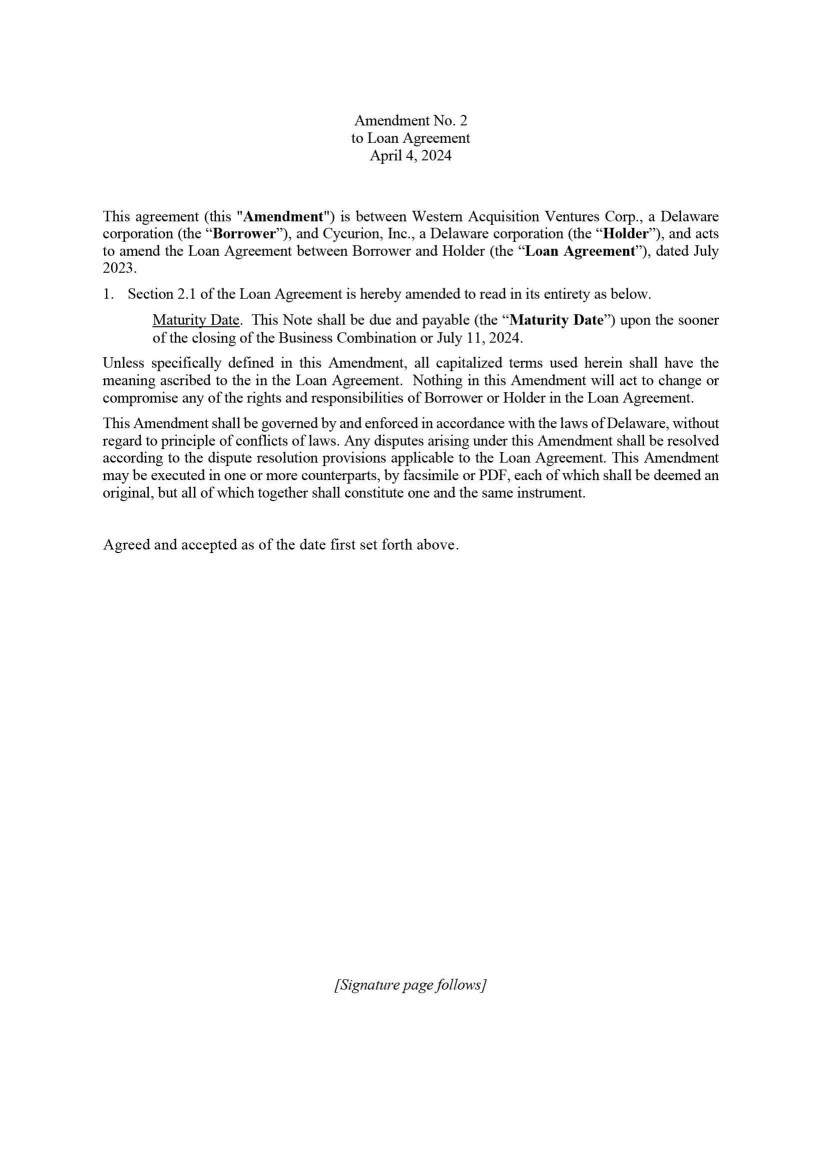

'_"GBN'PGX!T[QK\._&GBSPQ?

M^"++0)K#2U\JZTW4(G<3K.DKH4216BQ,&P/*'/0U^@/I1ZT ?'U[X!\5Z!\1

MTGTK1M3U+2)[A1J&E:C;M++;!--$'VNQU,8.<*L1BDR6;)_

M!>J>(--U6V:[T..PL(=/UN]TO^S;^0)YP^RW$8Q'*T08?OXP%??CDCCZ*[T=

MJ /GKX8:'JOP1^*GQ/74M*O]1\/>+]9'B'3]7TZTDNA'(\21RVTR1AG0JT8*

MMC:5;&01BH_'>F:S??'/PWXAUSPS>:O\/I?#][IC6,=J;QK2]>6-Q-+ H8XD

MB5HP0#MS\Q4,:^B>]'I0!\'>#O@GJ&C>+/AY:^-_"E_KUM:>#=:L[]Y=,EOX

MH5DNHY;"TE9599'2%74 9P1C.2I.5X/^%VNVGAGX2Q6G@C6;+Q#+X&UO1=7.B^)+6%W7#I)'*WF ,/G&&.XXP-#^%G]H-X6&N^

M =7O/L_PC;2+Q;W0KB1!J2>5LA*F,@R#RW*GZ8.2,_?/:CO0!^>^M>'_ !MK

MGPRTO3T^'7B.'7[#0_"T@U(:8TES=R6LT;7"-)*V8FB(D 1%#ONW;F6NG^,W

M@35[_3/CO:+X%UJ\OM9U?2-6T>XM--:=9%6*S20*T>?G4Q3[AT&,D\KG[A]*

M/6@#XX^)7@/Q1XHG^-VG7GA[4=6O_%,-I/X+U:&T8BT*VZ+'&9" ;5H;@-*=

M^S_6$C)R*X?Q)\*]1L[7XG70\%ZQJ/B0>+] O].U.'0YVDF$0L_MEQ;OLRH+

M0W!8J1NXZAES]_\ >CM0!XE^T7IVOZU%\/=3TG3KO5]#TOQ';WVN:3!$3+<6

M?ER(&\H\R>7(\G[

MH=-2QT*V#FSA(V"3RP0?+3C(4$@=!P:^;/!7PK\0_"BR_9UFU/PK?:T^AZ)J

M>D:NFEVRSO;R7,<31I)@_P"KRKH6)*@]< YK[,]:.] 'PY\#O WB"QU7X":9

MXD\#:SI]OH^@:]INII>V!DMXO/DB\E9&3<@5U5^&(/'S 9&?2_V>OAS?^'/%

M&H^%M1L86\._#NZGL_#EVH5O,BN@DR ]U>"%UA]2')[U]%:UH\&O:7>:?/DR7,[SS2MC!

M>25R6=C@?,Q)X'I0!YA^U%!>W>E> $L=+U+5'MO%^EZA.NG6,MR8K>&8/+(_

MEJ=H ]>3V!YJ+]HQKV_O/A6]EI.IZD++QC9ZC=&PL)I_L]ND4RO))L4[0#(O

M!Y.>!P<>X>E!H Y.W^(=M/X^G\)'3M0AO8[$:@EY+!MM9X]X1ECDSRR%DW @

M??&,\X\R^)7CV+7?&UOH>H^#_%U_H^C7<-XOV'0;B:WU&Z0AXOWH78(HWVMD

ML 74'(53N]JAT6T@O9[Q(8UNYD$;S[!O91D@$^@)/'N:O]Z /CCQE\&_$UQX

M/^,'PZMM+N9W\<^+8]9LM46,FVCLYY+:2X:23[JM%Y,H"$Y;Y-H.>/2+SQW%

MXE^)NE6U_P"#O%[6N@W_ )>E@Z#<"VEN&4Q->/,RA BH[A>>A9NI4#W_ +4=

MZ /D35?A7\6-+^-OPGU">^T#6K2VU;4KW4-2L]&ND:,2VQ5C.[7+#+)B./

M4JHP0-M?4?ACQ$?$ME8HRE'>CTH /6CO1ZT=Z #M1WH[4=Z #TH]:/2CUH .]':CO

M1VH .]'I1WH]* #UH[T>M'>@ %':@4=J #O1Z4=Z/2@ ]:.]'K1WH .U'>CM

M1WH /2CUH]*/6@ [T=J.]':@ [T>E'>CTH /6CO1ZT=Z #M1WH[4=Z #TH]:

M/2CUH .]-/6G=Z:>M #N]'I1WH]* #UH[T>M'>@ [4=Z.U'>@ ]*/6CTH]:

M#O1VH[T=J #O1Z4=Z/2@"IJE[)I]E+/%:RWTD:%UMX"@DD('W5WLJY/N0/>O

M-O!'[06G>/\ X0S?$72_#NN?V,L<\T=I,ENMW.D+,LC(@F*\%'X9@3MX!R,^

MI.-R$>HQ7RE\!]7B\&_LLS> -41[7QIIT>JZ8^A2*1=RS/<7!B,<>,NCAT82

M#*X;.>#@ ^F_#6N_\)'HEEJ7V.XTX74*S"UNRGFQAAD!MC,N<8Z,:YC2_BU9

M:I\6=9\ #3KRWU+2]+M]6>ZFV"":*:1XT\O#%CAHW!R!R.]?)?QRSIOBCXS6

M3>*M9@DT3X;6-]IUK:ZS<0QPZK&;M5\E$HI-ZC

M'S#UZU\366KVOB;PC>:YX \<:RUE?ZM9R_9O%VG7-IHPFCAG,EJYVI)"C!5,

MCJ2@D6/@Y8&MKGC?Q3_8/A?Q#!87C.-,6.\\'7VHSC4&+7LR^?IEXO%Q(P3(

M21LC,9$!(<8) P!0!^A^X8ZBC<.>

M17PSX]U37OA_X@\5ZIX/U'Q#K?PF-SHL^L7%M/-JDENS/#PGJ5UK/C'Q'\%]6O]3-UJEW87*K:7+QP&V41K&)Q: _

M:0NX$"0@C(5< 'V'/KUW%XCM-.31[F6RFM9;B35%:/R(75D"Q,"P+=.>&M5L='^-_@72I_%NNZGX;E\ Z@LP\47,B/,$N+?RIIHG";96B$QW

M,JN54D]#7GWPGUG3_#_PY_9M;2]:ETU[CQ7=6VK6EO>/%'+$8KP@7$08# ?[

M-C>./,7'WN0#[[R#WKB_C#\4;+X-_#G7/&.H6%YJ=CI$!N9[>P"&4H",D;F4

M8&TU6_OE\22^.+7XJ^&Y]:?5-&TRTN=E_:GSO)VN4\GRA

M'Y30X8$.H R68-Y5XQ\;-J'PU^+5C;WU\^@:S\-;.YL+2?[7,'O#+<1R9EF

M\RX/[M9'4+N8 ;@Y&!S7R/>Z9H_P 3_P!I+5]!;56BMM6^&5O:)=:==&*5)#=.

MX:*1#D.JE7&#G&#TZ]C^S-!K'B^*/4O$ME/IVJ^$K9O"4J[W$=U=0R$7%RH)

MPZ.JPE&/(WR#UH ^AB< UP_PK^+%E\58?$SVNG7NEOH&M3Z'<17X0.TT21LS

M (S#:?,&.<\<@5Q?[3OBF[\)P^!;FY2\7P7+KRQ>);BR#EH;4P2^69-GS"+S

MQ"'(XQP?E+5\K:'XY_X0J\\1>:GB'3?AA<_$#5Y-0U.#2KN<)'+;6XLI&RFZ

M2 LDPRN[:PCSCY20#[D\>_$F#P5=Z1IL%A-K.N:O]H^PZ;;2(CS>3$99/F<@

M# S_$RCC.1<^'OC"\\;>'UU2^\.:EX6D=R$L=7\L7!3 *NRHS!NZZ

MFGZ-KWACQ+JGB[5O#MSX'E/@_4=8AN%GO[AGNO-W[$4^>$%L$60;Q'SU+T ?

M:?@7Q;;^//!FA>)+6&2VM=7T^WU"**;&]$EC615;'&0&&<5/I6MW.H:MJUI/

MI5Q8VUF\:P7LTD9CO0R!F:,*Q8!2=IW 2"1'2!$8%'4,,,I[<]1P03\L_%CQ?/9W7QNM8?&>L6CV?BSP\U@(-

M6F5XXG-N+F./#?ZH9GW(/E4@Y Q0!]XYR*S]5UZST>>S@N9TCN+UVBMHB?FF

M=8VD*J.YVHQ_"O"/VW=BUKJ"JLR26\[PN&"LP'S1MT)K>\-

M:W=:Y8SSWFDW&C.ES- D-U)&[2(CE5E!1F&UP P!.0#R >*^&/AAJECH6K?#

MG5[#7;N"XU3XD>([*]B349!;M8RRW\B;H-^S:7:V82%

MW%C?:9/<:;;2/9ZD=US"3$I*2GNXZ$^H-?/WQ7\--^TOI_Q%ATK6='CTW2K-

MM&L[FYW,]I=HR7+W2LI 4"5( &/'^CL02#0!]5Y&>M)D#'(KX)M*MM4FLXH[B.U4 2JCKLS)YFQ^"P( )%<]\,?%5]

M9Z?\#]6L?%.J7OB.\U+7-'N(]1U::9)K:..[6S2:-W*@;EM<.1N)93D[J /T

M%R.>:0L/4=*_/&+Q=_PDGP7\7ZRWBWQ[HWQ"TOPA=P:_I;V\]A'!J(0%'>3:

M TIF7$?E/EDL>,=:\(ZIXUM_!.L:OK,][X%TC57MX]0FO9FF-RRWD

MUNK,VV86QR$3'\! Z4 ?6^A?%VRUWXK>(_ :Z9>VFHZ)86FH2W-R$$,\=PTB

MH8L,2<&)P<@H_.OS:^+OB;0TU_XH:WX(U;7M.T^]\-^''TW4[&2

M]B665=0G6:(2D=?+D):,GDAS@E6QT7Q4O+31C^T''I'BW6]FAV.F:SX>2/7[

MJ3;J$D;>:T1\S]X2PB!CRR@M]T;J /T#W#CD4%A@\BOBN;QN_BGXO:AH?B7Q

M!XMT36SJUE?^%Y-!L9)+>_T[R86 2=4:(1EO.$P<@88\\+CE?!NO1V-[X&U2

M3Q;JU]=S?$W5M&G-_K,\R2:6QN@B2(S[6C/^CD.PSRF#@B@#[PT;6[37[5KF

MQN([JW662'S(FW+O1V1Q]0RL#[BK^<"OE[]D[QEX5^&WPBT#0;XG1=4N_$&H

M:1]GFM9DS=F]N#'$3LVJ?+VX)('*CJ0#[?\ &'6!X>^&7BC4V@U.Y2TTRYF:

M+1ZOXPU'3[S4[#3(Q)-!8!#+M+!

M<_,RC )&>>G8U7\.?%ZR\1_$WQ!X)CTV\M=0T:PL]1DN;C8(9XKDR!/+PQ)P

M8G!R!R*^)_''C)[[X9?'G3$OYY]"O_"^C7>DVX%U) TKF1)?*>;[[DI&&90N

MYE)VY!KZ&^&6OV&H_M<^.&M;N"X2;P=H:QO'(&#E9;QF (ZX66,G'0.N>HH

M^CR0.IQ1N&>HKPO]J/QM-X!/@;5-2M]1F\!?VL\?B233()97BA-O)Y+R+$"_

MDB;9NP/[N>,@^-?$CQ+I=KX&T?1=%U'QAJ27GA_6[S0M6UE+U1(V08D6-$25

MYT#8A:0J5C5F^;.: /MDL,'D<5SE[XR_LK4]274-/EL-%L; 7TFMW$L:VV-M2\2QZ]XO\3PWES\.-$U3388-3N[=QJK)<

MJSP1*RYD:2-/W8!WG)VGDT[XH-K^MZ9\3_#WB>]O-5UU_A5IUYD:U=Z;?-

MJ>DW%C-I]R]M/(19VR$+@AB,JZ,OJ&!Z$4 ?>44OF)N92AQD@]13RP'^&Y-/DBT^YDV2^09I60Q/!N$9B(<'H

M!QF@#ZAU?XNV>C?%GP_X!FTJ_-_K5C=7]O?!4%L$@*!U)W;MW[Q.-N.>O:NN

MUO6[3P_827U]/%:VD0!DFF;:JC.!S]2!^(KXL^%'BC2?$7QP^!^KV::[=ZJ/

M#FJ6FOO=VEV[V^HE+7>MQN4K&^]9 2<# 49QM%>W?MIZ5!J?P!UAY[)KU+.]

MTV[94C9V2.._MVE?"@G CWDXZ &@#W/(QUHW @\BOBW5/%D6L?%[5?#6KZUX

MP\,77V^PO/!G]@Z;,8[RQ$,+!4F,;(H,GG"59<#:WS< 8X/Q&D0^!OQ*\46W

MC;Q,_B#2_&\^F:=<+XCNF)L6U2 (OE^9M=3"KL&*G*AL':* /T.W+ZC\Z-P]

M17Y]?%"]M=$3]H!-(\6ZV!X?&E:KX=1-?NI/+O9(QYS1'S#YN6"AD)906/RC

M)KU?2/$^M?\ #0%A-!<#Q7X?U?5MJ&UN)8+W2@+$_?BR8KBQ8KN5UV[9)!U:

M@#ZOR >M(&''(KR;]J[2M0U;]GCX@QZ0EV^KIHEU+9?8&=9Q.L99#&4(;=N

MQBOG;6/&DGB_Q]XR/AKQ!JFF6.J^&- FL]4N+"\ETQ[A+R83"; 78CJ(XY&4

MJVW<<_(V #[C)'/-*+JQNM1M-(LY;V>WL55IFCC4L^T,0

M.%!/)' />OC?5?B=JNGZ5X1_X36UUOPOX%N9M7T^^U'11/J]I]M$T?V>6.54

M,IMF3S_);;\I SA33/B%K,EGX6\;^$_%EYXJU"RD^'Q7P=>ZK#.+C49O)N?

M.:41HO\ I7_'N"K@,$Z@9DH ^VO"/B2+Q?X6TC7+>*2"#4K.&]CBEQO19$#@

M''5(XY-Z[&8;2LJXR0?4

M"H?@5>B^^#'@IO)N+=DT6SC>*Z@>"5&6%58%'4,.0>H]^F*^0-9U:PT7Q-XX

M\1V?B"ZLM4M_B[IT<7V;49(XFM)%LX[DM$K!70H)@S," (VY&TT ??>X<ZU=6OB+3]/CTJXN+.Y@FEEU)'C$-LR%-L;@L&)?

MUOD5#;(8(][JYW;@V",87'/7BLK]HM+Z7X:7<6F:PNA:A) :^:;758?&?C#X+V'BF&70ME_XEANEMM9D>&2+RL+

M+;W>5D%LYR(^0<+M&0M 'W(S G->1>+OVDM)\'ZYX^TNYT'6)YO!V@Q^(KM

MH4B(N;9_-YAS(,E?)DSNV_=.,U\>2_$V]U7]G^UTY-2UZY\5VO@_6)M/U)[F

M[F!E@NIA"L:Q?,]TJ11MYCL-L; X8.<=OXX\76.KZ_\ &Z]DO0TM]\&[:$&0

M%6DG9;[* $ ER9H_EZ_O$X^84 ?:GA7Q#%XK\,Z5K4$4D,.H6D5Y'%+C>JR(

M' /;(#"N>^'/Q4L_B/JOC+3[?3KW3KCPQJW]D7*WJH#*_D13"1-K-\A69<9P

M?4"E^"=[%??"'P9+ ZR1_P!BV8#*/PKXX\;:Q9:5XF^*_B:RUR[

ML=9L/BAH8M6M-0DBC:!HM.BN6:-6"RH8TN58L& $;]-IH ^_"P!Y(% (..17

MQ.WCP:U\>O"WV%M.)H4 8[<,&&

M6%=%X1\->+M*TKQMX-L+._N=8\ R:E?^']3O)97&IO\N(K9)YX[:,RL%WR.P5$7U)) Q7S1^RIXCT

MKQOKS:SINO\ C"?44TB.TUS1=:L);6VL[Q64YD,B -GRW$PB>3R(F$B,QV D ED'XB@#TGX,K"WTZ]TVX\+ZN='N5OE0&5_(BF$B;6;Y"LRXS@^H%=OD>M?G]XKUBPT?7O

MBAXFT_6[O3]4L/BCH8M/LM_+"AMFBTV&Y+0JP61/+2Y5BZL (GZ;37=?";Q7

M-XL^,2:=XAUGQ?I?Q%TC7[]Y](M].D%C=Z>TDHA9YRAB:U\EHBOS!@ZJ%Y)W

M 'V/Z4>M'I1ZT '>CM1WH[4 '>CTH[T>E !ZT=Z/6CO0 =J.]':CO0 >E'K1

MZ4>M !WIIZT[O33UH =WH]*.]'I0 >M'>CUH[T ':CO1VH[T 'I1ZT>E'K0

M=Z.U'>CM0 =Z/2CO1Z4 'I2;ASR*H:_'=RZ->"PN8[2^\EO)GEB\U8WQPQ3<

MNX ]LC-?'_PL^*GQ.\F%% 'VAD9ZBDW =Q7Q9X/_:1\9>/?#_@K0I?$&D^&_$FK^&;K45U

MF_FBM([RZANWMOE5X)4;:(UD>-0IQ(,,H!K7\7_'CQ5I%QI=U9>*K+5I[;5O

M#6F:K::791#38S?/"LP\R4F:1I$F\V,Q[0B[=V3G(!]>;ASR.*R= \5:=XED

MU-+&8RMIMVUC<[HW39,J*Q7Y@-V Z\KD<]>M?*=_\7_B-I^I>(]2E\46L]CH

MGQ0T[PJFG0:9$D5Q8W0L0RNQW.&3[4Q5E8'<#G(PHDO_ (Q?$D13PP^(M-2X

MA^+">#FF.E#!L7CA*A5W\,"[9)R3GJM 'U_D8/-<+\9OA9;_ !H\"W7A:ZU>

M\T>TN98I);BP2)I?W34O[.^(LW

MA6\UZ"QA-ZM@L F658$38T@=T5BL9 3+M8\&WEYXPE>:[;4

MKR*RDEM%M9);))W2WE>( ;6>,*Y! ^]T7. >B6<+6\"+)/Y[A55I" "Q'4X

M' SUXJQD9ZU\HCXZ:_'\6?"MG8^)8=7\.:WJFOZ>\ES:0VMG$;.&5T6/&9B8

MGA,;NYVOEBH'&,"T_:?\0^&[6UTKQI=WGAK7KB^T>QOYM5M[A /LPL !S7"^(OC9X/\(W%W!K.LPZ=);7MKI\@GCD7

M_2+@ PQJ=N'9LC[N<=\5XCXF\5_$>V\9^ _#.G?$C2;BU\0:_JNFOJUGIL$]

MPD"V$MU;[_\ EEYJ;5!"H WR$]2#R/QJ\6>*=8\,_%GPQK.L6^I#P]XG\)0:

M?<)9"':)KFSE9G56^8[VR>0.. M 'VOD$]:K7U_%IUK+M-6TQM8TJTM_%E^D5@+%+R&Z=H)G2)H@X

M>VC56,9XN4W9X)Z;P]\4?%L_COPS\/M;\9:4;K4SJUVNOZ*L4IECMS!Y-IF2

M(1&8+<%I&6, B+@+EL 'LMIK>F?''XA%>:?##XBZ]X=A

M\(^&F\2W\S>+/'WB/2KC6;Q()9+..UN+TQ(G[O;YDIA11O# !6VJ. #[-]:

MYKQC\1O#W@-])77-4M]/;5;Z+3;)96.Z>YD8*D2@ DDDCZ=37$?L\^-_$'BZ

MU\9L;: NY#@#H/G'Q -4N?"V

MN&?Q)>:A>1?&VQM(#?B)Q J7UNJ-A54\ J,9QA1@#K0!]TY'KWI<]>]?'A_:

M"\4^%;R]\-:UX@LYGC\?S^%D\2ZD8; 1P?V(+_P &2CQ'KFD^(-5ANIX1J.CG?"\8<^6&(5%:15(5RJJ"P. O0 '4

M^&_%&G^*[2>YTZ8S0P7,UH[-&\>)8G:.1<, 3AE(R.#C@D5KY'/-?'^F_%_X

MD:KH'@8_\)+80W>I_$35/"NH7,>F+\]O#+=I&T:ER$(%LO!W$YZ\<^R?LU>+

M]<\7^#O$,?B'4?[6U#1O$>IZ(-0,*0O<1V\[)&[H@"!RN,[0!QT% ';^,?B-

MX>\!R:0FN:I;Z>^K7L>FV*2L=UQ"<84!=HXKHHOV@_%GA_7KGP9

MJ_B&T>3_ (36^\.Q>)]1\BPQ''8174,;,('B65FF**?+PP3'WCF@#[&9@JEB

M>!R:Y+P=\5O"_P 0+K4;?P]J\&JRZ;*;>]6#C?(^5QD94\CTJG\&;

M_6]0\#6[^(M7TO7M6CEEAEU'1B3;S!9&"D':H+@8#;0!N!P .!YK^R;-%:-\

M1@'-32

MR;X?3P/8Z));(\>IP?9HK@M*67S/WPD=$,;+C:.IR*L77QT\0R?$KPG#I?B$

M76DZSXGN= NK::RMX[:S*6,LIA'/GR2Q2QC>^Y4.XJ!D9 !]6Y&>M(2 .M?(

M/PD^+OQ#U;5OA#>Z_P");?4K;Q9K&NZ/?:?#I\4,*BT-V89D89<-_HZC!8J5

M/3/S'Z)^+OB:]\->#[@Z3$]QKM\PL-,@BV[WN)#M5AN('R#=(Q[HW=>)@DGWL_OB2!67X:^)_Q5

M\2Z+::O;ZI+;PMX4O]3U87NBK]ET[4HRODPPN GG1,#+@AWR(U8-AN0#Z^)'

M/-&X9ZBOCS1?C)XVM=)^%EGK'C6RBO?B!H/]KQZC?+;Z=':3I;6Q^RQ.8)4<

MLTLDF'3)"D CI5FY^-GC?4-5@\$#QIX2TCQ1!X:CU1-=>Z6&PU*2A94,9_>'#8Q@ ^N<@=Q2[@.XKXG\1_&SXHZ=H_Q,UN/Q7IKGPAK6BP

MV]E::2GV:[ANX[4R1LSDR;/W[$,"K< \#*UL>*?C[XM^%WBGQ]X>UC7K74[3

M3M;T"S@UW4(8;)-/@U!)&D,K)&RB-&CVJ[HQ'F#=NQ0!]@9''--:15ZL!GID

M]:^4+SQ[\3K/Q3X$T(>/?#]]:Z]XFN]+EN],MH[N>.V_L^6XB#R;(X_-0QG[

ML0!#(2.H;%\ >-_%/CKXA_!Y]<\67?F1W_BO3KIK:*WABO38S^1%*Z>60'9,

M@[< ;CMVYH ^NM7T&TUR2S-VAE2UF6XCC).SS%.48CH2IP1GH0#U K-\;?$+

MP]\.M/AOO$FK6VBV,LJPBZO&*1!V( #/T7)( R1FM^WN8;M"\$J3("5+1L&&

M0<$9'<$$5YQ^T;H]CX@^$.LZ9J4"76GWDEK;7%O)]V2-[F)64^Q!(_&@#JO$

MOC[0_"!TW^U;]+0:C,+>TW*S>=(>B+M!RQZ@=\''2N@) QDXKY!T34==^#OQ

M!\%_"#Q(;O5-#?64NO!NORJSF6UCBF+V%P__ #VA4C:Q^_&!W4U)HOQU\9:_

MX.\ >-[:_9H_$?C"3PS?^%_LL0-E";B>%61]ID$\0A61MY93\_R@8P ?2NN?

M$;P]X<\1Z'X?O]4@M]:UQY8]-LF)+W+1H7?;@'&U5)).!5_6_%&GZ#?Z397D

MQBN-5G:UM%$3L))!&TA!*@A?E1CEB!QZU\3>#K?6=;\+?L\D^*;RXUB\\9ZZ

M#J%XD,\UOB+4U+*-HW,=N[Y]PR>FT;:[SP9\9O'>I0?">*ZURTN#JWBW7/#>

MJ3/IZ"2[2T%]Y,ORD*A_T5"RJHR2<$#B@#W/2/A&FD_%S7O'JZ[>S7.KZ?;:

M=+ISQ0BWCB@:1HRI"A\[II"26.<^U>@[AGJ*^/OAM\8/B->WWPTU#6_$MMJ<

M'B#Q3KGAN\TZ'3HH('2U^VF*96Y=7S:J,;MNT\@D;CTGP:^('Q'\>>*?!US?

M7=TVF7FGWMSXBM)-,2.WL;F.55MXK:?8/,1P9.0TA945@0#R ?0VN^*+#PY<

MZ3;WLIBDU2Z%E:@1.^^4HSA25!"_*C'+8'&,Y(K7)'K7D7QQ\:>(O"7C'X46

MNCW]O;:=KOB+^RM1@EMA(\L9M9Y5VON&S#0C.!DYZCOXYX'^+GQ%FU3P-?ZQ

MXHM[^VU/Q]JWA&[TZ#3HH87@A-YY/) !(W#.,BO,?VGVOHM0

M^$HM-=O=&BNO&EI:7'V0Q!94-O<.-V]&!PT:D \9Z@D#'C'A_P 5>)? ?B;Q

M+JND:X(M,O/C%_8EYIM;%?)Z_%WXE3Z?XO\ LA/B&ZT;

MQU=:.]IHD%O;WSZ;':I)BU2\?!CQE%X]^&.@^(8[Y[

M];VU#MQ!H Z6Y\2:;:ZY;:,]];KJL\#W4=D90)6A

M1E5I O4J"Z@GU85I%A@\BOBSXK:SJ&D^,/#_ ,?(](U-=.T76A93:@)H?LS>

M')L6\C;1+YF/-(N@3'TQG@9KHOC'\3?B'I?C/XL6>A>*[;3-,\->"H/%>FK#

MI<4K-)FZW12-(6#*_D#) !P?EP>2 ?661GK2 @]^]?'7B?\ :)\:_#6?7;[4

MM3@UJTG\"67BR"WDM5@CTR66[2WD 9 6:)5D\P[][?(><'%6O%OQ/^(VBZ=;

M7VE^/O#.KV.H>(=#M;5[-8]1FBMKN<0R!Y$CACVL3N4A"V PST8 'UVS!03D

M5SG@;XB>'OB1I]W?>&]5M]7L[2[DL9I[8DHLZ8WID@9(R.1Q7S=HOQP\567C

M:7P%K'B0O+)X[G\.Q>)9+2"*5+==-CO5CVA/*\UF?RU)3[H/!:N%^&GC'Q1X

M9UE-%T#Q5:HFN?%_7=&U2=[**:9U:&:5)1R%0[H/^T+=9IT6X+_#-I!?:3?R3Z)+(MW5SQE#T&<\Y .W+ #J.*YG7?B/H7AN^N+/4KY+.:WT^35)C,K

M+'';(P5I&DQM !(XSGOBOE+2?V@_&7AJY\)W'B;7[V\M-)O;_P ->,HHK.U1

M5U(-*+"9=L65$OEC"@@?OH.N3N] F\5>,M+^)5WX)UW7H]6L)/AW<:O-NLXX

MIOM@F$3$N@ *X8@ *O&,Y/- 'K>@_&OP;XGU/P]IVF:];7=]X@TS^V=,MT#[

M[FS^7]\ 1\J_.OWL9S[&NYSBOBSX!D'Q+^R9S_S3"]_]$Z;7N/Q\\;W_ (>O

M-'TO1_$;G/ KT+X%37M]\;/C0;WQ)=ZG#;ZCIJVUI*8C$DI7^

MKGP_X$TW5;+096C:!Y-VI94#9O"@QJYVL"<')( [?PAX_\ $UE\9O#'ANXU

MD>+_ [XC\+2:V+T6\4;6+++P/JD'AF/6M)N[](FCOYWFFC96\P$&*/RHMRIASYW48KQ_P"(WC'Q

M1X2\:?'7QMX>\00:?>Z'X6\/:HXAM8YXKY@MV=A,@)6)AGEHI-P ZBOE;Q=\;O$&G?$G08]&\2)J.E77C2'PU>VILX([6U5[)G>+<3Y\DR

M/M