UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the fiscal year ended

OR

For the transition period from _______________ to _______________

OR

Date of event requiring this shell company report _______________

For the transition period from ___________________________ to ___________________________

Commission file number

(Exact name of Registrant specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Ontario,

(Jurisdiction of incorporation or organization)

905-739-0593

(Address of principal executive offices)

Chief Executive Officer

+1 (

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of Each Class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Not Applicable

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Not Applicable

(Title of Class)

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of business of the period covered by the annual report.

Common Shares

Indicate by check mark if the Registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Yes ☐

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer,” “large accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☐ |

| Emerging Growth Company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards † pursuant to Section 13(a) of the Exchange

Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued | Other ☐ | |

| by the International Accounting Standards Board ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b 2 of the Exchange Act):

Yes ☐

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether Registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

Not applicable.

TABLE OF CONTENTS

| i |

FORWARD LOOKING STATEMENTS

This annual report contains statements that constitute “forward-looking statements”. Any statements that are not statements of historical facts may be deemed to be forward-looking statements. These statements appear in a number of different places in this annual report and, in some cases, can be identified by words such as “anticipates”, “estimates”, “projects”, “expects”, “contemplates”, “intends”, “believes”, “plans”, “may”, “will”, or their negatives or other comparable words, although not all forward-looking statements contain these identifying words. Forward-looking statements in this annual report may include, but are not limited to, statements and/or information related to: strategy, future operations, projected production capacity, projected sales or rentals, projected costs, expectations regarding demand and acceptance of our products, availability of material components, trends in the market in which we operate, plans and objectives of management.

We believe that we have based our forward-looking statements on reasonable assumptions, estimates, analysis and opinions made in light of our experience and our perception of trends, current conditions and expected developments, as well as other factors that we believe to be relevant and reasonable in the circumstances at the date that such statements are made, but which may prove to be incorrect. Although management believes that the assumption and expectations reflected in such forward-looking statements are reasonable, we may have made misjudgments in preparing such forward-looking statements. Assumptions have been made regarding, among other things: our expected production capacity; labor costs and material costs, no material variations in the current regulatory environment and our ability to obtain financing as and when required and on reasonable terms. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which may have been used.

The forward-looking statements, including the statements contained in Item 3.D “Risk Factors”. In particular, without limiting the generality of the foregoing disclosure, the statements contained in Item 4.B. – “Business Overview”, Item 5 – “Operating and Financial Review and Prospects” and Item 11 – “Quantitative and Qualitative Disclosures About Market Risk” and elsewhere in this annual report, are subject to known and unknown risks, uncertainties and other factors that may cause actual results to be materially different from those expressed or implied by such forward-looking statements.

Although management has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Forward-looking statements might not prove to be accurate, as actual results and future events could differ materially from those anticipated in such forward-looking statements or we may have made misjudgments in the course of preparing the forward-looking statements. Accordingly, readers should not place undue reliance on forward-looking statements. We wish to advise you that these cautionary remarks expressly qualify, in their entirety, all forward-looking statements attributable to our company or persons acting on our company’s behalf. We do not undertake to update any forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting such statements, except as, and to the extent required by, applicable securities laws. You should carefully review the cautionary statements and risk factors contained in this annual report and other documents that we may file from time to time with the securities regulators.

OTHER STATEMENTS IN THIS ANNUAL REPORT

Unless the context otherwise requires, in this annual report, the term(s) “we”, “us”, “our”, “Company”, “our company”, “our business” and “VEDU” refer to Visionary Education Technology Holdings Group Inc. together with its consolidated subsidiaries.

CAD” or “C$” refers to the Canadian dollar, all “U.S. Dollar,” “USD,” “dollar” or “$” references when used in this annual report refer to United States dollar.

| ii |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

An investment in our common shares carries a significant degree of risk. You should carefully consider the following risks, as well as the other information contained in this annual report, including our historical financial statements and related notes included elsewhere in this annual report, before you decide to purchase the common shares. Any one of these risks and uncertainties has the potential to cause material adverse effects on our business, prospects, financial condition and operating results which could cause actual results to differ materially from any forward-looking statements expressed by us and a significant decrease in the value of our ordinary shares. Refer to “Special Note Regarding Forward-Looking Statements”.

We may not be successful in preventing the material adverse effects that any of the following risks and uncertainties may cause. These potential risks and uncertainties may not be a complete list of the risks and uncertainties facing us. There may be additional risks and uncertainties that we are presently unaware of, or presently consider immaterial, that may become material in the future and have a material adverse effect on us. You could lose all or a significant portion of your investment due to any of these risks and uncertainties.

Risks Related to Our Business and Industry

Our business, results of operations and financial condition have been adversely impacted by the COVID-19 pandemic.

Although the COVID-19 pandemic has been declared over worldwide, the adverse impacts that it has developed upon the private education business are still severe and greatly affecting our growth in terms of the number of oversea students and revenue. The economic situation in the countries, which are the major sources for our oversea student recruiting, are largely damaged during and after the COVID-19 pandemic. Consequentially, families who had plan to send their children to oversea for education are no longer capable of doing so due to their damaged financial situation.

We still experienced challenges in enrolling new students in the fiscal year ended March 31, 2023. Even though we had a significant increase in our tuition revenue for the fiscal year ended March 31, 2023 compared to the fiscal year ended March 31, 2022, the number of students, especially international students, remained low. The number of students is very slowly recovering but is still adversely impacted by the negative outcomes of the pandemic. Now that the pandemic is declared over and the economy in our targeted countries and regions is slowly recovering, we anticipate that the number of students will increase by the end of 2023.

| 1 |

We have limited operating history providing education services, which makes it difficult to predict our prospects and our business and financial performance.

Although we have been engaged in the real estate business since 2013 and have management with prior experience in providing education services, we have only been providing education services and operating schools through several acquisitions beginning in November 2017 when we purchased a majority interest in Toronto ESchool. Additionally, our limited history of operating our planned main business lines may not serve as an adequate basis for evaluating our prospects and operating results, including net revenue, cash flows, profitability, or prospects. We have encountered, and may continue to encounter in the future, risks, challenges, and uncertainties associated with operating a private education business, such as addressing regulatory compliance and uncertainty, engaging, training, and retaining high-quality teachers and administrators, and expanding our school network. If we do not manage these risks successfully, our operating and financial results may differ materially from our expectations and our business and financial performance may suffer.

Some of our schools are in the early stages of development and have only limited operations. A negative change in the development or implementation of our PPP programs or 2+2 programs with public colleges or public universities, could cause delays in the execution of our business plan. Our inability to successfully increase the utilization rate for the schools that are in the ramp-up stage or adverse changes in our development of our PPP programs could have a material adverse effect on our results of operations, financial condition, and prospects.

In addition, as some of our schools commenced operations recently, they have not yet reached their full capacity. For newly established schools, we have recruited students only for certain grades, which leads to a relatively lower utilization rate for such schools. With our existing students progressing into the next grades in school and as we fill up new entry classes, we expect the utilization rates of our newly established schools to increase accordingly. We cannot assure you that we will be able to successfully increase the utilization rate for the schools that are in the ramp-up stage, which may materially and adversely affect our business growth and profitability.

The report of our independent registered public accounting firm on our financial statements for the years ended March 31, 2023 includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern, and if our business is unable to continue it is likely investors will lose all of their investment.

As discussed in Note 1 to the consolidated financial statements to this Annual Report, the Company has suffered significant losses from operations and has a significant decrease in working capital that raises substantial doubt about its ability to continue as a going concern. Our auditor, MNP LLP, has indicated in their report on the Company’s financial statements for the fiscal year ended March 31, 2023 that there is “substantial doubt about our ability to continue as a going concern”. A “going concern” opinion could impair our ability to finance our operations through the sale of equity, incurring debt, or other financing alternatives.

Management’s plan to alleviate the substantial doubt about our ability to continue as a going concern include working to improve the Company’s liquidity and capital sources mainly through cash flow from its operations, renewal of bank borrowings and borrowing from related parties. In order to fully implement its business plan and sustain continued growth, the Company may also seek equity financing from outside investors. At the present time, however, the Company does not have commitments of funds from any potential investors. There can be no assurance that additional financing, if required, would be available on favorable terms or at all and/or that these plans and arrangements will be sufficient to fund the Company’s ongoing capital expenditures, working capital, and other requirements. If we are unable to achieve these goals, our business will be jeopardized and we may not be able to continue. If we ceased operations, it is likely that all of our investors will lose their investment.

If we fail to establish and maintain proper internal financial reporting controls, our ability to produce accurate financial statements or comply with applicable regulations could be impaired.

We will be in a continuing process of developing, establishing, and maintaining internal controls and procedures that will allow our management to report on, and our independent registered public accounting firm to attest to, our internal controls over financial reporting if and when required to do so under Section 404 of the Sarbanes-Oxley Act of 2002. Although our independent registered public accounting firm is not required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act until the date we are no longer an emerging growth company, our management will be required to report on our internal controls over financial reporting under Section 404.

| 2 |

As of March 31, 2023, our management assessed the effectiveness of our internal control over financial reporting. The material deficiencies relate to that the Company does not have in-house accounting personnel with sufficient knowledge of US GAAP and SEC reporting experiences. In addition, the Company does not have adequate controls in place for the overall accounting function and oversight of financial reporting which resulted in audit adjustments. Management concluded that as of March 31, 2023, our internal control over financial reporting was ineffective.

In order to address and resolve the foregoing material weaknesses, we have implemented measures designed to improve our internal control over financial reporting to remediate the material weaknesses, including hiring consultants who have requisite training and experience in the preparation of financial statements in compliance with applicable SEC requirements. In addition to hiring an outside consultant, we also plan to take remedial measures including (i) hiring more qualified accounting personnel with relevant U.S. GAAP and SEC reporting experience and qualifications to strengthen the financial reporting function and to set up a financial and system control framework; (ii) implementing regular and continuous U.S. GAAP accounting and financial reporting training programs for our accounting and financial reporting personnel; (iii) setting up an internal audit function as well as engaging an external consulting firm to assist us with assessment of Sarbanes-Oxley compliance requirements and improvement of overall internal control; and (iv) appointing independent directors, establishing an audit committee, and strengthening corporate governance.

The implementation of these measures may not fully address the material weaknesses in our internal control over financial reporting, and we cannot conclude that they have been fully remedied. Our failure to correct theses material weaknesses or our failure to discover and address any other material weaknesses could result in inaccuracies in our financial statements and could also impair our ability to comply with applicable financial reporting requirements and related regulatory filings on a timely basis. As a result, our business, financial condition, results of operations and prospects, as well as the trading price of our Ordinary Shares, may be materially and adversely affected. Moreover, ineffective internal control over financial reporting significantly hinders our ability to prevent fraud. In addition, once we cease to be an “emerging growth company” as such term is defined in the JOBS Act, our independent registered public accounting firm must attest to and report on the effectiveness of our internal control over financial reporting. Our management may conclude that our internal control over financial reporting is not effective. Moreover, even if our management concludes that our internal control over financial reporting is effective, our independent registered public accounting firm, after conducting its own independent testing, may issue a report that is qualified if it is not satisfied with our internal controls or the level at which our controls are documented, designed, operated or reviewed, or if it interprets the relevant requirements differently from us. In addition, as a public company, our reporting obligations may place a significant strain on our management, operational and financial resources and systems for the foreseeable future. We may be unable to timely complete our evaluation testing and any required remediation.

We are subject to the risks of the volatility of the real estate industry.

Revenue from the sale of real property, from leasing office space to third parties, and from construction activities accounted for 84.1% of our revenue for the fiscal year ended March 31, 2023, and 87.2% of our revenue for the fiscal year ended March 31, 2022, and lease revenue is likely to account for a substantial portion of our revenue for at least the next several years. We are subject to the volatility and uncertainty of the Toronto real estate market, particularly regarding our ability to refinance the mortgages on our office buildings and renew leases for office space at rents that are equivalent to or greater than the rents we currently receive, should we decide to not renew the leases and utilize the space for our own operations. In addition, defaults by a significant number of tenants would have a material adverse impact on our revenue. In such an event, there is no guaranty that we would be able to lease any space vacated by those tenants or lease such space at equivalent rents. A material reduction in lease revenue could have a material adverse effect on our ability to finance our operations and result in a loss from operations should revenue from the education business not offset any such reduction in revenue. As of June 22, 2023, we have sold 41 Metropolitan Road E., Toronto, Canada (the “41 Metropolitan Building”) for $13.3 million (C$ 18 million).

We do not expect to generate revenue from the sale of real estate in the future, which has been a principal source of our revenue in recent fiscal periods.

In fiscal year ended March 31, 2022, we sold all eight lots of vacant land to third parties, and realized approximately $2.2 million revenue from the sales. We do not have any remaining lots available for sale and do not have any plans to sell any of the other real estate that we own. Therefore, we do not expect to generate any other revenue from the sale of real estate in future periods, and our principal sources of revenue will be from our educational business and leases of existing real estate that we own. If we are unable to generate additional income from those sources, our revenue will decline, which could have a material adverse effect on our results of operations.

Our strategy to use the space currently occupied by tenants for our operations upon termination of their leases could have a material adverse impact on our cash flow.

We intend to expand our operations into some, or all, of the office space currently occupied by unaffiliated tenants. Rental income provides a significant portion of our current revenue, which will continue after the expected acquisition of the property for Visionary University Town. Revenue from rent was $7,090,140 in the fiscal year ended March 31, 2023, and $2,298,198 in the fiscal year ended March 31, 2022. While we anticipate generating revenue from our education business to be located in these spaces to offset the potential loss of rental revenue, to the extent that such education revenue is less than the revenue currently being generated by space we no longer rent, our ability to finance our operations and service the mortgages on these properties will be impaired, which could lead to default.

| 3 |

We have limited experience operating some of our education businesses.

We have acquired several of our education companies since March 31, 2021, including Conbridge College of Business and Technology Inc., Visionary (formerly Lowell) Academy and MTM. While we have an experienced management team, operating those businesses and integrating them with our current operations is challenging and the inability to successfully operate one or more of these businesses could have a material adverse impact on our operations, financial condition, and prospects.

We have experienced losses and may not maintain profitability.

Although we have had profitable quarterly and annual periods, we have also experienced losses in the past and may experience losses in the future. We expect that our operating expenses and business development expenses will increase as we enroll more students, open new campuses and develop new programs. As a result, there can be no assurance we will be able to generate sufficient revenues to maintain profitability.

We assembled our management team beginning in late 2020. As a result, they have had a limited amount of time working in their positions and working together and may not be able to accomplish our business plan.

Our Chief Executive Officer, Chief Operating Officer, Chief Academic Officer Chief Financial Officer, and Chief Information Officer began employment in these positions at various times since November 2020. Ms. Zhou, our founder, majority shareholder, director, and Executive Director, served as Chief Executive Officer from April through October 2020. Ms. Fan Zhou was reappointed asour Chief Executive Officer on December 14, 2022 and became our Chairman of the Board on June 6, 2023. Our Chairman has experience in running private education institutions.

Our business, financial condition and results of operations may be adversely affected by a downturn in the global or Canadian economy.

Because our student enrollment may depend on our students’ and potential students’ and their parents’ levels of disposable income, perceived job prospects and willingness to spend on education courses, as well as the level of hiring demand of positions in the areas in which our schools train, our business and prospects may be affected by economic conditions in Canada or globally. The global financial markets experienced significant disruptions in 2008 and 2020. In both instances, Canada and other economies went into recession. The recovery from the lows of 2008 and 2009 was uneven and the global recovery from the lows in 2020 remains slow and inconsistent. While the COVID-19 pandemic has been declared over, Canada is open for international study visas and expects to gradually open for other categories of entry visas, the recovery of the economy in our targeted countries and regions is sluggish and unstable. As a result, our student recruiting this these countries and regions remains challenging and growth is lower than previously predicted.

Economic conditions in Canada and other countries from which we expect to draw our international students are sensitive to global economic conditions, as well as changes in domestic economic and political policies and the expected or perceived overall economic growth rate in Canada and those countries. A decline in the economic prospects in the industries in which our vocational training courses are concentrated could alter current or prospective students’ spending priorities and the demand for workers, and therefore the students’ job prospects, in these areas. We cannot assure you that education spending in general or with respect to our course offerings in particular will increase, or not decrease, from current levels. Therefore, a slowdown in Canada’s economy or the global economy may lead to a reduction in demand for the training covered by our courses, which could materially and adversely affect our financial condition and results of operations.

We will need additional capital to fully carry out our proposed expansion plan, and we may not be able to further implement our business strategy unless sufficient funds are raised, which could cause us to scale back our proposed plans or discontinue our expansion.

We will require significant expenditures of capital in order to carry out our full expansion plan. As of March 31, 2023, we had cash and cash equivalents of $651,490 and a negative working capital of approximately $58.1 million. While we completed an initial public offering for gross proceeds of $17 million in May 2022, we estimate that we will need additional financing of approximately $30 million to complete our proposed expansion plan for the next 12 months. This additional $30 million will be used for expanding our current businesses and possibly acquiring complementary businesses.

| 4 |

We may obtain the necessary additional funds from bank loans and the sale of additional securities, if required. However, there can be no assurance that we will obtain the financing required. If we are not able to obtain the necessary additional financing, we may be forced to scale back our expansion plans. Expending our cash resources on expansion could also negatively impact our current operations by reducing the amount of funds available to cover additional expenses that may arise in the future or offset losses should we suffer a decrease in revenues.

Historically, we have funded our operations primarily from loans from affiliates, revenue from our real estate operations and the sale of real property. Ms. Zhou, our founder, majority shareholder, director, and Executive Director, had outstanding advances to us of $4,165,912 as of March 31, 2023, and $7,149,165 as of March 31, 2022, interest free for the deposit on the acquisition of the proposed campus for VUT. Ms. Zhou is willing but not otherwise obligated to advance additional funds to us. However, our ability to obtain additional financing is subject to a number of factors, including market conditions and their impact on the market price of our common shares, the downturn in the global economy and resulting impact on stock markets and investor sentiment, our competitive ability, investor acceptance of our business or our expansion plan, and the political and economic environments of countries where we are doing business. These factors may make the timing, amount, terms and conditions of additional financing unattractive or unavailable to us. If we are unable to raise additional financing, we will have to significantly reduce, delay or cancel our planned activities. We cannot assure you that we will have sufficient resources to successfully conduct our expansion, or that we will be able to obtain any additional funding required, in which event we may not be able to continue our expansion or our expansion plan may fail. There can be no assurance that we will achieve our plans, or any of them.

The expansion of our business through acquisitions, joint ventures, and other strategic transactions creates risks that may reduce the benefits we anticipate from these strategic transactions.

We intend to enter into acquisitions, partnerships, joint ventures and other strategic transactions, directly or through our subsidiaries, as vehicles to expand our education business in Canada and other countries, particularly partnerships and licensing agreements with public colleges and other educational institutions. We continually seek out new business acquisitions, partnership opportunities and joint ventures to expand our operations. Our management is unable to predict whether or when any future strategic transactions will occur, including identifying suitable acquisition targets, partnership opportunities or joint venture partners, or the likelihood of any particular transaction being completed on terms and conditions that are favorable to us.

Acquisitions, partnerships, joint ventures or other strategic transactions may present financial, managerial and operational challenges. We may be exposed to successor liability relating to prior actions involving a predecessor company, or contingent liabilities incurred before a strategic transaction. Liabilities associated with an acquisition or a strategic transaction could adversely affect our financial performance. Any failure to integrate new businesses or manage any new alliances successfully could adversely affect our reputation and financial performance.

| 5 |

The operations of any businesses that we acquire are subject to their own risks, which we may not be able to manage successfully.

The financial results of any businesses that we acquire may be subject to many of the same factors that affect our financial condition and results of operations, including the seasonal nature of the education business, exposure to currency exchange rate fluctuations, the competitive nature of our markets, and regulatory, legislative and judicial developments. The financial results of any businesses acquired could be materially adversely affected as a result of any of these or other related factors, which we may not be able to manage successfully, and which could have a material adverse effect on our results of operations and financial condition on a consolidated basis.

We may have only limited recourse for losses relating to an acquisition.

The due diligence conducted in connection with an acquisition that we make and the indemnification that may be provided in the related acquisition agreement may not be sufficient to protect us from, or compensate us for, losses resulting from such acquisition. Subject to certain exceptions, the seller may only be liable for misrepresentations or breaches of representations and warranties for several months from the closing date of the acquisition. A material loss associated with the acquisition for which there is no adequate remedy under the acquisition agreement that becomes known to us after that time could materially adversely affect our results of operations and financial condition and reduce the anticipated benefits of the acquisition.

We may not be able to adopt new technologies important to our business.

Technology standards in internet and value-added telecommunications services and products in general, and in online education in particular, may change over time. If we fail to anticipate and adapt to technological changes, our market share and our business development could suffer, which in turn could have a material and adverse effect on our financial condition and results of operations. If we are unsuccessful in addressing any of the risks related to the technology that we utilize, our reputation and business may be materially and adversely affected.

Failure to effectively and efficiently manage the expansion of our school network may materially and adversely affect our ability to capitalize on new business opportunities.

We plan to pursue a number of different strategies to expand our operations. These strategies include:

| · | acquiring existing education institutions that align with our business plan, | |

| · | exploring blockchain and artificial intelligence technology to be applied into our business, | |

| · | expanding our relationship with agents who recruit students on our behalf, | |

| · | bringing international students to Canada who will pay higher tuition fees, thereby generating more revenues than domestic students, | |

| · | enhancing our infrastructure in Canada, and | |

| · | opening additional campuses in Canada. |

We acquired control of MTM and Conbridge on February 28, 2022 and September 1, 2021, respectively. We plan to expand their program offerings and partnerships. The rapid pace at which we have expanded and plan to continue expanding may place substantial demands on our management, faculty, administrators, operational, technological and other resources. In particular, we may face challenges in the following areas:

| · | controlling costs and developing operating efficiencies to manage the financial side of our expansion; | |

| · | maintaining the consistency of our teaching quality and our culture to ensure that recognition of our brands does not suffer; | |

| · | improving our existing operational, administrative and technological systems and our internal control over financial reporting; | |

| · | recruiting, training and retaining additional qualified instructors and management personnel as well as other administrative and sales and marketing personnel, particularly as we expand into new markets; | |

| · | continuing to market our brands to recruit new students for existing and future learning centers; and | |

| · | obtaining the necessary government approvals to operate in new schools and programs. |

| 6 |

We cannot assure you that we will be able to effectively and efficiently manage the growth of our operations. Any failure to effectively and efficiently manage our expansion may materially and adversely affect our ability to capitalize on new business opportunities or effectively run our existing operations, which in turn may have a material adverse impact on our business, our internal control over financial reporting, our financial condition and our results of operations.

If fewer international students aspire to study abroad, especially in the Canada, demand for our international schools may decline.

One of the principal drivers of the growth of our schools has been the increasing number of international students who aspire to study abroad, especially in Canada. As such, any adverse changes in immigration policy or political sentiments toward foreigners and immigrants, terrorist attacks, geopolitical uncertainties and any international conflicts involving these countries could increase the difficulty for international students to study overseas or decrease the appeal of studying in Canada to international students. Any significant change in admission standards for international students could also affect the demand for overseas education by international students.

In addition, any fluctuation in the currency exchange rate could have a negative impact on the translation of home country currencies into Canadian dollars, which may increase the costs of living and tuition for international students studying abroad. The attractiveness of pursuing education in Canada may decrease accordingly, which could adversely affect our business and profitability.

Furthermore, international students may also become less likely to study abroad due to other reasons, such as improving domestic education or employment opportunities associated with continued economic development in their home countries. These factors could cause declines in the demand for our schools, which may adversely affect our business and profitability.

Our students in Canada are subject to risks relating to financial aid and student loans. A substantial decrease in government student loans, or a significant increase in financing costs for our students, could have a material adverse effect on student enrollment and financial results.

Our Canadian and foreign students are highly dependent on government-funded financial aid programs. Students apply for student loans on an annual basis. Changes to financial aid program regulations that restrict student eligibility or reduce funding levels for student loans, may adversely affect our enrollment and collection of student billings, causing revenues to decline.

Students who are Canadian citizens also receive a tax deduction for all or a portion of the amount of tuition paid by the individual in a particular tax year, and an amount for textbooks (called an education tax credit) that is based on whether the student attended on a “full-time” or “part-time” basis, as set out in applicable Canadian and provincial income tax laws. The availability of these tax credits may impact the financial ability of our students to enroll in our programs and if such tax credits were to be eliminated or reduced, our enrollment levels may decline, which could result in a decrease in our revenues.

If we are not able to continue to attract students to enroll in our courses, our revenues may decline and we may not be able to maintain profitability.

The success of our business depends primarily on the number of students enrolled in our schools and courses and the amount of course fees that our students are willing to pay. Our ability to continue increasing our student enrollment levels without a significant decrease in course fees is critical to the continued success and growth of our business. This in turn will depend on several factors, including our ability to develop new programs and enhance existing programs to respond to changes in market trends and student demands, manage our growth while maintaining the consistency of our teaching quality, effectively market our programs to a broader base of prospective students, develop and license additional high-quality educational content and respond to competitive pressures. If we are unable to continue to attract students to enroll in our courses without a significant decrease in course fees, our financial condition, results of operations and cash flows could be materially adversely affected.

| 7 |

If we fail to develop and introduce new courses, services and products that meet our students’ expectations, our competitive position and ability to generate revenues may be materially and adversely affected.

Our core business is centered on providing our education programs and training services in Canada. Unexpected technical, operational, logistical, regulatory or other problems could delay or prevent the introduction of one or more new programs or services. Moreover, we cannot assure you that any of these programs or services will match the quality or popularity of those developed by our competitors, achieve widespread market acceptance, or generate the desired level of income.

Our new courses and services may compete with our existing courses and services.

We are constantly developing new courses and services to meet changes in student demands, school curriculum, testing materials, government policies, market trends and technologies. While some of the courses and services that we develop will expand our current course catalogue and services and increase student enrollment, others may compete with or render obsolete our existing courses and services without increasing our total student enrollment. If we are unable to increase our total student enrollment and profitability as we expand our course catalogue and services, our business and growth may be adversely affected.

Our quarterly results of operations are likely to fluctuate based on our seasonal student enrollment patterns.

Our business is seasonal in nature, and we receive the bulk of our cash flows at the beginning of each new school term. Accordingly, our results in a given quarter may not be indicative of our results in any subsequent quarter or annually. Our quarterly results of operations have tended to fluctuate as a result of seasonal variations in our education business in Canada, principally due to seasonal enrollment patterns. Our second quarter results tend generally to be relatively low as few students are enrolled in courses over the summer.

Changes in our total student population may influence our quarterly results of operations. Our student population varies as a result of new student enrollments, graduations and student attrition.

Our schools’ academic schedule generally does not affect our costs, and our costs do not fluctuate significantly on a quarterly basis. Fluctuations in quarterly results, however, may impact management’s ability to accurately project the available cash flows necessary for operating and growing expenses through internal funding. We expect quarterly fluctuations in results of operations to continue as a result of seasonal enrollment patterns. These patterns may change, however, as a result of new campus openings, new program offerings and increased enrollment of adult students. Our operating results have fluctuated and may continue to fluctuate widely.

We operate in a highly competitive industry, and competitors with greater resources could harm our business, decrease market share and put downward pressure on our tuition rates.

The secondary and post-secondary education market is highly fragmented and competitive. We compete for students with traditional high schools, public and private colleges and universities, other not-for-profit schools, including those that offer online learning programs, and alternatives to higher education, such as employment and military service. Many public and private high schools, colleges, and universities offer online programs. We expect to experience additional competition in the future as more high schools, colleges, universities, and for-profit schools offer an increasing number of online programs due in part to the pandemic. Public institutions receive substantial government subsidies, and public and private non-profit institutions have access to government and foundation grants, tax-deductible contributions, and other financial resources generally not available to for-profit schools. Accordingly, public and private nonprofit institutions may have instructional and support resources superior to those in the for-profit sector, and public institutions can offer substantially lower tuition prices. Some of our competitors in both the public and private sectors also have substantially greater financial and other resources than we have. We may not be able to compete successfully against current or future competitors and may face competitive pressures that could adversely affect our business, prospects, financial condition, and results of operations. These competitive factors could cause our enrollments, revenues, and profitability to significantly decrease.

| 8 |

Compliance with rules and requirements applicable to public companies may cause us to incur increased costs, which may negatively affect our results of operations.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002, the Dodd-Frank Wall Street Reform and Consumer Protection Act, and related regulations implemented by the SEC and NASDAQ are increasing legal and financial compliance costs and making some activities more time consuming. We are currently evaluating and monitoring developments with respect to new and proposed rules and cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. These laws, regulations and standards are subject to varying interpretations, in many cases due to their lack of specificity, and, as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. We intend to invest resources to comply with evolving laws, regulations and standards, and this investment may result in increased general and administrative expenses and a diversion of management’s time and attention from revenue-generating activities to compliance activities. If our efforts to comply with new laws, regulations and standards differ from the activities intended by regulatory or governing bodies due to ambiguities related to practice, regulatory authorities may initiate legal proceedings against us and our business may be harmed. We also expect that these new rules and regulations will make it more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. These factors could also make it more difficult for us to attract and retain qualified directors to sit on our board of directors, particularly to serve on our audit committee and compensation committee, and qualified executive officers.

We have an understanding with the Canadian Revenue Agency to satisfy our obligation to pay our income tax payable and other tax payable in 2022, but the failure to satisfy such obligation could have an adverse impact on our financial condition.

As of March 31, 2023, we had accrued and unpaid income tax liabilities of $1.5 million and other unpaid tax liabilities of $0.9 million, in both cases including penalties and interest. We believe that we have an oral understanding with the Canada Revenue Agency (the “CRA”) to pay all such tax liabilities by installments starting from September 1, 2023. If the CRA determines that there is a risk of not collecting all or part of the assessed corporate income tax debt, it can apply to the federal court or the superior court of a province for a jeopardy order, which will allow the CRA to seize any assets that the company owns and to take immediate action to collect the debt.

The CRA has not commenced or threatened any action to collect such delinquent tax payments as of the date of this annual report. We intend to satisfy these liabilities, including any penalties and interest, from our operating income and advances from affiliates, including Ms. Zhou. However, we expect the payments of unpaid taxes will have an adverse effect on our 2024 cash flow, but will not affect our operating income. The failure to pay these liabilities and any resulting enforcement action by the CRA could have a material adverse impact on our operations, financial condition, results of operations, and prospects.

Risks Related to Doing Business in Canada

Failure to obtain or maintain our cooperative relationship or partnership with public colleges in Canada may adversely affect our business.

We plan to partner with one or more colleges in Canada in the form of PPP. In a PPP partnership contract, we will provide to a public college applied arts and technology college programs leading to an Ontario College Credential. If we fail to obtain such partnerships or fail to maintain them, or if any unforeseeable events cause us to terminate our cooperation with our partner public colleges, we may not be able to accomplish our business goals and our prospects will suffer.

We are exposed to currency exchange risk which could cause our reported earnings or losses to fluctuate.

The value of the Canadian dollar, or CAD, against the U.S dollar fluctuates and is affected by, among other things, changes in political and economic conditions in Canada as well as the global economy. We can offer no assurance that the CAD will be stable against the U.S. dollar or any other foreign currency.

| 9 |

Our reporting currency is the U.S. dollar. However, all of our assets, liabilities, revenues and expenses are denominated in CAD. As a result, we are exposed to currency exchange risk on any assets and liabilities and revenues and expenses denominated in currencies other than the U.S. dollar. To the extent the U.S. dollar strengthens against CAD, the translation of CAD denominated transactions results in reduced revenue, operating expenses and net income or loss for our international operations. Similarly, to the extent the Canadian dollar weakens against foreign currencies, the translation of these foreign currency denominated transactions results in increased revenue, operating expenses and net income or loss for our international operations. We do not currently engage in currency hedging transactions to offset fluctuating currency exchange rates.

It may be difficult for non-Canadian citizens to enforce a judgment against us.

We were incorporated in Canada, and our corporate headquarters is located in Canada. A majority of our directors and executive officers and certain of the experts named in this annual report reside principally in Canada and all of our assets and all or a substantial portion of the assets of these persons are located outside the United States. It may be difficult for investors who reside in the United States to effect service of process upon these persons in the United States, or to enforce a U.S. court judgment predicated upon the civil liability provisions of the U.S. federal securities or other U.S. laws against us or any of these persons. There is substantial doubt whether an action could be brought in Canada in the first instance predicated solely upon U.S. federal securities laws. Canadian courts may refuse to hear a claim based on an alleged violation of U.S. securities laws against us or these persons on the grounds that Canada is not the most appropriate forum in which to bring such a claim. Even if a Canadian court agrees to hear a claim, it may determine that Canadian law and not U.S. law is applicable to the claim. If U.S. law is found to be applicable, the content of applicable U.S. law must be proved as a fact, which can be a time-consuming and costly process. Certain matters of court procedures will also be governed by Canadian law.

Operating Risks

Loss of certain key personnel may adversely impact our business.

The success of our business will depend on the management skills of Ms. Fan Zhou, our Chairman of the Board, and the relationships they and other key personnel have with educators, administrators and other business contacts they have overseas and in Canada. The loss of the services of any of our key personnel could impair our ability to successfully manage our business in Canada. We also depend on successfully recruiting and retaining qualified and experienced managers, salesperson and other personnel who can function effectively in Canada. In some cases, the market for these skilled employees is highly competitive. We may not be able to retain or recruit such personnel on acceptable terms to us, which could adversely affect our business prospects and financial condition.

The personal information that we collect may be vulnerable to breach, theft, or loss, which could subject us to liability or adversely affect our reputation and operations.

Possession and use of personal information in our operations subjects us to risks and costs that could harm our business and reputation. We collect, use and retain large amounts of personal information regarding our students and their families, including personal and family financial data. We also collect and maintain personal information of our employees in the ordinary course of business. Although we use security and business controls to limit access and use of personal information, a third party may be able to circumvent those security and business controls, which could result in a breach of student or employee privacy. In addition, errors in the storage, use or transmission of personal information could result in a breach of student or employee privacy. Possession and use of personal information in our operations also subjects us to legislative and regulatory burdens that could require us to implement certain policies and procedures, regarding the identity theft related to student credit accounts, and could require us to make certain notifications of data breaches and restrict our use of personal information. A violation of any laws or regulations relating to the collection or use of personal information could result in the imposition of fines against us. As a result, we may be required to expend significant resources to protect against the threat of these security breaches or to alleviate problems caused by these breaches. While we believe we take appropriate precautions and safety measures, there can be no assurances that a breach, loss or theft of any such personal information will not occur. Any breach, theft or loss of such personal information could have a material adverse effect on our financial condition, reputation and growth prospects and result in liability under privacy statutes and legal actions against us.

| 10 |

We may not be able to attract and retain a sufficient number of qualified teachers and principals.

As an education service provider, our ability to recruit and retain qualified teachers and principals is crucial to the quality of our education and services and our brand and reputation. To ensure our successful operation and growth, we need to retain and continue to hire high-quality teachers specialized in specific subjects that are able to teach the courses we offer or plan to offer to our students, as well as high-quality principals who are able to effectively manage the operation of our schools. We must provide competitive compensation and benefits packages to attract and retain qualified candidates. However, there is no guarantee that we would be able to keep recruiting teachers and principals meeting the high standards in the future, or retain our current, high-quality teachers and principals, especially when we seek a more rapid expansion plan to meet the growing demands for our services. Furthermore, under our business model, we may not be able to provide extensive training to our newly hired teachers for them to familiarize with our teaching methods and to retain existing teachers who can provide such trainings. A shortage of high-quality teachers and principals, a decrease in the quality of our teachers’ and principals’ performance, whether actual or perceived, or a significant increase in the cost to engage or retain high-quality teachers and principals would have a material adverse effect on our business, financial condition and results of operations.

Some students may decide not to continue taking our courses for a number of reasons, including a perceived lack of improvement in their performance in specific courses, a change in requirements or general dissatisfaction with our programs, which may adversely affect our business, financial condition, results of operations and reputation.

The success of our business depends in large part on our ability to retain our students by delivering a satisfactory learning experience and improving their performance in the courses they have taken. If students feel that we are not providing them the experience they are seeking, they may choose not to renew their existing packages. For example, our courses may fail to significantly improve a student’s performance in the relevant subject area. Student satisfaction with our programs may decline for a number of reasons, many of which may not reflect the effectiveness of our lessons and teaching methods. Students also need to be self-motivated in order to successfully complete the courses in which they enroll. If students’ performances decline as a result of their own study habits or inability to learn the course material, they may not renew their memberships with us or refer other students to us, which could materially adversely affect our business.

A student’s learning experience may also suffer if his user experience does not meet expectations. If a significant number of students fail to significantly improve their proficiency in the applicable course subject after taking our lessons or if their learning experiences with us are unsatisfactory, they may not renew their enrollment with us or refer other students to us and our business, financial condition, results of operations and reputation would be adversely affected.

Risks Related to Our Common Shares

Should our Common Shares not qualify for an exemption from being classified as a “Penny Stock,” the ability of shareholders to sell our Common Shares in the secondary market will be limited should our Common Shares not be listed on a national securities exchange.

The SEC has adopted regulations which generally define a “penny stock” to be an equity security that has a market price, as defined, of less than $5.00 per share, or an exercise price of less than $5.00 per share, subject to certain exceptions, including an exception of an equity security that is quoted on a national securities exchange. Should our Common Shares not be quoted on a national exchange such as NASDAQ and have a market price less than $5.00 per share, they will be subject to rules that impose additional sales practice requirements on broker-dealers who sell these securities. For example, the broker-dealer must make a special suitability determination for the purchaser of such securities and have received the purchaser’s written consent to the transactions prior to the purchase. Additionally, the rules require the delivery, prior to the transaction, of a disclosure schedule prepared by the SEC relating to the penny stock market. The broker-dealer also must disclose the commissions payable to both the broker-dealer and the registered Underwriters, and current quotations for the securities, and, if the broker-dealer is the sole market maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market. Finally, among other requirements, monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. The “penny stock” rules, may restrict the ability of our stockholders to sell our Common Shares in the secondary market.

| 11 |

One Person Has Significant Voting Power and May Take Actions That May Not Be in the Best Interests of Other Stockholders.

Ms. Zhou, our founder, majority shareholder, CEO and Chairman of the board of director, controls 46.7% of our voting securities. Ms. Zhou is able to exert significant control over our management and affairs requiring stockholder approval, including approval of significant corporate transactions. This concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of the Common Shares. This concentration of ownership may not be in the best interests of all of our stockholders. On April 23, 2018, the Guangdong Province Securities Regulatory Bureau, or the Bureau, of China gave a warning and minimal fine to Zhongqing Langdun (Taihu) Educational Culture Technology Co., Ltd. or Langdun China and to Fan Zhou (approximately $14,000) in an administrative proceeding. Langdun China was listed on the National Equities Exchange and Quotation, or the NEEQ, a Chinese over the counter market and had only 12 beneficial shareholders. The Bureau found that (i) Langdun China reported the purchase of certain assets later than was required and (ii) filed audited financial statements for 2014 that overstated its profits and understated certain expenses. The decision was upheld on appeal. Langdun China believed that it justifiably relied on the audited financial statements of China Langdun for 2014, which had been audited by Pan-China Certified Public Accountants LLP, one of the top three domestic accounting firms in China. Fan Zhou was included in the administrative proceeding because she served Langdun China as its Legal Representative (the principal employee who performs duties on behalf of the company in accordance with the law).

Certain provisions of our Amended Articles of Incorporation may make it more difficult for a third party to effect a change in control.

Our Amended Articles of Incorporation authorizes our board of directors to issue an unlimited number of shares of preferred stock. While no shares of preferred stock have been issued to date, the preferred stock may be issued in one or more series, the terms of which may be determined at the time of issuance by our board of directors without further action by the stockholders. These terms may include voting rights including the right to vote as a series on particular matters, preferences as to dividends and liquidation, conversion rights, redemption rights and sinking fund provisions. The issuance of any preferred stock could diminish the rights of holders of our Common Shares, and therefore could reduce the value of such Common Shares. In addition, specific rights granted to future holders of preferred shares could be used to restrict our ability to merge with, or sell assets to, a third party. The ability of our board of directors to issue preferred shares could make it more difficult, delay, discourage, prevent or make it more costly to acquire or effect a change-in-control, which in turn could prevent the stockholders from recognizing a gain in the event that a favorable offer is extended and could materially and negatively affect the market price of our Common Shares.

We are a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to U.S. domestic public companies.

Because we are a foreign private issuer under the Exchange Act, we are exempt from certain provisions of the securities rules and regulations in the United States that are applicable to U.S. domestic issuers, including:

| · | the rules under the Exchange Act requiring the filing of quarterly reports on Form 10-Q or current reports on Form 8-K with the SEC; |

| · | the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; |

| · | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| · | the selective disclosure rules by issuers of material nonpublic information under Regulation FD. |

We are required to file an annual report on Form 20-F within four months of the end of each fiscal year. Press releases relating to financial results and material events will also be furnished to the SEC on Form 6-K. However, the information we are required to file with or furnish to the SEC will be less extensive and less timely than that required to be filed with the SEC by U.S. domestic issuers. As a result, you may not be afforded the same protections or information that would be made available to you were you investing in a U.S. domestic issuer.

| 12 |

We are an emerging growth company within the meaning of the Securities Act and may take advantage of certain reduced reporting requirements.

We are an “emerging growth company,” as defined in the JOBS Act, and we may take advantage of certain exemptions from requirements applicable to other public companies that are not emerging growth companies including, most significantly, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 for so long as we remain an emerging growth company. As a result, if we elect not to comply with such auditor attestation requirements, our investors may not have access to certain information they may deem important. The JOBS Act also provides that an emerging growth company does not need to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards.

The market price for our Common Shares may be volatile.

The market price for our Common Shares may be volatile and subject to wide fluctuations in response to factors such as actual or anticipated fluctuations in our quarterly results of operations, changes in financial estimates by securities research analysts, changes in the economic performance or market valuations of other comparable companies, announcements by us or our competitors of material acquisitions, strategic partnerships, joint ventures or capital commitments, fluctuations of exchange rates between the Canadian dollar and the U.S. dollar, intellectual property litigation, release of lock-up or other transfer restrictions on our outstanding Common Shares, and economic or political conditions in Canada. In addition, the performance, and fluctuation in market prices, of other companies with business operations located mainly in Canada that have listed their securities in the United States may affect the volatility in the price and trading volumes of our Common Shares.

We may be classified as a passive foreign investment company, which could result in adverse U.S. federal income tax consequences to U.S. holders of our Common Shares.

We do not expect to be considered a “passive foreign investment company”, or PFIC, for U.S. federal income tax purposes for our taxable year ending March 31, 2023. However, the application of the PFIC rules is subject to ambiguity in several respects, and we must make a separate determination each taxable year as to whether we are a PFIC (after the close of each taxable year). Accordingly, we cannot assure you that we will not be a PFIC for the taxable year ending March 31, 2023 or any future taxable year. A non-U.S. corporation will be considered a PFIC for any taxable year if either (i) at least 75% of its gross income is passive income or (ii) at least 50% of the value of its assets is attributable to assets that produce or are held for the production of passive income. The market value of our assets generally will be determined based on the market price of our Common Shares, which is likely to fluctuate. In addition, the composition of our income and assets will be affected by how, and how quickly, we spend the cash we raised. A significant portion of our assets and income is attributable to real estate and may be passive income under PFIC rules. If we were treated as a PFIC for any taxable year during which a U.S. person held a Common Share, certain adverse U.S. federal income tax consequences could apply to such U.S. person. See “Taxation—U.S. Federal Income Tax Consequences – PFIC Rules”.

We do not intend to pay dividends and there will be fewer ways in which you can make a gain on any investment in us.

We have never paid any cash dividends and currently do not intend to pay any dividends for the foreseeable future. To the extent that we require additional funding currently not provided for in our financing plan, our funding sources may likely prohibit the payment of dividends. Because we do not intend to declare dividends, any gain on an investment in us will need to come through appreciation of our stock price.

We indemnify our directors and officers against liability, and this indemnification could negatively affect our operating results.

In accordance with our by-laws, we indemnify our officers and our directors for liability arising while they are carrying out their respective duties. Our by-laws also allow for reimbursement of certain legal defenses. In addition to this, we intend to provide insurance to our directors and officers against certain liabilities. The costs related to such indemnification and insurance coverage, if either one of them or both were to increase, could materially adversely affect our operating results and financial condition.

| 13 |

We have limited insurance coverage with respect to our business and operations.

We are exposed to various risks associated with our business and operations, and we have limited insurance coverage. We are exposed to risks including, among other things, accidents or injuries in our schools, loss of key management and personnel, business interruption, natural disasters, terrorist attacks and social instability or any other events beyond our control. We do not have any business interruption insurance, or key-man life insurance. Any business interruption, legal proceeding or natural disaster or other events beyond our control could result in substantial costs and diversion of our resources, which may materially and adversely affect our business, financial condition and results of operations.

ITEM 4. INFORMATION ON THE COMPANY

| A. | History and Development of the Company |

Introduction

Visionary Education Technology Holdings Group Inc. was founded in 2013 by Ms. Zhou, a vocational educator in Canada. We were incorporated by Ms. Zhou on August 20, 2013, as 123 Natural Food Ontario Ltd., a company limited by shares, under the Ontario Business Corporations Act. Our original goal was to develop and operate an international education platform focused on vocational education based on agricultural technology. However, we did not pursue this goal due to marketing barriers caused by the over specialization of the concept and a limited market.

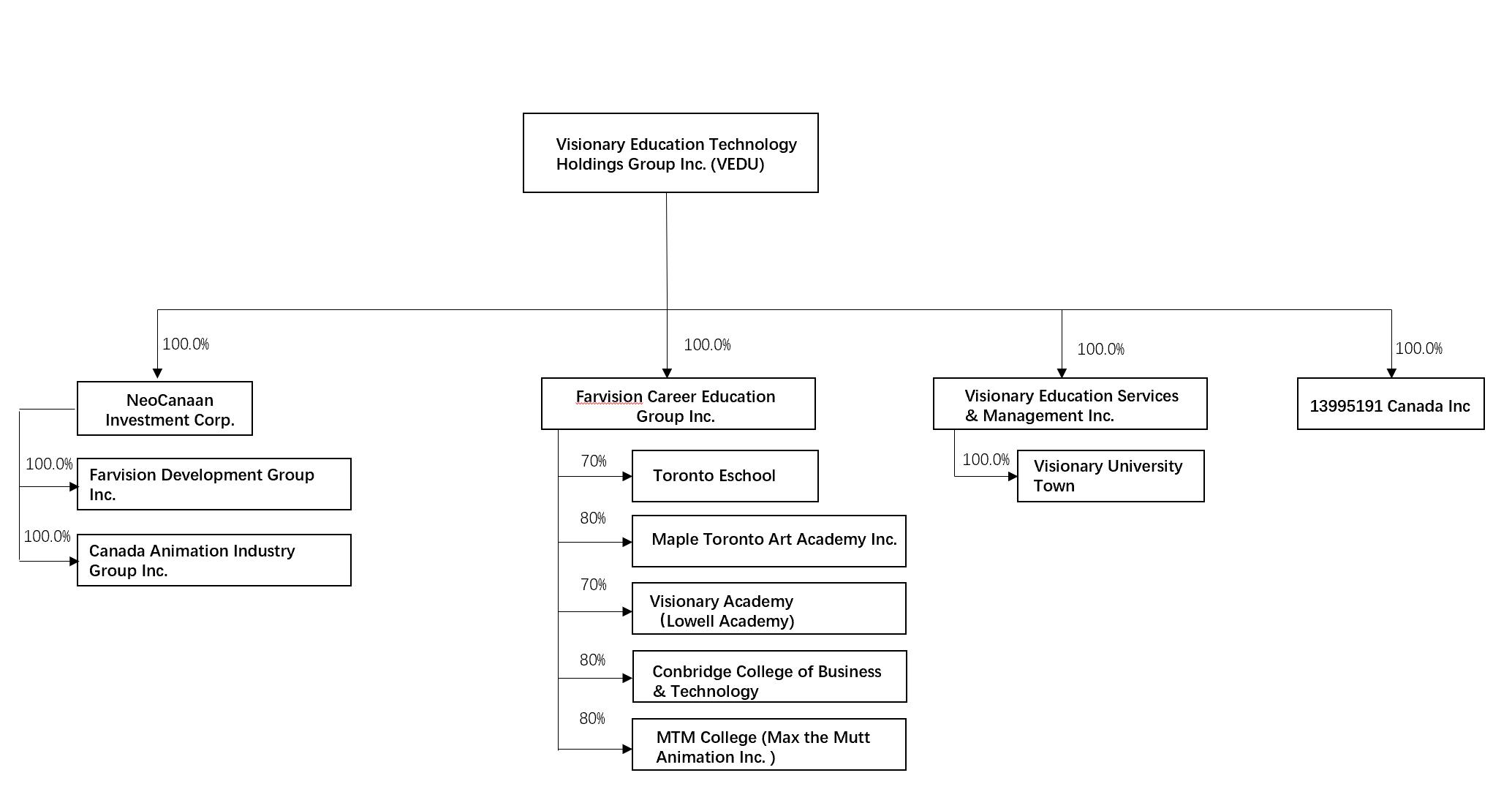

In 2015, Ms. Zhou redirected our business toward an international education program focused on the OSSD. She launched a new company, China Youth Langton (Canada) Education Technology Ltd., or Langton. Langton, as the majority investor, and unaffiliated third-party investors organized Toronto ESchool Inc., or Toronto ESchool, on March 7, 2016, to provide grades 9 through 12 online OSSD courses. On November 15, 2017, we entered into a share purchase agreement to acquire a 55% equity interest in Toronto ESchool from Langton for a nominal purchase price of $0.8. Ms. Zhou sold her interest in Langton in 2018 to an unaffiliated party. On June 19, 2020, we acquired an additional 15% equity interest in Toronto ESchool from one of its third-party investors for $31,808. As a result of this transaction, we own a 70% equity interest of Toronto ESchool. On June 19, 2020, we transferred our 70% equity interest in Toronto ESchool to our wholly owned subsidiary Farvision Education Group Inc.

Concurrently with our organization, Ms. Zhou founded a separate company to acquire and develop educational real estate facilities as a complement to the education company. To better explore the international market and to enhance our competitiveness, Ms. Zhou increased her investment in teaching facilities through 123 Real Estate Development Ontario Ltd., or 123 Real Estate, which she organized on August 20, 2013. From 2013 through 2015 123 Real Estate purchased 22.4 acres of vacant land in Peterborough, Ontario, which was originally planned to be developed into an international student housing center. On November 14, 2015, 123 Real Estate purchased a building at 41 Metropolitan Road, Toronto, for use as a headquarters and teaching facility for international education On April 1, 2019, we acquired all the shares of 123 Real Estate from Ms. Zhou for $3,210,000 to enable us to own the office building and the vacant land and develop the land into a facility for international student services. In April 2021, we purchased office buildings at 200 and 260 Town Centre Blvd. to provide additional revenue from leasing and space for expansion of our educational facilities. On May 28, 2021, 123 Real Estate Development Ontario Ltd. changed its name to Visionary Education Real Estate Group Inc. On October 15, 2021, Visionary Education Real Estate Group Inc changed its name to Visionary Education Services and Management Inc.

On February 25, 2019, Visionary Education Services and Management Inc., then known as 123 Real Estate Development Ontario Ltd., entered into a share purchase agreement to acquire 100% of the equity interests in PrideMax Construction Group Inc., or PrideMax Construction, from its original shareholder for a nominal fee of $0.80. Incorporated on July 20, 2010 in Scarborough, Ontario, PrideMax Construction had no active business since its inception. The transaction was completed on April 1, 2019. On May 23, 2020, 123 Real Estate Development Ontario Ltd. transferred its 100% ownership in PrideMax Construction to NeoCanaan Investment Corporation, which was 100% owned by us, for a nominal fee of $0.80. On June 16, 2021, PrideMax Construction changed its name to Farvision Development Group Inc., or Farvision Development; On Novebmber 3, 2022, Farvision Development Group Inc. changed its name to Farvision Digital Technology Group Inc., or Farvision Digital.

Between 2017 and 2019, we conducted a survey of the international market for OSSD. Based on the promising market opportunity for OSSD, we gradually built up a network of agents in Southeast Asia, India and South America to recruit students for our OSSD programs. In the meantime, we also developed online teaching dossiers for more than 60 OSSD courses (core courses and a broad range of elective courses). We established collaboration with educational organizations such as Mississauga District School Board and Trent University. The collaboration includes developing OSSD teaching methods and technologies, school management, and student promotion. We concluded that the initial results of this initiative and operation were promising.

| 14 |

However, we were adversely impacted by the COVID-19 pandemic beginning early in 2020. Our tuition and other revenue dropped precipitously. Without exception, the entire education industry in Canada has suffered from the difficulties caused by the pandemic. To survive while still creating opportunity to grow, we made significant changes to our strategic plan and commenced exploring new businesses. In response to the special economic environment in Canada, we optimized our educational assets so our operation could concentrate in the Toronto metropolitan area. We sold most of our land in Peterborough and channeled the income to the acquisition of quality educational organizations and institutional buildings. We have grown through the acquisition of seven educational organizations and two institutional buildings at what we believe are favorably low prices. These acquisitions and the reorganization of our corporate structure are described below.

On May 14, 2020, Farvision Education Group Inc., or Farvision Education, was incorporated under the Canada Business Corporation Act. Farvision Education is our wholly owned subsidiary of Visionary Education Technology Holdings Group Inc. On February 2, 2023, Farvision Education Group Inc, has changed its name to Farvision Career Education Group Inc.