UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

FOR

THE FISCAL YEAR ENDED

OR

FOR THE TRANSITION PERIOD FROM _______ TO ___________

COMMISSION FILE

NO.

(Exact name of registrant as specified in charter)

| (State or other jurisdiction of incorporation) | (IRS Employer Identification No.) |

(Address of principal executive offices and zip code)

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of each class: | Trading Symbol(s) | Name of each exchange on which registered: | ||

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “small reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

The registrant was not a public company as of June 30, 2023 the last business day of the registrant’s most recently completed second fiscal quarter, and therefore it cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates at such date. The registrant’s common shares began trading on the CBOE on February 23, 2024.

There were

VOCODIA HOLDINGS CORP

TABLE OF CONTENTS TO ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2023

In this Annual Report on Form 10-K, unless otherwise stated or as the context otherwise requires, references to “Vocodia Holdings Corp,” “Vocodia,” the “Company,” “we,” “us,” “our” and similar references refer to Vocodia Holdings Corp, a Wyoming corporation. Our logo and other trademarks or service marks of the Company appearing in this Annual Report on Form 10-K are the property of Vocodia Holdings Corp.

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements represent our expectations, beliefs, intentions, or strategies concerning future events, including, but not limited to, any statements regarding our assumptions about financial performance; the continuation of historical trends; growth strategies; the sufficiency of our cash balances for future liquidity and capital resource needs; the expected impact of changes in accounting policies on our results of operations, financial condition or cash flows; anticipated problems and our plans for future operations; our future financing plans and anticipated needs for working capital; and the economy in general or the future of the food production industry, all of which were subject to various risks and uncertainties. Such statements, when used in this Annual Report on Form 10-K and other reports, statements, and information we have filed with the Securities and Exchange Commission (“SEC”), in our press releases, presentations to securities analysts or investors, in oral statements made by or with the approval of an executive officer, are generally identifiable by use of the words “may,” “will,” “should,” “expect,” “anticipate,” “continue,” “estimate,” “believe,” “intend,” or “project” or the negative of these words or other variations on these words or comparable terminology. However, any statements contained in this Annual Report on Form 10-K that are not statements of historical fact may be deemed to be forward-looking statements. These statements are expressed in good faith and based upon a reasonable basis when made, but there can be no assurance that these expectations will be achieved or accomplished.

This information may involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from the future results, performance, or achievements expressed or implied by any forward-looking statements. These statements may be found under Part I Item 1 “Business” and Part II Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as in other parts of this Annual Report on Form 10-K. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors as described in this Annual Report on Form 10-K generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this Annual Report on Form 10-K will in fact occur. In addition to the information expressly required to be included in this filing, we will provide such further material information, if any, as may be necessary to ensure that the required statements, in light of the circumstances under which they are made, are not misleading.

Although forward-looking statements in this Annual Report on Form 10-K reflect the good faith judgment of our management, forward-looking statements are inherently subject to known and unknown risks, business, economic and other risks and uncertainties that may cause actual results to be materially different from those discussed in these forward-looking statements. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. We assume no obligation to update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this Annual Report on Form 10-K, other than as may be required by applicable law or regulation. Readers are urged to carefully review and consider the various disclosures made by us in our reports filed with the Securities and Exchange Commission (“SEC”) which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operation and cash flows. If one or more of these risks or uncertainties materialize, or if the underlying assumptions prove incorrect, our actual results may vary materially from those expected or projected.

This Annual Report on Form 10-K also contains estimates, projections, and other information concerning our industry, our business, and particular markets, including data regarding the estimated size of those markets. Information that is based on estimates, forecasts, projections, market research, or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market, and other data from reports, research surveys, studies, and similar data prepared by market research firms and other third parties, industry, general publications, government data, and similar sources.

ii

PART I

ITEM 1. BUSINESS

Overview

Vocodia Holdings Corp (“VHC”) was incorporated in the State of Wyoming on April 27, 2021 and is a conversational AI technology provider. Our technology is designed to drive better sales and services for its customers. Clients turn to us for their product and service needs.

We are an AI software company that build practical AI functions and makes them easily obtainable for businesses on cloud-based platform solutions at low costs and scalable to multiagent vast enterprise solutions.

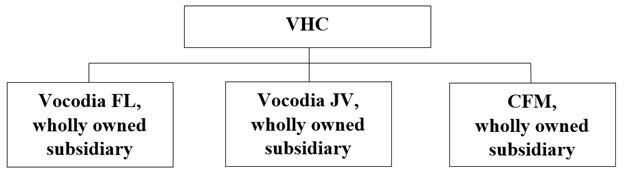

Our operations include three wholly owned subsidiaries: (1) Vocodia FL, LLC, which was incorporated in the State of Florida on June 2, 2021 and manages all of VHC’s human resources and payroll functions, (2) Vocodia JV, LLC, which was incorporated in the State of Delaware on October 7, 2021 and was formed with the intention to conduct any and all joint ventures or acquisitions for VHC, which do not exist as of the date of this report, and (3) CFM, which was incorporated in the State of Florida on November 26, 2019 and is an IT services provider. CFM was formerly owned by James Sposato, who is an officer and director of the Company. CFM was wholly acquired by the Company from Mr. Sposato per the Contribution Agreement dated August 1, 2022. CFM was formerly owned by James Sposato, who is an officer and director of the Company. CFM was acquired by the Company from Mr. Sposato per the Contribution Agreement, dated August 1, 2022. In the Contribution Agreement, Mr. Sposato, as Contributor, has contributed, assigned, transferred and delivered to us, the outstanding capital stock of CFM and we have accepted the contributed shares from the Contributor. As full consideration for the Contribution, we have paid the Contributor consideration in the amount of $10.

We aim to offer corporate clients scalable enterprise AI sales and customer service solutions intended to rapidly increase sales and service, while lowering employment costs.

We seek to enhance rapport and relationship building for customers, which is as necessary component to sales. We believe that there is a positive correlation between AI which sounds similar to a human voice over the phone and better customer rapport and customer service benefits. With our advanced AI, we believe that it will be difficult for customers to distinguish between speaking to a human sales representative and to an AI bot. We believe we can increase customer satisfaction and maximize potential service efficiency for its clients. Our goal is to provide quick training and deployment, potentially unlimited scalability, easy integration with existing corporate platforms and other benefits to our customers from AI’s efficiency.

We strive to help our customers manage budgets and perform better than the high costs of existing sales and service personnel.

1

Corporate History

We were incorporated under the laws of the State of Wyoming on April 27, 2021.

Our principal executive office is located at 6401 Congress Avenue, Suite #160 Boca Raton, FL 33487. Our telephone number is (561) 484-5234. Our website address is https://vocodia.com/ and our general email is sales@vocodia.com. The information contained on our website is not incorporated by reference into this report, and you should not consider any information (nor use the same in deciding whether to purchase our common stock) contained on, or that can be accessed through, our website as part of this report.

A 1-for-20 Reverse Stock Split of our common stock became effective on January 27, 2023. Pursuant to the Reverse Stock Split, every twenty (20) shares of common stock issued and outstanding upon the effectiveness of the Reverse Stock Split was combined and converted into one (1) share of common stock. No fractional shares were issued in connection with the Reverse Stock Split but was rounded up to the nearest whole number. The Reverse Stock Split had no effect on the authorized amount or par value of the common stock, preferred stock, or the currently issued and outstanding series of preferred stock and presently issued and outstanding preferred stock.

Our Organizational Structure

As of the date of this report, we employ 13 personnel, all of whom are contractors, in connection with its business operations. Our organizational structure currently consists of three executive officers (the Chief Executive Officer, the Chief Financial Officer, and Chief Product Officer), we have four personnel in operations who work directly with the Chief Executive Officer, a software engineer and database engineer who work directly with the Chief Technology Officer, and a bookkeeper and part-time advisor in the finance and accounting department.

Significant Products & Services

We are a conversational AI software developer and provider. Our mission is to maximize value in communications between organizations and their consumer bases from “hello” to “goodbye”. Our goal is to be the conversational leader in corporate and organizational, agenda driven communications, to drive convenience, scale, and empowerment, while reducing operational costs and risk.

We offer our corporate clients scalable enterprise-level AI sales and customer service solutions which allow for AI sales representatives to reduce human labor costs and responsibilities while increasing the reach and efficacy of human-led, purposeful, agenda driven and conversational communications. We deliver our patent pending conversational AI software in the form of Digital Intelligent Sales Agents, which we refer to as DISAs® (the “DISAs”). The DISAs are built with AI software programmed for the DISAs to sound and feel human and to perform business tasks that require humans to converse with one another effectively, and thus to provide the best representation for each of our customers’ businesses.

We have developed and released its first software product and platform, which we refer to as “DISA”, a humanized conversational AI technology, that can complete each stage of the conversational aspect of the sales process, business-to-business (“B2B”) and business-to-consumer (“B2C”).

Our prospects for direct software sales are any enterprise clients who are in the phone and call center markets. The initial sales targets were call centers who needed to replace poor performing staff in the pre-Covid-19 era. Now, our sales targets have shifted to filling empty seats in the call centers. Our technology powers our virtual agent, the DISA. In the current marketplace, we consider any corporate client with a 50-seat call center at a telephony location a potential sales client. These potential clients span many industry verticals, including but not limited to, health, solar, employee retention credit, insurance, recruiting and real estate, automotive, cruise lines and hospitality and lodging.

Our AI sales agents not only sell and serve prospects and customers, but also gather and report robust intelligence from customers and the marketplace. Vocodia’s DISAs are programmed to instantly answer customer service calls and to upsell and provide personalized customer care.

2

Our DISAs have been programmed to provide the marketplace with an alternative to human sales representatives in the function of (1) sales; (2) customer service; (3) supportive agency; (4) intermediary communications; and (5) alerts with automated transfers and queuing. The DISAs are tailored to serve the specific requirements of each of our customers and are delivered via our proprietary platform.

We view our DISAs as the total solution for those in need of sales and customer service automation, which provides the marketplace alternative to a role that has primarily been serviced by humans in the sales and customer service departments, in part or in whole, to increase our clients’ revenues and lower costs, providing them with the ability to produce campaigns fast and scale them up or down as necessary.

Our AI software is intended to provide a solution for operational costs and efficiency deficits by improving business automation and reducing the inefficiencies caused by human limitations. Our motto is to “Go Beyond Human”, with AI alternative of human salespeople and customer service representatives. We aim to lower costs associated with sales campaigns that rely on humans and provide scalability of agent quantity, style, mission, and other personalization at varying levels for each organization’s needs.

We have developed and released its first software product and platform, which we refer to as “DISA”, a humanized conversational AI technology, that can complete each stage of the conversational aspect of the sales process, business-to-business (“B2B”) and business-to-consumer (“B2C”).

Our prospects for direct software sales are any enterprise clients who are in the phone and call center markets. The initial sales targets were call centers who needed to replace poor performing staff in the pre-Covid-19 era. Now, our sales targets have shifted to filling empty seats in the call centers. Our technology powers our virtual agent, the DISA. In the current marketplace, we consider any corporate client with a 50-seat call center at a telephony location a potential sales client. These potential clients span many industry verticals, including but not limited to, health, solar, employee retention credit, insurance, recruiting and real estate, automotive, cruise lines and hospitality and lodging.

Our AI sales agents not only sell and serve prospects and customers, but also gather and report robust intelligence from customers and the marketplace. Vocodia’s DISAs are programmed to instantly answer customer service calls and to upsell and provide personalized customer care.

We have achieved a new milestone. Our telephonic switch, connecting our conversational AI to the world via telephone, can now manage and connect a single DISA to 20,000 simultaneous unique telephone conversations (unique customers). We call this quantity of active telephone lines, “Clusters”.

We can add on new Clusters in 4 to 5 minutes, and to date, we have not identified a limit of Clusters managing simultaneous conversations. Using Voice Over Internet Protocol (VOIP) and our proprietary switch, customers can dial in on 20,000 lines and be answered by our AI representatives, as well as dial out and initiate full sales and customer service functions. The advantage of this technology is that organizations may now manage surges of interest, customer service, or emergencies, without backlog or hold times.

We believe this scale of “telephone switch clusters” is a unique service in the world, providing benefit to organizations in unanticipated surges of customer services, sales and information exchange demand.

Market Overview

Growth for most businesses means increasing sales and services. However, growth is often limited by available resources, such as customers and employees. Planning, recruiting, training and retaining employees to focus on growth (sales), and retaining such employees (attrition), is typically expensive and costs can be prohibitive. Further, labor costs can be a considerable percentage of overall costs for running the business as they include, without limitation, employee wages, benefits, payroll or other related taxes. There may be no relief for businesses faced with the necessary employment costs of sales agents and customer service personnel.

| ● | Voice Quality: We provide AI with high-level voice quality and seeks to deliver superior service in the marketplace. |

3

| ● | Quality Sales: We use the following sales and marketing strategy: Prospects – Qualifies – Closes – Processes Orders – Upsells. Our DISAs are able to generate more leads and more transfers to clients so they can sell or upsell their new leads and transfers on their products. We believe that our customers can become more efficient by hiring DISA “fronters”, rather than traditional “fronters”. These traditional human “fronters” have served as the driving force in call centers making 150 or so calls daily to qualify potential clients. Once qualified, they then transfer the call to another department of the call center which handles the final transactional element of the sales call. The fronter position is the high turnover, low pay, very hard to hire, part for call centers that are the costliest and least productive. We automate this part of the process using AI to make these calls, instead of the human fronters. In addition, AI only has to be trained once, does not take vacation, can call 24/7, and could cost less than human fronters. Thereby, corporate clients can receive the same level of sales expected from their top 85% of employees. We deliver effective, dependable, scalable to the hour, low variance sales and customer service solutions. |

| ● | Affordability: AI sales agents (also known as AI bots) cost less than one-third of human sales agents without human issues that tend to affect the processes, human resources and bottom line. |

| ● | Scalability: Our software is cloud-based and Application Programming Interface (“API”)-friendly, which is interoperable with third-party platforms. We offer companies scalable enterprise-level AI sales and customer service solutions which reduce human labor costs and responsibilities while increasing the reach and efficacy of human led, purposeful, agenda driven and conversational communications. |

| ● | Compliance: DISAs parameters are set by our clients’ needs and uploaded data. These inputs can include, but are not limited to, recordings, scripts and rebuttals supplied by a respective client. We use our clients’ data and trains their respective DISAs to converse with prospective customers, qualify them, and then transfer the call to a “closer” to sell to the customer. The AI/DISA can only say what they are trained and programmed to say. We believe this will lead to higher level of compliance, avoiding impromptu human errors which will not occur for our DISAs. | |

| ● | Speedy Training: The AI can be trained in 3 days with: recordings of existing sales calls; and sales script for baseline and target goals. AI bots also continue to learn on the job from call interactions, thus machine learning progressively improves over time. |

Strategy

Technology

We believe that we have built, and will continue to build, AI conversational systems that sound virtually the same as humans. Proprietary software and systems have been developed in-house from scratch with streamlined integration and a growing number of customer relationship managements (“CRMs”) and platforms all over the world. Our software uses Artificial Intelligence, Augmented Intelligence, Natural Language Processing and Machine Learning to provide a robust, continuously learning engine which can perform multiagent functions simultaneously. Our software is cloud-based, permitting easy API integration with most systems and platforms commonly used by businesses today.

Products

We have developed and released its first software product and platform, which we refer to as “DISA”, a humanized conversational AI technology, that can complete each stage of the conversational aspect of the sales process, business-to-business (“B2B”) and business-to-consumer (“B2C”).

Our prospects for direct software sales are any enterprise clients who are in the phone and call center markets. The initial sales targets were call centers who needed to replace poor performing staff in the pre-Covid-19 era. Now, our sales targets have shifted to filling empty seats in the call centers. Our technology powers our virtual agent, the DISA. In the current marketplace, we consider any corporate client with a 50-seat call center at a telephony location a potential sales client. These potential clients span many industry verticals, including but not limited to, health, solar, employee retention credit, insurance, recruiting and real estate, automotive, cruise lines and hospitality and lodging.

Our AI sales agents not only sell and serve prospects and customers, but also gather and report robust intelligence from customers and the marketplace. Vocodia’s DISAs are programmed to instantly answer customer service calls and to upsell and provide personalized customer care.

4

Development Strategy

We plan three phases of development to become the largest and most profitable AI service provider, globally, in the next five years:

| ● | Integrate AI sales agents and customer service offerings directly into existing enterprises and then via CRM applications; |

| ● | Increase sales of AI-assisted workflow to more enterprises in a variety of functions and industries (e.g., food ordering, administration, accounting, bookkeeping and human resources). Grow revenue streams, including based upon market pricing where our DISAs can perform at advantageous margins such as notable efficiencies or less operational costs to achieve the same function to the satisfaction of the end customer (acquisitions may become a significant part of our growth strategy, but at this time we have not identified any specific candidates that meet our objectives); and |

| ● | Integrate personal AI assistants to individuals for overall life assistance, integrated with existing sales and other AI bots, to serve members of the community. |

Acquisition Strategy

Our strategy includes seeking to selectively pursue acquisitions, including companies with revenue streams where our DISAs can perform at advantageous margins with noticeable efficiency or less operational costs to achieve the same function. We will concentrate on several important priorities in evaluating potential acquisition candidates, including the key considerations and objectives we hope to achieve, which are listed below:

| ● | acquiring beneficial technology or use; | |

| ● | accelerating market share; | |

| ● | increasing revenue; | |

| ● | enhancing efficiencies in product and service delivery; | |

| ● | identifying and addressing possible threats to our organization; | |

| ● | acquiring access to targeted and specified client base; | |

| ● | reducing client acquisition costs by reducing our demands on resources and time (opportunity costs); | |

| ● | acquiring client bases from companies who have service relationships with consumers and acquisitions of companies with or without offerings of similar services; | |

| ● | reducing our client acquisition costs, preserving going rates of such services, and extending our wrapped services to such client base; and | |

| ● | maintaining our dynamic pricing thereby potentially creating greater value opportunities and allows us to minimize market price arbitrage to maximize profit potential. |

Management and Operating Strategy

Our management is market-receptive: as a new technology company, we seek to continuously identify new markets as well as industries where our services would be beneficial to potential customers. We believe that our technologies offer businesses and consumers significant advantages, but our technology is not yet generally recognized. We remain open to discovering new opportunities to offer our technology solutions.

5

We believe that we have an attractive operating model due to the scalability of our AI platform, the recurring nature of our revenue (Software-as-a Service (“SaaS”)) and the potentially high operating margins. We rely on conversions (sales) to generate increased free cash flow. Conversions happen for us when our clients use our services to sell their products/services to their customers. Our operational structure and AI focus allow us to convert enterprise clients in their call center environments (allowing us to rapidly convert clients in a cost-effective manner).

Given the fixed-cost nature of our technology, DISAs allow us to scale our solutions quickly with low marginal costs. These DISAs can pitch and close, as well as manage full customer service operations, in high data interactive demand-based industries, while providing a full human conversation experience to human customers. We offer our customers a contract term of 12 months, with a monthly fee of $1,495 per DISA per month. Additionally, we offer custom setup for a fee to begin building a DISA for a client (i.e., one-time setup fee for each client campaign). We believe that our recurring revenue, combined with our robust sales pipeline and enterprise customer base, will continue to contribute to our long-term growth and strong operating margins, giving us flexibility to allocate capital for our continued success.

Growth Strategy

We believe that we are well positioned for continued growth across the various markets in the call center space. Our strategy for achieving growth includes the following:

Continue to innovate

We believe a significant opportunity exists to enhance our technology platform and analytics using our vast database. We intend to expand our technology services offerings to capitalize on the evolving call center and customer service environment. Our investments in human capital, technology and services capabilities position us to continue to pursue rapid innovation. Examples of our recent innovations include upgrading our own proprietary switch. Our platform depends on phone switch capability (generally voice over internet protocol switches) to generate the actual connection from AI to the customer on the outside. Thus, we are dependent on outside telecom switches and infrastructure to manage the speed of our connection pace. This dynamic creates operational risk, due to the reliance of each switch provider’s technology and infrastructure limits. The bulk of our challenges come from switch uncertainty. Therefore, our goal is to improve our own company-controlled switch, which is critical to our economic health, growth and can facilitate easier delivery of services provided in each software sale. We believe this development would provide us with switch independence, allowing us to obtain more control, efficiency and certainty of delivery while lowering internal costs and managing traffic to external, non-company managed switches. The benefits of building our own switch allows us to scale faster in the quantity of software licenses, the variety of industries and verticals served, the independent scale of service utilized by each individual software licensee (end user), and the quantity of connections made by the hour.

Expand portfolio through strategic acquisitions

We have developed an internal capability to source, evaluate and integrate acquisitions that have created value for our stockholders. We plan to target strategic acquisitions subsequent to the closing of this initial public offering, but we have not currently entered into any agreements for the acquisition of significant assets, businesses or companies. While there is no guarantee that any acquisition will be completed, successful acquisitions may bring a collection of complimentary technology and existing revenue to us. We also plan to continue to pursue strategic acquisitions to grow our platform and enhance our ability to provide more services to our clients. We also expect to seek favorable commercial opportunities, primarily in the areas of technological platforms, data suppliers and consulting services providers.

Customers

We have a diversified pipeline of potential clients. Current clients include health insurance providers, health insurance recruiting new agents, employee retention credits, solar, real estate recruitment and real estate new clients. Through the development of our proprietary switch (as described below) and technical team, we have the ability to scale our DISAs over time. We also intend to scale our client base by strategically adding new sales development personnel and customer service and support team members. We believe that we are in the early stages of penetrating this expanding market with our DISA technology platform. Key elements of this strategy include:

| ● | widely commercializing this new humanized conversational AI platform in the marketplace; |

| ● | increasing the enterprise client usage by increasing the number of DISAs per client; |

| ● | adding multi-channel capabilities to our platform in the form of text message, voicemail, social media (such as LinkedIn), etc. to increase connection rates; and |

| ● | acquiring new strategic partners who bring enhanced complimentary technology and revenue to help us increase market share. |

6

We are in formal negotiations with SEDENA – Secretaría de la Defensa Nacional (The National Defense Department of Mexico) – to provide services of AI driven information and emergency services. We have initiated a Spanish library creation of SEDENA’s AI conversation engine to fulfill this potential arrangement. We believe that the launch of our services with SEDENA will exemplify case use of citizen warnings, alerts and intelligence gathering for other government agencies and municipalities. The negotiations with SEDENA are ongoing and we cannot assure you that we will be able to reach a definitive agreement with respect to the arrangement.

We have also recently completed the approved build-out of a sales DISA for Vertical Merchant Solutions (“VMS”), a large merchant services credit card processing provider. VMS is a pre-release client under agency capacity and is preparing to expand its operations with our technology in 2024. VMS has indicated interest in exclusive software licensing for the merchant services industry.

Competition

We operate in a competitive market with many competitors. The artificial intelligence and customer service market opportunity is large, and many companies compete in these sectors.

We are in the humanized conversational AI market. We are specifically in the call center market, changing the way call centers do business. We help fill the empty seats in call centers.

We are unique in the AI sector in that it has client service systems which allow for quicker delivery than competitors of partial or full replacement humans in conversation-dependent job functions. We use our proprietary augmented and AI software to match, duplicate or reimagine specific conversation-dependent job functions. We create a unique system of individual agents for each customer. We also have a proprietary deployment platform which allows for agenda-driven conversations to be connected from ‘computer’ to humans over telephonic networks. Further, each conversation is recorded and timestamped, creating a deliverable recording and transcript of each exchange between computer and human client. Our greatest differentiator is the ability to scale up or down the quantity of human equivalent agents to meet client demands. Our platform permits speedy delivery, cost effective alternatives to traditional sales, marketing and market intelligence. We use agenda-driven, consumer-targeted engagement campaigns. We believe that our software and platform provides significant benefits to call centers, both commercial exchange services and independent internal call centers, regardless of their size.

Trademarks and Patents

On August 1, 2022, Mr. Podolak and Mr. Sposato, each an officer and director of the Company, assigned to the Company (the “Parties”) significant intellectual property pursuant to a Bill of Sale and Assignment entered into by the Parties (“Bill of Sale and Assignment”). The consideration for the assignment was 300,000 shares of the Company’s common stock issued on January 5, 2023. Mr. Podolak and Mr. Sposato each received 150,000 shares, respectively. The intellectual property consists of various systems, software and other core technology used in our business and operations.

We currently have one outstanding patent application with the U.S. Patent and Trademark Office on our technology and processes.

Sales and Marketing

We intend to use the following sales and marketing strategy: Prospects – Qualifies – Closes – Processes Orders – Upsells. Our DISAs are able to generate more leads and more transfers to clients so they can sell or upsell their new leads and transfers on their products. We believe that our customers can become more efficient by hiring DISA “fronters”, rather than traditional “fronters”. These traditional human “fronters” have served as the driving force in call centers making 150 or so calls daily to qualify potential clients. Once qualified, they then transfer the call to another department of the call center which handles the final transactional element of the sales call. The fronter position is the high turnover, low pay, very hard to hire, part for call centers that are the costliest and least productive. We automate this part of the process using AI to make these calls, instead of the human fronters. In addition, AI only has to be trained once, does not take vacation, can call 24/7, and could cost less than human fronters. Thereby, corporate clients can receive the same level of sales expected from their top 85% of employees. We intend to deliver effective, dependable, scalable to the hour, low variance sales and customer service solutions.

Government Regulation

We are subject to a variety of domestic and foreign laws and regulations in the United States and abroad involving matters that are important to (or may otherwise impact) our various websites, such as broadband internet access, online commerce, privacy and data security, advertising, intermediary liability, consumer protection, taxation, worker classification and securities compliance. These domestic and foreign laws and regulations, which in some cases can be enforced by private parties in addition to government entities, are continually evolving and can be subject to significant change. As a result, the application, interpretation and enforcement of these laws and regulations (and any amended, proposed or new laws and regulations) are often uncertain, particularly in the Internet industry, and may vary from jurisdiction to jurisdiction and over time, which could result in conflicts with the current policies and practices of our websites.

7

Because we conduct substantially all of our business on the Internet, we are particularly sensitive to laws and regulations that could adversely impact the popularity or growth in use of the Internet and/or online products and services generally, restrict or otherwise unfavorably impact whether or how we may provide our products and services, regulate the practices of third parties upon which we rely to provide our products and services and/or undermine an open and neutrally administered Internet access. For example, in December 2017, the U.S. Federal Communications Commission adopted the Restoring Internet Freedom Order. This order, which was released in January 2018 and took effect in June 2018, reversed net neutrality protections in the United States that had been in place since 2015, including the repeal of specific rules against blocking, throttling or “paid prioritization” of content or services by Internet service providers. Also, Section 230 of the Communications Decency Act of 1996 (“Section 230”), which generally provides immunity for website publishers from liability for third party content appearing on their platforms and the good faith removal of third party content from their platforms that they may deem obscene or offensive (even if constitutionally protected speech), since its adoption has been (and continues to be) subject to a number of challenges. The immunities conferred by Section 230 could also be narrowed or eliminated through amendment, regulatory action or judicial interpretation. In 2018, the U.S. Congress amended Section 230 to remove certain immunities and most recently, in 2020, various members of the U.S. Congress introduced bills to further limit Section 230, and a petition was filed by a Department of Commerce entity with the Federal Communications Commission to commence a rulemaking to further limit Section 230. Any future adverse changes to Section 230 could result in additional compliance costs for us and/or exposure for additional liabilities.

Because we receive, store and use a substantial amount of information received from or generated by our users and subscribers, we are also impacted by laws and regulations governing privacy, the storage, sharing, use, processing, disclosure and protection of personal data and data security, primarily in the case of our operations in the United States and the European Union and the handling of personal data of users located in the United States and the European Union. Recent examples of comprehensive regulatory initiatives in the area of privacy and data security include a comprehensive European Union privacy and data protection reform, the GDPR, which became effective in May 2018. The GDPR, which applies to certain companies that are organized in the European Union or otherwise provide services to (or monitor) consumers who reside in the European Union, imposes significant penalties (monetary and otherwise) for non-compliance, as well as provides a private right of action for individual claimants. The GDPR will continue to be interpreted by European Union data protection regulators, which may require us to make changes to our business practices and could generate additional risks and liabilities. The European Union is also considering an update to its Privacy and Electronic Communications Directive to impose stricter rules regarding the use of cookies.

In addition, in October 2015, the European Court of Justice (“ECJ”) invalidated the U.S.-EU Safe Harbor framework that had been in place since 2000 for the transfer of personal data from the European Economic Area (the “EEA”) to the United States, and on July 16, 2020, the ECJ invalidated the EU-U.S. Privacy Shield as an adequate safeguard when transferring personal data from the EEA to the U.S. These regulations continue to evolve and may ultimately require us to devote resources towards compliance and/or make changes to our business practices to ensure compliance, all of which could be costly. Also, the exit from the European Union by the United Kingdom could result in the application of new and conflicting data privacy and protection laws and standards to our operations in the United Kingdom and our handling of personal data of users located in the United Kingdom. At the same time, many jurisdictions abroad in which we do business have already or are currently considering adopting privacy and data protection laws and regulations.

Moreover, while multiple legislative proposals concerning privacy and the protection of user information are being considered by the U.S. Congress and various U.S. state legislatures, certain U.S. state legislatures have already enacted privacy legislation, one of the strictest and most comprehensive of which is the California Consumer Privacy Act of 2018, which became effective on January 1, 2020 (the “CCPA”). The CCPA provides new data privacy rights for California consumers, and restricts the ability of certain of our websites to use personal California user and subscriber information in connection with their various products, services and operations. The CCPA also provides consumers with a private right of action for security breaches, as well as provides for statutory damages. In addition, on November 3, 2020, California voters approved Proposition 24, which amends certain provisions of the CCPA and becomes effects January 1, 2023, will further restrict the ability of certain of our websites to use personal California user and subscriber information in connection with their various products, services and operations and/or impose additional operational requirements on such websites. Lastly, the U.S. Federal Trade Commission has also increased its focus on privacy and data security practices, as evidenced by the first-of-its-kind, $5 billion dollar fine against a social media platform for privacy violations in 2019. As a result, we could be subject to various private and governmental claims and actions in this area.

As a provider of certain subscription-based products and services, we are also impacted by laws or regulations affecting whether and how our websites may periodically charge users for membership or subscription renewals. For example, the European Union Payment Services Directive, which became effective in 2018, could impact the ability of certain of our websites to process auto-renewal payments for, as well as offer promotional or differentiated pricing to, users who reside in the European Union. Similar laws exist in the U.S., including the federal Restore Online Shoppers Confidence Act and various U.S. state laws, and legislative and regulatory enactments or amendments are under consideration in a number of U.S. states.

8

We are also sensitive to the adoption of new tax laws. The European Commission and several European countries have recently adopted (or intend to adopt) proposals that would change various aspects of the current tax framework under which certain of our European websites are taxed, including proposals to change or impose new types of non-income taxes (including taxes based on a percentage of revenue).

We are also subject to laws, rules and regulations governing the marketing and advertising activities of our various websites conducted by or through telephone, email, mobile digital devices and the Internet, including the Telephone Consumer Protection Act of 1991, the Telemarketing Sales Rule, the CAN-SPAM act and similar state laws, rules and regulations, as well as local laws, rules and regulations and relevant agency guidelines governing background screening.

Further, all of our websites could subject to the Americans with Disabilities Act (the “ADA”). The ADA does not explicitly address online compliance. With no specific coverage under the law, it usually falls to the courts to determine how ADA standards apply to websites-or whether they do at all.

Listing on Cboe BZX Exchange, Inc.

Our Common Stock, Series A Warrants and Series B Warrants are listed on the Cboe BZX Exchange, Inc. (the “CBOE”) under the symbols “VHAI,” “VHAI+A” and “VHAI+B, respectively.

Legal Proceedings

From time to time, we may be involved in various disputes and litigation matters that arise in the ordinary course of business.

The Company received a letter dated August 28, 2023, from an attorney hired on behalf of a former employee of the Company. This former employee offered her resignation, which was accepted on July 12, 2023. This letter contains allegations that the former employee was sexually harassed and terminated wrongfully by the Company. The Company is of the opinion that allegations in this letter lack merit. The former employee recently filed a charge with the Equal Employment Opportunity Commission and the Fair Employment Practices Agencies (EEOC/FEPA) alleging discrimination based on sex and retaliation, among other specific allegations including disparate impact/intent and/or treatment and discrimination/harassment/retaliation based on being a female. She also claims she was subjected to a sexually hostile environment. The Company has reported this matter to its insurance carrier and outside counsel has been engaged. The Company denies liability and intends to continue to vigorously defend any action, although the probability of a favorable or unfavorable outcome is difficult to estimate as of this date. The result or impact of such allegations are uncertain, including whether or not they could result in damages and/or awards of attorneys’ fees or expenses.

Property

We are the lessee in a 5-year and 4-month commercial lease agreement that commenced on August 1, 2021 and will expire on November 20, 2026, unless otherwise terminated by Vocodia or the lessor. The leased property is office space located at 6401 Congress Avenue, Suite #160, Boca Raton, Florida. The lessor to the agreement is Catexor Limited Partnership-I, a Florida limited partnership.

Employees

As of December 31, 2023, we have a total of 13 personnel, all of whom are contractors, in connection with its business operations.

Available Information

Our website address is https://vocodia.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q (when filed), Current Reports on Form 8-K, any amendments to those reports, proxy and registration statements filed or furnished with the SEC, are available free of charge through our website. We make these materials available through our website as soon as reasonably practicable after we electronically file such materials with, or furnish such materials to, the SEC. The reports filed with the SEC by our executive officers and directors pursuant to Section 16 under the Exchange Act are also made available, free of charge on our website, as soon as reasonably practicable after copies of those filings are provided to us by those persons. These materials can be accessed through the “Investor Relations” section of our website. The information contained in, or that can be accessed through, our website is not part of this Annual Report on Form 10-K.

9

ITEM 1A. RISK FACTORS

Our business is subject to many risks and uncertainties, which may affect our future financial performance. If any of the events or circumstances described below occur, our business and financial performance could be adversely affected, our actual results could differ materially from our expectations, and the price of our securities could decline. The risks and uncertainties discussed below are not the only ones we face. There may be additional risks and uncertainties not currently known to us or that we currently do not believe are material that may adversely affect our business and financial performance. The statements contained in this Annual Report on Form 10-K that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our securities could decline, and investors in our securities may lose all or part of their investment.

Risks Related to Our Business - General

We will need to raise additional capital to expand our business to meet our long-term business objectives. We have limited revenues and we cannot predict when we will achieve significant revenues and sustained profitability.

We have limited revenues and cannot definitively predict when we will achieve significant revenues and sustained profitability. We do not anticipate generating significant revenues and execute our business strategy and operations, of which we can give no assurance. We are unable to determine when we will generate significant revenues from our operations. We cannot predict when we will achieve profitability, if ever. Our inability to become profitable may force us to sell certain of our websites, reduce operations or reduce our staff. Furthermore, we cannot assure you that profitability, if achieved, can be sustained on an ongoing or long-term basis.

We require additional capital to support our present business plans and our anticipated business growth, and such capital may not be available on acceptable terms, or at all, which would adversely affect our ability to operate.

We will require additional funds to further develop our business plan. Based on our current operating plans, we plan to use approximately $500,000 in capital to fund our acquisitions of websites, technologies or other assets (as of the date of this report, we have no agreements in place to make any acquisitions), approximately $1,500,000 for research and development, and approximately $2,350,000 for sales and marketing, working capital and general corporate purposes. We may choose to raise additional capital beyond these amounts in order to expedite and propel growth more rapidly. We can give no assurance that we will be successful in raising any additional funds. Additionally, if we are unable to generate sufficient revenues from our sales and operating activities, we may need to raise additional funds, doing so through debt and equity offerings, in order to meet our expected future liquidity and capital requirements, including capital required for operations. Any such financing that we undertake will likely be dilutive to current stockholders.

We intend to continue to make investments to support our business growth, including acquiring additional assets. In addition, we may also need additional funds to respond to other business opportunities and challenges, including our ongoing operating expenses, protecting our intellectual property, and enhancing our operating infrastructure. While we may need to seek additional funding for such purposes, we may not be able to obtain financing on acceptable terms, or at all. In addition, the terms of our financings may be dilutive to, or otherwise adversely affect, holders of our common stock. We may also seek to raise additional funds through arrangements with collaborators or other third parties. We may not be able to negotiate any such arrangements on acceptable terms, if at all. If we are unable to obtain additional funding on a timely basis, we may be required to curtail or terminate some or all our business plans.

We cannot predict our future capital needs and we may not be able to secure additional financing.

We will need to raise additional funds in the future to fund our working capital needs and to fund further expansion of our business. We may require additional equity or debt financings, collaborative arrangements with corporate partners or funds from other sources for these purposes. No assurance can be given that necessary funds will be available for us to finance our development on acceptable terms, if at all. Furthermore, such additional financings may involve substantial dilution of our stockholders or may require that we relinquish rights to certain of our technologies or products. In addition, we may experience operational difficulties and delays due to working capital restrictions. If adequate funds are not available from operations or additional sources of financing, we may have to delay or scale back our growth plans.

10

Our independent auditors concurred with our management’s assessment that raises substantial doubt as to our ability to continue as a going concern.

Management has determined and has stated in the notes to the Company’s 2023 and 2022 Consolidated Financial Statements that we have suffered recurring losses from operations that raise substantial doubt about our ability to continue as a going concern, which are still present. Our independent auditors concurred with our management’s assessment that raises substantial doubt as to our ability to continue as a going concern.

If we fail to retain certain of our key personnel and attract and retain additional qualified personnel, we might not be able to pursue our growth strategy.

Our future success will depend upon the continued services of Brian Podolak, our Chief Executive Officer, Scott Silverman, our Chief Financial Officer, James Sposato, our Chief Technology Officer, and other members of our key management team and our consultants. We especially consider Mr. Podolak to be critical to the management of our business and operations and the development of our strategic direction. Though no individual is indispensable, the loss of the services of these individuals could have a material adverse effect on our business, operations, revenues or prospects. We do not currently maintain key man life insurance on the lives of these individuals. Our future success will also depend on our ability to identify, hire, develop, motivate and retain highly skilled personnel. Competition in our industry for qualified employees is intense, and our compensation arrangements may not always be successful in attracting new employees and/or retaining and motivating our existing employees. Future acquisitions by us may also cause uncertainty among our current employees and employees of the acquired business, which could lead to the departure of key individuals. Such departures could have an adverse impact on the anticipated benefits of an acquisition.

Our Chief Financial Officer is currently employed on a part-time basis.

Our Chief Financial Officer, Scott Silverman, is a consultant who works with other small, private companies as chief financial officer and may not commit his full time to our affairs, which may result in a conflict of interest in allocating his time between our business and the other businesses. Mr. Silverman intends to spend at least 20-30 hours per week working on our matters, although he is not obligated to contribute any specific number of his hours per week to our affairs. If other business affairs require Mr. Silverman to devote a greater portion of his time and attention, it could limit his ability to devote time to our affairs and could have a negative impact on our ability to expand our business or could cause us to experience delays in the processing and preparation of our financial information which is necessary for the timely filing our financial reports with the SEC. Failure to file SEC disclosures in both an accurate and timely manner could cause a material adverse effect on the Company’s business and has an impact on the Company’s ability to remain listed. The Company does not plan to hire a full time Chief Financial Officer until a later, but as of yet undetermined date, which could have a material adverse impact on the Company’s business.

We are anticipating a period of rapid growth in our headcount and operations, which may place, to the extent that we are able to sustain such growth, a significant strain on our management and our administrative, operational and financial reporting infrastructure.

Our success will depend in part on the ability of our senior management to manage this expected growth effectively. To do so, we believe we will need to continue to hire, train and manage new employees as needed. If our new hires perform poorly, or if we are unsuccessful in hiring, training, managing and integrating these new employees, or if we are not successful in retaining our existing employees, our business may be harmed. To manage the expected growth of our operations and personnel, we will need to continue to improve our operational and financial controls and update our reporting procedures and systems. The expected addition of new employees and the capital investments that we anticipate will be necessary to manage our anticipated growth and will increase our cost base, which may make it more difficult for us to offset any future revenue shortfalls by reducing expenses in the short term. If we fail to successfully manage our anticipated growth, then we will be unable to execute our business plan.

Negative publicity could adversely affect our reputation, our business, and our operating results.

Negative publicity about our Company (including, but not limited to the quality and reliability of our products and services, our privacy and security practices, and litigation involving or relating to us) could adversely affect our reputation which, in turn, could adversely affect our business, results of operations and financial condition. Because Vocodia is in a competitive industry where public perception is important, any harm to the Company’s reputation could be significant. Negative perception about the Company or its software and platform could harm sales and business prospects.

11

Natural disasters and other events beyond our control could materially adversely affect us.

Natural disasters or other catastrophic events may cause damage or disruption to our operations, international commerce and the global economy, and thus could have a strong negative effect on us. Our business operations are subject to interruption by natural disasters, fire, power shortages, pandemics and other events beyond our control. Such events could make it difficult or impossible for us to deliver our products and services to our customers and could decrease demand for our products and services.

Additionally, we depend on the efficient and uninterrupted operations of our third-party data centers and hardware systems. The data centers and hardware systems are vulnerable to damage from earthquakes, tornados, hurricanes, fire, floods, power loss, telecommunications failures and similar events. If any of these events results in damage to third-party data centers or systems, we may be unable to provide our clients with our products and services until the damage is repaired and may accordingly lose clients and revenues. In addition, subject to applicable insurance coverage, we may incur substantial costs in repairing any damage.

Political and economic factors may negatively affect our financial condition or results of operations.

Supply chain interruptions, regulatory changes, or political climate concerns could potentially adversely impact our relationships. Additionally, rising inflation could cause our product, marketing, and labor costs to rise beyond an acceptable level to us or cause us to increase our prices to a level not accepted by consumers. Furthermore, market volatility and macro-economic risks, including a slowdown or potential recession, could harm us and our business. We operate in the sales and customer service sector, and reductions in discretionary spending or consumer demand could have a significant negative impact on our operations and prospects. Any of the foregoing factors could negatively impact our financial condition or the results of our operations.

The COVID-19 pandemic has negatively affected our operations and may continue to do so in the future.

The World Health Organization declared the COVID-19 outbreak a pandemic. The COVID-19 pandemic has negatively affected our operations and may continue to do so in the future. The COVID-19 pandemic has resulted in social distancing, travel bans and quarantine, which has limited access to our facilities, potential customers, management, support staff and professional advisors and can, in the future, impact our supply chain. These factors, in turn, may not only impact our operations, financial condition and demand for our products but our overall ability to react in a timely manner, to mitigate the impact of this event.

In the past, the pandemic negatively affected the development of software, limited identification and cooperation with development partners and slowed the progress of development and deployment. We were also negatively affected due to lack of coordination with early customers, which paid and contracted with management to provide our software as it was developed. We believe that business contracts were jeopardized due to lack of cooperation and the business disruption resulting from stay-at-home policies which severely derailed our coordination with other parties. Further we believe that the pandemic had an adverse effect on development of other in-development partners, including key personnel in software coding and development who suffered health conditions during the pandemic and limited our performance.

The extent of the impact of the COVID-19 pandemic on our operational and financial performance will depend on certain developments, including the duration and spread of the outbreak and the impact on our customers and employees, all of which are uncertain and cannot be predicted. At this point, the overall extent to which COVID-19 may impact our financial condition or results of operations in the future is uncertain.

12

Market and economic conditions may negatively impact our business, financial condition and share price.

Concerns over the COVID-19 pandemic, inflation, energy costs, geopolitical issues, the U.S. mortgage market and unstable real estate market, unstable global credit markets and financial conditions, and volatile oil prices have led to periods of significant economic instability, diminished liquidity and credit availability, declines in consumer confidence and discretionary spending, diminished expectations for the global economy and expectations of slower global economic growth going forward, increased unemployment rates, and increased credit defaults in recent years. Our general business strategy may be adversely affected by any such economic downturns, volatile business environments and continued unstable or unpredictable economic and market conditions. If these conditions continue to deteriorate or do not improve, it may make any necessary debt or equity financing more difficult to complete, more costly, and more dilutive. Failure to secure any necessary financing in a timely manner and on favorable terms could have a material adverse effect on our growth strategy, financial performance, and overall plan of business.

We are authorized to issue preferred stock without stockholder approval, which could adversely impact the rights of holders of our securities.

Our articles of incorporation authorize us to issue up to 24,000,000 shares of Preferred Stock, consisting of 4,000,000 shares of Series A Preferred Stock and 3,000 shares of Series B Preferred Stock, of which 4,000,000 and 1,305 shares are currently issued and outstanding respectively. Any shares or series of preferred stock that we issue in the future may rank ahead of our other securities in terms of dividend priority or liquidation premiums and may have greater voting rights than our common stock. In addition, we may issue preferred stock that could contain provisions allowing those shares to be converted into shares of common stock, which could dilute the value of our common stock to current stockholders and could adversely affect the market price, if any, of our common stock. In addition, the preferred stock could be utilized, under certain circumstances, as a method of discouraging, delaying or preventing a change in control of our Company.

Our inability to fulfill debt obligations could adversely affect working capital needs and financial condition.

As our business is currently unable to meet cash flow demands to fulfill debt obligations timely, we have defaulted on our outstanding indebtedness and there is a continued risk of additional defaults on debt to creditors. The 2022 Convertible Notes issued in August through December 2022, totaling $2,427,059, are currently in default. We recorded a default penalty of $485,412 for the year months ended December 31, 2023. During the years ended December 31, 2023 and 2022, the Company recorded interest expense of $2,769,308 and $60,096, respectively, which included amortization of debt discount of $1,941,999 and $60,096, respectively, default penalty of $485,412 and $0, respectively, and accrued interest of $339,221 and $0, respectively. As of January 31, 2024, we have entered into the Note Extension with the holders of the 2022 Convertible Notes and the 2023 Convertible Notes to extend the maturity dates of each of the 2022 Convertible Notes and the 2023 Convertible Notes to February 14, 2024, in exchange for the Increased Conversion Shares. Simultaneously with its initial public offering, the Company also issued 495,076 Series C Warrants (each, a “Series C Warrant”) to purchase one share of Common Stock each to certain holders. The Series C Warrants will not be registered with the U.S. Securities and Exchange Commission under the Securities Act of 1933 and will not be listed on any stock exchange.

Risks Related to Our Business – Operating Our Website

If we are unable to attract new customers and retain customers on a cost-effective basis, our business and results of operations will be adversely affected.

To succeed, we must attract and retain customers on a cost-effective basis. We rely on a variety of methods to attract new customers, such as paying providers of online services, search engines, directories and other websites to provide content, advertising banners and other links that direct customers to our website, direct sales and partner sales. If we are unable to use any of our current marketing initiatives or the cost of such initiatives were to significantly increase or such initiatives or our efforts to satisfy our existing customers are not successful, we may not be able to attract new customers or retain customers on a cost-effective basis and, as a result, our revenue and results of operations would be adversely affected.

13

Additionally, factors outside of our control, such as new terms, conditions, policies, or other changes made by the online services, search engines, directories and other websites that we rely upon to attract new customers could cause our websites to experience short- or long-term business disruptions, which could adversely affect our revenue and results of operations.

If we fail to develop our brands cost-effectively, our business may be adversely affected.

Successful promotion of our Company’s brands will depend largely on the effectiveness of our marketing efforts and on our ability to provide reliable and useful products and services at competitive prices. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we incur in building our brands. If we fail to successfully promote and maintain our brands or incur substantial expenses in an unsuccessful attempt to promote and maintain our brands, we may fail to attract enough new customers or retain existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, and our business and results of operations could suffer.

The market in which we participate is competitive and, if we do not compete effectively, our operating results could be harmed.

The market for our clients, goods and services is competitive and rapidly changing, and the barriers to entry are relatively low. With the influx of new entrants to the market, we expect competition to persist and intensify in the future, which could harm our ability to increase sales, limit customer attrition and maintain our prices. Competition could result in reduced sales, reduced margins or the failure of our products and services to achieve or maintain more widespread market acceptance, any of which could harm our business. We compete with large established companies possessing large, existing customer bases, substantial financial resources and established distribution channels, as well as smaller less established businesses. If either of these types of competitors decide to develop, market or resell competitive services, acquire one of our existing competitors or form a strategic alliance with one of our competitors, our ability to compete effectively could be significantly compromised and our operating results could be harmed. Our current and potential competitors may have significantly more financial, technical, marketing and other resources than we do and may be able to devote greater resources to the development, promotion, sale and support of their products and services. Our current and potential competitors have more extensive customer bases and broader customer relationships than we have. If we are unable to compete with such companies, the demand for our products could substantially decline.

Risks Related to Information Technology Systems, Intellectual Property and Privacy Laws

We are reliant upon information technology to operate our business and maintain our competitiveness.

Our ability to leverage our technology and data scale is critical to our long-term strategy. Our business increasingly depends upon the use of sophisticated information technologies and systems, including technology and systems (cloud solutions, mobile and otherwise) utilized for communications, marketing, productivity tools, training, lead generation, records of transactions, business records (employment, accounting, tax, etc.), procurement and administrative systems. The operation of these technologies and systems is dependent upon third-party technologies, systems and services, for which there are no assurances of continued or uninterrupted availability and support by the applicable third-party vendors on commercially reasonable terms. We also cannot assure that we will be able to continue to effectively operate and maintain our information technologies and systems. In addition, our information technologies and systems are expected to require refinements and enhancements on an ongoing basis, and we expect that advanced new technologies and systems will continue to be introduced. We may not be able to obtain such new technologies and systems, or to replace or introduce new technologies and systems as quickly as our competitors or in a cost-effective manner. Also, we may not achieve the benefits anticipated or required from any new technology or system, and we may not be able to devote financial resources to new technologies and systems in the future.

14

Any significant disruption in service on our website or in our computer systems, or in our customer support services, could reduce the attractiveness of our services and result in a loss of customers.

The satisfactory performance, reliability and availability of our services are critical to our operations, level of customer service, reputation and ability to attract new customers and retain customers. Most of our computing hardware is co-located in third-party hosting facilities. None of the companies who host our systems guarantee that our customers’ access to our products will be uninterrupted, error-free or secure. Our operations depend on their ability to protect their and our systems in their facilities against damage or interruption from natural disasters, power or telecommunications failures, air quality, temperature, humidity and other environmental concerns, computer viruses or other attempts to harm our systems, criminal acts and similar events. If our arrangements with third-party data centers are terminated, or there is a lapse of service or damage to their facilities, we could experience interruptions in our service as well as delays and additional expense in arranging new facilities. Any interruptions or delays in access to our services, whether as a result of a third-party error, our own error, natural disasters or security breaches, whether accidental or willful, could harm our relationships with customers and our reputation. These factors could damage our brand and reputation, divert our employees’ attention, reduce our revenue, subject us to liability and cause customers to cancel their accounts, any of which could adversely affect our business, financial condition and results of operations.

We do not have a disaster recovery system, which could lead to service interruptions and result in a loss of customers.

Although we have all of our data backed up with multiple services, we do not have any disaster recovery systems. In the event of a disaster in which our software or hardware are irreparably damaged or destroyed, we would experience interruptions in access to our services. Any or all these events could cause our customers to lose access to our services.

If a third party asserts that we are infringing its intellectual property, whether successful or not, it could subject us to costly and time-consuming litigation or require us to obtain expensive licenses, and our business may be adversely affected.

Our industry is characterized by the existence of a large number of patents, trademarks and copyrights and by frequent litigation based on allegations of infringement or other violations of intellectual property rights. Third parties may assert patent and other intellectual property infringement claims against us in the form of lawsuits, letters or other forms of communication. These claims, whether or not successful, could:

| ● | divert management’s attention; |

| ● | result in costly and time-consuming litigation; |

| ● | require us to enter into royalty or licensing agreements, which may not be available on acceptable terms, or at all; |

| ● | in the case of any open source software-related claims, require us to release our software code under the terms of an open source license; or |

| ● | require us to redesign our software and services to avoid infringement. |

As a result, any third-party intellectual property claims against us could increase our expenses and adversely affect our business. Even if we have not infringed any third parties’ intellectual property rights, we cannot be sure our legal defenses will be successful, and even if we are successful in defending against such claims, our legal defense could require significant financial resources and management time. Finally, if a third party successfully asserts a claim that our products infringe its proprietary rights, royalty or licensing agreements might not be available on terms we find acceptable or at all, and we may be required to pay significant monetary damages to such third party.

15