UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the fiscal year ended

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______, 20 ____, to ______, 20_____.

Commission

File Number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The

|

Securities registered pursuant to section 12(g) of the Act:

| N/A |

| (Title of class) |

| N/A |

| (Title of class) |

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

The

registrant was not a public company as of June 30, 2021, the last business day of its most recently completed second fiscal quarter,

and therefore, cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such

date. The registrant’s common stock began trading on The Nasdaq Capital Market on January 7, 2022. The aggregate market value of

the voting and non-voting common equity held by non-affiliates based upon the closing price of $3.23 per share of common stock

as of March 28, 2022 was $

As of March 29, 2022, there were shares of common stock, par value $0.0001 per share, of the registrant issued and outstanding.

Table of Contents

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements contained in this annual report may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this annual report are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, the following risks, uncertainties and other factors:

| ● | the level of demand for our products and services; | |

| ● | competition in our markets; | |

| ● | our ability to grow and manage growth profitably; | |

| ● | our ability to access additional capital; | |

| ● | changes in applicable laws or regulations; | |

| ● | our ability to attract and retain qualified personnel; | |

| ● | the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and | |

| ● | other risks and uncertainties, including those listed under the captions “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

| 3 |

PART I

ITEM 1. BUSINESS

This Business section, along with other sections of this annual report on Form 10-K, includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that these industry publications and third-party research, surveys and studies are reliable, we have not independently verified such data and we do not make any representation as to the accuracy of the information. Unless the context otherwise requires, “Hour Loop,” “we,” “us,” “our,” or the “Company” refers to Hour Loop, Inc. and its consolidated subsidiaries.

Overview

Our Business

We are an online retailer engaged in e-commerce retailing in the U.S. market. We have operated as a third-party seller on www.amazon.com since 2013. We have also sold merchandise on our website at www.hourloop.com since 2013. We expanded our operations to www.walmart.com in October 2020. To date, we have generated practically all of our revenue as a third-party seller on www.amazon.com and only a negligible amount of revenue from our operations on our website at www.hourloop.com and as a third-party seller on www.walmart.com. We manage more than 100,000 stock-keeping units (“SKUs”). Product categories include home/garden décor, toys, kitchenware, apparels, and electronics. Our primary strategy is to bring most of our vendors product selections to the customers. We have advanced software that assists us in identifying product gaps so we can keep such products in stock year-round including the entirety of the last quarter (holiday season) of the calendar year (“Q4”). In upcoming years, we plan to expand our business rapidly by increasing the number of business managers, vendors and SKUs.

Business Model

There are three main types of business models on Amazon: wholesale, private label and retail arbitrage. Our business model is wholesale, also known as reselling, which refers to buying products in bulk directly from the brand or manufacturer at a wholesale price and making a profit by selling the product on Amazon. We sell merchandise on Amazon and the sales are fulfilled by Amazon. We pay Amazon fees for allowing us to sell on their platform. Our relationship with Walmart is also similar. We pay Walmart fees for allowing us to sell our merchandise on their platform. As stated above, to date, we have generated only a negligible amount of revenues as a third-party seller on www.walmart.com.

The advantages of selling via a wholesale model:

| - | Purchase lower unit quantities with wholesale orders than private label products. | |

| - | Selling wholesale is less time intensive and easier to scale than sourcing products via retail arbitrage. | |

| - | More brands will want to work with us because we can provide broader Amazon presence. |

The challenges of selling via a wholesale model:

| - | Fierce competition on listing for Buy Box on amazon.com (as described below). | |

| - | Developing and maintaining relationships with brand manufacturers. |

| 4 |

Market description/opportunities

Total retail sales increased 6.9% to $4.04 trillion in 2020 from $3.78 trillion in 2019. Consumers spent $861.12 billion online with U.S. merchants in 2020, which is around 21.3% of total retail sales for 2020, compared to 15.8% for 2019.

Amazon accounted for nearly a third of all e-commerce in the United States. With a more than 5% gain in e-commerce penetration for U.S. retail sales in 2020, we anticipate a larger market in the upcoming years.

Formation and Management

We were originally incorporated under the laws of the State of Washington on January 13, 2015. However, we converted from a Washington corporation to a Delaware corporation on April 7, 2021. The company was founded in 2013 by Sam Lai and Maggie Yu. With their vision, leadership, and software development skills, the company grew rapidly. From 2013 to 2021, sales grew from $0 to $62,792,981.

Competitive advantage

Among 9.7 million sellers on Amazon, we believe we have two main competitive advantages. First, we have strong operations and sales teams experienced in listing, shipment, advertising, reconciliation and sales. By delivering high quality results and enhancing procedures through the process, our teams are competitive. Second, we believe our proprietary software system gives us an advantage over our competition. The system is highly customized to our business model; it collects and processes large amounts of data every day to optimize our operation and sales. Through advanced software, we can identify product gaps and keep them in stock all year round.

With respect to our advertising strategy, we advertise those products that we estimate will have greater demand based on our experience. This lets us allocate our advertising budget in a fashion that delivers positive value. We advertise our products on Amazon. We allocate our advertising dollars prudently. This is accomplished by advertising items that deliver the most return for our advertising spending. We monitor the items being advertised by our competitors. On the operations side, we constantly refine our processes based on learnings from historical data. The combination of managing the business operations effectively along with allocating our advertising budget to high value items allows us to grow profitably. In cases, where the advertising is fierce, we allocate the spending appropriately. Our strategy for competing with larger competitors is to monitor their pricing and not compete with them when their pricing is low or at a loss. Competitors sell at low prices or at a loss due to a variety of reasons, including, but not limited to, their desire to liquidate inventory or achieve short term increase in revenue. During these times, we avoid matching their prices. This strategy allows us to stay profitable.

Historical Performance

Our year end gross revenues and net profits from 2013 through 2021 is presented in the table below:

| Year-over- | Year-over | |||||||||||||||||||

| Year | Revenue | Year % | Income | Net Income % | -Year % | |||||||||||||||

| 2013 | $ | 26,135 | - | $ | 4,682 | 18 | % | - | ||||||||||||

| 2014 | $ | 1,102,237 | 4117 | % | $ | 150,300 | 14 | % | 3110 | % | ||||||||||

| 2015 | $ | 2,567,267 | 133 | % | $ | 228,009 | 9 | % | 52 | % | ||||||||||

| 2016 | $ | 7,337,012 | 186 | % | $ | 77,752 | 1 | % | NA | |||||||||||

| 2017 | $ | 17,487,124 | 138 | % | $ | -122,176 | -1 | % | -257 | % | ||||||||||

| 2018 | $ | 24,402,144 | 40 | % | $ | 657,821 | 3 | % | NA | |||||||||||

| 2019 | $ | 26,564,693 | 9 | % | $ | -423,073 | -2 | % | -165 | % | ||||||||||

| 2020 | $ | 38,655,264 | 46 | % | $ | 3,820,698 | 10 | % | NA | |||||||||||

| 2021 | $ | 62,792,981 | 62 | % | $ | 4,779,083 | 8 | % | 25 | % | ||||||||||

In 2021 and 2020, 100% of our revenue was through or with the Amazon sales platform.

| 5 |

Pricing Strategy and Policies

In an ideal world, we would like to price our products at key stone pricing or double wholesale cost. However, we operate in a hyper competitive environment and we must stay competitive. Therefore, we must draw a good balance between gross margin and revenue. Our main objectives focus on increasing volume and maximizing profits, which is achieved with a customized auto pricing system we developed internally, in combination with well-trained business managers’ judgment on pricing skills as well as constant monitoring. One principal feature of the pricing system is that it automatically syncs public data of competing offers from Amazon regularly, so business managers can make price settings and adjustments based on accurate data, and thus be able to set optimal selling prices for products. In addition, the system is constantly improved with new features and optimizations.

At a high level, our automated pricing tool helps us stay competitive while our business managers mainly focus on increasing gross margins. Our proprietary repricing tool analyze sales trend, projected sales, inventory age, inventory cost, potential profits, FBA fees, competing offers, and seasonality and determines an urgency level, then depending on the level of urgency, it automatically adjusts prices accordingly.

Business managers, after establishing the bases for prices, begin to develop pricing strategies for each product while taking the current market conditions, company goals (ex: increasing short-term or long-term profits) and strategies into consideration. Furthermore, business managers consider different marketing segments such as costs and competitions in order to develop effective pricing strategies and policies.

The following subsections provide more insight into various pricing strategies we have developed over the years. Our internal training mainly focuses on competition-based pricing policy and value-based pricing policy.

| 1. | Competition-Based Pricing Policy: 20% of our products are toys, which are extremely popular and competitive. In this type of environment where volume is high but gross margin is low, our main strategy is to purchase large quantities, so we can increase sales volume and price competitively while maintaining an average return on investment (“ROI”) of at least 15%. We are using the competition-based pricing policy to match competitor’s prices, which means constantly winning Buy Box (as described below). Our pricing system is capable of automatically matching all Buy Box. | |

| 2. | Promotional Pricing Policy: To boost lagging sales, we adapted our own promotional pricing policy, which involves offering modest discounts on products with inventory age over 45 days, which proves to be a cost-effective at reducing the number of low turn-over SKUs. | |

| 3. | Value-Based Pricing Policy: We incorporate a value-based pricing strategy when inventories are constrained, which can happen when customer demand suddenly spikes due to external factors, supply shortage, or seasonal spikes. We set prices to reflect the value perceived by customers, especially on products under gift categories when consumer demands are higher. Contrary to a typical seller, we opt to maintain high gross margin instead of marking down prices and running special deals during the high-demand season during Q4. Therefore, business managers can achieve increases in both sales and high average ROI of 40%. |

Buy Box on amazon.com is the top right section on a product page where customers can directly add items to their shopping carts. Since many sellers on amazon.com can sell the same product, they must compete to “win the Buy Box” for a certain product. Winning the Amazon Buy Box simply means that you were chosen for the Buy Box placement. When you win this placement, customers have a button to directly add your product to their carts, giving you an advantage over competing sellers. For a seller to be eligible for the Buy Box, they must meet a set of performance-based requirements including order defect rate, customer shopping experience, time and experience on the Amazon selling platform, and status as a professional seller.

| 6 |

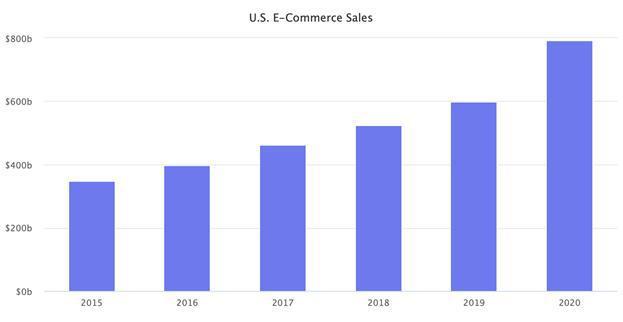

Overview of Market & Competition

According to Marketplace Pulse, U.S. e-commerce grew 32% in 2020 to reach $790 billion, up from $598 billion the year before. According to the Department of Commerce, e-commerce represented 14% of total retail spending, a significant increase from 11.3% in 2019.

For the past 10 years, e-commerce in the U.S. grew, on average, 15% year-over-year. In 2020, the market reached a total sales figure it would have otherwise gotten to in 2021. Thus, two years of e-commerce growth in one year.

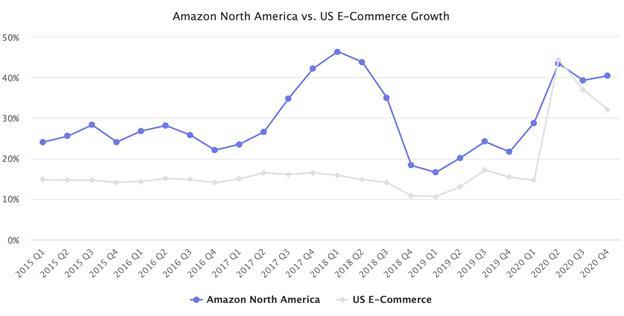

According to Marketplace Pulse, Amazon was one of the big winners in the fourth quarter, a record quarter with nearly $250 billion in e-commerce spending. While during the first two quarters boosted by the pandemic - Q2 and Q3 - it grew at or below the overall U.S. e-commerce growth rate. In the fourth quarter, Amazon grew faster than the market (based on a naive comparison of its reported North America segment growth). Its fulfillment capacity allowed the company to be more confident with deliveries than its main rivals.

| 7 |

Target market size

Total Addressable Market

As an e-commerce company retailing in the U.S. market, our total addressable market covers all U.S. residents with Internet access, where segmentally includes repeat customers and new customers to online shopping every year.

Growth of E-commerce vs. Total Retail Sales

According to the U.S. Department of Commerce data, the e-commerce’s share of total retail sales has steadily been on the rise, where total volume increased by an incredible 44% of year-over-year growth. The total retail sales increased by 6.9% to $4.04 trillion from 2019 to 2020, and all growths came from the e-commerce sales. Consumers spent $861.12 billion online with U.S. merchants in 2020, which is around 21.3% of total retail sales for the year compared to 15.8% in 2019. The strong growth of U.S. online spending shows the future potential of our target market size. The U.S. e-commerce sales accounted for more than 20% of total retail sales in 2020, and Amazon represented one-third of the total.

Growth of Amazon Prime Members

In 2021, Amazon had over 150 million Prime Members in the U.S., and we were seeing continuous year-over-year growth over the past years. The number of Amazon Prime users in the U.S. is forecasted to reach more than 153 million by 2022, with 3% annual growth.

Operational Advantages

According to Marketplace Pulse, Hour Loop is one of the top 100 third-party sellers on U.S. Amazon. In 2019 there were only 18,000 sellers, out of 2,700,000 (or 0.67%) that exceeded $1 million in annual sales. Our sales in 2019 were $26.6 million.

Automation

We developed a proprietary software that is tailor made to all our operational needs. This includes managing order review process, shipment managements, inventory management, accounting, and complete end-to-end third-party integrations. This allows us to scale, reduce cost, and improve quality.

Profitability Management

We have experienced operations managers tracking team performances with key performance indicators. We have departments specializing in logistic costs, advertising, marketing, and product management. We hold monthly process reviews to identify early red flags and look for areas to optimize. Each quarter we set increasingly difficult bars both to grow gross margin and further reduce expenses.

Continuous Process Optimization

In order to improve operating efficiencies, we have effective process optimization adapting to the changing policies of the e-commerce marketplace. We continuously analyze our performance based on data. We conduct pricing, inventory planning and profitability analysis using this data. This analysis provides us with insights on the processes that add the most value. Using these insights, we develop guidelines that help us improve our operations. These guidelines are incorporated into our operations which include (but are not limited to), identifying and ordering at optimal inventory levels, managing merchandise storage costs, optimizing transit times, and pricing at appropriate levels. Our operations staff follows these guidelines which help them perform optimally. By continuously analyzing data, we are able to find insights for improving our business. This drives continuous process optimization and its implementation into our operations. In addition, our proprietary software allows us to continually accelerate process effectiveness based on specific requirements. Over time, our system eliminates unnecessary procedures that could be replaced by an advanced algorithm. For instance, we simplify Fulfillment by Amazon (“FBA”) shipments process through application programming interface (“API”) integration. Our self-developed system also tracks insightful analysis of our profitability, clearer visualizes the drivers and optimums to better manage operational costs. We monitor operational parameters that drive our business and proactively try to optimize them. These include fine tuning our item selection, managing our inventory levels, estimating demand and pricing to maximize our profitability.

| 8 |

Data-Driven Approach

We make decisions based on analysis and interpretation of the data sets rather than observations over the market trend. By standardizing processes and combine data-driven management, we can ensure the organization maintains consistency that is high quality. Our business managers use historical data and sales projection provided by our proprietary software to find potential product gaps and keep products in stock all year round. This advantage enables powerful predictive insights in correlating real-time data with past sales patterns.

Training Programs

Our effective training programs accelerates employees’ professional development and enables the company to hire new graduates or people without experience. Our training programs are very task-specific and we continually improve the materials in order to fit new industry needs. Other than the training material, we assign mentors to evaluate and monitor trainees’ performance at each stage of the training program.

Task Generalization

By generalizing each task with a standard process, we are able to shift assignments at regular intervals in order to find the most suitable employee for each specific task. Moreover, business managers are also able to rotate the vendors they manage easily. This allows our organization to effectively and consistently manage a vendor when a key employee who previously managed such vendor is no longer with the company. In addition, the task generalization allows the company to hire remote teams to further reduce labor costs.

Multicultural Management

We have a multicultural management team that is linguistically and culturally diverse in order to make judgments from different perspectives. Our remote teams in Taiwan and the Philippines provide diverse professional insights on specific tasks.

Technological advantages

Our software architecture was designed from the ground up to be scalable, secured, and easily extensible. By using JRuby on Rails, we can make use the best parts of Java, Ruby, and Rails without paying for their disadvantages. For example, we can use the massive collections of Java library, portability, speed, multi-threading, and maturity, but we do not have to be tied down with verbose code and strict typing. Rails allow us to quickly build web pages and integrate both the frontend and the backend. The application runs on Amazon Web Services (“AWS”) and can be easily scaled up to as many hosts as needed. It is accessible from a browser, so there is no need to setup or install anything on the client-side.

Cost advantage

Access to Low Product Costs

We lower our product average costs by direct import items that have high volume, purchasing in bulk with better prices, and negotiating discounts or rebates over increased purchase volume every year. Our strong growth of purchase every year allows us to negotiate better discounts than the rivals. Therefore, we have the cost advantages to compete at low prices.

Efficient Processes and Technologies

Our proprietary software allows us to tailor make tools based on our specific use cases and leverage technologies to greatly reduce manual operations. We also saved the expense of using third-party software in managing inventory, orders, product listings, and especially the advertising analytic tool.

| 9 |

Low Distribution and Logistic costs

We saved the cost of managing the warehouse, shipping, and product distribution as we are enrolled in Amazon’s FBA program. The program allows us to reduce fixed costs of the physical assets and quickly scale up the business without thinking much about infrastructure complexity. Apart from using the FBA program, we also use FedEx, Amazon partnered carrier, Amazon Freight, and Amazon Global Logistics to reduce expense. The competitive shipping rates we secured provide us a cost-efficient way to deliver shipments from overseas and domestic to Amazon warehouse.

Efficiently Managed Operations

We have a good management structure within the firm and a data-driven system that allows employees to manage tasks quickly and cost-efficiently.

Reduced Labor Costs

Our labor cost is below 5% of our revenue. We leverage third-party logistic companies to forward or prep our shipments to Amazon, which reduces our logistic operation labor costs. We also worked with labor outsourcing partner located in Philippines. They provide virtual assistants to help us with data entries and repetitive work, which is a very cost-effective way to do a lot of grunt work.

Key Competitors by Market Size/Share

Our key competitor is Amazon Retail. Amazon Retail frequently buys from the same brands we sell and sells them at a loss. Amazon Retails offers can be identified by the “Sold by Amazon” tag on Amazon’s site, and they are formed by the two components: (i) Amazon Vendor Central, and (ii) Sold by Amazon program. We do not consider other third-party sellers as key competitors, because none of them represent enough market share to influence sales outcome. The addressable market is incredibly vast, thus we believe there are plenty of opportunities for everyone.

Amazon Vendor Central

Amazon Vendor Central allows manufacturers and brand owners to sell directly to Amazon as a first-party seller. This is one of the key competitive factors as Amazon usually buys bulk from the brands and sells at a very low price, which leads to hyper-competitive pricing. On pricing control, Amazon does not always follow the Minimum Advertised Pricing guidelines from manufacturers, which also puts us at a disadvantage when selling the same products.

Sold by Amazon Program

With the rise of e-commerce platforms, Amazon is looking for opportunities to attract customers away from its retail store rivals. In 2019, Amazon rolled out a new program entitled Sold by Amazon (“SBA”) to help sellers grow their business. This program gives brand owners the control of inventory management and listings with Amazon having the authority to constantly monitor and change the price to make sure customers are getting the best deals. Once the products are enrolled in the SBA program, Amazon will set the Minimum Gross Proceeds (“MGP”) to pay sellers the lowest possible amount on each unit sold. This new program is another threat to our company as Amazon is the one taking control of pricing, and they set the price very low in order to compete with competitors’ low price strategy.

Competitor Strengths and Weaknesses

Strengths of Sold by Amazon

First, ship from and Sold by Amazon creates competition for potential customers who prefer to buy products from Amazon rather than a third-party seller. Secondly, Amazon monitors and manages pricing which makes the product price range at a highly competitive level. In fact, the chance of Amazon winning buy box is even higher as they have the best deal for customers. Finally, Amazon is not restricted by its policy to third-party sellers. One of the critical policies is the restock limit. Amazon limits certain items restock quantities based on recent sales activity, and this affects the in-stock rate of popular items that needs a greater volume.

| 10 |

Weaknesses of Sold by Amazon

As Amazon focuses on sales more than relationships with vendors, they do not follow vendors’ Minimum Advertised Pricing (“MAP”) strictly. We believe this has led to the devaluation of brands and will have a negative impact on building a long-term relationship with the vendors. Once the vendor hands over their price control to Amazon, we believe it is unlikely for them to sell at their original target price further, and it influences their offline sales. And in fact, it makes a huge difference in profitability to both Amazon and the vendor when reacts to the competitive pricing changes.

Apart from the weaknesses of business relationships, we believe Amazon also has disadvantages in the niche marketplaces, where product offerings are narrower and more personalized. As a third-party seller, we cooperate with vendors in developing custom projects that bring product differentiation and scarcity effect. However, we believe Amazon only concentrates on the masses, which gives them the deficiency of having products that are targeted in certain market segments.

Potential Substitute Products Posing Credible Threat to Company Products

No potential substitute products would pose a credible threat to our company as we have developed a wide product diversification.

As a company that focuses on reselling wholesale products, we have the resilience to find substitution of products or brands. We established product diversification by managing wide range of SKUs and continually expand our product categories. Our business strategy allows us to mitigate risk and generate significant profit by selling low volumes items diversified across a large variety of products.

In contrast, private labels sellers manage small number of SKUs that have large volumes in return with higher profit per unit. However, private labels have much higher risk when experiencing stagnant or declining sales as they would have lower capability to find sales replacements that are already established.

Strength of Barriers to Entry

Higher Capital, Low Margin: Selling online is general low margin, but it requires high capital investment in order to purchase goods and run advertising.

Product Differentiation: Our proprietary software allows us to manage a huge number of SKUs. This allows us to participate in profitable long-tail products in addition to well-known popular ones. The turnover rate for long-tail products is slow, so newcomers are not likely to enter. It also requires a sophisticated system to manage. Furthermore, vendor relationships do not happen overnight.

Advanced System: We have already developed a highly sophisticated system which has been refined over time to become highly effective. Even if a new entrant has a team of the best software engineers in the world, it will still take them many years to refine their system. There is a myriad of intricacies as to the effectiveness of a system. Even if the new entrants have the system built, it will still take them years to collect historical sales data. By the time new entrants have done all that, our system would have continued to mature. This means we would be able to manage more SKUs more profitably with lower costs.

Risk of Entry- Potential Entrants

Vendor Vertical Integration: A vendor may forward integrate into the e-commerce marketplace in order to directly engage with their online customers.

Multichannel E-commerce: There is a chance of established online retail firms such as sellers on eBay, Walmart, and Etsy expanding their business to the Amazon marketplace.

Brick-and-Mortar: As the online retail is growing and offline retail is contracting, there are more brick-and-mortar stores migrating from offline to online.

| 11 |

Improving Sales of Popular Items and Securing the Inventories Without Paying Higher Storage Fees By Engaging the Services of Third Party Warehouses

As a retailer our success is heavily influenced by the inventory control of our suppliers (vendors). However, many of our suppliers are having difficulties to maintain their stock level due to various reasons, such as the shortage of shipping containers, lack of labor, or disruption in manufacturing. The situation exacerbates during the pandemic and in peak season. In order to secure the inventories, we start to order large quantities of popular items or buying them out to store in the Amazon fulfillment center (“FC”). However, the monthly storage fee of Amazon FC in peak season (Q4) is 3.5 times higher than normal season, which puts pressure on our profits. To maintain the balance of inventory level and margins, we are currently contracting the warehousing services of third-party warehouses, including, Rahl Distribution, Inc., Rite Prep Shipping, 3Plzen, Carolina Prep & Ship, and West FBA to support our overall stock planning process. By doing this, we can improve sales by preventing popular items from going out of stock, since we had secured adequate inventories ahead of time. Furthermore, we can also avoid paying higher Amazon storage fees in Q4.

Growth Objectives

In 2021, we plan to grow the number of suppliers from 226 to 300, the number of business managers from 20 to 50, the number of active SKUs from 42,000 to 60,000, and the number of total employees from 60 to 120. In 2022, we plan to grow the number of suppliers to 650, the number of business managers to 200, the number of active SKUs to 130,000, and the number of total employees to 250. In 2023, we plan to grow the number of suppliers to 1,200, the number of business managers to 350, the number of active SKUs to 200,000, and the number of total employees to 500. In 2024, we plan to grow the number of suppliers to 2000, the number of business managers to 600, the number of active SKUs to 300,000, and the number of total employees to 900. We believe in order to be successful in the long-term, we must invest in talents.

New business managers are the key to growth, they are analogous to new stores in a traditional brick and mortar retail business. Although the return on investment is extremely high over the long-term when investing in people, initially the return is very low or even negative. Therefore, as we continue to fuel the rapid growth, we will need to increase the number of people faster than the growth. We anticipate that ratio to improve when we reached critical mass of highly proficient business managers from the new hires.

Market and Supplier Development - Establishing a Vendor Acquisition Team

In order to continue growing at a rapid pace, we must onboard new vendors at scale. We anticipate establishing a vendor acquisition team dedicated to onboarding new vendors would drastically improve our vendor acquisition success rate. This team would specialize in the skills required to convince vendors to sell us their goods. Currently, this is being done by individual business managers with varying skill levels. The success rate by the individual business managers varies. Establishing this new team should ensure more consistency, so we can better plan for the future. The team would consist of three to five executive managers who are responsible for researching and contacting potential vendors. Furthermore, on a monthly basis, the team would be reviewing the lists of potential vendors who are not yet collaborating with us and reach out to them to reconnect. The objective of the vendor and supplier team is to on board 150 vendors per year and increasing our product range as well as diversifying our product categories.

| 12 |

COVID-19

Our business, results of operations, and financial condition may be materially adversely impacted if a public health outbreak, including the recent COVID-19 pandemic, interferes with our ability, or the ability of our employees, contractors, suppliers, and other business partners to perform our and their respective responsibilities and obligations relative to the conduct of our business.

The COVID-19 pandemic has adversely affected and may continue to adversely affect the economies and financial markets worldwide, resulting in an economic downturn that could impact our business, financial condition and results of operations. As a result, our ability to fund through public or private equity offerings, debt financings, and through other means at acceptable terms, if at all, may be disrupted, in the event our financing needs for the foreseeable future are not able to be met by our balances of cash, cash equivalents and cash generated from operations.

In addition, the continuation of the COVID-19 pandemic and various governmental responses in the United States has adversely affected and may continue to adversely affect our business operations, including our ability to carry on business development activities, restrictions in business-related travel, delays or disruptions in our on-going projects, and unavailability of the employees of the Company or third parties with whom we conduct business, due to illness or quarantines, among others. Our business was negatively impacted by disruptions in our supply chain, which limited our ability to source merchandise, and limits on products fulfillment placed by Amazon. For example, we may be unable to launch new products, replenish inventory for existing products, ship into or receive inventory in our third-party warehouses in each case on a timely basis or at all. The extent to which COVID-19 could impact our business will depend on future developments, which are highly uncertain and cannot be predicted with confidence, and will depend on many factors, including the duration of the outbreak, the effect of travel restrictions and social distancing efforts in the United States and other countries, the scope and length of business closures or business disruptions, and the actions taken by governments to contain and treat the disease. As such, we cannot presently predict the scope and extent of any potential business shutdowns or disruptions. Possible effects may include, but are not limited to, disruption to our customers and revenue, absenteeism in our labor workforce, unavailability of products and supplies used in our operations, shutdowns that may be mandated or requested by governmental authorities, and a decline in the value of our assets, including various long-lived assets.

Bank of America Loan

On June 18, 2019, the Company issued a Promissory Note (the “BofA Note”) in the amount of $785,000 to Bank of America (the “Lender”) for a loan in the amount of $785,000. The BofA Note matures on June 18, 2024 and bears interest at a rate of 8.11% per annum. The monthly payment is $15,963, consisting of $11,398 of principal and $4,565 of interest. As of December 31, 2021, the aggregate principal amount of the BofA Note outstanding was $0 . As of March 29, 2022, there is an outstanding balance of deferred interest of $27,996

PPP Loan

On April 7, 2020, the Company issued a Promissory Note (the “Note”) in the amount of $27,012 under the Paycheck Protection Program (“PPP”) to JP Morgan Chase Bank, N.A. (the “Lender”). The PPP, established as part of the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”), which was enacted March 27, 2020, provides for loans to qualifying businesses for amounts up to 2.5 times of the average monthly payroll expenses of the qualifying business. The Note matures on April 7, 2022 and bears interest at a rate of 0.98% per annum, payable monthly commencing October 5, 2020, following an initial deferral period as specified under the PPP loan. The Note may be prepaid at any time prior to maturity with no prepayment penalties. The Paycheck Protection Program Flexibility Act (the “Flexibility Act”), signed on June 5, 2020, amended certain provisions of the PPP, including the deferral period and repayment terms. The Flexibility Act extends the deferral period of payments of PPP loan principal, interest, and fees to the date when the U.S. Small Business Administration makes a final decision on the borrower’s application for forgiveness, or 10 months after the last day of the covered period if a borrower has not applied for forgiveness (whichever is earlier). This extension applies regardless of the terms of the PPP and does not require an amendment of the PPP. As such, the Company has not made any payments on the Note during 2020.

Under the terms of the PPP loan, up to the entire amount of principal and accrued interest may be forgiven to the extent PPP loan proceeds are used for qualifying expenses as described in the CARES Act and applicable implementing guidance issued by the U.S. Small Business Administration under the PPP loan. On May 6, 2021, the entire amount of principal and accrued interest on the Note was forgiven.

Conversion of S Corporation to C Corporation

On June 30, 2021, the Company completed a corporate reorganization to convert its status from a S corporation to a C corporation with an effective date of July 27, 2021. Retained earnings in the amount of $4,170,418 were distributed by the Company to the S corporation stockholders ($2,085,209 to each of Mr. Lai and Ms. Yu) on July 27, 2021.

| 13 |

Affiliated Loans

December 2020 Loan

On December 31, 2020, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, made a loan (“December 2020 Loan”) to us of $1,041,353 in a single payment ($520,676 attributable to each of Mr. Lai and Mrs. Yu). The loan is memorialized in a Loan Agreement dated December 31, 2020. Pursuant to the terms of the Loan Agreement, the loan bore no interest and was payable on demand.

On September 16, 2021, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, and the Company amended and restated the Loan Agreement to modify the terms of the December 2020 Loan, whereby the interest rate became 2% per annum (applied retroactively) rather than non-interest bearing and maturity date became December 31, 2021 rather than payable on demand.

On December 31, 2021, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, and the Company amended and restated the Loan Agreement to modify the term of the December 2020 Loan, whereby the maturity date was extended from December 31, 2021 to January 31, 2022.

On February 8, 2022, the outstanding principal balance and accrued interest on the December 2020 Loan was paid in full.

July 2021 Loan

On July 27, 2021, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, made a loan (“July 2021 Loan”) to us of the outstanding retained earnings of approximately $4,170,418 in a single payment ($2,085,209 attributable to each of Mr. Lai and Mrs. Yu). The loan is memorialized in a Loan Agreement dated October 15, 2021. Pursuant to the terms of the Loan Agreement, the loan bears interest of 2% per annum and the principal of the loan ($4,170,418) and accrued interest becomes due and payable on December 31, 2022.

As of December 31, 2021, the outstanding principal balance was approximately $4,170,418 and accrued interest was $21,023 on the July 2021 Loan.

Stock Splits

On September 22, 2021, our board of directors and shareholders approved a forward stock split in a ratio of 4.44-for-1 (“Forward Stock Split”) and on September 27, 2021, we filed a certificate of amendment to our Certificate of Incorporation implementing the Forward Stock Split in a ratio of 4.44-for-1, effective September 27, 2021. Therefore, on September 27, 2021, following the Forward Stock Split, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, each held 22,200,000 shares of common stock (for an aggregate of 44,400,000 shares of common stock).

On November 29, 2021, our board of directors and shareholders approved a reverse stock split in a ratio of 0.75-for-1 (“Reverse Stock Split”) and on December 1, 2021, we filed a certificate of amendment to our Certificate of Incorporation implementing the Reverse Stock Split in a ratio of 0.75-for-1, effective December 3, 2021. Therefore, on December 3, 2021, following the Reverse Stock Split, Sam Lai, our Chief Executive Officer, and Maggie Yu, our Senior Vice President, each held 16,650,000 shares of common stock (for an aggregate of 33,300,000 shares of common stock).

Except as otherwise indicated, all references to our common stock, share data, per share data and related information has been adjusted for the Forward Stock Split ratio of 4.44-for-1 and Reverse Stock Split ratio of 0.75-for-1 as if they had occurred at the beginning of the earliest period presented. The Forward Stock Split, divided each share of our outstanding common stock into 4.44 shares of common stock, and the Reverse Stock Split, divided each share of our outstanding common stock into 0.75 shares of common stock, without any change in the par value per share, and the Forward Stock Split and the Reverse Stock Split correspondingly adjusted, among other things, the exercise rate of our warrants into our common stock. No fractional shares were issued in connection with the Forward Stock Split and the Reverse Stock Split, and any fractional shares resulting from the Forward Stock Split and Reverse Stock Split were rounded up to the nearest whole share.

| 14 |

Approval of the Hour Loop, Inc. 2021 Equity Incentive Plan

On June 27, 2021, our Board of Directors and shareholders holding a majority of our outstanding shares of common stock approved the Hour Loop, Inc. 2021 Equity Incentive Plan (the “2021 Plan”). Under the 2021 Plan, a total of 4,995,000 shares of common stock are authorized for issuance pursuant to the grant of stock options, stock appreciation rights, restricted stock, restricted stock units, performance units, performance shares or other cash- or stock-based awards to officers, directors, employees and eligible consultants to the Company or its subsidiaries. Subject to adjustment as provided in the 2021 Plan, the maximum aggregate number of shares that may be issued under the 2021 Plan will be cumulatively increased on January 1, 2022 and on each subsequent January 1, by a number of shares equal to the smaller of (i) 3% of the number of shares of common stock issued and outstanding on the immediately preceding December 31, or (ii) an amount determined by our Board of Directors. Accordingly, as of March 29, 2022, there were 4,995,000 shares of common stock were authorized for issuance under the 2021 Plan, and 4,987,247 shares available for issuance under the 2021 Plan.

Initial Public Offering

On January 11, 2022, we closed our initial public offering of 1,725,000 shares of common stock, which included the full exercise of the underwriter’s over-allotment option, at a public offering price of $4.00 per share, for aggregate gross proceeds of $6.9 million, prior to deducting underwriting discounts, commissions, and other offering expenses. Our common stock began trading on Nasdaq on January 7, 2022, under the symbol “HOUR”. EF Hutton, division of Benchmark Investments, LLC (“EF Hutton”), acted as sole book-running manager for the offering.

Employees

As of March 29, 2022, we had 3 full-time employees. As of March 29, 2022, our subsidiary, Flywheel Consulting Limited had 180 full time employees. None of our employees or Flywheel Consulting Limited’s employees is represented by a union. Flywheel Consulting Limited and us consider our relations with our employees to be good.

Legal Proceedings

From time to time, we are involved in various claims and legal actions arising in the ordinary course of business. To the knowledge of our management, there are no legal proceedings currently pending against us which we believe would have a material effect on our business, financial position or results of operations and, to the best of our knowledge, there are no such legal proceedings contemplated or threatened.

Properties

Our corporate headquarters are located at 8201 164th Ave NE #200, Redmond, WA 98052-7615, where we rent a virtual office from an unaffiliated third party under a virtual office/meeting room agreement. This agreement provides for daily telephone answering, messaging and fax services, and paid access to conference rooms on an as-needed basis. The virtual office arrangement expires on August 31, 2021. Terms of the virtual office arrangement provide for a rent payment of $29.50 per month. We also lease a warehouse located at Floor 35, No. 1123-1139, Fangshan Beier Road, Xiangbei Industry District, Xiamin, China, where we lease approximately 1680 square feet from an unaffiliated third party. This lease expires on January 1, 2022. Terms of this lease provides for a base rent payment of RMB$21,840 (approximately US$3,116) per month. Our wholly owned subsidiary, Flywheel Consulting Limited also has an office at 27F. No.251, Mingquan 1st Rd., Xinxing Dist., Kaohsiungcity, Taiwan, where we lease approximately 2,230 rentable square feet of office space from an unaffiliated third party. This lease expires on August 31, 2022. Terms of the Taiwan office lease provide for a base rent payment of NTD$94,500 (approximately US$3,400) per month. We believe that these facilities are adequate for our current and near-term future needs.

| 15 |

ITEM 1A. RISK FACTORS

An investment in our securities carries a significant degree of risk. You should carefully consider the following risks, as well as the other information contained in this annual report on Form 10-K, including our historical financial statements and related notes included elsewhere in this annual report on Form 10-K, before you decide to purchase our securities. Any one of these risks and uncertainties has the potential to cause material adverse effects on our business, prospects, financial condition and operating results which could cause actual results to differ materially from any forward-looking statements expressed by us and a significant decrease in the value of our common shares and warrants. Refer to “Cautionary Statement Regarding Forward-Looking Statements.”

We may not be successful in preventing the material adverse effects that any of the following risks and uncertainties may cause. These potential risks and uncertainties may not be a complete list of the risks and uncertainties facing us. There may be additional risks and uncertainties that we are presently unaware of, or presently consider immaterial, that may become material in the future and have a material adverse effect on us. You could lose all or a significant portion of your investment due to any of these risks and uncertainties.

Below is a summary of material risks, uncertainties and other factors that could have a material effect on the Company and its operations:

| ● | We face intense competition; | |

| ● | Our business depends on our ability to build and maintain strong product listings on e-commerce platforms. We may not be able to maintain and enhance our product listings if we receive unfavorable customer complaints, negative publicity or otherwise fail to live up to consumers’ expectations, which could materially adversely affect our business, results of operations and growth prospects; | |

| ● | We experience significant fluctuations in our operating results and growth rate; | |

| ● | We face risks related to successfully optimizing and operating our fulfillment and customer service operations; | |

| ● | The variability in our retail business places increased strain on our operations; | |

| ● | Continued increases in Amazon Marketplace fulfillment and storage fees could have an adverse impact on our profit margin and results of operations; | |

| ● | A change in one or more of the Company’s vendors’ policies or the Company’s relationship with those vendors could adversely affect the Company’s results of operations; | |

| ● | Our revenue is dependent upon maintaining our relationship with Amazon and failure to do so, or any restrictions on our ability to offer products on the Amazon Marketplace, could have an adverse impact on our business, financial condition and results of operations; | |

| ● | Loss of key personnel or the inability to attract, train and retain qualified employees could adversely affect the Company’s results of operations; | |

| ● | We may face difficulties in meeting our labor needs to effectively operate our business; | |

| ● | Our business could be adversely affected by increased labor costs, including costs related to an increase in minimum wage and health care; | |

| ● | Breach of data security could harm our business and standing with our customers; | |

| ● | Our hardware and software systems are vulnerable to damage, theft or intrusion that could harm our business; |

| 16 |

| ● | Our inability or failure to protect our intellectual property rights, or any claimed infringement by us of third-party intellectual rights, could have a negative impact on our operating results; | |

| ● | The Company’s business is influenced by general economic conditions | |

| ● | Disruption of global capital and credit markets may have a material adverse effect on the Company’s liquidity and capital resources; | |

| ● | The Company is dependent upon access to capital for its liquidity needs; | |

| ● | We may complete a future significant strategic transaction that may not achieve intended results or could increase the number of our outstanding shares or amount of outstanding debt or result in a change of control; | |

| ● | Historically, we have experienced declines, and we may continue to experience fluctuation in our level of sales and results from operations; | |

| ● | The ability of the Company to satisfy its liabilities and to continue as a going concern will continue to be dependent on the implementation of several items, the success of which is not certain; | |

| ● | Parties with whom the Company does business may be subject to insolvency risks or may otherwise become unable or unwilling to perform their obligations to the Company; | |

| ● | Failure to comply with legal and regulatory requirements could adversely affect the Company’s results of operations; | |

| ● | Litigation may adversely affect our business, financial condition and results of operations; | |

| ● | The effects of natural disasters, terrorism, acts of war, and public health issues may adversely affect our business; | |

| ● | A pandemic, epidemic or outbreak of an infectious disease, such as COVID-19, may materially and adversely affect our business; | |

| ● | The loss of key senior management personnel or the failure to hire and retain highly skilled and other key personnel could negatively affect our business; | |

| ● | The ability of Sam Lai, our Chairman of the Board, Chief Executive Officer and Interim Chief Financial Officer, and Maggie Yu, our Senior Vice President, who are husband and wife, to control our business may limit or eliminate minority stockholders’ ability to influence corporate affairs; | |

| ● | Government regulation is evolving and unfavorable changes could harm our business; | |

| ● | We are subject to product liability claims when people or property are harmed by the products we sell; | |

| ● | We could face prior period sales tax and corporate tax liabilities, penalties and collection obligations; | |

| ● | There can be no assurance that we will be able to comply with continued listing standards of The Nasdaq Capital Market (“Nasdaq”); | |

| ● | High state income tax rates could impact our financials negatively; | |

| ● | The market price of our common stock may be volatile, and you could lose all or part of your investment; and | |

●

|

Our current accounting and inventory tracking systems could impair our ability to file accurate and timely financial statements. |

| 17 |

Risks Related to Our Business

We face intense competition.

The online retail business is rapidly evolving and intensely competitive. Some of our current and potential competitors have greater resources, longer histories, and/or more customers. They may secure better terms from vendors, adopt more aggressive pricing, and devote more resources to technology, infrastructure, fulfillment, and marketing.

Competition continues to intensify, including with the development of new business models and the entry of new and well-funded competitors, and as our competitors enter into business combinations or alliances and established companies in other market segments expand to become competitive with our business. In addition, new and enhanced technologies, including search, web and infrastructure computing services, digital content, and electronic devices continue to increase our competition. The Internet facilitates competitive entry and comparison shopping, which enhances the ability of new, smaller, or lesser-known businesses to compete against us. As a result of competition, our product offerings may not be successful, we may fail to gain or may lose business, and we may be required to increase our spending or lower prices, any of which could materially reduce our sales and profits.

Our business depends on our ability to build and maintain strong product listings on e-commerce platforms. We may not be able to maintain and enhance our product listings if we receive unfavorable customer complaints, negative publicity or otherwise fail to live up to consumers’ expectations, which could materially adversely affect our business, results of operations and growth prospects.

Maintaining and enhancing our product listings is critical in expanding and growing our business. However, a significant portion of our perceived performance to the customer depends on third parties outside of our control, including suppliers and third-party delivery agents as well as online retailers such as Amazon and Walmart. Because our agreements with our online retail partners are generally terminable at will, we may be unable to maintain these relationships, and our results of operations could fluctuate significantly from period to period. Because we rely on third parties to deliver our products, we are subject to shipping delays or disruptions caused by inclement weather, natural disasters, labor activism, health epidemics or bioterrorism. We may also experience shipping delays or disruptions due to other carrier-related issues relating to their own internal operational capabilities. Further, we rely on the business continuity plans of these third parties to operate during pandemics, like the COVID-19 pandemic, and we have limited ability to influence their plans, prevent delays, and/or cost increases due to reduced availability and capacity and increased required safety measures.

Customer complaints or negative publicity about our products, delivery times, or marketing strategies, even if not accurate, especially on blogs, social media websites and third-party market sites, could rapidly and severely diminish consumer view of our product listings and result in harm to our brands. Customers may also make safety-related claims regarding products sold through our online retail partners, such as Amazon, which may result in an online retail partner removing the product from its marketplace. We have from time to time experienced such removals and such removals may materially impact our financial results depending on the product that is removed and length of time that it is removed. We also use and rely on other services from third parties, such as our telecommunications services, and those services may be subject to outages and interruptions that are not within our control.

We experience significant fluctuations in our operating results and growth rate.

We are not always able to accurately forecast our growth rate. We base our expense levels and investment plans on sales estimates. A significant portion of our expenses and investments is fixed, and we are not always able to adjust our spending quickly enough if our sales are less than expected.

| 18 |

Our revenue growth may not be sustainable, and our percentage growth rates may decrease. Our revenue and operating profit growth depend on the continued growth of demand for the products offered by us, and our business is affected by general economic and business conditions. A softening of demand, whether caused by changes in customer preferences or a weakening of the U.S. economy, may result in decreased revenue or growth.

Our sales and operating results will also fluctuate for many other reasons, including due to factors described elsewhere in this section and the following:

| ● | our ability to retain and increase sales to existing customers, attract new customers, and satisfy our customers’ demands; | |

| ● | our ability to retain and expand our network of vendors; | |

| ● | our ability to offer products on favorable terms, manage inventory, and fulfill orders; | |

| ● | the introduction of competitive products, price decreases, or improvements; | |

| ● | changes in usage or adoption rates of the Internet, e-commerce, electronic devices, and web services; | |

| ● | timing, effectiveness, and costs of expansion and upgrades of our systems and infrastructure; | |

| ● | the extent to which we finance, and the terms of any such financing for, our current operations and future growth; | |

| ● | the outcomes of legal proceedings and claims, which may include significant monetary damages or injunctive relief and could have a material adverse impact on our operating results; | |

| ● | variations in the mix of products we sell; | |

| ● | variations in our level of merchandise and vendor returns; | |

| ● | the extent to which we offer fast and free delivery and provide additional benefits to our customers; | |

| ● | factors affecting our reputation; | |

| ● | the extent to which we invest in technology and content, fulfillment, and other expense categories; | |

| ● | increases in the prices of fuel and gasoline, as well as increases in the prices of other energy products and commodities like paper and packing supplies and hardware products; | |

| ● | the extent to which operators of the networks between our customers and us, the online retailer, successfully charge fees to grant our customers unimpaired and unconstrained access to our online services; | |

| ● | our ability to collect amounts owed to us when they become due; | |

| ● | the extent to which new and existing technologies, or industry trends, restrict online advertising or affect our ability to customize advertising or otherwise tailor our product and service offerings; | |

| ● | the extent to which use of our services is affected by spyware, viruses, phishing and other spam emails, denial of service attacks, data theft, computer intrusions, outages, and similar events; and | |

| ● | disruptions from natural or man-made disasters, extreme weather, geopolitical events and security issues (including terrorist attacks and armed hostilities), labor or trade disputes, and similar events. |

We face risks related to successfully optimizing and operating our fulfillment and customer service operations.

Failures to adequately predict customer demand or otherwise optimize and operate our fulfillment and customer service operations successfully from time to time result in excess or insufficient fulfillment or customer service capacity, increased costs, and impairment charges, any of which could materially harm our business. As we continue to add fulfillment and customer service capability or add new businesses with different requirements, our fulfillment and customer service operations become increasingly complex and operating them becomes more challenging. There can be no assurance that we will be able to operate our operations effectively.

In addition, failure to optimize inventory in our fulfillment operations increases our net shipping cost by requiring long-zone or partial shipments. We may be unable to adequately staff our fulfillment and customer service operations. Our failure to properly handle such inventory or to accurately forecast product demand may result in us being unable to secure sufficient storage space or to optimize our fulfillment operations or cause other unexpected costs and other harm to our business and reputation.

We rely on a limited number of shipping companies to deliver inventory to us and completed orders to our customers. The inability to negotiate acceptable terms with these companies or performance problems or other difficulties experienced by these companies or by our own transportation systems could negatively impact our operating results and customer experience. In addition, our ability to receive inbound inventory efficiently and ship completed orders to customers also may be negatively affected by natural or man-made disasters, extreme weather, geopolitical events and security issues, labor or trade disputes, and similar events.

| 19 |

The variability in our retail business places increased strain on our operations.

Demand for our retail products can fluctuate significantly for many reasons, including as a result of seasonality, promotions, product launches, or unforeseeable events, such as in response to natural or man-made disasters, extreme weather, or geopolitical events. For example, we expect a disproportionate amount of our retail sales to occur during our fourth quarter. Our failure to stock or restock popular products in sufficient amounts such that we fail to meet customer demand could significantly affect our revenue and our future growth. When we overstock products, we may be required to take significant inventory markdowns or write-offs and incur commitment costs, which could materially reduce profitability. We regularly experience increases in our net shipping cost due to FBA fee increases, split-shipments, and additional long-zone shipments necessary to ensure timely delivery for the holiday season. If too many customers access the websites on which we engage in online retailing within a short period of time due to increased demand, we may experience system interruptions that make the websites unavailable or prevent us from efficiently fulfilling orders, which may reduce the volume of goods we offer or sell and the attractiveness of our products. In addition, we may be unable to adequately staff for fulfillment of orders and customer service during these peak periods and delivery and other fulfillment companies and customer service co-sourcers may be unable to meet the seasonal demand.

As a result of holiday sales, as of December 31 of each year, our cash, cash equivalents, and marketable securities balances typically reach their highest level (other than as a result of cash flows provided by or used in investing and financing activities). This operating cycle results in a corresponding increase in accounts payable as of December 31. Our accounts payable balance generally declines during the first three months of the year, resulting in a corresponding decline in our cash, cash equivalents, and marketable securities balances.

Continued increases in Amazon Marketplace fulfillment and storage fees could have an adverse impact on our profit margin and results of operations.

The Company utilizes Amazon’s Fulfillment by Amazon (“FBA”) platform to store their products at the Amazon fulfillment center and to pack and distribute these products to customers. If Amazon continues to increase its FBA fees, our profit margin could be adversely affected.

A change in one or more of the Company’s vendors’ policies or the Company’s relationship with those vendors could adversely affect the Company’s results of operations.

The Company is dependent on its vendors to supply merchandise in a timely and efficient manner. If a vendor fails to deliver on its commitments, whether due to financial difficulties or other reasons, the Company could experience merchandise shortages that could lead to lost sales.

Historically, the Company has not experienced difficulty in obtaining satisfactory sources of supply and management believes that it will continue to have access to adequate sources of supply. No individual vendor exceeded 15% of purchases in fiscal 2021.

Our revenue is dependent upon maintaining our relationship with Amazon and failure to do so, or any restrictions on our ability to offer products on the Amazon Marketplace, could have an adverse impact on our business, financial condition and results of operations.

To date, we have generated practically all of our revenue as a third-party seller on Amazon Marketplace. In 2021 and 2020, 100% and 100%, respectively, of our net revenue was through or with the Amazon sales platform. Therefore, we depend entirely on our relationship with Amazon for growth. In particular, we depend on our ability to offer products on the Amazon Marketplace. We also depend on Amazon for the timely delivery of products to customers. Any adverse change in our relationship with Amazon, including restrictions on the ability to offer products or termination of the relationship, could adversely affect our continued growth and financial condition and results of operations.

Our profit is dependent reimbursements from Amazon and any change in Amazon’s policy regarding reimbursement could adversely impact our ability to generate profits

Amazon reimburses us for any lost and damaged merchandise. These reimbursements form a substantial portion of our profits. Any change in Amazon policy regarding these reimbursements could impact our profit adversely. Additionally, we are dependent on Amazon’s ability to track and process these reimbursements. Any deficiencies in Amazon’s ability to process these reimbursements could impact our profits.

| 20 |

Loss of key personnel or the inability to attract, train and retain qualified employees could adversely affect the Company’s results of operations.

The Company believes that its future prospects depend, to a significant extent, on the services of its executive officers. Our future success will also depend on our ability to attract and retain qualified key personnel. The loss of the services of certain of the Company’s executive officers and other key management personnel could adversely affect the Company’s results of operations.

In addition to our executive officers, the Company’s business is dependent on our ability to attract, train and retain qualified team members. Our ability to meet our labor needs while controlling our costs is subject to external factors such as unemployment levels, health care costs and changing demographics. If we are unable to attract and retain adequate numbers of qualified team members, our operations and support functions could suffer. Those factors, together with increased wage and benefit costs, could adversely affect our results of operations.

We may face difficulties in meeting our labor needs to effectively operate our business.

We are heavily dependent upon our labor workforce. Our compensation packages are designed to provide benefits commensurate with our level of expected service. However, we face the challenge of filling many positions at wage scales that are appropriate to the industry and competitive factors. We also face other risks in meeting our labor needs, including competition for qualified personnel, overall unemployment levels, and increased costs associated with complying with regulations relating to COVID-19. Changes in any of these factors, including a shortage of available workforce, could interfere with our ability to adequately service our customers and could result in increasing labor costs.

Our business could be adversely affected by increased labor costs, including costs related to an increase in minimum wage and health care.

Labor is one of the primary components in the cost of operating our business. Increased labor costs, whether due to competition, unionization, increased minimum wage, state unemployment rates, health care, or other employee benefits costs may adversely impact our operating expenses. Additionally, there is no assurance that future health care legislation will not adversely impact our results or operations.

Breach of data security could harm our business and standing with our customers.

The protection of our supplier (vendor), employee and business data is critical to us. Our business, like that of most companies, involves confidential information about our employees, our suppliers and our Company. We rely on commercially available systems, software, tools and monitoring to provide security for processing, transmission and storage of all such data, including confidential information. Despite the security measures we have in place, our facilities and systems, and those of our third-party service providers, may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming or human errors, or other similar events. Unauthorized parties may attempt to gain access to our systems or information through fraud or other means, including deceiving our employees or third-party service providers. The methods used to obtain unauthorized access, disable or degrade service, or sabotage systems are also constantly changing and evolving, and may be difficult to anticipate or detect. We have implemented and regularly review and update our control systems, processes and procedures to protect against unauthorized access to or use of secured data and to prevent data loss. However, the ever-evolving threats mean we must continually evaluate and adapt our systems and processes, and there is no guarantee that they will be adequate to safeguard against all data security breaches or misuses of data. Any security breach involving the misappropriation, loss or other unauthorized disclosure of customer payment card or personal information or employee personal or confidential information, whether by us or our vendors, could damage our reputation, expose us to risk of litigation and liability, disrupt our operations, harm our business and have an adverse impact upon our net sales and profitability. As the regulatory environment related to information security, data collection and use, and privacy becomes increasingly rigorous, with new and changing requirements applicable to our business, compliance with those requirements could also result in additional costs. Further, if we are unable to comply with the security standards established by banks and the credit card industry, we may be subject to fines, restrictions and expulsion from card acceptance programs, which could adversely affect our retail operations.

| 21 |

We face risks related to system interruption and lack of redundancy

We experience occasional system interruptions and delays that make the websites on which we engage in online retailing unavailable or slow to respond and prevent us from efficiently accepting or fulfilling orders or providing services to third parties, which may reduce our net sales and the attractiveness of our products and services. Steps we take to add software and hardware, upgrade our systems and network infrastructure, and improve the stability and efficiency of our systems may not be sufficient to avoid system interruptions or delays that could adversely affect our operating results.

Our computer and communications systems and operations in the past have been, or in the future could be, damaged or interrupted due to events such as natural or man-made disasters, extreme weather, geopolitical events and security issues (including terrorist attacks and armed hostilities), computer viruses, physical or electronic break-ins, and similar events or disruptions. Any of these events could cause system interruption, delays, and loss of critical data, and could prevent us from accepting and fulfilling customer orders and providing services, which could make our product offerings less attractive and subject us to liability. Our systems are not fully redundant and our disaster recovery planning may not be sufficient. In addition, our insurance may not provide sufficient coverage to compensate for related losses. Any of these events could damage our reputation and be expensive to remedy.