of such SPV fails to make the required registration or to update the registration, the subsidiary of such SPV in China may be prohibited from distributing its profits or the proceeds from any capital reduction, share transfer or liquidation to the SPV, and the SPV may also be prohibited from making additional capital contributions into its subsidiary in China. In February, 2015, SAFE promulgated a Notice on Further Simplifying and Improving Foreign Exchange Administration Policy on Direct Investment, or SAFE Notice 13. Under SAFE Notice 13, applications for foreign exchange registration of inbound foreign direct investments and outbound direct investments, including those required under SAFE Circular 37, must be filed with qualified banks instead of SAFE. Qualified banks should examine the applications and accept registrations under the supervision of SAFE. We have used our best efforts to notify PRC residents or entities who directly or indirectly hold shares in our U.S. holding company and who are known to us as being PRC residents to complete the foreign exchange registrations. However, we may not be informed of the identities of all the PRC residents or entities holding direct or indirect interest in our company, nor can we compel our beneficial owners to comply with SAFE registration requirements. We cannot assure you that all other shareholders or beneficial owners of ours who are PRC residents or entities have complied with, and will in the future make, obtain or update any applicable registrations or approvals required by, SAFE regulations. Failure by such shareholders or beneficial owners to comply with SAFE regulations, or failure by us to amend the foreign exchange registrations of our PRC subsidiary, could subject us to fines or legal sanctions, restrict our overseas or cross-border investment activities, and limit our PRC subsidiary’s ability to make distributions or pay dividends to us or affect our ownership structure, which could adversely affect our business and prospects.

Furthermore, as these foreign exchange and outbound investment related regulations are relatively new and their interpretation and implementation has been constantly evolving, it is unclear how these regulations, and any future regulation concerning offshore or cross-border investments and transactions, will be interpreted, amended and implemented by the relevant government authorities. For example, we may be subject to a more stringent review and approval process with respect to our foreign exchange activities, such as remittance of dividends and foreign-currency-denominated borrowings, which may adversely affect our financial condition and results of operations. We cannot assure you that we have complied or will be able to comply with all applicable foreign exchange and outbound investment related regulations. In addition, if we decide to acquire a PRC domestic company, we cannot assure you that we or the owners of such company, as the case may be, will be able to obtain the necessary approvals or complete the necessary filings and registrations required by the foreign exchange regulations. This may restrict our ability to implement our acquisition strategy and could adversely affect our business and prospects.

In light of the various requirements imposed by PRC regulations on loans to, and direct investment in, PRC entities by offshore holding companies, we cannot assure you that we will be able to complete the necessary government registrations or obtain the necessary government approvals on a timely basis, if at all, with respect to future loans to our PRC subsidiary or future capital contributions by us to our PRC subsidiary. If we fail to complete such registrations or obtain such approvals, our ability to use the proceeds we expect to receive from this offering and to fund our PRC operations may be negatively affected, which could materially and adversely affect our liquidity and our ability to fund and expand our business.

| 7 |

Changes in the policies of the PRC government could have a significant impact upon our ability to operate profitably in the PRC.

We conduct all of our operations and all of our revenue is generated in the PRC. Accordingly, economic, political and legal developments in the PRC will significantly affect our business, financial condition, results of operations and prospects. Policies of the PRC government can have significant effects on economic conditions in the PRC and the ability of businesses to operate profitably. Our ability to operate profitably in the PRC may be adversely affected by changes in policies by the PRC government, including changes in laws, regulations or their interpretations.

PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Uncertainties with respect to the PRC legal system, including those regarding the enforcement of laws, and sudden or unexpected changes, with little advance notice, in laws and regulations in China could adversely affect us and limit the legal protections available to you and us.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations including, but not limited to, the laws and regulations governing our business and the enforcement and performance of our arrangements with customers in certain circumstances. The laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement could be unpredictable, with little advance notice. The effectiveness and interpretation of newly enacted laws or regulations, including amendments to existing laws and regulations, may be delayed, and our business may be affected if we rely on laws and regulations which are subsequently adopted or interpreted in a manner different from our understanding of these laws and regulations. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business.

Our subsidiary, RLSP is formed under and governed by the laws of the PRC. The PRC legal system is a civil law system based on written statutes. Unlike the common law system, prior court decisions under the civil law system may be cited for reference, but have limited precedential value. Since these laws and regulations are relatively new and the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and the enforcement of these laws, regulations and rules involves uncertainties.

In 1979, the PRC government began to promulgate a comprehensive system of laws and regulations governing economic matters in general, such as foreign investment, corporate organization and governance, commerce, taxation and trade. The overall effect of legislation over the past three decades has significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties and sudden changes, sometimes with little advance notice. As a significant part of our business is conducted in China, our operations are principally governed by PRC laws and regulations, which may limit legal protections available to us. Uncertainties due to evolving laws and regulations could also impede the ability of a China-based company, such as our company, to obtain or maintain permits or licenses required to conduct business in China. In the absence of required permits or licenses, governmental authorities could impose material sanctions or penalties on us. In addition, some regulatory requirements issued by certain PRC government authorities may not be consistently applied by other PRC government authorities (including local government authorities), thus making strict compliance with all regulatory requirements impractical, or in some circumstances impossible. For example, we may have to resort to administrative and court proceedings to enforce the legal protection that we enjoy either by law or contract. However, since PRC administrative and court authorities have discretion in interpreting and implementing statutory and contractual terms, it may be more difficult to predict the outcome of administrative and court proceedings and the level of legal protection we enjoy than in more developed legal systems. Furthermore, the PRC legal system is based in part on government policies and internal rules, some of which are not published on a timely basis or at all and may have retroactive effect. As a result, we may not be aware of our violation of any of these policies and rules until sometime after the violation. In addition, any administrative and court proceedings in China may be protracted, resulting in substantial costs and diversion of resources and management attention.

| 8 |

The PRC government has significant oversight and discretion over the conduct of our business and may intervene or influence our operations as the government deems appropriate to further regulatory, political and societal goals. The PRC government has recently published new policies that significantly affected certain industries such as the education and internet industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding our industry that could adversely affect our business, financial condition and results of operations. Furthermore, the PRC government has recently indicated an intent to exert more oversight and control over securities offerings and other capital markets activities that are conducted overseas and foreign investment in China-based companies like us. Any such action, once taken by the PRC government, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or in extreme cases, become worthless.

Furthermore, if China adopts more stringent standards with respect to certain areas such as environmental protection or corporate social responsibilities, we may incur increased compliance costs or become subject to additional restrictions in our operations. Certain areas of the law, including intellectual property rights and confidentiality protections in China may also not be as effective as in the United States or other countries. In addition, we cannot predict the effects of future developments in the PRC legal system on our business operations, including the promulgation of new laws, or changes to existing laws or the interpretation or enforcement thereof. These uncertainties could limit the legal protections available to us and our investors, including you.

We may become subject to a variety of laws and regulations in the PRC regarding privacy, data security, cybersecurity, and data protection. We may be liable for improper use or appropriation of personal information provided by our customers.

We may become subject to a variety of laws and regulations in the PRC regarding privacy, data security, cybersecurity, and data protection. These laws and regulations are continuously evolving and developing. The scope and interpretation of the laws that are or may be applicable to us are often uncertain and may be conflicting, particularly with respect to foreign laws. In particular, there are numerous laws and regulations regarding privacy and the collection, sharing, use, processing, disclosure, and protection of personal information and other user data. Such laws and regulations often vary in scope, may be subject to differing interpretations, and may be inconsistent among different jurisdictions.

We expect to obtain information about various aspects of our operations as well as regarding our employees and third parties. We also maintain information about various aspects of our operations as well as regarding our employees. The integrity and protection of our customer, employee and company data is critical to our business. Our customers and employees expect that we will adequately protect their personal information. We are required by applicable laws to keep strictly confidential the personal information that we collect, and to take adequate security measures to safeguard such information.

The PRC Criminal Law, as amended by its Amendment 7 (effective on February 28, 2009) and Amendment 9 (effective on November 1, 2015), prohibits institutions, companies and their employees from selling or otherwise illegally disclosing a citizen’s personal information obtained during the course of performing duties or providing services or obtaining such information through theft or other illegal ways. On November 7, 2016, the Standing Committee of the National People’s Congress of China (SCNPC) issued the Cyber Security Law of the PRC, or Cyber Security Law, which became effective on June 1, 2017.

Pursuant to the Cyber Security Law, network operators must not, without users’ consent, collect their personal information, and may only collect users’ personal information necessary to provide their services. Providers are also obliged to provide security maintenance for their products and services and shall comply with provisions regarding the protection of personal information as stipulated under the relevant laws and regulations.

The Civil Code of the PRC (issued by the PRC National People’s Congress on May 28, 2020 and effective from January 1, 2021) provides main legal basis for privacy and personal information infringement claims under the Chinese civil laws. PRC regulators, including the Cyberspace Administration of China, MIIT, and the Ministry of Public Security have been increasingly focused on regulation in the areas of data security and data protection.

| 9 |

The PRC regulatory requirements regarding cybersecurity are constantly evolving. For instance, various regulatory bodies in China, including the Cyberspace Administration of China, the Ministry of Public Security and the SAMR, have enforced data privacy and protection laws and regulations with varying and evolving standards and interpretations. In April 2020, the Chinese government promulgated Cybersecurity Review Measures, which came into effect on June 1, 2020. According to the Cybersecurity Review Measures, operators of critical information infrastructure must pass a cybersecurity review when purchasing network products and services which do or may affect national security.

In November 2016, the SCNPC passed China’s first Cybersecurity Law (“CSL”), which became effective in June 2017. The CSL is the first PRC law that systematically lays out the regulatory requirements on cybersecurity and data protection, subjecting many previously under-regulated or unregulated activities in cyberspace to government scrutiny. The legal consequences of violation of the CSL include penalties of warning, confiscation of illegal income, suspension of related business, winding up for rectification, shutting down the websites, and revocation of business license or relevant permits. In April 2020, the Cyberspace Administration of China and certain other PRC regulatory authorities promulgated the Cybersecurity Review Measures, which became effective in June 2020. Pursuant to the Cybersecurity Review Measures, operators of critical information infrastructure must pass a cybersecurity review when purchasing network products and services which do or may affect national security. On July 10, 2021, the Cyberspace Administration of China issued a revised draft of the Measures for Cybersecurity Review for public comments (“Draft Measures”), which required that, in addition to “operator of critical information infrastructure,” any “data processor” carrying out data processing activities that affect or may affect national security should also be subject to cybersecurity review, and further elaborated the factors to be considered when assessing the national security risks of the relevant activities, including, among others, (i) the risk of core data, important data or a large amount of personal information being stolen, leaked, destroyed, and illegally used or exited the country; and (ii) the risk of critical information infrastructure, core data, important data or a large amount of personal information being affected, controlled, or maliciously used by foreign governments after listing abroad. The Cyberspace Administration of China has said that under the proposed rules companies holding data on more than 1,000,000 users must now apply for cybersecurity approval when seeking listings in other nations because of the risk that such data and personal information could be “affected, controlled, and maliciously exploited by foreign governments,” The cybersecurity review will also investigate the potential national security risks from overseas IPOs. On June 10, 2021, the SCNPC promulgated the PRC Data Security Law, which took effect on September 1, 2021. The Data Security Law also sets forth the data security protection obligations for entities and individuals handling personal data, including that no entity or individual may acquire such data by stealing or other illegal means, and the collection and use of such data should not exceed the necessary limits The costs of compliance with, and other burdens imposed by, CSL and any other cybersecurity and related laws may limit the use and adoption of our products and services and could have an adverse impact on our business. Further, if the enacted version of the Measures for Cybersecurity Review mandates clearance of cybersecurity review and other specific actions to be completed by companies like us, we face uncertainties as to whether such clearance can be timely obtained, or at all.

On August 20, 2021, the SCNPC promulgated the PRC Personal Information Protection Law, which will take effect in November 2021. The Personal Information Protection Law provides that any entity involving processing of personal information (“Personal Information Processer”)shall take various measures to prevent the disclosure, modification or losing of the personal information processed by such entity, including, but not limited to, formulating a related internal management system and standard of operation, conducting classified management of personal information, taking safety technology measures to encrypt and de-identify the processed personal information, providing regular safety training and education for staff and formulating a personal information safety emergency accident plan. The Personal Information Protection Law further provides that a Personal Information Processer shall conduct a prior evaluation of the impact of personal information protection before the occurrence of various situations, including, but not limited to, processing of sensitive personal information (personal information that, once leaked or illegally used, may lead to discrimination against an individual or serious harm to an individual’s personal or property safety, including information on an individual’s ethnicity, religious beliefs, personal biological characteristics, medical health, financial accounts, personal whereabouts), using personal information to make automated decisions and providing personal information to any overseas entity.

| 10 |

On November 14, 2021, the Cyberspace Administration of China or the CAC released the Regulations on Network Data Security (draft for public comments) and accepted public comments until December 13, 2021. The draft Regulations on Network Data Security provide that data processors refer to individuals or organizations that autonomously determine the purpose and the manner of processing data. If a data processor that processes personal data of more than one million users intends to list overseas, it shall apply for a cybersecurity review. In addition, data processors that process important data or are listed overseas shall carry out an annual data security assessment on their own or by engaging a data security services institution, and the data security assessment report for the prior year should be submitted to the local cyberspace affairs administration department before January 31 of each year. On December 28, 2021, the Measures for Cybersecurity Review (2021 version) was promulgated and took effect on February 15, 2022, which iterates that any “online platform operators” controlling personal information of more than one million users which seeks to list in a foreign stock exchange should also be subject to cybersecurity review. As advised by our PRC legal counsel, Shanghai SISU Law Firm (“Shanghai SISU”) in their legal opinion dated on July 29, 2022, we are not among the “operator of critical information infrastructure” or “data processor” as mentioned above. The Company, through RLSP, is a supplier of automotive rubber sealing products in China, and designs, develops and manufactures auto rubber related products, and neither the Company nor its subsidiary is engaged in data activities as defined under the Personal Information Protection Law, which includes, without limitation, collection, storage, use, processing, transmission, provision, publication and deletion of data. In addition, neither the Company nor its subsidiary is an operator of any “critical information infrastructure” as defined under the PRC Cybersecurity Law and the Security Protection Measures on Critical Information Infrastructure. However, Measures for Cybersecurity Review (2021 version) was recently adopted and the Regulations on Network Data Security (draft for comments) is in the process of being formulated and the Opinions remain unclear on how it will be interpreted, amended and implemented by the relevant PRC governmental authorities.

There remains uncertainties as to when the final measures will be issued and take effect, how they will be enacted, interpreted or implemented, and whether they will affect us. If we inadvertently conclude that the Measures for Cybersecurity Review (2021 version) do not apply to us, or applicable laws, regulations, or interpretations change and it is determined in the future that the Measures for Cybersecurity Review (2021 version) become applicable to us, we may be subject to review when conducting data processing activities, and may face challenges in addressing its requirements and make necessary changes to our internal policies and practices. We may incur substantial costs in complying with the Measures for Cybersecurity Review (2021 version), which could result in material adverse changes in our business operations and financial position. If we are not able to fully comply with the Measures for Cybersecurity Review (2021 version), our ability to offer or continue to offer securities to investors may be significantly limited or completely hindered, and our securities may significantly decline in value or become worthless.

The CSRC has released the Trial Administrative Measures of Overseas Securities Offering and Listing by domestic companies and five guidelines, which will come into effect on March 31, 2023. The Chinese government may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to offer or continue to offer our common stock to investors and could cause the value of our common stock to significantly decline or become worthless

On December 24, 2021, the CSRC released the Administrative Provisions of the State Council Regarding the Overseas Issuance and Listing of Securities by Domestic Enterprises (Draft for Comments) (the “Draft Administrative Provisions”) and the Measures for the Overseas Issuance of Securities and Listing Record-Filings by Domestic Enterprises (Draft for Comments) (the “Draft Filing Measures”, and collectively with the Draft Administrative Provisions, the “Draft Rules Regarding Overseas Listing”), which stipulate that Chinese-based companies, or the issuer, shall fulfill the filing procedures after the issuer makes an application for initial public offering and listing in an overseas market, and certain overseas offering and listing such as those that constitute a threat to or endanger national security, as reviewed and determined by competent authorities under the State Council in accordance with law, may be prohibited under the Draft Rules Regarding Overseas Listing. On February 17, 2023, with the approval of the State Council, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Measures”) and five supporting guidelines, which will come into effect on March 31, 2023. According to the Trial Measures, among other requirements, (1) domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedures with the CSRC; if a domestic company fails to complete the filing procedures, such domestic company may be subject to administrative penalties; and (2) where a domestic company seeks to indirectly offer and list securities in an overseas market, the issuer shall designate a major domestic operating entity responsible for all filing procedures with the CSRC, and such filings shall be submitted to the CSRC within three business days after the submission of the overseas offering and listing application. On the same day, the CSRC also held a press conference for the release of the Trial Measures and issued the Notice on Administration for the Filing of Overseas Offering and Listing by Domestic Companies, which clarifies that (1) on or prior to the effective date of the Trial Measures, domestic companies that have already submitted valid applications for overseas offering and listing but have not obtained approval from overseas regulatory authorities or stock exchanges may reasonably arrange the timing for submitting their filing applications with the CSRC, and must complete the filing before the completion of their overseas offering and listing; (2) a six-month transition period will be granted to domestic companies which, prior to the effective date of the Trial Measures, have already obtained the approval from overseas regulatory authorities or stock exchanges, but have not completed the indirect overseas listing; if domestic companies fail to complete the overseas listing within such six-month transition period, they shall file with the CSRC according to the requirements; (3) the CSRC will solicit opinions from relevant regulatory authorities and complete the filing of the overseas listing of companies with contractual arrangements which duly meet the compliance requirements, and support the development and growth of these companies; and (4) domestic companies that are already listed on overseas exchanges by or before March 31, 2023 are not required to make any filings with CSRC unless they raise additional equity financing.

| 11 |

As of the date of this Form 10-K, neither we nor our PRC subsidiary has been subject to any investigation, or received any notice, warning, or sanction from the CSRC or other applicable government authorities related to our listing. If we are required to file with the CSRC for our future offering, there is no assurance that we can complete such filing in a timely manner or even at all. Any failure by us to comply with such filing requirements may result in an order to rectify, warnings and fines against us and could materially hinder our ability to offer or continue to offer our securities.

We are a holding company and will rely on dividends paid by our subsidiary for our cash needs. Any limitation on the ability of our subsidiary to make dividend payments to us, or any tax implications of making dividend payments to us, could limit our ability to pay our parent company expenses or pay dividends to holders of our common stocks.

We are a holding company and conduct substantially all of our business through our PRC subsidiary, which is a limited liability company established in China. We may rely on dividends to be paid by our PRC subsidiary to fund our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders, to service any debt we may incur and to pay our operating expenses. If our PRC subsidiary incurs debt on its own behalf in the future, the instruments governing the debt may restrict its ability to pay dividends or make other distributions to us.

Under PRC laws and regulations, our PRC subsidiary, which is a wholly foreign-owned enterprise in China, may pay dividends only out of its accumulated profits as determined in accordance with PRC accounting standards and regulations. In addition, a wholly foreign-owned enterprise is required to set aside at least 10% of its accumulated after-tax profits each year, if any, to fund a certain statutory reserve fund, until the aggregate amount of such fund reaches 50% of its registered capital.

Our PRC subsidiary generates primarily all of its revenue in Renminbi, which is not freely convertible into other currencies. As a result, any restriction on currency exchange may limit the ability of our PRC subsidiary to use its Renminbi revenues to pay dividends to us. The PRC government may continue to strengthen its capital controls, and more restrictions and substantial vetting process may be put forward by SAFE for cross-border transactions falling under both the current account and the capital account. Any limitation on the ability of our PRC subsidiary to pay dividends or make other kinds of payments to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends, or otherwise fund and conduct our business.

In addition, the Enterprise Income Tax Law, or EIT, and its implementation rules provide that a withholding tax rate of up to 10% will be applicable to dividends payable by Chinese companies to non-PRC-resident enterprises unless otherwise exempted or reduced according to treaties or arrangements between the PRC central government and governments of other countries or regions where the non-PRC resident enterprises are incorporated. Any limitation on the ability of our PRC subsidiary to pay dividends or make other distributions to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends, or otherwise fund and conduct our business.

| 12 |

Because our business is conducted in RMB and the price of our common stock is quoted in United States dollars, changes in currency conversion rates may affect the value of your investments.

Our business is conducted in the PRC, our books and records are maintained in RMB, which is the currently of the PRC, and the financial statements that we file with the SEC and provide to our shareholders are presented in United States dollars. Changes in the exchange rate between the RMB and dollar affect the value of our assets and the results of our operations in United States dollars. The value of the RMB against the United States dollar and other currencies may fluctuate and is affected by, among other things, changes in the PRC’s political and economic conditions and perceived changes in the economy of the PRC and the United States. Any significant revaluation of the RMB may materially and adversely affect our cash flows, revenue and financial condition. Further, our common stock offered by this prospectus are offered in United States dollars, we will need to convert the net proceeds we receive into RMB in order to use the funds for our business. Changes in the conversion rate between the United States dollar and the RMB will affect that amount of proceeds we will have available for our business.

The value of the Renminbi against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions in China and by China’s foreign exchange policies. On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the Renminbi to the U.S. dollar, and the Renminbi appreciated more than 20% against the U.S. dollar over the following three years. Between July 2008 and June 2010, this appreciation halted and the exchange rate between the Renminbi and the U.S. dollar remained within a narrow band. Since June 2010, the Renminbi has fluctuated against the U.S. dollar, at times significantly and unpredictably. On November 30, 2015, the Executive Board of the International Monetary Fund (IMF) completed the regular five-year review of the basket of currencies that make up the Special Drawing Right, or the SDR, and decided that with effect from October 1, 2016, Renminbi is determined to be a freely usable currency and will be included in the SDR basket as a fifth currency, along with the U.S. dollar, the Euro, the Japanese yen and the British pound. In the fourth quarter of 2016, the Renminbi depreciated significantly in the backdrop of a surging U.S. dollar and persistent capital outflows of China.

This depreciation halted in 2017, and the RMB appreciated approximately 7% against the U.S. dollar during this one-year period. The Renminbi in 2018 depreciated approximately by 5% against the U.S. dollar. Starting from the beginning of 2019, the Renminbi has depreciated significantly against the U.S. dollar again. In early August 2019, the PBOC set the Renminbi’s daily reference rate at RMB7.0039 to US$1.00, the first time that the exchange rate of Renminbi to U.S. dollar exceeded 7.0 since 2008. With the development of the foreign exchange market and progress towards interest rate liberalization and Renminbi internationalization, the PRC government may in the future announce further changes to the exchange rate system, and we cannot assure you that the Renminbi will not appreciate or depreciate significantly in value against the U.S. dollar in the future. It is difficult to predict how market forces or PRC or U.S. government policy may impact the exchange rate between the Renminbi and the U.S. dollar in the future.

There remains significant international pressure on the Chinese government to adopt a flexible currency policy to allow the Renminbi to appreciate against the U.S. dollar. Significant revaluation of the Renminbi may have a material and adverse effect on your investment. Substantially all of our revenues and costs are denominated in Renminbi. Any significant revaluation of Renminbi may materially and adversely affect our revenues, earnings and financial position, and the value of, and any dividends payable on, our common stock in U.S. dollars.

To the extent that we need to convert U.S. dollars we receive from this offering into Renminbi for capital expenditures and working capital and other business purposes, appreciation of the Renminbi against the U.S. dollar would have an adverse effect on the Renminbi amount we would receive from the conversion. Conversely, a significant depreciation of the Renminbi against the U.S. dollar may significantly reduce the U.S. dollar equivalent of our earnings, which in turn could adversely affect the price of our common stock, and if we decide to convert Renminbi into U.S. dollars for the purpose of making dividend payments on our common stock, strategic acquisitions or investments or other business purposes, appreciation of the U.S. dollar against the Renminbi would have a negative effect on the U.S. dollar amount available to us.

Very limited hedging options are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions in an effort to reduce our exposure to foreign currency exchange risk. While we may decide to enter into hedging transactions in the future, the availability and effectiveness of these hedges may be limited and we may not be able to adequately hedge our exposure or at all. In addition, our currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert Renminbi into foreign currency. As a result, fluctuations in exchange rates may have a material adverse effect on your investment.

| 13 |

Governmental control of currency conversion may limit our ability to utilize our net revenues effectively and affect the value of your investment.

The PRC government imposes controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of China. We receive substantially all of our net revenues in RMB. Under our current corporate structure, our Company in the United States relies on dividend payments from our PRC subsidiary to fund any cash and financing requirements we may have. Under existing PRC foreign exchange regulations, payments of current account items, such as profit distributions and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior approval from SAFE by complying with certain procedural requirements. Therefore, our PRC subsidiary is able to pay dividends in foreign currencies to us without prior approval from SAFE, subject to the condition that the remittance of such dividends outside of the PRC complies with certain procedures under PRC foreign exchange regulation, such as the overseas investment registrations by the beneficial owners of our Company who are PRC residents. But approval from or registration with appropriate government authorities is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies.

In light of the flood of capital outflows of China in 2016 due to the weakening RMB, the PRC government has imposed more restrictive foreign exchange policies and stepped up scrutiny of major outbound capital movement. More restrictions and substantial vetting process are put in place by SAFE to regulate cross-border transactions falling under the capital account. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currencies to satisfy our foreign currency demands, we may not be able to pay dividends in foreign currencies to our shareholders.

Under the PRC Enterprise Income Tax Law, or the EIT Law, we may be classified as a “resident enterprise” of China, which could result in unfavorable tax consequences to us and our non-PRC shareholders.

The EIT Law and its implementing rules provide those enterprises established outside of China whose “de facto management bodies” are located in China are considered “resident enterprises” under PRC tax laws. The implementing rules promulgated under the EIT Law define the term “de facto management bodies” as a management body which substantially manages, or has control over the business, personnel, finance and assets of an enterprise. In April 2009, the State Administration of Taxation, or SAT, issued the Circular on Issues Concerning the Identification of Chinese-Controlled Overseas Registered Enterprises as Resident Enterprises in Accordance With the Actual Standards of Organizational Management, known as Circular 82, which has provided certain specific criteria for determining whether the “de facto management bodies” of a PRC-controlled enterprise that is incorporated offshore is located in China. However, there are no further detailed rules or precedents governing the procedures and specific criteria for determining “de facto management body.” Although our board of directors and management are located in the PRC, it is unclear if the PRC tax authorities will determine that we should be classified as a PRC “resident enterprise.”

If we are deemed as a PRC “resident enterprise,” we will be subject to PRC enterprise income tax on our worldwide income at a uniform tax rate of 25%, although dividends distributed to us from our existing PRC subsidiary and any other PRC subsidiary which we may establish from time to time could be exempt from the PRC dividend withholding tax due to our PRC “resident recipient” status. This could have a material and adverse effect on our overall effective tax rate, our income tax expenses and our net income. Furthermore, dividends, if any, paid to our shareholders may be decreased as a result of the decrease in distributable profits. In addition, if we were considered a PRC “resident enterprise”, any dividends we pay to our non-PRC investors, and the gains realized from the transfer of our common stock may be considered income derived from sources within the PRC and be subject to PRC tax, at a rate of 10% in the case of non-PRC enterprises or 20% in the case of non-PRC individuals (in each case, subject to the provisions of any applicable tax treaty). It is unclear whether holders of our common stock would be able to claim the benefits of any tax treaties between their country of tax residence and the PRC in the event that we are treated as a PRC resident enterprise. This could have a material and adverse effect on the value of your investment in us and the price of our common stock.

| 14 |

Changes in international trade policies, trade dispute or the emergence of a trade war, may have a material adverse effect on our business.

Political events, international trade disputes, and other business interruptions could harm or disrupt international commerce and the global economy, and could have a material adverse effect on us and our customers, service providers and other partners.

International trade disputes could result in tariffs and other protectionist measures that could adversely affect our business. Tariffs could increase the cost of the goods and products which could affect consumers’ discretionary spending levels and therefore adversely impact our business. In addition, political uncertainty surrounding international trade disputes and the potential of the escalation to trade war and global recession could have a negative effect on consumer confidence, which could adversely affect our business.

Inflation in the PRC could adversely impact our financial condition and results of operations.

Our wholly owned subsidiary, RLSP, is the only operating entity that conducts business in the PRC. Since the inception of RLSP, inflation in China has not materially impacted our results of operations. According to the National Bureau of Statistics of China, the year-over-year percent changes in the consumer price index for 2019, 2020 and 2021 were increases of 2.9 %, 2.5% and 0.9%, respectively. The PRC overall economy is expected to continue to grow. Although we have not in the past been materially affected by inflation, we can provide no assurance that we will not be affected in the future by higher rates of inflation in China. Future increases in the PRC’s inflation may adversely impact our financial condition and result of operations unless we are able to pass on these costs to our customers by increasing the prices of our products.

U.S. regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China.

Any disclosure of documents or information located in China by foreign agencies may be subject to jurisdiction constraints and must comply with China’s state secrecy laws, which broadly define the scope of “state secrets” to include matters involving economic interests and technologies. There is no guarantee that requests from U.S. federal or state regulators or agencies to investigate or inspect our operations will be honored by us, by entities who provide services to us or with whom we associate, without violating PRC legal requirements, especially as those entities are located in China.

The PRC Securities Law was promulgated in December 1998 and was subsequently revised in October 2005, June 2013, August 2014 and December 2019. According to Article 177 of the PRC Securities Law, or Article 177, which became effective in March 2020, no overseas securities regulator is allowed to directly conduct investigation or evidence collection activities within the territory of the PRC. While there is no detailed interpretation regarding the rule implementation under Article 177, it will be difficult for an overseas securities regulator to conduct investigation or evidence collection activities in China.

The disclosures in our reports and other filings with the SEC and our other public pronouncements are not subject to the scrutiny of any regulatory bodies in the PRC.

We are regulated by the SEC and our reports and other filings with the SEC are subject to SEC review in accordance with the rules and regulations promulgated by the SEC under the Securities Act and the Exchange Act. Our SEC reports and other disclosure and public pronouncements are not subject to the review or scrutiny of any PRC regulatory authority. For example, the disclosure in our SEC reports and other filings are not subject to the review by China Securities Regulatory Commission, a PRC regulator that is responsible for oversight of the capital markets in China. Accordingly, you should review our SEC reports, filings and our other public pronouncements with the understanding that no local regulator has done any review of us, our SEC reports, other filings or any of our other public pronouncements.

| 15 |

Any disruption in the supply chain of raw materials and our products could adversely impact our ability to produce and deliver products.

As to the products we manufacture, we must manage our supply chain for raw materials and delivery of our products. Supply chain fragmentation and local protectionism within China further complicate supply chain disruption risks. Local administrative bodies and physical infrastructure built to protect local interests pose transportation challenges for raw material transportation and product delivery. In addition, profitability and volume could be negatively impacted by limitations inherent within the supply chain, including competitive, governmental, legal, natural disasters, and other events that could impact supply and price. Any of these occurrences could cause significant disruptions to our supply chain, manufacturing capability, and distribution system that could adversely impact our ability to produce and deliver products.