UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2023

OR

For the transition period from __________ to __________.

Commission file number: 001-40973

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (786 ) 709-9690

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | x | ||||||||||||||||||

| Non-accelerated filer | o | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the common shares held by non-affiliates of the registrant as of the last business day of the registrant's most recently completed second fiscal quarter was $113.4 million.

The registrant had 57,422,246 shares of common stock outstanding as of February 26, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the 2024 Annual Meeting of Stockholders, or an amendment to Form 10-K

to be filed with the Securities and Exchange Commission not later than 120 days from the end of the registrant’s most

recently completed fiscal year, are incorporated by reference into Part III of this Annual Report on Form 10-K

Table of Contents

| Page | |||||

Signatures | |||||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

We have made statements in the sections titled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Quantitative and Qualitative Disclosures About Market Risk” and in other sections of this Annual Report on Form 10-K that are forward-looking statements. In some cases, you can identify these statements by forward-looking words such as “may,” “might,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential” or “continue,” the negative of these terms and other comparable terminology, but the absence of these words does not mean that a statement is not forward-looking. These forward-looking statements, which are subject to risks, uncertainties and assumptions about us, may include projections of our future financial performance, our anticipated growth strategies and anticipated trends in our business. These statements are only predictions based on our current expectations and projections about future events. You are cautioned that there are important risks and uncertainties, many of which are beyond our control, that could cause our actual results, level of activity, performance or achievements to differ materially from the projected results, level of activity, performance or achievements that are expressed or implied by such forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

Our future results could be affected by a variety of other factors, including, but not limited to, failure to open and operate new centers in a timely and cost-effective manner; inability to open new centers due to rising interest rates and increased operating expenses due to rising inflation; increased competition in the weight loss and obesity solutions market, including

as a result of the recent regulatory approval, increased market acceptance, availability and customer awareness of

weight-loss drugs; shortages or quality control issues with third-party manufacturers or suppliers; competition for surgeons; litigation or medical malpractice claims; inability to protect the confidentiality of our proprietary information; changes in the laws governing the corporate practice of medicine or fee-splitting; changes in the regulatory, macroeconomic conditions, including inflation and the threat of recession, economic and other conditions of the states and jurisdictions where our facilities are located; and business disruption or other losses from war, pandemic, terrorist acts or political unrest.

We discuss many of these risks and uncertainties in “Item 1A. Risk Factors” of this Annual Report on Form 10-K and in other filings we make from time to time with the U.S. Securities and Exchange Commission. There also may be other risks and uncertainties that are currently unknown to us or that we are unable to predict at this time.

Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, level of activity, performance or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements. Forward-looking statements represent our estimates and assumptions only as of the date of this Annual Report on Form 10-K, which are inherently subject to change, and we are under no duty and we assume no obligation to update any of these forward-looking statements, or to update the reasons actual results could differ materially from those anticipated, after the date of this Annual Report on Form 10-K to conform our prior statements to actual results or revised expectations, except as required by law. Given these uncertainties, investors should not place undue reliance on these forward-looking statements.

1

Part I

Item 1. Business

Unless otherwise indicated or the context otherwise requires, references in this Annual Report on Form 10-K to the “Company,” “AirSculpt,” “we,” “us” and “our” refer to AirSculpt Technologies, Inc. and its consolidated subsidiaries and the Professional Associations (as defined hereinafter).

Our Company

AirSculpt is a next-generation body contouring treatment designed to optimize both comfort and precision, available exclusively at AirSculpt offices. The minimally invasive procedure removes fat and tightens skin, while sculpting targeted areas of the body, allowing for quick healing with minimal bruising, tighter skin, and precise results.

We believe our treatment results and elite patient experience have positioned AirSculpt as a preferred body contouring brand. We performed 14,932 body contouring procedures in 2023. Our proprietary and patented AirSculpt® method is minimally invasive because it requires no needle, no scalpel, no stitches and no general anesthesia to achieve transformational change that appears both natural and smooth. Our patients are guided by surgeons, nurses and patient care consultants through every step of the experience.

We have a broad offering of fat removal procedures across treatment areas. We also offer innovative fat transfer procedures that use the patient’s own fat cells to enhance the breasts, buttocks, hips or other areas and do not require silicone or foreign materials to be implanted. Our innovative body contouring procedures include the Power BBL®, a Brazilian butt lift procedure, the Up a Cup™, a breast enhancement procedure, and the Hip Flip™, an hourglass contouring procedure. Our motivation to provide the best body contouring outcomes for our patients fuels our innovation.

Further, the Company introduced AirSculpt® + and AirSculpt® Smooth in fiscal year 2022. AirSculpt® + is a new procedure that permanently removes fat and tightens the skin with unparalleled precision and finesse. Patients first target any area containing excess fat with AirSculpt®, then have that same area treated with a new technology that instantly tightens skin and improves laxity. This advanced, minimally invasive treatment combines helium gas and radiofrequency energy to create a plasma specially equipped to correct sagging skin and restore a youthful, natural appearance. AirSculpt® Smooth delivers effective and long-lasting cellulite reduction with one single treatment. AirSculpt® Smooth uses an advanced cellulite removal tool, which is FDA-cleared to target cellulite on the buttocks and thighs. Results appear almost instantly, and because AirSculpt® Smooth is heat-free, it can be used on any skin type.

Our treatment results—highlighted by a vast gallery of “before and after” photos across gender, body shape and treatment areas—are a powerful tool to build our brand through digital marketing on our website and social media accounts. We also leverage AirSculpt® TV, which takes viewers into procedure rooms to watch our surgeons use AirSculpt® body contouring procedure to achieve dramatic results and hear patient testimonials. We utilize celebrity and influencer endorsements, as well as word-of-mouth referrals, to drive new patient acquisition.

We deliver our body contouring procedures through a growing, nationwide footprint of 27 centers across 18 U.S. states, Canada, and the United Kingdom as of February 27, 2024. Our centers, located in metropolitan and suburban areas, offer a premium patient experience and luxurious, spa-like atmosphere. Due to restrictions on the corporate practice of medicine in many states, the professional associations (each, a “Professional Association,” and collectively, the “Professional Associations”) owned by the surgeons that operate our centers are responsible for all clinical aspects of the medical operations that take place in each of our centers, including contracting with the surgeons who perform procedures on patients at our centers.

We are a holding company and all of our operations are conducted through the Professional Associations and our wholly-owned subsidiaries, which own and operate the non-clinical assets and provide Management Services to the Professional Associations through Management Service Agreements (“MSAs”).

The value proposition provided by our services results in exceptional unit-level economics, which in turn helps to support predictable and recurring revenue and attractive cash flow. Additionally, we require 100% private pay upfront and, therefore, face no reimbursement risk.

Under the stewardship of our founder and Executive Chairman of our board of directors, Dr. Aaron Rollins, our Lead Independent Director, Adam Feinstein, and the other management team members, we have built a results-driven culture. For the year ended December 31, 2023, we generated $195.9 million of revenue compared to $168.8 million for the year ended December 31, 2022, which represents approximately 16.1% growth. Additionally, we have invested in our social media and marketing capabilities to drive our brand awareness and increase consumer acceptance for our procedures. We believe we have significant opportunity to further grow our brand awareness, open new centers in the United States and internationally, and increase sales in our existing centers.

1

Our Growing Market Opportunity

Our Market Opportunity

We operate within the large and growing market for body fat reduction procedures. Our market includes both surgical procedures, such as liposuction and abdominoplasty procedures, as well as non-surgical procedures, such as cryolipolysis, ultrasound, laser lipolysis and other non-surgical body fat reduction procedures. The United States market for body fat reduction procedures was estimated to be $5.2 billion in 2021 by LifeSci Consulting, growing at approximately a 8.8% compound annual growth rate (“CAGR”) since 2017 and expected to grow at a 10% CAGR through 2026, according to Global Market Insights. The global market for body fat reduction procedures was estimated to be in excess of $10 billion in 2021.

The recent regulatory approval, increased market acceptance, availability and customer awareness of weight-loss drugs has

negatively impacted demand in the market for body fat reduction procedures by causing some patients to reject surgical

options in favor of non-invasive and less expensive solutions. It is difficult to predict the long-term outlook of the market

for weight-loss drugs, including their long-term efficacy and potential drawbacks. As a result, we cannot be certain that the

market for body fat reduction procedures which we operate in will continue to grow and that it will not be reduced or

eliminated due to the growth of the market for weight-loss drugs.

Our Growth Drivers

The market for surgical aesthetic procedures is growing, fueled by favorable trends including:

•Self-Image Awareness: increased consumer awareness and focus on beauty consciousness driven by social media and prioritization of healthy lifestyles;

•Social Acceptance: consumers have embraced cosmetic treatment and reduced the social stigma, especially through the proliferation of shared patient photos on social media;

•Improved Safety and Recovery Profile: advances in technology have led to reduced recovery times and introduction of more minimally-invasive procedures;

•Rise in Disposable Income: the global rise in disposable income provides individuals with greater discretionary funds for personal appearance enhancements including cosmetic surgery; and

•Increased Weight Gain in the Overall Population: worldwide prevalence of overweight and obesity in individuals continues to rise.

The combination of these growth drivers continue to propel the market.

Limitations to Existing Procedures

Fat reduction and body contouring procedures have become increasingly popular, but many offerings have significant limitations. Existing procedures for fat reduction or body contouring, other than AirSculpt®, currently include surgical procedures such as liposuction and abdominoplasty (tummy tuck) and non-surgical procedures that use cooling, injected medication or heat to reduce fat cells. We believe these procedures often have limited, inconsistent and less predictable results than AirSculpt®. Many procedures can also involve significant pain and may require excess recovery time post-surgery.

The AirSculpt® Difference

AirSculpt® is a minimally invasive procedure delivered in one session while the patient is awake. Each procedure is done by a trained surgeon for customized and precise results. As for discomfort, patients typically report limited soreness the next day following the procedure. We believe our procedures offer dramatic results to our patients.

Our Competitive Strengths

We attribute our success to the following strengths that differentiate us from our competitors:

Trusted Brand Redefining Body Contouring

The AirSculpt® method was created to offer patients a gentler alternative to traditional fat removal procedures with transformative results delivered in a luxurious, spa-like environment. We specialize in body contouring through the minimally invasive removal of unwanted fat. The proprietary AirSculpt® method empowers our surgeons to use their high level of skill and artistry to deliver dramatic results personalized to our patients.

2

Beneficial Treatment Results and Premium Patient Experience, Underpinned by Proprietary AirSculpt® Technology

We believe that our AirSculpt® procedures offer beneficial results and a premium patient experience. Our AirSculpt® procedures are differentiated by our patented technology, broad and innovative procedures, elite patient experience, and highly skilled surgeons.

•AirSculpt® Technology: Our patented and precision-engineered method, AirSculpt®, permanently removes fat and tightens skin while sculpting targeted areas of the body through minimally invasive body contouring procedures. Unlike traditional liposuction which uses cannulae in a scraping motion, AirSculpt® drives a cannula 1,000 times per minute in a corkscrew motion to remove fat cells while tightening skin simultaneously. It requires no needle, no scalpel, no stitches and no general anesthesia to create dramatically natural, smooth results. AirSculpt® is minimally invasive, providing transformative results, all delivered in one session while the patient is awake.

As of December 31, 2023, our patent portfolio is comprised of two issued U.S. utility patents and one pending U.S. utility patent application, each of which we own directly. The tools we use to perform our fat removal and fat transfer procedures are purchased from third parties, and we do not own the proprietary rights to such tools. Instead of protecting specific, individual liposuction components (such as a particular handpiece design), our issued patents and our pending application relate to certain proprietary implementations of the process described in the section “Our Technique, Training and Equipment,” and the combination of multiple components to form proprietary systems that are specially configured for carrying out those proprietary processes. We believe the systems and methodologies claimed in our issued patents provide impressive results with less patient trauma relative to other systems and methods, such as liposuction and abdominoplasty (tummy tuck), that require more invasive surgical procedures.

•Broad Offering of Innovative, Body Sculpting Procedures: We offer our patients a comprehensive suite of customized body contouring procedures, including fat removal and fat transfer, to meet their wants and needs.

Our fat removal procedures remove a patient’s stubborn fat from a variety of treatment areas, such as the stomach, back and buttocks. We created our popular 48-Hour Six Pack™ procedure to enhance and reveal abdominal muscles in just one session by removing the stubborn pockets of fat hiding one’s six-pack.

We also offer fat transfer procedures, during which our surgeons transfer a patient’s collected fat cells to enhance the buttocks, breast, hips or aging hands to naturally enhance or sharpen a patient’s contours. Some of our most popular fat transfer procedures are:

•Power BBL® (“Brazilian Butt Lift”), which removes a patient’s unwanted fat from areas such as tummy or thighs and transfers it to the buttocks, giving a flatter stomach and slimmer waist, while shaping the buttocks and tightening the skin;

•Up a CupTM Breast Augmentation, which removes a patient’s natural fat, typically from the tummy or thighs, and transfers it to the breasts to increase size by about one cup. AirSculpt® enhanced breasts are all natural. No silicone or other foreign material is implanted; and

•Hip Flip®, which removes unwanted fat from one area of the body and transfers it to the hips to fill in the “hip dip” to create the coveted hourglass figure. It is often performed in combination with the Power BBL®.

We are continuously innovating to better serve our patients. In 2020, we started performing and trademarked the Hip Flip® procedure. Since then, we have continued to innovate and in 2020 we introduced the CankCure® procedure which removes fat and contours the calf and ankle area. In 2022, we introduced AirSculpt® + and AirSculpt® Smooth, as discussed above. We are only in the beginning stages of innovation and have much more to introduce to the body contouring field.

•Premium Patient Experience: We offer our patients a premium consumer experience. From the initial consultation to the day of procedure, our patients are guided by knowledgeable patient care consultants. Our centers are located near high end retail environments, such as Rodeo Drive in Beverly Hills and Fifth Avenue in New York. The centers are designed and furnished with furniture from a high-end retailer with the patient experience in mind, offering a comfortable and calming environment ahead of and after the procedure. In 2020, we began to offer our patients the choice of virtual consults prior to their procedures.

3

•Elite Surgeons: Our surgeons are chosen not only for their medical skills, generally as plastic or cosmetic surgeons, but also for their artistic vision. They are selected to join our nationwide practice because they are at the top of their profession, specialize in body sculpting, and have artistic skill. Before working on AirSculpt patients, each surgeon completes extensive AirSculpt® training to ensure the best results for every patient and treatment.

We offer our surgeons a compelling economic opportunity, with annual compensation for part-time work at AirSculpt often higher than the average full-time salary in a private practice. By joining AirSculpt, surgeons are also able to grow their private practices by attracting Elite patients to their private practice for non-body contouring procedures, such as face lifts and injectables. Our surgeons are also featured on our social media platforms.

AirSculpt® allows the surgeon to provide high quality outcomes to patients while being less physically demanding on the surgeon than traditional liposuction. As AirSculpt® is only available for use at AirSculpt centers, we protect our brand and are able to retain high quality surgeons.

National and International Footprint Fueled by Attractive Unit Economics

We have a growing national footprint consisting of 27 centers across 18 U.S. states, Canada, and the United Kingdom as of February 27, 2024. Our centers are located primarily in metropolitan cities near retail shops that our patients frequent and popular areas. On average, our centers contain two procedure rooms with the capacity to perform up to 36 surgeries a week, in addition to additional consultation offices for prospective patients. Our accreditation as an office-based practice under the Joint Commission demonstrates our commitment to safety and quality. In 2023, we generated revenue per case of $13,121 on average. We require 100% private pay upfront and face no reimbursement risk.

Our centers generate highly attractive unit-level economics and require only a modest investment to open. Given the consistently high level of demand for our services and the average price of our procedures, our centers typically achieve profitability within approximately three months, providing AirSculpt with a highly attractive and near-immediate return on invested capital.

Scaled Platform and Consistent Demand Drives Attractive Growth and Free Cash Flow

Our operating model is highly scalable and enables capital efficient growth. We have generated double digit growth in each of the years since 2015. For the year ended December 31, 2023, we generated approximately $196 million of revenue compared to approximately $169 million for the year ended December 31, 2022, which represents approximately 16.1% growth. We have a capital efficient business that requires minimal maintenance capital expenditures and working capital to support our operations, enabling us to generate strong cash flows to fund future growth. We have achieved consistent, self-funded growth since our founding in 2012 and have accelerated our performance in recent years.

Experienced Founder-Led Management Team to Support Growth

We are led by an experienced team united by our vision to redefine body contouring and a belief in our future growth potential. Our founder and Executive Chairman of our board of directors, Dr. Aaron Rollins, is a celebrity cosmetic surgeon that is recognized as a leader in body sculpting and has been featured across digital, print and TV. Dr. Rollins has been a licensed cosmetic surgeon since 2004. In addition, our Lead Independent Director, Adam Feinstein, who founded Vesey Street Capital Partners, L.L.C., our private equity sponsor (“Sponsor”), has 25 years of experience working with many of the leading healthcare services companies, including service as a member of public and private healthcare company board of directors. Our Chief Financial Officer, Dennis Dean, who has over 20 years of experience in the healthcare industry, including at Envision Healthcare and Surgery Partners, joined the team in 2021 prior to our IPO.

Further, AirSculpt's founder and former Chief Executive Officer, Dr. Aaron Rollins, serves as Executive Chairman of the board of directors. Dr. Rollins is primarily focused on leading the Company’s overall vision and providing strategic guidance. In addition, Todd Magazine became Chief Executive Officer at the end of January 2023. Mr. Magazine brings to AirSculpt more than 30 years of experience in retail operations and brand-building. For the past 10 years, he has been the CEO of Blink Fitness, a subsidiary of Equinox, where he led the company of over 1,500 employees from four locations to over 100 and increased membership 25x. Previously, he was North American President of Pfizer's OTC business, held president's roles for Gatorade and Quaker Oats at PepsiCo, and led various marketing teams at Procter & Gamble. We have built a strong and diverse team across our marketing and operations functions that is highly scalable and capable of supporting future growth. We have a results-driven team culture. We believe our combination of talent, experience, and culture gives us the ability to drive sustainable growth.

Our Growth Strategies

We intend to deliver sustainable growth in revenue and profitability by executing on the following strategies:

•Continue to Grow Our Brand Awareness and Attract New Patients: We believe that consumer trends towards greater acceptance of body contouring and cosmetic treatments will continue to expand the market for our services.

4

We believe we are a leading provider of body contouring procedures and that there is a significant opportunity to drive awareness and adoption of our AirSculpt® method and procedure offerings.

•Continue to Drive Sales Growth of Our Centers: We employ the following strategies to increase our procedures performed and drive higher revenue per procedure with the aim of continuing to accelerate our growth in existing centers:

◦Continue to add new procedure rooms: Our centers typically have two procedure rooms. We have the opportunity to continue to both add procedure rooms and adapt our schedule from primarily open six days to seven days a week in order to meet the strong demand from our patients for our services. Through referral and outreach, we plan to continue recruiting surgeons to operate on our growing number of patients and staff to conduct consultations and organize appointments.

◦Increase speed and efficiency of patient onboarding to increase utilization and reduce patient waiting times: We have and will continue to execute initiatives that increase the speed through which patients convert from initial consultation to procedure. These initiatives include hiring additional sales support staff to respond to patient inquiries and utilizing virtual consultations that enable our patients to speak with surgeons and qualified patient care representatives in the convenience of their own home or office, making it easier and quicker to schedule a procedure and reduce overall waiting time.

◦Continue to introduce new, innovative procedures: Since our founding in 2012, we have demonstrated our ability to innovate with the novel introduction of the AirSculpt® method to the cosmetic surgery field. Over the past decade, we have generated more revenue per patient, which we believe is a direct result of our successful introduction of new procedures to meet our patients’ needs. Fat transfer has been a highly successful innovation and is now a critical component of our offering, enabling the artistry of many of our most popular and highest revenue procedures. We also continue to develop new procedures, such as the Hip Flip® and CankCure®, to meet our patients’ demand and drive traffic to our centers.

◦Increase prices on procedures: We have an ability to increase prices on our procedures driven by the strong value proposition that our services offer to our patients.

We employ the following strategies to drive brand awareness:

•Developing digital content, including a “before and after” photo gallery and AirSculpt® TV: We have collected a catalog of over 215,000 “before and after” photos, showcasing our treatment outcomes. Our AirSculpt® TV program, featured on our AirSculpt Instagram page and website, provides a never-before seen transparency in our space, encouraging further growth. We will continue to develop high quality digital content that highlights the transformative power of our minimally invasive procedures.

•Social, digital and traditional marketing: Our in-house marketing team generates continuous media coverage of our offering across social, digital, and traditional media channels, such as magazines and TV. By using web-based lead generation, we generate over 450,000 monthly website visits, primarily through optimized spend on Google’s marketing engine.

•Celebrity endorsements: We collaborate with celebrity influencers and TV personalities to drive continuous media coverage that raises brand awareness and social acceptance of our procedures.

•Patient testimonials: Our patients are some of the best advocates for our brand, with many recommending our procedures to family and friends. We encourage our patients to share their “before and after” photos on social media.

We employ the following strategies to expand our footprint:

•Expand Footprint by Opening New Centers in the United States: We believe our track record of successfully opening new AirSculpt centers consistently generating strong unit-level economics validates our strategy across the United States and to domestically expand our footprint. In order to ensure our new centers are profitable, we follow the same business plan for each new center. A new center is generally profitable within the first few months of opening, supported by our 100% upfront private pay policy. We have strong conviction in our ability to continuously improve our unit economics as we open additional centers in the United States. With our patient care consultants and surgeons performing virtual consultations ahead of store openings, we are able to pre-book procedures and can begin performing surgeries on a center’s opening day, accelerating the ramp up of those centers.

•Disciplined Approach to Choosing Potential Markets: Management uses a disciplined approach to choose potential markets, opening centers at minimal cost located near premium retail shops that our patients frequent. We believe

5

there is a significant domestic growth opportunity and will continue to opportunistically evaluate new center openings and target opening three to four centers each year.

•Expand Internationally: We believe our brand has global appeal. We draw clients from international markets that travel to our existing centers for body contouring procedures. We believe there is significant opportunity to open new centers in densely populated, affluent international metropolitan regions. We opened our first international facility in Toronto, Canada in December 2022, and our second in London, United Kingdom in June 2023.

6

Our Technique, Training and Equipment

AirSculpt® is a proprietary, patented method of tumescent liposuction that removes unwanted fat from several targeted areas of the body in a minimally invasive procedure, producing dramatic results. By contrast to traditional liposuction, AirSculpt® requires no needle, no scalpel, no stitches and no general anesthesia, with patients remaining awake during the procedure. We train our surgeons in the AirSculpt® procedure, for which we possess a patent covering the process. Our surgeons are contractually prohibited from performing AirSculpt’s proprietary procedures, including the AirSculpt® procedure, if they leave AirSculpt.

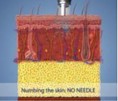

1. Pain Management |  | Prior to the procedure, patient is given a sedative cocktail and local anesthesia via air pressure from a needleless jet injector. *Patient remains fully awake during the procedure | ||||||

| 2. Access Point Creation |  | One to three entryways are created by the jet injector, which are widened to 2mm (freckle-sized) by means of a biopsy punch. | ||||||

| 3. Local Numbing |  | A thin cannula is inserted in each entryway, at which point a local numbing solution is dispersed subdermally to the target areas. | ||||||

| 4. Fat Removal Process |  | Proprietary fat removal process uses industry accepted, FDA approved tools to grab, separate, and remove fat cells. An FDA-approved handpiece drives cannula 1,000 times per minute in a corkscrew motion to remove fat cells, without harming surrounding tissue and structures. The amount of fat removed via the AirSculpt® method depends on patient body size, desired outcomes and state regulations. After the procedure is complete, a piece of dry gauze is used to cover the entryway to protect against infection. | ||||||

7

Across our centers, we use a network of independent surgeons to perform the AirSculpt® procedure. We believe that the desire to be an AirSculpt surgeon has provided us with ready access to talented providers, making recruitment a selective process. Additionally, through referral and outreach, we plan to continue recruiting surgeons to perform procedures on our growing number of patients. We conduct background checks on prospective surgeons, confirming licensure and checking surgeon records contained in the National Practitioner Data Bank. Furthermore, we consider the body of work of prospective surgeons, including before and after photos and areas of specialization. Following this initial selection process, our prospective surgeons undergo in-house training through the Elite Fellowship Program where they receive proprietary information regarding the AirSculpt® method and approved body markings, observe videos of experienced AirSculpt® surgeons, observe those surgeons complete eight to ten procedures in-person, and later complete three procedures under the in -person supervision of those surgeons. If a prospective surgeon successfully completes the Elite Fellowship Program, they are permitted to conduct the AirSculpt® method without restrictions. Otherwise, they are observed in additional training procedures or are not chosen to join the AirSculpt team. Additionally, there is a comprehensive ongoing review process of all surgeons conducted by our experienced AirSculpt® surgeons, which includes on-site visits at centers to help maintain quality standards, and feedback from other staff members, including members of our nursing team.

In connection with the AirSculpt® method, we currently use an FDA-approved handpiece manufactured by Euromi S.A., a Belgian company that specializes in the manufacturing and distribution of medical, dermatological and plastic surgery products, and other FDA- approved parts, such as the cannula and vacuum pump, from other manufacturers. The handpiece we use costs significantly more than other handpiece models, and we believe it is more powerful while being gentler for the patient, helping to produce better results. Some of the other parts used are customized for us by our suppliers for our procedure. Although using FDA-approved equipment in medical procedures is the practice of medicine and does not itself require further FDA review or approval, FDA regulations require that we report certain information about adverse medical events if our AirSculpt® procedures have caused or contributed to those adverse events.

While we recruit our surgeons with a focus on excellence and skill, the handpiece we use in connection with the AirSculpt® method is designed to automatically shut off if any issues are detected in the process (e.g., excessive heat levels). As of the date of this Annual Report on Form 10-K, we are not aware of any adverse events in connection with the AirSculpt® procedure that would require reporting under any regulations.

We are continuously working to innovate to make the AirSculpt® procedure easier to perform, deliver enhanced results, and be more pleasant for our patients, all with a goal of providing the best body contouring results possible. Moreover, we continue to develop AirSculpt® for new procedures and also seek to incorporate new technologies into our current procedures.

Center Format and Selection

Our centers are approximately 3,000 square feet each and are typically open six days per week, with select centers open seven days per week, from 9 am to 5 pm. Certain centers may operate outside of typical hours to accommodate client schedules. Most existing locations have two procedure rooms. Our centers are typically staffed by three surgeons, who are independent contractors, nurses, office managers, sales consultants, sales assistants and front desk concierges/administrative assistants.

Our target markets include affluent metropolitan and suburban areas. We conduct in-person site visits to proposed center locations. We use a disciplined approach when opening de novo centers and conduct extensive diligence of potential markets through social research, economic analysis of each market and conduct in-person site visits to proposed center locations.

Our Marketing and Sales Efforts and Third-Party Financing

Our marketing efforts are driven by an in-house team of professionals that focus on digital and other platforms. In addition to monitoring and managing our social media presence, our team is focused on search engine optimization on our digital platform. For the year ended December 31, 2023, our total advertising costs were $25.9 million, split approximately 85% digital advertising and 15% other advertising platforms.

Selling expenses consist of advertising costs for social, digital and traditional marketing and sales and marketing personnel. Our total selling expenses for 2023 were approximately $36.8 million, or approximately 18.8% of revenue. Our customer acquisition costs were approximately $2,465 per customer in 2023.

Our sales assistants respond to inquiries from prospective patients and schedule virtual or in-person consultations. Starting in 2020, we began to offer our patients the choice of a pre-procedure virtual consult. Rather than making an in-office appointment, our patients are able to speak with our surgeons and qualified patient care consultants in the convenience of their own home or office typically within 24-72 hours. We encourage a strong relationship between our patients and surgeons, from initial consultation, through procedure, to after treatment. Nearly all of our patient-facing consultants are

8

former patients and can speak to their personal AirSculpt experiences. Based on these efforts, together with discussions with our surgeons, our patients elect to move forward and schedule a procedure date. Many patients, satisfied with results and experience, return to AirSculpt to receive further AirSculpt® treatments on additional body parts.

Our consultants provide patients pricing information the day of their consult and, if requested by the patient, assist patients with securing third-party financing from entities such as CareCredit, Cherry and Alphaeon, among others, enabling consumers to more quickly schedule their procedures. We do not face any risk in default of payment under that financing arrangement, which is solely between the patient and third party financing vendor. In 2023, approximately 47% of our cases involved the patient securing third-party financing.

Our Intellectual Property

As of December 31, 2023, our patent portfolio is comprised of two issued U.S. utility patents and one pending U.S. utility patent application, each of which we own directly. The tools we use to perform our fat removal and fat transfer procedures are purchased from third parties and we do not own the proprietary rights to such tools. Instead of protecting specific, individual liposuction components (such as a particular handpiece design), our issued patents and our pending application relate to certain proprietary implementations of the process described in the section “Our Technique, Training and Equipment,” and the combination of multiple components to form proprietary systems that are specially configured for carrying out those proprietary processes. We believe the systems and methodologies claimed in our issued patents provide impressive results with less patient trauma relative to other systems and methods, such as liposuction and abdominoplasty (tummy tuck), that require more invasive surgical procedures. In general, patents have a term of 20 years from the application filing date or earliest claimed non-provisional priority date. We expect our issued patents to expire in 2033 or later.

AirSculpt®, AirSculpt+®, AirSculpting™, AirSculpt Plus™, Elite Body Sculpture®, RevisionSculpt®, AirSculpt Lift™, No Needle, No Scalpel, No Stitches®, If You Can Pinch It, We Can Take It®, Power BBL®, Tiny Tuck®, 48 Hour Six Pack®, AirSculpt is for Everybody®, Cure for the Hip Dip®, Hip Flip®, CankCure®, Stubborn Fat, It’s All We Do®, The 48 Hour Difference™, What a Difference A Day Makes™, and our logo are U.S. registered trademarks or trademarks for which registration is pending in the United States. We have also registered AirSculpt® and certain other trademarks outside of the United States.

We seek to protect our intellectual property by filing patent applications in the United States related to our procedures that are important to our business. We rely on a combination of confidentiality, non-disclosure and assignment of invention agreements with our employees, surgeons, consultants, contractors and other partners and collaborators. We further rely on copyright, trademark and trade secret laws to protect our brands, proprietary technologies, know-how, data, and copyrighted content (including our library of before and after photographs).

Competition

We believe that our brand recognition and minimally invasive procedures with results meeting or exceeding our customer expectations distinguish us in the rapidly growing market for body contouring.

While we believe we are transforming and growing the body contouring market, our primary competition includes individual and small practice group providers of traditional liposuction, which we believe require a longer patient recovery time than AirSculpt® and some national providers of other minimally-invasive techniques, which we believe are less effective than AirSculpt®. Additionally, university and hospital systems, medical spas and centers and beauty and rejuvenation centers include the body contouring services in their offerings. While we primarily operate in the body

contouring market, we also compete with companies that offer non-surgical methods of fat reduction, including weight-loss

drugs, and other non-invasive weight loss and obesity solutions. Because of the high growth potential of the market for

weight loss and obesity solutions, existing and potential competitors have historically dedicated, and will continue to

dedicate, significant resources to aggressively develop and commercialize their products.

The areas in which we compete include:

•Patients: We compete for patients to utilize our procedures through our marketing efforts and exceptional brand reputation.

•Procedure Offering: We compete with providers of liposuction, abdominoplasty (tummy tuck) and gastric bypass surgery, weight-loss drugs and non-surgical procedures that use cooling, injected medication or heat to reduce fat cells. Many procedures can also involve significant pain and may require excess post-surgical recovery time.

9

•Surgeons and other professionals: We compete for high quality surgeons and other professionals across the body contouring and cosmetic surgery industry to ensure we are able to continue to provide our patients with a smooth process, premium service, and high quality results.

The principal competitive factors that companies in our industry need to consider include, but are not limited to: enhanced products and services, procedure safety, competitive pricing policies, vision for the market and procedure innovation, strength of sales and marketing strategies, technological advances, brand awareness and reputation, and access to financing. We believe we compete favorably across all of these factors and we have developed a business model that is difficult to replicate.

Surgeon Practice Structure

Due to the prevalence of the corporate practice of medicine doctrine, including in many of the states where we conduct our business, our affiliated surgeons are organized in traditional physician practice group structures.

In accordance with applicable state laws, our surgeons have exclusive control and responsibility for all clinical decision-making and the provision of medical care to patients. The Professional Associations are set up as legal entities, separate from AirSculpt, organized in accordance with applicable state laws regarding the types of entities that may operate a physician practice group. Each of the Professional Associations under which our affiliated surgeons operate is owned by a licensed, qualified physician. Our structure enables more effective and efficient sharing of results among our affiliated surgeons, including with respect to educating and training them as to best demonstrated clinical processes, provides them with access to our sophisticated information systems, and helps to shield us from professional liability.

Each of the Professional Associations contracts with surgeons to provide body contouring services to its patients. Each such surgeon must hold an active license to practice medicine in the state where the applicable Professional Association operates. In most cases, surgeons enter into independent contractor agreements with the applicable Professional Association, under which the surgeon is paid a percentage of the professional fees collected by the Professional Association for each surgery the surgeon personally performs, net of any adjustments for financing fees, patient refunds, or any other allowances applicable to the services provided. A typical agreement with our surgeons will have a term of two to three years. The Professional Associations are generally responsible for billing patients for services rendered by our surgeons. Subject to applicable state laws governing enforceability of restrictive covenants relating to physicians, our surgeons contracted by the Professional Associations have agreed not to compete during the contracted period and have agreed not to use or disclose AirSculpt’s proprietary information, including the AirSculpt® procedure, even after the terms of their respective contracts.

Management Services Agreements

We have entered into MSAs with each of the Professional Associations, under which the Company, through its wholly-owned subsidiaries, provides the Professional Associations with exclusive, administrative, management and other business support services, including, but not limited to, billing and collection, accounting, legal, human resources, information technology, compliance and recruiting assistance (the “Management Services”). The Professional Associations retain exclusive control and responsibility for all clinical aspects of the practice of medicine and the delivery of medical services and for contracting with all surgeons and other licensed professionals performing procedures through the Professional Associations. The MSAs are long-term in nature, typically with an initial term of 10 years that automatically renews for successive 5 year terms unless either party provides notice not to renew before the end of the then-current term, subject only to a right of termination in the case of uncured material breach. Under the terms of the MSAs, and subject to state laws and other regulations governing professional fee-splitting, our wholly-owned subsidiaries are typically paid either a flat monthly fee or where permitted, a monthly fee structured as (i) a flat dollar amount for all marketing and advertising advice, assistance, and services provided and (ii) a fee equal to a percentage of the Professional Association’s gross revenues for the applicable month. These agreements also generally provide opportunities for supplemental bonuses. In addition, the Professional Associations have also agreed to reimburse us for certain expenses. See “Governmental Regulation—State Corporate Practice of Medicine and Fee-Splitting Laws.”

10

Continuity Agreements

We have entered into Continuity Agreements at all of our Professional Associations, with the exception of New York, with Dr. Rollins and the other Surgeon Owners, whereby they are the sole directors, officers, and owners of the Professional Associations. The Continuity Agreements (i) prohibit the Surgeon Owners from freely transferring or selling their interests in the Professional Associations, (ii) provide for the ability to add a second Surgeon Owner to help ensure continuity of the Professional Association, and (iii) provide that the ownership interests of the Surgeon Owners will automatically be transferred to another licensed professional designated by us in accordance with the terms of the Continuity Agreement upon the occurrence of certain events, which include, but are not limited to, the Surgeon Owner’s death, the termination of the Surgeon Owner’s employment, the Surgeon Owner’s license to practice medicine being revoked or terminated, the Surgeon Owner filing a petition for bankruptcy, the Surgeon Owner becoming indicted for or convicted of any felony or any misdemeanor offense involving moral turpitude, the Surgeon Owner breaching any provision of the Continuity Agreement, the Surgeon Owner’s gross negligence, willful misconduct or fraud with respect to the Professional Association, and the Surgeon Owner’s disability or incapacity.

Each Continuity Agreement will remain in effect until it is terminated (i) by written agreement signed by or on behalf of each party, (ii) upon the 21-year anniversary of the death of the Surgeon Owner, or (iii) only by the manager (being our wholly-owned subsidiaries), upon at least 30 days prior written notice of such termination to the Professional Association.

Governmental Regulation

Our business and the healthcare industry generally are highly regulated. While we believe that we have structured our agreements and operations in material compliance with applicable healthcare laws and regulations, there can be no assurance that we will be able to successfully address changes in the current regulatory environment or changes in interpretation of existing laws and regulations. We believe that our business operations materially comply with applicable healthcare laws and regulations. However, some of the healthcare laws and regulations applicable to us are subject to limited or evolving interpretations, and a review of our business or operations by a court, law enforcement or a regulatory authority might result in a determination that could have a material adverse effect on us. Furthermore, the healthcare laws and regulations applicable to us may be amended or interpreted in a manner that could have a material adverse effect on our business, prospects, results of operations and financial condition.

Licensing, Medical Practice, Certification

The practice of medicine, including the performance of surgery, is subject to various federal, state and local certification and licensing laws, regulations, approvals and standards, relating to, among other things, the adequacy of medical care, the practice of medicine (including the provision of remote care and consultations), equipment, personnel, operating policies and procedures, prerequisites for the prescription of medication, ordering tests and other professional services.

Physicians, surgeons and licensed professionals who provide professional medical services to patients must hold a valid license to practice medicine or otherwise be certified or qualified to provide the licensed professional service in the state in which the patient is located. Failure to comply with these laws and regulations could result in licensure actions against the professionals, rendered services being found to be non-reimbursable, or prior payments being subject to recoupments and can give rise to civil, criminal or administrative penalties. Our centers are operated as physician office-based practices, which generally rely on the licenses of the surgeons performing medical services through the affiliated Professional Associations at our locations, as well as other permits and licenses including CLIA certifications, medical waste permits, and local operating permits. Some states also require the applicable Professional Association to hold its own clinic license or permit. Through the affiliated Professional Associations, we voluntarily seek accreditation from The Joint Commission for all of our centers. The Joint Commission is a not-for-profit with over 70 years of experience in health care accreditation. Accreditation and certification for each of our centers requires an on-site evaluation of the quality and safety of patient care. A leading nationally-recognized accreditation, for an office-based practice, demonstrates our commitment to safety and quality. Our ability to operate profitably will depend in part upon our centers, the affiliated Professional Associations and their surgeons obtaining and maintaining all necessary licenses and other approvals and operating in compliance with applicable healthcare regulations. Failure to do so could have a material adverse effect on our business.

Our centers are subject to other federal, state and local laws dealing with issues such as occupational safety, employment, medical leave, insurance regulations, civil rights, discrimination, building codes and other environmental issues. Federal, state and local governments are expanding the regulatory requirements on businesses like ours. The imposition of these regulatory requirements may have the effect of increasing operating costs and reducing the profitability of our operations.

State Corporate Practice of Medicine and Fee-Splitting Laws

The laws in many of the states in which we operate or may in the future operate, prohibit entities owned by non-physicians from practicing medicine, exercising control over surgeons, employing surgeons or otherwise interfering with the

11

independent professional judgment of surgeons. This prohibition on the corporate practice of medicine, is intended to prevent unlicensed persons from interfering with the practice of medicine by licensed surgeons or interfering in any way with the independent professional judgment of physicians as it pertains to patient treatment and related clinical matters. Activities other than those directly related to the delivery of healthcare may be considered an element of the practice of medicine in many states. In certain states where we currently, or in the future, may operate, the corporate practice of medicine doctrine and other licensed professions restrictions may be implicated by decisions and activities such as contracting, setting rates and the hiring and management of clinical or licensed personnel. Many states also have regulations that prevent professional fee-splitting, which is the unlawful sharing of professional fees with unlicensed persons or entities owned by unlicensed persons, often in connection with referrals or other business generated by such persons. Corporate practice of medicine and fee splitting laws and rules vary from state to state and are not always consistent. In addition, these requirements are subject to broad interpretation and enforcement by state regulators. Thus, regulatory authorities or other persons, including the Professional Associations’ contracted surgeons, may assert that, notwithstanding the careful structuring of our management arrangements, that we are engaged in the corporate practice of medicine or that the fees earned by us under our contractual arrangements with the Professional Associations constitute unlawful fee splitting. In such event, failure to comply could lead to adverse judicial or administrative action against us and/or our surgeons, civil, criminal or administrative penalties, receipt of cease and desist orders from state regulators, loss of provider licenses, the need to make changes to the terms of engagement with the Professional Associations (or their terms of engagement with their contracted surgeons), in each case that interfere with our business, our profitability and may have other materially adverse consequences.

Healthcare Fraud and Abuse Laws

Even though our services are not currently covered by any government healthcare program or other third-party payor, the laws in some of the states in which we operate, or may in the future operate, prohibit surgeons and other healthcare providers from referring patients to centers in which the surgeon or other healthcare provider has a financial interest unless an exception applies or providing any form of remuneration or a “kickback” for referrals of patients for medical items or services. Some state fraud and abuse laws apply to items or services reimbursed by any payor, including patients and commercial insurers, not just those reimbursed by a federally funded healthcare program. Because of the breadth of these laws and the narrowness of available statutory and regulatory exceptions, it is possible that some of our business activities could be subject to challenge under one or more of such laws. If we or our operations are found to be in violation of any of these laws or any other governmental regulations that apply to us, we may be subject to penalties, including civil and criminal penalties, damages, fines, imprisonment and the curtailment or restructuring of our operations, any of which could materially adversely affect our ability to operate our business and our financial results.

Antitrust Laws

The federal government and most states have enacted antitrust laws that prohibit certain types of conduct deemed to be anti-competitive. These laws prohibit price fixing, concerted refusal to deal, market monopolization, price discrimination, tying arrangements, acquisitions of competitors and other practices that have, or may have, an adverse effect on competition. Violations of federal or state antitrust laws can result in various sanctions, including criminal and civil penalties. Antitrust enforcement in the healthcare industry is currently a priority of the Federal Trade Commission (the “FTC”). We believe we are in compliance with federal and state antitrust laws, but courts or regulatory authorities may reach a determination in the future that could have a material adverse effect on our business, prospects, results of operations and financial condition.

Employees

As of December 31, 2023, we employed approximately 346 full-time employees and approximately 35 part-time employees. We also had contracts with approximately 90 surgeons. While each center varies depending on its size, case volume and case types, we employ an average of approximately 10 full-time equivalent employees at our centers.

While we provide “full-time equivalent” information, a number of our employees work on flexible schedules rather than full-time, which increases our staffing efficiency. As a result, these employees also do not participate in our benefits structure, which we believe reduces the relative cost of our benefits plans to us. None of our employees is represented by a collective bargaining agreement.

Additional Information

The Company was founded by Dr. Rollins in 2012 and reorganized in 2018 as part of the acquisition by our Sponsor of a majority stake in the company prior to the IPO. AirSculpt Technologies, Inc. was incorporated in Delaware on June 30, 2021 and completed an IPO on October 28, 2021.

12

Our website address is www.airsculpt.com and our investor relations website is located at https://investors.elitebodysculpture.com. The information posted on our website is not incorporated into this Annual Report. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”) are available free of charge on our investor relations website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission (“SEC”).

13

Item 1A. Risk Factors

We are subject to risks and uncertainties that could cause our actual financial condition, results of operations, business and prospects to differ materially from those contemplated by the forward-looking statements contained in this report or our other filings with the SEC. Some of these risks and uncertainties are discussed below. If any of the following risks, or other risks and uncertainties, actually occurred, our business, financial condition and operating results could suffer.

The following is a summary of some of these risks:

Risk Factors Summary

We are providing the following summary of the risk factors contained in this Annual Report on Form 10-K to enhance the readability and accessibility of our risk factor disclosures. We encourage you to carefully review the full risk factors contained in this Annual Report on Form 10-K in their entirety for additional information regarding the material factors that make an investment in our securities speculative or risky. These risks and uncertainties include, but are not limited to, the following:

Risks Related to Our Business

•Macroeconomic trends including inflation and rising interest rates may adversely affect our financial condition and results of operations.

•We have a limited operating history and our past results may not be indicative of our future performance.

•Our success depends on our ability to maintain the value and reputation of the AirSculpt® brand.

•We have grown rapidly in recent years and have limited operating experience at our current scale of operations.

•Our financial results will be harmed if there is not sufficient patient demand for AirSculpt® procedures.

•Our success depends largely upon patient satisfaction with the effectiveness of the AirSculpt® procedure.

•We may fail to open and operate new centers in a timely and cost-effective manner.

•We may not be able to successfully continue to expand in markets outside of North America.

•If our competitors are able to develop and market solutions that are safer, more effective, easier to use or more

readily adopted by patients and healthcare providers, our commercial opportunities may be reduced or eliminated.

•Increasing scrutiny and evolving expectations from customers, regulators, investors, and other stakeholders with respect to our environmental, social and governance practices may impose additional costs on us or expose us to new or additional risks.

•Our business, financial condition and results of operations could be adversely affected by disruptions in the global economy resulting from the ongoing military conflict between Russia and Ukraine.

•Use of social media may materially and adversely affect our reputation or subject us to fines or other penalties.

•Our business relies heavily on email and other messaging services, and any restrictions on the sending of emails or messages or an inability to timely deliver such communications could materially adversely affect our net revenue and business.

•Changes in laws and regulations related to the internet, perceptions toward the use of social media and changes in internet infrastructure itself may diminish our ability to drive new customer acquisition.

•Regulations related to healthcare may hamper our availability to provide virtual consultations.

•We face competition for surgeons and other workers that provide our medspa and cosmetic services.

•We outsource the manufacturing of key elements of the tools we use for AirSculpt® procedures to a single third-party manufacturer, Euromi, who is dependent upon third-party suppliers.

•In some jurisdictions, we are precluded or limited in our ability to enter into non-compete agreements with our surgeons.

•Our centers and our affiliated Professional Associations may become subject to medical liability claims.

•Our revenue could decline due to changes in credit markets and decisions made by credit providers.

•We may be adversely affected if we lose any member of our senior management.

•The interests of our Sponsor may conflict with the interests of the Company and its other stockholders.

•Our leverage could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and expose us to interest rate risk.

•Restrictive covenants in our debt instruments may adversely affect us.

•Any failure to meet our debt service obligations could have a material adverse effect on our business, prospects, results of operations and financial condition.

•We are a holding company with no operations of our own.

14

•Our variable rate debt exposes us to risks associated with rising interest rates, including as a result of the phase out

of LIBOR, which could adversely affect our cash flows.

•If there is a change in accounting standards by the Financial Accounting Standards Board or the interpretation thereof affecting consolidation of entities, it could have a material adverse effect on our consolidation of total revenue derived from the Professional Associations.

•Our management team has limited experience managing a public company.

•Our centers may be adversely impacted by weather and other factors beyond our control, and disruptions in our disaster recovery systems or management continuity planning could limit our ability to operate our business effectively.

•Use and storage of paper medical records increases risk of loss, destruction and could increase human error with respect to documentation and patient care.

•Our internal computer systems, or those of any of our manufacturers, other contractors, consultants, or collaborators, may fail or suffer security or data privacy breaches or other unauthorized or improper access to, use of, or destruction of our proprietary or confidential data, employee data, or personal data.

•Security breaches, loss of data, and other disruptions could compromise sensitive information related to our business or our patients, or prevent us from accessing critical information or systems and expose us to liability, and could adversely affect our business and our reputation.

Risks Related to Intellectual Property

•Our competitors could develop and commercialize procedures and products similar or identical to ours.

•We may become a party to intellectual property litigation or administrative proceedings that could be costly and could interfere with our ability to market and perform our services.

•If we are unable to protect the confidentiality of our other proprietary information, our business and competitive position may be harmed.

•We may not be able to protect our intellectual property rights throughout the world to the same extent as in the United States.

Risks Related to Government Regulations

•If we fail to comply with numerous laws and regulations relating to the operation of our centers, we could incur significant penalties or other costs or be required to make significant changes to our operations.

•AirSculpt® procedures may cause or contribute to adverse medical events that we are required to report to the FDA and if we fail to do so, we could be subject to sanctions that would materially harm our business.

•If laws governing the corporate practice of medicine or fee-splitting change, we may be required to restructure some of our relationships.

•We may be subject to various federal and state laws pertaining to healthcare fraud and abuse, including anti-kickback, self-referral, false claims and fraud laws, and any violations by us of such laws could result in fines or other penalties.

•We are subject to numerous environmental, health and safety laws and regulations, and must maintain licenses or permits, and non-compliance with these laws, regulations, licenses, or permits may expose us to significant costs or liabilities.

•Certain risks are inherent in providing prescription and over the counter (“OTC”) treatments, and our insurance may not be adequate to cover any claims against us.

•We are subject to rapidly changing and increasingly stringent laws, regulations, industry standards, and other obligations relating to privacy, data protection, and data security. The restrictions and costs imposed by these requirements, or our actual or perceived failure to comply with them, could materially harm our business.

Risks Related to Ownership of Our Common Stock

•We are an “emerging growth company,” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

•Our stock price could be extremely volatile, and, as a result, you may not be able to resell your shares at or above the price you paid for them.

•There may be sales of a substantial amount of our common stock by our current stockholders, and these sales could cause the price of our common stock to fall.

15

•Certain of our directors and executive officers hold a substantial portion of our common stock, which may lead to conflicts of interest with other stockholders over corporate transactions and other corporate matters.

•Provisions in our charter documents and Delaware law may deter takeover efforts that could be beneficial to stockholder value.

•We have no plans to pay cash dividends on our common stock for the foreseeable future.

•Our internal controls may not be effective.

•The requirements of being a public company may strain our resources and distract our management, which could make it difficult to manage our business.

•Our stock price and trading volume could decline if securities or industry analysts do not publish research or publish inaccurate or unfavorable research about our business.

•We may be subject to securities litigation, which is expensive and could divert management attention.

Risks Related to Our Business

Macroeconomic trends including inflation and rising interest rates may adversely affect our financial condition and results of operations.

Macroeconomic trends, including increases in inflation and rising interest rates, may adversely impact our business, financial condition and results of operations. Rising inflation could have an adverse impact on our operating expenses and our credit facilities and there is no guarantee that we would be able to mitigate its impact. Increases in interest rates on any of our debt will result in higher debt service costs, which will adversely affect our cash flows. We cannot assure you that our access to capital and other sources of funding will not become constrained, which could adversely affect the availability and terms of future borrowings. Such future constraints could increase our borrowing costs, which would make it more difficult or expensive to obtain additional financing or refinance existing obligations and commitments, which could slow or deter future growth.

We have a limited operating history and our past results may not be indicative of our future performance. Further, our revenue growth rate is likely to slow as our business and our market matures.

We began operations in 2012. We have a limited history of generating revenue. As a result, our historical revenue growth should not be considered indicative of our future performance. In particular, we have experienced periods of high revenue growth, including most recently, during the global pandemic, that we do not expect to continue as the business, and the body contouring market, matures. Estimates of future revenue growth and future growth rates are subject to many risks and uncertainties and our future revenue may differ materially from our projections. We have encountered, and will continue to encounter, risks and difficulties frequently experienced by growing companies in rapidly changing industries, including market acceptance of our procedures, attracting new patients, hiring surgeons and responding to increasing competition and expenses as we expand our business. We cannot be sure that we will be successful in addressing these and other challenges we may face in the future, and our business may be adversely affected if we do not manage these risks.

Our success depends on our ability to maintain the value and reputation of the AirSculpt® brand.

We believe that our brand is important to attracting patients and high-quality surgeons. Maintaining, protecting, and enhancing our brand depends largely on our ability to deliver results for our patients and the success of our marketing efforts. We believe that the importance of our brand will increase as competition further intensifies. Our brand could be harmed if we fail to achieve these objectives or if our public image were to be tarnished by negative publicity. Unfavorable publicity about us, including our procedures and technology, could diminish confidence in the AirSculpt® brand. Such negative publicity also could have an adverse effect on our business, financial condition, and operating results.

We have grown rapidly in recent years and have limited operating experience at our current scale of operations. If we are unable to manage our growth effectively, our brand, company culture, and financial performance may suffer.

We have expanded rapidly and have limited operating experience at our current size. To effectively manage and capitalize on our growth, we must continue to expand our marketing, focus on innovation and upgrade our management information systems and other processes. Our continued growth could strain our existing resources and we could experience ongoing operating difficulties in managing our business across numerous jurisdictions, including difficulties in hiring, training, and managing surgeons and other staff in our centers through the Professional Associations. Failure to scale and preserve our high-performance, results-driven culture during this period of growth could harm our future success. If we do not adapt to meet these evolving challenges or if our management team does not effectively scale with our growth, we may experience erosion to our brand and our company culture may be harmed.

16

Our growth strategy contemplates expanding our footprint by opening new centers around the world. Many of our centers are relatively new and we cannot assure you that these centers or that future centers will generate revenue comparable with those generated by our more mature locations, especially as we move to new geographic markets. Further, many of our centers are leased pursuant to multi-year leases, and our ability to negotiate favorable terms on an expiring lease or for a lease renewal option may depend on factors that are not within our control. Expanding internationally will require significant additional investment. Successful implementation of our growth strategy will require significant expenditures before any substantial associated revenue is generated and we cannot guarantee that these increased investments will result in corresponding and offsetting revenue growth.

Our planned expansion will place increased demands on our existing operational, managerial, and administrative resources. These increased demands could strain our resources and cause us to operate our business less effectively, which in turn could cause the performance of our new and existing centers to suffer. Opening new centers may result in inadvertent oversaturation, temporarily or permanently divert customers from our existing centers to new centers and reduce comparable centers revenue, thus adversely affecting our overall financial performance. In addition, oversaturation or the risk of oversaturation may reduce or adversely affect the number or location of centers we plan to open, and could thereby materially and adversely affect our growth plans overall or in particular markets.