00018565252021FYfalsehttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberhttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberhttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberhttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberhttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberhttp://fasb.org/us-gaap/2021-01-31#ProductAndServiceOtherMemberoneonethree yearsseven yearsP1Y00018565252021-02-012022-01-3000018565252021-08-01iso4217:USD0001856525us-gaap:CommonClassAMember2022-03-25xbrli:shares0001856525us-gaap:CommonClassBMember2022-03-2500018565252022-01-3000018565252021-01-310001856525us-gaap:CommonClassAMember2022-01-30iso4217:USDxbrli:shares0001856525us-gaap:CommonClassBMember2022-01-3000018565252020-02-032021-01-3100018565252019-02-042020-02-0200018565252021-02-012021-07-2200018565252021-07-232022-01-300001856525us-gaap:CapitalUnitsMember2019-02-0300018565252019-02-030001856525us-gaap:CapitalUnitsMember2019-02-042020-02-020001856525us-gaap:CapitalUnitsMember2020-02-0200018565252020-02-020001856525us-gaap:CapitalUnitsMember2020-02-032021-01-310001856525us-gaap:CapitalUnitsMember2021-01-310001856525us-gaap:CapitalUnitsMember2021-02-012021-07-220001856525us-gaap:CapitalUnitsMember2021-07-2200018565252021-07-220001856525us-gaap:CapitalUnitsMember2021-07-232022-01-300001856525us-gaap:AdditionalPaidInCapitalMember2021-07-232022-01-300001856525us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-07-232022-01-300001856525us-gaap:CommonStockMemberus-gaap:CommonClassBMember2021-07-232022-01-300001856525us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2021-07-232022-01-300001856525us-gaap:NoncontrollingInterestMember2021-07-232022-01-300001856525us-gaap:RetainedEarningsMember2021-07-232022-01-300001856525us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMembercnm:InterestRateSwapOneMember2021-07-232022-01-300001856525cnm:InterestRateSwapOneMemberus-gaap:NoncontrollingInterestMember2021-07-232022-01-300001856525cnm:InterestRateSwapOneMember2021-07-232022-01-300001856525us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMembercnm:InterestRateSwapTwoMember2021-07-232022-01-300001856525us-gaap:NoncontrollingInterestMembercnm:InterestRateSwapTwoMember2021-07-232022-01-300001856525cnm:InterestRateSwapTwoMember2021-07-232022-01-300001856525us-gaap:CapitalUnitsMember2022-01-300001856525us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-01-300001856525us-gaap:CommonStockMemberus-gaap:CommonClassBMember2022-01-300001856525us-gaap:AdditionalPaidInCapitalMember2022-01-300001856525us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2022-01-300001856525us-gaap:RetainedEarningsMember2022-01-300001856525us-gaap:NoncontrollingInterestMember2022-01-30cnm:branch_locationcnm:state0001856525us-gaap:IPOMemberus-gaap:CommonClassAMember2021-07-272021-07-270001856525us-gaap:IPOMember2021-07-270001856525us-gaap:IPOMember2021-07-272021-07-2700018565252021-07-272021-07-270001856525us-gaap:OverAllotmentOptionMemberus-gaap:CommonClassAMember2021-08-202021-08-200001856525us-gaap:OverAllotmentOptionMember2021-08-2000018565252021-08-202021-08-200001856525cnm:SecondaryOfferingMembercnm:SellingStockholdersMemberus-gaap:CommonClassAMember2022-01-102022-01-100001856525cnm:SecondaryOfferingMembercnm:SellingStockholdersMember2022-01-100001856525cnm:SecondaryOfferingMemberus-gaap:CommonClassAMember2022-01-102022-01-100001856525us-gaap:CommonClassAMember2022-01-100001856525cnm:FormerLimitedPartnersMemberus-gaap:CommonClassAMember2022-01-1000018565252022-01-100001856525us-gaap:OverAllotmentOptionMember2021-08-202021-08-200001856525cnm:SecondaryOfferingMember2022-01-102022-01-100001856525cnm:ContinuingLimitedPartnersMemberus-gaap:CommonClassAMember2022-01-100001856525cnm:ContinuingLimitedPartnersMember2022-01-100001856525us-gaap:CommonClassBMembercnm:ContinuingLimitedPartnersMember2022-01-100001856525cnm:BlockerCompanyMember2021-07-27cnm:segment0001856525srt:MinimumMemberus-gaap:BuildingAndBuildingImprovementsMember2021-02-012022-01-300001856525srt:MaximumMemberus-gaap:BuildingAndBuildingImprovementsMember2021-02-012022-01-300001856525us-gaap:TransportationEquipmentMembersrt:MinimumMember2021-02-012022-01-300001856525srt:MaximumMemberus-gaap:TransportationEquipmentMember2021-02-012022-01-300001856525cnm:FurnitureFixturesAndEquipmentMembersrt:MinimumMember2021-02-012022-01-300001856525srt:MaximumMembercnm:FurnitureFixturesAndEquipmentMember2021-02-012022-01-300001856525us-gaap:TransferredOverTimeMember2021-02-012022-01-300001856525us-gaap:TransferredOverTimeMember2020-02-032021-01-310001856525us-gaap:TransferredOverTimeMember2019-02-042020-02-020001856525cnm:FormerLimitedPartnersMember2022-01-30xbrli:pure0001856525cnm:ContinuingLimitedPartnersMember2022-01-300001856525us-gaap:SoftwareAndSoftwareDevelopmentCostsMembersrt:MinimumMember2021-02-012022-01-300001856525srt:MaximumMemberus-gaap:SoftwareAndSoftwareDevelopmentCostsMember2021-02-012022-01-300001856525cnm:PipesValvesAndFittingProductsMember2021-02-012022-01-300001856525cnm:PipesValvesAndFittingProductsMember2020-02-032021-01-310001856525cnm:PipesValvesAndFittingProductsMember2019-02-042020-02-020001856525cnm:StormDrainageProductsMember2021-02-012022-01-300001856525cnm:StormDrainageProductsMember2020-02-032021-01-310001856525cnm:StormDrainageProductsMember2019-02-042020-02-020001856525cnm:FireProtectionProductsMember2021-02-012022-01-300001856525cnm:FireProtectionProductsMember2020-02-032021-01-310001856525cnm:FireProtectionProductsMember2019-02-042020-02-020001856525cnm:MeterProductsMember2021-02-012022-01-300001856525cnm:MeterProductsMember2020-02-032021-01-310001856525cnm:MeterProductsMember2019-02-042020-02-020001856525us-gaap:NonUsMember2021-02-012022-01-300001856525us-gaap:NonUsMember2020-02-032021-01-310001856525us-gaap:NonUsMember2019-02-042020-02-020001856525cnm:LMBagAndSupplyCoIncMember2021-08-302021-08-300001856525cnm:PacificPipeCompanyIncMember2021-08-092021-08-090001856525cnm:WaterWorksSupplyCoMember2020-08-172020-08-170001856525cnm:WaterWorksSupplyCoMemberus-gaap:CustomerRelationshipsMember2020-08-170001856525cnm:WaterWorksSupplyCoMember2020-08-170001856525cnm:RBCoMember2020-03-112020-03-110001856525cnm:RBCoMember2020-03-110001856525cnm:LongIslandPipeMember2019-07-082019-07-080001856525cnm:LongIslandPipeMember2020-03-112020-03-110001856525cnm:LongIslandPipeMember2019-07-080001856525cnm:LongIslandPipeMembersrt:MinimumMember2019-07-082019-07-080001856525cnm:LongIslandPipeMembersrt:MaximumMember2019-07-082019-07-080001856525cnm:LongIslandPipeMember2021-02-012022-01-300001856525cnm:LongIslandPipeMember2020-02-032021-01-310001856525cnm:LongIslandPipeMember2019-02-042020-02-020001856525cnm:MaskellPipeAndSupplyMember2019-02-042019-02-040001856525cnm:MaskellPipeAndSupplyMember2019-02-040001856525cnm:MaskellPipeAndSupplyMemberus-gaap:CustomerRelationshipsMember2019-02-040001856525us-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2021-02-012022-01-300001856525us-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2019-02-042020-02-020001856525cnm:LMBagAndSupplyCoIncMember2021-08-300001856525cnm:PacificPipeCompanyIncMember2021-08-090001856525cnm:LMBagAndSupplyCoIncMemberus-gaap:CustomerRelationshipsMember2021-08-302021-08-300001856525cnm:PacificPipeCompanyIncMemberus-gaap:CustomerRelationshipsMember2021-08-092021-08-090001856525us-gaap:TrademarksMembercnm:PacificPipeCompanyIncMember2021-08-092021-08-090001856525cnm:WaterWorksSupplyCoMemberus-gaap:CustomerRelationshipsMember2020-08-172020-08-170001856525cnm:RBCoMemberus-gaap:CustomerRelationshipsMember2020-03-112020-03-110001856525cnm:LongIslandPipeMembercnm:CustomerRelationshipsRetailMember2019-07-082019-07-080001856525cnm:LongIslandPipeMembercnm:CustomerRelationshipsDistributionMember2019-07-082019-07-080001856525cnm:LongIslandPipeMemberus-gaap:OtherIntangibleAssetsMember2019-07-082019-07-080001856525cnm:MaskellPipeAndSupplyMemberus-gaap:CustomerRelationshipsMember2019-02-042019-02-040001856525cnm:LMBagAndSupplyCoIncMember2021-02-012022-01-300001856525cnm:LMBagAndSupplyCoIncMember2020-02-032021-01-310001856525cnm:LMBagAndSupplyCoIncMember2019-02-042020-02-020001856525cnm:PacificPipeCompanyIncMember2021-02-012022-01-300001856525cnm:PacificPipeCompanyIncMember2020-02-032021-01-310001856525cnm:PacificPipeCompanyIncMember2019-02-042020-02-020001856525cnm:RBCoMember2021-02-012022-01-300001856525cnm:RBCoMember2020-02-032021-01-310001856525cnm:RBCoMember2019-02-042020-02-020001856525cnm:OtherAcquisitions2021Member2021-02-012022-01-300001856525us-gaap:CustomerRelationshipsMember2022-01-300001856525us-gaap:CustomerRelationshipsMember2021-01-310001856525us-gaap:OtherIntangibleAssetsMember2022-01-300001856525us-gaap:OtherIntangibleAssetsMember2021-01-310001856525cnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2022-01-300001856525cnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2021-01-310001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2022-01-300001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-01-310001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueSeptember2024Member2022-01-300001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueSeptember2024Member2021-01-310001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueAugust2025Member2022-01-300001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueAugust2025Member2021-01-310001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:RevolvingCreditFacilityMember2022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:RevolvingCreditFacilityMember2021-01-310001856525cnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2021-07-270001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-07-272021-07-270001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:RevolvingCreditFacilityMember2021-07-272021-07-270001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:RevolvingCreditFacilityMember2021-07-270001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueSeptember2024Member2021-07-272021-07-270001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueAugust2025Member2021-07-272021-07-270001856525cnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2021-07-272021-07-270001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueSeptember2024Member2021-02-012022-01-300001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueAugust2025Member2021-02-012022-01-300001856525cnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2021-02-012022-01-300001856525us-gaap:CashFlowHedgingMemberus-gaap:InterestRateSwapMember2021-02-012022-01-300001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-02-012022-01-300001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-07-272022-01-300001856525us-gaap:LondonInterbankOfferedRateLIBORMembercnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-07-272022-01-300001856525cnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMembercnm:BaseRateComponentFederalFundsRateMember2021-07-272022-01-300001856525cnm:BaseRateComponentLIBORMembercnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-07-272022-01-300001856525cnm:BaseRateComponentAdditionToPrimeLIBORFederalFundsRateMembercnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2021-07-272022-01-300001856525us-gaap:FairValueInputsLevel2Membercnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:LondonInterbankOfferedRateLIBORMembersrt:MinimumMemberus-gaap:RevolvingCreditFacilityMember2021-02-012022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:LondonInterbankOfferedRateLIBORMembersrt:MaximumMemberus-gaap:RevolvingCreditFacilityMember2021-02-012022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Membersrt:MinimumMemberus-gaap:BaseRateMemberus-gaap:RevolvingCreditFacilityMember2021-02-012022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Membersrt:MaximumMemberus-gaap:BaseRateMemberus-gaap:RevolvingCreditFacilityMember2021-02-012022-01-300001856525cnm:SeniorABLCreditFacilityDueJuly2026Memberus-gaap:RevolvingCreditFacilityMember2021-02-012022-01-300001856525cnm:SeniorTermLoanDueAugust2024Membersrt:MinimumMemberus-gaap:LoansPayableMember2021-01-310001856525us-gaap:LondonInterbankOfferedRateLIBORMembercnm:SeniorTermLoanDueAugust2024Membersrt:MinimumMemberus-gaap:LoansPayableMember2020-02-032021-01-310001856525us-gaap:LondonInterbankOfferedRateLIBORMembersrt:MaximumMembercnm:SeniorTermLoanDueAugust2024Memberus-gaap:LoansPayableMember2020-02-032021-01-310001856525cnm:SeniorTermLoanDueAugust2024Membersrt:MinimumMemberus-gaap:BaseRateMemberus-gaap:LoansPayableMember2020-02-032021-01-310001856525srt:MaximumMembercnm:SeniorTermLoanDueAugust2024Memberus-gaap:BaseRateMemberus-gaap:LoansPayableMember2020-02-032021-01-310001856525us-gaap:SeniorNotesMembercnm:SeniorNotesDueSeptember2024Member2019-09-160001856525cnm:InterestRateSwapOneMemberus-gaap:CashFlowHedgingMember2018-02-280001856525cnm:InterestRateSwapOneMemberus-gaap:CashFlowHedgingMember2021-07-272021-07-270001856525cnm:InterestRateSwapOneMemberus-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMember2021-01-310001856525cnm:InterestRateSwapOneMemberus-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMember2020-02-020001856525cnm:InterestRateSwapOneMemberus-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMember2019-02-030001856525cnm:InterestRateSwapOneMember2021-02-012022-01-300001856525cnm:InterestRateSwapOneMember2020-02-032021-01-310001856525cnm:InterestRateSwapOneMember2019-02-042020-02-020001856525cnm:InterestRateSwapOneMemberus-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMember2022-01-300001856525us-gaap:CashFlowHedgingMembercnm:InterestRateSwapTwoMember2021-07-270001856525srt:ScenarioForecastMemberus-gaap:CashFlowHedgingMembercnm:InterestRateSwapTwoMember2023-07-270001856525srt:ScenarioForecastMemberus-gaap:CashFlowHedgingMembercnm:InterestRateSwapTwoMember2024-07-270001856525srt:ScenarioForecastMemberus-gaap:CashFlowHedgingMembercnm:InterestRateSwapTwoMember2025-07-270001856525us-gaap:CashFlowHedgingMembercnm:InterestRateSwapTwoMember2022-01-300001856525us-gaap:LondonInterbankOfferedRateLIBORMembercnm:SeniorTermLoanDueJuly2028Memberus-gaap:LoansPayableMember2022-01-302022-01-300001856525cnm:InterestRateSwapTwoMember2022-01-300001856525us-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMembercnm:InterestRateSwapTwoMember2021-01-310001856525cnm:InterestRateSwapTwoMember2021-02-012022-01-300001856525us-gaap:AccumulatedGainLossCashFlowHedgeIncludingNoncontrollingInterestMembercnm:InterestRateSwapTwoMember2022-01-300001856525us-gaap:CommonClassAMember2022-01-280001856525cnm:ContinuingLimitedPartnersMember2022-01-302022-01-300001856525us-gaap:LandMember2022-01-300001856525us-gaap:LandMember2021-01-310001856525us-gaap:BuildingAndBuildingImprovementsMember2022-01-300001856525us-gaap:BuildingAndBuildingImprovementsMember2021-01-310001856525us-gaap:TransportationEquipmentMember2022-01-300001856525us-gaap:TransportationEquipmentMember2021-01-310001856525cnm:FurnitureFixturesAndEquipmentMember2022-01-300001856525cnm:FurnitureFixturesAndEquipmentMember2021-01-310001856525us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2022-01-300001856525us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2021-01-310001856525us-gaap:ConstructionInProgressMember2022-01-300001856525us-gaap:ConstructionInProgressMember2021-01-310001856525cnm:CoreAndMainHoldingsLPMembercnm:CoreAndMainIncMember2021-07-230001856525cnm:ContinuingLimitedPartnersHoldingsMembercnm:CoreAndMainHoldingsLPMember2021-07-230001856525cnm:CoreAndMainHoldingsLPMember2021-07-230001856525cnm:CoreAndMainHoldingsLPMembercnm:CoreAndMainIncMember2021-07-232021-07-230001856525cnm:ContinuingLimitedPartnersHoldingsMembercnm:CoreAndMainHoldingsLPMember2021-07-232021-07-230001856525cnm:CoreAndMainHoldingsLPMember2021-07-232021-07-230001856525cnm:CoreAndMainHoldingsLPMembercnm:CoreAndMainIncMember2021-07-242022-01-300001856525cnm:ContinuingLimitedPartnersHoldingsMembercnm:CoreAndMainHoldingsLPMember2021-07-242022-01-300001856525cnm:CoreAndMainHoldingsLPMember2021-07-242022-01-300001856525cnm:CoreAndMainHoldingsLPMembercnm:CoreAndMainIncMember2022-01-300001856525cnm:ContinuingLimitedPartnersHoldingsMembercnm:CoreAndMainHoldingsLPMember2022-01-300001856525cnm:CoreAndMainHoldingsLPMember2022-01-300001856525cnm:CoreAndMainHoldingsLPMembercnm:CoreAndMainIncMember2022-01-302022-01-300001856525cnm:ContinuingLimitedPartnersHoldingsMembercnm:CoreAndMainHoldingsLPMember2022-01-302022-01-300001856525cnm:CoreAndMainHoldingsLPMember2022-01-302022-01-300001856525srt:PartnershipInterestMember2021-01-310001856525srt:PartnershipInterestMember2021-02-012021-07-220001856525srt:PartnershipInterestMember2021-07-220001856525srt:PartnershipInterestMember2021-07-232022-01-300001856525srt:PartnershipInterestMember2022-01-300001856525srt:PartnershipInterestMember2021-07-232021-07-230001856525srt:PartnershipInterestMember2021-07-230001856525srt:PartnershipInterestMember2021-07-242022-01-300001856525srt:PartnershipInterestMember2021-02-012022-01-300001856525srt:PartnershipInterestMember2020-02-032021-01-310001856525srt:PartnershipInterestMember2019-02-042020-02-020001856525us-gaap:StockAppreciationRightsSARSMember2021-01-310001856525us-gaap:StockAppreciationRightsSARSMember2021-02-012021-07-220001856525us-gaap:StockAppreciationRightsSARSMember2021-07-220001856525us-gaap:StockAppreciationRightsSARSMember2021-07-232021-07-230001856525us-gaap:StockAppreciationRightsSARSMember2021-07-230001856525us-gaap:StockAppreciationRightsSARSMember2021-07-242022-01-300001856525us-gaap:StockAppreciationRightsSARSMember2022-01-300001856525us-gaap:StockAppreciationRightsSARSMember2021-02-012022-01-300001856525us-gaap:StockAppreciationRightsSARSMember2019-02-042020-02-020001856525cnm:OmnibusEquityIncentivePlan2021Memberus-gaap:CommonClassAMember2021-07-310001856525cnm:OmnibusEquityIncentivePlan2021Memberus-gaap:StockAppreciationRightsSARSMemberus-gaap:CommonClassAMember2021-07-310001856525us-gaap:RestrictedStockUnitsRSUMember2021-01-310001856525us-gaap:RestrictedStockUnitsRSUMember2021-02-012022-01-300001856525us-gaap:RestrictedStockUnitsRSUMember2022-01-300001856525srt:AffiliatedEntityMembercnm:CDAndRTransactionsMember2021-02-012022-01-300001856525srt:AffiliatedEntityMembercnm:CDAndRTransactionsMember2020-02-032021-01-310001856525srt:AffiliatedEntityMembercnm:CDAndRTransactionsMember2022-01-300001856525srt:AffiliatedEntityMembercnm:CDAndRTransactionsMember2021-01-310001856525srt:AffiliatedEntityMembercnm:CDAndRTransactionsMember2019-02-042020-02-020001856525srt:ParentCompanyMember2022-01-300001856525srt:ParentCompanyMemberus-gaap:CommonClassAMember2022-01-300001856525srt:ParentCompanyMemberus-gaap:CommonClassBMember2022-01-300001856525srt:ParentCompanyMember2021-04-092022-01-300001856525srt:ParentCompanyMember2021-04-08

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 30, 2022

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For transition period from to

Commission File Number 001-40650

Core & Main, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 86-3149194 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

1830 Craig Park Court

St. Louis, Missouri 63146

(314) 432-4700

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Class A common stock, par value $0.01 per share | | CNM | | The New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $924 million.

As of March 25, 2022, there were 167,522,403 shares of the registrant’s Class A common stock, par value $0.01 per share, and 78,398,141 shares of the registrant’s Class B common stock, par value $0.01 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the registrant’s 2022 Annual Meeting of Stockholders have been incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include, without limitation, all statements other than statements of historical facts contained in this Annual Report, including statements relating to our intentions, beliefs, assumptions or current expectations concerning, among other things, our future results of operations and financial position, business strategy and plans and objectives of management for future operations, including, among others, statements regarding expected growth, future capital expenditures and debt service obligations, and the anticipated impact of the novel coronavirus, or COVID-19, on our business, are forward-looking statements.

Some of the forward-looking statements can be identified by the use of forward-looking terms such as “believes,” “expects,” “may,” “will,” “shall,” “should,” “would,” “could,” “seeks,” “aims,” “projects,” “is optimistic,” “intends,” “plans,” “estimates,” “anticipates” or the negative versions of these words or other comparable terms.

Forward-looking statements are subject to known and unknown risks and uncertainties, many of which may be outside our control. We caution you that forward-looking statements are not guarantees of future performance or outcomes and that actual performance and outcomes, including, without limitation, our actual results of operations, financial condition and liquidity, and the development of the market in which we operate, may differ materially from those made in or suggested by the forward-looking statements contained in this Annual Report on Form 10-K. In addition, even if our results of operations, financial condition and cash flows, and the development of the market in which we operate, are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, those results or developments may not be indicative of results or developments in subsequent periods. A number of important factors, including, without limitation, the risks and uncertainties discussed under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Annual Report on Form 10-K, could cause actual results and outcomes to differ materially from those reflected in the forward-looking statements. Furthermore, new risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Form on Form 10-K. Factors that could cause actual results and outcomes to differ from those reflected in forward-looking statements include, without limitation:

•declines, volatility and cyclicality in the U.S. residential and non-residential construction markets;

•slowdowns in municipal infrastructure spending and delays in appropriations of federal funds;

•price fluctuations in our product costs, particularly with respect to the commodity-based products that we sell;

•our ability to manage our inventory effectively, including during periods of supply chain disruptions;

•our ability to obtain product;

•general business and economic conditions;

•risks involved with acquisitions and other strategic transactions, including our ability to identify, acquire, close or integrate acquisition targets successfully;

•the impact of seasonality and weather-related impacts, including natural disasters or similar extreme weather events;

•the fragmented and highly competitive markets in which we compete and consolidation within our industry;

•our ability to competitively bid for municipal and private contracts;

•the development of alternatives to distributors of our products in the supply chain;

•our ability to hire, engage and retain key personnel, including sales representatives, qualified branch, district and region managers and senior management;

•our ability to identify, develop and maintain relationships with a sufficient number of qualified suppliers and the potential that our exclusive or restrictive supplier distribution rights are terminated;

•the availability and cost of freight and energy, such as fuel;

•the ability of our customers to make payments on credit sales;

•changes in supplier rebates or other terms of our supplier agreements;

•our ability to identify and introduce new products and product lines effectively;

•the spread of, and response to, COVID-19, and the inability to predict the ultimate impact on us;

•costs and potential liabilities or obligations imposed by environmental, health and safety laws and requirements;

•regulatory change and the costs of compliance with regulation;

•exposure to product liability, construction defect and warranty claims and other litigation and legal proceedings;

•potential harm to our reputation;

•difficulties with or interruptions of our fabrication services;

•safety and labor risks associated with the distribution of our products as well as work stoppages and other disruptions due to labor disputes;

•impairment in the carrying value of goodwill, intangible assets or other long-lived assets;

•the domestic and international political environment with regard to trade relationships and tariffs, as well as difficulty sourcing products as a result of import constraints;

•our ability to operate our business consistently through highly dispersed locations across the United States;

•interruptions in the proper functioning of our information technology systems, including from cybersecurity threats;

•risks associated with raising capital;

•our ability to continue our customer relationships with short-term contracts;

•risks associated with exporting our products internationally;

•our ability to renew or replace our existing leases on favorable terms or at all;

•our ability to maintain effective internal controls over financial reporting and remediate any material weaknesses;

•our substantial indebtedness and the potential that we may incur additional indebtedness;

•the limitations and restrictions in the agreements governing our indebtedness, the Second Amended and Restated Agreement of Limited Partnership of Holdings and the Tax Receivable Agreements (each as defined herein);

•increases in interest rates and the impact of transitioning from LIBOR (as defined herein) as the benchmark rate in contracts;

•changes in our credit ratings and outlook;

•our ability to generate the significant amount of cash needed to service our indebtedness;

•our organizational structure, including our payment obligations under the Tax Receivable Agreements, which may be significant;

•our ability to sustain an active, liquid trading market for our Class A common stock;

•the significant influence that CD&R (as defined herein) has over us and potential conflicts between the interests of CD&R and other stockholders; and

•risks related to other factors discussed under “Risk Factors” in this Annual Report on Form 10-K.

You should read this Annual Report on Form 10-K completely and with the understanding that actual future results may be materially different from expectations. All forward-looking statements made in this Annual Report on Form 10-K are qualified by these cautionary statements. These forward-looking statements are made only as of the date of this Annual Report on Form 10-K, and we do not undertake any obligation, other than as may be required by law, to update or revise any forward-looking or cautionary statements to reflect changes in assumptions, the occurrence of events, unanticipated or otherwise, and changes in future operating results over time or otherwise.

PART I

Item 1. Business

Our Company

Core & Main, Inc. (“Core & Main” and collectively with its subsidiaries, the “Company,” “we,” “our” or “us”) is a holding company and its sole material asset is its direct and indirect ownership interest in Core & Main Holdings, LP, a Delaware limited partnership (“Holdings”). We are a leading specialized distributor of water, wastewater, storm drainage and fire protection products, and related services, to municipalities, private water companies and professional contractors across municipal, non residential and residential end markets nationwide. Our specialty products and services are used in the maintenance, repair, replacement and new construction of water and fire protection infrastructure. We are one of only two national distributors operating across large and highly fragmented markets, which we estimate to represent approximately $32 billion in annual revenue.

As of January 30, 2022, we have a network of approximately 300 branch locations in 48 states across the U.S, which serve as a critical link between over 4,500 suppliers and a diverse and long-standing base of over 60,000 customers. Our sales reach, technical knowledge, broad product portfolio, customer service, project planning and delivery capabilities, and ability to provide local expertise nationwide, make us a critical partner to both our customers and suppliers.

We offer a comprehensive portfolio of approximately 200,000 stock keeping units (“SKUs”) covering a full spectrum of specialized products and services, including pipes, valves & fittings, storm drainage and erosion control solutions, fire protection products and fabrication services, and smart metering products and technology. Our products are unique to our industry and are tailored to local specifications.

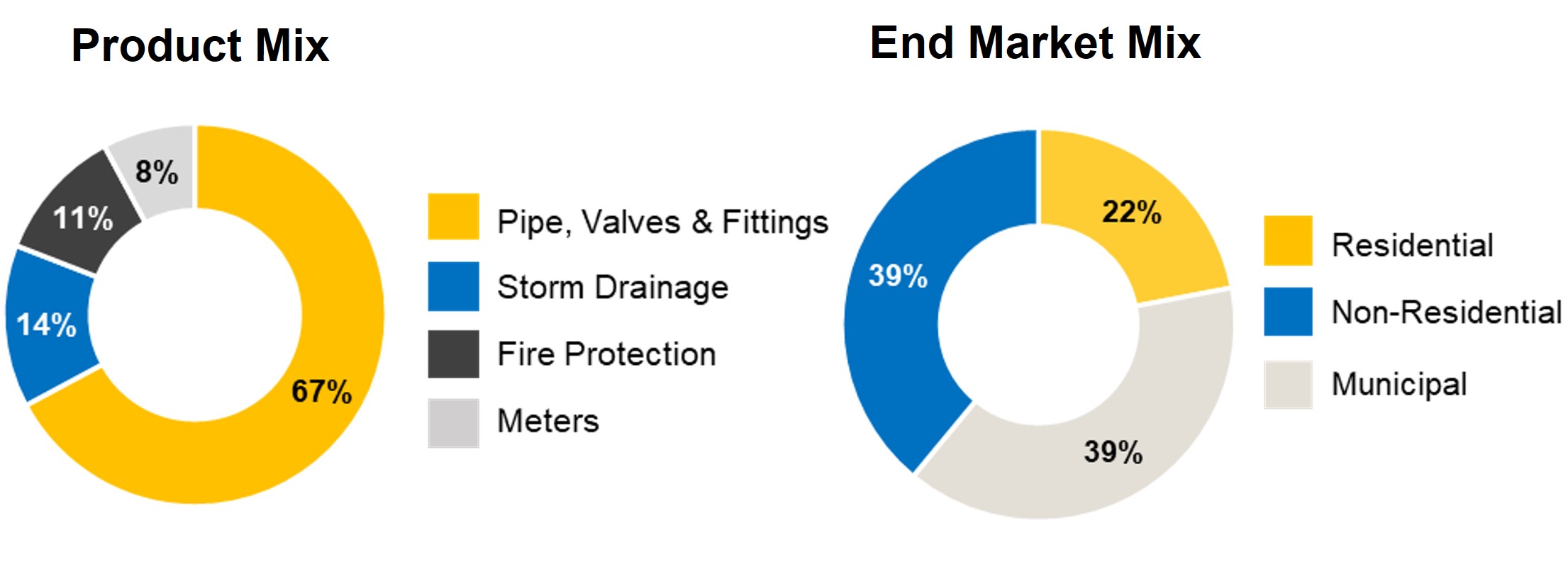

We have a balanced mix of sales across product categories, end markets and construction sectors. We derived approximately 39% of our net sales for the fiscal year ended January 30, 2022 (“fiscal 2021”) from the municipal construction sector, 39% from the non-residential construction sector, and 22% from the residential construction sector. Furthermore, we had an equal mix of sales related to construction on new projects and existing repair and replace projects in fiscal 2021.

Our company and our people are committed to the provision of safe and sustainable water infrastructure. Our mission is to serve as an industry leader, supplying local expertise, products and services to build innovative water, wastewater, storm drainage and fire protection solutions for the communities we serve. We support our customers and their communities in their efforts to find both short- and long-term solutions to conserve water and manage consumption. We embrace our responsibility in contributing to the continued evolution of our industry over the long term, providing innovative technology solutions and giving visibility to the critical importance of sustainable water infrastructure and fire safety systems.

The impact of climate change and increased natural flooding disasters have highlighted the need in the U.S. for improvements in storm drainage infrastructure solutions. As flooding events accelerate, storm water management systems with higher water volume handling capabilities become more critical to avoiding disasters, and we are well-positioned to support this increasing need given our extensive storm drainage offering. There is also an increasing demand for solutions that restore and reuse water, particularly in areas of the country facing threats from droughts. Our reclaimed water products help address these water shortage concerns.

For a discussion of the impact of seasonality and weather on our business, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Factors Affecting Our Business—Seasonality” of this Annual Report on Form 10-K.

Our History

Our first legacy distribution company dates back to 1874 and over the years, our company has grown through organic growth and a series of mergers and acquisitions. In 2005, The Home Depot acquired National Waterworks Holdings and subsequently merged it with Hughes Supply Inc. to establish one of the leading waterworks distributors in the United States. Under The Home Depot’s ownership, we became HD Supply Waterworks and completed several small acquisitions to further expand our geographic footprint. In 2007, a group of private equity investors acquired the HD Supply business from The Home Depot and subsequently executed an initial public offering in 2013. In August 2017, HD Supply Waterworks was acquired by Clayton, Dubilier & Rice, LLC (“CD&R”) from HD Supply and was subsequently rebranded as Core & Main. On July 27, 2021, we completed our initial public offering of Class A common stock (the “IPO”).

Our End Markets

We have diversified end market exposure across three primary construction sectors: (i) municipal; (ii) non-residential; and (iii) residential.

Based on management’s estimates, we believe that our addressable market in the U.S. for the wholesale distribution of water, wastewater, storm drainage and fire protection products, and related services, represented approximately $32 billion in revenue in 2021. Growth in our industry is driven by a broad array of factors, including municipal water infrastructure spending, water and wastewater utility rates, commercial construction, housing starts, population growth and other demographic trends.

Municipal

We estimate that approximately 39% of or net sales in fiscal 2021 were to contractors and municipalities for municipal funded projects, including the repair, replacement, upgrade and new construction of water and wastewater supply, filtration, storage and distribution systems. Municipalities establish local product specifications based on regulatory requirements and engineering standards. Given our extensive geographic footprint and technical knowledge of products and local specifications, we believe we are best equipped to anticipate and serve local needs as well as large private underground utility contractors who require national reach and an extensive product offering.

Municipal demand has exhibited steady growth over the long term due to the critical and immediate need to replace aged water infrastructure. However, due to limited available funding over the last decade, the pace of investment has significantly lagged the need to upgrade water systems throughout the U.S. and has resulted in significant underinvestment in water supply, water safety and wastewater management. In November 2021, the Infrastructure Investment and Jobs Act was signed into law, which includes $55 billion to invest in water infrastructure across the United States. In the coming years, we expect increased federal infrastructure investment to have a core focus on the upgrade, repair and replacement of municipal waterworks systems and to address demographic shifts and serve the growing population. We believe these dynamics, coupled with expanding municipal budgets, create the backdrop for a favorable funding environment and accelerated investment in projects that will benefit our business.

Non-Residential

We estimate that approximately 39% of our net sales in fiscal 2021 were directly related to clean water and wastewater infrastructure, storm drainage and fire protection systems supporting U.S. non-residential construction activity, including industrial, commercial, institutional, warehouse and multi-family development projects. Our products are often installed while breaking ground on new lot development during the initial construction phase, though some products, like storm drainage, are used during both new construction and repair and replace activities. Our fire protection products are typically installed at later stages of construction projects compared to most of our products and exhibit less seasonal patterns because they are generally installed indoors and are therefore less impacted by weather conditions.

Demand across the U.S. non-residential construction market has historically lagged residential construction activity as commercial development is necessary to support new housing development. With the recent growth in residential housing, we expect non-residential construction activity to increase as communities expand and demand increases for our waterworks, storm drainage and fire protection products. Furthermore, the Infrastructure Investment and Jobs Act provides funding to protect against droughts, floods, heat and wildfires, funding to repair roads and bridges, and funding to create more modern and resilient airport infrastructure, which could provide sustained benefits for non-residential construction activity.

Residential

We estimate that approximately 22% of our net sales in fiscal 2021 were directly related to clean water and wastewater infrastructure projects to supply and service U.S. residential construction activity. Residential spending in our industry is driven by new land and lot development for single-family housing. U.S. residential construction activity has accelerated in recent years and is expected to continue to grow as a result of population growth, low housing inventory, affordable interest rates and demographic population shifts. The current under-build of housing in the U.S. compared with household formations implies significant pent-up demand and continued growth going forward.

Our Strategies

We intend to capitalize on our competitive strengths to deliver profitable growth and create shareholder value through the following core strategies:

Utilize Scale and Platform to Accelerate New Product Adoption

We utilize our vast geographic footprint, customer relationships, local industry knowledge and training capabilities to introduce and accelerate the adoption of new products and technology in our industry. Examples include the advancement of smart metering and fusible HDPE solutions to waterworks customers, fabrication and kitting assemblies for fire protection contractors and new water retention and erosion control products for residential and non-residential developers.

We have identified a number of underpenetrated product categories in large and attractive markets where we can grow and enhance our market share. Erosion control is representative of these opportunities as it is a complementary product offering to existing customers in a fragmented market and furthers our focus on clean water given its role in stormwater run-off prevention. We believe that we can expand our presence in these underpenetrated product categories without investing significant capital or incurring substantial incremental costs as a result of our existing branch network, favorable supplier relationships and low working capital requirements.

Opportunistically Pursue Strategic Acquisitions

We have a strong track record of acquiring and integrating businesses. We have executed 16 acquisitions since becoming an independent company in 2017, adding more than $645 million in annualized net sales. We take a disciplined approach to sourcing, acquiring and integrating complementary businesses that help us expand into new geographic areas, acquire key talent or offer new products and services. We have a strong acquisition platform in place, which bolsters our ability to pursue attractive assets in the market. Our experienced mergers and acquisitions team actively develops a large pipeline of synergistic acquisition targets and coordinates with field leadership to identify, pursue and integrate new businesses. Through favorable purchasing capabilities, overhead cost reduction, facility optimization and our scalable information technology platform, we have been able to generate significant margin improvement and synergistic value from our acquired businesses.

We believe we are widely viewed as the acquirer of choice in our industry due to our long-standing relationships, an entrepreneurial culture, and our investment in the development and well-being of our people.

Replicate Successful Expansion in Underpenetrated Geographies

We have demonstrated an ability to successfully expand in underpenetrated geographies. We intend to continue to pursue opportunities to strengthen our presence in metropolitan statistical areas (“MSAs”) where we have an established footprint as well as in certain underserved markets. We believe we are well-positioned to do so through our market intelligence and ability to attract and develop sales talent. We also intend to continue to selectively drive greenfield expansion. We believe we can efficiently open new branches in geographies with attractive market trends given our highly capable talent pool, ability to capitalize on our scale and learning curve advantages based on past successes in entering new geographies. We have identified over 170 MSAs where we believe we are underpenetrated and thus have opportunities to pursue greenfield expansion or offer more product lines and services.

Increase Penetration with Strategic Accounts

Through our strategic accounts program, we partner with national contractors and private water companies who typically pursue large-scale, complex projects that require greater technical expertise and specialized procurement needs. Sales through our strategic accounts program represented less than 5% of our fiscal 2021 net sales. We believe that we are well-positioned to grow our share with these customers due to our dedicated sales team that includes engineers and other experts who can provide significant insights on large, complex projects, including cases in which our customers are asked to design and build new water systems or wastewater treatment plans. Our partnerships with these customers extend throughout the entire project lifecycle, from the pre-bidding design phase to post-project support. We believe our strategic partnerships and national supplier relationships will continue to generate cross-selling opportunities and future business, while driving adoption within our distribution model.

Execute on Gross Margin Enhancement Initiatives

From the fiscal year ended February 3, 2019 (“fiscal 2018”) to fiscal 2021, our gross margin has improved by roughly 350 basis points in part through several initiatives, including our private label program, category management optimization, data-driven pricing strategies and an expansion of value-added products and services. We have complemented these initiatives with accretive acquisitions, which has resulted in sustained margin expansion.

Our private label initiative has accelerated since our acquisition of Long Island Pipe Supply, Inc. ("LIP"), through which we gained access to a highly scalable assortment of private brands and products utilized throughout the fire protection product line. We believe our ability to leverage our global sourcing capabilities and strong international supplier relationships, as well as the potential for automated distribution and logistics, will continue to create competitive pricing advantages. We are expanding our direct sourcing and distribution capabilities in order to drive further margin expansion in the future.

Our category management team has identified numerous opportunities to continue shifting spend to suppliers with the best pricing and payment programs in order to optimize supplier incentives to expand gross margins.

Additionally, we have a specialized team dedicated to driving sustainable margin improvement through pricing analytics. An end-to-end review of our pricing strategies identified key margin enhancement opportunities, including continued optimization of system-wide pricing through IT enhancements, data-driven customer and product analysis that enable us to identify price opportunities and mitigate potential margin impacts from price changes. We believe these gross margin initiatives, in addition to our ability to leverage fixed costs, create a path to drive continued EBITDA margin expansion over the long term.

Invest in Attracting, Retaining and Developing World-Class Talent

We believe that our continued investment in the development and well-being of our people, together with our focus on our foundational core values of honesty and integrity, support our commitment to our associates and to customer service. Our award-winning training programs enable us to accelerate development of our top talent to drive profitable growth while maintaining a supportive and mission-driven culture.

We intend to continue investing our already strong talent base by attracting and developing associates. Our training and leadership curricula and expanded diversity and inclusion programs drive high associate engagement and a positive associate experience. In addition, we deliver attractive career growth opportunities to our associates while leveraging their knowledge and expertise.

Our Products & Services

Our comprehensive product portfolio consists of over 200,000 SKUs from approximately 4,500 suppliers. Our offering consists of pipes, valves & fittings, storm drainage and erosion control solutions, fire protection products and fabrication services, and smart metering products, services and technology. Our customers value our product breadth and geographic reach, as well as our technical product knowledge and consultation services. While pricing is important to our customers, availability, convenience, reliability and expertise are also important factors in their purchase decisions. In addition to many of our other capabilities, our ability to coordinate the logistics of on-time, last-mile jobsite delivery provides us with a competitive advantage over many competitors who offer a more limited selection of services.

Pipes, Valves & Fittings

Pipe, valves, hydrants and fittings are used in the distribution and flow control of water within water and wastewater transmission networks. Our pipe products, which typically range in diameter from 1/2” to 60”, include materials such as PVC, ductile iron, fusible high-density polyethylene, steel and copper tubing. Our valves are used to control the flow of water within water transmission networks and are often custom engineered to meet the specific needs of each project. Our hydrants provide a point-of-access for fire fighters to quickly tap into pressurized water systems and vary based on local specifications and regulations. Our fittings and restraints, made from a variety of materials depending on local specifications and regulations, are used to connect pipe sections, valves and other devices to each other. This category also includes other complementary products and services used for the service and repair of underground water infrastructure.

Pipes, valves & fittings products accounted for approximately 67% of our net sales in fiscal 2021.

Storm Drainage

Our storm drainage products are used in the construction of stormwater and erosion control management systems to retain, detain and divert stormwater runoff. Our storm drainage product offering includes corrugated HDPE and metal piping systems, retention basins, inline drains, manholes, grates and other related products. Our storm drainage product offering varies by market depending on local codes and engineering specifications.

Storm drainage products accounted for approximately 14% of our net sales in fiscal 2021.

Fire Protection

Our fire protection products are installed in industrial, commercial, institutional and warehouse buildings and are used to extinguish and prevent the spread of fires. These products are typically installed at later stages of the construction cycle than many of our other products, and as these products are generally installed indoors, the installation process can be completed in cold weather months and therefore have seasonality characteristics that offset some of our other product offerings. Typical fire protection products include pipe, sprinkler heads and devices, fire suppression systems, accessories and specialty fabrication services. Our fire protection products meet strict quality standards, and our offering often varies by market based on local specifications, regulations and fire codes.

Fire protection products accounted for approximately 11% of our net sales in fiscal 2021.

Meters

Our smart meters are used for water volume measurement and regulation and include automated meter reading and advanced metering infrastructure technologies. We offer multi-stage smart metering solutions to our customers, including meter installation, network infrastructure and software installation, training and long-term service contracts to deliver cost efficiencies to our customers. Our smart meters and advanced metering technology provide labor savings benefits for our municipal customers and help reduce water loss through leak detection.

Meter products accounted for approximately 8% of our net sales in fiscal 2021.

Our Customers

We have a fragmented customer base that consists of over 60,000 customers. Our top 50 customers represented approximately 12% of our net sales in fiscal 2021, with our largest customer accounting for less than 1% of net sales. We have long-tenured relationships with our customers, as approximately 84% of our net sales in fiscal 2021 were to customers that purchased products from us in each of the last five years, and we expect to continue to derive a significant portion of our net sales from our existing customers in the future.

Our customers choose us for our breadth of products and services, extensive industry knowledge, familiarity with local specifications, convenient branch locations, and timely and reliable delivery. We utilize our deep supply chain relationships to provide customers with a “one-stop-shop” experience and customized support in their efforts to maintain and construct water, wastewater, storm drainage and fire protection systems. Our scale and geographic footprint allows us to obtain preferred access to products for our customers, even during periods of material shortages. We have the ability to serve both smaller, local customers and larger, national customers with relevant expertise and the right inventory on hand. Our local sales associates take a consultative sales approach, using knowledge of the local regulatory requirements and specifications to provide customer-specific product and service solutions. We are deeply involved in our customers’ planning processes, and we have the ability to support our customers by converting engineered drawings and specifications into accurate and comprehensive material project plans. For specific smart metering, treatment plant, storm drainage and erosion control, or fusible pipe solutions, our sales associates partner with a deep and dedicated team of nearly 200 national and regional product specialists to assist customers in project scoping and specialized product selection. Our technical knowledge and experience are complemented by our proprietary customer facing digital technology tools, which enable us to work closely and efficiently with our customers in material management, timely inventory purchasing, quoting and coordinated jobsite delivery. We believe our customer facing technology tools build customer loyalty and drive repeat business, and also create a competitive advantage over smaller competitors who may not have the scale or resources to provide similar technology or services.

Our Suppliers

We have a diverse base of suppliers who view us as integral partners in the supply chain. We have strong relationships with our suppliers due to our long history in the industry, substantial purchasing scale, national footprint and ability to reach a fragmented customer base. Our national footprint and reach to local communities is essential to our suppliers, as we have a highly developed understanding of the relevant market, customer base and growth opportunities. We believe we are one of the largest volume customers for many of our suppliers, leading to favorable purchasing arrangements regarding product availability, payment terms and pricing. Our scale also enables us to secure distribution rights that are either exclusive or given to a limited number of distributors in key product categories, and to provide key products to customers that are unavailable to our competitors. Our size and scale, supplier relationships, and technical knowledge of products and local specifications enable us to obtain preferred access to specialized products and preferred access to products during periods of material shortages, or when shorter-than-usual lead times are required for certain projects. This provides us with a competitive advantage versus smaller competitors, particularly for large and complex projects. Our largest single supplier represented 7% of product expenditures in fiscal 2021, and our top ten suppliers represented 42% of total product expenditures during the same period. We strategically conduct business with our top suppliers in order to optimize our scale advantages, but we also have the flexibility to source the majority of our products from a number of alternate suppliers when necessary.

Our Competition

The U.S. water, wastewater, storm drainage and fire protection products wholesale distribution industry, and the end markets we serve, are highly fragmented. We face competition on a national level from only one other national distributor, but we are unique in our dedicated focus on the water sector. The remainder of our market is served by hundreds of regional, local and specialty niche distributors, and through direct sales by manufacturers to end users. We estimate that our net sales accounted for approximately 16% of our $32 billion addressable market in fiscal 2021, and that we and our largest national competitor had a similar market share in fiscal 2021.

The principal competitive factors in our industry include the breadth, availability and pricing of products and services, technical knowledge and project planning capabilities, local expertise, as well as delivery capability and reliability. We believe that we are a leader in the local markets that we serve, and our national scale gives us meaningful competitive advantages compared to our smaller competitors.

Our Operating Structure

We strategically organize our branch network to meet the specific needs of our customers in each local market, and we support our branches with the resources of a large company, delivered through district and regional management, including company-wide sales, operations and back-office functions. We believe this allows each local branch manager to tailor his or her branch’s strategy, marketing and product and service offerings to address the needs of customers in each of their markets, while maintaining many of the benefits of our company’s scale. Our branch associates have the opportunity to earn competitive compensation through our performance-based compensation plans, which are based on local performance.

We support our network of approximately 300 branches with the following company-wide resources: strategic accounts, product specialists, category management, sourcing, supply chain, finance, tax, accounting, pricing analytics, payroll, marketing communications, human resources, legal, safety and information technology. Nearly all of our branches operate on an integrated technology platform, allowing us to utilize our combined capabilities for procurement, inventory management, financial support, data analytics and performance reporting.

Our branch operational structure is organized by region and then by district to optimize both the oversight and sharing of resources and products. Each region is led by a regional vice president who manages a multistate territory. This regional structure enables us to address the specific management, strategic and operational needs of each region.

Our Distribution Network

Our branch-based business model is the core of our operations and the primary component of our distribution network. Our branches are strategically located near our customers and vary in size depending on local demand and customer needs. Our branches average approximately 10 associates and include branch management, sales representatives, warehouse staff and other support staff. In our larger branches, the staff may also include a sales manager, purchasing manager or estimator. Each branch carries approximately 4,500 SKUs on average, with many of them on hand as inventory and the rest available for delivery. Our branch managers have the autonomy to optimize their product and service offerings based on the local specifications, regulations and customer preferences within each local market.

Our branch network connects large suppliers with smaller volume customers whose consumption patterns tend to make them uneconomical to be served directly by our suppliers. Our branches receive products in both large and small quantities from our suppliers and stock products in warehouses and yards for purchase. Our specialized fleet of delivery equipment allows us to deliver materials to our customers’ worksites in a timely and cost-efficient manner.

We also offer direct distribution options to our customers on a wide range of products. This value-added service includes logistics and sourcing for larger products and quantities between our suppliers and our customers, which we believe helps our customers with inventory management and delivery scheduling, particularly when working on large-scale projects with multiple phases and delivery schedules. Contractors work with our sales teams throughout all phases of the project life cycle, including estimating and material “take-off,” product sourcing and bid preparation through delivery. Leveraging our vast supplier network, we are able to arrange convenient direct shipment to jobs, which can be aligned to each phase of the project.

Our Sales Force

As of January 30, 2022, we had approximately 1,600 sales representatives, the majority of whom were inside sales representatives based at local branches. Inside sales representatives are responsible for project management, coordinating incoming orders, providing estimates and ordering material. Our sales representatives also include approximately 525 field sales representatives who directly support customers outside of local branches. These field sales representatives remain attuned to activity in their local market, identifying and tracking active projects, and are responsible for generating sales and identifying new customers and projects. They also directly assist and educate customers, taking a consultative approach and helping with custom projects and product solutions tailored to our customers’ needs. While our sales representatives are typically assigned to a local branch and report to a branch manager, they can service an entire district and report to a district manager based on a specific customer or project need and the size of the branch.

Our sales representatives are highly experienced with in-depth product and technical knowledge, significant local insights and strong long-term customer relationships, all of which are critical to our success. On average, our field sales representatives have over 10 years of experience in the water, wastewater, storm drainage and fire protection industry. Our sales approach is highly consultative, as our representatives are often deeply involved in our customers’ processes and assist in project scoping, product selection and materials management. Our sales force also includes a deep and dedicated team of nearly 200 technical product specialists at the national and regional levels who have expertise in specific product and service offerings, and who support our other sales representatives with product training and technical support.

Our Human Capital

We believe our associates are the key drivers of our success, and we are focused on attracting, training, promoting and retaining industry-leading talent. Our authentic, purpose-driven culture enables our associates to thrive in our company and our industry. We have a strong track record of developing our associates for success and driving high employee engagement. Our ability to attract and retain talent is based on four foundational pillars: pay for performance, training and development, diversity and inclusion and benefits.

As of January 30, 2022, we employed approximately 4,100 associates, including approximately 250 in branch management positions, 1,200 in branch operations, 1,600 in sales positions, 500 in warehouse positions and 550 in other positions supporting the company. Approximately 100 of our associates were covered by collective bargaining agreements. The collective bargaining agreements for 46 of these associates will expire in 2022.

Pay for Performance

We believe that our strong culture, consistent investment in our people and competitive compensation programs result in low turnover rates among our associates. Sales associates have the opportunity to earn competitive compensation through our performance-based compensation structure, which aligns our interests with those of our associates. Our leadership incentive programs link compensation levels to the achievement of branch or region-specific goals based on profitability and return on investment. Our “local business, nationwide” philosophy incentivizes both our sales force and our operations team to be entrepreneurial, making decisions grounded in a customer-centric approach. Most other associates also participate in a profit sharing plan that aligns their compensation to profitability and return on investment.

Training and Development

Our associates are the most essential resource to our company. Their knowledge, expertise and growth are critical to our company’s success. We believe that our continued investment in the development and well-being of our people, and our focus on our foundational core values of honesty and integrity, support our commitment to hands-on customer service. At Core & Main, our associates develop by learning from the best of the best—on the job, in our national learning center, through in-house subject matter experts and with virtual and online academies.

Our learning team offers a wide range of award-winning training programs and courses such as sales, operations, product expertise, leadership, management and safety. We also provide customized training, talent reviews and early career rotational programs for college graduates to develop as future leaders. We utilize our suppliers to enhance our knowledge base as new products and best practices are continually rolled out.

This talent-first approach enables us to develop and promote top talent to drive profitable growth while maintaining a supportive and mission-driven culture. Year after year, associates rate our learning opportunities as one of the most valuable aspects of working at Core & Main.

Diversity and Inclusion

We believe our diversity and inclusion efforts are critical to the success of our talent strategy. A core element of our mission is to build strong relationships with one another and in the communities we serve. Some of our efforts are well established, such as our Women’s Network, and are intended to develop women in our industry. More recently, we have created an internal diversity and inclusion advisory group, a mental health council, and an associate caring fund. Through our training programs, we are taking a proactive approach to grow and retain our own talent and develop more diverse leaders in our industry. In fiscal 2020, we began to access new talent pipelines to attract talent from diverse and underrepresented communities, as well as the military. We frequently check the pulse of our associates, in addition to our annual engagement survey to listen and act on feedback. This ongoing, two-way dialogue provides our associates with a voice in creating and improving our culture, and the overall associate experience. We believe being included and having a voice is vital for associate engagement and underscores our core principle: Team members are family.

Benefits

Our comprehensive benefits program, “Live Well,” reflects our overall belief that benefits should address the whole associate experience, including health and well-being. We offer associates a comprehensive benefits package, which includes access to a concierge service to help them navigate their benefits. These efforts are representative of our focus on promoting a consistent, positive experience for all associates.

Our Intellectual Property

We rely on trademarks, trade names and licenses to maintain and improve our competitive position. We believe that we have the trademarks, trade names and licenses necessary for the operation of our business as we currently conduct it. We rely on both trademark registration and common law protection for trademarks. Trademark rights may potentially extend indefinitely and are dependent upon national laws and our continued use of the trademarks.

Except for the Core & Main trademark and licenses of commercially available third-party software, we do not consider our trademarks, trade names or licenses to be material to the operation of our business taken as a whole. We nevertheless face intellectual property-related risks and may be unable to obtain, maintain and enforce our intellectual property rights. Assertions by third parties that we violate their intellectual property rights could have a material adverse effect on our business, financial condition and results of operations.

Regulation

We are subject to various federal, state, and local laws and regulations, compliance with which increases our operating costs and subjects us to the possibility of regulatory actions or proceedings. Noncompliance with these laws and regulations can subject us to penalties, fines or various forms of civil, administrative, or criminal actions, any of which could have a material effect on our financial condition, results of operations, cash flows or competitive position.

These federal, state, and local laws and regulations include laws relating to wage and hour, permitting and licensing, state contractor laws, workers’ safety, transportation, tax, business with disadvantaged business enterprises, collective bargaining and other labor matters, environmental and associate benefits.

Our facilities and operations are subject to a broad range of federal, state and local environmental, health and safety laws, including those relating to the release of hazardous materials into the environment, the emission or discharge of pollutants or other substances into the air, water, or otherwise into the environment, the management, treatment, storage and disposal of hazardous materials and wastes, the investigation and remediation of contamination and the protection of the health and safety of our associates.

Our failure to comply with environmental, health and safety laws may result in fines, penalties and other sanctions as well as liability for response costs, property damages and personal injuries resulting from past or future releases of, or exposure to, hazardous materials. The cost of compliance with environmental, health and safety laws and capital expenditures required to meet regulatory requirements is not currently anticipated to have a material effect on our financial condition, results of operations, cash flows or competitive position. New laws or changes in or new interpretations of existing laws, the discovery of previously unknown contamination or the imposition of other environmental, health or safety liabilities or obligations in the future may lead to additional compliance or other costs, which could have a material effect on our financial condition, results of operations, cash flows or competitive position.

Organizational Structure

Core & Main was incorporated on April 9, 2021 for the purpose of facilitating the IPO and other related transactions in order to carry on the business of Holdings and its consolidated subsidiaries. Core & Main is a holding company, and its sole material asset is its ownership interest in Holdings, a portion of which is held indirectly through CD&R WW, LLC. Holdings has no operations and no material assets of its own other than its indirect ownership interest in Core & Main LP, the legal entity that conducts the operations of Core & Main. For more information regarding the IPO, the Reorganization Transactions (as defined below under in Item 7. “Management’s Discussion and Analysis of Financial Conditions and Results of Operations—Significant Events During Fiscal 2021”) and our holding company structure, see Note 1 to the consolidated financial statements included elsewhere in the Annual Report on Form 10-K.

Available Information

Our principal executive offices are located at 1830 Craig Park Court, St. Louis, MO 63146, and our telephone number is (314) 432-4700. Our website is www.coreandmain.com. We use our website as a routine channel for distribution of information that may be material to investors, including news releases, financial information, presentations and corporate governance information. None of the information contained on, or that may be accessed through, our website or any other website identified herein is part of, or incorporated into, this Annual Report on Form 10-K, and you should not rely on any such information in connection with your decision to invest in our Class A common stock. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available on our website, free of charge, as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the U.S. Securities and Exchange Commission (“SEC”). Additionally, the SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us, at www.sec.gov.

Item 1A. Risk Factors

Risks Related to Our Business

You should carefully consider the factors described below, in addition to the other information set forth in this Annual Report on Form 10-K. These risk factors are important to understanding the contents of this Annual Report on Form 10-K and of other reports. Our reputation, business, financial position, results of operations and cash flows are subject to various risks. The risks and uncertainties described below are not the only ones relevant to us. Additional risks and uncertainties not currently known to us or that we currently believe are immaterial may also adversely impact our reputation, financial position, results of operations and cash flows.

We have been, and may continue to be, adversely impacted by declines and volatility in the U.S. residential and non-residential construction markets.

Our business is largely dependent on activity in the U.S. residential and non-residential construction markets, which are volatile and subject to cyclical market pressures. The length and magnitude of these cycles have varied over time and by market. Approximately 22% and 39% of our net sales in fiscal 2021 were directly related to the U.S. residential and non-residential end markets, respectively. The level of activity in the U.S. residential and non-residential construction markets is based on numerous factors such as availability of credit, interest rates, general economic conditions, consumer confidence and other factors that are beyond our control. For example, in 2020, residential construction activity accelerated, in part due to the COVID-19 pandemic, as demand shifted away from densely populated urban centers, while non-residential construction slowed due to the COVID-19 pandemic. A significant downturn in activity in either the U.S. residential or non-residential construction markets could have a material adverse effect on our business, financial position, results of operations and cash flows.

We cannot predict the duration of the residential or non-residential construction industry market conditions or the timing of the recovery of residential or non-residential construction activity back to the historical averages. We also cannot provide any assurances that the operational strategies we have implemented to address current or future market conditions will be successful. Weakness in the residential or non-residential construction industry could have a material adverse effect on our business, financial position, results of operations and cash flows. Due to these factors and the potential volatility in the residential and non-residential construction markets, there may be fluctuations in our operating results, and the results for any historical period may not be indicative of results for any future period. Any uncertainty about current or future economic conditions can pose a risk to our business, financial position, results of operations and cash flows, as participants in the U.S. residential and non-residential construction industries may postpone spending in response to tighter credit, negative financial news or declines in income or asset values, which could have a material negative effect on the demand for our products.

Our business and the market for our products and services generally are subject to slowdowns in municipal infrastructure spending, which have in the past, and may in the future, result in a decrease in our net sales and operating results through reduced sales of our products to our municipal and contractor customers.

The market for the distribution of our products and services is affected by national, regional and local slowdowns in the amount spent by municipalities on waterworks infrastructure. We supply many of our products to contractors in connection with municipal projects. Approximately 39% of our net sales in fiscal 2021 were related to the municipal market. Many of the factors that influence waterworks sales are not within our control.

Municipal water infrastructure spending depends largely on availability and commitment of public funds for municipal spending, interest rates, water system capacity and general economic conditions. Product sales are subject to the availability of funding for municipal projects and reduced municipal funding could adversely affect our net sales. Economic downturns in any of our markets could reduce the level of infrastructure spending and construction activity and thus our net sales.

In addition, municipal budget processes and conditions in the municipal bond market can impact municipal spending. If a municipality is experiencing budget difficulties, or if a municipality is unable to access capital through the municipal bond market, it may allocate less funding to water infrastructure projects. Any slowdown in municipal spending on water infrastructure projects could have a material adverse effect on our business, financial position, results of operations and cash flows.