Table of Contents

As filed with the Securities and Exchange Commission on May 26, 2023

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GEN Restaurant Group, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 5812 | 87-3424935 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

11480 South Street Suite 205

Cerritos, CA 90703

(562) 356-9929

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

David Kim

Jae Chang

Co-Chief Executive Officers

GEN Restaurant Group, Inc.

11480 South Street Suite 205

Cerritos, CA 90703

(562) 356-9929

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Michael Flynn Peter Wardle Gibson, Dunn & Crutcher LLP 3161 Michelson Drive Irvine, CA 92612-4412 (949) 451-3800 |

Ryan Wilkins Amanda McFall Stradling Yocca Carlson & Rauth, P.C. 660 Newport Center Drive, Suite 1600 Newport Beach, CA 92660 (949) 725-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated May 26, 2023

PROSPECTUS

Shares

GEN Restaurant Group, Inc.

Class A Common Stock

This is GEN Restaurant Group, Inc.’s initial public offering. We are selling shares of our Class A common stock.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. After pricing of the offering, we expect that the shares of our Class A common stock will trade on The Nasdaq Global Market, or the Exchange, under the symbol “GENK.”

Each share of Class A common stock will entitle the holder to one vote, while each share of Class B common stock will entitle the holder to ten votes. The holders of our Class B common stock, all of whom were members of GEN LLC prior to this offering, including our co-founders, will hold an equal number of units of GEN LLC upon the completion of this offering, and will hold % of the combined voting power of our common stock immediately after this offering. The holders of our Class B common stock will have the ability to control the outcome of matters submitted to our stockholders for approval. See “Organizational Structure.”

We will be a “controlled company” under the corporate governance listing standards of the Exchange, following the completion of this offering. See “Management—Controlled Company Exemption.”

We are an “emerging growth company” and “smaller reporting company” as defined under the U.S. federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary—Implications of Being an Emerging Growth Company and Smaller Reporting Company.”

Investing in our Class A common stock involves risks that are described in the “Risk Factors” section beginning on page 18 of this prospectus.

| Per Share |

Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discount |

$ | $ | ||||||

| Proceeds to us, before expenses |

$ | $ | ||||||

The underwriters may also exercise an option to purchase up to an additional shares of our Class A common stock from us, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares of Class A common stock will be ready for delivery on or about , 2023.

Sole Book-Running Manager

| Roth Capital Partners |

Co-Managers

| Craig-Hallum Capital Group | The Benchmark Company |

The date of this prospectus is , 2023.

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Page | ||

| 1 | ||

| 18 | ||

| 51 | ||

| 53 | ||

| 61 | ||

| 62 | ||

| 63 | ||

| 64 | ||

| UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL INFORMATION AND OTHER DATA |

66 | |

| 70 | ||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

71 | |

| 92 | ||

| 105 | ||

| 111 | ||

| 115 | ||

| 117 | ||

| 124 | ||

| 130 | ||

| MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS FOR NON-U.S. HOLDERS OF CLASS A COMMON STOCK |

132 | |

| 136 | ||

| 145 | ||

| 145 | ||

| 145 | ||

| F-1 |

Neither we nor the underwriters have authorized anyone to provide you with information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are offering to sell, and seeking offers to buy, Class A common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our Class A common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Through and including , 2023 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside of the United States: We have not and the underwriters have not, done anything that would permit this offering, or possession or distribution of this prospectus, in any jurisdiction where action for that purpose is required, other than the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our Class A common stock and the distribution of this prospectus outside of the United States.

i

Table of Contents

GENERAL INFORMATION

Unless otherwise indicated or the context otherwise requires, references in this prospectus to (i) “GEN Inc.” refers to GEN Restaurant Group, Inc., a Delaware corporation, the company conducting the offering made pursuant to this prospectus and not to any of its subsidiaries, (ii) “GEN Restaurant Group” refers to an unconsolidated group of entities listed in the historical financial statements included in this prospectus and owned primarily by either David Kim or Jae Chang, our co-Chief Executive Officers and Directors, (iii) “GEN LLC” refers to GEN Restaurant Companies, LLC, a Delaware limited liability company and subsidiary of GEN Inc., and (iv) the “Company,” “we,” “us,” “our” and “GEN” refer to GEN Inc. and its consolidated subsidiaries. GEN Inc. was incorporated as a Delaware corporation on October 28, 2021 and, prior to the consummation of the Reorganization described herein and our initial public offering, did not conduct any activities other than those incidental to our formation and our initial public offering.

Basis of Presentation

This prospectus includes certain historical financial and other data for GEN Restaurant Group. The results of GEN Restaurant Group represent the combined results of 19 restaurants owned primarily by David Kim and 12 restaurants owned primarily by Jae Chang. These restaurants have been operated by Mr. Kim or Mr. Chang independently on an unconsolidated basis, but in a substantially similar manner under the name GEN Korean BBQ House. Just prior to the consummation of this offering, as a part of the Reorganization, these 31 restaurants, in addition to the restaurant opened in 2023, will be consolidated into a single corporate structure under GEN LLC. Following this offering and the Reorganization, GEN Restaurant Group will be the predecessor of GEN Inc. for financial reporting purposes. Immediately following this offering, GEN Inc. will be a holding company, and its sole material asset will be a controlling equity interest in GEN LLC. As the sole managing member of GEN LLC, GEN Inc. will operate and control all of the business and affairs of GEN LLC and, through GEN LLC and its subsidiaries, conduct our business. GEN Inc. will consolidate GEN LLC on its consolidated financial statements and record a noncontrolling interest related to the Class B units held by the Class B stockholders on its consolidated balance sheet and statement of operations. See “Organizational Structure.”

Numerical figures included in this prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

Market and Industry Data

This prospectus contains estimates, projections and other information concerning our industry, our business and the markets for our restaurants. Some market data and statistical information contained in this prospectus are also based on management’s estimates and calculations, which are derived from our review and interpretation of the independent sources listed below, our internal research and knowledge of our market. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such information. We have not independently verified market data and industry forecasts provided by any of these or any other third-party sources referred to in this prospectus. In addition, projections, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in the sections titled “Risk Factors” and “Forward-Looking Statements” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the projections and estimates made by the independent third parties and us.

Unless otherwise expressly stated, we obtained industry, business, market and other data from the reports, publications and other materials and sources listed herein. In some cases, we do not expressly refer to the sources from which this data is derived. In that regard, when we refer to one or more sources of this type of data in any paragraph, you should assume that other data of this type appearing in the same paragraph is derived from the same sources, unless otherwise expressly stated or the context otherwise requires.

ii

Table of Contents

Information contained on any website or linked therein or otherwise connected thereto does not constitute part of and is not incorporated by reference into this prospectus or the registration statement of which this prospectus forms a part. We have included the website address in this prospectus solely as an inactive textual reference.

Trademarks

We own or have the rights to use various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not, imply a relationship with, or endorsement or sponsorship by, us. Solely for convenience, the trademarks, service marks and trade names presented in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks, service marks and trade names.

Non-GAAP Financial Measures

Adjusted EBITDA is not recognized under GAAP. We define Adjusted EBITDA as net income (loss) before net interest expense, income taxes, depreciation and amortization, and consulting fees paid to a related party and we also exclude non-recurring items, such as gain on extinguishment of debt, and Restaurant Revitalization Fund, or RRF, grants, employee retention credits, litigation accruals, aborted deferred IPO costs written off and non-cash lease expenses. Adjusted EBITDA Margin is defined as Adjusted EBITDA divided by revenue. We define Restaurant-Level Adjusted EBITDA as Income (loss) from operations plus adjustments to add-back the following expenses: depreciation and amortization, pre-opening costs, general and administrative expenses, related party consulting fees, management fees and non-cash lease expense. We define Restaurant-Level Adjusted EBITDA Margin as Restaurant-Level Adjusted EBITDA divided by revenue.

Adjusted EBITDA, Adjusted EBITDA Margin, Restaurant-Level Adjusted EBITDA and Restaurant-Level Adjusted EBITDA Margin are intended as supplemental measures of our performance that are neither required by, nor presented in accordance with, GAAP. We are presenting Adjusted EBITDA, Adjusted EBITDA Margin, Restaurant-Level Adjusted EBITDA and Restaurant-Level Adjusted EBITDA Margin because we believe that they provide useful information to management and investors regarding certain financial and business trends relating to our financial condition and operating results. We believe that the use of these non-GAAP financial measures provide additional tools for investors to use in evaluating ongoing operating results and trends and in comparing the Company’s financial measures with those of comparable companies, which may present similar non-GAAP financial measures to investors. Our presentation of these measures should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Our computation of these measures may not be comparable to other similarly titled measures computed by other companies, because all companies may not calculate these non-GAAP measures in the same fashion.

Because of these limitations, Adjusted EBITDA, Adjusted EBITDA Margin, Restaurant-Level Adjusted EBITDA and Restaurant-Level Adjusted EBITDA Margin should not be considered in isolation or as substitutes for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using these non-GAAP measures on a supplemental basis.

For reconciliations of Adjusted EBITDA, Adjusted EBITDA Margin, Restaurant-Level Adjusted EBITDA and Restaurant-Level Adjusted EBITDA Margin to their nearest GAAP financial measures, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures.”

Additional Financial Metrics and Other Data

As used in this prospectus, unless otherwise noted or the context otherwise requires:

| • | “Net Income Margin” means Net Income divided by revenue. |

iii

Table of Contents

| • | “Average Unit Volume” or “AUV” means the average annual restaurant sales for all restaurants open for a full 18 months before the end of the period measured. We have not made any adjustments to exclude restaurants in 2021 that experienced temporary closures and mandated capacity limitations caused by the COVID-19 pandemic. |

| • | “Cash-On-Cash Returns” means Restaurant-Level Adjusted EBITDA divided by Net Build-Out Costs. |

| • | “Net Build-Out Costs” means all capitalized construction and construction-related costs plus pre-opening costs associated with a new restaurant, less tenant improvement allowances provided by the landlord. |

| • | “Payback Period” means the length of time, in years, required to recoup Net Build-Out Costs after the restaurant opening date. |

| • | “Revenue Per Square Foot” means the average annual restaurant sales for all restaurants opened a full 18 months before the end of the period measured divided by average square footage of all such restaurants. |

iv

Table of Contents

This summary highlights selected information discussed in this prospectus. The summary is not complete and does not contain all of the information you should consider before investing in our Class A common stock. Therefore, you should read this entire prospectus carefully, including the sections titled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements and the related notes included elsewhere in this prospectus, before making a decision to purchase shares of our Class A common stock. Some of the statements in this summary constitute forward-looking statements. See “Forward-Looking Statements.”

Who We Are

GEN Korean BBQ is one of the largest Asian casual dining restaurant concepts by total revenue in the United States. Founded by two Korean immigrants, we have grown over the last eleven years to 32 company-owned restaurants as of May 26, 2023 by delivering an engaging and interactive dining experience where our guests serve as their own chefs. We offer an extensive menu of traditional Korean and Korean-American food, including high-quality meats, poultry, seafood and mixed vegetables, all at a superior value. Our restaurants have modern décor, lively Korean pop music playing in the background and embedded grills in the center of each table. Our food is served family style and requires guests to share and coordinate their cooking responsibilities, which fosters more meaningful interaction than traditional casual dining. We believe our unique culinary experience appeals to a vast segment of the population, particularly Millennials and Gen Z.

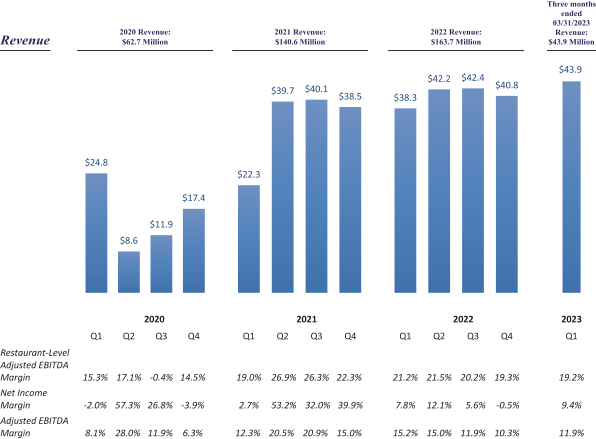

Our co-founders, Jae Chang and David Kim, both highly experienced and successful restaurateur, joined forces to create our new Korean barbeque concept, opening our first restaurant in 2011 in Tustin, California. Since then, we have successfully opened profitable restaurants in multiple new markets. As of May 26, 2023, we operated 32 locations across California, Arizona, Nevada, Hawaii, Texas and New York. Our revenues in the year ended December 31, 2022 surpassed the revenue levels in 2021. In 2022, we achieved a Net Income Margin of 6.3%, a Restaurant-Level Adjusted EBITDA Margin of 20.5% and an Adjusted EBITDA Margin of 13.1%. In the three months ended March 31, 2023, we achieved a Net Income Margin of 9.4%, a Restaurant-Level Adjusted EBITDA Margin of 19.2% and an Adjusted EBITDA Margin of 11.9%.

1

Table of Contents

Select Financial Results by Quarter

(unaudited)

For reconciliations of Net income to Adjusted EBITDA Margin and Restaurant-Level Adjusted EBITDA Margin, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quarterly Results of Operations.”

GEN Korean BBQ: An Engaging Dining Experience

We believe our restaurants offer a memorable dining experience. When our guests arrive, they are frequently met with crowds of other enthusiastic patrons eager to be seated. Guests are able to join our waitlist upon arrival, or ahead of time by checking in online, and can request their preferred seating option, choosing from our conventional table top grills, bars and, where available, outdoor seating areas.

As guests make their way to their tables, they are immediately met with the mouth-watering aromas and sizzling sounds of our offerings. From the unique modern décor, to the motion of our friendly staff quickly completing orders and the sounds of vibrant Korean pop music, the atmosphere in our restaurants is distinct and engages the senses.

2

Table of Contents

Once seated, guests are welcomed with a diverse assortment of appetizing side dishes, or banchan. After sampling the banchan, guests turn their attention to our extensive menu, which encourages adventurous dining. Our curated selection features premium cuts of unmarinated and marinated beef, pork, poultry, seafood and mixed vegetables. Our thinly sliced tender briskets, thick cut pork belly, sweet marinated chicken and spicy shrimp, among other favorites, make for a delicious culinary experience. Our guests are able to place unlimited orders of any food item all for one affordable, fixed price. Guests can also purchase alcoholic beverages to enjoy throughout their dining experience. Since our guests serve as their own chefs and cook the majority of their meals themselves on a grill embedded in the center of each table, they experience minimal wait times once seated, have full control over their portions and are able to grill their food at their desired pace and temperatures.

Our Innovative Approach Drives Our Competitive Strengths

We believe we have been able to distinguish ourselves from other restaurant concepts by taking an innovative approach, focused on efficiency without compromising quality, highlighted by the following strengths:

| • | Unlimited Orders at One Affordable, All-Inclusive Price. Our guests can order unlimited quantities of food for a fixed price generally ranging from $17.95 to $20.99 for lunch and $25.95 to $29.95 for dinner as of March 31, 2023, except $35.95 for dinner at the Miracle Mile at Las Vegas, NV location and $26.95 for lunch, $32.95 for regular dinner and $36.95 for late dinner at the Manhattan, NY location. Our affordable price points make our concept accessible to multiple demographics and allow our guests to discover a variety of traditional Korean and Korean-American fusion dishes at a fixed price compared to the a la carte pricing found at other casual dining restaurants. |

| • | Efficient “Cook-It-Yourself” Business Model. Using our “cook-it-yourself” model, we have been able to operate our restaurants with no chefs and limited personnel needed to process orders in the kitchen. Our menu items come ready-to-serve from our suppliers, allowing us to quickly fill guest orders after a simple transfer from package to plate. This approach ensures consistent food quality across all of our restaurants and provides for more efficient operations than traditional restaurants, which in turn allows us to cater to high traffic levels. Additionally, because our guests serve as their own chefs, we believe our kitchens require a smaller percentage of our footprint than other casual dining restaurant concepts, enabling more space for guest seating. |

| • | Strong Supplier Network Provides Foundation for Growth. We currently have informal arrangements with our key suppliers precluding them from selling Korean barbeque-related products to other distributors. In addition to our primary suppliers, we have established relationships with potential new suppliers that we can quickly engage if we are faced with supply chain disruptions. To date, we have not experienced any such disruptions. Our longstanding and consistent partnerships allow us to meet any increased demand we experience. As we continue to scale and open new restaurants, we believe our strong supply network has the ability to support our growth. |

| • | Large Community of Loyal Enthusiasts. Based in part on our online reviews, we believe we have attracted a passionate and loyal group of customers, including Millennial and Gen Z enthusiasts who enjoy trying new cuisines of various ethnic origins. We believe these “foodies” enjoy our diverse menu of flavorful Korean and Korean-American food, affordable price points and differentiated dining ambience. |

| • | Unique Guest Experience Drives Positive Customer Ratings. Many of our guests express their enthusiasm for our concept experience by rating and reviewing our restaurants online. As of May 24, 2023, we have a 4.0 and 4.2 average star rating on Yelp and Google across our restaurants with 2,722 and 1,293 average reviews per restaurant on Yelp and Google, respectively. These strong, positive reviews have allowed us to rely on this type of word-of-mouth advertising to increase brand awareness in lieu of more traditional marketing efforts. As a result, in 2022 and 2021, our annual marketing expenses comprised 0.1% of our total revenue. |

| • | In-House Design and Fabrication Capabilities. Well-functioning ventilation systems are critical to Korean barbeque restaurant concepts due to the need to simultaneously ventilate each table. In order to ensure a proper setup, many of our competitors rely on third-party contractors, who can be prohibitively expensive and require |

3

Table of Contents

| lengthy lead times. We take a different approach, designing and fabricating our ventilation systems in-house, which in turn provides us with greater control than our competition over quality, costs and lead times. |

| • | An Inspirational Founder-led Management Team. Our team is led by experienced and passionate senior management who are committed to providing the highest quality service and experience for our guests. Our co-founder, Jae Chang, has over 25 years of entrepreneurial experience in the restaurant and hospitality industry. Jae has grown a number of successful Asian restaurant concepts, including locations under the Shabuya, Sumo, Octopus, H2O Sushi and California Gogi brands. Our other co-founder, David Kim, is a seasoned restaurateur and entrepreneur who successfully established a career in the restaurant industry as a multi-unit franchisee of Denny’s, Carl’s Jr., Golden Corral and Pick-Up Stix. Prior to GEN, David led an investor consortium that purchased Baja Fresh from Wendy’s International, Inc., and later La Salsa, Inc. from CKE Restaurants. As CEO of Baja Fresh, David oversaw a company with sales of over $400 million and over 400 locations. |

Our Performance

All restaurants were operating with no COVID-19 capacity restrictions beginning with the second quarter of 2022. We achieved the following financial results for the three months ended March 31, 2023 compared to the three months ended March 31, 2022:

| • | Our revenue grew 14.7% to $43.9 million from $38.3 million. |

| • | Our net income attributable to GEN Restaurant Group increased 38.3% to $4.1 million from $3.0 million. |

| • | Our Restaurant-Level Adjusted EBITDA increased 3.6% to $8.4 million from 8.1 million. Our Restaurant Level Adjusted EBITDA Margin decreased to 19.2% from 21.2%. |

| • | Our Adjusted EBITDA decreased 10.3% to $5.2 million from $5.8 million. Our Adjusted EBITDA Margin decreased to 11.9% from 15.2%. |

We have also achieved the following financial metrics:

| • | AUVs of approximately $5.9 million for the 28 restaurants that were opened 18 full months prior to December 31, 2022 and $6.0 million for the 28 restaurants that were opened 18 full months prior to March 31, 2023. |

| • | Revenue per square foot of $890 for the 28 restaurants that were opened for 18 full months prior to December 31, 2022, and revenue per square foot of $899 for the 28 restaurants opened 18 full months prior to March 31, 2023. |

| • | Average Net Build-Out Costs of approximately $1.8 million for new units opened during 2018 and 2019 and $1.9 million for new units opened in 2022. |

| • | Average Cash-On-Cash Returns of 88% for the 28 restaurants open for all of 2022. |

| • | Average Payback Period of 1.4 years for the 21 restaurants that had covered initial investment costs prior to the temporary COVID-19 shutdowns in early 2020. |

We also achieved the following financial results for the year ended December 31, 2022 compared to the year ended December 31, 2021:

| • | Revenue for the year ended December 31, 2022 was $163.7 million compared to 2021 revenue of $140.6 million, an increase of $23.2 million or 16.5%. |

4

Table of Contents

| • | From 2021 to 2022, our net income attributable to GEN Restaurant Group decreased 79.4% from $49.9 million to $10.3 million largely due to $22.3 million of loan forgiveness and $13.0 million from a Restaurant Revitalization Fund grant we recognized only in 2021. Our Net Income Margin decreased to 6.3% in 2022 from 35.5% in 2021. |

| • | Our Restaurant-Level Adjusted EBITDA decreased to $33.6 million in 2022 from $34.1 million in 2021. Our Restaurant-Level Adjusted EBITDA Margin decreased to 20.5% from 24.2%. |

| • | Our Adjusted EBITDA decreased to $21.4 million from $25.0 million. Our Adjusted EBITDA Margin decreased to 13.1% from 17.8%. |

For reconciliations of net income to Adjusted EBITDA and to Restaurant-Level Adjusted EBITDA see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures.”

Our Response to the COVID-19 Pandemic and How We Emerged as a Stronger Company

During the COVID-19 pandemic, we temporarily closed all of our existing restaurants in March 2020. Faced with mandatory restaurant closures, imposed capacity limitations and other pandemic-related challenges, our foundational roots of persistence and resilience served us well. In response to the pandemic, we took various steps to reduce non-essential spend and postpone restaurant development.

Since the height of the COVID-19 pandemic, we believe the loosening of government restrictions, vaccine roll-outs and consumers yearning for pre-pandemic lifestyles have driven our successful recovery. By the end of 2021 we had reopened all of our 28 restaurants for dinner and a majority of them for lunch, and as of the end of the first quarter of 2022 all of our restaurants had returned to pre-pandemic operations.

Between April and June 2020 and during 2021, we received aggregate proceeds of $23.0 million from loans under the Paycheck Protection Program of the Coronavirus Aid, Relief, and Economic Security Act, or the CARES Act, which we used to retain current employees, maintain payroll and make lease and utility payments. To date, we have received formal notices of loan forgiveness in the amount of approximately $22.7 million related to these loans, of which $22.3 million was reflected in income in 2021 and $0.4 million was reflected in income in the first quarter of 2022. In addition, the Company has received approximately $16.8 million from the Restaurant Revitalization Fund, or RRF, under The American Rescue Plan Act of 2021 and has received $4.7 million from the Employee retention credits. For further information, see “Risk Factors—Our Paycheck Protection Program loan and our applications for such loan could in the future be determined to have been impermissible or could result in damage to our reputation.” While these loans and grants were important factors for our cash flow and operations for the last two years, given the closures and restrictions in connection with the COVID-19 pandemic, we do not believe that our results of operations going forward will be impacted by the lack of further loans or grants. Because these loans and grant enabled us to retain most of our employees, we were able to quickly resume our operations once restrictions were lifted.

For further information regarding our operations during the COVID-19 pandemic, see “Management’s Discussion and Analysis of Financial Results and Operations—Business Trends; Effects of COVID-19 on Our Business.”

Our Growth Strategies

Open Additional Restaurants in New and Existing Markets. Since opening our original restaurant in Tustin, California, we have successfully opened profitable new restaurants throughout Southern and Northern California, and in Nevada, Texas, Hawaii, Arizona and New York. We intend to leverage our expertise opening new

5

Table of Contents

restaurants to expand further into new geographies with the same rigorous and thoughtful new site and restaurant build-out process that we have successfully demonstrated in the past. Prior to the pandemic, we opened four new restaurants in both 2018 and 2019. Due to the COVID-19 pandemic, we opened no new restaurants in 2020 and 2021. With COVID-19 restrictions eased, we have restarted our pipeline of new restaurants and during 2022 we opened three new restaurants in Webster, Texas, Las Vegas, Nevada and New York, New York. We have also signed leases for nine other locations. These locations are in Kapolei, Hawaii, Fort Lauderdale, Florida, Chandler, Arizona, Westheimer, Texas, Seattle, Washington, Jacksonville, Florida, Dallas, Texas, Maui, Hawaii and Cerritos, California (at which we opened a new restaurant on April 4, 2023). We currently expect to open six or seven additional locations during the rest of 2023. We currently plan to open eight to ten new restaurants annually in new and existing domestic markets. We expect to open restaurants in new markets in states such as Oregon, Georgia, Virginia, Utah and also in the District of Columbia. Based on an internal study we conducted, we believe that we have long-term total restaurant potential for over 250 restaurants in the United States. Our restaurants have historically generated average Payback Periods of approximately 1.4 years with average Net Build-Out Costs of approximately $1.8 million for eight new units opened during 2018 and 2019. During 2022, we opened three restaurants with average Net Build-Out Costs of approximately $1.9 million. The last of the three restaurants opened in 2022 had Net Build-Out Costs of $2.6 million. Going forward, we are targeting average Net Build-Out Costs of $3.0 million with AUVs of approximately $5.0 million for our new restaurant units, resulting in a target Payback Period of approximately 2.5 years, which may vary depending on the specific market. The combination of our strong expertise in constructing new restaurants and tremendous whitespace opportunity positions us well to expand our concept into new markets.

Increase Restaurant Sales and Profitability. We initiated modest price increases in the second half of 2021 and in 2022 with no discernable change in guest behavior. We plan to continue to analyze and monitor price receptivity from our customers, and we believe there may be additional opportunities to implement modest price increases in the future with no material impact on customer traffic. Additionally, our strong supply chain capabilities and ability to operate with a limited number of employees have allowed us to control our costs. We continually look to invest in new technologies through rigorous testing and analyses to further improve and maintain an optimal cost structure, as well as to enhance our dining experience.

Selectively Pursue Wholesale Opportunities. With the favorable pricing terms we have established with our suppliers and distributors, during the pandemic we were able to continue providing a limited number of guests with our high-quality meats by introducing temporary bulk purchase options in 21 of our restaurants. Considering the positive response from our guests, we plan to selectively pursue wholesale opportunities going forward. We have engaged in early stage discussions with several national food retailers to offer our ready-to-serve meats. The COVID-19 pandemic served as an opportunity to not only assess the viability of a wholesale segment, but also to begin exploring other new service offerings we may be able into introduce to our existing business.

Corporate Information

GEN Inc. was incorporated in Delaware on October 28, 2021 as a Delaware corporation. It had no business operations prior to this offering. In connection with the consummation of this offering, GEN Inc. will become the managing member of GEN LLC, pursuant to the Reorganization described under “Organizational Structure—The Reorganization.” Our principal executive offices are located at 11480 South Street Suite 205, Cerritos, CA 90703 and our telephone number is (562) 356-9929. Our website address is www.genkoreanbbq.com. Information contained on our website or linked therein or otherwise connected thereto does not constitute part of and is not incorporated by reference into this prospectus or the registration statement of which this prospectus forms a part. We have included our website address in this prospectus solely as an inactive textual reference.

6

Table of Contents

Summary of Risks Affecting Our Business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section entitled “Risk Factors” immediately following this prospectus summary. These risks include, but are not limited to, the following:

| • | We have experienced and continue to experience inflationary conditions with respect to the cost for food, ingredients, labor, construction and utilities, and we may not be able to increase prices or implement operational improvements sufficient to fully offset inflationary pressures on such costs, which may adversely impact our revenues and results of operations. |

| • | The COVID-19 pandemic has adversely affected, and may continue to adversely affect, our operations, financial condition and financial results. |

| • | Our long-term success is highly dependent on our ability to successfully identify and secure appropriate sites and timely develop and expand our operations in existing and new markets. |

| • | Our expansion into new markets may present increased risks due in part to our unfamiliarity with the areas and also due to consumer unfamiliarity with our concept and may make our future results unpredictable. |

| • | The impact global and domestic economic conditions have on consumer discretionary spending could materially adversely affect our financial performance. |

| • | Opening new restaurants in existing markets may negatively affect sales at our existing restaurants. |

| • | New restaurants, once opened, may not be profitable, and the increases in average restaurant sales and comparable restaurant sales that we have experienced in the past may not be indicative of future results. |

| • | Our sales and profit growth could be adversely affected if comparable restaurant sales are less than we expect. |

| • | Our failure to manage our growth effectively could harm our business and operating results. |

| • | Our limited number of restaurants, the significant expense associated with opening new restaurants and the unit volumes of our new restaurants makes us susceptible to significant fluctuations in our results of operations. |

| • | Our restaurant base is geographically concentrated, and we could be negatively affected by conditions specific to our markets. |

| • | Our plans to open new restaurants, and the ongoing need for capital expenditures at our existing restaurants, require us to spend capital. |

| • | We rely significantly on certain vendors and suppliers, which could adversely affect our business, financial condition or results of operations. |

| • | Changes in food and supply costs could adversely affect our business, financial condition or results of operations. |

| • | Failure to receive frequent deliveries of fresh food ingredients and other supplies could harm our business, financial condition or results of operations. |

| • | We face intense competition, and if we are unable to continue to compete effectively in the restaurant industry in general and, in particular, within the dining segments of the restaurant industry in which we compete, our business, financial condition and results of operations would be adversely affected. |

| • | Food safety and foodborne illness concerns as well as outbreaks of flu, viruses or other diseases could have an adverse effect on our business, financial condition or results of operations. |

7

Table of Contents

| • | New information or attitudes regarding diet and health could result in changes in regulations and consumer consumption habits that could adversely affect our business, financial condition or results of operations. |

| • | We rely significantly on the operation of our equipment, and any mechanical failure could prevent us from effectively operating our restaurants. |

| • | The loss of any registered trademark or other intellectual property or our failure to maximize or successfully assert our intellectual property rights could enable other companies to compete more effectively with us. |

| • | Negative publicity relating to one of our restaurants could reduce sales at some or all of our other restaurants. |

| • | We are subject to all of the risks associated with leasing space subject to long-term non-cancelable leases. |

| • | Our Paycheck Protection Program loan and our applications for such loans could in the future be determined to have been impermissible or could result in damage to our reputation. |

| • | If we face labor shortages, increased labor costs or unionization activities, our growth, business, financial condition and operating results could be adversely affected. |

| • | Failure to obtain and maintain required licenses and permits or to comply with alcoholic beverage or food control regulations could lead to the loss of our liquor and food service licenses and, thereby, harm our business, financial condition or results of operations. |

| • | Governmental regulation may adversely affect our ability to open new restaurants or otherwise adversely affect our business, financial condition or results of operations. |

| • | We could be party to litigation that could adversely affect us by distracting management, increasing our expenses or subjecting us to material monetary damages and other remedies. |

| • | Our current insurance may not provide adequate levels of coverage against claims. |

| • | Changes to accounting rules or regulations may adversely affect our business, financial condition or results of operations. |

| • | The Internal Revenue Service, or the IRS, might challenge the tax basis step-ups and other tax benefits we receive in connection with this offering and the related transactions and in connection with future acquisitions of GEN LLC units. |

| • | GEN Inc. will be required to pay over to members of GEN LLC (other than GEN Inc.) most of the tax benefits GEN Inc. receives from tax basis step-ups (and certain other tax benefits) attributable to its acquisition of units of GEN LLC in the future, and the amount of those payments are expected to be substantial. |

| • | In certain circumstances, GEN LLC will be required to make distributions to us and the other members of GEN LLC, and the distributions that GEN LLC will be required to make may be substantial. |

| • | Future changes to tax laws or our effective tax rate could materially and adversely affect our company and reduce net returns to our stockholders. |

| • | Our charter documents and the Delaware General Corporation Law, or the DGCL, could discourage takeover attempts and other corporate governance changes. |

| • | Our amended and restated certificate of incorporation will include an exclusive forum clause, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us. |

| • | We have no history operating as a consolidated entity. |

8

Table of Contents

| • | The requirements of being a public company may strain our resources, divert our management’s attention and affect our ability to attract and retain qualified board members. |

| • | Failure to retain our senior management may adversely affect our operations. |

| • | We have identified two material weaknesses in our internal control over financial reporting, which could impact our ability to produce timely, accurate and reliable financial statements could be impaired. |

You should carefully consider all of the information set forth in this prospectus and, in particular, the information in the section entitled “Risk Factors” beginning on page 18 of this prospectus prior to making an investment in our common stock. These risks could, among other things, prevent us from successfully executing our strategies and could have a material adverse effect on our business, financial condition and results of operations.

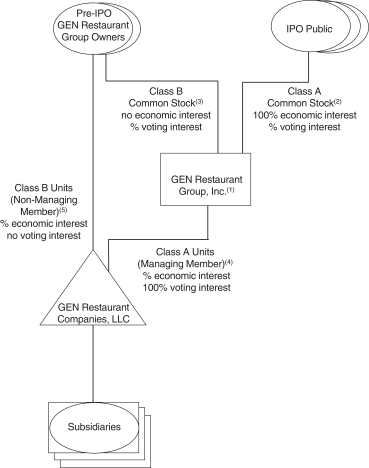

Organizational Structure

In connection with this offering, we will undertake certain transactions as part of the Reorganization, described under “Organizational Structure” below. The Reorganization will be conducted through what is commonly referred to as an “UP-C” structure, which is often used by partnerships and limited liability companies undertaking an initial public offering. The UP-C approach provides the current owners of GEN Restaurant Group with the tax advantage of owning interests in a pass-through structure and provides current and potential future tax benefits for the public company and economic benefits for the existing members of GEN LLC when they ultimately exchange their pass-through interests and corresponding shares of Class B common stock for shares of Class A common stock. Following the Reorganization and this offering, GEN Inc. will be a holding company and its sole asset will be ownership of Class A units of GEN LLC, of which it will be the managing member. The members of GEN LLC holding common units received in exchange for the ownership interests of the entities comprising GEN Restaurant Group prior to this offering will hold Class B units of GEN LLC and will also own an equal number of shares of Class B common stock of GEN Inc. upon completion of this offering.

Prior to the Reorganization, certain companies within GEN Restaurant Group, as separate private entities, have made, and will continue to make, distributions to their members which will impact our cash position upon completion of this offering. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

GEN Inc. will enter into a tax receivable agreement for the benefit of the members of GEN LLC or their permitted assignees (not including GEN Inc.), or the Tax Receivable Agreement, pursuant to which GEN Inc. will pay 85% of the amount of the net cash tax savings, if any, that GEN Inc. realizes (or, under certain circumstances, is deemed to realize) as a result of (i) increases in tax basis (and utilization of certain other tax benefits) resulting from GEN Inc.’s acquisition of a member’s GEN LLC units in future exchanges and (ii) any payments GEN Inc. makes under the Tax Receivable Agreement (including tax benefits related to imputed interest). Payments made pursuant to the Tax Receivable Agreement are expected to be substantial. Generally, payments under the Tax Receivable Agreement will be made to certain members of GEN LLC (not including GEN Inc.) pursuant to the terms of the Tax Receivable Agreement. Such payments will reduce the amount of cash resulting from the tax savings previously described, that would have otherwise been available to GEN LLC for other uses, including reinvestment or dividends to GEN Inc. Class A stockholders. See “Organizational Structure” and “Certain Relationships and Related Person Transactions—Tax Receivable Agreement.”

The amount payable under the Tax Receivable Agreement will be based on an annual calculation of the reduction in our U.S. federal, state and local taxes resulting from the utilization of certain tax benefits resulting

9

Table of Contents

from sales and exchanges by certain continuing members of GEN LLC of their GEN LLC units. See “Certain Relationships and Related Person Transactions—Tax Receivable Agreement.” Assuming no material changes in the relevant tax law and that we earn sufficient taxable income to realize all tax benefits that are subject to the Tax Receivable Agreement, we expect that the reduction in tax payments for us associated with the federal, state and local tax benefits described above would aggregate to approximately $ million through 2037. Under such scenario we would be required to pay certain continuing members of GEN LLC 85% of such amount, or $ million through 2037.

The diagram below illustrates our structure and anticipated ownership immediately after the Reorganization and this offering (assuming no exercise of the underwriters’ option to purchase additional shares) and does not reflect the issuances of awards pursuant to our 2023 Equity Incentive Plan, or the 2023 Plan.

Amounts may not sum to total due to rounding.

| (1) | At the closing of this offering, the members of GEN LLC other than GEN Inc. will be certain historic owners of GEN Restaurant Group, all of whom, in the aggregate, will own Class B units of GEN LLC and shares of Class B common stock of GEN Inc. after this offering assuming no exercise of the underwriters’ option to purchase additional shares and Class B units of GEN LLC and shares of Class B common stock of GEN Inc. if the underwriters exercise their option to purchase additional shares in full. |

10

Table of Contents

| (2) | Each share of Class A common stock will be entitled to one vote and will vote together with the Class B common stock as a single class, except as provided in our amended and restated certificate of incorporation or required by law. See “Organizational Structure—Voting Rights of Class A Common Stock and Class B Common Stock.” |

| (3) | Each share of Class B common stock is entitled to ten votes and will vote together with the Class A common stock as a single class, except as provided in our amended and restated certificate of incorporation or required by law. The Class B common stock will not have any economic rights in GEN Inc. |

| (4) | GEN Inc. will own all of the Class A units of GEN LLC after the Reorganization, which upon the completion of this offering will represent the right to receive approximately % of the distributions made by GEN LLC assuming no exercise of the underwriters’ option to purchase additional shares and approximately % of the distributions made by GEN LLC if the underwriters exercise their option to purchase additional shares in full. While this interest represents a minority of economic interests in GEN LLC, it represents 100% of the voting interests, and GEN Inc. will act as the managing member of GEN LLC. As a result, GEN Inc. will operate and control all of GEN LLC’s business and affairs and will be able to consolidate its financial results into GEN Inc.’s financial statements. |

| (5) | The historic owners of the GEN Restaurant Group will collectively hold all Class B common stock of GEN Inc. outstanding after this offering. They also will collectively hold all Class B units of GEN LLC, which upon the completion of this offering will represent the right to receive approximately % of the distributions made by GEN LLC assuming no exercise of the underwriters’ option to purchase additional shares and approximately % of the distributions made by GEN LLC if the underwriters exercise their option to purchase additional shares in full. The historic owners of the GEN Restaurant Group will have no voting rights in GEN LLC on account of the Class B units, except for the right to approve amendments to the GEN LLC Agreement that adversely affect their rights as holders of Class B units. However, through their ownership of shares of Class B common stock, the historic owners of the GEN Restaurant Group will control a majority of the voting power of the common stock of GEN Inc., the managing member of GEN LLC, and will therefore have indirect control over GEN LLC. Class B units may be exchanged for shares of our Class A common stock or, at our election, for cash, subject to certain restrictions pursuant to the GEN LLC Agreement described in “Organizational Structure—GEN LLC Agreement.” When a Class B stockholder exchanges Class B units for the corresponding number of shares of our Class A common stock or, at our election, for cash, it will result in the automatic retirement of the corresponding number of shares of our Class B common stock and, therefore, will decrease the aggregate voting power of our historic owners of the GEN Restaurant Group. Any beneficial holder exchanging Class B units must ensure that the applicable corresponding number of shares of Class B common stock are delivered to us for retirement as a condition of exercising its right to exchange Class B units for shares of our Class A common stock or, at our election, for cash. |

Implications of Being an Emerging Growth Company and Smaller Reporting Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an emerging growth company, or EGC, as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. For so long as we remain an EGC, we are permitted and have elected to rely on exemptions from specified disclosure requirements that are applicable to other public companies that are not EGCs. These exemptions include:

| • | being permitted to provide only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

| • | not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting; |

11

Table of Contents

| • | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit, the financial statements and Critical Audit Matters; |

| • | reduced disclosure obligations regarding executive compensation; and |

| • | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and on the frequency of such votes as well as stockholder approval of any golden parachute payments not previously approved. |

We may take advantage of these provisions for up to five years or such earlier time when we are no longer an EGC. We will cease to be an EGC if we have more than $1.07 billion in annual revenue, have more than $700 million in market value of our capital stock held by non-affiliates or issue more than $1 billion of non-convertible debt over a three-year period. We may choose to take advantage of some, but not all, of the available exemptions. We have taken advantage of some reduced reporting burdens in this prospectus. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you may hold stock.

The JOBS Act provides that an EGC may take advantage of an extended transition period for complying with new or revised accounting standards. This provision allows an EGC to delay the adoption of accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of this extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption is required for private companies.

We are also a “smaller reporting company” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, or the Exchange Act. We may continue to be a smaller reporting company even after we are no longer an emerging growth company. We may take advantage of certain of the scaled disclosures available to smaller reporting companies and will be able to take advantage of these scaled disclosures for so long as our voting and non-voting common stock held by non-affiliates is less than $250 million measured on the last business day of our second fiscal quarter, or our annual revenue is less than $100.0 million during the most recently completed fiscal year and our voting and non-voting common stock held by non-affiliates is less than $700.0 million measured on the last business day of our second fiscal quarter.

Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock, and our financial statements may not be comparable to the financial statements of issuers who are required to comply with the effective dates for new or revised accounting standards that are applicable to public companies. See “Risk Factors—Risks Related to Our Common Stock and This Offering—We are an “emerging growth company” and a “smaller reporting company” and as a result of the reduced disclosure requirements applicable to emerging growth companies and smaller reporting companies, our common stock may be less attractive to investors.”

12

Table of Contents

THE OFFERING

| Issuer |

GEN Restaurant Group, Inc. | |

| Class A common stock offered by us |

shares | |

| Underwriters’ option to purchase additional shares of Class A common stock from us |

shares | |

| Class A common stock outstanding immediately after this offering |

shares of Class A common stock (or shares of Class A common stock if the underwriters exercise their option to purchase additional shares of Class A common stock in full). | |

| Class B common stock outstanding immediately after this offering |

shares of Class B common stock. Class B common stock will be issued to holders of Class B units in GEN LLC. One share of Class B common stock will be issued for each Class B unit of GEN LLC outstanding. | |

| Use of proceeds |

We estimate that our net proceeds from this offering, based on an assumed initial public offering price of $ per share of Class A common stock (the midpoint of the price range set forth on the cover of this prospectus), after deducting estimated underwriting discounts and commissions but before deducting expenses of this offering and the Reorganization payable by us, will be approximately $ million, or approximately $ million if the underwriters exercise in full their option to purchase additional shares of Class A common stock.

We intend to use $ million of the net proceeds from this offering to purchase newly issued Class A units of GEN LLC, at a per-unit price equal to the per-share price paid by the underwriters for shares of our Class A common stock in this offering.

We intend to cause GEN LLC to use the remaining net proceeds to pay the expenses incurred by us in connection with this offering and the Reorganization, and for working capital and other general corporate purposes, including new unit openings. See “Use of Proceeds” for a more complete description of the intended use of proceeds from this offering. | |

| Representative’s Warrants |

Upon the closing of this offering, we will issue to Roth Capital Partners, LLC, as representative of the several underwriters, warrants, or the Representative’s Warrants, entitling it to purchase a number of shares of common stock equal to % of the shares of common stock sold in this offering by us at an exercise price equal to 100% of the public offering price of the common stock in this offering. The Representative’s Warrants will expire five years after the effective date of the registration | |

13

Table of Contents

| statement of which this prospectus forms a part. See “Underwriting.” | ||

| Dividend policy |

We have no present intention to pay cash dividends on our common stock. Any determination to pay dividends to holders of our common stock will be at the discretion of our board of directors and will depend upon many factors, including our financial condition, results of operations, projections, liquidity, earnings, legal requirements, restrictions in our existing and any future debt agreements and other factors that our board of directors deems relevant. Holders of our Class B common stock will not be entitled to dividends from GEN Inc.

Following the Reorganization and this offering, GEN Inc. will be a holding company and its sole asset will be ownership of the Class A units of GEN LLC, of which it will be the managing member. Subject to funds being legally available for distribution, we intend to cause GEN LLC to make distributions to each of its members, including GEN Inc., in an amount intended to enable each member to pay applicable taxes on taxable income allocable to each member and to allow GEN Inc. to make payments under the Tax Receivable Agreement. If the amount of tax distributions to be made exceeds the amount of funds available for distribution, GEN Inc. shall receive a tax distribution calculated using the corporate rate before the other members receive any distribution and the balance, if any, of funds available for distribution shall be distributed to the other members in accordance with the GEN LLC Agreement. See “Dividend Policy.” | |

| Voting rights |

We have two classes of authorized common stock: Class A common stock and Class B common stock. Each share of Class A common stock will entitle the holder to one vote, while each share of Class B common stock will entitle the holder to ten votes.

Holders of our Class A common stock and Class B common stock will vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise provided in our amended and restated certificate of incorporation or as required by applicable law. See “Description of Capital Stock.” When a Class B stockholder exchanges Class B units for the corresponding number of shares of our Class A common stock or, at our election, for cash, it will result in the automatic retirement of the corresponding number of shares of our Class B common stock and, therefore, will decrease the aggregate voting power of our Class B stockholders. Immediately following the completion of this offering, the outstanding shares of our Class B common stock will represent approximately % of the voting power of our outstanding stock (or % if the underwriters exercise their option to purchase additional shares). The holders of our Class B common stock, all of whom were members of GEN LLC prior to this offering, including our co-founders, will | |

14

Table of Contents

| have the ability to control the outcome of matters submitted to our stockholders for approval, including the election of directors. See “Organizational Structure—Voting Rights of Class A Common Stock and Class B Common Stock.” | ||

| Exchange of Class B units |

We have reserved for issuance shares of our Class A common stock, which is the aggregate number of shares of our Class A common stock expected to be issued over time upon the exchanges by the Class B unitholders. See “Organizational Structure.” | |

| GEN LLC Agreement |

The GEN LLC Agreement will entitle certain of its members (and certain permitted transferees thereof) to exchange their Class B units, together with an equal number of shares of Class B common stock, for shares of Class A common stock on a one-for-one basis or, at our election, for cash. When a Class B unit is exchanged for a share of our Class A common stock, the corresponding share of our Class B common stock will automatically be retired. See “Organizational Structure—GEN LLC Agreement” and “Certain Relationships and Related Person Transactions—GEN LLC Agreement.” | |

| Tax Receivable Agreement |

GEN Inc. will enter into the Tax Receivable Agreement for the benefit of the members of GEN LLC or their permitted assignees (not including GEN Inc.) pursuant to which GEN Inc. will pay 85% of the amount of the net cash tax savings, if any, that GEN Inc. realizes (or, under certain circumstances, is deemed to realize) as a result of (i) increases in tax basis (and utilization of certain other tax benefits) resulting from GEN Inc.’s acquisition of a member’s GEN LLC units in future exchanges and (ii) any payments GEN Inc. makes under the Tax Receivable Agreement (including tax benefits related to imputed interest). Payments made pursuant to the Tax Receivable Agreement are expected to be substantial. See “Organizational Structure” and “Certain Relationships and Related Person Transactions—Tax Receivable Agreement.” | |

| Risk factors |

You should carefully read and consider the information set forth in the section entitled “Risk Factors” beginning on page 18, together with all of the other information set forth in this prospectus, before deciding whether to invest in our Class A common stock. | |

| Symbol |

“GENK” | |

Unless otherwise noted, Class A common stock outstanding after the offering and other information based thereon in this prospectus does not reflect any of the following:

| • | shares of Class A common stock issuable upon exercise of the underwriters’ option to purchase additional shares; |

| • | shares of Class A common stock issuable upon the exercise of the Representative’s Warrants; |

15

Table of Contents

| • | shares of Class A common stock issuable under the 2023 Plan (under which no equity awards have been granted as of ), including: |

(i) shares of Class A common stock underlying restricted stock units or other awards to be granted to certain employees and non-employee directors pursuant to the 2023 Plan immediately after the closing of this offering; and

(ii) additional shares of Class A common stock to be reserved for future issuance of awards under the 2023 Plan; and

| • | shares of Class A common stock reserved for issuance upon exchange of the Class B units of GEN LLC (and corresponding shares of Class B common stock) that will be outstanding immediately after this offering. |

Unless otherwise indicated in this prospectus, all information in this prospectus assumes the completion of the Reorganization and that shares of our Class A common stock will be sold in this offering at $ per share (the midpoint of the price range set forth on the cover page of this prospectus).

Throughout this prospectus, we present performance metrics and financial information regarding the business of GEN Restaurant Group. This information is generally presented on an enterprise-wide basis. The new public stockholders will be entitled to receive a pro rata portion of the economics of GEN LLC’s operations through their ownership of our Class A common stock. GEN Inc.’s ownership of Class A units initially will represent a minority share of GEN LLC. The existing owners of GEN Restaurant Group initially will continue to hold a majority of the economic interest in GEN LLC’s operations as non-controlling interest holders, primarily through direct and indirect ownership of Class B units of GEN LLC. Prospective investors should be aware that the owners of the Class A common stock initially will be entitled only to a minority economic position, and therefore should evaluate performance metrics and financial information in this prospectus accordingly. As Class B units are exchanged for Class A common stock (or cash) over time, the percentage of the economic interest in GEN LLC’s operations to which GEN Inc. and the public stockholders are entitled will increase proportionately.

16

Table of Contents

SUMMARY HISTORICAL FINANCIAL INFORMATION

The following table sets forth certain summary financial information and other data of GEN Restaurant Group on a historical basis. GEN Restaurant Group is considered our predecessor for accounting purposes and its financial statements will be our historical financial statements following this offering. The following summary historical statements of operations data for the years ended December 31, 2022 and 2021 and the summary historical balance sheet data as of December 31, 2022 and 2021 have been derived from GEN Restaurant Group’s audited financial statements included elsewhere in this prospectus. We have derived the statements of operations data for the three months ended March 31, 2023 and March 31, 2022 and the balance sheet data as of March 31, 2023 from our unaudited interim financial statements included elsewhere in this prospectus. This summary historical financial information should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus. Our historical results and growth rates are not necessarily indicative of the results or growth rates to be expected in future periods.

| Three months ended March 31, | Year ended December 31, | |||||||||||||||

| (in thousands) | 2023 | 2022 | 2022 | 2021 | ||||||||||||

| (unaudited) | (restated) | |||||||||||||||

| Revenue |

$ | 43,862 | $ | 38,252 | $ | 163,729 | $ | 140,561 | ||||||||

| Restaurant operating expenses: |

||||||||||||||||

| Food cost |

14,305 | 12,899 | 54,357 | 44,688 | ||||||||||||

| Payroll and benefits |

13,652 | 11,299 | 48,866 | 40,710 | ||||||||||||

| Occupancy expenses |

3,432 | 2,702 | 12,110 | 10,151 | ||||||||||||

| Operating expenses |

4,126 | 3,284 | 15,019 | 12,533 | ||||||||||||

| Depreciation and amortization |

1,113 | 1,055 | 4,314 | 4,337 | ||||||||||||

| Pre-opening Costs |

519 | 158 | 1,455 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total restaurant operating expenses |

37,147 | 31,397 | 136,121 | 112,419 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| General and administrative |

2,055 | 1,764 | 7,988 | 4,882 | ||||||||||||

| Consulting fees - related party |

880 | 2,077 | 4,897 | 4,269 | ||||||||||||

| Management fees |

588 | 535 | 2,332 | 2,280 | ||||||||||||

| Depreciation and amortization - corporate |

18 | 7 | 39 | 26 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and expenses |

40,688 | 35,780 | 151,377 | 123,876 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from operations |

3,174 | 2,472 | 12,352 | 16,685 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gain on extinguishment of PPP debt |

— | 387 | 387 | 22,285 | ||||||||||||

| Restaurant revitalization fund grant |

— | — | — | 12,963 | ||||||||||||

| Employee retention credits |

1,165 | 45 | 3,532 | — | ||||||||||||

| Aborted deferred IPO costs written off |

— | — | (4,036 | ) | — | |||||||||||

| Other income (expenses) |

— | — | (835 | ) | 22 | |||||||||||

| Interest expense, net |

(189 | ) | (82 | ) | (634 | ) | (197 | ) | ||||||||

| Equity in income of equity method investee |

381 | 540 | 966 | 1,086 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

4,531 | 3,362 | 11,732 | 52,844 | ||||||||||||

| Less: Net Income attributable to noncontrolling interest |

397 | 373 | 1,451 | 2,985 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income attributable to GEN Restaurant Group |

$ | 4,134 | $ | 2,989 | $ | 10,281 | $ | 49,859 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Three months ended March 31, | Year ended December 31, | |||||||||||

| (amounts in thousands) | 2023 | 2022 | 2021 | |||||||||

| (unaudited) | (restated) | |||||||||||

| Combined Selected Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

9,775 | 11,195 | 9,890 | |||||||||

| Total assets |

139,474 | 138,878 | 53,836 | |||||||||

| Total liabilities |

143,263 | 144,139 | 41,643 | |||||||||

| Total permanent equity (deficit) |

(5,289 | ) | (6,761 | ) | 10,693 | |||||||

17

Table of Contents

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the following risks and uncertainties described below, together with all other information contained in this prospectus, including our consolidated financial statements and the related notes appearing at the end of this prospectus, before deciding to invest in our Class A common stock. The occurrence of any of the following risks, as well as any risks or uncertainties not currently known to us or that we currently do not believe to be material, could materially and adversely affect our business, prospects, financial condition, results of operations and cash flow, in which case, the trading price of our Class A common stock could decline and you could lose all or part of your investment.

Risks Related to Our Growth Strategy and Restaurant Expansion

We have experienced and continue to experience inflationary conditions with respect to the cost for food, ingredients, labor, construction and utilities, and we may not be able to increase prices or implement operational improvements sufficient to fully offset inflationary pressures on such costs, which may adversely impact our revenues and results of operations.

The strength of our revenues and results of operations are dependent upon, among other things, the price and availability of food, ingredients, labor, construction and utilities. In the year ended 2021 and the year ended 2022, the costs of commodities, labor, energy and other inputs necessary to operate our restaurants significantly increased. Fluctuations in economic conditions, weather, demand and other factors also affect the cost of the ingredients and products that we buy. From 2021 to 2022, the percentage of sales of food costs increased from 31.8% to 33.2% and the percentage of sales of payroll and benefits costs increased from 29.0% to 29.8%. Our inability to anticipate and respond effectively to one or more adverse changes in any of these factors could have a significant adverse effect on our results of operations. We expect the inflationary pressures and other fluctuations impacting the cost of these items to continue to impact our business in the year ended 2023. Our attempts to offset cost pressures, such as through menu price increases and operational improvements, may not be successful. We initiated modest price increases in the second half of 2021 and in 2022 with no discernible change in guest behavior. We seek to provide a moderately priced product, and, as a result, we may not seek to or be able to pass along price increases to our customers sufficient to completely offset cost increases. Traffic may also be negatively impacted with menu price increases as consumers may be less willing to pay our menu prices and may increasingly visit lower-priced competitors, may reduce the frequency of their visits, or may forgo some purchases altogether. To the extent that price increases are not sufficient to offset higher costs adequately or in a timely manner, and/or if they result in significant decreases in revenue volume, our revenues and results of operations may be adversely affected.

The COVID-19 pandemic has adversely affected, and may continue to adversely affect, our operations, financial condition and financial results.