Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission file number 001-40860

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

Address not applicable1 | ||||||||||||||

(Address of Principal Executive Offices) | ||||||||||||||

(310 ) 691-0776

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting stock held by non-affiliates of the registrant on June 30, 2022 was approximately $1.9 billion.

As of February 21, 2023, the registrant had 651,896,249 shares of common stock, par value $0.001 per share, outstanding.

1Olaplex Holdings, Inc. is a fully remote company. Accordingly, it does not maintain a principal executive office.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement relating to its 2023 Annual Meeting of stockholders, to be filed with the Securities and Exchange Commission within 120 days after registrant’s fiscal year end of December 31, 2022, are incorporated by reference into Part III of this Annual Report.

Table of Contents

TABLE OF CONTENTS

| Page | |||||

3

Table of Contents

GLOSSARY

As used in this Annual Report on Form 10-K (“Annual Report”), the terms identified below have the meanings specified below unless otherwise noted or the context indicates otherwise. Except where the context otherwise requires or where otherwise indicated, the terms “OLAPLEX” “we,” “us,” “our,” “our company,” “the Company,” and “our business” refer to Olaplex Holdings, Inc. and its consolidated subsidiaries.

•“2020 Credit Agreement” refers to the Credit Agreement, dated as of January 8, 2020, by and among Olaplex, Inc., Penelope Intermediate Corp., MidCap Financial Trust, as administrative agent, collateral agent and swingline lender, and each lender and issuing bank from time to time party thereto, as amended by the First Incremental Amendment to the 2020 Credit Agreement, dated as of December 18, 2020. The 2020 Credit Agreement was refinanced and replaced by the 2022 Credit Agreement.

•“2022 Credit Agreement” refers to the Credit Agreement, dated as of February 23, 2022, by and among Olaplex, Inc., Penelope Intermediate Corp, Goldman Sachs Bank USA, as administrative agent, collateral agent and swingline lender, and each lender and issuing bank from time to time party thereto. The 2022 Credit Agreement refinanced and replaced the 2020 Credit Agreement.

•“IPO” refers to the initial public offering of shares of common stock of Olaplex Holdings, Inc., completed on October 4, 2021.

•“Penelope” refers to Penelope Holdings Corp., which is an indirect parent of Olaplex, Inc., the Company’s primary operating subsidiary.

•“Penelope Group Holdings” refers to Penelope Group Holdings L.P., which prior to the IPO was the direct parent of Penelope.

•“Pre-IPO Stockholders” refers to, collectively, (i) the former limited partners of Penelope Group Holdings prior to the Reorganization Transactions and (ii) holders of options to purchase shares of common stock of Penelope that were vested as of the consummation of the Reorganization Transactions.

•“Reorganization Transactions” refers to the internal reorganization completed in connection with our IPO, pursuant to which Olaplex Holdings, Inc. became an indirect parent of Olaplex, Inc. For further information, see “Reorganization Transactions” in “Note 1 - Nature of Operations and Basis of Presentation” to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report.

•“Tax Receivable Agreement” refers to the income tax receivable agreement entered into by the Company in connection with the Reorganization Transactions under which the Company is required to pay the Pre-IPO Stockholders 85% of the cash savings, if any, in United States (“U.S.”) federal, state or local tax that the Company actually realizes on its taxable income following the IPO, as specified in the Tax Receivable Agreement.

4

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains certain forward-looking statements and information relating to us that are based on the beliefs of our management as well as assumptions made by, and information currently available to, us. These statements include, but are not limited to, statements about our strategies, plans, objectives, expectations, intentions, expenditures and assumptions and other statements contained in or incorporated by reference in this Annual Report that are not historical or current facts. When used in this document, words such as “may,” “will,” “could,” “should,” “intend,” “potential,” “continue,” “anticipate,” “believe,” “estimate,” “expect,” “plan,” “target,” “predict,” “project,” “seek” and similar expressions as they relate to us are intended to identify forward-looking statements.

The forward-looking statements in this Annual Report reflect our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operation. Examples of forward-looking statements include, among others, statements we make regarding: our financial position and operating results; our business plans, strategies and objectives; general economic and industry trends; our business prospects; our reputation and brand; future product development and introduction, including entry into adjacent and other categories; growth and expansion opportunities, including expansion in existing markets and into new markets; our sales channels and omnichannel strategy; our customer base; our supply chain and global distribution network; our technology and cybersecurity profile; our social and environmental initiatives and programs; our employees and culture; our operational capabilities; and our expenses, working capital and liquidity. Forward-looking statements are predictions based upon assumptions that may not prove to be accurate, and they are not guarantees of future performance. As such, you should not place significant reliance on our forward-looking statements. Neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements, including any such statements taken from third party industry and market reports.

Forward-looking statements involve known and unknown risks, inherent uncertainties and other factors that are difficult to predict which may cause our actual results, performance, time frames or achievements to be materially different from any future results, performance, time frames or achievements expressed or implied by the forward-looking statements, including, without limitation:

•our ability to anticipate and respond to market trends and changes in consumer preferences and execute on our growth strategies and expansion opportunities, including with respect to new product introductions;

•our ability to develop, manufacture and effectively and profitably market and sell future products;

•our ability to accurately forecast customer and consumer demand for our products;

•competition in the beauty industry;

•our ability to effectively maintain and promote a positive brand image and expand our brand awareness;

•our dependence on a limited number of customers for a large portion of our net sales;

•our ability to attract new customers and consumers and encourage consumer spending across our product portfolio;

•our ability to successfully implement new or additional marketing efforts;

•our relationships with and the performance of our suppliers, manufacturers, distributors and retailers and our ability to manage our supply chain;

•impacts on our business from political, regulatory, economic, trade and other risks associated with operating internationally;

•our ability to attract and retain senior management and other qualified personnel;

•our reliance on our and our third-party service providers’ information technology;

•our ability to maintain the security of confidential information;

•our ability to establish and maintain intellectual property protection for our products, as well as our ability to operate our business without infringing, misappropriating or otherwise violating the intellectual property rights of others;

•the outcome of litigation and regulatory proceedings;

•the impact of changes in federal, state and international laws, regulations and administrative policy;

•our existing and any future indebtedness, including our ability to comply with affirmative and negative covenants under the 2022 Credit Agreement;

5

Table of Contents

•our ability to service our existing indebtedness and obtain additional capital to finance operations and our growth opportunities;

•volatility of our stock price;

•our “controlled company” status and the influence of investment funds affiliated with Advent International Corporation over us;

•the impact of an economic downturn and inflationary pressures on our business;

•fluctuations in our quarterly results of operations;

•changes in our tax rates and our exposure to tax liability; and

•the other factors identified in the “Risk Factors” section of this Annual Report and in other documents that we file with the Securities and Exchange Commission from time to time.

Many of these factors are macroeconomic in nature and are, therefore, beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from those described in this Annual Report as anticipated, believed, estimated, expected, intended, planned or projected. We discuss many of these risks in greater detail in the “Risk Factors” section included elsewhere in this Annual Report. The forward-looking statements included in this Annual Report are made only as of the date hereof. Unless required by law, we neither intend nor assume any obligation to update these forward-looking statements for any reason after the date of this Annual Report to conform these statements to actual results or to changes in our expectations or otherwise.

6

Table of Contents

RISK FACTORS SUMMARY

An investment in our common stock involves risks. You should consider carefully the following risks, which are discussed more fully in “Item 1A. Risk Factors”, and all of the other information contained in this Annual Report before investing in our common stock. These risks include, but are not limited to, the following:

•Our inability to anticipate and respond to market trends and changes in consumer preferences could adversely affect our financial results;

•Our historical rapid growth may not be indicative of future growth, and we expect our growth rate to ultimately slow over time. If we are unable to manage our growth effectively, our business, financial condition and results of operations could be adversely affected;

•If we are unable to accurately forecast customer and consumer demand, manage our inventory and plan for future expenses, our results of operations could be adversely affected;

•The beauty industry is highly competitive, and if we are unable to compete effectively, our business, financial condition and results of operations could be adversely affected;

•Our brand is critical to our success, and the value of our brand may be adversely impacted by negative publicity through traditional or social media channels. If we fail to maintain the value of our brand or our marketing efforts are not successful, our business, financial condition and results of operations could be adversely affected;

•We depend on a limited number of customers for a large portion of our net sales, and the loss of one or more of these customers could reduce our net sales and have an adverse effect on our business, financial condition and cash flows;

•If we fail to attract new customers and consumers, retain existing customers and consumers, or fail to maintain or increase sales to those customers and consumers, our business, prospects, results of operations, financial condition, cash flows and growth prospects could be harmed;

•We may be affected by changes in consumer shopping preferences, shifts in distribution channels and changes in the salon and retail environments, and such changes could have an adverse impact on the demand for our products and on our business, financial condition and results of operations;

•We rely on single source manufacturers and suppliers for the majority of our products. The loss of manufacturers or suppliers or shortages in the supply of raw materials or finished products could harm our business, prospects, results of operations, financial condition and cash flows;

•A disruption in manufacturing, supply chain or our shipping distribution and warehouse management network could adversely affect our business, financial condition and results of operations;

•We are subject to risks related to the global scope of our sales channels;

•We rely on the use of our and our third-party service providers’ information technology. Any significant failure, inadequacy, interruption or data security incident impacting our information technology and websites, or those of our third-party service providers, could have an adverse effect on our business, prospects, results of operations, financial condition or cash flows;

•Failure to adequately maintain the security of confidential information could materially adversely affect our business;

•Our processing of personal information and other sensitive data could give rise to significant costs and liabilities, which may have an adverse effect on our reputation, business, financial condition and results of operations;

•Our efforts to register, maintain and protect our intellectual property rights may not be sufficient to protect our business;

•Third parties may allege that we are infringing, misappropriating or otherwise violating their intellectual property rights, which could involve substantial costs and adversely impact our business;

•Disputes and other legal or regulatory proceedings could adversely affect our financial results;

•If our products are found to be defective or unsafe, we may be subject to various product-related claims, which could harm our reputation and business.

•Our business is subject to federal, state and international laws, regulations and policies that could have an adverse effect on our business, prospects, results of operations, financial condition and cash flows;

•Government regulations relating to the marketing and advertising of our products may restrict, inhibit or delay our ability to sell our products and harm our business.

7

Table of Contents

•Our significant indebtedness could adversely affect our financial condition;

•We may be unable to generate sufficient cash flow to service our debt obligations;

•Our stock price may be extremely volatile and, as a result, you may not be able to resell your shares at or above the price you paid for them;

•Investment funds affiliated with Advent International Corporation own a significant percentage of our common stock and have significant influence over us;

•The Tax Receivable Agreement with our Pre-IPO Stockholders requires us to make cash payments to them and exposes us to certain risks. These payments may be substantial and could exceed actual tax benefits. The timing of these payments may also be accelerated, and we will not be reimbursed for any payments made under the Tax Receivable Agreement in the event that any tax benefits are disallowed. Changes in tax law, and in particular the tax rate applicable to U.S. corporations and the tax rules on amortization of intangible assets, may materially impact the timing and amounts of payments by us to the Pre-IPO stockholders pursuant to the Tax Receivable Agreement;

•There may be sales of a substantial amount of our common stock, and these sales could cause the price of our common stock to fall;

•We are a “controlled company” within the meaning of the corporate governance standards of The Nasdaq Stock Market LLC. As a result, we qualify for, and rely on, exemptions from certain corporate governance standards;

•A general economic downturn or sudden disruption in business conditions may affect consumer purchases of discretionary items and the financial strength of our customers, which could adversely affect our business, financial condition and results of operations; and

•Our quarterly results of operations may fluctuate, and if our operating and financial performance in any given period does not meet the guidance that we have provided to the public or the expectations of our investors and securities analysts, the trading price of our common stock may decline.

8

Table of Contents

PART I

ITEM 1. BUSINESS

Company Overview

OLAPLEX is an innovative, science-enabled, technology-driven beauty company. Since our inception in 2014, we have focused on delivering effective, patent-protected and proven performance in the prestige haircare category. Our mission is to blaze new paths to well-being that ignite confidence from the inside out.

We offer science-backed solutions that are designed to improve hair health and are trusted by stylists and consumers. We identify our consumers’ most relevant haircare concerns in collaboration with our passionate and highly engaged community of professional hairstylists and consumers and strive to address them through our proprietary technology and innovation capabilities.

Our Products

OLAPLEX disrupted and revolutionized the prestige haircare category by creating the bond-building space in 2014. We have grown from an initial offering of three products sold exclusively through the professional channel to a broader suite of products offered through the professional, specialty retail and Direct to Consumer (“DTC”) channels that have been strategically developed to address three key uses: treatment, maintenance and protection. Our current product portfolio is comprised of fifteen unique and complementary products specifically developed to provide a holistic regimen for hair health. Our proprietary, patent-protected ingredient, Bis-aminopropyl diglycol dimaleate (“Bis-amino”), serves as a key differentiator in our ability to create trusted, high-quality products. Underpinning our product range is a portfolio of more than 160 worldwide patents which protects our proprietary technology and we believe creates both barriers to entry and a foundation for us to enter adjacent and other categories over time. Our patent claims are broadly drafted and include claims covering applications across adjacent categories in haircare and also other categories such as skin care and nail health.

Professional Products

Our current hair health platform is championed by four products that can be purchased and applied only by professional hairstylists, No. 1, No. 2, our 4-in-1 Moisture Mask and our Broad Spectrum Chelating Treatment. These products often serve as an introduction to our brand and a gateway to the remainder of our products that can be used both at home and in the salon.

9

Table of Contents

Retail Products

10

Table of Contents

Our Channels

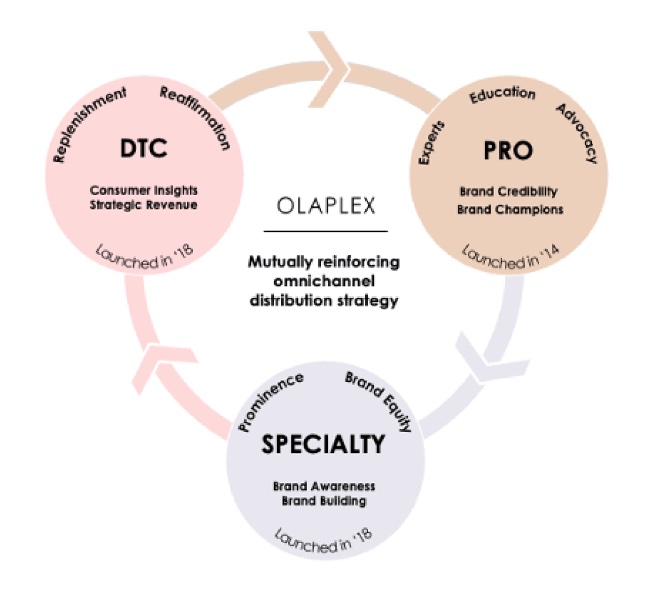

We believe that a key differentiator of OLAPLEX is our synergistic omnichannel strategy. Our three sales channels, Professional, Specialty Retail, and Direct-to-Consumer, work together to reinforce relationships with current customers and introduce our products to an expanded potential customer base.

Professional Channel Rooted in our Hairstylist Community

In our professional channel, our products are sold primarily through wholesale beauty supply distributors who then sell those products to professional beauty industry outlets, such as professional beauty supply stores, salons and licensed hairstylists, for use in the salon or for hairstylists to sell to consumers for use at home. In 2022, we sold our products through over 115 professional distributors. Our international distributors are generally only permitted to sell our products to professional beauty industry outlets in specific territories, with some having the exclusive right to sell our products in the territory. Our agreements with professional beauty distributors also typically contain minimum purchase and sell-through requirements and prohibit the distributor from selling products deemed competitive with ours.

Specialty Retail Channel Focused on Reaching Consumers

Our specialty retail customers include specialty retailers with online and/or brick and mortar presences. In 2022, we sold our products through approximately 50 retailers in more than 20 countries throughout the world.

Direct to Consumer Channel Leveraging our Digital Capabilities

We sell our products directly to consumers through our branded website, Olaplex.com, and third-party e-commerce platforms, including Amazon and pure play beauty and wellness partners. We have dedicated resources to implement creative, coordinated, brand-building strategies across our online activities to increase our direct access to consumer insights, which we believe has led to higher engagement and conversion, and can further enhance our innovation and branding performance.

Innovation

We believe that one of the key differentiators of our business is a powerful innovation platform. We conduct research in our OLAPLEX laboratory and employ a dedicated in-house research and development team, which includes scientists, product and packaging innovation specialists, and regulatory and compliance experts. We also incorporate feedback from our community of professional hairstylists and consumers to better understand their respective needs. These insights, combined with the efforts of our in-house research and development team, independent third party laboratory testing, and real-world salon testing, create a virtuous feedback loop. We develop our products in our laboratory and in partnership with national co-manufacturers, universities, and biotech companies to remain on the cutting edge of beauty technology. As our business continues to grow globally, we intend to focus on developing proprietary new technologies, improving existing products and exploring adjacent and other categories.

11

Table of Contents

We do not perform, nor do we commission any third parties on our behalf to perform, testing of our products or ingredients on animals.

Our principal research and development center is located in the U.S. See “Item 2. Properties”.

Marketing

Our strategy to market and showcase our products begins with our omnichannel platform across the professional, specialty retail and DTC channels. In our professional channel, we market our products using educational seminars on our products’ application methods and consumer benefits. We have a dedicated portal on our website for professional customers to purchase and learn more about our products and have developed a mobile app for our professional community that serves as a resource on our brand and products and offers us the opportunity to more directly engage with hairstylists about our products. In addition, we use professional trade advertising, social media and other digital marketing to communicate to professionals and consumers the quality and performance characteristics of our products.

In our specialty retail channel, we support our authorized retailers to drive in-store and e-commerce sales of our products, and we work with them to ensure the optimal presentation of our products in their stores or on their e-commerce sites. Advertising activities, in-store displays and online navigation are designed to attract new consumers, build demand and loyalty and introduce existing consumers to other product offerings. Our marketing efforts also benefit from cooperative advertising programs with some retailers.

In our DTC channel, our digital first approach to performance marketing is designed to offer best-in-class customer experience on Olaplex.com, from load times, site navigation to a more intuitive check-out experience, all of which is designed to increase brand awareness, site traffic and conversion.

In addition, top celebrity hairstylists and colorists from around the world serve as Olaplex brand ambassadors. These brand ambassadors help market our brand through educational events, social media and other publicity. We also are investing in new analytical capabilities to promote a more predictive and personalized experience across our sales channels. For example, we developed an online hair diagnostic quiz that allows consumers to discover our products by identifying their personal hair health needs, which are used to provide customized product recommendations.

Our Customers

Our strategy is to build and maintain strong customer relationships globally, and we have over 215 customers across our omnichannel sales platform. Our products are sold in more than 100 countries across the world. During the years ended December 31, 2022, 2021, and 2020, respectively, the Company’s customers with net sales exceeding 10% of total net sales consisted of one customer which represented 16%, two customers which represented 25% in aggregate, and three customers which represented 32% in aggregate of total net sales. The accounts receivable balance for these customers as a percentage of total accounts receivable was immaterial as of December 31, 2022 and 11% at December 31, 2021. The Company has not experienced material bad debt losses due to this concentration.

In 2022, approximately 56% of our net sales were generated in the U.S. and approximately 44% of our net sales were international, based upon the geographic location of customers who purchase our products. However, the majority of net sales are transacted in U.S. Dollars, our functional and reporting currency.

Supply Chain and Global Distribution Network

We believe that we have developed a flexible and resilient third-party supply chain that is capable of supporting long-term growth at scale. A core tenet of our supply chain strategy is leveraging strong relationships with our manufacturers and logistics partners to create an expansive supply network that is designed to create ample capacity without requiring significant additional capital investment.

Our finished products are manufactured in the U.S. and Europe by four manufacturers. Two of these manufacturers are located in the U.S., one is located in Europe, and one maintains facilities in the U.S. and Europe. Cosway Company Inc. (“Cosway”) manufactures products that accounted for more than 77% of our net sales in 2022, and we continue to rely upon Cosway to manufacture a majority of our current product offerings. We are currently negotiating a new agreement with Cosway. In order to allow sufficient time to facilitate these negotiations, we have amended our current agreement with Cosway to expire on June 30, 2023. In support of our efforts to expand our manufacturing network, this amendment also removes the requirement that we exclusively purchase certain finished products from Cosway. We expect to be able to complete such negotiations prior to the expiration date of the current Cosway agreement (or be able to extend the expiration date as necessary until such time as we are able to enter into a new agreement with Cosway). In addition, as part of our manufacturing expansion efforts, on July 7, 2022, we entered into a supply agreement with our fourth manufacturer and began manufacturing in October 2022.

We utilize third parties with key operational facilities located inside and outside the U.S. to warehouse and distribute our products for sale throughout the world. We believe that our manufacturing and distribution network is sufficient to meet anticipated

12

Table of Contents

demand. In addition, we have disaster recovery programs in place under some of our agreements with suppliers that allow for shifting of manufacturing capacity if necessary to account for disruptions due to natural disasters and other events outside of our or their control. We continue to implement improvements in capacity, technology, resiliency, and productivity and to align our manufacturing and distribution capabilities with anticipated regional and international sales demand and expansion of our customer base in targeted geographies. In 2022, we transitioned our primary U.S. warehouse and logistics center to a new provider and launched a new business to consumer third party warehouse and logistics center in Canada.

Seasonality

Our results of operations typically are slightly higher in the second half of the fiscal year due to increased levels of purchasing by consumers for special and holiday events and by retailers for the holiday selling seasons. However, fluctuations in net sales in any fiscal quarter may be attributable to a number of other factors, including macroeconomic factors, competitive activity and the level and scope of new product introductions by or promotional activities of our retail customers, which may impact their order placement and receipt of goods.

Competition

Competition in the beauty industry is based on a variety of factors, including innovation, product efficacy, accessible pricing, brand recognition and loyalty, service to the consumer, promotional activities, advertising, special events, new product introductions, e-commerce initiatives and other activities. Our competitors include Estee Lauder, Henkel AG & Co. KGaA, Kao Corporation, L’Oreal S.A. and Unilever. We also face competition from a number of independent brands. Certain of our competitors also have ownership interests in third parties that are our customers.

We believe we have a well-recognized and strong reputation in our core markets and that the quality and performance of our products, our emphasis on innovation, and our engagement with our professional and consumer communities position us to compete effectively.

Intellectual Property

We rely on a combination of patent, trademark, copyright, trade secret, and other intellectual property laws, nondisclosure and assignment of inventions agreements and other measures to protect our intellectual property.

As of December 31, 2022, we owned over 300 trademark registrations and applications globally. Our flagship trademark is OLAPLEX. We seek to register our OLAPLEX mark in all jurisdictions where we do business. In addition, as of December 31, 2022, we owned over 160 issued patents worldwide, including 15 U.S. patents, and over 45 pending patent applications worldwide. During the year ended December 31, 2022, we filed 237 new trademark applications and were granted 61 new trademark registrations. We also filed three new patent applications and were issued seven new patents.

Our patent portfolio includes a family of patents that includes approximately 100 granted patents with claims that cover Olaplex’s commercial formulations Nos. 0-9, as well as their uses, and patents with claims that cover other haircare, nail and skincare products and/or their uses. The patents issued in this family have been granted in the U.S., Australia, throughout Europe, Brazil, Canada, Israel, New Zealand and Japan. The patents in this family are generally expected to expire in 2034. Any additional patents that grant from pending applications in this patent family would also be expected to expire in 2034.

Our patent portfolio also includes a family of patents with claims to protect us against competitor products that do not contain our Bis-amino ingredient. This patent family includes approximately 50 patents worldwide, including patents that have been granted in the U.S., throughout Europe, Brazil, Canada, Israel and Japan. The patents in this family are generally expected to expire in 2035. Any additional patents that grant from pending applications in this patent family would also be expected to expire in 2035.

For more information, see “Risk Factors— Risks Related to Intellectual Property Matters.”

Information Technology

Information technology supports all aspects of our business, including operations, marketing, sales, order processing, production and distribution networks, customer experience, finance, business intelligence, and product development. We continue to maintain and enhance our information technology systems and customer experiences in alignment with our long-term strategy. An increasing portion of our global information technology infrastructure is cloud-based and in partnership with industry-leading service providers. We believe this approach enables a high performance platform to support current and future requirements and enhances our scale and flexibility to respond to the demands of the business by leveraging advanced and leading-edge technologies.

We recognize that technology presents opportunities to build a competitive advantage, and we continue to invest in new capabilities across various aspects of our business. During 2022, we continued to improve our business-to-business and business-to-consumer integration, cybersecurity and technology infrastructure, supply chain network and integrations, business resilience capabilities, and analytics. In addition, in 2022 we improved our e-commerce experience, launched DTC sites in France and

13

Table of Contents

Canada, continued our investment in business intelligence to drive deeper consumer insight and built a multi-language certification and education platform for our professional hairstylist and consumer communities.

In 2022 we expanded our data privacy program and our vendor risk program to protect our customers and our business and to align with the privacy regulations of countries in which we do business. We have enhanced and will continue to enhance our cybersecurity posture to align with industry standard cybersecurity frameworks. We review and assess our cybersecurity profile on an ongoing basis, and our policies and procedures establish processes for risk assessment, risk management, risk oversight, data protection, incident management, operations security, end user training, third-party reviews and implementation of general cybersecurity best practices. We have assessed, and will continue to assess, the adequacy of our policies, procedures, and internal controls for ensuring we meet defined cybersecurity standards.

Commitment to Social and Environmental Consciousness

We believe our responsibility extends beyond our products that build better hair. We continue to evaluate the impact we have on our environment and communities in an effort to further integrate sustainability and social impact into our strategy and business operations. In 2022 we began a partnership with a sustainability strategy firm to perform a double materiality assessment of various Environmental, Social and Governance factors relevant to the Company. This assessment, which will also incorporate feedback from several of our stakeholder groups, will be used by us to develop our multi-year Environmental, Social and Governance strategy.

•Environmental Sustainability. Our cruelty-free, non-toxic formulas are free of Parabens, Sodium Lauryl Sulfate “SLS”, Sodium Lauryl Ether Sulfate “SLES”, Phthalates and Phosphates. From our early days we have also limited the use of secondary packaging for our products. We estimate that between 2015 to 2022 we avoided the use of approximately 6.9 million pounds of paper packaging, which we estimate prevented approximately 56 million pounds of greenhouse gas from being emitted into the environment, conserved approximately 91 million gallons of water and saved approximately 70,000 trees from deforestation. In 2022, we also began a partnership with a leading sustainability rating provider to assess the sustainability practices of our third party manufacturing and logistics partners.

•Charitable donations. In March 2022, we introduced the Shopping Gives program to our website. Shopping Gives is a charitable initiative whereby we donate $1 for every order that a retail or professional customer places, at no additional cost to the customer. Customers can choose from a list of causes to benefit from their purchase.

•Supporting Small Businesses. We are invested in the success of our hairstylist community as their businesses grow alongside ours. We are especially focused on providing support to the small business community and minority hairstylists. Currently, 98% of our salon community is made up of small businesses and a meaningful percentage of our hairstylists identify as racial or ethnic minorities.

Employees and Human Capital Resources

Employees

As of December 31, 2022, Olaplex employed 174 employees, 167 of whom are based in the U.S. and seven of whom are based in the United Kingdom (“U.K.”). We also leverage contractors to supplement work in areas that are quickly growing such as technology, operations and accounting. We do not have any employees governed by a union. We utilize professional employer organizations (“PEO”), who are the employer of record of our U.S. and U.K. employees and administer our human resources, payroll and employee benefits functions.

Culture

We believe our commitment to our heritage in the prestige haircare category and encouragement of our employees to bring their whole self to work has created a culture that is paramount to our success. We are passionate about what we do, how our products impact lives and what our brand means to our community.

Diversity, Equity and Inclusion

We believe it is important that our employees reflect the diversity of our hairstylist and consumer communities, and our focus on Diversity, Equity and Inclusion remains a key differentiator in both our consumer strategy and internal culture. Our current Olaplex employees include former hairstylists whose unique perspectives and insights have helped us better understand our diverse consumer base and what matters to them. As a result of our efforts, we have created a diverse workplace environment where 76% of our employees identify as female and 45% identify as non-white as of December 31, 2022. Additionally, eight of the ten members of our board of directors (the “Board of Directors”) identify as female. We know through experience that different ideas, perspectives and backgrounds create a stronger and more creative work environment that can deliver better results.

In January 2021, we established DEI Champions within the Company who reinforce our collective commitment to foster a diverse, equitable and inclusive culture. Their roles are to identify opportunities to further engage our teammates through training

14

Table of Contents

and education, encouraging candid conversations and leading by example. The team is led by a diverse group of six individual volunteers across different departments.

Compensation and Benefits

The core objective of our compensation program is to provide a package that will attract, motivate and reward exceptional employees. Through our “Healthy Hair ~ Healthy Body ~ Healthy Mind” wellness strategy, we are committed to providing comprehensive benefit options that will allow our employees and their families to live healthier and more secure lives. We leverage both formal and informal programs to identify, foster and retain top talent. Our talent development is further supported by a professional development reimbursement program and an educational assistance plan designed to provide financial assistance to eligible team members.

Government Regulation

Our products are subject to regulation by the Food and Drug Administration (“FDA”) and the Federal Trade Commission (“FTC”) in the U.S., as well as various other local and foreign regulatory authorities in the countries in which we operate. These laws and regulations principally relate to the ingredients, proper labeling, advertising, packaging, marketing, manufacture, safety, shipment and disposal of our products.

In the U.S., our products are considered “cosmetics” under the Federal Food, Drug, and Cosmetic Act (“FDCA”). The labeling of cosmetic products is subject to the requirements of the FDCA, the Fair Packaging and Labeling Act, the Poison Prevention Packaging Act and other FDA regulations. Cosmetics are not subject to pre-market approval by the FDA. However, certain ingredients, such as color additives, must be pre-approved for the specific intended use of the product and are subject to certain restrictions on their use. FDA regulations also prohibit or otherwise restrict the use of certain types of ingredients in cosmetic products. If a company has not adequately substantiated the safety of its products or ingredients, then a specific warning label is required. The FDA may, by regulation, require other warning statements on certain cosmetic products for specified hazards associated with such products.

In addition, the FDA requires that cosmetic labeling and claims be truthful and not misleading. Moreover, cosmetics may not be marketed or labeled for their use in treating, preventing, mitigating, or curing disease or other conditions or in affecting the structure or function of the body, as such claims would cause the products to be a drug and subject to regulation as a drug. The FDA has issued warning letters to cosmetic companies alleging improper drug claims regarding their cosmetic products, including, for example, product claims regarding hair growth or preventing hair loss. In addition to FDA requirements, the FTC and state consumer protection laws and regulations can subject a cosmetics company to a range of requirements and theories of liability, including similar standards regarding false and misleading product claims, under which FTC or state enforcement or class-action lawsuits may be brought.

The FDA has not promulgated regulations establishing Good Manufacturing Practices (“GMPs”) for cosmetics. However, the FDA’s draft guidance on cosmetic GMPs, most recently updated in June 2013, provides recommendations related to process documentation, recordkeeping, building and facility design, equipment maintenance and personnel, and compliance with these recommendations can reduce the risk that the FDA finds such products have been rendered adulterated or misbranded in violation of applicable law. The FDA monitors compliance of cosmetic products through market surveillance and inspection of cosmetic manufacturers and distributors to ensure that the products are not manufactured under insanitary conditions or labeled in a false or misleading manner. Inspections also may arise from consumer or competitor complaints filed with the FDA. In the event the FDA identifies any violation of FDA regulation, the FDA may request or a manufacturer may independently decide to conduct a recall or market withdrawal of product or to make changes to its manufacturing processes, product formulations or labels.

The Modernization of Cosmetics Regulation Act (“MoCRA”), signed into law on December 29, 2022, will expand the FDA’s regulatory oversight of cosmetics when it becomes effective on December 29, 2023. MoCRA will require, among other things, that manufacturers of cosmetics products register their facilities and list their cosmetic products with the FDA, maintain for FDA review records demonstrating adequate substantiation of cosmetic product safety, comply with GMP regulations for cosmetic products and report serious adverse events associated with their cosmetic products to the FDA. MoCRA also grants the FDA authority to issue mandatory recalls of cosmetic products that pose a risk of serious adverse health consequences.

The FTC also regulates and can bring enforcement action against cosmetic companies for deceptive advertising and lack of adequate scientific substantiation for claims. The FTC has specialized requirements for certain types of claims. For example, the FTC’s “Green Guides” regulate how “free-of,” “non-toxic” and similar claims must be framed and substantiated. In addition, the FTC regulates the use of endorsements and testimonials in advertising as well as relationships between advertisers and social media influencers pursuant to the FTC’s Endorsement Guides. The Endorsement Guides provide that an endorsement must reflect the honest opinion of the endorser, based on “bona fide” use of the product, and cannot be used to make a claim about a product that the product’s marketer could not itself legally make. Additionally, companies marketing a product must disclose any material connection between an endorser and the company that consumers would not expect that would affect how consumers evaluate the endorsement. If an advertisement features endorsements from people who achieved above average results from using a product,

15

Table of Contents

the advertiser must have proof that the endorser’s experience can generally be achieved using the product as described; otherwise, an advertiser must clearly communicate the generally expected results of a product and have a reasonable basis for such representations.

Although the Green Guides and Endorsement Guides do not operate directly with the force of law, they provide guidance about what the FTC generally believes the Federal Trade Commission Act, or FTC Act, requires in the context using of “green” claims and endorsements and testimonials in advertising. Any practices inconsistent with the Green Guides and Endorsement Guides can result in violations of the FTC Act’s proscription against unfair and deceptive practices.

In the European Union, the sale of cosmetic products is regulated under the E.U. Cosmetics Regulation (EC) No 1223/2009, which provides the general regulatory framework for finished cosmetic products placed on the E.U. market. The overarching requirement is that a cosmetic product made available on the E.U. market must be safe for human health when used under normal or reasonably foreseeable conditions of use, taking account of the following: (a) presentation including conformity with Directive 87/357/EEC regarding health and safety of consumers; (b) labelling; (c) instructions for use and disposal; (d) any other indication or information provided by the responsible person; and (e) the maintenance of a product safety report.

Generally, there is no requirement for pre-market approval of cosmetic products in the European Union. However, manufacturers are required to notify their products via the centralized E.U. cosmetic products notification portal. Manufacturers are responsible for safety of their marketed finished cosmetic products and must undergo an appropriate scientific safety assessment before cosmetic products are sold. The E.U. Cosmetics Regulation requires the manufacture of cosmetic products to comply with GMPs, which is presumed where the manufacture is in accordance with the relevant harmonized standards. In addition, text, names, trademarks, pictures and figurative or other signs used in the labelling and advertising of cosmetic products cannot imply that these products have characteristics or functions they do not actually have. Any product claims in labelling must be capable of being substantiated.

The E.U. Cosmetics Regulation has been retained in U.K legislation, subject to certain amendments, and is applicable to Great Britain (England, Scotland and Wales) and Northern Ireland. Such amendments include notification of cosmetic products made available to consumers in Great Britain to the Office for Product and Safety Standards and the requirement to have a responsible person established in the U.K. We rely on expert consultants, Obelis, for our E.U. and U.K. product registrations and review of our labelling for compliance with E.U. and U.K. regulation.

We are also subject to a number of federal, state and international laws and regulations that affect companies conducting business on the Internet. These laws and regulations may involve user privacy, data protection, content, intellectual property, distribution, electronic contracts and other communications, competition, protection of minors, consumer protection, telecommunications, product liability, taxation, economic or other trade prohibitions or sanctions and online payment services. Many of these laws and regulations are still evolving and being tested in courts.

We are subject to federal, state, local and international laws regarding privacy and data protection. Such laws and regulations are evolving and may be subject to significant change. In addition, the application, interpretation and enforcement of these laws and regulations are often uncertain, and they may be interpreted and applied inconsistently by different regulators and inconsistently with our current policies and practices. In the European Union, the General Data Protection Regulation (“GDPR”) imposes a strict data protection compliance regime and provides for significant potential fines or penalties for violations. The GDPR applies to the processing and transfer of personal data. The GDPR has also been incorporated into the laws of the U.K. (“U.K. GDPR”) alongside the Data Protection Act 2018. Additionally, a 2020 decision from the Court of Justice of the European Union and related regulatory guidance may impact our ability to transfer personal data from the European Economic Area or the U.K. to the U.S. and other jurisdictions. Recently enacted U.S. state privacy laws require many companies that process personal information, including us, to make disclosures to consumers about their data collection, use and sharing practices. In some instances, these laws allow individuals to request access to, or correction or deletion of, their personal information, as well as to opt out of the sale, or sharing for cross-context behavioral advertising purposes, of such information to third parties, or to opt out of the processing of their personal information for targeted advertising or certain automated decision making and profiling activities. Certain of these laws also require companies, including us, to obtain prior opt-in consent to the processing of specified sensitive personal information or to provide the opportunity to limit the use or disclosure of such information in certain circumstances. These new state privacy laws could mark the beginning of a trend toward more stringent privacy legislation in the U.S., both at the state and federal level.

Available Information

Our Internet address is www.Olaplex.com. Our website and the information contained on, or that can be accessed through, the website will not be deemed to be incorporated by reference in, and are not considered part of, this Annual Report on Form 10-K. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, current reports on Form 8-K, including exhibits, proxy and information statements and amendments to those reports filed or furnished pursuant to Sections 13(a), 14, and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available through the “Investors” portion of our website

16

Table of Contents

free of charge as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. In addition, our filings with the SEC may be accessed through the SEC’s Interactive Data Electronic Applications system at http://www.sec.gov. All statements made in any of our securities filings, including all forward-looking statements or information, are made as of the date of the document in which the statement is included, and we do not assume or undertake any obligation to update any of those statements or documents unless we are required to do so by law.

ITEM 1A. RISK FACTORS

An investment in our common stock involves risks. You should carefully consider the following information about these risks, together with the other information contained in this Annual Report. The risks described below are those that we believe are the material risks that we face. If any of the following risks actually occurs, our business, prospects, operating results and financial condition could suffer materially, and the trading price of our common stock could decline. Some of the following risks and uncertainties are, and will be, exacerbated by any worsening of the global business and economic environment. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial also may materially and adversely affect our business, prospects, operating results or financial condition. See “Special Note Regarding Forward-Looking Statements” elsewhere in this Annual Report.

Risks Related to Our Business

Our inability to anticipate and respond to market trends and changes in consumer preferences could adversely affect our financial results.

Our continued success depends on our ability to anticipate, gauge and react in a timely, effective manner to changes in consumer tastes for haircare and other beauty products, attitudes toward our industry and brand and where and how consumers shop. We must continually work to maintain and enhance the recognition of our brand, develop, manufacture and market new products, maintain and adapt to existing and emerging distribution channels, successfully manage our inventories and modernize and refine our approach as to how and where we market and sell our products. Our new products and innovations on existing products may not receive the same level of consumer acceptance as our products have in the past.

Consumer tastes and preferences cannot be predicted with certainty and can change rapidly. This risk is increased by the use of digital and social media by consumers and the speed by which information and opinions are shared. Even if we are successful in anticipating consumer needs and preferences, our ability to timely and adequately address those needs and preferences will in part depend upon our continued ability to develop and introduce innovative, high-quality products and maintain our distinctive brand identity as we expand the range of products we offer. The acceptance of new product launches and other product innovations may not be as high as we anticipate due to lack of acceptance of the products themselves, the price of the products, the strengths of our competitors or the limited effectiveness of our marketing strategies. In addition, new product innovation may place a strain on our employees and our financial resources, including incurring expenses in connection with product innovation, development and marketing that are not subsequently supported by a sufficient level of sales.

As part of our ongoing business strategy, we may expand our product launches into adjacent and other categories. The success of such product launches could be hampered by our relative inexperience operating in such categories, the strength of our competitors in such categories or any of the other risks described elsewhere in this “Risk Factors” section. Our failure to anticipate and effectively respond to changing consumer preferences and trends in the market for our products or to effectively introduce new products in our traditional product categories, new products in adjacent or other categories or innovations on existing products that appeal to consumers, or the introduction by our competitors of similar products in a more timely fashion, could lead to, among other things, lower sales, excess inventory or inventory shortages, markdowns and write-offs and diminished brand loyalty, and our business, financial condition and results of operations could suffer.

These risks have been and may continue to be exacerbated by the current macroeconomic environment. Consumer spending habits and confidence have shifted and may continue to change in light of inflationary pressures and other risks described elsewhere in this “Risk Factors” section.

Our historical rapid growth may not be indicative of future growth, and we expect our growth rate to ultimately slow over time. If we are unable to manage our growth effectively, our business, financial condition and results of operations could be adversely affected.

While we have experienced significant and rapid growth, our historical rate of growth may not be indicative of our future rate of growth, and our net sales could decline or grow more slowly than we expect. We believe that continued growth in net sales, as well as our ability to improve or maintain margins and profitability, will depend upon, among other factors, our ability to address the challenges, risks and difficulties described elsewhere in this “Risk Factors” section. We cannot provide assurance that we will be able to successfully manage any such challenges or risks to our future growth. Any of these factors could cause our net sales growth to slow or decline and may adversely affect our margins and profitability. Even if our net sales increase, our growth rate may slow for a number of other reasons, including a decrease in demand for our products, increased competition, an increase in

17

Table of Contents

sales of lower margin products such as holiday kits, a decrease in the growth or reduction in the size of our overall market or if we cannot capitalize on growth opportunities. In addition, from time to time, sales growth or profitability may be concentrated in a relatively small number of our products or countries. Failure to continue to grow our net sales or improve or maintain margins would adversely affect our business, financial condition and results of operations. You should not rely on our historical rate of growth as an indication of our future performance.

Our growth has in the past, and may in the future, strain our ability to effectively manage our operations, as it requires us to expand our management team, sales and marketing, product development and logistics and distribution functions. Growth may require us to further upgrade our management information systems, internal processes and procedures and technology. It also requires us to obtain sufficient raw materials and manufacturing capacity and additional operational capabilities and facilities to warehouse and distribute our products, particularly as we continue to expand internationally. Ineffective execution to support growth could result in, among other things, product delays or shortages, operating errors, outages, inadequate customer service, inappropriate claims or promotions by our marketing team or brand ambassadors and governmental inquires and investigations, all of which could harm our revenue and ability to generate sustained growth and result in unanticipated expenses. Expansion into new international markets may create operating difficulties in managing our business across numerous jurisdictions and ultimately may not be successful, which could result in slower revenue growth, higher operating costs and lower margins than anticipated and could impair our ability to enter into additional new markets. In addition, we need to continue to attract and develop qualified management personnel to sustain growth. If we are not able to successfully retain and develop existing personnel and identify, hire and integrate new personnel, our business, financial condition and results of operations would be adversely affected.

If we are unable to accurately forecast customer and consumer demand, manage our inventory and plan for future expenses, our results of operations could be adversely affected.

We base our current and future inventory needs and expense levels on our operating forecasts and estimates of future demand. To ensure adequate inventory supply, we must be able to forecast inventory needs and expenses and place orders sufficiently in advance with our manufacturers and suppliers based on our estimates of future demand for particular products. Failure to accurately forecast demand for new or existing products has resulted in, and may in the future result in, inefficient inventory supply or increased costs. For example, we experienced a slowdown in sales momentum during the second half of 2022, in part, due to inventory rebalancing across certain of our customers. Inventory levels in excess of customer demand may result in inventory write-downs or write-offs or the sale of excess inventory at discounted prices, which would cause our gross margins to suffer and could impair the strength and premium nature of our brand. Further, lower than forecasted demand could result in excess manufacturing capacity or reduced manufacturing efficiencies, which could result in lower margins. Conversely, if we underestimate customer demand, including as a result of unanticipated growth and the launch of new products, our manufacturers and suppliers may not be able to deliver products to meet our requirements, and we may incur higher costs in order to secure the necessary production capacity or additional or expedited shipping. An inability to meet customer demand and delays in the delivery of our products to our customers could result in reputational harm and damaged customer relationships and have an adverse effect on our business, prospects, results of operations, financial condition and cash flows.

While we devote significant attention to forecasting efforts, the volume, timing, value and type of the orders we receive are inherently uncertain. Historical growth rates, trends and other key performance metrics may not predict future growth. Our business and our ability to forecast demand is affected by general economic and business conditions in the U.S. and customer confidence in future economic conditions, and our ability to forecast demand will be increasingly affected by conditions in international markets as we continue to expand internationally. A portion of our expenses are fixed, and as a result, we may be unable to adjust our spending in a timely manner to compensate for any unexpected shortfall in net revenues. Any failure to accurately predict demand for our products or expenses could cause our operating results to be lower than expected, which could adversely affect our financial condition.

The beauty industry is highly competitive, and if we are unable to compete effectively, our business, financial condition and results of operations could be adversely affected.

We face competition in the beauty industry from companies throughout the world, including multinational consumer product companies and new independent beauty brands. Some of our competitors have greater resources than we do and may be able to respond to changing business and economic conditions more quickly than we can, and some are competing in distribution channels or territories where we are less represented. Certain of our competitors have and may continue to attempt to gain market share by offering products at prices at or below the prices at which our products are typically offered, including through the use of discounts or other promotions, or by marketing their products as lower cost or as more effective versions of certain of our products. Competition in the beauty industry is based on a variety of factors, including innovation, product efficacy, accessible pricing, brand recognition and loyalty, service to the consumer, promotional activities, advertising, special events, new product introductions, e-commerce initiatives and other activities. It is difficult for us to predict the timing and scale of our competitors’ actions in these areas. In addition, as we expand into adjacent or other categories, we have faced, and will continue to face, different and, in some cases, more formidable competition.

18

Table of Contents

Our ability to compete depends on a number of factors, including the continued strength of our brand and quality of our products, our ability to attract and retain key personnel, the success of our marketing and innovation strategies, our ability to execute our strategic plan, the successful management of new product introductions and innovations, the influence of our brand ambassadors and brand advocates, the efficiency of our third-party manufacturing facilities and distribution network, our relationships with our key customers and our ability to maintain and protect our intellectual property and other rights used in our business. In addition, certain of our competitors have ownership interests in third parties that are customers of ours, and, as a result, such customers may have an interest in promoting theses competing brands over our products. Our inability to continue to compete effectively could have an adverse effect on our business, financial condition and results of operations.

Our brand is critical to our success, and the value of our brand may be adversely impacted by negative publicity through traditional or social media channels. If we fail to maintain the value of our brand or our marketing efforts are not successful, our business, financial condition and results of operations could be adversely affected.

Maintaining, promoting and positioning our brand depends largely on the success of our marketing and merchandising efforts and our ability to provide consistent, high-quality products. Our brand could be adversely affected if we fail to achieve these objectives or if our public image or reputation were to be tarnished by negative publicity through traditional or social media channels. We cannot guarantee that our brand development strategies will increase the recognition of our brand or increase revenues.

We frequently use third-party social media platforms to raise awareness of our brand and engage with our hairstylist and consumer communities. We also partner with brand ambassadors and brand advocates who promote and market our products, participate in product launches, engage with our professional hairstylist and consumer communities and educate them about our products. If we are unable to cost-effectively develop and continuously improve our consumer-facing presence on existing, evolving or new social media platforms, our ability to acquire new and retain existing customers and consumers may suffer, and we may not be able to provide a convenient and consistent experience to our professional hairstylists and consumers, regardless of the sales channel. This could negatively affect our ability to compete with other companies and result in diminished loyalty to our brand and decreased sales.

The use of social media by us, our brand ambassadors, our brand advocates and our consumers carries the risk that our image and reputation could be negatively impacted. Negative commentary or false statements disseminated by others about the brand, the safety and efficacy of our products, our brand ambassadors and brand advocates and other third parties who are affiliated with us have been, and may in the future be, posted on social media platforms. The rising popularity of social media and other consumer-oriented technologies has increased the speed and reach of information dissemination, and our target consumers often act on such information without further investigation into its accuracy. The harm resulting from the dissemination of such negative commentary and false statements may be immediate and could have an adverse effect on our brand, business, financial condition and results of operations.

Our ability to maintain relationships with our existing ambassadors and advocates and to identify new ambassadors and advocates is critical to expanding and maintaining our customer and consumer base. As our market becomes increasingly competitive and as we expand internationally, recruiting and maintaining new ambassadors and advocates may become increasingly difficult. If we are not able to develop and maintain strong relationships with our ambassador and advocate network, our ability to promote and maintain consumer awareness of our brand may be adversely affected. Further, if we incur excessive expenses in this effort, our business, financial condition and results of operations may be adversely affected. Our ambassadors or advocates could engage in behavior or use their platforms in a manner that reflects poorly on our brand or is in violation of applicable platform terms of service, laws or regulations, including with respect to product or marketing claims. These actions may be attributed to us or could subject us to regulatory investigations, class action lawsuits, liability, fines or other penalties.

In addition, the importance of our brand may increase as we continue to experience increased competition, which could require additional expenditures for our brand marketing activities. Maintaining and enhancing our brand image may also require us to make additional investments in areas such as merchandising, marketing and online operations. These investments may be substantial and may not be successful. Moreover, if we are unsuccessful in protecting our intellectual property rights in our brand, the value of our brand may be harmed. Any harm to our brand or reputation could adversely affect our ability to attract and engage customers and consumers and expand our business and could negatively impact our business, financial condition and results of operations.

We depend on a limited number of customers for a large portion of our net sales, and the loss of one or more of these customers could reduce our net sales and have an adverse effect on our business, financial condition and cash flows.

We expect that certain of our largest customers in 2022 will continue to account for a substantial portion of our net sales for the foreseeable future. The loss of a significant customer, a shift in the level of support for our brand by any of these customers, or any significant decrease in sales to these customers, including as a result of the restructuring or bankruptcy of one of our customers, consolidation among such customers, retail store closures, decrease in consumer demand or other factors, could reduce

19

Table of Contents

our net sales and operating income, lead to a decrease in customer confidence in our brand and cause a loss of other customers, and therefore could have an adverse effect on our business, financial condition and cash flows.

If we fail to attract new customers and consumers, retain existing customers and consumers, or fail to maintain or increase sales to those customers and consumers, our business, prospects, results of operations, financial condition, cash flows and growth prospects could be harmed.

Our success depends in large part upon widespread adoption of our products by consumers. In order to attract new consumers and continue to expand our customer and consumer base, we must appeal to and attract hairstylists and consumers who identify with our products. If we fail to deliver a high-quality consumer experience or if hairstylists or our current or potential customers or consumers are not convinced that our products are of high-quality or superior to alternatives, then our ability to retain existing customers and consumers, acquire new customers and consumers and grow our business may be harmed. We have made significant investments in marketing, enhancing our brand, attracting new customers and consumers and interacting with our hairstylist and consumer communities, and we expect to continue to make significant investments to promote our products. Such campaigns can be expensive and may not result in new customers or consumers or increased sales of our products. Further, as our brand becomes more widely known, we may not attract new consumers or increase our net sales at the same rates as we have in the past. If we are unable to acquire new customers and consumers who purchase products in numbers sufficient to grow our business, we may not be able to generate the scale necessary to drive efficiencies with our suppliers, our net revenues may decrease, and our business, financial condition and operating results may be adversely affected.

In addition, our future success depends in part on our ability to increase sales to our existing customers over time. We may not be successful in maintaining or increasing sales to, or maintaining strong relationships with, our existing customers as we expand our customer base, introduce new products and grow our own e-commerce business, which competes with our professional and specialty retail customers for consumer sales. We also have been, and may in the future be, affected by changes in the policies and demands of our professional and specialty retail customers relating to inventory management, changes in pricing, marketing, advertising and/or promotional strategies by such customers, space allocations by our customers or any significant decrease in our display space or online prominence.

We may be affected by changes in consumer shopping preferences, shifts in distribution channels and changes in the salon and retail environments, and such changes could have an adverse impact on the demand for our products and on our business, financial condition and results of operations.

We cannot ensure that there will always be a demand for salon treatments. We may be affected by changes to the salon environment, and our professional customers may limit their product supply if demand for salon treatments decreases. For example, in the second half of 2022, we believe that shifting consumer spending habits due to macroeconomic factors, including inflationary pressures, resulted in a decline in the demand for professional salon treatments and take-home products purchased from salons. Further, there may be consolidation of the salon market. If consolidation leads to customers gaining purchasing power, we may need to reduce the cost of our products, which will have an impact on our earnings. Consolidation among our customers may also increase the risk of customer concentration.

In addition, consumer preferences have and may continue to shift with respect to retail traffic in brick and mortar stores. For example, in the first half of 2022, traffic in the brick and mortar stores in our specialty retail channel increased following a slowdown in traffic in those stores during the COVID-19 pandemic. Further, any consolidation or liquidation in the retail trade may result in us becoming increasingly dependent on key retailers and could result in an increased risk related to the concentration of our customers. A severe, adverse impact on the business operations of our customers could have a corresponding material adverse effect on us.

We rely on single source manufacturers and suppliers for the majority of our products. The loss of manufacturers or suppliers or shortages in the supply of raw materials or finished products could harm our business, prospects, results of operations, financial condition and cash flows.