00018806612023FYFalsehttp://fasb.org/us-gaap/2023#RelatedPartyMemberhttp://fasb.org/us-gaap/2023#RelatedPartyMemberhttp://fasb.org/us-gaap/2023#RelatedPartyMemberhttp://fasb.org/us-gaap/2023#RelatedPartyMemberP2YP1YP1YP3Yhttp://fasb.org/us-gaap/2023#OtherAssetshttp://fasb.org/us-gaap/2023#OtherAssets.3333.2http://fasb.org/us-gaap/2023#OtherLiabilitiesP3Y15400018806612023-01-012023-12-3100018806612023-06-30iso4217:USD0001880661us-gaap:CommonClassAMember2024-02-20xbrli:shares0001880661us-gaap:NonvotingCommonStockMember2024-02-200001880661us-gaap:CommonClassBMember2024-02-200001880661us-gaap:ConsolidatedEntityExcludingVieMember2023-12-310001880661us-gaap:ConsolidatedEntityExcludingVieMember2022-12-3100018806612023-12-3100018806612022-12-310001880661us-gaap:AssetPledgedAsCollateralMember2023-12-310001880661us-gaap:AssetPledgedAsCollateralMember2022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2022-12-310001880661us-gaap:CommonClassAMember2022-12-31iso4217:USDxbrli:shares0001880661us-gaap:CommonClassAMember2023-12-310001880661us-gaap:CommonClassBMember2022-12-310001880661us-gaap:CommonClassBMember2023-12-3100018806612022-01-012022-12-3100018806612021-01-012021-12-310001880661us-gaap:ConsolidatedEntityExcludingVieMember2023-01-012023-12-310001880661us-gaap:ConsolidatedEntityExcludingVieMember2022-01-012022-12-310001880661us-gaap:ConsolidatedEntityExcludingVieMember2021-01-012021-12-310001880661us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001880661us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001880661us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-3100018806612022-01-012022-01-1800018806612022-01-192022-12-310001880661tpg:PartnerCapitalMember2020-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2020-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2020-12-310001880661us-gaap:AdditionalPaidInCapitalMember2020-12-310001880661us-gaap:RetainedEarningsMember2020-12-310001880661us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001880661us-gaap:ParentMember2020-12-310001880661us-gaap:NoncontrollingInterestMember2020-12-3100018806612020-12-310001880661tpg:PartnerCapitalMember2021-01-012021-12-310001880661us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001880661tpg:PartnerCapitalMember2021-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2021-12-310001880661us-gaap:AdditionalPaidInCapitalMember2021-12-310001880661us-gaap:RetainedEarningsMember2021-12-310001880661us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001880661us-gaap:ParentMember2021-12-310001880661us-gaap:NoncontrollingInterestMember2021-12-3100018806612021-12-310001880661tpg:PartnerCapitalMember2022-01-012022-01-180001880661us-gaap:NoncontrollingInterestMember2022-01-012022-01-180001880661tpg:PartnerCapitalMember2022-01-012022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-01-012022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2022-01-012022-12-310001880661us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001880661us-gaap:RetainedEarningsMember2022-01-012022-12-310001880661us-gaap:ParentMember2022-01-012022-12-310001880661us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMemberus-gaap:IPOMember2022-01-012022-12-310001880661us-gaap:IPOMemberus-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001880661us-gaap:IPOMemberus-gaap:ParentMember2022-01-012022-12-310001880661us-gaap:IPOMemberus-gaap:NoncontrollingInterestMember2022-01-012022-12-310001880661us-gaap:IPOMember2022-01-012022-12-310001880661us-gaap:NoncontrollingInterestMember2022-01-192022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMemberus-gaap:OverAllotmentOptionMember2022-01-012022-12-310001880661us-gaap:AdditionalPaidInCapitalMemberus-gaap:OverAllotmentOptionMember2022-01-012022-12-310001880661us-gaap:ParentMemberus-gaap:OverAllotmentOptionMember2022-01-012022-12-310001880661us-gaap:OverAllotmentOptionMember2022-01-012022-12-310001880661us-gaap:AdditionalPaidInCapitalMember2022-01-012022-01-180001880661us-gaap:ParentMember2022-01-012022-01-180001880661us-gaap:RetainedEarningsMember2022-01-192022-12-310001880661us-gaap:ParentMember2022-01-192022-12-310001880661us-gaap:AdditionalPaidInCapitalMember2022-01-192022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2022-12-310001880661us-gaap:AdditionalPaidInCapitalMember2022-12-310001880661us-gaap:RetainedEarningsMember2022-12-310001880661us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001880661us-gaap:ParentMember2022-12-310001880661us-gaap:NoncontrollingInterestMember2022-12-310001880661us-gaap:RetainedEarningsMember2023-01-012023-12-310001880661us-gaap:ParentMember2023-01-012023-12-310001880661us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001880661us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2023-01-012023-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2023-01-012023-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassAMember2023-12-310001880661us-gaap:CommonStockMemberus-gaap:CommonClassBMember2023-12-310001880661us-gaap:AdditionalPaidInCapitalMember2023-12-310001880661us-gaap:RetainedEarningsMember2023-12-310001880661us-gaap:ParentMember2023-12-310001880661us-gaap:NoncontrollingInterestMember2023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2023-01-012023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2022-01-012022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2021-01-012021-12-310001880661us-gaap:IPOMember2022-01-122022-01-120001880661us-gaap:IPOMember2022-01-120001880661tpg:NonControllingInterestHolderOfTPGOperatingGroupMemberus-gaap:IPOMember2022-01-122022-01-120001880661us-gaap:CommonClassAMemberus-gaap:IPOMember2022-01-122022-01-120001880661us-gaap:NonvotingCommonStockMemberus-gaap:IPOMember2022-01-122022-01-120001880661us-gaap:CommonClassAMemberus-gaap:OverAllotmentOptionMember2022-02-092022-02-090001880661us-gaap:CommonClassAMembertpg:NonControllingInterestHolderOfTPGOperatingGroupMemberus-gaap:OverAllotmentOptionMember2022-02-092022-02-090001880661us-gaap:OverAllotmentOptionMember2022-02-092022-02-090001880661us-gaap:CommonClassAMemberus-gaap:OverAllotmentOptionMember2022-02-090001880661us-gaap:NonvotingCommonStockMemberus-gaap:OverAllotmentOptionMember2022-02-090001880661tpg:TPGOperatingGroupMember2023-12-31xbrli:pure0001880661tpg:ManagementFeesMember2023-01-012023-12-310001880661tpg:ManagementFeesMember2022-01-012022-12-310001880661tpg:ManagementFeesMember2021-01-012021-12-310001880661tpg:MonitoringFeesMember2023-01-012023-12-310001880661tpg:MonitoringFeesMember2022-01-012022-12-310001880661tpg:MonitoringFeesMember2021-01-012021-12-310001880661tpg:TransactionFeesMember2023-01-012023-12-310001880661tpg:TransactionFeesMember2022-01-012022-12-310001880661tpg:TransactionFeesMember2021-01-012021-12-310001880661tpg:IncentiveFeesMember2023-01-012023-12-310001880661tpg:IncentiveFeesMember2022-01-012022-12-310001880661tpg:IncentiveFeesMember2021-01-012021-12-310001880661tpg:ExpenseReimbursementsAndOtherMember2023-01-012023-12-310001880661tpg:ExpenseReimbursementsAndOtherMember2022-01-012022-12-310001880661tpg:ExpenseReimbursementsAndOtherMember2021-01-012021-12-310001880661tpg:CommittedCapitalMembersrt:MinimumMember2023-12-310001880661tpg:CommittedCapitalMembersrt:MaximumMember2023-12-310001880661srt:MinimumMembertpg:ActivelyInvestedCapitalMember2023-12-310001880661srt:MaximumMembertpg:ActivelyInvestedCapitalMember2023-12-310001880661tpg:NetFundedCapitalCommitmentsMembersrt:MinimumMember2023-12-310001880661tpg:NetFundedCapitalCommitmentsMembersrt:MaximumMember2023-12-310001880661tpg:CostOfInvestmentsMembersrt:MinimumMember2023-12-310001880661tpg:CostOfInvestmentsMembersrt:MaximumMember2023-12-310001880661srt:MinimumMembertpg:NetAssetValueMember2023-12-310001880661srt:MaximumMembertpg:NetAssetValueMember2023-12-310001880661tpg:YTPGMember2023-12-310001880661us-gaap:CommonClassAMembertpg:YTPGMember2023-04-170001880661tpg:AFTRMember2023-12-310001880661tpg:AFTRMemberus-gaap:CommonClassAMember2023-08-160001880661srt:MinimumMember2023-12-310001880661srt:MaximumMember2023-12-310001880661tpg:FurnitureFixturesEquipmentAndComputerEquipmentMembersrt:MinimumMember2023-12-310001880661srt:MaximumMembertpg:FurnitureFixturesEquipmentAndComputerEquipmentMember2023-12-310001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-11-012023-11-010001880661tpg:VestedCommonUnitMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:CommonUnitsMember2023-11-012023-11-010001880661tpg:UnvestedCommonUnitMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:CommonUnitsMember2023-11-012023-11-01tpg:installment0001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:AggregateAnnualCashHoldbackAmountMember2023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:EarnoutPaymentMember2023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembersrt:AffiliatedEntityMember2023-11-010001880661tpg:VestedCommonUnitMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-11-012023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:AcquisitionCommonUnitsMember2023-11-012023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMemberus-gaap:RestrictedStockUnitsRSUMember2023-11-012023-11-010001880661tpg:InvestmentManagementAgreementsMembertpg:ValuationTechniqueMultiPeriodExcessEarningsMethodMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-11-012023-11-010001880661tpg:InvestmentManagementAgreementsMembertpg:ValuationTechniqueMultiPeriodExcessEarningsMethodMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembersrt:MinimumMember2023-11-012023-11-010001880661tpg:InvestmentManagementAgreementsMembertpg:ValuationTechniqueMultiPeriodExcessEarningsMethodMembersrt:MaximumMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-11-012023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMemberus-gaap:ValuationTechniqueDiscountedCashFlowMembertpg:AcquiredCarriedInterestMember2023-11-012023-11-010001880661tpg:ValuationTechniqueReplacementCostAnalysisAndReliefFromRoyaltyAnalysisMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMemberus-gaap:TechnologyBasedIntangibleAssetsMember2023-11-012023-11-010001880661us-gaap:TradeNamesMembertpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:ValuationTechniqueReliefFromRoyaltyMethodMember2023-11-012023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-01-012023-12-310001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2022-01-012022-12-310001880661tpg:NewQuestHoldingsCaymanLimitedMember2022-01-310001880661tpg:NewQuestHoldingsCaymanLimitedMemberus-gaap:CommonClassAMember2022-01-012022-01-310001880661tpg:NewQuestHoldingsCaymanLimitedMembertpg:CommonUnitsMember2022-01-012022-01-310001880661tpg:NewQuestHoldingsCaymanLimitedMember2022-01-012022-01-310001880661tpg:PerformanceAllocationsMember2023-12-310001880661tpg:PerformanceAllocationsMember2022-12-310001880661us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001880661us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001880661tpg:CapitalInterestsMember2023-12-310001880661tpg:CapitalInterestsMember2022-12-310001880661tpg:OtherEquityMethodInvestmentsMember2023-12-310001880661tpg:OtherEquityMethodInvestmentsMember2022-12-3100018806612021-09-012021-09-300001880661tpg:NewQuestHoldingsCaymanLimitedMember2021-01-012021-12-310001880661tpg:TPGSMember2021-12-012021-12-310001880661tpg:NerdyIncMember2023-12-310001880661us-gaap:CommonClassAMembertpg:NerdyIncMember2023-12-310001880661us-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:NerdyIncMemberus-gaap:WarrantMember2023-09-012023-09-300001880661us-gaap:CommonClassAMembertpg:NerdyIncMember2023-09-012023-09-300001880661tpg:ClassAEarnoutSharesMembertpg:NerdyIncMember2023-12-310001880661tpg:NerdyIncMember2022-12-310001880661us-gaap:CommonClassAMembertpg:NerdyIncMember2022-12-310001880661tpg:ClassAEarnoutSharesMembertpg:NerdyIncMember2022-12-310001880661tpg:NerdyIncMemberus-gaap:WarrantMember2022-12-310001880661us-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661tpg:TPGSMember2021-12-012021-12-310001880661tpg:TPGFundsAndPublicSPACsMember2022-12-310001880661tpg:TPGFundsAndPublicSPACsMember2023-12-310001880661tpg:TPGFundsAndPublicSPACsMember2023-12-310001880661tpg:TPGFundsAndPublicSPACsMember2022-12-310001880661tpg:TPGFundsAndPublicSPACsMember2021-12-310001880661tpg:TPGFundsAndPublicSPACsMember2023-01-012023-12-310001880661tpg:TPGFundsAndPublicSPACsMember2022-01-012022-12-310001880661tpg:TPGFundsAndPublicSPACsMember2021-01-012021-12-310001880661tpg:TPGFundsAndPublicSPACsMember2021-01-012021-12-310001880661tpg:ForeignPrivateAgreementsMember2023-12-310001880661tpg:ForeignPrivateAgreementsMember2022-12-310001880661us-gaap:WarrantMember2023-12-310001880661us-gaap:WarrantMember2022-12-310001880661us-gaap:SwapMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001880661us-gaap:SwapMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001880661us-gaap:SwapMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-310001880661us-gaap:ForeignExchangeContractMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001880661us-gaap:ForeignExchangeContractMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001880661us-gaap:ForeignExchangeContractMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-310001880661tpg:PublicWarrantsMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2023-01-012023-12-310001880661tpg:PublicWarrantsMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2022-01-012022-12-310001880661tpg:PublicWarrantsMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2021-01-012021-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:ForwardContractsMember2023-01-012023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:ForwardContractsMember2022-01-012022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:ForwardContractsMember2021-01-012021-12-310001880661us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:AggregateAnnualCashHoldbackAmountMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:AggregateAnnualCashHoldbackAmountMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:AggregateAnnualCashHoldbackAmountMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:AggregateAnnualCashHoldbackAmountMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:EarnoutPaymentMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:EarnoutPaymentMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:EarnoutPaymentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661tpg:EarnoutPaymentMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001880661us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:FairValueInputsLevel1Memberus-gaap:WarrantMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:FairValueInputsLevel2Memberus-gaap:WarrantMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:FairValueInputsLevel3Memberus-gaap:WarrantMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661us-gaap:WarrantMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001880661tpg:FinancialLiabilityMember2022-12-310001880661tpg:FinancialLiabilityMember2021-12-310001880661tpg:FinancialLiabilityMember2023-01-012023-12-310001880661tpg:FinancialLiabilityMember2022-01-012022-12-310001880661tpg:FinancialLiabilityMember2023-12-310001880661us-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2022-12-310001880661us-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2021-12-310001880661us-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2023-01-012023-12-310001880661us-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2022-01-012022-12-310001880661us-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2023-12-310001880661us-gaap:MarketApproachValuationTechniqueMembertpg:AggregateAnnualCashHoldbackAmountMemberus-gaap:FairValueInputsLevel3Member2023-12-310001880661us-gaap:MarketApproachValuationTechniqueMembertpg:AggregateAnnualCashHoldbackAmountMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMember2023-12-310001880661us-gaap:MarketApproachValuationTechniqueMembertpg:EarnoutPaymentMemberus-gaap:FairValueInputsLevel3Member2023-12-310001880661us-gaap:MeasurementInputPriceVolatilityMemberus-gaap:MarketApproachValuationTechniqueMembertpg:EarnoutPaymentMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001880661us-gaap:FairValueInputsLevel3Member2023-12-310001880661tpg:ContractualPerformanceFeeAllocationsMember2023-12-310001880661tpg:ContractualPerformanceFeeAllocationsMember2022-12-310001880661tpg:ManagementContractsMember2023-12-310001880661tpg:ManagementContractsMember2022-12-310001880661us-gaap:TechnologyBasedIntangibleAssetsMember2023-12-310001880661us-gaap:TechnologyBasedIntangibleAssetsMember2022-12-310001880661tpg:InvestorRelationshipsMember2023-12-310001880661tpg:InvestorRelationshipsMember2022-12-310001880661us-gaap:TradeNamesMember2023-12-310001880661us-gaap:TradeNamesMember2022-12-310001880661us-gaap:OtherIntangibleAssetsMember2023-12-310001880661us-gaap:OtherIntangibleAssetsMember2023-12-310001880661us-gaap:OtherIntangibleAssetsMember2022-12-310001880661us-gaap:OtherIntangibleAssetsMember2022-12-310001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMember2023-12-310001880661us-gaap:OtherIntangibleAssetsMember2022-12-310001880661us-gaap:OtherIntangibleAssetsMember2023-12-310001880661us-gaap:LeaseholdImprovementsMember2023-12-310001880661us-gaap:LeaseholdImprovementsMember2022-12-310001880661us-gaap:ComputerEquipmentMember2023-12-310001880661us-gaap:ComputerEquipmentMember2022-12-310001880661us-gaap:FurnitureAndFixturesMember2023-12-310001880661us-gaap:FurnitureAndFixturesMember2022-12-310001880661us-gaap:PropertyPlantAndEquipmentOtherTypesMember2023-12-310001880661us-gaap:PropertyPlantAndEquipmentOtherTypesMember2022-12-310001880661tpg:NorthwoodsEuropeanManagementLLCMembertpg:NearwaterMemberus-gaap:RepurchaseAgreementsMember2023-12-31iso4217:EUR0001880661tpg:CitibankNAMembertpg:NorthwoodsEuropeanManagementLLCMemberus-gaap:RepurchaseAgreementsMember2023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:NonrelatedPartyMember2023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:NonrelatedPartyMember2022-12-310001880661us-gaap:RelatedPartyMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2023-12-310001880661us-gaap:RelatedPartyMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembersrt:MinimumMembertpg:RemainCoMember2023-01-012023-12-310001880661srt:MaximumMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembertpg:RemainCoMember2023-01-012023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembertpg:RemainCoMember2022-01-012022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembertpg:RemainCoMember2023-01-012023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembersrt:ScenarioForecastMembertpg:RemainCoMember2024-01-012024-12-310001880661srt:AffiliatedEntityMembertpg:AnnualAdministrationMember2023-01-012023-12-310001880661us-gaap:SecuredDebtMembertpg:TrancheAMember2018-12-310001880661us-gaap:SecuredDebtMembertpg:TrancheBMember2019-12-310001880661us-gaap:SecuredDebtMembertpg:SecuredNotesMember2023-12-310001880661us-gaap:SecuredDebtMembertpg:SecuredNotesMember2022-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:SecuredDebtMember2023-12-310001880661us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:SecuredDebtMember2022-12-310001880661us-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMember2023-12-310001880661us-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMember2022-12-310001880661tpg:SeniorUnsecuredTermLoanAgreementMemberus-gaap:LineOfCreditMember2023-12-310001880661tpg:SeniorUnsecuredTermLoanAgreementMemberus-gaap:LineOfCreditMember2022-12-310001880661us-gaap:SecuredDebtMembertpg:SecuredBorrowingsTrancheAMember2023-12-310001880661us-gaap:SecuredDebtMembertpg:SecuredBorrowingsTrancheAMember2022-12-310001880661tpg:SecuredBorrowingsTrancheBMemberus-gaap:SecuredDebtMember2023-12-310001880661tpg:SecuredBorrowingsTrancheBMemberus-gaap:SecuredDebtMember2022-12-310001880661us-gaap:LineOfCreditMembertpg:A364DayRevolvingCreditFacilityMember2023-12-310001880661us-gaap:LineOfCreditMembertpg:A364DayRevolvingCreditFacilityMember2022-12-310001880661us-gaap:LineOfCreditMembertpg:SubordinatedCreditFacilityMember2023-12-310001880661us-gaap:LineOfCreditMembertpg:SubordinatedCreditFacilityMember2022-12-310001880661us-gaap:LineOfCreditMember2023-12-310001880661us-gaap:SecuredDebtMember2023-12-310001880661us-gaap:SecuredDebtMember2022-12-310001880661us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMember2023-12-310001880661srt:MaximumMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMemberus-gaap:BaseRateMember2023-09-012023-09-300001880661srt:MaximumMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMembertpg:SecuredOvernightFinancingRateSOFRMember2023-09-012023-09-300001880661us-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMembertpg:FundCashConsiderationOfAcquisitionMember2023-01-012023-12-310001880661tpg:WorkingCapitalPurposesMemberus-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMember2023-01-012023-12-310001880661tpg:SeniorUnsecuredTermLoanAgreementMemberus-gaap:LineOfCreditMembertpg:SecuredOvernightFinancingRateSOFRMembertpg:TermLoansMember2023-01-012023-12-310001880661tpg:SeniorUnsecuredTermLoanAgreementMembertpg:SecuredOvernightFinancingRateSOFRMembertpg:TermLoansMember2023-01-012023-12-31tpg:tranche0001880661us-gaap:LineOfCreditMembertpg:A364DayRevolvingCreditFacilityMember2023-04-142023-04-140001880661us-gaap:LineOfCreditMembertpg:A364DayRevolvingCreditFacilityMember2023-04-140001880661us-gaap:LineOfCreditMembertpg:FederalFundsRateMember2023-01-012023-12-310001880661us-gaap:LineOfCreditMembertpg:SecuredOvernightFinancingRateSOFRMember2023-01-012023-12-310001880661us-gaap:LineOfCreditMemberus-gaap:BaseRateMembersrt:MinimumMember2023-01-012023-12-310001880661srt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:BaseRateMember2023-01-012023-12-310001880661us-gaap:LineOfCreditMembertpg:RiskFreeRateMembersrt:MinimumMember2023-01-012023-12-310001880661srt:MaximumMemberus-gaap:LineOfCreditMembertpg:RiskFreeRateMember2023-01-012023-12-310001880661us-gaap:LineOfCreditMembersrt:MinimumMembertpg:SterlingOvernightIndexAverageMember2023-01-012023-12-310001880661srt:MaximumMemberus-gaap:LineOfCreditMembertpg:SterlingOvernightIndexAverageMember2023-01-012023-12-310001880661us-gaap:LineOfCreditMember2023-01-012023-12-310001880661us-gaap:RevolvingCreditFacilityMembertpg:SubordinatedCreditFacilityMemberus-gaap:SubordinatedDebtMember2014-08-012014-08-31tpg:creditFacility0001880661us-gaap:RevolvingCreditFacilityMembertpg:SubordinatedCreditFacilityOneMemberus-gaap:SubordinatedDebtMember2014-08-310001880661us-gaap:RevolvingCreditFacilityMembertpg:SubordinatedCreditFacilityTwoMemberus-gaap:SubordinatedDebtMember2014-08-310001880661us-gaap:RevolvingCreditFacilityMembertpg:SubordinatedCreditFacilityMemberus-gaap:SubordinatedDebtMember2014-08-310001880661us-gaap:RevolvingCreditFacilityMembertpg:SecuredOvernightFinancingRateSOFRMembertpg:SubordinatedCreditFacilityMemberus-gaap:SubordinatedDebtMember2023-01-012023-12-310001880661us-gaap:RevolvingCreditFacilityMembertpg:SubordinatedCreditFacilityMemberus-gaap:SubordinatedDebtMember2023-01-012023-12-310001880661us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:UnsecuredDebtMember2023-12-310001880661us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:UnsecuredDebtMember2022-12-310001880661us-gaap:SecuredDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2023-12-310001880661us-gaap:SecuredDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001880661us-gaap:SecuredDebtMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2023-12-310001880661us-gaap:SecuredDebtMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310001880661us-gaap:LineOfCreditMembertpg:SeniorUnsecuredRevolvingCreditFacilityMemberus-gaap:SubsequentEventMember2024-01-012024-01-310001880661us-gaap:DomesticCountryMember2023-01-012023-12-310001880661us-gaap:DomesticCountryMember2022-01-012022-12-310001880661us-gaap:DomesticCountryMember2021-01-012021-12-310001880661us-gaap:ForeignCountryMember2023-01-012023-12-310001880661us-gaap:ForeignCountryMember2022-01-012022-12-310001880661us-gaap:ForeignCountryMember2021-01-012021-12-310001880661us-gaap:ForeignCountryMember2023-12-310001880661tpg:PortfolioCompaniesMembersrt:AffiliatedEntityMember2023-12-310001880661tpg:PortfolioCompaniesMembersrt:AffiliatedEntityMember2022-12-310001880661tpg:PartnersAndEmployeesMembersrt:AffiliatedEntityMember2023-12-310001880661tpg:PartnersAndEmployeesMembersrt:AffiliatedEntityMember2022-12-310001880661tpg:OtherRelatedEntitiesMembersrt:AffiliatedEntityMember2023-12-310001880661tpg:OtherRelatedEntitiesMembersrt:AffiliatedEntityMember2022-12-310001880661tpg:UnconsolidatedVIEsMembersrt:AffiliatedEntityMember2023-12-310001880661tpg:UnconsolidatedVIEsMembersrt:AffiliatedEntityMember2022-12-310001880661srt:AffiliatedEntityMember2023-12-310001880661srt:AffiliatedEntityMember2022-12-310001880661us-gaap:RelatedPartyMembertpg:RelatedPartyInvestmentsMember2023-01-012023-12-310001880661us-gaap:RelatedPartyMembertpg:RelatedPartyInvestmentsMember2022-01-012022-12-310001880661us-gaap:RelatedPartyMemberus-gaap:NotesReceivableMember2023-12-310001880661us-gaap:RelatedPartyMemberus-gaap:NotesReceivableMember2022-12-3100018806612022-01-012022-01-310001880661us-gaap:RelatedPartyMembertpg:AnnualAdministrationMember2023-01-012023-12-310001880661us-gaap:RelatedPartyMembertpg:AnnualAdministrationMember2022-01-012022-12-310001880661us-gaap:RelatedPartyMembertpg:OtherRelatedPartyTransactionsMember2023-01-012023-12-310001880661us-gaap:RelatedPartyMembertpg:OtherRelatedPartyTransactionsMember2022-01-012022-12-310001880661us-gaap:RelatedPartyMembertpg:OtherRelatedPartyTransactionsMember2021-01-012021-12-310001880661tpg:UnitsMembertpg:AFTRMemberus-gaap:IPOMember2021-08-012021-08-310001880661tpg:UnitsMembertpg:AFTRMemberus-gaap:IPOMember2021-08-310001880661tpg:AFTRMemberus-gaap:CommonClassAMember2021-08-310001880661tpg:AFTRMemberus-gaap:IPOMember2021-08-310001880661tpg:AFTRMemberus-gaap:SeriesAPreferredStockMember2023-08-160001880661tpg:UnitsMemberus-gaap:IPOMembertpg:YTPGMember2021-04-012021-04-300001880661tpg:UnitsMemberus-gaap:IPOMembertpg:YTPGMember2021-04-300001880661us-gaap:CommonClassAMembertpg:YTPGMember2021-04-300001880661us-gaap:IPOMembertpg:YTPGMember2021-04-300001880661us-gaap:SeriesAPreferredStockMembertpg:YTPGMember2023-04-170001880661tpg:UnitsMemberus-gaap:IPOMembertpg:TPGYMember2020-10-012020-10-310001880661tpg:UnitsMemberus-gaap:IPOMembertpg:TPGYMember2020-10-310001880661us-gaap:CommonClassAMembertpg:TPGYMember2020-10-310001880661us-gaap:IPOMembertpg:TPGYMember2020-10-310001880661tpg:TPGYMemberus-gaap:SeriesAPreferredStockMember2022-10-110001880661us-gaap:IPOMembertpg:PublicSPACsMember2021-01-012021-12-310001880661us-gaap:IPOMembertpg:PublicSPACsMember2023-01-012023-12-310001880661us-gaap:IPOMembertpg:PublicSPACsMember2022-01-012022-12-310001880661tpg:AFTRMemberus-gaap:WarrantMember2021-08-310001880661tpg:TPGYMemberus-gaap:WarrantMember2020-10-310001880661tpg:April2024Member2023-12-310001880661tpg:August2025Member2023-12-310001880661tpg:March2026Member2023-12-310001880661tpg:June2026Member2023-12-310001880661tpg:December2026Member2023-12-310001880661tpg:September2028Member2023-12-310001880661tpg:June2030Member2023-12-310001880661tpg:HellasInvestmentMember2023-01-012023-12-31tpg:partnertpg:individual0001880661tpg:HellasInvestmentMembertpg:TPGAndApaxRelatedPartiesMember2018-02-012018-02-280001880661tpg:TPGMembertpg:HellasInvestmentMember2018-02-012018-02-280001880661tpg:HellasInvestmentMemberstpr:NY2023-12-31tpg:cases00018806612022-01-1300018806612023-01-062023-01-0600018806612023-01-060001880661us-gaap:RestrictedStockUnitsRSUMember2022-02-092022-02-090001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2023-11-012023-11-010001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsIPOServiceAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsIPOServiceAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsIPOServiceAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsExecutiveServiceAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsExecutiveServiceAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsExecutiveServiceAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsOrdinaryServiceAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsOrdinaryServiceAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsOrdinaryServiceAwardsMember2022-01-012022-12-310001880661tpg:RestrictedStockUnitsOrdinaryPerformanceConditionAwardsMember2023-12-310001880661tpg:RestrictedStockUnitsOrdinaryPerformanceConditionAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsOrdinaryPerformanceConditionAwardsMember2022-01-012022-12-310001880661us-gaap:RestrictedStockUnitsRSUMember2023-12-310001880661us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001880661us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001880661us-gaap:GeneralAndAdministrativeExpenseMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001880661us-gaap:GeneralAndAdministrativeExpenseMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001880661tpg:ServiceAwardsMember2023-01-012023-12-310001880661tpg:RestrictedStockUnitsAcquisitionServiceAwardsMember2023-11-012023-11-010001880661tpg:ServiceAwardsMember2022-12-310001880661tpg:ServiceAwardsMember2023-12-310001880661us-gaap:CommonClassAMemberus-gaap:SubsequentEventMembertpg:ServiceAwardsMember2024-01-012024-01-310001880661us-gaap:SubsequentEventMembertpg:RestrictedStockUnitsOrdinaryServiceAwardsMember2024-01-012024-01-310001880661tpg:RestrictedStockUnitsAcquisitionServiceAwardsMemberus-gaap:SubsequentEventMember2024-01-012024-01-310001880661srt:MinimumMemberus-gaap:SubsequentEventMembertpg:ServiceAwardsMember2024-01-012024-01-310001880661srt:MaximumMemberus-gaap:SubsequentEventMembertpg:ServiceAwardsMember2024-01-012024-01-310001880661tpg:RestrictedStockUnitsOrdinaryPerformanceConditionAwardsMember2022-12-310001880661tpg:RestrictedStockUnitsIPOServiceVestingAndMarketConditionIPOAwardsMember2022-01-182022-01-180001880661tpg:RestrictedStockUnitsIPOServiceAwardsMember2022-01-182022-01-180001880661tpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2022-01-182022-01-180001880661us-gaap:ShareBasedCompensationAwardTrancheOneMembertpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2022-01-182022-01-180001880661us-gaap:ShareBasedCompensationAwardTrancheTwoMembertpg:RestrictedStockUnitsIPOMarketConditionAwardsMember2022-01-182022-01-180001880661tpg:RestrictedStockUnitsExecutiveServiceAwardsMembersrt:ChiefExecutiveOfficerMember2023-11-302023-11-300001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-11-302023-11-300001880661us-gaap:ShareBasedCompensationAwardTrancheThreeMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-11-302023-11-300001880661us-gaap:ShareBasedCompensationAwardTrancheTwoMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-11-302023-11-300001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2023-11-302023-11-300001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMembertpg:ShareBasedPaymentArrangementTrancheFourMember2023-11-302023-11-300001880661us-gaap:CommonClassAMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2023-11-302023-11-300001880661us-gaap:CommonClassAMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-11-302023-11-300001880661us-gaap:CommonClassAMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-11-302023-11-300001880661us-gaap:CommonClassAMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMembertpg:ShareBasedPaymentArrangementTrancheFourMember2023-11-302023-11-300001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2023-01-012023-12-310001880661us-gaap:ShareBasedCompensationAwardTrancheTwoMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-01-012023-12-310001880661us-gaap:ShareBasedCompensationAwardTrancheThreeMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-01-012023-12-310001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMembertpg:ShareBasedPaymentArrangementTrancheFourMember2023-01-012023-12-310001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2023-12-310001880661us-gaap:ShareBasedCompensationAwardTrancheTwoMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-12-310001880661us-gaap:ShareBasedCompensationAwardTrancheThreeMembersrt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMember2023-12-310001880661srt:ChiefExecutiveOfficerMembertpg:RestrictedStockUnitsExecutiveMarketConditionAwardsMembertpg:ShareBasedPaymentArrangementTrancheFourMember2023-12-310001880661tpg:MarketConditionAwardsMember2022-12-310001880661tpg:MarketConditionAwardsMember2023-01-012023-12-310001880661tpg:MarketConditionAwardsMember2023-12-310001880661tpg:NewQuestHoldingsCaymanLimitedMember2022-12-310001880661tpg:TPHUnitsMember2023-12-310001880661tpg:TPHUnitsMember2023-01-012023-12-310001880661tpg:TPHUnitsMember2022-01-012022-12-310001880661tpg:RPHUnitsMember2023-12-310001880661tpg:RPHUnitsMember2023-01-012023-12-310001880661tpg:RPHUnitsMember2022-01-012022-12-310001880661tpg:TPHUnitsAndRPHUnitsMember2023-12-310001880661tpg:TPHUnitsAndRPHUnitsMember2023-01-012023-12-310001880661tpg:TPHUnitsAndRPHUnitsMember2022-01-012022-12-310001880661tpg:TOGCommonUnitsMember2023-12-310001880661tpg:TOGCommonUnitsMember2023-01-012023-12-310001880661tpg:TOGCommonUnitsMember2022-01-012022-12-310001880661us-gaap:CommonClassAMember2023-01-012023-12-310001880661us-gaap:CommonClassAMember2022-01-012022-12-310001880661tpg:AcquisitionCommonUnitsMember2023-12-310001880661tpg:AcquisitionCommonUnitsMember2023-01-012023-12-310001880661tpg:AcquisitionCommonUnitsMember2022-01-012022-12-310001880661tpg:OtherAwardsMember2023-12-310001880661tpg:OtherAwardsMember2023-01-012023-12-310001880661tpg:OtherAwardsMember2022-01-012022-12-310001880661tpg:TPHUnitsMember2022-12-310001880661tpg:RPHUnitsMember2022-12-310001880661tpg:TOGUnitsMember2022-12-310001880661us-gaap:CommonClassAMember2022-12-310001880661tpg:TOGUnitsMember2023-01-012023-12-310001880661us-gaap:CommonClassAMember2023-01-012023-12-310001880661tpg:TOGUnitsMember2023-12-310001880661us-gaap:CommonClassAMember2023-12-310001880661tpg:AcquisitionCommonUnitsAndTOGCommonUnitsMember2023-12-310001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:OtherLiabilityClassifiedAwardsMember2023-01-012023-12-310001880661tpg:AngeloGordonCoLPAgFundsLPAndAGPartnersLPMembertpg:OtherLiabilityClassifiedAwardsMember2023-12-310001880661tpg:TRTXAwardMember2023-01-012023-12-310001880661tpg:TRTXAwardMember2022-01-012022-12-31tpg:classOfStock0001880661tpg:CommonClassAVotingMember2023-12-310001880661us-gaap:NonvotingCommonStockMember2023-12-310001880661us-gaap:CommonClassBMember2023-01-012023-12-310001880661us-gaap:CommonClassAMember2022-05-102022-05-100001880661us-gaap:CommonClassAMember2022-08-092022-08-090001880661us-gaap:CommonClassAMember2022-11-092022-11-090001880661us-gaap:CommonClassAMember2023-02-152023-02-150001880661us-gaap:CommonClassAMember2023-05-152023-05-150001880661us-gaap:CommonClassAMember2023-08-082023-08-080001880661us-gaap:CommonClassAMember2023-11-072023-11-070001880661us-gaap:CommonClassAMemberus-gaap:SubsequentEventMember2024-02-132024-02-1300018806612023-03-300001880661us-gaap:CommonClassAMember2023-03-300001880661us-gaap:CommonClassBMember2023-03-300001880661tpg:DeborahMessemerMember2023-01-012023-12-3100018806612023-10-012023-12-310001880661tpg:DeborahMessemerMember2023-10-012023-12-310001880661tpg:DeborahMessemerMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2023 |

OR

| | | | | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission file number 001-41222

TPG Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 87-2063362 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

301 Commerce Street, Suite 3300 | 76102 |

Fort Worth, TX | (Zip Code) |

(817) 871-4000

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Class A common stock | TPG | The Nasdaq Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | |

| Large accelerated filer | x | | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | | Smaller reporting company | ¨ |

| | | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the common stock of the Registrant held by non-affiliates as of June 30, 2023 was $1,928.6 million.

As of February 20, 2024, there were 74,762,397 shares of the registrant’s Class A common stock, 8,258,901 shares of the registrant’s nonvoting Class A common stock and 281,657,626 shares of the registrant’s Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement relating to its 2024 annual meeting of the shareholders (the “2024 Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. The 2024 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report may contain forward-looking statements. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects” and similar references to future periods, or by the inclusion of forecasts or projections. Examples of forward-looking statements include, but are not limited to, statements we make regarding the outlook for our future business and financial performance, estimated operational metrics, business strategy and plans and objectives of management for future operations, including, among other things, statements regarding expected growth, future capital expenditures, fund performance, dividends and dividend policy and debt service obligations, such as those contained in “Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy and other future conditions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by any forward-looking statements. Important factors that could cause actual results to differ materially from those in the forward-looking statements include the inability to recognize the anticipated benefits of the acquisition of Angelo Gordon (as defined herein); purchase price adjustments; unexpected costs related to the integration of the Angelo Gordon business and operations; our ability to manage growth and execute our business plan; and regional, national or global political, economic, business, competitive, market and regulatory conditions, including, but not limited to, those described in “Item 1A.—Risk Factors” and “Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this report. Any forward-looking statement made by us in this speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

On November 1, 2023, TPG Inc., TPG Operating Group II, L.P., an indirect subsidiary of TPG Inc., and certain of their affiliated entities (collectively, the “TPG Parties”) completed the acquisition (the “Acquisition”) of Angelo, Gordon & Co., L.P., AG Funds L.P. and AG Partners, L.P. (collectively, the “Angelo Gordon Parties”) pursuant to the terms and subject to the conditions set forth in the Transaction Agreement, dated as of May 14, 2023, by and among the TPG Parties and the Angelo Gordon Parties. Accordingly, the results of TPG Angelo Gordon included in our consolidated results of operations are from November 1, 2023 through December 31, 2023.

Risk Factor Summary

The following is only a summary of the principal risks that may materially adversely affect our business, financial condition, results of operations and cash flows. The following should be read in conjunction with the more complete discussion of the risk factors we face, which are set forth more fully in “Part I. Item 1A. Risk Factors.”

•our dependence on our senior leadership and key investment and other professionals;

•our ability to attract, retain and motivate investment and other key professionals;

•the performance of our funds;

•our ability to raise new funds or capital for our funds and obtain favorable economic terms;

•our ability to incorporate TPG Angelo Gordon into the Company and achieve the intended benefits of the Acquisition;

•our execution of new investment strategies or expansion into new markets and businesses;

•increasing scrutiny from fund investors and regulators on ESG (as defined herein) matters;

•the variability of part of our revenue, earnings and cash flow;

•our funds’ historical returns not being indicative of returns on investing in our Class A common stock;

•the performance of our funds’ portfolio companies;

•our investment in companies based outside of the United States;

•changes in China’s governmental policies and interventions by China’s government in industries in which we are invested;

•our ability to maintain the security of our information and technology networks;

•our ability to manage conflicts of interest, including conflicts of interests relating to our funds’ investment activities, conflicts of interest with our partners, directors and senior advisors, and conflicts of interest that may arise between our public stockholders and our management and certain other affiliates;

•the potential misconduct, fraud or other deceptive practices of our employees, advisors or third-party service providers or our funds’ portfolio companies;

•pending and future litigation and related liabilities and reputational harm;

•clawback or contingent repayment obligations if and when triggered under our funds’ governing agreements;

•the historical pro forma financial information in this report not being predictive of future performance;

•our reliance on exemptions from certain governance requirements as a “controlled company” within the meaning of Nasdaq listing standards;

•our status as a holding company, with our only material asset being our interest in the TPG Operating Group (as defined herein);

•us potentially being deemed an “investment company” under the Investment Company Act (as defined herein);

•the disparity in the voting rights among the classes of our common stock;

•our ability to pay dividends;

•the effect on our share price of the large number of shares eligible for future sale and exchange;

•the acceleration of payments under the Tax Receivable Agreement (as defined herein);

•changes in the debt financing markets or higher interest rates;

•the intense competition in the investment management business;

•climate change and related regulations;

•difficult economic and market conditions;

•the extensive regulation of our businesses and increased regulatory focus on our industry, including proposed legislative changes that would modify the tax treatment of performance allocations or otherwise adversely impact our business model;

•changes in the U.S. political and financial regulatory environment; and

•our structure, which involves complex provisions of U.S. federal tax law.

TERMS USED IN THIS REPORT

As used in this Annual Report on Form 10-K, unless the context otherwise requires, references to:

•“TPG,” “the Company,” “we,” “our,” and “us,” or like terms, refer to TPG Inc. and its consolidated subsidiaries taken as a whole.

•“Acquired Interests” refers to all of the outstanding limited partnership interests in AG OpCo and AG CarryCo (each as defined herein), as well as all the outstanding limited liability company interests in AG GP, LLC and limited partnership interests in AG Partner Investments, L.P. acquired in connection with the Acquisition.

•“Angelo Gordon” refers, collectively, to Angelo, Gordon & Co., L.P. (“AG OpCo”) and AG Funds L.P. (“AG CarryCo”), each a Delaware limited partnership. Following the closing of the Acquisition, we refer to Angelo Gordon as “TPG Angelo Gordon.”

•“Class A common stock” refers to Class A common stock of TPG Inc., which entitles the holder to one vote per share. When we use the term “Class A common stock” in this Annual Report on Form 10-K, we are referring exclusively to such voting Class A common stock and not to “nonvoting Class A common stock.”

•“Class B common stock” refers to Class B common stock of TPG Inc., which entitles the holder to ten votes per share until the Sunset but carries no economic rights.

•“Co-Invest Leverage Facility” refers to the agreement whereby TPG Holdings II Sub, L.P., TPG Holdings I, L.P., TPG Holdings II, L.P., TPG Holdings III, L.P. and certain of our other subsidiaries agreed to guarantee then existing and future secured recourse loans made to eligible employees and certain other participants.

•“Common Unit” refers to a common unit in the TPG Operating Group.

•“Exchange Act” refers to the Securities Exchange Act of 1934, as amended.

•“Excluded Assets” refers to the assets and economic entitlements transferred to RemainCo listed in Schedule A to the master contribution agreement entered into in connection with the Reorganization (as defined herein), which primarily include (i) minority interests in certain sponsors unaffiliated with TPG, (ii) the right to certain performance allocations in TPG funds, (iii) certain co-invest interests and (iv) cash.

•“Founders” refers to David Bonderman and James G. (“Jim”) Coulter.

•“GP LLC” refers to TPG GP A, LLC, the owner of the general partner of TPG Group Holdings.

•“GP Services Credit Facility” refers to the agreement whereby TPG Holdings I, L.P., TPG Holdings II Sub, L.P., TPG Holdings II, L.P., TPG Holdings III, L.P. and certain of our other wholly-owned subsidiaries agreed to guarantee the revolving credit facility entered into between GP Services (as defined herein) and a financial institution.

•“IPO” refers to our initial public offering of Class A common stock of TPG Inc. that was completed on January 18, 2022.

•“nonvoting Class A common stock” refers to the nonvoting Class A common stock of TPG Inc., which has no voting rights and is convertible into shares of Class A common stock upon transfer to a third party as and when permitted by the Investor Rights Agreement.

•“Pre-IPO Investors” refers to certain sovereign wealth funds, other institutional investors and certain other parties that entered into a strategic relationship with us prior to the Reorganization.

•“Promote Unit” refers to a promote unit in TPG Operating Group, which entitles the holder to certain distributions of performance allocations received by TPG Operating Group.

•“Public SPACs” refers to Pace Holdings Corp., TPG Pace Holdings Corp., TPG Pace Tech Opportunities Corp., TPG Pace Beneficial Finance Corp., TPG Pace Energy Holdings Corp., TPG Pace Solutions Corp., TPG Pace Beneficial II Corp. and AfterNext HealthTech Acquisition Corp.

•“RemainCo” refers to, collectively, Tarrant Remain Co I, L.P., a Delaware limited partnership, Tarrant Remain Co II, L.P., a Delaware limited partnership, and Tarrant Remain Co III, L.P., a Delaware limited partnership, which owns the Excluded Assets, and Tarrant Remain Co GP, LLC, a Delaware limited liability company serving as their general partner.

•“Securities Act” refers to the Securities Act of 1933, as amended.

•“Specified Company Assets” refers to TPG general partner entities from which holders of Common Units (including us) received an estimated 20% performance allocation after giving effect to the Reorganization.

•“Sunset” refers to the event that will occur on the date that a majority of the independent directors are elected at the first annual meeting of stockholders (or pursuant to a consent of stockholders in lieu thereof) after the earlier of (i) the earliest date specified in a notice delivered to the Company by GP LLC and its members pursuant to that certain GP LLC limited liability company agreement promptly following the earliest of: (a) the date that is three months after the date that neither Founder continues to be a member of GP LLC, (b) a vote of GP LLC to trigger the Sunset and (c) upon 60-days advance notice, the date determined by either Founder who is then a member of the Control Group to trigger the Sunset, if, following a period of at least 60 days, the requisite parties are unable to agree on the renewal of Mr. Winkelried’s employment agreement or the selection of a new CEO in the event that Mr. Winkelried ceases to serve as our CEO, and (ii) the first day of the quarter immediately following the fifth anniversary of the IPO.

•“Tax Receivable Agreement" refers to the Amended and Restated Tax Receivable Agreement entered into by TPG Inc. and the other parties thereto on November 1, 2023.

•“TPG general partner entities” refers to certain entities that (i) serve as the general partner of certain TPG funds and (ii) are, or historically were, consolidated by TPG Group Holdings.

•“TPG Group Holdings” refers to TPG Group Holdings (SBS), L.P., a Delaware limited partnership that is considered our predecessor for accounting purposes and is a TPG Partner Vehicle and direct owner of certain Common Units and Class B common stock.

•“TPG Operating Group” refers (i) for periods prior to giving effect to the Reorganization (as defined herein), to the TPG Operating Group partnerships and their respective consolidated subsidiaries; (ii) for periods beginning after giving effect to the Reorganization through November 1, 2023, (A) to the TPG Operating Group partnerships and their respective consolidated subsidiaries and (B) not to RemainCo and (iii) for periods after November 1, 2023, to TPG Operating Group II, L.P., a Delaware limited partnership, and its respective consolidated subsidiaries, including TPG Operating Group I, L.P. and TPG Operating Group III, L.P.

•“TPG Operating Group partnerships” refers to TPG Operating Group I, L.P., a Delaware limited partnership formerly named TPG Holdings I, L.P., TPG Operating Group II, L.P., a Delaware limited partnership formerly named TPG Holdings II, L.P., and TPG Operating Group III, L.P., a Delaware limited partnership formerly named TPG Holdings III, L.P.

•“TPG Partner Holdings” refers to TPG Partner Holdings, L.P., a Delaware limited partnership, which is a TPG Partner Vehicle that indirectly owns substantially all of the economic interests of TPG Group Holdings, a TPG Partner Vehicle.

•“TPG Partner Vehicles” refers to, collectively, the vehicles through which the Founders and current and former TPG partners (including such persons’ related entities and estate planning vehicles) hold their equity in the TPG Operating Group, including TPG Group Holdings and TPG Partner Holdings.

•“Transaction Agreement” refers to that certain transaction agreement dated as of May 14, 2023, by and among TPG, the TPG Operating Group, GP LLC, Angelo Gordon and certain of its affiliated entities, as amended on October 3, 2023 and October 31, 2023.

In addition, for definitions of “Gross IRR,” “Net IRR,” “Gross MoM,” “Net IRR,” “Investor Net MoM,” and related terms, see “Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Net Accrued Performance Allocations—Fund Performance Metrics.”

PART I

Item 1. Business

Overview

TPG is a leading global alternative asset manager with $221.6 billion in assets under management (“AUM”) as of December 31, 2023. We have built our firm through more than 30 years of successful innovation and growth, and believe that we have delivered attractive risk-adjusted returns to our clients and established a premier investment business focused on the fastest-growing segments of both the alternative asset management industry and the global economy. We believe that we have a distinctive business approach as compared to other alternative asset managers and a diversified, innovative array of investment platforms that position us well to continue generating sustainable growth across our business.

We primarily invest in complex asset classes such as private equity, credit, real estate and public market strategies, which is distinct from most other asset managers that invest only in traditional asset classes such as stocks, bonds or commodities. We have constructed a high-quality base of assets under management within highly attractive sub-segments of the alternative asset management industry. The strength of our investment performance, our ability to innovate within our business and our focus on strategic, inorganic growth has led to consistent historical growth in our assets under management, all on a scaled infrastructure that gives our business a high degree of operating leverage. From 2019 to December 31, 2023, our assets under management have grown 160.7% from $85.0 billion to $221.6 billion. The following table presents AUM over the last five years:

| | | | | | | | |

| | Assets Under Management |

| | ($ in Billions) |

| 2019 | | $ | 85 | |

| 2020 | | 90 | |

| 2021 | | 114 | |

| 2022 | | 135 | |

| 2023 | | 222 | |

As of December 31, 2023, we employed approximately 1,850 people, including over 650 investment and operations professionals, in offices across 16 countries, providing us with a substantial global footprint and network. Our investment and operations professionals are organized into industry sector teams, which share investment themes across platforms to drive firmwide pattern recognition. Through multiple decades of experience, we have developed an ecosystem of insight, engagement and collaboration across our platforms and products, which currently include over 300 active portfolio companies, over 300 real estate properties and over 5,000 credit positions across more than 30 countries.

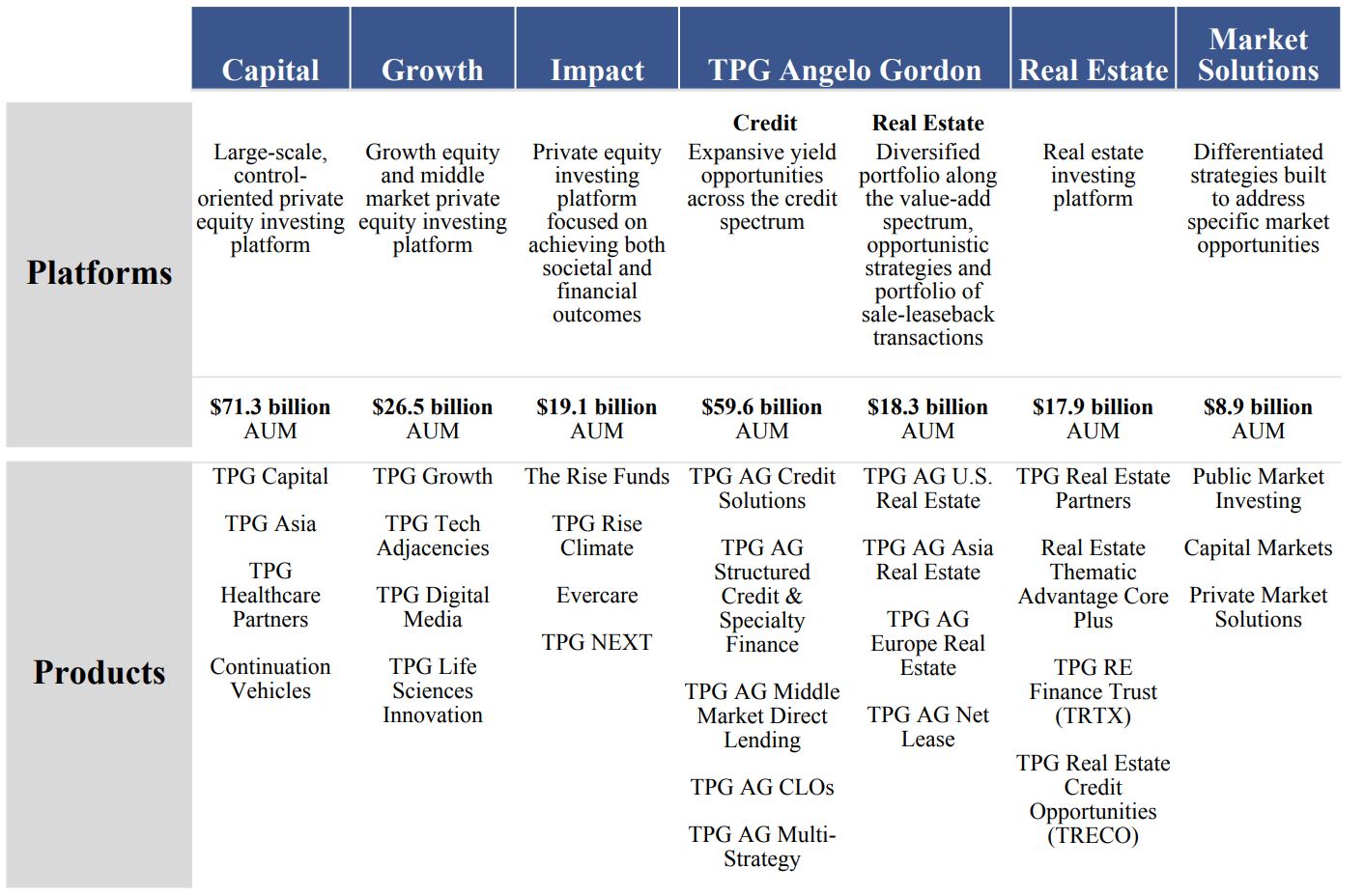

Our firm consists of six multi-strategy investment platforms: (1) Capital, (2) Growth, (3) Impact, (4) TPG Angelo Gordon, (5) Real Estate and (6) Market Solutions. We have developed our investment platforms organically over time by identifying areas where our track record and thematic depth provide opportunities to create differentiated solutions to address market needs. We have also grown inorganically, including through our acquisition on November 1, 2023 of Angelo Gordon, an alternative investment firm focused on credit and real estate investing.

_________________

Note: AUM as of December 31, 2023.

Platforms

Platform: Capital

Our Capital platform is focused on large-scale, control-oriented private equity investments. Our Capital platform funds are organized in four primary products: (1) TPG Capital, (2) TPG Asia, (3) TPG Healthcare Partners and (4) Continuation Vehicles.

The following table presents certain data about our Capital platform as of December 31, 2023 (dollars in billions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| AUM | | Fee-earning AUM | | Active Funds | | Available Capital | | Investment Professionals |

| $ | 71 | | | $ | 39 | | | 10 | | $ | 17 | | | 130 |

Product: TPG Capital

TPG Capital is our North America and Europe-focused private equity investing business, with $41.8 billion in assets under management and 83 investment professionals around the world as of December 31, 2023. TPG Capital seeks to invest through leveraged buyouts and large-scale growth equity investments in market leaders with fundamentally strong business models which are expected to benefit from long-term secular growth trends. We also seek to help our portfolio companies accelerate their growth under our ownership through operational improvements, by investing in organic and inorganic growth, and by leveraging our human capital team to upgrade or enhance our management teams and boards.

Product: TPG Asia

TPG Asia consists of 47 investment professionals focused on pursuing investments in the Asia-Pacific region, including Australia, India, Korea and Southeast Asia, with $21.8 billion in assets under management as of December 31, 2023. Our distributed regional footprint has provided a foundation to pursue the region’s highly attractive investing opportunities with both new and existing products and strategies. We invest through a variety of transaction structures, including through partnerships with large corporations and families.

Product: TPG Healthcare Partners

We established TPG Healthcare Partners, or “THP”, in 2019 to pursue healthcare-related investments, primarily in partnership with other TPG funds. THP provides our limited partners with a dedicated healthcare investment platform that touches all areas of healthcare, including providers, payors, pharmaceuticals, medical devices and healthcare technology.

Product: Continuation Vehicles

Periodically, across our platforms, we identify portfolio companies in which certain of our limited partners would like to remain invested but which we own in a fund nearing the end of its life. In these situations, we have utilized single-asset continuation vehicles (“CVs”) managed by TPG that allow the limited partners who choose to do so to remain invested in a portfolio company beyond the life of the TPG fund that initially invested in the company. CVs are attractive for both our limited partners, who retain ongoing exposure to strong assets, and for TPG, as these vehicles extend the duration of our capital. CVs provide opportunities for TPG to continue creating value for our investors and earning management and performance fees.

Platform: Growth

TPG Growth is our dedicated growth equity and middle market investing vehicle. Our Growth platform provides us with a flexible mandate to capitalize on investment opportunities that are earlier in their life cycle, are smaller in size and/or have different profiles than would be considered for our Capital platform. Our Growth funds are organized in four primary products: (1) TPG Growth, (2) TPG Tech Adjacencies, (3) TPG Digital Media and (4) TPG Life Sciences Innovation.

The following table presents certain data about our Growth platform as of December 31, 2023 (dollars in billions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| AUM | | Fee-earning AUM | | Active Funds | | Available Capital | | Investment Professionals |

| $ | 27 | | | $ | 12 | | | 10 | | $ | 5 | | | 47 |

Product: TPG Growth

TPG Growth is our dedicated growth equity and middle market investing product, with $17.0 billion in assets under management and 47 dedicated investment professionals as of December 31, 2023. TPG Growth seeks to make growth buyout and growth equity investments, primarily in North America and India.

Product: TPG Tech Adjacencies

TPG Tech Adjacencies, or “TTAD”, with $6.7 billion in assets under management as of December 31, 2023, is a product we developed organically to pursue minority and/or structured investments in internet, software, digital media and other technology sectors. Specifically, TTAD aims to provide flexible capital for founders, employees and early investors looking for liquidity, as well as primary structured equity solutions for companies looking for additional, creative capital for growth.

Product: TPG Digital Media

TPG Digital Media, or “TDM”, is a flexible source of capital to pursue opportunities to invest in digital media. TDM seeks to pursue investments in businesses in which we have the opportunity to capitalize on our long history of studying and pursuing content-centric themes.

Product: TPG Life Sciences Innovation

TPG Life Sciences Innovation, or “LSI”, is a new product which will invest in the life sciences sector in novel therapeutics as well as digital health, medical devices, diagnostics, and tech-enabled services. LSI will invest across different therapeutic areas and stages from company creation to IPO, and will leverage TPG’s broad experience in the healthcare sector.

Platform: Impact

Our multi-fund Impact platform pursues both competitive financial returns and measurable societal benefits at scale, harnessing the diverse skills of a differentiated group of stakeholders:

• Y Analytics: A public benefit organization that is wholly owned by TPG and which we founded to provide impact research and rigorous assessment measures for impact investments, and today functions as TPG’s firm-wide ESG and impact performance arm.

• The TPG Rise Global Advisory Board: A group of experienced investors and global thought leaders with a deep personal and professional commitment to driving social and environmental change.

• The TPG Rise Climate Coalition: A partnership between TPG and 28 leading global corporations to identify and share best practices for considering climate solutions investment opportunities through TPG Rise Climate.

Based on our investment strategy, we believe our impact investments can deliver profit and positive impact in tandem. Our Impact funds are organized in four primary products: (1) The Rise Funds, (2) TPG Rise Climate, (3) Evercare and (4) TPG NEXT.

The following table presents certain data about our Impact platform as of December 31, 2023 (dollars in billions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| AUM | | Fee-earning AUM | | Active Funds | | Available Capital | | Investment Professionals |

| $ | 19 | | | $ | 14 | | | 6 | | $ | 5 | | | 60 |

Product: The Rise Funds

The Rise Funds are our dedicated vehicles for investing in companies that generate a demonstrable and significant positive societal impact alongside business performance and strong returns, with $8.7 billion in assets under management and 27 dedicated investment professionals as of December 31, 2023. The Rise Fund’s core areas of focus include climate and conservation, education, financial inclusion, food and agriculture, healthcare and impact services, and invest globally.

Product: TPG Rise Climate

TPG Rise Climate is our dedicated climate impact investing product. TPG Rise Climate has raised $7.3 billion in total commitments, and is innovative in matching significant capital from traditional limited partners with over $2.6 billion in commitments from 28 leading global corporations. In addition to committing capital to the fund, the companies joined TPG in forming the TPG Rise Climate Coalition, an effort focused on identifying and sharing best practices for considering investment opportunities, among the corporate group and more broadly across the TPG Impact platform. TPG Rise Climate’s core areas of focus include energy transition, green mobility, sustainable fuels, sustainable materials and products and carbon solutions.

Product: Evercare

The Evercare Health Fund (“Evercare”) is an emerging markets healthcare fund that is striving to provide affordable, high-quality healthcare in emerging markets. Evercare’s investments are integrated under a common operating platform, The Evercare Group, an integrated healthcare delivery platform in emerging markets across Africa and South Asia, including India, Pakistan, Bangladesh, Kenya and Nigeria.

Product: TPG NEXT

TPG NEXT is designed to support the next generation of diverse alternative asset managers. TPG announced the launch of the TPG NEXT fund in 2022 to seed new managers, strengthen their access to capital, offer business building expertise and provide strategic advisory support to talent that is chronically underrepresented in alternative asset management. TPG NEXT began investing in 2023 and aims to increase the number of diverse-led firms in alternative assets, furthering an effort we began in 2019 with our investments in Harlem Capital and VamosVentures.

Platform: TPG Angelo Gordon

TPG AG Credit

TPG Angelo Gordon’s alternative credit products (collectively referred to as “TPG AG Credit”) are: (1) TPG AG Credit Solutions, (2) TPG AG Structured Credit & Specialty Finance, (3) TPG AG Middle Market Direct Lending, (4) TPG AG Collateralized Loan Obligations (“CLOs”), and (5) TPG AG Multi-Strategy. TPG AG Credit’s capabilities span private and tradeable credit across corporate and asset-backed markets.

The following table presents certain data about our TPG AG Credit platform as of December 31, 2023 (dollars in billions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| AUM | | Fee-earning AUM | | Active Funds | | Available Capital | | Investment Professionals |

| $ | 60 | | | $ | 40 | | | 73 | | $ | 7 | | | 141 |

Product: TPG AG Credit Solutions

TPG AG Credit Solutions, with $12.9 billion in assets under management and 21 investment professionals as of December 31, 2023, invests in stressed, distressed and special situation corporate credit opportunities, primarily in North America and Europe, and can dynamically pivot between the public and private markets. We employ what we believe to be a differentiated, solutions-based approach that is capable of being executed in any market environment. TPG AG Credit Solutions seeks to align with companies, financial sponsors and business owners and to use its structuring skill and capital base to create bespoke, bilaterally-negotiated financing transactions that help resolve complex and idiosyncratic financial challenges. TPG AG Credit Solutions funds may also opportunistically invest in securities acquired at what the investment team believes are discounted prices relative to their intrinsic value and offer the potential for contractual income and/or price appreciation. TPG AG Credit Solutions invests through its Credit Solutions and Essential Housing closed-ended funds, as well as its Corporate Credit Opportunities open-ended fund.

Product: TPG AG Structured Credit & Specialty Finance

TPG AG Structured Credit & Specialty Finance focuses on major non-corporate credit sectors, including consumer, residential and commercial real estate, and specialty lending markets, and also has substantial CLO debt and equity investing capabilities. TPG AG Structured Credit & Specialty Finance invests through Mortgage Value Partners Fund, an open-ended hedge fund, the Asset Based Credit Fund, a closed-ended fund, separately managed accounts (“SMAs”) and AG Mortgage Investment Trust, Inc. (NYSE: MITT) (“MITT”), an externally-managed, publicly traded residential mortgage real estate investment trust focused on investing in a diversified risk-adjusted portfolio of residential mortgage-related assets in the U.S. mortgage market. As of December 31, 2023, TPG AG Structured Credit & Specialty Finance had $15.8 billion in assets under management and 30 investment professionals.

Product: TPG AG Middle Market Direct Lending

TPG AG Middle Market Direct Lending, Twin Brook Capital Partners, focuses on sourcing, underwriting and actively managing a diversified portfolio of middle market, floating rate, senior secured loans, including revolvers, first lien debt and, opportunistically, second lien debt. As a direct lender to private equity sponsored middle market companies, the product focuses on opportunities where we can receive a pricing premium relative to broadly syndicated loans and relies on ongoing borrower support from sponsors. TPG AG Middle Market Direct Lending includes the MMDL closed-ended fund series, as well as a public, non-traded business development company (“BDC”), AG Twin Brook Capital Income Fund

(“TCAP”). As of December 31, 2023, TPG AG Middle Market Direct Lending had $20.6 billion in assets under management and 70 investment professionals.

Product: TPG AG CLOs

TPG AG CLOs, with $8.4 billion in assets under management and 14 investment professionals as of December 31, 2023, invests predominantly in non-investment grade senior secured bank loans. TPG AG issues U.S. CLOs investing predominantly in U.S. dollar-denominated loans, and Euro CLOs investing predominantly in Euro-denominated loans and secured bonds. TPG AG CLOs include performing credit bespoke vehicles, collateralized loan obligation (“CLO”) funds and direct investment in the tranches of Northwoods CLOs.

Product: TPG AG Multi-Strategy

TPG AG Multi-Strategy, with $2.0 billion in assets under management and 6 investment professionals as of December 31, 2023, invests across the breadth of TPG AG Credit, with a geographic focus in the United States and Western Europe. TPG AG Multi-Strategy offers actively managed co-mingled funds, including its Super Fund (“Super Fund”), in addition to bespoke vehicles and various multi-strategy credit funds of one. These funds invest in public and private investment opportunities sourced from across TPG AG Credit, as well as arbitrage strategies, including convertible arbitrage and merger arbitrage. TPG AG Multi-Strategy funds invest in, among other products, corporate loans and bonds; residential, consumer and asset-based loans and securities; hybrid instruments; and derivative securities, including currency and interest rate hedges.

TPG AG Real Estate

TPG Angelo Gordon’s real estate products (collectively referred to as “TPG AG Real Estate”) are (1) TPG AG U.S. Real Estate, (2) TPG AG Asia Real Estate, (3) TPG AG Europe Real Estate, and (4) TPG AG Net Lease. TPG AG Real Estate products in the United States, Asia and Europe primarily focus on the acquisition of equity interests of underperforming and undervalued assets in the United States, Asia and Europe, where we employ our opportunistic and value-add strategies to improve performance. TPG AG Net Lease primarily invests in single tenant commercial real estate acquired in simultaneous sale-leaseback transactions.

The following table presents certain data about our TPG AG Real Estate platform as of December 31, 2023 (dollars in billions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| AUM | | Fee-earning AUM | | Active Funds | | Available Capital | | Investment Professionals |

| $ | 18 | | | $ | 14 | | | 26 | | $ | 7 | | | 85 |

Product: TPG AG U.S. Real Estate

TPG AG U.S. Real Estate, with $6.8 billion in assets under management, manages assets across various product sectors and has been active in many of the major U.S. real estate markets. TPG AG U.S. Real Estate focuses on purchasing what we believe to be underperforming and undervalued real estate assets, where we then execute an active asset management strategy to reposition and stabilize the properties. TPG AG U.S. Real Estate is diversified across property sectors, with a thematic portfolio construction focused on rental residential, industrial, self-storage, life science, student housing and medical office, among other sectors. As of December 31, 2023, TPG AG U.S. Real Estate had 28 real estate investment professionals in New York, Los Angeles and Bethesda focused by region and working with a network of over 90 local operating partners.

Product: TPG AG Asia Real Estate