UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number

(Exact name of Registrant as specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|||

|

☑ |

|

Smaller reporting company |

|

||

|

|

|

|

|

|

|

Emerging growth company |

|

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of common stock on June 30, 2023, was $

The number of shares of Registrant’s Common Stock outstanding as of March 28, 2024 was

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980)

Table of Contents

|

|

Page |

PART I |

|

|

Item 1. |

3 |

|

Item 1A. |

9 |

|

Item 1B. |

27 |

|

Item 1C. |

27 |

|

Item 2. |

28 |

|

Item 3. |

29 |

|

Item 4. |

29 |

|

|

|

|

PART II |

|

|

Item 5. |

30 |

|

Item 6. |

30 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

31 |

Item 7A. |

45 |

|

Item 8. |

46 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

85 |

Item 9A. |

85 |

|

Item 9B. |

86 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

86 |

|

|

|

PART III |

|

|

Item 10. |

87 |

|

Item 11. |

87 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

87 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

87 |

Item 14. |

87 |

|

|

|

|

PART IV |

|

|

Item 15. |

88 |

|

Item 16. |

88 |

i

PART I

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains and incorporates by reference estimates, projections, statements relating to our business plans, objectives, and expected operating results that are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements may appear throughout this report, including the following sections: “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These forward-looking statements generally are identified by the words “may,” “believe,” “anticipate,” “expect,” “plan,” “predict,” “estimate,” “will be,” or other similar words and phrases. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties that may cause actual results to differ materially. We describe risks and uncertainties that could cause actual results and events to differ materially in “Risk Factors” (Part I, Item 1A of this Form 10-K), “Management’s Discussion and Analysis of Financial Condition and Results of Operation” (Part II, Item 7), and “Quantitative and Qualitative Disclosures about Market Risk”) (Part II, Item 7A). We undertake no obligation to update or publicly revise any forward-looking statements, whether because of new information, future events, or otherwise, except to the extent required by applicable law.

Important factors that could cause actual results to differ materially from those contained in the forward‑looking statements include, but are not limited to:

1

2

Item 1. Business.

Unless the context otherwise requires, all references in this section to the “Company,” “DTIC,” “we,” “us,” or “our” refer to the business of Drilling Tools International Corporation and its consolidated subsidiaries following the consummation of the Merger (defined below), and to Drilling Tools International Holdings, Inc. and its consolidated subsidiaries prior to the consummation of the Merger.

Our Company

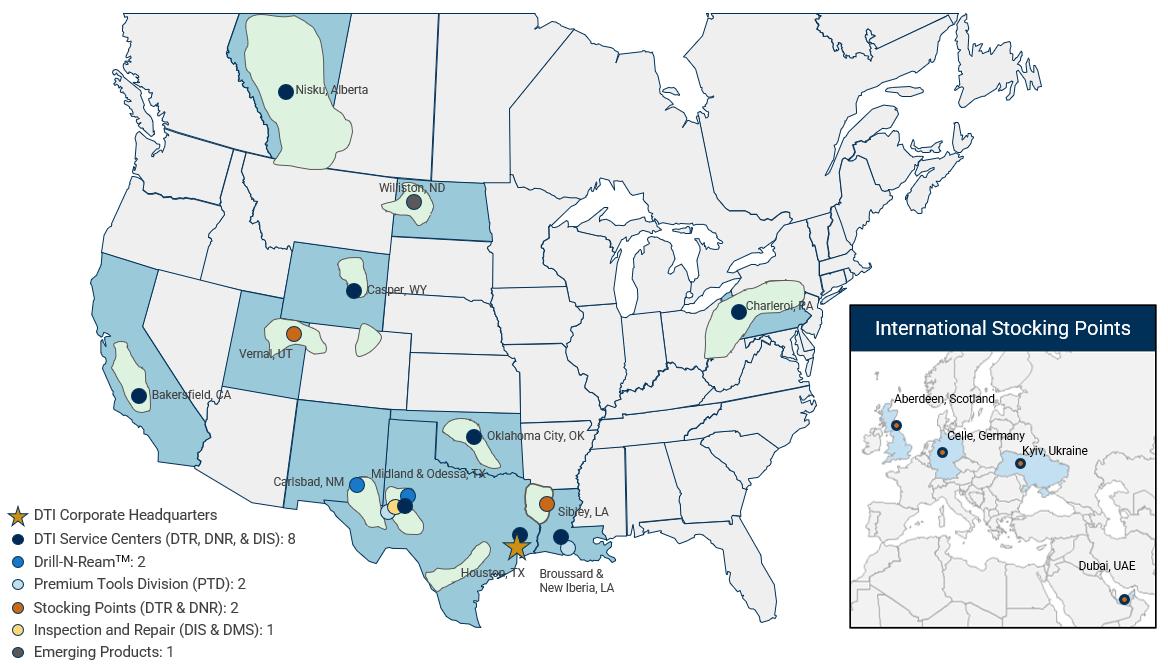

Drilling Tools International Corporation provides oilfield equipment and services to oil and natural gas sectors in North America, Europe, and the Middle East. We offer downhole tool rentals, machining, and inspection services to support the global drilling and wellbore construction industry. Our primary products are bottom hole assembly components such as stabilizers, subs, non-magnetic and steel drill collars, hole openers, roller reamers, as well as drill pipe and drill pipe accessories. In addition, we provide proprietary technology in our wellbore optimization business supplying the patented Drill-N-Ream (trademark) wellbore conditioning tool, and the patented RotoSteer (trademark), rotational steering tool for use in the extended reach horizontal drilling industry. We also offer a wide variety of ancillary equipment and handling tools to support our rental platform. Those tools include float valves, ring gauges, tool baskets, lift bail, lift subs, mud magnets, elevators, bracket and bail assemblies, slips, tongs, stabbing guides and safety clamps. We also offer a limited product line of blowout preventers and pressure control accessory equipment. We were founded in 1984 and we are headquartered in Houston, Texas. We operate from 16 locations in North America and maintain 4 international stocking points in Europe and the Middle East.

Drilling and producing oil and gas is a complex endeavor that requires tools of various shapes and sizes. Many of our customers rent these tools, as opposed to owning them, because of the many factors that affect which tools are needed for a specific task. Such factors include different formations, drilling methodologies, drilling engineer preferences, drilling depth and hole size. We believe that we are successful because we meet our customers’ wide demands by operating from multiple locations with over 65,000 tools in our fleet.

We are led by an accomplished management team that has significant experience in the oil and gas industry and has worked together for much of the last decade. Since 2012, we have grown the business and strengthened our standing in the industry. Specifically, we have:

Merger

On June 20, 2023 (the "Closing Date"), a merger transaction between Drilling Tools International Holdings, Inc. ("DTIH"), ROC Energy Acquisition Corp ("ROC"), and ROC Merger Sub, Inc., a directly, wholly owned subsidiary of ROC ("Merger Sub"), was completed (the "Merger”) pursuant to the initial merger agreement dated February 13, 2023 and subsequent amendment to the merger agreement dated June 5, 2023 collectively, (the "Merger Agreement"). In connection with the closing of the Merger, ROC changed its name to Drilling Tools International Corporation. The common stock of DTIC ("Common Stock" or the "DTIC Common Stock") commenced trading on the Nasdaq Stock Market LLC ("Nasdaq") under the symbol "DTI" on June 21, 2023. See Note 3 - Merger for further discussion of the Merger.

Operating Activities

3

Our operating activities are divided into four divisions:

Our Industry

The Role of Rental Tool Companies in the Production of Oil and Gas

Wellbore construction is a critical stage in the production of oil and gas. Wellbore construction is comprised of drilling the wellbore, logging the target producing formation to determine if commercial amounts of hydrocarbons exist, installing casing, cementing casing and performing completion procedures to prepare the well for production. Even after wellbore construction is complete, production products and services are needed over the well’s full life cycle.

Oil and gas companies typically hire a drilling contractor with an appropriate drilling rig to begin wellbore construction. However, drilling contractors generally do not have all the necessary tools to complete the project, and instead focus their business on the rig and its main components and rarely rent tools on behalf of oil and gas operators. Instead, oil and gas companies prefer to procure the products and services involved in drilling and subsequent procedures on a temporary basis from entities operating in the oil field services ("OFS") industry. This enables them to obtain the best quality, service, and pricing value directly from the service and equipment suppliers. As a result, upon completion of the well, the oil and gas operator does not hold assets that it no longer needs.

The tools provided by rental tool companies vary from select bottom hole assembly components, drill string tools, pressure control devices and a wide variety of specialty items. Rental tool companies purchase assets and rent them to their oil and gas operator customers, who in turn use these tools to complete their respective projects. Rental tool companies typically charge daily rental fees, but fees also can be structured as hourly, footage, weekly, or monthly charges. Rental tool companies also bill customers for repair charges if tools are damaged beyond normal wear and tear. In addition, if the tools are lost in the well, or damaged beyond repair, the customer is charged a replacement fee. Rental tool companies’ ability to charge such fees are particularly important in light of the acceleration of drilling rates, as such acceleration has led to an increase in the number of damaged or lost-in-hole tools. We believe

4

that this commercial arrangement has been standard practice in the industry for over 70 years. Given the cyclical nature of the oil and gas industry, commercial terms will be more favorable to rental tool companies when oil and gas industry activity is higher.

Oil and Gas Drilling Activity

Rental tool companies’ financial and operating results are tied to the level of oil and gas drilling activity in their respective regions of operation, which, in our case, are generally the United States and Canada. Historically, the level of activity was measured by the number of active drilling rigs. As of December 31, 2023, the weekly average U.S. and Canadian onshore rig count as reported by Baker Hughes was 667 and 176, respectively. These figures have increased by 249 rigs, or 59%, in the United States and by 88 rigs, or 100%, in Canada since the average weekly lows of 2020.

Despite a reduction in the rig count since the highs of 2012, a rig can now accomplish more than one could have in the past. Drilling rigs now operate faster and drill longer wells, resulting in more efficient production than ever before. Accordingly, we believe that well count and feet drilled are better indicators of the level of oil and gas drilling activity.

Our Strategy

We intend to (i) maximize the profitability of our core rental tool business, (ii) commercialize new high-value rental tools that make the drilling process more efficient (iii) extend our reach into other segments of a well’s lifecycle, such as completion and production and (iv) expand geographically. We intend to execute our strategy through the following:

5

Our Competitive Strengths

To implement the strategies discussed above, we plan to leverage the following competitive strengths:

6

Customers

Our customer base is comprised of: (i) diversified OSCs account for approximately 50% of 2023 revenue, including but not limited to Baker Hughes Company, Halliburton Company, Phoenix Energy, and SLB (formerly Schlumberger); (ii) E&P operators account for approximately 47% of 2023 revenue, included but not limited to ConocoPhillips, EOG Resources Inc., Occidental Petroleum Corporation, Pioneer Energy Services Corp.; and (iii) oil and gas equipment manufacturers account for approximately 3% of 2023 revenue, included but not limited to Liberty Lift Solutions and National Oilwell Varco.

7

Conducting business with top tier customers requires world class service quality, safety and auditable work processes. These operating requirements are contained in MSAs with our clients. Obtaining MSAs can be difficult and time-consuming. We believe this creates a barrier to entry for smaller, less competent providers and provides us an industry advantage.

Employees and Employee Safety

We have 394 employees and contractors, all of whom were full-time. Our workforce includes over 29 sales professionals who are divided between city-sales and field-sales teams. Keeping our workforce safe and healthy is a key priority, and management is committed to ensuring our employees return home safely after each shift. In 2018, we implemented “Safety Now,” a rigorous safety program that is part of DTI’s Safe, Inspired, Productive incentive program (“SIP”). SIP has helped reduce our total recordable incident rate from 2.3 in 2018 to 1.23 in 2023, which is lower than the industry average. The success of SIP is necessary for us to do business with many of our customers, including Baker Hughes Company, EOG Resources Inc., Occidental Petroleum Corporation and SLB.

Properties

We operate from 16 locations in North America and maintain 4 international stocking points in Europe and the Middle East, as shown below:

Government Regulation and Environmental, Health and Safety Measures

Our business is significantly affected by federal, state and local laws and other regulations. These regulations primarily impact the operation of our facilities. The laws and regulations relate to, among other things:

8

Our internal environmental group monitors our compliance with applicable laws and regulations. We also engage third parties to review our compliance with such.

We cannot predict the level of enforcement of existing laws and regulations or how such laws and regulations may be interpreted by enforcement agencies or court rulings in the future. We also cannot predict whether additional laws and regulations will be adopted, including changes in regulatory oversight, increase of federal, state or local taxes, increase of inspection costs, or the effect such changes may have on us, our business or our financial condition.

Competition

We believe that there are a limited number of competitors in the oil and gas drilling rental tools industry. It is our view that we enjoy a competitive advantage with respect to these competitors due to our large relevant tool inventory, strong management team and significant scale.

Corporate Information

Our operations date to the founding of Directional Rentals, Inc. in 1984. Its name was changed to “Drilling Tools International, Inc.” in 2014, and it is a wholly owned subsidiary of DTIH. As a result of the Business Combination, DTIH became a wholly owned subsidiary of ROC. In connection with the Business Combination, ROC changed its name to “Drilling Tools International Corporation”. Our website address is www.drillingtools.com. The information found on our website is not part of this or any other report we file with, or furnish to, the SEC and is expressly not incorporated by reference into this document. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements, and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available on our website, free of charge, as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. Alternatively, you may access these reports at the SEC’s website at www.sec.gov.

Item 1A. Risk Factors.

Risks Related to Our Business

Demand for our products and services depends on oil and gas industry activity and customer expenditure levels, which are directly affected by trends in the demand for, and price of, crude oil and natural gas as well as the availability of capital.

Demand for our products and services depends primarily upon the general level of activity in the oil and gas industry, including the number of drilling rigs in operation, the number of oil and gas wells being drilled, the depth and drilling conditions of these wells, the volume of production, the number of well completions and the cumulative feet drilled, the level of well remediation activity, and the corresponding capital spending by oil and gas companies. Oil and gas activity is in turn heavily influenced by, among other factors, current and anticipated oil and natural gas prices locally and worldwide. Historically, such prices have been volatile, and declines, whether actual or anticipated, thereof could negatively affect the level of oil and gas activity and related capital spending. Decreases in oil and gas activity and related capital spending could, in turn, adversely affect demand for our products and services and, in certain instances, result in the cancellation, modification or curtailing of demand for our services and the ability of our customers to pay us for our products and services. These factors could have an adverse effect on our business, results of operations, financial condition and cash flows.

Factors affecting the prices of oil and natural gas include, but are not limited to, the following:

9

The oil and gas industry is cyclical and has historically experienced periodic downturns. These downturns have been characterized by diminished demand for our products and services and downward pressure on the prices we charge. These downturns generally cause many E&P companies to reduce their capital budgets and drilling activity. Any future downturn or expected downturn could result in a significant decline in demand for OFS and adversely affect our business, results of operations and cash flows.

Customer expenditure levels could also drop if our customers face difficulty in accessing capital. If commodity prices drop, our customers may face liquidity constraints and the deterioration of their respective credit worthiness. Moreover, our customers may have limited viable financing alternatives in light of unfavorable lending and investment policies held by financial institutions associated with concerns about environmental impacts of the oil and gas industry or its products. Similarly, certain institutional investors have divested themselves of investments in this industry. If any of our customers experience any of these challenges, they may reduce spending, which could adversely affect our business, results of operations and cash flows.

Growth in U.S. drilling activity, and our ability to benefit from such growth, could be adversely affected by any significant constraints in equipment, labor or takeaway capacity in the regions in which we operate.

Growth in U.S. drilling activity may be impacted by, among other things, the availability and cost of drilling equipment, pipeline capacity, and material and labor shortages. Significant growth in drilling activity could strain availability of the equipment, materials and labor required to drill and complete a well, together with the ability to move the produced oil and natural gas to market. Should significant constraints develop that materially impact the efficiency and economics of oil and gas producers, growth in U.S. drilling activity could be adversely affected. This would have an adverse impact on the demand for the products we sell and rent, which could have a material adverse effect on our business, results of operations and cash flows.

We depend on a relatively small number of customers in a single industry. The loss of an important customer could adversely affect our business, results of operations and financial condition.

Our customers are primarily diversified OFS companies and E&P operators. Historically, we have been dependent on a relatively small number of customers for our revenues. During the years ended December 31, 2023 and 2022, 28.2% and 27.6%, respectively, of our total revenue was earned from our two largest customers. Our business, results of operations and financial condition could be materially adversely affected if an important customer ceases to engage us for our services on favorable terms, or at all, or fails to pay or delays paying us significant amounts of our outstanding receivables.

We have operated under a first call supply agreement with our largest customer since 2013. We and this customer have agreed to multiple extensions of this agreement, the most recent of which extends the agreement until February 28, 2025. However, if we are unable to successfully negotiate extensions in the future, then our ability to do business with this customer may be greatly reduced. Moreover, the supply agreements that we have entered into with our other customers are also of limited duration and require periodic extensions. Similarly, a failure to agree to such extensions may hinder our ability to do business with these customers.

10

Additionally, the E&P industry is characterized by frequent consolidation activity. Changes in ownership of our customers may result in the loss of, or reduction in, business from those customers. Moreover, customers may use their size and purchasing power to seek economies of scale and pricing concessions. Consolidation may also result in reduced capital spending by some of our customers, which may lead to a decreased demand for our services and equipment. We cannot assure you that we will be able to maintain our level of sales to a customer that has consolidated or replace that revenue with increased business activity with other customers. As a result, the acquisition of one or more of our primary customers may have a significant negative impact on our business, results of operations, financial condition or cash flows. We are unable to predict what effect consolidations in the industry may have on price, capital spending by our customers, our market share and selling strategies, our competitive position, our ability to retain customers or our ability to negotiate favorable agreements with our customers.

Termination of, or failure to comply with, the terms of our non-exclusive distribution agreement with SDPI could have a material adverse effect on our business.

In 2016, we entered into an exclusive distribution agreement with SDPI with respect to the Drill-N-Ream™. In 2017, SDPI determined that we did not meet defined market share goals, and as a result our distribution rights with respect to the Drill-N-Ream™ are no longer contractually exclusive. Accordingly, SDPI could choose to distribute the Drill-N-Ream™ through other companies who will then compete with us in this space. These risks could be exacerbated if SDPI were to enter into an exclusive distribution agreement with, or sell the intellectual property rights to the Drill-N-Ream™ to, one of our competitors, or if one of our competitors were to acquire SDPI. While we remain the Drill-N-Ream™’s sole North American distributor, we cannot guarantee that this will remain the case. Our inability to remain the sole North American distributor of the Drill-N-Ream™ could have a material adverse effect on our business, results of operations and cash flows.

We may be unable to employ a sufficient number of skilled and qualified workers to sustain or expand our current operations.

The delivery of our products and services requires personnel with specialized skills and experience. Our ability to be productive and profitable will depend upon our ability to attract and retain skilled workers. In addition, our ability to expand our operations depends in part on our ability to increase the size of our skilled labor force. The demand for skilled workers is high, and the cost to attract and retain qualified personnel has increased. During industry downturns, skilled workers may leave the industry, reducing the availability of qualified workers when conditions improve. In addition, a significant increase in the wages paid by competing employers both within and outside of our industry could result in increases in the wage rates that we must pay. Throughout 2021 and 2022, our expenses related to salaries and wages increased materially, especially those expenses related to certain key oil and gas producing regions, as we sought to meet increasing customer demand. During the year ended December 31, 2023, we experienced similar increases. If we are not able to employ and retain skilled workers, our ability to respond quickly to customer demands or strong market conditions may inhibit our growth, which could have a material adverse effect on our business, results of operations and cash flows.

Our business depends on the continuing services of certain of our key managers and employees.

We depend on key personnel. The loss of key personnel could adversely impact our business if we are unable to implement our strategy and successfully manage our business in their absence. The loss of qualified employees or an inability to retain and motivate additional highly-skilled employees required for the operation and expansion of our business could hinder our ability to successfully maintain and expand our market share.

Equity interests in us are a substantial portion of the net worth of our executive officers and several of our other senior managers. As a result, those executive officers and senior managers may have less incentive to remain employed by us if they were to sell their equity interests. After terminating their employment with us, some of them may become employed by our competitors.

We are an emerging growth company and smaller reporting company and as such are subject to various risks unique only to emerging growth companies and smaller reporting companies, including but not limited to, no requirement to provide an assessment of the effectiveness of internal controls over financial reporting.

We are an “emerging growth company” as defined in the Jumpstart Out Business Startups Act of 2012 ("JOBS Act"). We will remain an emerging growth company until the earlier of (i) December 31, 2026, the last day of the fiscal year following the fifth anniversary of the date of the ROC initial public offering; (ii) the last day of the fiscal year in which we have total annual gross revenues of $1.235 billion or more; (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under applicable Securities and Exchange Commission ("SEC") rules.

11

We expect that we will remain an emerging growth company for the foreseeable future but cannot retain our emerging growth company status indefinitely and will no longer qualify as an emerging growth company on or before December 31, 2026. References herein to “emerging growth company” have the meaning associated with it in the JOBS Act.

For so long as we remain an emerging growth company, we are permitted and intend to rely on exemptions from specified disclosure requirements that are applicable to other public companies that are not emerging growth companies. These exemptions include:

Additionally, as an emerging growth company and smaller reporting company our status as such carries various unique risks such as the risk that our financial statements may not be comparable to those of other public companies, and the risk that we will not be required to provide an assessment of the effectiveness of our internal controls over financial reporting until our second annual report following our initial public offering.

For as long as we continue to be an emerging growth company, we expect that we will take advantage of the reduced disclosure obligations available to us as a result of that classification. We have taken advantage of certain of those reduced reporting burdens in these financial statements. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock.

An emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to avail ourselves of this extended transition period and, as a result, we will not be required to adopt new or revised accounting standards on the dates on which adoption of such standards is required for other public reporting companies.

We are also a “smaller reporting company” as defined in Rule 12b-2 of the Exchange Act, and have elected to take advantage of certain of the scaled disclosure available for smaller reporting companies.

The lack of availability of the tools we purchase to rent to our customers and inflation may increase our cost of operations beyond what we can recover through price increases.

Our ability to source tools, such as drill collars, stabilizers, crossover subs, wellbore conditioning tools, drill pipe, hevi-wate drill pipe and tubing, at reasonable cost is critical to our ability to successfully compete. Due to a shortage of steel caused primarily by production disruptions during the COVID-19 pandemic and increased demand as economies rebounded, steel and assembled component prices have been and continue to be elevated. Our business and results of operations may be adversely affected by our inability to manage rising costs and the availability of the tools that we rent to our customers. Additionally, freight costs, specifically ocean freight costs, have risen significantly due to a number of factors including, but not limited to, a scarcity of shipping containers, congested seaports, a shortage of commercial drivers, capacity constraints on vessels or lockdowns in certain markets. We cannot assure you that we will be able to continue to purchase and move these tools on a timely basis or at commercially viable prices, nor can we be certain of the impact of changes to tariffs and future legislation that may impact trade with China or other countries. Should our current suppliers be unable to provide the necessary tools or otherwise fail to deliver such tools timely and in the quantities required, resulting delays in the provision of rentals to our customers could have a material adverse effect on our business, results of operations and cash flows.

The United States has recently experienced the highest inflation in decades primarily due to supply-chain issues, a shortage of labor and a build-up of demand for goods and services. The most noticeable adverse impact to our business has been increased freight, materials and vehicle-related costs as well as higher salaries and wages. To date, we do not believe that inflation has had a material impact on our financial condition or results of operations because we have been able to increase the prices we receive from our

12

customers. We cannot be sure how long elevated inflation rates will continue. We cannot be confident that all costs will return to the lower levels experienced in prior years even as the rate of inflation abates. Our business and results of operations may be adversely affected by these rising costs to the extent we are unable to recoup them from our customers.

Delays in obtaining, or inability to obtain or renew, permits or authorizations by our customers for their operations could impair our business.

Our customers are required to obtain permits or authorizations from one or more governmental agencies or other third parties to perform drilling and completion activities, including hydraulic fracturing. Such permits or approvals are typically required by state agencies but can also be required by federal and local governmental agencies or other third parties. The requirements for such permits or authorizations vary depending on the location where such drilling and completion activities will be conducted. As with most permitting and authorization processes, there is a degree of uncertainty as to whether a permit will be granted, the time it will take for a permit or approval to be issued and the conditions which may be imposed in connection with the granting of the permit. In some jurisdictions, certain regulatory authorities have delayed or suspended the issuance of permits or authorizations while the potential environmental impacts associated with issuing such permits can be studied and appropriate mitigation measures evaluated.

In Texas, rural water districts have begun to impose restrictions on water use and may require permits for water used in drilling and completion activities. In addition, in January 2021, President Biden indefinitely suspended new oil and natural gas leases on public lands or in offshore waters pending completion of a comprehensive review and reconsideration of federal oil and gas permitting and leasing practices. Although the moratorium was enjoined nationwide in June 2021, and again in August 2022 after the U.S. Court of Appeals for the Fifth Circuit vacated the June 2021 injunction, the Biden Administration may take further actions to limit new oil and natural gas leases.

In November 2021, the Department of the Interior completed its review and issued a report on the federal oil and gas leasing program. The Department of the Interior’s report recommends several changes to federal leasing practices, including changes to royalty payments, bidding and bonding requirements. The effects of this report or other initiatives to reform the federal leasing process could result in additional restrictions or limitations on the issuance of federal leases and permits for drilling on public lands. Permitting, authorization or renewal delays, the inability to obtain new permits or the revocation of current permits could impact our customers’ operations and cause a loss of revenue and potentially have a materially adverse effect on our business, results of operations and cash flows.

Competition within the oil and gas drilling tool rental industry may adversely affect our ability to market our services.

The oil and gas drilling tool rental tool industry is highly competitive and fragmented. The number of rental tool companies active in a given market may exceed the corresponding demand therefor, which could result in active price competition. Some oil and gas drilling companies prioritize rental prices when choosing to contract with a rental tool company, which may further increase competition based primarily on price. In addition, adverse market conditions lower demand for drilling equipment, which results in excess equipment and lower utilization rates. If market conditions in our operating areas deteriorate from current levels or if adverse market conditions persist, the prices we are able to charge and utilization rates may decline. Moreover, our customers may choose to purchase some or all of the tools that they typically rent from us, thereby reducing the volume of business that we conduct with such customers. Any significant future increase in overall market capacity for the rental equipment or services that we offer could adversely affect our business, results of operations and cash flows.

We may fail to fully execute, integrate, or realize the benefits expected from acquisitions, which may require significant management attention, disrupt our business and adversely affect our results of operations.

As part of our business strategy and to remain competitive, we continually evaluate acquiring or making investments in complementary companies, products or technologies. We may not be able to find suitable acquisition candidates or complete such acquisitions on favorable terms. We may incur significant expenses, divert employee and management time and attention from other business-related tasks and our organic strategy and incur other unanticipated complications while engaging with potential target companies where no transaction is eventually completed.

If we do complete acquisitions, we may not ultimately strengthen our competitive position or achieve our goals or expected growth, and any acquisitions we complete could be viewed negatively by our customers, or we could experience unexpected competition from market participants. Any integration process may require significant time and resources. We may not be able to manage the process successfully and may experience a decline in our profitability as we incur expenses prior to fully realizing the benefits of the acquisition. We could also expend significant cash and incur acquisition related costs and other unanticipated liabilities associated with the acquisition, the product or the technology, such as contractual obligations, potential security vulnerabilities of the acquired company and its products and services and potential intellectual property infringement. In addition, any acquired technology or

13

product may not comply with legal or regulatory requirements and may expose us to regulatory risk and require us to make additional investments to make them compliant.

We may not successfully evaluate or utilize the acquired technology or personnel, or accurately forecast the financial impact of an acquisition transaction, including accounting charges and tax liabilities. We could become subject to legal claims following an acquisition or fail to accurately forecast the potential impact of any claims. Any of these issues could have a material adverse impact on our business and results of operations.

New technology may cause us to become less competitive.

New technology that enhances the functionality, performance reliability and design of downhole drilling tools currently on the market may become prevalent in the OFS industry. We may face difficulty obtaining these new tools for the purpose of renting them to our customers. Although we believe our fleet of rental equipment currently gives us a competitive advantage, if competitors develop fleets that are more technically advanced than ours, we may lose market share or be placed at a competitive disadvantage. Further, we may face competitive pressure to acquire certain new tools at a substantial cost. Some of our competitors have greater financial, technical and personnel resources that may allow them to enjoy various competitive advantages in the acquisition of new tools. We cannot be certain that we will be able to continue to acquire new tools or convert our existing tools to meet new performance requirements. Such an inability may have a material adverse effect on our business, results of operations and cash flows, including a reduction in the value of assets, and the rates that may be charged for their rental.

We rent tools used in the drilling of oil and gas wells. This equipment may subject us to liability, including claims for personal injury, property damage and environmental contamination, or reputational harm if it fails to perform to specifications.

We rent tools used in oil and gas exploration, development and production. Some of these tools are designed to operate in high-temperature and/or high-pressure environments, and some tools are designed for use in hydraulic fracturing operations. Because of applications to which our tools are exposed, particularly those involving high pressure environments, a failure of such tools, or a failure of our customers to maintain or operate the tools properly, could cause damage to the tools, damage to the property of customers and others, personal injury and environmental contamination and could lead to a variety of claims against us or reputational harm that could have an adverse effect on our business, results of operations and cash flows.

We indemnify our customers against certain claims and liabilities resulting or arising from our provision of goods or services to them. In addition, we rely on customer indemnifications, generally, and third-party insurance as part of our risk mitigation strategy. However, our insurance may not be adequate to cover our liabilities. In addition, our customers may be unable to satisfy indemnification claims against them. Further, insurance companies may refuse to honor their policies, or insurance may not generally be available in the future, or if available, premiums may not be commercially justifiable. We could incur substantial liabilities and damages that are either not covered by insurance or that are in excess of policy limits, or incur liability at a time when we are not able to obtain liability insurance. Such potential liabilities could have a material adverse effect on our business, results of operations and cash flows.

Our operations, and those of our customers, are subject to hazards inherent in the oil and gas industry, which could expose us, and our customers, to substantial liability and cause us to lose substantial revenue.

Risks inherent in our industry include the risks of equipment defects, installation errors, the presence of multiple contractors at the wellsite over which we have no control, vehicle accidents, fires, explosions, blowouts, surface cratering, uncontrollable flows of gas or well fluids, pipe or pipeline failures, abnormally pressured formations and various environmental hazards such as oil spills and releases of, and exposure to, hazardous substances. For example, our operations are subject to risks associated with hydraulic fracturing, including any mishandling, surface spillage or potential underground migration of fracturing fluids, including chemical additives. Both we and our customers are subject to these risks.

The occurrence of any of these events could result in substantial losses to us or to our customers due to injury or loss of life, severe damage to or destruction of property, natural resources and equipment, pollution or other environmental damage, clean-up responsibilities, regulatory investigations and penalties, suspension of operations and repairs required to resume operations. The cost of managing such risks may be significant. The frequency and severity of such incidents will affect operating costs, insurability and relationships with customers, employees and regulators.

Should these risks materialize for us, our customers may elect not to rent our tools or utilize our services if they view our environmental or safety record as unacceptable, which could cause us to lose customers and substantial revenues. Should these risks materialize for our customers, they may also suffer similar negative consequences with respect to their own customers and clients. If

14

this were to happen, our customers may no longer be in a position to do business with us, thereby adversely affecting our business, results of operations and cash flows.

Our insurance may not be adequate to cover all losses or liabilities we may suffer. Also, insurance may no longer be available to us, or its availability may be at premium levels that do not justify its purchase. The occurrence of a significant uninsured claim, a claim in excess of the insurance coverage limits maintained by us or a claim at a time when we are not able to obtain liability insurance could have a material adverse effect on our ability to conduct normal business operations and on our business, results of operations, financial condition and cash flows. In addition, we may not be able to secure additional insurance or bonding that might be required by new governmental regulations. This may cause us to restrict our operations, which might severely impact our business, results of operations and cash flows.

Oilfield anti-indemnity provisions enacted by many states may restrict or prohibit a party’s indemnification of us.

We typically enter into agreements with our customers governing the provision of our services, which usually include certain indemnification provisions for losses resulting from operations. Such agreements may require each party to indemnify the other against certain claims regardless of the negligence or other fault of the indemnified party. However, many states place limitations on contractual indemnity agreements, particularly agreements that indemnify a party against the consequences of its own negligence. Furthermore, certain states, including Louisiana, New Mexico, Texas and Wyoming, have enacted statutes generally referred to as “oilfield anti-indemnity acts” expressly prohibiting certain indemnity agreements contained in or related to OFS agreements. Such oilfield anti-indemnity acts may restrict or void a party’s indemnification of us, which could have a material adverse effect on our business, results of operations and cash flows.

Restrictive covenants in the Credit Facility Agreement could limit our growth and our ability to finance our operations, fund our capital needs, respond to changing conditions and engage in other business activities that may be in our best interests.

The Amended and Restated Revolving Credit, Security and Guaranty Agreement among Drilling Tools International, Inc., certain of its subsidiaries, DTIC and PNC Bank, National Association, dated June 20, 2023 (“Credit Facility Agreement”) imposes operating and financial restrictions. These restrictions limit our ability to, among other things, subject to permitted exceptions:

The restrictions contained in the Credit Facility Agreement could:

The Credit Facility Agreement requires compliance with a specified financial ratio. The ability to comply with this ratio may be affected by events beyond our control and, as a result, this ratio may not be met in circumstances when it is tested. This financial ratio restriction could limit the ability to obtain future financings, make needed capital expenditures, withstand a continued downturn in our business or a downturn in the economy in general or otherwise conduct necessary corporate activities. Declines in oil and natural gas prices, and therefore a reduction in our customers’ activity, could result in failure to meet one or more of the covenants under the Credit Facility Agreement which could require refinancing or amendment of such obligations resulting in the payment of consent fees or higher interest rates, or require a capital raise at an inopportune time or on terms not favorable.

A breach of any of these covenants or the inability to comply with the required financial ratios or financial condition tests could result in a default under the Credit Facility Agreement. A default under the Credit Facility Agreement, if not cured or waived, could result in acceleration of all indebtedness outstanding thereunder.

We may incur indebtedness to execute our long-term growth strategy, which may reduce our profitability.

15

Maintaining a relevant rental fleet requires significant capital. We may require additional capital in the future to maintain and refresh our fleet. For the years ended December 31, 2023 and 2022, we spent $44 million, and $25 million, respectively, to purchase property, plant and equipment. Historically, we have financed these investments through cash flows from operations and external borrowings. These sources of capital may not be available to us in the future. If we are unable to fund capital expenditures for any reason, we may not be able to capture available growth opportunities or effectively maintain our existing assets and any such failure could have a material adverse effect on our business, results of operations and financial condition. If we incur additional indebtedness, our profitability may be reduced.

Political, regulatory, economic and social disruptions in the countries in which we conduct business could adversely affect our business or results of operations.

In addition to our facilities in the United States, we operate stocking points in Scotland and Germany and facilities in Canada and the United Arab Emirates. Additionally, we rent downhole drilling tools in Ukraine to Ukraine-based directional drilling companies and drilling contractors through Denimex, which acts as our representative in Ukraine. Instability and unforeseen changes in any of the markets in which we conduct business could have an adverse effect on the demand for, or supply of, the products that we rent and the services that we provide, which in turn could have an adverse effect on our business, results of operations and cash flows. These factors include, but are not limited to:

We may not be able to manage our growth successfully.

The growth of our operations will depend upon our ability to expand our customer base in our existing markets and to enter new markets in a timely manner at reasonable costs, organically or through acquisitions. In order for us to recover expenses incurred in entering new markets and obtaining new customers, we must attract and retain customers on economic terms and for extended periods. Customer growth depends on several factors outside of our control, including economic and demographic conditions, such as population changes, job and income growth, housing starts, new business formation and the overall level of economic activity. We may experience difficulty managing our growth, integrating new customers and employees, and complying with applicable regulations. Expanding our operations also may require continued development of our operating and financial controls and may place additional stress on our management and operational resources. We may be unable to manage our growth and development successfully.

A failure of our information technology infrastructure and cyberattacks could adversely impact us.

16

We depend on our IT systems, in particular COMPASS, for the efficient operation of our business. Accordingly, we rely upon the capacity, reliability and security of our IT hardware and software infrastructure and our ability to expand and update this infrastructure in response to our changing needs. Despite our implementation of security measures, our systems are vulnerable to damage from computer viruses, natural disasters, incursions by intruders or hackers, failures in hardware or software, power fluctuations, cyber terrorists and other similar disruptions. Moreover, we cannot guarantee that COMPASS, or features thereof, are not the protected intellectual property of third parties. If this is the case, these third parties may seek to protect their respective intellectual property rights, thereby hindering, or completely eliminating, our ability to use COMPASS and leverage its benefits.

Additionally, we rely on third parties to support the operation of our IT hardware and software infrastructure, and in certain instances, utilize web-based applications. We also provide proprietary and client data to certain third parties, and such third parties may be the subject of IT failures or cyberattacks. The failure of our IT systems or those of our vendors or third parties to whom we disclose certain information to perform as anticipated for any reason or any significant breach of security could disrupt our business and result in numerous adverse consequences, including reduced effectiveness and efficiency of operations, inappropriate disclosure of confidential and proprietary information, reputational harm, increased overhead costs and loss of important information, which could have a material adverse effect on our business and results of operations. In addition, we may be required to incur significant costs to protect against damage caused by these disruptions or security breaches in the future.

Our results of operations and financial condition could be negatively impacted by changes in accounting principles.

The accounting for our business is subject to change based on the evolution of our business model, interpretations of relevant accounting principles, enforcement of existing or new regulations, and changes in policies, rules, regulations, and interpretations of accounting and financial reporting requirements of the SEC or other regulatory agencies. Adoption of a change in accounting principles or interpretations could have a significant effect on our reported results of operations and could affect the reporting of transactions completed before the adoption of such change. It is difficult to predict the impact of future changes to accounting principles and accounting policies over financial reporting, any of which could adversely affect our results of operations and financial condition and could require significant investment in systems and personnel.

Adverse and unusual weather conditions may affect our operations.

Our operations may be materially affected by severe weather conditions in areas where we operate. Severe weather, such as hurricanes, high winds and seas, blizzards and extreme temperatures may cause evacuation of personnel, curtailment of services and suspension of operations, inability to deliver tools to customers in accordance with contract schedules and loss of or damage to our tools and facilities. In addition, variations from normal weather patterns can have a significant impact on demand for oil and natural gas, thereby reducing demand for our tools and services.

Risks Related to Legal and Regulatory Matters

Our operations require us to comply with various domestic and international regulations, violations of which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We are exposed to a variety of federal, state, local and international laws and regulations relating to matters such as environmental, workplace, health and safety, labor and employment, customs and tariffs, export and re-export controls, economic sanctions, currency exchange, bribery and corruption and taxation. These laws and regulations are complex, frequently change and have tended to become more stringent over time. They may be adopted, enacted, amended, enforced or interpreted in such a manner that the incremental cost of compliance could adversely impact our business, results of operations and cash flows.

In addition to our U.S. operations, we operate stocking points in Scotland and Germany and facilities in Canada and the United Arab Emirates. Additionally, we rent downhole drilling tools in Ukraine to Ukraine-based directional drilling companies and drilling contractors through Denimex, which acts as our representative in Ukraine. Our operations outside of the United States require us to comply with numerous anti-bribery and anti-corruption regulations. The U.S. Foreign Corrupt Practices Act, among others, applies to us and our operations. Our policies, procedures and programs may not always protect us from reckless or criminal acts committed by our employees or agents, and severe criminal or civil sanctions may be imposed as a result of violations of these laws. We are also subject to the risks that our employees and agents outside of the United States may fail to comply with applicable laws.

In addition, we purchase tools for use in the United States, Canada, the United Kingdom, Germany, the United Arab Emirates and Ukraine for use in such countries. Most movement of these tools involves imports and exports. As a result, compliance with multiple trade sanctions, embargoes and import/export laws and regulations pose a constant challenge and risk to us since a portion of our business is conducted outside of the United States through our subsidiaries. Our failure to comply with these laws and regulations could materially affect our business, results of operations and cash flows.

17

Compliance with environmental laws and regulations may adversely affect our business and results of operations.

Environmental laws and regulations in the United States and foreign countries affect the services we provide and the equipment we rent and service, as well as the facilities we operate. Such laws and regulations also impact the oil and gas industry more broadly, thereby impacting demand for our products and equipment. For example, we may be affected by such laws as the Resource Conservation and Recovery Act, the Comprehensive Environmental Response, Compensation, and Liability Act, the Clean Water Act, the Clean Air Act and the Occupational Safety and Health Act of 1970. Further, our customers may be subject to a range of laws and regulations governing hydraulic fracturing, drilling and greenhouse gas emissions.

We are required to invest financial and managerial resources to comply with environmental laws and regulations and believe that we will continue to be required to do so in the future. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, the imposition of remedial and mitigation obligations, and the issuance of orders enjoining operations. These laws and regulations, as well as the finalizing of other new laws and regulations affecting our operations or the exploration and production and transportation of crude oil and natural gas by our customers, could adversely affect our business and operating results by increasing our costs of compliance, increasing the costs of compliance and costs of doing business for our customers, limiting the demand for our products and services, or restricting our operations. Increased regulation or a move away from the use of fossil fuels caused by additional regulation could also reduce demand for our products and services.

Existing or future laws and regulations related to greenhouse gases and climate change and related public and governmental initiatives and additional compliance obligations could have a material adverse effect on our business, results of operations, prospects, and financial condition.

Changes in environmental requirements related to greenhouse gas emissions, climate change, or alternative energy sources may negatively impact demand for our products and services. For example, oil and natural gas E&P may decline as a result of environmental requirements or laws, regulations and policies promoting the use of alternative forms of energy, including land use policies and other actions to restrict oil and gas leasing and permitting in response to environmental and climate change concerns. In January 2021, the Acting Secretary of the Department of the Interior issued an order suspending new leasing and drilling permits for fossil fuel production on federal lands and waters for 60 days. President Biden then issued an executive order indefinitely suspending new oil and natural gas leases on public lands or in offshore waters pending completion of a comprehensive review and reconsideration of federal oil and gas permitting and leasing practices. Several states filed lawsuits challenging the suspension and in June 2021, a judge in the U.S. District Court for the Western District of Louisiana issued a nationwide temporary injunction blocking the suspension. The Department of the Interior successfully appealed the U.S. District Court’s ruling in August 2022, but the moratorium was again enjoined that month. However, the Biden Administration may take further actions to limit new oil and natural gas leases. Further, to the extent that the Department of Interior’s report or other initiatives to reform federal leasing practices result in the development of additional restrictions on drilling, limitations on the availability of leases, or restrictions on the ability to obtain required permits, it could impact our customers’ opportunities and reduce demand for our products and services in the aforementioned areas.

Federal, state and local agencies continue to evaluate climate-related legislation and other regulatory initiatives that would restrict emissions of greenhouse gases in areas in which we conduct business. For example, the United States Environmental Protection Agency has proposed new methane emissions regulations for certain oil and gas facilities, while the Inflation Reduction Act of 2022 established a charge on methane emissions above certain limits from such facilities . Because our business depends on the level of activity in the oil and gas industry, existing or future laws and regulations related to greenhouse gases could have a negative impact on our business if such laws or regulations reduce demand for oil and natural gas. Likewise, such laws or regulations may result in additional compliance obligations with respect to the release, capture, sequestration and use of greenhouse gases. These additional obligations could increase our costs and have a material adverse effect on our business, results of operations, prospects and financial condition.

Many of our customers utilize hydraulic fracturing in their operations. Environmental concerns have been raised regarding the potential impact of hydraulic fracturing on underground water supplies and seismic activity. These concerns have led to several regulatory and governmental initiatives in the United States to restrict the hydraulic fracturing process, which could have an adverse impact on our customers’ production activities. Although we do not conduct hydraulic fracturing, increased regulation and attention given to the hydraulic fracturing process could lead to greater opposition to oil and gas production activities using hydraulic fracturing techniques. In December 2021, the Texas Railroad Commission, which regulates the state’s oil and gas industry, suspended the use of deep wastewater disposal wells in four oil-producing counties in West Texas. The suspension is intended to mitigate earthquakes thought to be caused by the injection of waste fluids, including saltwater, that are a byproduct of hydraulic fracturing into disposal wells. The ban will require oil and gas production companies to find other options to handle the wastewater, which may include piping or trucking it longer distances to other locations not under the ban. The finalization of new laws or regulations at the federal, state, local or foreign level imposing reporting obligations on, or otherwise limiting, delaying or banning, the hydraulic fracturing process or

18

other processes on which hydraulic fracturing and subsequent hydrocarbon production relies, such as water disposal, could make it more difficult to complete oil and natural gas wells. Further, it could increase our customers’ costs of compliance and doing business, and otherwise adversely affect the hydraulic fracturing services they perform, which could negatively impact demand for our products.

Increasing attention by the public and government agencies to climate change and Environmental, Social and Governance (“ESG”) matters could also negatively impact demand for our products and services and the products of our oil and gas producing customers. In recent years, increasing attention has been given to corporate activities related to ESG in public discourse and the investment community. A number of advocacy groups, both domestically and internationally, have campaigned for governmental and private action to promote change at public companies related to ESG matters, including through the investment and voting practices of investment advisers, public pension funds, universities and other members of the investing community. These activities include increasing attention and demands for action related to climate change and energy rebalancing matters, such as promoting the use of substitutes to fossil fuel products and encouraging the divestment of fossil fuel equities, as well as pressuring lenders and other financial services companies to limit or curtail activities with fossil fuel companies. If this were to continue, it could have a material adverse effect on the valuation of the Common Stock and our ability to access equity capital markets.

In addition, our business could be impacted by initiatives to address greenhouse gases and climate change and incentives to conserve energy or use alternative energy sources. For example, the Inflation Reduction Act of 2022, signed into law by President Biden in August 2022, includes financial and other incentives to increase wind and solar electric generation and encourage consumers to use these alternative energy sources. Additional similar state or federal initiatives to incentivize a shift away from fossil fuels could reduce demand for hydrocarbons, thereby reducing demand for our products and services and negatively impacting our business.

Changes in tax laws or tax rates, adverse positions taken by taxing authorities and tax audits could impact our operating results.

We are subject to the jurisdiction of numerous domestic and foreign taxing authorities. Changes in tax laws or tax rates, the resolution of tax assessments or audits by various tax authorities could impact our operating results. In addition, we may periodically restructure our legal entity organization. If taxing authorities were to disagree with our tax positions in connection with any such restructurings, our effective income tax rate could be impacted. The final determination of our income tax liabilities involves the interpretation of local tax laws, tax treaties and related authorities in each taxing jurisdiction, as well as the significant use of estimates and assumptions regarding future operations and results and the timing of income and expenses. We may be audited and receive tax assessments from taxing authorities that may result in assessment of additional taxes that are ultimately resolved with the authorities or through the courts. We believe these assessments may occasionally be based on erroneous and even arbitrary interpretations of local tax law. Resolution of any tax matter involves uncertainties and there are no assurances that the outcomes will be favorable. If U.S. or foreign tax authorities change applicable tax laws, our overall taxes could increase, and our business, financial condition or results of operating may be adversely impacted.

If we are unable to fully protect our intellectual property rights or trade secrets, we may suffer a loss in revenue or any competitive advantage or market share we hold, or we may incur costs in litigation defending intellectual property rights.

While we have some patents and others pending, we do not have patents relating to many of our key processes and technology. If we are not able to maintain the confidentiality of our trade secrets, or if our competitors are able to replicate our technology or services, our competitive advantage would be diminished. We also cannot provide any assurance that any patents we may obtain in the future would provide us with any significant commercial benefit or would allow us to prevent our competitors from employing comparable technologies or processes. We may initiate litigation from time to time to protect and enforce our intellectual property rights. In any such litigation, a defendant may assert that our intellectual property rights are invalid or unenforceable. Third parties from time to time may also initiate litigation against us by asserting that our businesses infringe, impair, misappropriate, dilute or otherwise violate another party’s intellectual property rights. We may not prevail in any such litigation, and our intellectual property rights may be found invalid or unenforceable or our products and services may be found to infringe, impair, misappropriate, dilute or otherwise violate the intellectual property rights of others. The results or costs of any such litigation may have an adverse effect on our business, results of operations and financial condition. Any litigation concerning intellectual property could be protracted and costly, is inherently unpredictable and could have an adverse effect on our business, regardless of its outcome.

Moreover, third parties on whom we rely for certain tools may be subject to litigation to defend their intellectual property rights. If such litigation ends adversely for the third party with whom we deal, our ability to obtain such tools could be significantly limited or restricted. This could have a material adverse effect on our business.

As a result of plans to expand our business operations, including to jurisdictions in which tax laws may not be favorable, our obligations may change or fluctuate, become significantly more complex or become subject to greater risk of examination by taxing authorities, any of which could adversely affect our after-tax profitability and financial results.

19

Our effective tax rates may fluctuate widely in the future, particularly if our business expands domestically or internationally. Future effective tax rates could be affected by operating losses in jurisdictions where no tax benefit can be recorded under U.S. generally accepted accounting principles (“GAAP”), changes in deferred tax assets and liabilities, or changes in tax laws. Factors that could materially affect our future effective tax rates include, but are not limited to: (a) changes in tax laws or the regulatory environment, (b) changes in accounting and tax standards or practices, (c) changes in the composition of operating income by tax jurisdiction and (d) pre-tax operating results of our business.

Additionally, we are subject to significant income, withholding, and other tax obligations in the United States and may become subject to taxation in numerous additional U.S. state and local and non-U.S. jurisdictions with respect to income, operations and subsidiaries related to those jurisdictions. Our after-tax profitability and financial results could be subject to volatility or be affected by numerous factors, including (a) the availability of tax deductions, credits, exemptions, refunds and other benefits to reduce tax liabilities, (b) changes in the valuation of deferred tax assets and liabilities, if any, (c) the expected timing and amount of the release of any tax valuation allowances, (d) the tax treatment of stock-based compensation, (e) changes in the relative amount of earnings subject to tax in the various jurisdictions, (f) the potential business expansion into, or otherwise becoming subject to tax in, additional jurisdictions, (g) changes to existing intercompany structure (and any costs related thereto) and business operations, (h) the extent of intercompany transactions and the extent to which taxing authorities in relevant jurisdictions respect those intercompany transactions, and (i) the ability to structure business operations in an efficient and competitive manner. Outcomes from audits or examinations by taxing authorities could have an adverse effect on our after-tax profitability and financial condition. Additionally, the Internal Revenue Service (“IRS”) and several foreign tax authorities have increasingly focused attention on intercompany transfer pricing with respect to sales of products and services and the use of intangibles. Tax authorities could disagree with our intercompany charges, cross-jurisdictional transfer pricing or other matters and assess additional taxes. If we do not prevail in any such disagreements, our profitability may be affected.

Our after-tax profitability and financial results may also be adversely affected by changes in relevant tax laws and tax rates, treaties, regulations, administrative practices and principles, judicial decisions and interpretations thereof, in each case, possibly with retroactive effect.

Risks Related to Ownership of the Common Stock

If we fail to maintain an effective system of disclosure controls and internal control over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable regulations could be impaired, which may adversely affect investor confidence in us and, as a result, the market price of the Common Stock.

As a public company, we are required to comply with the Sarbanes-Oxley Act, which requires, among other things, that we maintain effective disclosure controls and procedures and internal control over financial reporting. We continue to refine our disclosure controls and other procedures that are designed to ensure that information required to be disclosed by us in filings with the SEC is recorded, processed, summarized and reported within the time periods specified in SEC rules, and that information required to be disclosed in reports under the Exchange Act is accumulated and communicated to our management, including our principal executive and financial officers.

We will continue to refine our internal control over financial reporting. We will be required to make a formal assessment of the effectiveness of our internal control over financial reporting and once we cease to be an emerging growth company, we will be required to include an attestation report on internal control over financial reporting issued by our independent registered public accounting firm. To achieve compliance with these requirements within the prescribed time period, we have been engaging, and will continue to engage, in a process to document and evaluate our internal control over financial reporting. This process is both costly and challenging, and requires us to dedicate significant internal resources. We may also engage outside consultants and hire new employees with the requisite skillset and experience. We are developing a plan to assess and document the adequacy of our internal control over financial reporting, validate through testing that controls are functioning as documented and implement a continuous reporting and improvement process for internal control over financial reporting. There is a risk that we will not be able to conclude, within the prescribed time period or at all, that our internal control over financial reporting is effective as required by Section 404 of the Sarbanes-Oxley Act. Moreover, our testing, or the subsequent testing by our independent registered public accounting firm, may reveal additional deficiencies in our internal control over financial reporting that are deemed to be material weaknesses.

Any failure to implement and maintain effective disclosure controls and procedures and internal control over financial reporting, including the identification of one or more material weaknesses, could cause investors to lose confidence in the accuracy and completeness of our financial statements and reports, which would likely adversely affect the market price of the Common Stock. In addition, we could be subject to sanctions or investigations by Nasdaq, the SEC and other regulatory authorities.

The market price of the Common Stock may be volatile, which could cause the value of your investment to decline.

20