UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

EXCHANGE ACT OF 1934

OR

OF 1934

OR

ACT OF 1934

For

the year ended

OR

EXCHANGE ACT OF 1934

Date of event requiring this shell company report_________________

For the transition period from to

Commission

file number

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

Beijing

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Symbol | Name of each exchange on which registered | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the transition report: ordinary shares, par value $0.001 per share, as of December 31, 2021.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐

Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐

Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | |

| Non-accelerated filer ☐ | Emerging

growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act:

☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International

Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

☐

Yes ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

MOXIAN (BVI) INC

FORM 20-F ANNUAL REPORT

TABLE OF CONTENTS

| i |

PART I

CERTAIN INFORMATION

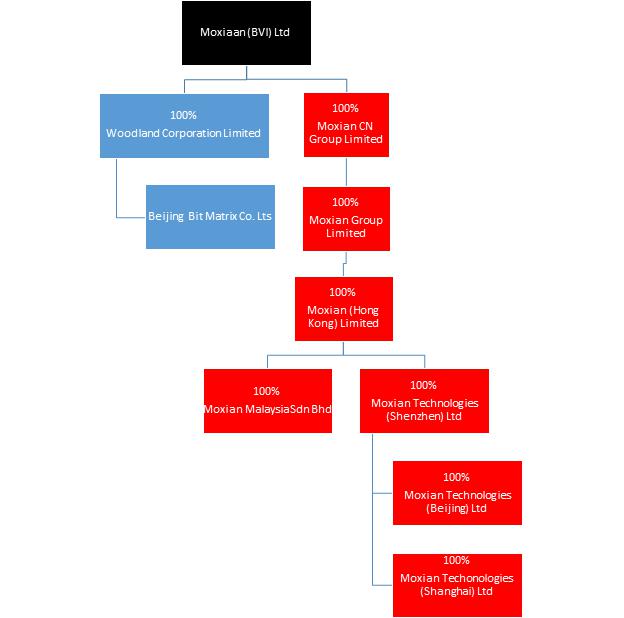

In this annual report on Form 20-F, unless otherwise indicated, “we,” “us,” “our,” the “Company,” “Moxian BVI” and “Moxian” refer to Moxian (BVI) Inc, a company incorporated in the British Virgin Islands, its predecessor entity and its subsidiaries, including its offshore subsidiaries and PRC subsidiaries.

References to “offshore subsidiaries” are to:

| ● | Moxian CN Group Limited (“Moxian Samoa”), a company established under the laws of Samoa and a wholly-owned subsidiary of Moxian; |

| ● | Woodland Corporation Limited (“Woodland”), a company established under the laws of Hong Kong SAR and a wholly-owned subsidiary of Moxian; |

| ● | Moxian (Hong Kong) Limited (“Moxian HK”), a company established under the laws of Hong Kong SAR and a wholly-owned subsidiary of Moxian Group Limited; |

| ● | Moxian Group Limited, a company established under the laws of the British Virgin Islands and wholly-owned subsidiary of Moxian Samoa; |

| ● | Moxian Malaysia Sdn.Bhd, a company established under the laws of Malaysia and a wholly-owned subsidiary of Moxian HK; and |

| ● | Abit USA, Inc., a Delaware corporation and wholly-owned subsidiary of the Company. |

References to “PRC subsidiaries” are to:

| ● | Moxian Technology Services (Shenzhen) Co. Ltd (“Moxian Shenzhen”), a wholly-owned subsidiary of Moxian HK; |

| ● | Moxian Technology Services (Beijing) Co. Ltd. (“Moxian Beijing”), a wholly-owned subsidiary of Moxian Shenzhen; |

| ● | Moxian Technology Services (Shanghai) Co. Ltd (“Moxian Shanghai”), a wholly-owned subsidiary of Moxian Shenzhen; |

| ● | Beijing BitMarix Co. Ltd. (“BitMarix”), a wholly-owned subsidiary of Woodland. |

Unless the context indicates otherwise, all references to “China” and the “PRC” refer to the People’s Republic of China, all references to “Renminbi” or “RMB” are to the legal currency of the People’s Republic of China, all references to “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States. This annual report contains translations of Renminbi amounts into U.S. dollars at specified rates solely for the convenience of the reader. We make no representation that the Renminbi or U.S. dollar amounts referred to in this report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 that represent our beliefs, projections and predictions about future events. All statements other than statements of historical fact are “forward-looking statements,” including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. Words such as “may”, “will”, “should”, “could”, “would”, “predicts”, “potential”, “continue”, “expects”, “anticipates”, “future”, “intends”, “plans”, “believes”, “estimates” and similar expressions, as well as statements in the future tense, identify forward-looking statements.

These statements are necessarily subjective and involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements described in or implied by such statements. Actual results may differ materially from expected results described in our forward-looking statements, including with respect to correct measurement and identification of factors affecting our business or the extent of their likely impact, and the accuracy and completeness of the publicly available information with respect to the factors upon which our business strategy is based or the success of our business.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of whether, or the times by which, our performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and management’s belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those factors discussed under the headings “Risk Factors”, “Operating and Financial Review and Prospects,” and elsewhere in this report.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable for annual reports on Form 20-F.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable for annual reports on Form 20-F.

| 1 |

ITEM 3. KEY INFORMATION

Our Corporate Structure and the Operations of Our PRC Subsidiaries

Moxian (BVI) Inc, or Moxian BVI, is not a PRC operating company but a British Virgin Islands holding company with operations primarily conducted through its operating subsidiaries located in China and the United States. During the 2019, 2020 and 2021 fiscal years, substantially all of the business operations were conducted in the People’s Republic of China (“PRC” or “China”) by our PRC subsidiaries. None of our PRC subsidiaries operates with a variable interest entity (“VIE”) structure, but Chinese regulatory authorities could disallow our current operating structure, which would likely result in a material change in our operations and/or cause the value of such securities to significantly decline or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in China — The Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or cause the value of our securities to significantly decline or be worthless.”

We face significant legal and operational risks and uncertainties relating to our subsidiaries’ operations in China. The Chinese government may intervene or influence the operation of our PRC subsidiaries and exercise significant oversight and discretion over the conduct of their business and may intervene in or influence their operations at any time, or may exert more control over securities offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in operations of our PRC subsidiaries and/or the value of our common stock. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. We do not believe that we are directly subject to these regulatory actions or statements, as we do not have a variable interest entity structure and our operations are not subject to cybersecurity review requirements, or involve any other type of restricted industry. In addition, starting from the first quarter of 2022, we have changed our primary business operations from digital advertising in China to bitcoin mining operations in the United States. Because these PRC government statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies in China will respond to them, or what existing or new laws or regulations will be modified or promulgated, if any, or the potential impact such modified or new laws and regulations will have on our daily business operations or our ability to accept foreign investments and list on an U.S. exchange.

Permissions Required from the PRC Authorities for Our Operations and Issuance of Securities

We conduct our business primarily through our subsidiaries, including our PRC subsidiaries in China. Our operations in China are governed by PRC laws and regulations. Our digital advertising business operations are conducted by Moxian Technology Services (Beijing) Co. Ltd. (“Moxian Beijing”). Moxian Beijing is required to obtain a Business License and has obtained such license. The remaining subsidiaries have not been in active operations and are not currently required to obtain a license or permit from the government authorities. However, given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by government authorities, we cannot assure you that we have obtained all the permits or licenses required by the PRC government authorities for conducting our business in China. We may be required to obtain additional licenses, permits, filings or approvals for the functions and services in our business operations in the future. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in China—We may be adversely affected by the complexity, uncertainties and changes in PRC regulation of internet- related or finance-related businesses and companies, and any lack of requisite approvals, licenses, permits or filings applicable to our business may have a material adverse effect on our business and results of operations.”

Furthermore, we are subject to PRC rules and regulations relating to overseas listing and securities offering, and a substantial extension of the PRC government’s oversight over our business operations or overseas listings may hinder our ability to offer or continue to offer our securities. Under current PRC laws, regulations and regulatory rules, we, our PRC subsidiaries may be required to obtain permissions from the China Securities Regulatory Commission, or the CSRC in connection with any future offering and listing on overseas capital markets.

| 2 |

On June 10, 2021, the Standing Committee of the National People’s Congress of China promulgated the Data Security Law which took effect on September 1, 2021. The Data Security Law provides for data security and privacy obligations of entities and individuals carrying out data activities, prohibits entities and individuals in China from providing any foreign judicial or law enforcement authority with any data stored in China without approval from the competent PRC authority, and sets forth the legal liabilities of entities and individuals found to be in violation of their data protection obligations, including rectification order, warning, fines of up to RMB10 million, suspension of relevant business, and revocation of business permits or licenses. The Data Security Law is relatively new, and therefore there are substantial uncertainties with respect to the interpretation and implementation of the law. We may need to adjust our operations to comply with data security requirements from time to time. If we were found to have violations, we may be ordered to rectify and terminate any actions that are deemed illegal by the government authorities and become subject to fines and other government sanctions, which may materially and adversely affect our business, financial condition, and results of operations.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Severe and Lawful Crackdown on Illegal Securities Activities, which took effect on the same day. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies. These opinions proposed to take effective measures, such as promoting the construction of relevant regulatory systems, to deal with the risks and incidents facing China-based overseas-listed companies and the demand for cybersecurity and data privacy protection. As of the date of this report, no official guidance and related implementation rules have been issued in relation to these recently issued opinions and the interpretation and implementation of these opinions remain unclear at this stage.

On July 10, 2021, the Cyberspace Administration of China and other regulatory agencies issued the Revised Measures for Cybersecurity Review (the “Revised Cybersecurity Measures”), which was finalized in December 2021 and took effect on February 15, 2022. The Revised Cybersecurity Measures authorize the relevant government authorities to conduct cybersecurity review on a range of activities that affect or may affect national security, including listings in foreign countries by companies that possess personal data of more than one million users. The PRC National Security Law covers various types of national security, including technology security and information security. Given the nature of our business of digital advertising in China and the fact that none of our PRC subsidiaries is an “internet platform operator,” or runs an App, we believe that we are not subject to a cybersecurity review pursuant to the Revised Cybersecurity Measures.

On December 24, 2021, the CSRC issued Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Administration Provisions”), and the Provisions of the State Council on the Administrative Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Measures”). The Administration Provisions and Measures for overseas listings lay out specific requirements for filing documents and include unified regulation management, strengthening regulatory coordination, and cross-border regulatory cooperation. Domestic companies seeking to list abroad must carry out relevant security screening procedures if their businesses involve such supervision. Companies endangering national security are among those off-limits for overseas listings. According to Relevant Officials of the CSRC Answered Reporter Questions (“CSRC Answers”), after the Administration Provisions and Measures are implemented upon completion of public consultation and due legislative procedures, the CSRC will formulate and issue guidance for filing procedures to further specify the details of filing administration and ensure that market entities could refer to clear guidelines for filing, which means it will still take time to put the Administration Provisions and Measures into effect. As of the date of this report, the Administration Provisions and Measures have not yet come into effect. However, according to CSRC Answers, only new initial public offerings and financing by existing overseas listed Chinese companies will be required to go through the filing process; other overseas listed companies will be allowed sufficient transition period to complete their filing procedure. The Company may be required to obtain approval of and filling with the CSRC or other PRC government authorities for its future financing. However, it is uncertain when the Administration Provision and the Measures will take effect or if they will take effect as currently drafted. Currently, the period for public comment on these draft regulations has ended and their provisions and anticipated adoption or effective date are subject to changes and thus their interpretation and implementation remain substantially uncertain. It also remains unclear on whether a US-listed company, like us, is subject to the CSRC filing procedures, to maintain the listing of its securities in a foreign country. As of the date of this report, we cannot predict the impact of these regulations on maintaining the listing status of our ordinary shares and/or other securities, or any of our future offerings of securities in the overseas markets.

| 3 |

Based on PRC laws and regulations effective as of the date of this report and subject to different interpretations of these laws and regulations that may be adopted by PRC authorities, we believe that, as of the date of this report, we and our PRC subsidiaries are not required to obtain any permission from the CSRC, the CAC or any other PRC authority in connection with our securities offerings. As a result, we have not submitted any application to the CSRC, the CAC or other PRC authorities for the approval of our securities offerings. As of the date of this report, we and our PRC subsidiaries have not received any inquiry, notice, warning or objection in relation to our securities offerings from the CSRC, the CAC or any other PRC authorities. If we fail to obtain the relevant approval or complete other review or filing procedures for any future offshore offering or listing, we may face sanctions by the CSRC, CAC or other PRC regulatory authorities, which may include fines and penalties on our operations in China, limitations on our operating privileges in China, restrictions on or prohibition of the payments or remittance of dividends by our PRC subsidiaries, restrictions on or delays to our future financing transactions, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our common shares. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in China—The PRC government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or cause the value of our securities to significantly decline or be worthless.”

Cash and Other Assets Transfers within our Organization and Dividend Distribution

Cash may be transferred within our organization in the following manners: (i) Moxian BVI may transfer funds to our subsidiaries, including our PRC subsidiaries, by way of capital contributions or loans, through intermediate holding companies or otherwise; (ii) we and our intermediate holding subsidiaries may provide loans to our operating subsidiaries and vice versa; and (iii) our subsidiaries may make dividends or other distributions to us through intermediate holding companies or otherwise. As a holding company, Moxian BVI, may rely on dividends and other distributions on equity paid by our subsidiaries for our cash and liquidity requirements. As of the date of this report, none of our subsidiaries has made any dividends or other distributions to Moxian BVI, nor have we ever made a dividend or distribution to our shareholders.

During the 2019, 2020 and 2021 fiscal years, no assets other than cash were transferred through our organization. Moxian BVI, through its intermediate holding companies, transferred approximately $3.1 million to its subsidiaries in China in fiscal year 2021.

Our subsidiaries presently intend to retain any earnings to fund their operations and business expansions. We do not anticipate paying dividends or other distributions to our shareholders in the foreseeable future.

The Holding Foreign Companies Accountable Act

Our common shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the HFCAA if the PCAOB determines it is unable to inspect or investigate completely our auditors for three consecutive years beginning in 2021. Further, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”) and on February 4, 2022, the U.S. House of Representatives passed the America Creating Opportunities for Manufacturing Pre-Eminence in Technology and Economic Strength (COMPETES) Act of 2022, or the COMPETES Act. If either the AHFCAA or COMPETES Act is enacted into law, it would amend the HFCAA and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections or complete investigations for two consecutive years instead of three.

Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China and (2) Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Since our auditor, Centurion ZD CPA & Co. is located in Hong Kong, a jurisdiction where the PCAOB found it has been unable to inspect or investigate completely the audit work by auditors because of a position taken by the authorities in Hong Kong, which may impact our ability to remain listed on a United States or other foreign exchange. The related risks and uncertainties could cause the value of our shares to significantly decline. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PCAOB is currently unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections or investigation completely over our auditor deprives our investors with the benefits of such inspections” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Our ordinary shares will be prohibited from trading in the United States under the HFCAA in 2024 if the PCAOB is unable to inspect or fully investigate auditors located in China, or as early as 2023 if proposed changes to the law are enacted. The delisting of our ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment.”

Merger

The Company is the surviving company following a merger in August 2021 with its predecessor company, Moxian, Inc., which was incorporated in Nevada, U.S. As an offshore holding company incorporated in the British Virgin Islands, we are qualified as a “foreign private issuer” within the meaning of the rules under the Exchange Act. As such, we are exempt from certain rules under the Exchange Act that are applicable to U.S. domestic issuers. Moreover, we are not required to provide as many Exchange Act reports, or as frequently or as promptly, as U.S. domestic issuers. We are also not required to provide the same level of disclosure on certain issues. In addition, as a company incorporated in the British Virgin Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from that applied to the U.S. domestic issuers under the Nasdaq listing rules. These exemptions and practices may afford less protection to our shareholders than they would enjoy if we were a U.S. domestic issuer.

| 4 |

On December 28 2021, the shareholders of the Company approved a private placement of up to 20,000,000 new ordinary shares at a price of $2.50 per share and to use the proceeds as working capital for a bitcoin mining business as the Company intended to diversify its business operations. Pursuant to these approvals, in February 2022, the Company issued 16,000,000 ordinary shares for aggregate gross proceeds of $40 million and acquired mining assets and related equipment for $29.8 million. On March 5, 2022 the first of these bitcoin mining machines began operation near Buffalo in the United States and the other machines will progressively be utilized in operation in the ensuing months.

Selected Financial Data

The Company has a December 31 fiscal year-end which is different from that of its predecessor company which fiscal year-end was September 30. Because of this change, the following table presents the selected consolidated financial information of our Company as of December 31, 2021, the transitional period for the three months ended December 31, 2020 and the fiscal years ended September 30, 2020 and 2019. The selected consolidated statements of operations data and the selected consolidated balance sheets data have been derived from our audited consolidated financial statements, which are included in this annual report. These audited consolidated financial statements begin on F-1 and are prepared and presented in accordance with accounting principles generally accepted in the United States, or U.S. GAAP. Our historical results do not necessarily indicate results expected for any future period. You should read the following selected financial data in conjunction with the consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this report.

Summary Consolidated Statements of Operations:

| For the period ended | ||||||||||||||||

| December 31, 2021 | December 31, 2020 | September 30, 2020 | September 30, 2019 | |||||||||||||

| Revenues | $ | 219,330 | $ | - | $ | 946,466 | $ | 370,411 | ||||||||

| Operating expenses | (3,085,470 | ) | (387,160) | (873,750) | (900,105 | ) | ||||||||||

| Adjustment for accrued expenses no longer required | - |

- |

- |

830,149 |

||||||||||||

| Other income, net | 126,290 | - | - | - | ||||||||||||

| Loss before income taxes | (2,739,850 | ) | (387,160) | 72,716 | 300,455 | |||||||||||

| Income tax | - | - | - | - | ||||||||||||

| Net (loss)/profit | $ | (2,739,850 | ) | $ | (387,160) | $ | 72,716 | $ | 300,455 | |||||||

Summary Consolidated Balance Sheet Data:

The following table presents our summary consolidated balance sheet data as of December 31, 2021, December 31, 2020, September 30, 2020 and 2019.

| December 31, | December 31, | September 30, | September 30, | |||||||||||||

| 2021 | 2020 | 2020 | 2019 | |||||||||||||

| Cash and cash equivalents | $ | 2,507,404 | $ | 19,402 | $ | 5,249 | $ | 425,632 | ||||||||

| Digital Asset | 5,000,000 |

- | - | - | ||||||||||||

| Other assets | 229,708 | 2,172,790 | 2,290,408 | 2,100,000 | ||||||||||||

| Total assets | 7,737,112 | 2,192,192 | 2,295,657 | 2,525,632 | ||||||||||||

| Total liabilities | 1,170,096 | 2,100,912 | 1,894,884 | 2,376,945 | ||||||||||||

| Total shareholders’ equity | $ | 6,567,016 | $ | 91,280 | $ | 400,773 | $ | 148,687 | ||||||||

| 5 |

3B. Capitalization and Indebtedness

Not Applicable for annual reports on Form 20-F.

3C. Reasons for The Offer and Use of Proceeds

Not Applicable for annual reports on Form 20-F.

3D. Risk Factors

An investment in our ordinary shares involves a high degree of risk. You should carefully consider the risks and uncertainties described below together with all other information contained in this annual report, including the matters discussed under the headings “Forward-Looking Statements” and “Operating and Financial Review and Prospects” before you decide to invest in our ordinary shares. We are a holding company with operations in China and are subject to a legal and regulatory environment that in many respects differs from the United States. If any of the following risks, or any other risks and uncertainties that are not presently foreseeable to us, actually occur, our business, financial condition, results of operations, liquidity and our future growth prospects could be materially and adversely affected.

Summary Of Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows, and prospects. These risks are discussed more fully below and include, but are not limited to, risks related to:

General Risks

| ● | Failure to manage our liquidity and cash flows may materially and adversely affect our financial conditions and results of operations. As a result, we may need additional capital, and financing may not be available on terms acceptable to us, or at all. | |

| ● | We have a history of operating losses, and we may not be able to achieve or sustain profitability; we have recently shifted our bitcoin mining business, and we may not be successful in this business. | |

| ● | Our results of operation may fluctuate significantly and may not fully reflect the underlying performance of our business. | |

| ● | We may acquire other businesses, form joint ventures or acquire other companies or businesses that could negatively affect our operating results, dilute our stockholders’ ownership, increase our debt or cause us to incur significant expense; notwithstanding the foregoing, our growth may depend on our success in uncovering and completing such transactions. | |

| ● | From time to time we may evaluate and potentially consummate strategic investments or acquisitions, which could require significant management attention, disrupt our business and adversely affect our financial results. | |

| ● | We incur significant costs and demands upon management and accounting and finance resources as a result of complying with the laws and regulations affecting public companies; if we fail to maintain proper and effective internal controls, our ability to produce accurate and timely financial statements could be impaired, which could harm our operating results, our ability to operate our business and our reputation. | |

| ● | We face risks related to the novel Coronavirus (COVID-19) outbreak, which could significantly disrupt our operations and financial results. |

Risks related to Bitcoin Mining

| ● | Our results of operations are expected to vary with Bitcoin price volatility. | |

| ● | Our mining operating costs outpace our mining revenues, which could seriously harm our business or increase our losses. | |

| ● | We have an evolving business model which is subject to various uncertainties. | |

| ● | Regulatory changes or actions may alter the nature of an investment in us or restrict the use of cryptocurrencies in a manner that adversely affects our business, prospects or operations. | |

| ● | The development and acceptance of cryptographic and algorithmic protocols governing the issuance of and transactions in cryptocurrencies is subject to a variety of factors that are difficult to evaluate. | |

| ● | Banks and financial institutions may not provide banking services, or may cut off services, to businesses that engage in bitcoin-related activities or that accept cryptocurrencies as payment, including financial institutions of investors in our securities. | |

| ● | We may face risks of Internet disruptions, which could have an adverse effect on the price of cryptocurrencies. | |

| ● | Acceptance and/or widespread use of bitcoin is uncertain. | |

| ● | The decentralized nature of bitcoin systems may lead to slow or inadequate responses to crises, which may negatively affect our business. | |

| ● | Our bitcoins may be subject to loss, theft or restriction on access. | |

| ● | There is a lack of liquid markets, and possible manipulation of blockchain/bitcoin-based assets. | |

| ● | Incorrect or fraudulent bitcoin transactions may be irreversible. | |

| ● | Our reliance primarily on a single model of miner may subject our operations to increased risk of mine failure. | |

| ● | Our future success will depend in large part upon the value of bitcoin; the value of bitcoin may be subject to pricing risk and has historically been subject to wide swings. | |

| ● | Cryptocurrencies, including those maintained by or for us, may be exposed to cybersecurity threats and hacks. |

| 6 |

| ● | We are subject to risks associated with our need for significant electrical power. Government regulators may potentially restrict the ability of electricity suppliers to provide electricity to mining operations, such as ours. | |

| ● | We may not adequately respond to price fluctuations and rapidly changing technology, which may negatively affect our business. |

Risks related to our Digital Advertising Business

| ● | We are dependent on our relationship with Xinhua New Media. | |

| ● | We may not be able to attract new clients and retain key staff. | |

| ● | Our business is largely centered in Beijing and our services provided to our clients are geographically limited. |

Risks Involving Intellectual Property

| ● | Bitcoin and bitcoin mining operations rely on software and specialized technology. | |

| ● | We may not be able to prevent others from unauthorized use of our intellectual property, which could harm our business and competitive position. | |

| ● | We may be subject to intellectual property infringement claims, which may be expensive to defend and may disrupt our business and operations | |

| ● | Our platform and internal systems rely on software that is highly technical, and if it contains undetected errors, our business could be adversely affected. |

Risks Related to Doing Business in China

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and results of operations. | |

| ● | Uncertainties in the interpretation and enforcement of Chinese laws and regulations could limit the legal protections available to us. | |

| ● | The PRC government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or cause the value of our securities to significantly decline or be worthless. | |

| ● | PRC regulations establish complex procedures for some acquisitions conducted by foreign investors, which could make it more difficult for us to pursue growth through acquisitions in China. | |

| ● | The PCAOB is currently unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections or investigation completely over our auditor deprives our investors with the benefits of such inspections. | |

| ● | Our ordinary shares will be prohibited from trading in the United States under the HFCAA in 2024 if the PCAOB is unable to inspect or fully investigate auditors located in China, or as early as 2023 if proposed changes to the law are enacted. The delisting of our ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. | |

| ● | PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may limit our ability to inject capital into our PRC subsidiaries, limit our subsidiaries’ ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us | |

| ● | PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using offshore funds to make loans to our PRC subsidiaries, or to make additional capital contributions to our PRC subsidiaries. | |

| ● | Regulatory bodies of the United States may be limited in their ability to conduct investigations or inspections of our operations in China. | |

| ● | Enhanced scrutiny over acquisition transactions by the PRC tax authorities may have a negative impact on potential acquisitions we may pursue in the future. | |

| ● | Fluctuations in exchange rates could have a material adverse effect on our results of operations and the value of your investment. |

| 7 |

Risks Related to Our Ordinary Shares

| ● | Our ordinary shares may be thinly traded and you may be unable to sell at or near ask prices or at all if you need to sell your shares to raise money or otherwise desire to liquidate your shares. | |

| ● | We are not likely to pay cash dividends in the foreseeable future. | |

| ● | You may face difficulties in protecting your interests as a shareholder, as the laws of British Virgin Islands provides substantially less protection when compared to the laws of the United States and it may be difficult for a shareholder of ours to effect service of process or to enforce judgements obtained in the United States courts. | |

| ● | Volatility in our ordinary shares price may subject us to securities litigation. | |

| ● | We may be unable to comply with the applicable continued listing requirements of the Nasdaq Capital Market, which may adversely impact our access to capital markets and may cause us to default certain of our agreements |

General Risks

If we are unable to successfully execute our bitcoin mining, it would adversely affect our financial and business condition and results of operations.

As of the date of this Report, the Company has yet to fully implement its plan to diversify into bitcoin mining as various mining sites have not been finalized. If we cannot execute the bitcoin mining, it would seriously affect our financial and business condition and deepen the losses of the Company.

Failure to manage our liquidity and cash flows may materially and adversely affect our financial conditions and results of operations. As a result, we may need additional capital, and financing may not be available on terms acceptable to us, or at all.

The Company is new to bitcoin mining and is operating in the United States for the first time. If we fail to manage our liquidity and cash flows, it will seriously affect our financial condition and results of operations. We may need additional financing and such access may be limited or at unacceptable terms.

We have a history of operating losses, and we may not be able to achieve or sustain profitability; we have recently shifted our bitcoin mining business, and we may not be successful in this business.

We are not profitable and have incurred losses since our inception. We expect to continue to incur losses for the foreseeable future, and these losses could increase as we continue to work to develop our business. We were previously engaged in the business of mobile payments which we ceased operation in June 2018. Whilst we continue with the digital advertising business, it is proving to be increasingly difficult because of restrictions on online gaming. which is a key business of our clients. Starting in March 2022, we diversified into the bitcoin mining business. Our current strategy is new and unproven, is in an industry that is relatively itself new and evolving and is subject to the risks discussed below. Even if we achieve profitability in the future, we may not be able to sustain profitability in subsequent periods.

Our results of operation may fluctuate significantly and may not fully reflect the underlying performance of our business.

Our results of operations, including the levels of our net revenues, expenses, net loss and other key metrics, may vary significantly in the future due to a variety of factors, some of which are outside of our control, and period-to-period comparisons of our operating results may not be meaningful, especially given our limited operating history. Accordingly, the results for any one quarter are not necessarily an indication of future performance. Fluctuations in quarterly results may adversely affect the market price of our ordinary shares. Factors that may cause fluctuations in our quarterly financial results include:

| ● | the amount and timing of operating expenses related to our new business operations and infrastructure; |

| ● | fluctuations in the price of bitcoin; and |

| ● | general economic, industry and market conditions. |

| 8 |

We may acquire other businesses, form joint ventures or acquire other companies or businesses that could negatively affect our operating results, dilute our stockholders’ ownership, increase our debt or cause us to incur significant expense; notwithstanding the foregoing, our growth may depend on our success in uncovering and completing such transactions.

We are actively seeking other business opportunities, however, we cannot offer any assurance that acquisitions of businesses, assets and/or entering into strategic alliances or joint ventures will be successful. We may not be able to find suitable partners or acquisition candidates and may not be able to complete such transactions on favorable terms, if at all. If we make any acquisitions, we may not be able to integrate these acquisitions successfully into our existing infrastructure. In addition, in the event we acquire any existing businesses we could assume unknown or contingent liabilities.

Any future acquisitions also could result in the issuance of stock, incurrence of debt, contingent liabilities or future write-offs of intangible assets or goodwill, any of which could have a negative impact on our cash flows, financial condition and results of operations. Integration of an acquired company may also disrupt ongoing operations and require management resources that otherwise would be focused on developing and expanding our existing business. We may experience losses related to potential investments in other companies, which could harm our financial condition and results of operations. Further, we may not realize the anticipated benefits of any acquisition, strategic alliance or joint venture if such investments do not materialize.

To finance any acquisitions or joint ventures, we may choose to issue ordinary shares, preferred stock or a combination of debt and equity as consideration, which could significantly dilute the ownership of our existing stockholders or provide rights to such preferred stock holders in priority over our common stock holders. Additional funds may not be available on terms that are favorable to us, or at all. If the price of our common stock is low or volatile, we may not be able to acquire other companies or fund a joint venture project using stock as consideration.

From time to time we may evaluate and potentially consummate strategic investments or acquisitions, which could require significant management attention, disrupt our business and adversely affect our financial results.

We may evaluate and consider strategic investments, combinations, acquisitions or alliances in both the bitcoin mining business. These transactions could be material to our financial condition and results of operations if consummated. If we are able to identify an appropriate business opportunity, we may not be able to successfully consummate the transaction and, even if we do consummate such a transaction, we may be unable to obtain the benefits or avoid the difficulties and risks of such transaction.

Strategic investments or acquisitions will involve risks commonly encountered in business relationships, including:

| ● | difficulties in assimilating and integrating the operations, personnel, systems, data, technologies, products and services of the acquired business; | |

| ● | inability of the acquired technologies, products or businesses to achieve expected levels of revenue, profitability, productivity or other benefits; | |

| ● | difficulties in retaining, training, motivating and integrating key personnel; | |

| ● | diversion of management’s time and resources from our normal daily operations; | |

| ● | difficulties in successfully incorporating licensed or acquired technology and rights into our businesses; | |

| ● | difficulties in maintaining uniform standards, controls, procedures and policies within the combined organizations; | |

| ● | difficulties in retaining relationships with customers, employees and suppliers of the acquired business; | |

| ● | risks of entering markets, including the U.S., in which we have limited or no prior experience; |

| 9 |

We may not make any investments or acquisitions, or any future investments or acquisitions may not be successful, may not benefit our business strategy, may not generate sufficient revenues to offset the associated acquisition costs or may not otherwise result in the intended benefits. In addition, we cannot assure you that any future investment in or acquisition of new businesses or technology will lead to the successful development of new or enhanced loan products and services or that any new or enhanced loan products and services, if developed, will achieve market acceptance or prove to be profitable.

Our loss of any of our management team, our inability to execute an effective succession plan, or our inability to attract and retain qualified personnel, could adversely affect our business.

Our success and future growth will depend to a significant degree on the skills and services of our management, including our Chief Executive Officer and Chief Financial Officer. We will need to continue to grow our management in order to alleviate pressure on our existing team and in order to continue to develop our business. If our management, including any new hires that we may make, fails to work together effectively and to execute our plans and strategies on a timely basis, our business could be harmed. Furthermore, if we fail to execute an effective contingency or succession plan with the loss of any member of management, the loss of such management personnel may significantly disrupt our business.

The loss of key members of management could inhibit our growth prospects. Our future success also depends in large part on our ability to attract, retain and motivate key management and operating personnel. As we continue to develop and expand our operations, we may require personnel with different skills and experiences, and who have a sound understanding of our business and the bitcoin industry. The market for highly qualified personnel in this industry is very competitive and we may be unable to attract such personnel. If we are unable to attract such personnel, our business could be harmed.

We incur significant costs and demands upon management and accounting and finance resources as a result of complying with the laws and regulations affecting public companies; if we fail to maintain proper and effective internal controls, our ability to produce accurate and timely financial statements could be impaired, which could harm our operating results, our ability to operate our business and our reputation.

As a public reporting company, we are required to, among other things, maintain a system of effective internal control over financial reporting. Ensuring that we have adequate internal financial and accounting controls and procedures in place so that we can produce accurate financial statements on a timely basis is a costly and time-consuming effort that needs to be re-evaluated frequently. Substantial work will continue to be required to further implement, document, assess, test and remediate our system of internal controls.

If our internal control over financial reporting is not effective, we may be unable to issue our financial statements in a timely manner, we may be unable to obtain the required audit or review of our financial statements by our independent registered public accounting firm in a timely manner or we may be otherwise unable to comply with the periodic reporting requirements of the SEC, our common stock listing on Nasdaq could be suspended or terminated and our stock price could materially suffer. In addition, we or members of our management could be subject to investigation and sanction by the SEC and other regulatory authorities and to stockholder lawsuits, which could impose significant additional costs on us and divert management attention.

Because cryptocurrencies may be determined to be investment securities, we may inadvertently violate the Investment Company Act and incur large losses as a result and potentially be required to register as an investment company or terminate operations and we may incur third party liabilities.

We are engaged in the mining of bitcoins which the SEC said is currency and not securities. We therefore believe that we are not engaged in the business of investing, reinvesting, or trading in securities, and we do not hold ourselves out as being engaged in those activities. However, under the Investment Company Act a company may be deemed an investment company under section 3(a)(1)(C) thereof if the value of its investment securities is more than 40% of its total assets (exclusive of government securities and cash items) on an unconsolidated basis.

| 10 |

If, as a result of our investments and our mining activities, including investments in which we do not have a controlling interest, the investment securities we hold could exceed 40% of our total assets, exclusive of cash items and, accordingly, we could determine that we have become an inadvertent investment company. The bitcoins we own, acquire or mine may be deemed an investment security by the SEC, although we do not believe any of the cryptocurrencies we own, acquire or mine are securities. An inadvertent investment company can avoid being classified as an investment company if it can rely on one of the exclusions under the Investment Company Act. One such exclusion, Rule 3a-2 under the Investment Company Act, allows an inadvertent investment company a grace period of one year from the earlier of (a) the date on which an issuer owns securities and/or cash having a value exceeding 50% of the issuer’s total assets on either a consolidated or unconsolidated basis and (b) the date on which an issuer owns or proposes to acquire investment securities having a value exceeding 40% of the value of such issuer’s total assets (exclusive of government securities and cash items) on an unconsolidated basis. We may take actions to cause the investment securities held by us to be less than 40% of our total assets, which may include acquiring assets with our cash and bitcoin on hand or liquidating our investment securities or bitcoin or seeking a no-action letter from the SEC if we are unable to acquire sufficient assets or liquidate sufficient investment securities in a timely manner.

As the Rule 3a-2 exception is available to a company no more than once every three years, and assuming no other exclusion were available to us, we would have to keep within the 40% limit for at least three years after we cease being an inadvertent investment company. This may limit our ability to make certain investments or enter into joint ventures that could otherwise have a positive impact on our earnings. In any event, we do not intend to become an investment company engaged in the business of investing and trading securities.

Classification as an investment company under the Investment Company Act requires registration with the SEC. If an investment company fails to register, it would have to stop doing almost all business, and its contracts would become voidable. Registration is time consuming and restrictive and would require a restructuring of our operations, and we would be very constrained in the kind of business we could do as a registered investment company. Further, we would become subject to substantial regulation concerning management, operations, transactions with affiliated persons and portfolio composition, and would need to file reports under the Investment Company Act regime. The cost of such compliance would result in the Company incurring substantial additional expenses, and the failure to register if required would have a materially adverse impact to conduct our operations.

We face risks related to the novel Coronavirus (COVID-19) outbreak, which could significantly disrupt our operations and financial results.

We believe that our results of operations, business and financial condition has been adversely impacted by the effects of the novel Coronavirus (COVID-19). Currently, substantially all of our employees and operations are in China. In addition to global macroeconomic effects, the novel Coronavirus (COVID-19) outbreak and any other related adverse public health developments may cause disruption to our mining activities.

The novel Coronavirus (COVID-19) or other disease outbreak will in the short-term, and may over the longer term, adversely affect the economies and financial markets of many countries, resulting in an economic downturn that may adversely affect demand for bitcoin and impact our operating results. Although the magnitude of the impact of the novel Coronavirus (COVID-19) outbreak on our business and operations remains uncertain, the continued spread of the novel Coronavirus (COVID-19) or the occurrence of other epidemics and the imposition of related public health measures and travel and business restrictions will adversely impact our business, financial condition, operating results and cash flows. In addition, we have experienced and will experience disruptions to our business operations resulting from quarantines, self-isolations, or other movement and restrictions on the ability of our employees to perform their jobs. If we are unable to effectively service our miners, our ability to mine bitcoin will be adversely affected as miners go offline, which would have an adverse effect on our business and the results of our operations.

| 11 |

China has also limited the shipment of products in and out of its borders, which could negatively impact our ability to receive mining equipment from our China-based suppliers. Our third-party manufacturers, suppliers, sub-contractors and customers have been and will continue to be disrupted by worker absenteeism, quarantines, restrictions on employees’ ability to work, office and factory closures, disruptions to ports and other shipping infrastructure, border closures, or other travel or health-related restrictions. Depending on the magnitude of such effects on our supply chain, shipments of parts for our existing miners, as well as any new miners we purchase, may be delayed. As our miners require repair or become obsolete and require replacement, our ability to obtain adequate replacements or repair parts from their manufacturer may therefore be hampered. Supply chain disruptions could therefore negatively impact our operations. If not resolved quickly, the impact of the novel Coronavirus (COVID-19) global pandemic could have a material adverse effect on our business.

The coronavirus pandemic is an emerging serious threat to health and economic wellbeing affecting our employees, investors and our sources of supply.

The sweeping nature of the novel Coronavirus (COVID-19) pandemic makes it extremely difficult to predict how the company’s business and operations will be affected in the longer run. However, the likely overall economic impact of the pandemic is viewed as highly negative to the general economy.

Increases in labor costs in the PRC may adversely affect our business and results of operations.

The economy in China has experienced increases in inflation and labor costs in recent years. As a result, average wages in the PRC are expected to continue to increase. In addition, we are required by PRC laws and regulations to pay various statutory employee benefits, including pension, housing fund, medical insurance, work-related injury insurance, unemployment insurance and maternity insurance to designated government agencies for the benefit of our employees. The relevant government agencies may examine whether an employer has made adequate payments to the statutory employee benefits, and those employers who fail to make adequate payments may be subject to late payment fees, fines and/or other penalties. We expect that our labor costs, including wages and employee benefits, will continue to increase. Unless we are able to control our labor costs or pass on these increased labor costs to our users by increasing the fees of our services, our financial condition and results of operations may be adversely affected.

If we cannot maintain our corporate culture as we grow, we could lose the innovation, collaboration and focus that contribute to our business.

We believe that a critical component of our success is our corporate culture, which we believe fosters innovation, encourages teamwork and cultivates creativity. As we develop the infrastructure of a public company and continue to grow, we may find it difficult to maintain these valuable aspects of our corporate culture. Any failure to preserve our culture could negatively impact our future success, including our ability to attract and retain employees, encourage innovation and teamwork and effectively focus on and pursue our corporate objectives.

We do not have any business insurance coverage.

Insurance companies in China currently do not offer as extensive an array of insurance products as insurance companies in more developed economies. Currently, we do not have any business liability or disruption insurance to cover our operations. We have determined that the costs of insuring for these risks and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Any uninsured business disruptions may result in our incurring substantial costs and the diversion of resources, which could have an adverse effect on our results of operations and financial condition.

| 12 |

Risks related to Bitcoin Mining

Our results of operations are expected to vary with Bitcoin price volatility

The price of Bitcoin has experienced significant fluctuations over its relatively short existence and may continue to fluctuate significantly in the future.

We expect our results of operations to continue to be affected by the Bitcoin price as most of the revenue is from bitcoin mining production as of the filing date. Any future significant reductions in the price of Bitcoin will likely have a material and adverse effect on our results of operations and financial condition. We cannot assure you that the Bitcoin price will remain high enough to sustain our operation or that the Bitcoin price will not decline significantly in the future.

Various factors, mostly beyond our control, could impact the Bitcoin price. For example, the usage of Bitcoins in the retail and commercial marketplace is relatively low in comparison with the usage for speculation, which contributes to Bitcoin price volatility. Additionally, the reward for Bitcoin mining will decline over time, with the most recent halving event occurred in May 2020 and next one four years later, which may further contribute to Bitcoin price volatility.

Our mining operating costs outpace our mining revenues, which could seriously harm our business or increase our losses.

Our mining operations are costly and our expenses may increase in the future. We intend to use funds on hand from our private placement to continue to purchase bitcoin mining machines. This expense increase may not be offset by a corresponding increase in revenue. Our expenses may be greater than we anticipate, and our investments to make our business more efficient may not succeed and may outpace monetization efforts. Increases in our costs without a corresponding increase in our revenue would increase our losses and could seriously harm our business and financial perform

We have an evolving business model which is subject to various uncertainties.

As bitcoin assets may become more widely available, we expect the services and products associated with them to evolve. In order to stay current with the industry, our business model may need to evolve as well. From time to time, we may modify aspects of our business model relating to our strategy. We cannot offer any assurance that these or any other modifications will be successful or will not result in harm to our business. We may not be able to manage growth effectively, which could damage our reputation, limit our growth and negatively affect our operating results. Further, we cannot provide any assurance that we will successfully identify all emerging trends and growth opportunities in this business sector and we may lose out on those opportunities. Such circumstances could have a material adverse effect on our business, prospects or operations.

Regulatory changes or actions may alter the nature of an investment in us or restrict the use of cryptocurrencies in a manner that adversely affects our business, prospects or operations.

As cryptocurrencies have grown in both popularity and market size, governments around the world have reacted differently to cryptocurrencies; certain governments have deemed them illegal, and others have allowed their use and trade without restriction, while in some jurisdictions, such as in the U.S., subject to extensive, and in some cases overlapping, unclear and evolving regulatory requirements. Ongoing and future regulatory actions may impact our ability to continue to operate, and such actions could affect our ability to continue as a going concern or to pursue our new strategy at all, which could have a material adverse effect on our business, prospects or operations.

| 13 |

The development and acceptance of cryptographic and algorithmic protocols governing the issuance of and transactions in cryptocurrencies is subject to a variety of factors that are difficult to evaluate.

The use of cryptocurrencies to, among other things, buy and sell goods and services and complete transactions, is part of a new and rapidly evolving industry that employs bitcoin assets based upon a computer-generated mathematical and/or cryptographic protocol. Large-scale acceptance of cryptocurrencies as a means of payment has not, and may never, occur. The growth of this industry in general, and the use of bitcoin, in particular, is subject to a high degree of uncertainty, and the slowing or stopping of the development or acceptance of developing protocols may occur unpredictably. The factors include, but are not limited to:

| ● | continued worldwide growth in the adoption and use of cryptocurrencies as a medium to exchange; | |

| ● | governmental and quasi-governmental regulation of cryptocurrencies and their use, or restrictions on or regulation of access to and operation of the network or similar bitcoin systems; | |

| ● | changes in consumer demographics and public tastes and preferences; | |

| ● | the maintenance and development of the open-source software protocol of the network; |

| 14 |

| ● | the increased consolidation of contributors to the bitcoin blockchain through mining pools; | |

| ● | the availability and popularity of other forms or methods of buying and selling goods and services, including new means of using fiat currencies; | |

| ● | the use of the networks supporting cryptocurrencies for developing smart contracts and distributed applications; | |

| ● | general economic conditions and the regulatory environment relating to cryptocurrencies; and | |

| ● | negative consumer sentiment and perception of bitcoin specifically and cryptocurrencies generally. |

The outcome of these factors could have negative effects on our ability to continue as a going concern or to pursue our business strategy at all, which could have a material adverse effect on our business, prospects or operations as well as potentially negative effect on the value of any bitcoin or other cryptocurrencies we mine or otherwise acquire or hold for our own account, which would harm investors in our securities.

Banks and financial institutions may not provide banking services, or may cut off services, to businesses that engage in bitcoin-related activities or that accept cryptocurrencies as payment, including financial institutions of investors in our securities.

A number of companies that engage in bitcoin and/or other bitcoin-related activities have been unable to find banks or financial institutions that are willing to provide them with bank accounts and other services. Similarly, a number of companies and individuals or businesses associated with cryptocurrencies may have had and may continue to have their existing bank accounts closed or services discontinued with financial institutions in response to government action, particularly in China, where regulatory response to cryptocurrencies has been to exclude their use for ordinary consumer transactions within China. We also may be unable to obtain or maintain these services for our business. The difficulty that many businesses that provide bitcoin and/or derivatives on other bitcoin-related activities have and may continue to have in finding banks and financial institutions willing to provide them services may be decreasing the usefulness of cryptocurrencies as a payment system and harming public perception of cryptocurrencies, and could decrease their usefulness and harm their public perception in the future.

The usefulness of cryptocurrencies as a payment system and the public perception of cryptocurrencies could be damaged if banks or financial institutions were to close the accounts of businesses engaging in bitcoin and/or other bitcoin-related activities. This could occur as a result of compliance risk, cost, government regulation or public pressure. The risk applies to securities firms, clearance and settlement firms, national stock and derivatives on commodities exchanges, the over-the-counter market, and the Depository Trust Company, which, if any of such entities adopts or implements similar policies, rules or regulations, could negatively affect our relationships with financial institutions and impede our ability to convert cryptocurrencies to fiat currencies. Such factors could have a material adverse effect on our ability to continue as a going concern or to pursue our new strategy at all, which could have a material adverse effect on our business, prospects or operations and harm investors.

We may face risks of Internet disruptions, which could have an adverse effect on the price of cryptocurrencies.

A disruption of the Internet may affect the use of cryptocurrencies and subsequently the value of our securities. Generally, cryptocurrencies and our business of mining cryptocurrencies is dependent upon the Internet. A significant disruption in Internet connectivity could disrupt a currency’s network operations until the disruption is resolved and have an adverse effect on the price of cryptocurrencies and our ability to mine cryptocurrencies.

| 15 |

The impact of geopolitical and economic events on the supply and demand for cryptocurrencies is uncertain.

Geopolitical crises may motivate large-scale purchases of bitcoin and other cryptocurrencies, which could increase the price of bitcoin and other cryptocurrencies rapidly. This may increase the likelihood of a subsequent price decrease as crisis-driven purchasing behavior dissipates, adversely affecting the value of our inventory following such downward adjustment. Such risks are similar to the risks of purchasing commodities in general uncertain times, such as the risk of purchasing, holding or selling gold. Alternatively, as an emerging asset class with limited acceptance as a payment system or commodity, global crises and general economic downturn may discourage investment in cryptocurrencies as investors focus their investment on less volatile asset classes as a means of hedging their investment risk.

As an alternative to fiat currencies that are backed by central governments, cryptocurrencies, which are relatively new, are subject to supply and demand forces. How such supply and demand will be impacted by geopolitical events is largely uncertain but could be harmful to us and investors in our common stock. Political or economic crises may motivate large-scale acquisitions or sales of cryptocurrencies either globally or locally. Such events could have a material adverse effect on our ability to continue as a going concern or to pursue our new strategy at all, which could have a material adverse effect on our business, prospects or operations and potentially the value of any bitcoin or any other cryptocurrencies we mine or otherwise acquire or hold for our own account.

Acceptance and/or widespread use of bitcoin is uncertain.

Currently, there is a relatively limited use of any bitcoin in the retail and commercial marketplace, thus contributing to price volatility that could adversely affect an investment in our securities. Banks and other established financial institutions may refuse to process funds for bitcoin transactions, process wire transfers to or from bitcoin exchanges, bitcoin-related companies or service providers, or maintain accounts for persons or entities transacting in bitcoin. Conversely, a significant portion of bitcoin demand is generated by investors seeking a long-term store of value or speculators seeking to profit from the short- or long-term holding of the asset. Price volatility undermines any bitcoin’s role as a medium of exchange, as retailers are much less likely to accept it as a form of payment. Market capitalization for a bitcoin as a medium of exchange and payment method may always be low.

The relative lack of acceptance of bitcoins in the retail and commercial marketplace, or a reduction of such use, limits the ability of end users to use them to pay for goods and services. Such lack of acceptance or decline in acceptances could have a material adverse effect on our ability to continue as a going concern or to pursue our new strategy at all, which could have a material adverse effect on our business, prospects or operations and potentially the value of bitcoins we mine or otherwise acquire or hold for our own account.

Transactional fees may decrease demand for bitcoin and prevent expansion.

As the number of bitcoins currency rewards awarded for solving a block in a blockchain decreases, the incentive for miners to continue to contribute to the bitcoin network may transition from a set reward to transaction fees. In order to incentivize miners to continue to contribute to the bitcoin network, the bitcoin network may either formally or informally transition from a set reward to transaction fees earned upon solving a block. This transition could be accomplished by miners independently electing to record in the blocks they solve only those transactions that include payment of a transaction fee. If transaction fees paid for bitcoin transactions become too high, the marketplace may be reluctant to accept bitcoin as a means of payment and existing users may be motivated to switch from bitcoin to another bitcoin or to fiat currency. Either the requirement from miners of higher transaction fees in exchange for recording transactions in a blockchain or a software upgrade that automatically charges fees for all transactions may decrease demand for bitcoin and prevent the expansion of the bitcoin network to retail merchants and commercial businesses, resulting in a reduction in the price of bitcoin that could adversely impact an investment in our securities. Decreased use and demand for bitcoin may adversely affect its value and result in a reduction in the price of bitcoin and the value of our common stock.

| 16 |

The decentralized nature of bitcoin systems may lead to slow or inadequate responses to crises, which may negatively affect our business.

The decentralized nature of the governance of bitcoin systems may lead to ineffective decision making that slows development or prevents a network from overcoming emergent obstacles. Governance of many bitcoin systems is by voluntary consensus and open competition with no clear leadership structure or authority. To the extent lack of clarity in corporate governance of bitcoin systems leads to ineffective decision making that slows development and growth of such cryptocurrencies, the value of our common stock may be adversely affected.

It may be illegal now, or in the future, to acquire, own, hold, sell or use bitcoin, ether, or other cryptocurrencies, participate in blockchains or utilize similar bitcoin assets in one or more countries, the ruling of which would adversely affect us.

Although currently cryptocurrencies generally are not regulated or are lightly regulated in most countries, one or more countries such as China and Russia, which have taken harsh regulatory action, may take regulatory actions in the future that could severely restrict the right to acquire, own, hold, sell or use these bitcoin assets or to exchange for fiat currency. In many nations, particularly in China and Russia, it is illegal to accept payment in bitcoin and other cryptocurrencies for consumer transactions and banking institutions are barred from accepting deposits of cryptocurrencies. Such restrictions may adversely affect us as the large-scale use of cryptocurrencies as a means of exchange is presently confined to certain regions globally. Such circumstances could have a material adverse effect on our ability to continue as a going concern or to pursue our new strategy at all, which could have a material adverse effect on our business, prospects or operations and potentially the value of any bitcoin or other cryptocurrencies we mine or otherwise acquire or hold for our own account, and harm investors.

There is a lack of liquid markets, and possible manipulation of blockchain/bitcoin-based assets.